On Multivariate Singular Spectrum Analysis

and its Variants

Abstract

We introduce and analyze a variant of multivariate singular spectrum analysis (mSSA), a popular time series method to impute and forecast a multivariate time series. Under a spatio-temporal factor model we introduce, given time series and observations per time series, we establish prediction mean-squared-error for both imputation and out-of-sample forecasting effectively scale as . This is an improvement over: (i) error scaling of SSA, the restriction of mSSA to a univariate time series; (ii) error scaling for matrix estimation methods which do not exploit temporal structure in the data. The spatio-temporal model we introduce includes any finite sum and products of: harmonics, polynomials, differentiable periodic functions, and Hölder continuous functions. Our out-of-sample forecasting result could be of independent interest for online learning under a spatio-temporal factor model. Empirically, on benchmark datasets, our variant of mSSA performs competitively with state-of-the-art neural-network time series methods (e.g. DeepAR, LSTM) and significantly outperforms classical methods such as vector autoregression (VAR). Finally, we propose extensions of mSSA: (i) a variant to estimate time-varying variance of a time series; (ii) a tensor variant which has better sample complexity for certain regimes of and .

keywords:

, and

1 Introduction

Multivariate time series data is of great interest across many application areas, including cyber-physical systems, finance, retail, healthcare to name a few. An important goal across these domains can be summarized as accurate imputation and forecasting of a multivariate time series in the presence of noisy and/or missing data.

Setup. We consider a discrete time setting with time indexed as . For , let the collection be the latent time series of interest. For and , we observe where for ,

| (1) |

Here represents a missing observation and represents the per-step noise, which we assume to be an independent (across ) mean-zero random variable. Though is independent, we note that the underlying time series, , is of course strongly dependent across . Indeed the presence of per-step noise and missing values (denoted by ) represent an additional challenge of measurement error in our setup. The generic spatio-temporal factor model for described in Section 3 without additional noise or missingness already provides an expressive model for a time series including any finite sum of products of harmonics and polynomials, any differentiable periodic function, and any Hölder continuous function.

Goal. Our objective is two-folds, for : (i) imputation – estimating for all ; (ii) out-of-sample forecasting – predicting for .

1.1 Multivariate Singular Spectrum Analysis

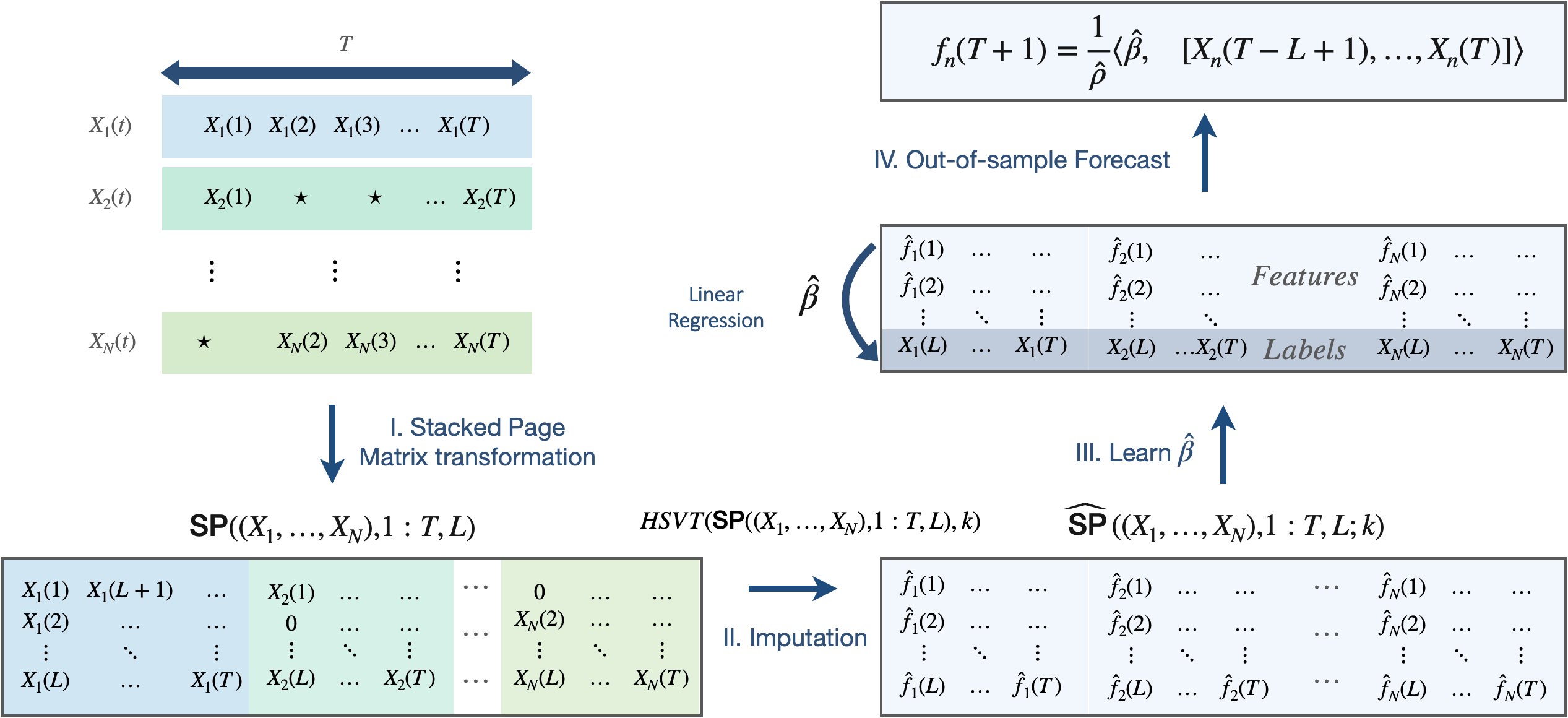

Multivariate singular spectrum analysis (mSSA) is a known method to impute and forecast a multivariate time series (see [10, 28, 18, 27, 23, 22, 9]). mSSA has been used for both imputation and forecasting, and signal extraction—decomposing a time series into a small number of simpler time series (e.g., periodic, trend, autoregressive component). However, despite its heavy use in practice, the theoretical properties of mSSA are not well understood. Hence, we introduce a variant of mSSA for which we provide a rigorous finite-sample analysis of its imputation and out-of-sample forecasting properties; such a finite-sample analysis of mSSA has been missing from the literature. We note that we do not focus on the task of signal extraction which we leave as important future work. The variant of mSSA we introduce is arguably much simpler to implement than the original mSSA method and we begin by describing it in detail below. In Section 2, we compare the original mSSA method with this variant and discuss key differences. See Figure 1 for a visual depiction of the key steps in this variant of mSSA.

Singular spectrum analysis (SSA). For ease of exposition and to build intuition, we start with , i.e. a univariate time series. There are two algorithmic parameters: and . For simplicity and without loss of generality assume that is an integer multiple of , i.e. and . When , by applying both the imputation and forecasting algorithms for two ranges, and , this condition will be satisfied in each range and will provide imputation and forecasting for all . Here refers to the floor of . We give guidance on how to pick and when we discuss our theoretical results.

First, transform the time series into an matrix where the entry of the matrix in row and column is . This matrix induced by the time series is called the Page matrix, and we denote it as .

Imputation. After replacing missing values (i.e. ) in the matrix by , we compute its singular value decomposition, which we denote as

| (2) |

where denote its ordered singular values, and denote its left and right singular vectors, respectively, for . Let be the fraction of observed entries of , precisely defined as . Let the normalized, truncated version of be

| (3) |

i.e., we perform Hard Singular Value Thresholding (HSVT) on to obtain . We then define the de-noised and imputed estimate of the original time series, denoted by , as follows: for , equals the entry of in row and column . Here refers to the ceiling of .

Forecasting. To forecast, we learn a linear model , which is the solution to

| (4) |

where , for . 111 To establish theoretical results for the forecasting algorithm, we produce estimates for by applying the imputation algorithm on after setting its th row equal to . Also, in the definition of is computed using only the first rows of . This avoids dependencies in the noise between and for . Note to define we impute missing values in by . We now describe how to use to produce both in-sample and out-of-sample forecasts. (i) In-sample forecast: for time and , the forecast is given by . (ii) Out-of-sample forecast: for , i.e., for time , the forecast is given by where after imputing missing values in by .

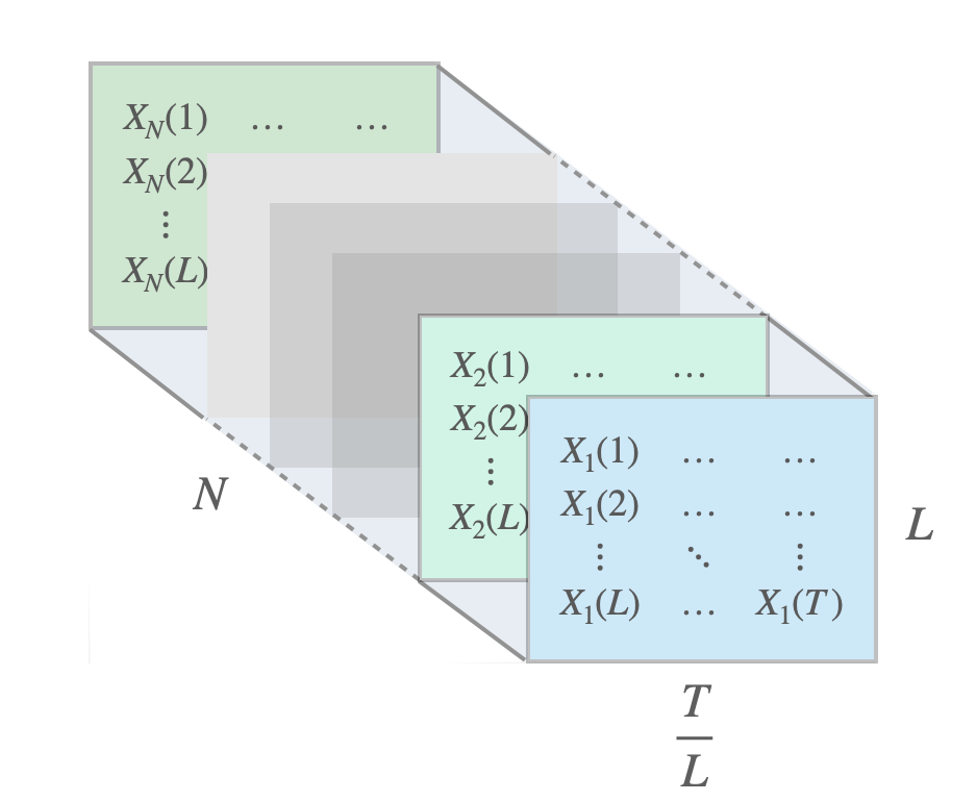

Multivariate singular spectrum analysis (mSSA). Below we describe the variant of mSSA we propose, which is an extension of the SSA algorithm described above, to when we have a multivariate time series, i.e., . The key change is in the first step where we construct the Page matrix—instead of considering the Page matrix of a single time series, we now consider a ‘stacked’ Page matrix, which is obtained by a column-wise concatenation of the Page matrices induced by each time series separately. Specifically, like SSA, it has two algorithmic parameters, and . For each time series, , create its Page matrix , where the entry in row and column is . We then create a stacked Page matrix from these time series by performing a column wise concatenation of the matrices, . We denote this matrix as , and note that it has rows and columns.

