Shrinking the eigenvalues of M-estimators of covariance matrix

Esa Ollila, , Daniel P. Palomar, and Frédéric Pascal

E. Ollila is with the Department of Signal

Processing and Acoustics, Aalto University, P.O. Box 15400, FI-00076

Aalto, Finland. D. Palomar is with the Hong Kong University of Science and Technology, Hong Kong. F. Pascal is with Université Paris-Saclay, CNRS, CentraleSupélec, Laboratoire des signaux et systèmes, 91190, Gif-sur-Yvette, France.Manuscript received November xx, 202X; revised xx, 202X.

Abstract

A highly popular regularized (shrinkage) covariance matrix estimator is the shrinkage sample covariance matrix (SCM) which shares the same set of eigenvectors as the SCM but shrinks its eigenvalues toward the grand mean of the eigenvalues of the SCM. In this paper, a more general approach is considered in which the SCM is replaced by an M-estimator of scatter matrix and a fully automatic data adaptive method to compute the optimal shrinkage parameter with minimum mean squared error is proposed. Our approach permits the use of any weight function such as Gaussian, Huber’s, Tyler’s, or weight functions, all of which are commonly used in M-estimation framework. Our simulation examples illustrate that shrinkage M-estimators based on the proposed optimal tuning combined with robust weight function do not loose in performance to shrinkage SCM estimator when the data is Gaussian, but provide significantly improved performance when the data is sampled from an unspecified heavy-tailed elliptically symmetric distribution. Also, real-world and synthetic stock market data validate the performance of the proposed method in practical applications.

Index Terms:

I Introduction

Consider a sample of -dimensional vectors sampled from a distribution of a random vector with mean vector equal to zero (i.e., ). One of the first task in the analysis of high-dimensional data is to estimate the covariance matrix. The most commonly used estimator is the sample covariance matrix (SCM), ,

but its main drawbacks are its loss of efficiency when sampling from distributions which have heavier

tails than the multivariate normal (MVN) distribution and its sensitivity to outliers. Although being unbiased estimator of

the covariance matrix for any sample length , it is well-known that the eigenvalues are poorly estimated when is not orders of magnitude larger than . In such cases, one commonly uses a regularized SCM (RSCM) with a linear shrinkage towards a scaled identity matrix, defined as

(1)

where is the regularization parameter. The RSCM shares the same set of eigenvectors as the SCM , but its eigenvalues are shrinked towards the grand mean of the eigenvalues of the SCM . That is, if denote the eigenvalues of , then are the eigenvalues of , where . Optimal computation of such that has minimum mean squared error (MMSE) has been developed for example in [1, 2] or in [3] for certain structured target matrices.

A Bayesian approach has been considered in [4].

However, the estimator in (1) remains sensitive to outliers and non-Gaussianity. M-estimators of scatter [5] are popular robust alternatives to SCM. We consider the situation where and hence a conventional M-estimator of scatter exists under mild conditions on the data (see [6]) and can thus be used in place of the SCM in (1). We then propose a fully automatic data adaptive method to compute the optimal shrinkage parameter . First, we derive an approximation for the optimal parameter attaining the minimum MSE and then propose a data adaptive method for its computation. The benefit of our approach is that it can be easily applied to any M-estimator using any weight function . Our simulation examples illustrate that a shrinkage M-estimator using the proposed tuning and a robust weight function does not loose in performance to optimal shrinkage SCM estimator when the data is Gaussian, but is able to provide significantly improved performance in the case of heavy-tailed data and in the presence of outliers.

Earlier works, e.g., in [7, 8, 9, 10, 11, 12, 13, 14, 15], proposed regularized M-estimators of scatter matrix either by adding a penalty function to M-estimation objective function or a diagonal loading term to the respective first-order solution (M-estimating equation). We consider a simpler approach that uses a conventional M-estimator and shrinks its eigenvalues to the grand mean of the eigenvalues. Our approach permits computation of the optimal shrinkage parameter for any M-estimation weight function. Preliminary study of the proposed estimators has appeared in a conference proceeding [16].

Finally, we note some related but different approaches to what is pursed in this paper. For example, covariance matrix estimation in the low sample size large dimensionality setting commonly arises in radar signal processing, where often some constrained, mismatched or structured estimation framework of the covariance matrix is exploited. See e.g., [17, 18, 19, 20, 21, 22]. On the other hand, there are also other approaches for parameter tuning of regularized covariance matrix estimators such as cross-validation or expected likelihood approach [23, 24, 25].

The paper is structured as follows. section II introduces the proposed shrinkage M-estimator framework while

section III discusses automatic computation of the optimal shrinkage parameter under the assumption of sampling from unspecified elliptical distribution. Extension to complex case is discussed in subsection III-A. section IV addresses the most commonly used M-estimators, namely, the Gaussian weight function, Huber’s weight function, Tyler’s weight and -distribution weight function. We provide simulation studies in section V and experimental results in section VI. In section VI we validate the promising performance of the proposed approach

both in the case of real-world and synthetic stock market data. Finally, section VII concludes, while proofs of theorems and lemmas are kept in the Appendix.

II Shrinkage M-estimators of scatter

In this paper, we assume that (except for Gaussian loss) and consider an M-estimator of scatter matrix [5] that

solves an estimating equation

(2)

where is a non-increasing weight function. An M-estimator is a sort of adaptively weighted SCM with weights determined by function . To guarantee existence of the solution, it is required that the data verifies the condition stated in [6]. An M-estimator of scatter which shrinks the eigenvalues towards the grand mean of the eigenvalues is then defined as:

(3)

Thus is indexed by the shrinkage parameter . If , then coincides with the conventional M-estimator in (2) while if , then equals an identity matrix scaled by mean of the eigenvalues of . Next we discuss the commonly used weight functions .

The RSCM in (1) is obtained when one uses the Gaussian weight function . Terminology ‘Gaussian’ stems from the fact that is the maximum likelihood estimate (MLE) of the covariance matrix of MVN distribution. We return to this in section III. Huber’s weight function is defined as

(4)

where is a user defined tuning constant that determines the robustness and efficiency of the estimator and

is a scaling factor; see subsection IV-B for more details.

Another popular choice is MVT-weight function [6]:

(5)

in which case the corresponding M-estimator is also the MLE of the scatter matrix parameter of the multivariate (MVT) distribution with degrees of freedom (d.o.f.). We return to this estimator in subsection IV-D.

