Suffocating Fire Sales

Abstract

Fire sales are among the major drivers of market instability in modern financial systems. Due to iterated distressed selling and the associated price impact, initial shocks to some institutions can be amplified dramatically through the network induced by portfolio overlaps. In this paper, we develop a mathematical framework that allows us to investigate central characteristics that drive or hinder the propagation of distress. We investigate single systems as well as ensembles of systems that are alike, where similarity is measured in terms of the empirical distribution of all defining properties of a system. This asymptotic approach ensures a great deal of robustness to statistical uncertainty and temporal fluctuations. A characterization of those systems that are resilient to small shocks emerges, and we provide criteria that regulators might exploit in order to assess the stability of a financial system. We illustrate the application of these criteria for some exemplary configurations in the context of capital requirements and test the applicability of our results for systems of moderate size by Monte Carlo simulations.

1 Introduction

Modern financial systems exhibit an inevitably complex structure of dependencies. This complexity is visible on multiple levels, including for example the intricate distribution of corporate obligations and also the – sometimes significant – overlap in the asset holdings of the participating institutions. This interlocking and pervasive structures can make the system fragile to possible initial local shock events. The problem of modeling, understanding, and managing this notion of systemic risk has been an important research topic, and it has become particularly prominent after the strike of the global financial crisis in the years 2007/08.

One of the first quantitative papers to address systematically the effect of – what they termed – cyclical dependencies among the market participants was the seminal work [21]. They considered default contagion, that is, the successive default on liabilities across financial institutions, and showed, among other results, that under mild assumptions a unique clearing vector exists that clears the obligations of all members. From today’s viewpoint, however, it is well understood that there are various other important channels of contagion. For instance, in the book [31], Asset Correlation, Default Contagion, Liquidity Contagion and Asset Fire Sales are listed as the four main channels of direct and indirect default propagation.

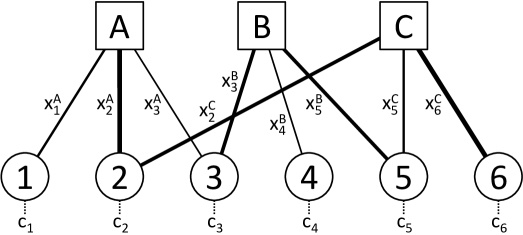

Here we focus on fire sales, which is widely accepted as one of the main drivers of market instability ([22],[33],[17],[10],[24]). A recent example of a fire sales event is the selloff that followed the decline in the stock price of ViacomCBS on March 24, 2021. It was particularly amplified due to the leveraged bets by the hedge fund Archegos Capital, which as a result of the price drop was forced to unwind its positions in ViacomCBS.111https://www.reuters.com/article/usa-markets-blocktrades-timeline-idUSL1N2LS332 The underlying dynamics that we consider are defined abstractly as follows. Consider a system of institutions that are invested in certain assets, where each institution is equipped with some initial capital (equity) and holds some number of shares of an asset (see also Figure 1). The portfolios of the institutions may therefore overlap, and the dependencies are quantified by the collection of the ’s. As a reaction to some initial shock event, one or more of the institutions sell according to an individual strategy a non-negligible number of shares of their assets. These sales may cause a decline of the assets’ share prices and all investors in the assets that were sold incur losses in their portfolio values. This may start another round of asset sales, possibly on an extended set of assets, again reducing share prices and so on. By this iterative process the initial stress is propagated through the system and can be amplified considerably. In particular, institutions that were spared from the initial shock can get into trouble, if their portfolios overlap with those of distressed investors.

Literature Various approaches have been developed to model and understand the impact of fire sales. The works [14, 37, 39, 3, 13] extend the classical setting from [21] for given financial networks so that various aspects of fire sales are incorporated. [9] use a branching process approximation to model fire sales, and they find that the system is stable when certain market parameters are below a critical value that they specify. In a two-period model [28] show how contagion effects propagate across the banking sector. [32] study the benefits and disadvantages of overlapping portfolios not only from the perspective of single institutions, but also for the market as a whole. An important consequence of their model is that for some specifications a divergence between private and social welfare may arise. Alike and related considerations are also made in [5], where a small number of assets is considered, and in [38], where using a microfounded model it is shown that the risk of joint liquidation motivates institutions to create heterogeneous portfolios. A related setting for reinsurance markets with overlapping insured objects is analyzed by [34]. [17] analyze the impact of fire sales on asset price dynamics and correlation in continuous time. [23] propose a continuous time model for price-mediated contagion and derive conditions based on the risk-weights of assets that ensure that a solution to the model exists. In [18], extending and building upon work of [33], they further describe the impact of the liquidation of large portfolios on the covariance structure of asset returns and provide a quantitative explanation for spikes in volatility and correlations observed.

Apart from the theoretical work there is a significant amount of empirical studies that consider the effect of fire sales, develop viable models and propose measures to capture quantitatively their effects. In [29] the topology of the network of common asset holdings is analyzed and [7] proposes a network representation to quantify the interrelations induced by common asset holdings. [15] develops a stress testing framework for fire sales that is extended by indices of centrality for institutions participating in a fire sales process in [16]. There are several works that develop exposure- and market-based measures to depict the effect of fire sales. For example, [27] uses the scalar product of two portfolios’ weights, and [35] uses the so-called absorption ratio, the degree of variation induced by the first principal components of asset returns, to measure dependence between different sources of risk in a portfolio. Additional measures are constructed from a statistical analysis of the equity returns of institutions, as in [1, 8, 2].

Our Contribution We study a fairly general fire sales process here that accounts for the actual losses incurred in each round, which makes the model complex and its dynamics quite involved. To analyze our model we resort to a simpler related auxiliary model that is based on one clearing price for all shares. The final outcome of this simpler process can then be determined by a fixed-point equation. The dimensionality of this fixed-point equation only depends on the number of assets and not on the size of the financial system. This is in contrast to previous works ([14, 37, 39]) in which the clearing vector for a financial system has been derived by solving a fixed-point equation with dimensionality equal to the size of the system. The auxiliary process only serves as a tool for us and we establish coupling results that tie the auxiliary process to the original process in a novel way that provides both, lower and upper bounds for the outcome of the original process. These results enable us to determine the final state of the system at the end of the original fire sales process.

However, we are also interested in a more fundamental question: what are the important underlying structures that propel the process of fire sales? In other words, which system characteristics favor the emergence of large fire sales cascades, and which prohibit them? In order to address these questions, we establish quite involved continuity properties for the fixed-point of the auxiliary system with respect to changes in the empirical distribution of the system. Facilitating these results, instead of restricting our attention only to a single system, we can then consider an ensemble of systems that share common structural characteristics. By reducing any particular system to its bare bone characteristics, we obtain robustness and flexibility. Moderate uncertainties of the precise system configuration are absorbed and we can study large financial systems (, the number of institutions) given that their empirical distribution converges. This asymptotic approach then allows us to detect unstable system configurations and provides a parameter-free notion of resilience of a given system. This parameter free notion of (non)-resilience inherently captures a large system phenomenon, depending only on the tails of the system’s empirical distribution. It thus focuses on fire sales in large systems due to its asymptotic nature. Establishing these results is possible again by continuity arguments where we study whether the fixed-point is converging to zero as the initial shock becomes small (resilient system). If the system is not resilient on the contrary, small shocks may have disastrous outcome.