Imputation. We replace missing values (i.e. s) in by . Similar to (3), we perform HSVT on and denote its normalized, truncated version as (instead of , we now normalize by ). From , like in SSA, we can read off for , the de-noised and imputed estimate of the time series over time steps. In particular, let refer to sub-matrix of induced by selecting only its ] columns. Then for , equals the entry of in row and column .

Forecasting. Similar to SSA, to forecast, we learn a linear model , which is the solution to

| (5) |

where is the th component of , and corresponds to the vector formed by the entries of the first rows in the th column of 222 Similar to the SSA forecasting algorithm, when creating a forecasting model in mSSA, we produce by first setting the th row of equal to zero before performing the SVD and the subsequent truncation. Also, in the definition of is computed only using the first rows of . for . Note, to define , we impute missing values in by . (i) In-sample forecast: for time step for and for time series , the forecast is given by where . (ii) Out-of-sample forecast: for , i.e., for time , and for time series , the forecast is given by , where after imputing missing values in by . See Figure 1 for a visual depiction of the key steps above.

Page vs. Hankel mSSA. See Appendix A for a detailed discussion of the various benefits and drawbacks of the using the Page matrix representation as we propose in our variant, instead of the Hankel representation used in the original mSSA.

Empirical performance of mSSA. This variant of mSSA we propose is fully described above, with its two major steps consisting of simply singular value thresholding and ordinary least squares. A key question is how well does it perform empirically? In Table 1, we provide a summary comparison of mSSA’s performance for imputation and forecasting on benchmark datasets with respect to state-of-the-art time series algorithms. We find that by using the stacked Page matrix in mSSA, it greatly improves performance over SSA; indicating that mSSA is effectively utilizing information across multiple time series. Surprisingly, our variant of mSSA performs competitively or outperforms popular neural network based methods, such as LSTM and DeepAR—we note that these state-of-the-art neural network based methods have no associated theoretical analysis. Further, it significantly outperforms classical multivariate forecasting methods such as VAR. Indeed, apart from its use in practice, the empirical performance of (our variant of) mSSA strongly motivates a theoretical analysis of when and why mSSA works.

|

|

|||||||||||||

| Electricity | Traffic | Synthetic | Financial | M5 | Electricity | Traffic | Synthetic | Financial | M5 | |||||

| mSSA | 0.398 | 0.508 | 0.416 | 0.238 | 0.883 | 0.485 | 0.536 | 0.281 | 0.251 | 1.021 | ||||

| SSA | 0.514 | 0.713 | 0.675 | 0.467 | 0.958 | 0.632 | 0.696 | 0.665 | 0.303 | 1.068 | ||||

| LSTM | NA | NA | NA | NA | NA | 0.558 | 0.478 | 0.559 | 1.205 | 1.034 | ||||

| DeepAR | NA | NA | NA | NA | NA | 0.479 | 0.464 | 0.415 | 0.316 | 1.050 | ||||

| TRMF | 0.641 | 0.460 | 0.564 | 0.430 | 0.916 | 0.495 | 0.508 | 0.422 | 0.291 | 1.032 | ||||

| Prophet | NA | NA | NA | NA | NA | 0.569 | 0.614 | 1.010 | 1.286 | 1.100 | ||||

| VAR | NA | NA | NA | NA | NA | 1.291 | 1.092 | 2.987 | 1.218 | 1.120 | ||||

1.2 Our Contributions

As our primary contribution, we provide an answer to the question posed above—under a spatio-temporal factor model that we introduce, the finite-sample analysis we carry out of mSSA’s estimation error for imputation and out-of-sample forecasting establishes consistency, as well as its ability to effectively utilize both the spatial and temporal structure in a multivariate time series. Below, we detail the various aspects of our contribution with respect to the: (a) spatio-temporal factor model; (b) finite sample analysis of mSSA; (c) algorithmic extensions (and associated theoretical analysis) of mSSA to do time-varying variance estimation, and a tensor variant of mSSA which we show has a better imputation error convergence rate compared to mSSA for certain relative scalings of and .

Spatio-temporal factor model. Note that the collection of latent multivariate time series , for can be collectively viewed as a matrix. To capture the spatial structure, i.e. the relationship across rows, we model this matrix to be low-rank—there exists a low-dimensional latent factor (or feature) associated with each of time series; analogously, there exists a low-dimensional latent factor associated with each of the time steps. To capture the temporal structure, we further assume that each component of the latent temporal factor has an approximately low-rank Hankel matrix representation (see Definition 3.1 for the Hankel matrix induced by a time series), i.e., the Hankel—and therefore Page—matrix induced by each component of the latent temporal factor is approximately low-rank. This additional structure imposed on the temporal factors is what motivates using the stacked Page matrix representation in mSSA, which is of dimension , where is a hyper-parameter. We note that for this subsumes the model considered to explain the success of SSA in [1] as a special case.

As stated earlier, our model is expressive in that it includes any finite sum of products of harmonics and polynomials, any differentiable periodic function, and any Hölder continuous function. Further, we establish that the set of time series that have an approximately low-rank Hankel representation is closed under component-wise addition and multiplication. Such a model calculus helps characterize the representational strength of the spatio-temporal factor model we introduce.

Finite sample analysis of mSSA. Under the spatio-temporal factor model, we establish that mean squared imputation error scales as (see Theorem 4.1) and the out-of-sample forecasting error scales as (see Theorem 4.3, and Corollary 4.1). When , the error rate is . When , one can simply divide the various time series into sets of size ; this will result in a mean squared error rate of . Hence, effectively the error is of order . For exact details on the relative scaling of and , please refer to Theorem 4.3. For , it implies that the SSA algorithm described above has imputation and forecasting error scaling as . That is, mSSA improves performance by a factor over SSA by utilizing information across the time series. This also improves upon the prior work of [1] which established the weaker result that SSA has imputation error scaling as (i.e., when ). Further [1] does not establish a result for the out-of-sample forecasting error of SSA. We note that the asymmetry in our finite-sample analysis between and is to be expected as we impose further structure on the latent temporal factors; they satisfy a low-rank Hankel representation, which is not assumed of the spatial factors.

Further, existing matrix estimation based methods applied to the matrix of time series observations (i.e, without first performing the Page matrix transformation as done in mSSA) establish that the imputation prediction error scales as . This is indeed the primary result of the works [45, 29], as seen in Theorem 2 of [29]. 333There seems to be a typo in Corollary 2 of [45] in applying Theorem 2: square in Frobenius-norm error is missing. That is, while the algorithm stated in [45, 29] utilizes the temporal structure in addition to the spatial structure, the theoretical guarantees do not reflect it—the guarantees provided by such methods are weaker (since ) than that obtained by mSSA. Again, we emphasize that the existing analysis of SSA and matrix estimation based methods (for example [1, 45, 29]) do not establish (finite-sample) bounds for out-of-sample forecasting error.

Algorithmic extensions: variance and tensor SSA (tSSA). First, we extend mSSA to estimate the latent time-varying variance, i.e. . We establish the efficacy of such an extension when the time-varying variance is also modeled through a spatio-temporal factor model. To the best of our knowledge, this is the first result that provides provable finite-sample performance guarantees for estimating the time-varying variance of a time series. Second, we propose a novel tensor variant of SSA, termed tSSA, which exploits recent developments in the tensor estimation literature. In tSSA, rather than doing a column-wise stacking of the Page Matrices induced by each of the time series to form a larger matrix, we instead view each Page matrix as a slice of a order-three tensor. In other words, the entry of the tensor with indices and equals the entry of with indices . In Proposition 7.2, with respect to imputation error, we characterize the relative performance of tSSA, mSSA, and “vanilla” matrix estimation (ME). We find that when , mSSA outperforms tSSA; when tSSA outperforms mSSA; when , standard matrix estimation methods are equally as effective as mSSA and tSSA. See Figure 2 for a graphical depiction.

Summary of contributions. We now briefly summarize our contributions:

-

1.

A novel spatio-temporal factor model to analyze mSSA. We show that a large family of time series dynamics fall within our factor model.

-

2.

Finite-sample analysis for imputation and out-of-sample forecasting. The tools we use for imputation borrow from the existing literature on matrix estimation. However, our out-of-sample forecasting requires making novel technical contributions. We believe these tools might be of interest for online learning with a spatio-temporal factor model.

-

3.

A novel time-varying variance estimation algorithm with theoretical guarantees. To the best of our knowledge, neither such an algorithm nor an associated theoretical analysis exists.

-

4.

A novel tensor variant of the mSSA algorithm called tSSA, which exploits recent developments in the tensor estimation literature. We find that when is large compared to , tSSA has better sample complexity compared to mSSA. We believe this tensor variant opens a direction to future work to understand the appropriate statistical and computational trade offs for time series analysis.

2 Literature Review

Given the ubiquity of multivariate time series analysis, it will not be possible to do justice to the entire literature. We focus on a few techniques most relevant to compare against, either theoretically or empirically.

SSA and mSSA. A good overview of the literature on SSA can be found in [19]. As alluded to earlier, the original SSA method differs from the variant discussed in [1] and in this work. The key steps of the original SSA method are: Step 1–create a Hankel matrix from the time series data; Step 2–do a Singular Value Decomposition (SVD) of it; Step 3–group the singular values based on user belief of the model that generated the process; Step 4–perform diagonal averaging to “Hankelize” the grouped rank-1 matrices outputted from the SVD to create a set of time series; and Step 5–learn a linear model for each “Hankelized” time series for the purpose of forecasting. The theoretical analysis of this original SSA method has been focused on proving that many univariate time series have a low-rank Hankel representation, and secondly on defining sufficient asymptotic conditions for when the singular values of the various time series components are separable, thereby justifying Step 3 of the method. Step 3 of the original SSA method requires user input and Steps 4 and 5 are not robust to noise and missing values due to the strong dependence across entries of the Hankel representation of the time series. To overcome these limitations, in [1] a simpler and practically useful version as described in Section 1.1 was introduced. As discussed earlier, this work improves upon the analysis of [1] by providing stronger bounds for imputation prediction error, and gives new bounds for forecasting prediction error, which were missing in [1]. The original mSSA method, like the original SSA method, involves the five steps described above, but first the Hankel matrices induced by each of the time series are stacked either column-wise (horizontal mSSA) or row-wise (vertical mSSA); see [24].

