[catoptions]

Flexible Mixture Priors for Large Time-varying Parameter Models

Time-varying parameter (TVP) models often assume that the TVPs evolve according to a random walk. This assumption, however, might be questionable since it implies that coefficients change smoothly and in an unbounded manner. In this paper, we relax this assumption by proposing a flexible law of motion for the TVPs in large-scale vector autoregressions (VARs). Instead of imposing a restrictive random walk evolution of the latent states, we carefully design hierarchical mixture priors on the coefficients in the state equation. These priors effectively allow for discriminating between periods where coefficients evolve according to a random walk and times where the TVPs are better characterized by a stationary stochastic process. Moreover, this approach is capable of introducing dynamic sparsity by pushing small parameter changes towards zero if necessary. The merits of the model are illustrated by means of two applications. Using synthetic data we show that our approach yields precise parameter estimates. When applied to US data, the model reveals interesting patterns of low-frequency dynamics in coefficients and forecasts well relative to a wide range of competing models.

JEL: C11, C30, C53, E44, E47

KEYWORDS: Time-varying parameter vector autoregressions, hierarchical modeling, clustering, forecasting

1. Introduction

A growing number of papers introduces time-varying parameters (TVP) in econometric models for capturing structural breaks in relations across macroeconomic fundamentals (see, for example, Cogley and Sargent, 2005; Primiceri, 2005; Sims and Zha, 2006; Korobilis, 2013; Eickmeier et al., 2015; Mumtaz and Theodoridis, 2018; Paul, 2019) and to achieve more accurate macroeconomic forecasts (see, for instance, Koop and Korobilis, 2012, 2013; D’Agostino et al., 2013; Groen et al., 2013; Bauwens et al., 2015; Hauzenberger et al., 2019; Huber et al., 2020a, b).

In this paper, we focus on estimating TVP vector autoregressive (VAR) models with a large number of endogenous variables. Due to severe overfitting issues in large TVP-VARs, special emphasis is paid to important modeling decisions, such as whether coefficients evolve gradually, change abruptly or remain constant for subset of periods. In macroeconomic applications, it is common to assume that coefficients evolve according to a random walk, implying that parameters change smoothly over time. As noted by the recent literature (see, for example, Lopes et al., 2018; Hauzenberger et al., 2019), however, this assumption might be overly simplistic and lead to model misspecification.

In large TVP-VARs it is often reasonable to assume that most parameters remain constant over time, while only few vary. To capture this behaviour, the Bayesian literature frequently uses shrinkage priors on the state innovation variances to sufficiently push them towards zero (Frühwirth-Schnatter and Wagner, 2010; Belmonte et al., 2014). A severe drawback of this strategy is that it only accounts for the case that a given coefficient is constant for all points in time (labeled static sparsity).

Another common situation faced by researchers is that coefficients change only at certain points in time (this is referred to as dynamic sparsity). Using a mixture distribution on the innovation variances, for example, allows to push small parameter changes towards zero (see, inter alia, McCulloch and Tsay, 1993; Gerlach et al., 2000; Giordani and Kohn, 2008; Koop et al., 2009; Huber et al., 2019).111Other dynamic sparsification techniques include different forms of dynamic shrinkage processes (see, inter alia, Kalli and Griffin, 2014; Uribe and Lopes, 2017; Rockova and McAlinn, 2020; Kowal et al., 2019; Hauzenberger et al., 2020), latent threshold models (Nakajima and West, 2013) or dynamic model selection techniques (Chan et al., 2012; Koop and Korobilis, 2013). Alternatively, Hauzenberger et al. (2019) introduce a more flexible law of motion by assuming a conjugate hierarchical location mixture prior directly on the time-varying part of the coefficients. This location mixture allows for a dynamically adjusting the prior mean on the TVPs to capture situations with a low, moderate or even large number of structural breaks in the coefficients. However, both techniques come with drawbacks. For instance, the mixture innovation model of Huber et al. (2019), equipped with a latent threshold mechanism, discriminates between a high and a low innovation variance state. However, the authors do not discard the random walk law of motion, which might be too restrictive. Hauzenberger et al. (2019) use either a conjugate g-prior (Zellner, 1986) or a conjugate Minnesota prior (Doan et al., 1984; Litterman, 1986), potentially lacking flexibility to disentangle abrupt from gradual changes.

In this paper, we carefully design suitable mixture priors for the state equation. In a first variant, a mixture prior is not only introduced on the state innovations, but also on the autoregressive coefficients in the state equation to obtain sufficient flexibility. To achieve parsimony in large models, a latent binary indicator determines the law of motion for the TVPs and detect periods where coefficients evolve according to a random walk and times where the TVPs are better characterized by a stationary stochastic process. Combined with a mixture on the innovation volatilites and suitable shrinkage priors, this approach is capable of automatically capturing a wide range of typical parameter changes. In a second variant, the sparse finite location mixture model of Hauzenberger et al. (2019) is extended by considering non-conjugate shrinkage priors and by replacing the location mixture with a location-scale mixture. Here, an additional mixture on the state variances captures the notion that structural breaks in coefficients happen infrequently (with potentially large TVP innovations), while most of the time coefficients are constant (with TVP innovations pushed towards zero), similar to mixture innovation models.

In the previous paragraphs we repeatedly stated that our techniques are well suited to handle overfitting issues in large TVP-VARs. But large TVP models also raise the question of computational feasibility. In this contribution, computational complexity is reduced by using recent advances in estimating large-scale TVP regression (see Chan and Jeliazkov, 2009; McCausland et al., 2011; Hauzenberger et al., 2020). These are based on rewriting the TVP model in its static regression form. In this representation, the TVP model is treated as a very big regression model and the techniques proposed in Bhattacharya et al. (2016) can be used. Since these algorithms are designed for single equation models, we estimate the VAR model using its structural representation and thus estimate a set of unrelated TVP regressions (see Carriero et al., 2019).

Based on two applications we investigate the merits of the techniques developed in the paper. First, in an application using synthetic data we illustrate that the proposed methods work well in detecting small and large structural breaks in coefficients. Second, we employ a large US macroeconomic dataset for an empirical application. Our proposed methods reveal interesting patterns in the low-frequency relationship between unemployment and inflation. Moreover, to evaluate predictive performance of our approach, we perform a comprehensive forecasting exercise. This forecasting horse race shows that the proposed framework works well relative to a wide range of competing models. Even for large TVP-VARs introducing flexible mixture priors in the state equation tends to improve forecast accuracy.

The remainder of the paper is structured as follows. Section 2 introduces a TVP regression model with flexible mixture priors and sketches the main contributions of the paper. Section 3 generally outlines inference in these models, while Section 4 discusses the posterior sampling algorithm of Bhattacharya et al. (2016), when applied to non-centerred TVP regressions. Section 5 and Section 6 show the results for artificial data and US data, respectively. Finally, Section 7 summarizes and concludes.

2. Econometric Framework

2.1. A TVP Regression

Let denote a scalar time series and refer to a -dimensional vector of predictors, then the observation equation for a TVP regression can be written as:

| (1) |

Here, is a -dimensional vector of TVPs that relates to the quantity of interest and denotes the measurement error with mean zero and time-varying variance . For the state equation of , we assume a stochastic volatility (SV) specification and refer to Appendix A.1 and Kastner and Frühwirth-Schnatter (2014) for details.

Typically, is assumed to evolve according to a random walk (RW). In this paper, interest centers on relaxing this assumption. In the following, to achieve both sufficient flexibility and model parsimony, we use two different hierarchical mixture specifications for . In the first variant, we assume that coefficients evolve according to a mixture of a random walk and a white noise process. In the second variant, interest centers on extending the methods proposed in Hauzenberger et al. (2019).

2.2. A Hierarchical Mixture between a Random Walk and a White Noise Process

For a mixture between a random walk and white noise process we assume that the evolution of is given by:

| (2) |

with denoting a -dimensional intercept vector, being a -dimensional diagonal autoregressive coefficient matrix and denoting a -dimensional vector of state innovations, which are centered on zero and feature a -dimensional variance-covariance matrix . Moreover, we assume and to evolve according to a regime-switching process:

| (3) |

and

| (4) |

with denoting a binary indicator matrix with being either zero or one, being a -dimensional identity matrix while and denote -dimensional diagonal matrices. Eq. (missing) 3 assumes that coefficients evolve according to a mixture of a random walk and a white noise process, while Eq. (missing) 4 ensures sufficient flexibility of the state innovations, respectively. For example, if the covariate-specific indicator in the period, the covariate follows a random walk with state innovation variance , while if in the period, it follows a stochastic process with variance .

This specification (henceforth labeled as TVP-MIX) nests a wide variety of popular TVP models, such as standard RW state equations and mixture innovation models.222In the empirical application, these are considered as important benchmarks. A standard random walk evolution is trivially obtained by setting . A so-called mixture innovation model assumes and specifies similar to Eq. (missing) 4 (Gerlach et al., 2000; Giordani and Kohn, 2008; Koop et al., 2009; Huber et al., 2019). Additionally, mixture innovation specifications restrict with being a small value close to zero and being a diagonal matrix collecting variable specific scaling parameters.333Related to literature on variable selection (George and McCulloch, 1993, 1997), here is commonly referred to as slab component and as spike component (see, for example, Huber et al., 2019).

Apart from discussing the relation to other popular TVP models, it is also worth highlighting additional features of the model proposed in (2) to (4). If a parameter is almost constant, but also features larger abrupt changes for some periods, we would expect that . This case is of particular interest, when compared to a standard mixture innovation model with random walk state equation. Conversely, if a coefficient features large, more persistent swings, but also some periods of parameter stability, we would expect . Intuitively, the relative proportions of and depend mainly on the nature of coefficient changes. Alternatively, if the coefficient is constant or negligible (static sparsity), this can be achieved with and/or close to zero (Lopes et al., 2018). Note that in the special case of constant coefficients, the proposed specification is not identified. We address this issue in the context of interpreting the state indicators .

2.3. A Hierarchical Pooling Specification

For a hierarchical pooling specification, we follow Hauzenberger et al. (2019) and assume that the time-varying part of follows a sparse finite mixture in the spirit of Malsiner-Walli et al. (2016).

The specification of the state equation (labeled as TVP-POOL) reads as:

| (5) |

Here, denotes a -dimensional constant coefficient vector and is assumed to be a -dimensional vector of random coefficients featuring a specific structure. That is, conditional on latent group indicators that takes a value , follows a multivariate Gaussian distribution:

| (6) |

where refers to the group-specific mean and denotes the variance-covariance matrix. It is also worth noting that serves as group indicator for . The probability that is assigned to cluster is defined as .

