Convex optimization based on global lower second-order models

Nikita Doikov

Catholic University of Louvain,

Louvain-la-Neuve, Belgium

Nikita.Doikov@uclouvain.be

&Yurii Nesterov

Catholic University of Louvain,

Louvain-la-Neuve, Belgium

Yurii.Nesterov@uclouvain.be

&

Institute of Information and Communication Technologies,

Electronics and Applied Mathematics (ICTEAM)Center for Operations Research and Econometrics (CORE)

Abstract

In this paper, we present new second-order algorithms for composite convex optimization,

called Contracting-domain Newton methods.

These algorithms are affine-invariant and based on global

second-order lower approximation for the smooth component of the objective.

Our approach has an interpretation both as

a second-order generalization of the conditional gradient method,

or as a variant of trust-region scheme.

Under the assumption, that the problem domain is bounded, we prove

global rate of convergence in functional residual,

where is the iteration counter,

minimizing convex functions with Lipschitz continuous Hessian.

This significantly improves the previously known bound for this type of algorithms.

Additionally, we propose a stochastic extension of our method,

and present computational results

for solving empirical risk minimization problem.

1 Introduction

Classical Newton method is one of the most popular

optimization schemes for solving ill-conditioned problems.

The method has very fast quadratic convergence, provided

that the starting point is sufficiently close to the

optimum bennett1916newton ; kantorovich1948functional ; nesterov2018lectures .

However, the questions related to its global behaviour for

a wide class of functions are still open, being in the

area of active research.

The significant progress in this direction was made

after nesterov2006cubic , where Cubic regularization

of Newton method with its global complexity bounds were

justified. The main idea of nesterov2006cubic is to

use a global upper approximation model of the

objective, which is the second-order Taylor’s polynomial

augmented by a cubic term. The next point in the iteration

process is defined as the minimizer of this model. Cubic

Newton attains global convergence for convex functions

with Lipschitz continuous Hessian. The rate of convergence

in functional residual is of the order (here

and later on, is the iteration counter). This is much

faster than the classical rate of the Gradient

Method nesterov2018lectures . Later on,

accelerated nesterov2008accelerating ,

adaptive cartis2011adaptive1 ; cartis2011adaptive2

and

universal grapiglia2017regularized ; doikov2019minimizing ; grapiglia2019accelerated

second-order schemes based on cubic regularization were

developed. Randomized versions of Cubic Newton, suitable

for solving high-dimensional problems were proposed

in doikov2018randomized ; hanzely2020stochastic .

Another line of results on global convergence of Newton

method is mainly related to the framework of

self-concordant

functions nesterov1994interior ; nesterov2018lectures .

This class is affine-invariant. From the global

perspective, it provides us with an upper

second-order approximation of the objective, which

naturally leads to the Damped Newton Method. Several new

results are related to its analysis for generalized

self-concordant

functions bach2010self ; sun2019generalized , and the

notion of Hessian stability karimireddy2018global .

However, for more refined problem classes, we can often

obtain much better complexity estimates, by using the

cubic regularization

technique dvurechensky2018global .

In this paper, we investigate a different approach, which

is motivated by a new global second-order lower

model of the objective function, introduced in

Section 3.

We incorporate this model into a new second-order

optimization algorithm, called Contracting-Domain Newton

Method (Section 4). At every

iteration, it minimizes a lower approximation of the

smooth component of the objective, augmented by a

composite term. The next point is defined as a convex

combination of the minimizer, and the previous point. By

its nature, it is similar to the scheme of Conditional

Gradient Method (or, Frank-Wolfe

algorithm, frank1956algorithm ; nesterov2018complexity ).

Under assumption of boundedness of the problem domain, for

convex functions with Hölder continuous Hessian of

degree , we establish its global rate of convergence in functional residual.

In the case , for the class of convex function

with Lipschitz continuous Hessian, this gives

rate of convergence. As compared with Cubic Newton, the

new method is affine-invariant and universal, since it

does not depend on the norms and parameters of the problem

class. When the composite component is strongly convex

(with respect to arbitrary norm), we show rate for a universal scheme. If the parameters of

problem class are known, we can prove a global linear

convergence.

We also provide different trust-region

interpretations for our algorithm.

In Section 5, we present aggregated models,

which accumulate second-order information into quadratic

Estimating Functions nesterov2018lectures . This

leads to another optimization process, called Aggregating

Newton Method, with the global convergence of the same

order as for general convex case. The

latter method can be seen as a second-order counterpart of

the dual averaging gradient

schemes nesterov2009primal ; nesterov2013gradient .