We note given the popularity of mSSA, there are many algorithmic variants of it proposed in the literature motivated by different applications: see [10, 28, 18, 27, 23, 22, 9]. A significant focus of these works is signal extraction, i.e., decomposing the observed time series into a small number of simpler time series (e.g., periodic, trend, autoregressive component); these extracted signals are then subsequently utilized for imputation and forecasting as described in the preceding paragraph. As stated earlier, despite the popularity of the mSSA framework, a rigorous finite-sample analysis of its imputation and out-of-sample forecasting properties are missing in the literature; the challenge in such an analysis is exacerbated with missing data and measurement error. In this work, as described in Section 1.1, we introduce a simpler variant of mSSA that uses the Page instead of the Hankel matrix representation. This variant is simpler as it focuses only on the task of imputation and forecasting, and not signal extraction. We do a finite-sample analysis of our variant of mSSA and establish its consistency with respect to imputation and forecasting, which so far has been missing from the mSSA literature. In Appendix A, we compare our variant to the original version of mSSA which use the Hankel matrix, both with respect to their theoretical and practical properties.

Matrix factorization based methods for multivariate time series. There is a rich line of work in econometrics and statistics on viewing multiple time series as a matrix, and where some form of matrix factorization is performed to learn the spatial and temporal factors induced by the matrix; such models have also been called dynamic factor models. Some representative papers (and by no means exhaustive) include [35, 16, 21, 14, 5, 7]. [35] consider the estimation by principal components of this matrix. They use the model for signal extraction and forecasting. Also, they proposed an expectation-maximization (EM) algorithm to handle missing data and imputation. [16, 21] also estimate principal components and restrict the singular vectors to be related to the Fourier basis. [14, 7] consider maximum likelihood estimation based on Kalman filtering and also consider forecasting and signal extraction. [5] show how to handle missing data and imputation. Similar to the mSSA literature, the general focus of these works is first signal extraction, which can then be subsequently used for imputation and forecasting. The theoretical analysis of these methods has generally been asymptotic in nature, and has focused on recovery of the spatial and temporal factors, i.e., signal extraction. Our work complements this literature as we focus directly on finite-sample analysis for imputation and out-of-sample forecasting (without first needing to signal extraction), and establish consistency for the variant of mSSA we propose. To the best of our knowledge, finite-sample consistency results such as ours are limited in the literature.

Additionally, there is a recent line of work from the machine learning literature which also employs matrix factorization based methods (see [40, 45]). Most such methods make strong prior model assumptions on the underlying time series and the algorithm changes based on the assumptions made on the time series dynamics that generated the data. Further, finite sample analysis, especially with respect to forecasting error, of such methods is usually lacking. We highlight one method, Temporal Regularized Matrix Factorization (TRMF) (see [45]), which we directly compare against due to its popularity, and as it achieves state-of-the-art empirical imputation and forecasting performance. The authors in [45] provide finite sample imputation analysis for an instance of the model considered in this work, but forecasting analysis is absent. As discussed earlier, they establish that imputation error scales as . This is a direct consequence of the low-rank structure of the original matrix. But they fail to utilize, at least in the theoretical analysis, the temporal structure. Indeed, our analysis captures such temporal structure and hence our imputation error scales as which is a stronger guarantee. For example, for , their error bound remains for any , suggesting that TRMF [45] fails to utilize the temporal structure for better estimation, while the error for mSSA would vanish as grows.

Other relevant literature. We take a brief note of some popular time series methods in the recent literature. In particular, recently neural network (NN) based approaches have been popular and empirically effective. Some industry standard neural network methods include LSTMs, from the Keras library (a standard NN library, see [12]) and DeepAR (an industry leading NN library for time series analysis, see [31]). Though they have no theoretical guarantees, which is the focus of our work, we compare with them empirically.

3 Model

3.1 Spatio-Temporal Factor Model

Below, we introduce the spatio-temporal factor model we use to explain the success of mSSA. In short, the model requires that the underlying latent multivariate time series satisfies Properties 1 and 2, which capture the “spatial” and “temporal” structure within it, respectively.

Spatial structure in data. Consider the matrix , where its entry in row and column , is equal to , the value of the latent time series at time . We posit that the matrix is low-rank. Precisely,

Property 1.

Let . That is, for any , where , for constants .

Property 1 effectively captures the “spatial” structure amongst the time series. Similar to the dynamic factor model literature, we can interpret this model as there existing latent time series for , and each time series is a linear combination of these time series, where the weights are given by .

Temporal structure in data. To explicitly capture the temporal structure in the data, we impose additional structure on . To that end, we introduce the notion of the Hankel matrix induced by a time series.

Definition 3.1 (Hankel Matrix).

Given a time series , its Hankel matrix associated with observations over time steps, , is given by the matrix with for .

Now, for a given , consider the time series for . Let denote its Hankel matrix restricted to , i.e. for .

Property 2.

For each and for any , the Hankel Matrix associated with time series has rank at most .

Property 2 captures the temporal structure within the latent factors associated with time; indeed, such a low-rank Hankel representation includes a rich family of time series dynamics as noted in Proposition 3.1 below.

Proposition 3.1 (Proposition 5.2, [1]).

Consider a time series with its element at time denoted as

| (6) |

where are parameters, is a degree polynomial in . Then satisfies Property 2. In particular, consider the Hankel matrix of over , denoted as with for . For any , the rank of is at most , where .

Proposition 3.1 states any finite sum of (products of) harmonics, polynomials, and exponentials has a low-rank Hankel representation. Each of these functions are popular to model various aspects of a time series such as periodicity and trend. Further, we note that the spectral representation of generic stationary processes, which includes autoregressive processes, implies that any sample-path of a stationary process can be decomposed into a weighted sum (precisely an integral) of harmonics, where the weights in the sum are sample path dependent—see Property 4.1, Chapter 4 of [30]. That is, a finite (weighted) sum of harmonics provides a good model representation for stationary processes with the model becoming more expressive as the number of harmonics grows. In Section 5, we extend this model when Property 2 is only approximately satisfied. In particular, we quantify the approximation error based on the smoothness of the underlying time series and the number of harmonics used in the summation to approximate it.

Spatio-temporal model implies stacked Page matrix is low-rank. Recall that the primary representation utilized by mSSA, as described in Section 1.1, is the stacked Page matrix (with parameter ). Observe that the Page matrix of a univariate time series for any is simply the sub-matrix of the associated Hankel matrix: precisely, the Page matrix can be obtained by restricting to the top rows and columns of the Hankel matrix. Therefore, the rank of the Hankel matrix is a bound on the rank of the Page matrix. Under the spatio-temporal factor model satisfying Properties 1 and 2, we establish the following low-rank property of the Page matrix of any particular time series as well as that of the stacked Page matrix.

Proposition 3.2.

3.2 A Diagnostic Test for the Spatio-Temporal Model

In Sections 4 and 5, under the model described above, we theoretically establish the efficacy of mSSA. Beyond this model though, our work does not provide any guarantees for mSSA. Therefore, to utilize the guarantees of this work, it would be useful to have a data-driven diagnostic test that can help identify scenarios when the model of Section 3 may or may not hold. We discuss one such test in this section.

In particular, Proposition 3.2 suggests a “data driven diagnosis test” to verify whether mSSA is likely to succeed as per the results of this work. Specifically, if the (effective) rank—defined as the minimum number of singular values capturing of its spectral energy—of the Page matrix associated with any of the univariate components and the (effective) rank of stacked Page matrix associated with the multivariate time series with component are very different, then mSSA may not be effective compared to SSA, but if they are very similar then mSSA is likely to be more effective compared to SSA. Our finite-sample results in Sections 4 and 5 indicate that the optimal value for is . Thus as a further test, if the effective rank of the stacked Page matrix does not scale much slower than for , then SSA (and mSSA) are unlikely to be effective methods.

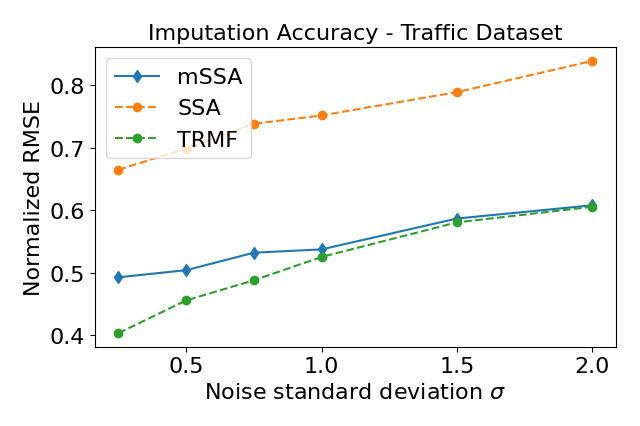

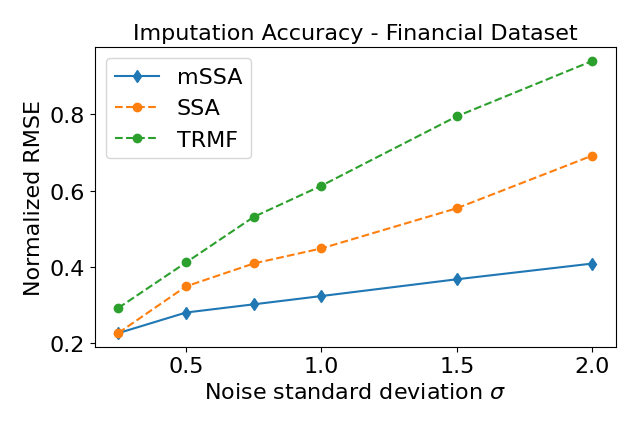

Table 2 compares the (effective) rank of the stacked Page matrices for different benchmark time series data sets. The value of equals , , and for the Financial, Electricity, and Traffic datasets respectively (see Appendix B for details on the datasets). We set for all datasets. When , this corresponds to equals , , and for the Financial, Electricity, and Traffic datasets respectively. Table 2 shows the effective rank in each dataset as we vary . As can be seen, for , the effective rank is much smaller than (or ) suggesting that SSA is likely to be effective. For Electricity and Financial datasets, the rank does not change by much as we increase . However, relatively the rank does increase substantially for the Traffic dataset. This might explain why mSSA is relatively less effective for the Traffic dataset in contrast to the Financial and Electricity datasets as noted in Table 1.

| Dataset | N = 1 | N =10 | N = 100 | N = 350 |

|---|---|---|---|---|

| Electricity | 19 | 37 | 44 | 31 |

| Financial | 1 | 3 | 3 | 6 |

| Traffic | 14 | 32 | 69 | 116 |

4 Main Results

We now provide bounds on the imputation and forecasting prediction error for mSSA under the spatio-temporal model introduced in Section 3. We start by defining the metric by which we measure prediction error. For imputation, we define prediction error as

| (7) |

Here, the imputed estimate are produced by the imputation algorithm of Section 1.1. For forecasting, we define the in-sample prediction error as

| (8) |

Further, let such that . Then, we define the out-of-sample prediction error as

| (9) |

Again, the forecasted estimate are produced by the forecasting algorithm of Section 1.1. In (7), (8), and (9), the expectation is with respect to the randomness in observations due to noise and missingness.