This structure is closely related to the setup of Hauzenberger et al. (2019). In the following, we extend their location mixture prior to a location-scale mixture prior by introducing a regime-switching specification on similar to Eq. (missing) 4. That is:

| (7) |

with both and being diagonal matrices and denoting a binary indicator matrix. Similar to standard mixture innovation models one component serves to detect larger breaks, while a second component handles dynamic sparsity. We therefore discard the conjugate prior assumption of Hauzenberger et al. (2019) and instead assume non-conjugate shrinkage priors on both state variances (described in more detail in Subsection 3.1).

Before proceeding, it is also worth sketching the general idea of this random coefficient specification. This model can be seen as a stochastic variant of multiple break point specifications (Koop and Potter, 2007), which is capable of capturing situations with a low, moderate or even large number of structural breaks. To estimate the number of regimes, we follow Malsiner-Walli et al. (2016) and Hauzenberger et al. (2019) and specify an “overfitting” model by setting to a large integer (i.e. consider many regimes a priori). To achieve parsimony, we come up with an estimate for the number of clusters (usually ) by specifying a shrinkage prior on both the mixture weights and the component means. Thus, overall shrinkage is determined between two interacting objectives: we aim at eliminating irrelevant clusters, while at the same time attempting to avoid highly overlapping component means.

At this stage one might ask, why we do not assume different state innovation variances (i.e. using the group indicators for both and )? Here, it is worth discussing two important considerations. First, denotes a large integer and might lead to overfitting issues without assuming additional hierarchical shrinkage/pooling priors on the state innovation variances. Second, covariate-specific binary indicators () for the scales already render the model highly flexible and it allows to introduce shrinkage on the state innovation variances in a simpler way. Moreover, the two-state mixture on the state variances (see Eq. (missing) 7) is designed to support inference about the locations , for . We expect that many elements in cluster around zero (i.e. coefficients are constant with close to zero), while occasionally there are structural breaks in some coefficients (requires relatively large values in ). Especially we aim to detect these two extremes (changes/no changes in ) with .

2.4. The Latent State Indicator Matrix

Sofar we remained silent on the evolution of . There are many different possibilities how the binary indicators , for evolve over time. In the following, we assume two laws of motion:

-

1.

Pooled Markov-switching process: When assuming a first-order Markov process for each independently, sampling the state indicators can be computationally cumbersome, especially if is large. Since one has to rely on forward filtering backward sampling algorithms, computation time quickly adds up. Therefore, we replace with . In the following, is assumed to be common to all covariates in period and governed by a joint Markov process.444Alternatively, Koop et al. (2009) group coefficients and assume class-specific indicators. This process is driven by a transition probability matrix given by:

with transition probabilities from state to denoted by and following a Beta distribution , for (see Uribe and Lopes, 2017).

-

2.

Independent over time and covariate-specific indicators: The assumption that a joint indicator governs the evolution of large number of coefficients might be too inflexible in certain cases. For this reason, we also specify covariate-specific indicators, coupled with independent mixture priors (see Lopes et al., 2018). In contrast to covariate-specific Markov processes, mixture priors are assumed to be independent over time and thus do not involve computationally demanding forward filtering backward sampling algorithms. In the following, is assumed to follow an independent Bernoulli distribution with and being Beta distributed, i.e. .

Moreover, it should be noted that the prior choice on the binary indicators is quite influential. For the random walk/white noise mixture (TVP-MIX), the hyperparameters are chosen in such a way that it is more likely that gradual changes have a higher (unconditional) expected duration (with than abrupt changes (with ). In the empirical application we therefore set , for the Markov-switching process and , , , for the independent mixture distribution. For the location-scale mixture (TVP-POOL with solely governing the state innovation variances, we take a more agnostic approach by assuming and .

3. Bayesian Inference

To discuss inference for both variants outlined in Section 2, we introduce a very general state equation for :

| (8) |

Eq. (missing) 8 nests both approaches with the first variant (TVP-MIX) being obtained by setting , while the second approach (TVP-POOL) is given by defining and , if .

3.1. The Non-Centered Parameterization

In this subsection we exploit the non-centered parameterization to write and as part of the observation equation, enabling shrinkage on the regime-switching state innovation volatilities (Frühwirth-Schnatter and Wagner, 2010).

We therefore recast the model as follows:

| (9) | ||||

Here, is a -dimensional vector of normalized states, defined as and with denoting the (matrix) square-root of . Using the definition of in Eq. (missing) 4 (or Eq. (missing) 7) the observation equation in Eq. (missing) 9 can be rewritten as:

and, more compactly, as a standard regression model:

Here, denotes a -dimensional covariate vector with referring to the dot product and being a -dimensional coefficient vector.

On the time-invariant we use a hierarchical global-local shrinkage prior (see Polson and Scott, 2010):

where refers to the element in , induces local shrinkage with mixing density and denotes a global shrinkage parameter with density . In the empirical application, we focus on the Normal-Gamma (Griffin and Brown, 2010) shrinkage prior and choose and accordingly. This shrinkage prior has been proven to be successful in macroeconomic and financial application (see, for example, Huber and Feldkircher, 2019) and is quite common in the literature.555It is worth noting that any global-local shrinkage prior might be used. Other popular choices are the SSVS prior (George and McCulloch, 1993, 1997), the Horseshoe prior (Carvalho et al., 2010), the Bayesian Lasso (Park and Casella, 2008) or the Triple-Gamma prior (Cadonna et al., 2020). See also Huber et al. (2020a), Kastner and Huber (2020) and Cross et al. (2020) for thorough studies of global-local shrinkage priors in macroeconomic applications. The exact prior specification is outlined in Appendix A.2.

3.2. The Static Representation

If interest centers on estimating the latent states , we can straightforwardly recast Eq. (missing) 9 in a static regression form by conditioning on , the state innovation volatilities and the stochastic volatilities in . We define as a -dimensional vector, as a -dimensional matrix and as a -dimensional vector with , and on the position, respectively. Then, the static form of Eq. (missing) 9 is:

Here, is a -dimensional latent state vector, is a -dimensional intercept vector and is a -dimensional shock vector. After defining , the precise structure of and is given by:

with denoting -dimensional zero matrix. Solving for yields:

implying that with prior mean and prior variance-covariance matrix of (see, for instance, Chan and Jeliazkov, 2009; Chan and Strachan, 2020). In the special case of , for all , (and thus ) reduces to an identity matrix, while , for any , induces a (specific) banded lower-triangular (block diagonal) structure of ().666Note that , for , is always true for the TVP-POOL model, but not ruled out for the TVP-MIX specification. Moreover, if , . Here it is worth emphasizing, that the prior variance-covariance matrix solely depends on state indicators .

Moreover, the prior mean also depends on the structure of and . The simplest thing is to set to a zero vector, which we implicitly assume for the TVP-MIX variants. For the TVP-POOL approach we use a hierarchical mixture prior on , described in detail next.

3.3. A Hierarchical Prior Mean

The model outlined in (5) to (7) denotes a sparse finite location-scale mixture. After recasting the model in the non-centered parameterization, we are able to replace the location-scale mixture prior on (outlined in Eq. (missing) 6) with a location mixture prior on the normalized latent states , since the scales of Eq. (missing) 7 ( and ) are now part of the observation equation. That is:

| (10) |

with group-specific mean , for and variance-covariance matrix . In the following, the prior mean is defined as , with if .

The sparse finite location mixture in Eq. (missing) 10 allows us to use a similar prior setup as proposed in Malsiner-Walli et al. (2016) and Hauzenberger et al. (2019). To ensure model parsimony we use a Dirichlet prior on :

with referring to an intensity parameter. The prior on the intensity parameter is specified as:

with in the empirical application. Here, we closely follow Malsiner-Walli et al. (2016), who show that this prior choice is successful in detecting superfluous components and obtaining a parsimonious mixture representation.

Moreover, on the group means we specify the following shrinkage prior:

with being centered on zero and prior variance-covariance matrix . Here, and with denoting the range of . Moreover, we specify a Gamma prior on the elements in :

Following Yau and Holmes (2011) and Malsiner-Walli et al. (2016), we define to push the group-specific prior means towards zero.

4. Posterior computation

In this subsection, we outline the MCMC sampling step for . We stress that drawing is computationally fast, also for relatively large , but sampling the -dimensional vector is computationally demanding (Hauzenberger et al., 2020). Thus for (and the remaining parameters) we use standard MCMC techniques with sampling steps and conditional posteriors outlined in Appendix A.3.

For , irrespectively of the structure of and , we obtain standard conditional Gaussian posterior quantities with and :

The main issue, however, is that the inversion of is computationally costly, since it is -dimensional matrix with and being potentially large integers.

Thus, to avoid high-dimensional full matrix inversions and Cholesky decompositions for drawing the normalized latent states , we rely on the algorithms proposed in Bhattacharya et al. (2016), applied to TVP models in Hauzenberger et al. (2020). This method involves the following steps:

-

1.

Draw a -dimensional vector

-

2.

Sample a -dimensional vector

-

3.

Define , with denoting the lower Cholesky factor of , and

-

4.

Compute

-

5.

Set

-

6.

Obtain a draw for

Moreover, using the static representation for a TVP regression the involved matrices are sparse, which can be exploited to achieve additional computational gains (see Chan and Jeliazkov, 2009; Hauzenberger et al., 2019, 2020). Depending on the structure of there a two extreme cases as briefly discussed in Subsection 3.2. Computationally the most expensive case is a random walk state equation (, ), while having no autoregressive structure in the state equation (, ) it is computationally less demanding.777See Hauzenberger et al. (2020) for a comparison between the two extremes. Recall, the former has a specific lower triangular structure (rendering block diagonal) and in the latter both and are diagonal. Thus, even for a random walk state equation (the most dense case), using sparse algorithms pays off in terms of computation. Moreover, if , for some , we have to account for an intermediate computational burden lying between the two extremes that eventually depend on the exact structure of ().

4.1. Equation-wise estimation for a TVP-VAR

The methods outlined in the previous subsection are designed for single equation models. To use these algorithms also for posterior inference in TVP-VARs, we rewrite the multivariate model as a set of unrelated TVP regressions (see Carriero et al., 2019).

This can be done by using the structural form of the TVP-VAR:

| (11) |

Here, denotes an -dimensional vector of endogenous variables with being an -dimensional strictly lower-triangular matrix (with zero main diagonal) defining contemporaneous relationships between the elements of . Moreover, , for , denotes an -dimensional time-varying coefficient matrix, is an -dimensional intercept vector and refers to an -dimensional Gaussian distributed error vector, centered on zero and with time-varying -dimensional diagonal variance-covariance matrix . Before proceeding, it is convenient to define .

In the following, for , the equation of is given by:

with denoting a -dimensional covariate vector with and a -dimensional vector of time-varying coefficients. Here refers to the element of , denotes the row of and the element of . Moreover, for the first equation () we have and .

