George Bouzianis and Lane P. Hughston

Department of Computing, Goldsmiths College, University of London

New Cross, London SE14 6NW, United Kingdom

email: gbouz001@gold.ac.uk, l.hughston@gold.ac.uk

Abstract

We consider the problem of optimal hedging in an incomplete market with an established pricing kernel. In such a market, prices are uniquely determined, but perfect hedges are usually not available. We work in the rather general setting of a Lévy-Ito market, where assets are driven jointly by an -dimensional Brownian motion and an independent Poisson random measure on an -dimensional state space. Given a position in need of hedging and the instruments available as hedges, we demonstrate the existence of an optimal hedge portfolio, where optimality is defined by use of an least expected squared error criterion over a specified time frame, and where the numeraire with respect to which the hedge is optimized is taken to be the benchmark process associated with the designated pricing kernel.

This paper is concerned with optimal hedging in incomplete markets. Hedging is important, since it lies at the heart of risk management. Historically, hedging in complete markets has played a significant role in the foundations of option-pricing theory Black Scholes ; Merton 1973 ; Cox Ross Rubenstein ; Harrison Pliska ; Bensoussan .

From a modern perspective, however, hedging arguments need not be invoked in the determination of prices. Instead, pricing is achieved by use of a pricing kernel. The connection between the two approaches is that in a complete market the specification of the price processes of a sufficiently large number of assets is enough to allow one to determine the pricing kernel associated with that market. Nevertheless, in the absence of market frictions, the prices of all of financial assets are determined in an incomplete market, including those of derivatives, once we designate a pricing kernel. In the incomplete market situation, however, one can not in general form a perfect hedge of a given position. This leaves us with a more precise statement of our problem: namely, determination of the optimal strategy for hedging a financial position in an incomplete market, given the set of hedging assets at the hedger’s disposal. The optimal hedge corresponds to the maximal possible elimination of risk in a financial position making use of the instruments available for this purpose.

The paper is structured as follows. In Section II we briefly summarize some of the mathematical ideas that we require. We define what we mean by a Lévy-Ito process and in Proposition 1 we recall the general form of Ito’s formula applicable to Lévy-Ito processes. Then in Proposition 2 we give a version of the Ito formula that holds when the large jumps are moderated, which is useful in financial applications. In Proposition 3 we comment on the form that the Ito isometry takes in the Lévy-Ito setting.

In Section III we introduce the family of risky assets that we work with in the hedging problem. We argue that the most natural approach to hedging arises when the values of the various assets under consideration are expressed in units of the benchmark process associated with the pricing kernel. In Section IV we consider the hedging of a position in a risky asset in a one-dimensional Lévy-Ito market in the situation where the hedging instrument is another risky asset driven by the same one-dimensional

Lévy-Ito process. In general, a perfect hedge is not possible in such a market, so one aims for a best possible hedge instead. We take the view that the goal is that of optimal elimination of the risk, which we characterize in a natural way using a quadratic optimization criterion. See Arai 2005 ; Biagini Oksendal 2006 ; Cerny Kallsen 1984 ; Cont Tankov Voltchkova ; Delbaen Schachermayer 1996 ; Follmer Sondermann 1986 ; Gourieroux Laurent Pham 1998 ; Hubalek Kallsen Krawczyk 2006 ; Lim 2006 ; Pham 2000 ; Schweizer 2001 for aspects of quadratic hedging. In Proposition 4 we obtain a formula for the optimal hedge in the case of a single hedging asset. We refer to the asset being hedged as the contract asset. The terminology is inherited from the language of derivatives pricing, though in the present context the asset being hedged need not be a derivative; indeed, the various assets involved are essentially on an equal footing. In Section V we consider the situation where we hedge the contract asset with a position in risky assets. In Proposition 5 we work out an expression for the optimal hedge in such a market, and in Proposition 6 we show that if there is negligible redundancy among the hedging assets then the optimal hedge obtained with hedging instruments is better than the optimal hedge obtained with such instruments.

In Section VI we look in more detail at the case where two hedging assets are available to hedge the contract asset, and an explicit formula for the optimal hedge is given in Proposition 7. We illustrate the results in the simplest possible situation: this is the case of a geometric Lévy asset for which the Lévy process is a linear combination of a Brownian motion and a Bernoulli process. We refer to a Lévy process of this type as a Bernoulli jump diffusion. By a Bernoulli process we mean a compound Poisson process for which each jump is characterized by an independent Bernoulli random variable taking one of two possible values. We consider the situation where the contract asset and the hedging assets are geometric Bernoulli jump diffusions driven by the same Lévy-Ito process. We illustrate the fundamental fact that a better hedge can be obtained by using both of the hedging assets rather than just a single hedging asset, even though a perfect hedge is not obtainable as long as the Brownian component of the driving process is present. On the other hand, if the Brownian volatility is small for the various assets under consideration, then a nearly perfect hedge can be obtained.

