Bayesian Changepoint Analysis

Tobias Siems

Department of Mathematics and Computer Science

University of Greifswald

A thesis submitted for the degree of

Doctor of Natural Sciences

October 25, 2019

1 The changepoint universe (a poetic view)

Changepoint problems unite three worlds: the world of counting, the world of placement and the world of change. These worlds constitute universes, which receive their rough shape from statistical models applied to data and are further refined through parameters.

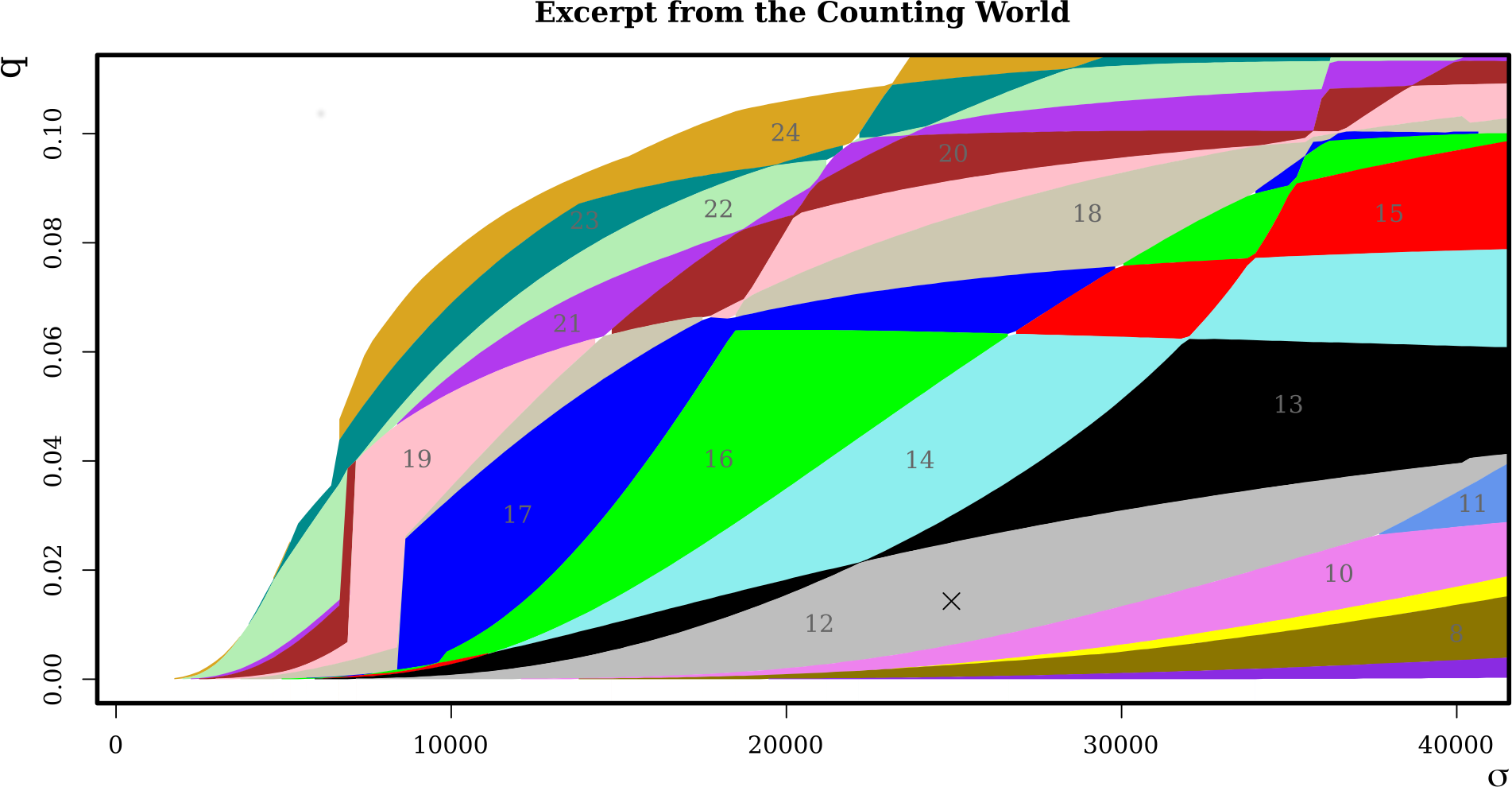

Even though the defining elements of such universes are grasped so quickly, we can never fully understand them as a composite whole. Like a physicist, we need to rely on lenses revealing tiny pictures of the incredible truth, such as the astonishing glimpse into the counting world unveiled by Figure 1.

This thesis gives you the unique opportunity to gain an understanding of the fantastic scale of Bayesian changepoint universes. To this end, we will look through a range of enlightening lenses, forged in the mighty fires of mathematics and operated on a highly sophisticated calculator, to discover places no one has known before.

2 Introduction

Changepoint analysis deals with time series where certain characteristics undergo occasional changes. Having observed such a time series, the latent changepoint process can be investigated in various ways. The following four examples provide an insight into the tasks that may arise in practice.

The examination of ion channels is a popular example for changepoint analysis. Ion channels are proteins and part of the cell membrane. Their purpose is to control the flow of ions, like potassium, into and out of the cell. New drugs must pass extensive tests for ion channel activity (Camerino et al., 2007). Depending on the type of the channel, they can be activated and deactivated through chemical reactions or electrical currents.

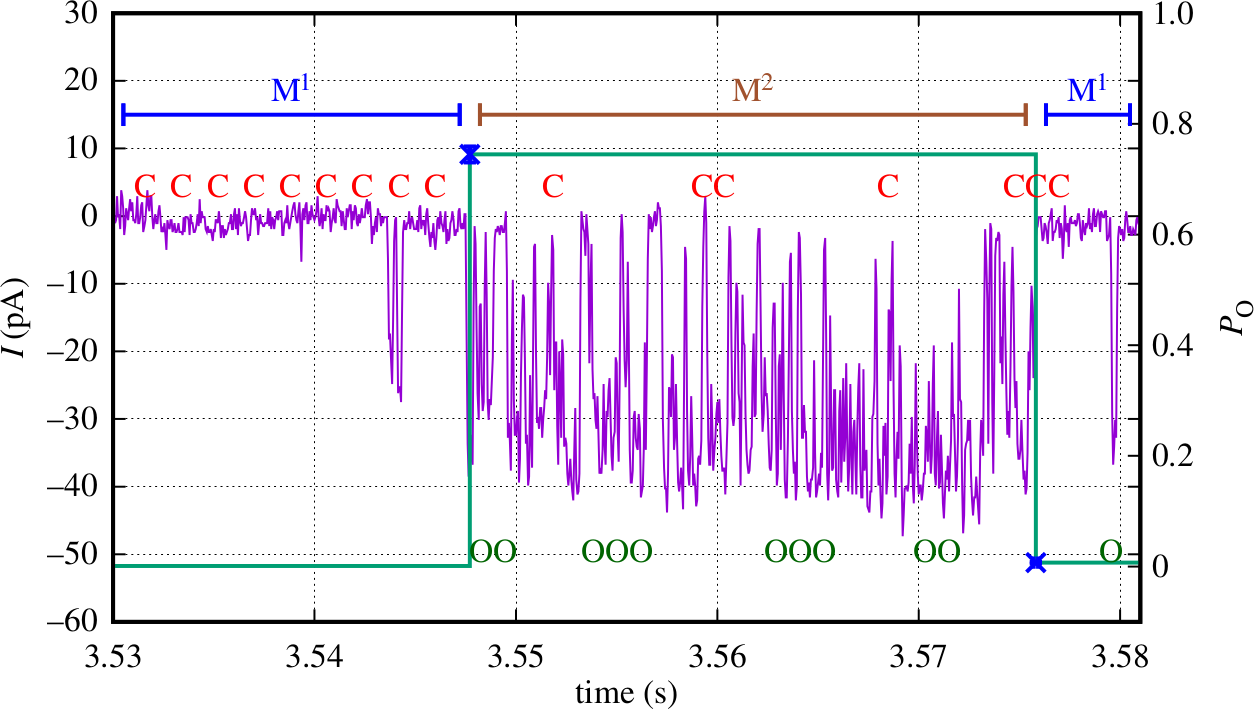

A Nobel prize wining technique to gather data from single ion channels is the patch clamp technique (Sakmann and Neher, 1984). It allows to record the electrical current that is generated by the flow of ions. Figure 2 shows a data set gathered from an inositol trisphosphate receptor, which controls the flow of calcium ions (Siekmann et al., 2016). The purple lines represent the measured currents, the C’s and O’s mark the times where the channel was closed or opened, respectively. This is called gating and can be understood as a changepoint process. However, there is a second superordinate changepoint process indicated by and . It models the modes of the channel’s activity.

These modes reflect the stochastic nature of how the cell controls the flow of ions. Thus, it is of high interest to find and understand the possible modes an ion channel takes. Each mode can be represented through a time continuous Markov chain that describes its gating behavior (Siekmann et al., 2016). The transitions between the modes may again be modeled as a Markov chain leading to a hierarchical model. A challenging problem hereby is the amount of quantities which are to be estimated in order to determine the model and the associated non-identifiability. Inference in these models may be drawn by means of approximate sampling through Markov chain Monte Carlo (MCMC) (Siekmann et al., 2011; Siekmann et al., 2012, 2014; Siekmann et al., 2016).

