Learning Bounds for Risk-sensitive Learning

Abstract

In risk-sensitive learning, one aims to find a hypothesis that minimizes a risk-averse (or risk-seeking) measure of loss, instead of the standard expected loss. In this paper, we propose to study the generalization properties of risk-sensitive learning schemes whose optimand is described via optimized certainty equivalents (OCE): our general scheme can handle various known risks, e.g., the entropic risk, mean-variance, and conditional value-at-risk, as special cases. We provide two learning bounds on the performance of empirical OCE minimizer. The first result gives an OCE guarantee based on the Rademacher average of the hypothesis space, which generalizes and improves existing results on the expected loss and the conditional value-at-risk. The second result, based on a novel variance-based characterization of OCE, gives an expected loss guarantee with a suppressed dependence on the smoothness of the selected OCE. Finally, we demonstrate the practical implications of the proposed bounds via exploratory experiments on neural networks.

1 Introduction

The systematic minimization of the quantifiable uncertainty, or risk [28], is one of the core objectives in all disciplines involving decision-making, e.g., economics and finance. Within machine learning contexts, strategies for risk-aversion have been most actively studied under sequential decision-making and reinforcement learning frameworks [25, 9], giving birth to a number of algorithms based on Markov decision processes (MDPs) and multi-armed bandits. In those works, various risk-averse measures of loss have been used as a minimization objective, instead of the risk-neutral expected loss; popular risk measures include entropic risk [25, 7, 8], mean-variance [47, 17, 35], and a slightly more modern alternative known as conditional value-at-risk (CVaR [19, 11, 50]). Yet, with growing interest to the societal impacts of machine intelligence, the importance of risk-aversion under non-sequential scenarios has also been spotlighted recently. For instance, Williamson and Menon [53] give an axiomatic characterization of the fairness risk measures, and propose a convex fairness-aware objective based on CVaR. Also, Curi et al. [14] empirically demonstrate the effectiveness of their CVaR minimization algorithm to account for the covariate shift in the data-generating distribution.

The advantage of risk-sensitive (either risk-seeking or risk-averse) objectives in machine learning, however, is not limited to tasks involving social considerations. Indeed, there exists a rich body of works which implicitly propose to minimize risk-sensitive measures of loss, as a technique to better optimize the standard expected loss. For example, the idea of prioritizing low-loss samples for learning is prevalent in noisy label handling [22] or curriculum learning [30]. In those contexts, high-loss samples are viewed as either mislabeled, or correctly labeled but detrimental to training dynamics due to their “difficulty.” Such algorithms can be viewed as implicitly optimizing a risk-seeking counterpart of CVaR (see Section 2.2). Contrarily (and ironically), it is also common to focus on high-loss samples to improve the model accuracy or accelerate the optimization [10]. Such algorithms can be viewed as minimizing risk-averse measures of loss; for instance, learning with average top- loss [16] is equivalent to the CVaR minimization when the number of samples is fixed.

Given this widespread use of risk-sensitive learning algorithms, theoretical understandings of their generalization properties are still limited. For risk-seeking learning, the risk measure being minimized is typically not explicitly stated; see [22], for instance. For risk-averse learning, existing theoretical results are focused on validating the stability and convergence of the algorithm (e.g. [35]), instead of providing generalization/excess-risk guarantees. Some exceptions in this respect are the recent works on CVaR [16, 14, 48]; the guarantees, however, are highly specialized for the algorithmic setups considered, such as support vector machines with reproducing kernel Hilbert spaces [16], finite function class111We note that the most recent version of [14] (also appearing NeurIPS 2020) now provides an extension to the case of finite VC-dimension. Lemma 3 refines the extended result as well. [14], or requiring additional smoothness assumptions [48].

To fill this gap, we propose to study risk-sensitive learning schemes under a statistical learning theory viewpoint [23], where the focus is on the convergence properties of the risk measure itself; learning algorithms are simply abstracted as a procedure of finding a hypothesis minimizing the target risk measure on training data. To discuss various risk-sensitive measures under a unified framework, we rejuvenate the notion of optimized certainty equivalent (OCE [5]). With a careful choice of the disutility function governing the deviation penalty, OCE covers a wide range of risk-averse measures including the entropic risk, mean-variance, and CVaR (see Section 2). To formalize risk-seeking learning schemes, we newly define inverted OCE as a natural counterpart of OCE; inverted OCE covers learning algorithms that only utilize a fraction of samples with smallest losses.

Under this general framework, we establish two performance guarantees for the empirical OCE minimization (EOM) procedure (see Section 3); we also provide analogous results for inverted OCEs.

-

•

Theorem 4 provides a general bound on the excess OCE of the EOM hypothesis via Rademacher averages. For the case of CVaR, the bound provides a first data-dependent bound that improves or recovers the existing data-independent bounds (e.g., VC dimension). For the case of expected loss, the bound recovers the standard risk guarantee. The proof is based on the contraction properties [31] of a product space constructed with the original hypothesis space and dual parameter space.

-

•

Theorem 7 controls the expected loss of the EOM hypothesis via a novel variance-based characterization of OCE (Lemma 6). In contrast to the OCE guarantee in Theorem 4, the expected loss guarantee does not depend crucially on the properties of the target OCE measure in the realizable case, i.e., the hypothesis space is rich enough to contain a hypothesis with an arbitrarily small loss.

Finally, we empirically validate an implication of Lemma 6 that EOM can be relaxed to the sample variance penalization (SVP) procedure. The relaxed version is known to enjoy stronger generalization properties, making the algorithm an attractive candidate to be considered as an alternative baseline method for the OCE minimization. In our experiments on CIFAR-10 [29] with ResNet18 [24], we find that batch-based SVP indeed outperforms batch-based CVaR minimization (see Section 4).

All proofs are deferred to the Appendix A.

Notations. For a real number , we let . We write to denote the set of all nonnegative real numbers. When , we let . For a real-valued function , we write to denote its subgradient set, and to denote its Lipschitz constant (on the considered domain). The pushforward measure of a distribution by a mapping , i.e., the distribution of where , is denoted by . For the probability distribution of a real random variable, the notation denotes the quantile function , where is the cumulative distribution function of . All s are base .

| Name | Definition | Disutility function | ||

|---|---|---|---|---|

| Expected loss | ||||

| Entropic risk | ||||

| Mean-variance | ||||

| Conditional Value-at-Risk |

-

The conditional expectation representation holds only for the pairs generating continuous pushforwards . A more general definition that covers the discrete case can be found in [41].

2 Measures for risk-sensitive learning

We start from the standard statistical learning framework [23]. We have a class of probability measures called data-generating distributions, defined on a measurable instance space . We are also given a hypothesis space of measurable functions , quantifying the loss incurred by a decision rule when applied to a data instance . A standard measure to aggregate samplewise losses of a hypothesis over a population of data instances is to take an expected loss,222We avoid using more popular terminologies (“risk” and “empirical risk”) to prevent unnecessary confusion. defined as

| (1) |

We assume that the data-generating distribution is not known to the learner. Instead, the learner is assumed to have an access to copies of training samples independently drawn from . Then, the expected loss can be estimated by the empirical loss

| (2) |

where denotes the empirical distribution of training samples. Both expected loss and empirical loss are risk-neutral measures that assign uniform weight on the samples regardless of their losses.

2.1 Risk-averse measures: optimized certainty equivalents

Among the diverse set of measures for risk-aversion in economics (see Appendix C for details), we focus on the optimized certainty equivalents (OCE) introduced by Ben-Tal and Teboulle [5].

Definition 1 (OCE risk).