Finally, we set out some useful formulae from the Lévy-Ito calculus in an Appendix.

II Mathematical preliminaries

We begin with a brief account of the mathematical context in which we formulate the hedging problem. Most of the material in this section is well known, but we find it convenient to set out various details. The Lévy-Ito market provides a modelling framework of considerable generality. In particular, it contains all of the familiar Brownian motion driven models and Lévy driven models as special cases. The setup is as follows. We fix a probability space that supports an -dimensional Brownian motion alongside an independent Poisson random measure with mean measure , where is taken to be the Lévy measure associated with an -dimensional pure-jump Lévy process. Thus is a -finite measure on such that and

(1)

We write for the augmented filtration generated by and . See Applebaum ; Oksendal Sulem 2014 ; Jeanblanc Yor Chesney ; BHJS ; Eberlein Kallsen

for aspects of the theory of Lévy-Ito processes. In the one-dimensional case, by a Lévy-Ito process driven by and we mean a process satisfying a dynamical equation of the form

(2)

where

(3)

We require that and be -adapted, that and be -predictable, and that

(4)

for . We note that the integral with respect to in equation (2) and similar expressions of this type is defined by means of a limiting procedure as the origin is approached, as described, e.g., in reference Sato 1990 at page 120. Then we have the following generalization of Ito’s formula (see, for example, reference Applebaum , Theorem 4.4.7):

Proposition 1.

Let admit a continuous second derivative and let be a Lévy-Ito process for which the dynamics are as in (2). Then for it holds that

(5)

We can use the generalized Ito formula to work out Ito product and quotient rules for such processes. These results are very useful, so for the convenience of the reader we set them down in detail in the Appendix.

In some situations will be appropriate to consider processes for which the dynamical equation takes the form

(6)

where the integral involving the large jumps is taken with respect to the compensated Poisson random measure. In order for this to be possible, must satisfy

(7)

which is sufficient to ensure that the integral with respect to the compensated Poisson random measure exists for large jumps. If we impose the stronger condition

(8)

we can simplify and unify the notation by using a common symbol for the coefficients of the compensated Poisson random measures for small jumps and large jumps. Then we write

(9)

and the associated condition on the coefficients takes the form

(10)

in place of (4), where the subscript denotes integration over the whole of the real line.

We shall refer to processes satisfying (9) and (10) as being “symmetric” since large and small jumps are treated similarly. Symmetric processes turn out to be useful in financial applications, where the stronger condition on the integrability of the jump volatility with respect to the Lévy measure for large jumps is not unreasonable. In the symmetric case Ito’s formula takes the following form:

Proposition 2.

Let admit a continuous second derivative and let be a symmetric Lévy-Ito process for which the dynamics are as in (9). Then for we have

(11)

The higher-dimensional analogues of Propositions 1 and 2 are straightforward. Finally, we note that the Ito isometry can be generalized in the present context. So far, we have not imposed any integrability conditions on the processes that we have considered. For the Lévy-Ito analogue of the Ito isometry we require that the process satisfies an condition.

Proposition 3.

Let be a Lévy-Ito process such that

(12)

where is a constant and

(13)

If

for , then is a martingale and for it holds that

(14)

Again, the corresponding result for an -dimensional Lévy-Ito process is straightforward.

III Risky assets

We proceed to consider the problem of optimal hedging. It should be emphasized from the outset that we are not concerned here with the problem of derivative pricing via hedging arguments. We assume that prices are known and we look instead at the problem of hedging a position in one asset by use of a self-financing portfolio of other assets. In a complete market we know that an exact hedge can be obtained in such a situation; but we work in an incomplete market, where exact hedges are generally not available, so we look for an optimal hedge instead.

We fix a probability space where is the real-world measure. The market filtration is taken to be the augmented filtration generated by a one-dimensional Brownian motion and an independent one-dimensional Poisson random measure , where the Poisson random measure is that associated with a one-dimensional pure-jump Lévy process in the sense discussed in Section II.

We introduce a fiat currency, which we call the domestic currency, in units of which prices are conventionally expressed. The market is assumed to be endowed with a pricing kernel for which the dynamics take the form

(15)

We assume that the domestic short rate and the Brownian market price of risk are adapted and that the jump market price of risk is predictable and such that

for and . The solution for the pricing kernel is then

(16)

where is defined by

(17)

We assume that the market includes a money market asset satisfying ,

along with one or more risky assets. For a typical risky asset we let denote the price process, and for simplicity we assume that the asset pays no dividend. The associated dynamics are taken to be of the form

(18)

where is adapted, is predictable, and for and . We shall require that the dynamics of are non-degenerate in the following sense. Let denote the subset of over which it holds that

(19)

We say that has non-degenerate dynamics if has measure 0. An alternative way of expressing the non-degeneracy condition is as follows. Let the support of the Lévy measure be defined as the set comprising all such that for any open set containing (Sato 1990 , page 148). Then can be defined to be the set

(20)

It should be evident that these definitions of the degeneracy subset are equivalent, and it is useful to keep both in mind.