4.1 Assumptions

To state the main results, we make the following assumptions. Recall from (1) that for each and , we observe with probability independently. We shall assume that noise satisfy the following property.

Property 3.

For , are independent sub-gaussian random variables, with and .

For definition of -norm, see [37], for example.

Property 4.

(Balanced spectra). Denote the stacked Page matrix associated with all time series as . Under the setup of Proposition 3.2, and . Then, for , is such that for some absolute constant , where is the -th largest singular value of .

Note that if , then one can verify that Property 4 holds. Indeed, assuming that the non-zero singular values are ‘well-balanced’ is standard in the matrix/tensor estimation literature. To state our results for out-of-sample forecasting error, let be the stacked Page matrix associated with all time series entries for . We assume an analogous condition on as we do for .

Property 5.

(Balanced spectra (out-of-sample)). Under the setup of Proposition 3.2, we have that and . Then, for , is such that for some absolute constant , where is the -th largest singular value of .

Again, note that if , then one can verify that Property 5 holds.

Lastly, we shall first impose some restrictions on the complexity of the time series for . Let denote the matrix formed using the top rows of . Define analogously with respect to . Let and denote the subspace of spanned by the columns of and , respectively. We assume the following property.

Property 6.

(Subspace inclusion). .

Intuitively, this requires that to effectively forecast, the associated stacked Page matrix of the out-of-sample time series is only as “rich” as that of .

Picking hyper-parameter . The proof of Theorems 4.1, 4.2, and 4.3 imply the optimal choice of is to set it to . Intuitively, this choice of leads to the stacked Page matrix to be as square as possible, and our analysis implies that the error rate is inversely proportional to the minimum of the number of the rows and columns of . Hence, for the remainder of the paper, we state our results for .

Picking hyper-parameter . For our theoretical result, we assume that we pick , where is the rank of . Empirically, we pick to equal the “effective rank” of the observed Page matrix as defined in Section 3.2.

4.2 Finite-sample Analysis for Imputation and Forecasting

Now we state the main results. In what follows, we let denote a constant thats depends only (polynomially) on model parameters . We also remind the reader that are defined in Property 1, in 2, in Property 3 and in Property 4.

Imputation. We begin with our imputation result.

Theorem 4.1 (Imputation).

In-sample forecasting. Recall from (5) that in mSSA, we learn a linear model between the last row of and the rows above it (after de-noising the sub-matrix induced these rows via HSVT). Hence, we first establish that in the idealized scenario (no noise, no missing values), there does indeed exist a linear model between the last row and the rows above of . Let denote the -th row of and recall denotes the sub-matrix of formed by selecting top rows. In the proposition below, we show there exists a linear relationship between and .

Theorem 4.2 (In-sample forecasting).

Out-of-sample forecasting.

Theorem 4.3 (Out-of-sample Forecasting).

Corollary 4.1.

Let the conditions of Theorem 4.3 hold. Then, with , we have

| (13) |

5 Approximate Low-Rank Hankel Representation

In this section, we extend the model presented in Section 3 by relaxing Property 2 to only hold approximately. We establish a ‘calculus’ for this extended model – the set of time series functions which have this approximate low-rank Hankel representation is closed under component-wise addition and multiplication. We show important examples of time series dynamics studied in the literature have an approximate low-rank Hankel representation. Lastly, we present generalizations of Theorems 4.1 and 4.2 for this extended model.

5.1 Approximate Low-rank Hankel Representation and Hankel Calculus

We first introduce the definition of the approximate rank of a matrix.

Definition 5.1 (-approximate rank).

Given , a matrix is said to have -approximate rank at most if there exists a rank matrix such that .

Definition 5.2 (-Hankel Time Series).

For a given and , a time series is called a -Hankel time series if for any , its Hankel matrix has -approximate rank .

Property 7.

For each and for any , the Hankel Matrix associated with time series has -approximate rank at most for . That is, for each , is a -Hankel time series.

We state an implication of the above stated properties on the stacked Page matrix.

Proposition 5.1.

Hankel calculus. We present a key property of the model class satisfying Property 7, i.e. time series that have an approximate low-rank Hankel matrix representation. To that end, we define ‘addition’ and ‘multiplication’ for time series. Given two time series , define their addition, denoted as for all . Similarly, their multiplication, denoted as Now, we state a key property for the model class satisfying Property 7 (proof in Appendix E).

Proposition 5.2.

For , let be a -Hankel time series for . Then, is a -Hankel time series and is a -Hankel time series.

5.2 Examples of -Hankel Time Series

We establish that many important classes of time series dynamics studied in the literature are instances of -Hankel time series, i.e. they satisfy Property 7. In particular, any differentiable periodic function (Proposition 5.4), and any time series with a Hölder continuous latent variable representation (Proposition 5.5). Proofs of Propositions 5.3, 5.4, and 5.5 can be found in Appendix E.

Example 1. -LRF time series. We start by defining a linear recurrent formula (LRF), which is a standard model for linear time-invariant systems.

Definition 5.3 (-LRF).

For and , a time series is said to be a -Linear Recurrent Formula (LRF) if for all and , there exists such that

where for all , (i) with constants , and (ii) .

Now we establish a time series that is a -LRF is also -Hankel.

Proposition 5.3.

If is -LRF representable, then it is -Hankel representable.

LRF’s cover a broad class of time series functions, including any finite sum of products of harmonics, polynomials and exponentials. In particular, it can be easily verified that a time series described by (6) is a -LRF, where with .

Example 2. “smooth” and periodic time series. We establish that any differentiable periodic function is -LRF and hence -Hankel for appropriate choices of and .

Definition 5.4 ().

For and , we use to denote the class of all time series such that it is periodic, i.e. for all and the -th derivative of , denoted , exists and is continuous.

Proposition 5.4.

Any is

for any . Here is a term that depends only on and .

Example 3. time series with latent variable model (LVM) structure. We now show that if a time series has a LVM representation, and the latent function is Hölder continuous, then it has a -Hankel representation for appropriate choice of and . We first define the Hölder class of functions; this class of functions is widely adopted in the non-parametric regression literature [38]. Given a function , and a multi-index , let the partial derivate of at , if it exists, be denoted as where and .

Definition 5.5 (-Hölder Class).

Given , the Hölder class on is defined as the set of functions whose partial derivatives satisfy for all , Here refers to the greatest integer strictly smaller than and .

Note that if , then the definition above is equivalent to the -Lipschitz condition, i.e., for . Given a time series , for any , recall the Hankel matrix is defined such that its entry in row and column is given by . We call a time series to have -Hölder smooth LVM representation for if for any given , the corresponding Hankel matrix satisfies: for , where are latent parameters and for any . It can be verified that a -Hankel time series is an instance of such a LVM representation with corresponding . Thus in a sense, this model is a natural generalization of the -Hankel matrix representation. The following proposition connects this LVM representation to the -Hankel representation for appropriately defined .

Proposition 5.5.

Given , let have -Hölder smooth LVM representation. Then for all , is

Here is a term that depends only on and .

5.3 Extending Main Results

Below, we provide generalizations of the imputation and in-sample forecasting results stated in Section 4. To do so, we utilize Property 8 which is analogous to Property 4 but for the approximate low-rank setting.

Property 8.

(Approximately balanced spectra). Under the setup of Proposition 5.1, we can represent the stacked Page matrix associated with all time series as with and and . Then, for , is such that for some absolute constant , where is the -th largest singular value of .

Theorem 5.6 (Imputation).

6 Experiments

We describe experiments supporting our theoretical results for mSSA. In particular, we provide details of the experiments run to create the summary results described earlier in Table 1. In Appendix B, we describe the datasets utilized and the various algorithms we compare with as well as the procedure for selecting the hyper-parameters in each algorithm. In Section 6.1 and 6.2, we report the imputation and forecasting results. Note that in all experiments, we use the Normalized Root Mean Squared Error (NRMSE) as out accuracy metric. That is, we normalize all the underlying time series to have zero mean and unit variance before calculating the root mean squared error. We use this metric as it weighs the error on each time series equally.

