Generalized and Scalable Optimal Sparse Decision Trees

Abstract

Decision tree optimization is notoriously difficult from a computational perspective but essential for the field of interpretable machine learning. Despite efforts over the past 40 years, only recently have optimization breakthroughs been made that have allowed practical algorithms to find optimal decision trees. These new techniques have the potential to trigger a paradigm shift where it is possible to construct sparse decision trees to efficiently optimize a variety of objective functions without relying on greedy splitting and pruning heuristics that often lead to suboptimal solutions. The contribution in this work is to provide a general framework for decision tree optimization that addresses the two significant open problems in the area: treatment of imbalanced data and fully optimizing over continuous variables. We present techniques that produce optimal decision trees over a variety of objectives including F-score, AUC, and partial area under the ROC convex hull. We also introduce a scalable algorithm that produces provably optimal results in the presence of continuous variables and speeds up decision tree construction by several orders of magnitude relative to the state-of-the art.

1 Introduction

Decision tree learning has served as a foundation for interpretable artificial intelligence and machine learning for over half a century (Morgan & Sonquist, 1963; Payne & Meisel, 1977; Loh, 2014). The major approach since the 1980’s has been decision tree induction, where heuristic splitting and pruning procedures grow a tree from the top down and prune it back afterwards (Quinlan, 1993; Breiman et al., 1984). The problem with these methods is that they tend to produce suboptimal trees with no way of knowing how suboptimal the solution is. This leaves a gap between the performance that a decision tree might obtain and the performance that one actually attains, with no way to check on (or remedy) the size of this gap–and sometimes, the gap can be large.

Full decision tree optimization is NP-hard, with no polynomial-time approximation (Laurent & Rivest, 1976), leading to challenges in proving optimality or bounding the optimality gap in a reasonable amount of time, even for small datasets. It is possible to create assumptions that reduce hard decision tree optimization to cases where greedy algorithms suffice, such as independence between features (Klivans & Servedio, 2006), but these assumptions do not hold in reality. If the data can be perfectly separated with zero error, SAT solvers can be used to find optimal decision trees rapidly (Narodytska et al., 2018); however, real data is generally not separable, leaving us with no choice other than to actually solve the problem.

Decision tree optimization is amenable to branch-and-bound methods, implemented either via generic mathematical programming solvers or by customized algorithms. Solvers have been used from the 1990’s (Bennett, 1992; Bennett & Blue, 1996) to the present (Verwer & Zhang, 2019; Blanquero et al., 2018; Nijssen et al., 2020; Bertsimas & Dunn, 2017; Rudin & Ertekin, 2018; Menickelly et al., 2018; Vilas Boas et al., 2019), but these generic solvers tend to be slow. A common way to speed them up is to make approximations in preprocessing to reduce the size of the search space. For instance, “bucketization” preprocessing is used in both generic solvers (Verwer & Zhang, 2019) and customized algorithms (Nijssen et al., 2020) to handle continuous variables. Continuous variables pose challenges to optimality; even one continuous variable increases the number of possible splits by the number of possible values of that variable in the entire database, and each additional split leads to an exponential increase in the size of the optimization problem. Bucketization is tempting and seems innocuous, but we prove in Section 3 that it sacrifices optimality.

Dynamic programming methods have been used for various decision tree optimization problems since as far back as the early 1970’s (Garey, 1972; Meisel & Michalopoulos, 1973). Of the more recent attempts at this challenging problem, Garofalakis et al. (2003) use a dynamic programming method for finding an optimal subtree within a predefined larger decision tree grown using standard greedy induction. Their trees inherit suboptimality from the induction procedure used to create the larger tree. The DL8 algorithm (Nijssen & Fromont, 2007) performs dynamic programming on the space of decision trees. However, without mechanisms to reduce the size of the space and to reduce computation, the method cannot be practical. A more practical extension is the DL8.5 method (Nijssen et al., 2020), which uses a hierarchical upper bound theorem to reduce the size of the search space. However, it also uses bucketization preprocessing, which sacrifices optimality; without this preprocessing or other mechanisms to reduce computation, the method suffers in computational speed.

The CORELS algorithm (Angelino et al., 2017, 2018; Larus-Stone, 2017), which is an associative classification method rather than an optimal decision tree method, breaks away from the previous literature in that it is a custom branch-and-bound method with custom bounding theorems, its own bit-vector library, specialized data structures, and an implementation that leverages computational reuse. CORELS is able to solve problems within a minute that, using any other prior approach, might have taken weeks, or even months or years. Hu et al. (Hu et al., 2019) adapted the CORELS philosophy to produce an Optimal Sparse Decision Tree (OSDT) algorithm that leverages some of CORELS’ libraries and its computational reuse paradigm, as well as many of its theorems, which dramatically reduce the size of the search space. However, OSDT solves an exponentially harder problem than that of CORELS’ rule list optimization, producing scalability challenges, as we might expect.

This work addresses two fundamental limitations in existing work: unsatisfying results for imbalanced data and scalability challenges when trying to fully optimize over continuous variables. Thus, the first contribution of this work is to massively generalize sparse decision tree optimization to handle a wide variety of objective functions, including weighted accuracy (including multi-class), balanced accuracy, F-score, AUC and partial area under the ROC convex hull. Both CORELS and OSDT were designed to maximize accuracy, regularized by sparsity, and neither were designed to handle other objectives. CORELS has been generalized (Aïvodji et al., 2019; Chen & Rudin, 2018) to handle some constraints, but not to the wide variety of different objectives one might want to handle in practice. Generalization to some objectives is straightforward (e.g., weighted accuracy) but non-trivial in cases of optimizing rank statistics (e.g., AUC), which typically require quadratic computation in the number of observations in the dataset. However, for sparse decision trees, this time is much less than quadratic, because all observations within a leaf of a tree are tied in score, and there are a sparse number of leaves in the tree. Taking advantage of this permits us to rapidly calculate rank statistics and thus optimize over them. The second contribution is to present a new representation of the dynamic programming search space that exposes a high degree of computational reuse when modelling continuous features. The new search space representation provides a useful solution to a problem identified in the CORELS paper, which is how to use “similar support” bounds in practice. A similar support bound states that if two features in the dataset are similar, but not identical, to each other, then bounds obtained using the first feature for a split in a tree can be leveraged to obtain bounds for the same tree, were the second feature to replace the first feature. However, if the algorithm checks the similar support bound too frequently, the bound slows the algorithm down, despite reducing the search space. Our method uses hash trees that represent similar trees using shared subtrees, which naturally accelerates the evaluation of similar trees. The implementation, coupled with a new type of incremental similar support bound, is efficient enough to handle a few continuous features by creating dummy variables for all unique split points along a feature. This permits us to obtain smaller optimality gaps and certificates of optimality for mixed binary and continuous data when optimizing additive loss functions several orders of magnitude more quickly than any other method that currently exists.

Our algorithm is called Generalized and Scalable Optimal Sparse Decision Trees (GOSDT, pronounced “ghost”). A chart detailing a qualitative comparison of GOSDT to previous decision tree approaches is in Appendix A.

2 Notation and Objectives

We denote the training dataset as , where are binary features. Our notation uses , though our code is implemented for multiclass classification as well. For each real-valued feature, we create a split point at the mean value between every ordered pair of unique values present in the training data. Following notation of Hu et al. (2019), we represent a tree as a set of leaves; this is important because it allows us not to store the splits of the tree, only the conditions leading to each leaf. A leaf set contains distinct leaves, where is the classification rule of the leaf , that is, the set of conditions along the branches that lead to the leaf, and is the label prediction for all data in leaf . For a tree , we define the objective function as a combination of the loss and a penalty on the number of leaves, with regularization parameter :

| (1) |

Let us first consider monotonic losses , which are monotonically increasing in the number of false positives () and the number of false negatives (), and thus can be expressed alternatively as . We will specifically consider the following objectives in our implementation. (These are negated to become losses.)

-

•

Accuracy = : fraction of correct predictions.

-

•

Balanced accuracy = : the average of true positive rate and true negative rate. Let be the number of positive samples in the training set and be the number of negatives.

-

•

Weighted accuracy = for a predetermined threshold : the cost-sensitive accuracy that penalizes more on predicting positive samples as negative.

-

•

F-score = : the harmonic mean of precision and recall.

Optimizing F-score directly is difficult even for linear modeling, because it is non-convex (Nan et al., 2012). In optimizing F-score for decision trees, the problem is worse – a conundrum is possible where two leaves exist, the first leaf containing a higher proportion of positives than the other leaf, yet the first is classified as negative and the second classified as positive. We discuss how this can happen in Appendix D and how we address it, which is to force monotonicity by sweeping across leaves from highest to lowest predictions to calculate the F-score (see Appendix D).

We consider two objectives that are rank statistics:

-

•

Area under the ROC convex hull (AUC): the fraction of correctly ranked positive/negative pairs.

-

•

Partial area under the ROC convex hull (pAUC) for predetermined threshold : the area under the leftmost part of the ROC curve.

Some of the bounds from OSDT (Hu et al., 2019) have straightforward extensions to the objectives listed above, namely the Upper Bound on Number of Leaves and Leaf Permutation Bound. The remainder of OSDT’s bounds do not adapt. Our new bounds are the Hierarchical Objective Lower Bound, Incremental Progress Bound to Determine Splitting, Lower Bound on Incremental Progress, Equivalent Points Bound, Similar Support Bound, Incremental Similar Support Bound, and a Subset Bound. To focus our exposition, derivations and bounds for balanced classification loss, weighted classification loss, and F-score loss are in Appendix B, and derivations for AUC loss and partial AUC loss are in Appendix C, with the exception of the hierarchical lower bound for AUC, which appears in Section 2.1 to demonstrate how these bounds work.

2.1 Hierarchical Bound for AUC Optimization

Let us discuss objectives that are rank statistics. If a classifier creates binary (as opposed to real-valued) predictions, its ROC curve consists of only three points (0,0), (FPR, TPR), and (1,1). The AUC of a labeled tree is the same as the balanced accuracy, because , and since , we have . The more interesting case is when we have real-valued predictions for each leaf and use the ROC convex hull (ROCCH), defined shortly, as the objective.

Let be the number of positive samples in leaf ( is the number of negatives) and let be the fraction of positives in leaf . Let us define the area under the ROC convex hull (ROCCH) (Ferri et al., 2002) for a tree. For a tree consisting of distinct leaves, , we reorder leaves according to the fraction of positives, . For any , define a labeling for the leaves that labels the first leaves as positive and remaining as negative. The collection of these labelings is , where each defines one of the points on the ROCCH (see e.g., Ferri et al., 2002). The associated misranking loss is then 1-AUC:

| (2) |

Now let us derive a lower bound on the loss for trees that are incomplete, meaning that some parts of the tree are not yet fully grown. For a partially-grown tree , the leaf set can be rewritten as , where is a set of fixed leaves that we choose not to split further and is the set of leaves that can be further split; this notation reflects how the algorithm works, where there are multiple copies of a tree, with some nodes allowed to be split and some that are not. and are fractions of positives in the leaves. If we have a new fixed , which is a superset of , then we say is a child of . We define to be all such child trees:

| (3) |

Denote and as the number of positive and negative samples captured by respectively. Through additional splits, in the best case, can give rise to pure leaves, where positive ratios of generated leaves are either 1 or 0. Then the top-ranked leaf could contain up to positive samples (and 0 negative samples), and the lowest-ranked leaf could capture as few as 0 positive samples and up to samples. Working now with just the leaves in , we reorder the leaves in by the positive ratios (), such that . Combining these fixed leaves with the bounds for the split leaves, we can define a lower bound on the loss as follows.

Theorem 2.1.

(Lower bound for negative AUC convex hull) For a tree using as the objective, a lower bound on the loss is , where:

| (4) | |||||

This leads directly to a hierarchical lower bound for the negative of the AUC convex hull.

Theorem 2.2.

(Hierarchical objective lower bound for negative AUC convex hull) Let be a tree with fixed leaves and be any child tree such that its fixed leaves contain , and , then .

This type of bound is the fundamental tool that we use to reduce the size of the search space: if we compare the lower bound for partially constructed tree to the best current objective , and find that , then there is no need to consider or any subtree of , as it is provably non-optimal. The hierarchical lower bound dramatically reduces the size of the search space. However, we also have a collection of tighter bounds at our disposal, as summarized in the next subsection.

We leave the description of partial AUC to Appendix C. Given a parameter , the partial AUC of the ROCCH focuses only on the left area of the curve, consisting of the top ranked leaves, whose FPR is smaller than or equal to . This metric is used in information retrieval and healthcare.

2.2 Summary of Bounds

Appendix B presents our bounds, which are crucial for reducing the search space. Appendix B presents the Hierarchical Lower Bound (Theorem B.1) for any objective (Equation 1) with an arbitrary monotonic loss function. This theorem is analogous to the Hierarchical Lower Bound for AUC optimization above. Appendix B also contains the Objective Bound with One-Step Lookahead (Theorem B.2), Objective Bound for Sub-Trees (Theorem B.3), Upper Bound on the Number of Leaves (Theorem B.4), Parent-Specific Upper Bound on the Number of Leaves (Theorem B.5), Incremental Progress Bound to Determine Splitting (Theorem B.6), Lower Bound on Incremental Progress (Theorem B.7), Leaf Permutation Bound (Theorem B.8), Equivalent Points Bound (Theorem B.9), and General Similar Support Bound (Theorem B.10). As discussed, no similar support bounds have been used successfully in prior work. In Section 4.2, we show how a new Incremental Similar Support Bound can be implemented within our specialized DPB (dynamic programming with bounds) algorithm to make decision tree optimization for additive loss functions (e.g., weighted classification error) much more efficient. Bounds for AUC and pAUC are in Appendix C, including the powerful Equivalent Points Bound (Theorem C.3) for AUC and pAUC and proofs for Theorem 2.1 and Theorem 2.2. In Appendix G, we provide a new Subset Bound implemented within DPB algorithm to effectively remove thresholds introduced by continuous variables.

Note that we do not use convex proxies for rank statistics, as is typically done in supervised ranking (learning-to-rank). Optimizing a convex proxy for a rank statistic can yield results that are far from optimal (see Rudin & Wang, 2018). Instead, we optimize the original (exact) rank statistics directly on the training set, regularized by sparsity.