We require that for any risky asset the process determined by the product of the pricing kernel and the asset price should be a -martingale. Thus we have

(21)

for , where denotes conditional expectation with respect to .

There is another way of expressing this condition which turns out to be useful for our purposes. It is well known that the process defined by for can be interpreted as a “natural numeraire” or “benchmark”. By the definition of the pricing kernel, we see that for any asset that pays no dividend the process defined by represents the price of the original asset expressed in units of the natural numeraire. It follows that the “natural” price of any such asset is a martingale. Then we have

(22)

for , or equivalently

(23)

Equation (22) shows that the domestic value of the asset at time can be represented as the product of the natural numeraire (which can be interpreted as a dividend-adjusted proxy for the market as a whole) and a fluctuating term, given by the conditional expectation of the natural value of the asset at some later time .

A form of (23) is used in the theory of derivatives, for instance, when we make use of the pricing formula

(24)

valid for , which shows that the natural value of the derivative at is given by the conditional expectation of the natural value of the payoff .

A calculation making use of (15), (18) and Lemma 5 (see Appendix) shows that the dynamical equation satisfied by the natural value of the risky asset takes the form

(25)

where and

,

or equivalently

(26)

The relations given in (26) demonstrate that the Brownian and jump volatilities of the asset with domestic price process

can each be decomposed into terms involving only the intrinsic “natural” volatility of the asset and terms associated with the volatility of the domestic pricing kernel but not associated with any particular asset.

One can check that as a consequence of (15) and Proposition 2 (or Lemma 6), the dynamical equation satisfied by takes the form

(27)

which is indeed of the type appropriate to an asset that pays no dividend, as one sees by comparing (18) with (27). The benchmark process has the property that its Brownian proportional volatility coincides with the Brownian market price of risk and its jump proportional volatility is given by an invertible function of the jump market price of risk.

The significance of the benchmark asset in the present investigation is as follows. We are concerned with the problem of hedging a position in a risky asset with a position in a portfolio consisting of one or more other risky assets. Now, when such a hedge is carried out, this involves a choice of base currency with respect to which the hedge is optimized. Clearly, the choice of base currency is largely arbitrary, and it does not make sense to insist on minimizing exclusively the magnitude of the residual value of the hedge portfolio in units of the domestic currency. Sometimes it is argued that there may be a favoured choice of base currency – for example the currency in which a household has to meet its daily obligations, or in which a business has to accommodate a series of cashflows in connection with its activities. But such considerations bring additional elements of structure into the argument, and the fact remains that there is no a priori reason why one fiat currency should be favoured over another in the absence of a more detailed specification of the problem. Of all the choices of hedging currencies there is, however, a “preferred” numeraire involving no additional elements of structure, and this is the benchmark. So we take the view that the optimization problem takes the form of minimizing a function of the magnitude of the value of the hedge portfolio when that value is expressed in units of the benchmark.

Proceeding with our investigation of optimal hedging, let us write for the domestic price process of another risky asset, which we call the contract asset. We shall assume that is strictly positive and that

(28)

where is adapted, is predictable, and for and .

We can think of as representing the domestic value process of the position that we wish to hedge, and as being the domestic value process of the hedging asset.

For applications, one usually needs to impose stronger conditions on the price processes under consideration. For example, in the case of a derivative, with payoff at time , it is reasonable to assume not merely that the payoff should satisfy , but also that it should satisfy . In other words, for derivative risk management, we typically desire that some measure of the uncertainty of the payoff can be worked out, such as its variance. Indeed, in financial markets, one does not really wish to be working with instruments that are so volatile or ill-behaved that it is not possible to assign a meaningful value to the variance of the payoff. Since, in international markets, there is no particular reason to prefer one currency to another, it makes sense to introduce a minimalist assumption to the effect that the variance of the natural value of the payoff should be quantifiable. Thus, we shall assume at the very least that . One could consider other choices for a measure of the riskiness of the payoff, and one could work this out in other units, but the choice that we have indicated is convenient from a mathematical perspective since the category of square-integrable random variables is well understood, and the use of natural units is well defined already under the assumptions that we have made. One might object that insisting on a finite variance is too strong an assumption; but the reply can be put in normative terms – namely, that for a financial instrument to be considered as a legitimate object of commerce, it needs in principle to be capable of being risk-managed in a reasonably conventional manner; and the requirement that the value of the instrument can be modelled as having a finite variance is a step in this direction, an embodiment of this idea.