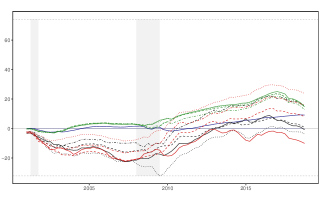

5. Simulation study

In this section we use synthetic data to illustrate the features of the proposed mixture variants. For the data generating process (DGP) we assume that the number of observations is and the number of covariates is given by . The covariates are simulated with for and with being a -dimensional vector of ones. For the error variance , we assume an SV specification with following a random walk process. That is, with and . For the time-varying parameters we assume quite specific laws of motion. We define as initial level and assume that both regime-switching autoregressive parameters and regime-switching variances in the state equation are governed by a joint Markov process . Here, we let , , with and . The joint indicator is simulated with transition probabilities and , effectively leading to a higher unconditional probability that follows a random walk evolution.

In particular, the first coefficient features larger, more persistent parameter changes (with ), while for a small number of periods is basically constant (achieved through the white noise state equation with close to zero). The second parameter features small gradual changes over time (), but also larger abrupt breaks (). The third parameter is similar to the first coefficient, but assumes . The fourth coefficient is assumed to be constant over time ( and are both close to zero) and, finally, the fifth parameter features some extremely large breaks (with ), while it is otherwise assumed to be constant (here achieved through the random walk state equation with close to zero).

To assess the flexibility of our approaches we compare them to models assuming a standard random walk evolution of coefficients and to those assuming constant coefficients. Moreover, we consider a typical mixture innovation model as an important benchmark. For each model we use a Normal-Gamma (Griffin and Brown, 2010) prior on the constant part and allow for SV in the measurement error variance. Furthermore, each TVP model features a Normal-Gamma prior on the square root of the state innovation variances, which are potentially regime-switching (see Eq. (missing) 9).

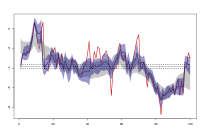

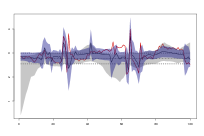

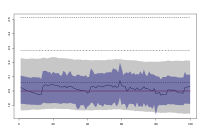

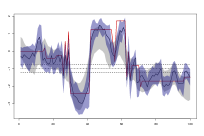

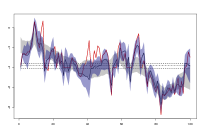

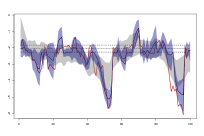

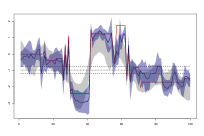

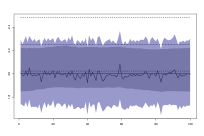

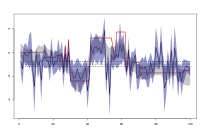

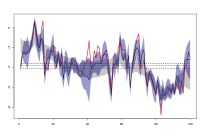

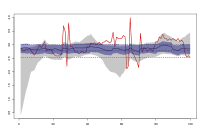

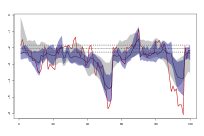

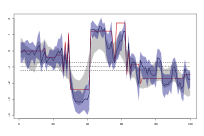

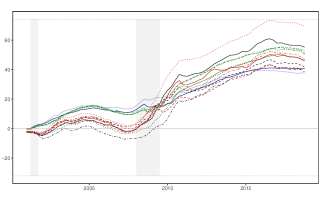

Panels (a) to (c) in Figure 1 depict the evolution of regression parameters estimated with our proposed methods, while panel (d) shows estimates with a typical mixture innovation model. The red solid lines denote the true coefficients, the blue shaded areas represent the posterior credible interval (with the blue solid lines referring to the posterior median), the gray shaded area represent the respective credible set of a standard TVP model with random walk state equation and the black-dotted lines indicate the // percentiles of a constant coefficient model.

The results with artificial data reveal at least three important features. First, all TVP models yield reasonable estimates for constant coefficients, which is most important for forecasting applications. Focussing on the the fourth parameter, considering a more flexible model pays off to produce less biased and more precise estimates, especially when compared to the constant coefficient model. Second, the TVP-MIX specifications are capable in capturing both rapid shifts and smooth adjustments in the regression coefficients. Our methods in panel (a) and (b) tend to quickly adjust when facing high frequency changes, rendering the methods even more flexible when compared to a typical mixture innovation specification in panel (d). Third, the TVP-POOL model in panel (c) tends to detect sudden changes in the parameters quite well, but is less capable in capturing low frequency movements. This feature differs form a standard random walk evolution assumption on the TVPs. Assuming a standard random walk implies smoothly evolving coefficients makes capturing high frequency changes difficult. Interestingly, the time-varying intercept (the fifth coefficients) tends to soak up movements of other parameters. Models that do not truly detect the large breaks of the third coefficient are particularly prone to this issue (TVP-POOL but also TVP-RW specifications).

coefficient with true parameters:

coefficient with true parameters:

coefficient with true parameters:

coefficient with true parameters:

coefficient with true parameters:

(a) TVP-MIX with flexible state variances (FLEX) and (MS):

(b) TVP-MIX with flexible state variances (FLEX) and covariate-specific indicators (MIX):

(c) TVP-POOL with flexible state variances (FLEX) and covariate-specific indicators (MIX):

(d) TVP-RW with SSVS-type state variances (SSVS) and covariate-specific indicators (MIX):

6. Empirical application

Structural analysis and forecasting key macroeconomic indicators is of great relevance for policy makers. In the empirical work, we focus on output growth, inflation, unemployment, and/or the interest rate. Focussing on these variables we investigate the merits of our approach by using the popular quarterly US data described in McCracken and Ng (2016). The data set includes macroeconomic and financial variables and ranges from :Q to :Q.888In the empirical application we start with :Q and use the first observations for transformations.

In Subsection 6.1 we show some stylized in-sample features of our methods for a small-scale model. By including the four target variables in a small-scale VAR (henceforth S-VAR) we present posterior probabilities of the state indicator matrix and estimate the low-frequency relationship between unemployment and inflation (Phillips Curve). For instance, the recent literature highlights the existence of potential non-linear dynamics in both the inflation persistence and the relationship of the Phillips Curve in the US (for a thorough discussion, see Cogley et al., 2010; Ball and Mazumder, 2011; Watson, 2014; Coibion and Gorodnichenko, 2015).

Moreover, in Subsection 6.2, this variable set forms the basis for evaluating the predictive performance of our methods in a comprehensive forecast exercise. For the forecasting exercise, we consider two additional information sets. In our largest specification (L-VAR) we pick macroeconomic indicators, which are commonly considered by the recent literature for forecasting (see, for example, Huber et al., 2020a; Pfarrhofer, 2020).999In Appendix C we provide further details on the specific variable set, included in the largest specification, and the transformation applied. In particular, we include financial market indicators that carry important information about the future stance of the economy (see Bańbura et al., 2010). Moreover, we consider a factor-augmented VAR (FA-VAR). Here, we augment the target variables with six principal components compromising information of the remaining variables in the data set, effectively leading to VAR with ten endogenous variables.101010The number of principal components is motivated by the specification in Stock and Watson (2012), who also consider six factors. In such larger scale-models our methods are capable of handling less frequent (but important) parameter instabilities in a genuine way.

Especially forecasting these important macroeconomic aggregates remains a challenging task, since (at least) two issues arise. First, we have to decide on a set of variables, which we want to include in our econometric model. The recent literature on constant parameter VARs highlights that exploiting large information sets yields forecast gains (see, for example, Bańbura et al., 2010; Koop, 2013). Second, it is well documented that important economic indicators feature instabilities in structural parameters and innovation volatilities.111111See, for example Stock and Watson (2012), Ng and Wright (2013) and Aastveit et al. (2017), which put special emphasis on the recent financial crisis. In the literature there is strong agreement that SV is important in macroeconomic applications (see Clark, 2011). There is also strong empirical support for shifting parameters in small-scale models (see D’Agostino et al., 2013). However, there is less consensus for time-varying parameters in larger-scale models. With increasing amount of information overall time-variation in parameters tends to reduce. Recent contributions dealing with large-scale TVP-VARs argue that in smaller models the TVP part controls for an omitted variable bias (see Feldkircher et al., 2017; Huber et al., 2020b).121212Since estimating TVP models with typical MCMC methods remains computationally demanding, several studies take this argument as a reason to opt for approximating the TVP part or rely on dimension reduction techniques, yielding fast inference while accepting a certain risk of misspecification (see, inter alia Chan et al., 2020; Korobilis, 2019; Hauzenberger et al., 2020; Huber et al., 2020b; Korobilis and Koop, 2020).

In the following empirical application, note thate we consider two lags for every model and allow for SV.

6.1. In-sample evidence

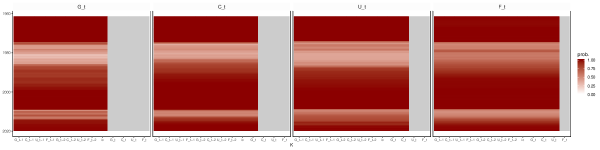

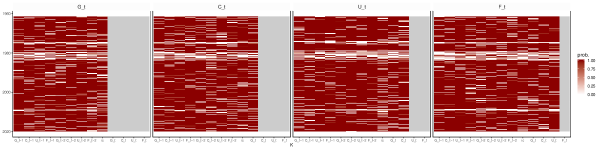

Before proceeding, we briefly elaborate on a potential identification problem when interpreting the state indicators (see Frühwirth-Schnatter, 2001). For the TVP-MIX models, identification is ensured by construction (if coefficients indeed feature time variation). Assuming (see Eq. (missing) 3) automatically imposes inequality constraints on the autoregressive coefficients in the state equation. However, non-identifiability can occur when coefficients are constant. In such a case, elements in are hard to interpret, since a no change evolution is supported by both a random walk and a white noise process. Interpreting for the TVP-POOL specification is an even more challenging task, since in these models solely controls the evolution of state innovations. Here, inference about the state indicator matrix is only useful in combination with inference about the size of state innovation variances and and with imposing an inequality restriction ex-post (for example, ).

Therefore, we solely focus on two variants of a TVP-MIX model to illustrate the switching behaviour. Figure 2 depicts the posterior median of the diagonal elements in . Panel (a) shows a TVP-MIX model with and following a first-order Markov process (MS). Panel (b) depicts a specification with elements in following an independent mixture distribution (MIX). A comparison between both approaches highlights that a joint indicator evidently leads to a different posterior median of than covariate-specific indicators. By restricting , all covariates are driven solely by a single indicator that pushes all covariates towards either a random walk or white noise state equation in period . Conversely, with covariate-specific indicators, we see more dispersion across covariates. However, both approaches agree on a white noise state equation in times of turmoil, suggesting a need for abruptly adjusting parameters in these periods. This model feature is in line with the discussion in Primiceri (2005), who suggests that an economically stable period favours more gradual changes (which are more consistent with a random walk state equation) in the coefficients, while shifts in policy rules require quickly adjusting coefficients (which is better captured by using a white noise state equation).