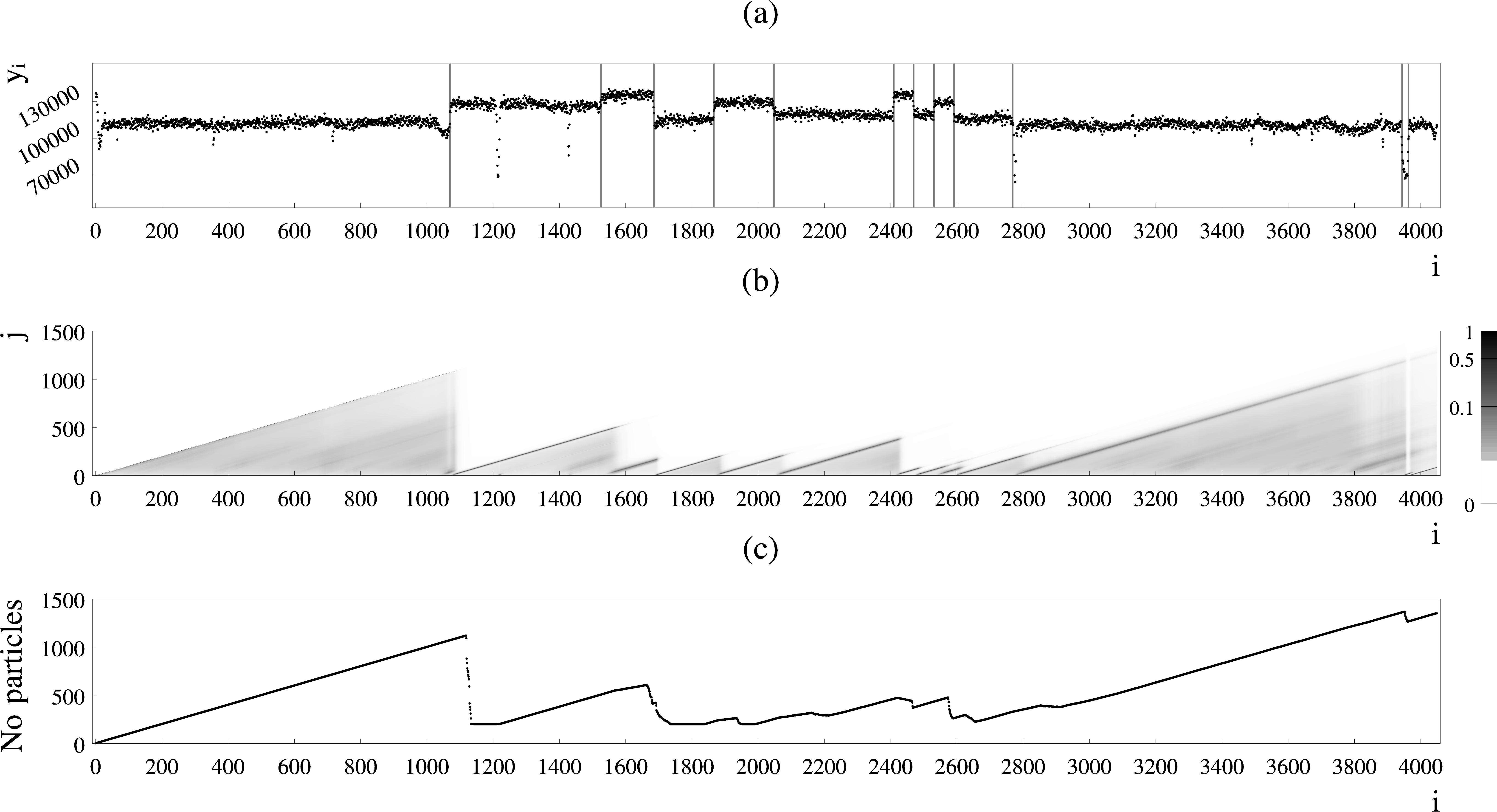

A different example for changepoint analysis, which arises in geology, is the well-log drilling data in Figure 3. It shows the nuclear-magnetic response of underground rocks (Fearnhead, 2006).

In order to build a changepoint model here, we may regard coherent parts of the data as noisy versions of one and the same state and allow these states to change occasionally. This can be understood as a change in location problem whereby the states are interpreted as the location parameter of the datapoints, e.g. median or mean. Sequences of related datapoints are then considered to stem from the same material.

Interestingly, there are challenging perturbations in form of heavy outliers and smaller abrupt, but also gradual location changes. These irregularities are prone to be confused with the desired location changes, which gives rise to robust changepoint inference (Fearnhead, 2006; Fearnhead and Rigaill, 2019; Weinmann et al., 2015). The task here is to maintain a good balance between sensitivity and specificity.

This exciting data set serves as the main demonstration example throughout this thesis.

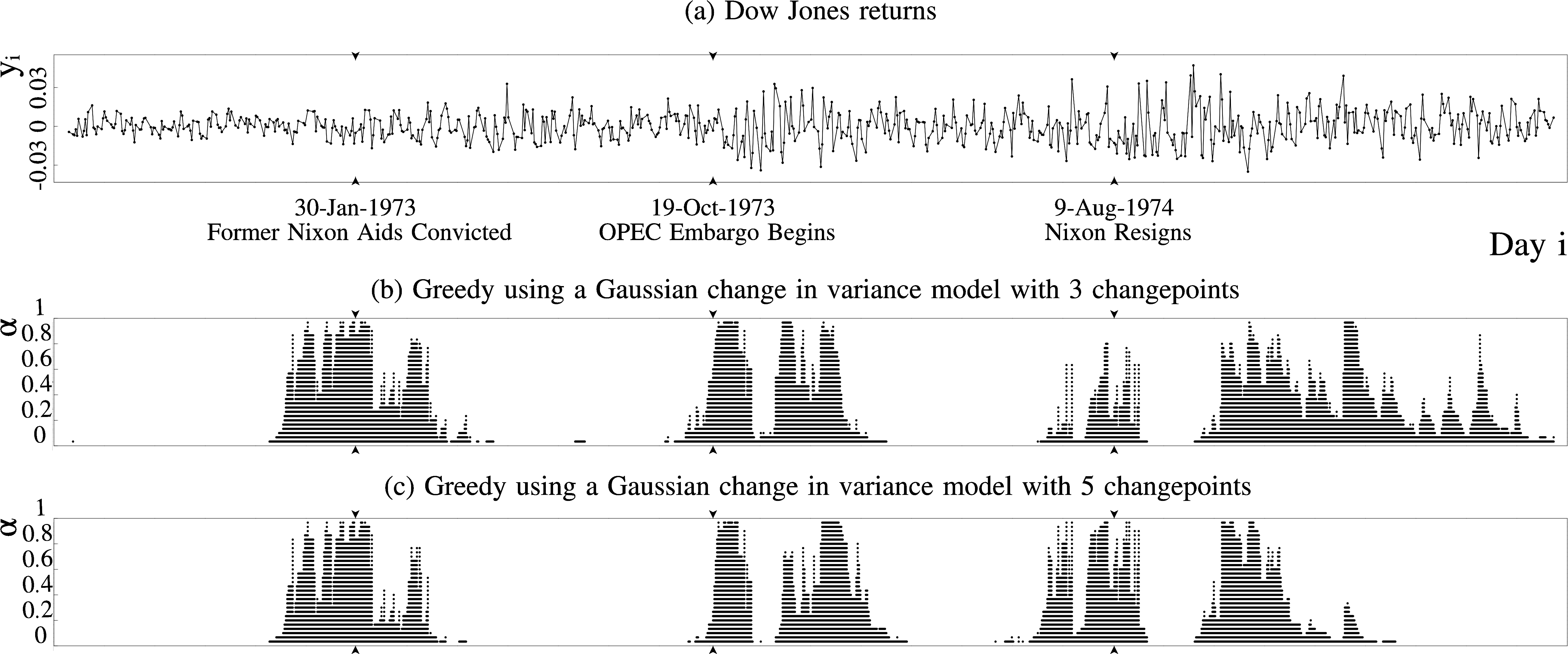

Stock markets pose another important changepoint application. Consider for example Figure 4. It depicts daily Dow Jones returns observed between 1972 and 1975 (Adams and MacKay, 2007) and highlights three events on January 1973, October 1973 and August 1974.

This can be understood as a change in variation problem, whereby the data is split into regions of similar spread. Changepoint analysis may be used for a real time detection of high risk or to understand the effect of political decisions on the economy.

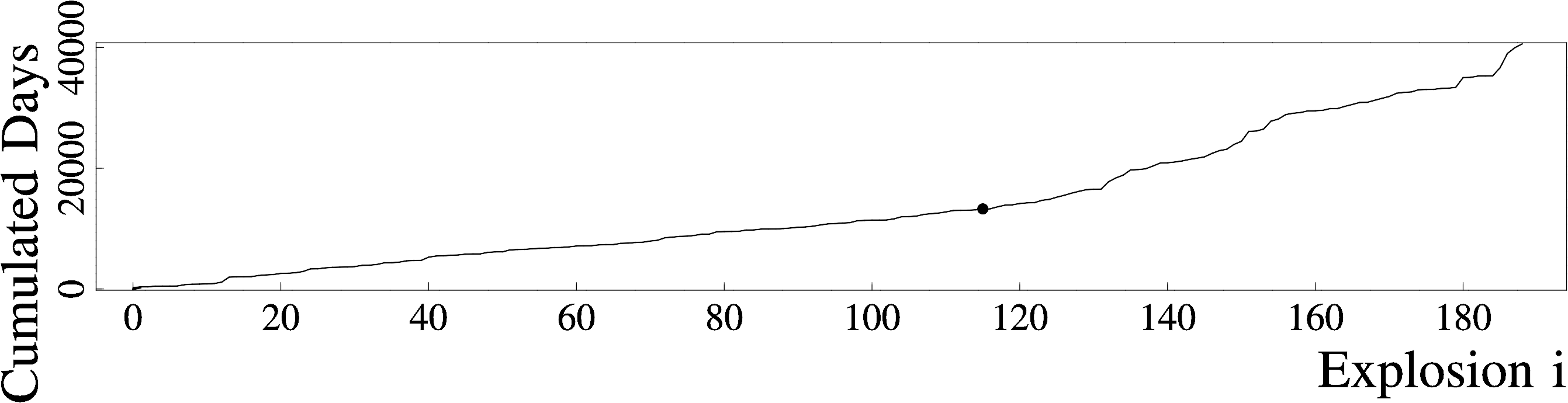

Our last example concerns coal mine explosions between March 15, 1851 and March 22, 1962 that killed ten or more people. Figure 5 counts up the days from one explosion to the next. The black dot points to the Coal Mines Regulations Act in 1887, which also roughly marks a change in the period of time it took from one explosion to the next.

