MS-OPT-20-01985.R2

Neufeld, Papapantoleon, Xiang

Model-free bounds for multi-asset options and their exact computation

Model-free bounds for multi-asset options using option-implied information and their exact computation

Ariel Neufeld \AFFDivision of Mathematical Sciences, Nanyang Technological University, 21 Nanyang Link, 637371 Singapore, \EMAILariel.neufeld@ntu.edu.sg \AUTHORAntonis Papapantoleon \AFFDelft Institute of Applied Mathematics, TU Delft, 2628 Delft, The Netherlands & Institute of Applied and Computational Mathematics, FORTH, 70013 Heraklion, Greece, \EMAILa.papapantoleon@tudelft.nl \AUTHORQikun Xiang \AFFDivision of Mathematical Sciences, Nanyang Technological University, 21 Nanyang Link, 637371 Singapore, \EMAILqikun001@e.ntu.edu.sg

We consider derivatives written on multiple underlyings in a one-period financial market, and we are interested in the computation of model-free upper and lower bounds for their arbitrage-free prices. We work in a completely realistic setting, in that we only assume the knowledge of traded prices for other single- and multi-asset derivatives, and even allow for the presence of bid–ask spread in these prices. We provide a fundamental theorem of asset pricing for this market model, as well as a superhedging duality result, that allows to transform the abstract maximization problem over probability measures into a more tractable minimization problem over vectors, subject to certain constraints. Then, we recast this problem into a linear semi-infinite optimization problem, and provide two algorithms for its solution. These algorithms provide upper and lower bounds for the prices that are -optimal, as well as a characterization of the optimal pricing measures. These algorithms are efficient and allow the computation of bounds in high-dimensional scenarios (e.g. when ). Moreover, these algorithms can be used to detect arbitrage opportunities and identify the corresponding arbitrage strategies. Numerical experiments using both synthetic and real market data showcase the efficiency of these algorithms, while they also allow to understand the reduction of model risk by including additional information, in the form of known derivative prices.

model-free bounds, option-implied information, multi-asset options, bid–ask spread, cutting plane method, no-arbitrage gap, arbitrage detection

1 Introduction

The classical paradigm in finance and theoretical economics assumes the existence of a model that provides an accurate description of the evolution of asset prices, and all subsequent computations about hedging strategies, exotic derivatives, risk measures, and so forth, are based on this model. However, academics, practitioners, and regulators have realized that all models provide only a partially accurate description of this reality, thus, either methods need to be developed in order to aggregate the results of many models, or approaches have to be devised that allow for computations in the absence of a specific model. The first approach led to the introduction of robust methods in asset pricing and no-arbitrage theory, see e.g. Bayraktar et al. (2015), Beissner (2017), Beissner and Riedel (2019), Bouchard and Nutz (2015), Bouchard et al. (2019), Dana and Riedel (2013), Epstein and Ji (2013), Maruhn (2009), Neufeld and Nutz (2013), Possamaï et al. (2013), Rigotti and Shannon (2005), and Yan et al. (2018), while the second one led to model-free methods in asset pricing and no-arbitrage theory, see e.g. Acciaio et al. (2016), Bartl et al. (2019), Bartl et al. (2020), Beiglböck et al. (2013), Bertsimas and Bushueva (2006), Burzoni et al. (2016), Burzoni et al. (2019), Burzoni et al. (2021), Cheridito et al. (2017), Davis et al. (2014), Dolinsky and Soner (2014a), Dolinsky and Neufeld (2018), Galichon et al. (2014), Henry-Labordère (2013), Hobson (1998), Hu et al. (2019), Lütkebohmert and Sester (2019), and Riedel (2015).

In this work, we consider derivatives written on multiple underlyings in a one-period financial market, and we are interested in the computation of upper and lower bounds for their arbitrage-free prices. We work in a completely realistic setting, in that we only assume the knowledge of traded prices for other single- and multi-asset derivatives, and even allow for the presence of bid–ask spread in these prices. In other words, we work in a model-free setting in the presence of option-implied information, and make no assumption about the probabilistic evolution of asset prices (i.e. their marginal distributions) or their dependence structure.

The computation of bounds for the prices of multi-asset options, most often basket options, is a classical problem in the mathematical finance literature and has connections with several other branches of mathematics, such as probability theory, optimal transport, operations research, and optimization. In the most classical setting, one assumes that the marginal distributions are known and the joint law is unknown; this framework is known as dependence uncertainty. In this framework, several authors have derived bounds for multi-asset options using tools from probability theory, such as copulas and Fréchet–Hoeffding bounds, see e.g. Chen et al. (2008), Dhaene et al. (2002a, b), and Hobson et al. (2005a, b). These bounds turned out to be very wide for practical applications, hence recently there was an interest in methods that allow for the inclusion of additional information on the dependence structure, in order to reduce this gap. This led to the creation of improved Fréchet–Hoeffding bounds and the pricing of multi-asset options in the presence of additional information on the dependence structure, see e.g. Tankov (2011), Lux and Papapantoleon (2017), and Puccetti et al. (2016).

The setting of dependence uncertainty is intimately linked with optimal transport theory, and its tools have also been used in order to derive bounds for multi-asset option prices, see e.g. Bartl et al. (2017) for a formulation in the presence of additional information on the joint distribution. More recently, De Gennaro Aquino and Bernard (2020), Eckstein and Kupper (2019), and Eckstein et al. (2021) have translated the model-free superhedging problem into an optimization problem over classes of functions, by extending results in optimal transport, and used neural networks and the stochastic gradient descent algorithm for the computation of the bounds.

Ideas from operations research and optimization have also been applied for the computation of model-free bounds in settings that are closer to ours, and do not necessarily assume knowledge of the marginal distributions (or, equivalently, knowledge of call option prices for a continuum of strikes). Bertsimas and Popescu (2002) consider the computation of the model-free bounds on a single-asset call option given the moments of the underlying asset price as well as the model-free bounds on a single-asset call option given other single-asset call and put option prices. In addition, they also consider specific conditions under which the model-free bounds on a multi-asset option can be theoretically computed in polynomial time. d’Aspremont and El Ghaoui (2006) consider a framework where the prices of forwards and single-asset call options are known, and compute upper and lower bounds on basket options prices using linear programming. In the more general case where the prices of other basket options are also known, they derive a relaxation to the problem which can be solved using linear programming. This work was later extended by various authors. Peña et al. (2010b) improve the results of d’Aspremont and El Ghaoui (2006) when computing the lower bounds on basket options prices in two special cases: (i) when the number of assets is limited to two and prices of basket options are known; and (ii) when the prices of only a forward and a single-asset call option per asset are known. Peña et al. (2012) develop a linear programming-based approach for the problem of computing the upper price bound of a basket option given bid and ask prices of vanilla call options. Peña et al. (2010a) study the problem of computing the upper and lower bounds on basket and spread option prices when the prices of other basket and spread option prices are known. Their approach involves solving a large linear programming problem via the Dantzig–Wolfe decomposition in which the corresponding subproblem is solved using mixed-integer programming. Compared to d’Aspremont and El Ghaoui (2006), Peña et al. (2010a), and Peña et al. (2010b, 2012), the numerical methods we develop in Section 3 apply to settings that are much more general, where the derivative being priced and the traded derivatives with known prices can be any continuous piece-wise affine function (including, but not limited to, vanilla, basket, spread, and rainbow options, as well as any linear combination of these options). Moreover, as we demonstrate in Section 4, these methods are able to efficiently compute the price bounds in high-dimensional scenarios, e.g. when 60 assets are considered. This is considerably higher compared to existing studies. Daum and Werner (2011) develop a discretization-based algorithm for solving linear semi-infinite programming problems that returns a feasible solution, and apply the algorithm to compute the upper bounds on basket or spread options prices when single-asset call, put, and exotic options prices are known. Cho et al. (2016) develop methods similar to Daum and Werner (2011) but for lower bounds on basket or spread options prices. The algorithm we introduce in Section 3.1 takes a similar approach, but is able to solve the problem when the prices of multi-asset options with a more general class of payoff functions are known. Kahalé (2017) uses a central cutting plane algorithm to compute the super- and sub-replicating prices of financial derivatives using hedging portfolios that consist of other financial derivatives in the multi-period discrete-time setting. The algorithm only works under the assumption that the underlying state space (i.e. the space of asset prices) is finite. When the state space is infinite, it is discretized before applying the central cutting plane algorithm, and the discretization error is analyzed. However, the approach of discretizing the state space has limited applicability to the multi-dimensional settings (i.e. with multiple underlying assets) due to the curse of dimensionality. The algorithm we develop in Section 3.2 is also based on a central cutting plane algorithm, but it allows us to efficiently compute model-free price bounds in high-dimensional state spaces for financial derivatives that depend on multiple assets.