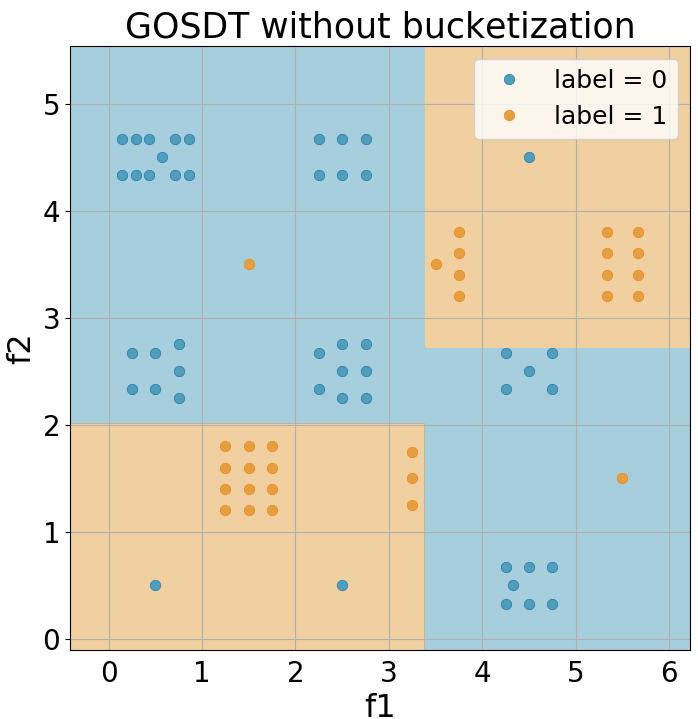

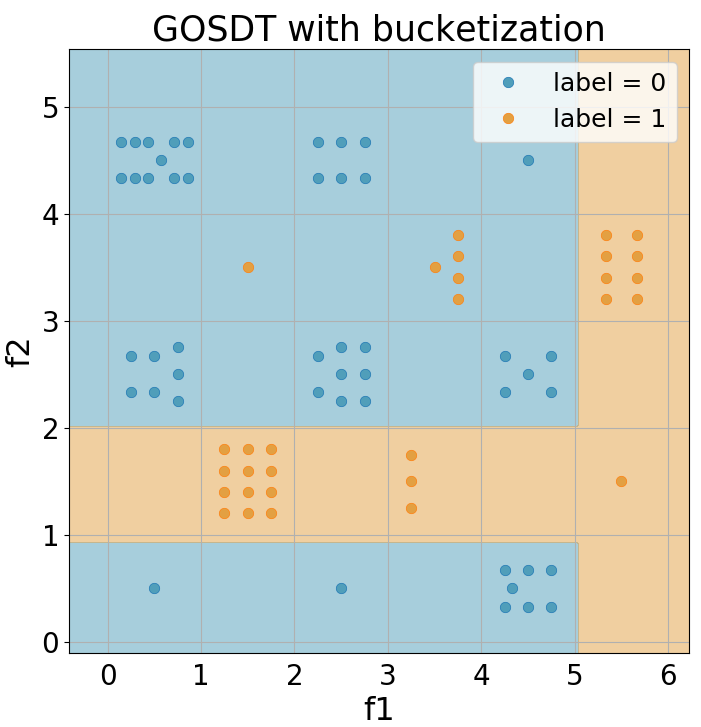

3 Data Preprocessing Using Bucketization Sacrifices Optimality

As discussed, a preprocessing step common to DL8.5 (Nijssen et al., 2020) and BinOct (Verwer & Zhang, 2019) reduces the search space, but as we will prove, also sacrifices accuracy; we refer to this preprocessing as bucketization.

Definition: The bucketization preprocessing step proceeds as follows. Order the observations according to any feature . For any two neighboring positive observations, no split can be considered between them. For any two neighboring negative observations, no split can be considered between them. All other splits are permitted. While bucketization may appear innocuous, we prove it sacrifices optimality.

Theorem 3.1.

The maximum training accuracy for a decision tree on a dataset preprocessed with bucketization can be lower (worse) than the maximum accuracy for the same dataset without bucketization.

The proof is by construction. In Figure 1 we present a data set such that optimal training with bucketization cannot produce an optimal value of the objective. In particular, the optimal accuracy without bucketization is 93.5%, whereas the accuracy of training with bucketization is 92.2%. These numbers were obtained using BinOCT, DL8.5, and GOSDT. Remember, the algorithms provide a proof of optimality; these accuracy values are optimal, and the same values were found by all three algorithms.

Our dataset is two-dimensional. We expect the sacrifice to become worse with higher dimensions.

4 GOSDT’s DPB Algorithm

For optimizing non-additive loss function, we use PyGOSDT: a variant of GOSDT that is closer to OSDT (Hu et al., 2019). For optimizing additive loss functions we use GOSDT which uses dynamic programming with bounds (DPB) to provides a dramatic run time improvement. Like other dynamic programming approaches, we decompose a problem into smaller child problems that can be solved either recursively through a function call or in parallel by delegating work to a separate thread. For decision tree optimization, these subproblems are the possible left and right branches of a decision node.

GOSDT maintains two primary data structures: a priority queue to schedule problems to solve and a dependency graph to store problems and their dependency relationships. We define a dependency relationship between problems and if and only if the solution of depends on the solution of . Each is further specified as or indicating that it is the left or right branch produced by splitting on feature .

Sections 4.1, 4.2, and 4.3 highlight two key differences between GOSDT and DL8.5 (since DL 8.5 also uses a form of dynamic programming): (1) DL8.5 uniquely identifies a problem by the Boolean assertion that is a conjunctive clause of all splitting conditions in its ancestry, while GOSDT represents a problem by the samples that satisfy the Boolean assertion. This is described in Section 4.1. (2) DL8.5 uses blocking recursive invocations to execute problems, while GOSDT uses a priority queue to schedule problems for later. This is described in Section 4.3. Section 4.4 presents additional performance optimizations. Section 4.5 presents a high-level summary of GOSDT. Note that GOSDT’s DPB algorithm operates on weighted, additive, non-negative loss functions. For ease of notation, we use classification error as the loss in our exposition.

4.1 Support Set Identification of Nodes

GOSDT leverages the Equivalent Points Bound in Theorem B.9 to save space and computational time. To use this bound, we find the unique values of , denoted by , so that each equals one of the ’s. We store fractions and , which are the fraction of positive and negative samples corresponding to each .

Define as a Boolean assertion that is a conjunctive clause of conditions on the features of (e.g., is true if and only if the first feature of is 1 and the second feature of is 0). We define support set as the set of that satisfy assertion :

| (5) |

We implement each as a bit-vector of length and use it to uniquely identify a problem in the dependency graph. The bits of are defined as follows.

| (6) |

With each , we track a set of values including its lower bound () and upper bound () of the optimal objective classifying its support set .

In contrast, DL8.5 identifies each problem using Boolean assertion rather than : this is an important difference between GOSDT and DL8.5 because many assertions could correspond to the same support set . However, given the same objective and algorithm, an optimal decision tree for any problem depends only on the support set . It does not depend on if one already knows . That is, if two different trees both contain a leaf capturing the same set of samples , the set of possible child trees for that leaf is the same for the two trees. GOSDT solves problems identified by . This way, it simultaneously solves all problems identified by any that produces .

4.2 Connection to Similar Support Bound

No previous approach has been able to implement a similar support bound effectively. We provide GOSDT’s new form of similar support bound, called the incremental similar support bound. There are two reasons why this bound works where other attempts have failed: (1) This bound works on partial trees. One does not need to have constructed a full tree to use it. (2) The bound takes into account the hierarchical objective lower bound, and hence leverages the way we search the space within the DBP algorithm. In brief, the bound effectively removes many similar trees from the search region by looking at only one of them (which does not need to be a full tree). We consider weighted, additive, non-negative loss functions: . Define the maximum weighted loss:

Theorem 4.1.

(Incremental Similar Support Bound) Consider two trees and that differ only by their root node (hence they share the same and values). Further, the root nodes between the two trees are similar enough that the support going to the left and right branches differ by at most fraction of the observations. (That is, there are observations that are captured either by the left branch of and right branch of or vice versa.) Define as the maximum of the support within and : For any child tree grown from (grown from the nodes in , that would not be excluded by the hierarchical objective lower bound) and for any child tree grown from (grown from nodes in , not excluded by the hierarchical objective lower bound), we have:

The proof is in Appendix F. Unlike the similar support bounds in CORELS and OSDT, which require pairwise comparisons of problems, this incremental similar support bound emerges from the support set representation. The descendants and share many of the same support sets. Because of this, the shared components of their upper and lower bounds are updated simultaneously (to similar values). This bound is helpful when our data contains continuous variables: if a split at value was already visited, then splits at values close to can reuse prior computation to immediately produce tight upper and lower bounds.

4.3 Asynchronous Bound Updates

GOSDT computes the objective values hierarchically by defining the minimum objective of problem as an aggregation of minimum objectives over the child problems and of for .

| (7) |

Since DL8.5 computes each and in a blocking call to the the child problems and , it necessarily computes after solving and , which is a disadvantage. In contrast, GOSDT computes bounds over that are available before knowing the exact values of and . The bounds over and are solved asynchronously and possibly in parallel. If for some and the bounds imply that , then we can conclude that ’s solution no longer depends on and . Since GOSDT executes asynchronously, it can draw this conclusion and focus on without fully solving .

To encourage this type of bound update, GOSDT uses the priority queue to send high-priority signals to each parent of when an update is available, prompting a recalculation of using Equation 7.

4.4 Fast Selective Vector Sums

New problems (i.e., and ) require initial upper and lower bounds on the optimal objective. We define the initial lower bound and upper bound for a problem identified by support set as follows. For , define:

| (8) |

This is the fraction of minority class samples in equivalence class . Then,

| (9) |

This is a basic equivalence points bound, which predicts all minority class equivalence points incorrectly. Also,

| (10) |

This upper bound comes from a baseline algorithm of predicting all one class.

We use the prefix sum trick in order to speed up computations of sums of a subset of elements of a vector. That is, for any vector (e.g., , , ), we want to compute a sum of a subsequence of : we precompute (during preprocessing) a prefix sum vector of the vector defined by the cumulative sum . During the algorithm, to sum over ranges of contiguous values in , over some indices through , we now need only take . This reduces a linear time calculation to constant time. This fast sum is leveraged over calculations with the support sets of input features–for example, quickly determining the difference in support sets between two features.

4.5 The GOSDT Algorithm

Algorithm 1 constructs and optimizes problems in the dependency graph such that, upon completion, we can extract the optimal tree by traversing the dependency graph by greedily choosing the split with the lowest objective value. This extraction algorithm and a more detailed version of the GOSDT algorithm is provided in Appendix J. We present the key components of this algorithm, highlighting the differences between GOSDT and DL8.5. Note that all features have been binarized prior to executing the algorithm.

Lines 8 to 11: Remove an item from the queue. If its bounds are equal, no further optimization is possible and we can proceed to the next item on the queue.

Lines 12 to 18: Construct new subproblems, , by splitting on feature . Use lower and upper bounds of and to compute new bounds for . We key the problems by the bit vector corresponding to their support set . Keying problems in this way avoids processing the same problem twice; other dynamic programming implementations, such as DL8.5, will process the same problem multiple times.

Lines 19 to 23: Update with and computed using Equation 7 and propagate that update to all ancestors of by enqueueing them with high priority ( will have multiple parents if two different conjunctions produce the same support set). This triggers the ancestor problems to recompute their bounds using Equation 7. The high priority ensures that ancestral updates occur before processing and . This scheduling is one of the key differences between GOSDT and DL8.5; by eagerly propagating bounds up the dependency tree, GOSDT prunes the search space more aggressively.

Lines 26 to 32: Enqueue and only if the interval between their lower and upper bounds overlaps with the interval between ’s lower and upper bounds. This ensures that eventually the lower and upper bounds of converge to a single value.

Lines 34 to 42: Define FIND_OR_CREATE_NODE, which constructs (or finds an existing) problem corresponding to support set , initializing the lower and upper bound and checking if is eligible to be split, using the Incremental Progress Bound to Determine Splitting (Theorem B.6) and the Lower Bound on Incremental Progress (Theorem B.7) (these bounds are checked in subroutine fails_bounds). get_lower_bound returns using Equation 9. get_upper_bound returns using Equation 10.

An implementation of the algorithm is available at: https://github.com/Jimmy-Lin/GeneralizedOptimalSparseDecisionTrees.

| 1: | input: , , , , // risk, samples, regularizer | |||

| 2: | // priority queue | |||

| 3: | // dependency graph | |||

| 4: | // bit-vector of 1’s of length | |||

| 5: | FIND_OR_CREATE_NODE() // root | |||

| 6: | // add to priority queue | |||

| 7: | while do | |||

| 8: | // index of problem to work on | |||

| 9: | // find problem to work on | |||

| 10: | if then | |||

| 11: | continue // problem already solved | |||

| 12: | // loose starting bounds | |||

| 13: | for each feature do | |||

| 14: | // create children | |||

| 15: | FIND_OR_CREATE_NODE | |||

| 16: | FIND_OR_CREATE_NODE | |||

| // create bounds as if were chosen for splitting | ||||

| 17: | ||||

| 18: | ||||

| // signal the parents if an update occurred | ||||

| 19: | if or then | |||

| 20: | ||||

| 21: | ||||

| 22: | for do | |||

| // propagate information upwards | ||||

| 23: | ||||

| 24: | if then | |||

| 25: | continue // problem solved just now | |||

| // loop, enqueue all children | ||||

| 26: | for each feature do | |||

| // fetch and in case of update | ||||

| 27: | repeat line 14-16 | |||

| 28: | ||||

| 29: | ||||

| 30: | if and then | |||

| 31: | ||||

| 32: | ||||

| 33: | return | |||

| ——————————————————————– | ||||

| 34: | subroutine FIND_OR_CREATE_NODE(G,s) | |||

| 35: | if // not yet in graph | |||

| 36: | // identify by | |||

| 37: | ||||

| 38: | ||||

| 39: | if fails_bounds then | |||

| 40: | // no more splitting allowed | |||

| 41: | G.insert(p) // put in dependency graph | |||

| 42: | return G.find(s) |

5 Experiments

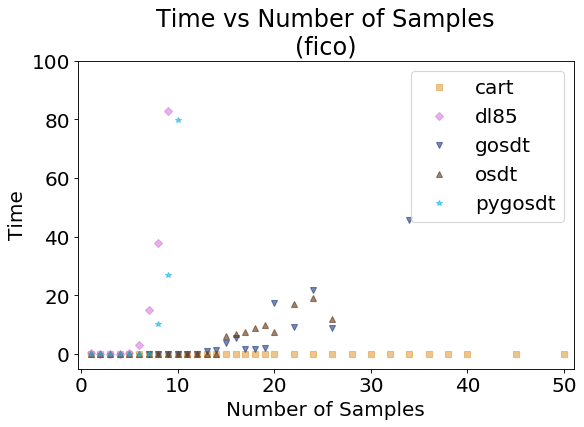

We present details of our experimental setup and datasets in Appendix I. GOSDT’s novelty lies in its ability to optimize a large class of objective functions and its ability to efficiently handle continuous variables without sacrificing optimality. Thus, our evaluation results: 1) Demonstrate our ability to optimize over a large class of objectives (AUC in particular), 2) Show that GOSDT outperforms other approaches in producing models that are both accurate and sparse, and 3) Show how GOSDT scales in its handling of continuous variables relative to other methods. In Appendix I we show time-to-optimality results.