In Section 6, we consider the problem of

finite-sum minimization. We propose stochastic extensions

of our method. During the iterations of the basic variant,

we need to increase the batch size for randomized

estimates of gradients and Hessians up to the order

and respectively. Using the

variance reduction

technique for the gradients,

we reduce the batch size up to the

level for both estimates. At the same time, the global convergence

rate of the resulting methods

is of the order ,

as for general convex functions with Lipschitz continuous Hessian.

Section 7 contains numerical

experiments. Section 8 contains some final remarks.

All necessary proofs are provided in

Appendix.

2 Problem formulation and notations

Our goal is to solve the following composite convex

minimization problem:

(1)

where is a

simple proper closed convex function, and

function is convex and twice continuously

differentiable at every point . Let us

fix an arbitrary (possibly non-Euclidean) norm on . We denote by the corresponding diameter

of :

(2)

Our main assumption on problem (1) is that

is bounded:

(3)

The most important example of is -indicator of a simple compact convex set . In particular, for a ball in

-norm with , this is

(4)

From the machine learning perspective, is usually considered as a regularization parameter in this setting. We denote by the standard scalar product of two vectors,

:

For function , we denote its gradient by , and its Hessian matrix by . Having fixed the norm for

primal variables , the dual norm

can be defined in the standard way:

The dual norm is necessary for measuring the size of

gradients. For a matrix ,

we use the corresponding induced operator norm, defined as

3 Second-order lower model of objective function

To characterize the complexity of

problem (1), we need to introduce some

assumptions on the growth of derivatives. Let us assume

that the Hessian of is Hölder continuous of degree

on :

(5)

The actual parameters of this problem class may be

unknown. However, we assume that for some inequality (5) is satisfied

with corresponding constant .

The direct consequence of (5) is the

following global bounds for Taylor’s approximation,

for all

(6)

(7)

Recall, that in addition to (5), we assume that is convex:

(8)

Employing both smoothness and convexity, we are able to enhance this global lower

bound, as follows.

{framedlemma}

For all and , it holds

(9)

Note that the right-hand side of (9) is

concave in , and for we obtain the

standard first-order lower bound. The maximization

of (9) over gives

(10)

with

Thus, (10) is always tighter

than (8), employing additional global

second-order information. The relationship between them

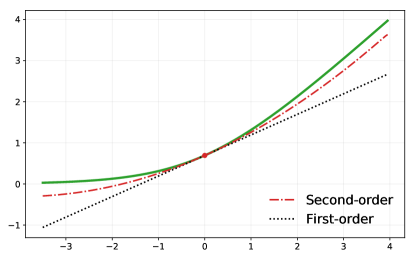

is shown on Figure 1. Hence, it seems

natural to incorporate the second-order lower bounds into

optimization schemes.

Figure 1: Global lower bounds for logistic regression loss, .

4 Contracting-Domain Newton Methods

Let us introduce a general scheme of

Contracting-Domain Newton Method, which is based

on global second-order lower bounds. Note, that the right

hand side of (10) is nonconvex in .

Hence, it can hardly be used directly in a computational

algorithm. To tackle this issue, we use a sequence of

contracting coefficients . Each

coefficient can be seen as an

appropriate substitute of

in (10). Then, we minimize the

corresponding global lower bound augmented by the

composite component . The next point is taken

as a convex combination of the minimizer and the current

point. Let us present this method formally, as

Algorithm 1.

Algorithm 1 Contracting-Domain Newton Method, I

1:Choose .

2:.

3:Pick up .

4:Compute

5:Set .

There is a clear connection of this method with

Frank-Wolfe algorithm, frank1956algorithm . Indeed,

instead of the standard first-order

approximation (8), we use the lower global

quadratic model. Thus, as compared with the gradient

methods, every iteration of Algorithm 1

is more expensive. However, this is a standard situation

with the second-order schemes (see the below discussion on

the iteration complexity). At the same time, our method is

affine-invariant, since it does not depend on the

norms.

It is clear, that for we obtain

iterations of the classical Newton method. Its local

quadratic convergence for composite optimization problems

was established in lee2014proximal . However, for

the global convergence, we need to adjust the contracting

coefficients accordingly. To state the global convergence

result, let us introduce the following linear

Estimating Functions

(see nesterov2018lectures ):

(11)

for the sequence of test points and positive

scaling coefficients . We relate them with contracting coefficients,

as follows

(12)

{framedtheorem}

Let , and consequently, .

Then for the sequence generated by

Algorithm 1, we have

(13)

For the case (convex functions with Lipschitz

continuous Hessian), estimate (13) gives

the convergence rate of the order .

This is the same rate, as we can achieve on this

functional class by Cubic Regularization of Newton

Method nesterov2006cubic . In accordance

to (13), in order to obtain

-accuracy in functional residual, , it is enough to perform

(14)

iterations of Algorithm 1.