6.1 Imputation

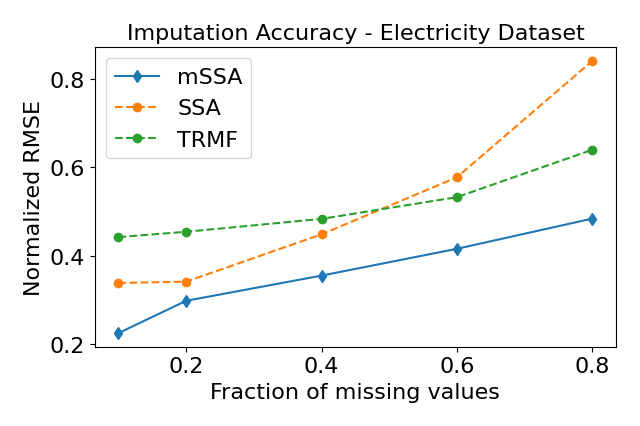

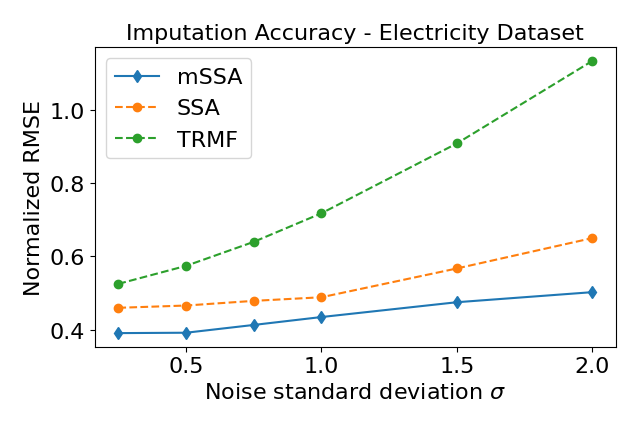

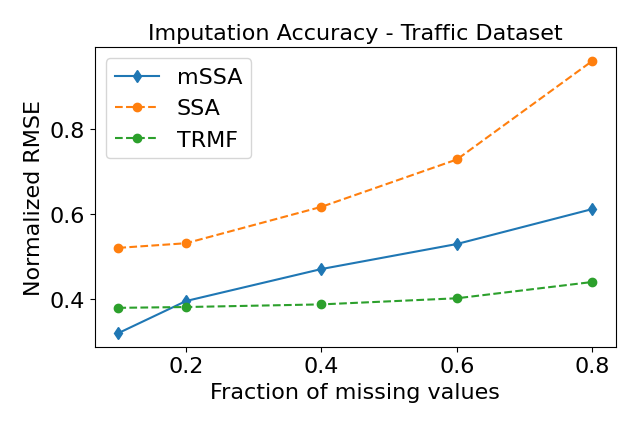

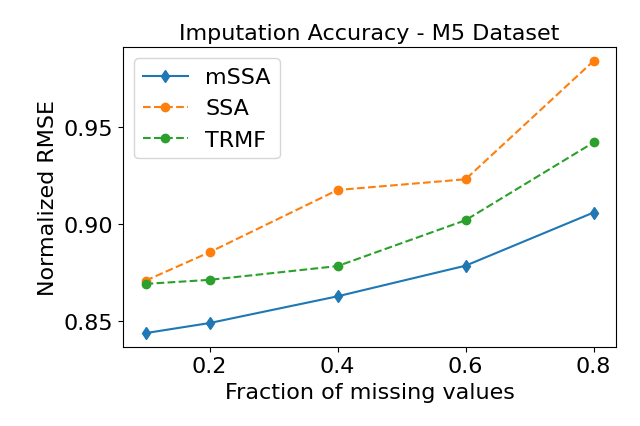

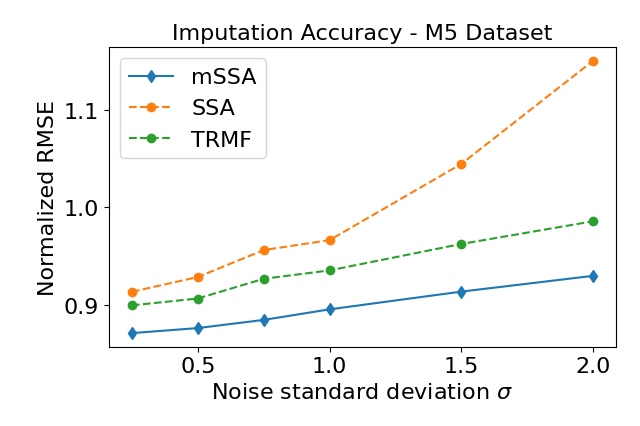

Setup. We test the robustness of the imputation performance by adding two sources of corruption to the data - varying the percentage of observed values and varying the amount of noise we perturb the observations by. We test imputation performance by how accurately we recover missing values. We compare the performance of mSSA with TRMF, a method which achieves state-of-the-art imputation performance. Further, to analyze the added benefit of exploiting the spatial structure in a multivariate time series using mSSA, we compare with the SSA variant introduced in [1] .

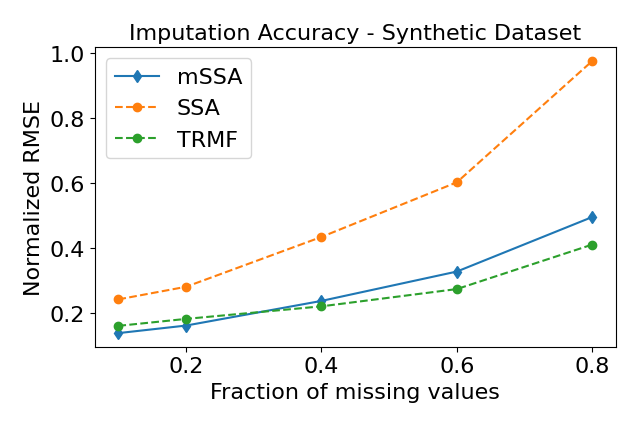

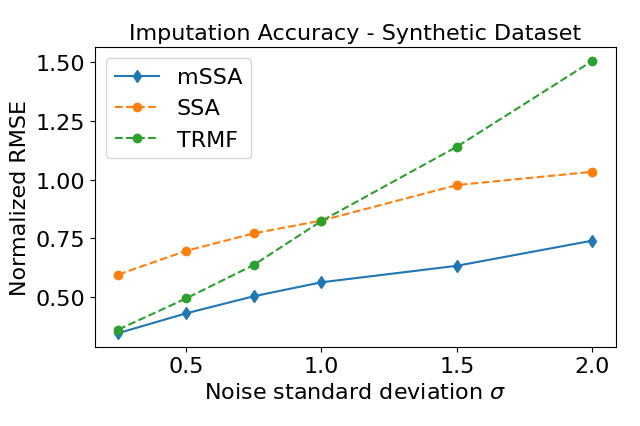

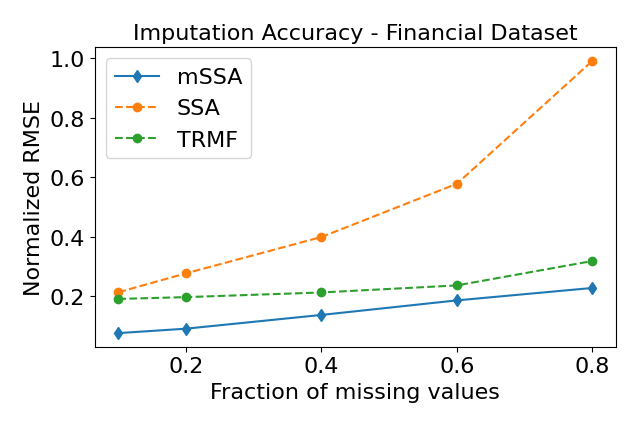

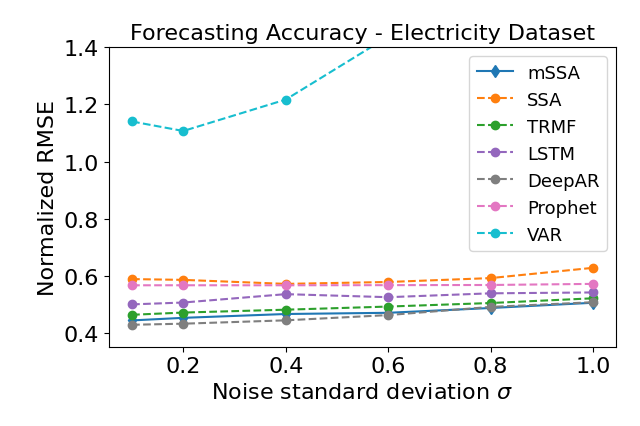

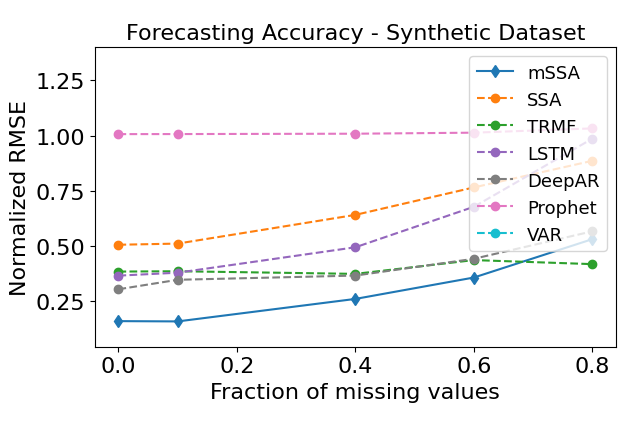

Results. Figures 3(a), 3(c), 3(e), 4(a), and 4(c) show the imputation error in the aforementioned datasets as we vary the fraction of missing values, while Figures 3(b), 3(d), 3(f), 4(b), and 4(d) show the imputation error as we vary , the standard deviation of the gaussian noise. We see that as we vary the fraction of missing values and noise levels, mSSA outperforms both TRMF and SSA in 75% of experiments run. It is noteworthy the large empirical gain in mSSA over SSA, giving credence to the spatio-temporal model we introduce. The average NRMSE across all experiments for each dataset is reported in Table 1, where mSSA outperforms every other method across all datasets except for the Traffic dataset.