Finally, another classic choice, with nice robustness properties, is Tyler’s [26] M-estimator, in which case the weight function is

(6)

Both Huber’s and MVT-weight function yield Tyler’s weight function as special cases; namely,

for , one notices that and in the limit case

as Huber’s weight function tends to Tyler’s weight function.

We would like to stress that is a necessary assumption for all but Gaussian weight functions for a solution to (2) to exist. We do not include the limit case since any affine equivariant M-estimator when and data is in general position is just a scalar multiple of the SCM , that is, for some [27]. For example, M-estimator based on Huber’s or -weights are affine equivariant. Moreover, note that Theorem 2 in [28] ensures similar results in the large sample regime. Namely, the following convergence is proved

with and is an appropriate weighted SCM, and the norm denotes the spectral norm.

An M-estimator is a consistent estimator of the M-functional of scatter matrix, defined as

(7)

If the population M-functional is known, then by defining a 1-step estimator

(8)

we can compute

(9)

which serves as a proxy for . Naturally, such an estimator is fictional, since the initial value is unknown.

The 1-step estimator is, by its construction, an unbiased estimator of , i.e., .

Ideally we would like to find the value of for which the corresponding estimator attains the minimum MSE, that is,

(10)

where denotes the Frobenius matrix norm (i.e., and for real-valued and complex-valued matrices, respectively, where denotes the Hermitian transpose).

Since solving (10) is not feasible due to the implicit form of M-estimators, we instead solve the following

much simpler problem:

(11)

Such approach was also used in [29] to derive an optimal parameter for the shrinkage Tyler’s M-estimator of scatter proposed by the authors,

Before stating the expression for we introduce a sphericity measure of scatter, defined as

(12)

Sphericity [30, 31] measures how close is to a scaled identity matrix:

where if and only if and if has rank equal to 1.

Theorem 1.

Suppose is an i.i.d. random sample from any -variate distribution, and

is a weight function for which the expectation exists.

The oracle parameter in (11)

is

(13)

(14)

where and is defined in (12). Note that and the value of the MSE

at the optimum is

In the next section, we derive a more explicit form of by assuming that the data is generated from an unspecified elliptically symmetric distribution.

III Shrinkage parameter for elliptical samples

Maronna [5] developed M-estimators of scatter matrices originally within the framework of elliptically symmetric distributions [32, 33]. The probability density function (p.d.f.) of centered (zero mean) elliptically distributed

random vector, denoted by , is

(16)

where is a positive definite symmetric matrix parameter, called the scatter matrix, is the

density generator, which is a fixed function that is independent of

and , and is a normalizing constant ensuring

that integrates to 1.

The density generator determines

the elliptical distribution. For example, the MVN distribution is obtained when

and the -distribution with d.o.f., denoted ,

is obtained when . Then the weight function for the MLE of scatter matrix corresponds to the case that the weight function is of the form

This yields (5) as the weight function for

the MLE of scatter for -distribution. If the second moments of exists, then can be defined so that represents the covariance matrix of , i.e., ; see [33] for details.

When , then the M-functional in (7) is related to underlying scatter matrix parameter via the relationship

(17)

where is a solution to an equation

(18)

where and .

Often needs to be solved numerically from (18) but in some cases an analytic expression

can be derived. If and the used weight function matches with the data distribution, so

, then .

Next we derive expressions for and appearing in the denominator of in (14).

These depend on a constant (which depends on weight function via ) as follows:

(19)

where the statistical expectation is again computed w.r.t. distribution of

the positive random variable .

Follows from Theorem 1 after substituting the values for and

derived in 1 into the denominator of in (14).

∎

A closely related result is derived in [34, Theorem 1]. Namely, [34] considers oracle estimator as in (9) but using a shrinkage target equal to identity matrix instead of as in this paper. This is due to the fact that [34] assumes that . Another difference is that [34] assumes that (so ), i.e., that the used M-estimator is consistent to the scatter matrix of the underlying elliptical population. This assumption implies knowledge of the underlying elliptical distribution in which case it is natural to use the ML-weight as was done in [34].

Thus Theorem 2 compared to [34, Theorem 1] holds in the more general case when the scale is not known apriori and no assumption on the knowledge of the elliptical distribution is imposed. Furthermore, in the next subsesction, we extend the result to the complex-valued case which was not considered in [34].

1 also allows to construct an unbiased estimate of as is shown next.

Theorem 3.

Suppose is an i.i.d. random sample from .

Then an unbiased estimate of for any finite and any is

Then substituting the values of and from 1 into (23) yields .

∎

It is instructive to consider in more detail the case of Gaussian loss. In this case, equals the SCM, , and

the statistic no longer depends on the unknown . Furthermore, if data is generated from a Gaussian distribution , then , and in (21) reduces to the estimator that is identical to one proposed by [31, Lemma 2.1] in the case that location is known (); see also [3, Theorem 2]. Moreover, [2, Theorem 4] is obtained in the general elliptical case, again assuming known location parameter ().

III-AAn extension to the complex-valued case

Consider the case that , are complex-valued (i.e., ) and represent a random sample from a (circular) complex elliptically symmetric (CES) distribution [33]. The p.d.f. of a random vector with centered (zero mean)

CES distribution, denoted using same notation , is

where is the positive definite hermitian (PDH) matrix parameter, called the scatter matrix, is the

density generator, which is a fixed function that is independent of and , and is a normalizing constant ensuring

that integrates to 1.

An M-estimator of scatter matrix is a PDH matrix that solves an estimating equation

(24)

where is a non-increasing weight function. Again, gives the SCM ,

Huber’s and Tyler’s weight functions are as earlier, stated in (4) and

(6), respectively, whereas corresponds to MLE

of the scatter matrix parameter when sampling from a -variate complex -distribution with d.o.f. We refer to

[33, 35] for more details. We may now define the shrinkage M-estimator as in (3). Definitions

(7)-(9) hold also in the complex-valued case with obvious modifications (replacing transpose by the Hermitian transpose).

Theorem 1 did not require an assumption that random vectors are real-valued, i.e., it holds also when are i.i.d. complex-valued random vectors. This means that we only need to derive expectations in 1 in the case of random sampling from a CES distribution. First, we define the parameter in the complex-valued case as

(25)

where the expectation is w.r.t. , where . The analog of 1 to complex case is given next.

