∗Department of Electrical Engineering, Stanford University, CA 94043, USA.

‡Department of Radiation Oncology, Stanford University, CA 94043, USA.

A Mean-Field Theory for Learning the Schönberg Measure of Radial Basis Functions

Abstract.

We develop and analyze a projected particle Langevin optimization method to learn the distribution in the Schönberg integral representation of the radial basis functions from training samples. More specifically, we characterize a distributionally robust optimization method with respect to the Wasserstein distance to optimize the distribution in the Schönberg integral representation. To provide theoretical performance guarantees, we analyze the scaling limits of a projected particle online (stochastic) optimization method in the mean-field regime. In particular, we prove that in the scaling limits, the empirical measure of the Langevin particles converges to the law of a reflected Itô diffusion-drift process. The distinguishing feature of the derived process is that its drift component is also a function of the law of the underlying process. Using Itô lemma for semi-martingales and Grisanov’s change of measure for the Wiener processes, we then derive a Mckean-Vlasov type partial differential equation (PDE) with Robin boundary conditions that describes the evolution of the empirical measure of the projected Langevin particles in the mean-field regime. In addition, we establish the existence and uniqueness of the steady-state solutions of the derived PDE in the weak sense. We apply our learning approach to train radial kernels in the kernel locally sensitive hash (LSH) functions, where the training data-set is generated via a -mean clustering method on a small subset of data-base. We subsequently apply our kernel LSH with a trained kernel for image retrieval task on MNIST data-set, and demonstrate the efficacy of our kernel learning approach. We also apply our kernel learning approach in conjunction with the kernel support vector machines (SVMs) for classification of benchmark data-sets.

1. Introduction

Radial basis functions (RBFs) are key tools in statistical machine learning to approximate multivariate functions by linear combinations of terms based on a single univariate function. Such non-parametric regression schemes are typically used to approximate multivariate functions or high-dimensional data [39],[8] which are only known at a finite number of points or too difficult to evaluate otherwise, so that then evaluations of the approximating function can take place often and efficiently. The accuracy and performance of such techniques, however, relies to a large extent on a good choice of RBF kernel that captures the structure of data. Standard regression methods based on RBF kernels requires the input of a user-defined kernel—a drawback if a good representation of underlying data is unknown a priori. While statistical model selection techniques such as cross-validation or jackknife [14] can conceptually resolve those statistical model selection issues, they typically slow down the training process on complex data-sets as they repeatedly refit the model. It is thus imperative to devise efficient learning algorithms to facilitate such model selection problems.

In this paper we put forth a novel optimization framework to learn a good radial kernel from training data. Our kernel learning approach is based on a distributionally robust optimization problem [12, 16] to learn a good distribution for the Schönberg integral representation of the radial basis functions from training samples [47, Thm. 1]. Since optimization with respect to the distribution of RBF kernels is intractable, we consider a Monte Carlo sample average approximation to obtain a solvable finite dimensional optimization problem with respect to the samples of the distribution. We then use a projected particle Langevin optimization method to solve the approximated finite dimensional optimization problem. We provide a theoretical guarantee for the consistency of the finite sample-average approximations. Based on a mean-field analysis, we also show the consistency of the proposed projected particle Langevin optimization method in the sense that when the number of particles tends to infinity, the empirical distribution of the Langevin particles follows the path of the gradient descent flow of the distributionally robust optimization problem on the Wasserstein manifold.

1.1. Related works

The proposed kernel learning approach in this paper is closely related to the previous work of the authors in [26]. Therein, we proposed a particle stochastic gradient descent method in conjunction with the random feature model of Rahimi and Recht [41, 42] to optimize the distribution of the random features in generative and discriminative machine learning models using training samples. We also showed numerically that compared to the importance sampling techniques for kernel learning (e.g., [48]), the particle SGD in conjunction with the kernel SVMs yields a lower training and test errors on benchmark data-sets. Nevertheless, we observed that the particle SGD scales rather poorly with data dimension and the number of random feature samples, rendering it inapplicable for discriminative analysis of high dimensional data-sets. In this work, we address the scalability issue by optimizating the kernel over the sub-class of the radial kernels which includes important special cases such as the Gaussian, inverse multiquadrics, and Matérn kernels. While we characterize a distributionally robust optimization framework similar to [26], in this work we optimize distributions defined on the real line instead of high dimensional distributions in [26].

This work is also closely related to the copious literature on the kernel model selection problem, see, e.g., [28, 9, 1, 19]. For classification problems using kernel SVMs, Cortes, et al. studied a kernel learning procedure from the class of mixture of base kernels. They have also studied the generalization bounds of the proposed methods. The same authors have also studied a two-stage kernel learning in [9] based on a notion of the kernel alignment. The first stage of this technique consists of learning a kernel that is a convex combination of a set of base kernels. The second stage consists of using the learned kernel with a standard kernel-based learning algorithm such as SVMs to select a prediction hypothesis. In [28], the authors have proposed a semi-definite programming for the kernel-target alignment problem. However, semi-definite programs based on the interior point method scale rather poorly to a large number of base kernels.

Our proposed kernel learning framework is related to the work Sinha and Duchi [48] for learning shift invariant kernels with random features. Therein, the authors have proposed a distributionally robust optimization for the importance sampling of random features using -divergences. In [26], we proposed a particle stochastic gradient descent to directly optimize the samples of the random features in the distributionally robust optimization framework, instead of optimizing the weight (importance) of the samples. However, for the high dimensional data-sets the particles are high dimensional, and the particle SGD scales poorly. In this paper, we address the scalibility issue by restricting the kernel class to the radial kernels.

The mean-field description of SGD dynamics has been studied in several prior works for different information processing tasks. Wang et al. [57] consider the problem of online learning for the principal component analysis (PCA), and analyze the scaling limits of different online learning algorithms based on the notion of finite exchangeability. In their seminal papers, Montanari and co-authors [33, 23, 32] consider the scaling limits of SGD for training a two-layer neural network, and characterize the related Mckean-Vlasov PDE for the limiting distribution of the empirical measure associated with the weights of the input layer. They also establish the uniqueness and existence of the solution for the PDE using the connection between Mckean-Vlasov type PDEs and the gradient flows on the Wasserstein manifolds established by Otto [36], and Jordan, Kinderlehrer, and Otto [24]. Similar mean-field type results for two-layer neural networks are also studied recently in [45, 50]

1.2. Paper Outline

The rest of this paper is organized as follows:

-

•

Empirical Risk Minimization in Reproducing Kernel Hilbert Spaces: In Section 2, we review some preliminaries regarding the empirical risk minimization in reproducing kernel Hilbert spaces. We also provide the notion of the kernel-target alignment for optimizing the kernel in support vector machines (SVMs). We then characterize a distributionally robust optimization problem for multiple kernel learning.

-

•

Theoretical Results: In Section 3, we provide the theoretical guarantees for the performance of our kernel learning algorithm. In particular, we establish the non-asymptotic consistency of the finite sample approximations. We also analyze the scaling limits of the kernel learning algorithm.

-

•

Empirical Evaluation on Synthetic and Benchmark Data-Sets: In Section 4, we evaluate the performance of our proposed kernel learning model on synthetic and benchmark data-sets. In particular, we analyze the performance of our kernel learning approach for the hypothesis testing problem. We also apply our proposed kernel learning approach to develop hash codes for image query task from large data-bases.

2. Preliminaries and the Optimization Problem for Kernel Learning

In this section, we review preliminaries of kernel methods in classification and regression problems.

2.1. Reproducing Kernel Hilbert Spaces and Kernel Alignment Optimization

Let be a metric space. A Mercer kernel on is a continuous and symmetric function such that for any finite set of points , the kernel matrix is positive semi-definite.

The reproducing kernel Hilbert space (RKHS) associated with the kernel is the completion of the linear span of the set of functions with the inner product structure defined by . That is

| (2.1) |

The reproducing property takes the following form

| (2.2) |

In the classical supervised learning models, we are given feature vectors and their corresponding uni-variate class labels , . For the binary classification and regression tasks, the target spaces is given by and , respectively. Given a loss function , a classifier is learned from the function class via the minimization of the regularized empirical risk

| (2.3) |

where is a function norm, and is the parameter of the regularization. Consider a Reproducing Kernel Hilbert Space (RKHS) with the kernel function , and suppose . Then, using the expansion , and optimization over the kernel class yields the following primal and dual optimization problems

| (2.4a) | |||

| (2.4b) | |||

respectively, where is the Fenchel’s conjugate, and is the kernel Gram matrix.

In the particular case of the soft margin SVMs classifier , the primal and dual optimizations take the following forms

| (2.5a) | |||

| (2.5b) | |||

where is the Hadamard (element-wise) product of vectors. The form of the dual optimization in Eq. (2.5) suggests that for a fixed dual vector , the optimal kernel can be computed by optimizing the following -statistics known as the kernel-target alignment, i.e.

| (2.6) |

In this paper, we focus on the class of radial kernels 111Compare the kernel class in Eq. (2.7) with that of we considered in [26], where is the set of all translation invariant kernels.

| (2.7) |

which includes the following important special cases:

-

•

Gaussian:, for ,

-

•

Inverse multiquadrics: for ,

-

•

Matèrn: , where is the modified Bessel function of the third kind, and is the Euler Gamma function.

The radial kernel is a positive semi-definite kernel (a.k.a. Mercer kernel) if the uni-variate function is positive semi-definite. A uni-variate function which is positive semi-definite or positive definite on every d admits an integral representation due to Schöenberg [47, Thm. 1]:

Theorem 2.1.

(I. J. Schöenberg [47, Thm. 1]) A continuous function is positive semi-definite if and only if it admits the following integral representation

| (2.8) |

for a finite positive Borel measure on +. Moreover, if then is positive definite, where denotes the support of the measure .

From the Schönberg’s representation theorem [47], the following integral representation for the radial kernels follows

| (2.9) |

where is the set of all finite non-negative Borel measures on +. Due to the integral representation of Equation (2.9), a kernel function is completely characterized in terms of the probability measure . Therefore, we can reformulate the kernel-target alignment as an optimization with respect to the distribution of the kernel

| (2.10) |

where is a distribution sub-set. In the sequel, we consider a distribution ball with the radius and the (user-defined) center , where is the support of the distributions. Moreover, given the metric space , for the measures , is the -Wasserstein metric defined below

| (2.11) |

where the infimum is taken with respect to all couplings of the measures , and is the set of all measures for which and are marginals, i.e.,

| (2.12) |

for all the maps and , and and are the push-forwards of .