Our contributions are three-fold: Firstly, we provide a fundamental theorem of asset pricing for the market model described above, as well as a superhedging duality, that allows to transform the abstract maximization problem over probability measures into a more tractable problem over vectors, subject to certain constraints. Secondly, we recast this problem into a linear semi-infinite optimization problem, and provide two algorithms for its solution. These algorithms provide upper and lower bounds for the prices of multi-asset derivatives that are -optimal, as well as a characterization of the optimal pricing measures. These algorithms are efficient and allow the computation of bounds in high-dimensional scenarios (e.g. when ), that were not possible by previous methods. Moreover, these algorithms can be used to detect arbitrage opportunities in multi-asset financial markets and to identify the corresponding arbitrage strategies. Thirdly, we perform numerical experiments using synthetic data as well as real market data to showcase the efficiency of these algorithms. These experiments allow us to understand the reduction of the no-arbitrage gap, i.e. the difference between the upper and lower no-arbitrage bounds, by including additional information in the form of known derivative prices. The no-arbitrage gap directly reflects the model-risk associated to a particular derivative and the information available in the market. The numerical experiments show a decrease of the model-risk by the inclusion of additional information, although this decrease is not uniform and depends on the form of information and the specific structure of the payoff functions.

This paper is organized as follows: In Section 2, we present the modeling framework, state the no-arbitrage theorem and the superhedging duality, and discuss a setting that is relevant for practical applications. In Section 3, we present the algorithms that have been developed for the computation of model-free bounds and state theorems that show the validity of these algorithms. In Section 4, we discuss various numerical experiments using both synthetic and real market data that show the efficiency of the algorithms and the reduction of model-risk by the inclusion of additional information in the form of known derivative prices. We also perform a numerical experiment to show the ability of the algorithms to detect arbitrage opportunities. Appendix 5 contains the proofs of the main results of this paper. The online appendices contain additional remarks and discussions about the theoretical results, the numerical methods, and the numerical experiments, as well as the proofs of the results in Section 2.

2 Duality in the presence of option-implied information

In this section, we introduce a general framework for a model-free, one-period, financial market where multiple assets and several single- and multi-asset derivatives written on these assets are traded simultaneously. Model-free means that we will not make any assumption about the probabilistic model that governs the evolution of asset prices. Instead, we will utilize information available in the financial market and implied by the prices of single- and multi-asset derivatives. We will provide both a fundamental theorem and a superhedging duality in this setting, where our results and proofs are inspired by Bouchard and Nutz (2015). Moreover, we will describe concrete examples of this framework that are of practical interest.

Throughout this work, all vectors are column vectors unless otherwise stated. We denote vectors and vector-valued functions by boldface symbols. For a vector in a Euclidean space, let denote the -th component of . For simplicity, we also use to denote when there is no ambiguity. Let denote the Euclidean norm of . Let denote the Euclidean inner product of two vectors and . We denote by the -th standard basis vector of a Euclidean space, by the vector with all entries equal to zero, i.e. , and by the vector with all entries equal to one, i.e. . We call a subset of a Euclidean space a polyhedron or a polyhedral set if it is the intersection of finitely many closed half-spaces. We call a subset of a Euclidean space a polytope if it is a bounded polyhedron.

Let be a Polish space equipped with its Borel -algebra denoted by . Let denote the set of Borel probability measures on . Let be Borel measurable for , for some fixed , and let denote the vector-valued Borel measurable function where the -th component corresponds to . Let be such that for . Let and define as

| (1) |

where . Let denote the function .

We make the following no-arbitrage assumption. {assumption}[No-Arbitrage] The following implication holds for any :

where the inequality and the equality are both understood as point-wise.

Remark 2.1

Assumption 2 is inspired by the no-arbitrage assumption introduced in Definition 1.1 of Bouchard and Nutz (2015), where the set of possible models for the market is , i.e. all Borel probability measures, and a single time step is considered. The difference between Assumption 2 and the no-arbitrage assumption in Bouchard and Nutz (2015) is that the price of a financial derivative in the present work is not a singleton but can lie anywhere between the corresponding bid and ask prices. Note that there are other notions of no-arbitrage that are weaker than Assumption 2, for example the “no uniform strong arbitrage” assumption in Definition 2.1 of Bartl et al. (2017).

Let be a Borel measurable function, and define the functional as follows:

| (2) |

Let be defined as follows:

The main results of this section are the following fundamental theorem and superhedging duality, whose proofs are provided in Appendix 9.

Theorem 2.2 (Fundamental Theorem)

The following are equivalent:

-

(i)

Assumption 2 holds.

-

(ii)

For all , there exists such that .

Theorem 2.3 (Superhedging duality)

Remark 2.4

No-arbitrage conditions and Fundamental Theorems of Asset Pricing are essential tools to understand and characterize the viability of a model in a financial market. They have to be tailored to the modeling assumptions and the specific applications in mind, hence a multitude of comparable statements exist in the literature. Analogously to our no-arbitrage condition, the Fundamental Theorem presented in Theorem 2.2 is closely related to the First Fundamental Theorem in Bouchard and Nutz (2015). The main difference is the presence of a bid–ask spread, which means that we cannot exactly reduce our results to their theorem and another proof is needed; this proof is motivated by the results in Bouchard and Nutz (2015). There are several other versions of a Fundamental Theorem in the presence of model uncertainty in the mathematical finance literature; see e.g. Acciaio et al. (2016), Bayraktar and Zhang (2016), Bayraktar et al. (2014), and Burzoni et al. (2021) for discrete time models, and Biagini et al. (2017) and Dolinsky and Soner (2014b) for continuous time ones.

Let us point out that the Fundamental Theorem presented here plays a particular role in conjunction with the numerical methods developed in the next section. More specifically, it provides a sufficient condition for the detection of arbitrage opportunities by numerically testing the violation of the no-arbitrage condition. Moreover, it provides a sufficient condition for repairing derivative prices by removing arbitrage opportunities from the market, in the same spirit as Cohen et al. (2020). These results are novel in the related literature on multi-asset model-free price bounds, and are facilitated by the tailor-made Fundamental Theorem.

Remark 2.5

Superhedging dualities are also classical and essential tools in mathematical finance, typically tailored to specific modeling assumptions and applications. The superhedging duality presented in Theorem 2.3 is motivated by the superhedging theorem in Bouchard and Nutz (2015), with the main difference being once again that we are considering an interval of bid and ask prices instead of a single price. There are multiple comparable duality results or superhedging theorems in various areas of mathematics. In the mathematical finance literature, these results are known as superhedging theorems or (martingale) optimal transport dualities, see e.g. Beiglböck et al. (2013), Acciaio et al. (2016), Bayraktar et al. (2014), Cheridito et al. (2017), and Dolinsky and Soner (2014a). In the operations research literature, these results are known as perfect or strong dualities, see e.g. Bertsimas and Popescu (2002), d’Aspremont and El Ghaoui (2006), Nishihara et al. (2007), and Peña et al. (2010b). These latter dualities are typically based on classical results in mathematical programming, see e.g. Karlin and Studden (1966), and Hettich and Kortanek (1993).

The canonical way to interpret the framework developed above is as follows: when , then there exist underlying risky assets that are traded in the financial market, and represents the (non-negative) prices of the assets at a fixed future date. Investing into a unit of the asset then corresponds to the payoff function for . Moreover, there exist traded derivatives (typically ) with known bid and ask prices , written either on single or on multiple assets. The payoff function of a single-asset derivative depends on the price of only a single asset, i.e. for some and . For example, corresponds to a call option with strike . The payoff function of a multi-asset derivative depends on the prices of multiple assets. For example, corresponds to a basket call option with weight and strike . These derivatives encode all the information available in this market. Specifically, information about the marginals of the probability measures in is implied by the bid and ask prices of single-asset derivatives, while partial information on the joint distribution is implied by the bid and ask prices of multi-asset derivatives.

In this setting, the right-hand side of (3) is the model-free upper bound for the price of a derivative with payoff function written on these assets. The optimization takes place over all probability measures that are compatible with the option-implied information, i.e. all probability measures that produce prices for a given option within its respective bid and ask prices. The duality result in (3) states that this model-free upper bound equals the least superhedging price achieved by trading in the derivatives according to the strategy , i.e. holding units of cash and units of derivative for , where the minimization takes place over all such that the payoff is dominated, i.e. .

Section 6 in the online appendices contains additional discussions about the duality result, including Example 6.2 which demonstrates that the supremum on the right-hand side of (3) is not necessarily attained, as well as Proposition 6.3 which provides a specific setting in which Assumption 2 holds.

3 Numerical methods for the computation of bounds

The superhedging duality in Theorem 2.3 allows to transform the abstract maximization problem over probability measures into a more tractable minimization problem over vectors that satisfy certain constraints. The aim of this section is to develop novel numerical methods for the exact and efficient computation of upper and lower bounds on . More specifically, we will develop methods for the computation of upper and lower bounds and which are -optimal, i.e.

for . Our methods allow us to also characterize the optimal pricing measure associated with the primal maximization problem. Therefore, we provide a complete solution to both optimization problems, and can characterize the solution both in terms of -optimal hedging strategies and in terms of the optimal pricing measure.