Lemma 2.

Suppose is an i.i.d. random sample from a (circular) complex elliptically symmetric distribution . Then

Plugging in the expectations above into derived in Theorem 1 yields the following result.

Theorem 4.

Let denote an i.i.d. random sample from a (circular) -variate complex elliptically symmetric

distribution and assume that expectation (25) exists.

Then the oracle parameter that

minimizes the MSE in Theorem 1 is

is an unbiased estimate of for any finite and any .

III-BComputing the shrinkage parameter

In order to construct a data-adaptive estimate of (either in real- or complex-valued cases), all we need to estimate is the sphericity and the constant . An estimate of is constructed separately for each weight function (Gaussian, Huber’s, MVT- and Tyler’s weight function) in section IV. However, it is also possible to use an empirical (sample mean) version of (19).

Next we discuss computation of the sphericity estimator .

As an estimator we use the estimate derived in [14], which was named as Ell1-estimator in [2], and defined as

(27)

which for complex-valued case is defined analogously (transpose replaced with the Hermitian transpose).

Next recall that defined in (21) is an unbiased estimator of . This statistics depends on and which are unknown, but a plug-in estimate of can be constructed by replacing and with

and , respectively. Dividing this plug-in statistic further by , leads to another estimator of sphericity, named as Ell2-estimator, and defined as

(28)

where the constants and are as defined in Theorem 3 (and Theorem 4 in complex case) but with replaced by its estimate . When one uses Gaussian weight function, then and , where is an estimate of elliptical kurtosis (cf.subsection IV-A). In this case, corresponds to Ell2-estimator of sphericity proposed in [2, Sect. IV.B].

In order to guarantee that the estimators remain in the valid interval, , we use

(29)

as our final estimator (and similarly for Ell2-estimator). The related shrinkage parameter can then computed as

and again similarly for Ell2-estimator.

IV Important special cases

IV-ARegularized SCM (RSCM) estimator

If one uses Gaussian weight function , then a necessary assumption is that the underlying elliptical distribution possesses finite 4th-order moments. As discussed earlier, one may then assume w.l.o.g. that the scatter matrix parameter equals the covariance matrix, i.e., . When , one has that and and hence , meaning that the approximate MMSE solution is exact in this case. Finally, we may relate with an elliptical kurtosis [36] parameter :

(30)

where the expectation is over the distribution of the random variable . The elliptical kurtosis parameter is defined as a generalization of the kurtosis parameter to the vector case, and as such it vanishes (so ) when has MVN distribution (denoted ).

Since exists for any , we can drop the assumption that in this case.

Corollary 1.

Let denote an i.i.d. random sample from an (real or complex)

elliptical distribution with finite 4th order moments and covariance matrix .

Then for the shrinkage SCM estimator in (1) one has that

(31)

where

Proof.

The result follows from Theorem 2 and Theorem 4 since and the M-functional for Gaussian loss is and . Since for Gaussian loss, , we notice from (19) and (25) hat

(32)

Plugging into in Theorem 2 and Theorem 4 yields the stated expressions, respectively.

∎

The elliptical kurtosis parameter can be easily estimated using the following relationship to kurtosis even in the cases when .

First, recall that kurtosis of a random variable in the real and complex case is defined as

(33)

respectively. Kurtosis vanishes when the random variable has real or complex Gaussian distribution with variance .

The following result establishes the relationship of elliptical kurtosis parameter with marginal kurtosis.

Lemma 3.

Assume that is a random vector from real or complex elliptically symmetric distribution with covariance matrix possessing finite 4th order moments.

Then

Since all marginal variables possess the same kurtosis, an estimate can be formed simply as the mean of marginal sample kurtosis statistics.

This is the same estimate of the elliptical kurtosis proposed in [2].

Note that [2] only considered the real-valued case, and thus 1 allows us to extend the RSCM estimator in [2] to complex-valued case.

In the sequel, we use acronym RSCM-Ell1 to refer to estimator with computed

as with given by (31) and being the estimate of sphericity defined in (29) and an estimate of elliptical kurtosis described above. An RSCM-Ell2 estimator is defined similarly but now using Ell2-estimator of sphericity.

A natural competitor for RSCM-Ell1 or RSCM-Ell2 estimators (at least in the real-valued case) is the estimator proposed by Ledoit and Wolf [1], referred to as LWE. We note that LWE also uses RSCM , but the parameter is computed in a different manner. An extra benefit of our approach is that an estimator of the optimal shrinkage parameter can be computed for real- or complex-valued observations while LWE assumes real-valued observations.

IV-BRegularized Huber’s M-estimator (RHub)

Next consider the Huber’s weight function in (4). Note that is a scaling constant; if is Huber M-estimator of scatter when , then the Huber M-estimator of scatter when is simply . The scaling constant is usually chosen so that the resulting scatter estimator is Fisher consistent for the covariance matrix at MVN distribution, i.e, when . In the real case, this holds when

where denotes the cumulative distribution function (c.d.f.) of chi-squared distribution with d.o.f.

Since has a -distribution when , the tuning constant is chosen as th upper quantile of -distribution:

(35)

for some . Tuning constant and scaling factor can be determined similarly in the complex-valued case; see [33, 35] for details.

Let us define a winsorized observation based on as

where is the threshold of Huber’s weight function and is the respective scaling factor.

The winsorized r.v. also has an elliptically symmetric distribution since the contours remain elliptical in shape (so the p.d.f. is still defined by (16) but for a truncated density generator ) and thus it shares the properties of elliptical random vectors.

If we take (which holds at least when has MVN distribution), then the constant can be written as

where is the elliptical kurtosis parameter (cf.3) of an elliptical random vector .

An estimate of can be then calculated similarly as for RSCM-Ell1 or RSCM-Ell2 estimators defined earlier (recall relation

(32)). The only difference is that is now computed for winsorized data , where and denotes the Huber’s M-estimator.

In the sequel, we use acronym RHub-Ell1 or RHub-Ell2 to refer to shrinkage M-estimator that uses Huber’s weight with threshold determined from (35) for user specified and shrinkage parameter .

or , respectively.