Alternatively, we can recast the distributional optimization problem as a risk minimization aiming to match the output of the target kernel with the ideal kernel on the training data-set

| (2.13) |

As , the optimization problem in Eq. (2.14) tends to that of Eq. (2.10). The distributional optimization in Eq. (2.14) is infinite dimensional. To characterize a finite dimensional optimization problem, we instead optimize the samples (particles) of the target distribution. In particular, we consider the independent identically distributed samples , and let . Let . Then, we consider the following empirical risk function

| (2.14) |

where and , and

| (2.15) |

2.2. Surrogate Loss Function

Using for the constraint , a partial Lagrangian is

| (2.16) |

where is the Lagrange multiplier. The Wasserstein distance in Eq. (2.14), the minimization in Eq. (2.14) is computationally prohibitive. Therefore, we instead minimize a surrogate loss function. To obtain the surrogate loss function, we define the empirical measure of the samples (particles) at each iteration as follows

| (2.17) |

Then, the surrogate loss for the Wasserstein distance in Eq. (2.14) can be obtained as follows. We denote the joint distribution of the particle-pair by . Then, we obtain that

| (2.18) |

where the set of couplings are given by

| (2.19) |

is a linear program that is challenging to solve in practice for a large number of particles . To improve the computational efficiency, Cuturi [10] have proposed to add an entropic regularization to the Wasserstein distance. The resulting Sinkhorn divergence solves a regularized version of Equation (2.18):

| (2.20) |

where is the entropic barrier function enforcing the non-negativity constraint on the entries ’s, with the regularization parameter . Moreover, has a similar definition as in Eq. (2.19), except that , and thus .The Sikhorn divergence is now computed as follows

| (2.21) |

Notice that the entropic regularization term is absent from Eq. (2.21).222The divergence in Eq. (2.21) is sometimes referred to as the sharp Sinkhorn divergence to differentiate it from its regularized counterpart ; see, e.g., [29].

We thus consider the following surrogate loss function

| (2.22) |

The loss function acts as a proxy for the empirical loss that we wish to optimize.

After introducing the Lagrange multipliers and for the constraints on the marginals of , we obtain that

| (2.23) |

The optimal values of can be derived explicitly using the KKT condition

| (2.24) |

where , and . Alternatively, the transportation matrix is given by

| (2.25) |

where , , , and denotes the diagonal element of the matrix. The vectors and can be computed efficiently via the Sinkhorn-Knopp matrix scaling algorithm [49]

| (2.26) |

where is the following contraction mapping

| (2.27) |

where . Moreover,

| (2.28) |

To optimize Eq. (2.14), we consider the projected noisy stochastic gradient descent optimization method (a.k.a. Langevin dynamics). In particular, at each iteration , two samples and uniformly and randomly are drawn from the training data-set. Then, we analyze the following iterative optimization method

| (2.29) |

where Above, is the temperature parameter, is the step-size, and is the isotropic Gaussian noise. Note that when , the iterations in Eq. (2.29) correspond to the projected stochastic gradient descent method. Moreover, is the projection onto the sub-set . Furthermore, is the stochastic gradient that has the following elements

| (2.30) |

where

| (2.31a) | ||||

| (2.31b) | ||||

for all . To update the Lagrange multiplier , we note that Eq. (2.22) is concave in , and is a scaler. Therefore, a bisection method can be applied to optimize the Lagrange multiplier . In Algorithm 1, we summarize the main steps of the proposed kernel learning approach. To analyze the complexity of Algorithm 1, we note that the Sinkhorn’s divergence can be computed in time [10]. Since the Euclidean projection in Eq. (2.29) is onto the hyper-cube , it can be computed efficiently in time by computing and for each particle . Overall, the -optimal solution to problem (2.22) can be reached in .

| (2.32) |

| (2.33) |

3. Main Results

In this section, we state our main theoretical results regarding the performance of the proposed kernel learning procedure. The proof of theoretical results is presented in Appendix.

3.1. Assumptions

To state our theoretical results, we first state the technical assumptions underlying our theoretical results:

-

(A.1)

The feature space has a finite diameter, i.e.,

-

(A.2)

The slater condition holds for the empirical loss functions. In particular, we suppose there exists and such that , and .333The relative interior of a convex set , abbreviated , is defined as , where denotes the affine hull of the set , and is a ball of the radius centered on .

-

(A.3)

The Langevin particles are confined to a compact sub-set of +, i.e., , for some .

-

(A.4)

The Langevin particles are initialized by sampling from a distribution whose Lebesgue density exists. Let denotes the associated Lebesgue density.

We remark that while (A.3) is essential to establish theoretical performance guarantees for Algorithm 1 in this paper, in practice, the same algorithm can be employed to optimize distributions with unbounded support.

3.2. Non-asymptotic consistency

In this part, we prove that the value of the population optimum evaluated at the solution of the finite sample optimization problem in Eq. (2.14) approaches its population value as the number of training data , the number of Langevin particles , the regularization parameter , and the inverse of the parameter of the Sinkhorn transport tend to infinity.

Theorem 3.1.

(Non-asymptotic Consistency of Finite-Sample Estimator) Further, consider the distribution balls and of the radius that are defined with respect to the -Wasserstein and Sinkhorn’s divegences, respectively. Define the optimal values of the population optimization and its finite sample estimate

respectively. Then, with the probability of (at least) over the training data samples and the Langevin particles , the following non-asymptotic bound holds

where , and , and is a constant independent of .

3.3. Scaling limits for the unconstrained optimization

In this part, we provide a mean-field analysis of the projected particle optimization in Eq. (2.29) for the special case of the unconstrained optimization. In particular, throughout this part, we assume in the distributional ball (thus ). We then analyze the following Langevin optimization method for unconstrained distributional optimization:

| (3.1) |

where . The first result of this paper is concerned with the scaling limits of the Langevin optimization method in Eq. (3.1) in the mean-field regime:

Theorem 3.2.

(Mean-Field Partial Differential Equation) Suppose Assumptions - are satisfied. Let denotes the continuous-time embedding of the empirical measure associated with the projected Langevin particles in Eq. (3.1), i.e.,

| (3.2) |

associated with the projected particle Langevin optimization in Eq. (3.1).444For a real , stands for the largest integer not exceeding . Suppose the step size satisfies , , and as . Furthermore, suppose the Lebesgue density exists. Then, for any fixed , as , where the Lebesgue density of the limiting measure is a solution to the following distributional dynamics with Robin boundary conditions as well as an initial datum555The notion of weak convergence of probability measures is formally defined in Appendix A.

| (3.3a) | ||||

| (3.3b) | ||||

| (3.3c) | ||||

| (3.3d) | ||||

| (3.3e) | ||||

where the functional is defined

Above, the expectations are taken with respect to the tensor product of the joint distribution of the features and class labels, and its marginal , respectively.

Let us make several remarks regarding the distributional dynamics in Theorem 3.2.

First, we notice that despite some resemblance between Eq. (3.3) and the Fokker-Plank (a.k.a. forward Kolmogorov) equations for the diffusion-drift processes, they differ in that the drift of Eq. (3.3) is a functional of the Lebesgue density of the law of the underlying process. In the context of kinetic gas theory of statistical physics, such distributional dynamics are known as the Mckean-Vlasov partial differential equations; see, e.g., [6].

Second, the proof of Theorem 3.2 is based on the notion of propogation of chaos or asymptotic freedom [54, 26], meaning that the dynamics of particles are decoupled in the asymptotic of infinitely many particles . To formalize this notion, we require the following definitions:

Definition 3.3.

(Exchangablity) Let be a probability measure on a Polish space and. For , we say that is an exchangeable probability measure on the product space if it is invariant under the permutation of indices. In particular,

| (3.4) |

for all Borel subsets .

An interpretation of the exchangablity condition (3.4) can be provided via De Finetti’s representation theorem which states that the joint distribution of an infinitely exchangeable sequence of random variables is as if a random parameter were drawn from some distribution and then the random variables in question were independent and identically distributed, conditioned on that parameter.

Next, we review the mathematical definition of chaoticity, as well as the propagation of chaos in the product measure spaces:

Definition 3.4.

(Chaoticity) Suppose is exchangeable. Then, the sequence is -chaotic if, for any natural number and any test function , we have

| (3.5) |

According to Eq. (3.5) of Definition 3.4, a sequence of probability measures on the product spaces is -chaotic if, for fixed the joint probability measures for the first coordinates tend to the product measure on . If the measures are thought of as giving the joint distribution of particles residing in the space , then is -chaotic if particles out of become more and more independent as tends to infinity, and each particle’s distribution tends to . A sequence of symmetric probability measures on is chaotic if it is -chaotic for some probability measure on .

If a Markov process on begins in a random state with the distribution , the distribution of the state after seconds of Markovian random motion can be expressed in terms of the transition function for the Markov process. The distribution at time is the probability measure is defined by the kernel

| (3.6) |

Definition 3.5.

(Propogation of Chaos) A sequence functions

| (3.7) |

whose -th term is a Markov transition function on that satisfies the permutation condition

| (3.8) |

propagates chaos if whenever is chaotic, so is for any , where is defined in Eq. (3.6).

In the context of this paper, the propagation of chaos simply means that the time-scaled empirical measures (say, on the path space) converge weakly in probability to the deterministic measure , or equivalently that the law of converges weakly to the product measure for any fixed , where is the law of the following reflected diffusion-drift Itô process

| (3.9) |

In Eqs. (3.9), and are the non-negative reflection processes from the boundaries and , respectively. In particular, and are non-decreasing, cádlág, with the initial values , and

| (3.10) |

where the integrals are in the Stieltjes sense. In fact, we show that the law of the Langevin particles converges in the -Wasserstein distance to . Alternatively, due to the bounded equivalence of the Wasserstein distance and the total variation distance on compact metric spaces (cf. (A.3)), the sense in which converges in probability to can be strengthened; rather than working with the usual weak-∗ topology induced by duality with bounded continuous test functions (see, e.g., [26]), we work with the stronger topology induced by duality with bounded measurable test functions.

Third, the Robin boundary conditions in Eq. (3.3b) captures the effect of an elastic reflection of the particles in the projected particle Langevin optimization method. Alternatively, the Robin boundary conditions asserts that the flux of particles in and out of the boundaries is zero. In particular, the particles are constrained to stay in by barriers at and , in such a way that when the particle hits the barrier with incoming velocity , it will instantly bounce back with velocity , where is a parameter called the velocity restitution coefficient. When we say that the reflection is perfectly elastic; when it is said to be a rigid reflection resulting in the Neumann boundary conditions instead of the Robin boundary conditions. By definition of the Euclidean projection in the projected Langevin particle of Eq. (3.1), the particles are bounced off of the boundary of the projection space with the elastic parameter .