In a changepoint approach, the days between consecutive explosions could be modeled as geometrically distributed and changes in success rate would be examined. The task here is to elaborate the effect of the regulations act by detecting or rejecting one single change. This kind of single changepoint approach can be applied to a large variety of applications where we expose if something has generally changed.

For the time being, this should be enough to motivate changepoint analysis. However, for further elaborations of different changepoint approaches see, for example, Eckley et al. (2011).

2.1 Time series, segmentations and changepoints

Time series are ordered sequences of data. This order can, for example, account for successive loci on a DNA sequence or indeed the times the observations were made and allows us to speak of segmentations.

Let be a set and be a time series with indexes . Any sequence, with , of successive datapoints is considered as a segment with segment length . A segmentation of is a collection of non-overlapping segments that covers as a whole.

A segmentation is uniquely determined by a number and a sequence of successive indexes as follows

whereby indicates that the whole time series corresponds to one segment. In the context of changepoints, represents the number of changepoints and the are the changepoint locations or simply changepoints. For now, changepoints at timepoint one are excluded. However, this will be relaxed later on.

As mentioned earlier, the segmentation features changes in certain characteristics of the time series, e.g. location or scale. These characteristics are expressed through parameters, the so-called segment heights that take values within a set, say . Consequently, we assign each segment of a segmentation a value within . In practice, a change in segment height typically triggers a changepoint.

In non-trivial cases, the segment heights are latent and algorithms for finding changepoints in a time series trace possible timepoints where they change their value. In doing so, they strive for persistency but also selectivity or as the statistician would put it, they govern a trade-off between specificity and sensitivity. While a too high sensitivity yields too many changepoints overfitting the segmentation to the data, a too high specificity disregards valuable changepoints and impairs the changepoint detection.

The existing literature captures approaches to detect at most one changepoint as well as multiple changepoints. Even though single changepoint methods can be applied recursively to detect multiple changepoints (Fryzlewicz et al., 2014), in this thesis, we focus solely on techniques that surmise multiple changepoints in the first place.

2.2 Changepoint estimation via minimizing a penalized cost

A natural approach for finding multiple changepoints in a time series is to assign each segmentation a rating and then select one of the best ones. This rating should express the goodness of fit, but also regularize the number of changepoints to avoid overfitting. However, instead of speaking about goodness of fit and regularization, it is common to use opposite terms like cost and penalization. Thus, changepoints are inferred by minimizing a penalized cost.

For the sake of computational convenience, the costs and penalizations are often defined individually for the segments instead of the whole segmentation at once. This can be achieved through a segmental cost and a penalization constant . For the time being, we may ignore the segment heights.

Minimizing the penalized cost then yields the optimization problem which finds one element of

| (1) |

This can be solved through a Viterbi algorithm (Viterbi, 1967), also known as Bellman recursion (Bellman, 1966) or dynamic programming. In oversimplified terms, the algorithm performs a forward search from 1 to , whereby in each iteration it performs a backward search in order to evaluate a best candidate for the most recent changepoint prior to . Subject to the condition that can be augmented by new observations in constant time, i.e. can be derived from in constant time for all , this yields a space and time complexity of . A long series of papers explains this algorithm in detail (see for example Jackson et al. (2005); Friedrich et al. (2008) and Killick et al. (2012)).

Furthermore, an approach developed by Friedrich et al. (2008) computes solutions to (1) for all possible at once. It does so, by exploiting the linearity of the penalized cost w.r.t. . Almost identical ideas are provided by Haynes et al. (2017).

A discovery that earned considerable popularity is described in Killick et al. (2012). It allows under some circumstances to reduce the expected space and time complexity of solving (1) to . We briefly discuss the idea behind it.

Assume that for any sequence and . This makes sense, because splitting a segment usually results in a tighter fit and thus a lower cost. Let further be a solution to (1) w.r.t. , i.e.

If for we get , we can take an arbitrary and get

This states that placing the most recent changepoint prior to at , is at least as good as placing it at . Thus, we may skip in any backward search past . An implementation of the corresponding algorithm called PELT, can be found in the R-Package changepoint (Killick et al., 2012).

The starting point for setting up the segmental cost is usually another function , which takes the data within a segment and the segment height. can, for example, be derived as the negative loglikelihood of a statistical model. However, M-estimators are also viable (Friedrich et al., 2008; Fearnhead and Rigaill, 2019).

We may put directly into (1) and additionally minimize over the individual segment heights or equivalently, use . The solution can then be interpreted as a piecewise constant function with values corresponding to the optimal segment heights. Consequently, we can speak of a regression method here.

In contrast, the Bayesian statistician may integrate over the segment heights in order to get rid of them completely. This involves a more complex approach since we need to put a prior on the segment heights and perform an integration for each considered segment.

2.3 Bayesian changepoint models

By applying priors, we pave the way for an interpretation of segmentations as random. This allows for the treatment of the data, changepoints and segment heights within the same methodological realm of stochastics. As a result, a more complex modeling approach is required here.

To begin with, the changepoints are represented by continuous or discrete random times, over . The changepoint process starts at a certain timepoint, say , whereby the first changepoint is , the second and so forth. Consequently, represents the length of the -th segment.

Furthermore, the segment heights are modeled accordingly through a family of random variables over a measurable space , whereby represents the -th segment height. Finally, the observations constitute a family over a measurable space . Each observation was measured at a timepoint , whereby .

An in some ways minimal requirement for a statistical model to be expedient, is the feasibility of its likelihood. This enables the use of MCMC techniques like Metropolis-Hastings and thus, pioneers an abundance of inference strategies. However, before we can set up the likelihood, we need to consider an issue that typically results from the data collection.

In practice, often remains unknown. It is thus reasonable to build the changepoint model solely within . Consequently, we interpret the first segment as a clipped random length with a yet to be determined distribution. Given the first changepoint within , the second segment length will follow the same distribution as the ’s and so forth. As soon as a segment exceeds the process ends irrespective of its concrete length.

We may account for the lack of knowledge about by considering the limit . To this end, assume that is a renewal process (Doob, 1948) and independent of all other random variables within the changepoint model. Renewal theory (Lawrance, 1973) teaches us that the distribution of the random length from to the first changepoint exhibits the density w.r.t. the Lebesgue measure. These partial lengths are referred to as residual times or forward recurrence times.

The case where turns out to be more challenging since the distribution of the residual times now depends on , and can be very difficult to compute especially in the continuous case.

There are two important exceptions here. The residual times of an exponential renewal process are independent of and correspond to the same exponential distribution again. Similarly, for a geometric renewal process that exhibits changepoints only on a known discrete grid, we can again take the same geometric distribution for the residual times.

A similar issue arises with the segment heights. A not too restrictive assumption is that is described by a Markov chain. If , related theory may be applicable to derive the distribution of the segment height of the segment that contains .

Having considered this, we can now set up the joint likelihood of the data, changepoint locations and segment heights in order to use MCMC methods like Metropolis-Hastings to perform approximate inference.

2.4 The purpose of this thesis and its structure

In this thesis, we elaborate upon Bayesian changepoint analysis, whereby our focus is on three big topics: approximate sampling via MCMC, exact inference and uncertainty quantification. Besides, modeling matters are discussed in an ongoing fashion. Our findings are underpinned through several changepoint examples with a focus on the aforementioned well-log drilling data.

In the following, you find four strongly interrelated, but also widely self-contained sections. While Section 3 provides an understanding of the mathematical foundations of MCMC sampling, Section 4 considers the Metropolis-Hastings algorithm particularly for changepoint related scenarios. Both sections do not intend to develop completely new methods. Instead, Section 3 explains important convergence theorems and gives very basic and simple proofs. Furthermore, our elaboration of the Metropolis-Hastings algorithm aims at clarifying the apparently difficult topic of sampling within mixtures of spaces.

Section 5 talks extensively about exact inference in Bayesian changepoint models with independence induced by changepoints. It develops the bulk of existing algorithms, like exact sampling, and builds novel, very efficient algorithms for pointwise inference and an EM algorithm. At the same time, new scopes for applying approximate changepoint samples are opened up.

Finally, Section 6 develops a notion of credible regions for multiple changepoint locations. They are built from either exact or approximate changepoint samples and illustrated by a new type of plot. This plot greatly facilitates uncertainty quantification, model selection and changepoint analysis. The implementation of our credible regions gives rise to a novel NP-complete optimization problem, which is approached either exactly by solving an ILP or through a fast and accurate greedy heuristic.

The Sections 4 and 6 begin with an outline to summarize their purposes. Besides, each of the following four sections provides an introductory part, which puts its topic into context with existing research and further clarifies the actual subject. Sections 4, 5 and 6 conclude with a discussion. Section 7 concludes this whole thesis with final remarks.