More than a mere description of the fire sales process, a central objective can then be to devise measures to prevent disastrous fire sales cascades. We show for a stylized system how our mathematical framework may be used to derive explicit capital requirements that ensure the stability of the system. For this example setting, it turns out that for each institution the capital requirement is solely based on its own asset holdings, thus ensuring full transparency and fairness, which is an essential question to address when determining the systemic riskiness of the involved institutions. As a further application, our results allow us to quantify the effects of portfolio diversification and similarity. Similarly as in ([32, 5, 38, 11]) we find that diversification, when it comes at the cost of portfolio similarity, leads to larger fire sales cascades. However, heterogeneous, diversified portfolios are favorable from a systemic risk perspective. We also find that for well-capitalized systems, diversification is beneficial, even if it comes at the cost of portfolio similarity. We hope that some of these and additional findings that can be derived from our model will contribute to ongoing discussions on financial market regulation.

Currently the main burden to apply our results might be the availability of data. Although we show in simulations that the different regimes (resilience/non-resilience) are already visible for systems of moderate size (), current regulatory stress tests are applied to only the most systemically important banks. In fact, the 2021 stress test of the European Banking Authority (EBA) is only based on 50 banks from EU and EEA countries.222https://www.eba.europa.eu/risk-analysis-and-data/eu-wide-stress-testing Applying our asymptotic results to such a small set of banks will most likely not provide useful information about the resilience of the actual system. In this regard our method calls for more data collection and an analysis on a larger data set, which might become available at some point. In fact, the financial systems of many economies are quite large. For instance, Germany alone is home to more than banks. Adding other financial institutions and possibly even assessing the risk on a European level, one easily reaches a size of the financial system for which the asymptotic effects become relevant, as shown in the simulations. Without the availability of larger data sets, we think that one can still obtain some useful general structural conclusions from the results, as shown in some first examples.

Outline In Section 2 we present our model of fire sales, we introduce the aforementioned notion of resilience and outline our main results. Section 3 deals with the analysis of the simpler auxiliary model. Then, in Section 4 we build the bridge between the two models, and in particular we derive abstract and explicit criteria that guarantee resilience for the original fire sales system. Section 5 deals with applications of the developed theory and provides simulations, as outlined in the previous paragraph. The paper closes with a conclusion that summarizes future research directions, in particular the problem of applying our results to systems of moderate size. All proofs that are omitted in the main part and some generalized results can be found in Section 7.

2 Model, Resilience and Overview of the Results

In this section we present our model of fire sales and outline our results.

2.1 The Fire Sales Process

Model Parameters We consider a financial system consisting of institutions that can invest in different (not perfectly liquid) assets or asset classes. To each institution we assign the number of shares that institution holds of asset . Here, by we denote the set of positive real numbers including zero. See Figure 1 for an illustration. Further, we denote by the initial capital of institution . This could for example be the equity for a leveraged institutions, such as a bank, or the portfolio value for an institution that exclusively invests in assets, such as a fund. We assume that the capitals incur exogenous losses due to some shock event. In the case of a market crash for instance, it could be that , where denotes the initial price of one share of asset and is the relative price shock on the asset. Furthermore, let the empirical distribution of the institutions’ parameters be denoted by

| (2.1) |

and let in the following be a random vector with distribution .

Asset Sales We assume that due to the exogenous losses some of the institutions are forced to liquidate parts of their asset holdings in order to comply with regulatory or market-imposed constraints (e. g. leverage constraints), self-imposed risk preferences and policies to adjust the portfolio size, or to react to investor redemptions. These sales are described by a non-decreasing function such that each institution incurring a loss of sells of its shares of asset . The fraction describes the relative loss of institution measured against its initial equity. It is hence sensible to assume that

If at default of an institution the whole portfolio is to be liquidated, then . In general, however, the remaining assets at default may be frozen by the insolvency administrator and only be sold to the market on a longer time scale. In this case, . Our assumptions on are rather mild and allow for a flexible description of various scenarios. A simple example is given by , which describes complete liquidation of the portfolio at default (if the institution is leveraged) resp. dissolution. More realistic examples, as for instance derived from leverage constraints, can be found in Section 7.3.

Some remarks are in order here. First, to simplify the exposition and the notation in the main part, we restrict our analysis to continuous , and we refer to Section 7, where we provide proofs of all our results in full generality. Second, it is possible to consider a more general model in which we choose different sales functions for the assets to account for different asset specific aspects. It is then possible to replace the scalar function by the diagonal matrix in all forthcoming considerations. Further, we may partition the set of institutions into different types (banks, insurance companies, hedge funds, …) and choose different or for each type. Finally, our proofs in this article also work for arguments (of ) other than (where are the losses), but for the sake of simplicity we stick to this particular form.

Price Impact Since the assets are not perfectly liquid (the limit order book has finite depth), the sales of shares triggered by the exogenous shock cause prices to decline. This on the other hand causes further losses for all the institutions invested in the assets due to mark-to-market accounting. We model the price loss of asset by a continuous function which is non-decreasing in each coordinate. That is, if and shares of asset have been sold in total, then we assume that the price of drops by .

Note the relative parametrization with the number of institutions , where we assumed that (instead of ) shares of asset are sold. For fixed this is arbitrary; however, in due course we will consider an ensemble of systems (see Assumption 2.1 below), and then this parametrization will turn out to be rather convenient to state our results. In particular, it reflects the fact that the market depth scales with the number of institutions involved.

Fire Sales Triggered by some exogenous event the institutions start selling a portion of their assets and drive down the prices. Due to mark-to-market effects, this means that institutions experience further losses and are forced into further sales. This iterative process continues until the system stabilizes and no further sales, losses and price changes occur. More specifically, let us denote by the vector of cumulatively sold shares at the beginning of round , that is, the number of actually sold shares in round is and, obviously, . Moreover, for each bank and any round let

-

•

be the number of shares that holds at the beginning of round ;

-

•

be the total loss of accumulated until the beginning of round .

From these definitions we readily obtain that the number of shares held at the beginning of round is

| (2.2) |

and the total number of sold shares is given by

| (2.3) |

Moreover, from the specification of the fires sales process we obtain that

| (2.4) |

since at the beginning of round there remain shares which are affected with a price impact of , and in any preceding round the number of sold shares is , sold with a loss of . We remark that the realized price for units sold during round , which is is based on the losses triggered by , the total cumulative assets sold up to (and including) round . The losses due to the asset sales in round itself are not endogenized for this round.

By induction is non-decreasing componentwise and bounded by . The limit

| (2.5) |

that is, the vector of finally sold shares, exists. In addition to we will also be interested in the number of defaulted institutions given by and hence

| (2.6) |

The set provides additional information about the vulnerability of the financial system and the impact of fire sales on leveraged institutions such as banks or hedge funds. This completes the description of the model for fire sales that we study here. We would like to mention that within the already existing work, the model used in [28] is possibly closest to the setup presented above. In [28] the authors consider a fire sales process in a financial system of institutions that try to maintain a fixed leverage ratio. In contrast to our setting, the price impact is assumed to be linear and the asset sales in one asset do not have a direct effect on the price of other assets. In addition, the authors focus on first order effects while we are particularly interested in higher order effects.

2.2 Ensembles of Systems

Up to now we have described the fire sales process in any specific (finite) system. Our aim is, however, to understand qualitatively the characteristics of a system that promotes or hinders the spread of fire sales. As portrayed in the introduction, in the following we thus consider an ensemble of systems that are similar in the sense that they all share some (observed) statistical characteristics. This similarity is measured in terms of the most natural parameters, namely the joint empirical distribution (2.1) of the asset holdings, the capital/equity, and the initial losses. In particular, we assume that we have a collection of systems with a varying number of institutions with the property that the sequence stabilizes, i.e., has a limit. Additionally, we assume convergence of the average asset holdings to a finite value; this is a standard assumption avoiding condensation of the distribution of the asset holdings.

Assumption 2.1.