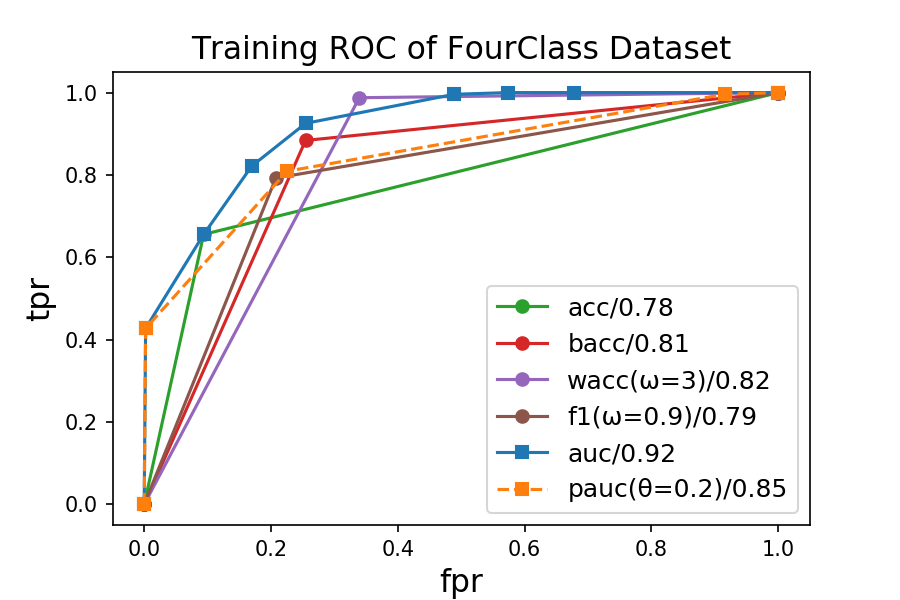

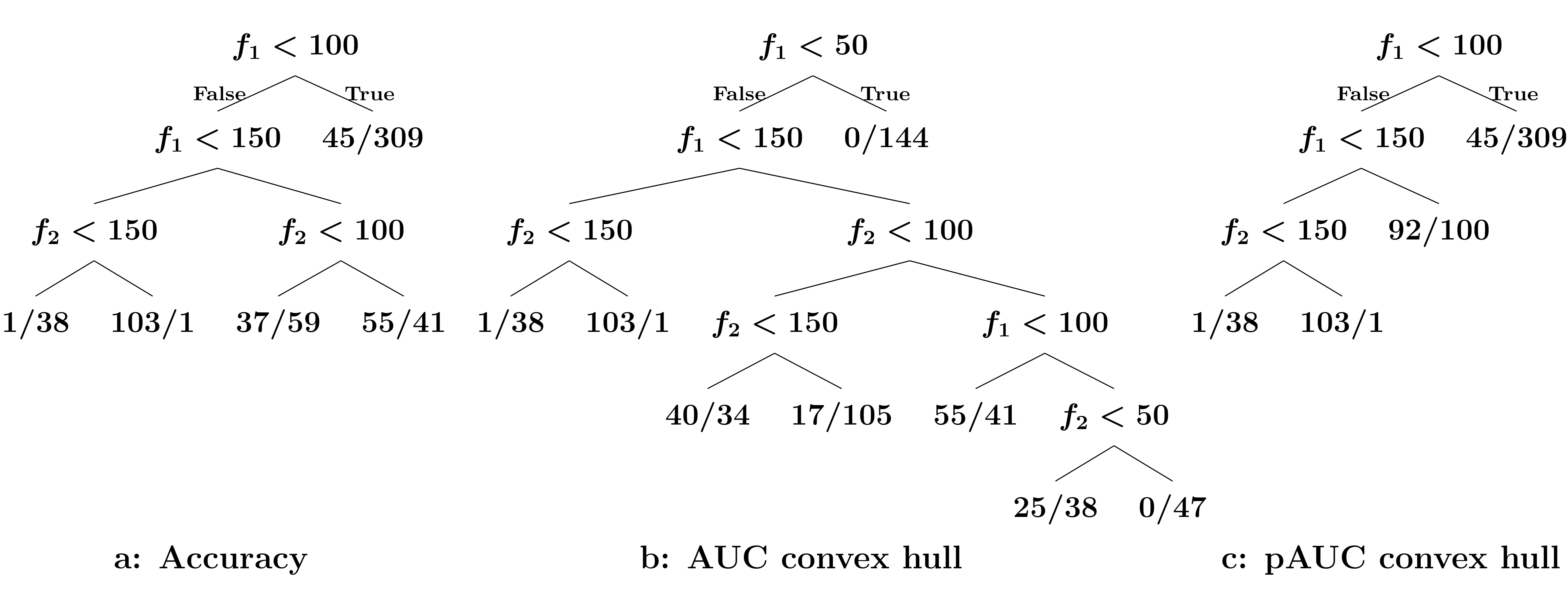

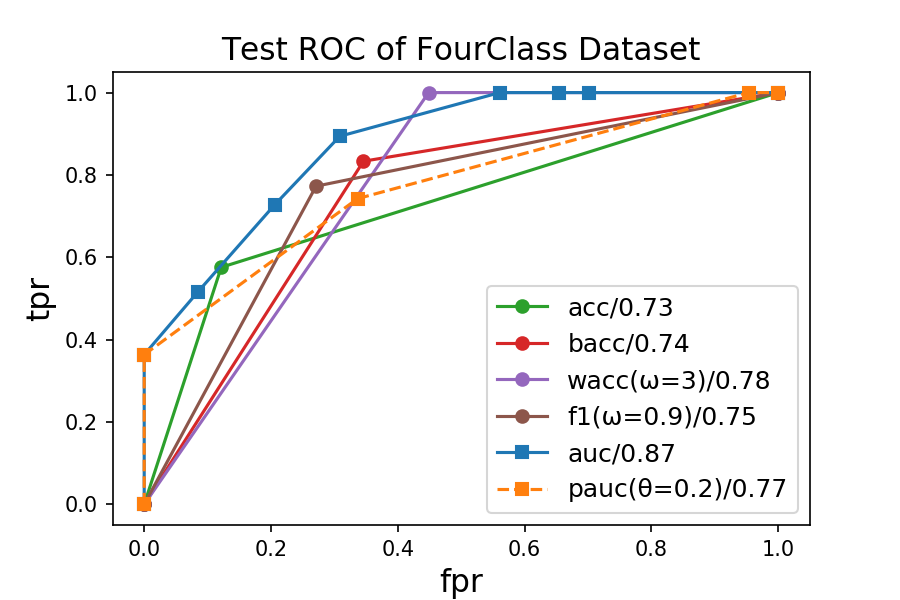

Optimizing Many Different Objectives: We use the FourClass dataset (Chang & Lin, 2011) to show optimal decision trees corresponding to different objectives. Figures 3 and 3 show the training ROC of decision trees generated for six different objectives and optimal trees for accuracy, AUC and partial area under ROC convex hull. Optimizing different objectives produces different trees with different and . (No other decision tree method is designed to fully optimize any objective except accuracy, so there is no comparison to other methods.)