Section 8 lists related papers that I co-authored and considerable contributions of other researchers to this thesis.

References to the supplementary material can be found in Section A. Section B contains the appendix. At the very end, we provide lists of symbols, figures, tables, pseudocodes and references.

3 Markov chain Monte Carlo on finite state spaces

In this section, we elaborate the idea behind Markov chain Monte Carlo (MCMC) methods in a mathematically coherent, yet simple and understandable way. Therefore, we prove a pivotal convergence theorem for finite Markov chains and a minimal version of the Perron-Frobenius theorem. Only very basic knowledge about matrices, convergence of real sequences and probability theory is required here. A convenient summary of analogues results for general state spaces can be found in Tierney (1994).

MCMC techniques aim at drawing samples from prespecified distributions. They do so in an indirect, approximate fashion through Markov chains. This is important since the distributions deployed in practice are often too complex to be dealt with directly or even unavailable in closed form.

There exists a tremendous number of scientific articles and books about MCMC. See, for example, Bishop and Mitchell (2014) for a vivid and more comprehensive introduction without mathematical proofs.

Let be a probability distribution over a finite state space and the probability of state under . By virtue of the strong law of large numbers, independent samples from (so-called i.i.d. samples) can be used universally to approximate expectations w.r.t. . Thus, for a set of such samples, say , and an arbitrary function , we get that . This simple recipe poses one of the most powerful tools in statistics.

An example for is the indicator function for events . It is one if the condition in the brackets is true and zero otherwise. Its expectation yields the probability of .

A Markov chain over is defined through an (arbitrary) initial state and a transition kernel . is a non-negative function over such that for all . can be interpreted as a conditional distribution.

The Markov chain starts in state and evolves according to in an iterative fashion: the distribution of the first link in the chain is and given the first link, say , the distribution of the second link is and so forth. This results in a potentially infinite sequence of random variables , whereby represents the -th link in the chain. Consequently, we get that for and .

Later on, we will deal with the (unconditional) distributions of the -th links. To this end, w.l.o.g. we assume that . Therewith, we describe as a matrix in and as a column vector in . Any such quadratic matrix with non-negative entries and rows that sum to one is called stochastic matrix. Therewith, , i.e. the -fold matrix product of evaluated at and . A further generalization is to set the law of to an arbitrary distribution . This yields , whereby the indicates transposition.

We say that a distribution is an invariant distribution of if . Thus, transitioning according to doesn’t affect . Once a link in a Markov chain with transition kernel follows the law , all subsequent links will do likewise. In this case, the chain is considered to be in equilibrium. Equilibrium can be enforced by setting the distribution of to , but it may also be reached (approximately) in the long run through convergence.

The foundation of MCMC sampling is that under some circumstances the distributions of the -th links of a Markov chain converge towards an invariant distribution regardless of the initial state. Thus, by simulating such a chain until equilibrium is reached sufficiently, we may obtain an approximate sample of this invariant distribution. On these grounds, MCMC methods provide schemes to build Markov chains with a predefined unique invariant distribution.

3.1 Convergence towards and existence of invariant distributions

This section first considers the convergence of the distributions of the -th links of certain Markov chains. This convergence forms the very basis of MCMC sampling. Afterwards, we provide a version of the Perron-Frobenius theorem, which gives further insights into the existence of invariant distributions. The following two properties of play a fundamental role.

is called irreducible if for every there exists an such that . Thus, regardless of the state the Markov chain starts in, every state can eventually be reached with positive probability.

is called aperiodic if there exists an such that for all and all . Thus, regardless of the state the Markov chain starts in, in the long run, it can always reach any state in one step with positive probability.

The name irreducible suggests that the Markov chain does not divide into separate, mutually inaccessible classes. In turn, aperiodicity excludes the case where parts of are reached in a periodic fashion, for example, only through either an even or odd number of transitions. Aperiodicity implies irreducibility, but not vice versa.

It is obvious that a periodic behavior may impede convergence of the distributions of the -th links. For a general convergence theorem, aperiodicity is thus a necessary condition. We will now see that it is also sufficient. The following theorem is a simplified version of a convergence theorem for Markov chains over countable state spaces provided inter alia by Koenig (2005).

Theorem 1.

For an aperiodic stochastic matrix with invariant distribution , we get that for all .

Proof.

Assume that is a Markov chain with transition kernel that starts with an arbitrary but fixed state . Furthermore, consider the Markov chain with transition kernel and initial distribution , i.e. for all . and are supposed to be independent of each other.

Let be the random variable that represents the first where and equal, i.e. . We want to show that is finite with probability one. Due to the aperiodicity of , we may choose an such that has solely positive entries. Let be the smallest entry of and consider that

Define further . The Markov chain starts with copying and switches to as soon as both equal the first time. We are interested in the distribution of . To this end, consider an arbitrary path , define for and observe that

whereby we used that . This shows that is a Markov chain with transition kernel and initial state .

Altogether, we may state that

and for all . ∎

Given a distribution , MCMC methods seek an aperiodic transition kernel with invariant distribution . Thus, it is possible to sample approximately from by simulating a Markov chain with transition kernel until equilibrium is reached to a sufficient extend. The last link within this chain is then taken as a single approximate sample from . In particular, this procedure is independent of the state the Markov chain has started in. The pace by which equilibrium is approached is referred to as the mixing time.

Now, we consider a version of the well-known Perron-Frobenius theorem (Frobenius, 1912). It is usually stated in a more general context and corresponding proofs can be fairly complicated. In turn, we provide our own convenient proof based on simple arithmetics and matrix algebra.

Theorem 2 (Perron-Frobenius Theorem).

An irreducible transition kernel has a unique invariant distribution .

Proof.

Since any stochastic matrix has a right eigenvector with corresponding eigenvalue 1, it also has such a left eigenvector. In particular, any such left 1-eigenvector exhibits non-zero elements. Let be a left 1-eigenvector of . If has only non-negative or non-positive entries, we can immediately derive an invariant distribution of through normalizing , i.e. .

Assume now that exhibits positive entries for and negative entries for . The following applies

| (2) |

Hence, the l.h.s and r.h.s. of (2) have to be zero, which implies that for all and . Consequently, for all , and .

Since the existence of positive and negative entries implies reducibility, we conclude that irreducibility implies that any left 1-eigenvector has either solely non-positive or non-negative entries. Thus, an irreducible transition kernel exhibits at least one invariant distribution .

Finally, assume that there is a second invariant distribution . In order to represent a distribution, not all components of can be either larger or smaller than the components of . Thus, must have positive and negative entries. However, is a left 1-eigenvector of and thus, can’t be irreducible, which contradicts the existence of . ∎

The Perron-Frobenius theorem shows that invariant distributions can certainly be found for an abundance of stochastic matrices, especially for aperiodic ones. In the context of MCMC, it is, however, only a nice-to-have result and not utterly necessary. In fact, there is great freedom in choosing aperiodic transition kernels that exhibit a prespecified invariant distribution and each MCMC method provides its very own approach to do so.

4 A note on the Metropolis-Hastings acceptance probabilities for mixture spaces

4.1 Outline

This work is driven by the ubiquitous dissent over the abilities and contributions of the Metropolis-Hastings and reversible jump algorithm within the context of transdimensional sampling. In a mathematically coherent and at times somewhat journalistic elaboration, we aim to demystify this topic by taking a deeper look into the implementation of Metropolis-Hastings acceptance probabilities with regard to general mixture spaces.

Whilst unspectacular from a theoretical point of view, mixture spaces gave rise to challenging demands concerning their effective exploration. An often applied but not extensively studied tool for transitioning between distinct spaces are so-called translation functions.

We give an enlightening treatment of this topic that yields a generalization of the reversible jump algorithm and unveil a further important translation technique. Furthermore, by reconsidering the well-known Metropolis-within-Gibbs paradigm, we come across a dual strategy to develop Metropolis-Hastings sampler. We underpin our findings and compare the performances of our approaches by means of a changepoint example. Thereafter, in a more theoretical context, we revitalize the somewhat forgotten concept of maximal acceptance probabilities. This allows for an interesting classification of Metropolis-Hastings algorithms and gives further advice on their usage. A review of some errors in reasoning that have led to the aforementioned dissent concludes this whole section.

4.2 Introduction

The Metropolis-Hastings algorithm is one of the most well-known MCMC methods. It traverses through the state space by means of a user defined proposal distribution. Each proposed state undergoes an accept-reject step, which decides whether the proposed state or the previous link in the chain is chosen to be the next link. This step alone secures the invariance of the Metropolis-Hastings Markov kernel towards the target distribution.

Originally, Metropolis-Hastings proposals were designed conveniently through kernel densities w.r.t. the same measure that runs the density of the target distribution (Metropolis et al., 1953; Hastings, 1970). In this case, the acceptance probability used in the accept-reject step is determined by the likelihood ratio of the transition in backward and forward direction. However, upcoming applications like variable selection (Mitchell and Beauchamp, 1988), point processes (Geyer and Møller, 1994) and changepoint analysis (Fearnhead, 2006; Siems et al., 2019) raised higher demands.

Common for these applications is that the elements of the state spaces are inhomogeneous in their dimension, i.e. the spaces are transdimensional. Obviously, such mixtures of different spaces are not straightforwardly accessible through standard techniques like random walk proposals. The first methods to conduct a change in dimension were plain births and deaths (Geyer and Møller, 1994). However, this is prone to ignore the relations shared among several coordinates and therewith promotes poor acceptance rates. Consequently, the exploration of the entire state space performs differently within the same and across the dimensions impairing the overall mixing time.