Let the disutility function be a nondecreasing, closed, convex function with and . Then, the corresponding OCE risk is given as333We omit or in when clear from context.

| (3) |

Definition 1, having its root in the expected utility theory [52], may look mysterious at first glance. To demystify a little bit, consider the following reparametrization: define the excess disutility as the difference of the disutility and the identity . From Definition 1, we know that the excess disutility is a nonnegative, convex function satisfying , with a nondecreasing . Then, the OCE risk can be written as

| (4) |

In other words, OCE additionally penalizes the expected deviation of the random object from some optimized anchor point . The penalty is described by the selection of a “bowl-shaped” excess disutility (or equivalently, the selection of disutility ).

With a careful choice of , Definition 1 covers a wide range of risk-averse measures used in machine learning literature, including the expected loss, entropic risk, mean-variance, and CVaR; popular OCE risks and corresponding choices of disutility are summarized in Table 1. The measures have been used in the following machine learning contexts. (1) Entropic risk: The risk has been used in one of the earliest works on risk-sensitive MDPs [25], and is often revisited in modern reinforcement learning contexts [7, 8, 39]. In a concurrent work, Li et al. [33] re-introduces the entropic risk to enhance outlier-robustness and fairness. (2) Mean-variance: Markowitz’s mean-variance analysis [36] is typically relaxed to the variance regularization in the context of MDPs [17, 35], multi-armed bandits [43, 51], and reinforcement learning [47, 1]. (3) CVaR: CVaR is used in more recent works on risk-averse reinforcement learning regarding bandits [19, 9] and MDPs [11, 50]. CVaR also enjoys connections to distributional robustness and fairness under general learning scenarios [53, 14, 48].

Similar to the expected loss, the OCE risk of a data-generating distribution can be estimated from the samples by using the empirical distribution as a proxy measure: we define the empirical OCE risk as

| (5) |

The empirical OCE underestimates the population OCE in general, due to its variational definition. Indeed, the OCE risk for a mixture distribution is always greater than or equal to the weighted average of OCE risks , as the inequality holds. From this observation, one may expect a slower two-sided uniform convergence of empirical OCE than empirical loss; this intuition is confirmed later (see Lemma 3).

We also note that OCE risks satisty the following properties, which enable an efficient computation and optimization (see [6] for derivations): (a) Convexity, i.e., , (b) Shift-additivity, i.e., , (c) Monotonicity, i.e., if with probability , then . Convexity is especially useful whenever the loss function underlying the hypotheses are also convex; interested readers are referred to Appendix C.

2.2 Risk-seeking measures: inverted OCEs

Unlike in financial economics literature, it often occurs in machine learning schemes [30, 22] to focus on the minimization of losses on easy examples (i.e., the samples already with low loss) and disregard hard examples. To formally address such learning algorithms, we propose considering the following family of risk-seeking measures constructed by inverting OCE risks.

Definition 2 (Inverted OCE risk).

Let be a nondecreasing, closed, convex function with and . Then, the corresponding inverted OCE risk is given as

| (6) |

We call the measure (6) an “inverted” OCE risk due to the following reason: Roughly speaking, the inverted OCE risk is designed to treat the sample at bottom- loss quantile as the OCE risk treats the sample at top- loss quantile. This goal can be achieved by defining the inverted OCE risk to satisfy , which gives the form (6). Analogously to Eq. 4, the inverted OCE risk can be written alternatively as

| (7) |

where again . In other words, the inverted OCE risk rewards the deviation from the optimized anchor , using the excess utility function to shape the reward.

It is straightforward to see that inverted OCE risks can be used to describe the algorithms that disregard samples with high loss. For example, Han et al. [22] propose the following algorithm to handle noisy labels: two models are trained simultaneously, by selecting and feeding -fraction of samples with the lowest loss to each other. Such a training objective can be described as an inverted version of CVaR, i.e., by using . Indeed, we can see the equivalence from the following proposition (see Section A.1 for the proof).

Proposition 1 (Average bottom- loss as inverted CVaR).

Let be the desired number of samples. Then, by the choice of disutility function , i.e., , we get

| (8) |

where denotes the index of the sample with -th smallest value of among .

The proposed notion of inverted OCE can thus be viewed as a generalized class of optimands for easy example first algorithms, that comes with theoretical performance guarantees (Theorems 4 and 7). We note that this class also includes a “softer” variant of the algorithm considered in Proposition 1, where a weighted sum of sample losses is taken with weights instead of for the bottom- fractions and top- fraction, respectively; we naturally assume that and holds. Indeed, one can simply choose to get the desired risk.

Given this connection, can we explain the empirical robustness of the noisy label handling algorithms (such as [22]) by analyzing the properties of inverted OCE risks? While this question is not under the main scope of this paper, we provide a partial answer to this question by analyzing the influence function [21], which is one of the key notions in the discipline of robust statistics. The function measures the sensitivity of a statistic to a distributional shift which may represent an outlier or contaminated data. Formally, the influence function of a statistic with respect to is given as

| (9) |

where denotes the point probability mass at , and denotes the distribution of uncontaminated samples. If we use the OCE risk as a target statistic (i.e., ), then the influence function can be viewed as a sensitivity of OCE minimization procedure against a distributional contamination. As a historical remark, we note that the influence function (9) is typically studied under a parametric framework, e.g., gauging the robustness of an estimator of distributional parameters such as moments (see the seminal treatise of Huber and Ronchetti [26] for a comprehensive overview). Nevertheless, we are not the first to analyze the influence function under a nonparametric scenario; for instance, Christmann and Steinwart [12] have studied the influence function of penalized empirical risk minimization procedure.

In the following proposition, we show that the inverted versions of popular OCE measures have better robustness characteristics than the expected loss (see Section A.2 for the proof).

Proposition 2 (Influence function of ).

The influence function for the inverted entropic risk and the inverted mean-variance are given as follows.

-

•

Entropic risk: .

-

•

Mean-variance: .

Whenever has a continuous density, then the influence function of inverted CVaR is given as

-

•

CVaR: .

From Proposition 2, we observe that the influence functions of the example inverted OCE risks have a smaller worse-case value than the influence function of the expected loss, which is . In particular, whenever there exists some such that is arbitrarily large, then the influence function of the expected loss can grow arbitrarily large as well. On the other hand, influence functions of the example inverted OCE risks are bounded from above by

| (10) |

respectively for inverted entropic risk, mean-variance, and CVaR.

3 Performance guarantees for empirical OCE minimizers

We now consider an empirical OCE minimization (EOM) procedure, finding

| (11) |

instead of the ordinary empirical risk minimization (ERM), which aims to minimize the empirical loss. Existing learning algorithms that implement EOM, either explicitly or implicitly, can be roughly categorized into two categories, depending on their purposes. In the works of the first category (e.g. [16, 14, 48]), the primary goal is to minimize the population OCE risk (i.e., ) for risk-aversion or fairness considerations. In the works of the second category (e.g. [10, 37, 33]), the ultimate goal is to optimize the population expected loss (i.e., ), and risk-sensitive measures are used with the belief that minimizing the measures may help accelerate/stabilize the learning dynamics. To address both lines of research, we provide performance guarantees in terms of both OCE and expected loss. In particular, we show that the empirical OCE minimizer (11) has the OCE risk and the expected loss similar to those of

| (12) |

(shown in Section 3.1 and Section 3.2, respectively). We also give analogous results for the empirical inverted OCE minimization (EIM), where the hypotheses achieving minimum empirical and population will be denoted by and .

3.1 OCE guarantee via uniform convergence

First, we provide an excess OCE guarantee of the empirical OCE minimizer based on the uniform convergence of the empirical OCE risk to the population OCE risk. To formalize, recall that the Rademacher average [4] of a hypothesis space given training samples is defined as

| (13) |

where are independent Rademacher random variables, i.e., . With this definition at hand, we can state our key lemma characterizing uniform convergence properties of OCE risks and inverted OCE risks (see Section A.3 for the proof).