Let be a fixed number of assets. For each consider a system with institutions and with asset holdings , capitals , and exogenous losses . Let be the empirical distribution function of these parameters for (as in (2.1)) and let

Then assume the following.

-

(a)

Convergence in distribution: There is a distribution function such that as , at all continuity points of .

-

(b)

Convergence of means: Let . Then as ,

An ensemble of systems satisfying Assumption 2.1 will be called an -system with initial shock in the sequel. A particular and probably the most relevant example is as follows. Suppose that a distribution is specified, possibly obtained by an empirical analysis of a real system. Then, for each we construct a system by assigning to each institution independently asset holdings, capital and losses sampled from . By the strong law of large numbers, with probability 1, the sequence of systems that we obtain satisfies Assumption 2.1. As in the (deterministic) model our aim is to describe in this broader setting the final state of the system. As institutions without any asset holdings play no role in the process and can be removed, we shall assume that .

In order to simplify the presentation in the main part of this article we assume that the sales function is strictly increasing around 0. It can be waived and the results in full generality are presented the Section 7.1 and proved in Section 7.2.

Assumption 2.2.

The sales function is continuous and strictly increasing in a neighbourhood of .

(Non-)Resilience In this part of the section we approach the heart of the matter and develop a notion of how resilient or non-resilient a given -system is with respect to fire sales, triggered by some initial shock . Note that all information about the system itself comes from , whereas an initial shock is specified by the random variable . We can then consider shocks of different magnitudes on the same, crucially, a priori unshocked system. From a regulator’s perspective, for example, a desirable property of an -system is the ability to absorb small local shocks without larger parts of the system being harmed. In our model we can even vary the statistical properties of arbitrarily. The following way of defining resilience thus emerges naturally: we let the shock ‘become small’ in the sense that , and we call the system resilient if the asymptotic number of sold shares (that now – explicitly – depends on ) also tends to . We would like to stress that we do not pose any restrictions on the joint distribution of . In particular, we do not assume that the shock is independent of .

Definition 2.3 (Resilience).

An -system is said to be resilient, if for any there exists such that for all with it holds for all .

Our definition of resilience is in terms of the final number of sold shares. There are also other options, for example instead we could have based it on the final fraction of institutions that defaulted, which is the ‘standard’ choice in the default contagion literature, see i.e. [19, 20]. However, we selected the final number of sold shares, as the economic cost of fire sales can be large even when the number of defaults is rather small. In any case, all our results can easily be adapted to a resilience condition based on the default fraction.

We now move on to define non-resilient systems. In complete analogy to the previous considerations, we call a financial system non-resilient if the fraction of eventually sold shares is lower bounded by some positive constant which – crucially – does not dependent on the specification of the shock , as long as this is positive. In order to ensure that the process starts at all, the shock has to affect some banks, so we require to be such that .

Definition 2.4 (Non-Resilience).

An -system is non-resilient, if there exists and an asset such that for any initial shock with .

The definition of non-resilience is rather strong, as we only require , and apart from that, it is not really the complement of the notion of resilience in Definition 2.3. Rather surprisingly, we will see later that under Assumption 2.2 there is essentially no gap between Definition 2.3 and Definition 2.4, that is, in most cases a system is either resilient or non-resilient. However, when is not strictly increasing, the situation may be different. This is a particularly interesting and important setting, as it describes a situation where shock driven asset sales only occur if some institutions have been affected to some larger extent. It thus ensures that minor losses (e.g. resulting from mark-to-market accounting of naturally volatile assets) and major shocks as the default of Lehman Brothers in 2008 are treated differently. Since in Section 7 we consider a sales function that is not strictly increasing close to , we provide the required notion of weak non-resilience here.

Definition 2.5 (Weak Non-Resilience).

An -system is weakly non-resilient, if it is not resilient, that is there exists and an asset such that for every there exists an initial shock such that but .

We will later see that, with the exception of some pathological cases, exists for all and thus , which shows that Definition 2.5 complements Definition 2.3.

Overview of the Results Having defined the notions of (non-)resilience we can give an informal overview of our main findings. Given an -system with initial shock we first derive explicit bounds for the final number of sold shares , (Section 3.2), and for the default fraction in Section 7.2). To this end, we resort to a different auxiliary process described in the next section, which makes an important simplification to the rather involved fire-sales process given by (2.2)–(2.6): instead of considering the actual losses incurred in some round , we overestimate them and replace them by the simple upper bound , where is the vector of the total number of sold shares in the first rounds. The advantage is that this auxiliary process can be handled analytically by solving a fixed-point equation. We then derive continuity properties of the fixed-point as a function of the system’s parameters, which allow us to describe the auxiliary process for an ensemble of systems by a collection of functions . These functions essentially describe the evolution of the price of the corresponding asset during the execution of the process. The joint zero of these functions coincides with the final number of sold shares in the auxiliary process. The disadvantage of turning to the auxiliary process, however, is that it is not clear how much this simplification distorts from the behavior of the original process. Here we provide an explicit connection of the two processes: we manage to ‘sandwich’ the fire sales process between two carefully crafted auxiliary processes, so that (non-)resilience properties are not or minimally affected (see Section 4.1).

With this coupling at hand we manage to derive explicit (non-)resilience criteria for -systems. As it turns out (see Section 4.1 and 4.2), the resilience of such a system is linked to the behavior of the functions near zero. We are then able to derive qualitative criteria that depend on the parameters of system – , – and of the process – the sales function and the price impact – only and characterize resilience. For example for a system with one asset (), linear price impact and such that , we show that if , then the system is non-resilient: the capital is too small in direct comparison to the asset holdings, and selling begins immediately as a response to a price drop. On the other hand, if and , then the system is resilient. We also consider cases in which and ; there we show that the actual interplay between and (price drop) determines if the system is resilient or not. Several results of this kind and their interpretations are presented in Section 4.2.

3 The Auxiliary Model

3.1 The Auxiliary Process

As already described previously, the aim of this section is to formulate an auxiliary process that will turn out useful for an analytic treatment of the fire sales process defined by (2.2)–(2.6). Note that the essence of the fire sales process lies in Equation (2.4): the behavior is rather complex, as we need to keep track of the asset sales in all rounds. In order to make the analysis tractable, we will substitute (2.4) in the auxiliary process as follows: we forget the actual prices at which assets were sold in previous rounds, and calculate the loss by using the price impact in the current round – which is of course at least as large as the impact in previous rounds. More specifically, it holds that

| (3.1) |

In the auxiliary fire sales process we thus replace the actual loss by this simple upper bound.

We now provide a description of the final state of the system after this auxiliary fire sales process is completed; in particular, we are interested in the vector of the number of finally sold shares divided by and the final price impact on any asset .

| Fire Sales Process | Auxiliary Process | |

|---|---|---|

| vector of finally sold shares | ||

| divided by | ||

| vector of cumulatively sold shares | ||

| in rounds |

In order to describe we again consider the process in rounds, where in each round institutions react to the price changes from the previous round. Denote by the vector of cumulatively sold shares in round . We readily obtain

| (3.2) |

Similarly, in round

| (3.3) |

Thus, by induction is non-decreasing componentwise and bounded by . The limit – the vector of finally sold shares in the auxiliary process – exists.

Table 2 contrasts our notation for the fire sales process and the auxiliary process which will be used throughout the rest of the paper. We want to remind the reader that we work with a given financial system at this point and that the distribution of is chosen such that we can rewrite the deterministic sums appearing in (3.2) and (3.3) in terms of expectations. This turns out to be convenient later when we consider ensembles satisfying Assumption 2.1, as it avoids long expressions involving multivariate integrals.

In contrast to the original fire sales process, it turns out that for the auxiliary process, the number of sold shares can be derived by solving a rather simple equation.

Proposition 3.1.