IV Optimal Hedging in a Lévy-Ito market

We consider setting up a trading strategy to hedge the natural value of a position in a given asset. Going forward, we shall for this purpose assume that all values are given in natural units – that is, in units of the natural benchmark numeraire. Thus, we henceforth drop the use of the “bar” notation, and let and denote the natural prices of the hedging asset and the contract asset, respectively. For the associated price dynamics we write

(29)

and

(30)

Writing

(31)

one can use the Proposition 2 to show that the corresponding price processes are given by the expressions

(32)

and

(33)

The hedging problem can be formulated as follows. The hedger is holding a position in one unit of the contract asset. The value process of this asset is in natural units. The value process of the hedging asset is in natural units. We assume that the hedging asset can be borrowed in any quantity at no cost, and that a short position in the hedging asset can be maintained and adjusted on a continuous basis at no cost. The value of the hedge portfolio at time is

(34)

where the predictable process denotes the number of units of the hedging asset being shorted, and the predictable process denotes the number of benchmark units held in the hedge portfolio. Initially, we have . That is to say, the proceeds of the initial short sale of the hedging asset are deposited in the benchmark account. Thereafter, the portfolio is managed on a self-financing basis: thus, the change in the value of the portfolio over a small interval of time is given by

(35)

It follows from (34) and (35) that the position in the benchmark account at time is

(36)

or equivalently

(37)

where the integrals on the right-hand sides (36) and (37) are understood as being over the intervals and , respectively. Then for the dynamics of the hedge portfolio we have

(38)

Now, if both of the assets are driven purely by the Brownian motion, and there are no jumps, then a perfect hedge can be carried out in such a way that the value of the hedge portfolio is constant. In that case a short calculation shows that

(39)

The expression for the hedge ratio will look familiar, of course, but one should keep in mind that the hedge here is for the natural value of the contract asset, not its value in units of the fiat currency. In the general situation, when jumps are allowed, it is not possible to find a perfect hedge in the sense of completely erasing the riskiness of the position. Instead, we proceed as follows. We assume that the natural values of the assets under consideration are square-integrable in the sense that

(40)

for , and that the self-financing hedging strategy is such that the portfolio value at any time over which the hedge is maintained satisfies

(41)

Again, these assumptions are reasonable from a financial point of view, since we would not wish to consider assets that fail to satisfy such conditions as suitable for trading on a commercial basis. We fix a time interval . Our goal is to choose the hedging strategy so as to minimize the expected squared deviation of the value of the hedge portfolio at time from its value at time . Note that once we specify the positions held in the risky assets, the self-financing condition determines the corresponding holding required in the benchmark asset. Thus, if for any admissible choice of the strategy

we write

(42)

for the corresponding mean squared error, then we have

It follows that the mean squared error takes the form

(43)

where

Thus we are led to the following.

Proposition 4.

Let be hedged with units of

and units of the benchmark. Then the optimal hedge is given a.e.- by

(44)

Proof.

A standard argument using the calculus of variations establishes (44) as a candidate for the optimal hedge. The non-degeneracy condition imposed on the hedging asset ensures that the denominator is non-vanishing on . To prove that the candidate is indeed optimal, we need to show that the mean squared error in any alternative hedge is no less than the mean squared error in the candidate hedge. Let denote an alternative hedge. We say that two strategies and over are distinct if

(45)

A calculation then gives

(46)

where , and one sees that the right hand side is nonnegative for any alternative hedge. In fact, the optimal hedge dominates any distinct alternative.

∎

We remark, incidentally, that one can substitute the optimal hedging strategy

(44) back into the hedge portfolio value process with dynamics

(35) to check that the condition (41) is satisfied. In fact, one can use (46) as a shortcut to get this result. If we compare the error when no hedge is put on to the error when the optimal hedge is put on, then we have

(47)

which gives a bound on . We just need to check that the terms on the right hand side of this relation are both finite. But

(48)

which is finite on account our assumption that is square integrable. Then since we assume that is square integrable and that is integrable, for the second term we get

(49)

where

(50)

By virtue of the Cauchy-Schwartz inequality we have , and this allows to conclude that the second term is also finite.

V Optimal Hedging with Multiple Hedging Assets

Let us now consider the more general problem of setting up a trading strategy to hedge the natural value of a position in a given contract asset with a collection of hedging assets each with dynamics

of the form (29). Thus we have

(51)

We shall assume the collection is non-degenerate in the sense that no one of the assets can be replicated by holding a portfolio in the remaining assets along with a position in the benchmark. More precisely, let the degeneracy subset be the collection of points defined by

(52)

If follows that on the complement , no self-financing trading strategy in the hedging assets and the benchmark exists such that

(53)

for in the support of the Lévy measure. Our assumption is that the degeneracy subset should have -measure zero. We assume further that

(54)

for , . When such risky assets with negligible degeneracy are available for hedging, the hedge portfolio for the contract asset takes the form

(55)

and we impose the self-financing condition

(56)

Our goal is to choose the hedging strategy in such a way that the mean squared error in the portfolio value

(57)

is minimized. Then by (30), (51), (56) and (57) we have

and by use of the Ito isometry we obtain

Expanding the squares and gathering together the various terms we get

(58)

where

(59)

(60)

(61)

Applying a perturbation

(62)

to the hedging strategy, we find that the difference in the corresponding expressions for the mean squared errors is given by

(63)

A sufficient condition for the right-hand side of (63) to vanish to first order in the perturbing variables, and hence lead to a candidate optimum, is that the should satisfy

(64)

and we are thus led to the following.