IV-CRegularized Tyler’s M-estimator (RTyl)

Let denote a shape matrix (normalized scatter matrix), defined as

where denotes the scatter matrix parameter of the ES distribution. Note that . If one uses Tyler’s weight function in (6), then (17) holds with , i.e., , that is,

Tyler’s M-estimator is an estimate of the shape matrix. The following result hence follows at once from Theorem 2 and Theorem 4.

Corollary 2.

Let denote an i.i.d. random sample from a (real or complex)

elliptical distribution . When using Tyler’s weight (6), it holds that

Proof.

The real-valued case follows by noting that in (19) is equal to

for all random vectors regardless of (i.e., the functional form of the density generator) and that . Plugging into (20) yields the stated expression. The complex-valued case follows similarly.

∎

Since Tyler’s M-estimator verifies , the shrinkage estimator in (3) simplifies to

(36)

where is Tyler’s M-estimator, i.e., an M-estimator based on weight (6).

By RTyl-Ell1 we refer to (36), where the shrinkage parameter is computed as with given by 2 and by (29).

A related regularized Tyler’s estimator was proposed by [7] as the limit of the algorithm

(37)

where is a fixed shrinkage parameter. This algorithm represents a diagonally loaded version of the fixed-point algorithm given for Tyler’s M-estimator. Uniqueness and convergence of the recursive algorithm has been later derived in [29, 12].

By CWH estimator we now refer to estimator obtained by iterating (37) using same value as for RTyl-Ell1. An interesting question then is how different is RTyl-Ell1 in its performance from CWH. We explore this by simulation studies later. This is interesting as the former is simply shrinking the eigenvalues of Tyler’s M-estimator towards its grand mean where as the latter does not have an explicit connection to Tyler’s M-estimator for any .

IV-DRegularized M-estimator for MVT distribution (RMVT)

We assume that the data is arising from a MVT distribution but the d.o.f. parameter is unknown and is adaptively estimated from the data using Algorithm 1 explained below. Once is found, we use function to compute the underlying M-estimator for the postulated MVT distribution.

Yet, we need to address the question of how the constant is computed. Due to data adaptive estimation of , we can assume that since the scaling factor equals unity for an MLE of the scatter matrix parameter.

We use the fact that for MVT distribution (i.e., when ), the parameter is111Note that the -weight in the complex case is [33]: .

Hence, a natural estimate is in the real case. An estimate of is constructed similarly in the complex case. We use acronym RMVT-Ell1 to refer to shrinkage M-estimator that uses with shrinkage parameter calculated by . RMVT-Ell2 is constructed similarly, but now Ell2-estimator of sphericity is used.

Next we discuss our approach for estimating from the data.

Assume and denote . Then,

and hence . This means that

from which we obtain the relation

(38)

The above relation holds true in both real and complex cases. Then given an estimate of , we may compute an estimate which in turn provides an estimate via (38).

This gives rise to an iterative algorithm to estimate detailed in Algorithm 1. In the simulations, the algorithm converged, but already 2 iterations are sufficient to yield accuracy to first decimal; see Figure 1 for an illustration.

The initial estimate is , where is an estimate of marginal kurtosis explained in subsection IV-A (see also [2] for more details) and is a small number. The initial start is based on the following relationship with elliptical kurtosis parameter, , i.e., which holds true both in real and complex cases. Again the estimate in the complex-valued case is constructed similarly. Note that also other estimators of are proposed in the literature, for example in [34].

Figure 1: Average by running the Algorithm 1 with different choices of . Also shown is the initial estimate .

The samples are generated from a -variate -distribution with d.o.f., where follows the same AR(1) covariance matrix structure

explained in the simulation set-up of section V; and , As can be noted, converge to as increases, albeit the convergence is a bit slow.

Input : data matrix of size , maximum number of iterations

Initialize :

Compute ,

where is an estimate of explained in the text.

fordo

Set , where denotes the -MLE based on current estimate of d.o.f. parameter , i.e., solving the M-estimating equation

with is the MVT-weight function.

Update the ratio .

Upate the d.o.f. parameter .

ifthen

break

Output :

Algorithm 1Automatic data-adaptive computation of the d.o.f. parameter

V Simulation studies

In the simulation study, we generate samples from real ES distributions with a scatter matrix following an AR(1) structure, , where and scale parameter . When , then is close to an identity matrix scaled by , and when , tends to a singular matrix of rank 1.

The results are reported for the proposed shrinkage M-estimators using shrinkage parameter estimates based on Ell1-estimator of sphericity. However, for notational convenience, we drop the suffix -Ell1 from the proposed estimators. Thus the proposed estimators, described in section IV are referred to as RSCM, RMVT, RHub, and RTyl. Furthermore, acronyms LW, CWH and RBLW are used to refer to estimators proposed in [1] (see also subsection IV-A),

[29] (see also subsection IV-C and (37)) and [8], respectively. RBLW is the Rao-Blackwellized LW estimator, but unlike LW estimator, it assumes that the data distribution is Gaussian.

We also compare to RSCM estimator in (1), but now the shrinkage parameter is chosen via -fold cross-validation (CV), where as cross-validation fit we use , where is the SCM based on the validation set (data fold that was left out) and is the RSCM computed on the training set (data based on remaining folds) for a given .

As a grid for for the CV method we use a uniform grid in with increments and -fold cross-validation. We call this method as RSCM-CV or simply CV. All simulation results in this section are averaged over 2000 Monte-Carlo trials. Since is assumed for all estimators expect for RSCM, we do not consider the case low sample regime, , in our simulation studies. Furthermore, we adopt the MSE (squared Frobenius norm) as our performance metric as it is used in deriving the optimal shrinkage parameters in this paper. It is important to keep in mind, however, that in the low sample regime and for different performance metrics, the performance differences between estimators can often be noticeable and even quite different than in the regime that is considered here; See e.g., [8, 4, 2] for numerical illustrations and [37, 38] for different distances between covariances that could be used instead of the MSE metric.

V-AGaussian data

Figure 2: NMSE as a function of when samples are drawn from a MVN distribution with an AR(1) structure; and .

Figure 3: Shrinkage parameter as a function of when samples are drawn from a MVN distribution (left panel) and a -distribution with d.o.f. (right panel), where has an AR(1) structure; and .

The data is generated from MVN distribution , where has an AR(1) covariance matrix structure with .

