Bailout Stigma

Abstract

We develop a model of bailout stigma where accepting a bailout signals a firm’s balance-sheet weakness and worsens its funding prospect. To avoid stigma, high-quality firms either withdraw from subsequent financing after receiving bailouts or refuse bailouts altogether to send a favorable signal. The former leads to a short-lived stimulation with a subsequent market freeze even worse than if there were no bailouts. The latter revives the funding market, albeit with delay, to the level achievable without any stigma, and implements a constrained optimal outcome. A menu of multiple bailout programs also compounds bailout stigma and worsens market freeze.

Keywords: Adverse selection, bailout stigma, shorted-lived and delayed stimulation

JEL Codes: D82, G01, G18

History is fraught with financial crises and large-scale government interventions, the latter often involving a highly visible and significant wealth transfer from taxpayers to banks and their creditors. As a recent example, during the 2007-2009 Great Recession, the US government paid $125 billion for assets worth $86-109 billion to the nine largest banks under the Troubled Asset Relief Program (TARP) (Veronesi and Zingales (2010)). A rationale for such public interventions – to be called bailouts throughout the paper – is that the government can jump-start a market that would otherwise freeze due to adverse selection. By cleaning up bad assets, or “dregs skimming,” through public bailouts, the government can improve market confidence, thereby galvanizing transactions in healthier assets (Philippon and Skreta (2012), Tirole (2012)). However, the flip side of such dregs-skimming is that bailouts can attach stigma to their recipients, increasing future borrowing costs. The fear of this stigma may in turn discourage financially distressed firms from accepting bailout offers in the first place, undermining the effectiveness of such interventions.111Such a concern is echoed in a speech by the former Federal Reserve chairman Ben Bernanke in 2009: “The banks’ concern was that their recourse to the discount window, if it became known, might lead market participants to infer weakness—the so-called stigma problem.” Several anecdotes suggest that this concern is well-founded. Ford refused rescue loans under the Auto Industry Program in the TARP, with a view to “legitimately portraying itself as the healthiest of Detroit’s automakers” (“A risk for Ford in shunning bailout, and possibly a reward,” The New York Times, December 19, 2008). It is also well known that Jamie Dimon, CEO of JP Morgan Chase, wanted to exit the TARP to avoid the stigma (“Dimon says he’s eager to repay ‘Scarlet Letter’ TARP,” Bloomberg, April 16, 2009). The fear of stigma is not the only reason for an early exit. Wilson and Wu (2012) find that early exit by banks is also related to CEO pay, bank size, capital, and other financial conditions. These factors, especially the restrictions on executive compensation, are also found to cause the reluctance to accept bailouts (Bayazitova and Shivdasani (2012), Cadman et al. (2012)). The literature documenting the empirical evidence on stigma is reviewed in Section V.,222Policy makers during the Great Recession were aware of such a fear and took efforts to alleviate the stigma. At the now-famous meeting held on October 13, 2008, Henry Paulson, then Secretary of the Treasury, “compelled” the CEOs of the nine largest banks to be the initial participants in the TARP, precisely to eliminate the stigma (“Eight days: the battle to save the American financial system,” The New Yorker, September 21, 2009). The rates at the Fed’s discount window, usually set above the federal funds rate, were cut half a percentage point to counteract the stigma attached to using the window (Geithner (2015, p. 129)).

The purpose of this paper is to study a dynamic model of bailouts to understand how reputational concerns affect the effectiveness of public bailouts and how an optimal bailout policy should be designed in light of these concerns. To address these questions, we present a two-period model of a bailout program in which the government offers to purchase assets from firms. The focus on asset-purchase as the bailout tool allows us to capture firms’ reputational concerns in a simple parsimonious way. There is a continuum of firms, each with one unit of a legacy asset in each period. The quality of asset in both periods is identical for each firm and is its private information. In each period, firms have access to profitable investment opportunities. However, liquidity constraints and the non-pledgeability of projects imply that firms need to sell assets to fund those projects. As in Tirole (2012), we focus on the case where adverse selection leads to a market freeze and calls for a public bailout. To understand the reputational consequence of accepting a bailout, we assume that the government runs a bailout program in the first period only. The sale of assets in the market is not publicly observed, but firms’ acceptance of the bailout offer is observed. The market updates its belief on the quality of assets based on the observation of firms’ decisions in the first period, and thus makes its second-period offer accordingly.