Let and . The minimization problem in (2) can be equivalently formulated as a linear semi-infinite programming (LSIP) problem, i.e. as an optimization problem with a linear objective and an infinite number of linear constraints, one for each ,

| (4) | ||||

LSIP problems are classical optimization problems that have been thoroughly studied in the related literature; see e.g. Goberna and López (1998, 2018). More general semi-infinite programming problems, including non-linear semi-infinite programming problems and generalized semi-infinite programming problems (where the index set can depend on the decision variable) have also been studied in the literature; see e.g. Reemtsen and Rückmann (1998), López and Still (2007), and Stein (2012). In this section, we develop novel algorithms tailored to solving (4) under different assumptions on the space , and the functions and .

Let us first introduce the notion of CPWA functions and their radial functions.

Definition 3.1 (Continuous piece-wise affine function and its radial function)

We call a function a CPWA function if it can be represented as

| (5) |

where , for , and , , for . The radial function of , denoted by , is defined as

The class of CPWA functions contains many popular payoff functions in finance, including vanilla call and put options, basket options, spread options, call/put-on-max options, call/put-on-min options, best-of-call options, etc. We refer the reader to Section 7.1 in the online appendices for the CPWA representations of these payoff functions as well as some properties of CPWA functions.

3.1 CPWA payoff functions on unbounded domains

In the first setting, we work under the following assumptions. {assumption}[Setting 1] We assume the following:

-

(i)

;

-

(ii)

and are CPWA functions on ;

-

(iii)

and .

In the sequel, for notational reasons, we use in place of when is a subset of the Euclidean space. Let us introduce the notion of the slack function for the LSIP problem in (4).

Definition 3.2 (Slack function)

Let be fixed, and denote the slack function of the LSIP problem in (4) by , which is defined as: .

To numerically solve the LSIP problem (4), let us now introduce the cutting plane discretization method, detailed in Algorithm 1, which is inspired by the Conceptual Algorithm 11.4.1 in Goberna and López (1998). In Line 1 of Algorithm 1, the so-called “radial constraints” are generated using Algorithm 4 in Section 7.2 of the online appendices. The purpose of this step is to generate sufficient and necessary constraints on to guarantee that the slack function is bounded from below. We refer the reader to Section 7.2 for a detailed explanation about this step. In Line 1 and 1, the global minimization problem is solved by formulating it into a mixed-integer linear programming (MILP) problem in (7.8), as discussed in Lemma 7.13. The MILP problem can be solved efficiently by state-of-the-art solvers such as Gurobi (Gurobi Optimization, LLC (2020)), that uses the so-called Branch-and-Bound (BnB) algorithm. We refer the reader to Remark 11 for a brief description of the BnB algorithm.

We name Algorithm 1 the exterior cutting plane (ECP) method, since every constraint (also known as cut) generated in Line 1 does not restrict the feasible set of (4), hence is exterior to the feasible set. We refer the reader to Section 7.2 for detailed discussions about various aspects of Algorithm 1. Specifically, Remark 7.16 explains the inputs of Algorithm 1, and Remark 7.17 discusses the differences between Algorithm 1 and the Conceptual Algorithm 11.4.1 in Goberna and López (1998). Under the assumption that the inputs of Algorithm 1 are specified according to Remark 7.16, Theorem 3.3 below shows the properties of Algorithm 1, whose proof is provided in Appendix 5.1.

Theorem 3.3 (Properties of Algorithm 1)

Remark 3.4

In Section 3.2, under the more restrictive assumption that for some 111 (see Assumption 3.2), we show that Algorithm 1 also produces an -optimal solution to the right-hand side of (3), which corresponds to the most extreme pricing measure in the original model-free superhedging problem. This will be explained in detail in Corollary 3.6.

3.2 CPWA payoff functions on bounded domains

In the second setting, we adopt similar but more restrictive assumptions than in the first one.

[Setting 2] We assume the following:

-

(i)

for ;

-

(ii)

and are CPWA functions on ;

-

(iii)

and .

Let us introduce a version of the accelerated central cutting plane (ACCP) method inspired by Betrò (2004), detailed in Algorithm 2. In Algorithm 2, we maintain and update a sequence of lower bounds of , a sequence of upper bounds of , and polytopes in that are denoted by , which have the form

| (6) | ||||

where , specify a bounding box, and specify the lower and upper bounds on , and specifies a collection of feasibility constraints. In Algorithm 2, is between the lower bound and the upper bound , and is used as a speculative upper objective cut. The idea of Algorithm 2 is that is a non-decreasing sequence of lower bounds that approach from below while is a non-increasing sequence of upper bounds that approach from above. These facts will be made clear later in Theorem 3.5. Algorithm 2 has various advantages over Algorithm 1. Most importantly, the MILP problem in Line 2 of Algorithm 2 only needs to be solved approximately with a large error tolerance, and some linear constraints are removed in Line 3 to make solving the LP problem in Line 2 faster. We refer the reader to Betrò (2004) and Section 11.4 of Goberna and López (1998) for further discussions.

A crucial step of Algorithm 2 is to compute the Chebyshev center, that is, the center of the largest inscribed ball, of the polytope in Line 2. It is well-known that the Chebyshev center of a polytope can be computed by solving an LP problem (see, for example, the Conceptual Algorithm 11.4.2 of Goberna and López (1998)).

We refer the reader to Section 7.3 for detailed discussions about various aspects of Algorithm 2. Specifically, Remark 7.19 explains its inputs, and Remark 7.20 discusses the differences between Algorithm 2 and the ACCP algorithm by Betrò (2004). Assuming that the inputs of Algorithm 2 are specified according to Remark 7.19, Theorem 3.5 below shows the properties of Algorithm 2, whose proof is provided in Appendix 5.2.

Theorem 3.5 (Properties of Algorithm 2)

Theorem 3.5(iii) explicitly provides a pricing measure which is an -optimal solution to the original model-free superhedging problem. The ECP method (Algorithm 1) is also applicable in Setting 2 with Line 1 removed. It has the same property as Theorem 3.5(iii), which is detailed in the next corollary and proved in Appendix 5.2.

Corollary 3.6

Remark 3.7

Under Assumptions 3.1 and 3.2, the payoff functions of the traded derivatives and the target derivative must be continuous piece-wise affine (CPWA) functions. Thus, the proposed Algorithms 1 and 2 are unable to directly treat derivatives with non-CPWA payoff functions, such as digital and power options. Hence, it would be necessary to first approximate these payoff functions by CPWA functions in order to treat such derivatives using the proposed algorithms. Existing studies have proposed methods to treat non-CPWA payoff functions under more restrictive assumptions. Bertsimas and Popescu (2002) develop a method to compute the price bounds on a single vanilla call option given moments of the underlying asset price. Moreover, in the multi-asset setting, they show that the theoretical time complexity to compute the price bounds is polynomial when all payoff functions are the sum of a CPWA function and a quadratic function, under the assumption that all of the CPWA functions share the same partition of and that the number of polyhedra in the partition is polynomial in the number of assets and the number of traded derivatives. However, this assumption is rather restrictive, since the presence of a fixed number of traded vanilla options written on each asset incurs a partition of in which the number of polyhedra is exponential in the number of assets. In Daum and Werner (2011), a method is developed to compute the price bounds on a basket call option given the prices of vanilla call and put options and the prices of single-asset digital and power options. In this setting, due to the structure of the basket call option, the global optimization problem associated with the LSIP problem can be reduced to a sequence of one-dimensional global optimization problems which can then be efficiently solved.

On the computational side, our assumption that all derivatives have CPWA payoff functions makes it possible to formulate the global minimization problem associated with the LSIP problem (4) into an MILP problem, which then allows us to efficiently solve the LSIP problem in high-dimensional situations (e.g. when ) using state-of-the-art solvers. On the practical side, the exclusion of derivatives with non-CPWA payoff functions does not harm the applicability of the methods we have developed, since most relevant financial derivatives have CPWA payoff functions; see Example 7.1. Let us point out, that many trading platforms of digital options are un-regulated, some adopt ethically questionable practices, while the involved risk is anyhow difficult to manage and hedge. Because of these, the trading of digital options has been banned in many countries including Australia222https://asic.gov.au/about-asic/news-centre/find-a-media-release/2021-releases/21-064mr-asic-bans-the-sale-of-binary-options-to-retail-clients/, accessed: April 18, 2021., Canada333https://www.investmentexecutive.com/news/from-the-regulators/binary-options-ban-takes-effect/, accessed: April 18, 2021., Israel444https://www.reuters.com/article/us-israel-binaryoptions-lawmaking/israel-ban-on-binary-options-gets-final-parliamentary-approval-idUSKBN1CS2L1, accessed: April 18, 2021., and all EU countries555https://www.esma.europa.eu/press-news/esma-news/esma-agrees-prohibit-binary-options-and-restrict-cfds-protect-retail-investors, accessed: April 18, 2021.. Power options, on the other hand, are conceptual financial derivatives that are not traded in real markets.