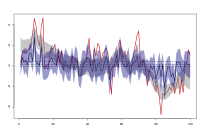

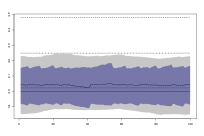

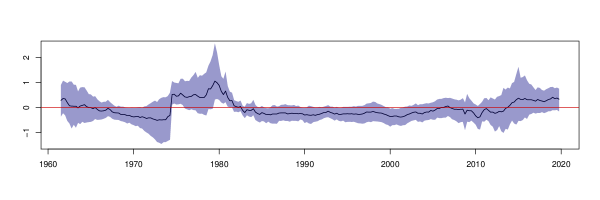

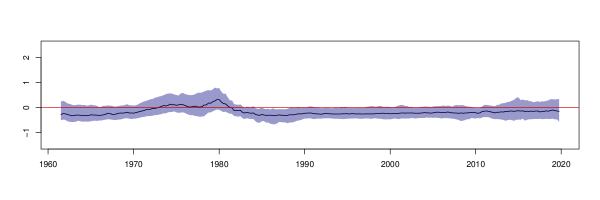

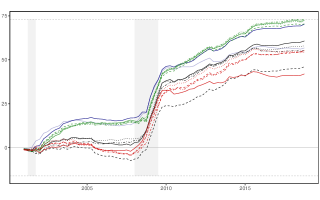

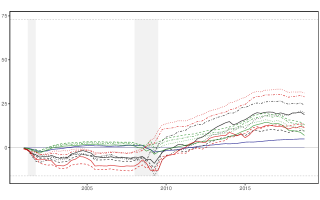

To further illustrate the proposed methods, we estimate the low-frequency relationship between unemployment and inflation. This low-frequency measure corresponds to a long-run coefficient of distributed-lag regression models (Whiteman, 1984) and disentangles systematic co-movements from short-run fluctuations.131313Sargent and Surico (2011) and Kliem et al. (2016) suggest that a TVP-VAR framework, additionally, allows to account for changes in the transmission channels (time-varying coefficients) and changes in the error volatilities (SV). For further details see Appendix A.4.

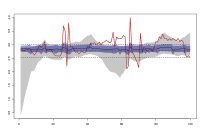

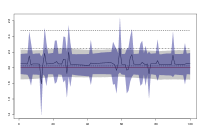

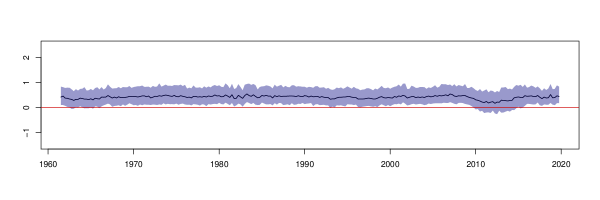

Panel (a) to (c) in Figure 3 depict the obtained low-frequency component with our proposed approaches and panel (d) shows estimates with a standard TVP model assuming a standard random evolution assumption. Starting with a comparison between the random walk/white noise mixture (TVP-MIX) and a classic random walk TVP model, we observe a similar pattern for both approaches during tranquil periods. However, during recessions, the approaches significantly differ. Both TVP-MIX models are capable of detecting a major structural break in the low-frequency relationship after the oil crisis in the 1970s and strongly support a long-lasting stagflation period (i.e. positive relationship between unemployment and inflation). While TVP-MIX methods are designed to quickly capture these large abrupt breaks in parameters, a standard random walk state equation translates into a low-frequency component that gradually adapts over time. However, the TVP-MIX model with covariate-specific indicators MIX is slightly more sensitive with respect to abrupt changes in parameters than the TVP-MIX MS model.

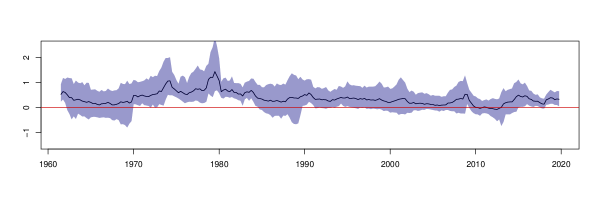

Panel (c) shows the sparse scale-location mixture (TVP-POOL) approach with covariate-specific indicators (MIX). We observe that this method almost resembles a constant coefficient specification with SV. In the mid 1980s and in the financial crisis movement in the low-frequency relationship is slightly more erratic compared to other periods, but it stays mostly constant and significant.

Overall, considering TVP-MIX methods seem to improve the economic interpretability of the low-frequency component, while a TVP-POOL model aggressively pushes coefficients towards a constant evolution, which could pay off for forecasting.

(a) with following an MS process:

(b) Elements in follow an independent mixture specification:

(a) TVP-MIX with flexible state variances (FLEX) and (MS):

(b) TVP-MIX with flexible state variances (FLEX) and covariate-specific indicators (MIX):

(c) TVP-POOL with flexible state variances (FLEX) and covariate-specific indicators (MIX):

(d) Standard TVP-VAR with random walk state equation:

6.2. Forecasting evidence

In the forecast exercise we consider a wide range of models varying along the evolution assumption of parameters and the information set considered.

With respect to the evolution of parameters, it proves convenient to summarize the different specifications (see Table 1). The models differ along three dimensions: the autoregressive parameters , the innovation variances and the state indicator matrix . First, our main specifications vary between a model that assumes a binary indicator matrix on the autoregressive parameter with (labeled as TVP-MIX) and a model that introduces a hierarchical prior on the TVP-part (TVP-POOL). For the latter we implicitly assume that , for all , in Eq. (missing) 5. Regarding the autoregressive parameter, a natural competing model is a standard random walk assumption with , for all (TVP-RW). Second, the models differ in the treatment of the state innovation variances. The most flexible innovation variance specification does not restrict and (labeled as FLEX), a second specification assumes (SSVS), while the most restrictive specification fixes , for all , to a a single variance state (SINGLE). In the empirical exercise, we set and with , for, , denoting ordinary least square (OLS) variances obtained from an AR() model (see Huber et al., 2019). Third, with regards to the state indicator matrix , we discriminate between a joint Markov-switching indicator (labeled as MS) and covariate-specific indicators following an independent mixture distribution (MIX). Recall, that for the TVP-MIX models adjusts both the autoregressive parameters and the state innovation variances, while for the TVP-POOL and TVP-RW models only controls the state innovations. In the following, we define TVP-MIX, TVP-POOL and TVP-RW as the Class of the TVP model and the combination of the acronyms for the innovation variances and indicator matrix as the Subclass of the specification. A single model is identified by a combination of all three acronyms. For example, a TVP-MIX FLEX MIX specification denotes a model with a random walk/white noise mixture for the state equation, with unrestricted two-state variances and with the elements in following an independent mixture distribution.

| TVP-MIX | Related to: | |||

|---|---|---|---|---|

| FLEX MS | ||||

| FLEX MIX | ||||

| SINGLE | ||||

| SSVS MIX | Chan et al. (2012) | |||

| TVP-POOL | ||||

| FLEX MS | ||||

| FLEX MIX | ||||

| SINGLE | Hauzenberger et al. (2019) | |||

| SSVS MIX | ||||

| TVP-RW | ||||

| FLEX MS | ||||

| FLEX MIX | ||||

| SINGLE | Standard TVP-RW | |||

| SSVS MIX | e.g. Huber et al. (2019) |

All these TVP models feature a Normal-Gamma (Griffin and Brown, 2010) on .141414Note with a single-state variance (), collapses to a -dimensional vector (see Bitto and Frühwirth-Schnatter, 2019). We compare our methods to two constant parameter models.151515A constant coefficient model can be obtained by either offsetting or setting . One variant features a Normal-Gamma (const. (NG)) prior, while the second variant assumes a Minnesota (const. (MIN)) prior. We consider a non-conjugate Minnesota prior, capturing the notion that own lags are more important than lags from other variables (Doan et al., 1984; Litterman, 1986). We estimate this set of models for three information sets (FA-VAR, L-VAR and S-VAR) with each featuring a different number of endogenous variables. Every considered specification features two lags and SV.

To asses one-quarter-, one-year- and two-year-ahead predictions, we treat observations ranging from :Q to :Q as an initial sample and the periods from :Q to :Q as a hold-out sample. The initial sample is then recursively expanded until the penultimate quarter (:Q) is reached. For each forecast comparison, a small-scale Minnesota VAR with constant parameters (S-VAR const. (MIN)) serves as our benchmark. In the following, Table 2 shows the best performing models for point and density forecasts, being a tractable summary of Table 3 and Table 4. Table 3 depicts root-mean squared error ratios (RMSEs) as point forecast measures and Table 4 the log predictive Bayes factors (LPBFs) as density forecast metrics. The best performing models within each column are indicated by bold numbers. In Table B.1 we provide additional results on continuous rank probability score (CRPS) ratios. This alternative density forecast measure is more robust to outliers than log predictive scores (Gneiting and Raftery, 2007). With three different measures at three different horizons we obtain a comprehensive picture to evaluate our methods jointly and marginally along the four target variables.

| Variable | 1-quarter-ahead | 1-year-ahead | 2-years-ahead | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Size | Class | Subclass | Size | Class | Subclass | Size | Class | Subclass | ||||

| Point forecasts | ||||||||||||

| RMSE ratios | ||||||||||||

| TOT | L-VAR | TVP-POOL | SINGLE | L-VAR | TVP-POOL | SINGLE | FA-VAR | TVP-POOL | SINGLE | |||

| GDPC1 | L-VAR | TVP-POOL | FLEX MIX | FA-VAR | TVP-POOL | FLEX MS | FA-VAR | TVP-MIX | FLEX MIX | |||

| CPIAUCSL | S-VAR | TVP-MIX | FLEX MIX | S-VAR | TVP-RW | FLEX MIX | L-VAR | TVP-RW | SINGLE | |||

| UNRATE | L-VAR | TVP-POOL | SSVS MIX | L-VAR | TVP-POOL | SINGLE | FA-VAR | TVP-POOL | SSVS MIX | |||

| FEDFUNDS | FA-VAR | TVP-RW | SSVS MIX | FA-VAR | TVP-RW | SSVS MIX | FA-VAR | TVP-POOL | SINGLE | |||

| Density forecasts | ||||||||||||

| LPBFs | ||||||||||||

| TOT | L-VAR | TVP-POOL | FLEX MIX | L-VAR | TVP-POOL | SSVS MIX | L-VAR | const (NG.) | ||||

| GDPC1 | L-VAR | TVP-POOL | FLEX MS | FA-VAR | TVP-POOL | SSVS MIX | FA-VAR | TVP-POOL | SINGLE | |||

| CPIAUCSL | S-VAR | TVP-MIX | SSVS MIX | L-VAR | const. (NG) | L-VAR | const. (NG) | |||||

| UNRATE | L-VAR | TVP-POOL | SSVS MIX | L-VAR | TVP-POOL | SSVS MIX | L-VAR | TVP-MIX | SSVS MIX | |||

| FEDFUNDS | L-VAR | TVP-POOL | SSVS MIX | FA-VAR | TVP-RW | FLEX MIX | FA-VAR | const. (Min) | ||||

Table 2 summarizes the main findings of our forecast exercise. First, larger-scale models (FA-VAR, L-VAR) generally outperform the small-scale specifications across horizon-variable combinations, indicating that an increasing amount of information pays off for forecasting (see Bańbura et al., 2010). One exception is inflation. For inflation, flexible S-VARs yield more accurate forecasts than FA-VARs and L-VARs for one-quarter- and one-year-ahead point forecasts and one-quarter-ahead density forecasts. Comparing FA-VARs with L-VARs, the results are mixed. One pattern worth noting is that L-VARs tend to outperform FA-VARs for the one-quarter-ahead horizon while the picture reverses for higher-order forecasts. Second, with respect to parameter changes we see that the TVP-POOL specifications forecast particularly well across all horizons and target variables. These models substantially improve upon a wide range of benchmarks. Overall, Table 2 shows that all TVP classes that provide accurate point predictions generally also perform well in terms of density forecasts.

