Simplified Calculus for Semimartingales:

Multiplicative Compensators and Changes of Measure

Abstract

The paper develops multiplicative compensation for complex-valued semimartingales and studies some of its consequences. It is shown that the stochastic exponential of any complex-valued semimartingale with independent increments becomes a true martingale after multiplicative compensation when such compensation is meaningful. This generalization of the Lévy–Khintchin formula fills an existing gap in the literature. It allows, for example, the computation of the Mellin transform of a signed stochastic exponential, which in turn has practical applications in mean–variance portfolio theory. Girsanov-type results based on multiplicatively compensated semimartingales simplify treatment of absolutely continuous measure changes. As an example, we obtain the characteristic function of log returns for a popular class of minimax measures in a Lévy setting.

keywords:

Girsanov , Lévy-Khintchin , Mellin transform , Predictable compensator , Process with independent increments , Semimartingale representationMSC:

[2020] 60E10, 60G07, 60G44, 60G48, 60G51, 60H05, 60H30, 91G101 Introduction

Multiplicatively compensated semimartingales are an important tool in stochastic modelling. They appear, among others, in the following contexts.

-

•

Computation of characteristic functions, e.g., Jacod and Shiryaev [18, Section III.7].

-

•

Esscher-type measure changes including a variety of minimax martingale measures, e.g., Goll and Rüschendorf [15], Jeanblanc et al. [19]; martingale measures associated with ad-hoc numeraire changes, e.g., Eberlein et al. [12]; but also non-martingale measures, e.g., the opportunity-neutral measure in semimartingale mean-variance theory, e.g., Černý and Kallsen [5, Section 3.4]. A very general take on Esscher-type measures is presented in Kallsen and Shiryaev [22].

-

•

Proofs of moment bounds, e.g., to show existence and uniqueness of BSDE solutions, e.g., Kazi-Tani et al. [25, Lemma A.5]; to estimate variation distance of probability measures in Kabanov et al. [20, Theorem 2.1]; to prove uniform integrability of local martingales, e.g., Lépingle and Mémin [28, Théorème III.1], Ruf [32, Corollary 5].

- •

- •

This paper examines some of the consequences of multiplicative compensation for signed (and even complex-valued) semimartingales. The next statement is a special case of Theorem 4.1(2).

Theorem 1.1.

Let be a special –valued semimartingale with independent increments. Then

Here denotes the stochastic exponential111By convention, any stochastic exponential starts at , i.e., here . of a semimartingale and the predictable finite-variation part (here also called the drift) in the canonical decomposition of a special semimartingale .222We assume that , which makes the finite variation part unique; see [18, I.4.22]. Theorem 1.1 with , a Lévy process, , and the identity function recovers the Lévy–Khintchin formula for (Corollary 4.3). The operation denotes, roughly speaking, the –variation of (Definition 2.3). Observe that in Theorem 1.1 the process is deterministic.

To illustrate the novelty of Theorem 1.1, consider the task of computing the distribution of when the stochastic exponential is signed. Here, one can evaluate and for separately to obtain the Mellin transforms of the positive and negative parts, respectively (Example 4.4),

| (1.1) | ||||

| (1.2) |

The standard Lévy-Khintchin formula is unable to deliver such a result. The Mellin transform can then be used to solve, at least numerically, previously intractable questions concerning mean-variance portfolio allocation (Example 4.5).

Next, as a special case of Theorem 3.1(1) below, we have a complex-valued extension of a classical but perhaps not sufficiently well-known result due to Lépingle and Mémin [28, Proposition II.1].

Theorem 1.2.

Let be a special –valued semimartingale such that . Then is a multiplicative compensator of , that is, is a local martingale.

In the main body of the paper (see Theorem 3.1), we allow to explode on approach to a stopping time, which later allows study of a larger class of non-equivalent measure changes. In the context of Theorem 1.2, Theorem 1.1 asserts that is a true martingale whenever has independent increments (Theorem 4.1(3)).

Multiplicative compensation of semimartingales is, of course, not new (see, e.g., Yoeurp and Meyer [34], Azéma [2], Jacod [17], Mémin [29], Lépingle and Mémin [28], and Kallsen and Shiryaev [22]). We wish to emphasize the strength and flexibility of Theorem 1.2 when coupled with semimartingale representations. For example, Theorem 2.19 in [22] follows immediately from Theorem 1.2 by writing (see Example 3.6)

where stands for the stochastic integral . Many computations in [28] follow from Theorem 1.2 by taking (for and a local martingale ),

Theorem 1.2 is a stepping stone to Girsanov-type results for measure changes relying on non-negative multiplicatively compensated semimartingales.

Theorem 1.3.

Let be a special –valued semimartingale such that and is a uniformly integrable martingale. For the measure Q given by and a semimartingale , the following are equivalent.

-

(i)

is Q–special.

-

(ii)

is P–special.

-

(iii)

is P–special.

If either of these conditions holds, then and

where stands for the additive Q–compensator of the Q–special semimartingale . Furthermore, the following are equivalent.

-

(i’)

is a Q–local martingale.

-

(ii’)

is a P–local martingale.

-

(iii’)

is a P–local martingale.

As a practical application of Theorem 1.3, Example 5.6 in the main body of the paper computes the characteristic function of log returns for a popular class of minimax measures. Additionally, Example 5.11 showcases the usefulness of Theorem 1.3 by streamlining an otherwise fairly involved calculation appearing in [28].

In the rest of the paper we proceed as follows. Section 2 provides the setup of this paper. Section 3 discusses the construction of multiplicative compensators and provides several examples. Section 4 considers multiplicative compensation for stochastic exponentials of processes with independent increments. Section 5 introduces a version of Girsanov’s theorem and considers additive and multiplicative compensation after a change of measure. Finally, Section 6 concludes.

2 Setup and notation

The applications in this paper rely on semimartingale representations worked out in Černý and Ruf [8]. A whittled-down summary of the relevant definitions and results from [8] is provided in Subsections 2.1–2.5. We suggest skipping the details on the first reading and instead making use of the following “executive summary.” One can also consult the introductory paper [7] for further context and examples.