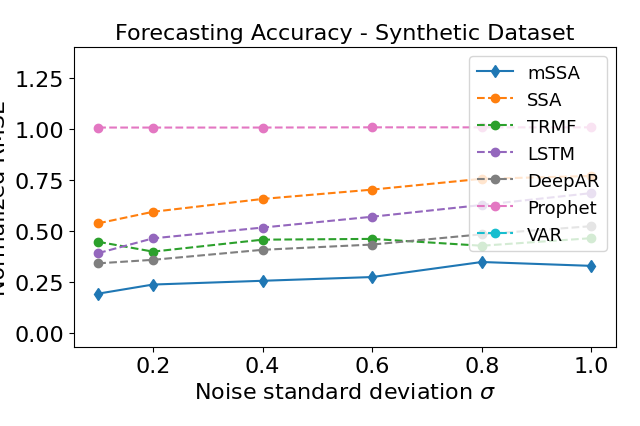

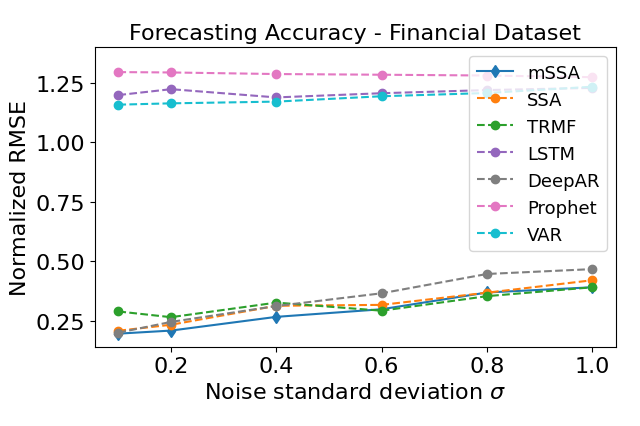

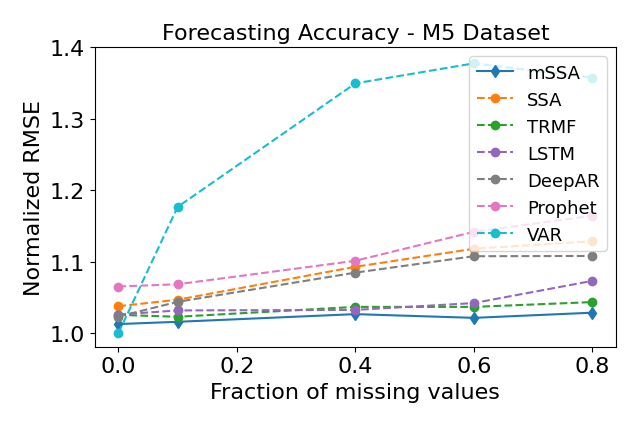

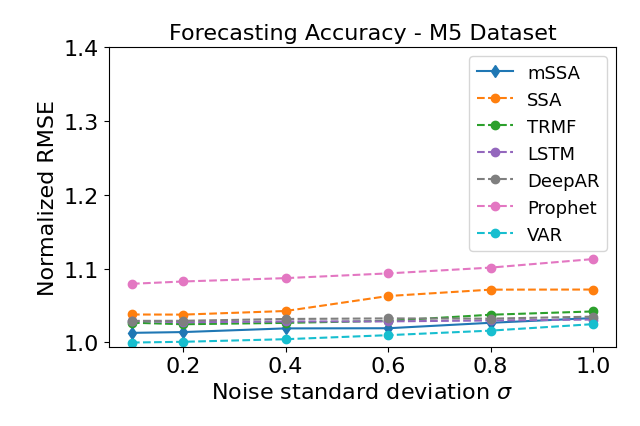

6.2 Forecasting

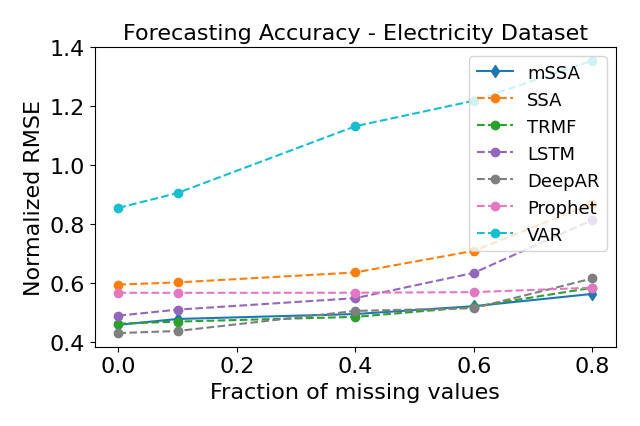

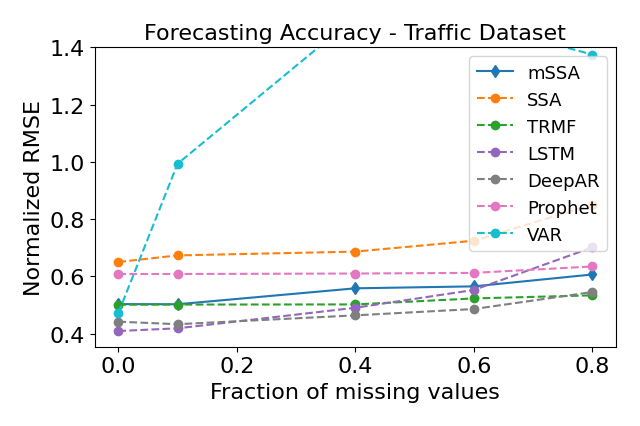

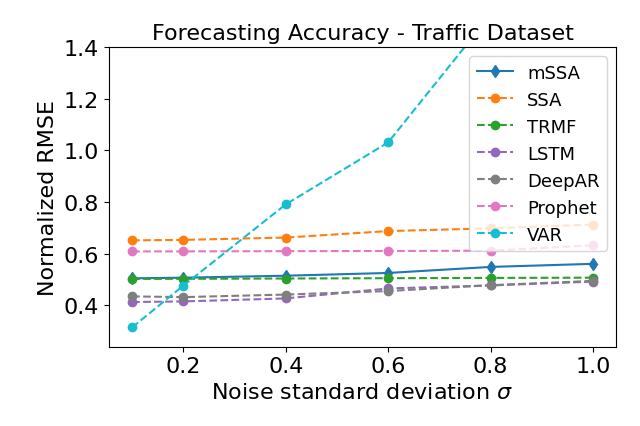

Setup. We test the forecasting accuracy of the proposed mSSA against several state-of-the-art algorithms. For each dataset, we split the data into training, validation, and testing datasets as outlined in Appendix B.1. As was done in the imputation experiments, we vary how much each dataset is corrupted by varying the percentage of observed values and the noise levels.

Results. Figures 5(a), 5(c), 5(e), 6(a), and 6(c) show the forecasting accuracy of mSSA and other methods in the aforementioned datasets as we vary the fraction of missing values, while Figures 5(b), 5(d), 5(f), 6(b), and 6(d) show the forecasting accuracy as we vary the standard deviation of the added gaussian noise. We see that as we vary the fraction of missing values and noise level, mSSA is the best or comparable to the best performing method in 80% of experiments. In terms of the average NRMSE across all experiments, we find that mSSA performs similar to or better than every other method across all datasets except for the traffic dataset as was reported in Table 1.

7 Algorithmic Extensions of mSSA

7.1 Variance Estimation

We extend the mSSA algorithm to estimate the time-varying variance of a time series by making the following simple observation. If we apply mSSA to the squared observations, , we will recover an estimate of (for ). However, observe that . Therefore, by applying mSSA twice, once on and once on for and , and subsequently taking the component-wise difference of the two estimates will lead to an estimate of the variance. This suggests a simple algorithm which we describe next. We note this observation suggests any mean estimation algorithm (or imputation) in time series analysis can be converted to estimate the time varying variance – this ought to be of interest in its own right.

Algorithm. As described in Section 1.1, let and be algorithm parameters. First, apply mSSA on observations to produce imputed estimates using the hyper-parameters and . Next, apply mSSA on observations to produce imputed estimates using the hyper-parameters and . Lastly, we denote as our estimate of the time-varying variance.

Model. For , let be the time-varying variance of the time series observations, i.e., if then . Let be the matrix induced by the latent time-varying variances of the time series of interest, i.e., the entry in row at time in is . To capture the “spatial” and “temporal” structure across the latent time-varying variances, we assume the latent variance matrix satisfies Properties 9 and 10. These properties are analogous to those assumed about the latent mean matrix (defined in Section 3); in particular, Properties 1 and 2. We state them next.

Property 9.

Let , i.e, for any , where the factorization is such that , for .

Like Property 1, the above property captures the “spatial” structure within time series of variances. To capture the “temporal” structure, next we introduce an analogue of Property 2. To that end, for each , define the Hankel matrix of each time series as , where for .

Property 10.

For each , the Hankel Matrix associated with time series has rank at most .

Result. To establish the estimation error for the variance estimation algorithm under the spatio-temporal model above, we need the following additional property (analogous to Property 4).

Property 11 (Balanced spectra).

Theorem 7.1 (Variance Estimation).

7.2 Tensor SSA

Page tensor. We introduce an order-three tensor representation of a multivariate time series which we term the ‘Page tensor’. Given time series, with observations over time steps and hyper-parameter , define such that

| (17) |

The corresponding observation tensor, , is

| (18) |

See Figure 7 for a visual depiction of .

Let the CP-rank of an order- tensor be the smallest value of such that , where are latent factors for . Under the model described in Section 3, we have the following properties.

Proposition 7.1.

tSSA: time series imputation using the Page tensor representation. The Page tensor representation and Proposition 7.1 collectively suggest that time series imputation can be reduced to low-rank tensor estimation, i.e., recovering a tensor of low CP-rank from its noisy, partial observations. Over the past decade, the field of low-rank tensor (and matrix) estimation has received great empirical and theoretical interest, leading to a large variety of algorithms including spectral, convex optimization, and nearest neighbor based approaches. We list a few works which have explicit finite-sample rates for noisy low-rank tensor completion [6, 42, 11, 44, 34]). As a result, we “blackbox” the tensor estimation algorithm used in tSSA as a pivotal subroutine. Doing so allows one the flexibility to use the tensor estimation algorithm of their choosing within tSSA. Consequently, as the tensor estimation literature continues to advance, the “meta-algorithm” of tSSA will continue to improve in parallel. To that end, we give a definition of a tensor estimation algorithm for a generic order- tensor. Note that when , this reduces to standard matrix estimation (ME).

Definition 7.2 (Matrix/Tensor Estimation).

For , denote as an order- tensor estimation algorithm. It takes as input an order- tensor with noisy, missing entries, where and is the probability of each entry in being observed. then outputs an estimate of denoted as .

We assume the following ‘oracle’ error convergence rate for ; for ease of exposition, we restrict our attention to the setting where .

Property 12.

For , assume satisfies the following: the estimate , which is the output of with , satisfies

| (19) |

Here, suppresses dependence on noise, i.e., , factors, and CP-rank of .

Property 12 holds for a variety of matrix/tensor estimation algorithms. For , it holds for HSVT as we establish in the proof of Theorem 4.1 for mSSA of . It is straightforward to show that this is the best rate achievable for . For , it has recently been shown that Property 12 provably holds for a spectral gradient descent based algorithm [11] (see Corollary 1.5 of [11]), conditioned on certain standard “incoherence” conditions imposed on the latent factors of ; another spectral algorithm that achieved the same rate was furnished in [42], which the authors also establish is minimax optimal.

tSSA algorithm. We now define the “meta” tSSA algorithm; the two algorithmic hyper-parameters are (defined in (18)) and (the order-three tensor estimation algorithm one chooses). First, using for , construct Page tensor as in (18). Second, obtain as the output of and read off by selecting appropriate entry in .

Algorithmic comparison: tSSA vs. mSSA vs. ME. We now provide a unified view of tSSA, mSSA, and “vanilla” ME (which we describe below) to do time series imputation. All three methods have two key steps: (i) data transformation – converting the observations into a particular data representation/structure; (ii) de-noising– applying some form of matrix/tensor estimation to de-noise the constructed data representation.

- •

-

•

mSSA – using , create the stacked Page matrix as detailed in Section 1.1; apply to get (where we use HSVT for ); read off by selecting appropriate entry in .

-

•

ME – using , create , where is equal to ; apply (e.g. using HSVT as in mSSA) to get ; read off by selecting appropriate entry in .

This perspective also suggests that one can use any “blackbox” matrix estimation routine to de-noise the constructed stacked Page matrix in mSSA; HSVT is one such choice that we analyze.

Theoretical comparison: tSSA vs. mSSA vs. ME. We now do a theoretical comparison of the relative effectiveness of tSSA, mSSA, and ME in imputing a multivariate time series for , as we vary and . To that end, let , , and denote the imputation error for tSSA, mSSA, and ME, respectively.

Proposition 7.2.

For tSSA and mSSA, pick hyper-parameter , respectively. Let Property 12 hold. Then,

-

(i)

: ;

-

(ii)

: , ;

-

(iii)

: , ,

where , suppresses dependence on noise parameters, CP-rank, poly-logarithmic factors.

We note given Property 12, is optimal for tSSA and is optimal for mSSA. See Figure 2 in Section 1 for a graphical depiction of the different regimes in Proposition 7.2. Proofs of Proposition 7.1 and 7.2 below can be found in Appendix L.

Application to Time-varying Recommendation Systems In Appendix C, we discuss the extension of our spatio-temporal model and tSSA to time-varying recommendation systems.

8 Conclusion

We provide theoretical justification of a practical, simple variant of mSSA, a method heavily used in practice but with limited theoretical understanding. We show how to extend mSSA to estimate time-varying variance and introduce a tensor variant, tSSA, which builds upon recent advancements in tensor estimation. We hope this work motivates future inquiry into the connections between the classical field of time series analysis and the modern, growing field of matrix/tensor estimation.

Appendix A Page vs. Hankel mSSA

This section discusses the benefits and drawbacks of using the Page matrix representation, as we propose in our variant, instead of the Hankel representation used in the original mSSA. Recall the key steps of the original SSA method in Section 2. The extension to mSSA is done by stacking the Hankel matrices induced by each of the time series either column-wise (horizontal mSSA) or row-wise (vertical mSSA) [24]. In this section, we will use mSSA to denote our mSSA variant, and hSSA/vSSA to denote the original horizontal/vertical mSSA. In what follows, we will compare our mSSA variant with hSSA/vSSA in terms of their: (i) theoretical analysis; (ii) computational complexity; and (iii) empirical performance.