| Specification | 1-quarter-ahead | 1-year-ahead | 2-years-ahead | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Class | Subclass | TOT | GDPC1 | CPIAUCSL | UNRATE | FEDFUNDS | TOT | GDPC1 | CPIAUCSL | UNRATE | FEDFUNDS | TOT | GDPC1 | CPIAUCSL | UNRATE | FEDFUNDS | ||||

| FA-VAR | ||||||||||||||||||||

| const. (Min.) | 0.91* | 0.87 | 0.94 | 0.79 | 1.22 | 0.92** | 0.84* | 1.03 | 0.80 | 1.11 | 0.93* | 1.00 | 1.04 | 0.86 | 0.78*** | |||||

| const. (NG) | 0.88** | 0.81* | 0.95 | 0.80 | 1.14 | 0.90** | 0.84** | 0.99 | 0.81 | 1.02 | 0.92 | 1.00 | 1.01 | 0.87 | 0.75** | |||||

| TVP-MIX | FLEX MIX | 0.89** | 0.80* | 0.97 | 0.81 | 0.91 | 0.94* | 0.92 | 0.98 | 0.88 | 0.98 | 1.01 | 0.86 | 1.10* | 1.08 | 0.95 | ||||

| FLEX MS | 0.91** | 0.83 | 0.98 | 0.77 | 0.89 | 0.91 | 0.89 | 1.00 | 0.80 | 0.83* | 0.94 | 0.96 | 1.00 | 0.92 | 0.89 | |||||

| SINGLE | 0.92* | 0.82 | 1.01 | 0.79 | 0.85** | 0.91* | 0.87 | 1.00 | 0.81 | 0.86* | 0.97 | 0.93 | 1.12 | 0.94 | 0.87 | |||||

| SSVS MIX | 0.89** | 0.83 | 0.96 | 0.79 | 0.95 | 0.92* | 0.89 | 0.98 | 0.83 | 0.98 | 0.95 | 0.93 | 1.09 | 0.88 | 0.92 | |||||

| TVP-POOL | FLEX MIX | 0.88** | 0.79* | 0.95 | 0.77 | 1.06 | 0.88** | 0.80** | 0.99 | 0.77 | 0.96 | 0.89 | 0.95 | 1.01 | 0.82 | 0.73* | ||||

| FLEX MS | 0.88*** | 0.79* | 0.96 | 0.76 | 1.05 | 0.87** | 0.80** | 0.98 | 0.77 | 0.97 | 0.89 | 0.96* | 1.00 | 0.82 | 0.73* | |||||

| SINGLE | 0.87*** | 0.79* | 0.95 | 0.77 | 1.05 | 0.87** | 0.81** | 0.98 | 0.77 | 0.95 | 0.88 | 0.94** | 1.00 | 0.82 | 0.73* | |||||

| SSVS MIX | 0.89** | 0.81* | 0.96 | 0.76 | 1.06 | 0.88** | 0.81** | 1.00 | 0.77 | 0.98 | 0.89 | 0.98 | 1.01 | 0.82 | 0.73* | |||||

| TVP-RW | FLEX MIX | 0.89** | 0.83 | 0.95 | 0.77 | 0.89** | 0.88* | 0.86 | 0.97 | 0.76 | 0.81** | 0.93 | 1.00 | 1.00 | 0.88 | 0.79 | ||||

| FLEX MS | 0.89** | 0.80 | 0.96 | 0.80 | 0.91 | 0.90* | 0.88 | 0.99 | 0.79 | 0.87 | 0.95 | 1.00 | 1.00 | 0.93 | 0.83 | |||||

| SINGLE | 0.91* | 0.83 | 0.99 | 0.81 | 0.92 | 1.04 | 0.99 | 1.07 | 1.02 | 1.23 | 1.20 | 0.90 | 1.24 | 1.30* | 1.36 | |||||

| SSVS MIX | 0.92* | 0.84 | 0.99 | 0.79 | 0.83** | 0.90* | 0.90 | 0.96 | 0.83 | 0.80* | 0.96 | 0.99 | 1.02 | 0.94 | 0.83 | |||||

| L-VAR | ||||||||||||||||||||

| const. (Min.) | 1.02 | 0.99 | 1.05 | 0.72 | 1.52 | 0.92** | 0.93 | 0.95* | 0.79 | 1.00 | 0.97** | 1.02 | 0.98 | 0.95 | 0.88** | |||||

| const. (NG) | 0.91** | 0.85 | 0.96 | 0.71 | 1.10 | 0.88*** | 0.89* | 0.92** | 0.74 | 0.98 | 0.92** | 1.00 | 0.97 | 0.89 | 0.79** | |||||

| TVP-MIX | FLEX MIX | 1.04 | 0.90 | 1.14 | 0.71 | 2.19 | 0.91* | 0.82 | 1.02 | 0.81 | 1.09 | 0.92 | 0.93 | 0.99 | 0.89 | 0.90 | ||||

| FLEX MS | 1.06 | 0.92 | 1.17 | 0.72 | 1.51 | 0.90* | 0.86 | 0.95 | 0.79 | 1.08 | 1.22 | 1.56 | 1.30 | 0.90 | 1.13 | |||||

| SINGLE | 0.92* | 0.86 | 0.98 | 0.74 | 0.90** | 0.87* | 0.82* | 0.94 | 0.83 | 0.87* | 0.92 | 0.94 | 0.97 | 0.91 | 0.86 | |||||

| SSVS MIX | 0.96 | 0.98 | 0.94 | 0.72 | 1.20 | 0.90 | 0.86 | 0.98 | 0.78 | 1.00 | 0.95 | 0.96 | 1.06 | 0.91 | 0.89 | |||||

| TVP-POOL | FLEX MIX | 0.88*** | 0.79** | 0.96 | 0.68 | 0.86*** | 0.87** | 0.87 | 0.94 | 0.74 | 0.89** | 0.91 | 0.99 | 1.01 | 0.84 | 0.79** | ||||

| FLEX MS | 0.88*** | 0.82* | 0.94 | 0.67 | 0.87*** | 0.86** | 0.85* | 0.94 | 0.72 | 0.90** | 0.90 | 0.99 | 0.99 | 0.83 | 0.77** | |||||

| SINGLE | 0.87*** | 0.79** | 0.95 | 0.68* | 0.88*** | 0.86** | 0.86* | 0.93 | 0.71 | 0.88** | 0.91 | 0.99 | 0.99 | 0.84 | 0.78** | |||||

| SSVS MIX | 0.88*** | 0.81* | 0.95 | 0.67* | 0.89*** | 0.86** | 0.85* | 0.94 | 0.72 | 0.88** | 0.90 | 0.98 | 1.01 | 0.83 | 0.78** | |||||

| TVP-RW | FLEX MIX | 0.96 | 0.97 | 0.97 | 0.71 | 1.09 | 0.88* | 0.85 | 0.94 | 0.80 | 0.93* | 0.95 | 1.00 | 0.97 | 0.94 | 0.87 | ||||

| FLEX MS | 0.98 | 0.97 | 0.99 | 0.73 | 0.93** | 0.86* | 0.81* | 0.92 | 0.84 | 0.96 | 0.96 | 0.97 | 0.96 | 0.96 | 0.93 | |||||

| SINGLE | 1.24 | 1.09 | 1.37 | 0.75 | 1.75 | 0.93 | 0.88 | 0.97*** | 0.84 | 1.23 | 0.94 | 0.91 | 0.93 | 0.96 | 0.95 | |||||

| SSVS MIX | 0.94 | 0.93 | 0.95 | 0.73 | 1.17 | 0.88* | 0.85 | 0.93 | 0.82 | 0.97 | 0.96 | 0.95 | 0.98 | 0.95 | 0.95 | |||||

| S-VAR | ||||||||||||||||||||

| const. (Min.) | 0.60 | 0.83 | 0.85 | 0.15 | 0.11 | 0.76 | 1.00 | 0.87 | 0.62 | 0.41 | 0.91 | 0.93 | 0.85 | 1.10 | 0.73 | |||||

| const. (NG) | 0.99** | 0.99* | 0.99 | 1.00 | 1.01 | 0.96** | 0.94* | 0.98 | 0.98* | 0.98 | 0.97 | 0.99 | 0.98 | 0.97** | 0.95 | |||||

| TVP-MIX | FLEX MIX | 0.93** | 0.94* | 0.92 | 0.92 | 0.91*** | 0.89 | 0.84 | 0.94 | 0.92 | 0.93 | 0.93 | 0.89 | 1.01 | 0.93 | 0.92 | ||||

| FLEX MS | 0.96 | 0.96 | 0.96 | 0.91 | 0.87 | 0.93 | 0.92 | 0.95 | 0.91 | 0.96 | 0.96 | 0.97 | 1.01 | 0.92 | 0.95 | |||||

| SINGLE | 0.97 | 0.97 | 0.96 | 0.97 | 0.85* | 0.93 | 0.91 | 0.95 | 0.95 | 0.97 | 0.95 | 0.96 | 0.99 | 0.94 | 0.93 | |||||

| SSVS MIX | 0.95** | 0.96 | 0.94** | 0.98 | 0.94*** | 0.91* | 0.86 | 0.94 | 0.93 | 0.92 | 0.95 | 0.94 | 1.00 | 0.94 | 0.92 | |||||

| TVP-POOL | FLEX MIX | 0.98*** | 0.97** | 0.99 | 0.95 | 0.98 | 0.95** | 0.93* | 0.98 | 0.94 | 0.94 | 0.95 | 0.99 | 0.96 | 0.93 | 0.90 | ||||