For a function that is constant in the first argument and twice continuously differentiable in the second argument and for an –valued semimartingale , the partial sums

converge uniformly on compact time intervals in probability to

| (2.1) |

as the time partition becomes finer; see Émery [13, Théorème 2a]. In such case, can be interpreted as the –variation of . Here and below we write for the process stopped at some stopping time .

Formula (2.1) also makes sense for some predictable functions . In particular, it makes sense for all predictable functions in the universal class defined below, including all twice-continuously differentiable deterministic time-constant functions. For , is not necessarily a –variation. We then speak more broadly of semimartingale representations, saying that is represented in terms of if there is such that . The functions in , such as , need not be defined everywhere. For to exist, it is enough that is compatible with , i.e., is finite almost surely.

The Émery formula (2.1) has a natural counterpart for complex-valued functions of several complex variables and the definition of takes this into account. Semimartingale representations in conveniently capture common operations on semimartingales. For example, locally bounded stochastic integration corresponds to “linear variation”

smooth transformation, too, has a simple representation in ,

Furthermore, is closed under composition, with

This turns common stochastic operations into algebraic manipulations of predictable functions, which is both more effective and more compact than the standard calculus. It yields formulae such as or for . Unlike the canonical decompositions that commonly appear in classical stochastic calculus, semimartingale representations are measure-invariant.

Semimartingale representations allow a systematic evaluation of the predictable compensator (drift, ) of a represented process in terms of the predictable characteristics of the representing process ; this follows naturally from the Émery formula (2.1). The drift calculation is further simplified by uniquely decomposing into two components, and , where is quasi-left-continuous and equals the sum of its jumps at predictable times in the semimartingale topology. Only the drift of is evaluated via (2.1) since at predictable stopping times one has the simpler formula

In practice, is often an Itô semimartingale. One may then rephrase the drift computation for the component in terms of time rates, reverting to drift rates, quadratic variation rates (squared volatilities), and jump intensities (Lévy measures).

The rules of semimartingale representations together with drift evaluation give rise to the simplified calculus of the title. In summary, the calculus provides a clear, systematic way to perform the “” operations that we have showcased in the introduction and which we shall encounter again in various applications.

We shall now provide a rigorous setup of the paper. Below, we mostly rely on the notation of Jacod and Shiryaev [18]. Throughout this section, let denote an integer.

2.1 Preliminaries

We explicitly shall allow quantities to be complex-valued. The reader interested only in real-valued calculus can easily always replace the general ‘–valued’ by the special case ‘–valued’ in their mind. We write for some ‘non-number’ . We introduce the functions and by for all and by

respectively. Observe that for contains the values of and , interlaced. The introduction of simplifies treatment of functions with undefined values, such as , that frequently arise in applications.

We fix a probability space with a right-continuous filtration . We shall assume, without loss of generality, that all semimartingales are right-continuous, and have left limits almost surely. For a brief review of standard results without the assumption that the filtration is augmented by null sets, see Perkowski and Ruf [31, Appendix A].

We denote the left-limit process of a (complex-valued) semimartingale by and use the convention . We also set . We write and for stopped at some stopping time .

For –valued semimartingales and we set

If is –valued, then denotes the corresponding –valued quadratic variation, formally given by

where denotes the identity matrix and the Kronecker product. Furthermore, we write for the continuous part of the quadratic variation .

As in [18, II.1.4], we consider the notion of a predictable function on . Observe that every time-constant deterministic function, such as or , can be considered a predictable function via the natural embedding of into . Let denote the jump measure of a semimartingale and its predictable compensator (under a fixed probability measure P). Then for a –valued bounded predictable function with we have

provided . If is special, we let denote the predictable finite-variation part in the canonical decomposition of , always assumed to start in zero, i.e., . Recall from [18, II.2.29a] that

| (2.2) |

In this paper we call a time-constant deterministic function a truncation function for if and if

| (2.3) |

is special.

Next, let us briefly discuss stochastic integrals. Consider a –valued process and a –valued semimartingale . If is real-valued then we write if both and are integrable with respect to (in the standard sense). We then write . If is complex–valued, then we say if , where represents the Kronecker product. We then write

for the stochastic integral of with respect to .

We sometimes shall work on stochastic intervals , where is a foretellable time, i.e., a stopping time that is almost surely equal to a predictable time. An example is discussed in Subsection 2.3, where this setup allows to define the stochastic logarithm of a semimartingale that hits zero. Let be a foretellable time with announcing sequence , i.e., and on . Then we say a process is a semimartingale (local martingale, etc.) on if is a semimartingale (local martingale, etc.) for each . We refer to Carr et al. [4] and Larsson and Ruf [27] for more details.

2.2 Decomposition of a semimartingale into ‘continuous-time’ and ‘discrete-time’ components

Denote by the set of finite variation semimartingales; by the subset of such that

and by the set of semimartingales that belong sigma-locally to the class of pure-jump finite variation processes .

The following proposition recalls a unique decomposition of a semimartingale into a semimartingale that jumps at predictable times and a quasi-left-continuous semimartingale .

Proposition 2.1 ([6], Proposition 3.15).

Every semimartingale has the unique decomposition

where , is a quasi-left-continuous semimartingale, jumps only at predictable times, and . We then have .

2.3 Stochastic exponentials and logarithms

If is a –valued semimartingale, then the stochastic exponential of is given by the formula (see [11, Théorème 1])

| (2.4) |

In order to handle non-equivalent changes of measures, we extend the definition of stochastic logarithm (see [18, II.8.3]) to processes that can hit zero. To this end, for a –valued semimartingale define the stopping times333Since we have not assumed the filtration to be complete, the Debut theorem may not be applied. Hence, and themselves might not be stopping times. However, there always exists a stopping time almost surely equal to and a predictable time almost surely equal to , respectively. Without loss of generality, we shall assume to work with such stopping times.

| (2.5) | ||||

| (2.6) |

Here is the first time the running infimum of reaches zero continuously. Let us now additionally assume that is absorbed in zero if it ever hits zero. The stochastic logarithm of is then given by

where is defined to be zero on the set , for all ; see also Larsson and Ruf [26].