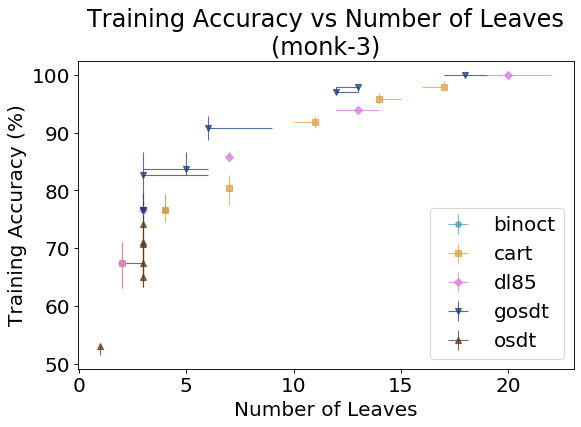

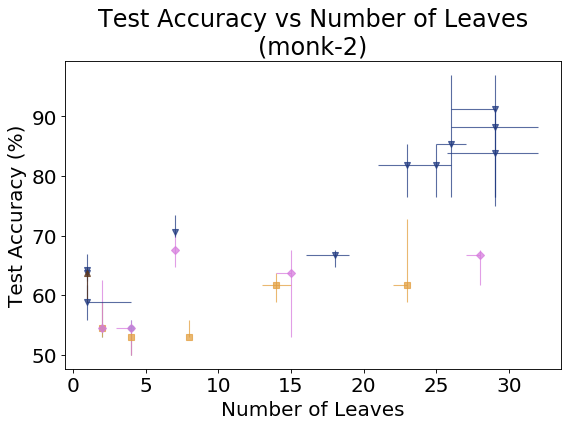

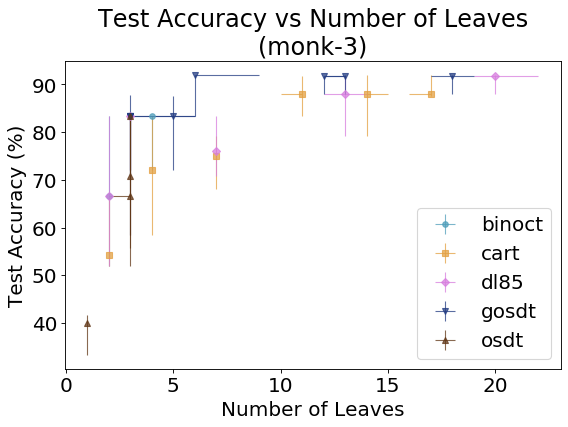

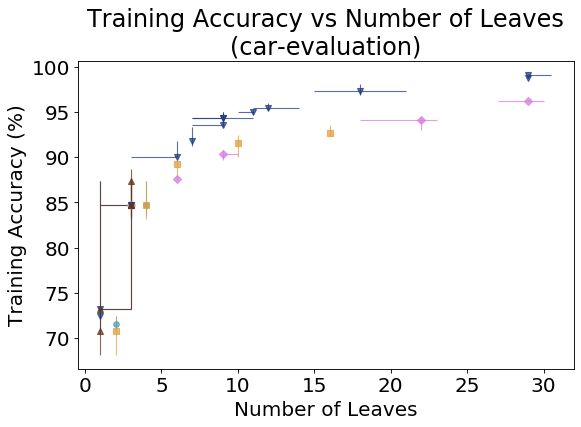

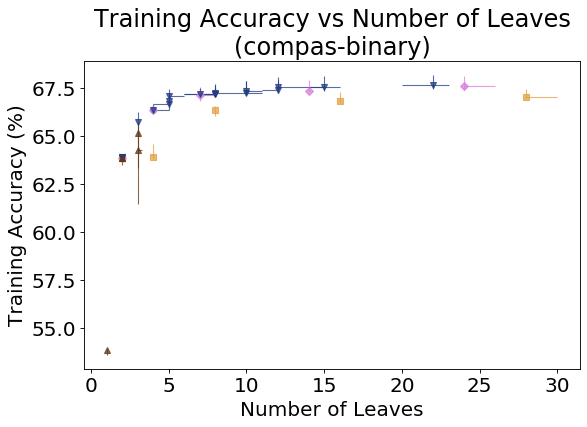

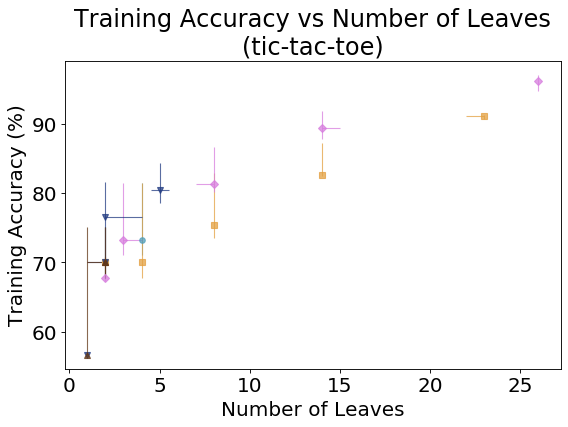

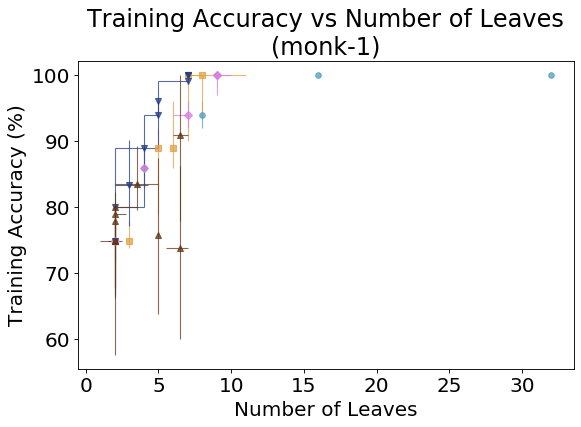

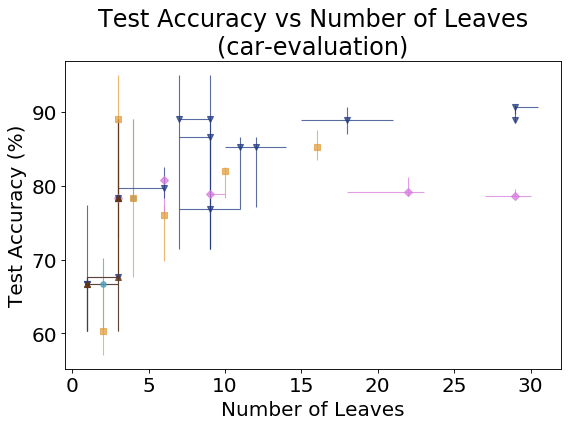

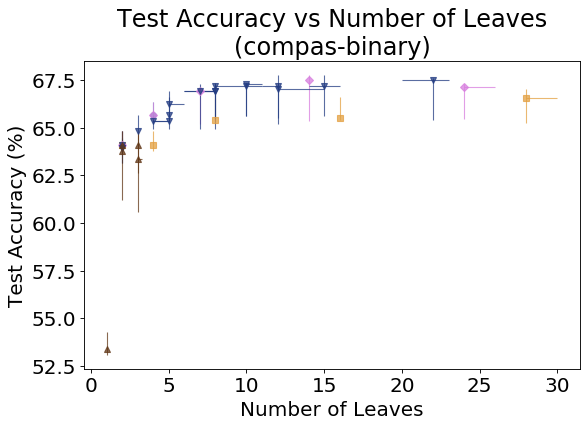

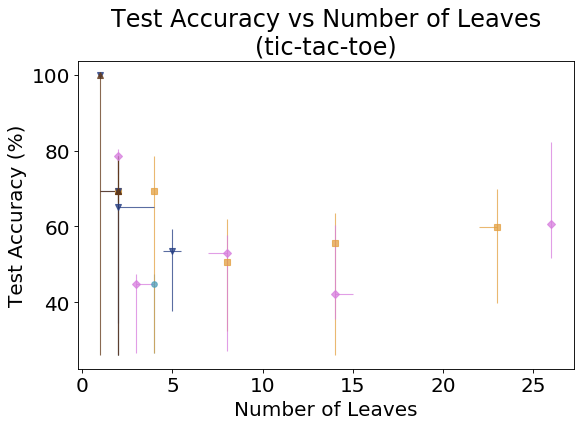

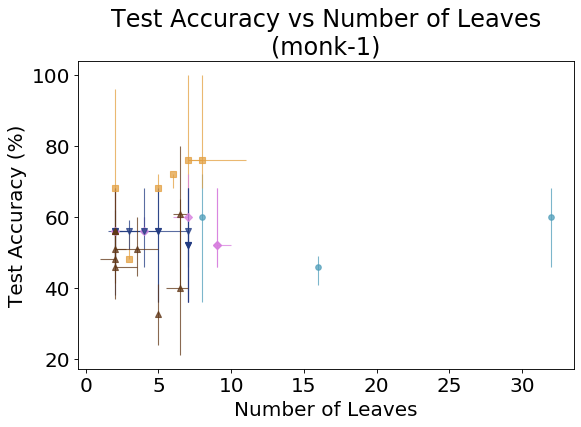

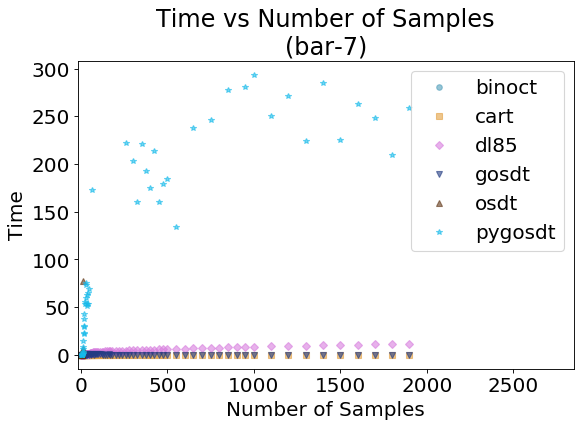

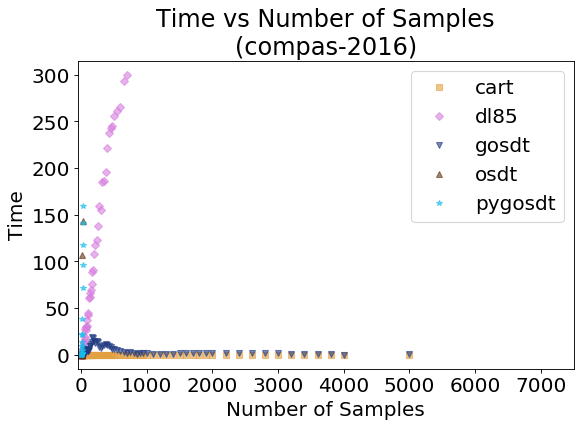

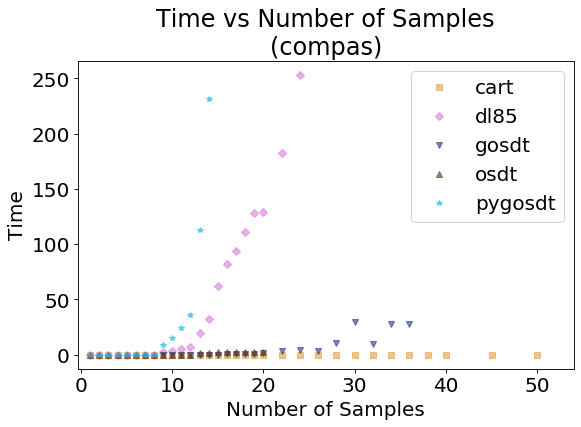

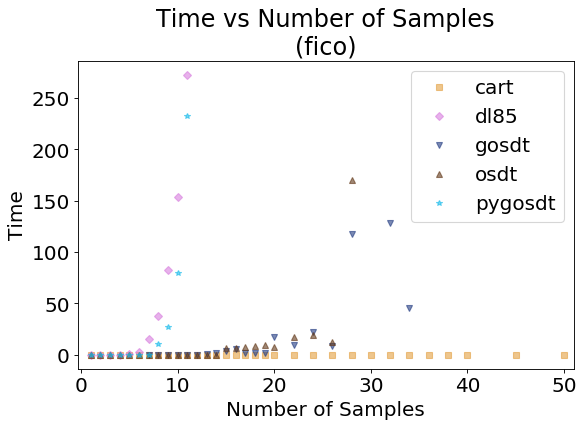

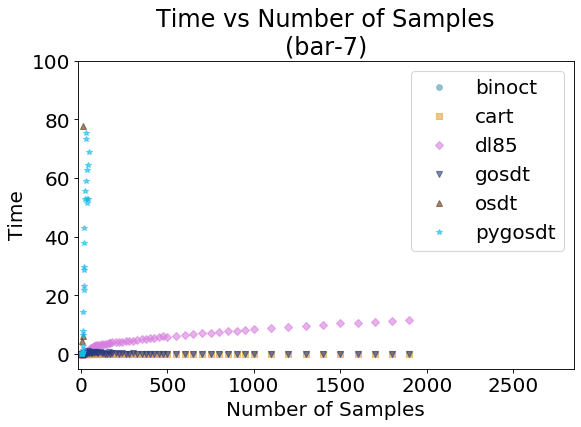

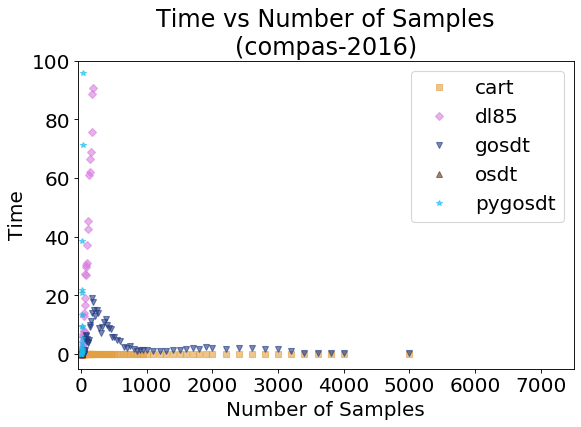

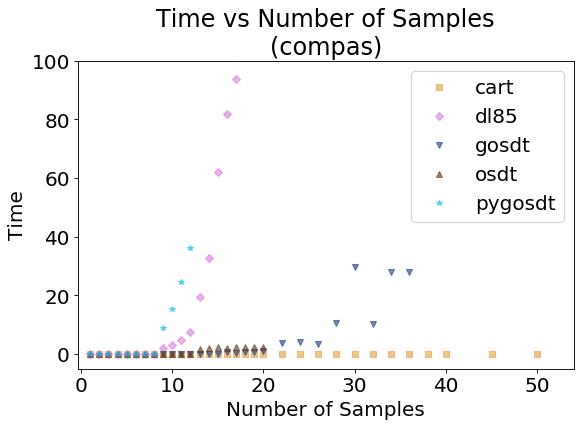

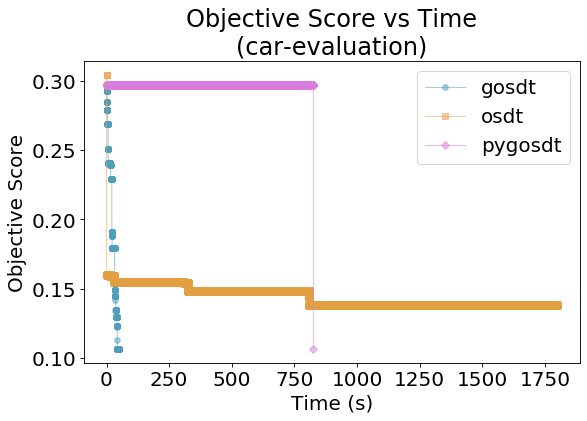

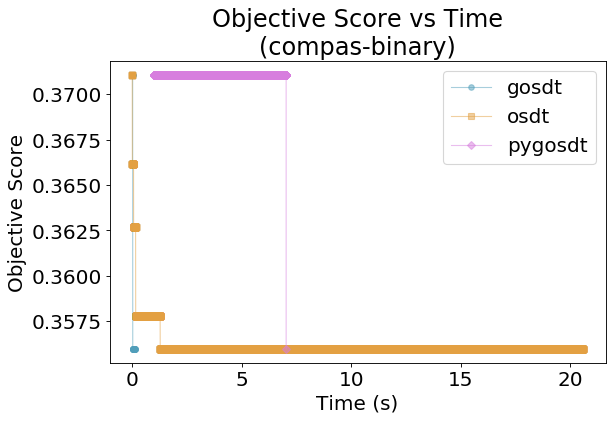

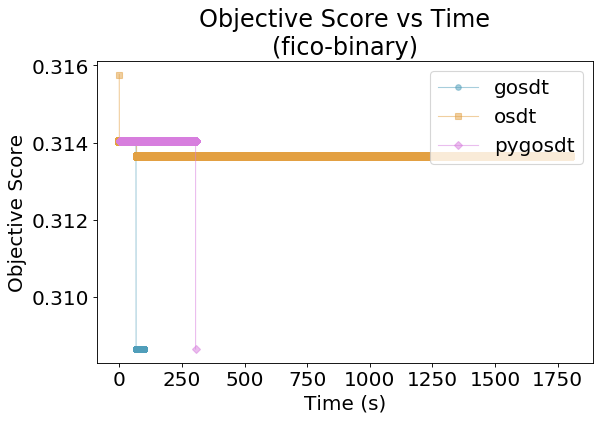

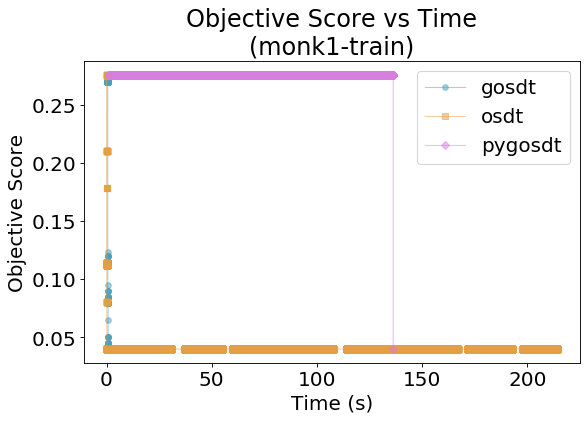

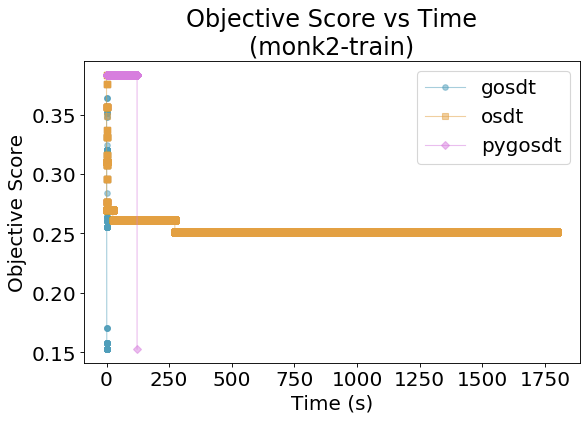

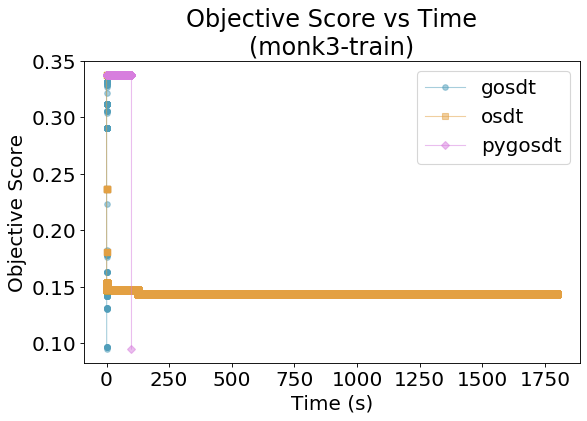

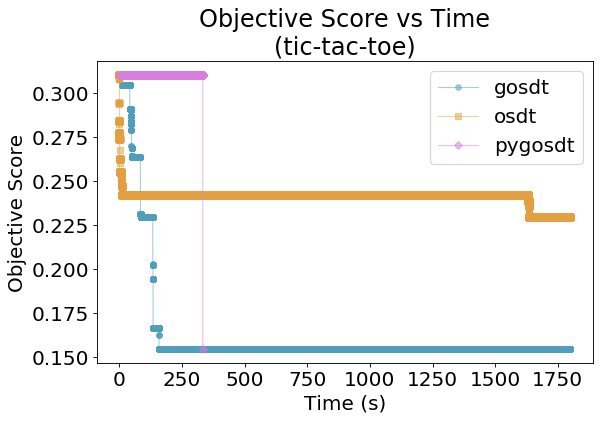

Binary Datasets, Accuracy vs Sparsity: We compare models produced from BinOCT (Verwer & Zhang, 2019), CART (Breiman et al., 1984), DL8.5 (Nijssen et al., 2020), OSDT (Hu et al., 2019), and GOSDT. For each method, we select hyperparameters to produce trees of varying numbers of leaves and plot training accuracy against sparsity (number of leaves). GOSDT directly optimizes the trade-off between training accuracy and number of leaves, producing points on the efficient frontier. Figure 4 and 5 show (1) that GOSDT typically produces excellent training and test accuracy with a reasonable number of leaves, and (2) that we can quantify how close to optimal the other methods are. Learning theory provides guarantees that training and test accuracy are close for sparse trees; more results are in Appendix I.

