Does the -norm Learn a Sparse Graph under Laplacian Constrained Graphical Models?

Abstract

We consider the problem of learning a sparse graph under the Laplacian constrained Gaussian graphical models. This problem can be formulated as a penalized maximum likelihood estimation of the Laplacian constrained precision matrix. Like in the classical graphical lasso problem, recent works made use of the -norm regularization with the goal of promoting sparsity in Laplacian constrained precision matrix estimation. However, we find that the widely used -norm is not effective in imposing a sparse solution in this problem. Through empirical evidence, we observe that the number of nonzero graph weights grows with the increase of the regularization parameter. From a theoretical perspective, we prove that a large regularization parameter will surprisingly lead to a complete graph, i.e., every pair of vertices is connected by an edge. To address this issue, we introduce the nonconvex sparsity penalty, and propose a new estimator by solving a sequence of weighted -norm penalized sub-problems. We establish the non-asymptotic optimization performance guarantees on both optimization error and statistical error, and prove that the proposed estimator can recover the edges correctly with a high probability. To solve each sub-problem, we develop a projected gradient descent algorithm which enjoys a linear convergence rate. Finally, an extension to learn disconnected graphs is proposed by imposing additional rank constraint. We propose a numerical algorithm based on based on the alternating direction method of multipliers, and establish its theoretical sequence convergence. Numerical experiments involving synthetic and real-world data sets demonstrate the effectiveness of the proposed method.

Keywords: Sparse graph learning, Laplacian constrained Gaussian graphical model, Graph Laplacian, Nonconvex optimization, Graph signal processing.

1 Introduction

Gaussian graphical models (GGM) have been widely used in a number of fields such as finance, bioinformatics, and image analysis (Banerjee et al., 2008; Hartemink et al., 2000; Li and Gui, 2006; Park et al., 2017). Graph learning under GGM can be formulated to estimate the precision matrix that captures the conditional dependency relations between random variables (Dempster, 1972; Lauritzen, 1996). In this paper, the goal is to learn a sparse graph under the Laplacian constrained GGM, where the precision matrix obeys the Laplacian constraints.

The general GGM has received broad interest in statistical machine learning, where the problem can be formulated as a sparse precision matrix estimation. The authors Banerjee et al. (2008); d’Aspremont et al. (2008); Yuan and Lin (2007) proposed the -norm penalized maximum likelihood estimation method, also known as graphical lasso, to encourage sparsity in its entries. Numerous methods have been developed for solving this optimization problem. To solve the primal problem, first-order methods including Nesterov’s smooth gradient method (d’Aspremont et al., 2008), augmented Lagrangian method (Scheinberg et al., 2010), and second-order methods like inexact interior point method (Li and Toh, 2010), and Newton’s method (Dinh et al., 2013; Hsieh et al., 2014; Oztoprak et al., 2012; Schmidt et al., 2009; Wang et al., 2010) have been proposed for sparse precision matrix estimation. To solve the dual problem, block coordinate ascent method (Banerjee et al., 2008; Friedman et al., 2008), projected subgradient method (Duchi et al., 2008), and accelerated gradient descent method (Lu, 2009) have been proposed to estimate a sparse precision matrix. In addition, various extensions of graphical lasso and their theoretical properties have also been studied (Honorio et al., 2012; Mazumder and Hastie, 2012; Ravikumar et al., 2011; Shojaie and Michailidis, 2010; Yang et al., 2012, 2014). However, those methods mentioned above focus on general graphical models and cannot be directly extended to Laplacian constrained GGM because of the multiple constraints on the precision matrix. Moreover, unlike the case of GGM, this paper will show that the -norm is not effective in promoting sparsity in the penalized maximum likelihood estimation under Laplacian constrained GGM.

In recent years, Laplacian constrained GGM has received increasing attention in signal processing and machine learning over graphs (Dong et al., 2019; Ortega et al., 2018; Shuman et al., 2013; Ying et al., 2021a). Under Laplacian constrained GGM, graph learning can be formulated as Laplacian constrained precision matrix estimation. Unlike general GGM with a general positive definite precision matrix, the precision matrix in Laplacian constrained GGM enjoys the spectral property that its eigenvalues and eigenvectors can be interpreted as spectral frequencies and Fourier basis (Shuman et al., 2013), which is very useful in computing graph Fourier transform in graph signal processing (Ortega et al., 2018; Shuman et al., 2013), and graph convolutional networks (Bruna et al., 2014; Niepert et al., 2016; Ruiz et al., 2019). Dong et al. (2016); Egilmez et al. (2017); Gadde and Ortega (2015); Zhang and Florêncio (2012) formulated the graph signals as random variables under the Laplacian constrained GGM. The learned graph under Laplacian constrained GGM favours smooth graph signal representations (Dong et al., 2016), since the graph Laplacian quadratic term quantifies the smoothness of graph signals (Kalofolias, 2016; Kumar et al., 2020). Kumar et al. (2019) proposed to learn structured graphs under the Laplacian constrained GGM where a number of graph structures can be learned by imposing different Laplacian spectral constraints. A regularized Laplacian constrained GGM was proposed for graph structure discovery (Lake and Tenenbaum, 2010) and dimensionality reduction (Lawrence, 2012), where the precision matrix is a Laplacian matrix plus a very small diagonal matrix. The underlying assumption in (Lake and Tenenbaum, 2010; Lawrence, 2012) is that each data feature is independent and identically distributed sampled from a regularized Laplacian constrained GGM. Cardoso et al. (2021, 2022) extended the Laplacian constrained GGM to handle heavy-tailed settings for the scenario of learning graphs in financial markets. However, sparse graph learning under Laplacian constrained GGM remains to be further explored. For example, how to effectively and efficiently learn a sparse graph and how to characterize the statistical error of the estimation under Laplacian constrained GGM are to be investigated.

This paper focuses on learning a sparse graph under the Laplacian constrained GGM, which can be formulated as the penalized maximum likelihood estimation of the Laplacian constrained precision matrix. The main contributions of this paper are fourfold:

-

•

We find an unexpected behavior of the -norm in learning a sparse connected graph under the Laplacian constrained GGM. More specifically, through empirical evidence, we observe that the number of nonzero graph weights grows as the regularization parameter increases. From a theoretical perspective, we prove that a large regularization parameter of the -norm will surprisingly lead to a solution representing a complete graph, i.e., every pair of vertices is connected by an edge, instead of a sparse graph.

-

•

To overcome the issue of the norm, we introduce the nonconvex sparsity penalty, and propose a new estimator by solving a sequence of weighted -norm penalized sub-problems. We establish the non-asymptotic optimization performance guarantees on both optimization error and statistical error. We prove that the proposed estimator can recover the graph edges correctly with a high probability.

-

•

To obtain the new estimator, we develop a projected gradient descent algorithm to solve each sub-problem, and prove that the algorithm enjoys a linear convergence rate. Then we extend our method to learn disconnected graphs by imposing the rank constraint. We propose an algorithm based on the Alternating Direction Method of Multipliers (ADMM), and establish the theoretical sequence convergence.

-

•

Numerical experiments on both synthetic and real-world data sets demonstrate the effectiveness of the proposed method in learning sparse and interpretable graphs.

A short version of this paper (Ying et al., 2020) has been published in NeurIPS 2020. On what concerns the new contributions of this paper in comparison to the short version, we would like to highlight the following novelties: first, it was unknown in the short version whether the learned graph edges are correct or not, while this paper establishes the edge recovery consistency; second, this paper establishes the linear convergence rate of the proposed algorithm; third, the method proposed in the short version is limited to learning connected graphs, while this paper proposes a new algorithm to learn disconnected graphs, and establishes its theoretical convergence; finally, extensive numerical experiments including new graph structures and new data sets are considered in this paper.

The paper proceeds as follows: Section 2 formulates the problem and reviews related work. Section 3 discusses the -norm issue in learning sparse graphs and proposes nonconvex methods. We present the theoretical results in Section 4. An extension to learn disconnected graphs and the experimental results are presented in Sections 5 and 6, respectively. Section 7 concludes and discusses the findings. Proofs and technical lemmas are in Appendixes A and B. The corresponding open source package is available on GitHub at https://github.com/mirca/sparseGraph.

Notation

Lower case bold letters denote vectors and upper case bold letters denote matrices. Both and denote the -th entry of . denotes transpose of . denotes the set . Let for . We use to denote that each element of is non-negative. denotes the least integer greater than or equal to . The all-zero and all-one vectors or matrices are denoted by and . , and denote Euclidean norm, Frobenius norm and operator norm, respectively. denotes the -operator norm given by , and denotes the -operator norm given by . Let denote the maximum eigenvalue of . The inner product of two vectors is defined as . Let and . For functions and , we use if for some constant . and denote the sets of positive semi-definite and positive definite matrices with size , respectively. denotes the set of positive real numbers.