Fourth, we note that the solution of the distributional dynamics in Eq. (3.3) is absolutely continuous with respect to , and lacks atoms at the boundaries and . This is due to the fact that the boundaries are non-absorbing.

In the next proposition, we establish the existence and uniqueness of the steady-state solutions of the mean-field PDE (3.3):

Proposition 3.1.

(Existence and Uniqueness of the Steady-State Solution) Suppose Assumptions - are satisfied. Then, the following assertions hold:

4. Performance Evaluation on Synthetic and Benchmark Data-Sets

For simulations of this section, we consider kernel SVMs in conjunction with the random feature model of Rahimi and Recht [41, 42]. Specifically, we consider the following model random feature model:

| (4.1) |

where is the random feature. For translation invariant kernels, we have , where is a random bias term. Given the i.i.d. samples , then we minimize the following risk function

| (4.2) |

To compute the random features associated with the radial kernels, we note that the probability measure of the random feature has the following Lebesgue’s density

More specifically, due to the fact that

| (4.3) |

the Tonelli-Fubini theorem is admissible. Therefore, we may change the order of integral to derive

where we recognize the last term as the integral representation of the radial kernel in Eq. (2.9). Let denotes the vector outputs of Algorithm 1. We draw the random features,

| (4.4) |

where .

We compare our method with three alternative kernel learning techniques, namely, the importance sampling of Sinha and Duchi [48], the Gaussian bandwidth optimization via nearest neighbor (-NN) [7], and our proposed particle SGD in [26]. In the sequel, we provide a brief description of each method:

-

•

Importance Sampling: the importance sampling of Sinha and Duchi [48] which proposes to assign a weight to each sample for . The weights are then optimized via the following standard optimization procedure

(4.5) where is the distributional ball, and is the divergence. Notice that the complexity of solving the optimization problem in Eq. (4.5) is insensitive to the dimension of random features .

-

•

Gaussian Kernel with -NN Bandwidth Selection Rule: In this method, we fix the Gaussian kernel . To select a good bandwidth for the kernel, we use the deterministic nearest neighbor (NN) approach of [7]. In particular, we choose the bandwidth according to the following rule

(4.6) where is defined as nearest neighbor of . In our experiments, we let . We then generate random Fourier features , with and .

-

•

Particle Stochastic Gradient Descend Method: This is the method that we proposed in the earlier work [26], where we optimized the samples in the random feature model of Eq. (4.1). In particular,

(4.7) for . Notice that in the random feature model of [41, 42], the explicit feature map is given by , where the dimension of the particles in Eq. (4.7) is the same as the dimension of the feature vectors . As a result, for high dimensional data-sets , the computational complexity per iterations of Eq. (4.7) is potentially prohibitive.

4.1. Empirical Results on the Synthetic Data-Set

For experiments with the synthetic data, we use the setup of [26]. The synthetic data-set we consider is as follows:

-

•

The distribution of training data is ,

-

•

The distribution of generated data is .

To reduce the dimensionality of data, we consider the embedding , where and . In this case, the distribution of the embedded features are , and .

Note that is a parameter that determines the separation of distributions. In particular, the Kullback-Leibler divergece of the two multi-variate Gaussian distributions is controlled by ,

| (4.8) |

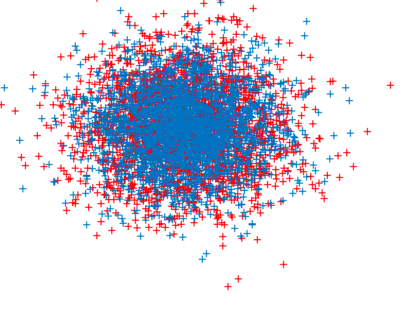

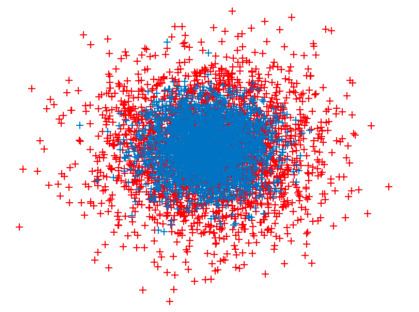

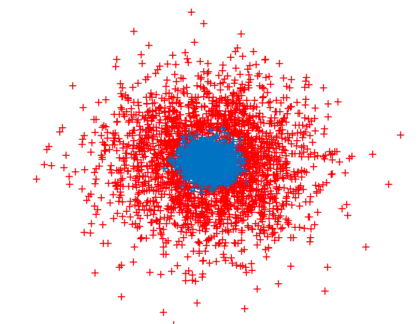

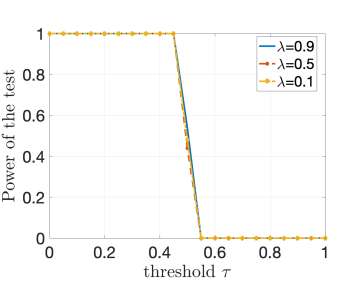

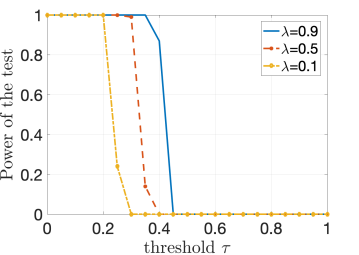

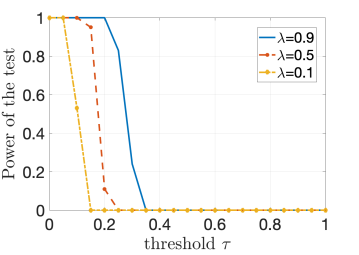

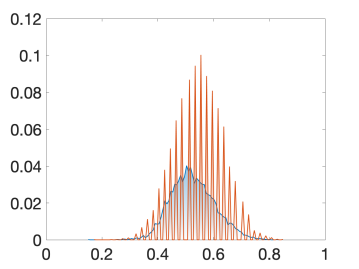

In Figure 1, we show the i.i.d. samples from the distributions and for different choices of variance parameter of , , and . Notice that for larger the divergence is reduced and thus performing the two-sample test is more difficult. From Figure 1, we clearly observe that for large values of , the data-points from the two distributions and have a large overlap and conducting a statistical test to distinguish between these two distributions is more challenging.

4.1.1. Kernel Learning Approach

Figure 4 depicts our two-phase kernel learning procedure. The kernel learning approach consists of training the auto-encoder for the dimensionality reduction and the kernel optimization sequentially, i.e.,

| (4.9) |

where the function class is defined , and . Here, is the sigmoid non-linearity. Now, we consider a two-phase optimization procedure:

-

•

Phase (I): we fix the kernel function, and optimize the auto-encoder to compute a co-variance matrix and the bias term for the dimensionality reduction.

-

•

Phase (II): we optimize the kernel based from the learned embedded features .

This two-phase procedure significantly improves the computational complexity of SGD as it reduces the dimensionality of random feature samples , .

(a) (b) (c)

4.1.2. Statistical Hypothesis Testing with the Kernel MMD

Let , and . Given these i.i.d. samples, the statistical test is used to distinguish between these hypotheses:

-

•

Null hypothesis (thus ),

-

•

Alternative hypothesis (thus ).

To perform hypothesis testing via the kernel MMD, we require that is a universal RKHS, defined on a compact metric space . Universality requires that the kernel be continuous and, be dense in . Under these conditions, the following theorem establishes that the kernel MMD is indeed a metric:

Theorem 4.1.

(Metrizablity of the RKHS) Let denotes a unit ball in a universal RKHS defined on a compact metric space with the associated continuous kernel . Then, the kernel MMD is a metric in the sense that if and only if .

A radial kernel is universal if the support of the measure in the integral representation in Eq. (2.9) excludes the origin, i.e., , see [53].

To design a test, let denotes the solution of SGD in (4.7) for solving the optimization problem. Consider the following MMD estimator consisting of two -statistics and an empirical function

| (4.10) |

Given the samples and , we design a test statistic as below

| (4.11) |

where is a threshold. Notice that the unbiased MMD estimator of (4.10) can be negative despite the fact that the population MMD is non-negative. Consequently, negative values for the statistical threshold (4.11) are admissible. Nevertheless, int our simulations, we only consider non-negative values for the threshold .

A Type I error is made when is rejected based on the observed samples, despite the null hypothesis having generated the data. Conversely, a Type II error occurs when is accepted despite the alternative hypothesis being true. The significance level of a test is an upper bound on the probability of a Type I error: this is a design parameter of the test which must be set in advance, and is used to determine the threshold to which we compare the test statistic. The power of a test is the probability of rejecting the null hypothesis when it is indeed incorrect. In particular,

| (4.12) |

In this sense, the statistical power controls the probability of making Type II errors.

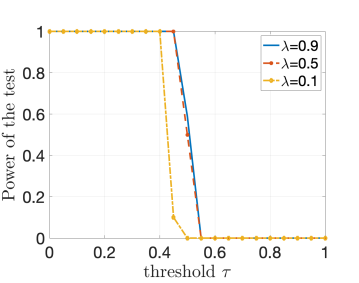

4.2. Empirical results on benchmark data-sets

In Figure 4, we evaluate the power of the test for trials of hypothesis test using the test statistics of (4.11). To obtain the result, we used an autoencoder to reduce the dimension from to . Clearly, for the trained kernel in Panel (a) of Figure 4, the threshold for which increases after learning the kernel via the two phase procedure described earlier. In comparison, in Panel (b), we observe that training an auto-encoder only with a fixed standard Gaussian kernel attains lower thresholds compared to our two-phase procedure. In Panel (c), we demonstrate the case of a fixed Gaussian kernel without an auto-encoder. In this case, the threshold is significantly lower due to the large dimensionality of the data. We also observer that the particle SGD for optimization we proposed in [26] to optimize the translation invariant kernels provides the highest statistical power for a given threshold value. Nevertheless, as we observe in Figure 4, the run-time of the particle SGD for a given number of particles is significantly higher than Algorithm 1. This is due to the fact that the dimension of the particles in the particle SGD is dependent on the number of hidden layers of auto-encoder. In contrast, the particles in Algorithm 1 are one dimensional.

(a) (b) (c) (d)

(a) (b) (c) (d)

(e) (f) (g) (h)

5. Application to Locally Sensitive Hashing

(a) (b) (c)

(d) (e) (f)

(a) (b) (c)

(a) (b) (c)

(a) (b) (c)

(d) (e) (f)

(g) (h) (i)

(j) (k) (l)

The research on computer systems and web search in the mid-nineties was focused on designing “hash” functions that were sensitive to the topology on the input domain, and preserved distances approximately during hashing. Constructions of such hash functions led to efficient methods to detect similarity of files in distributed file systems and proximity of documents on the web. We describe the problem and results below. Recall that a metric space is given by a set (here the set of cells) and a distance measure which satisfies the axioms of being a metric.