Proposition 5.

Let be hedged with units of

for and units of the benchmark. Then the optimal hedge takes the form

(65)

where is the inverse of on .

Proof.

The inverse of the matrix exists on on account of the non-degeneracy condition that we have imposed on the collection of hedging assets. In particular, it follows from the definition of that

if and only if the inequality

(66)

holds for any non-vanishing hedging strategy . But this relation is equivalent to

(67)

which shows that is positive definite on , and hence possesses an inverse. The solution of equation (64) then gives a candidate optimal hedge. As in the case of a single hedging asset, we need to show that the error in any alternative hedge is no less than the error in the candidate solution. Putting (65) back into (58), we get

(68)

Then, letting be any alternative hedge that is distinct from the candidate (65), one finds that

(69)

The right side of (69) is strictly positive, and we deduce that is optimal and indeed that it dominates any strategy distinct from it.

∎

Next, we wish to show that if we add a further non-redundant hedging asset to an existing collection of hedging assets satisfying a non-degeneracy condition, the hedge will be improved by using all of the hedging assets. This is a characteristic feature of incomplete markets. Given and , let denote the optimal hedge determined in Proposition 5, and let be another hedging asset, which is taken to be non-redundant in the sense that it cannot be realized as a portfolio formed from the original hedging assets together with the benchmark asset.

More precisely, let us now write (in place of ) for the degeneracy set associated with the original hedging instruments, which we have assumed to be of -measure zero, and let us write for the degeneracy set of the enhanced collection of heading instruments, which we also assume to have -measure zero. It should be evident that , since there may be points in at which the enhanced collection degenerates even though the original collection is non-degenerate. Then we have the following.

Proposition 6.

For any contract asset , the optimal hedge obtained by use of the enhanced collection of hedging assets is strictly better than the optimal hedge obtained by use of the original hedging assets .

Proof.

The argument proceeds in two steps. First, let denote the value process of the optimal hedge position

constructed from the original hedging assets together with the benchmark asset, as determined in Proposition 5. Thus, we have

(70)

where is given as in (65). It follows by the self-financing condition that itself can be treated as an asset. Now consider a hedging strategy of the form where denotes the holdings in , where denotes the holdings in , and denotes the holdings in the benchmark asset. It is easy to see that an optimal hedge involving a pair of non-redundant risky hedging instruments will perform better than the optimal hedge obtained by use of just one of the two risky instruments. This is because the optimal hedge involving a single risky instrument is an example of a sub-optimal hedge involving two risky instruments. It follows that as a hedge for the strategy with value process will perform strictly better than the strategy with value process . That is to say,

(71)

On the other hand, we observe that if denotes the optimal enhanced hedging strategy involving the assets now available for hedging, along with a position in the benchmark, then the portfolio considered above at (71) is merely an example of a hedge involving the hedging assets, and though it might be optimal, in general it will be suboptimal. Therefore

(72)

and hence

(73)

It follows that the optimal hedge involving hedging instruments will perform better than the optimal hedge formed from any of them.

∎

VI Simulations

In conclusion, we propose in this section to look in more detail at the case and consider simulating the optimal trading strategy to hedge the natural value of a position in a given contract asset by use of two risky hedging assets. The problem will be framed in the case where all three of the assets are driven by a one-dimensional Brownian motion and an independent one-dimensional Poisson random measure . The hedging assets each have dynamics of the form (29). We write for the hedging assets, and we write for the holdings in these assets. Then the rather general construction given in Section V leads to the following:

Proposition 7.

Let the contract asset be hedged over with units of

, units of

, and units of the benchmark. Then the optimal hedge is given by

(74)

on the non degeneracy subset , where we write

As a numerical illustration of the general methodology let us consider the situation where each of the assets follows a geometric

Lévy process for which the Lévy process takes the form of a jump diffusion consisting of a standard Brownian motion superposed on a compound Poisson process. It should be recalled that even if the driving process in the exponent of the asset price is a Lévy process, the asset price itself follows a Lévy-Ito process.