Subsequently, it became utterly popular to utilize functions that translate between points of different dimensions. Green (1995) pioneered this approach through the reversible jump algorithm. It was developed for purely continuous spaces and describes a particular class of proposals that act detached from the target space. As a result, the density of the target distribution and the kernel density of the proposal do not necessarily share the same underlying measure anymore. Nevertheless, Green (1995) was able to derive correct acceptance probabilities through a nifty application of the change of variable theorem.

According to Google scholar, Green (1995) has been cited over 5000 times. Unfortunately, Green (1995) and others caused a misperception about the abilities of the Metropolis-Hastings algorithm, which is nowadays ubiquitous. It is agreed among a significant number of scientific writings that the reversible jump algorithm has somehow made trans dimensional sampling possible and that other MCMC algorithms like Metropolis-Hastings are not applicable in these scenarios. Green (1995), Carlin and Chib (1995) and Chen et al. (2012) even substantiate this wrong conclusion, which was acknowledged by Besag (2001); Waagepetersen and Sorensen (2001); Green (2003); Green and Hastie (2009); Sisson (2005); Sambridge et al. (2006) and many others. A thorough search for papers which oppose this stance indirectly, in one way or another, revealed only Geyer and Møller (1994); Tierney (1998); Andrieu et al. (2001); Godsill (2001); Jannink and Fernando (2004) and Roodaki et al. (2011).

This poses a significant division within the MCMC community, which requires a thorough treatment. To this end, we take up on the original task of exploring mixture spaces by means of the Metropolis-Hastings paradigm, whereby the very focus lies on the computation of acceptance probabilities. At the appropriate places, we will investigate the results of Tierney (1998) and Roodaki et al. (2011) and make conclusions beyond that. Furthermore, the discussion gives a more detailed consideration of the aforementioned claims of Green (1995); Carlin and Chib (1995) and Chen et al. (2012).

We will see that the foundation of the computation of acceptance probabilities in its most theoretical to most practical form is the compatibility of the involved densities towards a common underlying measure. For example, the generalized Metropolis-Hastings algorithm from Tierney (1998), which is applicable to virtually any combination of target distribution and proposal, derives the required densities through the Radon-Nikodym theorem (Nikodym, 1930). Unfortunately, the nonconstructive nature of this theorem yields only little practical value.

Therefore, subject to the aforementioned compatibility, the design of proposals comprises a trade-off between mutability and feasibility. As a consequence, each of the following methods exhibits its very own conditions and possibilities that need to be considered carefully in order to build the right Metropolis-Hastings sampler.

Similar to Green (1995), we examine so-called translation functions, which convey between pairs of spaces. However, we consider two different ways to apply them: before and after proposing new states and refer to these concepts as ad-hoc and post-hoc translations, respectively.

In accordance with the reversible jump algorithm, the main feature of post-hoc translations is the detachment of the proposal from the space the target distribution acts on. This entails an integral transformation which imposes strict conditions and requirements on the translation functions. Consequently, a sophisticated design in practical and mathematical terms is essential here.

In return, post-hoc translations support parsimony regarding the number of random variables that need to be generated. This enables very tightly adapted and even deterministic transitions. Furthermore, they grant access to certain proposals defining intractable compound distributions like convolutions, marginal distributions or factor distributions.

In contrast, ad-hoc translations support arbitrary translation functions, as long as they act on the mixture space exclusively. We may, for example, deploy partial maximizers of the likelihood. This represents a straightforward way to improve the acceptance rates of difficult transitions.

On the downside, ad-hoc translations require that the proposal kernel densities comply with the underlying measure space. Thus, the freedom in choosing translation functions comes at the prize of a smaller adaptability in terms of the generation of random states.

Whilst the name ad-hoc results from the ability to use simple and purposive translation functions, the term post-hoc refers to the moment when the translation function is applied.

The well-known Metropolis-within-Gibbs approach confines the set of possible transitions through conditioning and is therewith able to steer the exploration of the state space in specific ways. Consequently, it employs conditional densities defined on suitable measure spaces. It turns out that proposals set up directly on these measure spaces yield straightforward acceptance probabilities.

This shifts the challenges of creating a Metropolis-Hastings sampler to deriving conditional densities of the target distribution. We consider this in some way novel and innovative perspective to be dual to the traditional one that puts the definition of proposals first.

Metropolis-within-Gibbs can be applied in the usual way to reduce the number of coordinates that need to be considered and is therewith capable of relaxing the terms of ad-hoc translations. In addition, it captures far more difficult cases like so-called semi deterministic translations, an important kind of post-hoc translations.

Our methods are scrutinized by means of a changepoint example. For this sake, we compare the acceptance rates of several birth and death like proposals. It turns out that ad-hoc proposals (combined with Metropolis-within-Gibbs) or post-hoc proposals are vital here. While the post-hoc translations are derived from delicate properties of the target distribution, the ad-hoc translations just trace for high likelihood values. Despite their strong differences, both methods achieve comparable acceptance rates.

The notion of maximal acceptance probabilities as introduced by Peskun (1973) and Tierney (1998) doesn’t seem to have gained a lot of attention so far. The reason for this might be that there is usually only one choice for the acceptance probability in place. We revitalize this dusted property and show that post-hoc translations do not necessarily yield maximal acceptance probabilities. Therewith, they may sometimes differ from their maximal counterpart.

Transitions between pairs of different spaces are usually performed by separate proposals, which are combined to a mixture proposal. This allows for a clear modular design and is thus pursued primarily here.

As stated in Tierney (1998) already, acceptance probabilities can either be computed based on unique pairs of the individual proposals or from the mixture proposal as a whole. Albeit unintentionally, Roodaki et al. (2011) elaborates conditions upon when both approaches yield maximality. We will investigate their main result and put them into our context.

This work is structured as follows. At first, we consider the Metropolis-Hastings approach in applied terms in Section 4.3. This involves an introduction of the important detailed balance condition together with the primal Metropolis-Hastings algorithm. Furthermore, in Section 4.3.1 we talk about mixture spaces, mixture proposals and translations. Section 4.3.2 is concerned with the Metropolis-within-Gibbs approach. Subsequently, we elaborate a changepoint example in Section 4.4. The general consideration of Metropolis-Hastings and maximal acceptance probabilities is pursued in Section 4.5. Section 4.5.1 further transfers these observations to mixture proposals. We conclude with a discussion and a brief literature review in Section 4.6.

4.3 The Metropolis-Hastings algorithm in applied terms

In this section, we deal with practical implementations of the Metropolis-Hastings algorithm. To this end, we develop ways to design proposals based on kernel densities w.r.t. sigma finite measure spaces. These comprise so-called ad-hoc and post-hoc translations and a new perspective for the Metropolis-within-Gibbs framework.

The Metropolis-Hastings algorithm is usually introduced on the basis of densities w.r.t. a common measure.6 For this sake, we are given a sigma finite measure space and a probability measure with a density such that . The user provides a Markov kernel from to in form of a kernel density such that . This Markov kernel is referred to as the proposal and as the proposal kernel density.

Algorithm 1 (Metropolis-Hastings).

(I) Choose an initial state (II) In step , given the previous state , propose a new state according to and set with probability

| (3) |

otherwise . We set to zero wherever it is not defined.

We refer to (3) as the acceptance probability and to the second argument within the braces as the acceptance ratio.

Let further

| (4) |

represents the Markov kernel whose application constitutes step (II) of Algorithm 1. Consequently, executing Algorithm 1 corresponds to simulating successive links of a Markov chain with initial state and Markov kernel .

The crucial point here is that, subject to some conditions, the unconditional distributions of these links converge in total variation to (Tierney, 1994). Thus, after simulating the chain for a sufficiently long time, the last link can be regarded as an approximate sample of .

In this work, we mainly focus on the most basic of these conditions, the invariance of towards . This invariance can be accomplished through the acceptance probability alone. To this end, we will examine different families of proposals and how closed solutions for the acceptance probabilities are calculated. The other conditions to secure convergence rely on the specific form of and have to be checked rather individually from case to case (Tierney, 1994).

The required invariance proofs are facilitated by means of the following condition.

Definition 1.

The Markov kernel preserves the detailed balance condition w.r.t. if

for all .

If preserves the detailed balance condition w.r.t. , is an invariant distribution of since . The opposite implication does not hold in general.

Markov chains build from Markov kernels that preserve the detailed balance w.r.t. another distribution are called reversible. This is because, they exhibit same probabilities in forward and backward direction once a link in the chain follows the law of this distribution. Consequently, MCMC methods that preserve the detailed balance condition are also called reversible.

Lemma 1 (Hastings (1970)).

Proof.

There is nothing to prove for with . Since is the disjoint union of , , and we can w.l.o.g. assume that . We get

whereby we have used that and Fubini’s theorem in *. ∎

By looking at , we see that normalization constants w.r.t. cancel out. Thus, the algorithm may deal with conditional versions of by deploying unchanged. This greatly facilitates data processing by means of conditioning.

4.3.1 Mixture state spaces and translations

Now, we elaborate sampling across alternating measurable spaces with the help of functions that translate between these spaces. We consider two naturally arising approaches, the so-called ad-hoc and post-hoc translations. Both exhibit their very own challenges and advantages in terms of feasibility and adaptability.

Let be a finite or countable set and let be a family of disjoint sigma finite measure spaces. The mixture measure space of is defined through

whereby is the smallest sigma algebra that comprises all ’s. The sole purpose of the identities with is to lift states from the component spaces into the mixture space.

As before, we assume that exhibits a density w.r.t. . A Metropolis-Hastings algorithm for can now be build as usual. A natural way to set up proposals on the mixture space is by pursuing a modular design through a mixture of Markov kernels, whereby each component solely transitions within a pair of the spaces. We want to use the term move to feature the available transitions.