2.4 Further details about predictable functions

For this subsection, fix some . For two predictable functions and we shall write to denote the function with the convention . If and are predictable, then so is .

For a predictable function we shall write and for the –th component of , where . We also write and for the real derivatives of , i.e., is the composition of the –th element of the gradient of and the lift and is the composition of the –th element of the Hessian of and the lift , for . Note that has dimension , has dimension , and the domains of , equal that of , i.e., . If is analytic at a point, say , then we also write and for the corresponding derivatives.

We want to allow for predictable functions such as whose effective domain is not the entire . To this end, we say that

2.5 Semimartingale representation

Often it will be useful to rely on representing a semimartingale with respect to another one. Such representations are worked out in Černý and Ruf [8]. Throughout this subsection let denote an –dimensional semimartingale.

The following class of predictable functions enjoys closedness with respect to common operations and a certain universality. A more general definition is possible (see [8, Definition 3.2]), but for our purposes, this universal class will suffice.

Definition 2.2 ([8], Definition 3.4).

Let denote the set of predictable functions such that the following properties hold, P–almost surely.

-

(1)

, for all .

-

(2)

is twice real-differentiable at zero, for all .

-

(3)

and are locally bounded.

-

(4)

There is a predictable locally bounded process such that

We write . ∎

Definition 2.3 ([8], Definition 3.8).

For a predictable function compatible with we use the notation

| ∎ |

The following properties of semimartingale representations are worth pointing out.

-

•

If is analytic or if is real-valued, then we may omit the hats on top of , , , and in the previous two definitions.

-

•

Using the notation of Proposition 2.1, we always have

(2.7) -

•

For sufficiently smooth , the partial sums converge in ucp to as the time partition becomes finer; see Émery [13, Théorème 2a].

Example 2.4 ([8], Proposition 3.13(3)).

We have , , for all , with

| ∎ |

Proposition 2.5 ([8], Proposition 3.13(6)).

Let be a predictable semimartingale of finite variation. Consider some compatible with and assume . Then is in and compatible with . Furthermore,

Proposition 2.6 (Adapted from [8], Proposition 3.14).

Let be a locally bounded –valued predictable process. Then and

Proposition 2.7 ([8], Proposition 3.15).

Let be an open set such that and let be twice continuously real-differentiable. Then the predictable function defined by

belongs to and is compatible with . Moreover,

| ∎ |

Theorem 2.8 ([8], Theorem 3.17).

The class is closed under (dimensionally correct) composition, i.e., if and is another predictable function with then . Furthermore, if is compatible with and is compatible with , then is compatible with and

Proposition 2.9 ([8], Proposition 4.1).

Assume . If then

Next assume instead that , , does not go to zero continuously, and is absorbed in zero if it ever hits zero. Furthermore, let be the first time . Then

Proposition 2.10 ([8], Proposition 4.2).

We have

| (2.8) | ||||

| (2.9) |

If , then

| (2.10) | ||||

where denotes the principal value logarithm.

Proposition 2.11 (Adapted from [8], Proposition 4.3).

Consider a –valued semimartingale and . If , assume furthermore . We then have

| (2.11) |

Recall the notion of a truncated process from (2.3).

Proposition 2.12 ([8], Proposition 5.6).

Fix compatible with and let (resp., ) be a truncation function for (resp., ). Then the following terms are well defined and the predictable compensator of is given by

If is analytic at , –almost everywhere, the following terms are well defined and

Remark 2.13 ([8], Remark 5.7).

Fix compatible with . Recall that in the notation of Proposition 2.1, (2.7) gives

Suppose now is special. One then has

Since the drift of has a simple form given next, in practice Proposition 2.12 is only used with to obtain . Indeed, the drift at predictable jumps times is given by

Here, denotes a countable family of stopping times that exhausts the jumps of . For each , there are many ways to choose ; it is sufficient to fix an arbitrary such family for each . ∎

Corollary 2.14 ([8], Corollary 5.8).

Let for some compatible with . Then the following holds.

Proposition 2.15.

If has independent increments and if is compatible with and deterministic, then , too, has independent increments. Moreover, if is a Lévy process and if is compatible, deterministic, and time-constant, then is also a Lévy process.

Proof.

By [18, II.4.15–19], has independent increments (respectively, is a Lévy process) if and only if its characteristics are deterministic (respectively, the characteristics are absolutely continuous with respect to time and their Radon-Nikodym derivatives with respect to time are time-constant) relative to a truncation function for . The claim now follows from Proposition 2.12 and Corollary 2.14. ∎

3 Multiplicative compensator

In many applications one seeks, for a given –valued semimartingale , a predictable process of finite variation that starts at and makes a local martingale. For example, changes of measure are frequently of the form where is a real-valued process that after hitting zero remains in zero. Another application arises when happens to be deterministic and to be a martingale. Then the multiplicative compensator is a device for computing expectations, namely,

We will see in Section 4 that the Lévy-Khintchin formula is but a special case of such setup.

Although we have in mind a situation where has further structure, it transpires that one may express directly in terms of . This result (Theorem 3.1) is of independent interest because it simplifies and generalizes existing characterizations of multiplicative compensators; see Jacod and Shiryaev [18, II.8.21], Kallsen and Shiryaev [22, Theorem 2.19], and also Lépingle and Mémin [28, Proposition II.1]. Recall from (2.6) that is the first time reaches zero continuously.

Theorem 3.1 (Multiplicative compensator).

Let be a –valued semimartingale absorbed in zero if it ever hits zero. Assume that is special on . Assume next that

| (3.1) |

Then the following statements hold.

-

(1)

We have on and the process is a local martingale on .

-

(2)

If is special (e.g., if is special and on ), then is a local martingale on the whole positive real line.

Example 3.8 below illustrates how can fail to be a local martingale on the whole positive real line without the assumptions of (2).

Proof of Theorem 3.1.

From (3.1) one obtains on . Proposition 2.9 yields

| (3.2) |

Consequently, Proposition 2.12 yields

which proves is a local martingale on .