Bailout stigma is captured in our model by the unfavorable terms that bailout recipients suffer from the sale of their assets in the second period. As shown by Philippon and Skreta (2012) and Tirole (2012), a key function of a public bailout is dregs-skimming: by taking out the left tail of the worst quality assets, a bailout improves the perceived quality of remaining assets, thereby rejuvenating asset trade in the market. But this means that the market will believe those that accept the bailout have worse assets than those that refuse the bailout. Such a belief is reflected in the differential treatment of the two groups of firms in the second period: the market’s offer to bailout recipients would be in general in worse terms than that made to the bailout holdouts.

The precise mechanism by which the bailout stigma affects the efficacy of the bailout crucially depends on firms’ strategic responses to the bailout offer, manifested in two possible equilibrium outcomes—short-lived stimulation and delayed stimulation.

A short-lived stimulation equilibrium arises when high-quality firms strategically avoid the bailout stigma by accepting a bailout in the first period but withdrawing from the market in the second period. Suppose that high-type firms indeed behave in this way. Then, the market in would believe that the bailout recipients that do participate in the second-period have bad assets, and assign stigma to them. To avoid that stigma, firms would rather choose to sell their assets to the market at discount in the first period. This in turn deteriorates their sale terms, ultimately inflicting a commensurate haircut on the market-sellers; in effect, the bailout stigma “spreads” from bailout recipients to market sellers in this equilibrium. This contagion of stigma in turn leads firms with high-quality assets to accept a bailout offer but withdraw from the second-period market altogether to avoid that stigma, thus validating the initial hypothesis.333The withdrawal from the second-period funding market should not be literally interpreted as a firm exiting from the funding market altogether. Our model is (inevitably) stylized, so the results should be interpreted with some care. In practice, a firm’s withdrawal from the funding market will more realistically correspond to its cutting back on additional projects at the margin that it would otherwise pursue.

The presence of high-type firms that withdraw from the subsequent market/financing undermines the overall efficacy of the bailout. Their withdrawal exacerbates the stigma for those participating in the subsequent market, which has the chilling effect on the asset markets in both periods. Unlike Tirole (2012) where the government intervention boosts the confidence in private markets, intervention now undermines market confidence. The consequence is devastating: the market freeze is even worse than if there were no bailout! However, this does not mean that a bailout has no effect. The increased investment by bailout recipients in the first period may outweigh the dampening effect on the markets. Nevertheless, stimulation is short-lived in this equilibrium. We show that the policy maker can avoid this equilibrium by offering sufficiently generous bailout terms—that is, high purchase prices for assets, in which case the stigma will manifest itself in a different form: “delayed stimulation.”

A delayed stimulation equilibrium arises when high-quality firms refuse to sell either to the government or to the market in the first period. They do so to build a good reputation in order to sell their assets in the second period at favorable terms. This equilibrium is possible when the bailout offer is generous enough to attract a large fraction of firms with low-quality assets. This allows firms to send a credible signal about their asset quality when they refuse the bailout offer. Buyers will then respond with a very attractive price offer in the second period—one that makes it worthwhile for high-quality firms to forego asset sale in the first period. In sum, the equilibrium endogenously creates an opportunity for high-quality firms to signal their financial strength by rejecting the government’s generous offer.

Such a favorable signaling opportunity offsets the adverse effect of bailout stigma, even though market rejuvenation is delayed to the second period. The presence of firms rejecting a bailout means that the volume of asset trade in the first period is lower than that of the one-period benchmark with the same bailout offer. In an extreme case, it is even possible that the bailout has no stimulation effect in the first period relative to the laissez-faire economy. Such an initial lack of response may be seen as a policy failure. However, the policy “quietly” strengthens market confidence in the asset quality of refusing firms, which bears dividends in the second period. In fact, the overall trade volume is higher than that in a short-lived stimulation equilibrium; remarkably, it is the same as if there were no bailout stigma—that is, if the identities of bailout recipients were concealed successfully, which is often difficult to achieve in practice. Strikingly, a bailout offer is more effective when many firms reject it (to build a favorable reputation) rather than accept it. Rejection of bailouts could therefore be a blessing in disguise.