Remark 3.8

Algorithms 1 and 2 both solve a sequence of constrained optimization problems which are relaxations of the LSIP problem (4) where the semi-infinite constraint is reduced to finitely many constraints. This approach is known as the discretization method. Instead of enforcing these constraints strictly, there is an alternative discretization method in which the constraints are replaced by penalty functions, see e.g. Coope and Price (1998) and Auslender et al. (2009). In this method, a sequence of unconstrained optimization problems are solved. We refer the reader to Auslender et al. (2015) for a comparison of different variants of this method. Another approach that is based on penalization is the integral-type penalization method, see e.g. Borwein and Lewis (1991a, b), Lin et al. (1998), and Auslender et al. (2009). This approach transforms the original LSIP problem into an unconstrained convex optimization problem with an integral-type penalty term, which can be subsequently solved by the stochastic (sub)gradient descent (SGD) algorithm. This is similar to a recent approach adopted for solving optimal transport, martingale optimal transport, and related problems, see e.g. Eckstein et al. (2020), Eckstein and Kupper (2019), Eckstein et al. (2021), and De Gennaro Aquino and Bernard (2020). We have empirically tested the integral-type penalization plus SGD approach in our problem, and found that it is unstable and highly sensitive to the initialization and the hyper-parameter settings of the SGD algorithm.

4 Numerical experiments and results

In this section, we perform three experiments using synthetically generated derivative prices and one experiment using real market data, in order (i) to demonstrate the performance of the proposed approaches under these settings, (ii) to quantify the effect of the additional information from traded multi-asset options on the width of the no-arbitrage gap, i.e. the difference between the upper and lower model-free bounds, and (iii) to show that the proposed algorithms are capable of detecting arbitrage opportunities in a financial market.

We refer the reader to Section 7.4 in the online appendices for details about the implementation of the proposed numerical algorithms. The code used in this work is available on GitHub666https://github.com/qikunxiang/ModelFreePriceBounds. In the subsequent numerical experiments, we consider financial derivatives with the following CPWA payoff functions, whose representations are discussed in Example 7.1.

-

(i)

Trading in the -th asset: .

-

(ii)

Vanilla call option on the -th asset with strike : .

-

(iii)

Basket call option with weights and strike : .

-

(iv)

Spread call option with weights (e.g. ) and strike , e.g.: .

-

(v)

Call-on-max (rainbow) option on assets with strike : .

-

(vi)

Call-on-min (rainbow) option of assets with strike : .

-

(vii)

Best-of-calls option of assets with strikes : .

Moreover, in the numerical experiments with synthetically generated prices, we consider market models of the following type:

-

•

The marginal distribution of the price of an asset at terminal time is a log-normal distribution. Under Setting 2, the -th marginal distribution is truncated to for .

-

•

The dependence structure among the marginals of the assets at terminal time is a -copula with a positive definite correlation matrix and degrees of freedom.

Given these market models, the prices of the single-asset derivatives listed above can be computed in closed-form by taking the discounted expectations of the corresponding payoff functions (w.r.t. a pricing measure). We have assumed that the interest rate is equal to zero, for the sake of simplicity. For the multi-asset derivatives listed above, we approximate their prices via Monte Carlo integration by randomly generating one million independent samples from the copula model and subsequently using these samples to approximate the expectations of the payoff functions. The markets models are also used to compute reference prices for the target derivatives (with payoff ). However, they are not used in the computation of the model-free bounds. In the computation of the bounds, the only information used are the prices of single- and multi-asset derivatives that are synthetically generated from these market models. In order to simulate an incomplete market with the presence of bid–ask spread, we specify multiple market models with different parameters and subsequently take the minimum (resp. maximum) price of a derivative among its prices under all models as the bid (resp. ask) price of the derivative.

Notice that under the market models described above, the pricing measure has strictly positive density with respect to the Lebesgue measure on . Moreover, the way the prices of derivatives are generated guarantees that . Therefore, Assumption 2 holds by Proposition 6.3.

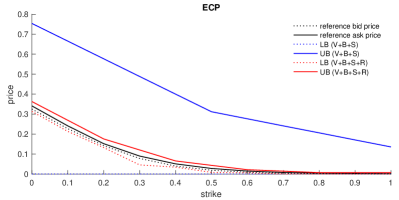

4.1 Experiment 1

In this experiment, we consider a financial market with 5 assets (). We consider Setting 2 (i.e. Assumption 3.2) where . Our goal is to compute the model-free lower and upper price bounds for a call-on-max option with payoff function , where the strike price ranges from 0 to 10 with an increment of . We assume that a total of 439 financial derivatives are traded in the market (). These include:

-

•

The 5 assets .

-

•

Vanilla call options on the 5 assets with strikes .

-

•

Basket call options with the following weights and strikes :

, , , , , , , , , , , . -

•

Spread call options with the following weights and strikes :

, , , , , , , , , , , , , , , , , . -

•

Call-on-max (rainbow) options on the following 6 groups of assets and strikes : , , , , , .

The bid and ask prices of the assets and derivatives are synthetically generated from the market models specified in Section 8.1. We consider five cases, where we use certain subsets of the traded derivatives to compute the model-free lower and upper price bounds for the target derivative:

-

•

Case 1 (denoted as V): we use only vanilla options;

-

•

Case 2 (V+B): we use vanilla and basket options;

-

•

Case 3 (V+B+S): we use vanilla, basket, and spread options;

-

•

Case 4 (V+B+S+R): we use vanilla, basket, spread and call-on-max (rainbow) options;

-

•

Case 5 (V+R): we use vanilla and call-on-max options.

We compute the lower and upper bounds of the call-on-max option with payoff function using the ECP method (Algorithm 1 with Line 1 removed) and the ACCP method (Algorithm 2). The inputs of the two algorithms for this experiment are specified in Section 8.1.

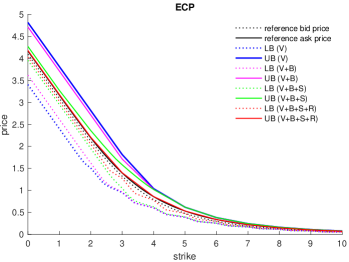

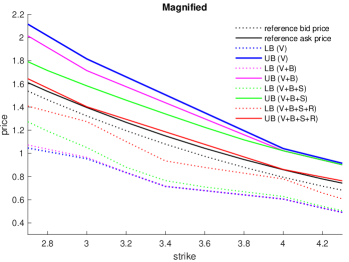

Figure 1 shows the computed lower and upper price bounds of the call-on-max option with different strikes, along with their reference bid and ask prices. Let us point out that the price bounds computed by the two algorithms are almost identical. Indeed, we have checked that all of the absolute differences between the bounds computed by the two algorithms are below . This is a consequence of Theorem 3.3(ii) and Theorem 3.5(ii) and confirms the correctness of the computed price bounds.

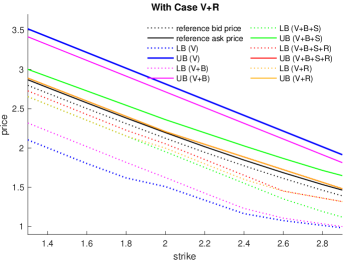

The following observations ensue from the price bounds computed in this example; see Figure 1 for illustrations. (i) The price bounds in the Cases 1–4 are distinct, and the gap between the lower and upper bounds shrinks when the prices of more traded derivatives are added. This means that observing the market prices of more traded derivatives substantially restricts the class of possible pricing measures and reduces the no-arbitrage gap between the bounds. On the dual side (2), this can be equivalently interpreted as having the information about more traded derivatives provides more ways to sub-replicate and super-replicate the given payoff function and thus makes the gap between the sub-replication price and the super-replication price smaller. (ii) The addition of rainbow options (R) in Case 4 results in a significant reduction of the no-arbitrage gap. For example, in Case 4, when the strike is 3.2, the upper bound is higher than the reference ask price and the lower bound is lower than the reference bid price. The respective percentages in Case 3 are and for the upper and lower bounds. The reason is that the traded call-on-max options provide more information to determine the price of the target derivative, since they are similar in structure to the target derivative. This becomes concrete when one considers the dual optimization problem (2), where these call-on-max options offer direct ways to sub-replicate and super-replicate the target payoff, e.g. . (iii) On the other hand, the addition of spread options (Case 3) to vanilla and basket options (Case 2) only yields a significant improvement to the bounds for small strikes (), because spread options with large strikes are not traded in the market. (iv) In all cases, we observe that the no-arbitrage gap is significantly smaller for the (integer) strikes, where traded derivative prices are present. In the bottom left panel of Figure 1, for example, the red line (Case V+B+S+R) almost touches the black line (reference price) for the upper bound at strikes 3 and 4, being only and higher than the respective reference ask prices, while for the lower bound the gap is very small at the same strikes, being and lower than the respective reference bid prices. On the other hand, for the intermediate strikes between 3 and 4, for example when the strike is 3.4, the gap grows to for the upper bound and to for the lower bound. This is due to the fact that all of the traded options in the synthetic financial market have integer strike prices. In the dual optimization problem (2), one needs to interpolate traded options with integer strike prices in order to sub-replicate and super-replicate the call-on-max option with non-integer strike prices. Therefore, whenever possible, practitioners should include in the sub- and super-replicating portfolios derivatives with the same strike price as that of the target derivative, in order to reduce the no-arbitrage gap. (v) As observed from the bottom right panel of Figure 1, the upper bounds in Case 5 (V+R) coincide with the upper bounds in Case 4, while the lower bounds in Case 5 coincide with Case 3 for strikes between 0 and 1.8, coincide with Case 4 for strikes between 2.6 and 10, and fall between Case 3 and Case 4 for strikes between 2 and 2.4. This shows that although the inclusion of more derivatives produces tighter bounds than fewer derivatives, derivatives with similar payoff structure provide more improvement than other derivatives. Therefore, since the computation of price bounds is faster when fewer derivatives are included in the sub- and super-replicating portfolios, practitioners should prioritize including derivatives with payoff structure similar to that of the target derivative when the computation time is limited.