Lemma 3 (Uniform convergence).

Suppose that the hypothesis space is bounded, i.e. there exists some such that holds for all . Then, for any ,

| (14) |

holds with probability at least .

Moreover, the same bound holds whenever the are replaced by .

Similar to typical uniform convergence guarantees for the empirical loss [4], the bound (14) vanishes to zero at the rate for standard hypothesis spaces whose expected Rademacher averages could be bounded from above by a term. Indeed, Lemma 3 closely recovers the usual uniform convergence bound for expected loss if we plug in , with a slack of that is small compared to the other terms. We also note that the Lipschitz constant of disutility functions cannot be smaller than one, and thus Lemma 3 cannot be used to guarantee a strictly faster convergence rate than the bound for the expected loss.

Lemma 3 generalizes and improves over existing guarantees on CVaR [44, 49, 14, 48]. Indeed, all previous results (up to our knowledge) are described in terms of data-independent complexity measures of the hypothesis space, e.g. VC-dimension; roughly, this is due to the proof technique relying on a direct use of union bound. In contrast, by considering a dual product space approach (see, e.g. [32]) combined with contraction principles [31], we arrive at the bound described via Rademacher averages. Rademacher average is a data-dependent complexity measure [4] which enjoys a significant benefit in the analysis of modern hypothesis spaces. Indeed, the data-dependency is considered an irreplaceable element to understanding the generalization properties of neural networks [54]. At the same time, Rademacher averages can be controlled by data-independent complexity measures such as VC-dimension, to recover existing results; see [4] for an extensive discussion.

Using Lemma 3, we give an excess OCE risk guarantee on the hypothesis minimizing the empirical OCE risk (see Section A.4 for the proof).

Theorem 4 (OCE guarantee).

Suppose that the hypothesis space is bounded, i.e. there exists some such that holds for all . Then, the empirical OCE minimizer (11) satisfies

| (15) |

with probability at least . For the empirical inverted OCE minimizer, we analogously have

| (16) |

with probability at least .

For sufficiently expressive hypothesis spaces, will become close to zero, and the upper bound becomes directly proportional to the Lipschitz constant of the disutility function.

3.2 Expected loss guarantee via variance-based characterization

To establish expected loss guarantees for the empirical OCE minimizer, we give two inequalities relating moments of the loss population to the OCE risk. The first one follows directly from the definitions of and (see Section A.5 for the proof).

Proposition 5 (Mean-based characterization).

For any and , we have

| (17) |

Combining Proposition 5 with Lemma 3, one can obtain an elementary expected loss guarantee on the EOM hypothesis: With probability at least , we have

| (18) |

The explanatory power of Ineq. (18), however, is clearly limited. To see this, consider a sufficiently expressive hypothesis space, so that one can always find a hypothesis perfectly fitting the training data. In this case, the EOM hypothesis also minimizes the expected loss, as we know that holds from Proposition 5. Then, one may expect an expected loss guarantee of the EOM hypothesis to be similar to that of the ERM hypothesis, not scaling with .

In light of this observation, we provide an alternative bound which relates OCE risks to both mean and variance of the loss population. For conciseness, we first introduce a shorthand notation for the loss variance of a hypothesis .444Again, we drop whenever the choice is clear from context, and write for the empirical version.

| (19) |

Now we can prove the following lemma bounding the difference of OCE risks and expected loss in terms of loss variance (see Section A.6 for the proof).

Lemma 6 (Variance-based characterization).

Let be a bounded function, i.e. there exists some such that holds. Then, we have

| (20) | ||||

| (21) |

where .

We note that Gotoh et al. [20] also relates (dual forms of) OCE risks to variance, where the authors assume the twice continuous differentiability of the convex conjugate of the disutility function and use Taylor expansion to arrive at an asymptotic expression for the case . Lemma 6, on the other hand, exploits the convexity of and the dominance relations between disutility functions to provide nonasymptotic bound without requiring further smoothness assumptions on . For example, the conjugate disutility function of CVaR is not differentiable, but Lemma 6 holds with and .

Using Lemma 6, we can prove the following theorem (see Section A.7 for the proof).

Theorem 7 (Expected loss guarantee).

Let be a fixed, unknown data-generating distribution, and let hypothesis space be bounded, i.e. there exists some such that holds almost surely for all . Then, for any and , we have

| (22) |

with probability at least . Under the same assumptions, we have

| (23) |

with probability at least . Moreover, one can replace in (22), (23) by any fixed .

In contrast to (18), the bound (22) is related to the disutility function only through a term proportional to . To see the benefit of this suppressed dependence, consider a case where the hypothesis space is a universal approximator (also known as the realizable case). Then, the first and second moment of loss population becomes zero, and Theorem 7 gives an ERM-like expected loss guarantee on the empirical OCE minimizer.

Regarding the bound for the EIM hypothesis, we remark that the non-vanishing term in the bound (23) depends on the behavior of the learned hypothesis on the training data only, unlike in (22); such discrepancy can help to recover ERM-like bounds under a milder assumption than universal approximability, for inverted OCE measures that make small (e.g., inverted entropic risk).

We remark that Lemma 6 indicates a potential connection of EOM to the sample variance penalization (SVP) procedure suggested by Maurer and Pontil [37]. Under suitable setups, one can show that the excess expected loss of the SVP hypothesis is , even when the excess expected loss of ordinary ERM decays no faster than . An interesting open question is whether, and under what conditions, the EOM can provide a similar acceleration. Indeed, we observe that EOM provides a nontrivial acceleration under at least one specific scenario: the stylized example of [37].

Example.

Consider a hypothesis space consisting of only two hypotheses , such that under the presumed data-generating distribution we have

| (24) |

for some . We are interested in the probability that EOM erroneously learns and incur the excess risk of size . More formally, we aim to provide lower and upper bound on the excess risk probability as . If we focus on the case of CVaR, the excess risk probability becomes where , and analyze the binomial tail to give the following proposition (see Section A.8 for the proof).

Proposition 8 (Faster convergence).

There exists an absolute constant , such that

| (25) |

holds for the empirical CVaR minimizer with .

We observe that can be made less than by taking , regardless of .