The desirability of the delayed stimulation equilibrium is further reinforced when the costs of bailouts are taken into account. When such social costs are included in the model, we show that a delayed stimulation equilibrium (as well as a secret bailout) induced by a suitable bailout offer is constrained optimal among all bailout mechanisms offered in , including those involving a menu of multiple bailout terms. By contrast, a short-lived stimulation equilibrium is strictly suboptimal, regardless of the bailout terms. This is because the severe stigma arising from that equilibrium requires a high deficit, and a correspondingly high social cost, to generate the same degree of stimulation in trade. To eliminate the possibility of this less desirable equilibrium, the policy maker may wish to make the terms of bailout even more generous than would be optimal. This approach, although departing from the classical Bagehot’s rule,444Bagehot’s rule, orginating from the 1873 book, Lombard Street, by William Bagehot, prescribes that central banks should charge a higher rate than the markets to discourage banks from borrowing once the crisis subsides. Bailout stigma was not a serious issue in 1873, however, since the regulatory system in 1873 Britain ensured concealment of the identities of emergency borrowers, as Gorton (2015) points out. is consistent with the approach taken by policy makers during the Great Recession. Finally, the optimality of a single bailout program calls into question the wisdom of offering a menu of multiple bailouts, which can never be socially desirable. Multiple programs give firms increased opportunities and the incentives for signaling, which compounds the overall level of stigma and market freeze.

The remainder of the paper is organized as follows. Section I presents our model while Section II analyses several benchmark cases. In Section III, we study various equilibria under government intervention. Section IV provides the welfare analysis of bailout policy. Section V discusses related literature. Section VI concludes. Proofs not contained in the main text are deferred to Appendix and Online Appendix.

I Model

We adopt a model that extends Tirole (2012) to a setup which admits a bailout stigma. There is a continuum of firms each endowed with two units of legacy assets with the same value; one unit of the asset becomes available in each of two periods () for possible sale.555One can think of the assets as account receivable or the contract for (securitized) assets to be delivered over two periods. The asset value of each firm is privately known to that firm and distributed on according to cdf with density . For convenience, we hereafter call a firm with legacy asset a type- firm. Throughout, we assume that is log-concave, that is, . Log-concavity of implies intuitive properties we will use on truncated conditional expectation: for any , (see Bagnoli and Bergstrom (2005)). We additionally assume that for each , is increasing in for any . These properties, which hold for many well-known distributions, facilitate the characterization of our equilibria.

In each period, an investment project becomes available to each firm. The project is socially valuable with net return but requires funding of . The firm can finance the project by selling its legacy asset each period. As we will see, the outcome from this laissez-faire regime will typically be inefficient due to the adverse selection associated with uncertain asset value. This inefficiency rationalizes a government bailout in the form of an offer to purchase legacy assets at some price . The government purchase price is initially exogenous (at level above ); we later discuss how it may be chosen optimally in Section IV in light of the public cost of a bailout. The timeline of our full game is depicted in Figure 1.

To focus our attention on the main issue—namely, bailout stigma—we make several simplifying assumptions.

First, just like Tirole (2012), we assume that the limited pledgeability of the project inhibits direct financing. This means that the sale of legacy assets is the only means of funding the project for firms. In the same vein, we consider the government’s purchase of legacy assets as the only means of government bailout.666In fact, the asset purchase can be interpreted as a loan collateralized by the associated asset. Due to the non-pledgeability, the asset must be seized and liquidated, which makes the loan qualitatively equivalent to the asset purchase. This is primarily a simplifying assumption. As shown by Philippon and Skreta (2012), the main thrust of the analysis extends to the case in which the project can be pledged along with legacy assets as collateral to obtain financing.777Their insight appears to apply to our context, which suggests that debt contracts would be optimal in our context as well. Since the stigma issue is separable from the issue of contract form, we abstract from it in the current paper. From this broader perspective, adverse selection with respect to legacy assets must be interpreted as pertaining to their values as collateral required for financing; and our results can be translated into this broader context naturally.

Second, to simplify the analysis, we assume that the return from project is not pledgeable, and does not accrue until each firm needs to fund its project. This implies that the firm is not able to use the return from project to finance the project.

Third, as is standard in the literature, we assume that asset buyers in the market are competitive and make purchase offers in Bertrand fashion. Specifically, we require that an equilibrium admit no deviation offer that a positive measure of firms have strict incentives to accept and at least breaks even for the deviating buyer.888This requirement is only slightly stronger than the standard equilibrium assumption, and can be seen as a refinement that bolsters the credibility of a selected equilibrium. In particular, this means that in equilibrium all buyers must break even, since otherwise, there will be a weakly profitable deviating offer that will be attractive for a positive measure of firms. Buyers live for one period and make offers that would break even in expectation. Importantly, buyers in can make rational inference about firms’ types from their observable behavior in , in particular with their acceptance/rejection of a bailout offer.