Assume now that on . As is predictable, we may assume by localization that for some ; see [27, Lemma 3.2]. If additionally is special, then clearly so is . Let us now assume that is special. Then we may assume that is uniformly integrable. Let now denote a non-decreasing sequence of stopping times such that is a uniformly integrable martingale and such that . With these localizations in place, we now fix with and some and observe that

proving the claim. ∎

Remark 3.2.

When is –valued, condition (3.1) makes sure that the expected percentage change in is never equal to . The next remark deals with the case where is strictly positive. Note that and themselves may be –valued.

Remark 3.3.

Remark 3.4.

When can jump to zero, its multiplicative compensator on the interval is not defined uniquely. One may obtain another multiplicative compensator of by replacing in Theorem 3.1 with another special semimartingale that is indistinguishable from on the interval and satisfies a condition analogous to (3.1). This insight is used in the statement of Theorem 4.1 and again in Corollary 5.10.∎

The next proposition contains some auxiliary results concerning the drift of the stochastic logarithm. These results contain sufficient conditions for the statements in Theorem 3.1 to hold.

Proposition 3.5 (Drift of stochastic logarithm).

Let be a –valued semimartingale absorbed in zero if it ever hits zero. If is special then is special on . Moreover, if (3.1) holds then

As Example 3.8 below shows, being special on in conjunction with (3.1) does not guarantee that is special (on the whole positive real line).

Proof of Proposition 3.5.

Observe that the process is locally bounded on . Hence, if exists, then, with the help of Proposition 2.12, so does

This yields the first part of the statement.

Example 3.6 (Multiplicative compensator of an exponential process).

Assume that is a special semimartingale of the form for some –valued semimartingale and compatible . Assume for simplicity that is analytic at . Thanks to Proposition 2.10 and Theorem 2.8 we have . Proposition 2.12 now yields for that

| (3.3) |

This also gives

Theorem 3.1 now yields and

Consider now the special case of the above with for some locally bounded .444The following results also hold for general . However, for simplicity, in this paper we only discuss representations using the universal class , which requires the local boundedness of . For more details on generalizations, see the concluding Section 6. By Proposition 2.6, we have while (3.3) simplifies to

Hence, by (2.4) and Remark 2.13 the multiplicative compensator of equals

| (3.4) |

Kallsen and Shiryaev [22, Theorem 2.19] obtain (3.4) for real-valued and . In their work, the process is called the exponential compensator of . ∎

Example 3.7 (Multiplicative compensator of a power of a stochastic exponential).

Example 3.8 ( special on but not special on the whole time line).

Fix and consider the function

Here is the explosion time (to ) of . Observe that satisfies for all .

Let now denote a non-negative continuous local martingale with , for all , and for all . Such a local martingale can be obtained, for example, by appropriately time-changing a Brownian motion started at one. Moreover, let denote an independent Poisson process with unit intensity. Denote the stochastic process by and define next the non-negative process

which is a semimartingale as the product of a continuous local martingale and a process of finite variation. Then and is special on with

Hence on and Theorem 3.1 yields

is a local martingale on with jumps

Hence, for each one has

and is special by (2.2). However,

yields

| (3.5) |

thus is not special, again by (2.2).

This now shows that requiring to be special is strictly weaker than requiring to be special. This also gives an example where is special on but is not special (on the whole positive line).

We now modify this example slightly to illustrate that in Theorem 3.1 is not always a local martingale (on the whole positive line) if it is not required to be special a priori. To see this, take to be a compound Poisson process with jumps of size with equal intensity, still independent of . Now on , hence . However, as in (3.5), the jumps of are not locally integrable, hence cannot be a local martingale. ∎

4 Compensators of processes with independent increments

The following generalization of the Lévy-Khintchin formula in Theorem 4.1(2) seems to be missing in the literature. Kallsen and Muhle-Karbe [21, Proposition 3.12] prove a special case of Theorem 4.1(3), assuming strict positivity (and real-valuedness) of the stochastic exponential, which allows an application of a measure change technique in their proof. In the same context, Cont and Tankov [10, Proposition 8.23] do not require positivity but only treat the special case of Lévy processes.

Theorem 4.1 (Stochastic exponential of a process with independent increments).

Let denote a –valued semimartingale with independent increments and define the deterministic time

Then the following statements hold.

-

(1)

For with , is special if and only if . Moreover, in this case we have

(4.1) -

(2)

is special on if and only if for all . Moreover, in this case we have

-

(3)

is a local martingale if and only if it is a martingale.

The proof of the theorem relies on the following lemma.

Lemma 4.2.

Let denote a –valued semimartingale with independent increments such that for all . Then for all .

Proof.

Proof of Theorem 4.1.

We first prove the assertion in (1). To this end, fix with . Define next the process

| (4.2) |

By Proposition 2.11, we have and by Proposition 2.15, has independent increments. Moreover, by (2.2) and Corollary 2.14 we have that is special if and only if is special. Hence it suffices to argue the equivalence assertion with replaced by .

Assume now that is special. By assumption we also have . Thanks to Theorem 3.1 and Remark 3.4, the process is a non-negative local martingale; in particular, its expectation is bounded by one. By [18, II.4.15–19], is deterministic, we thus have , concluding the proof of the first implication.

Now assume that . First, fix and note that by Lemma 4.2 is the product of two independent random variables, none of which is identically zero. Thus we get

which then yields . Next, define the process

Fix now with and . Then again by the independence of increments we have

hence is a martingale. Denote by the first time jumps by . The process , given by

is a semimartingale uniformly bounded on compacts. In turn, this shows that is special as the product of a martingale and a uniformly bounded on compacts semimartingale. Proposition 3.5 now yields is special, proving the reverse implication in (1). We also note that on paths where by Theorem 3.1, hence for all by Lemma 4.2.

Let us now consider the final assertion in (1), namely (4.1), provided is special. We have already established that then also for all . Consider now the time . Then is deterministic. Independence of increments yields

therefore we have for all . Thus, without loss of generality, we may now just assume that ; in particular, that on . Then Theorem 3.1 and Remark 3.4 yield that is a local martingale. Its absolute value is bounded by

the product of a non-negative martingale and a deterministic semimartingale. This shows that itself is a martingale, yielding the assertion.