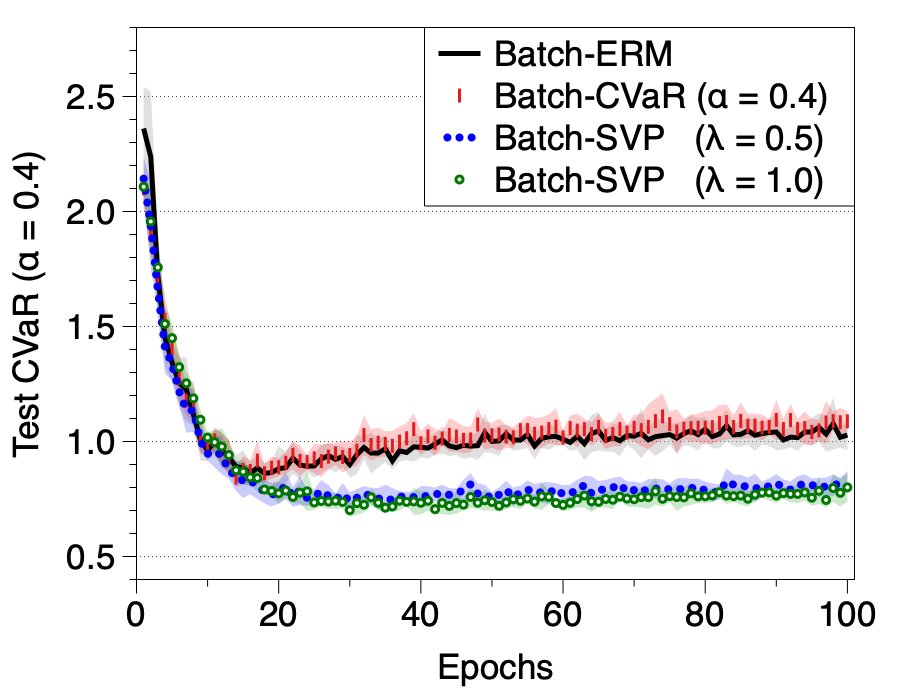

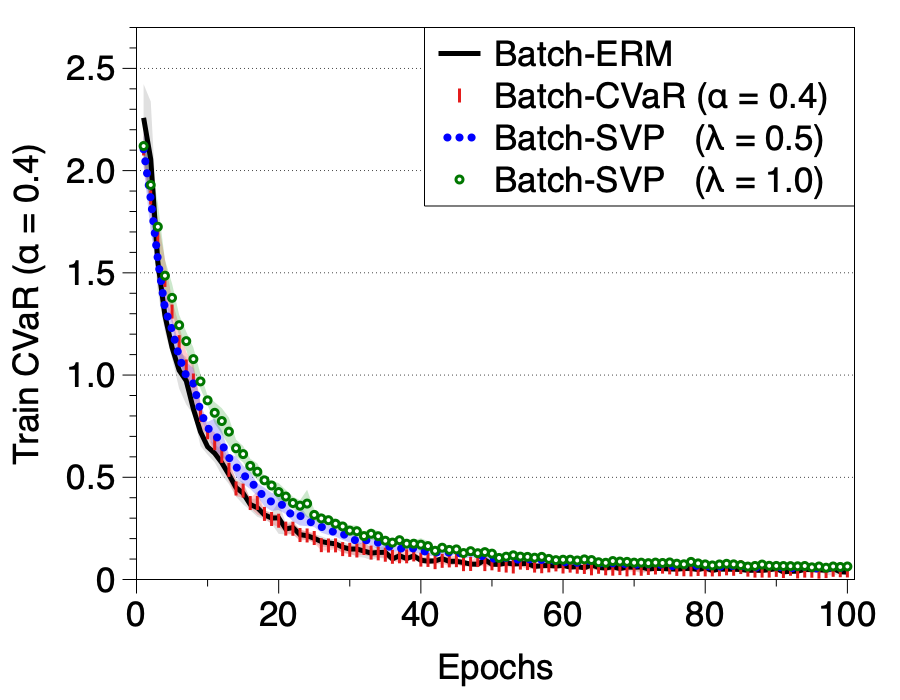

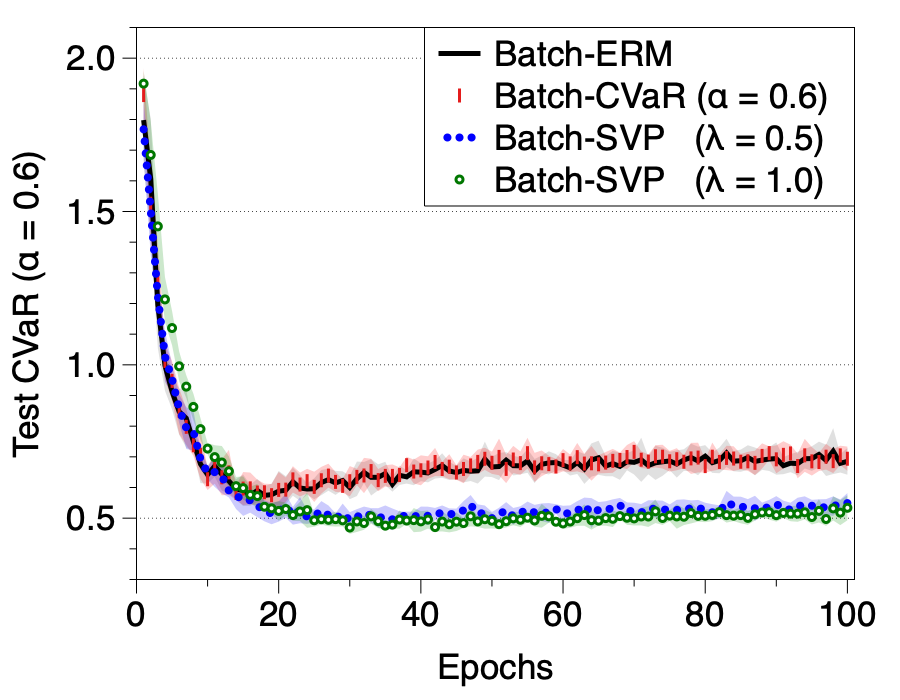

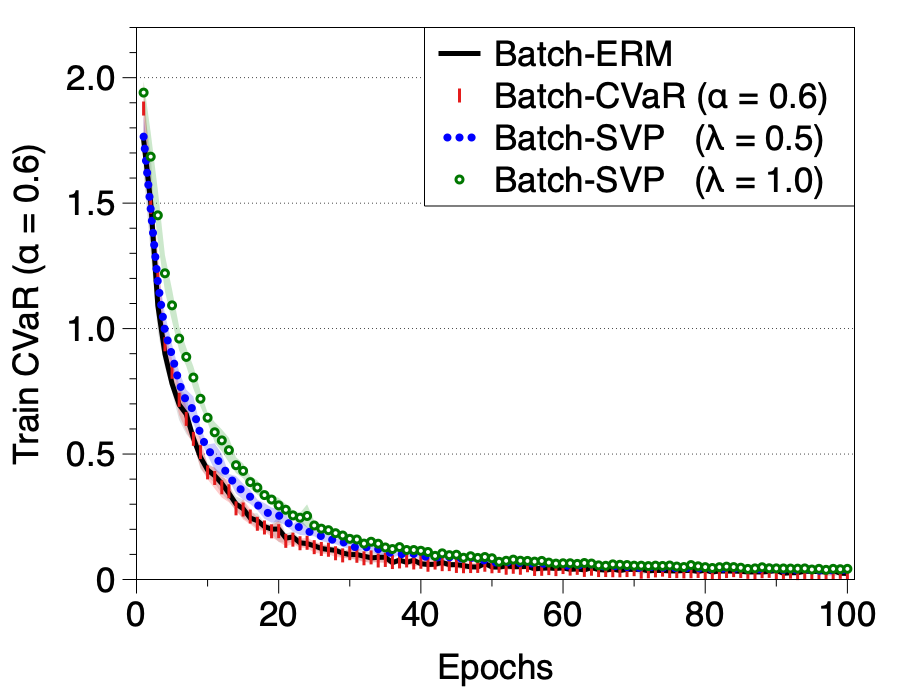

4 Numerical simulations: Batch-SVP for CVaR minimization

Recall that Lemma 6 implies that the EOM can be relaxed to the SVP, where one aims to find