Fourth, we assume that the sale of assets to the market in is private and therefore not revealed to buyers in . This implies that buyers in the market cannot distinguish between those that sold in the market and those that did not. Again the primary reason for this assumption is to simplify the analysis by shutting off channels of dynamic information revelation. However, this assumption is well justified given that many important financial and real assets are sold privately over the counter. The main thrust of our results extends to the case of observable sale, as shown by the working paper version of our paper (see Che et al. (2018)). Moreover, this assumption makes a comparison with Tirole (2012) transparent, which helps to isolate the effect of stigma.

Fifth, a government bailout is available only in . This is consistent with the observed practice: governments refrain from engaging in long-term bailouts and from complete “nationalization” of distressed firms (which would be equivalent to purchasing two units of the asset in our model). Our goal is to study the reputational consequence of accepting or rejecting a bailout, which can be studied most effectively when no bailout is available in the second period.999Like Tirole (2012), our focus is on market freezes and the government’s role to alleviate them. This focus means that we abstract from other relevant issues such as the moral hazard associated with firms’ excessive risk taking or shirking in anticipation of bailouts. These moral hazard problems suggests the desirability of the government committing not to bail out firms that are ex post in need of rescue. This problem and the associated time inconsistency problem are discussed in Green (2010), Chari and Kehoe (2016), and Keister (2016). Since firms make no effort or risk taking decisions in our model, these issues do not arise in our model, thus allowing us to focus on the market freeze problem.

Finally, we focus on “transparent” bailouts; namely, the market observes the identities of firms that have accepted bailouts. Not only do transparent bailouts highlight the stigma effect most clearly, but they are also important from a practical perspective. While secret bailouts may address the stigma problem, secrecy is often difficult to achieve in practice. Nevertheless, one may consider suppressing information about bailouts totally or partially in the spirit of information design (Bergemann and Morris (2019)). Our analysis in Section IV encompasses this general information design perspective, and shows that a transparent bailout is without loss given the selection of equilibrium.

II Preliminary Analysis

Before proceeding, we study several benchmarks. They will facilitate comparison with, and provide a context for, our main results, which will follow in Section III.

II.A Laissez-faire without Government Bailout

We first consider the benchmark without a bailout. The timeline is the same as Figure 1, except that the government’s bailout is absent. Since the sale of the assets is private and not publicly revealed, there is no linkage between the market outcomes across two periods. Thus, the game reduces to a one-period game (repeated twice) whose equilibrium coincides with that of Tirole’s game without bailout.

Fix any period. The equilibrium outcome is understood best as a form of Akerlof’s lemons problem, which is depicted in Figure 2.

The figure plots two curves both as functions of the marginal type of firm selling to the market. The marginal type effectively represents the “quantity” sold since types sell if and only if in equilibrium.101010This feature follows from the single-crossing property: if a type- firm sells, then type- firm strictly prefers to sell. The quantity sold is thus which corresponds to in one-to-one manner. The marginal type faces as the opportunity cost of selling: by selling the firm loses the asset of value but gains the net surplus . Since the marginal type must be indifferent to selling in equilibrium, we have , giving rise to the supply curve. Meanwhile, buyers of asset quality enjoy benefit on average. Bertrand competition among buyers means that average benefit must equal price in equilibrium, giving rise to the average benefit curve.

Clearly, supply and average benefit curves must intersect at the equilibrium marginal type , where satisfies

| (1) |

The log-concavity assumption means that the average benefit curve always crosses the supply curve from above. Hence, there is a unique threshold satisfying this requirement, which induces a unique equilibrium.111111It is routine to check that if is log-concave ( for all ), then there is a unique satisfying (1); see Tirole (2012). Finally, for trade to occur in equilibrium, price must be at least , or else there are no gains from trade.

Figure 3 summarizes the equilibrium configuration.121212As mentioned, buyers cannot update their information since the market transactions are private. If market transactions were observable, then trading decisions become dynamic, which makes analysis complicated; see Che et al. (2018).

Adverse selection means that the above outcome is typically inefficient. Specifically, if , then , so not all firms sell and finance their projects. It is also possible that , in which case the market freezes completely. To focus on the nontrivial case, we assume . For expositional ease, it is also convenient to focus on the partial freeze case () in what follows. We will discuss the full freeze case () later in Remark 2.