For the statement in (2) note that on . Also is special on if and only if is special for all . Then the statement follows from the assertion in (1).

Finally, let us argue (3) and let us assume that is a local martingale. We may assume that is constant after its first jump by , i.e., with . Then is a local martingale; hence for all by [18, I.2.31], yielding . As above, the local martingale is again bounded in absolute value by , the product of a non-negative martingale and a deterministic semimartingale. This yields that is a martingale, concluding the proof. ∎

Corollary 4.3 (Lévy–Khintchin formula).

Fix and assume is an –valued semimartingale with independent increments starting at 0. Then

Furthermore, if is a truncation function for and if is a Lévy process with drift rate (relative to ) and jump measure one obtains

Proof.

Example 4.4 (Mellin transform of a signed stochastic exponential of an –valued process with independent increments).

Fix and for let denote the functions with

The functions and are now extended to in the natural way by considering them to be constant in , , and in the imaginary component. Note that . Moreover, from Propositions 2.6 and 2.7, and Theorem 2.8 we obtain, for and any –valued semimartingale ,

| (4.3) |

yielding

which is a further generalization of (2.9) for real-valued .555In this setting, is defined for any –valued semimartingale but the value of is insensitive to the imaginary part of by construction, so is real-valued for all practical purposes. Observe that one can extend the functions and from to differently to get some action on the imaginary part of . For example, one could set, on , keep the same definition of and , and then extend to by making these functions constant in and . In such case, the first two equalities in (4.3) remain valid for arbitrary –valued and the left-hand side is sensitive to , but the third equality in (4.3) still only works for real-valued . Hence, in the context of this example, it is reasonable to proceed with computations in (4.4) that are specialized to real-valued and no longer hold for arbitrary –valued .

Next, assume that is special for ; for example, this holds when because the jumps of are then bounded. Then, for , Proposition 2.12 yields

| (4.4) |

where we may take . Assume now that has independent increments. An application of Theorem 4.1(2) together with (2.4) and Remark 2.13 yields for that

| (4.5) |

where from (4.4) one has

From now on we shall fix and acknowledge the explicit dependence on by writing and for . Next define

From (4.5) we then have

| (4.6) |

and similarly,

| (4.7) |

Next, define the following two conditional expectations:

We can then compute

provided and . We have now obtained the Fourier transform of the the random variable conditional on . One is thus able to characterize the distribution of via Mellin/Fourier inversion methods; see for example Galambos and Simonelli [14].

Observe also that although the distribution of conditional on corresponds to a strictly positive random variable, it cannot be thought of as a natural exponential of a process with independent increments (except in the trivial case when or , P–almost surely). Hence the characteristic functions and cannot be obtained from the classical Lévy-Khintchin formula or from its generalization for processes with independent increments in [21, Proposition 3.12]. ∎

The next example illustrates the novelty of Example 4.4 in a financial context. Throughout, denotes the drift rate of a special Lévy process .

Example 4.5.

Let be a Lévy process with characteristics , where denotes the cumulative normal distribution with a given mean and variance, respectively. Later we will use the specific numerical values , , , and , which are broadly consistent with the empirical distribution of the logarithmic returns of a well-performing stock. For simplicity we will use a zero risk-free rate.

Financial economics is concerned with optimal portfolio allocation over a period of time, e.g., year. Here we will consider optimality in the sense of mean–variance preferences. It is known that the optimal wealth process in this setting is given by where

see, for example, Proposition 3.6, Lemma 3.7, Corollary 3.20, and Proposition 3.28 in Černý and Kallsen [5]. Note that is the ratio of first and second moment of the arithmetic return of the stock.

In practice, it is useful to know the distribution of the optimal terminal wealth

If the stochastic exponential is strictly positive, which is true in the empirically less important case , this can be done by applying the Lévy-Khintchin formula to the Lévy process

to obtain the characteristic function of the logarithm. In the commonly encountered situation with , the model under investigation (and indeed all named Lévy models used in finance) leads to a signed stochastic exponential. The Lévy–Khintchin formula is thus of no help but Example 4.4 offers a way out.

Keeping the definitions of , , , and from Example 4.4, we start by evaluating

where

Next we obtain from (4.6) and (4.7)

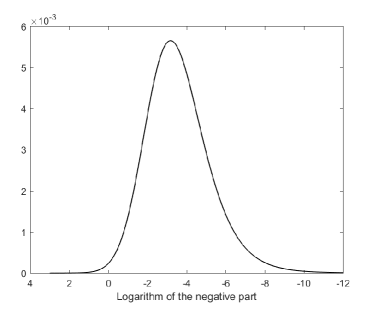

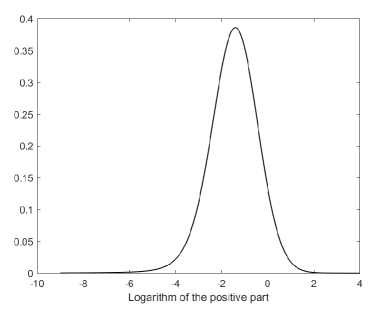

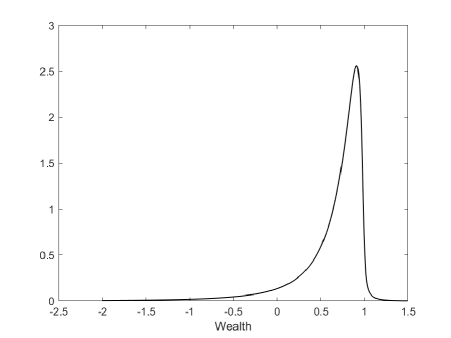

Observe that without fixed jump times one has and with also . In our setting we obtain with representing the probability that the stochastic exponential is negative in year. The conditional characteristic functions are clearly integrable, hence the standard density inversion formula can be applied. Figure 4.1 illustrates the subdensities of the logarithm of the negative and the positive part of the signed stochastic exponential . Figure 4.2 shows the resulting distribution of the terminal wealth on the one-year horizon. ∎

The next example illustrates how, in a general semimartingale model, the drift computation can be performed separately on predictable jump times.

Example 4.6 (Multiplicative compensator calculation with predictable times of jumps).