2 Problem Formulation and Related Work

We first present the definition of Laplacian constrained Gaussian Markov random fields and formulate the problem of learning a graph under the Laplacian constrained GGM. After that, we discuss related work.

2.1 Laplacian constrained Gaussian Graphical Model

We define a weighted, undirected graph containing no graph loops or multiple edges, where denotes the set of nodes, and the pair if and only if there is an edge between node and node . is the weighted adjacency matrix with denoting the graph weight between node and node . Note that the graph is undirected, and thus is symmetric. The graph Laplacian , also known as combinatorial graph Laplacian, is defined as

| (1) |

where is a diagonal matrix with . A graph is called connected if there is a path between every pair of vertices. The sparse connected graphs include tree graph, modular graphs, grid graph, line graph, star graphs and so on. A graph is called complete if every pair of vertices is connected by an edge.

In this paper, we will focus on the problem of learning sparse connected graphs first, and then we will extend our method to learn multiple component graphs. From spectral graph theory (Chung, 1997), the rank of the Laplacian matrix for any connected graph with nodes is . Therefore, the set of Laplacian matrices for connected graphs can be formulated as

| (2) |

where and denote the constant zero and one vectors, respectively. Next, we define the Laplacian constrained Gaussian Markov random fields, and without loss of generality we assume that the random vector has zero mean.

Definition 2.1.

A zero-mean random vector is called a Laplacian constrained Gaussian Markov Random Fields (LGMRF) with parameters with , if and only if its density function follows

| (3) |

where denotes the pseudo determinant defined by the product of nonzero eigenvalues (Holbrook, 2018), and is a -dimensional subspace of the coordinate space defined by .

Note that we restrict into a subspace because the LGMRF does not have a density with respect to the -dimensional Lebesgue measure. According to the disintegration theorem, we can construct a conditional probability measure defined on and then the density of LGMRF with this measure satisfies (3). In this sense, the LGMRF can be interpreted as a GMRF conditioned on the linear constraint and thus each observation of an LGMRF also satisfies . For convenience, we still denote in (3) as the precision matrix, though it formally does not exist (Rue and Held, 2005).

Unlike GGM, the elements of the precision matrix in the Laplacian constrained GGM can quantify the similarity between two nodes. More specifically, because of the Laplacian constraints, its probability density function can be written as

| (4) |

where . If the element is large, then there will be a relatively high probability that is small. This property is desired in modelling smooth graphs where a large graph weight between two nodes indicates a significant similarity between their signal values. The Laplacian constrained GGM has been widely explored in graph signal processing (Dong et al., 2016) and semi-supervised learning (Zhu et al., 2003), where the underlying graphs are usually assumed smooth.

Compared with GGM, there is an additional sign assumption on the Laplacian constrained GGM. More specifically, define , the projection of into the subspace , where follows a general multivariate Gaussian distribution. Then the precision matrix of will satisfy . If we add sign assumption that , then forms a Laplacian constrained GGM. The sign constraints on the entries of precision matrices are also explored in Gaussian distributions or general exponential families of distributions with multivariate total positivity (Fallat et al., 2017; Lauritzen et al., 2019b, a; Slawski and Hein, 2015; Wang et al., 2020; Cai et al., 2021; Ying et al., 2023). Exploring the advantages of the sign constraint in precision matrices is currently an active research topic. Lauritzen et al. (2019b); Slawski and Hein (2015) proved that the maximum likelihood estimator (MLE) for Gaussian distributions with multivariate total positivity exists if the sample size , irrespective of the underlying dimension. This yields a drastic reduction from in general Gaussian graphical models. More recently, Lauritzen et al. (2019a) showed that the MLE for the totally positive binary distributions may exist with observations, which is striking given that is required for the MLE to exist in the unconstrained binary exponential families.

Sparse graph learning under the Laplacian constrained Gaussian graphical model can be formulated as the penalized maximum likelihood of the Laplacian constrained precision matrix,

| (5) |

where is the sample covariance matrix, is a regularizer, depending on a regularization parameter , which serves to enforce sparsity, e.g., . is a constant matrix with each element equal to . Note that we replace with in (5) as done in (Egilmez et al., 2017), which follows from the fact that the matrix is rank one, and the nonzero eigenvalue of is whose eigenvector is orthogonal to the row and column spaces of . It is worth mentioning that the estimation method in (5) only uses the component in of the data samples for estimation, and the mean of each data sample is filtered out. Therefore, the estimator obtained by (5) is invariant to the mean of the data samples.

We finish the subsection with discussions on the motivations of imposing Laplacian constraints in (5). We consider data that fits the Laplacian constrained GGM well, for example the stock data which has been justified in Section 6.2.1. Imposing Laplacian constraints usually achieves a smaller estimation error than the GGM method without constraints, because the former introduces more prior knowledge and has a smaller search space. Furthermore, the learned graph weights under Laplacian constraints can quantify the similarity between two nodes, which is useful in community detection. Experimental results in Section 6.2.1 show that imposing Laplacian constraints can produce a more representative graph on the stock data than the GGM method without constraints.

2.2 Related Work

The -norm regularized maximum likelihood estimation under GGM has been extensively studied (Friedman et al., 2008; Hsieh et al., 2014; Mazumder and Hastie, 2012; Rothman et al., 2008; Shojaie and Michailidis, 2010; Yuan and Lin, 2007). To reduce estimation bias, nonconvex regularizers have been introduced in estimating a sparse precision matrix (Breheny and Huang, 2011; Chen et al., 2018; Lam and Fan, 2009; Loh and Wainwright, 2015; Shen et al., 2012; Zhang et al., 2010). Some popular nonconvex penalties include the smooth clipped absolute deviation (SCAD) (Fan and Li, 2001), minimax concave penalty (MCP) (Zhang et al., 2010), and capped -penalty (Zhang, 2010). Several types of algorithms including local quadratic appoximation (Fan and Li, 2001), minimization-maximization (Hunter and Li, 2005; Sun et al., 2016), and local linear approximation (Zou and Li, 2008) were proposed to solve the nonconvex optimization. Recently, Fan et al. (2018); Loh and Wainwright (2015); Sun et al. (2018) presented theoretical analysis to characterize nonconvex estimators with desired statistical guarantees. However, all those methods cannot be directly extended to Laplacian constrained GGM because we aim to learn a precision matrix that must satisfy the constraints in (2), while the learned precision matrix under GGM is a general positive definite matrix.

Recent works (Egilmez et al., 2017; Liu et al., 2019; Zhao et al., 2019) proposed the -norm penalized maximum likelihood estimation under Laplacian constrained GGM with the goal of learning a sparse graph. The authors Egilmez et al. (2017); Zhao et al. (2019) designed a primal-dual algorithm that introduces additional variables to handle Laplacian constraints. The authors Liu et al. (2019) proposed a block coordinate descent method to solve the optimization problem. The authors Kumar et al. (2019) proposed a -norm regularized maximum likelihood estimation method with Laplacian spectral constrains to learn structured graphs such as -component graphs. More recently, the authors Kumar et al. (2020) proposed a framework with re-weighted -norm to learn structured graphs by imposing spectral constraints on graph matrices. But, the proposed algorithms in (Kumar et al., 2020, 2019) have to compute the eigenvalue decomposition in each iteration which is computationally expensive in the high-dimensional regime. Note that all the methods mentioned above lack theoretical analysis on estimation error and algorithm convergence rate. In this paper, through theoretical analysis and empirical experiments, we show that the -norm is not effective in promoting sparsity in the Laplacian constrained GGM, and further propose a nonconvex estimator with theoretical guarantees on the estimation consistency of the precision matrix and the selection consistency of the graph edges. The approach of theoretical analysis in this paper may be extended to characterize statistical properties of other estimators under the Laplacian constrained GGM.

3 Proposed Method

In this section, we first focus on sparse connected graph learning. In Section 3.1, we present an unexpected behavior of the -norm in learning a sparse connected graph under the Laplacian constrained GGM. Then, in Section 3.2, we introduce the nonconvex sparsity penalty, and propose a new estimator by solving a sequence of weighted -norm penalized sub-problems. We further develop a projected gradient descent algorithm with backtracking line search to solve each sub-problem.

3.1 -norm Regularizer

Sparsity is often explored in high-dimensional Gaussian graphical models in order to reduce the number of samples required. The effectiveness of the -norm regularized maximum likelihood estimation, also known as graphical lasso, has been widely demonstrated in a number of fields. One common rule of thumb for graphical lasso is that the estimated graph will get sparser if a larger regularization parameter is used. However, we find an unexpected behavior of the -norm in sparse graph learning under the Laplacian constrained GGM.