Theoretical analysis. We re-emphasize that to the best of our knowledge, the theoretical analysis of the mSSA algorithm, both hSSA and vSSA, have been absent from the literature, despite their popularity. We do a comprehensive theoretical analysis of the variant of mSSA we propose. By utilizing the Page matrix, it allows us to invoke results from random matrix theory to prove our imputation and forecasting results. However, extending our analysis to the Hankel matrix representation is challenging as the Hankel matrix has repeated entries of the same time series observation. This leads to correlation in the noise in the observation of the entries of the Hankel matrix, which prevents us from invoking the results from random matrix theory in a straightforward way. The Page matrix representation does not have repeated entries of the same observation, and thus allows us to circumvent this issue in our theoretical analysis.

Computational complexity. Our mSSA variant is computationally far more efficient than both hSSA and vSSA. This is because the Page matrix representation of a multivariate time series with N time series and T time steps is a matrix of dimension (with )., i.e., it has a total of entries. In contrast, the Hankel matrix representation is of dimension for hSSA and for vSSA (we set the parameter to as recommended in [24]), i.e., both variants of the Hankel matrix have entries. This makes computing the SVD (the most computationally intensive step of mSSA) prohibitive for hSSA and mSSA even for the standard time series benchmarks we consider in Section 6.

To empirically demonstrate the computational efficiency of our variant of mSSA, we compare its training time to that of hSSA and vSSA. Specifically, we measure the training time for mSSA, hSSA, and vSSA as we increase the number of time steps . We perform this experiment on two datasets: (i) the synthetic dataset; (ii) a subset of the electricity dataset, where we choose only 50 of the available 370 time series. Both datasets are described in details in Appendix B. Figure 8 shows that in both datasets, the training time of both hSSA and vSSA can be as 600-1000x as high as the training time of our mSSA variant as we increase .

Empirical performance. Here, we compare the forecasting performance of mSSA to that of hSSA and vSSA. We report performance in terms of the NRMSE of the three methods as we increase the number of time steps in the aforementioned synthetic and electricity dataset. The goal in the synthetic dataset is to predict the next 50 time steps using one step ahead forecasts, while the goal in the electricity dataset is to predict the next three days using day-ahead forecasts. For hSSA and vSSA, we choose as recommended in [24]; and for mSSA, we choose . For all three methods, we choose the number of retained singular values based on the thresholding procedure outlined in [17].

Figures 9 shows the performance of the three methods in both datasets. We find that initially, with few data points ( in the synthetic data and in the electricity data), both hSSA and vSSA outperform mSSA. As we increase , mSSA performance significantly improves and eventually outperforms vSSA. In the electricity dataset, mSSA performs similar to hSSA for . These experiments suggest that if only a few observations were available, hSSA and vSSA might provide better performance. However, if the number of observations were relatively large, then the performance of mSSA is superior to vSSA and relatively similar to hSSA.

Importantly, the electricity dataset experiment illustrates a critical advantage of our mSSA variant. Specifically, when is large such that running hSSA or vSSA is computationally infeasible, then one can achieve better accuracy using mSSA. For example, while we could not run the hSSA and vSSA on the electricity dataset with due to memory constraints, we were able to run mSSA and achieve a lower NRMSE. This suggests that our mSSA variant is the more practical mSSA algorithm when it comes to efficiently utilizing large multivariate time series.

Appendix B Experiment Details

In Appendix B.1, we describe the datasets utilized. In Appendix B.2, we describe the various algorithms we compare with as well as the choice of hyper-parameters used for each of them.

B.1 Datasets

We use four real-world datasets and one synthetic dataset. The description and preprocessing we do for each of these datasets are as follows.

| Dataset |

|

|

|

|

|

|

|

|

||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Electricity | 370 | 26136 | 24 | 1 to 25824 | 2 | 25825 to 25968 | 7 | 25969 to 26136 | ||||||||||||||||

| Traffic | 963 | 10560 | 24 | 1 to 10248 | 2 | 10249 to 10392 | 7 | 10393 to 10560 | ||||||||||||||||

| Synthetic | 50 | 15000 | 10 | 1 to 13700 | 10 | 13701 to 14000 | 100 | 14001 to 15000 | ||||||||||||||||

| Financial | 839 | 3993 | 1 | 1 to 3693 | 40 | 3694 to 3813 | 180 | 3814 to 3993 | ||||||||||||||||

| M5 | 15678 | 1941 | 28 | 1 to 1829 | 1 | 1830 to 1913 | 1 | 1914 to 1941 |

Electricity Dataset. This is a public dataset obtained from the UCI repository which shows the 15-minutes electricity load of 370 households [36]. As was done in [45],[33],[31], we aggregate the data into hourly intervals and use the first 25824 time-points for training, the next 288 points for validation, and the last 168 points for testing in the forecasting experiments. Specifically, in our testing period, we do 24-hour ahead forecasts for the next seven days (i.e. 24-step ahead forecast). See Table 3 for more details.

Traffic Dataset. This public dataset obtained from the UCI repository shows the occupancy rate of traffic lanes in San Francisco [36]. The data is sampled every 15 minutes but to be consistent with previous work in [45], [33], we aggregate the data into hourly data and use the first 10248 time-points for training, the next 288 points for validation, and the last 168 points for testing in the forecasting experiments. Specifically, in our testing period, we do 24-hour ahead forecasts for the next seven days (i.e. 24-step ahead forecast). See Table 3 for more details.

Financial Dataset. This dataset is obtained from the Wharton Research Data Services (WRDS) and contains the average daily stocks prices of 839 companies from October 2004 till November 2019 [41]. The dataset was preprocessed to remove stocks with any null values, or those with an average price below 30$ across the aforementioned period. This was simply done to constrain the number of time series for ease of experimentation and we end up with 839 time series (i.e. stock prices of listed companies) each with 3993 readings of daily stock prices. In our forecasting experiments, we train on the first 3693 time points, validate on the next 120 time points, while for testing we consider the task of predicting 180 time-points ahead one point at a time. That is, the goal here is to do one-day ahead forecasts for the next 180 days (i.e. 1-step ahead forecast). We choose to do so as this is a standard goal in finance. See Table 3 for more details.

M5 Dataset. This public dataset obtained from Kaggle’s M5 Forecasting competition include daily sales data of 30490 items across different Walmart stores for 1941 days [26]. The dataset was preprocessed to only include items that has more than zero sales in at least 500 days. For forecasting, as is the goal in the Kaggle competition, we consider the task of predicting the sales for the next 28 days (i.e. 28-step ahead forecast). We use the first 1829 points for training, the next 84 points for cross validation, and the last 28 points for testing.

Synthetic Dataset. We generate the observation tensor by first randomly generating the two matrices and ; we do so by randomly sampling each coordinate of independently from a standard normal. Then, we generate mixtures of harmonics where each mixture is generated as: where the parameters are selected uniformly at randomly from the ranges and , respectively. Then each value in the observation tensor is constructed as follows: where is the tensor rank, , . In our experiment, we select , , , and . This gives us time series each with observations per time series. In the forecasting experiments, we use the first points for training, the next 300 points for validation, while for testing, we do -step ahead forecasts for the final points. See Table 3 for more details.

B.2 Algorithms.

In this section, we describe the algorithms used throughout the experiments in more detail and the hyper-parameters/implementation used for each method.

mSSA & SSA. Note that since the SSA’s variant described in [1] is a special case of our proposed mSSA algorithm, we use our mSSA’s implementation to perform the SSA experiments; key difference in SSA is that we do not “stack” the various Page matrices induced by each time series. For all experiments we choose the parameters through the cross validation process detailed in Appendix B.3, where we perform a grid search for the following parameters:

-

1.

The number of retained singular values, . This parameter is chosen using one of the following data-driven methods: (i) we choose based on the thresholding procedure outlined in [17], where the threshold is determined by the median of the singular values and the shape of the matrix; (ii) we choose as the minimum number of singular values capturing of its spectral energy; (iii) we choose a constant low rank, specifically .

-

2.

The shape of the Page matrix. For mSSA, we vary the shape of the Page matrix by choosing for the electricity and Traffic datasets, for the synthetic dataset, for the financial dataset, and for the M5 dataset . For SSA, we choose in the electricity and Traffic datasets, in the synthetic dataset, in the financial dataset, and in the M5 dataset.

-

3.

Missing values initialization. Initializing the missing values is done according to one of two methods: (i) set the missing values to zero; (ii) perform forward filling where each missing value is replaced by the nearest preceding observation, followed by backward filling to accommodate the situation when the first observation is missing.

DeepAR. We use the “DeepAREstimator” algorithm provided by the GluonTS package. We choose the parameters through a grid search for the following parameters:

-

1.

Context length. This parameter determines the number of steps to unroll the RNN for before computing predictions. We choose this from the set , where is the prediction horizon.

-

2.

Number of Layers. This parameter determines the number of RNN layers. We choose this from the set .

TRMF. We use the implementation provided by the authors in the Github repository associated with the paper ([45]). We choose the parameters through a grid search, as suggested by the authors in their codebase, for the following parameters:

-

1.

Matrix rank . This parameter represents the chosen rank for the time series matrix, we choose from the set .

-

2.

Regularization parameters . We choose these parameters from as suggested in the authors repository.

For the lag indices , we include the last day and the same weekday in the last week for the traffic and electricity data, the last 30 points for the financial and synthetic dataset, and the last 10 points for the M5 dataset.

LSTM. Across all datasets, we use an LSTM network with hidden layers each, with neurons per layer, as is done in [33]. We use the Keras implementation of LSTM. As with other methods’ parameters, is chosen via cross validation.

Prophet. We used Prophet’s Python library with the parameters selected using a grid search of the following parameters as suggested in [15]:

-

1.

Changepoint prior scale. This parameter determines how much the trend changes at the detected trend changepoints. We choose this parameter from .

-

2.

Seasonality prior scale. This parameter controls the magnitude of the seasonality. We choose this parameter from .

-

3.

Seasonality Mode. Which is chosen to be either ’additive‘ or ’multiplicative‘.

VAR. We used the VAR estimator in the python package “statsmodels” ([32]). We apply the method on the first difference of the time series and verify that the series are not non-stationary using a unit root test (specifically, Augmented Dickey–Fuller test). For all datasets except M5, we choose the best value for the parameter max_lag . This parameter corresponds to the maximum number of lags used in fitting the VAR process. For M5, we choose max_lag , as fitting the model for larger values is computationally infeasible.

B.3 Parameters Selection

In all experiments, we choose the hyperparameters for out method and for the baselines by using cross-validation. Below, we detail the procedure for both imputation and forecasting experiments.

Imputation Experiments. To select the parameters in our imputation experiments, we additionally mask 10% of the observed data uniformly at random. Then, we evaluate the performance of each parameter choice in recovering these additionally masked observations. This process is repeated 3 times, and the choice of parameters that achieves the best performance (in NRMSE) across these runs is selected. In our results, we report the accuracy of the selected parameters in recovering the original missing values.