Definition 5.1.

(Locally Sensitive Hash Function) Given a metric space and the set , a family of function is said to be a basic locality sensitive hash (LSH) family if there exists an increasing invertible function such that for all , we have

| (5.1) |

To contrast the locally sensitive hash functions with the standard hash function families note that in the latter, the goal is to map a domain to a range such that the probability of a collision among any pair of elements is small. In contrast, with LSH families, we wish for the probability of a collision to be small only when the pairwise distance is large, and we do want a high probability of collision when is small. Indyk and Motwani [22] showed that such a hashing scheme facilitates the construction of efficient data structures for answering approximate nearest-neighbor queries on the collection of objects.

In the sequel, we describe a family of locally sensitive hash functions due to Raginsky, et al. [40], where the measure is determined by a kernel function. We draw a random threshold and define the quantizer . The following theorem is due to Raginsky, et al. [40]:

Lemma 5.2.

(Kernel Hash Function, Raginsky, et al. [40]) Consider a translation invariant kernel . Define the following hamming -code

| (5.2) |

where , , and , where is the distribution in the Rahimi and Recht random feature model

| (5.3) |

Furthermore, is a mapping defined as follows

| (5.4) |

Fix . For any finite data set , is such that

| (5.5) |

where is the Hamming distance. Furthermore,

| (5.6) |

The construction of LSH in Eq. (5.4) of Lemma (5.2) is based on the random feature model of Rahimi and Recht [41, 42], and is restricted to the Hamming codes defined on a hyper-cube. In the sequel, we present an alternative kernel LSH using the embedding of functions in space into -spaces, generalizing the result of Lemma 5.2 to any finite integer alphabet . To describe the result, we define the Lee distance between two code-words of length as follows

| (5.7a) | ||||

| (5.7b) | ||||

In the special cases of and , the Lee distance corresponds to the Hamming distance as distances are for two single equal symbols and 1 for two single non-equal symbols. For this is not the case anymore, and the Lee distance can become larger than one.

Lemma 5.3.

(Generalized Kernel LSH) Consider a translation invariant kernel . Define a random map through the following function

| (5.8) |

where , . Moreover, , where , and . Then, the probability of collision is bounded as follows

where is defined

| (5.9) |

The proof of Lemma 5.3 is presented in Appendix A.12, and uses the property of the stable distributions.

5.1. Description of the experiment

We present image retrieval results for 10000 images from MNIST databases [10]. The images are 28 by 28 pixels and are compressed via an auto-encoder with 500 hidden layers, which have proven to be effective at learning useful features. For this experiment, we randomly select 1,000 images to serve as queries, and the remaining 9,000 images make up the “database”. To distinguish true positives from false positives for the performance evaluation retrieval performance, we select a “nominal” neighborhood.

5.2. Results

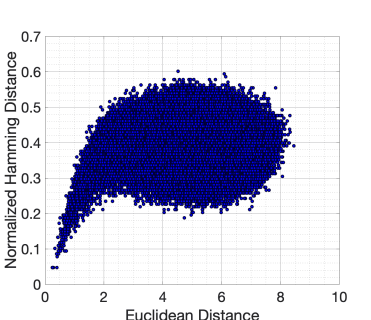

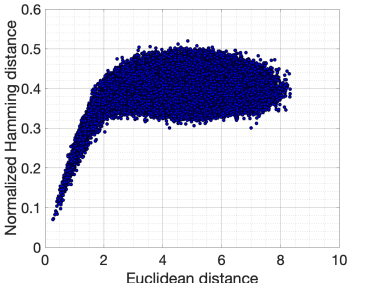

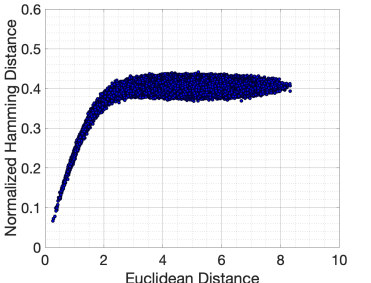

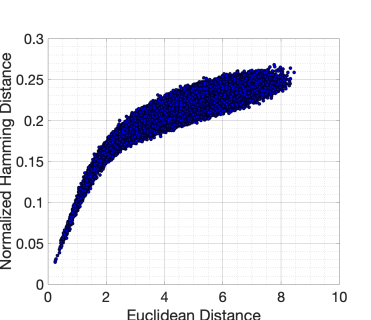

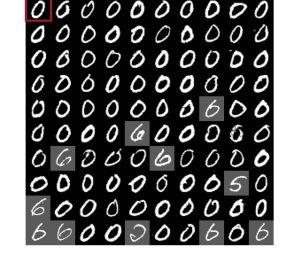

In Figure 4, we illustrate the scatter plots of the hash codes of length bits. In Figure 4 (a)-(c), we show the scatter plots for Hamming codes constructed by Lemma 5.2 using an untrained Gaussian kernel . From Figure 4 (a)-(c) we observe that as the number of bits of the Hamming code increase, the scatter plots concentrate around a curve that has a flat region. Evidently, this curve deviates from the ideal curve which is a straight line passing through the origin. In particular, in 4 (a)-(c), as the Euclidean distance changes on the interval of -axis, the normalized Hamming distance of the constructed codes remains constant.

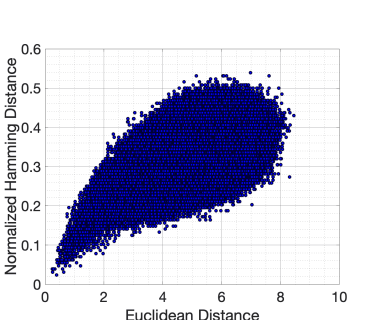

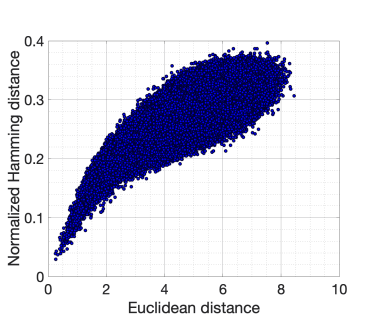

To attain proportionality between the Hamming distance and the Euclidean distance, we train the kernel using Algorithm 1. To generate the labels for kernel training, we first perform a -NN on 1000 images from 9,000 images of the data-base, where here . Then, we generate the binary class labels by assigning to the points in a randomly chosen cluster, and to the remaining data-points in other clusters (i.e., the one-versus-all rule). After training the kernel, the kernel is used to generate the Hash codes using the construction of Lemma 5.2. The resulting scattering plots are depicted in Figure 4 (d)-(f), and the Hamming distances are more proportional to the Euclidean distance.

Central to our study is the precision-recall curve, which captures the trade-off between precision and recall for different threshold. A high area under the curve represents both high recall and high precision, where high precision relates to a low false positive rate, and high recall relates to a low false negative rate. High scores for both show that the classifier is returning accurate results (high precision), as well as returning a majority of all positive results (high recall). Specifically,