Example 1.

Consider the uniform case, that is, . In this case, the equilibrium price is determined by . Suppose . Then, from the indifference condition , the cutoff type is uniquely determined as , and , if . If , then the equilibrium price cannot fund the project, so the market fully freezes, and hence . If , then for all , and therefore, .

II.B Bailout without Stigma: One-Period Model

We next consider another benchmark, the one-period bailout model by Tirole (2012) in which the government offers to purchase assets at price above the laissez-faire price before the market opens. Specifically, the timeline simply comprises in Figure 1.131313An astute reader will notice that this timeline differs slightly from that considered by Tirole (2012), where the market opens after firms have decided on the government offer. We adopt the current timeline since it is arguably more realistic, and also it permits equilibrium existence more broadly for our two-period extension. For the one-period version, the difference is immaterial, since the equilibrium under the current timeline is payoff-equivalent to Tirole’s equilibrium for all players involved. In addition, we do not invoke an equilibrium refinement adopted in Tirole (2012), as the central feature of the equilibrium holds irrespective of the refinement. See Remark 1. Since there is no consequence of accepting a bailout from the government in this one-period model, there is no bailout stigma—at least in the sense we will capture in our two-period model later.141414Note that Tirole (2012) and Philippon and Skreta (2012) do recognize “stigma” associated with the types of firms that accept a bailout, but they do not study its effect on the subsequent game nor on the initial decision to accept the bailout, the dual focuses of the current paper. Thus, this benchmark will help to identify the role of bailout stigma later in our main analysis.

Perfect Bayesian equilibrium in this game, which we simply refer to hereafter as an equilibrium, is characterized as follows. Let and denote the fractions of types that sell to the government and to the market, respectively, where . We first argue that . If no firm accepts the government offer, then the laissez-faire equilibrium will prevail, with marginal type and equilibrium price . Since , however, firms will deviate to accept the government offer, a contradiction.

Next, suppose , so the market is active in equilibrium.151515Under our timeline, the market may not be active in equilibrium. To see how such an equilibrium can be supported, suppose a buyer deviates and offers a price . Since firms have not yet accepted the government offer by then (given our timeline), all types would accept the deviation offer, and the deviating buyer will suffer a loss since . This implies that the market price must equal the government price , or else a lower offer will not be accepted. Given this, firms will sell (either to the government or to the market) if and only if . Let and denote the average values of assets sold to the government and the market, respectively ( can be arbitrary in case ). Clearly, we must have

| (2) |

Further, since market buyers must break even when , we have . Given , this in turn implies .

The central feature of Tirole (2012) follows from these observations:

Theorem 1 (dregs-skimming).

- (i)

-

In any equilibrium of the one-period benchmark with government offer , firms sell assets (either to the government or to the market) at price if and only if . Since , more firms finance their projects than without the government intervention.

- (ii)

-

If so that the market is active, then we must have ; that is, on average lower value assets are sold to the government than to the market.

Proof.

See Appendix A.1. ∎

Figure 4 illustrates the outcomes with and without government bailout. By offering a higher price than the laissez-faire price , the government does indeed take out relatively low-value assets, which in turn improves the perception of the assets sold to the market and thus alleviates adverse selection.

More importantly for our purpose, assets are sold to the government at the same price as they are sold to the market. This reflects the absence of stigma associated with accepting a bailout. Plainly, in the one-period problem, firms that accept the bailout can do so without fear of consequences, since the game ends immediately after the bailout.

Remark 1 (The role of the equilibrium refinement in Tirole (2012)).

To obtain the “dregs-skimming” role of bailout, Tirole (2012) invokes an equilibrium refinement—that the market sale collapses with an arbitrarily small probability. Given the single crossing property implicit in the firms’ payoffs, this refinement effectively “forces” the equilibrium to have the dregs-skimming feature: namely, there exists such that types all sell to the government and types all sell to the market.161616Suppose a market sale is subject to probability of cancellation. If a type- firm prefers to sell to the government, then , where is the equilibrium market price. This means that all types must strictly prefer to sell to the government. Consequently, this refinement makes unclear whether dregs-skimming is an artifact of the refinement or something more fundamental. By not invoking the refinement, Theorem 1 proves that dregs-skimming is fundamental (and not driven by the refinement). Without the refinement, however, there are multiple equilibria that differ in terms of and the value , but every such equilibrium exhibits the “dregs-skimming” feature.