| FLEX MS | 0.98** | 0.98* | 0.98 | 0.94** | 0.98* | 0.95** | 0.94* | 0.98 | 0.94 | 0.94 | 0.95 | 0.99 | 0.97 | 0.93 | 0.90* | |||||

| SINGLE | 0.98** | 0.98* | 0.99 | 0.94 | 0.98 | 0.95** | 0.93* | 0.99 | 0.94 | 0.94 | 0.95 | 0.99 | 0.97 | 0.93 | 0.90 | |||||

| SSVS MIX | 0.98** | 0.98* | 0.99 | 0.95 | 0.97* | 0.95** | 0.93* | 0.98* | 0.95 | 0.94 | 0.94 | 0.98 | 0.97 | 0.92 | 0.91 | |||||

| TVP-RW | FLEX MIX | 0.96** | 0.96 | 0.95 | 0.97 | 0.92** | 0.93* | 0.94 | 0.91 | 0.95 | 0.94 | 0.96 | 0.98 | 0.96 | 0.95 | 0.94 | ||||

| FLEX MS | 0.98 | 0.99 | 0.97 | 0.98 | 0.88* | 0.93 | 0.91 | 0.93 | 0.96 | 0.98 | 0.95 | 0.94 | 0.99 | 0.95 | 0.94 | |||||

| SINGLE | 0.96 | 0.92 | 1.00 | 0.92 | 0.86*** | 0.89 | 0.82 | 0.95 | 0.94 | 0.90 | 0.93 | 0.88 | 1.00 | 0.96 | 0.85 | |||||

| SSVS MIX | 0.98 | 1.00 | 0.96 | 0.98 | 0.89* | 0.94 | 0.92 | 0.93 | 0.99 | 0.97 | 0.97 | 0.96 | 0.97 | 0.97 | 0.95 | |||||

| Specification | 1-quarter-ahead | 1-year-ahead | 2-years-ahead | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Class | Subclass | TOT | GDPC1 | CPIAUCSL | UNRATE | FEDFUNDS | TOT | GDPC1 | CPIAUCSL | UNRATE | FEDFUNDS | TOT | GDPC1 | CPIAUCSL | UNRATE | FEDFUNDS | ||||

| FA-VAR | ||||||||||||||||||||

| const. (Min.) | 11.35 | 12.01** | 2.23 | 8.56 | -4.19 | 14.59 | 8.30** | 2.02 | 14.03 | 8.69 | 37.98** | 2.12 | 5.63 | 12.49 | 30.86*** | |||||

| const. (NG) | 18.88 | 13.48*** | 4.19 | 8.66 | 0.46 | 25.90*** | 9.01*** | 2.34 | 14.21 | 10.93 | 40.82*** | 3.08 | 7.01 | 12.22 | 28.66*** | |||||

| TVP-MIX | FLEX MIX | 23.23 | 12.71** | 2.78 | 11.15 | 12.95*** | 39.12** | 7.60 | 2.33 | 26.49 | 16.00 | 50.99 | 3.80 | 3.97 | 23.44 | 13.09 | ||||

| FLEX MS | 29.37 | 11.74** | 5.32 | 13.84 | 9.59* | 49.54** | 7.49 | 2.32 | 27.51 | 17.64 | 41.96 | 0.10 | 3.65 | 22.67 | 13.22 | |||||

| SINGLE | 24.87 | 11.07** | 2.24 | 10.12 | 17.01*** | 52.21** | 6.25 | 0.25 | 25.16 | 24.39 | 55.19 | 0.70 | 3.17 | 22.70 | 18.79 | |||||

| SSVS MIX | 25.93 | 13.23** | 2.59 | 10.60 | 6.38* | 40.29* | 7.92* | 1.90 | 23.53 | 10.64 | 40.57 | 3.38 | 1.82 | 25.83 | 7.45 | |||||

| TVP-POOL | FLEX MIX | 26.23 | 13.49*** | 3.44 | 10.51 | 7.28*** | 39.69*** | 10.63** | 2.06 | 19.71 | 15.86 | 53.01** | 3.61 | 6.18 | 22.98 | 28.67* | ||||

| FLEX MS | 28.06 | 14.49*** | 3.98* | 10.24 | 7.62*** | 34.75** | 10.85*** | 2.71 | 17.29 | 14.71 | 52.55** | 4.07 | 6.27 | 21.13 | 28.34* | |||||

| SINGLE | 25.63 | 14.42*** | 2.98 | 10.61 | 6.20*** | 34.67** | 10.54*** | 2.21 | 18.32 | 16.06 | 46.04** | 4.36 | 6.22 | 19.52 | 26.47 | |||||

| SSVS MIX | 25.54 | 14.08*** | 3.17* | 10.06 | 6.84*** | 35.28** | 11.02*** | 1.59 | 18.01 | 15.29 | 50.57** | 4.04 | 6.74 | 23.07 | 28.09 | |||||

| TVP-RW | FLEX MIX | 37.26 | 11.40** | 7.35** | 12.30 | 17.50*** | 63.22** | 7.80 | 1.93 | 29.72 | 27.66 | 69.42* | -1.76 | 5.94 | 27.99 | 29.14 | ||||

| FLEX MS | 26.44 | 11.88*** | 5.01 | 11.44 | 11.10** | 53.18** | 7.23 | 0.70 | 24.70 | 20.65 | 38.45 | -0.47 | 4.42 | 21.35 | 18.47 | |||||

| SINGLE | 20.52 | 11.81** | -2.21 | 11.01 | 13.10*** | 46.68** | 4.46 | 2.24 | 19.20 | 17.68 | 45.86 | -1.09 | -0.24 | 13.83 | 16.93 | |||||

| SSVS MIX | 38.78 | 11.12** | 6.46 | 9.69 | 16.94*** | 47.25*** | 6.07 | 0.96 | 21.05 | 27.08 | 47.06* | -1.64 | 5.28 | 17.38 | 25.21 | |||||

| L-VAR | ||||||||||||||||||||

| const. (Min.) | 15.05 | 13.32* | -0.29 | 12.15 | -3.68*** | 56.73** | 2.78 | 3.22*** | 32.41 | 11.78*** | 61.59*** | -3.86 | 3.18 | 15.52 | 18.28** | |||||

| const. (NG) | 28.70 | 15.97*** | 1.06 | 14.87 | 2.34 | 70.27*** | 7.40** | 6.76*** | 36.48 | 16.42* | 73.50*** | 0.33 | 8.80* | 17.46** | 21.68*** | |||||

| TVP-MIX | FLEX MIX | 21.50 | 13.39** | -3.42 | 14.97 | 6.06 | 57.99* | 7.63 | -0.49 | 36.44 | 6.38 | 50.44 | -3.40 | -0.52 | 27.14 | -1.18 | ||||

| FLEX MS | 13.65* | 10.32* | -0.35 | 13.39 | 7.88 | 46.02 | 6.19 | -0.16 | 32.55 | 7.15 | 44.48 | -6.69 | -0.73 | 28.69 | 0.75 | |||||

| SINGLE | 28.03 | 12.75** | 1.04 | 13.65 | 12.62 | 60.71* | 8.02 | 2.15 | 32.82 | 12.23 | 60.21 | -3.28 | 1.74 | 28.66 | 7.41 | |||||

| SSVS MIX | 16.40* | 11.52** | 1.00 | 12.90 | 11.67 | 55.25* | 8.09 | -0.77 | 34.05 | 9.97 | 41.64 | -0.87 | 1.23 | 31.10 | 1.53 | |||||

| TVP-POOL | FLEX MIX | 54.32 | 16.63*** | 0.86 | 16.78 | 22.62*** | 71.86*** | 8.08* | 3.09 | 35.86 | 24.24 | 63.16*** | 0.27 | 2.73 | 22.08 | 21.52** | ||||

| FLEX MS | 50.88 | 17.28*** | 1.72 | 16.95 | 21.29*** | 70.43** | 8.02** | 2.27 | 36.55 | 24.52 | 65.07*** | -0.06 | 2.43 | 20.10 | 22.50** | |||||

| SINGLE | 51.15 | 16.22*** | 1.44 | 16.75 | 22.24*** | 72.35*** | 8.14* | 2.47 | 36.30 | 24.31 | 60.97*** | -0.50 | 2.74 | 24.76 | 20.51 | |||||

| SSVS MIX | 49.90 | 16.39*** | -0.50 | 17.15 | 23.32*** | 73.08** | 6.80* | 2.06 | 36.87 | 25.34 | 63.73*** | -1.29 | 2.69 | 19.82 | 22.33* | |||||

| TVP-RW | FLEX MIX | 29.38 | 10.54** | 1.22 | 11.09 | 12.63 | 54.24 | 3.78 | 1.28 | 27.88 | 17.50 | 59.54 | -7.53 | -0.86 | 28.15 | 15.32 | ||||

| FLEX MS | 15.46 | 9.99** | -8.43 | 11.68 | 13.28 | 55.15* | 5.85 | 1.40 | 28.01 | 13.82 | 41.09 | -5.25 | -0.64 | 25.89 | 6.06 | |||||

| SINGLE | 12.39 | 12.04** | -1.38 | 12.34 | 7.23 | 41.96 | 4.35 | 0.38 | 28.51 | -2.50 | 28.63 | -9.08* | 0.76 | 20.03 | -6.91 | |||||

| SSVS MIX | 18.47 | 9.93* | 0.81 | 11.50 | 13.63 | 55.11 | 4.67 | 2.12 | 27.41 | 13.44 | 46.83 | -3.83 | 1.76 | 23.01 | 6.32 | |||||

| S-VAR | ||||||||||||||||||||

| const. (Min.) | -22.11 | -82.64 | -80.74 | 45.02 | 86.64 | -256.48 | -97.26 | -83.70 | -69.04 | -29.94 | -383.84 | -92.27 | -89.84 | -125.53 | -87.85 | |||||

| const. (NG) | 4.55 | 1.97* | 0.71 | 0.62* | 1.39*** | 4.97 | 2.64* | 1.95* | 0.03 | 2.30 | 9.15 | 0.58 | 3.07 | 2.99 | 1.37 | |||||

| TVP-MIX | FLEX MIX | 24.41 | 3.97* | 5.52 | 2.90 | 12.18*** | 15.60 | 9.64** | 3.98 | 8.50 | 5.03 | -3.76 | 3.00 | 3.74 | -0.02 | -7.71 | ||||

| FLEX MS | 18.00 | 2.66 | 3.57 | 6.42 | 5.86** | 9.48 | 5.25* | -0.44 | 12.27 | -0.22 | 0.77 | -1.60 | 0.83 | 10.35 | -11.26 | |||||

| SINGLE | 7.18** | 2.45 | -1.98 | 0.85 | 13.26*** | 12.51 | 5.42 | 3.33 | 6.38 | 7.12* | -0.80 | -2.74 | 1.19 | 2.14 | -5.03 | |||||