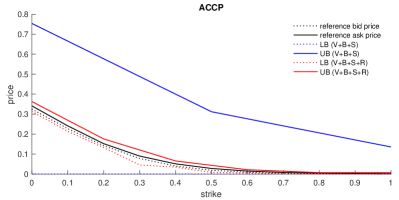

4.2 Experiment 2

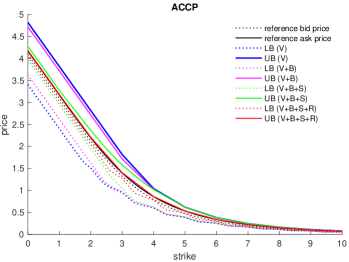

In this experiment, we consider a financial market with 60 assets (). We consider Setting 2 (i.e. Assumption 3.2) where . We use Algorithms 1 and 2 to compute the model-free lower and upper price bounds for a call-on-min option on the first 50 out of the 60 assets, with the strike price ranging from 0 to 1 with an increment of 0.1. The purpose of this experiment is to demonstrate that Algorithms 1 and 2 work even when the number of assets is large.

A total of 400 financial derivatives are traded in the market (). These financial derivatives include: the 60 assets, 180 vanilla call options (V), 3 basket call options (B), 147 spread call options (S), and 10 call-on-min options (R). The bid and ask prices of the assets and derivatives are synthetically generated using the market models specified in Section 8.2. For simplicity, we only consider Cases V+B+S and V+B+S+R in this experiment. The inputs of the two algorithms for this experiment are detailed in Section 8.2.

Figure 2 shows the computed lower and upper price bounds for the call-on-min option with different strikes, along with the reference bid and ask prices. Once again, the price bounds computed by the two algorithms are almost identical, and we have checked that all of the absolute differences between the bounds computed by the two algorithms are below . The following observations ensue from this example, which are mostly in line with the observations from the previous one. (i) The price bounds in the two cases are distinct, and the addition of more information improves the bounds and reduces the no-arbitrage gap. (ii) The addition of traded prices of call-on-min options results in a significant improvement of the bounds, since the payoffs used for sub- and super-replicating and the target payoff are of the same type. (iii) However, in this high-dimensional example, we notice that the lower price bounds in Case V+B+S are identically zero, showing that the traded vanilla, basket, and spread options do not provide enough information for a non-trivial lower price bound of the call-on-min options, and that it is not possible to sub-replicate the payoff of a call-on-min option with these traded options. Therefore, we conclude once again that, whenever possible, practitioners should include in their sub- and super-replicating portfolios not only as many derivatives as possible, but also as many derivatives with similar payoff structure as possible.

| Algorithm | Problem | V+B+S | V+B+S+R |

|---|---|---|---|

| ECP | LP | 4789 | 3339 |

| MILP | 4789 | 3339 | |

| ACCP | LP | 1639 | 1714 |

| MILP | 1461 | 1574 |

Table 1 shows the total number of LP and MILP problems solved throughout this experiment by the two algorithms. The ACCP algorithm achieved convergence faster than the ECP algorithm in this experiment. Moreover, in the ACCP algorithm, the MILP problems were only approximately solved with relative gap tolerance , as explained in Remark 7.19. As a result, the ACCP algorithm was much faster than the ECP algorithm in this experiment.

4.3 Experiment 3

In this experiment, we want to demonstrate how the Fundamental Theorem can be combined with the numerical algorithms developed in order to detect arbitrage opportunities in the financial market. We consider the case where the no-arbitrage assumption (i.e. Assumption 2) does not hold and use Algorithm 2 to detect the presence of arbitrage opportunities in the market. We can actually detect a very delicate form of arbitrage, since we consider a financial market with several single-asset options and two multi-asset options; the multi-asset options are priced within their own no-arbitrage intervals, i.e. when considered separately from each, there is no arbitrage in the market. However, when they are considered together an arbitrage opportunity arises and this is detected by the numerical algorithm. This experiment is inspired by similar examples in Tavin (2015, Section 4) and Papapantoleon and Yanez Sarmiento (2020, Section 5.2); in their setting, the marginals of the pricing measure are given.

We consider Setting 2 (i.e. Assumption 3.2) where , and consider the 5 assets , , , , and vanilla call options on the 5 assets with strikes as the traded financial derivatives. In addition, we include a call-on-min option on the five assets with strike 1 and a put-on-min option on the five assets with strike 4. The bid and ask prices of the single-asset derivatives are synthetically generated using the method specified at the beginning of Section 4.

We set the bid and ask prices of the call-on-min option as 0.83 and 0.85, respectively. As for the put-on-min option, we set its bid and ask prices as 3.18 and 3.20, respectively. Subsequently, we let and run Algorithm 2 with , , , , , , , . When only the call-on-min option is considered as traded multi-asset option, Algorithm 2 terminates without reaching Line 3, and the outputs satisfy , . Similarly, when only the put-on-min option is considered as traded multi-asset option, Algorithm 2 terminates without reaching Line 3, and the outputs again satisfy , . These numerical results imply that there is no arbitrage opportunity in the market with the single-asset derivatives and the call-on-min option, as well as in the market with the single-asset derivatives and the put-on-min option. However, when the single-asset derivatives together with both the call-on-min option and the put-on-min option are considered as traded options, Algorithm 2 reaches Line 3 before termination, indicating the violation of Assumption 2 and the presence of an arbitrage opportunity, as stated by Theorem 3.5(iv). The detected arbitrage strategy is given by and , which specify a portfolio with non-negative payoff such that .

In Experiment 4 (see Section 4.4), a similar procedure for detecting arbitrage opportunities using Algorithm 1 is applied to Setting 1 (i.e. Assumption 3.1) where bid and ask prices of traded derivatives are obtained from real market data. This demonstrates the real-world applicability of the proposed algorithms for arbitrage detection.

4.4 Experiment 4

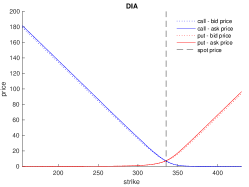

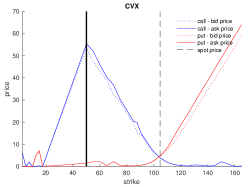

In this experiment, we use real market prices of European call and put options written on the Dow Jones Industrial Average (DJIA) index as well as European call and put options written on the 30 constituent stocks of the DJIA index. This type of market data has been considered by Hobson et al. (2005b), d’Aspremont and El Ghaoui (2006), and Peña et al. (2010b, 2012) for illustrations.

Data collection

The following market prices (corresponding to the closing prices on April 5, 2021 at 16:00 EDT) were collected from MarketWatch777http://marketwatch.com on April 6, 2021.

-

•

The prices of the 30 constituent stocks of the DJIA.

-

•

The bid and ask prices of the call and put options written on the 30 constituent stocks of the DJIA with expiration date May 21, 2021.

-

•

The bid and ask prices of the call and put options written on the SPDR Dow Jones Industrial Average ETF Trust (symbol: DIA), which is an exchange traded fund (ETF) that tracks the DJIA index. These DIA options are regarded as basket options written on the 30 constituent stocks with equal weights . The weight is equal to of the inverse of the Dow divisor888See e.g. https://www.investopedia.com/terms/d/dowdivisor.asp, accessed: April 30, 2021. calculated based on the stock prices on April 5, 2021.

Remark 4.1

Even though Experiments 1 and 2 have demonstrated that one should gather the market prices of as many derivatives as possible in order to obtain tight price bounds, exotic options such as, e.g., spread options, call-on-max options, and call-on-min options are usually only traded in over-the-counter (OTC) markets. Therefore, the prices of these exotic options are not publicly available and we are thus unable to collect real market data of this type.