In grapiglia2017regularized , there were proposed

first universal second-order methods (which do

not depend on parameters and of the

problem class), having complexity guarantees of the same

order (14). These methods are based on

Cubic regularization and an adaptive search for estimating

the regularization parameter at every iteration. It is

important that Algorithm 1 is both

universal and affine-invariant. Additionally, convergence

result (13) provides us with a sequence

of computable accuracy

certificates, which can be used as a stopping criterion

of the method.

Now, let us assume that the composite component is strongly convex

with parameter . Thus, for all

and , it holds

(15)

In this situation, we are able to improve convergence

estimate (13), as follows.

{framedtheorem}

Let ,

and consequently, . Then for the

sequence generated by

Algorithm 1, we have

(16)

Moreover, if the second-order condition number

(17)

is known, then, defining , , and , , we obtain

the global linear rate of convergence

(18)

According to the estimate (18), in

order to get -accuracy in function value, it

is enough to perform

iterations of the method. Hence, condition number

plays the role of the main complexity

factor. This rate corresponds to that one of Cubically

Regularized Newton Method

(see doikov2019local ; doikov2019minimizing ).

At the same time, there exists a second variant of

Contracting-Domain Newton Method, where the next point is

defined by minimization of the full second-order model for

the smooth component augmented by the composite term over

the contracted domain (this explains the names of

our methods).

Algorithm 2 Contracting-Domain Newton Method, II

1:Choose .

2:.

3:Pick up .

4:Denote

5:Compute

Note, that Algorithm 1 admits similar

representation as well. 111Indeed, it is enough to

take . Both methods produce the same sequences of

points when is -indicator of

a convex set. Otherwise, they are different.

Using the same contraction technique,

it was shown in nesterov2018complexity

that the classical Frank-Wolfe algorithm can be extended

onto the case of the composite optimization problems.

Additionally, the second-order

Contracting Trust-Region method was proposed, which has

the same form as Algorithm 2.

However,

its convergence rate was established only at the level

. Here, we improve its rate as follows.

{framedtheorem} Let and

. Then for the sequence generated by

Algorithm 2, we have

(19)

This result is very similar to

Theorem 1. However, the first algorithm

can be accelerated on the class of strongly convex

functions (see

Theorem 4). Thus, it

seems that it is more preferable.

Finally, let us consider an example, when the composite

component is an -ball, as

in (4). Then, iterations of the method can be

represented as

(20)

In this form, it looks as a variant of Trust-Region

scheme. To solve the subproblem

in (20), we can use Interior Point

Methods (e.g. Chapter 5 in nesterov2018lectures ).

See also conn2000trust , for techniques, developed

for Trust-Region schemes. Usually, complexity of this step

can be estimated as arithmetic operations, which

comes from the cost of computing a suitable factorization

for the Hessian matrix. Alternatively, Hessian-free

gradient methods can be applied, for computing an inexact

step (see carmon2020first ; carderera2020second ).

5 Aggregated second-order models

In this section, we propose more advanced second-order

models, based on global lower

bound (9). Using the same notation as

before, consider a sequence of test points and sequences of coefficients

, ,

satisfying the relations (12). Then, we

can introduce the following Quadratic Estimating

Functions (compare with

definition (11)):

By (9), we have the main property of

Estimating Functions being satisfied. Namely, for all

(21)

Therefore, if we would be able to guarantee for our test

points the relation

(22)

then we could immediately obtain the global convergence in

function value. Fortunately, relation (22)

can be achieved by simple iterations.

Algorithm 3 Aggregating Newton Method

1:Choose . Set , .

2:.

3:Pick up . Set

and .

4:Update Estimating Function

5:

6:Compute

7:Set .

Clearly, the most complicated part of this process is

Step 3, which is computation of the minimum of Estimating

Function. However, the complexity of this step remains the

same, as that one for Contracting-Domain Newton Method. We

obtain the following convergence result. {framedtheorem} For the sequence generated by Algorithm 3,

relation (22) is satisfied. Consequently, for

the choice , we obtain

(23)

Now, for the accuracy certificate we have new expression

.

The value of is available within the method directly.

However, in order to compute in practice,

some estimate for is required.

Note, that for the given choice of coefficients ,

we have and .

Therefore, new information enters into the model

with increasing weights, which seems to be natural.

6 Stochastic finite-sum minimization

In this section, we consider the case when the smooth part of the objective (1)

is represented as a sum of

convex twice-differentiable components,

(24)

This setting appears in many machine learning

applications, such as empirical risk

minimization. Often, the number is very big. Thus, it

becomes expensive to evaluate the whole gradient or the

Hessian at every iteration. Hence, stochastic or

incremental methods are the methods of choice in

this situation. See bertsekas2011incremental

for a survey of first-order incremental methods.