Let denote a compound Poisson process with rate whose jumps have cumulative distribution function . Denote the jump times of by and set . Let denote an independent special Lévy process with drift rate , variance rate , and jump measure and set . Next, let denote the smallest right-continuous filtration such that is adapted and is –measurable, for each . Then is an –semimartingale and is –predictable, for each . Moreover, its ‘continuous-time component’ is precisely the Lévy process; i.e., . The ‘discrete times’ lie in the set of predictable times of jumps, i.e., .

We now interpret as the logarithmic price of an asset. Maximization of exponential utility calls for the multiplicative compensator of the utility process where is the cumulative yield of investment in asset with price . Due to the presence of jumps at predictable times, the optimal investment strategy will no longer be a constant dollar amount at all times, instead we will have one constant amount, say , on the ‘continuous’ times, i.e., outside , and a different constant amount, say , on the ‘discrete’ time set .

5 Change of measure and its representation

We now discuss how to compute drifts after an absolutely continuous change of measure. Since the collection of null sets of the new measure, say Q, may be larger than that of P, one is compelled to study Q–drifts of processes that a priori are not P–semimartingales. The next proposition addresses this issue by offering a specific way to ‘lift’ Q–semimartingales back up to P. Its proof is provided at the end of this section.

Proposition 5.1.

Remark 5.2.

In view of Proposition 5.1, it entails no loss of generality to assume that a given Q–semimartingale is also a P–semimartingale, at least on the open interval , where is the uniformly integrable martingale denoting the change of measure. This observation is relevant for Proposition 5.3, Theorem 5.4, and Corollaries 5.7, 5.9, and 5.10 below. Example 5.12(i) yields an instance where a Q–semimartingale is explicitly lifted to a P–semimartingale. ∎

We now proceed to formulate a relevant version of Girsanov’s theorem. For a stopping time and a predictable time , we say that process is a semimartingale (resp., a local martingale; special) on if is a semimartingale (resp., a local martingale; special) on .

Proposition 5.3 (Girsanov’s theorem).

Let be a real-valued, non-negative uniformly integrable P–martingale with and define the probability measure Q by . For a P–semimartingale , the following are equivalent.

-

(i)

is Q–special.

-

(ii)

is P–special on .

-

(iii)

is P–special on .

If either condition holds then the compensators corresponding to (i) and (iii) satisfy

| (5.1) |

Furthermore, the following are equivalent.

-

(i’)

is a Q–local martingale.

-

(ii’)

is a P–local martingale on .

-

(iii’)

is a P–local martingale on .

Proof.

We will first argue the equivalence of (i) and (ii) (and (i’) and (ii’), respectively) and then the equivalence of (ii) and (iii) (and (ii’) and (iii’), respectively).

Assume first that (i) holds, i.e., is a local Q–martingale. As in [18, III.3.8] we then have is a local P–martingale on . Since is P–special on , we get (ii). Assume now that (ii) holds, i.e., is a local P–martingale on . Then is a local Q–martingale. Since is Q–special (as the product of the locally bounded process and the Q–local martingale ), so is , which yields (i). Note that the same arguments also yield the equivalence of (i’) and (ii’).

Theorem 5.4 (Drift after a change of measure).

Let be a semimartingale with , special on , and on . Assume that is a real-valued, non-negative uniformly integrable martingale and define the probability measure Q by . For a P–semimartingale , the following are equivalent.

-

(i)

is Q–special.

-

(ii)

is P–special on .

-

(iii)

is P–special on .

If one of these conditions holds, then one has

| (5.2) |

Furthermore, the following are equivalent.

-

(i’)

is a Q–local martingale.

-

(ii’)

is a P–local martingale on .

-

(iii’)

is a P–local martingale on .

Proof.

Example 2.4, Theorem 2.8, (3.2), Proposition 2.5, and Proposition 2.6 give, in this order,

| (5.3) |

By Proposition 5.3, (i) is equivalent to (ii), which in turn is equivalent to being P–special on . By (5.3) and Lemma 4.2 of Shiryaev and Cherny [33], the latter is equivalent to (iii). Proposition 5.3, identity (5.3), and Lemma 4.2 of Shiryaev and Cherny [33] also yield (5.2). The equivalence of (i’)–(iii’) is established similarly. ∎

The following statement is helpful when and are represented in terms of some common process because it delivers the same result as Theorem 5.4 without requiring the joint P–characteristics of and as an input.

Corollary 5.5.

Consider and Q as in Theorem 5.4 and suppose there are compatible with a P–semimartingale such that on and on . Then we have

The next example illustrates the convenience of Theorem 5.4 in a financial context when evaluating characteristic functions under a new measure. Throughout, denotes the drift rate of a special Lévy process .

Example 5.6.

Let be such that is a Lévy process. It is known from, e.g., Bender and Niethammer [3] that under suitable conditions on the characteristics of , the absolutely continuous local martingale measure for whose density has the smallest norm is obtained by setting

where solves

For completeness, we discuss the remaining two Q–characteristics of . The second characteristic remains trivially unchanged. The third characteristic can be obtained from the following corollary. Note that [18, III.3.17] provides an alternative expression to (5.4) below.

Corollary 5.7 (Predictable compensator under the new measure).

Consider and Q as in Theorem 5.4. For a P–semimartingale , we have

| (5.4) |

Proof.

Remark 5.8.

Corollary 5.9 (Multiplicative compensator after a change of measure).

Consider and Q as in Theorem 5.4. Assume is a –valued P–semimartingale and Q–almost surely absorbed in zero if it eve hits zero. Moreover, suppose that is special under Q on and

Then is P–special on and the multiplicative compensator of under Q is given by

Proof.

Corollary 5.10 (Independent increments and change of measure).

Consider and Q as in Theorem 5.4. Assume for some P–semimartingale (hence ). Consider a –valued P–semimartingale and write

Assume that and have jointly independent increments under P. Then is P–special, has independent increments under Q, and the following are equivalent for any time .

-

(i)

.

-

(ii)

is P–special on .

Furthermore, if one of these conditions holds, then

Proof.