Forecasting Experiments. For parameters selection in the forecasting experiments, we use cross-validation on a rolling basis as typically used in time-series forecasting models [25]. In this procedure, there are multiple validation sets. For each validation set, we train the model only on previous observations. That is, no future observations can be used in training the model, which will occur when a typical cross-validation procedure is followed for time series data. In our experiments, we start with a subset of the data used for training, then we forecast the first validation set using -step ahead forecasts for windows , where the horizon and the number of validation windows are detailed in Table 3. We do this for three validation sets, each of length , and select the choice of parameters that achieves the best performance (in NRMSE) for evaluation on the test set. When evaluating on the test set, both the training and validation periods are used for training.

Appendix C Time-varying Recommendation Systems

In Section 7.2, we considered the setting where the matrix induced by the latent time series is low-rank; in particular, Property 1 captures this spatial structure across these time series. However, in many settings there is additional spatial structure across the time series.

Recommendation systems – time-varying matrices/tensors. For example, in recommendation systems, for each , there is a matrix, of interest. The -th row and -th column of denotes the latent rating user has for product , i.e., denotes the value of the latent time series at time step . To capture the latent structure across users and products, one typically assumes that each is low-rank. More generally, at each time step , could be an order- tensor. That is, denotes the value of the latent time series at time step for . For example, if , might represent the -th measurement for a collection of -spatial coordinates. Let denote the order tensor induced by viewing each order- tensor as the -th ‘slice’ of , for . Again, to capture the spatial and temporal structure of these latent time series, we posit the following spatio-temporal model for , which is a higher-order analog of the model assumed in Property 1.

Property 13.

Let have CP-rank at most . That is, for any

| (20) |

where the factorization is such that , for constants .

As before, to explicitly model the temporal structure, we continue to assume Property 2 holds for the latent time factors for .

Order- Page tensor representation. We now consider the following order- Page tensor representation of . In particular, given the hyper-parameter , define such that for ,

| (21) |

The corresponding observation tensor, , is

| (22) |

Recall from (1) that is the noisy, missing observation we get of . and then have the following property:

Proposition C.1.

Analogous to Proposition 7.1, Proposition C.1 also establishes that order- Page tensor representation of the various latent time series has CP-rank that continues to be bounded by . Proof of Proposition C.1 can be found in Appendix L.

Higher-order tensor singular spectrum analysis (htSSA). Proposition C.1 motivates the following algorithm, which exploits the further spatial structure amongst the time series. We now define the “meta” htSSA algorithm. The two algorithmic hyper-parameters are (defined in (18)) and (the order- tensor estimation algorithm one chooses). First, using the observations for we construct the higher-order Page tensor as in (22). Second, we obtain as the output of , and read off by selecting the appropriate entry in .

Relative effectiveness of mSSA, htSSA, and tensor estimation (TE). Again, for ease of exposition, we consider the case where . We now briefly discuss the relative effectiveness of htSSA, mSSA,and “vanilla” tensor estimation (TE) in imputing to estimate . mSSA and htSSA have been previously described. In TE, one directly de-noises the original order- tensor induced by the noisy observations, which we denote , where . In particular, one produces an estimate of , and then produces the estimates by reading off the appropriate entry of . Let , , and denote the imputation error for htSSA, mSSA, and TE, respectively. Now if we assume Property 12 holds, we have

| (23) | ||||

| (24) | ||||

| (25) |

Then just as was done in the proof of Proposition 7.2, for any given , one can reason about the relative effectiveness of htSSA, mSSA, and TE for different asymptotic regimes of the relative ratio of and .

Appendix D Proof of Proposition 5.1

Below, we present the proof of Proposition 5.1. First we define the stacked Hankel matrix of time series over time steps. Precisely, given latent time series , consider the stacked Hankel matrix induced by each of them over time steps, , defined as follows. It is where its entry in row and column , , is given by

| (26) |

We now establish Proposition D.1, which immediately implies Proposition 5.1 – the stacked Page matrix can be viewed as a sub-matrix of , by selecting the appropriate columns.

Proposition D.1.

Proof.

We have latent time series satisfying Properties 1 and 7. Consider their stacked Hankel matrix over , . By definition for and for , we have

| (27) |

That is,

| (28) |

Let be the Hankel matrix associated with over . Due to Property 7, there exists a low-rank matrix such that (a) , (b) . That is, for any , we have that for some . Therefore, for any , we have that

| (29) |

From (28) and (29), we conclude that

| (30) |

Define matrix with its entry for row and column for given by

| (31) |

where and . Further,

| (32) |

That is, the stacked Hankel matrix of time series of has -approximate rank with . This completes the proof. ∎

Appendix E Proofs For Section 5

E.1 Proof of Proposition 5.2

Proof.

Let have a and -Hankel representation, respectively. For any , let be the Hankel matrices of , respectively, over the time interval . By definition, there exists matrices such that , and , .

Component-wise addition. Note the Hankel matrix of over is . Then, matrix has rank at most since for any two matrices and , it is the case that . Further, . Therefore it follows that has -Hankel representation.

Component-wise multiplication. For , its Hankel over is given by where we abuse notation of in the context of matrices as the Hadamard product of matrices. Let . Then since for any two matrices and , . Now

| (33) |

This completes the proof of Proposition 5.2. ∎

E.2 Proof of Proposition 5.3

E.3 Proof of Proposition 5.4

E.3.1 Helper Lemmas for Proposition 5.4

We begin by stating some classic results from Fourier Analysis. To do so, we introduce some notation. Throughout, we have .

and functions. is the set of real-valued, continuous functions defined on . is the set of square integrable functions defined on , i.e.

Inner Product of functions in . is a space endowed with inner product defined as , and associated norm as .

Fourier Representation of functions in . For , define its -order Fourier representation, as

| (34) |

where with are called the Fourier coefficients of , defined as

We now state a classic result from Fourier analysis.

Theorem E.1 ([20]).

Given , let . Then, for any (or more generally ),

| (35) |

We next argue that if , then its Fourier coefficients decay rapidly.

Lemma E.2.

Given , let . Then, for , the -order Fourier coefficient of , the -th derivative of , recursively satisfy the following relationship: for ,

| (36) |

E.3.2 Completing Proof of Proposition 5.4

Proof.

For , let be defined as in (34). Then for

where is a constant that depends only on and ; (a) follows from Theorem E.1; (b) follows from Lemma E.2; (c) follows from Cauchy-Schwarz inequality and fact that for any ; (d) which can be bounded as which is at most since ; (e) follows from Bessel’s inequality, i.e. .

Thus, for any , we have a uniform error bound for being approximated by which is a sum of harmonics. Noting harmonics can be represented by an order- LRF (by Proposition 3.1),we complete the proof. ∎

E.4 Proof of Proposition 5.5

This analysis is adapted from [43].

Proof.

Step 1: Partitioning the space . Consider an equal partition of . Precisely, for any , we partition the the set into half-open intervals of length , i.e, It follows that can be partitioned into cubes of forms with . Let be such a partition with denoting all such cubes and denoting the centers of those cubes.

Step 2: Taylor Expansion of . Consider a fixed . To reduce notational overload, we suppress dependence of on , and abuse notation by using in what follows.

For every with , define as the degree- Taylor’s series expansion of at point :

| (37) |

where is a multi-index with , and is the partial derivative defined in Section 5.2. Note similar to , really refers to .

Now we define a degree- piecewise polynomial

| (38) |

For the remainder of the proof, let (recall refers to the largest integer strictly smaller than ). Since , it follows that

| (39) |

where (a) follows from multivariate version of Taylor’s theorem (and using the Lagrange form for the remainder) and is a vector that can be represented as for ; (b) follows from (37); (c) follows from Holder’s inequality; (d) follows from Definition 5.5.

Step 3: Construct Low-Rank Approximation of Time Series Hankel Using . Recall the Hankel matrix, induced by the original time series over , where with for any . We now construct a low-rank approximation of it using . Define , where .

By (39), we have that for all ,

It remains to bound the rank of . Note that since is a piecewise polynomial of degree for any given , it has the following decomposition: for ,

| (40) |

where for any ,

the vector of all monomials of degree less than or equal to , and is a vector collecting the corresponding coefficients. The number of such monomials is easily show to be equal to . That is, where are of dimension at most for each . That is, has rank at most . Setting completes the proof. ∎

Appendix F Helper Lemmas

We recall known concentration and perturbation inequalities that will be useful throughout.

Theorem F.1 (Bernstein’s Inequality [8]).

Suppose that are independent random variables with zero mean, and M is a constant such that with probability one for each . Let and . Then for any ,

Theorem F.2 (Norm of matrices with sub-gaussian entries [37]).

Let be an random matrix whose entries are independent, mean zero, sub-gaussian random variables. Then, for any , we have

with probability at least . Here, .

Lemma F.3 (Maximum of sequence of random variables [37]).

Let , , be a sequence of random variables, which are not necessarily independent, and satisfy for some and all . Then, for every ,

| (41) |

We note that Lemma F.3 implies that if are random variables with for all , then

Lemma F.4 (Modified Hoeffding Inequality [2] ).

Let be random vector with independent mean-zero sub-Gaussian random coordinates with . Let be another random vector that satisfies almost surely for some constant . Then for all ,

where is a universal constant.

Lemma F.5 (Modified Hanson-Wright Inequality [2] ).

Let be a random vector with independent mean-zero sub-Gaussian coordinates with . Let be a random matrix satisfying and almost surely for some . Then for any ,

Lemma F.6 (Weyl’s inequality).

Given , let and be the -th singular values of and , respectively, in decreasing order and repeated by multiplicities. Then for all ,

Appendix G Matrix Estimation via HSVT

This section describes and analyzes a well-known matrix estimation method, Hard Singular Value Thresholding (HSVT). While the analysis utilizes known arguments from the literature, we need to adapt it for the setting where the underlying ‘signal’ is only approximately low-rank.

G.1 Setup, Notations

Setup. Given a deterministic matrix with and , a random matrix is such that all of its entries, are mutually independent and for any given ,

| (42) |

for some with are independent random variables with and . Given this, we have . Defineff

| (43) |

Goal of Matrix Estimation. The goal of matrix estimation is to produce an estimate from observation so that is close to . In particular, we will be interested in bounding the error between and using the following metric: .

G.2 Matrix Estimation using HSVT

Hard Singular Value Thresholding (HSVT) Map. We define the HSVT map. For any , consider a matrix such that . Here for , is the th largest singular value of and are the corresponding left and right singular vectors respectively. Then, for given any , we define the map , which simply shaves off the singular values of the input matrix that are below the threshold . Precisely,

| (44) |

Matrix Estimating using HSVT map. We define a matrix estimation method using the HSVT map that is utilized by mSSA for imputation. Precisely, we estimate from as follows: given parameter ,

| (45) |

where , i,e. the th largest singular value of .

G.3 A Useful Linear Operator