Data preprocessing

We apply a procedure using Algorithm 1 to detect whether arbitrage opportunities are present with the bid and ask prices of call and put options written on each of the stocks and on DIA, similar to Experiment 3. We found that the prices of DIA options are arbitrage-free, while arbitrage opportunities are present among the prices of options written on 5 of the 30 underlying stocks. Before proceeding to the next step of the experiment, we adjust the bid and ask prices slightly to remove these arbitrage opportunities. In this process, the -norm of the price adjustment is minimized to encourage sparsity in the same spirit as Cohen et al. (2020). We refer the reader to Section 8.3 in the online appendices for details of this arbitrage removal process. After this process, 27 out of the 4304 prices have been adjusted and the largest change (in absolute value) is $0.38. This shows that only very few options were mis-priced and the market was close to being arbitrage-free.

Experimental setting

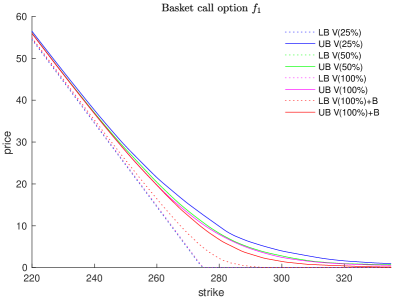

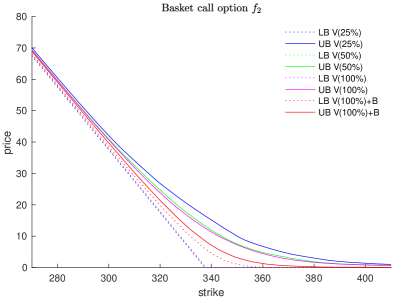

We consider Setting 1 (i.e. Assumption 3.1) and let . We rank the 30 constituent stocks of the DJIA index based on the market capitalization of the respective companies, i.e., in , corresponds to the stock price of the company with the highest market capitalization, and corresponds to the stock price of the company with the lowest market capitalization. Our goal is to use Algorithm 1 to compute the model-free lower and upper price bounds of two basket call options with the following payoff functions:

| (9) | ||||

where is the strike price that is varied in this experiment. Therefore, is the payoff of a basket call option written on DIA with the five largest companies in terms of market capitalization excluded (i.e. a basket option written on a subset of the 30 constituent stocks of the DJIA index). is the payoff of a basket call option written on a weight-adjusted version of DIA, where the weights of the ten largest companies are increased by 20% and the weights of the ten smallest companies are decreased by 20%.

After preprocessing, we are left with the following 2152 traded financial derivatives ():

-

•

980 vanilla call options and 980 vanilla put options written on the 30 stocks.

-

•

96 basket call options and 96 basket put options written on DIA.

We consider four different cases when computing the model-free lower and upper bounds. In the first three cases, denoted by V(25%), V(50%), and V(100%), we randomly select 25%, 50%, and 100% of the vanilla options, respectively. In the fourth case, denoted by V(100%)+B, we use all vanilla and basket options. The inputs of the ECP algorithm for this experiment are similar to those in Experiment 1.

Experimental results

Figure 3 shows the computed model-free upper and lower price bounds of the two basket call options with payoff functions and defined in (9). When pricing the first basket call option , the results from the first three cases show that when more vanilla options are considered, the uncertainty about the marginals of the pricing measure decreases and the model-free upper and lower price bounds are improved, where the improvements of the upper bounds are much more noticeable compared to the lower bounds. In Case V(100%)+B, when other basket options are considered in addition to the vanilla options, the upper price bounds are further improved for large strikes, and the lower price bounds are improved substantially, especially for strikes between $260 and $280. Compared to Case V(100%), the inclusion of basket options results in a maximum reduction of $5.59 in the no-arbitrage gap when the strike is $275, which reduces the gap by 54.7%. The results when pricing the second basket call option are in line with the results from pricing , and the improvements of the upper and lower price bounds in Case V(100%)+B are more significant across all strikes. Compared to Case V(100%), the inclusion of basket options results in a maximum reduction of $9.79 in the no-arbitrage gap when the strike is $338, which corresponds to a reduction of 79.4%. We conclude from these observations that when pricing a derivative using real market data, the inclusion of more traded derivatives in the sub- and super-replicating portfolios, especially derivatives whose payoff structures are similar to the target derivative, can produce substantial improvements to the arbitrage-free price bounds, and that the proposed algorithms are applicable to real market data.

5 Proofs of the main results

5.1 Proof of Theorem 3.3

Proof 5.1

Proof of Theorem 3.3 By the assumption about in Remark 7.16, there exist and such that and . For any and such that , it holds that and thus . By Assumption 2, , and so , thus . This implies that . Let be an optimizer of (4), which exists due to Theorem 2.3(ii). We have . Let denote the system of linear inequalities at iteration . Proposition 7.10 states that if and only if satisfies all constraints in . It hence holds by Line 1 that satisfies all constraints in for all . Consequently, we have

| (10) | ||||

is non-decreasing in because more constraints are added to . Moreover, by Proposition 7.6(iv) and the assumption on , for any that satisfies all constraints in , it holds that . By Definition 3.2, for all and for any ,

| (11) | ||||

and thus by Line 1, . This and (10) also show that . We have proved statement (i).

If Algorithm 1 terminates, then by (11), it holds for all that . Therefore, is feasible for (2) and follows directly from statement (i). We have at termination, and thus and is -optimal. We now show that Algorithm 1 terminates. Proposition 7.6(iv) states that there exists a partition of , such that each is a polytope, , and that for all , is an affine function when restricted to each . Let999A convex subset of a convex set is called a face of if for all and , implies that , see (Rockafellar 1970, Section 18). . By Theorem 18.2 of Rockafellar (1970),

| (12) |

Moreover, by Theorem 19.1 of Rockafellar (1970), . Let be a minimizer of the MILP problem in Line 1, that is, . We prove that either Algorithm 1 terminates, or for each , there exists at most one such that . Suppose, for the sake of contradiction, that Algorithm 1 does not terminate, and that there exists , and for some . Since , we have by Line 1. We also have , since otherwise Algorithm 1 will terminate at the -th iteration. For every , let . Since , there exists such that . Since is an affine function when restricted to the set , we have by and that

contradicting the fact that is a minimizer of the MILP problem in Line 1. Since for each , for some as a consequence of (12), and since , Algorithm 1 terminates eventually. The proof of statement (ii) is now complete.

5.2 Proofs of Theorem 3.5 and Corollary 3.6

Proof 5.2

Proof of Theorem 3.5 If Assumption 2 holds, then by the same argument as in the proof of Theorem 3.3(i), . Hence, and follow from our assumptions. For , suppose that . Then, only when Line 2 is reached. This implies that . By the assumption in Remark 7.19, there exists an optimizer of (4) that satisfies , , . In particular, for all and

| (13) |

By (13) and by the assumption that , it holds that implies . Therefore, by Line 2, . Since also satisfies all constraints in the LP problem in Line 2, we have, again by (13), that . By induction, we have proved that is non-decreasing in and for all .

For , , , or only if Line 2 is reached. By Line 2 and Line 2, . By the same reasoning as in the proof of Theorem 3.3(i) in equation (11), we have and . We have thus proved statement (i).

If Assumption 2 holds and Algorithm 2 terminates, then and the feasibility and -optimality of follow directly from statement (i) and Line 2. Thus, we only need to show that Algorithm 2 terminates. Notice that the Strong Slater Condition in Theorem 1 of Betrò (2004) holds because one may take defined earlier and choose any . Subsequently, one checks that

Thus, satisfies the Strong Slater Condition. Moreover, under Assumption 3.2, . Suppose, for the sake of contradiction, that Algorithm 2 loops infinitely and does not terminate. Then, one can deduce that after finitely many iterations, Line 2 is never reached, since each time Line 2 is reached, by Line 2 and Line 2. Similarly, Line 2 is never reached again after finitely many iterations since each time Line 2 is reached . The rest of the proof of statement (ii) follows exactly as the proof of Theorem 1 in Betrò (2004).

For statement (iii), notice that since , Line 2 is reached at least once before termination. Thus, and are defined. Let and be defined in Line 2. Then, by Line 2, is an optimal solution of the LP problem:

| (14) | ||||

Thus, since is updated whenever are updated, we have , and for all . Let . By the assumption of statement (iii), , , , and we claim that is also optimal for the following LP problem:

| (15) | ||||

Suppose, for the sake of contradiction, that (15) has optimal solution with . Then, since is the optimal value of (14), we have , , . Let , , . Then, there exists some , such that , for all , and , contradicting the optimality of for (14). Therefore, is also optimal for (15), whose corresponding dual LP problem is exactly (7). Then, an optimal solution of (7) exists, its corresponding finitely supported measure is a probability measure which satisfies for , and thus . Moreover, due to the strong duality of LP problems, by statement (ii), and is -optimal for the right-hand side of (3) by Theorem 2.3(iii). We have completed the proof of statement (iii).

The proof of statement (iv) is exactly the same as the proof of Theorem 3.3(iii). The proof is now complete.