The Newton-type Incremental Method with superlinear

local convergence was proposed in rodomanov2016superlinearly .

Local linear rate of stochastic Newton methods was studied in kovalev2019stochastic .

Global convergence of sub-sampled Newton schemes,

based on Damped iterations, and on Cubic regularization, was established

in roosta2016sub ; kohler2017sub ; tripuraneni2018stochastic .

The basic idea of stochastic algorithms is to substitute the true

gradients and Hessians by some random unbiased estimators

, and , respectively, with and .

First, let us consider the simplest estimation strategy.

At iteration , we sample uniformly and independently

two subsets of indices . Their sizes are and , which are possibly different. Then, in

Algorithm 1, we can use the following

random estimators:

(25)

Let us present for this process a result on its global

convergence. Note that in this section, we use the standard Euclidean norm

for vectors and the corresponding induced spectral norm for matrices.

{framedtheorem}

Let each component be Lipschitz continuous on with constant ,

and have Lipschitz continuous gradients and Hessians on

with constants and , respectively.

Let . Set

(26)

Then, for the iterations of

Algorithm (1), based on

estimators (25), it holds

(27)

Therefore, in order to solve our problem with

-accuracy in expectation,

, we need to perform

iterations of the method. In this case, the total number

of gradient and Hessian samples are and , respectively. It is

interesting that we need higher accuracy for estimating

the gradients, which results in a bigger batch size.

To improve this result, we incorporate a simple

variance reduction strategy for the gradients.

This is a popular technique in stochastic convex optimization (see schmidt2017minimizing ; johnson2013accelerating ; defazio2014saga ; hazan2016variance ; allen2017katyusha ; nguyen2017sarah ; gorbunov2019unified and references therein).

At some iterations, we recompute the full gradient. However,

during the whole optimization process this happens

logarithmic number of times in total. Let us denote by

the maximal power of two, which is less than

or equal to : , for , and define . The

entire scheme looks as follows.

Algorithm 4 Stochastic Variance-Reduced Contracting-Domain Newton

1:Choose .

2:.

3:Set anchor point .

4:Sample random batch of size .

5:Compute variance-reduced stochastic gradient

6:Compute stochastic Hessian

7:Pick up .

8:Perform the main step

Note that this is just Algorithm 1 with random estimators and

instead ot the true gradient and Hessian. The following global convergence result holds.

{framedtheorem}

Let each component have Lipschitz continuous gradients and Hessians

on with constants and , respectively.

Let . Set batch size

It is thanks to the variance reduction that

we can use the same batch size for both estimators now.

To solve the problem with -accuracy in expectation,

we need

iterations of the method. And the total number

of gradient and Hessian samples during these iterations is

.

7 Experiments

Let us demonstrate computational results for the problem

of training Logistic Regression model, regularized by -ball constraints.

Thus, the smooth part of the objective has the finite-sum

representation (24), each component is

.

The composite part is given by (4), with .

Diameter plays the role of regularization parameter, while

vectors

are determined by the dataset222https://www.csie.ntu.edu.tw/~cjlin/libsvmtools/datasets/.

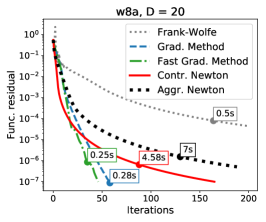

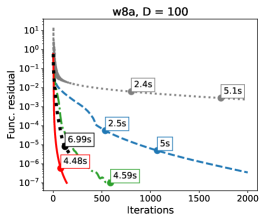

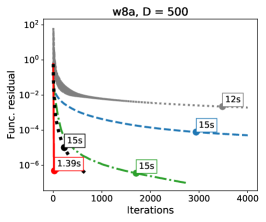

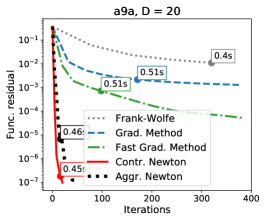

First, we compare the performance of Contracting-Domain

Newton Method

(Algorithm 1)

and Aggregating Newton Method (Algorithm 3)

with first-order optimization schemes:

Frank-Wolfe algorithm frank1956algorithm ,

the classical Gradient Method, and the Fast Gradient Method nesterov2013gradient .

For the latter two we use a line-search at each iteration, to estimate the Lipschitz constant.

The results are shown on Figure 2.

Figure 2: Training logistic regression, w8a .

We see, that for bigger , it becomes harder to solve the optimization problem.

Second-order methods demonstrate good performance both in terms of

the iterations, and the total computational time.