By Proposition 3.5, is P–special. Therefore by (2.2),

on paths where , hence for all by Lemma 4.2 since has independent increments. By (2.2) again, is P–special. Thanks to Theorem 5.4 and Corollary 5.7, the Q–characteristics of are deterministic if and have jointly independent increments under P, hence indeed has independent increments under Q by [18, II.4.15–19].

By Theorem 4.1(1), i is equivalent to

-

(i’)

is Q–special on ,

which by Theorem 5.4 is equivalent to

-

2.

is P–special on .

Example 5.11.

Theorem 1.3 in the introduction combines Theorem 5.4 and Corollary 5.9 in a simplified setting. We shall now illustrate the usefulness of Theorem 1.3 on a calculation appearing in [28]. Take as in Theorem 1.3. In addition, assume is a local P–martingale, i.e., , and is P–special. The implication from (iii) to (i) in Theorem 1.3 with now yields that is Q–special with compensator . Next, fix some and observe that is P–special, hence is Q–special by the implication from (ii) to (i) in Theorem 1.3. Now (2.10) yields

which by Jensen’s inequality is a local Q–submartingale; hence its Q–multiplicative compensator is non-decreasing. By the implication from (i’) to (ii’) in Theorem 1.3, this Q–multiplicative compensator coincides with the P–multiplicative compensator of

hence by Theorem 1.2 the Q–multiplicative compensator equals

The non-decreasing property deduced earlier now yields

which is the statement of a key inequality in [28, Lemma III.4, Equation (3.4)].∎

We conclude with an explicit example of drift calculation after a non-equivalent change of measure where is allowed to attain zero continuously.

Example 5.12.

Let and Q be as in Theorem 5.4. We shall compute the Q–drift of two Q–semimartingales, and .

-

(i)

We first consider the Q–semimartingale . Proposition 2.9 yields the representation

where we use to emphasize that this representation only holds under Q. The lifted version of from Proposition 5.1 reads

Then Corollary 5.5 with and yields

Q–almost surely. In particular, if is a uniformly integrable martingale, then and

-

(ii)

Let us now consider a second example in this setup. Assume that and consider the process

Note that is a P–semimartingale. Corollary 5.5 with and yields

where we have used . In particular, if is a uniformly integrable martingale, then and

∎

We conclude this section with a proof of Proposition 5.1.

Proof of Proposition 5.1.

By localization, we may and shall assume, without loss of generality, that .

Consider the process

Note that is a Q–semimartingale, Q–indistinguishable from , since . Define the two processes and by , , and for all . Then and are predictable. Hence, the first time that fails to be left-continuous, namely the first time when does not equal or is not real-valued, is a predictable time. Note that

since is a Q–semimartingale and hence . Moreover, since is constant on the interval , we have on , P–almost surely. Since is predictable, by [18, I.2.31] we have

Since on , this yields ; hence we have . This shows that is P–almost surely left-continuous; in particular, exists on and .

We also note that has right-continuous paths. Indeed, we use again, but now to denote the first time that fails to be right-continuous. Then is a stopping time. As above, since is a Q–semimartingale we have . Since is constant after time , we indeed have , yielding that has right-continuous paths with left limits, P–almost surely.

The Q–semimartingale can be written as the sum of a Q–local martingale and a Q–semimartingale that is Q–almost surely of finite variation. To show the proposition, it now suffices to argue that their corresponding lifts and are P–semimartingales.

Let us first consider . Denote by the first time that is of infinite variation. Then is a predictable time. Using the same arguments as above we can argue that , P–almost surely, then that on , P–almost surely, and then that indeed , P–almost surely. Thus, is right-continuous with left limits, and P–almost surely of finite variation, hence is a P–semimartingale.

Finally, let us consider , which is Q–indistinguishable from . Let denote a localization sequence so that is a Q–martingale and , Q–almost surely. Without loss of generality, we may assume that , P–almost surely. Next, let us define the stopping times

Then for all since . Hence is again a localization sequence for the Q–local martingale . Moreover, the limit exists and satisfies on , P–almost surely; hence for each . Therefore is P–almost surely equal to a predictable time and as above we have again . Now [18, III.3.8c] yields that is a P–local martingale. Dividing this process by the strictly positive P–semimartingale and adding the finite-variation process yields that is a P–semimartingale as claimed. ∎

6 Concluding remarks

We have presented the computation of (i) multiplicative compensators; and (ii) additive and multiplicative compensators under a new measure obtained by the multiplicative compensation of a given non-negative semimartingale. In Theorems 3.1 and 5.4 we have treated these tasks as problems in their own right.

In practice, the inputs to these computations are likely to come with more structure than indicated in the two theorems, i.e., the input processes and in Theorems 3.1 and 5.4 will typically be represented with respect to some common underlying, possibly multivariate, process, say . This is illustrated in Examples 3.6, 3.7, 4.5, and 5.6, and Corollary 5.5, respectively.

One should observe that here one may use the more general class of representing functions that are specific to ; see [8, Definition 3.2]. This is possible because a composition of a function in with a compatible element of remains in ; see [8, Corollary 3.20]. For instance, this observation allows the use of general integrands in Example 3.6.

Acknowledgements

We thank Jan Kallsen, Johannes Muhle-Karbe, two anonymous referees, and an associate editor for helpful comments.