Let be a finite or countable set, i.e. the set of moves. In order to build a mixture proposal, we define measurable functions with for all . is the probability of choosing move while being in . Furthermore, each move exhibits a kernel density that transitions between a pair of the spaces and complies with the measure of the target space.

For the sake of technical correctness, we need to lift each into the mixture space by setting it to 0 for unsupported arguments. Therewith, the mixture proposal that operates on the mixture space reads

with .

This time, the transition kernel for the Metropolis-Hastings algorithm for mixtures reads

| (5) |

Given the previous link , this kernel involves choosing a move according to at first, then proposing an according to and finally accepting or rejecting through .

This is in accordance with Algorithm 1, however, with the difference that we do not consider the mixture proposal as a whole. Instead, we incorporate the moves explicitly into the acceptance probability (see also Section 4.5.1).

Lemma 2.

Let be a bijection. The transition kernel of (5) with acceptance probability

preserves the detailed balance w.r.t. .

Proof.

For , , we get

whereby in * we have used the uniqueness of . ∎

stands for the unique backward or reverse move of . Consequently, if move transitions from to , move should transition in the opposite direction from to . Please note that the uniqueness of doesn’t imply that the transitions performed by move can only be reversed by move . In fact, the pairs of spaces are not supposed to be unique to the moves and the possible transitions determined by related move pairs may overlap arbitrarily.

Concerning the design of the moves, it is often not clear how to transition away from a point in one space to a point in another space. Especially random walk proposals pose a problem if there is no suitable measure of distance between the spaces available. This gives rise to two distinct approaches that employ functions as a device for translation.

In order to transition from to in move , our first approach employs a measurable function that translates between the spaces and a kernel density from to . Functions like are referred to as translation functions. Given the previous link in the chain , new states are proposed by virtue of . We call this procedure ad-hoc translation. Figure 6(a) illustrates it graphically.

Corollary 1.

The transition kernel of (5) with acceptance probability

preserves the detailed balance w.r.t. in ad-hoc translations.

Ad-hoc translations pose a flexible framework that is directly accessible through non-mathematicians with a basic understanding of the Metropolis-Hastings algorithm. In practice, however, another technically more demanding Metropolis-Hastings method has become the quasi gold-standard for sampling within mixed spaces. It is commonly referred to as the reversible jump algorithm (Green, 1995). We will allocate this approach to another type of translation and give a novel result that slightly generalizes this technique.

In contrast to ad-hoc translations, now, we propose first and then apply a translation to the proposed state. This allows us to detach the target space from the space where the proposal kernel density acts on. Thus, in move we may transition between a pair of the spaces, say from to , by detouring over another user-defined sigma finite measure space . To this end, we design a kernel density from to and a measurable function . Given the previous link , a random state is drawn by virtue of and the newly proposed state is obtained as . We call this procedure post-hoc translation. Figure 6(b) illustrates it graphically.

The case where and are discrete can be treated straightforwardly since the acceptance probability of move then reads

| (6) |

This applies, because the proposals in forward and backward direction are summarized as discrete and are thus compatible to . Though, the required feasibility of the integrals in (6) slightly restricts the set of possible post-hoc translations here.

However, most interesting cases arise when the proposal either doesn’t exhibit a kernel density w.r.t. or when it is computationally infeasible. Unfortunately, our methods so far do rely on such densities calling for a different approach here.

In practice, it would be desirable to derive the acceptance probabilities directly from the given proposal kernel densities. Thus, the trick is to accept and reject within yielding the actual post-hoc paradigm. In order for this procedure to be well-defined, any transition must exhibit a unique backward transition . Thus, we need to define additional measurable functions with

for all and .

This reasoning shows that the possible options for choosing post-hoc translations this way are somewhat limited. Therewith, the seemingly restrictive conditions of the next lemma can be considered as fairly universal.

Lemma 3.

Assume that for move with transitions from to and corresponding unique backward move , there exist measurable functions and with

The transition kernel

with

preserves the detailed balance w.r.t. in post-hoc translations.

Proof.

(I) implies that each is a bijection with inverse and (II) guides through an integral transformation by means of the densities . Since

we see that if and vice versa. Furthermore, for and , we get

The rest of the proof now follows the same scheme as before. ∎

In mathematically precise terms, it is incorrect to refer to as a proposal kernel density because it is generally not a kernel density of the proposal. However, in order to maintain a consistent language, we still want to keep this naming. Thus, the proof of Lemma 3 applies an integral transformation that secures the compatibility of the (joint) densities w.r.t. the transitions in forward and backward direction.

If all spaces are discrete coordinate spaces, we may choose arbitrary bijections that meet (I) and apply

(Fronk and Giudici, 2004) deploy post-hoc translation in this way.

It is common to require that if move transitions from to . Green (1995) pioneered the post-hoc translation approach and introduced this condition as dimension matching. His intention was to embed the spaces into a single superordinate one in order to avoid the inhomogeneity of the dimension. Around that time the nowadays ubiquitous term transdimensional sampling was coined.

The reversible jump algorithm of Green (1995) employs post-hoc translations over purely continuous coordinate spaces. It requires the dimension matching condition and that each is a diffeomorphism with Jacobi determinant . If (I) is met, the resulting acceptance probability reads

This follows from an integration by substitution for multiple variables since if we substitute .

Post-hoc translations are highly advanced, require very careful implementations and as it stands do only support certain kinds of state spaces. In return, they give the opportunity to generate random states within spaces of lower dimension than the target space. Therewith, they pave the way for tightly adapted, parsimonious sampling schemes where even deterministic transitions are viable.

Moreover, post-hoc translations may act on a space of higher dimension than the target space, which grands access to intractable compound distributions. To see this, consider the following minimal example to ordinarily transition from to by proposing values in through the kernel density . By employing the diffeomorphism we end up with equal forward and backward moves and

The corresponding proposal on the target space, i.e. , is the convolution of w.r.t and . If exhibits an intractable density on , the post-hoc paradigm proves functional here. Nevertheless, there is a little price to pay when we use the post-hoc paradigm this way. We lose the maximality of the acceptance probability. This topic will be discussed in Section 4.5.

4.3.2 Metropolis-within-Gibbs

Imagine a coordinate state space, whereby each step of the Metropolis-Hastings algorithm solely modifies one single coordinate. This evokes the Metropolis-within-Gibbs framework. Here we investigate this approach further. We will see that a generalization allows for the identification of new measure spaces to run proposals on. This creates an innovative perspective for an important class of post-hoc translations.

Given a countable set of moves , consider a family of measurable functions from into a measurable space with for all . Each determines a partition of the state space into measurable sets that yield the same values under . Given the previous link , the idea is to choose an out of and to propose a new state exclusively within the ensuing set

This entails the use of conditional versions of . For this sake, assume that is a random variable with and with a measure over and a kernel density from to . Furthermore, we stipulate that for all , the restriction of to is sigma finite.

On these grounds, we employ proposal kernel densities from to such that and for all and . We further define move probabilities as before.

Lemma 4.

The transition kernel of (5) with acceptance probability

| (7) |

preserves the detailed balance w.r.t. .

Proof.

Consider the following equality

For with we get

whereby we have used Fubini’s theorem together with the partial sigma finiteness of in *. ∎

The major application scenario for Metropolis-within-Gibbs is to simplify sampling within coordinate spaces. Let be an arbitrary coordinate space together with a product sigma algebra and for define . Move describes transitions where all but the -th coordinate remain fixed.

Let further with a product measure over . We define

with the counting measure . is negligible here since it cancels out in (7). is essentially build from a kernel density w.r.t. . If we chose plain probabilities for , we may write for transitions that differ in coordinate only.

The Metropolis-within-Gibbs approach exhibits a tremendous potential and even captures particular post-hoc translations. To see this, consider a translation function between two measure spaces and . The corresponding post-hoc translation from to applies in a deterministic manner. However, if is not injective, the backward move is usually not deterministic. In the following, we refer to this sort of moves as semi deterministic translations (SDT’s). In practice, SDT’s are the most commonly applied post-hoc translations.

Define

This yields Metropolis-within-Gibbs moves that mimic post-hoc translations. Even though transitions within one space and the same are not per se excluded here, we deem them as unsupported in this particular move.

In contrast to Lemma 3, is not subject to restrictions. Lemma 4 ensures that the acceptance probabilities are correct as long as we work within measure spaces that are in line with . The following lemma represents a reconciliation of Lemma 3 and 4.

Lemma 5.

Assume that there exist a sigma finite measure space and measurable functions and such that

For , we may write

| (8) |

Proof.

We have to show that for all and . To this end, consider that

This allows us to write

whereby in , we have set the proportionality constant in (8) to . ∎

Consequently, in accordance with Lemma 4, the proposal for transitioning from to complies with and thus applies deterministically. In turn, as in post-hoc translations, the backward move may exploit the form of . To this end, we employ a kernel density from to . A small contemplation yields that the acceptance probability for transitions from to then reads

with move probability . This is the same acceptance probability as in the corresponding post-hoc approach.

Please note that the Metropolis-within-Gibbs algorithm doesn’t capture all post-hoc translations. For translations that are not SDT’s, there is hardly a suitable available that yields the same sampling scheme. To see this, consider the relation defined by the viable transitions under the two translation functions that belong to a move and its backward move. is build from the partition of the two state spaces derived from the implied equivalence relation. However, for non-SDT’s this partition can easily contain the spaces as a whole rendering them useless.

4.4 A changepoint example

In this section, we scrutinize our theory by means of a small changepoint example. To this end, we consider three different implementations for so-called birth and death moves which either add or remove changepoints. Firstly, we employ very plain and unsophisticated proposals. Secondly, we apply ad-hoc translations that incorporate maximizers of certain partial likelihoods. Finally, we use tightly adapted post-hoc translations in the fashion of the reversible jump algorithm.