The -norm regularized maximum likelihood estimation under the Laplacian constrained Gaussian graphical model (Egilmez et al., 2017; Zhao et al., 2019) can be formulated as

| (6) |

where is the sample covariance matrix with each sample independently sampled from LGMRF, and is the regularization parameter. An intuition of using the -norm in (6) could be that increasing the parameter will make the graph sparser, and finally leads to the sparsest connected graph, i.e., a tree graph. However, through theoretical derivations and empirical experiments, we show that a large regularization parameter will lead to a complete graph instead, i.e., every pair of vertices is connected by an edge.

Theorem 3.1.

Theorem 3.1, proved in Appendix A.2, states that a large regularization parameter of the -norm will force every graph weight to be strictly positive, thus the resultant graph will be a complete graph.

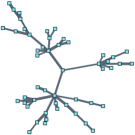

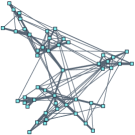

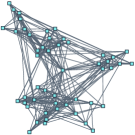

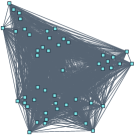

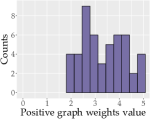

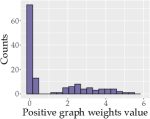

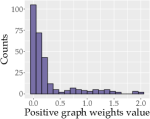

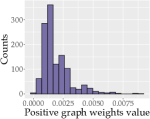

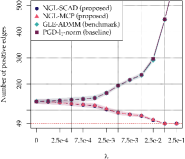

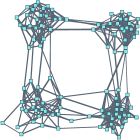

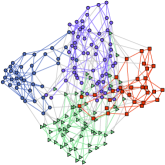

The theoretical result in Theorem 3.1 is consistent with empirical observations depicted in Figure 1, which shows that the number of positive edges learned by (6) grows along with the increase of , and finally the estimated graph in Figure 1 (d) is a complete graph. Figure 2 illustrates the histograms of the nonzero graph weights (associated with the positive edges) learned in Figure 1. Figure 2 (d) depicts the histogram for the graph in Figure 1 (d), where every weight is strictly positive. It is further observed in Figure 2 (d) that all the graph weights are very small. Therefore, a large regularization parameter will lead to a graph with every weight strictly positive and small. We can see that the histogram in Figure 2 (d) is significantly different from the true histogram in Figure 2 (a), implying that the estimated model fails to identify the true relationships among the data variables.

It is well-known that a larger regularization parameter of graphical lasso will lead to a larger threshold, and the elements in the solution with their absolute values less than the threshold will be shrunk to zero. Therefore, the resultant solution of the graphical lasso will get sparser. The unexpected behavior of the -norm characterized in Theorem 3.1 is due to the Laplacian constraints in the optimization (6). More specifically, because of the constrains and for any , then we have

| (7) |

To intuitively understand the behavior of the -norm with a large regularization parameter imposed in (6), suppose that is sufficiently large such that can be approximated by well. Then (6) will be reduced to the optimization problem as below

| (8) |

The global minimizer of the optimization (8) is shown in Corollary 3.2.

Corollary 3.2.

Let be the optimal solution of (8). Then obeys

| (9) |

Corollary 3.2, proved in Appendix A.2, shows that every estimated graph weight is strictly positive, and equal with each other. Moreover, the affect of the is negligible if a large is chosen. Therefore, no matter what kind of graph structure or connectivity the underlying graph has, the norm does not work as intended, i.e., as a sparsity promoting regularization. It is worth mentioning that it is the two constraints and together that make (7) hold, implying that the norm can still work well under the GGM with the generalized Laplacian constraints (Egilmez et al., 2017; Pavez et al., 2018; Pavez and Ortega, 2016; Ying et al., 2021b), where does not hold.

To solve the issue of the -norm in Laplacian constrained GGM, we introduce the nonconvex regularizer, and the effectiveness of the proposed method with the nonconvex regularizer has been demonstrated by numerical experiments in Section 6.

3.2 Proposed Algorithm

Problem (5) is a constrained optimization problem with including multiple constraints. We first simplify the Laplacian constraints in (2) as follows.

The constraints and in (2) are linear and there are only free variables in . Therefore, we use a linear operator defined in (Kumar et al., 2020) that maps a vector to a matrix as below.

Definition 3.3.

The linear operator , , is defined by

| (10) |

where .

A simple example is given below which illustrates the definition of the operator . Let . Then we have

The adjoint operator of is defined so as to satisfy , and .

Definition 3.4.

The adjoint operator , , is defined by

| (11) |

where obeying and .

By introducing the linear operator , we simplify the definition of in (2) in the following theorem, which is proved in Appendix A.3.

Theorem 3.5.

The Laplacian set defined in (2) can be written as

| (12) |

where and means every entry of is non-negative.

As a result of Theorem 3.5, we introduce the linear operator defined in (10) and reformulate the optimization (5) as

| (13) |

We can see that there is only non-negativity constraint in (13), which can be handled by simple projection. The variable contains all the graph weights, thus we transfer the problem of graph learning into the optimization problem in (13).

Notice that we remove the constraint in (13) compared with the constraint set in (12), because any in the feasible set of (13) must obey as shown as follows. Let . The feasible set of (13) is , where denotes the domain of the function . One can verify that

| (14) |

The set can be equivalently written as

| (15) |

which is due to the reason that must be positive semi-definite for any . The positive semi-definiteness of follows from the facts that is positive semi-definite for any because is a diagonally dominant matrix, and the matrix is rank one with the nonzero eigenvalue being 1 whose eigenvector is orthogonal to the row and column spaces of . Thus, on one hand, the condition in (14) guarantees that is non-singular. The non-singularity and positive semi-definiteness of together lead to in (15); On the other hand, the positive definiteness of can guarantee that in (14). Therefore, the feasible set of (13) is equivalent to (15).

To solve the problem (13), we follow the majorization-minimization framework (Sun et al., 2016), which consists of two steps. In the majorization step, we design a majorized function that locally approximates the objective function at satisfying

| (16) |

Then in the minimization step, we minimize the majorized function . In this paper, we assume is concave (refer to Assumption 4.1 for more details about the choices of ). Here we find the majorized function by linearizing . Set to simplify the notation and obtain

| (17) |

By minimizing , we establish a sequence by

| (18) |

where , . We can see is equivalent to because and by Assumption 4.1. Thus the problem (18) can be viewed as a weighted -norm penalized maximum likelihood estimation under Laplacian constrained Gaussian graphical model. The final estimator is obtained by solving a sequence of optimization problems (18). The iteration procedure is summarized in Algorithm 1.

To solve the optimization problem in (18), we develop an algorithm based on projected gradient descent with backtracking line search. To obtain , the algorithm starts with and then establishes the sequence by the projected gradient descent as below. In the -th iteration, we update by

| (19) |

where and . The sequence will converge to . Here we set which is the limit point of the sequence . The algorithm is summarized in Algorithm 2. Note that the users do not need to tune the step size manually because of the backtracking line search.

To establish the theoretical results in Section 4, the initial point of Algorithm 1 is chosen such that , where is the number of nonzero graph weights in the true graph. In other words, has no more than positive elements. Through the analysis of Algorithm 2 in Section 4, we will see that the sequence can be guaranteed in the feasible set of (13), implying that the estimated graph must be connected (refer to the proof of Theorem 4.7 for more details).

Though the proposed algorithm has two loops, we prove in Section 4 that for the outer loop, only iterations in Algorithm 1 are needed to achieve the desired order of estimation error, where and are two constants, independent of the dimension size and sample size . For the inner loop, the projected gradient descent in Algorithm 2 enjoys a linear convergence rate. In addition, the proposed method can be extended to estimate other structured matrices such as Hankel matrices with the usage of Hankel linear operator (Cai et al., 2016a; Ying et al., 2017).

4 Theoretical Results

In this section, we first present the non-asymptotic optimization performance guarantees of Algorithm 1 on both optimization error and statistical error in Section 4.1, and its edge recovery consistency in Section 4.2. The theoretical convergence of Algorithms 2 and 3 is established in Section 4.3.

We first list the assumptions needed for establishing our theoretical results. We denote the underlying true graph weights by , which are non-negative. Let be the support set of and be the number of the nonzero weights, i.e., . This paper focuses on learning connected graphs, and thus corresponds to the weights of a connected graph, i.e., every pair of vertices in the graph is connected. We impose some mild conditions on the sparsity-promoting function in Assumption 4.1 and the underlying graph weights in Assumption 4.2.

Assumption 4.1.