Consider the auxiliary fire sales process as described above. Then , the number of sold shares divided by at the end of the auxiliary process, is the smallest (componentwise) solution of

| (3.4) |

Proof.

By the Knaster-Tarski theorem there exists a smallest fixed point . Clearly, . Hence assume inductively that for . Then

| (3.5) |

by monotonicity of , and hence . By definition of it thus holds that . ∎

Further, given , we readily obtain that under the auxiliary process the set of finally defaulted institutions is and hence

| (3.6) |

Note that we slightly ‘overload’ the notation, as we use for both the fires sales and the auxiliary process. Since it will be always clear from the context which processes is studied, this should cause no confusion.

Let us close this section with a remark about the case of non-continuous sales function . The following example shows that also in this case it may be possible to determine the final state of the system by the smallest solution of (3.4). Consider , that is, institutions sell their portfolio as they go bankrupt. Then only if in round at least one institution defaults that was solvent in round . Since there are only institutions, the fire sales process stops after at most rounds and the vector of finally sold shares divided by solves (3.4). Again by (3.5) we then obtain is the smallest solution of (3.4). By a similar reasoning we derive more generally for any sales function with finitely many discontinuities that . The case of arbitrary non-decreasing sales function is more difficult and treated in Section 7.1.

3.2 The Auxiliary Process as

Proposition 3.1 describes the final state of any (finite) system when we consider the auxiliary process. Here we extend our considerations to an ensemble of systems. We are given an -system with initial shock , that is, an ensemble of systems, where for each a system with institutions and assets is specified by sequences of asset holdings, capitals and exogenous losses with joint distribution . We also assume that the system satisfies Assumption 2.1, that is, the distribution of converges to that of and the asset holdings are in .

Applying Proposition 3.1 to each one of the systems in the ensemble, we obtain that for each , the number of sold shares divided by at the end of the auxiliary process is the smallest solution of (3.4). Since it is thus natural to believe that for large , the number of finally sold shares is close to the smallest (componentwise) solution of the ‘limiting equation’

| (3.7) |

As it will turn out, except for few pathological situations, this intuition is indeed correct and motivates the following definitions. Let

| (3.8) |

Further, let

| (3.9) |

be the subset where all of the functions , , are non-negative. Let be the smallest joint root (which always exists by the Knaster-Tarski theorem) of the functions . While the necessity of Assumption 2.1 is obvious, it is surprising that in most cases it is actually also sufficient to ensure that

| (3.10) |

Finally, in analogy to (3.6) we can therefore expect for the ensemble that the final fraction of defaulted institutions in the auxiliary model is given by

| (3.11) |

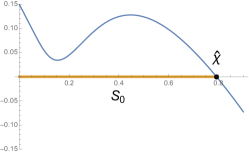

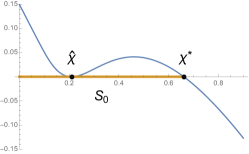

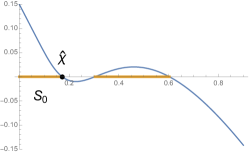

To illustrate under which conditions the previous statements are true and the intuition is right, let us look at an instructive example with one asset only (). This is a carefully crafted ‘toy example’ that is unlikely to model a real system, but it will reveal the important characteristics that determine the underlying behavior.

Example 3.2.

Consider a system defined by

where is independent of and . See Figure 3 for an illustration of , and . There is the only root of and the set is the interval . The situation changes, however, as we vary the capital. See Figure 3 for the case of . Then consists of two disjoint intervals and has three roots. In fact, one can observe the splitting of and thus a discontinuity of at , see Figure 3. The situation in Figure 3 presents a rather special and pathological case. In fact, only in this very special case above heuristics fail and the situation becomes more complex than suggested in (3.10) and (3.11).

In order to formalize the special situation encountered in the previous example, let us denote by the largest connected subset of containing (clearly ). Further, let

| (3.12) |

Lemma 3.3.

There exists a smallest joint root of all functions , , with . Further, as defined above is a joint root of the functions , , and .

The special case from Figure 3 is then described by , and in all other cases . We shall henceforth term the former case as ‘pathological’, since we can only obtain it if we maliciously fine-tune the parameters of the system to provoke such a behavior. We do not expect such situations to occur or to be particularly relevant, and in all settings that we study here it holds that . Note that in previous literature on fire sales the question of uniqueness of the fixed-point has been studied ([21, 37, 3]). We do not require uniqueness of the fixed-point here and the situation is only a stability property of the (component-wise) first fixed-point.

Our first result provides in non-pathological cases (that is, when ) the asymptotic number of finally sold shares for the auxiliary process and in all other cases upper and lower bounds.

3.3 Resilience Criteria for the Auxiliary Process

In the previous section we derived results that allow us to determine the final default fraction in -systems caused by the auxiliary process and sparked by some exogenous shock . In this section we go one step further and investigate whether a given system in an initially unshocked state is likely to be resilient to small shocks or susceptible to fire sales.

Note that all information about an initial shock comes from the random variable , whereas the system itself is specified by . So we can easily consider shocks of different magnitude on the same a priori unshocked system. The unshocked system itself can then be described by the case . In the following, whenever we use the notation , , and , we always mean the quantities (3.8)-(3.12) from the previous section for the -system with initial shock , i. e. the unshocked system.

Remark 3.5.

For , in particular the smallest joint root is always given by , as . Instead (non-)resilience will be described in terms of below. While in the previous subsection for (shocked systems), we remarked that only in pathological cases, we will see in this subsection for that describes an important and non-pathological case. In fact, for , if is such that , then always .

We shall first provide resilience criteria for the auxiliary system.

Theorem 3.6.

For each there exists such that for all with the number of finally sold shares of each asset for the auxiliary process satisfy

We immediately obtain the following handy resilience criterion.

Corollary 3.7 (Resilience Criterion).

If , then the -system is resilient under the auxiliary process.

We now turn to non-resilience criteria and study the case . Consider for example a system with one asset, assuming differentiability of . Then whenever . (If on the contrary , then and the system is resilient by Corollary 3.7.)

In fact, assuming that there is no additional zero between and , one can show that the first zero of any shocked system is lower bounded by and thus Theorem 3.4 guarantees that as , implying non-resilience of the system.

Theorem 3.8.

Consider an -system such that and such that no with (coordinate-wise) is a joint root of the functions . Then the system is non-resilient under the auxiliary process, more specifically

where is the number of finally sold shares of asset .

The assumption that there is no joint root between and can be weakened and the conclusion of non-resilience is for example also true if we request that there are only finitely many roots between and , or that such roots are bounded away from , an observation we shall regularly use in proofs. Constructing such highly artificial examples, where the infimum of the set of roots is , would require an enormous fine-tuning of the system parameters (and enough malicious energy).

Let us finally remark here that Theorem 3.8 is not true without the assumption that is strictly increasing. This becomes clear by looking at the particular example of sales at default. Asset sales will only happen if some banks default initially, that is, ; a shock which is such that can not trigger any sales. In Theorem 7.5 we show, however, that for the system is always weakly non-resilient. This completes our analysis of (non-)resilience under the auxiliary process. We close the section with an (again artificial) example demonstrating the qualitative difference between resilient and non-resilient systems.

Example 3.9.