We consider the simplest possible case, namely, that for which the pure-jump component of the Lévy process is a Bernoulli process. Let denote a compound Poisson process for which the jumps arrive randomly according to a Poisson process with rate . The jump sizes

are independent identically-distributed random variables. We assume that and are independent. Let us write for a typical element of the set . In the example under consideration we shall assume that has a Bernoulli distribution . Thus takes values in a set where

with and . The Lévy measure for such a process takes the form

(75)

where is the Dirac measure concentrated at and is the Dirac measure concentrated at . Then the price processes of the assets under consideration have dynamics of the form

(29)-(30), with deterministic time-independent volatilities. Since we are working with a geometric Lévy process, the jump volatility is of the form , for some . The price of a typical non-dividend paying risky asset in a Bernoulli jump diffusion market with this set up is thus of the form

(76)

where is a constant. For our simulations we consider a contract asset and a pair of hedging assets and , each of the form (76), with a view to forming an optimal hedge of the contract asset with positions in one or both of the hedging assets.

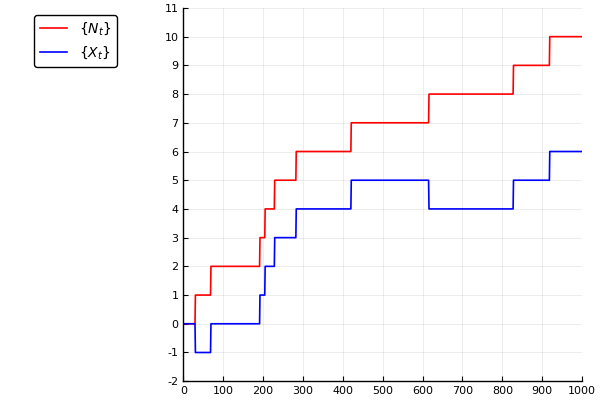

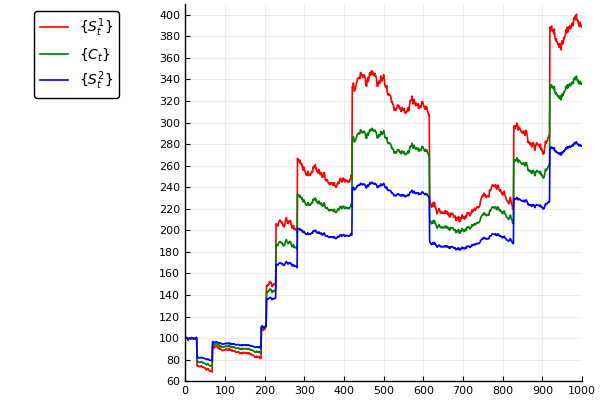

In Figure 1, we show on the left-hand side a random sample path for the Lévy process alongside the underlying Poisson process . On the right-hand side one finds the corresponding paths for the contract asset and the two hedging assets and . The inputs for this example are as follows: , , , , , , , , , , , , , and . The unit of time depicted on the -axis is divided into a thousand parts.

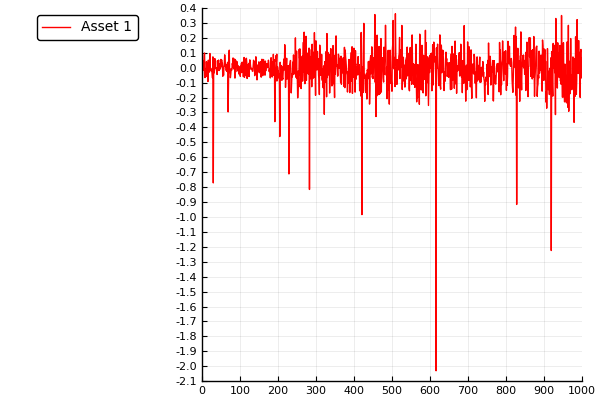

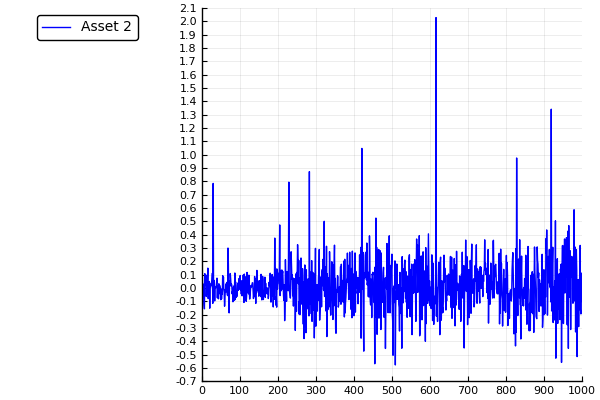

Now, we know from general theory that if the Brownian motion is non-vanishing then the hedge can never be perfect; but if the Brownian component is small for all three assets, then a reasonably good hedge should be obtainable using just two assets in the case of a Bernoulli jump diffusion. In Figure 2 we show the effect of using either or alone as a hedge and we plot the residual movements in the values of the hedged portfolios.