| SSVS MIX | 23.21 | 3.44* | 8.67** | 2.67 | 7.84*** | 22.03 | 6.18 | 1.77 | 10.22 | 5.15 | 15.68 | 1.32 | 6.23 | 14.46 | -3.63 | |||||

| TVP-POOL | FLEX MIX | 16.39 | 2.47*** | 2.63** | 1.29 | 6.18*** | 9.34 | 3.10* | 1.70 | 3.87* | 5.15 | 14.86 | 0.07 | 3.60* | 6.37 | 0.56 | ||||

| FLEX MS | 14.35 | 2.30** | 1.26* | 1.66 | 7.91*** | 11.74 | 3.65*** | 2.04** | 7.55* | 6.02 | 14.99 | -0.16 | 4.04** | 8.28 | 1.86 | |||||

| SINGLE | 16.46 | 2.68*** | 2.61* | 1.84 | 6.99*** | 5.61 | 3.52** | 1.73 | 3.43 | 5.59 | 14.77 | 0.21 | 3.13 | 10.10 | -0.22 | |||||

| SSVS MIX | 18.75 | 2.40** | 2.84* | 1.84 | 7.03*** | 11.67 | 3.66** | 2.70*** | 4.44** | 5.74 | 12.63 | 0.51 | 3.68** | 7.64 | 0.59 | |||||

| TVP-RW | FLEX MIX | 22.15 | 2.35 | 5.20*** | 2.14 | 11.56*** | 31.13* | 4.67 | 6.61* | 10.96 | 9.42 | 23.66 | -2.07 | 7.42 | 11.93 | 2.23 | ||||

| FLEX MS | 17.02 | 1.76 | 2.62 | 1.98 | 8.41** | 10.37 | 4.80 | 1.87 | 8.30 | 2.86 | 7.89 | -2.64 | 4.15 | 3.79 | -7.05 | |||||

| SINGLE | 13.68 | 6.02** | -3.98 | 1.79 | 12.17*** | 6.72 | 8.60 | 1.15 | 1.63 | 13.13 | -11.49 | 2.34 | 0.87 | -7.78 | 3.09 | |||||

| SSVS MIX | 20.25 | 1.26 | 5.76* | 0.31 | 12.10*** | 28.93* | 5.73 | 5.24 | 6.34 | 9.14 | 16.00 | -2.42 | 6.40 | 4.74 | -2.84 | |||||

When examining Table 3 and Table 4 in greater detail, note that a large number of models shown in the tables outperform the Minnesota benchmark in terms of RMSEs (indicated by ratios below one) and in terms of LPBFs (indicated by values above zero). However, the benchmark is a tough competitor when predicting inflation and for higher-order point forecasts. In particular, the result that inflation is hard to predict is a well-known fact in the literature (Stock and Watson, 2007). Commonly, it is found here that more sophisticated models with large information sets are outperformed by rather small-sized and simple models (see, for example, Giannone et al., 2015).

When focussing on the differences occuring through the varying treatment of parameter evolutions, our proposed methods, the TVP-POOL and TVP-MIX specifications, show that their good performance is mainly driven by improved forecast accuracy for output growth and unemployment. In terms of the innovation variance assumption for these specifications, we observe that additional flexibility tends to improve density forecasts performance and yields accurate point forecasts. For the TVP-POOL models this higher degree of flexibility generally pays off across variables and model sizes. For flexible TVP-MIX specifications, forecast ability tends to improve for S-VARs and FA-VARs and is competitive for the L-VARs. Especially the TVP-MIX SSVS MIX and TVP-MIX FLEX MIX models using a small information set yield quite accurate inflation forecasts, being the best performing models for the one-quarter-ahead horizon. Across variables, a notable exceptions is the interest rate for TVP-MIX models. Here, a TVP-MIX SINGLE specification is superior to models assuming a mixture on innovation volatilities.

When assessing random walk state equation (TVP-RW) specifications across the information sets, two things are worth noting. First, a standard TVP model with random walk assumption TVP-RW SINGLE is only competitive for one-year- and two-year-ahead forecasts and otherwise forecasts poorly. Second, more flexible TVP-RW variants produce quite accurate forecasts for FA-VARs. Constant parameter models with a Normal-Gamma prior show reasonable forecasts for L-VARs (especially for inflation), but lack flexibility in smaller-scale models. This observation is in line with the fact that in larger-scale model, time-variation in coefficients vanishes (see Huber et al., 2020b). However, few parameter instabilities might still be present since, apart from some exceptions, our methods provide improvements when compared to constant coefficient models.

(a) FA-VAR

(b) L-VAR

(c) S-VAR

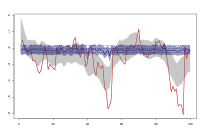

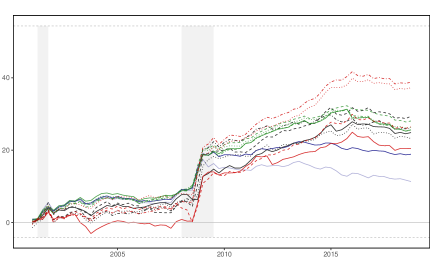

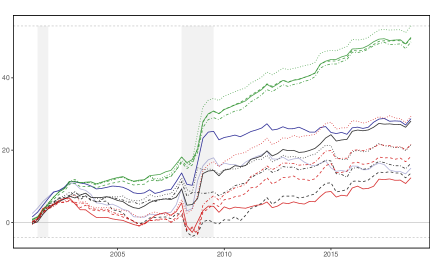

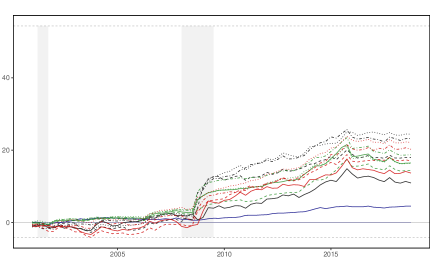

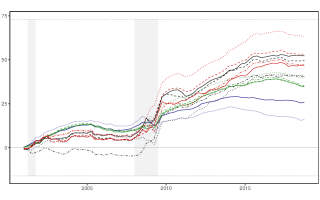

To illustrate the forecast performance over time, Figure 4 depicts the evolution of cumulated joint LPBFs relative to our benchmark. Overall we find that for all four target variable jointly our proposed methods never forecast poorly. Both TVP-MIX (black lines) and TVP-POOL (green lines) methods outperform a standard TVP model with random walk state equation (TVP-RW SINGLE denoted by the red solid line) across information sets (one exception is the TVP-MIX SINGLE model for the S-VAR). Moreover, allowing for occasional parameter changes during and in the aftermath of financial crisis tends to increase predictive ability.

A few points are worth discussing in greater detail. First, at the beginning of the hold-out sample is characterized by the early 2000s recession. Although this was a quite short crisis, it already leads to a quite diverse model performance across information sets. During this episode and its consecutive three years, L-VARs strictly dominate the other two information sets (FA-VARs and S-VARs). This implies, that for any TVP evolution assumption, the large-scale model outperforms its smaller-scale counterparts. Moreover, during the financial crisis, we observe a substantial increase in LPBFs for a wide range of FA-VARs and L-VARs, while for S-VARs we see similar improvements solely for some TVP-VARs. This feature might indicate that TVPs are capable of mitigating a potential omitted variable bias (Huber et al., 2020b).

Second, within each information set, performance across parameter evolution assumptions is mixed. Evidently, performance of the four L-VARs featuring a TVP-POOL specification stands out (depicted by green lines). In more tranquil periods they show constant improvements and yield substantial predictive gains during the financial crisis. Especially in the aftermath of the Great Recession, the LPBFs steadily increase compared to other large TVP-VARs. This episode also includes a time characterized by a (sluggish) recovery of the US economy after the financial crisis and the interest rate hitting the zero lower bound. With monetary policy shifting towards unconventional measures it might not only pay off to include financial market variables, such as longer-term yields, but also to allow for occasional changes in transmission channels in these variables. Moreover, it is worth noting that the four TVP-POOL variants tend to perform almost identical until 2010, while afterwards slight performance differences become evident. Hauzenberger et al. (2019) have made a similar observation, when varying the hyperparameters on their conjugate prior of the state equation.

Third, TVP-MIX methods generally forecast well for S-VARs and FA-VARs, while for L-VARs only the TVP-MIX SINGLE specification yields substantial gains. In particular for FA-VARs and S-VARs, a flexible variance modelling (TVP-MIX FLEX MIX and TVP-MIX SSVS MIX) generally pays off. For L-VARs these two models also yield reasonable forecast accuracy, while the TVP-MIX MS forfeits forecast accuracy. Thus, for a large-scale model, the assumption that a joint indicator governs the evolution of large number of coefficients might be less appropriate. Moreover, comparing TVP-MIX with TVP-RW specifications reveals that the random walk/white noise mixture yields gains in tranquil periods for larger-scale models (FA-VARs and L-VARs) and does particularly well in recessions for the small information set (S-VAR). Especially for small-scale VARs the TVP-MIX variants, featuring a mixture distribution on the state innovation volatilities, greatly improve predictive performance relative to TVP-RW models during the financial crisis. Moreover, it is worth noting that the TVP-RW SINGLE model forecasts poorly for larger-scale models (FA-VARs and L-VARs) during tranquil periods previous to the financial crisis, while performance slightly recovers in the middle of the Great Recession. A plausible explanation for this pattern might be that spurious movements in coefficients lead to overfitting, widening the predictive density of the TVP-RW SINGLE model. This feature is harming predictive accuracy in stable times, while it is to some extent helpful in times of turmoil (periods characterized by large outliers). In contrast to the TVP-RW SINGLE the other three flexible TVP-RW variants forecast particularly well, suggesting that flexible state innovation volatilities greatly increase precision for TVP coefficients. In particular for FA-VARs these models show improved forecast accuracy after the Great Recession.

7. Closing remarks

It is empirically well documented that macroeconomic time series feature instabilities in the parameters and innovation volatilities. In the literature there is strong agreement that stochastic volatility is important, while, especially in larger-scale models, there is less consensus for time-varying coefficients. With increasing amount of information overall time-variation in parameters tends to reduce, but might be still present at few points in time for some parameters. Detecting such occasional changes is challenging and requires highly flexible modeling techniques. To achieve such flexibility we introduce mixture priors on the time-varying part of the parameters. By additionally using hierarchical shrinkage priors on dynamic state variances, these methods are capable in imposing dynamic sparsity, as well as capturing a wide range of parameter changes. In a simulation study we show that our methods detect both sudden and gradual changes in parameters. In an empirical exercise we find that some coefficients tend to change abruptly in times of turmoil. Moreover, all proposed approaches forecast well. Even for large VARs flexible mixture priors improve forecast accuracy upon a wide range of benchmarks, suggesting that capturing these infrequent instabilities pays off.