It turns out that the ad-hoc and post-hoc approaches perform equally well on this example in terms of their computation times and acceptance rates. In contrast, the plain approach performs poorly, which justifies the need of sophisticated ad-hoc and post-hoc translations.

Figure 7 shows an artificial dataset. The datapoints were drawn independently from a normal distribution with variance 1 and mean values that where subject to 9 changes.

To build an exemplary Bayesian model here, we choose a prior for the changepoint locations and mean values, i.e. the segmentation and its heights. The time from one changepoint to the next is geometrically distributed with and the segment heights in case of a jump and at the beginning are distributed according to . The data at timepoint also follows a normal distribution with its respective mean at and variance equal to 1.

The sampling starts with no changepoints and an overall segment height of 0. Subsequently, new changepoint locations may be found or discarded through birth and death moves. Additionally, we employ shift moves to shift single changepoints and adjust moves to adjust single segment heights.

Each move only manipulates a subset of the segment heights or a single changepoint and leaves the rest as it is. The Metropolis-within-Gibbs framework as well as post-hoc translations support such moves and they can be applied directly without any extra effort.

Please note that the backward moves for adjust and shift are again adjust and shift. Similarly, death and birth will be reversed by birth and death, respectively. This arises naturally here, since each of the moves has its very own and unique complementary move, e.g. a birth can only be reversed by a death.

An adjust move relocates the old height of a uniformly chosen segment according to . In turn, a shift move shifts the location of a uniformly chosen changepoint uniformly to a new position within the neighboring changepoints.

Let be the density of the univariate normal distribution with mean and variance evaluated at . Adjusting the height of a segment to yields an acceptance probability of

Note that the probabilities of choosing the shift move, the segment and the density values of the datapoints within the untouched segments, cancel out. Furthermore, since the normal distribution is symmetric w.r.t. its mean, the proposal densities cancel out as well. What remains are the density values for the datapoints within the adjusted segment and the priors for the segment heights.

Consider and to be immutable auxiliary changepoints. In the shift move, we shift an existing changepoint, say at location , uniformly to a new location, say , within the neighboring changepoints. Let and be the changepoints to the left and right of the changepoint at and let respectively be the corresponding segment heights. The acceptance probability for the shift move reads

Here, the probabilities of choosing the move and the changepoint, the priors for the heights and the density values of the data within the untouched segments cancel out.

4.4.1 A plain implementation of birth and death

In the death move, we choose a changepoint uniformly, remove it and propose a new height for the remaining segment according to . In the birth move, we propose a new changepoint uniformly among the timepoints without a changepoint. The two heights left and right of the new changepoint are then proposed independently according to .

Let respectively be the probabilities to choose a death or a birth move, respectively. We perform a death move. Therefore, let be the timepoint of the changepoint that is to be removed and let and be the changepoints to the left and right of the changepoint at and let and be the corresponding segment heights. Finally, let be the ensuing single segment height. The acceptance probability reads , whereby is the number of changepoints without and and

In order to derive the acceptance probability for the corresponding birth move, we just take the reciprocal of the acceptance ratio.

4.4.2 An ad-hoc implementation of birth and death

Here, we utilize parts of the likelihood of the model. The likelihood of the data within a single segment can be maximized w.r.t. its segment height just by choosing the mean of the involved datapoints. Thus, by proposing new segment heights close to these means we might propose sensible states that yield good acceptance rates. To this end, our sampling approach proposes new segment heights through a normal distribution with variance and mean equal to the empirical mean of the associated data.

Let and for define . By using the notation of Section 4.4.1, the acceptance probability for the death move reads

4.4.3 A post-hoc implementation of birth and death

Now, we design birth and death moves by virtue of the reversible jump paradigm. It is crucial hereby to find a carefully adapted diffeomorphism. As we have argued already, a good estimator for a segment height is the empirical mean of the observations belonging to it. If is this mean and we split the segment, say from to , into two parts through a changepoint at , such that the lengths of the resulting segments are and and their associated mean values are and , we see that .

Furthermore, in order to build a diffeomorphism thereof, we introduce an auxiliary variable . A sense of parsimony is achieved by stipulating that . We treat as part of the target space by setting . That way, describes a diffeomorphism with Jacobi determinant .

The opportunity to embed the auxiliary variables directly into the target space often remains unnoticed in practical implementations. Instead, would be sampled independently, which is prone to forfeit acceptance rate by proposing unsuited states.

This yields an SDT, whereby we rely on the reasoning of Section 4.4.2 and draw from in the birth move. Therewith, the acceptance probability for the death move reads .

4.4.4 Convergence

Here, we want to verify the convergence of our three different Markov chains towards the posterior distribution, say , that is determined through the changepoint model and data. For this sake, we check irreducibility and aperiodicity as required by Theorem 1 in (Tierney, 1994). Additionally, Harris recurrence follows from Corollary 2 there.

We stipulate that the move probabilities are all positive. Consequently, the acceptance probabilities for all proposed transitions will as well be positive. Therefore, given an arbitrary state, in all three cases, any changepoint configuration can be occupied with positive probability through a finite amount of birth, death and shift moves.

In order to prove irreducibility, at first, we consider events, say , whose elements all exhibit the same changepoint configuration. For to be positive under , the set of possible segment heights for each segment must be positive under an arbitrary univariate normal distribution. Thus, starting from a state that exhibits the very same changepoint configuration as , transitioning into can be done with positive probability by applying adjust moves to each segment height correspondingly. Again, this requires only a finite number of steps.

Now, take an arbitrary event that is positive under and partition it by the different changepoint configurations present. Due to the finiteness of this partition, one of the ensuing subsets must be positive under . Given an arbitrary state, we reach the changepoint configuration of this subset and then transition into this subset, both with positive probability through a finite amount of moves. This shows the irreducibility.

To see the aperiodicity, consider the two sets of states that can be reached through one or two successive applications of the adjust move. These sets overlap significantly, contradicting periodicity. Thus, the chain is aperiodic.

Together with the invariance, ensured by the particular forms of the acceptance probabilities, we conclude that all three Markov chains converge in total variation towards , irrespective of the state they are started in.

4.4.5 Results and conclusions

We want to compare our proposals empirically in terms of their runtime and acceptance rates. To this end, we set all four move probabilities to , except in the boundary cases. If there is only one segment, birth and adjust have the same probability of 0.75 and if each timepoint accommodates a changepoint then death and adjust have the probabilities 0.5 respectively 0.25.

| Acceptance rates | Death move | Birth move | Shift move | Adjust move |

|---|---|---|---|---|

| Plain proposals | 0.0021 | 0.0022 | 0.0681 | 0.2896 |

| Ad-hoc translations | 0.0588 | 0.0594 | 0.0678 | 0.2904 |

| Post-hoc translations | 0.0639 | 0.0645 | 0.0681 | 0.2899 |

For each of the three Markov chains, we simulated successive links. On my computer (AMD 64 with a 3200 GHZ CPU), the sampling algorithm for the plain proposals and the post-hoc translations needed twelve seconds and the ad-hoc approach took 13 seconds.

Table 1 shows the acceptance rates for the individual moves. It becomes apparent that the plain birth and death moves struggle with finding alternate changepoint configurations. Thus, the Markov chain performs poorly in exploring the state space, which impairs the mixing time.

In contrast, our ad-hoc and post-hoc translations compare well with each other, though both exhibit fundamentally different strategies in proposing new segment heights. Several experiments revealed that an acceptance rate for birth and death moves of more than 6.5% is infeasible as long as the new changepoint locations are chosen in a plain uniform manner. Thus, the achieved rates are sound, however, higher rates are usually considered as better (Bedard, 2008).

This shows that sophisticated approaches like ad-hoc and post-hoc translations are key for sampling within mixed spaces. Whilst our post-hoc proposals can be regarded as ambitiously developed, the ad-hoc proposals constitute a simple independence sampler that was derived from straightforward ideas. This indicates the great potential of ad-hoc translations. In turn, post-hoc translations may reduce the number of random variables to be generated and therewith result in more tightly adapted proposals that exhibit a reduced computational runtime.

4.5 The Metropolis-Hastings algorithm in abstract terms

So far, we have considered different strategies to implement the Metropolis-Hastings algorithm based on densities and measure spaces. Conversely, Tierney (1998), provides the theoretic foundations for the Metropolis-Hastings algorithm to work with arbitrary choices of and directly. At the same time, it introduces the notion of a maximal Metropolis-Hastings algorithm. Even though this concept remained widely unrecognized, it gives important advice on the design of proposals and allows for a classification of Metropolis-Hastings approaches.

In this section, we will summarize the main outcomes of Tierney (1998) and put them in line with the results of Roodaki et al. (2011) for mixture proposals. Subsequently, we examine maximality with regards to our own methods.

Given a measurable space , for a set we define the transpose of as . We leave it to the reader to show that and that if and only if preserves the detailed balance w.r.t. .

In the following, we are given an arbitrary probability space and a Markov kernel from to . The idea is to use

as the acceptance ratio. is the density of w.r.t. evaluated at .

At first, we need to find a set where is guaranteed to exist. To this end, consider . and are absolutely continuous w.r.t. . Thus, the theorem of Radon-Nikodym (Nikodym, 1930) ensures the existence of and . Let further

On the density exists and equals the ratio of and .

Lemma 6 (Tierney (1998)).

The transition kernel in (4) with acceptance probability

| (9) |

preserves the detailed balance w.r.t. . Furthermore, is almost surely maximal over all such acceptance probabilities.

Proof.