Proof 5.3

Proof of Corollary 3.6 The proof that Algorithm 1 terminates is identical to the proof of Theorem 3.3(ii). Hence, as in Theorem 3.3(ii), we have . Since Line 1 is not used, and that , we have that is the optimal value of the following LP problem:

| minimize | |||

| subject to |

whose dual LP problem is exactly (8). Consequently, by the argument in the proof of Theorem 3.5(iii), , and is -optimal for the right-hand side of (3) by Theorem 2.3(iii).

We thank Daniel Bartl, Julien Guyon, and Steven Vanduffel for fruitful comments and discussions that initiated this project. We are also grateful to Stephan Eckstein and Michael Kupper for fruitful discussions during the work on these topics. AN gratefully acknowledges the financial support by his Nanyang Assistant Professorship Grant (NAP Grant) Machine Learning based Algorithms in Finance and Insurance. AP gratefully acknowledges the financial support from the Hellenic Foundation for Research and Innovation Grant No. HFRI-FM17-2152.

References

- Acciaio et al. (2016) Acciaio B, Beiglböck M, Penkner F, Schachermayer W (2016) A model-free version of the fundamental theorem of asset pricing and the super-replication theorem. Mathematical Finance 26(2):233–251.

- Auslender et al. (2015) Auslender A, Ferrer A, Goberna MA, López MA (2015) Comparative study of RPSALG algorithm for convex semi-infinite programming. Comput. Optim. Appl. 60(1):59–87.

- Auslender et al. (2009) Auslender A, Goberna MA, López MA (2009) Penalty and smoothing methods for convex semi-infinite programming. Mathematics of Operations Research 34(2):303–319.

- Bartl et al. (2017) Bartl D, Kupper M, Lux T, Papapantoleon A, Eckstein S (2017) Marginal and dependence uncertainty: bounds, optimal transport, and sharpness. Preprint, arXiv:1709.00641.

- Bartl et al. (2020) Bartl D, Kupper M, Neufeld A (2020) Pathwise superhedging on prediction sets. Finance and Stochastics 24(1):215–248.

- Bartl et al. (2019) Bartl D, Kupper M, Prömel DJ, Tangpi L (2019) Duality for pathwise superhedging in continuous time. Finance and Stochastics 23(3):697–728.

- Bayraktar et al. (2015) Bayraktar E, Huang YJ, Zhou Z (2015) On hedging American options under model uncertainty. SIAM Journal on Financial Mathematics 6(1):425–447.

- Bayraktar and Zhang (2016) Bayraktar E, Zhang Y (2016) Fundamental theorem of asset pricing under transaction costs and model uncertainty. Mathematics of Operations Research 41:1039–1054.

- Bayraktar et al. (2014) Bayraktar E, Zhang Y, Zhou Z (2014) A note on the fundamental theorem of asset pricing under model uncertainty. Risks 2:425–433.

- Beiglböck et al. (2013) Beiglböck M, Henry-Labordère P, Penkner F (2013) Model-independent bounds for option prices—a mass transport approach. Finance and Stochastics 17:477–501.

- Beissner (2017) Beissner P (2017) Equilibrium prices and trade under ambiguous volatility. Economic Theory 64(2):213–238.

- Beissner and Riedel (2019) Beissner P, Riedel F (2019) Equilibria under Knightian price uncertainty. Econometrica 87(1):37–64.

- Bertsimas and Bushueva (2006) Bertsimas D, Bushueva N (2006) Option pricing without price dynamics: a probabilistic approach. Preprint, arXiv:math/0612075.

- Bertsimas and Popescu (2002) Bertsimas D, Popescu I (2002) On the relation between option and stock prices: a convex optimization approach. Operations Research 50(2):358–374.

- Betrò (2004) Betrò B (2004) An accelerated central cutting plane algorithm for linear semi-infinite programming. Mathematical Programming 101(3):479–495.

- Biagini et al. (2017) Biagini S, Bouchard B, Kardaras C, Nutz M (2017) Robust fundamental theorem for continuous processes. Mathematical Finance 27:963–987.

- Borwein and Lewis (1991a) Borwein JM, Lewis AS (1991a) Convergence of best entropy estimates. SIAM Journal on Optimization 1(2):191–205.

- Borwein and Lewis (1991b) Borwein JM, Lewis AS (1991b) Duality relationships for entropy-like minimization problems. SIAM Journal on Control and Optimization 29(2):325–338.

- Bouchard et al. (2019) Bouchard B, Deng S, Tan X (2019) Superreplication with proportional transaction cost under model uncertainty. Mathematical Finance 29(3):837–860.

- Bouchard and Nutz (2015) Bouchard B, Nutz M (2015) Arbitrage and duality in nondominated discrete-time models. The Annals of Applied Probability 25(2):823–859.

- Burzoni et al. (2019) Burzoni M, Frittelli M, Hou Z, Maggis M, Obłój J (2019) Pointwise arbitrage pricing theory in discrete time. Mathematics of Operations Research 44(3):1034–1057.

- Burzoni et al. (2016) Burzoni M, Frittelli M, Maggis M (2016) Universal arbitrage aggregator in discrete-time markets under uncertainty. Finance and Stochastics 20(1):1–50.

- Burzoni et al. (2021) Burzoni M, Riedel F, Soner HM (2021) Viability and arbitrage under Knightian uncertainty. Econometrica 89(3):1207–1234.

- Chen et al. (2008) Chen X, Deelstra G, Dhaene J, Vanmaele M (2008) Static super-replicating strategies for a class of exotic options. Insurance Math. Econom. 42:1067–1085.

- Cheridito et al. (2017) Cheridito P, Kupper M, Tangpi L (2017) Duality formulas for robust pricing and hedging in discrete time. SIAM Journal on Financial Mathematics 8(1):738–765.

- Cho et al. (2016) Cho H, Kim KK, Lee K (2016) Computing lower bounds on basket option prices by discretizing semi-infinite linear programming. Optimization Letters 10:1629–1644.

- Cohen et al. (2020) Cohen SN, Reisinger C, Wang S (2020) Detecting and repairing arbitrage in traded option prices. Preprint, arXiv:2008.09454.

- Coope and Price (1998) Coope ID, Price CJ (1998) Exact penalty function methods for nonlinear semi-infinite programming. Semi-infinite programming, volume 25 of Nonconvex Optim. Appl., 137–157 (Kluwer Acad. Publ., Boston, MA).

- Dana and Riedel (2013) Dana RA, Riedel F (2013) Intertemporal equilibria with Knightian uncertainty. Journal of Economic Theory 148(4):1582–1605.

- d’Aspremont and El Ghaoui (2006) d’Aspremont A, El Ghaoui L (2006) Static arbitrage bounds on basket option prices. Math. Program. 106(3, Ser. A):467–489.

- Daum and Werner (2011) Daum S, Werner R (2011) A novel feasible discretization method for linear semi-infinite programming applied to basket option pricing. Optimization 60(10-11):1379–1398.

- Davis et al. (2014) Davis M, Obłój J, Raval V (2014) Arbitrage bounds for prices of weighted variance swaps. Mathematical Finance 24(4):821–854.

- De Gennaro Aquino and Bernard (2020) De Gennaro Aquino L, Bernard C (2020) Bounds on multi-asset derivatives via neural networks. Int. J. Theor. Appl. Finance 23(8):2050050, 31.

- Dhaene et al. (2002a) Dhaene J, Denuit M, Goovaerts MJ, Kaas R, Vyncke D (2002a) The concept of comonotonicity in actuarial science and finance: applications. Insurance Math. Econom. 31:133–161.

- Dhaene et al. (2002b) Dhaene J, Denuit M, Goovaerts MJ, Kaas R, Vyncke D (2002b) The concept of comonotonicity in actuarial science and finance: theory. Insurance Math. Econom. 31:3–33.

- Dolinsky and Neufeld (2018) Dolinsky Y, Neufeld A (2018) Super-replication in fully incomplete markets. Mathematical Finance 28(2):483–515.

- Dolinsky and Soner (2014a) Dolinsky Y, Soner HM (2014a) Martingale optimal transport and robust hedging in continuous time. Probability Theory and Related Fields 160(1-2):391–427.

- Dolinsky and Soner (2014b) Dolinsky Y, Soner HM (2014b) Robust hedging with proportional transaction costs. Finance and Stochastics 18:327–347.

- Eckstein et al. (2021) Eckstein S, Guo G, Lim T, Obłój J (2021) Robust pricing and hedging of options on multiple assets and its numerics. SIAM J. Financial Math. 12(1):158–188.

- Eckstein and Kupper (2019) Eckstein S, Kupper M (2019) Computation of optimal transport and related hedging problems via penalization and neural networks. Applied Mathematics & Optimization 1–29.

- Eckstein et al. (2020) Eckstein S, Kupper M, Pohl M (2020) Robust risk aggregation with neural networks. Mathematical Finance 30:1229–1272.