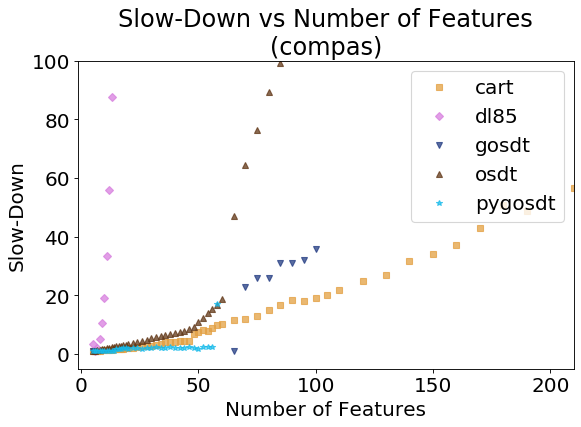

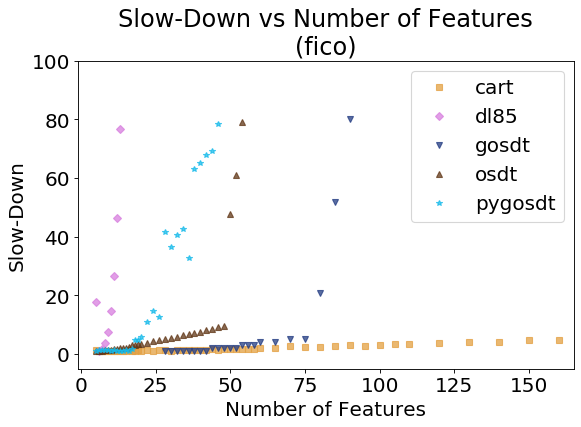

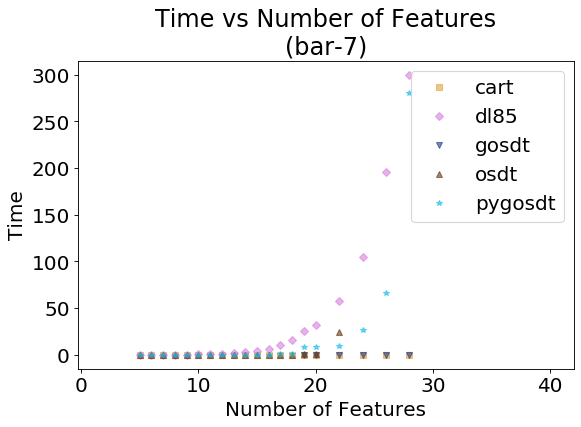

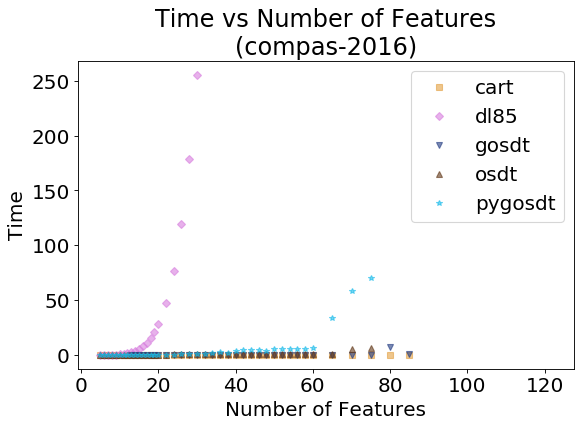

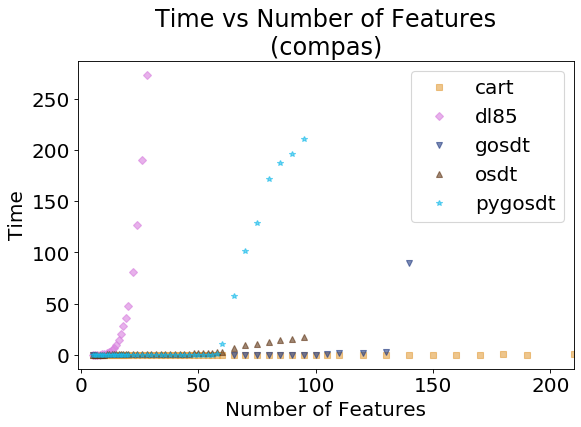

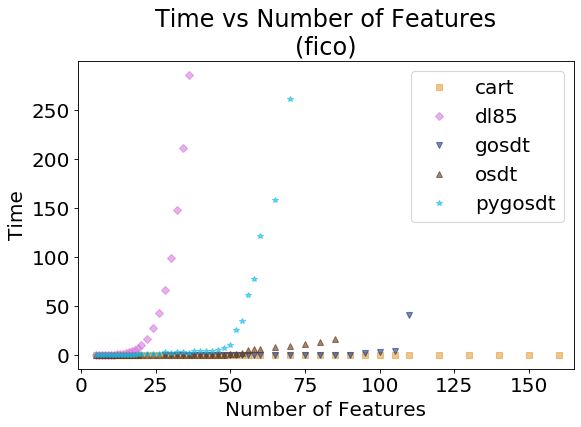

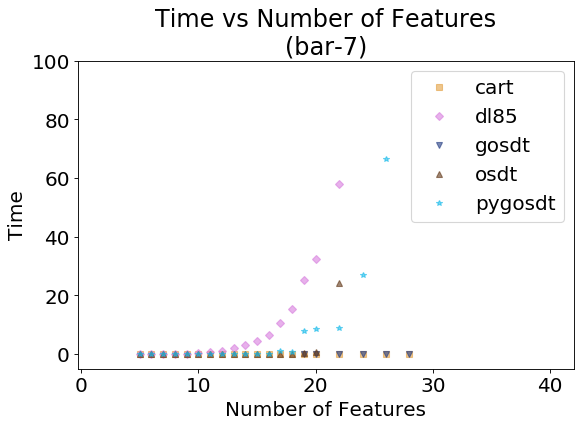

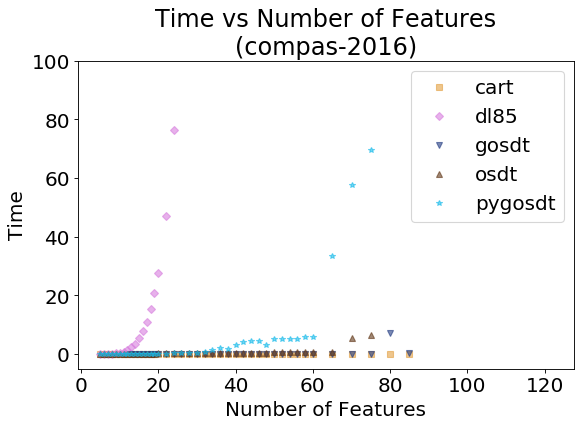

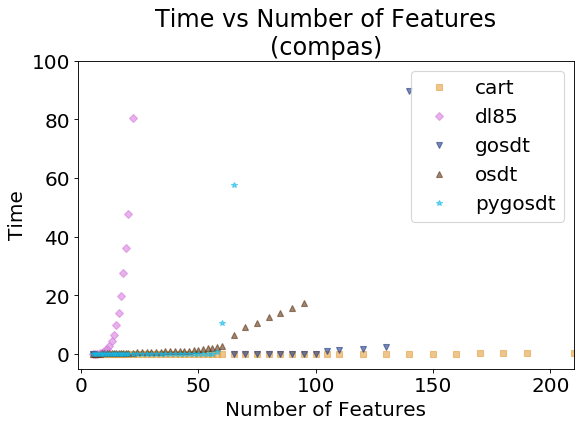

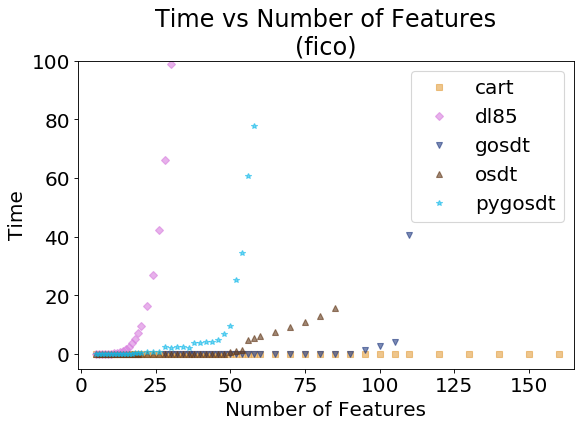

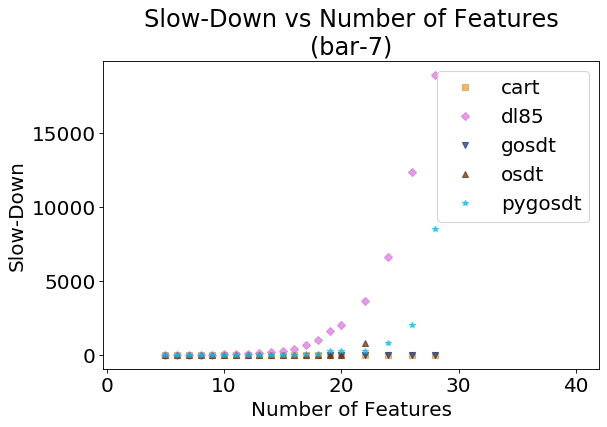

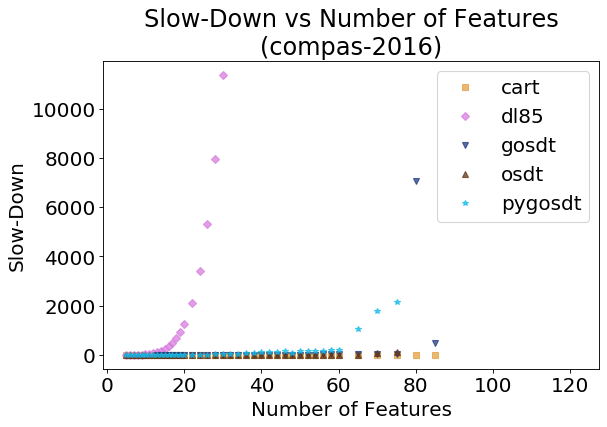

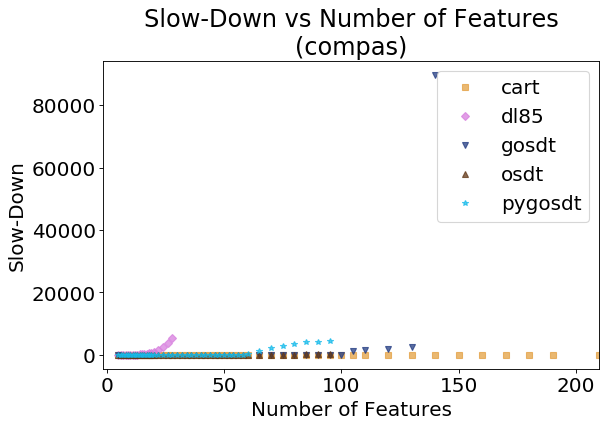

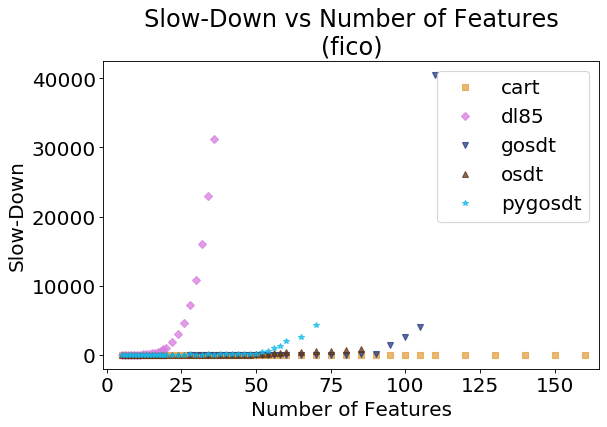

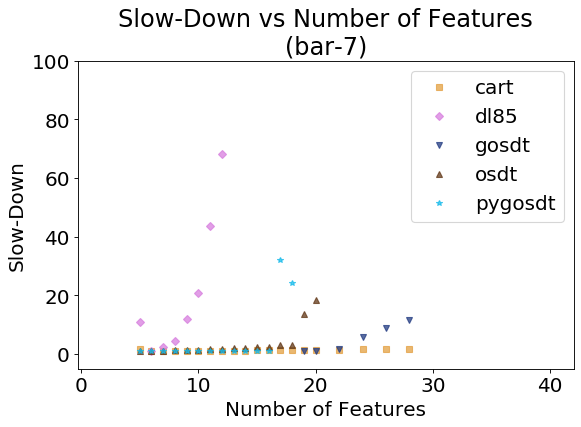

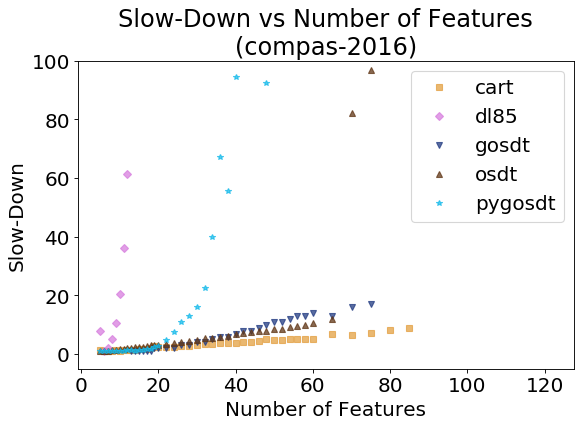

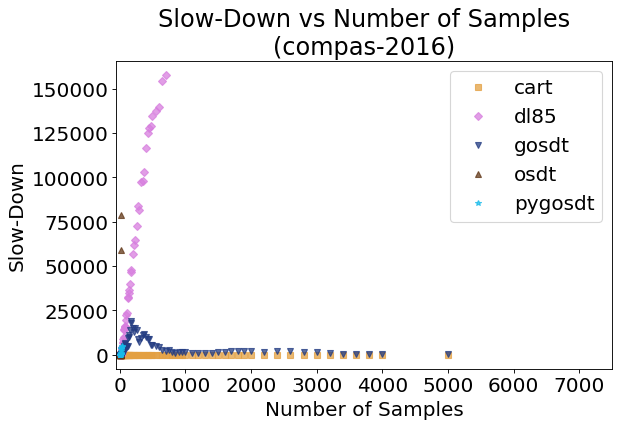

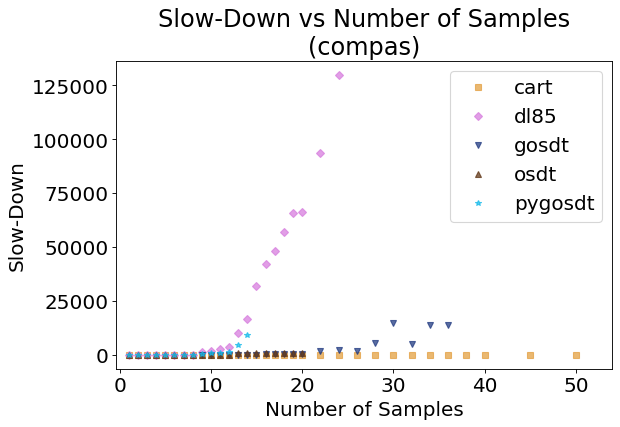

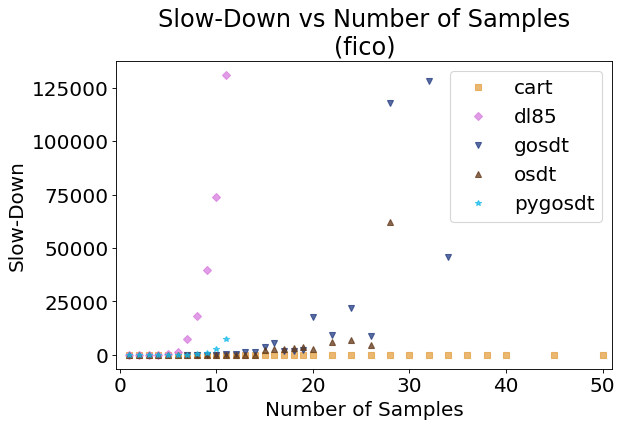

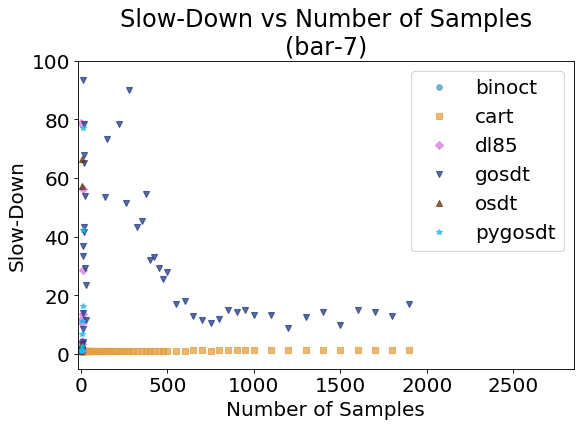

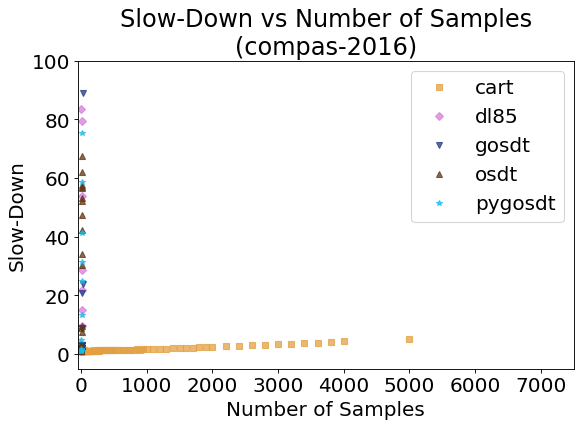

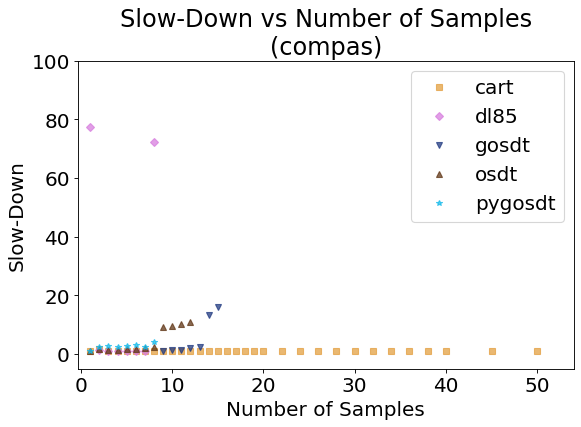

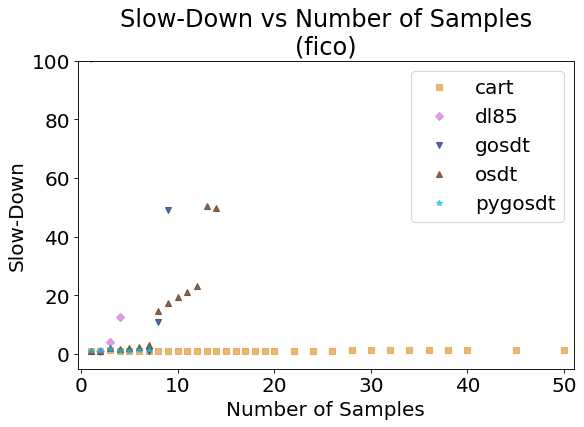

Continuous Datasets, Slowdown vs Thresholds: We preprocessed by encoding continuous variables as a set of binary variables, using all possible thresholds. We then reduced the number of binary variables by combining sets of variables for increasing values of . Binary variables were ordered, firstly, in order of the indices of the continuous variable to which they correspond, and secondly, in order of their thresholds. We measure the slow-down introduced by increasing the number of binary variables relative to each algorithm’s own best time. Figure 6 shows these results for CART, DL8.5, GOSDT, and OSDT. As the number of features increases (i.e., approaches 1), GOSDT typically slows down less than DL8.5 and OSDT. This relatively smaller slowdown allows GOSDT to handle more thresholds introduced by continuous variables.