The dimension is and varies from 60 to 280. Value determining the threshold is used in (35) for Huber’s weight.

Since Huber’s M-estimator is scaled to be consistent to the covariance matrix for Gaussian samples, the underlying population parameter coincides with the covariance matrix in this case. We also scaled the MVT-weight so that it is consistent to for Gaussian data.

Figure 2 compares the normalized MSE (NMSE) of different estimators w.r.t. increasing sample length .

It can be noted that all estimators provide essentially equally good estimator of the covariance matrix for Gaussian data; RSCM and RMVT are performing equally well, largely due to the effect of data-adaptive estimation of d.o.f. parameter . It should be noted that their performance difference to LW or RHub estimators are still marginal and differences can be spotted only by zooming in as in the sub-plot of Figure 2. As expected, RBLW estimator has a slight advantage over the other estimators in this case. The left panel of Figure 3 shows the (average) shrinkage parameter as a function of . As can be noted, the average shrinkage parameter of the proposed RSCM estimator can be seen to be roughly an average of CV and LW shrinkage parameters.

V-BHeavy-tailed data

Next we computed the NMSE curves when the data is generated from a heavy-tailed -distribution with and d.o.f. Note that NMSE of each estimator is now compared against the underlying population parameter of each M-estimator. Figure 4 displays the results. RBLW had a very poor performance which is due to its strict assumption of Gaussianity. It can be noted that CV method performs similarly, but slightly worse, than RSCM or LW.

This can be partially attested to poor robustness properties of cross-validation.

In the case of d.o.f., also the non-robust RSCM and LW provided large NMSE and thus all non-robust estimators are not visible in the right panel of Figure 4. This was expected since -distribution with d.o.f. is very heavy-tailed with non-finite kurtosis.

As can be noted, the proposed robust RHub and RMVT estimators provide significantly improved performance. We can also notice that RMVT estimator that adaptively estimates the d.o.f. from the data is able to outperform the regularized Huber’s estimator (RHub).

The right panel of Figure 3 depicts the (average) shrinkage parameter as a function of in the case that samples are drawn from a -distribution with d.o.f. As can be noted the robust shrinkage estimators (RHub and RMVT) use larger shrinkage parameter value than the non-robust RSCM and LW estimators. Compared to RSCM and LW, the RBLW (resp. CV) is seen to overestimate (resp. underestimate) the shrinkage parameter as it obtains much larger (resp. smaller) values.

Next we investigate how the estimators are able to estimate the shape matrix, i.e., the covariance matrix up to a scale.

Figure 5 displays the NMSE, , of different shrinkage shape matrix estimators, defined as when samples are generated from a -distribution with d.o.f.

Note that such normalization is not necessary for CWH or RTyl since they verify in the first place.

Figure 5 illustrate both the case when correlation parameter of the AR scatter matrix parameter is fixed while

varies and the case that is fixed while varies.

As can be seen from the top panel of Figure 5, all robust shape estimators are performing well and very similarly. In fact, performance of RMVT and CWH is essentially the same. We can also observe that the two different approaches for shrinking Tyler’s M-estimator, so CWH and the proposed RTyl are very similar. We can note from the bottom panels of Figure 5 that when (so is close to a scaled identity matrix) all estimators perform similarly. This is because all estimators are shrunk heavily towards the scaled identity matrix (namely, for all estimators). Similarly, when (so is close to a singular matrix of rank ), all estimators have a rather similar performance. This is because the true scatter matrix is poorly conditioned () and all estimators share similar difficulties of capturing the subspace structure due to limited training data and no a priori information about such structure. Indeed biggest differences between estimators are observed when has no particular structure, i.e., in the range .

Figure 4: NMSE as a function of when samples are drawn from a -variate -distribution with (left panel) and (right panel) d.o.f. The scatter matrix follows an AR(1) structure; and .

(a)

(b)

(c)

Figure 5: NMSE of different shrinkage estimators of shape matrix when samples are drawn a variate -distribution with d.o.f. having an AR(1) structure: (a) and sample length varies; (b) and (c) illustrate the case when varies while the sample length is fixed.

V-CComplex-valued data

Finally, we note that an important property of our shrinkage method is that it can be used for complex-valued data as well. Some other methods in the previous study, such as RBLW or LW assume real-valued data. In the supplementary material, we provide the results of a simulation study in the same set-up, but now the data being generated from circular complex Gaussian and heavy-tailed -distribution, respectively. These are distributions in the class of CES distributions. In our study we also include empirical Bayes diagonal loading estimator (EBDL) [4] which was developed for complex circular Gaussian data. Results obtained for complex-valued data attest the validity of the findings in the real-valued case.

VI Application to financial data and portfolio design

VI-AFinancial data

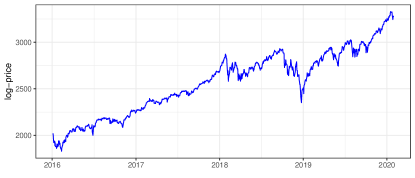

We use the S&P 500 stock market index (see Figure 6), which measures the stock performance of 500 large companies listed on stock exchanges in the United States, and its constituent stocks during the period 2016-01-01 to 2020-01-31.

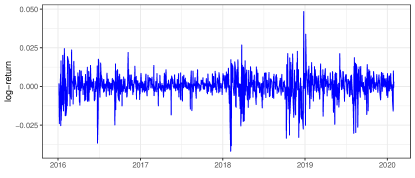

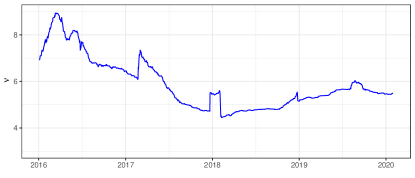

We can easily observe from the returns shown in Figure 7 the effect of volatility clustering over time that is responsible for heavy tails. More concretely, if we assume that the data follows an MVT distribution, then we can compute the degrees of freedom on a rolling-window basis and verify that indeed the data has heavy tails with (from mid-2017, varies between and ) as shown in Figure 8.

Figure 6: Log-prices of the S&P 500 index.

Figure 7: Log-returns of the S&P 500 index.

Figure 8: Degrees of freedom of the S&P 500 index.