| (26) |

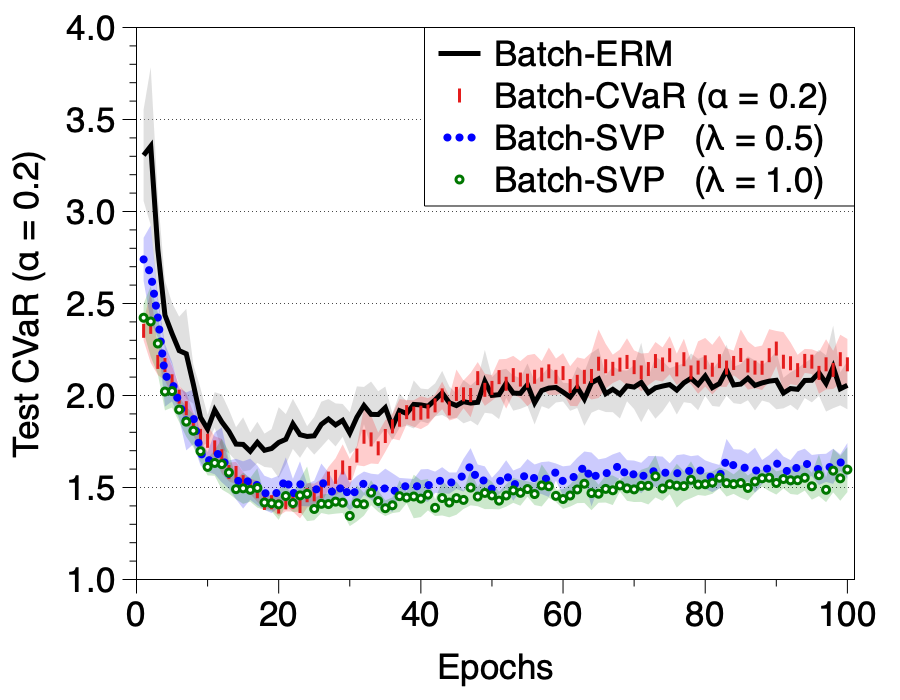

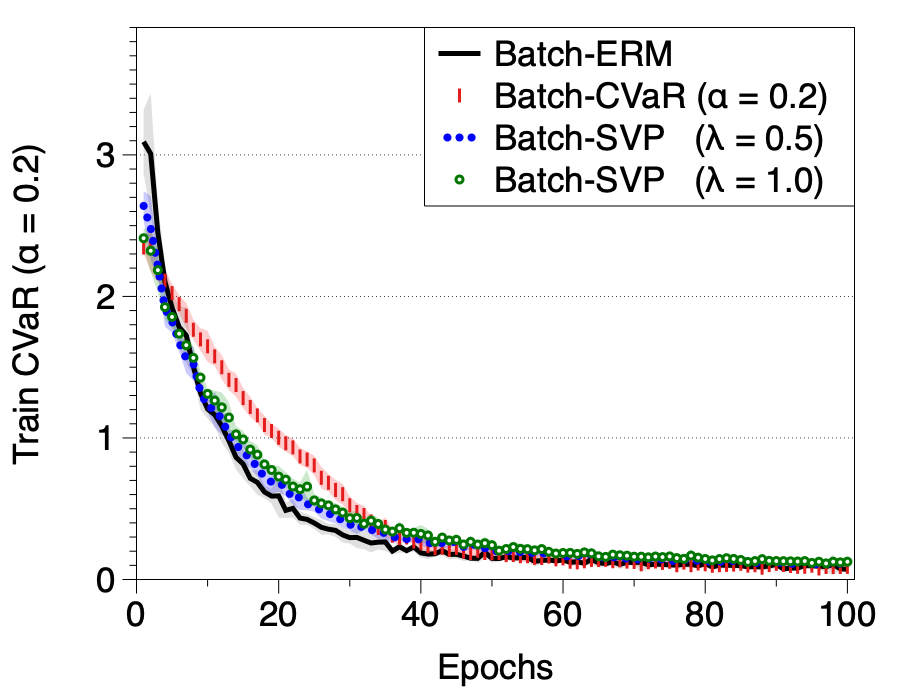

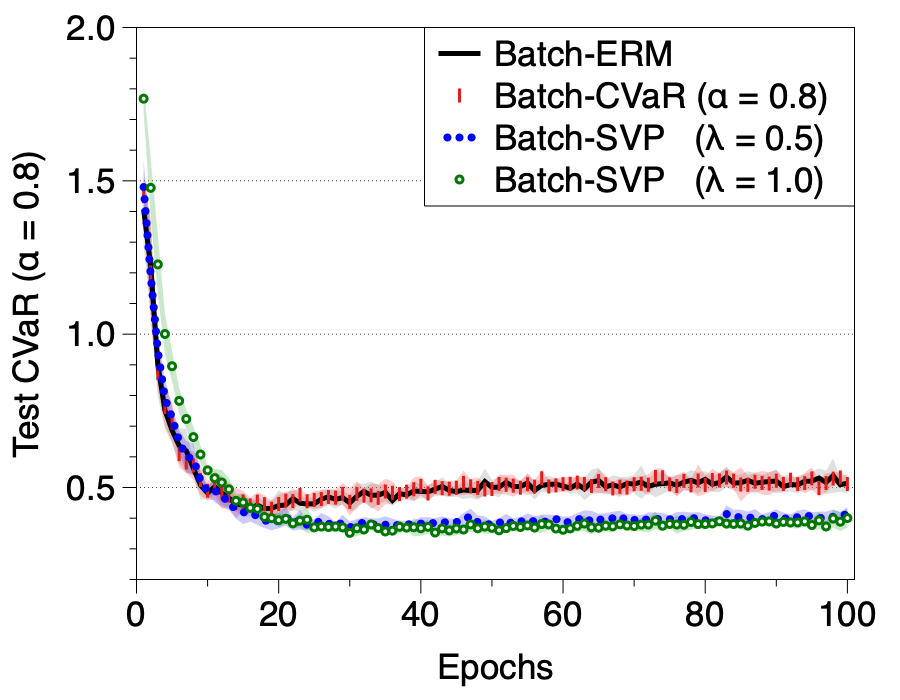

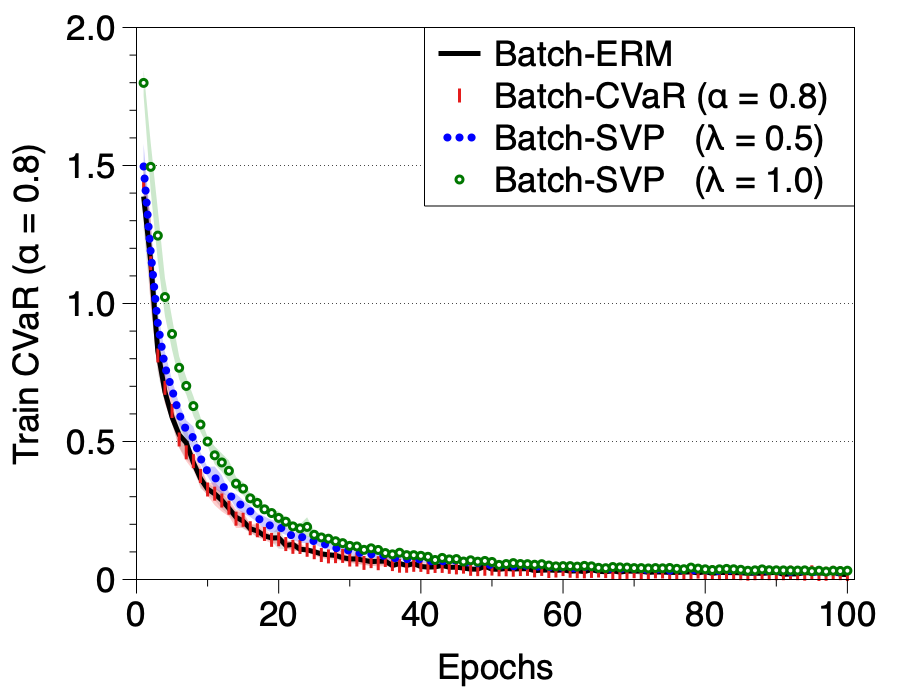

for some hyperparameter . At the same time, the relaxed form enjoys a favorable theoretical properties in terms of generalization [37], as briefly discussed in the previous section (although requiring a careful choice of ). In light of this observation, we explore the potential benefit of using SVP as an additional simple baseline for algorithmic studies on OCE minimization, along with a popularly used baseline of batch-based EOM; batch-based empirical CVaR minimization (dubbed batch-CVaR) has been used as a baseline in recent algorithmic works on CVaR minimization [14, 48]. As will be shown shortly, we find that batch-based SVP (dubbed batch-SVP) can outperform batch-CVaR without an overly sophisticated selection of the hyperparameter .