By considering the symmetry of and , the detailed balance can be proven in the same fashion as Lemma 1. Furthermore, any proper acceptance probability satisfies almost surely w.r.t. . Thus, on we get and a small contemplation yields that outside of we get . ∎

Lemma 6 allows us to speak of the maximal Metropolis-Hastings algorithm for the proposal when we use as in (9).

is almost surely uniquely defined and comprises all transitions an arbitrary Metropolis-Hastings sampler with proposal and target distribution can carry out.

Take, for example, an SDT with translation function and a state such that but . Let . Since and , we see that and are almost surely disjoint. Thus, the transitions defined by are not accessible for this SDT. In order to take advantage of such degenerated translation functions, we should resort to the ad-hoc paradigm instead. Section 4.4.2 provides an example for this.

4.5.1 Mixture proposals in general and maximality in particular

So far, we have build the acceptance probabilities for mixture proposals from unique pairs of forward and backward moves. However, the computation of the acceptance probability for the maximal Metropolis-Hastings algorithm involves the mixture proposal as a whole. Consequently, if the two approaches are different, the pairwise one is prone to yield smaller acceptance rates.

Nevertheless, the pairwise approach is an important measure of convenience. It exonerates us from evaluating the full, perhaps infinite range of component proposals. This gives rise to the following lemma that provides sufficient conditions for the pairwise approach to satisfy the maximality.

Lemma 7 (Roodaki et al. (2011)).

If for all , there exist disjoint with

we get

| (10) |

for .

Proof.

Define . For we get

This holds since (I) and (II) state that we can set for all . ∎

Strangely enough, Roodaki et al. (2011) seem to make a different statement with their theorem. They point out when the acceptance probabilities can be derived from pairs of component moves. Therewith, they appear to miss that this is always viable as long as the pairs are unique, a statement that has already been known from (Tierney, 1998).

Under the assumption that the conditions (I) and (II) of Lemma 7 are met, we may ask for the maximality of the approaches considered in this work. As a rule, it is sufficient to show that for each move the acceptance ratios correspond to the r.h.s. of (10). This is straightforward for the primal Metropolis-Hastings algorithm and ad-hoc translations, and also for (6) and (7).

However, post-hoc translations that accept within the auxiliary space are deviant. In the context of Lemma 3, we define

Furthermore, let be the proposal of move .

Lemma 8.

For move with transitions from to , we get

whereby is a random variable distributed according to .

Proof.

This holds since for and

whereby we have used the basic properties of the conditional expectation in and condition (I) and (II) of Lemma 3 in **. ∎

Thus, the acceptance probability for move of the maximal Metropolis-Hastings algorithm for the post-hoc translations of Lemma 3 reads

This states that given a previous link , we accept or reject the newly proposed state based on an expectation drawn from over those values of that yield . If is injective, holds and the post-hoc approach for this move is guaranteed to be maximal. This is the case for all SDT’s in the fashion of Lemma 3 and 5.

On the downside, consider a transition where the maximal Metropolis-Hastings algorithm exhibits an acceptance probability of one, i.e. . The corresponding post-hoc translation approach accepts with probability one if and only if . In non-injective cases, these two conditions can be very distinct and lead to significantly different results.

4.6 Discussion and literature review

In this section, we examined several practical and theoretical approaches to derive acceptance probabilities for the Metropolis-Hastings algorithm. Due to their tricky characteristics, post-hoc translations received the most attention. In accordance with Green (1995), key to their implementation is that the accept-reject step is performed within the auxiliary space rather than the target space. As a consequence, the translation functions need to be supplemented by auxiliary functions determining for each transition its unique backward transition. On top of this bijective completion, further conditions are imposed in order to enable a certain integral transformation.

In an abstract consideration of the Metropolis-Hastings algorithm, we came across the notion of maximality as introduced by Peskun (1973) and Tierney (1998). Post-hoc translations may lose this maximality if they are not carefully implemented. This renders SDT one of the most vital post-hoc approaches. Interestingly, we found that SDT’s are also accessible through the Metropolis-within-Gibbs paradigm.

Tierney (1998) was able to identify the superset of possible transitions a Metropolis-Hastings sampler is able to carry out. Therewith, we understood the limits and possibilities of SDT’s better. We found that translation functions that exhibit a certain degeneracy are ineffective in post-hoc approaches, a point that underlines the utter relevance of ad-hoc translations.

All considered methods made intense use of mixture proposals. They feature a modular design and are therefore of high practical value. It is further beneficial to compute the acceptance probabilities solely based on unique pairs of moves. However, we should avoid an overlap of their supports since this may forfeit maximality.

So far, we solely considered mixture proposals w.r.t. a countable set of moves. However, the set of moves can alternatively be part of any sigma finite measure space, whereby the move probabilities are replaced by a kernel density. Consequently, summation over mixture components is replaced by integration. As before, we need to define unique pairs of forward and backward moves. An analogy to this is a post-hoc translation having an auxiliary variable that represents the move with an associated auxiliary function that determines the corresponding backward move.

Our purposive contemplation of ad-hoc as well as post-hoc translations, and Metropolis within Gibbs opens up innovative ways of choosing sampling schemes that satisfy various demands regarding simplicity and sophistication. The author of this work hopes that this helps to eliminate the ubiquitous confusions surrounding transdimensional sampling.

In the remainder of this section, we discuss a sequence of far-reaching errors in reasoning. They all share the conclusion that ordinary MCMC methods struggle with transdimensional sampling.

Green (1995) concludes wrongly that we have to use dimension matching in order to pursue transdimensional moves. On page 715 in Green (1995), the acceptance probability solely utilizes single components of the mixture proposal. This implies that the density used to perform a move must also be used for the corresponding backward move. For transdimensional moves, this is obviously not possible and made it inevitably necessary to introduce the dimension matching condition. Thus, Green’s undeniably great idea appears to be the result of a simple error in reasoning.

Carlin and Chib (1995) claim, by referring to Tierney (1994), that transdimensional moves create absorbing states and therefore violate the convergence of Markov chains. Unfortunately, Tierney (1994) doesn’t seem to provide this statement. In order to circumvent this putative problem, they propose to work on the product space instead. Frankly speaking, this adds a huge burden just to avoid the inhomogeneous nature of the spaces. According to Google scholar, Carlin and Chib (1995) was cited over 1000 times, though a few of them question the necessity of this approach, e.g. Godsill (2001); Green (2003); Green and Hastie (2009); Green and O’Hagan (1998).

In a more measure theoretic context, Chen et al. (2012) comes to the conclusion that usual MCMC cannot transition across spaces of different dimensions. They argue with the lack of dominating measures and therewith ignore the fact that each countable collection of sigma finite measures indeed exhibits a common dominating measure.

As we have seen, the acceptance probability of the reversible jump algorithm is not necessarily maximal in the sense of Lemma 6. Interestingly, Green (1995) refers to Peskun (1973) in order highlight the maximality of his choice of acceptance probability.

These misperceptions have introduced a significant burden to the field of transdimensional sampling. The concerning literature is difficult to overview due to inconsistent claims and full of poor mathematical language due to the absurd overemphasis on dimensionality. As a result, it sometimes feels like reading some sort of star trek novel.

Finally, the name “reversible jump” apparently stems from Green’s wrong conviction that he constructed a method that overcomes the non-reversibility of transdimensional moves in the Metropolis-Hastings algorithm. Thus, this name lacks a proper meaning and collides awkwardly with “reversible MCMC” making these topics even harder to grasp for newcomers.

5 Exact inference in Bayesian changepoint models

A sequence of posterior samples obtained from a changepoint model and data allows us to derive various quantities like the expected number of changepoints, a changepoint histogram and many more. Siekmann et al. (2011) gives an impressive demonstration of what can be inferred from posterior samples based on ion channel data.

However, the number of possible changepoint configurations grows exponentially w.r.t. the data size and thus, only fractions of them can be covered by samples. This might often be sufficient as there are usually comparatively few relevant ones. Nonetheless, we can only be sure of the accuracy of our approaches if we apply exact inference algorithms, which is indeed feasible at times.

In this section, we elaborate exact inference strategies for a certain, but still broad, class of Bayesian changepoint models. A range of such algorithms already exists. However, across those papers the mathematical notations are quite diverse and in parts they convey similar contents.

The following list provides the Bayesian changepoint papers that are most relevant to this section. Fearnhead and Liu (2007); Adams and MacKay (2007) and Lai and Xing (2011), elaborate, inter alia, online changepoint detection algorithms. We can also find retrospective inference strategies like exact sampling (Fearnhead, 2006), changepoint entropy (Guédon, 2015), changepoint histograms (Nam et al., 2012; Rigaill et al., 2012; Turner et al., 2010; Aston et al., 2012), and approaches for parameter estimation (Lai and Xing, 2011; Yildirim et al., 2013; Bansal et al., 2008).

On this basis, we will develop novel inference algorithms. Though, in order to provide a comprehensive understanding of Bayesian changepoint analysis and its capabilities, we will implement the bulk of the existing approaches into our own lightweight and simple notational framework. This framework resembles that of Fearnhead and Liu (2007) most.

Meanwhile, we will keep an eye on inference in hidden Markov models (Rabiner and Juang, 1986), hidden semi-Markov models (Yu, 2010) and the Kalman-filter (Kalman, 1960; Rauch et al., 1965). This helps clarifying that inference in Bayesian changepoint models is closely related to inference in these more basic models. General terms for corresponding inference strategies comprise Bayes filtering and smoothing (Särkkä, 2013).

The basic innovation provided in this section concerns the development of very efficient pointwise inference. This paves the way for the computation of a wide range of pointwise expectations w.r.t. all timepoints at once with an overall linear complexity.