The function satisfies the following conditions:

-

1.

, and is monotone and Lipschitz continuous for ;

-

2.

There exists a such that for ;

-

3.

for and , where is a constant.

Assumption 4.2.

The graph weights represent a connected graph, i.e., defined in (2). The minimal nonzero graph weight satisfies , where and are defined in Assumption 4.1. There exists such that

| (20) |

where and are the second smallest eigenvalue and maximum eigenvalue of , respectively. Note that the smallest eigenvalue of is .

Remark 4.3.

In Assumption 4.1, the conditions on are mainly made over because of the nonnegativity constraint in the optimization (18). In Assumption 4.1, the first two conditions are made to promote sparsity and unbiasedness (Loh et al., 2017), and hold for a variety of nonconvex sparsity-promoting functions including the popular choices SCAD (Fan and Li, 2001) and MCP (Zhang et al., 2010). The two conditions also ensure that the derivative of is not constant to avoid the issue in Theorem 3.1. In the third condition, we specify for only for theoretical analysis. The condition can always hold by tuning parameters due to the conditions and . Therefore, it is flexible to design a sparsity-promoting function satisfying the conditions stated in 4.1. In Assumption 4.2, the conditions on the true graph weights are mild. In our theorems, the regularization parameter is taken with the order that could be very small when the sample size increases. The assumptions on the minimal magnitude of signals are often employed in the analysis of nonconvex optimization (Fan et al., 2018; Wang et al., 2016). The assumptions on the minimum nonzero eigenvalue are frequently made (Chen et al., 2018; Lyu et al., 2019; Wang et al., 2016) to establish a local contraction region.

4.1 Analysis of Estimation Error

We will characterize the estimation error of our proposed nonconvex optimization method. In the following theorem, proved in Appendix A.4, the choice of the regularization parameter is set according to a user-defined parameter . A larger yields a larger probability with which the claims hold, but also leads to a more stringent requirement on the number of samples.

Theorem 4.4.

Theorem 4.4 holds with overwhelming probability. According to Theorem 4.4, the estimation error between the estimated and underlying true graph weights is bounded by two terms, i.e., the optimization error and statistical error. The optimization error, , decays to zero at a linear rate with respect to the iteration number . The statistical error depends on the sample size , and a large sample size will lead to a small statistical error. We can see the statistical error is independent of , and thus will not decrease during iterations in the algorithm. Therefore, the estimation error of the output of the algorithm is mainly from the statistical error.

Corollary 4.5.

Corollary 4.5 presents the estimation error between the estimated and underlying true precision matrices in Laplacian constrained GGM. Similar to Theorem 4.4, the optimization error decays to zero at a linear rate. The order of statistical error is upper bounded by , which is consistent with the one obtained for Gaussian graphical models (Cai et al., 2016b; Ravikumar et al., 2011; Rothman et al., 2008). It is interesting to explore if is optimal for estimating sparse precision matrices with Laplacian constraints in future work. Furthermore, the proposed estimation method can achieve this order by solving only sub-problems. Notice that is independent of the dimension size and sample size .

4.2 Analysis of Edge Recovery

We show in Theorem 4.4 that the proposed estimator is consistent in terms of parameter estimation. However, it does not mean that the estimator necessarily consistently select the correct edges. In this subsection, we present Theorem 4.6, proved in Appendix A.5, showing that the proposed estimator can recover the edges correctly with a high probability.

An oracle knows the true support set, and the oracle estimator is defined as

| (21) |

where is the true support set. Note that the oracle estimator (21) exists and is unique with probability one (please refer to the proof of Theorem 4.6 for more details).

We define some constants which are only related to the underlying true graph weights . Let

| (22) |

where , and for , with the -th canonical basis of . Let be the maximum node degree of the graph, i.e., the maximum number of edges for each node.

Theorem 4.6.

The statement in Theorem 4.6 holds with a high probability for a reasonably large . Theorem 4.6 shows that the oracle estimator defined in (21) is a limit point of the sequence generated by Algorithm 1, and Algorithm 1 will converge to . Furthermore, we can see that the proposed estimator can recover the edges correctly with a high probability. Note that both and are non-negative. Thus the proposed estimator also enjoys the sign consistency. In addition, the condition on the initial point that could be always met if is set by some consistent estimator with sufficient samples.

4.3 Analysis of Algorithm Convergence

In this subsection, we establish the theoretical convergence of Algorithms 2 for solving each sub-problem.

In the theorem statement, the parameter is a user-defined parameter. A larger leads to a faster convergence rate, but a larger number of samples are required.

Theorem 4.7.

Theorem 4.7, proved in Appendix A.6, shows that the designed projected gradient descent algorithm enjoys a linear convergence rate in solving sub-problems (18). Note that when , Algorithm 2 may not enjoy a linear convergence rate because we only set a very mild condition on the initial point that . Thus may not be in the local region , where is -strongly convex and -smooth with and according to Lemma A.10. One may impose more conditions on the initial point such that , then Algorithm 2 also has a linear convergence rate for . Here , and is defined in Assumption 4.2.

It is observed that the required sample size in Theorem 4.7 is larger than the one in Theorem 4.4. Using the sample size in Theorem 4.4, one can still establish a local contraction region by introducing the lower level set such that Algorithm 2 also has a linear convergence. However, the region is much larger than , and the smoothness parameter of may be very large in . Here , where is defined in Lemma A.4.

5 Extension to Disconnected Graph Learning

We focus on the problem of learning sparse connected graphs in Sections 3 and 4. In this section, we extend our method to learn sparse disconnected graphs.

5.1 Algorithm

We consider the disconnected graph consisting of components. Following from the spectral graph theory, we obtain that the rank of Laplacian matrix is equal to the number of components in the graph. Then we can formulate the sparse -component graph learning problem as follows:

| (23) |

where is the set of all the Laplacian matrices with rank , defined by

| (24) |

Note that we have to impose the rank constraint in (23), because the pseudo determinant function is not continuous between sets of matrices of different ranks. It is worth mentioning that the GGM or the GGM with generalized Laplacian constraints does not need the rank constraint in learning multiple component graphs (Hsieh et al., 2012; Pavez et al., 2018), because the precision matrices can keep positive definite for disconnected graphs.

The challenge in solving (23) is that the Laplacian constraints and rank constraint in (24) are simultaneously imposed on one variable. To decouple those constraints in (24), we introduce an auxiliary variable , and reformulate (23) as

| (25) |

Now we can see that the Laplacian constraints are imposed on , and the rank constraint is imposed on . To solve the optimization (25), we propose an algorithm based on ADMM. The augmented Laplagian function of (25) is

| (26) |

where is the dual variable. We successively update each variable as follows.

To update , we have the following sub-problem,

| (27) |

The closed-form solution of (27) is

| (28) |

where is the eigenvalue decomposition of , and is a diagonal matrix containing the largest eigenvalues on the diagonal and contains the corresponding eigenvectors.

To update , we have the following sub-problem,

| (29) |

To solve the problem (29), we follow the majorization-minimization framework. In the -th iteration, we minimize the majorized function at and get

| (30) |

where with , , and following from Lemma 5.3. The closed-form solution of (30) is

| (31) |

We can establish the sequence , and set its limit point as .

5.2 Convergence

We present the theoretical convergence of Algorithm 3 in Theorem 5.1, which is proved in Appendix A.7.

Theorem 5.1.

The optimization problem (23) is nonconvex because of the nonconvex sparsity penalty and the rank constraint. Theorem 5.1 shows that Algorithm 3 will subsequently converge to a stationary point of (26) with a sufficiently large . In practice, we could iteratively increase the to a decently large value and treat this procedure as an initialization as adopted in (Ying et al., 2018).

6 Experimental Results

In this section, we conduct numerical experiments on both synthetic data and real-world data sets to verify the performance of the proposed method. The compared methods include the state-of-the-art GLE-ADMM algorithm (Zhao et al., 2019) and the baseline projected gradient descent with -norm.

We employ the performance measures: Relative Error (RE) and F-score (FS), which are defined as follows:

| (33) |

where and denote the estimated and true precision matrices, respectively.

The true positive number is denoted as tp, i.e., the case that there is an actual edge and the algorithm detects it, the false positive is denoted as fp, i.e., the case that there is no actual edge but algorithm detects one, and the false negative is denoted as fn, i.e., the case that the algorithm failed to detect an actual edge. The F-score takes values in , where indicates perfect structure recovery. For our method, we test two nonconvex penalties, MCP and SCAD, defined respectively by

where we define and only for because of the nonnegativity constraint in (18). We set equal to and in and in all the experiments, respectively. Note that the proposed method is not limited to using MCP and SCAD regularizers, and one can explore other sparsity-inducing functions (Bach et al., 2012) for interest.