| (5.10a) | |||

| (5.10b) | |||

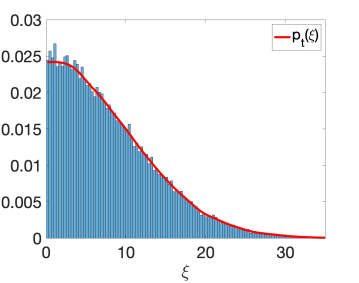

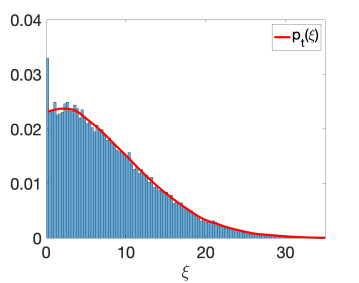

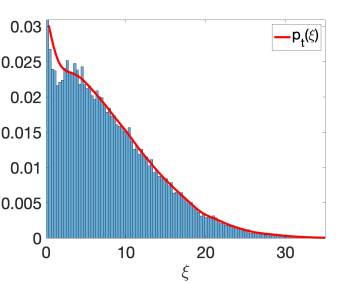

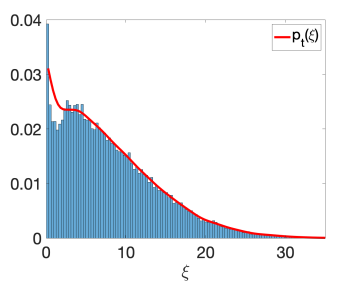

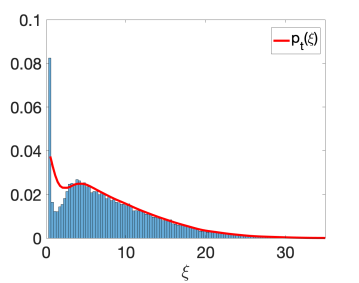

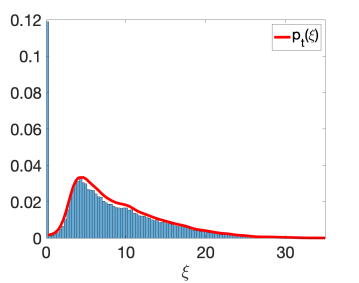

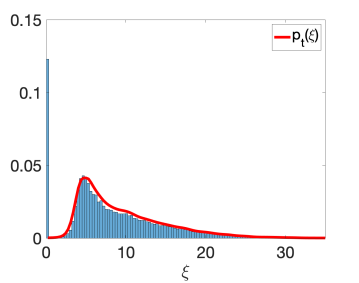

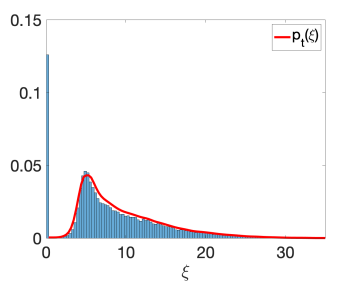

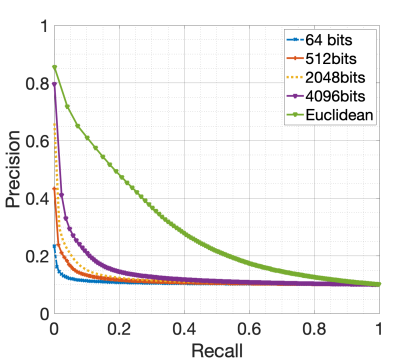

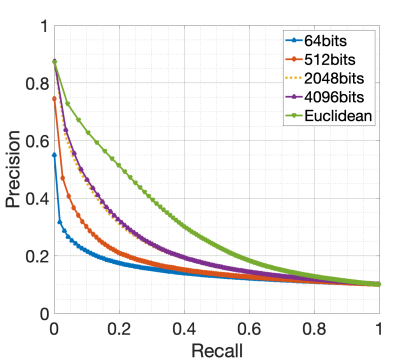

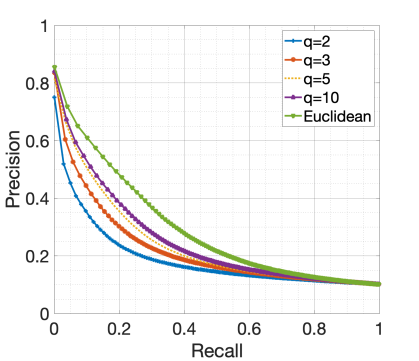

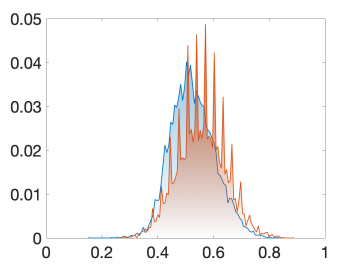

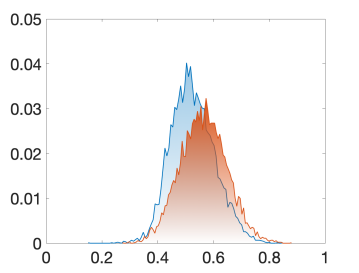

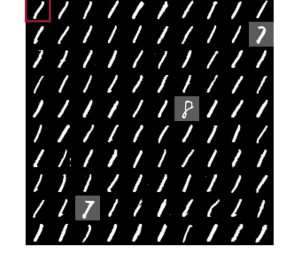

In Figure 5 we illustrate the precision-recall curves for Hamming codes of different lengths . We also depict the precision-recall curve for the Euclidean distance. We recall the notions of the recall and precision as follows From Figure 5(a), we depict the precision-recall curves for Hamming codes constructed from the Gaussian kernel. We observe that even Hamming codes of length bits attain the precision-recall curve that is significantly lower than the Euclidean curve. In Figure 5(b), we illustrate the precision-recall curves after training kernels using Algorithm 1. The curves from Hamming codes are markedly closer to the curve associated with the Euclidean distance. In Figure 5(c), we depict the precision-recall curves using the -ary codes in Lemma 5.3 for different quantization levels . Clearly, increasing leads to a better performance initially while larger values of has a diminishing return. This can be justified using Figure 6, where we plot the normalized histogram of the distance of a sample query point from each point of the MNIST data-base consisting of 9,000 of data-points. The blue color histogram depict the histogram using a Euclidean distance, and the orange color histogram with spikes depicts the histogram of the Lee distance. Figure 6(a)-(c) are plotted with the quantization levels , , and , respectively. As the quantization level increases, the histogram of the Lee distance provides a better approximation for the Euclidean distance histogram. However, even for large , there is a disparity between the two histograms, as the length of the -ary codes are fixed at and is finite.

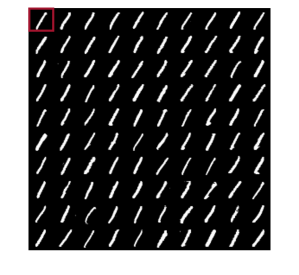

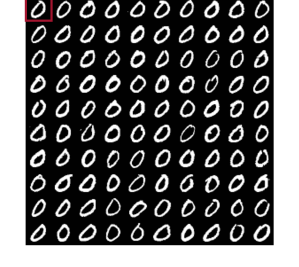

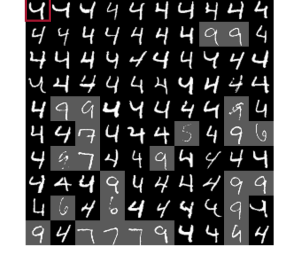

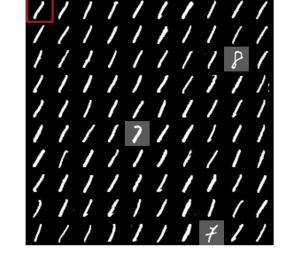

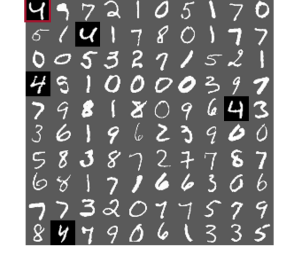

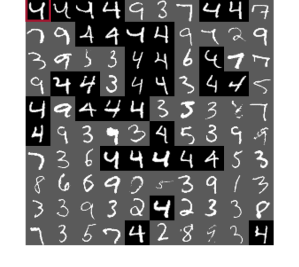

In Figure 7, we depict the retrieval results for three query digits on MNIST data-set. In Fig. 7(a)-(c), we show the performance of retrieval system using a Euclidean distance for searching nearest neighbor. In particular, for each query digit, the retrieval system returns 99 similar images among 9,000 images in the data-base using nearest neighborhood search. The retrieved images for less challenging digits such as 1 and 0 are all correct, while for more challenging query points such as 4, some erroneous images are retrieved. In Fig. 7(d)-(f), we depict the retrieved images using a Hamming distance for the nearest neighborhood search, where the Hamming codes for each feature vector are generated via the kernel LSH in Lemma 5.2, where a Gaussian kernel is employed. We observe that compared to the Euclidean distance in Fig. 7(a)-(c), the performance of Hamming based nearest neighbor search is significantly less accurate. However, we point out that from a computation complexity perspective, computing the Hamming distance is significantly more efficient than the Euclidean distance which is the main motivation in using LSH for nearest neighborhood search.

In Fig. 7 (g)-(i), we show the retrieval results after training the kernel using Algorithm 1. Clearly, the retrievals are more accurate on the digits and . However, the length of the Hamming code required to achieve such performance is quite large . In Fig. 7 (j)-(l), we show the retrieval performance using the -ary code of length and the quanitization level of . Although the length of the -ary code is significantly smaller than that of the Hamming code, the retrieval error is slightly less. However, the computational cost is slightly higher than that of the Hamming code.

In the future, we will test our method on data-sets consisting of millions of data points. At present, our promising initial results on MNIST data-set, combined with our comprehensive theoretical analysis, convincingly demonstrate the potential usefulness of our kernel learning scheme for large-scale indexing and search applications.

6. Classification on Benchmark Data-Sets

We now apply our kernel learning method for classification and regression tasks on real-world data-sets.

6.1. Data-Sets Description

We apply our kernel learning approach to classification and regression tasks of real-world data-sets. In Table 1, we provide the characteristics of each data-set. All of these datasets are publicly available at UCI repository.666https://archive.ics.uci.edu/ml/index.php

6.1.1. Online news popularity

This data-set summarizes a heterogeneous set of features about articles published by Mashable in a period of two years. The goal is to predict the number of shares in social networks (popularity).

6.1.2. Buzz in social media dataset

This data-set contains examples of buzz events from two different social networks: Twitter, and Tom’s Hardware, a forum network focusing on new technology with more conservative dynamics

6.1.3. Adult

Adult data-set contains the census information of individuals including education, gender, and capital gain. The assigned classification task is to predict whether a person earns over 50K annually. The train and test sets are two separated files consisting of roughly 32000 and 16000 samples respectively.

6.1.4. Epileptic Seizure Detection

The epileptic seizure detection data-set consists of a recording of brain activity for 23.6 seconds. The corresponding time-series is sampled into 4097 data points. Each data point is the value of the EEG recording at a different point in time. So we have total 500 individuals with each has 4097 data points for 23.5 seconds. The 4097 data points are then divided and shuffled every into 23 segments, each segment contains 178 data points for 1 second, and each data point is the value of the EEG recording at a different point in time.