- Epstein and Ji (2013) Epstein LG, Ji S (2013) Ambiguous volatility and asset pricing in continuous time. The Review of Financial Studies 26(7):1740–1786.

- Galichon et al. (2014) Galichon A, Henry-Labordère P, Touzi N (2014) A stochastic control approach to no-arbitrage bounds given marginals, with an application to lookback options. The Annals of Applied Probability 24(1):312–336.

- Goberna and López (1998) Goberna MA, López MA (1998) Linear Semi-Infinite Optimization (John Wiley & Sons).

- Goberna and López (2018) Goberna MA, López MA (2018) Recent contributions to linear semi-infinite optimization: an update. Annals of Operations Research 271(1):237–278.

- Gurobi Optimization, LLC (2020) Gurobi Optimization, LLC (2020) Gurobi optimizer reference manual. URL http://www.gurobi.com.

- Henry-Labordère (2013) Henry-Labordère P (2013) Automated option pricing: Numerical methods. International Journal of Theoretical and Applied Finance 16(08):1350042.

- Hettich and Kortanek (1993) Hettich R, Kortanek KO (1993) Semi-infinite programming: theory, methods, and applications. SIAM Review 35:380–429.

- Hobson et al. (2005a) Hobson D, Laurence P, Wang TH (2005a) Static-arbitrage optimal subreplicating strategies for basket options. Insurance Math. Econom. 37:553–572.

- Hobson et al. (2005b) Hobson D, Laurence P, Wang TH (2005b) Static-arbitrage upper bounds for the prices of basket options. Quant. Finance 5:329–342.

- Hobson (1998) Hobson DG (1998) Robust hedging of the lookback option. Finance and Stochastics 2(4):329–347.

- Hu et al. (2019) Hu J, Li J, Mehrotra S (2019) A data-driven functionally robust approach for simultaneous pricing and order quantity decisions with unknown demand function. Operations Research 67(6):1564–1585.

- Kahalé (2017) Kahalé N (2017) Superreplication of financial derivatives via convex programming. Management Science 63(7):2323–2339.

- Karlin and Studden (1966) Karlin S, Studden WJ (1966) Tchebycheff systems: With applications in analysis and statistics (John Wiley & Sons).

- Lin et al. (1998) Lin CJ, Fang SC, Wu SY (1998) An unconstrained convex programming approach to linear semi-infinite programming. SIAM Journal on Optimization 8(2):443–456.

- López and Still (2007) López M, Still G (2007) Semi-infinite programming. European J. Oper. Res. 180(2):491–518.

- Lütkebohmert and Sester (2019) Lütkebohmert E, Sester J (2019) Tightening robust price bounds for exotic derivatives. Quantitative Finance 19(11):1797–1815.

- Lux and Papapantoleon (2017) Lux T, Papapantoleon A (2017) Improved Fréchet–Hoeffding bounds on -copulas and applications in model-free finance. Ann. Appl. Probab. 27:3633–3671.

- Maruhn (2009) Maruhn JH (2009) Robust Static Super-Replication of Barrier Options (Walter de Gruyter GmbH & Co. KG, Berlin).

- Neufeld and Nutz (2013) Neufeld A, Nutz M (2013) Superreplication under volatility uncertainty for measurable claims. Electronic Journal of Probability 18.

- Nishihara et al. (2007) Nishihara M, Yagiura M, Ibaraki T (2007) Duality in option pricing based on prices of other derivatives. Oper. Res. Lett. 35(2):165–171.

- Papapantoleon and Yanez Sarmiento (2020) Papapantoleon A, Yanez Sarmiento P (2020) Detection of arbitrage opportunities in multi-asset derivatives markets. Preprint, arXiv:2002.06227.

- Peña et al. (2010a) Peña J, Saynac X, Vera JC, Zuluaga LF (2010a) Computing general static-arbitrage bounds for European basket options via Dantzig–Wolfe decomposition. Algorithmic Operations Research 5(2):65–74.

- Peña et al. (2010b) Peña J, Vera JC, Zuluaga LF (2010b) Static-arbitrage lower bounds on the prices of basket options via linear programming. Quant. Finance 10:819–827.

- Peña et al. (2012) Peña J, Vera JC, Zuluaga LF (2012) Computing arbitrage upper bounds on basket options in the presence of bid–ask spreads. European Journal of Operational Research 222(2):369–376.

- Possamaï et al. (2013) Possamaï D, Royer G, Touzi N (2013) On the robust superhedging of measurable claims. Electronic Communications in Probability 18.

- Puccetti et al. (2016) Puccetti G, Rüschendorf L, Manko D (2016) VaR bounds for joint portfolios with dependence constraints. Depend. Model. 4:368–381.

- Reemtsen and Rückmann (1998) Reemtsen R, Rückmann JJ (1998) Semi-infinite programming, volume 25 (Springer Science & Business Media).

- Riedel (2015) Riedel F (2015) Financial economics without probabilistic prior assumptions. Decisions in Economics and Finance 38(1):75–91.

- Rigotti and Shannon (2005) Rigotti L, Shannon C (2005) Uncertainty and risk in financial markets. Econometrica 73(1):203–243.

- Rockafellar (1970) Rockafellar RT (1970) Convex Analysis (Princeton University Press).

- Stein (2012) Stein O (2012) How to solve a semi-infinite optimization problem. European J. Oper. Res. 223(2):312–320.

- Tankov (2011) Tankov P (2011) Improved Fréchet bounds and model-free pricing of multi-asset options. J. Appl. Probab. 48:389–403.

- Tavin (2015) Tavin B (2015) Detection of arbitrage in a market with multi-asset derivatives and known risk-neutral marginals. J. Banking Finance 53:158–178.

- Yan et al. (2018) Yan Z, Cheng C, Natarajan K, Teo CP (2018) “Marginal estimation+ price optimization” for multi-product pricing problems. Technical report, Working paper.

Online Appendices

6 Additional remarks about the duality result

Remark 6.1

Theorem 2.3 is similar in spirit to the multi-marginal optimal transport problem, possibly under additional constraints, see e.g. Kellerer (1984), Rachev and Rüschendorf (1994), Zaev (2015), and Bartl et al. (2017). However, in contrast to these articles, we do not assume that the marginals are known and fixed. Moreover, notice the subtle differences in the attainment of supremum and infimum. In Theorem 2.3, the infimum in (2) corresponding to the super-replication portfolio is attained, whereas the supremum on the right-hand side of (3) corresponding to the “worst-case” probability measure is not necessarily attained. In the multi-marginal optimal transport problem, the supremum corresponding to the “worst-case” probability measure (or optimal coupling of the marginals) is attained due to compactness, which holds when the marginals of the pricing measure are fixed.

The following example demonstrates that the supremum on the right-hand side of (3) is not necessarily attained.

Example 6.2

Let , , and, for , set:

Clearly,

In the case where , , holds, and we have that , is an optimizer of (2). Thus . On the other hand, if is a probability measure on , , and , then

Since for , it is implied that , which is impossible. Hence, is not attained.

The following proposition presents a specific setting in which Assumption 2 holds, and its proof can be found in Section 9.

Proposition 6.3

Let for some , be continuous functions on , and assume there exists such that is equivalent to the Lebesgue measure on . Then, Assumption 2 holds.

7 Additional notes about the numerical methods

7.1 Notes about CPWA functions

Example 7.1

Many popular payoff functions in finance belong to the class of CPWA functions. The list below contains those payoff functions used in the present work, alongside their CPWA representation.

-

(i)

Setting and , we get the payoff of a call option on the -th asset with strike , via

-

(ii)

Using the previous setting and replacing with , we get the payoff of a basket call option on the assets with weights and strike , via

-

(iii)

Using the previous setting, and replacing with , for and , we get the payoff of a spread call option with strike , via

-

(iv)

Setting for all , and , we get the payoff of a call-on-max option on the assets with strike , via

-

(v)

Setting for all , and , , we get the payoff of a call-on-min option on the assets with strike , via

-

(vi)

Finally, setting for all , and , we get the payoff of a best-of-call option on the assets with strikes , via

Let us point out that these representations are not unique. Moreover, by replacing the vectors or with suitable vectors in examples (iii), (iv), (v), and (vi) above, one can create weighted versions of the aforementioned payoffs. These can be interpreted as options written on a number of indices.

The following properties of CPWA functions can be deduced from Definition 3.1.

Lemma 7.2

The following are properties of CPWA functions.

-

(i)

A finite linear combination of CPWA functions is again a CPWA function;

-

(ii)

If is a CPWA function, then it admits the following local representation:

(7.1) where for , , , is a polyhedron, and . In addition, for , . If , then , and thus the above function is well-defined.

-

(iii)

In the local representation (7.1), it can be assumed without loss of generality that for .

The following proposition establishes the connection between the lower-boundedness of a CPWA function and the non-negativity of its associated radial function.

Proposition 7.4

Let be a CPWA function, and let be its radial function. Then,

-

(i)

if and only if for all ;

-

(ii)