6.1 Synthetic Data

For experiments on synthetic data, we consider two types of graphs: Barabasi-Albert graphs of degree one (Albert and Barabási, 2002), and modular graphs. Estimating tree graphs is a crucial task that has an impact in the performance of many applications such as image segmentation (Wu and Leahy, 1993). Modular graph consists of a connected graph which contains clusters of nodes that share similar properties. The sparsity level in modular graphs are twofold: (1) intra-modular and (2) inter-modular. The first one refers to the number of connections among nodes that belong to the same module, whereas the second one refers to the number of connections among nodes in different modules. Modular graphs have been applied to a myriad of social network tasks such as community detection (Fortunato, 2010).

We generate the data matrix with each column independently sampled from LGMRF with , where contains the true weights from Barabasi-Albert graphs of degree one and modular graphs. The number of nodes in the Barabasi-Albert graph and modular graph is and , respectively. The weights associated with positive edges in both Barabasi-Albert graph and modular graph are uniformly sampled from . The modular graph is generated with probabilities of intra-module and inter-module connections and , respectively. The sample covariance matrix is constructed by , where is the number of samples. The curves in Figures 3, 4, 5 and 6 are the results of an average of Monte Carlo realizations and the shaded areas represent the one-standard deviation confidence interval.

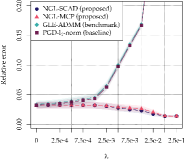

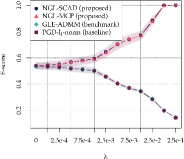

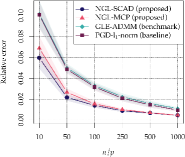

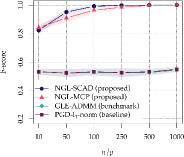

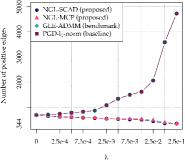

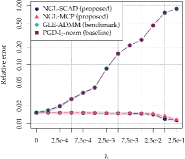

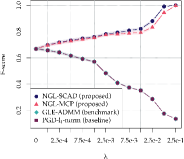

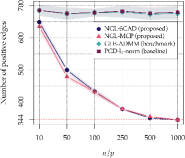

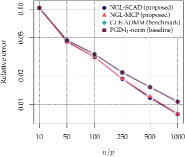

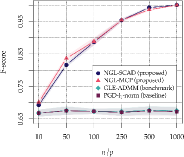

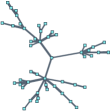

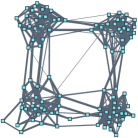

Figure 3 presents the results of learning Barabasi-Albert graphs by GLE-ADMM, projected gradient descent with -norm, and the proposed method with the two regularizers. It is observed that the numbers of positive edges learned by GLE-ADMM and projected gradient descent with -norm rise along with the increase of , implying that the graphs will get denser as increases. Figure 3 shows that both GLE-ADMM and projected gradient descent with -norm achieve the best performance in terms of sparsity, relative error, and F-score when , which defies the purpose of introducing the -norm regularizer. In contrast, the proposed NGL-SCAD and NGL-MCP enhance sparsity when increases. It is observed that, with equal to or , NGL-SCAD and NGL-MCP achieve the true number of positive edges, and an F-score of , implying that all connections and disconnections between nodes in the true graph are correctly identified.

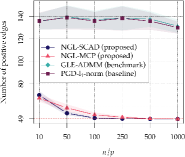

Figure 4 shows that the proposed NGL-SCAD and NGL-MCP always outperform both GLE-ADMM and the baseline projected gradient descent in terms of sparsity, relative error, and F-score under different samples size ratios.

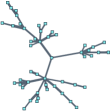

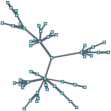

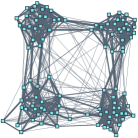

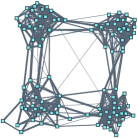

Figure 5 presents the results of learning modular graphs by GLE-ADMM, projected gradient descent with -norm, and the proposed NGL-SCAD and NGL-MCP. It is observed that a larger regularization parameter for GLE-ADMM and projected gradient descent with -norm will lead to a worse performance in terms of sparsity, relative error, and F-score. On the contrary, NGL-SCAD and NGL-MCP enhance the sparsity and improve the relative error and F-score as increases.

Figure 6 shows that the proposed method always leads to a better performance in learning modular graphs in terms of sparsity, relative error, and F-score, than the compared methods under different sample size ratios.

Figure 7 shows a sample result of learning a Barabasi-Albert graph via GLE-ADMM, NGL-SCAD and NGL-MCP. It is observed that the learned graphs via NGL-SCAD and NGL-MCP present the connection between any two nodes correctly, while there are many incorrect connections in the graph learned via GLE-ADMM. In addition, performance measures including sparsity, relative error, and F-score also indicate a better performance of the proposed method.

Figure 8 shows a sample result of learning a modular graph via GLE-ADMM, NGL-SCAD and NGL-MCP. It is observed that the learned graphs via NGL-SCAD and NGL-MCP are much more representative than the one learned via GLE-ADMM.

6.2 Real-world Data Sets

In this subsection, we conduct numerical experiments on real-world data sets including stock data sets and COVID-19 data set for connected graph learning, and animals data set for -component graph learning.

6.2.1 Stock data sets

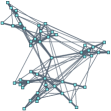

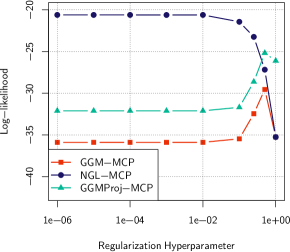

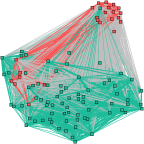

We first present an experiment to verify that the Laplacian constrained GGM could describe the stock data set better than the general GGM. We compare the log-likelihood of the general precision matrices and the Laplacian constrained precision matrices, estimated by the GGM method with the MCP penalty (GGM-MCP) and the proposed NGL-MCP, respectively, on a test set of stock data. Note that the log-likelihood of the general precision matrices is computed with the function , while that of the Laplacian constrained precision matrices is with because of the singularity of the Laplacian matrix. To make the comparison fairer, we add a comparison wit GGMProj-MCP which is obtained by projecting the precision matrices estimated by GGM-MCP such that they satisfy , then compute the log-likelihood using .

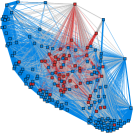

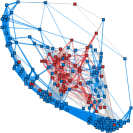

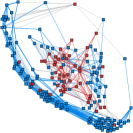

Figure 9 (a) shows that the NGL-MCP achieves the highest log-likelihood, indicating that the Laplacian constrained precision matrices describe the stock data better than the general precision matrices. Figure 9 (b) presents the graph weights with , where the precision matrix is obtained by GGMProj-MCP with the highest log-likelihood in Figure 9 (b). It is observed that most of the graph weights are non-negative, implying that the sign assumption is satisfied well on the stock data set.

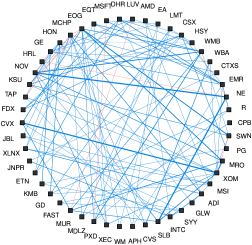

Next, we compare the proposed NGL-MCP with GLE-ADMM and GGM-MCP in learning graphs on a stock data set. It is observed in Figure 10 that the performance of NGL-MCP is the most significant, because most connections are between nodes within the same community, and only a few connections (gray edges) are between nodes from distinct communities. The modularity values for GLE-ADMM, GGM-MCP and NGL-MCP are 0.36, 0.37 and 0.51, respectively. A higher modularity value indicates a better representation of the actual network of stocks. The data set is from stocks composing the S&P 500 index. We select log-returns from 181 stocks from 4 sectors, namely: ”Industrials”, ”Consumer Staples”, ”Energy”, ”Information Technology”, during a period of 4 years from January 1st 2016 to May 20th 2020, with a total of 1101 observations. Then the data matrix has a size of .

6.2.2 COVID-19 data sets

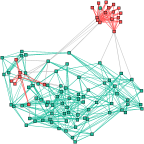

We conduct numerical experiments on the COVID-19 data set1112019-nCoV data is available in a queryable format via the R package nCov2019 which lives on GitHub: https://github.com/GuangchuangYu/nCov2019. from 98 anonymous Chinese patients affected by the outbreak of COVID-19 on early February, 2020. The features include age (integer), gender (categorical), and location (categorical). The label is a binary variable representing the life status of patients, alive (green) or no longer alive (red). Our goal is to construct a graph from the data features. To this end, we first pre-process the feature matrix so as to transform the categorical features into numerical ones via one-hot-encoding. The pre-processed feature matrix has the dimension , i.e., and . We then compute the sample covariance matrix and learn the graphs.