6.2. Quantitative Comparison

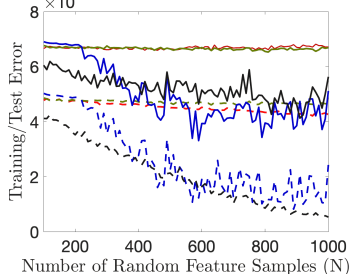

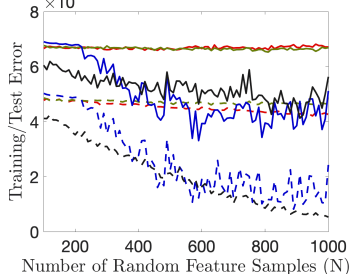

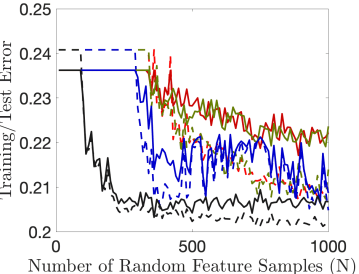

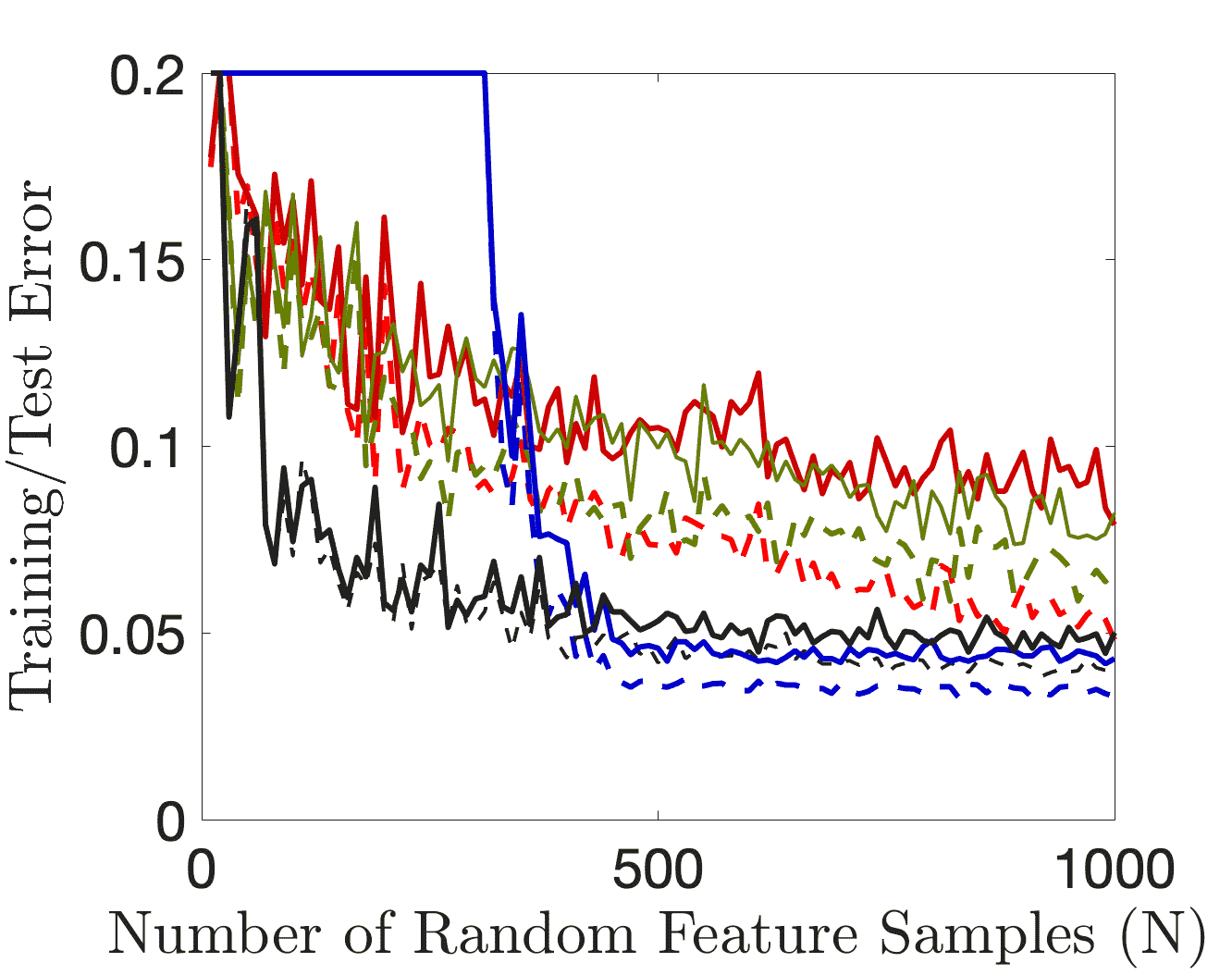

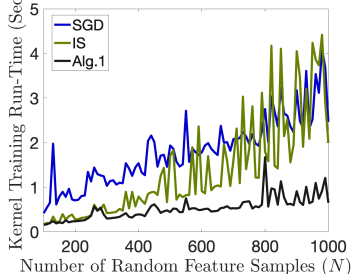

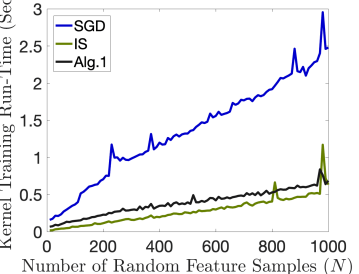

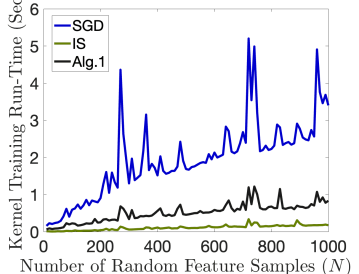

In Figure 9, we present the training and test results for regression and classification tasks on benchmark data-sets, using top features from each data-set and for different number of random feature samples . In all the experiments, the SGD method provides a better accuracy in both the training and test phases. Nevertheless, in the case of seizure detection, we observe that for a small number of random feature samples, the importance sampling and Gaussian kernel with NN for bandwidth outperforms SGD.

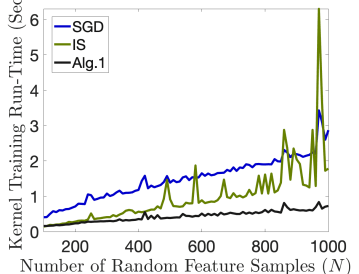

In Figure 9, we illustrate the time consumed for training the kernel using SGD and importance sampling methods versus the number of random features . For the linear regression on Buzz, and Online news popularity the difference between the run-times are negligible. However, for classification tasks using Adult and Seizure, the difference in run-times are more pronounced.

Those visual observations are also repeated in a tabular form in Table 2, where the training and test errors as well algorithmic efficiencies (run-times) are presented for , , , and number of features.

7. Conclusions

We have proposed and analyzed a distributionally robust optimization method to learn the distribution in the Schönberg integral representation of radial basis functions. In particular, we analyzed a projected particle Langevin dynamics to optimize the samples of the distribution in the integral representation of the radial kernels. We established theoretical performance guarantees for the proposed distributional optimization procedure. Specifically, we derived a non-asymptotic bound for the consistency of the finite sample approximations. Furthermore, using a mean-field analysis, we derived the scaling limits of a particle stochastic optimization method. We showed that in the scaling limits, the projected particle Langevin optimization converges to a reflected diffusion-drift process. We then derived a partial differential equation, describing the evolution of the law of the underlying reflected process. We evaluated the performance of the proposed kernel learning approach for classification on benchmark data-sets. We also used the kernel learning approach in conjunction with a -mean clustering method to train the kernel in the kernel locally sensitive hash functions.

| Data-set | Task | |||

|---|---|---|---|---|

| Buzz | Regression | 77 | 93800 | 46200 |

| Online news popularity | Regression | 58 | 26561 | 13083 |

| Adult | Classification | 122 | 32561 | 16281 |

| Seizure | Classification | 178 | 8625 | 2875 |

(a) (b) (c) (d)

(a) (b) (c) (d)

| Buzz | ||||

|---|---|---|---|---|

| Algorithm 1 | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.448e | 0.228e | 0.781e | 0.288e |

| Test Error | 0.635e | 0.554e | 0.512e | 0.397e |

| Run Time (sec) | 0.160 | 0.748 | 1.454 | 1.867 |

| Particle SGD | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.501e | 0.190e | 0.180e | 0.151e |

| Test Error | 0.501e | 0.190e | 0.180e | 0.151e |

| Run Time (sec) | 0.316 | 1.971 | 4.617 | 14.621 |

| Importance Sampling | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.486e | 0.466e | 0.460e | 0.455e |

| Test Error | 0.677e | 0.661e | 0.662e | 0.661e |

| Run Time (sec) | 0.188 | 1.527 | 3.592 | 4.955 |

| Gaussian Kernel | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.484e | 0.429e | 0.379e | 0.327e |

| Test Error | 0.673e | 0.673 | 0.709e | 0.744e |

| Online news popularity | ||||

| Algorithm 1 | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.463e | 0.239e | 0.676e | 0.288e |

| Test Error | 0.654e | 0.537e | 0.474e | 3.974e |

| Run Time (sec) | 0.165 | 0.686 | 1.264 | 1.736 |

| Particle SGD | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.501e | 0.190e | 0.180e | 0.151e |

| Test Error | 0.687e | 0.524e | 0.567e | 0.588e |

| Run Time (sec) | 0.309 | 2.071 | 3.152 | 5.054 |

| Importance Sampling | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.486e | 0.466e | 0.460e | 0.455e |

| Test Error | 0.677e | 0.662e | 0.662e | 0.661e |

| Run Time (sec) | 0.222 | 1.640 | 4.254 | 10.782 |

| Gaussian Kernel | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.484e | 0.429e | 0.379e | 0.327e |

| Test Error | 0.673e | 0.673e | 0.709e | 0.744e |

| Adult | ||||

| Algorithm 1 | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.221 | 0.201 | 0.199 | 0.199 |

| Test Error | 0.219 | 0.207 | 0.205 | 0.205 |

| Run Time (sec) | 0.155 | 0.645 | 1.426 | 1.802 |

| Particle SGD | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.240 | 0.204 | 0.199 | 0.197 |

| Test Error | 0.236 | 0.209 | 0.208 | 0.210 |

| Run Time (sec) | 0.274 | 1.784 | 9.272 | 11.295 |

| Importance Sampling | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.240 | 0.207 | 0.214 | 0.220 |

| Test Error | 0.236 | 0.219 | 0.222 | 0.223 |

| Run Time (sec) | 0.058 | 0.511 | 2.661 | 8.068 |

| Gaussian Kernel | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.240 | 0.206 | 0.201 | 0.197 |

| Test Error | 0.236 | 0.222 | 0.216 | 0.214 |

| Seizure | ||||

| Algorithm 1 | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.0814 | 0.0408 | 0.0364 | 0.0343 |

| Test Error | 0.0873 | 0.0480 | 0.0449 | 0.0470 |

| Run Time (sec) | 0.134 | 0.701 | 1.229 | 1.882 |

| Particle SGD | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.200 | 0.034 | 0.031 | 0.032 |

| Test Error | 0.200 | 0.043 | 0.043 | 0.043 |

| Run Time (sec) | 0.350 | 1.747 | 3.833 | 5.222 |

| Importance Sampling | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.135 | 0.078 | 0.055 | 0.051 |

| Test Error | 0.144 | 0.099 | 0.063 | 0.056 |

| Run Time (sec) | 0.038 | 0.138 | 0.352 | 0.404 |

| Gaussian Kernel | =100 | =1000 | =2000 | =3000 |

| Training Error | 0.146 | 0.056 | 0.033 | 0.030 |

| Test Error | 0.154 | 0.093 | 0.076 | 0.069 |

Appendix A Proof of Main Results

Notations. We define the following notion of distances between two measures on the metric space :

-

•

-divergence:

(A.1) In the case of , the corresponding distance is the Kullback-Leibler divergence which we denote by .

-

•

Wasserstein distance:

(A.2) where is the set of all measure and . For , the Kantorovich-Rubinstein duality yields

(A.3) where , where is the class of continuous functions.

-

•

Bounded Lipschitz metric:

(A.4) where .

We denote vectors by lower case bold letters, e.g. , and matrices by the upper case bold letters, e.g., . For a real , stands for the largest integer not exceeding . Let denote the Euclidean ball of radius centered at . For a sub-set of the Euclidean distance, we define its closure , and its boundary . Given a random variable , we denote its law with . We use for to denote the Sobolev space of functions whose weak derivatives up to order are in . The Sobolev space is denoted by , and is the space of functions in that vanishes at the boundary. The dual space of is denoted by .

To establish the concentration results in this paper, we require the following two definitions:

Definition A.1.

(Sub-Gaussian Norm) The sub-Gaussian norm of a random variable , denoted by , is defined as

| (A.5) |

For a random vector , its sub-Gaussian norm is defined as follows

| (A.6) |

Definition A.2.