Appendix I presents more results including training times several orders of magnitude better than the state-of-the-art.

An implementation of our experiments is available at: https://github.com/Jimmy-Lin/TreeBenchmark.

6 Discussion and Future Work

GOSDT (and related methods) differs fundamentally from other types of machine learning algorithms. Unlike neural networks and typical decision tree methods, it provides a proof of optimality for highly non-convex problems. Unlike support vector machines, ensemble methods, and neural networks again, it produces sparse interpretable models without using convex proxies–it solves the exact problem of interest in an efficient and provably optimal way. As usual, statistical learning theoretic guarantees on test error are the tightest for simpler models (sparse models) with the lowest empirical error on the training set, hence the choice of accuracy, regularized by sparsity (simplicity). If GOSDT is stopped early, it reports an optimality gap, which allows the user to assess whether the tree is sufficiently close to optimal, retaining learning theoretic guarantees on test performance. GOSDT is most effective for datasets with a small or medium number of features. The algorithm scales well with the number of observations, easily handling tens of thousands.

There are many avenues for future work. Since GOSDT provides a framework to handle objectives that are monotonic in and , one could create many more objectives than we have enumerated here. Going beyond these objectives to handle other types of monotonicity, fairness, ease-of-use, and cost-related soft and hard constraints are natural extensions. There are many avenues to speed up GOSDT related to exploration of the search space, garbage collection, and further bounds.

References

- Aïvodji et al. (2019) Aïvodji, U., Ferry, J., Gambs, S., Huguet, M.-J., and Siala, M. Learning Fair Rule Lists. arXiv e-prints, pp. arXiv:1909.03977, Sep 2019.

- Angelino et al. (2017) Angelino, E., Larus-Stone, N., Alabi, D., Seltzer, M., and Rudin, C. Learning certifiably optimal rule lists for categorical data. In Proc. ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (KDD), 2017.

- Angelino et al. (2018) Angelino, E., Larus-Stone, N., Alabi, D., Seltzer, M., and Rudin, C. Learning certifiably optimal rule lists for categorical data. Journal of Machine Learning Research, 18(234):1–78, 2018.

- Bennett (1992) Bennett, K. Decision tree construction via linear programming. In Proceedings of the 4th Midwest Artificial Intelligence and Cognitive Science Society Conference, Utica, Illinois, 1992.

- Bennett & Blue (1996) Bennett, K. P. and Blue, J. A. Optimal decision trees. Technical report, R.P.I. Math Report No. 214, Rensselaer Polytechnic Institute, 1996.

- Bertsimas & Dunn (2017) Bertsimas, D. and Dunn, J. Optimal classification trees. Machine Learning, 106(7):1039–1082, 2017.

- Blanquero et al. (2018) Blanquero, R., Carrizosa, E., Molero-Rıo, C., and Morales, D. R. Optimal randomized classification trees. August 2018.

- Breiman et al. (1984) Breiman, L., Friedman, J. H., Olshen, R. A., and Stone, C. J. Classification and Regression Trees. Wadsworth, 1984.

- Chang & Lin (2011) Chang, C.-C. and Lin, C.-J. Libsvm: a library for support vector machines, 2011. software available at http://www.csie.ntu.edu.tw/~cjlin/libsvm.

- Chen & Rudin (2018) Chen, C. and Rudin, C. An optimization approach to learning falling rule lists. In International Conference on Artificial Intelligence and Statistics (AISTATS), 2018.

- Dheeru & Karra Taniskidou (2017) Dheeru, D. and Karra Taniskidou, E. UCI machine learning repository, 2017. URL http://archive.ics.uci.edu/ml.

- Ferri et al. (2002) Ferri, C., Flach, P., and Hernández-Orallo, J. Learning decision trees using the area under the ROC curve. In International Conference on Machine Learning (ICML), volume 2, pp. 139–146, 2002.

- FICO et al. (2018) FICO, Google, Imperial College London, MIT, University of Oxford, UC Irvine, and UC Berkeley. Explainable Machine Learning Challenge. https://community.fico.com/s/explainable-machine-learning-challenge, 2018.

- Garey (1972) Garey, M. Optimal binary identification procedures. SIAM J. Appl. Math., 23(2):173––186, September 1972.

- Garofalakis et al. (2003) Garofalakis, M., Hyun, D., Rastogi, R., and Shim, K. Building decision trees with constraints. Data Mining and Knowledge Discovery, 7:187–214, 2003.

- Hu et al. (2019) Hu, X., Rudin, C., and Seltzer, M. Optimal sparse decision trees. In Proceedings of Neural Information Processing Systems (NeurIPS), 2019.

- Klivans & Servedio (2006) Klivans, A. R. and Servedio, R. A. Toward attribute efficient learning of decision lists and parities. Journal of Machine Learning Research, 7:587–602, 2006.

- Larson et al. (2016) Larson, J., Mattu, S., Kirchner, L., and Angwin, J. How we analyzed the COMPAS recidivism algorithm. ProPublica, 2016.

- Larus-Stone (2017) Larus-Stone, N. L. Learning Certifiably Optimal Rule Lists: A Case For Discrete Optimization in the 21st Century. 2017. Undergraduate thesis, Harvard College.

- Laurent & Rivest (1976) Laurent, H. and Rivest, R. L. Constructing optimal binary decision trees is np-complete. Information processing letters, 5(1):15–17, 1976.

- Loh (2014) Loh, W.-Y. Fifty years of classification and regression trees. International Statistical Review, 82(3):329–348, 2014.

- Meisel & Michalopoulos (1973) Meisel, W. S. and Michalopoulos, D. A partitioning algorithm with application in pattern classification and the optimization of decision tree. IEEE Trans. Comput., C-22, pp. 93–103, 1973.

- Menickelly et al. (2018) Menickelly, M., Günlük, O., Kalagnanam, J., and Scheinberg, K. Optimal decision trees for categorical data via integer programming. Preprint at arXiv:1612.03225, January 2018.

- Morgan & Sonquist (1963) Morgan, J. N. and Sonquist, J. A. Problems in the analysis of survey data, and a proposal. J. Amer. Statist. Assoc., 58:415–434, 1963.

- Nan et al. (2012) Nan, Y., Chai, K. M., Lee, W. S., and Chieu, H. L. Optimizing F-measure: A tale of two approaches. arXiv preprint arXiv:1206.4625, 2012.

- Narodytska et al. (2018) Narodytska, N., Ignatiev, A., Pereira, F., and Marques-Silva, J. Learning optimal decision trees with SAT. In Proc. International Joint Conferences on Artificial Intelligence (IJCAI), pp. 1362–1368, 2018.

- Nijssen & Fromont (2007) Nijssen, S. and Fromont, E. Mining optimal decision trees from itemset lattices. In Proceedings of the ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (KDD), pp. 530–539. ACM, 2007.

- Nijssen et al. (2020) Nijssen, S., Schaus, P., et al. Learning optimal decision trees using caching branch-and-bound search. In Thirty-Fourth AAAI Conference on Artificial Intelligence, 2020.

- Payne & Meisel (1977) Payne, H. J. and Meisel, W. S. An algorithm for constructing optimal binary decision trees. IEEE Transactions on Computers, C-26(9):905–916, 1977.

- Quinlan (1993) Quinlan, J. R. C4.5: Programs for Machine Learning. Morgan Kaufmann, 1993.

- Rudin & Ertekin (2018) Rudin, C. and Ertekin, S. Learning customized and optimized lists of rules with mathematical programming. Mathematical Programming C (Computation), 10:659–702, 2018.

- Rudin & Wang (2018) Rudin, C. and Wang, Y. Direct learning to rank and rerank. In International Conference on Artificial Intelligence and Statistics (AISTATS), pp. 775–783, 2018.

- Verwer & Zhang (2019) Verwer, S. and Zhang, Y. Learning optimal classification trees using a binary linear program formulation. In Proc. Thirty-third AAAI Conference on Artificial Intelligence, 2019.

- Vilas Boas et al. (2019) Vilas Boas, M. G., Santos, H. G., Merschmann, L. H. d. C., and Vanden Berghe, G. Optimal decision trees for the algorithm selection problem: integer programming based approaches. International Transactions in Operational Research, 2019.

- Wang et al. (2017) Wang, T., Rudin, C., Doshi-Velez, F., Liu, Y., Klampfl, E., and MacNeille, P. A Bayesian framework for learning rule sets for interpretable classification. Journal of Machine Learning Research, 18(70):1–37, 2017.

Appendix A Comparison Between Decision Tree Methods

| Attributes | GOSDT | DL8 | DL8.5 | BinOCT | DTC | CART |

|---|---|---|---|---|---|---|

| Built-in Preprocessor | Yes | No | No | Yes | No | No |

| Preprocessing Strategy | All values | Weka Discretization | Bucketization | Bucketization | None | None |

| Preprocessing Preserves Optimality? | Yes | No | No | No | N/A | N/A |

| Optimization Strategy | DPB | DP | DPB | ILP | Greedy Search | Greedy Search |

| Optimization Preserves Optimality? | Yes | Yes | Yes | Yes | No | No |

| Applies Hierarchical Upper bound to Reduce Search Space? | Yes | No | Yes | N/A | N/A | N/A |

| Uses Support Set Node Identifiers? | Yes | No | No | N/A | N/A | N/A |

| Can use Multiple Cores? | Yes | No | No | Yes | No | No |

| Can prune using updates from partial evaluation of subproblem? | Yes | No | No | Depends on (generic) solver | N/A | N/A |

| Strategy for preventing overfitting | Penalize Leaves | Structural Constraints | Structural Constraints | Structural Constraints | MDL Criteria | Structural Constraints |

| Can we modify this to use regularization? | N/A | Yes | Yes | Yes | N/A | No |

| Does it address class imbalance? | Yes | Maybe | Maybe | Maybe | Maybe | Maybe |

Appendix B Objectives and Their Lower Bounds for Arbitrary Monotonic Losses

Before deriving the bounds for arbitrary monotonic losses, we first introduce some notation. As we know, a leaf set contains distinct leaves, where is the classification rule of the leaf . If a leaf is labeled, then is the label prediction for all data in leaf . Therefore, a labeled partially-grown tree with the leaf set could be rewritten as , where is a set of fixed leaves that are not permitted to be further split, are the predicted labels for leaves , is the set of leaves that can be further split, and are the predicted labels for leaves .

B.1 Hierarchical objective lower bound for arbitrary monotonic losses

Theorem B.1.

(Hierarchical objective lower bound for arbitrary monotonic losses) Let loss function be monotonically increasing in and . We now change notation of the loss to be only a function of these two quantities, written now as . Let be a labeled tree with fixed leaves , and let and be the false positives and false negatives of . Define the lower bound to the risk as follows (taking the lower bound of the split terms to be 0):

Let be any child tree of such that its fixed leaves contain and and . Then, .

The importance of this result is that the lower bound works for all (allowed) child trees of . Thus, if can be excluded via the lower bound, then all of its children can too.

Proof.

Let and be the false positives and false negatives within leaves of , and let and be the false positives and false negatives within leaves of . Similarly, denote and as the false positives and false negatives of and let and be the false positives and false negatives of . Since the leaves are mutually exclusive, and . Moreover, since is monotonically increasing in and , we have:

| (11) |

Similarly, . Since , and , thus . Combined with , we have:

| (12) |

∎

Let us move to the next bound, which is the one-step lookahead. It relies on comparing the best current objective we have seen so far, denoted , to the lower bound.

Theorem B.2.

(Objective lower bound with one-step lookahead) Let be a -leaf tree with leaves fixed and let be the current best objective. If , then for any child tree , its fixed leaves include and . It follows that .

Proof.

According to definition of the objective lower bound,

| (13) |

where on the last line we used that since and are both integers, then . ∎

According to this bound, even though we might have a tree whose fixed leaves obeys lower bound , its child trees may still all be guaranteed to be suboptimal: if , none of its child trees can ever be an optimal tree.

Theorem B.3.

(Hierarchical objective lower bound for sub-trees and additive losses) Let loss functions be monotonically increasing in and , and let the loss of a tree be the sum of the losses of the leaves. Let be the current best objective. Let be a tree such that the root node is split by a feature, where two sub-trees and are generated with leaves for and leaves for . The data captured by the left tree is and the data captured by the right tree is . Let and be the objective lower bound of the left sub-tree and right sub-tree respectively such that and . If or or , then the tree is not the optimal tree.

This bound is applicable to any tree , even if part of it has not been constructed yet. That is, if a partially-constructed ’s left lower bound or right lower bound, or the sum of left and right lower bounds, exceeds the current best risk , then we do not need to construct since we have already proven it to be suboptimal from its partial construction.

Proof.

. If or or , then . Therefore, the tree is not the optimal tree. ∎

B.2 Upper bound on the number of leaves

Theorem B.4.

(Upper bound on the number of leaves) For a dataset with features, consider a state space of all trees. Let be the number of leaves of tree and let be the current best objective. For any optimal tree , its number of leaves obeys:

| (14) |

where is the regularization parameter.

Proof.

This bound adapts directly from OSDT (Hu et al., 2019), where the proof can be found. ∎

Theorem B.5.

(Parent-specific upper bound on the number of leaves) Let be a tree, be any child tree such that , and be the current best objective. If has lower bound , then

| (15) |

where is the regularization parameter.

Proof.

This bound adapts directly from OSDT (Hu et al., 2019), where the proof can be found. ∎

B.3 Incremental Progress Bound to Determine Splitting and Lower Bound on Incremental Progress

In the implementation, Theorem B.6 below is used to check if a leaf node within is worth splitting. If the bound is satisfied and the leaf can be further split, then we generate new leaves and Theorem B.7 is applied to check if this split yields new nodes or leaves that are good enough to consider in the future. Let us give an example to show how Theorem B.6 is easier to compute than Theorem B.7. If we are evaluating a potential split on leaf , Theorem B.6 requires and which are the false positives and false negatives for leaf , but no extra information about the split we are going to make, whereas Theorem B.7 requires that additional information. Let us work with balanced accuracy as the loss function: for Theorem B.6 below, we would need to compute but for Theorem B.7 below we would need to calculate quantities for the new leaves we would form by splitting into child leaves and . Namely, we would need , , , and as well.

Theorem B.6.

(Incremental progress bound to determine splitting) Let be any optimal tree with objective , i.e., . Consider tree derived from by deleting a pair of leaves and and adding their parent leaf , . Let . Then, must be at least .

Proof.

and . The difference between and is maximized when and correctly classify all the captured data. Therefore, is the maximal difference between and . Since , we can get , that is (and remember that is of size whereas is of size ), . Since is optimal with respect to , , thus, . ∎

Hence, for a tree , if any of its internal nodes contributes less than in loss, even though , it cannot be the optimal tree and none of its child tree could be the optimal tree. Thus, after evaluating tree , we can prune it.

Theorem B.7.

(Lower bound on incremental progress) Let be any optimal tree with objective , i.e., . Let have leaves and . Consider tree derived from by deleting a pair of leaves and with corresponding labels and and adding their parent leaf and its label . Define as the incremental objective of splitting to get : In this case, provides a lower bound s.t. .

Proof.