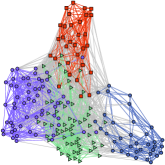

Figure 11 shows that the benchmark GLE-ADMM is unable to impose sparsity, diminishing interpretation capabilities of the graph severely. On the other hand, the proposed NGL-SCAD and NGL-MCP obtain sparse graphs with clearer connections. The learned graphs possibly provide guidance on priority setting in health care because green nodes (patients alive) that have stronger connections with red nodes (patients that passed away) may suffer a higher health risk.

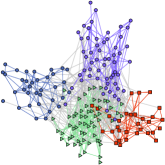

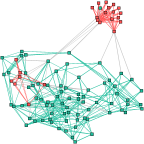

We next perform experiments on the COVID-19 data set222The data set is freely available at: https://www.kaggle.com/einsteindata4u/covid19. provided by the Israelite Hospital Albert Einstein in Brazil. The data set contains anonymized data from patients who had samples collected to perform the test for SARS-CoV-2. The features in the data set are mainly clinical coming from blood, urine, and saliva exams, e.g., hemoglobin level, platelets, red blood cells, etc. The original data set contains 108 features from 558 patients. Due to the high number of missing values, we do not consider features that were measured for at most 10 patients. In addition, a large number of patients had no record of any features. Finally, we end up with a data matrix of 182 patients with 57 features, i.e., and . The remaining missing values were filled in with zeros. We then compare the proposed method with the GLE-ADMM method on this data set. It is observed from Figure 12 that the proposed NGL-SCAD and NGL-MCP output a more interpretable representation of the network, where blue and red nodes denote patients who tested negative and positive for SARS-CoV-2, respectively.

It is worth mentioning that the real-world data sets may not exactly follow the Laplacian constrained Gaussian graphical models. In this case, our formulation in (5) can be related to the regularized log-determinant Bregman divergence optimization, and the learned graph weights can quantify the similarity between nodes. This is because the trace term can be written as Laplacian quadratic (Dong et al., 2016; Kalofolias, 2016), which tends to assign a large weight between nodes if their signal values are similar.

6.2.3 Disconnected Graph Learning

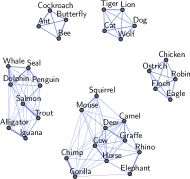

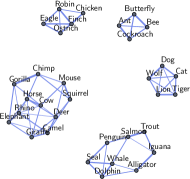

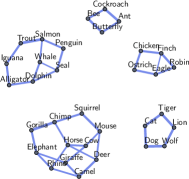

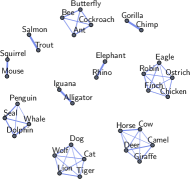

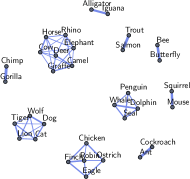

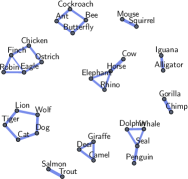

In this subsection, we conduct an experiment on the animals data set (Lake and Tenenbaum, 2010) for -component graph learning, and compare our proposed method with the state-of-the-art CLR (Nie et al., 2016) and SGL (Kumar et al., 2020). In this data set, every node denotes one animal and edge weights represent similarities among them. The animals data set consists of 33 animals and 102 features. The regularization parameter of the proposed method is set as 0.5 in Figure 13.

It is observed in Figure 13 that the animal groupings among the graphs learned by CLR, SGL and the proposed NGL-MCP vary slightly. The learned graphs in Figure 13 are meaningful, because similar animals such as (chimp, gorilla) and (salmon, trout) are grouped together in Figure 13 (d), (e) and (f) when setting . Note that the CLR method aims to learn a similarity graph, where a large graph weight between two nodes indicates a large similarity between them, and there is no underlying statistical assumption, while both SGL and NGL-MCP have the assumption of the Laplacian constrained Gaussian graphical models. Therefore, this experimental result justifies our statement in Section 2 that the graph weights in Laplacian constrained Gaussian graphical models can quantify the similarity between two nodes.

Figure 13 shows that our method can learn a more interpretable graph than CLR and SGL, because the connectivity within groups in the graphs learned by CLR and SGL is dense, which reduces the interpretability of graphs. For example, in Figure 13 (d) and (e), the connectivity in the group (tiger, lion, wolf, dog and cat) is full, i.e., every two nodes are connected by an edge. This is because CLR does not impose the sparsity explicitly, and SGL suffers the interplay between the spectral regularization term and the sparsity term.

7 Conclusions and Discussions

In this paper, we have considered learning a sparse graph under the Laplacian constrained Gaussian graphical models. We have proved that a large regularization parameter of the -norm leads to a complete graph. To overcome the issue of the -norm, we have proposed a new estimator by introducing the nonconvex sparsity penalty. We have established the non-asymptotic optimization performance guarantees on both optimization error and statistical error, and proved that the proposed estimator can recover the graph edges correctly with a high probability. A projected gradient descent algorithm has designed to solve each sub-problem which enjoys a linear convergence rate. We have further extended our method to learn disconnected graphs. Numerical results have demonstrated the effectiveness of the proposed method.

Finally, we propose several viable directions for future research. First, it would be intriguing to establish non-asymptotic optimization performance guarantees on both optimization and statistical errors in the context of learning disconnected graphs. Notably, the rank constraint may introduce numerous local minima, and the techniques required would significantly differ from those used for learning connected graphs. Second, this paper focuses on Laplacian constraints within Gaussian graphical models. Future work could expand this to explore Laplacian constraints within other Markov random fields, such as Ising models (Ravikumar et al., 2010).

Appendix A Proofs of Theorems

This section includes the proofs of Theorems 3.1, 3.5, 4.4, 4.6, 4.7 and 5.1, and Corollaries 3.2 and 4.5. Before proving the theorems, we first present some technical lemmas.

A.1 Technical Lemmas

Lemma A.1.

Let , with . Then for any , we have

Lemma A.2.

For any given satisfying , there must exist an unique such that

| (34) |

holds for any , where , in which with each element equal to 1.

Lemma A.3.

Denote by

Then we have .

Lemma A.4.

Let , . For any , with satisfying

where satisfying and , and is an index set defined by

Furthermore, we have and .

Lemma A.5.

Take and suppose for some , where is a constant defined in Lemma A.9. Let

where obeys for . If holds with the set satisfying and , then obeys

where is the support of .

Lemma A.6.

Lemma A.7.

Lemma A.8.

Take and suppose for some , where is a constant defined in Lemma A.9. Then one has

Lemma A.9.

Consider a zero-mean random vector is a LGMRF with precision matrix . Given i.i.d samples , the associated sample covariance matrix satisfies, for ,

where and are two constants.

Lemma A.10.

Lemma A.11.

Let . Define a local region of by

where , in which for any with defined in Lemma A.4, and . Then for any , we have

Lemma A.12.

(Willoughby, 1977) Suppose a positive matrix is diagonally scaled such that , , and , . Let and be the lower and upper bounds satisfying

and define by

Then the inverse matrix of exists and is an inverse -matrix if with .

Lemma A.13.

(Wainwright, 2019) (Sub-exponential tail bound) Suppose is sub-exponential with parameters . Then

A.2 Proofs of Theorem 3.1 and Corollary 3.2

Proof.

As a result of Theorem 3.5, the optimization (6) can be equivalently written as

| (36) |

Due to the non-negativity constraint , (36) can be further rewritten as

| (37) |

where .

We first prove that the optimization (37) has one global minimizer if . Let . The feasible set of (37) is , which is the same with the feasible set of (13). For any , the minimum eigenvalue of can be lower bounded by

where the second equality is due to Lemma A.1; the third equality follows from Lemma A.4; the last equality follows from the property of Kronecker product that the eigenvalues of are for , where and are the eigenvalues of and , respectively, and following from Lemma A.4; the last inequality follows from the fact that . Therefore, the optimization (37) is strictly convex, and thus (37) has at most one global minimizer.

The existence of minimizers of (37) can be guaranteed by the coercivity of . The function can be lower bounded by

| (38) |

where the second equality follows from (134) with ; the forth equality follows from ; the last inequality holds because , and , which follows from (172); the first inequality holds because the smallest eigenvalue and

holds for any non-negative real numbers of . A function is called coercive over , if every sequence with obeys , where . Let

A simple calculation yields if . For any sequence with , where is the closure of , one has , because . Then one obtains

where the first inequality follows from (38). Hence, is coercive over . Following from the Extreme Value Theorem (Drábek and Milota, 2007), if is non-empty and closed, and is lower semi-continuous and coercive, then the optimization has at least one global minimizer. Therefore, by the coercivity of , (37) has at least one global minimizer in .