II.C Secret Bailout

In order to identify the effects of bailout stigma, we need to understand what would happen if the policy maker could eliminate the stigma altogether. Imagine that the policy maker “completely and successfully” conceals the identities of the firms that accept the government offer. This kind of secrecy would be an important feature of the bailout policy and is worth studying in its own right, precisely because of the issue of stigma.171717Gorton and Ordoñez (2020) supports such a policy. During crises, debt contracts lose “information insensitivity” as investors scrutinize the downside risk of underlying collaterals, leading to an adverse selection. They argue that withholding information on whether borrowers borrow from discount windows of central banks can make debtors less information sensitive and alleviate adverse selection. As will be seen, secrecy has a more nuanced effect in our model. Nevertheless, we view secrecy primarily as a benchmark against which transparent bailouts are compared, given our premise that “complete” secrecy has been so far difficult to achieve despite many concerted efforts.181818The identities of banks borrowing from the discount window facilities (DW) are occasionally leaked to either the news media or the market participants through a number of channels. First, despite the apparent secrecy attached to DW, the access to DW by borrowing firms has been detected by news media (Armantier et al. (2015), Berry (2012)). For instance, the Financial Times reported the news that Deutsche Bank had borrowed from DW one day ago (see “Fed fails to calm money markets,” The Financial Times, August 20, 2007). Second, the market participants can identify DW borrowers from these banks’ market activities or the information released by the Fed. On its weekly report, the Fed discloses whether there is an increase in aggregate DW borrowing. In addition, financial institutions can observe whether a bank did not borrow or lend at the federal funds market at that time. Combining all the information, one can easily identify a DW borrower (Haltom (2011)).

The equilibrium under complete secrecy is very easy to analyze. Since, under secrecy, neither sales to the market nor sales to the government are observed, the former by assumption and the latter by secrecy, firms need not worry about the signaling consequences of their actions. Hence, the equilibrium in coincides with that of Theorem 1. Given no informational leakage, the outcome of coincides with the no-intervention benchmark.

Theorem 2 (Secret bailouts).

Suppose the government offers to purchase assets at with full secrecy. Then, in equilibrium, firms accept the government offer in if and only if . In , firms sell assets to the market at price if and only if .

III Government Bailout and Stigma

We now turn to the two-period game whose timeline is depicted in Figure 1. We continue to assume that the government offer is above the laissez-faire price: . Otherwise, there is only a trivial equilibrium in which the laissez-faire outcome prevails, with no firms accepting the government offer.

We begin by analyzing the structure of a possible equilibrium. We focus on the equilibrium obtained in the limit as the relative weight for the payoff approaches 1.191919The assumption of is meant to capture the fact that even though the reputational consequence of accepting a bailout may be important, its effect does not outweigh the direct payoff consequence of the decision, which appears to be first-order. Further, the reputational impact attached to bailouts does not usually persist after the financial crisis resolves. For instance, the total outstanding TARP bank funds, after the launch of TARP in October 2008, reached their peak at $235.3 billion in February 2009, but sharply decreased to $80.4 billion in January 2010 (go to https://www.treasury.gov/initiatives/financial-stability/reports/Pages/TARP-Tracker.aspx for more details). This observation indicates that the banks, after having joined TARP during 2007-2009 Great Recession, had little trouble securing funding through the market after the crisis was over.

Lemma 1.

In any equilibrium with , there are three cutoffs such that types sell assets in both periods, some measure of whom sell to the government and the remainder of whom sell to the market in ; types sell only to the government in but do not sell in ; types sell only in ; and types never sell their assets in either period.

The structure of an equilibrium is depicted in Figure 6.

Lemma 1 rests on several observations. First, firms’ preferences satisfy the single-crossing property, implying that a lower type has greater incentives to sell than a higher type in either period. This implies that the total number of units sold in equilibrium across the two periods must be non-increasing in . Second, the fact that buyers (either the government or the market) never ration sellers means that the quantity traded for each firm must be either zero or one in each period.202020 The same logic implies that virtually no partial sales would arise even though we allow for them. By the single crossing property of the payoff functions, partial sales, just like randomization, could occur in equilibrium only for a measure zero set of firm types, namely, the type that is indifferent between selling two or one units and the type that is indifferent between selling one unit and zero unit. Third, an arbitrarily small discounting of the second-period payoff, along with the first two observations, implies that, among those that sell only in one period, early sellers are of lower types than late sellers. These observations give rise to the stated cutoff structure, as depicted in Figure 6. We omit the formal proof since it follows from a standard argument based on these observations.