(Sub-exponential Norm) The sub-exponential norm of a random variable , denoted by , is defined as follows

| (A.7) |

For a random vector , its sub-exponential norm is defined below

| (A.8) |

A.1. Proof of Theorem 3.1

We begin the proof by recalling the following definitions from the main text:

| (A.9a) | ||||

| (A.9b) | ||||

Furthermore, we recall the definition of the regularized risk function:

| (A.10a) | ||||

| (A.10b) | ||||

In Eqs. (A.9) and (A.10), the kernel has the following integral form

| (A.11) |

Lemmas A.3 and A.4 provide consistency guarantees with respect to the training data and the particles .

Lemma A.3.

(Consistency with Respect to the Training Data) Suppose holds. Consider the distribution ball , where is an arbitrary distribution. Then,

| (A.12) |

with the probability of at least over the draw of the training data , where and .

The proof of Lemma A.3 is provided in Section A.4. Lemma A.3 asserts that when the number of training data tends to infinity, the error due to the finite sample approximation becomes negligible. In the next lemma, we provide a similar consistency type result for the sample average approximation with respect to the Langevin particles:

Lemma A.4.

(Consistency with Respect to the Langevin Particles) Suppose holds. Consider the distributional ball in Lemma A.3 and consider its empirical approximation . Then,

| (A.13) |

with the probability of at least over the draw of the initial particles .

In the next lemma, we quantify the amount of error due to including the regularization to the risk function:

Lemma A.5.

(Regularization Error) Suppose holds. Consider the empirical distribution ball of Lemma A.4, and define

| (A.14) |

Then, for any , the following upper bound holds

| (A.15) |

The last lemma of this part is concerned with the approximation error due to using the Sinkhorn divergence in lieu of the Wasserstein distance:

Lemma A.6.

(Sinkhorn Divergence Approximation Error) Suppose holds. Let denotes the empirical measure of Lemma A.5. Furthermore, consider the distribution ball , and

| (A.16) |

Then, for any , the following upper bound holds

| (A.17) |

where is a universal constant independent of .

A.2. Proof of Theorem 3.2

Consider the projected particle Langevin dynamics in Eq. (2.14) which we repeat here for the convenience of the reader

| (A.19) |

for all , where . Associated with the discrete-time process , we define the continuous-time cádlág process that is constant on the interval and satisfies the following recursion

| (A.20) |

for all , where , and is a -adapted Wiener process with the initial value , and independent increments

| (A.21) |

Therefore, by comparing the dynamics in Eqs. (A.19) and (A.20), we observe that for all .

We compare the iterations in Eq. (A.19) with the following decoupled -dimensional reflected Itô stochastic differential equation

| (A.22a) | ||||

| (A.22b) | ||||

where

-

•

,

-

•

, with ,

-

•

is the drift process defined as follows

(A.23) Moreover, is the gradient vector with the following elements

(A.24) -

•

is the local time of at the boundary of the projection space . In particular, is a measure on that is non-negative, non-decreasing, and whose support is defined

(A.25) -

•

and, is the normal vector to the boundary at the time .

Let us make some remarks about the stochastic differential equation in Eq. (A.22). First, let . Then, due to Skorokhod [51] and Tanka’s [55] theorems, it is known that the processes and are uniquely defined. The uniqueness property is also referred to as the Skorohod’s reflection mapping principle in stochastic calculus (cf. Definition A.18). Second, notice that at each given time , the drift of the th coordinate only depends on the location of the th particle , and is independent of other particles .

Now, consider the following càdlàg process , where , and

| (A.26) |

for all , where , and . We also consider the following càdlàg process that is constant on the interval , and has the following recursions

| (A.27) |

for all , where , , and is the Wiener process with a drift. In particular,

| (A.28) |

We notice that the processes and in Eqs. (A.26) and (A.27), respectively, only differ in the definition of the Wiener process.

In the sequel, we establish three propositions to derive bounds on the Wasserstein distances between the laws of cádlág processes in Eqs. (A.20),(A.22),(A.26), and (A.27):

Proposition A.1.

(Wasserstein Distance between the Laws of Cádlág Processes) Consider the empirical measure associated with the Langevin particles in Eq. (A.20). Furthermore, let denotes the law of the random variable defined by the recursion in Equation (A.20). Then, the following upper bound holds

| (A.29) |

with the probability of (at least) .

Proposition A.2.

Proposition A.3.

(Time Discreteization Error) Consider the laws and , where and are governed by the dynamics of Eqs. (A.26) and (A.27), respectively. Then, the following inequality holds.

| (A.30) |

Moreover, for any , the following maximal inequality holds

| (A.31) |

where the constants and are defined as follows

| (A.32a) | ||||

| (A.32b) | ||||

| (A.32c) | ||||

| (A.32d) | ||||

| Above, is a constant independent of and , and is the distance of the initial value from the boundary. | ||||

From the triangle inequality of the 2-Wasserstein distance, we obtain that

| (A.33) |

We now leverage the upper bounds in Propositions A.1, A.2, and A.3 to bound each term on the right hand side of Eq. (A.33). Taking the limit and choosing the prescribed step-size in Theorem 3.2 yields

| (A.34) |

For any pseudo-Lipschitz function and empirical measures , it holds that as if and only if , see [56, Thm. 6.9]. Therefore, due to Eq. (A.34), we conclude that uniformly on the interval .

In the sequel, we characterize a distributional dynamics describing the evolution of the Lebesgue density of the limiting measure :

Proposition A.4.

(McKean-Vlaso Mean-Field Equation) Let denotes a probability space, and consider the -adapted reflected diffusion-drift process described as follows

| (A.35a) | ||||

| (A.35b) | ||||

where is the law of the underlying process, and and are the reflection processes from the boundaries and , respectively. In particular, , non-decreasing, cádlág, and

| (A.36) |

Suppose the Lebesgue density exists. Then, the Lebesgue density of the law of the stochastic process at subsequent times is governed by the following one dimensional partial differential equation with Robin boundary conditions

| (A.37a) | |||

| (A.37b) | |||

| (A.37c) | |||

The proof of Theorem A.4 is a special case of the proof provided by Harrison and Reiman [20] for general multi-dimensional diffusion-drift processes that solve the Skorokhod problem for a general reflection matrix (cf. Definition A.18). More specifically, the proof of [20] is based on an extension of Itô’s formula proved by Kunita and Watanabe [27], and Grisanov’s change of measure technique in Theorem A.16.

To finish the proof, we apply the result of Proposition A.4 to each coordinate of the stochastic process in Eqs. (A.22).

A.3. Proof of Proposition A.3

We establish the existence and uniqueness via the standard technique of Lax-Milgram theorem in the theory of elliptic PDEs, see [15, Chapters 5,6], and [4, 5]. In particular, we closely follow the work of [4], and provide the proof for a slightly more general case, namely we consider the Poisson equation

| (A.38a) | ||||

| (A.38b) | ||||

where is the outward normal vectors at the boundary . Furthermore, we suppose the potential satisfies for every . In the steady-state regime (i.e. when ), the mean-field PDE in (3.3) is a special case of the general form described in Eq. (A.38) with , , for all , and , where is a steady-state solution of the mean-field PDE in (3.3). Equation (A.38) describes a probability in the space of probability measures in , and is to be interpreted in the weak sense. The main difficulty arises from assigning boundary values along to a function as it is not in general continuous. The following trace theorem attempts to address this issue:

Definition A.7.

(Trace Theorem, see, e.g., [15, Thm. 1]) Suppose is bounded and is in . Then, there exists a bounded linear operator such that

-

•

if

-

•

,

for each , with the constant depending only on and . Furthermore, is called the trace of on .

Equipped with Definition A.7, we can now provide the form of weak solutions of the PDE in Eq. (A.38):

Definition A.8.

(Weak Solutions of the Steady-State Poisson Equation) We say that a function is a weak solution to equation (A.38) supplemented with the boundary condition if for all the test functions the following identity holds

| (A.39) |

almost everywhere in time .

To establish the uniqueness of the steady-state solution, we reformulate the weak solution in terms of the Slotboom variable . The transformed flux is given by . Then, the weak formulation in Eq. (A.39) can be rewritten as follows

| (A.40) |

Define the following bilinear form

| (A.41) | ||||

| (A.42) |

The bilinear form is continuous on due to the Cauchy-Schwarz inequality and the fact that the Sobolev norm is controlled by the -norm of the gradient. Moreover, the bilinear form is non-coercive.777A bilinear form is coercive if for some constant .

A weak solution for Eq. (A.40) satisfies the following condition

| (A.43) |

We claim satisfies the hypotheses of Lax-Milgram on . In particular, we must show that there exist constants such that the following energy estimates are satisfied for all (see [15, 6.2.2 Theorem 2])

| (A.44a) | ||||

| (A.44b) | ||||

The first condition follows by boundedness of the trace operator in Definition A.7 as well as boundedness of and its gradient. In particular,

| (A.45) |

where and .

To establish the Gårding Inequality, we invoke the following variation of Sobolev type inequality for boundary value problems:

Theorem A.9.

(Sobolev Type Inequality for Bounded Domains, [44, p. 4]) For a bounded domain and for all the functions , there exists a constant depending on only, such that the following inequality holds

| (A.46) |

A.4. Proof of Lemma A.3

We begin the proof by writing the following basic inequalities

where the error term is defined as follows

| (A.47) |

where the last equality follows by using the integral representation of the kernel function in Equation (2.9).

Now, we invoke the following strong duality theorem [16]:

Theorem A.10.

(Strong Duality for Robust Optimization, [16, Theorem 1]) Consider the general metric space , and any normal distribution , where is the set of Borel probability measures on . Then,

| (A.48) |

provided that is upper semi-continuous in .

Under the strong duality of Theorem A.10, we obtain that

| (A.49) |

In the sequel, let . The Moreau’s envelope [38] of a function is defined as follows

| (A.50) |

where is the regularization parameter. We also define the proximal operator as follows:

| (A.51) |

When the function is differentiable, the following lemma is established in [26]:

Lemma A.11.

(Moreau’s envelope of Differentiable Functions) Suppose the function is differentiable. Then, the Moreau’s envelope defined in Eq. (A.50) has the following upper bound and lower bounds

| (A.52) |

In particular, when is -Lipschitz, we have

| (A.53) |

We now require the following result due to [43]:

Proposition A.5.

(Basic Properties of Moreau’s envelope,[43]) Let be a lower semi-continuous, proper and convex. The following statements hold for any :

-

•

The proximal operator is unique and continuous, in the sense that whenever with .

-

•

The value of is finite and depends continuously on , with for all as .