Figure 1: Bernoulli jump-diffusion market. The chart on the left above shows an outcome of chance for the Lévy process in blue, with the underlying Poisson process in red. The chart on the right above plots the value process of the contract asset in green. The high volatility hedging asset 1 is shown in red, and the low volatility hedging asset 2 is shown in blue.

Figure 2: Single-asset hedges. The chart on the left plots at each step the change in the value of the hedge portfolio, when asset 1 alone is used as the hedge. The lengthy downward spikes correspond to jumps, whereas the shorter spikes are due to Brownian volatility. In the chart on the right, asset 2 alone is used as the hedge. The lengthy upward spikes correspond to jumps.

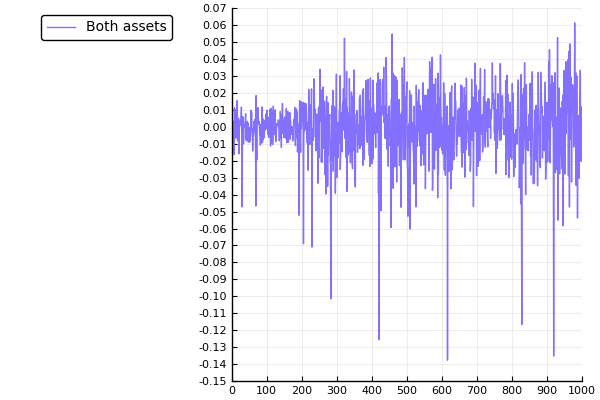

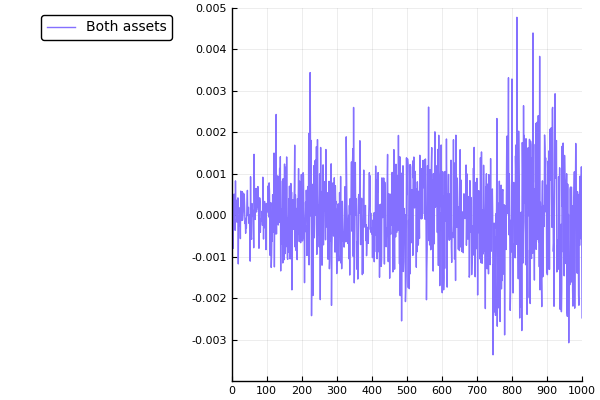

In Figure 3 we show the effect of using both hedging assets together to hedge the contract asset, and we note in particular the significant drop in the variance of the hedged portfolio. If we reduce the volatilities of the Brownian components still further, then we get a near perfect hedge, as illustrated in Figure 4. The Brownian volatilities for Figure 4 are given by , and .

Figure 3: Two-asset hedge. The figure above plots the change in the value of the hedge portfolio when both hedging asset 1 and hedging asset 2 are included in the hedging strategy for the contract asset. The Brownian volatilities in this example are , and .Figure 4: Two-asset hedge with reduced Brownian volatilities. This figure plots the change in the value of the hedge portfolio when both asset 1 and asset 2 are included in the hedging strategy for the contract, with , and . In this example, a near-perfect hedge is obtained. Note that the scale of the -axis is smaller than that of the previous figure.

It is sometimes said that Lévy markets are incomplete except in the Brownian case, in the situation where the number of available assets is no less than the number of Brownian motions. But this of course is not quite true, since a pure Poisson market is also complete. If a pair of geometric Lévy assets are driven by a common Poisson process, then either can be hedged by use of the other. A pure Bernoulli market is also complete, in the sense that if three geometric Lévy assets are driven by a common Bernoulli process, then any one can be hedged by use of the other two. Similarly, a compound Poisson process market with possible outcomes at each jump is complete if hedging assets are available. If a Brownian component is introduced into any of these scenarios, then the resulting market is incomplete; but if the Brownian volatilities are small, then near perfect hedges can be achieved, as we see in Figure 4.

APPENDIX

Here we present some useful versions of the Ito product and quotient rules for Lévy-Ito processes. The Brownian versions of these rules will be familiar, but the corresponding Lévy-Ito rules do not seem previously to have been presented systematically in all their different versions, so we do so here.

Let and be Lévy-Ito processes, each satisfying dynamical equations of the form

(2), such that

(77)

and

(78)

Lemma 1.

The product rule for Lévy-Ito processes takes the following form:

(79)

Proof.

This is similar to the proof of the corresponding result for Ito processes, and is obtained by applying Ito’s formula to each side of the identity

(80)

A calculation then gives the result claimed.

∎

Now let and be Lévy-Ito processes such that , are strictly positive. Then we obtain the following.

Lemma 2.

The quotient rule for Lévy-Ito processes is given by

(81)

Proof.