333Clock time was evaluated using the machine with Intel Core i5 CPU, 1.6GHz; 8 GB RAM.

All methods were implemented in C++.

The source code can be found at https://github.com/doikov/contracting-newton/

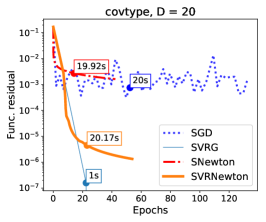

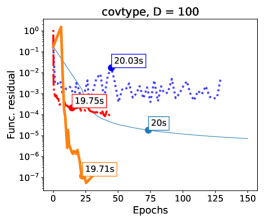

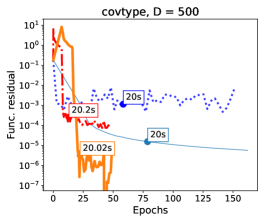

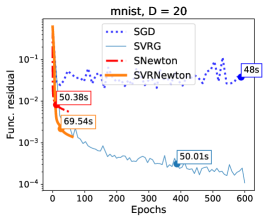

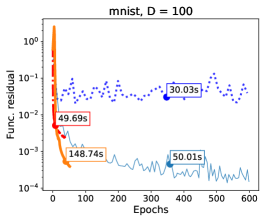

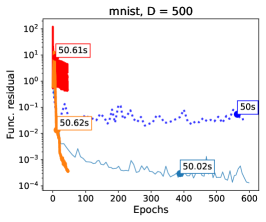

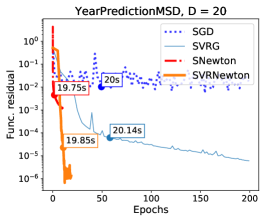

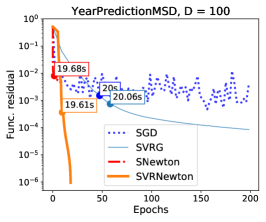

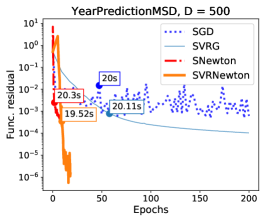

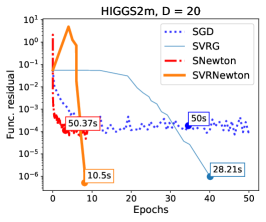

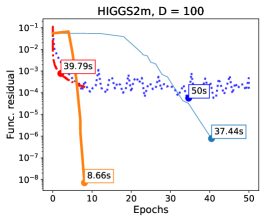

Figure 3: Stochastic methods for training logistic regression,

covtype .

In the next set of experiments, we compare the basic stochastic version of our method,

using estimators (25) — SNewton,

the method with the variance reduction

(Algorithm 4) — SVRNewton,

and first-order algorithms (with constant step-size, tuned for each problem): SGD and SVRG johnson2013accelerating .

We see (Figure 3) that using the variance reduction strategy

significantly improve the convergence for both first-order and second-order

stochastic optimization methods.

According to these graphs, our second-order algorithms can be

more efficient when solving ill-conditioned problems,

producing the better solution within a given computational time.

See also Section E in Appendix

for extra experiments.

8 Discussion

Let us discuss complexity estimates,

which we established in our work.

For the basic versions of our method

we have the global convergence in the functional residual

of the form

Note that the complexity parameter depends

only on the variation of the Hessian (in arbitrary norm).

It can be much smaller than the maximal eigenvalue

of the Hessian, which typically appears in the rates

of first-order methods.

It is important that our algorithms

are free from using the norms or any other particular

parameters of the problem class.

At the same time, the arithmetic complexity of one step of our methods

for simple sets can be estimated as the sum of the cost of computing the Hessian,

and additional operations (to compute a suitable factorization of the matrix).

For example, the cost of computing the gradient of Logistic Regression

is , and the Hessian is , where is the dataset size.

Hence, it is preferable to use our algorithms with exact steps

in the situation when is much bigger than .

Acknowledgments and Disclosure of Funding

The research results of this paper were obtained in the framework of ERC Advanced Grant 788368.

References

[1]

Zeyuan Allen-Zhu.

Katyusha: The first direct acceleration of stochastic gradient

methods.

The Journal of Machine Learning Research, 18(1):8194–8244,

2017.

[2]

Francis Bach.

Self-concordant analysis for logistic regression.

Electronic Journal of Statistics, 4:384–414, 2010.

[3]

Albert A Bennett.

Newton’s method in general analysis.

Proceedings of the National Academy of Sciences,

2(10):592–598, 1916.

[4]

Dimitri P Bertsekas.

Incremental gradient, subgradient, and proximal methods for convex

optimization: A survey.