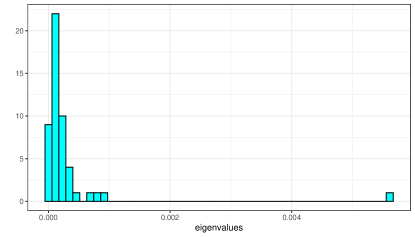

Factor model. Let denote the returns of the stocks at time . It turns out that the stock returns are largely driven by very few financial factors as

(39)

where is the factor loading matrix (which is very tall since ) and is the residual idiosyncratic component. As a consequence, the covariance matrix of these data has the form (assuming normalized factors):

(40)

where is the (diagonal) covariance matrix of the residuals. Typically, the term is much stronger than and this leads to the commonly used spike model in RMT (Random Matrix Theory) [39] which contains a few large eigenvalues and the rest small eigenvalues form the so-called bulk. Figure 9 shows the histogram of the empirical eigenvalues of the covariance matrix estimated from stocks from the S&P 500 market data, where a very strong eigenvalue can be observed corresponding to the market factor.

Figure 9: Histogram of empirical eigenvalues obtained from the market data () showing a strong market factor.

VI-BResults in terms of MSE

Since our shrinkage estimators are derived to minimize the MSE in the estimation of the covariance matrix, we start by showing the obtained MSE in the context of financial data. We consider seven methods in our comparison:

RSCM-Ell2, RMVT-Ell2, and RHub-Ell2 are as RSCM-Ell1, RMVT-Ell1, and RHub-Ell1, respectively, but using estimator of sphericity (cf.subsection III-B).

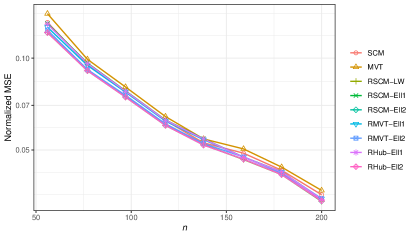

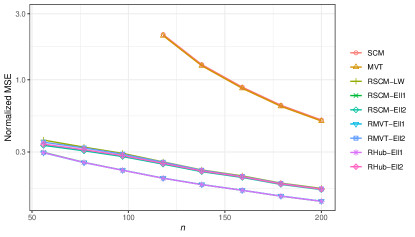

To make sure that the robust estimators do not underperform the benchmarks when the data is not heavy-tailed, we start by generating synthetic MVN data following the empirical covariance matrix previously obtained from market data (see Figure 9). Figure 10 displays the normalized MSE of the covariance matrix via 200 Monte-Carlo simulations. We do not observe any significant difference among the methods. Figure 11 shows the normalized MSE of the precision matrix via 200 Monte-Carlo simulations. The main observation is that the two methods without shrinkage significantly underperform.

Figure 10: Normalized MSE of covariance matrix vs number of observations for Gaussian data (with ).

Figure 11: Normalized MSE of precision matrix vs number of observations for Gaussian data (with ).

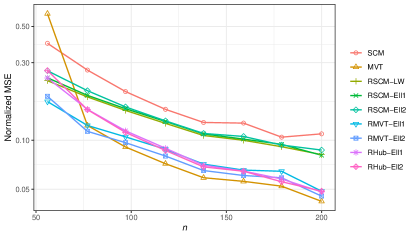

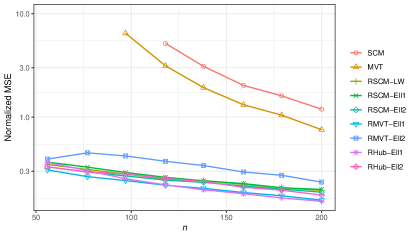

We now generate heavy-tailed synthetic data from a -distribution following the empirical covariance matrix previously obtained from market data (see Figure 9) and with d.o.f. . Figure 12 shows the normalized MSE of the covariance matrix. We can clearly observe a striking difference showing the superiority of robust estimators (i.e.,

MVT, RMVT, RHub) over non-robust estimators. Among the robust estimators, the proposed shrinkage methods clearly outperform the non-shrinkage

MVT in the low-sample regime, as expected. Figure 13 displays the normalized MSE of the precision matrix, with similar observations.

Figure 12: Normalized MSE of covariance matrix vs number of observations for -distributed data (with , ).

Figure 13: Normalized MSE of precision matrix vs number of observations for -distributed data (with , ).

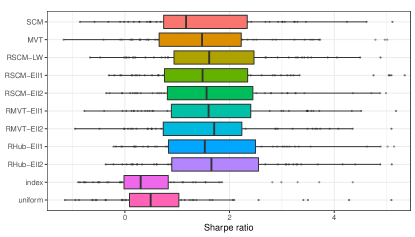

VI-CResults in terms of portfolio Sharpe ratio

After having shown the superiority of our proposed estimators, RMVT and RHub in terms of MSE in the estimation of the covariance matrix under heavy-tailed data, we now turn to assess the effects in terms of portfolio design. Note that an improvement of MSE in the covariance matrix may or may not translate into a significant improvement in terms of portfolio design; this depends on exactly what portfolio design is used and how it employs the estimated covariance matrix.

For simplicity, we consider the most basic Markowitz portfolio design [40]:

where is the expected return of the returns and is the minimum return desired for the portfolio.

We perform our backtest during the market period 2016-01-01 to 2020-01-31 on a rolling-window basis with a window length of 378 days (1.5 years). To make sure that our results are realistic, rather than performing a single backtest, we use the R package portfolioBacktest [41] to randomly select a large number of 200 datasets from the market data in the following way: each dataset chooses randomly stocks from the universe of 500, as well as a random period of 504 days (2 years) among the available period from 2016-01-01 to 2020-01-31.

Figure 14 shows a boxplot with the Sharpe ratio222The Sharpe ratio is defined as the expected return normalized with the volatility or standard deviation: , where is the return of the risk-free asset. obtained mean-variance portfolio according to different estimators for the covariance matrix (along with two benchmarks: the index and the or uniform portfolio). We can observe that the two methods without shrinkage underperform the shrinkage methods (in particular the SCM). Among the shrinkage methods, we can see that our robust estimators slightly outperform the others, although the improvement is not extremely significative.

Figure 14: Boxplot of Sharpe ratio obtained by the mean-variance portfolio according to different estimators for the covariance matrix.