First one uses Proposition 1 to work out the dynamics of the process . Then one uses Lemma 1 to work out the dynamics of the product .

∎

For applications in finance, one often makes use of the “proportional” versions of the Lévy-Ito product and quotient rules, which are applicable if we assume that , , , are strictly positive. The dynamical equations for and will be assumed in Lemmas 3 and 4 to take the proportional form

(82)

and

(83)

Then we have the following formulae, which arise as consequences of Lemmas 1 and 2.

Lemma 3.

In the proportional case, the product rule takes the form

(84)

Lemma 4.

In the proportional case, the quotient rule takes the form

(85)

The various forms of the Ito product and quotient rules simplify for symmetric proportional processes, and the resulting formulae are extremely useful in applications. Let , , , be strictly positive For symmetrical processes we can write

(86)

and

(87)

and we obtain the following.

Lemma 5.

In the symmetric proportional case the product rule takes the form

(88)

Lemma 6.

In the symmetric proportional case the quotient rule takes the form

(89)

The corresponding results for -dimensional Lévy-Ito process are straightforward.

Acknowledgements.

The authors wish to thank D. C. Brody, A. Ciatti, S. Jaimungal and L. Sánchez-Betancourt for helpful discussions. We are also grateful for the helpful comments of an anonymous referee. GB acknowledges support from Timelineapp Tech Ltd, Basildon.

References

(1) Applebaum, D. (2009) Lévy Processes and

Stochastic Calculus, second edition. Cambridge University Press.

(2)

Arai, T (2005) Some remarks on mean-variance hedging for discontinuous asset price processes. International Journal of Theoretical and Applied Finance8, 425-443.

(3)

Bensoussan, A. (1984) On the theory of option pricing. Acta Applicandae Mathematicae2, 139-158.

(4)

Biagini, F. & Oksendal, B. (2006) Minimal variance hedging for insider trading. International Journal of Theoretical and Applied Finance9, 1351-1375.

(5)

Black, F. & Scholes, M. (1973) The pricing of options and corporate liabilities. Journal of Political Economy81, 637-659.

(6)

Bouzianis, G., Hughston, L. P., Jaimungal, S. & Sánchez-Betancourt, L. (2019) Lévy-Ito models in finance. ArXiv:1907.08499.

(7)

Černý, A. & Kallsen, J. (1984) On the structure of general mean-variance hedging strategies. Annals of Probability35 (4), 1479-1531.

(8)

Cont, R., Tankov, P. & Voltchkova, E. (2012) Hedging with options in models with jumps.

Abel Symposia on Stochastic Analysis and Applications2, 197-217.

(9)

Cox, J. C., Ross, S. A. & Rubenstein, M. (1979) Option pricing: a simplified approach. Journal of Financial Economics7, 229-263.

(10)

Delbaen, F. & Schachermayer, W. (1996) The variance-optimal martingale measure for continuous processes. Bernoulli2, 81-105.

(11)

Eberlein, E. & Kallsen, J. (2020) Mathematical Finance. Springer.

(12)

Föllmer, H. & Sondermann, D. (1986) Hedging of nonredundant contingent claims. In: W. Hildenbrand & A. Mas-Colell (eds.) Contributions to Mathematical Economics, 205-223. Amsterdam: North-Holland.

(13)

Gourieroux, C., Laurent, J. P. & Pham, H. (1998) Mean-variance hedging and numeraire. Mathematical Finance8, 179-200.

(14)

Harrison, J. L. & Pliska, S. R. (1981) Martingales and stochastic integrals in the theory of continuous trading. Stochastic Processes and their Applications11 (3), 215-260.

(15)

Hubalek, F., Kallsen, J. & Krawczyk, L. (1998) Variance optimal hedging for processes with stationary independent increments. Annals of Applied Probability16 (2) 853-885.

(16)

Jeanblanc, M., Yor, M. & Chesney, M. (2009) Mathematical Models for Financial Markets. Springer.

(17)

Lim, A. E. B. (1998) Mean-variance hedging when there are jumps. SIAM Journal on Control and Optimization44, 1893-1922.

(18)

Merton, R. C. (1973) Theory of rational option pricing. Bell Journal of Economics and Management Science4, 141-183.

(19)

Oksendal, B. & Sulem, A. (1995) Stochastic control of Itô-Lévy processes with applications to finance. Communications on Stochastic Analysis 8 (1), 1-15.

(20)

Pham, H. (2000) On quadratic hedging in continuous time. Mathematical Methods of Operations Research51, 315-339.

(21)

Sato, K. (1999) Lévy Processes and Infinitely Divisble Distributions. Cambridge University Press.

(22)

Schweizer, M. (2001) A guided tour through quadratic hedging approaches. In: E. Jouini, J. Cvitanić & M. Musiela (eds.) Option Pricing, Interest Rates and Risk Management, 538-574. Cambridge University Press.