In what follows, we limit attention to the case of , namely, when the offer is not so high that all firms would accept the bailout.212121Given the condition, we will have . In case is higher so that all firms accept the bailout, the second-period would coincide with the laissez-faire outcome. Then, Lemma 1 implies that there are only two possible types of equilibria: (a) short-lived stimulation equilibria and (b) delayed stimulation equilibria, depending on whether the stimulation effect of a bailout arises in or delayed to . More formally, these two types of equilibria correspond to the cases where and , respectively, in the cutoff structure characterized in Lemma 1. In Online Appendix LABEL:Asec:equili_types, we formally show that these are the only possible types of equilibria.

III.A Short-lived Stimulation Equilibria (SSE)

This type of equilibrium corresponds to the case where in Lemma 1, and is depicted in Figure 7. Importantly, the segment of firms selling in in Lemma 1 (i.e., delayed selling) is of measure zero in this equilibrium. Consequently, a bailout triggers an immediate increase in trade volume in , but, as we will argue, this effect is short-lived.

The SSE are characterized as follows:

Theorem 3 (Short-lived stimulation equilibria).

In an SSE under an public offer , there exist such that the following holds:

- (i)

-

Types sell in both periods, and types sell only in to the government.

- (ii)

-

Among the types , the fraction with average quality accepts the bailout and the fraction with average quality sells to the market at in , where .

- (iii)

-

.

Proof.

See Appendix A.2. ∎

We highlight three features of SSE. First, bailout recipients suffer stigma. In the market, bailout recipients are believed to be of type (on average), while those that sell to the market in are believed to be of type . Thus, assets held by bailout recipients are sold at discount precisely equal to , since the market correctly infers the difference in their average asset values. Of course, this stigma must be compensated in , or else no firms would accept the bailout. In particular, the government must pay more than the market does for the asset in . Since the government offer is fixed at , this means that the market in must clear at price . In other words, buyers demand a haircut from firms selling to them for avoiding that stigma. So, the stigma leads to a commensurate mark-down of price for assets traded in market.222222While direct evidence for such a mark-down is not readily available, the phenomenon is similar to the finding in Armantier et al. (2015) that borrowing from the Discount Window was cheaper than using the Term Auction Facility due to the stigma attached to the former. Since the market is competitive, buyers cannot earn positive profit, so what this simply means is that the average type of firms selling to the market must (endogenously) equal .

Second, dregs-skimming by government bailout—featured prominently in Tirole’s model—does not occur here. More specifically, there is a positive measure of firms that accept the government offer. The assets sold by these firms have strictly higher value than , the highest value of asset sold to the market. This contrasts with the equilibrium in Tirole (2012), in which the assets sold to the government are worth strictly less than those sold to the private markets. Bailout stigma here creates the incentive for high-type firms to mitigate it or avoid it altogether. Selling to the market in instead is one option, but it is subject to a mark-down of asset price by ; effectively, bailout stigma has “spread” to market sellers in . Another way to avoid the collateral damage is to accept the bailout but simply withdraw from the market. Indeed, types find it strictly profitable to accept the bailout but refuse to sell assets in to avoid the stigma. The presence of these firms undercuts the government’s effort to take out the most toxic assets and boost the market reputation of the remaining firms. This has a long term effect, as we now turn to.

Third, the government bailout crowds out the private markets in both periods, and makes stimulation short-lived. This is caused by high-type firms’ withdrawal from the market to avoid stigma, which worsens the reputation of firms that do participate in the market: they are effectively revealed to be of type on average. The high-type firms’ behavior allows the stigma to spread to all firms, as noted above, and ends up suppressing the market prices in , including those that did not accept the bailout in . Naturally, this (anticipated) effect on the asset prices feeds back into the asset market in , dampening its price below . This stands in sharp contrast to Tirole’s static model, in which the government offer above the laissez-faire price raises the private market offer also above , in fact exactly to . Quite the contrary, here the government offer crowds out the markets in both periods, causing them to perform worse than even the laissez-faire benchmark. In fact, this negative effect is so severe that the market freezes more than if there were no bailout in : only types sell in , where importantly . By comparison, all types would have traded in in the absence of bailout (recall Figure 3). Clearly, transparency leads to a strict loss of trade. Compared with a secret bailout, the volume of trade (and investment) induced under the transparent bailout is the same in but strictly smaller in .