Let be the tree derived from by deleting a pair of leaves and , and adding their parent leaf . Then,

| (16) |

Since , then . ∎

In the implementation, we apply both Theorem B.6 and Theorem B.7. If Theorem B.6 is not satisfied, even though , it cannot be an optimal tree and none of its child trees could be an optimal tree. In this case, can be pruned, as we showed before. However, if Theorem B.6 is satisfied, we check Theorem B.7. If Theorem B.7 is not satisfied, then we would need to further split at least one of the two child leaves–either of the new leaves or –in order to obtain a potentially optimal tree.

B.4 Permutation Bound

Theorem B.8.

(Leaf Permutation bound) Let be any permutation of . Let and be trees with leaves and respectively, i.e., the leaves in correspond to a permutation of the leaves in d. Then the objective lower bounds of and are the same and their child trees correspond to permutations of each other.

Proof.

This bound adapts directly from OSDT (Hu et al., 2019), where the proof can be found. ∎

Therefore, if two trees have the same leaves, up to a permutation, according to Theorem B.8, one of them can be pruned. This bound is capable of reducing the search space by all future symmetries of trees we have already seen.

B.5 Equivalent Points Bound

As we know, for a tree , the objective of this tree (and that of its children) is minimized when there are no errors in the split leaves: and . In that case, the risk is equal to . However, if multiple observations captured by a leaf in have the same features but different labels, then no tree, including those that extend , can correctly classify all of these observations, that is and cannot be zero. In this case, we can apply the equivalent points bound to give a tighter lower bound on the objective.

Let be a set of leaves. Capture is an indicator function that equals 1 if falls into one of the leaves in , and 0 otherwise, in which case we say that . We define a set of samples to be equivalent if they have exactly the same feature values. Let be a set of equivalent points and let be the minority class label that minimizes the loss among points in . Note that a dataset consists of multiple sets of equivalent points. Let enumerate these sets.

Theorem B.9.

(Equivalent points bound) Let be a tree such that for and for . For any tree ,

| (17) |

| (18) |

Proof.

Since , where we have both for , which are the fixed leaves and also for . Note that for , .

Let which are the leaves in that are not in . Then , where and are false positives and false negatives in but not and and are false positives and false negatives in . For tree , its leaves in are those indexed from to . Thus, the sum over leaves of from to includes leaves from and leaves from .

| (19) |

For , the samples in are the same ones captured by either or , that is . Then

| (20) |

Similarly, . Therefore,

| (21) |

∎

B.6 Similar Support Bound

Given two trees that are exactly the same except for one internal node split by different features and , we can use the similar support bound for pruning.

Theorem B.10.

(Similar support bound) Define and to be two trees that are exactly the same except for one internal node split by different features. Let and be the features used to split that node in and respectively. Let be the left and right sub-trees under the node in and let be the left and right sub-trees under the node in . Let be the observations captured by only one of or , i.e.,

| (22) |

Let and be the false positives and false negatives of samples except . The difference between the two trees’ objectives is bounded as follows:

| (23) |

| (24) |

Then we have

| (25) |

Proof.

The difference between the objectives of and is largest when one of them correctly classifies all the data in but the other misclassifies all of them. If classifies all the data corresponding to correctly while misclassifies them,

| (26) |

We can get in the same way. Therefore, .

Appendix C Objectives and Their Lower Bounds for Rank Statistics

In this appendix, we provide proofs for Theorem 2.1 and Theorem 2.2, and adapt the Incremental Progress Bound to Determine Splitting and the Equivalent Points Bound for the objective . The Upper Bound on the Number of Leaves, Parent-Specific Upper Bound on the Number of Leaves, Lower Bound of Incremental Progress, and Permutation Bound are the same as the bounds in Appendix B. We omit these duplicated proofs here. At the end of this appendix, we define the objective and how we implement the derived bounds for this objective. As a reminder, we use notation to represent tree .

Lemma C.1.

Let be a tree. The AUC convex hull does not decrease when an impure leaf is split.

Proof.

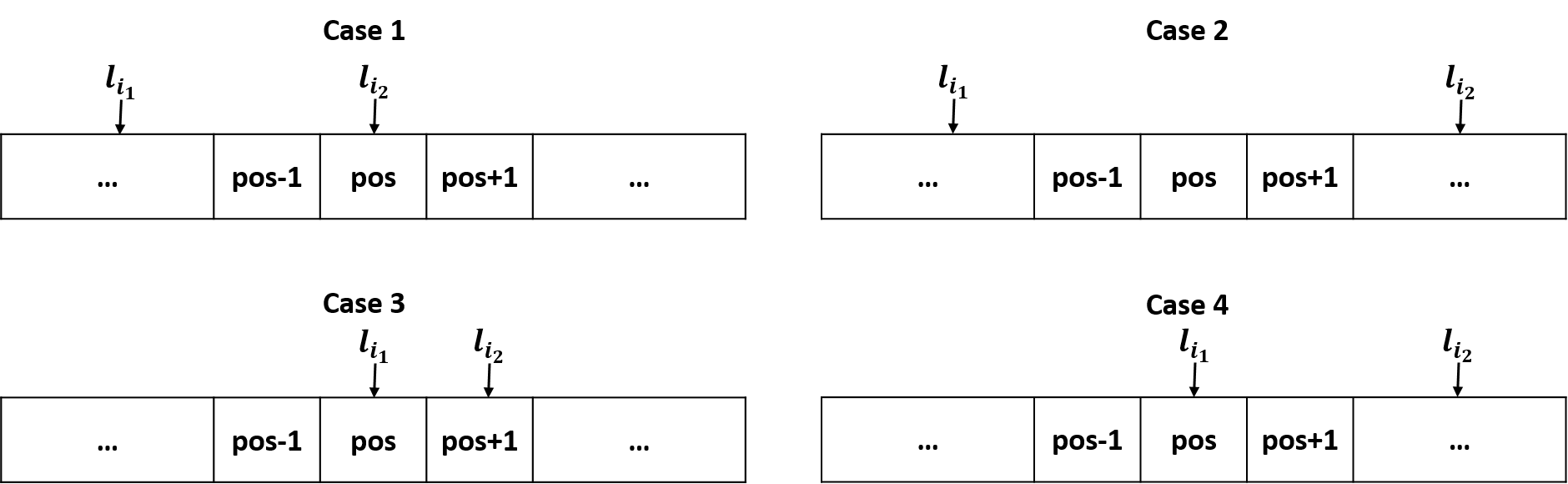

Let be the impure leaf that we intend to split, where . Let be the positive samples in and negative samples. Suppose is ranked in position “pos.” If the leaf is split once, it will generate two leaves and such that without loss of generality. Let be the tree that consists of the leaf set . If , then the rank order of leaves (according to the ’s) will not change, so will be unchanged after the split. Otherwise (if the rank order of leaves changes when introducing a child) we can reorder the leaves, leading to the following four cases. For the new leaf set , either:

-

1.

The rank of is smaller than and the rank of equals (requires and );

-

2.

The rank of is smaller than and the rank of is larger than (requires and );

-

3.

The rank of is equal to and the rank of is equal to (requires and );

-

4.

The rank of is and the rank of is larger than (requires and ).

Figure 7 shows four cases of the positions of and .

Let us go through these cases in more detail.

For the new leaf set after splitting , namely , we have that:

-

1.

has rank smaller than (which requires ) and has rank (which requires ).

Let be a collection of leaves ranked before and let be a collection of leaves ranked after but before . In this case, recalling Equation (2), a change in the after splitting on leaf is due only to a subset of leaves, namely . Then we can compute the change in the as follows:

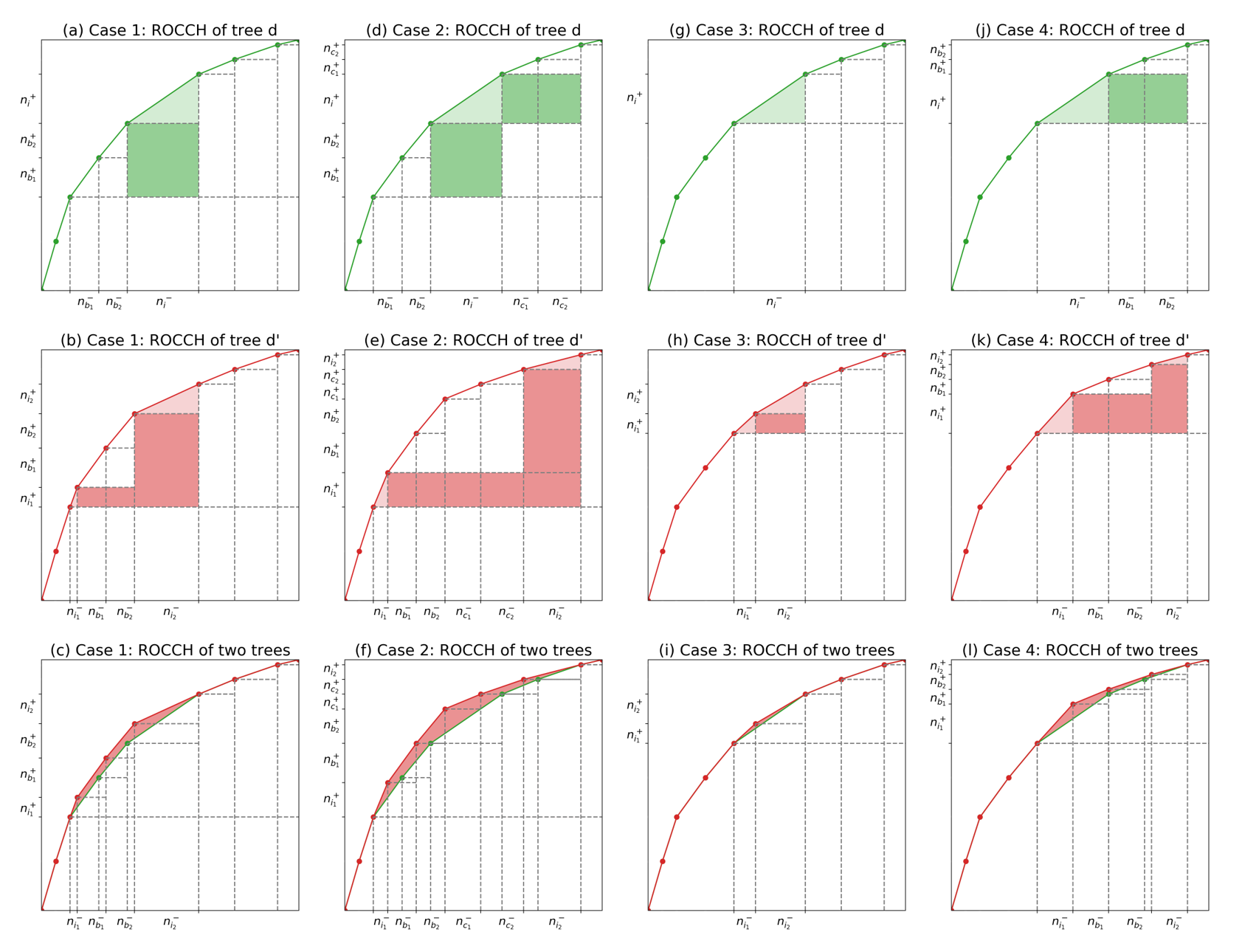

(28) To derive the expression for , we first sum shaded areas of rectangles and triangles under the ROC curves’ convex hull for both tree and its child tree , and then calculate the difference between the two shaded areas, as indicated in Figure 8 (a-c). This figure shows where each of the terms arises within the : terms and come from the area of rectangles colored in dark pink in Figure 8 (b). Terms and handle the top triangles colored in light pink. Term represents the rectangles colored in dark green in Figure 8 (a) and term deals with the triangles colored in light green. Subtracting green shaded areas from red shaded areas, we get , which is represented by the (remaining) pink area in Figure 8 (c).

Simplifying Equation (28), we get

(29) Recall that and . Then, simplifying,

(30) Since , . Then we can get . Hence . Similarly, because , . Then . Therefore, .

-

2.

has a ranking smaller than (which requires ) and has a ranking larger than (which requires ).

Let be a collection of leaves that ranked before and be a collection of leaves that ranked after but before , and be a collection of leaves that ranked after but before the rank of . In this case, the change is caused by . Then we can compute the change in the as follows:

(31) Similar to the derivation proposed in case 1, we first sum shaded areas of rectangles and triangles under the ROC curves’ convex hull for both tree and its child tree and then calculate the difference between two shaded areas as indicated in Figure 8 (d-f). These three subfigures show where each of the terms arises within the : terms , , and come from the area of rectangles colored in dark pink in Figure 8 (e). Terms and handle the top triangles colored in light pink. Terms and represent the rectangles colored in dark green in Figure 8 (d) and term deals with the triangles colored in light green. Subtracting green shaded areas from red shaded areas, we can get , which is represented by the light red area in Figure 8 (f).

Recall that and . Then, simplifying Equation (31), we get

(32) Since , , . Then we get . Thus, . Similarly, since , . Thus, . Moreover, because , . Hence, .

-

3.

has a ranking same as (which requires ) and has a ranking (which requires ).

In this case, the change of is caused by and . Then we compute the change in the as follows:

(33) We derive the expression in the similar way as case 1 and case 2. Term comes from the area of rectangle colored in dark pink in Figure 8 (h) and terms and handle the top triangles colored in light pink. Term deals with the top triangle colored in light green in Figure 8 (g). Subtracting green shaded areas from pink shaded areas, we get , which is represented by the (remaining) pink area in Figure 8 (i).

-

4.

has a ranking same as (which requires ) and has a ranking larger than (which requires ).

Let be a collection of leaves that ranked before and be a collection of leaves that ranked after but before . In this case the change of is caused by . Then we can compute the change as follows:

(35) The Figure 8 (j-l) show where each of the terms arises within the : terms and come from the area of rectangles colored in dark pink in Figure 8 (k) and terms and handle triangles colored in light pink. Term represents the rectangle colored in dark green in Figure 8 (j) and term deals with the triangle colored in light green. Subtracting green shaded areas from pink shaded areas, we get , which is represented by the (remaining) pink area in Figure 8 (l).

Therefore, once an impure leaf is split, the doesn’t decrease. If the split is leading to the change of the rank order of leaves, then increases. ∎

C.1 Proof of Theorem 2.1

Proof.

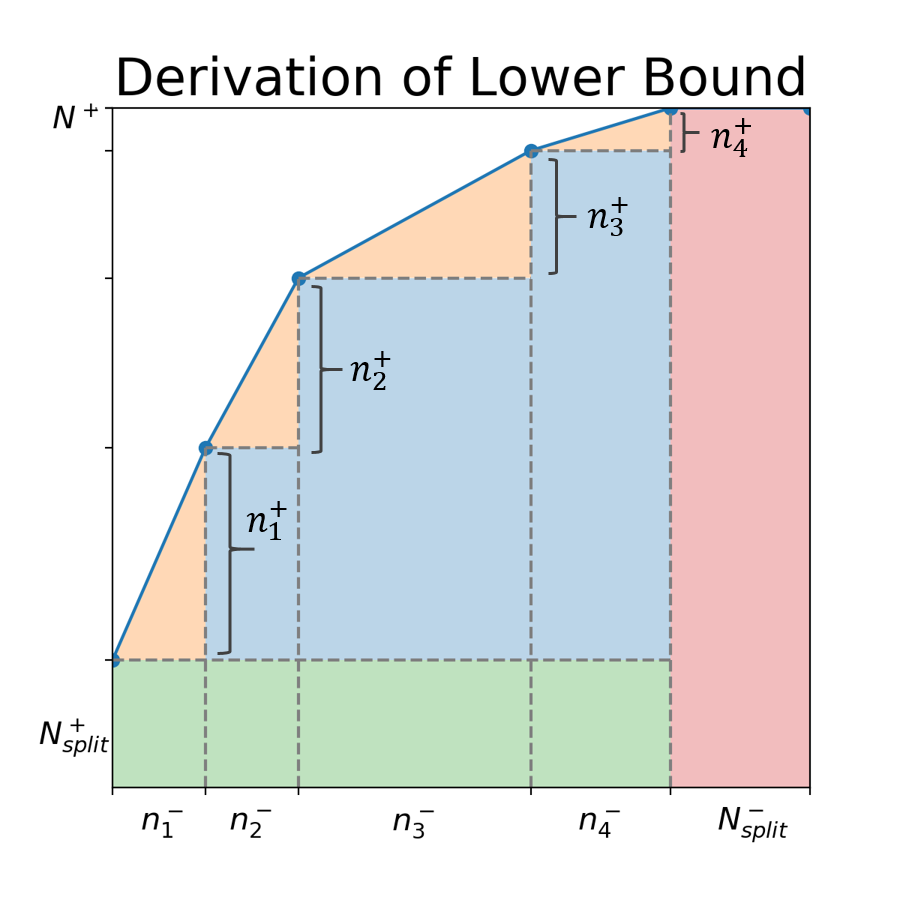

Let tree and leaves of tree are mutually exclusive. According to Lemma C.1, for leaves that can be further split, we can do splits to increase the . In the best possible hypothetical case, all new generated leaves are pure (contain only positive or negative samples). In this case, is maximized for . In this case, we will show that as defined by Equation (4). Then .