Optimization for Machine Learning, 2010(1-38):3, 2011.

[5]

Alejandro Carderera and Sebastian Pokutta.

Second-order conditional gradients.

arXiv preprint arXiv:2002.08907, 2020.

[6]

Yair Carmon and John C Duchi.

First-order methods for nonconvex quadratic minimization.

arXiv preprint arXiv:2003.04546, 2020.

[7]

Coralia Cartis, Nicholas IM Gould, and Philippe L Toint.

Adaptive cubic regularisation methods for unconstrained optimization.

Part I: motivation, convergence and numerical results.

Mathematical Programming, 127(2):245–295, 2011.

[8]

Coralia Cartis, Nicholas IM Gould, and Philippe L Toint.

Adaptive cubic regularisation methods for unconstrained optimization.

Part II: worst-case function-and derivative-evaluation complexity.

Mathematical programming, 130(2):295–319, 2011.

[9]

Andrew R Conn, Nicholas IM Gould, and Philippe L Toint.

Trust region methods.

SIAM, 2000.

[10]

Aaron Defazio, Francis Bach, and Simon Lacoste-Julien.

Saga: A fast incremental gradient method with support for

non-strongly convex composite objectives.

In Advances in neural information processing systems, pages

1646–1654, 2014.

[11]

Nikita Doikov and Yurii Nesterov.

Local convergence of tensor methods.

CORE Discussion Papers 2019/21, 2019.

[12]

Nikita Doikov and Yurii Nesterov.

Minimizing uniformly convex functions by cubic regularization of

Newton method.

arXiv preprint arXiv:1905.02671, 2019.

[13]

Nikita Doikov and Peter Richtárik.

Randomized block cubic Newton method.

In International Conference on Machine Learning, pages

1289–1297, 2018.

[14]

Pavel Dvurechensky and Yurii Nesterov.

Global performance guarantees of second-order methods for

unconstrained convex minimization.

Technical report, CORE Discussion Paper, 2018.

[15]

Marguerite Frank and Philip Wolfe.

An algorithm for quadratic programming.

Naval research logistics quarterly, 3(1-2):95–110, 1956.

[16]

Eduard Gorbunov, Filip Hanzely, and Peter Richtárik.

A unified theory of sgd: Variance reduction, sampling, quantization

and coordinate descent.

arXiv preprint arXiv:1905.11261, 2019.

[17]

Geovani N Grapiglia and Yurii Nesterov.

Regularized Newton methods for minimizing functions with

Hölder continuous Hessians.

SIAM Journal on Optimization, 27(1):478–506, 2017.

[18]

Geovani N Grapiglia and Yurii Nesterov.

Accelerated regularized Newton methods for minimizing composite

convex functions.

SIAM Journal on Optimization, 29(1):77–99, 2019.

[19]

Filip Hanzely, Nikita Doikov, Peter Richtárik, and Yurii Nesterov.

Stochastic subspace cubic Newton method.

arXiv preprint arXiv:2002.09526, 2020.

[20]

Elad Hazan and Haipeng Luo.

Variance-reduced and projection-free stochastic optimization.

In International Conference on Machine Learning, pages

1263–1271, 2016.

[21]

Rie Johnson and Tong Zhang.

Accelerating stochastic gradient descent using predictive variance

reduction.

In Advances in neural information processing systems, pages

315–323, 2013.

[22]

Leonid V Kantorovich.

Functional analysis and applied mathematics.

Uspekhi Matematicheskikh Nauk, 3(6):89–185, 1948.

[23]

Sai Praneeth Karimireddy, Sebastian U Stich, and Martin Jaggi.

Global linear convergence of Newton’s method without

strong-convexity or Lipschitz gradients.

arXiv preprint arXiv:1806.00413, 2018.

[24]

Jonas Moritz Kohler and Aurelien Lucchi.

Sub-sampled cubic regularization for non-convex optimization.

In International Conference on Machine Learning, pages

1895–1904, 2017.

[25]

Dmitry Kovalev, Konstantin Mishchenko, and Peter Richtárik.

Stochastic Newton and cubic Newton methods with simple local

linear-quadratic rates.

arXiv preprint arXiv:1912.01597, 2019.

[26]

Jason D Lee, Yuekai Sun, and Michael A Saunders.

Proximal Newton-type methods for minimizing composite functions.

SIAM Journal on Optimization, 24(3):1420–1443, 2014.

[27]

Yurii Nesterov.

Accelerating the cubic regularization of Newton’s method on convex

problems.

Mathematical Programming, 112(1):159–181, 2008.

[30]

Yurii Nesterov.

Complexity bounds for primal-dual methods minimizing the model of

objective function.