-

•

The Moreau envelope function is differentiable with respect to and the regularization parameter . Specifically, for all , the following properties are true:

(A.54a) (A.54b)

Now, we return to Equation (A.49). We leverage the lower bound on Moreau’s envelope in Eq. (A.52) of Lemma A.11 as follows

| (A.55) |

Let . Then, applying the union bound in conjunction with Inequality (A.55) yields

| (A.56) |

Now, we state the following lemma:

Lemma A.12.

(Tail Bounds for the Finite Sample Estimation Error) Consider the estimation error defined in Eq. (A.47). Then, the following statements hold:

-

•

is a sub-exponential random variable with the Orlicz norm of for every . Moreover,

(A.57) -

•

is a zero-mean sub-Gaussian random variable with the Orlicz norm of for every . Moreover,

(A.58)

A.5. Proof of Lemma A.4

We recall the definitions of the population and empirical distributional balls

| (A.60a) | ||||

| (A.60b) | ||||

Due to the strong duality result of Theorem A.10, the following identity holds

| (A.61) |

Similarly, we have

| (A.62) |

In Eqs. (A.61) and (A.62), has the following definition

| (A.63) |

Let and denote the solution of the optimization problems in Eqs. (A.61) and (A.62), respectively. We claim that

| (A.64) |

To establish the upper bound on , we first derive a crude upper bound on the objective value

| (A.65) |

where follows by evaluating the objective function at , and is due to the following inequality

| (A.66) |

which holds for all . To derive the last inequality, we used the fact that and for all . Now, for , we obtain that

| (A.67) |

where is due to the upper bound on Moreau’s envelop in Lemma A.11, and is due to the upper bound in Eq. (A.66). From Inequalities (A.65) and (A.67) we conclude that the objective value of the minimization for is strictly larger than the objective value evaluated at . Thus, necessarily . Using a similar argument (mutatis mutandis for the upper bound (A.66)), we can prove that .

Then, the following inequality holds

| (A.68) |

where the last inequality follows by the fact that for two bounded functions , we have .

Let and denote two sequences that differs in the -th coordinate for . Then,

| (A.70) | ||||

| (A.71) |

where last inequality follows from the fact that , and that . From McDiarmid’s martingale inequality [31] we obtain that

| (A.72) |

for any fixed , and . Consider an -net covering of the interval denoted by , where .

The mapping is Lipschitz on the domain . Indeed, for any , we obtain

We leverage Eq. (A.54b) of Proposition A.5 to obtain

| (A.73) |

where the last inequality is due to the fact that . Consequently, is -Lipschitz, and hence is -Lipschitz.

| (A.74) |

Using the union bound yields

| (A.75) |

Therefore, with the probability of (at least) , we have

| (A.76) |

We plug Eq. (A.76) into (A.74)

| (A.77) |

Since the size of the net is arbitrary, we let . Then, from Eq. (A.69) we obtain

| (A.78) |

with the probability of at least .

A.6. Proof of Lemma A.5

We define the solution of the population objective function as follows

| (A.79) |

We also define the solution of the empirical kernel alignment as follows

| (A.80) |

Due to the optimality of the empirical measure for the inner optimization in Eq. (A.79), the following inequality holds

| (A.81) |

We now expand to obtain the following inequality

After rearranging the terms in Eq. (A.81), we arrive at

| (A.82) |

where the last step follows by the fact that for radial kernels for all . Similarly, due to the optimality of the empirical measure for the optimization in Eq. (A.80) we have that

| (A.83) |

Combining Eqs. (A.82) and (A.83) now yields

| (A.84) |

A.7. Proof of Lemma A.6

To establish the proof, we state the following proposition due to [29, Proposition 1]:

Proposition A.6.

(Approximation Error in Sikhorn’s divergence, [29]) For any pair of discrete measures , the following inequality holds

| (A.85) |

where is a constant independent of , that depends on the support of , and .

Using Lagrange’s multipliers for the distributional constraints yield the following saddle point problems

| (A.86a) | ||||

| (A.86b) | ||||

Let and denote the saddle points of (A.86a) and (A.86b), respectively. Due to the approximation error in Eq. (A.85) of Proposition A.6, the following inequality holds for all ,

| (A.87) |

respectively. Due to the optimality of for the saddle point optimization (A.86a), we have that

| (A.88) |

Using the upper bound in Eq. (A.87) yields

| (A.89) |

Combining Eqs. (A.88) and (A.89) yields

| (A.90) |

Similarly, it can be shown that

| (A.91) |

Putting together Eqs. (A.90) and (A.91) yields the following inequality

| (A.92) |

From Eqs. (A.9) and (A.10), we also have

| (A.93) |

Plugging Eq. (A.92) into Eq. (A.93) and using the fact that for all yields

| (A.94) |

It now remains to show that the optimal Lagrange multipliers and in Equation (A.94) are bounded. To this end, define the following Lagrangian dual function

| (A.95a) | ||||

| (A.95b) | ||||

Furthermore, let and are the empirical measures in conjunction with the slater vectors in Assumption (A.2). We leverage [34, Lemma 1], to obtain following upper bounds

| (A.96a) | ||||

| (A.96b) | ||||

where is arbitrary, e.g. .

A.8. Proof of Proposition A.1

To compute the 2-norm difference between the processes and , we define the following auxiliary vectors

| (A.97a) | ||||

| (A.97b) | ||||

The recursions in Eqs. (A.20)-(A.26) then take the following forms

| (A.98a) | ||||

| (A.98b) | ||||

By the non-expansive property of the Euclidean projection onto a non-empty, closed, convex set we obtain (see [2])

| (A.99) |

Using a triangle inequality yields

| (A.100) |

Computing Eq. (A.100) recursively yields

| (A.101) |

Therefore, using the triangle inequality and based on the initialization , we can rewrite Eq. (A.101) as follows

| (A.102) |

In the sequel, we analyze each term separately:

A.8.1. Upper Bound on

Let denotes the -algebra generated by the samples , and the initial condition . Let . Then, taking the expectation with respect to the joint distribution yields

where has the following elements

| (A.103) |

where

| (A.104a) | ||||

| (A.104b) | ||||

Define the following random vector

| (A.105a) | ||||

| (A.105b) | ||||

with . Clearly, is a martingale . Moreover, it has a bounded difference

| (A.106) |

Now, for all , the following inequalities can be established using Assumption (A.1),

| (A.107a) | ||||

| (A.107b) | ||||

respectively. From Eq. (A.106) we have

| (A.108) |

Therefore, is (conditionally) zero mean and bounded, and is thus (conditionally) sub-Gaussian with the Orlicz norm of , i.e.,

| (A.109) |

We thus conclude that is sub-Gaussian with the Orlicz norm of . Now, we note that

| (A.110) |

Applying the Bernestein inequality yields

| (A.111) | ||||

| (A.112) |

Applying a union bound yields

| (A.113) |

Therefore, with the probability of at least , we obtain

| (A.114) |

A.8.2. Upper Bound on

To characterize the upper bound on , we write

| (A.115) | ||||

| (A.116) |

Moreover, using Eqs. (A.103)-(A.104) and the triangle inequality yields

| (A.117) |

The first term on the right hand side of Eq.(A.117) has the following upper bound

| (A.118) |

where we used the fact that the mapping is -Lipschitz, and follows by using Assumption (A.2).

The second term on the right hand side of Eq. (A.117) has the following upper bound

| (A.119) |

Plugging Eqs. (A.118), (A.119) into Eq. (A.117) yields

where the last inequality follows from the fact that , , and . Now, plugging Eq. (A.8.2) into Eq. (A.116) yields

| (A.120) |

Therefore, the error has the following upper bound

| (A.121) |

for all . Therefore,

| (A.122) |

A.8.3. Upper Bound on

To upper bound on , we bound the following norm

| (A.123) |

Each term inside the parenthesis on the right hand side of Eq. (A.123) has the following upper bound

| (A.124) |

where the last step is due to the triangle inequality. The first term on the right hand side of the last inequality in (A.124) has the following upper bound

| (A.125) |

The second term on the right hand side of the last inequality in (A.124) has the following upper bound

| (A.126) |

where the inequality follows by the fact that , and is the empirical measure associated with the samples , i.e.,

| (A.127) |

We use the upper bounds Eqs. (A.126) and (A.125) in conjunction with Inequality (A.124). We derive

| (A.128) |

We apply McDiarmid’s martingale inequality to obtain the following concentration inequality

| (A.129) |

Let . Then, we obtain for all that

| (A.130) | ||||

| (A.131) |

Applying a union bound yields

| (A.132) |

Therefore, with the probability of at least , we have

| (A.133) |

A.9. Combining the upper bounds

We now leverage the upper bounds on , , and in Eqs. (A.111), (A.122), and (A.133). Define

| (A.134) |

Applying a union bound yields the following inequality from Eq. (A.102)

| (A.135) |

with the probability of at least . In deriving the last inequality, we assumed that .

Now, we invoke the discrete Grönwall’s inequality [21]:

Lemma A.13.

(Discrete Grönwall’s inequality, [21]) If , , and are non-negative sequences, and

| (A.136) |

then,

| (A.137) |

Employing the (discrete) Grönwall’s inequalities (A.136)- (A.137) of Lemma A.13 in conjunction with Inequality (A.135) yields

| (A.138) |

with the probability of . Alternatively, since , we have

| (A.139) |

Recall the definition of the Wasserstein distance between two measures ,

| (A.140) |

where the infimum is over all pair of random variables with the marginals and . Accordingly,

| (A.141) |

For two measures on a compact metric space with the diameter , the following inequalities can be shown for all , (see, e.g., [37])

| (A.142a) | ||||

| (A.142b) | ||||

Specifically, Inequalities (A.142a) and (A.142b) are due to Jensen’s and Hölder’s inequalities, respectively. From Eqs. (A.142b) on the metric space with and and (A.141) we obtain that

| (A.143) |

where we used the fact that .

Now, we use the following tensorization property of the Wasserstein distances:

Theorem A.14.

(Tensorization, [30, Lemma 3]) Consider the metric measure space , and let and denotes two probability measures on n. Then,

| (A.144) |

for any . In the particular case of , the following exact identity holds

| (A.145) |

In particular, when and , then

| (A.146) |

and for ,

| (A.147) |

A.10. Proof of Proposition A.2

Let denotes a filtered probability space, and let denotes the Wiener processes that is -adapted. To establish the proof, we consider the mapping from the space of sample paths such that , where is defined recursively as follows

| (A.149) |

where , and . Then, , and . Let and . Furthermore, and , where and .

Then, for any measurable mapping , the following inequality holds

| (A.150) |

Therefore,

| (A.151) |