To derive the expression for , we sum areas of rectangles and triangles under the ROC curve’s convex hull. Figure 9 shows where each of the terms arises within this sum: the first term in the sum, which is , comes from the area of the lower rectangle of the ROC curve’s convex hull, colored in green. This rectangle arises from the block of positives at the top of the ranked list (within the split leaves, whose hypothetical predictions are 1). The term handles the areas of the growing rectangles, colored in blue in Figure 9. The areas of the triangles comprising the top of the ROCCH account for the third term . The final term comes from the rectangle on the right, colored red, stemming from the split observations within a hypothetical purely negative leaf.

∎

C.2 Proof of Theorem 2.2

C.3 Incremental Progress Bound to Determine Splitting for Rank Statistics

Theorem C.2.

(Incremental progress bound to determine splitting for rank statistics) Let be any optimal tree with objective , i.e., . Consider tree derived from by deleting a pair of leaves and and adding their parent leaf , . Let be the number of positive samples ( be the number of negative samples) in leaf . Calculate as in Equation (2). Define as the tree after dropping leaf , adding two hypothetical pure leaves (i.e., one has all positives and the other has all negatives), and reordering the remaining leaves based on the fraction of positives. Then, we can calculate the loss of the tree as

| (37) |

Let . Then must be at least .

Proof.

By the way is defined (using the same counting argument we used in the proof of Theorem 2.1), it is a lower bound for . These two quantities are equal when the split leaves are all pure. So, we have . Since , we can get , that is (and remember that is of size whereas is of size ), . Since is optimal with respect to , then , thus . ∎

Similar to the Incremental Progress Bound to Determine Splitting for arbitrary monotonic losses, for a tree , if any of its internal node contributes less than in loss, it is not the optimal tree. Thus, after evaluating tree , we can prune it.

C.4 Equivalent points bound for rank statistics

Similar to the equivalent points bound for arbitrary monotonic losses, for a tree , the objective of this tree and its children is minimized when leaves that can be further split to generate pure leaves. In the case when it is possible to split the data into pure leaves, the risk could be equal to . However, if multiple observations captured by a leaf in have the same features but different labels, then no tree, including those that extend , can correctly classify all of these observations; that is, leaves in can not generate pure leaves. In this case, we can leverage these equivalent points to give a tighter lower bound for the objective. We use the same notation for capture and set of equivalent points as in Appendix B, and minority class label is simply the label with fewer samples.

Let be a tree. Data in leaves from can be separated into equivalence classes. For , let , that is, the number of samples captured by belonging to equivalence set , and let be the number of minority-labeled samples captured by in equivalence point set . Then we define as the classification rule we would make on each equivalence class separately (if we were permitted):

Let us combine this with to get a bound. We order the combination of leaves in and equivalence classes by the fraction of positives in each, Sort from highest to lowest. Let us re-index these sorted elements by index . Denote as the number of positive samples in either the leaf or equivalence class corresponding to . (Define to be the number of negative samples analogously). We define our new, tighter, lower bound as:

| (38) |

Theorem C.3.

(Equivalent points bound for rank statistics) For a tree , Let tree be any child tree such that its fixed leaves contain and . Then , where is defined in Equation (38).

C.5 Partial area under the ROCCH

We discuss the partial area under the ROC convex hull in this section. The ROCCH for a decision tree is defined in Section 2.1, where leaves are rank-ordered by the fraction of positives in the leaves. Given a threshold , the partial area under the ROCCH () looks at only the leftmost part of the ROCCH, that is focusing on the top ranked leaves. This measure is important for applications such as information retrieval and maintenance (see, e.g., Rudin & Wang, 2018). In our implementation, all bounds derived for the objective can be adapted directly for , where all terms are calculated only for false positive rates smaller or equal to .

In our code, we implement all of the rank statistics bounds, with one exception for the partial AUCCH – the equivalent points bound. We do not implement the equivalent points bound for partial AUCCH since the statistic is heavily impacted by the leaves with high fraction of positives, which means that the leaves being repeatedly calculated for the objective tend not to be impure, and thus the equivalence points bound is less effective.

Appendix D Optimizing F-score with Decision Trees

For a labeled tree , the F-score loss is defined as

| (39) |

For objectives like accuracy, balanced accuracy and weighted accuracy, the loss of a tree is the sum of loss in each leaf. For F-score loss, however, and appear in both numerator and denominator, thus the loss no longer can be calculated using a sum over the leaves.

Lemma D.1.

The label of a single leaf depends on the labels of other leaves when optimizing F-score loss.

Proof.

Let be the leaves of tree . Suppose leaves are labeled. Let and be the number of false positives and false negatives of these leaves, respectively. Let and , and by these definitions, we will always have . Let be the number of positive samples in leaf and be the number of negative samples. The leaf’s predicted label can be either positive or negative. The loss of the tree depends on this predicted label as follows:

| (40) | |||||

| (41) |

Calculating loss (41) minus loss (40):

| (42) |

Denote as the numerator of (42), that is

Then we can get

| (43) | |||||

| (44) |

The value of depends on , , and . Hence, in order to minimize the loss, the predicted label of leaf is 0 if and 1 otherwise. Therefore, the predicted label of a single leaf depends on and , which depend on the labels of the other samples, as well as the positive and negative samples captured by that leaf. ∎

Theorem D.2.

(Optimizing F-score Poses a Unusual Challenge) Let be the leaves of tree and let be the number of positive samples in the dataset. Let and be two predicted labelings for the first leaves. Leaf has a fixed predicted label. Suppose the loss for the F-score (Equation (39)) of the first leaves based on labeling method is smaller than the loss based on labeling method (where in both cases, leaf has the same predicted label). It is not guaranteed that the loss of the tree based on the first labeling is always smaller than the loss based on the second labeling .

Proof.

Let and be the number of false positives and number of false negatives for the first leaves from the labeling method and similarly define and for labeling method . Denote and . Similarly, denote and . As we know from the assumptions of the theorem, .

Denote and be the number of false positives and number of false negatives of the last leaf .

Let and be the loss of the tree based on two different predicted labelings of the leaves.

Suppose the predicted label of leaf is 1. (An analogous result holds when the predicted label of leaf is 0.) Then and . Let be the numerator of .

| (45) | |||||

Since , , that is, the first two terms together are nonnegative. Meanwhile, and . Thus, could be negative or positive. Therefore, even though the labeling method leads to smaller loss for the first leaves and the label of the last leaf depends on the label of previous leaves, it is not guaranteed that the loss of the tree is smaller than that based on . It is easy to construct examples of , , , , and where the result is either positive or negative, as desired. ∎

Appendix E Dynamic Programming Formulation

Note that this section describes standard dynamic programming, where possible splits describe subproblems. The more interesting aspects are the bounds and how they interact with the dynamic programming.

We will work only with the weighted misclassification loss for the following theorem, so that the loss is additive over the data:

We denote as a data set of features and binary labels containing a total of samples and features.

Initial Problem: We define a tree optimization problem as a minimization of the regularized risk over the domain , where is a tree consisting of a single split leaf

| (46) |

Since all trees are descendants of a tree that is a single split leaf, this setup applies to tree optimization of any arbitrary data set , . We can rewrite the optimization problem as simply:

| (47) |

We partition the domain into cases: One Leaf Case and Tree Cases. We solve each case independently, then optimize over the solutions of each case:

The Leaf Case forms a base case in a recursion, while each Tree Case is a recursive case that further decomposes into two instances of tree optimization of the form described in (46).

Leaf Case: In this case, is a tree consisting of a single fixed leaf. This tree’s only prediction is a choice of two possible classes .

| (48) |

where a tie would be broken randomly.

Tree Case: For every possible in the set feature indices we designate an Tree Case and an as the optimal descendent of a tree . We define as a tree consisting of a root split on feature and two resulting split leaves and so that:

| (49) |

Instead of directly solving (49), we further decompose this into two smaller tree optimization problems that match the format of (46). Since we are working with the weighted misclassification loss, we can optimize subtrees extending from from and independently. We define data within the support set of as , . We define data within the support set of as , . For each , we define an optimization over the extensions of the left split leaf as:

| (50) |

By symmetry, we define an optimization over the extensions of the right split leaf :

| (51) |

is the optimal subtree that classifies and is the optimal subtree that classifies . Together, with a root node splitting on the feature, combines with to form . Thus, we can solve (50) and (51) to get the solution of (49).

In (46) we defined a decomposition of an optimization problem over the domain , where is a tree consisting of a single split leaf. Both expressions (50) and (51) are also optimizations over the domain of children of a tree consisting of a single split leaf. Recall that the descendants of any tree consisting of only a single split leaf covers the space of all possible trees, therefore the trees are optimized over an unconstrained domain. We can thus rewrite (50) as:

| (52) |

Symmetrically we can also rewrite (51) as:

| (53) |

Observe that (52) and (53) are simply tree optimization problems over a specific set of data (in this case and ). Hence, these tree optimizations form a recursion, and each can be solved as though they were (47).

Termination: To ensure this recursion terminates, we consider only splits where and are strict subsets of . This ensures that the support strictly decreases until a minimum support is reached, which prunes all of leaving only the leaf case described in (48).

Identifying Reusable Work: As we perform this decomposition, we identify each problem using its data set , by storing a bit vector to indicate it as a subset of the initial data set. At each recursive step, we check to see if a problem has already been visited by looking for an existing copy of this bit vector.

Figure 10 shows a graphical representation of the algorithm. Note that we use the following shortened notations in the figure:

| (54) |

| (55) |

| (56) |

Equation (54) denotes a data set filtered by the constraint that samples must respond positive to feature . Equation (55) denotes a data set filtered by the constraint that samples must respond negative to feature . Equation (56) denotes a data set filtered by the constraint that samples must respond positive to both feature and feature .

anchors/.style=anchor=#1,child anchor=#1,parent anchor=#1, /tikz/every node/.append style=font=, for tree= s sep=5mm,l=12mm, if n=0anchors=east if n=1anchors=eastanchors=west, content format=, , anchors=south, outer sep=2pt, nodot/.style=content format=,draw=none, dot/.style=tikz+=\draw[#1](.anchor)circle[radius=2pt];, if content=dot=fill [ (x,y),dot=fill [ Leaf,edge=dashed [1,edge=dashed] [0,edge=dashed] ] [ Tree_1 [ (x,y)^-1,dot=fill [ Leaf Case,edge=dashed [1,edge=dashed] [0,edge=dashed] ] [ Tree_2 [ (x,y)^-1,-2,dot=fill [ Leaf [1,edge=dashed] [0] ] ] [ (x,y)^-1,2,dot=fill [ Leaf [1] [0,edge=dashed] ] ] ] ] [ (x,y)^1,dot=fill [ Leaf [1,edge=dashed] [0] ] ] ] [ Tree_2,edge=dashed [ (x,y)^-2,dot=fill,edge=dashed […,edge=dashed] […,edge=dashed] ] [ (x,y)^2,dot=fill,edge=dashed […,edge=dashed] […,edge=dashed] ] ] ]

Appendix F Incremental Similar Support Bound Proof

We will work only with weighted misclassification loss for the following theorem, so that the loss is additive over the data:

Define the maximum possible weighted loss:

The following bound is our important incremental similar support bound, which we leverage in order to effectively remove many similar trees from the search region by looking at only one of them.

Theorem F.1.

(Incremental Similar Support Bound) Consider two trees and that differ only by their root node (hence they share the same and values). Further, the root nodes between the two trees are similar enough that the support going to the left and right branches differ by at most fraction of the observations. (That is, there are observations that are captured either by the left branch of and right branch of or vice versa.) Define as the maximum of the support within and :

For any child tree grown from (grown from the nodes in , that would not be excluded by the hierarchical objective lower bound) and for any child tree grown from (grown from the nodes in , that would not be excluded by the hierarchical objective lower bound), we have:

This theorem tells us that any two child trees of and that we will ever generate during the algorithm will have similar objective values. The similarity depends on , which is how many points are adjusted by changing the top split, and the other term involving is determined by how much of the tree is fixed. If most of the tree is fixed, then there can be little change in loss among the children of either or , leading to a tighter bound. In standard classification tasks, the value of is usually 1, corresponding to a classification error for an observation.

Proof.

We will proceed in three steps. The first step is to show that

The second step is to show:

for all feasible children of . The same bound will hold for and any of its children . The third step is to show

which requires different logic than the proof of Step 2. Together, Steps 2 and 3 give

From here, we use the triangle inequality and the bounds from the three steps to obtain the final bound:

which is the statement of the theorem. Let us now go through the three steps.

First step: Define “move” as the set of indices of the observations that either go down the left branch of the root of and the right of , or that go down the right of and the left of . The remaining data will be denoted “.” These remaining data points will be classified the same way by both and . The expression above follows from the additive form of the objective :

and since since this just considers overlapping leaves, we have:

(For the last inequality, the maximum is attained when one of and is zero and the other attains its maximum possible value.)

Second step: Recall that is a child of so that contains . Let us denote the leaves in that are not in by . Then,

Adding to both sides,

since the terms we removed were all nonnegative. Now,

Third step: Here we will use the hierarchical objective lower bound. We start by noting that since we have seen , we have calculated its objective , and it must be as good or worse than than the current best value that we have seen so far (or else it would have replaced the current best). So . The hierarchical objective lower bound (Theorem B.1) would be violated if the following holds. This expression states that is worse than (which is worse than the current best), which means we would have already excluded from consideration:

This would be a contradiction. Thus, the converse holds:

Thus,

Now to create an upper bound for as times the support of . Since is a child of , its support on the split leaves is less than or equal to that of , . Thus, . Hence, we have the result for the final step of the proof, namely:

∎

Appendix G Subset Bound Proof

We will work with the loss that is additive over the data for the following theorem. The following bound is our subset bound, which we leverage in order to effectively remove the thresholds introduced by the continuous variables, thus pruning the search space.

Theorem G.1.

(Subset Bound). Define and to be two trees with same root node. Let and be the features used to split the root node. Let , be the left and right sub-trees under the root node split by in and let and be the samples captured by and respectively. Similarly, let , be the left and right sub-trees under the root node split by in and let and be the samples captured by and respectively. Suppose , are the optimal trees for and respectively, and , are the optimal trees for corresponding and . If and , then .