VI-DSupplementary studies

Supplementary material to this paper also contain comparison of the proposed methods in the set-up described in [2], where the global mean variance portfolio (GMVP) is used as portfolio optimization strategy and the net returns correspond to stocks that are currently included in the Hang Seng Index (HSI).

Compared methods include GMVP weight vector based on LW estimator and an estimator proposed in [42] that uses robust regularized Tyler’s M-estimator with a tuning parameter selection optimized for GMVP strategy. We observed that GMVP based on the proposed RHub and RSCM are the best performing methods in terms of realized risk. We note that method of [42] was excluded in the study in subsection VI-C due to its high computational cost in the high-dimensional setting.

VII Conclusions and perspectives

This work proposed an original and fully automatic approach to compute an optimal shrinkage parameter in the context of heavy-tailed distributions and/or in presence of outliers. It has been shown that the performance of the method is similar to optimal one when the data is Gaussian while it outperforms shrinkage Gaussian-based methods when the data distribution turns out to be non-Gaussian. One of the benefits of the proposed adaptive shrinkage parameter selection is that it permits using real-valued or complex-valued data. Furthermore, a MATLAB toolbox called ShrinkM is freely available at http://users.spa.aalto.fi/esollila/shrinkM/ that includes functions to compute all of the proposed estimators (RHub, RTyl, RSCM, RMVT, and CV) as well as a script of one the simulation studies presented in the paper to reproduce the results.

Furthermore, this paper opens several ways, notably considering the challenging cases where which is left for future work. Supplementary materials also provide additional examples illustrating the benefits of the proposed estimators.

and .

Note that is a convex quadratic function in with a unique minimum given by

(42)

Substituting the expressions for constants and into yields the stated result.

The expression for MSE of then follows by substituting into expression for in (41)

and using the relation, ,

which follows from (42). This yields the MSE expression

This gives the stated MSE expression after noting that .

where and .

Recall that stochastic representation theorem of elliptical random vectors states that is independent of and -s

are i.i.d. on a uniform distribution on the unit sphere .

Then note that

(44)

In the second identity, we used the fact that is independent of and . In the 3rd identity we used that is independent of and in the 4th identity, we used that -s and -s are i.i.d.

Note that due to (18) and

.

Using these facts and the following results from [8]:

(45)

(46)

we get

Next note that

and hence

In the first identity we used that

as and the fact that is independent of .

In the second identity we used that samples are i.i.d. and due to (18) and

. The result then follows by substituting (45) into the last equation.

We show the result in the real case only as the result follows similarly for complex-valued case.

Write and note that .

The result

(51)

follows by recalling the stochastic decomposition. Namely, , where is independent of , and possesses a uniform distribution on the unit sphere . Thus we have that

where we used that (see e.g. [43, Lemma A.1.] and that . Furthermore, since , (51) states that . Then since , we have the stated result that .

References

[1]

O. Ledoit and M. Wolf, “A well-conditioned estimator for large-dimensional

covariance matrices,” J. Mult. Anal., vol. 88, no. 2, pp. 365–411,

2004.

[2]

E. Ollila and E. Raninen, “Optimal shrinkage covariance matrix estimation

under random sampling from elliptical distributions,” IEEE Trans.

Signal Process., vol. 67, no. 10, pp. 2707–2719, May 2019.

[3]

J. Li, J. Zhou, and B. Zhang, “Estimation of large covariance matrices by

shrinking to structured target in normal and non-normal distributions,”

IEEE Access, vol. 6, pp. 2158–2169, 2017.

[4]

A. Coluccia, “Regularized covariance matrix estimation via empirical bayes,”

IEEE Signal Process. Lett., vol. 22, no. 11, pp. 2127–2131, 2015.

[5]

R. A. Maronna, “Robust M-estimators of multivariate location and scatter,”

Ann. Stat., vol. 5, no. 1, pp. 51–67, 1976.

[6]

J. T. Kent and D. E. Tyler, “Redescending M-estimates of multivariate

location and scatter,” Ann. Stat., vol. 19, no. 4, pp. 2102–2119,

1991.

[7]

Y. I. Abramovich and N. K. Spencer, “Diagonally loaded normalised sample

matrix inversion (LNSMI) for outlier-resistant adaptive filtering,” in

Proc. IEEE International Conf. on Acoustics, Speech and Signal

Processing (ICASSP), Apr. 15–20 2007, pp. 1105–1108.

[8]

Y. Chen, A. Wiesel, Y. C. Eldar, and A. O. Hero, “Shrinkage algorithms for

MMSE covariance estimation,” IEEE Trans. Signal Process.,

vol. 58, no. 10, pp. 5016–5029, 2010.

[9]

L. Du, J. Li, and P. Stoica, “Fully automatic computation of diagonal loading

levels for robust adaptive beamforming,” IEEE Trans. Aerosp.

Electron. Syst., vol. 46, no. 1, pp. 449–458, 2010.

[10]

E. Ollila and D. E. Tyler, “Regularized -estimators of scatter matrix,”

IEEE Trans. Signal Process., vol. 62, no. 22, pp. 6059–6070, 2014.

[11]

F. Pascal, Y. Chitour, and Y. Quek, “Generalized robust shrinkage estimator

and its application to STAP detection problem,” IEEE Trans. Signal

Process., vol. 62, no. 21, pp. 5640–5651, 2014.

[12]

Y. Sun, P. Babu, and D. P. Palomar, “Regularized Tyler’s scatter estimator:

Existence, uniqueness, and algorithms,” IEEE Trans. Signal

Process., vol. 62, no. 19, pp. 5143–5156, 2014.

[13]

R. Couillet and M. McKay, “Large dimensional analysis and optimization of

robust shrinkage covariance matrix estimators,” J. Mult. Anal., vol.

131, pp. 99–120, 2014.

[14]

T. Zhang and A. Wiesel, “Automatic diagonal loading for Tyler’s robust

covariance estimator,” in IEEE Statistical Signal Processing Workshop

(SSP’16), 2016, pp. 1–5.

[15]

M. Yi and D. E. Tyler, “Shrinking the covariance matrix using convex penalties

on the matrix-log transformation,” Journal of Computational and

Graphical Statistics, no. just-accepted, pp. 1–10, 2020.

[16]

E. Ollila, D. P. Palomar, and F. Pascal, “M-estimators of scatter with

eigenvalue shrinkage,” in IEEE International Conf. on Acoustics,

Speech and Signal Processing (ICASSP), May 4–8 2020, pp. 5305–5309.