Setup. We focus on the case of CVaR minimization on CIFAR-10 image classification task [29] where we use the standard cross-entropy loss. As a model, we use ResNet18 [24]. As an optimizer, we use Adam with weight decay [34] with a batch size and PyTorch default learning rate. For CVaR, we have experimented with . For batch-SVP, we have simply tested over . All results are averaged over ten independent trials (more details at Appendix B).

Results and discussion. Trajectories of test and train CVaR for epochs are given in Fig. 1 for ; plots for are given in Appendix B. We observe that batch-SVP hypotheses achieve a similar or better performance than batch-CVaR at the best epoch, and have a much more stable learning curve due to the regularization properties of SVP. Moreover, after epochs, batch-CVaR start to perform worse than vanilla ERM. Similar phenomenon has been reported by [14], where batch-CVaR (and even other sophisticated methods) underperform the vanilla ERM under a number of settings. The trajectories suggest that such CVaR optimization methods are suffering from over-training. SVP provides a baseline method, which does not have such issues.

Code. Available at https://github.com/jaeho-lee/oce.

5 Summary and future directions

In this paper, we have (a) presented general theoretical guarantees for risk-sensitive learning (Theorems 4 and 7), (b) established a new framework to study risk-seeking learning scheme (Section 2.2), and (c) rejuvenated the sample variance penalization as a baseline algorithm for risk-averse learning (Section 4). As future work, we aim to address the generalization properties of learning algorithms that simultaneously train a hypothesis and a weighting function, according to which the hypothesis will be evaluated [40, 46]. Formalizing such scenarios may accompany an investigation of the complexity (e.g., Rademacher averages, VC-dimension) of the space of all possible weighting functions based on a generalized notion of spectral risk measures [2].

Broader impacts

This paper is focused on the subject of risk-sensitivity, which is a topic that is deeply intertwined with the safety, reliability, and fairness of machine intelligence (see, e.g., [42]). While our primary aim is to enhance theoretical understandings on the risk-sensitive learning, instead of proposing a new algorithm, we expect our results to have two broader consequences.

Facilitating algorithmic advances. For researchers trying to develop new risk-sensitive learning schemes, our general framework lowers the barrier to do so; we provide performance guarantees that applies for a broad class of algorithms that considers risk-seeking and risk-averse measures of loss (Theorems 4 and 7). Also, we provide a non-vacuous baseline to be compared with newly developed algorithms (Section 4). We believe that our theoretical framework will help stimulate further developments on risk-sensitive learning.

Pondering on the cost of fairness. One of our theoretical results (Theorem 4) can be interpreted as a characterization of (an instance of) the cost of fairness [13, 15, 38]. Indeed, recalling that CVaR is a fairness risk measure with an individual fairness criterion [53], Theorem 4 implies that the performance gap may grow wider if we try to apply a stricter fairness criterion. Such quantification of the cost of making a fairer decision is a double-edged sword; the cost may scare the decision-maker away from taking the fairness into account at all, or the cost may guide the decision-maker to find a fairest solution under the operational constraints. We sincerely hope that the latter is the case. Indeed, we also provide a result (Theorem 7) that the drawback of making a fair decision may not be big for modern machine learning applications!

Acknowledgements

JL thanks Aolin Xu, Maxim Raginsky, Insu Han, Sungsoo Ahn, and Sihyun Yu for their helpful feedbacks on the early version of the manuscript. JL also acknowledges the comments from an anonymous NeurIPS reviewer, which helped us refine the constant for Lemma 3.

Funding disclosure

This work was partly supported by Institute of Information & Communications Technology Planning & Evaluation (IITP) grant funded by the Korea government (MSIT, No.2019-0-00075, Artificial Intelligence Graduate School Program (KAIST)), and in part by the Engineering Research Center Program through the National Research Foundation of Korea (NRF) funded by the Korea Government (MSIT, NRF-2018R1A5A1059921).

References

- [1] Prashanth L. A. and Mohammad Ghavamzadeh. Actor-critic algorithms for risk-sensitive MDPs. In Advances in Neural Information Processing Systems, 2013.

- [2] Carlo Acerbi. Spectral measures of risk: A coherent representation of subjective risk aversion. Journal of Banking and Finance, 2002.

- [3] P. Artzner, F. Delbaen, J. M. Eber, and D. Heath. Coherent measures of risk. Mathematical Finance, 1999.

- [4] Peter L. Bartlett and Shahar Mendelson. Rademacher and Gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 2002.

- [5] Aharon Ben-Tal and Marc Teboulle. Expected utility, penalty functions and duality in stochastic nonlinear programming. Management Science, 1986.

- [6] Aharon Ben-Tal and Marc Teboulle. An old-new concept of convex risk measures: The optimized certainty equivalent. Mathematical Finance, 2007.

- [7] Vivek S. Borkar. A sensitivity formula for risk-sensitive cost and the actor-critic algorithm. Systems & Control Letters, 2001.

- [8] Vivek S. Borkar. Q-learning for risk-sensitive control. Mathematics of Operations Research, 2002.

- [9] Adrain R. Cardoso and Huan Xu. Risk-averse stochastic convex bandit. In Proceedings of the International Conference on Artificial Intelligence and Statistics, 2019.

- [10] Haw-Shiuan Chang, Erik Learned-Miller, and Andrew McCallum. Active bias: Training more accurate neural networks by emphasizing high variance samples. In Advances in Neural Information Processing Systems, 2017.

- [11] Yinlam Chow and Mohammad Ghavamzadeh. Algorithms for CVaR optimization in MDPs. In Advances in Neural Information Processing Systems, 2014.

- [12] Andreas Christmann and Ingo Steinwart. On robustness properties of convex risk minimization methods for pattern recognition. Journal of Machine Learning Research, 2004.

- [13] Sam Corbett-Davies, Emma Pierson, Avi Feller, Sharad Goel, and Aziz Huq. Algorithmic decision making and the cost of fairness. In Proceedings of the International Conference on Knowledge Discovery and Data Mining, 2017.

- [14] Sebastian Curi, Kfir Y. Levy, Stefanie Jegelka, and Andreas Krause. Adaptive sampling for stochastic risk-averse learning. In Advances in Neural Information Processing Systems, 2020. (to appear).

- [15] Michele Donini, Luca Oneto, Shai Ben-David, John Shawe-Taylor, and Massimiliano Pontil. Empirical risk minimization under fairness constraints. In Advances in Neural Information Processing Systems, 2018.

- [16] Yanbo Fan, Siwei Lyu, Yiming Ying, and Bao-Gang Hu. Learning with average top-k loss. In Advances in Neural Information Processing Systems, 2017.

- [17] Jerzy A. Filar, Lodewijk C. M. Kallenberg, and Huey-Miin Lee. Variance-penalized Markov decision processes. Mathematics of Operations Research, 1989.

- [18] Hans Föllmer and Alexander Schied. Convex measures of risk and trading constraints. Finance and Stochastics, 2002.

- [19] Nicolas Galichet, Michèle Sebag, and Olivier Teytaud. Exploration vs exploitation vs safety: Risk-aware multi-armed bandits. In Proceedings of Asian Conference on Machine Learning, 2013.

- [20] Jun-ya Gotoh, Michael J. Kim, and Andrew E. B. Lim. Robust empirical optimization is almost the same as mean-variance optimization. Operations Research Letters, 2018.