Mathematical Programming, 171(1-2):311–330, 2018.

[32]

Yurii Nesterov and Arkadii Nemirovskii.

Interior-point polynomial algorithms in convex programming.

SIAM, 1994.

[33]

Yurii Nesterov and Boris T Polyak.

Cubic regularization of Newton’s method and its global performance.

Mathematical Programming, 108(1):177–205, 2006.

[34]

Lam M Nguyen, Jie Liu, Katya Scheinberg, and Martin Takáč.

Sarah: A novel method for machine learning problems using stochastic

recursive gradient.

In International Conference on Machine Learning, pages

2613–2621, 2017.

[35]

Anton Rodomanov and Dmitry Kropotov.

A superlinearly-convergent proximal Newton-type method for the

optimization of finite sums.

In International Conference on Machine Learning, pages

2597–2605, 2016.

[36]

Farbod Roosta-Khorasani and Michael W Mahoney.

Sub-sampled newton methods i: globally convergent algorithms.

arXiv preprint arXiv:1601.04737, 2016.

[37]

Mark Schmidt, Nicolas Le Roux, and Francis Bach.

Minimizing finite sums with the stochastic average gradient.

Mathematical Programming, 162(1-2):83–112, 2017.

[38]

Tianxiao Sun and Quoc Tran-Dinh.

Generalized self-concordant functions: a recipe for Newton-type

methods.

Mathematical Programming, 178(1-2):145–213, 2019.

[39]

Nilesh Tripuraneni, Mitchell Stern, Chi Jin, Jeffrey Regier, and Michael I

Jordan.

Stochastic cubic regularization for fast nonconvex optimization.

In Advances in Neural Information Processing Systems, pages

2899–2908, 2018.

[40]

Joel A Tropp.

An introduction to matrix concentration inequalities.

Foundations and Trends® in Machine Learning,

8(1-2):1–230, 2015.

First, let us note that inequality (6) follows from the

following simple observation,

using Newton-Leibniz formula and Hölder continuity of the Hessian,

for all

We are ready to prove the lemma.

Lemma 1

For all and , it holds

Proof:

Let us prove the following bound,

for all and

(30)

For it follows from (6).

Therefore,

we may assume that .

Let us take .

Then, by convexity of , we have

Now, from Hölder continuity of the Hessian, we get

Thus we prove (30).

Then, the claim of the lemma can be obtained by

simple integration:

Appendix B Convergence of Contracting-Domain Newton Method

In this section, we prove the global convergence of

Algorithms 1 and 2.

We use the same notation as in the main part. There is

a sequence of controlling coefficients (see relations (12)),

and a sequence of linear Estimating Functions . We denote by the constant of strong convexity of .

We allow in the following auxiliary lemma,

in order to cover both the general convex and the strongly convex cases.

Lemma 2

For the sequences and ,

produced by Algorithm 1, we have

(31)

with

(32)

Proof:

Let us prove (31) by induction.

It obviously holds for , since ,

, and

by definition.

Assume that it holds for the current , and consider the next iterate.

Stationary condition for the method step is

(33)

for all . Then, we have

where and stand for convexity of , and strong convexity of ,

correspondingly. Thus we have (31) established

for all .

For the sequence generated by Algorithm 3,

relation (22) is satisfied.

Proof:

Let us establish the relation (22) by induction. It obviously

holds for . Assume that it is proven for the current iterate ,

and consider the next step:

Let us consider the following general iterations,

for solving optimization problem (1):

(37)

with .

This is Algorithm 1 with substituted vector

and matrix instead of the true gradient and the Hessian.

First, we need to study the convergence of this process. For simplicity,

let us study the case only

(convex functions with Lipschitz continuous Hessian,

we denote the corresponding Lipschitz constant by ).

Recall, that in this section we use the standard Euclidean norm

for vectors and induced spectral norm for matrices.

As before, we use the sequence of positive numbers

, and set

Now, we are ready to prove convergence results

for the process (37)

with the basic variant of stochastic estimators (25),

and with the variance reduction strategy for the gradients,

incorporated into Algorithm 4.

Let each component be Lipschitz continuous on with constant ,

and have Lipschitz continuous gradients and Hessians on

with constants and , respectively.

Let . Set

Then, for the iterations of

Algorithm (1), based on

estimators (25), it holds

Proof:

Let us fix iteration . For one uniform random sample , we have

(43)

Therefore, for the random batch of size , we obtain

(44)

More advanced reasoning for matrices (Matrix Bernstein Inequality; see Chapter 6 in [40]) gives

(45)

So, using these estimates together, we have, for every

So, using the variance reduction for the gradients,

and the basic estimate for the Hessians, we have, for every

Now, let us set , and thus , so

we have

(49)

where

We are going to prove by induction, for every

(50)

with

(51)

Hence, if (50) is true, then we essentially obtain the claim of the theorem.