Let and . is a closed set and is an open set. Then can be rewritten as . Consider the set , we have

| (39) |

where is the boundary of . Notice that every matrix on the boundary of the set of positive definite matrices is positive semi-definite and has zero determinant. Hence, one has . As a result, for any , . Therefore, (37) has at least one global minimizer and the minimizer must belong to the set . On the other hand, by the strict convexity of , (37) has at most one global minimizer in . Totally, we conclude that (37) has an unique global minimizer in if .

We prove the theorem through the KKT conditions. The Lagrangian of the optimization (37) is

where is a KKT multiplier. Let be any pair of points that satisfies the KKT conditions. Then we have

| ; | (40) | |||

| ; | (41) | |||

| . | (42) |

As we know, for any convex optimization with differentiable objective and constraint functions, any point that satisfies the KKT conditions (under Slater’s constraint qualification) must be primal and dual optimal. Therefore, must obey . Note that the pair of points that satisfies the KKT conditions is unique. To prove the optimal solution holds for (37), we can equivalently prove that the KKT conditions (40)-(42) hold for with and . It is further equivalent to prove that

| (43) |

holds for . Following from Lemma A.2 with the fact that , there must exist an unique such that

| (44) |

holds for any . Thus one has

| (45) |

where the first equality follows from (44) with ; the second equality holds because where is the null space of defined by . Combining (43) and (45) yields

| (46) |

where is invertible according to Lemma A.4. Recall that is the sample covariance matrix defined by

where are the samples independently drawn from LGMRF in Definition 2.1. According to the density function of LGMRF defined in (3), we get for . Therefore, is symmetric and obeys . It is easy to verify that , where is the range space of defined by . Hence, there must exist a such that . Thus . One further obtains

Then a simple calculation yields

| (47) |

Next, we construct a matrix with and have

| (48) |

where the first equality follows from (46); the second equality follows from (47); the third equality holds because and then one has .

Let be the normalized matrix of , where is a diagonal matrix containing the diagonals of . Notice that each diagonal element of is . Next, we will prove that, under some conditions, is an inverse -matrix, that is, is a -matrix. We say is an -matrix if

| (49) |

where is an element-wise non-negative matrix and , the spectral radius of . According to (48), one has

and

Define , , and . By the definition of , the lower bound and upper bound of the elements off the diagonal of can be obtained as below,

| (50) |

and

| (51) |

Define by . According to Lemma A.12, if and with , then is an inverse -matrix. We can see, provided that and the inequalities

| (52) |

hold, then one has

where the first inequality follows from . Therefore, if and (52) holds, then is an inverse -matrix.

Next, we will prove that if with , then and (52) holds. Substituting into (50) yields . Then it is clear that and . By comparing and defined in (50) and (51), respectively, one has . A simple algebra yields

where the first inequality follows from and because and . It is easy to verify that is large enough to establish the second inequality. Therefore, all the inequalities in (52) hold.

Consequently, by Lemma A.12, we conclude that is an inverse -matrix when with . Therefore, is an -matrix. Notice that the elements off the diagonal of an -matrix are non-positive according to (49). As a result, the elements off the diagonal of are non-positive, implying that the elements off the diagonal of are also non-positive, because is positive definite and thus the diagonal elements of are positive. The application of (44) with yields

One further obtains

where . Therefore, we establish

concluding that (43) holds for . Note that because , and , where following from and each diagonal element since is positive semi-definite.

A.3 Proof of Theorem 3.5

Proof.

Let . According to the definition of in (10), must obey , for any and .

Next, we will show that is positive semi-definite for any by the Gershgorin circle theorem (Varga, 2004). Given a matrix with entries . Let be the sum of the absolute values of the non-diagonal entries in the -th row. Then a Gershgorin disc is the disc centered at on the complex plane with radius . Gershgorin circle theorem (Gershgorin, 1931) shows that each eigenvalue of lies within at least one of the Gershgorin discs. For any , holds for each because and for any . For any given eigenvalue of , by Gershgorin circle theorem, there must exist one Gershgorin disc such that

| (54) |

indicating that . Note that the eigenvalues of are real since is symmetric. Therefore, one has

| (55) |

Finally, we will prove that , for any . On one hand, if , then admits the eigenvalue decomposition , where and is a diagonal matrix with the diagonal elements . Here are the nonzero eigenvalues of and is a matrix whose columns are the corresponding eigenvectors of . Note that the nonzero eigenvalue because . Therefore, one has . On the other hand, if , then because is full rank and is rank one. Furthermore, because . Therefore, we conclude that , completing the proof. ∎

A.4 Proofs of Theorem 4.4 and Corollary 4.5

Proof.

We first prove Theorem 4.4. Take the regularization parameter for some , and the sample size

| (56) |

where is a constant defined in Lemma A.9. Notice that the sample size in (56) satisfies the conditions on the number of samples in Lemmas A.5, A.6, A.7 and A.8. Recall that the initial point of Algorithm 1 satisfies .

Define an event . According to Lemma A.8, holds with probability at least . Under the event , one applies Lemma A.7 and obtains, for any ,

By induction, if for any with , then

| (57) |

Taking , and , one obtains

Under the event , can be bounded by

| (58) |

Therefore, under the event , which holds with probability at least , one has

Next, we prove the Corollary 3.9. Under the event , one applies Lemma A.7 and obtains

| (59) |

holds for any . Taking , and , by (57) one has

Similarly, according to (58), one obtains,

holds at least .

To apply Lemma A.5, we first check the necessary conditions of the lemma. Let satisfy , . Notice that for by Assumption 4.1. According to (35), , where . For any , one has

where the first inequality holds because for any , and is non-increasing according to Assumption 4.1; the second inequality directly follows from Assumption 4.1. Hence one has

One also obtains by Lemma A.6, and by the definition of . Therefore, one can apply Lemma A.5 with and and obtains

If , a simple algebra yields

| (61) |

Taking , and combining (60) and (61) together, we can conclude that

completing the proof. ∎

A.5 Proof of Theorem 4.6

Proof.

The proof consists of two prats: In Part I, we prove that the sequence will converge to the oracle estimator and under some conditions; In part II, we bound the probabilities that the conditions introduced in Part I hold.

Part I

The sequence is established by solving a sequence of sub-problems

| (62) |

We first show that the global minimizers of the optimization problems (21) and (62), i.e., and , exist and are unique with probability one. The uniqueness can be established by proving that the optimization problems (21) and (62) are strictly convex, and the existence can be guaranteed by proving that the (21) and (62) are coercive. The proof procedure is similar to the proof of the uniqueness and existence of the minimizer of the optimization (37) in Theorem 3.1, except one main modification in (38) for proving the coercivity. Let

Then can be be lower bounded by

| (63) |

where . Note that the sample covariance matrix is computed by , where are samples drawn from -dimensional LGMRF with the parameters . By calculation, one obtains, for any ,

| (64) |

where satisfy and . Define a set , where . Obviously, has measure zero in for any . Therefore, for , one has

| (65) |

In other words, in (63) with probability one. The other proof procedure is similar to that for the case of the optimization (37), and thus is omitted.

Define two events on that

| (66) |

and

| (67) |

Next, we will prove by induction that for any on the conditions that the events and hold.

We first prove that . Under the assumption that , for any , we have

Thus one has

| (68) |

On the other hand, for any ,

which yields by Assumption 4.1. Therefore, in the first iteration, we can rewrite (62) as

| (69) |

For any , one has

| (70) |

where the second inequality follows from the facts that which can be established by the KKT conditions as follows. Let be any pair of points that satisfies the KKT conditions of (21). Then one has

| (71) |

It is easy to verify that

For any , we obtain

| (72) |

where the first inequality follows from (70), the second equality follows from (71), and the last inequality is established by

which follows from (68) together with the event and the fact that . Therefore, we conclude that the objective function in (69) achieves the optimal value when . By the uniqueness of , we obtain that

| (73) |

Assume holds for . We will show that also holds. Under the event defined in (67), one has

| (74) |

Therefore, we can rewrite (62) as

| (75) |

Note that for any , and thus

Under the event , similar to (72),

holds for any . With the same argument for (73), we have

To sum up, under the events and , we obtain that

| (76) |

By the uniqueness of , we can conclude that the sequence converges to . Following from (76), we obtain

| (77) |

Under the event , there is no zero element for in the set . Therefore, together with (76), we further obtain

| (78) |

Part II

In this part, we bound the probability that the events and hold.

By the inequality

| (80) |

we can bound instead.