- [21] Frank R. Hampel, Elvezio M. Ronchetti, Peter J. Rousseauw, and Werner A. Stahel. Robust Statistics: The Approach based on Influence Functions. Wiley, 1986.

- [22] Bo Han, Quanming Yao, Xingrui Yu, Gang Niu, Miao Xu, Weihua Hu, Ivor W. Tsang, and Masashi Sugiyama. Co-teaching: Robust training of deep neural networks with extremely noisy labels. In Advances in Neural Information Processing Systems, 2018.

- [23] David Haussler. Decision theoretic generalizations of the PAC model for neural net and other applications. Information and Computation, 1989.

- [24] Kaiming He, Xiangyu Zhang, Shaoqing Ren, and Jian Sun. Deep residual learning for image recognition. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, 2016.

- [25] Ronald A. Howard and James E. Matheson. Risk-sensitive Markov decision processes. Management Science, 1972.

- [26] Peter J. Huber and Elvezio M. Ronchetti. Robust statistics. Wiley, 2nd edition, 2009.

- [27] J. Khim, L. Leqi, A. Prasad, and P. Ravikumar. Uniform convergence of rank-weighted learning. In Proceedings of the International Conference on Machine Learning, 2020.

- [28] Frank H. Knight. Risk, Uncertainty, and Profit. Houghton Mifflin, 1921.

- [29] Alex Krizhevsky. Learning multiple layers of features from tiny images. Technical report, University of Toronto, 2009.

- [30] M. Pawan Kumar, Benjamin Packer, and Daphne Koller. Self-paced learning for latent variable models. In Advances in Neural Information Processing Systems, 2010.

- [31] Michel Ledoux and Michel Talagrand. Probability in Banach Spaces. Springer, 1991.

- [32] Jaeho Lee and Maxim Raginsky. Minimax statistical learning with Wasserstein distances. In Advances in Neural Information Processing Systems, 2018.

- [33] Tian Li, Ahmad Beirami, Maziar Sanjavi, and Virginia Smith. Tilted empirical risk minimization. arXiv preprint 2007.01162, 2020.

- [34] Ilya Loshchilov and Frank Hutter. Decoupled weight decay regularization. In International Conference on Learning Representations, 2019.

- [35] Shie Mannor and John N. Tsitsiklis. Algorithmic aspects of mean-variance optimization in Markov decision processes. European Journal of Operational Research, 2013.

- [36] Harry M. Markowitz. Portfolio selection. The Journal of Finance, 1952.

- [37] Andreas Maurer and Massimiliano Pontil. Empirical Bernstein bounds and sample variance penalization. In Conference on Learning Theory, 2009.

- [38] Aditya K. Menon and Robert C. Williamson. The cost of fairness in binary classification. In Conference on Fairness, Accountability, and Transparency, 2018.

- [39] Takayuki Osogami. Robustness and risk-sensitivity in Markov decision processes. In Advances in Neural Information Processing Systems, 2012.

- [40] Mengye Ren, Wenyuan Zeng, Bin Yang, and Raquel Urtasun. Learning to reweight examples for robust deep learning. In Proceedings of the International Conference on Machine Learning, 2018.

- [41] R. Tyrrell Rockafellar and Stanislav Uryasev. Conditional value-at-risk for general loss distributions. Journal of Banking and Finance, 2002.

- [42] Cynthia Rudin. Stop explaining black box machine learning models for high stakes decisions and use interpretable models instead. Nature Machine Intelligence, 2019.

- [43] Amir Sani, Alessandro Lazaric, and Rémi Munos. Risk-aversion in multi-armed bandits. In Advances in Neural Information Processing Systems, 2012.

- [44] Bernard Schölkopf, Alex J. Smola, Robert C. Williamson, and Peter L. Bartlett. New support vector algorithms. Neural Computation, 2000.

- [45] Shai Shalev-Shwartz and Shai Ben-David. Understanding Machine Learning: From Theory to Algorithms. Cambridge University Press, 2014.

- [46] Jun Shu, Qi Xie, Lixuan Yi, Qian Zhao, Sanping Zhou, Zongben Xu, and Deyu Meng. Meta-weight-net: Learning an explicit mapping for sample weighting. In Advances in Neural Information Processing Systems, 2019.

- [47] Matthew J. Sobel. The variance of discounted Markov decision processes. Journal of Applied Probability, 1982.

- [48] Tasuku Soma and Yuichi Yoshida. Statistical learning with conditional value at risk. arXiv preprint 2002.05826, 2020.

- [49] Akiko Takeda and Takafumi Kanamori. A robust approach based on conditional value-at-risk measure to statistical learning problems. European Journal of Operational Research, 2009.

- [50] Aviv Tamar, Yonatan Glassner, and Shie Mannor. Optimizing the CVaR via sampling. In Proceedings of AAAI Conference on Artificial Intelligence, 2015.

- [51] Sattar Vakili, Keqin Liu, and Qing Zhao. Deterministic sequencing of exploration and exploitation for multi-armed bandit problems. IEEE Journal of Selected Topics in Signal Processing, 2013.

- [52] John von Neumann and Oskar Morgenstern. Theory of Games and Economic Behavior. Princeton University Press, 1947.

- [53] Robert C. Williamson and Aditya K. Menon. Fairness risk measures. In Proceedings of the International Conference on Machine Learning, 2019.

- [54] Chiyuan Zhang, Samy Bengio, Moritz Hardt, Benjamin Recht, and Oriol Vinyals. Understanding deep learning requires rethinking generalization. In International Conference on Learning Representations, 2017.

Appendix A Omitted proofs

A.1 Proof of Proposition 1

We begin by plugging the disutility function to the definition of the inverted OCE risk (Definition 2) to get

| (27) |

While the optimum-achieving may not be unique, we observe that achieves the optimum. To see this, first observe that increasing (non-strictly) increases the first term in the curly bracket () and decreases the second term (). By increasing by , the second term decreases at least by , since at least terms among are nonnegative. Likewise, by decreasing by , the increment in the second term is no bigger than .

Plugging in , we get what we want.

A.2 Proof of Proposition 2

We look at each inverted OCE separately.

1. Inverted entropic risk: From the elementary calculus, we know that

| (28) |

The corresponding influence function is then given as

| (29) | ||||

| (30) | ||||

| (31) |

2. Inverted mean-variance: From the elementary calculus, we know that

| (32) |

The corresponding influence function is then given as

| (33) | ||||

| (34) |

3. Inverted CVaR: Using the argument similar to [41], we get that

| (35) |

We denote the -contaminated distribution by . Then, the corresponding influence function can be written as

| (36) |

By adding and subtracting , we can rewrite as

| (37) |

Now, notice that the limiting term is whenever whenever does not have a point mass around . Indeed, is zero with probability , and with probability . Taking the limit, remaining terms cancel out.

A.3 Proof of Lemma 3

We begin by giving the following technical lemma.

Lemma 9.

Suppose that satisfies almost surely for . Then, we have

| (38) | ||||

| (39) |

Proof.

See Section A.9. ∎

In other word, the search space of the variational parameter appearing in the definition of OCE risk (3) can be constrained to a finite length interval, given that the random variable is also bounded. Using this result, we can take a closer look at the one-sided deviation; for any , we have

| (40) | ||||

| (41) |

where the inequality holds by selecting the first to be identical to the second . Taking supremum over on both sides, we get

| (42) |

where is a product hypothesis space constructed upon and . To bound the (one-sided) uniform deviation, we first control its expectation via Rademacher averages. As holds by definition, the contraction principle (see, e.g., [31, Eq. 4.20]) gives

| (43) |

Now, the Rademacher average of can be bounded as

| (44) | ||||

| (45) | ||||

| (46) | ||||

| (47) |

where the last line follows from the Jensen’s inequality . Combining (47) with (43), we get

| (48) |

Combining with the McDiarmid’s inequality to control the residual term, we have

| (49) | |||

| (50) |

The other direction can be derived similarly. Using the union bound, we get what we want.