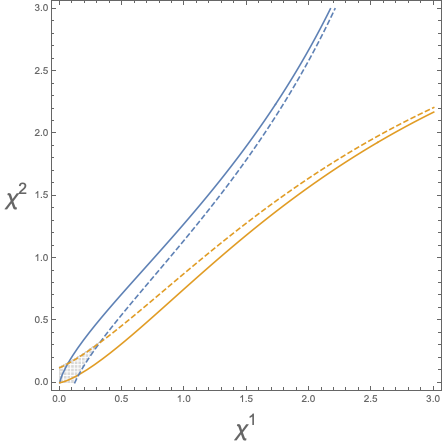

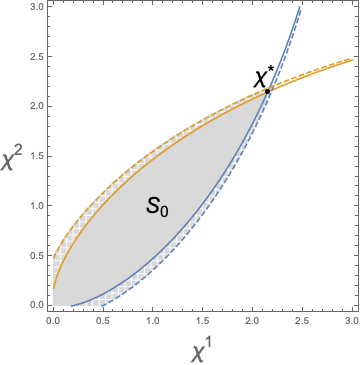

Let and let be a random variable with density . Consider a system with two assets () defined by

for some . Moreover, we consider a shock independent of with . See Figure 4 for an illustration of when and 4 for the case . The solid yellow and blue lines mark the zero sets of the functions and for the unshocked system. For (a) the system is resilient (, ) as the solid lines cross in , for (b) the system is non-resilient and is the area bounded by the solid lines, which cross first in . The dashed lines are the zero lines for the functions for the shocked system and the coordinates of their intersection mark the number of sold shares. With decreasing shock size, the dashed lines of the shocked system will approach the lines of the unshocked system. In the resilient case (a) this pushes the intersection of the dashed blue and yellow lines towards and only few shares are sold. In the non-resilient system (b), as the shock gets smaller, the intersection of the dashed lines is approaching and is thus lower bounded, no matter how small the shock is.

4 The Fire Sales Process

4.1 Bounding the Fire Sales Process with the Auxiliary Process

In this section we establish an explicit connection between the fire sales process (2.2)–(2.6) and the auxiliary process described and studied in the previous section. In particular, we will use the final number of sold assets in a specific auxiliary processes to bound the asset sales in the real process.

Let us start with a simple observation. For a given finite financial system with shock and specified functions and , it easily follows from (2.4) and (3.1) that the auxiliary process leads to more asset sales, to a higher price impact and as a result also to more defaults. Thus, the auxiliary process always serves as an upper bound for the fire sales process (regarding the actual asset sales and also the final default fraction). This is summarized in the following theorem. In the rest of this section we (silently) consider a -system with initial shock that satisfies Assumptions 2.1 and 2.2.

Theorem 4.1.

Let be the number of finally sold shares of asset divided by in the fire sales process. Let be as in (3.12). Then

Proof.

More surprisingly, as we shall see below, we can adapt carefully the parameters of the given system so as to also obtain lower bounds from the auxiliary process. The central idea is to define the auxiliary process on another system having smaller initial asset holdings and a sales function that is dominated point-wise by the original one. More specifically, let us fix . In addition to , define the sales function by . Further, we consider a system that is derived from the -system with initial shock but with asset holdings instead. In analogy to (3.8) we consider the functions

| (4.1) |

These functions describe a system where, in comparison to the original system, institutions hold fewer shares to start with and sell a smaller fraction of their assets as a reaction to a shock. Further, also in analogy to (3.9), let

and let be the largest connected subset of containing . Moreover, let the smallest joint root of the functions . We obtain the following crucial lower bound:

Theorem 4.2.

Let be the number of finally sold shares of asset divided by in the fire sales process. For every

Proof.

For every we consider a system satisfying Assumptions 2.1 and 2.2. Then it is immediate that the sequence satisfies Assumption 2.1 with limiting distribution . We now fix . As usual, let be the total number of assets sold in round in with sales function under the fire sales process. Further, let be the total number of assets sold in round in with sales function in the auxiliary process. We shall show that , which implies that and since by Theorem 3.4, , the claim follows. In order to show that we use induction. By definition . So, lets assume that . We determine the number of assets bank sells in round . First consider the case that , that is, the loss of bank at the beginning of round is bounded by and thus the fraction of shares sold so far is less than . As a result and thus

| (4.2) | |||||

| (4.3) |

If, on the contrary, , then

and again bank has sold more shares in step of the fire sales process in with sales function than in the auxiliary process in with sales function . We infer

and the induction step is completed. ∎

4.2 (Non-)Resilience Criteria for the Fire Sales Process

As considered before for the auxiliary process, we now investigate resilience properties of the fire sales process. We denote by the smallest joint root of the functions as defined in Section 4.1 with . Due to the conservative character of the auxiliary process, it is immediate that resilience of the auxiliary process for system implies resilience of the fire sales process for the system. Similarly, non-resilience under the fire sales process for implies non-resilience also under the auxiliary process for .

Corollary 4.3.

If , then the -system is resilient under the fire sales process. If there exists such that and such that no with (coordinate-wise) is a joint root of the functions , then the -system is non-resilient under the fire sales process.

Proof.

The first claim about resilience is a straightforward consequence of Theorem 4.1. For the second part note that if there exist such that , then the system with sales function is non-resilient for the auxiliary process by Theorem 3.8 (and its extension in 7.1.3) and for every shock , the number of sold assets over , it holds that . By Theorem 4.2 it follows that under the real process in the system with sales function the number of assets sold fulfills for every shock , which implies non-resilience. ∎

We will now present several more explicit (non-)resilience criteria for the fire sales process; in particular, we will show that in many natural situations the fire sales and the auxiliary processes behave the same with respect to their resilience properties. A starting point is the following observation, which states that in many cases an analysis of the derivatives at of the functionals describing the auxiliary system can be used to study (non-)resilience.

Theorem 4.4.

Assume that is differentiable in , and that there exists such that all partial right-derivatives exist (possibly with value ) and

| (4.4) |

Then the -system with sales function is non-resilient under the fire sales process.

Proof.

Let be the dimensional vector which has value in the -th entry and zero in all other entries. It is sufficient to show that there exists such that since is monotone increasing in the arguments . Using the lemma of Fatou and that for small , we obtain

and by (4.4) this expression is larger than zero for small . Thus non-resilience follows for the fire sales process. ∎

The previous theorem allows us to show that in many relevant situations actually the auxiliary and the real process are equivalent in terms of resilience. Let us consider the one dimensional system (i.e., ) in the important case of linear price impact (i.e., ). The following corollary shows that in most cases the resilience properties of the processes coincide.

Corollary 4.5.

Let and let be differentiable in . Then the following holds.

-

1.

If and : the system is non-resilient under both (original and auxiliary) fire sales processes.

-

2.

If : the systems are resilient under both processes if and non-resilient if .

Proof.

For 1. non-resilience follows from Theorem 4.4 as the expectation in (4.4) is infinite. For 2., if non-resilience follows again directly from Theorem 4.4. Let . To show resilience for , note that by the Dominated Convergence Theorem

and thus and , which implies with Corollary 3.7 that the system is resilient under the auxiliary process, and so also under the fire sales process. ∎

The conditions provided in Corollary 4.5 highlight two characteristics that fuel fire sales:

-

a)

The capital is too small in comparison to the asset holdings.

-

b)

Pronounced selling as a response to a drop in asset prices.

For a system with very low capitalization (), Corollary 4.5 1. shows that the system is non-resilient if market participants immediately react to price drops by selling assets (). For better capitalized systems (), the picture is more fine grained and Corollary 4.5 2. shows that the system is only non-resilient if the reaction to a price drop is prompt and strong (). It also follows that if and the system is resilient under both processes. However, it misses the case und . This case represents a scenario of a low capitalized, heterogeneous system with a rather low market reaction to stress, and is thus of particular interest. In this case the expectation in (4.4) equals 0 and based on Theorem 4.4 we cannot prove non-resilience of the real system. Moreover, we cannot use dominated convergence to derive the derivative of and conclude (non-)resilience.