References

- Aastveit et al. (2017) Aastveit KA, Carriero A, Clark TE, and Marcellino M (2017), “Have standard VARs remained stable since the crisis?” Journal of Applied Econometrics 32(5), 931–951.

- Ball and Mazumder (2011) Ball L, and Mazumder S (2011), “Inflation dynamics and the Great Recession,” Brookings Papers on Economic Activity 42(1 (Spring), 337–405.

- Bańbura et al. (2010) Bańbura M, Giannone D, and Reichlin L (2010), “Large Bayesian vector auto regressions,” Journal of Applied Econometrics 25(1), 71–92.

- Bauwens et al. (2015) Bauwens L, Koop G, Korobilis D, and Rombouts JV (2015), “The contribution of structural break models to forecasting macroeconomic series,” Journal of Applied Econometrics 30(4), 596–620.

- Belmonte et al. (2014) Belmonte MA, Koop G, and Korobilis D (2014), “Hierarchical shrinkage in time-varying parameter models,” Journal of Forecasting 33(1), 80–94.

- Bhattacharya et al. (2016) Bhattacharya A, Chakraborty A, and Mallick BK (2016), “Fast sampling with Gaussian scale mixture priors in high-dimensional regression,” Biometrika 103(4), 985–991.

- Bitto and Frühwirth-Schnatter (2019) Bitto A, and Frühwirth-Schnatter S (2019), “Achieving shrinkage in a time-varying parameter model framework,” Journal of Econometrics 210(1), 75–97.

- Cadonna et al. (2020) Cadonna A, Frühwirth-Schnatter S, and Knaus P (2020), “Triple the gamma–A unifying shrinkage prior for variance and variable selection in sparse state space and TVP models,” Econometrics 8(2), 20.

- Carriero et al. (2019) Carriero A, Clark TE, and Marcellino M (2019), “Large Bayesian vector autoregressions with stochastic volatility and non-conjugate priors,” Journal of Econometrics 212(1), 137–154.

- Carvalho et al. (2010) Carvalho CM, Polson NG, and Scott JG (2010), “The horseshoe estimator for sparse signals,” Biometrika 97(2), 465–480.

- Chan et al. (2020) Chan J, Eisenstat E, and Strachan R (2020), “Reducing the state space dimension in a large TVP-VAR,” Journal of Econometrics 218(1), 105 – 118.

- Chan and Jeliazkov (2009) Chan JC, and Jeliazkov I (2009), “Efficient simulation and integrated likelihood estimation in state space models,” International Journal of Mathematical Modelling and Numerical Optimisation 1(1-2), 101–120.

- Chan et al. (2012) Chan JC, Koop G, Leon-Gonzalez R, and Strachan RW (2012), “Time-varying dimension models,” Journal of Business & Economic Statistics 30(3), 358–367.

- Chan and Strachan (2020) Chan JC, and Strachan RW (2020), “Bayesian State Space Models in Macroeconometrics,” Technical report.

- Clark (2011) Clark T (2011), “Real-time density forecasts from BVARs with stochastic volatility,” Journal of Business & Economic Statistics 29, 327–341.

- Cogley et al. (2010) Cogley T, Primiceri GE, and Sargent TJ (2010), “Inflation-gap persistence in the US,” American Economic Journal: Macroeconomics 2(1), 43–69.

- Cogley and Sargent (2005) Cogley T, and Sargent TJ (2005), “Drifts and volatilities: monetary policies and outcomes in the post WWII US,” Review of Economic Dynamics 8(2), 262 – 302.

- Coibion and Gorodnichenko (2015) Coibion O, and Gorodnichenko Y (2015), “Is the Phillips curve alive and well after all? Inflation expectations and the missing disinflation,” American Economic Journal: Macroeconomics 7(1), 197–232.

- Cross et al. (2020) Cross JL, Hou C, and Poon A (2020), “Macroeconomic forecasting with large Bayesian VARs: Global-local priors and the illusion of sparsity,” International Journal of Forecasting 36(3), 899 – 915.

- D’Agostino et al. (2013) D’Agostino A, Gambetti L, and Giannone D (2013), “Macroeconomic forecasting and structural change,” Journal of Applied Econometrics 28(1), 82–101.

- Doan et al. (1984) Doan T, Litterman R, and Sims C (1984), “Forecasting and conditional projection using realistic prior distributions,” Econometric Reviews 3(1), 1–100.

- Eickmeier et al. (2015) Eickmeier S, Lemke W, and Marcellino M (2015), “Classical time varying factor-augmented vector auto-regressive models-estimation, forecasting and structural analysis,” Journal of the Royal Statistical Society: Series A (Statistics in Society) 178(3), 493–533.

- Feldkircher et al. (2017) Feldkircher M, Huber F, and Kastner G (2017), “Sophisticated and small versus simple and sizeable: When does it pay off to introduce drifting coefficients in Bayesian VARs?” arXiv:1711.00564 .

- Frühwirth-Schnatter (2001) Frühwirth-Schnatter S (2001), “Markov chain Monte Carlo estimation of classical and dynamic switching and mixture models,” Journal of the American Statistical Association 96(453), 194–209.

- Frühwirth-Schnatter and Wagner (2010) Frühwirth-Schnatter S, and Wagner H (2010), “Stochastic model specification search for Gaussian and partial non-Gaussian state space models,” Journal of Econometrics 154(1), 85–100.

- George and McCulloch (1993) George EI, and McCulloch RE (1993), “Variable selection via Gibbs sampling,” Journal of the American Statistical Association 88(423), 881–889.

- George and McCulloch (1997) ——— (1997), “Approaches for Bayesian variable selection,” Statistica Sinica 339–373.

- Gerlach et al. (2000) Gerlach R, Carter C, and Kohn R (2000), “Efficient Bayesian inference for dynamic mixture models,” Journal of the American Statistical Association 95(451), 819–828.

- Giannone et al. (2015) Giannone D, Lenza M, and Primiceri GE (2015), “Prior selection for vector autoregressions,” The Review of Economics and Statistics 97(2), 436–451.

- Giordani and Kohn (2008) Giordani P, and Kohn R (2008), “Efficient Bayesian inference for multiple change-point and mixture innovation models,” Journal of Business & Economic Statistics 26(1), 66–77.

- Gneiting and Raftery (2007) Gneiting T, and Raftery AE (2007), “Strictly proper scoring rules, prediction, and estimation,” Journal of the American Statistical Association 102(477), 359–378.

- Griffin and Brown (2010) Griffin J, and Brown P (2010), “Inference with normal-gamma prior distributions in regression problems,” Bayesian Analysis 5(1), 171–188.

- Groen et al. (2013) Groen JJ, Paap R, and Ravazzolo F (2013), “Real-time inflation forecasting in a changing world,” Journal of Business & Economic Statistics 31(1), 29–44.

- Hauzenberger et al. (2020) Hauzenberger N, Huber F, and Koop G (2020), “Dynamic Shrinkage Priors for Large Time-varying Parameter Regressions using Scalable Markov Chain Monte Carlo Methods,” arXiv:2005.03906 .

- Hauzenberger et al. (2019) Hauzenberger N, Huber F, Koop G, and Onorante L (2019), “Fast and Flexible Bayesian Inference in Time-varying Parameter Regression Models,” arXiv:1910.10779 .

- Huber and Feldkircher (2019) Huber F, and Feldkircher M (2019), “Adaptive shrinkage in Bayesian vector autoregressive models,” Journal of Business & Economic Statistics 37(1), 27–39.

- Huber et al. (2019) Huber F, Kastner G, and Feldkircher M (2019), “Should I stay or should I go? A latent threshold approach to large-scale mixture innovation models,” Journal of Applied Econometrics 34(5), 621–640.

- Huber et al. (2020a) Huber F, Koop G, and Onorante L (2020a), “Inducing sparsity and shrinkage in time-varying parameter models,” Journal of Business & Economic Statistics 0(ja).

- Huber et al. (2020b) Huber F, Koop G, and Pfarrhofer M (2020b), “Bayesian Inference in High-Dimensional Time-varying Parameter Models using Integrated Rotated Gaussian Approximations,” arXiv:2002.10274 .

- Kalli and Griffin (2014) Kalli M, and Griffin J (2014), “Time-varying sparsity in dynamic regression models,” Journal of Econometrics 178(2), 779 – 793.

- Kastner (2016) Kastner G (2016), “Dealing with stochastic volatility in time series using the R package stochvol,” Journal of Statistical Software 69(5), 1–30.

- Kastner and Frühwirth-Schnatter (2014) Kastner G, and Frühwirth-Schnatter S (2014), “Ancillarity-sufficiency interweaving strategy (ASIS) for boosting MCMC estimation of stochastic volatility models,” Computational Statistics & Data Analysis 76, 408–423.

- Kastner and Huber (2020) Kastner G, and Huber F (2020), “Sparse Bayesian Vector Autoregressions in Huge Dimensions,” Journal of Forecasting .

- Kim and Nelson (1999) Kim CJ, and Nelson CR (1999), “Has the US economy become more stable? A Bayesian approach based on a Markov-switching model of the business cycle,” The Review of Economics and Statistics 81(4), 608–616.

- Kliem et al. (2016) Kliem M, Kriwoluzky A, and Sarferaz S (2016), “On the Low-Frequency Relationship Between Public Deficits and Inflation,” Journal of Applied Econometrics 31(3), 566–583.

- Koop (2013) Koop G (2013), “Forecasting with medium and large Bayesian VARs,” Journal of Applied Econometrics 28(2), 177–203.

- Koop and Korobilis (2012) Koop G, and Korobilis D (2012), “Forecasting inflation using dynamic model averaging,” International Economic Review 53(3), 867–886.

- Koop and Korobilis (2013) ——— (2013), “Large time-varying parameter VARs,” Journal of Econometrics 177(2), 185–198.

- Koop et al. (2009) Koop G, Leon-Gonzalez R, and Strachan RW (2009), “On the evolution of the monetary policy transmission mechanism,” Journal of Economic Dynamics and Control 33(4), 997–1017.

- Koop and Potter (2007) Koop G, and Potter SM (2007), “Estimation and forecasting in models with multiple breaks,” The Review of Economic Studies 74(3), 763–789.

- Korobilis (2013) Korobilis D (2013), “Assessing the transmission of monetary policy using time-varying parameter dynamic factor models,” Oxford Bulletin of Economics and Statistics 75(2), 157–179.

- Korobilis (2019) ——— (2019), “High-dimensional macroeconomic forecasting using message passing algorithms,” Journal of Business & Economic Statistics 0(ja).

- Korobilis and Koop (2020) Korobilis D, and Koop G (2020), “Bayesian dynamic variable selection in high dimensions,” MPRA:100164 .

- Kowal et al. (2019) Kowal DR, Matteson DS, and Ruppert D (2019), “Dynamic shrinkage processes,” Journal of the Royal Statistical Society: Series B (Statistical Methodology) 81(4), 781–804.