A.4 Proof of Theorem 4

The claim is a direct consequence of Lemma 3. Indeed, we can proceed as

| (53) |

where the nonpositivity of second term follows from the definition of . The remaining terms can be bounded via Lemma 3 to get the claimed result.

The proof for can be done equivalently, by

| (54) |

A.5 Proof of Proposition 5

To get , plug in to Definition 2 to observe that

| (55) |

where the second inequality holds as is a nondecreasing function.

To get , we first observe that holds for all , as is a convex function with . Thus, we get

| (56) |

To get , use again that to proceed as

| (57) |

To get , observe that

| (58) |

where for the first inequality we plugged in the special case .

A.6 Proof of Lemma 6

We first prove the bounds for . To get the lower bound, we start from Lemma 9 and proceed as

| (59) | ||||

| (60) | ||||

| (61) |

where the inequality holds by the definition of . To get the upper bound, plug in to the variational definition (3) and observe that

| (62) | ||||

| (63) | ||||

| (64) | ||||

| (65) |

where the last line holds by the Jensen’s inequality.

The bounds for can be proved similarly. For the lower bound, we plug in to get

| (66) | ||||

| (67) | ||||

| (68) |

For the upper bound, we use the definition of to get

| (69) | ||||

| (70) | ||||

| (71) |

A.7 Proof of Theorem 7

To prove the first claim, we start with Lemma 6 to proceed as

| (72) | ||||

| (73) | ||||

| (74) | ||||

| (75) | ||||

| (76) |

As is a fixed object independent of the samples (for given ), Theorem 10 of [37] implies

| (77) |

Combining with standard symmetrization bounds on uniform deviation (see, e.g., [45]) with excess risk probability , we get the first claim.

The second claim can be proved similarly, but without invoking the concentration of sample variance. We proceed as follows.

| (78) | ||||

| (79) | ||||

| (80) | ||||

| (81) | ||||

| (82) |

Plugging in the standard Rademacher average bound, we get what we want.

A.8 Proof of Proposition 8

We begin by observing that for CVaR reduces to the binomial tail probability.

Lemma 10.

Let be the excess risk probability of empirical CVaR minimization for some . Then, we have , where .

Proof.

See Section A.10. ∎

To get the upper bound, observe that Lemma 10 can also be stated in the following form: the excess risk probability of the empirical CVaR minimization is

| (83) |

Then, the upper bound follows from the Hoeffding’s inequality.

For the lower bound, we bound the binomial tail from below by the largest term in the binomial sum. Using the Stirling’s approximation, we have for any ,

| (84) |

where denotes the binary Kullback-Leibler (KL) divergence. To complete the lower bound, we note the quadratic upper and lower bound on the binary KL divergence.

Lemma 11.

For any , we have . If we further assume , then we also have .

Proof.

See Section A.11. ∎

A.9 Proof of Lemma 9

We first prove Eq. 38. For simplicity, we use the shorthand notation

| (88) |

Note that is a continuous function, as the convexity of implies the convexity (and continuity) of . We prove the claim by contradiction; for any (supposedly optimal) , we show that there exists a corresponding such that .

Case ().

We show that for any . Indeed, by considering a negative random variable lying in the interval , we get

| (89) |

where the inequality holds because is a convex function having as a subgradient at .

Case ().

Similarly, we show for any . By considering a positive random variable , we get

| (90) |

where the inequality follows from the fact that is a convex function having as a subgradient at .

With being a continuous function and being a compact search space, we can replace the infimum by minimum. Eq. 39 can be proved in a similar manner.

A.10 Proof of Lemma 10

We begin by introducing the shorthand notation . From the setup, we know that . From Lemma 9, we can proceed as

| (91) | ||||

| (92) | ||||

| (93) |

Thus, holds if and only if .

A.11 Proof of Lemma 11

To get the lower bound, we view as a function of and use the Taylor’s theorem. The partial derivatives of the binary KL divergence with respect to are as follows.

| (94) |

Note that as , the second derivative is bounded from below by . Evaluating at , we have for some in the interval between and ,

| (95) |

To get the upper bound, we view as a function of and use the Taylor’s theorem again. The partial derivatives with respect to are

| (96) |

Given that , we know that the second derivative is uniformly upper bounded as

| (97) |

Evaluating at in the same manner as Eq. 95, we get the upper bound.

Appendix B Additional plots and other experimental details

We now provide extra experimental details that are not given in Section 4. Unless stated otherwise, we follow PyTorch default parameters. One may also find our (primitive) PyTorch-based implementation at the following URL: https://github.com/jaeho-lee/oce.

Dataset.

We use CIFAR-10 image classification dataset [29], normalized using the constants . We used random cropping (with padding of ) and random horizontal flipping for augmentation.

Optimization.

We use mini-batch gradient descent, i.e. sampling without replacement until every samples are drawn.

Appendix C Related work

Here, we give a slightly extended overview of the related work, in addition to what has been already introduced in the main text. In particular, we focus on the following three topics: optimization of OCE risks, comparisons with another risk-sensitivity framework, and connections to the algorithmic fairness literature.

Optimization of OCE. The OCE risk measures belong to a wider class of convex risk measures [18], which was originally proposed as a relaxation of the notion of coherent risk measures [3]. Under classic setups equipped with convexity assumptions on the loss function, the fact that “the composite function of convex functions are also convex” enables one to use standard optimization techniques developed for the expected loss. In modern machine learning applications which accompanies batch-based nonconvex optimization, the optimization can be done with some additional tricks. In [14], the authors propose to use DPP-based techniques for a more accurate estimation of the conditional value-at-risk. In [33], the authors give a stochastic optimization algorithm which often outperforms the batch-based version.

Comparison with rank-based measures. The utility-theoretic framework of OCE risks (and their inverses) is complementary to another class of risk measures revolving around the quantile function of the loss population. Known as spectral risk measures [2] in the financial mathematics and as L-statistics (see, e.g., [26, 27]) in the statistics literature, the quantile-based approach focuses on the risk measures that can be written as

| (98) |

for some weighting function (satisfying varying degree of assumptions). While two frameworks share some commonalities (e.g., having the conditional value-at-risk as its special case), there is a subtle yet important difference: the utility-based framework allows the relative weight of the samples to depend on the loss value itself, while the quantile-based framework does not. In this sense, the OCE framework can be viewed as having a little more room for adaptation with respect to different distributions of loss. On the other hand, it is also true that the quantile-based framework covers some risk measures that are not describable via the OCE framework, e.g., risk measures trimming both samples with small and large loss values. An in-depth comparative study on the theoretical and empirical benefits of two frameworks may be an interesting direction of future study.

Connections to algorithmic fairness. In [53], Williamson and Menon give an axiomatic definition of fairness risk measures for group fairness. In particular, they argue that the fairness risk measure should be convex, positively homogeneous, monotonic, lower semi-continuous, translation invariant, averse, and law invariant. From the axioms, the authors propose a fairness-aware objective based on minimizing the conditional value-at-risk, which is a special case of the OCE risk with the disutility function . Indeed, the conditional value-at-risk can be simply viewed as a solution of

| (99) |

(given that has a density on ), which is the worst-case subgroup error over all subgroups of fraction . In another concurrent work [33], Li et al. also empirically observe that minimizing the entropic risk (instead of the expected loss) mitigates the disparate impact of the learned hypothesis on subgroups.