Define a continuous map ,

where the entries of in equal to and the entries in equal to zero. Define

| (81) |

where is defined by

| (82) |

Note that is a convex compact set. We say maps the set to itself, if

| (83) |

holds. In the following, we will prove that with the assumption that (83) holds. After that, we will turn to prove (83).

By Brouwer’s Fixed Point Theorem, there exists a such that , i.e.,

where with entries in equal to and entries in equal to zero. Then one further obtains

We construct an such that

Take . Note that and because

We can verify that the pair satisfies all the KKT conditions in (71). By the uniqueness of , one has , thus and . Therefore, under (79), we can establish that

completing the proof.

Next, we will prove (83). By the sub-multiplicativity of the norm , we have , for any . Thus, for any with and , one has

| (84) |

where we use the definition of in (22), and the fact that the graph associated with has at most edges for each node. The last inequality in (84) follows from (79). As a result, we have the convergent matrix expansion,

| (85) |

where . We can write as

where is the unit vector with in position and zeros elsewhere. Then one obtains

where for . Note that , implying that for any . Then one has

| (86) |

Define

| (87) |

Together with (85), (86) and (87), one has

| (88) |

We bound as below,

| (89) |

We need to bound the terms , and . The term is a constant term and equals to defined in (22). The term can be written as according to (81). The term can be bounded as below,

| (90) |

where the first inequality follows from the fact that holds for any ; the second inequality is established by the inequality that for any and ; the forth inequality follows from and the sub-multiplicativity of ; the last inequality follows from by Lemma A.3, , and . We further have

| (91) |

where the last inequality follows from (84). Together with (90) and (91), we obtain

| (92) |

Thus, in (89) can be bounded by

Following from (79), we obtain

Therefore, we have established (83).

Next, we will show that holds under the conditions that

| (93) |

and

| (94) |

We have

Then we get

| (95) |

Recall that . By (88), we can obtain

| (96) |

where with . Note that is also a convergent matrix series under the condition (79). Similarly, we can obtain

| (97) |

Combining (96) and (97), we get

| (98) |

The KKT conditions in (71) together with yield , and thus

Then, we have

| (99) |

Together with (98) and (99), we obtain

| (100) |

Note that (92) also holds for . Thus, we have

| (101) |

where the last inequality follows from (93). Using the definition of in (22) and combining (100) and (101) yield

According to (95), we obtain

| (102) |

where the first and second inequalities follow from (93) and (94), respectively.

To sum up, we conclude that and hold under the conditions in (93) and (94). To guarantee the (93) hold with a high probability, we impose the condition that , where is a constant depending on the underlying true graph. Then (93) could be written as

| (103) |

Note that . Thus, to guarantee that , the sample size should be lower bounded by

Finally, we compute the probability that (94) and (103) hold. We apply Lemma 5.8 and obtain

with the condition on the sample size that

Similarly, we can get

with the condition on the sample size that

Therefore, (94) and (103) hold with probability at least , with the sample size lower bounded by

∎

A.6 Proof of Theorem 4.7

Proof.

Take the regularization parameter for some , and the sample size

| (104) |

where is a constant defined in Lemma A.9. The sample size in (104) satisfies the conditions on the number of samples in Lemmas A.5, A.6, A.7 and A.8. Define an event

According to Lemma A.8, the event holds with probability at least . Recall that the initial point of Algorithm 1 satisfies .

Define a local region around

where is defined in (20) and , and . Notice that must be nonempty because according to Theorem 3.5 together with the fact that contains the weights from a connected graph. According to Lemma A.10, is -strongly convex and -smooth in with and . Therefore, as defined in (17) is also -strongly convex and -smooth in , for any .

We define another local region

Next, we will prove that under the event ,

holds for any , where is defined in (18). Before applying Lemma A.5, we first check the necessary conditions of the lemma. Let satisfy , . One has for by Assumption 4.1. According to the definition of in (35), one has . For any , one further has

where the first inequality holds because for any , and is non-increasing by Assumption 4.1; the second inequality follows from Assumption 4.1. Hence one obtains

Under the event , holds for any following from Lemma A.6. Therefore, all the conditions in Lemma A.5 are satisfied with and , and one has

| (105) |

where the first inequality follows from (171) and the third inequality is established by plugging with . The (105) indicates that

| (106) |

holds for any . For any ,

indicating that . Consequently, one has

| (107) |

Therefore, is -strongly convex and -smooth in , for any .

Then we will establish that the whole sequence returned from Algorithm 2 is within the region for any . We first prove that for any and . Any returned from Algorithm 2 must obey because of the projection . Notice that must be positive semi-definite for any , because is positive semi-definite for any according to (55), and has an unique nonzero eigenvalue with the eigenvector orthogonal to the row and column spaces of . Therefore, any will lead to be singular and positive semi-definite, and thus the objective function will go to infinity. On the other hand, one has

| (108) |

where the first inequality is established by the backtracking exit inequality in Algorithm 2; the second inequality is established by

where . The equality follows from the updating rule and the inequality holds because of the projection theorem together with the fact that . More specifically, let be a closed and convex set. Then is the projection of on , if and only if one can establish

| (109) |

The (108) indicates that the objective function is not increasing with the increase of , and consequently one has . Hence, if is upper bounded, then is also upper bounded and thus . Notice that Algorithm 2 takes the initial point , which is the minimizer of the optimization (18). Thus, is upper bounded. is also upper bounded following from Assumption 4.1. Therefore, is upper bounded for any . Then, we can conclude that

| (110) |

holds for any and .

We will prove by induction that the sequence is in for any . For any given , when , one has

where the second inequality follows from (106). Together with (110), we conclude that . Suppose for some . Then one obtains

| (111) |

On the other hand, one has

| (112) |

where the first inequality follows from the backtracking exit inequality, and is -strongly convex in the region and . The last equality is obtained by plugging

The second inequality in (112) follows from

where and . The second equality follows from the updating rule and the inequality is established by the projection theorem as shown in (109), together with . Substituting into (112), one obtains

| (113) |

Substituting (113) into (111) yields

indicating that is within the region . Together with (110), we conclude that completing the induction. Therefore, the whole sequence is in , for any .

Finally, we will establish the lower bound of the step size for each iteration. Since is -smooth in , for any and in , one has

Thus any must satisfy the backtracking exit condition and the backtracking line search must terminate when with , implying that . Therefore, we establish

where , completing the proof.

∎

A.7 Proof of Theorem 5.1

Proof.

Before proving Theorem 5.1, we first establish the boundedness of the sequence generated by Algorithm 3, and the monotonicity of .

Now we begin to prove by induction that the sequence generated by Algorithm 3 is bounded. Let and be the initialization of the sequences and , respectively, and and are bounded. Recall that the sequence is established by

| (114) |

where is the eigenvalue decomposition of . When , is bounded because of the boundedness of and , and thus is bounded. The sequence is established by solving the sub-problems

| (115) |

The problem (115) is solved by majorization minimization framework. Thus the objective function value is monotonically decreasing during iterations and is a stationary point of (115). Let . We can check that is coercive, and thus is bounded. Finally, is updated by

| (116) |

Then we can see that is also bounded, because both and are bounded. Therefore, is bounded.

Assume that is bounded for some , i.e., each term in is bounded under -norm or Frobenius norm. Following from (114), we can obtain that is bounded. The coercivity of can lead to the boundedness of . Then is also bounded by (116). Thus, is bounded, completing the induction. Therefore, we conclude that the sequence is bounded, and thus there must exist at least one limit point of .

Next, we show that the sequence generated by Algorithm 3 is lower bounded, and decreasing for a sufficiently large .

According to (26), we have

| (117) |

By the definition of , the term is lower bounded. The boundedness of can establish that and are lower bounded. Thus is lower bounded.

For any , we have

| (118) |

where the inequality follows from the fact that

On the other hand, we obtain

| (119) |

where is Lipschitz continuous gradient constant of . The second equality follows from , the first inequality is established by the fact that is a stationary point of the problem

| (120) |

Let . The set of the stationary points of (120) is defined by

| (121) |

By setting and in (121), we have

| (122) |

The first inequality in (119) follows from (122). The last inequality in (119) is due to the fact that is a concave function and has -Lipschitz continuous gradient such that

| (123) |

holds for any . By calculation, we get that if is sufficiently large such that

| (124) |

then, together with (118), we obtain that

| (125) |

holds for any . Therefore, the sequence is decreasing.

Now we are ready to prove Theorem 5.1. We have proved that the sequence is bounded. Therefore, there exists at least one convergent subsequence , which converges to a limit point denoted by . We have also proved that the sequence is monotonically decreasing and lower bounded, and thus is convergent. Note that the function is continuous over the set . We can get

| (126) |

By taking in (125), we have . For any subsequence, we also have

| (127) |