[17]

A. Aubry, A. De Maio, L. Pallotta, and A. Farina, “Radar detection of

distributed targets in homogeneous interference whose inverse covariance

structure is defined via unitary invariant functions,” IEEE Trans.

Signal Process., vol. 61, no. 20, pp. 4949–4961, 2013.

[18]

Y. Sun, A. Breloy, P. Babu, D. P. Palomar, F. Pascal, and G. Ginolhac,

“Low-complexity algorithms for low rank clutter parameters estimation in

radar systems,” IEEE Trans. Signal Process., vol. 64, no. 8, pp.

1986–1998, 2016.

[19]

A. Aubry, A. De Maio, and L. Pallotta, “A geometric approach to covariance

matrix estimation and its applications to radar problems,” IEEE

Trans. Signal Process., vol. 66, no. 4, pp. 907–922, 2018.

[20]

A. De Maio, L. Pallotta, J. Li, and P. Stoica, “Loading factor estimation

under affine constraints on the covariance eigenvalues with application to

radar target detection,” IEEE Trans. Aerosp. Electron. Syst.,

vol. 55, no. 3, pp. 1269–1283, 2019.

[21]

M. Tang, Y. Rong, X. R. Li, and J. Zhou, “Invariance theory for adaptive

detection in non-gaussian clutter,” IEEE Trans. Signal Process.,

vol. 68, pp. 2045–2060, 2020.

[22]

O. Besson, “Maximum likelihood covariance matrix estimation from two possibly

mismatched data sets,” Signal Processing, vol. 167, p. 107285, 2020.

[23]

Y. Abramovich and O. Besson, “Regularized covariance matrix estimation in

complex elliptically symmetric distributions using the expected likelihood

approach-part 1: The over-sampled case,” IEEE Trans. Signal

Process., vol. 61, no. 23, pp. 5807–5818, 2013.

[24]

O. Besson and Y. Abramovich, “Regularized covariance matrix estimation in

complex elliptically symmetric distributions using the expected likelihood

approach-part 2: The under-sampled case,” IEEE Trans. Signal

Process., vol. 61, no. 23, pp. 5819–5829, 2013.

[25]

Y. I. Abramovich and O. Besson, “On the expected likelihood approach for

assessment of regularization covariance matrix,” IEEE Signal

Process. Lett., vol. 22, no. 6, pp. 777–781, 2015.

[26]

D. E. Tyler, “A distribution-free M-estimator of multivariate scatter,”

Ann. Stat., vol. 15, no. 1, pp. 234–251, 1987.

[27]

——, “A note on affine equivariant location and scatter statistics for

sparse data,” Statist. and Prob. Letters, vol. 80, pp. 1409–1413,

2010.

[28]

R. Couillet, F. Pascal, and J. W. Silverstein, “The Random Matrix Regime of

Maronna’s -estimator with elliptically distributed samples,” J.

Mult. Anal., vol. 139, pp. 56–78, July 2015. arXiv:1311.7034.

[29]

Y. Chen, A. Wiesel, and A. O. Hero, “Robust shrinkage estimation of

high-dimensional covariance matrices,” IEEE Trans. Signal Process.,

vol. 59, no. 9, pp. 4097 – 4107, 2011.

[30]

O. Ledoit, M. Wolf et al., “Some hypothesis tests for the covariance

matrix when the dimension is large compared to the sample size,” Ann.

Stat., vol. 30, no. 4, pp. 1081–1102, 2002.

[31]

M. S. Srivastava, “Some Tests Concerning the Covariance Matrix in High

Dimensional Data,” Journal of the Japan Statistical Society,

vol. 35, no. 2, pp. 251–272, 2005.

[32]

K.-T. Fang, S. Kotz, and K.-W. Ng, Symmetric Multivariate and Related

Distributions. London: Chapman and

hall, 1990.

[33]

E. Ollila, D. E. Tyler, V. Koivunen, and H. V. Poor, “Complex elliptically

symmetric distributions: survey, new results and applications,” IEEE

Trans. Signal Process., vol. 60, no. 11, pp. 5597–5625, 2012.

[34]

K. Ashurbekova, A. Usseglio-Carleve, F. Forbes, and S. Achard, “Optimal

shrinkage for robust covariance matrix estimators in a small sample size

setting,” hal-02378034v2, 2020.

[35]

A. M. Zoubir, V. Koivunen, E. Ollila, and M. Muma, Robust Statistics for

Signal Processing. Cambridge, UK:

Cambride University Press, Nov. 2018.

[36]

R. J. Muirhead, Aspects of Multivariate Statistical Theory. New York: Wiley, 1982, 704 pages.

[37]

S. T. Smith, “Covariance, subspace, and intrinsic Cramér-Rao bounds,”

IEEE Trans. Signal Process., vol. 53, no. 5, pp. 1610–1630, 2005.

[38]

A. Breloy, G. Ginolhac, A. Renaux, and F. Bouchard, “Intrinsic

Cramér-Rao bounds for scatter and shape matrices estimation in CES

distributions,” IEEE Signal Process. Lett., vol. 26, no. 2, pp.

262–266, 2019.

[39]

J. Bun, J.-P. Bouchaud, and M. Potters, “Cleaning correlation matrices,”

Risk Management, 2016.

[40]

H. Markowitz, “Portfolio selection,” J. Financ., vol. 7, no. 1, pp.

77–91, 1952.

[41]

D. P. Palomar and R. Zhou, portfolioBacktest: Automated Backtesting of

Portfolios over Multiple Datasets, 2019, r package version 0.2.1. [Online].

Available: https://CRAN.R-project.org/package=portfolioBacktest

[42]

L. Yang, R. Couillet, and M. R. McKay, “A robust statistics approach to

minimum variance portfolio optimization,” IEEE Trans. Signal

Process., vol. 63, no. 24, pp. 6684–6697, 2015.

[43]

E. Ollila, H. Oja, and C. Croux, “The affine equivariant sign covariance

matrix: asymptotic behavior and efficiencies,” J. Mult. Anal.,

vol. 87, no. 2, pp. 328–355, 2003.

Conversion to HTML had a Fatal error and exited abruptly. This document may be truncated or damaged.