In order to address this case we must make more refined assumptions. In particular, we assume that for some and for where describes sales at default (i.e. ). The next result, whose proof is presented in Section 7.2.2, shows that (non-)resilience is a property that depends on the interplay of and .

Theorem 4.6.

Let and . Then the following holds.

-

1.

: the system is non-resilient.

-

2.

: the system is resilient if and non-resilient if .

-

3.

or : Let . If , then the system is resilient. If and exists, then the system is non-resilient.

The last theorem adds another dimension to the picture and that is the interplay of and : Strong sales activity as a reaction to price drops needs to be compensated by low price impact to make the system resilient. If strong price impact comes together with strong sales as a reaction to price decline (), then the system is non-resilient, independent of the capital. For all other cases () the relation of asset and capital is crucial. Informally, the stronger the price impact, the more capital is required in relation to the asset holdings.

The previous results are restricted to systems with one asset only. They can be generalized to systems with multiple assets in various forms. For example, we can assume that for each asset with we have a specific price impact function . Then an argument as before shows that if , then the system is non-resilient. Moreover, if

the system is non-resilient (corresponding to a generalization of 2. in Theorem 4.6). Resilience is more difficult to characterize, as it may depend on the interplay among different assets. In these cases, Theorem 4.4 and Corollary 4.3 may be used to study resilience properties for the system at hand. We leave it as a research problem to extract further and more explicit (non-)resilience conditions from our main results.

5 Applications: Minimal Capital Requirements & The Effect of the Portfolio Structure

In this section we apply the theory developed in previous sections to investigate which structures or properties of systems hinder or promote the emergence and spread of fire sales. First, in Section 5.1 we address the important question of formulating adequate capital requirements: how much capital is necessary and sufficient for each bank, so that the system is resilient? We give an answer to this question in the specific setting where the asset holdings follow a power-law distribution, which is the most typical case to consider. Then, in Section 5.2 we consider systems parametrized by two orthogonal characteristic quantities: portfolio diversification and portfolio similarity. We first study their effect analytically based on our previous results, and we also verify our findings with simulations for finite systems of reasonable size. Our examples demonstrate the effects of portfolio diversification and similarity on resilience in various sensible settings.

5.1 Minimal Capital Requirements

While the results in the previous section might allow regulators to test the resilience of financial systems with respect to fire sales, a natural question from a regulatory perspective is to determine capital requirements that actually ensure resilience. This question is addressed now. In this section we have mainly leveraged institutions (for example banks) in mind.

Historically, the first approach to systemic risk was to apply a monetary risk measure to some aggregated, system-wide risk factor, see [12, 36, 30] for an axiomatic characterization of this family of risk measures. Another approach is to determine the total risk by specifying capital requirements on an institutional level before aggregating to a system-wide risk factor, see [4, 6, 25]. An important question is then whether from an institutional viewpoint the requirements correspond to fair shares of the systems risk, see e.g. [6]. In particular, a major problem in the implementation of the methodologies proposed in the aforementioned papers is that a given individual capital requirement in general depends on the configuration of the whole system. As a consequence, one institution’s capital requirement may be manipulated by other institutions’ behaviour, or the entrance of a new institution into the system would potentially alter the capital requirements of all other institutions. An important contribution of the methodology proposed here is that, besides certain global parameters that need to be determined by a regulating institution, the implied capital requirement for a given institution depends on its local parameters, i.e., its capital and asset holdings, only.

Abstractly, a capital requirement is a function that assigns to any bank with asset holdings a (minimal) required capital . For our ensemble this implies that the random variable is of the form and we would like to give conditions on that ensure resilience. We provide only stylized examples here for which analytic derivations are possible to illustrate the power of our asymptotic approach. For general system configurations one can always resort to numerical calculations.

Let us first restrict to one asset and assume that the distribution of asset holdings has power law tail in the sense that there exist constants such that for large enough

| (5.1) |

for some . There is empirical evidence for power laws in investment volumes, see e.g. [26]. Moreover, we assume the setting of Section 4.2, that is, we assume that for some and for .

One natural choice for the capitals as a function of the asset holdings is of power form. We immediately get the following corollary, whose proof is a direct consequence of Theorem 4.6, that determines sharply the magnitude of the minimal capital requirements to ensure resilience.

Corollary 5.1.

Let or and for and . Then,

-

1.

if , then the system is resilient,

-

2.

if , then the system is non-resilient.

Proof.

We verify the conditions of Theorem 4.6, i.e., we show that (resp. ) where . By the choice of capital we get that which is (resp. ) for (resp. . Under Assumption 1. then while under Assumption 2. . ∎

Additionally we can derive sufficient capital requirements in the multidimensional case. In this setting we assume that there exist constants and for such that for large enough

| (5.2) |

Corollary 5.2.

Let and for . Let or and for and . Let . Then,

-

1.

if , the system is resilient.

-

2.

if , the system is non-resilient.

Proof.

The proof is immediate from Lemma 5.3 below, which allows us to reduce to the one dimensional situation. ∎

The following simple result might be known, but we could not find it in the literature. We provide a proof for completeness.

Lemma 5.3.

Let be random variables with power law tails as above and let . Then there exists such that

| (5.3) |

Proof.

We assume that ; the result for general follows by induction. Let us further assume without loss of generality that for and . Clearly,

which provides the lower bound. By the union bound

and we obtain the upper bound. ∎

5.2 The Effect of Portfolio Diversification and Similarity

For simplicity, throughout this section we assume that the limiting total asset holdings are Pareto distributed with density for some exponent . One can generalize the example also to more general distributions. Further, we make the assumptions that and to simplify calculations, but also for other sensible choices our observations below are applicable.

In a first setting we consider a system of institutions whose investment in each asset makes up a fraction of their total asset holdings, where .

Example 5.4.

For a system as described above, the functions are given by

Let us write for short. Now assume similar to Corollary 5.1 that for some constants . Then

Motivated by the symmetry of the functions, we consider along direction , with . Then

Let and . We infer that if is small enough and or and , then for all . That is, and the auxiliary system is resilient by Corollary 3.7. On the other hand, if either or and , then for all and the system is non-resilient by Theorem 3.8. Since does not depend on the choice of , it makes sense to consider as a measure for stability of the system (the smaller , the more stable the system). Clearly, becomes minimized for for all and hence a perfectly diversified system requires least capital and can be seen as the most stable. This somewhat surprising observation is discussed after Example 5.5 in more detail.

Next, we consider a financial system that comprises of subsystems of equal size . For each subsystem there is a set of specialized assets that can only be invested in by institutions from . In addition to these specialized assets, there is a set of joint assets that can be invested in by any institution. Thus, each institution can choose from different assets to invest in. We call the diversification of the system. Further, let be the (portfolio) similarity in the system. Then, as in Example 5.4, one possible route to take is to determine the optimal investments for each institution (that is shifted towards investing in the specialized assets to avoid overlap with other subsystems). Instead we assume in the following example that each institution still perfectly diversifies its investment over the assets available to it.

Example 5.5.

Consider a system as described above consisting of subsystems and allowing each institution to invest in specialized assets and in joint assets in equal shares. Then the system is described by the following functions:

where , , and with small misuse of notation. Similar as in Example 5.4 we derive that

From the formula it is obvious that decreases (i. e. capital required to ensure resilience) as increases or decreases.