For , (50) follows directly from (49).

Assume that (50) holds for all , and consider

iteration :

where in we have used two simple bounds: ,

and , valid for all .

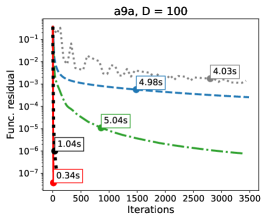

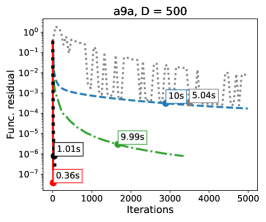

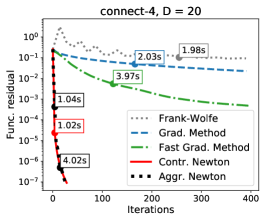

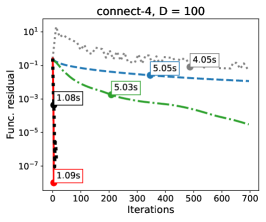

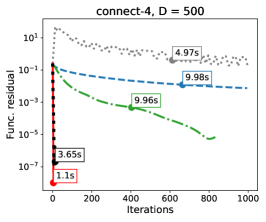

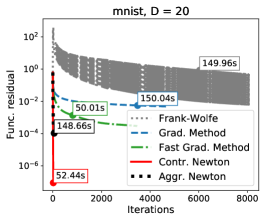

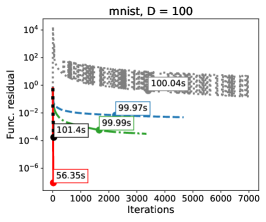

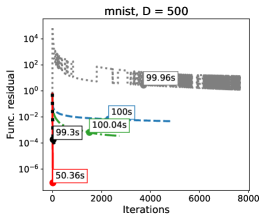

Appendix E Extra experiments

In this section, we provide additional experimental results for the problem

of training Logistic Regression model, regularized by -ball constraints:

Figure 4 for the exact methods, and

Figure 6 for the stochastic algorithms.

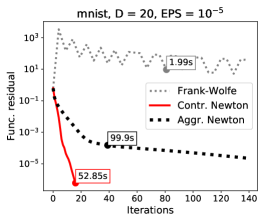

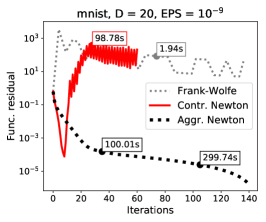

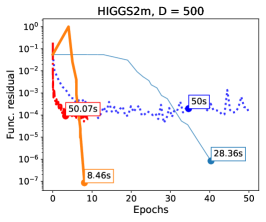

We see, that the second-order schemes usually outperforms first-order methods,

in terms of the number of iterations, and the number of epochs.

Despite the fact, that the Newton step is more expensive,

in many situations we see superiority of the second-order schemes

in terms of the total computational time as well.

Comparing Contracting-Domain Newton Method (Algorithm 1),

and Aggregating Newton Method (Algorithm 3), we conclude that both

of the algorithms show reasonably good performance in practice.

The latter one works a bit slower. However,

the aggregation of the Hessians helps to improve numerical stability.

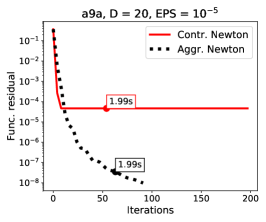

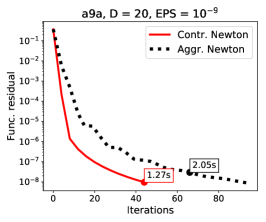

On Figure 5, we demonstrate

influence of the parameter of inner accuracy (EPS),

which we use in our subsolver, on the convergence of the algorithms.

We see much more robust behaviour for Aggregating Newton Method,

while the first algorithm can potentially stop, or even start to diverge,

if the parameter is chosen in a wrong way.

To compute one step of our second-order methods for this task,

we need to solve subproblem (20)

for . This is minimization of quadratic function over the standard Euclidean ball.

First, we compute tridiagonal decomposition of the Hessian

(it requires arithmetical operations).

Then, we solve the dual to our subproblem (which is maximization of one-dimensional concave function)

by classical Newton iterations (the cost of each iteration is ).

For more details, see Chapter 7 in [9].

Figure 5: Influence of the parameter of inner accuracy.

Figure 6: Stochastic methods for training logistic regression, datasets:

mnist ,

YearPredictionMSD ,

HIGGS2m .