References

- [1] A. Aksamit and M. Jeanblanc, Enlargement of Filtration with Finance in View, SpringerBriefs in Quantitative Finance, Springer, Cham, 2017. MR3729407

- [2] J. Azéma, Représentation multiplicative d’une surmartingale bornée, Z. Wahrscheinlichkeitstheorie verw. Gebiete 45 (1978), no. 3, 191–211. MR510025

- [3] C. Bender and C. R. Niethammer, On -optimal martingale measures in exponential Lévy models, Finance Stoch. 12 (2008), no. 3, 381–410. MR2410843

- [4] P. Carr, T. Fisher, and J. Ruf, On the hedging of options on exploding exchange rates, Finance Stoch. 18 (2014), no. 1, 115–144. MR3146489

- [5] A. Černý and J. Kallsen, On the structure of general mean–variance hedging strategies, Ann. Probab. 35 (2007), no. 4, 1479–1531. MR2330978

- [6] A. Černý and J. Ruf, Pure-jump semimartingales, Bernoulli 27 (2021), no. 4, 2624–2648. MR4303898

- [7] A. Černý and J. Ruf, Simplified stochastic calculus with applications in Economics and Finance, European J. Oper. Res. 293 (2021), no. 2, 547–560. MR4241583

- [8] A. Černý and J. Ruf, Simplified stochastic calculus via semimartingale representations, Electron. J. Probab. 27 (2022), 1–32, Paper No. 3. MR4362774

- [9] Z.-Q. Chen, P. J. Fitzsimmons, M. Takeda, J. Ying, and T.-S. Zhang, Absolute continuity of symmetric Markov processes, Ann. Probab. 32 (2004), no. 3, 2067–2098. MR2073186

- [10] R. Cont and P. Tankov, Financial Modelling with Jump Processes, Chapman & Hall/CRC Financial Mathematics Series, Chapman & Hall/CRC, Boca Raton, FL, 2004. MR2042661

- [11] C. Doléans-Dade, Quelques applications de la formule de changement de variables pour les semimartingales, Z. Wahrscheinlichkeitstheorie verw. Gebiete 16 (1970), 181–194. MR283883

- [12] E. Eberlein, A. Papapantoleon, and A. N. Shiryaev, Esscher transform and the duality principle for multidimensional semimartingales, Ann. Appl. Probab. 19 (2009), no. 5, 1944–1971. MR2569813

- [13] M. Émery, Stabilité des solutions des équations différentielles stochastiques application aux intégrales multiplicatives stochastiques, Z. Wahrscheinlichkeitstheorie verw. Gebiete 41 (1978), no. 3, 241–262. MR0464400

- [14] J. Galambos and I. Simonelli, Products of Random Variables, Monographs and Textbooks in Pure and Applied Mathematics, vol. 268, Marcel Dekker, Inc., New York, 2004. MR2077249

- [15] T. Goll and L. Rüschendorf, Minimax and minimal distance martingale measures and their relationship to portfolio optimization, Finance Stoch. 5 (2001), no. 4, 557–581. MR1862002

- [16] K. Itô and S. Watanabe, Transformation of Markov processes by multiplicative functionals, Ann. Inst. Fourier (Grenoble) 15 (1965), no. 1, 13–30. MR0184282

- [17] J. Jacod, Projection prévisible et décomposition multiplicative d’une semi-martingale positive, Séminaire de Probabilités, XII, Lecture Notes in Math., vol. 649, Springer, Berlin, 1978, pp. 22–34. MR519990

- [18] J. Jacod and A. N. Shiryaev, Limit Theorems for Stochastic Processes, 2nd ed., Comprehensive Studies in Mathematics, vol. 288, Springer, Berlin, 2003. MR1943877

- [19] M. Jeanblanc, S. Klöppel, and Y. Miyahara, Minimal -martingale measures of exponential Lévy processes, Ann. Appl. Probab. 17 (2007), no. 5-6, 1615–1638. MR2358636

- [20] Y. M. Kabanov, R. S. Liptser, and A. N. Shiryaev, On the variation distance for probability measures defined on a filtered space, Probab. Theory Related Fields 71 (1986), no. 1, 19–35. MR814659

- [21] J. Kallsen and J. Muhle-Karbe, Exponentially affine martingales, affine measure changes and exponential moments of affine processes, Stochastic Process. Appl. 120 (2010), no. 2, 163–181. MR2576885

- [22] J. Kallsen and A. N. Shiryaev, The cumulant process and Esscher’s change of measure, Finance Stoch. 6 (2002), no. 4, 397–428. MR1932378

- [23] C. Kardaras, On the stochastic behaviour of optional processes up to random times, Ann. Appl. Probab. 25 (2015), no. 2, 429–464. MR3313744

- [24] C. Kardaras and J. Ruf, Filtration shrinkage, the structure of deflators, and failure of market completeness, Finance Stoch. 24 (2020), no. 4, 871–901. MR3098435

- [25] N. Kazi-Tani, D. Possamaï, and C. Zhou, Second-order BSDEs with jumps: Formulation and uniqueness, Ann. Appl. Probab. 25 (2015), no. 5, 2867–2908. MR3375890

- [26] M. Larsson and J. Ruf, Stochastic exponentials and logarithms on stochastic intervals—A survey, J. Math. Anal. Appl. 476 (2019), no. 1, 2–12. MR3944415

- [27] M. Larsson and J. Ruf, Convergence of local supermartingales, Ann. Inst. H. Poincaré Probab. Stat. 56 (2020), no. 4, 2774–2791. MR4164856

- [28] D. Lépingle and J. Mémin, Sur l’intégrabilité uniforme des martingales exponentielles, Z. Wahrscheinlichkeitstheorie verw. Gebiete 42 (1978), no. 3, 175–203. MR489492

- [29] J. Mémin, Décompositions multiplicatives de semimartingales exponentielles et applications, Séminaire de Probabilités, XII, Lecture Notes in Math., vol. 649, Springer, Berlin, 1978, pp. 35–46. MR519991

- [30] A. Nikeghbali and M. Yor, Doob’s maximal identity, multiplicative decompositions and enlargements of filtrations, Illinois J. Math. 50 (2006), no. 1-4, 791–814. MR2247846

- [31] N. Perkowski and J. Ruf, Supermartingales as Radon-Nikodym densities and related measure extensions, Ann. Probab. 43 (2015), no. 6, 3133–3176. MR3433578

- [32] J. Ruf, A new proof for the conditions of Novikov and Kazamaki, Stochastic Process. Appl. 123 (2013), no. 2, 404–421. MR3003357

- [33] A. N. Shiryaev and A. S. Cherny, A vector stochastic integral and the fundamental theorem of asset pricing, Proc. Steklov Inst. Math. 237 (2002), 6–49. MR1975582

- [34] C. Yoeurp and P. A. Meyer, Sur la décomposition multiplicative des sousmartingales positives, Séminaire de Probabilités, X, Lecture Notes in Math., vol. 511, Springer, Berlin, 1976, pp. 501–504. MR0448545