For this particular setup it thus turns out that diversification reduces the capital necessary to ensure resilience whereas stronger similarity between the institutions’ portfolios increases it. The fact that diversification is favorable might seem at odds with other studies in the literature (see for example [32, 5, 38, 11]), which find that diversification, when it comes with higher portfolio similarity, can increase externalities and is less favorable from a systemic risk perspective. In the second example this discrepancy is not surprising, as increased diversity arises due to an increased number of assets. In the first example it is due to the fact that capital requirements ensure resilience and that amplification effects are small. The sales pressure arising from the shock to some banks is then distributed among more assets, each of them being less impacted. Spillover effects to other institutions are contained due to the nature of the capital requirements based on . In summary, in a well-capitalized system, diversification might actually be good to reduce the impact of small shocks. However, we want to stress that the results obtained in these two examples should not be considered as universal statements. They only show that our mathematical framework allows one to investigate these questions in quite some detail for flexible specifications of the system.

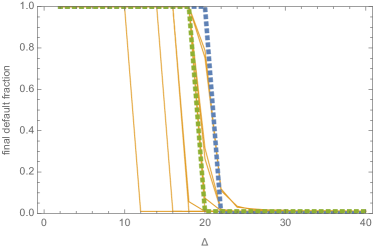

Simulation Study Note that all previous conclusions build on the (asymptotic) theory developed in the previous sections. To verify and back up the result for finite systems, however, we also provide a simulation based verification for a series of moderate size () systems. In the setting of the last example our choices of the parameters are as follows. We set and and . Then we obtain , , and . We assign to each institution the capital . Further, we draw the total asset holdings for each institution as random numbers according to the above described Pareto distribution. Finally, we randomly choose a set of initially defaulted institutions of size and equally distribute it across the subsystems.

To see the effect of diversification, we first fix and let vary from to (i.e. ). The results are plotted in Figure 5. Since we calibrated the capitals to the values and , the theoretical (asymptotic) final default fraction is for and otherwise. This curve is shown in blue. In orange we illustrate of the simulations. One can see that in each simulation the final default fraction rapidly decreases at a certain value for close to the theoretical value of . In green finally, we plot the median over all simulations which is very close to the theoretical curve despite the finite system size and hence verifies that systems become more resilient as increases. Deviations from the theoretical curve become smaller as increases.

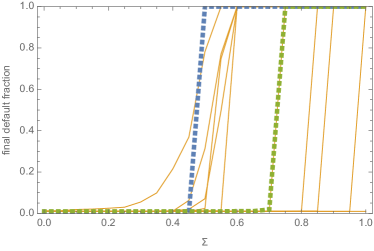

Furthermore, in the same setting we conducted simulations for systems of fixed diversification and varying similarity between and ( and ). The results are shown in Figure 5. Again, in blue we plot the theoretically predicted curve which is for and otherwise. In orange exemplary simulations are shown. For these, one can see that either there exists an individual threshold for close to at which the final default fraction rapidly increases or the final fraction stays constant at . The median over the simulations for each can be seen in green and it verifies that the system becomes less resilient as the similarity increases. Again deviations from the theoretical curve are due to finite size effects and become smaller as increases.

6 Conclusions & Future Research Directions

In this paper we introduced and studied a mathematical framework for fire sales. Our model describes the state of a financial system by specifying for each participant the capital and the amount of distinct assets that she possesses. All this information is concisely represented by the empirical distribution function of the previously mentioned parameters. Then this system gets initially shocked – the participants suffer losses – and, as a consequence, assets are sold. This causes the prices to go down, and an iterated process of selling and price decline starts rolling. We studied the final state of the system, in particular the number of sold assets and the final default fraction. Our main driving question was to understand which structural characteristics promote or hinder the outbreak of fire sales, and thus our approach is fundamentally asymptotic in nature: we ‘gathered’ all systems that are similar – in terms of the empirical distribution – and studied, as the system size gets large, the effect of various statistical parameters of the (limiting) distribution function. Our results provided a characterization for any system as either resilient or non-resilient. Moreover, it allowed us to formulate explicit capital requirements and to study the effect of portfolio correlations.

There is a whole bunch of questions that may be investigated within the framework developed here.

-

•

Finite Systems Our results about resilience are completely explicit for an ensemble of systems and thus, a priori, apply to large systems only. Our simulation studies show however that they are already good approximations for moderate-sized systems. A challenging direction for future research is to quantify precisely the finite-size effect: how do our results qualitatively carry over to systems of a given size ? How can we adapt the notions of (non-)resilience, and what effect does it have, for example on the capital requirements that we develop?

-

•

Refined Models Our model describes the process of (distressed) selling of the assets. However, there is no explicit modeling of market participants who might start buying when the price drops. These buyers might thus slow down the price decline. This effect is captured here in an abstract way by the price impact function . More refined models representing the statistical properties of further market participants and actions would constitute significant extensions of our model.

-

•

Capital Allocation Strategies The results presented here allow us to formulate minimal capital requirements that make the system resilient to fire sales. Thus, they constitute a building block of a more global capital allocation strategy that should be capable of making complex systems (including other types of interactions as default or liquidity contagion) resilient to initial stress. For example, our capital requirements can be combined with classical value-at-risk requirements used in the Basel III framework for leveraged institutions such as banks. Developing such global risk management strategies and studying the interplay of various contagion channels is an interesting research topic.

-

•

Portfolio Optimization Our results might not only be applicable from the view of regulators; they might also be utilized from market participants to optimize their portfolio with respect to systemic risk considerations. Developing adequate investment strategies by taking into consideration the effect of fire sales is a challenging open problem.

7 Generalized Statements and Proofs

7.1 Description and Analysis of the Fire Sales Process for a Discontinuous Sales Function

To focus on the underlying phenomena of fire sales, rather than being restrained by technical details, in the main part of this article we considered the special case of a continuous sales functions . As already the simple example of sales at default shows, however, it is not untypical for thresholds to exist at which institutions sell a positive fraction of their assets and thus may be discontinuous. By the explanation via thresholds, right-continuous sales functions are more natural than sales functions with discontinuities from the right, and we thus assume to be right-continuous in the sequel and denote by its left-continuous modification. Replacing by its right-continuous modification in the following, however, really makes our results applicable to any non-decreasing sales function . In addition to the results presented in the main body of the paper, the results presented here quantify, besides the final number of sold shares, also the final number of defaulted banks.

7.1.1 The Deterministic Model

As for the continuous case in the main part of this article, we start by considering the auxiliary process for a given system of size first. For a general non-decreasing sales function the equation

| (7.1) |

(compare (3.4)) has a smallest solution by the Knaster-Tarski theorem, and as in (3.5) it holds . For left-continuous in fact we would derive equality but for right-continuous it is in general possible that . This is the case if sold shares would be enough to start a new round of fire sales but this quantity is actually never reached in finitely many rounds. Then the following holds and extends Proposition 3.1; the proof is straight-forward by bounding from below with its left-continuous modification .

Proposition 7.1.

Consider the auxiliary process with a right-continuous sales function and the corresponding left-continuous modification . Let denote the smallest solution of (7.1). Moreover, let be the smallest solution of

Then the number of sold shares divided by at the end of the fire sales process satisfies

| (7.2) |

The equilibrium vector (in the sense of (7.1)) is thus a conservative bound on the final number of sold shares . However, as discussed above, the convergence of the fire sales process to a non-equilibrium heavily relies on the assumption of arbitrarily small sale sizes towards the end of the process. For real systems this is obviously not realistic since the least possible number of shares sold by an institution is lower bounded by . For all practical purposes it will therefore hold that and fire sales stop at an equilibrium state.

7.1.2 Large systems,

We now consider a sequence of financial systems of increasing size as before satisfying Assumption 2.1. As in Section 3.2 let , be given by

Moreover, motivated by the lower bound in Proposition 7.1 define the lower semi-continuous functions

| (7.3) |

and let

In addition to the sets and from Section 3.2, now also define

and denote by the largest connected subset of containing (clearly for all and thus ). Note that still and are closed sets as , , are upper semi-continuous for the choice of right-continuous sales function . Finally, as in Section 3.2 set

We can then state the following generalization of Lemma 3.3.

Lemma 7.2.

There exists a smallest joint root of all functions , , with . Further, as defined above is a joint root of the functions , , and .

In complete analogy to Theorem 3.4, but now without imposing Assumption 2.2, we can describe the extent and impact of the auxiliary process together with bounds for the number of defaulted institutions.

Theorem 7.3.

Consider a -system with initial shock satisfying Assumption 2.1. Assume that is right-continuous. Then for , the number of finally sold shares of asset divided by in the auxiliary process, and for the final default fraction ,

In particular, for the final price impact on asset

7.1.3 (Non-)Resilience

In this section we study (non-)resilience properties of -systems in the general setting; note that these notions did not depend on our previous Assumption 2.2. The following statement thus generalizes Theorem 3.6 and also includes a statement about the default fraction.

Theorem 7.4.

Consider a -system satisfying Assumption 1. Assume that is right-continuous. Then for each there exists such that for all initial shocks with , the number of finally sold shares of asset and the final set of defaulted institutions in the shocked system satisfy

Using the notations of Section 7.1.2, also the wording of Corollary 3.7 remains completely unchanged; that is, if , then the -system satisfying Assumption 1 with right-continuous is resilient.

We now consider . Theorem 3.8 remains unchanged in case that is strictly increasing in a neighborhood of . If is not strictly increasing, we distinguish between non-resilience and weak non-resilience.

Theorem 7.5.

Consider an -system satisfying Assumption 1. Assume that is right-continuous. Let . For every there exists a shock with and

In particular, from Theorem 7.5 we immediately get the following result.

Corollary 7.6 (Non-resilience Criterion).

If , then the -system is weakly non-resilient under the auxiliary process.

7.2 Proofs of Statements

7.2.1 Proofs for Section 3 and Section 7.1 (auxiliary process)

Proof of Lemma 7.2..

Existence of follows from the Knaster-Tarski theorem. We now construct a joint root such that we can conclude . It holds for all and thus (for any fixed ) for all such that by monotonicity of . Consider then the following sequence :

-

•

-

•

, where is the smallest possible value such that . It is possible to find such since is monotonically increasing in , and . By monotonicity of with respect to for all , it then holds for all and in particular .

-

•

, where is the smallest value such that . Again it is possible to find such since is monotonically increasing in , and . By monotonicity of with respect to for all , it then holds for all and in particular .

-

•

, , are found analogously, changing only the corresponding coordinate.

-

•

, where is the smallest value such that , which is again possible by monotonicity of , and . Further, it still holds .

-

•

Continue for , .

The sequence constructed this way has the following properties: it is non-decreasing in each coordinate and bounded inside . Hence by monotone convergence, each coordinate of converges and so exists. Since the convergence is from below,

and thus . Now suppose there is such that . By lower semi-continuity of then also for some and large enough. This, however, is a contradiction to the construction of the sequence since in every -th step. Hence for all and is a joint root of all functions , .

Now turn to the proof that . We first consider the case that is continuous (Lemma 3.3). We approximate by the sequence of smallest fixed-points for the functions . This allows us to apply the Knaster-Tarski Theorem and the monotonicity properties of as above. Simple topological arguments will then allow us to conclude that . Let for

and denote by the connected component of in . By the same procedure as for above, we now derive that there exists a smallest (componentwise) point such that for all . Clearly, is non-decreasing (componentwise) in and hence exists (we will show that in fact).

Now by monotonicity of , we derive that for all . Since is a closed set, it must hold that also for all and in particular, . Further, we derive that . Moreover, is the intersection of a chain of connected, compact sets in the Hausdorff space and it is hence a connected, compact set itself. Since it further contains , we can then conclude that and thus .

Consider now an arbitrary . We want to show that componentwise and thus . It suffices to show that for all . Then and . Hence assume that . By connectedness of we find with for all and equality for at least one coordinate (otherwise and is the union of two open non-empty sets and hence not connected). W. l. o. g. let this coordinate be . By monotonicity of with respect to for every , we thus derive that which is a contradiction to .

Now consider the general case that is right-continuous and let a sequence of continuous sales functions approximating from above. Denoting by the analogue of for the sales function , we derive that since clearly for all and further by dominated convergence for every ,

so that . If we further let denote the largest connected subset of containing , then is compact and connected for every and hence so is . Since further , we derive that . Let now denote the analogue of for the sales function . Then for all and hence . Now suppose there existed a vector and such that . Then also for large enough, and hence . This, however, contradicts the assumption that . Hence there exists no such and .

Finally, we show that is a joint root of , : Since , it holds that for all . Assume now that for some . We can then gradually increase the -coordinate of (until ). By monotonicity of with respect to for every , however, we can be sure that we do not leave the set by this procedure which is a contradiction to the definition of . Hence is a joint root of , . ∎

Remark 7.7.

In the proof of Lemma 7.2, for the case that is continuous, we constructed as the limit of a sequence such that for all . For non-continuous by the Knaster-Tarski theorem we still know that there exists a smallest vector such that , but the construction of as for in the proof of Lemma 3.3 fails and we can not be sure a priori that . Hence let further be defined as the smallest vector in such that . This vector exists again by the Knaster-Tarski theorem noting that analogously to Lemma 3.3 contains its componentwise supremum . Then by the same means as above, we derive that .

The rest of the section is devoted to the proof of Theorem 7.3 (and Theorem 3.4) which deal with a sequence of financial systems. The following technical lemma about the convergence of the smallest joint roots will be quite handy.

Lemma 7.8.

Let a sequence (for ) of financial systems be described by functions , , with smallest joint root . If pointwise for every , then , where denotes the smallest joint root of the functions , .

Proof.

The main difficulty in showing the claim is that only pointwise but not uniformly in . A further difficulty is the multidimensionality. The main idea is to construct a path in analogy to the construction in Lemma 7.2 that leads to a point smaller but close to . On this path the functions , are all positive for large. It can then be compared componentwise with a path leading to .

For this consider the construction of in Lemma 7.2 and change it in such a way that in each step (where and ) a point is chosen such that for some fixed (choose as the smallest possible value such that this inequality holds; it will then either be or ). Note that can only happen if in which case there exists such that and for all but and for . Then is a non-decreasing (componentwise) sequence bounded by and hence exists. Further, it holds that . Finally, is non-increasing componentwise in and bounded inside and thus exists. Moreover, and hence in particular .

Fix now and choose small enough such that for all . Further, choose large enough such that for all . In particular, . Now note that can be constructed by a sequence analogue to in the proof of Lemma 3.3 as well. We can then in each step cap the element of the constructing sequence at , which clearly does not increase the limit of the sequence. We want to make sure that in fact the cap is used in every step if we only choose large enough. Then we can conclude that and hence letting , .

We now show that the cap is applied in every step for large enough by an induction argument. For , clearly and the cap is applied. Now let us assume it holds for . If , then of course the cap is also applied in step as the sequence is increasing. Otherwise, note that by definition of , it holds for all such that and for all . Now choose a discretization of for such that , and for all . We now use the assumption that for every , where and for . Then for large enough, . Finally, for any linear interpolation between and (),

Hence the cap is applied in step . As there are only finitely many steps , this finishes the proof. ∎

Proof of Theorem 7.3..

We start by proving the lower bound. Recall from Proposition 7.1 that . Using weak convergence of the random vector and approximating from below by a sequence of continuous sales functions , we derive for that pointwise

Hence as and by monotone convergence,

| (7.4) |

and we can use Lemma 7.8 to derive that .

We now want to show the lower bound on the final default fraction. Fix some and choose large enough such that componentwise. Then