The properties identified so far are necessary but not sufficient for SSE. Specifically, for the existence of SSE, buyers targeting bailout recipients should not gain from raising their offers to attract the boycotters (i.e., types ), and the buyers targeting non-recipients should have no incentives to raise their offers to attract holdouts (i.e., types ) together with the market sellers. These conditions are formally stated and shown to be sufficient in Online Appendix LABEL:Asec:SL.

These conditions are not easy to check, so it is difficult to establish the existence of the equilibrium (or its sufficient condition) in a simple manner. Nevertheless, SSE exist for a range of bailout offers under many common distribution functions . For example, Figure 9-(a) in Section III.C) shows (a continuum of) SSE when is uniform.

On the other hand, SSE do not exist if is sufficiently high. More precisely, as stated in (iii) of Theorem 3, SSE disappear if . Roughly speaking, if is sufficiently high, accepting the government offer becomes very attractive, so the measure of firms selling to the market in vanishes. This induces the buyers in market to target holdouts with a high offer; anticipating this, in high-type firms would deviate to hold out instead of selling to the government, undermining the SSE. One implication of this condition is that the policy maker can avoid triggering undesirable SSE by making the bailout offer sufficiently generous—a point that will become clear as we now turn to delayed stimulation equilibria.

III.B Delayed Stimulation Equilibria (DSE)

Delayed Stimulation Equilibria (DSE) have the structure that in the characterization in Lemma 1, as illustrated in Figure 8. We call this delayed stimulation equilibrium since much of the stimulation effect materializes in . In particular, the highest type that trades does so in . Types act similarly as in the SSE: nonnegative fractions and of types sell respectively to the government and to the market, and types sell only to the government, where .

What makes this equilibrium possible is the incentive that buyers have to offer a sufficiently high price to high-type firms holding out in . Such an incentive was absent in SSE due to a sizable fraction of low-type market sellers. These firms cannot be distinguished from high-type hold-out firms and, therefore, would inflict a loss to buyers if they were to raise offers to attract high-type hold-out firms. In DSE, the fraction of low-type market sellers is sufficiently small, especially when is large, so that buyers do have an incentive to attract high-type holdouts, unlike in SSE.

We now provide the characterization of DSE.

Theorem 4 (Delayed stimulation equilibria).

There is a DSE if , where for each .232323In words, is the highest type such that types can be induced to sell to the market at a break-even price equal to their conditional expectation. In the DSE, , and such that the following holds.

- (i)

-

Types sell in both periods, a positive (possibly the entire) measure of which accept the bailout.

- (ii)

-

Among types , those that sell to the market in (if they exist) receive price in and in the market, and those that accept the bailout sell assets at price in . Furthermore, these two groups of firms have the same average value of .

- (iii)

-

Types sell only in and to the government at price .

- (iv)

-

Types sell only in at price . Higher-type firms never sell in either period.

Proof.

See Appendix A.3. ∎

DSE are similar to SSE in two ways. First, just as in SSE, firms suffer from accepting a bailout in the market. That is, the market in offers a strictly lower price to the bailout recipients than those that did not accept the bailouts, which include the firms that sold to the market in and those that held out. Also as with SSE, this differential treatment of bailout recipients relative to initial market sellers in the market can occur in equilibrium only if it is counterbalanced by the opposite treatment of these two groups in . Specifically, a form of the no-arbitrage condition must hold for the firms that sell in both periods:

where is the equilibrium market price for asset in , and and are the equilibrium market offers to the recipients and the non-recipients of the bailout, respectively. In short, those selling in both periods must receive the same total payment.

Despite these similarities, there is a crucial difference, pertaining to the level of . Recall that in SSE, high-type firms accept the bailout in but withdraw from the market; this means that those participating in the market tend to have low value, which “pushes down” the market prices (both and ) to a level below . Hence, as captured by the above no-arbitrage equation and Theorem 3, in SSE, bailout stigma spreads to all firms selling in both periods, with the consequence that market prices for all assets fall below the laissez-faire level in both periods.

By contrast, in DSE, high-type firms hold out in and sell to the market, and their participation in the market “pushes up” its price for the non-recipients of the bailout. In fact, equilibrium dictates that must be at least , or else the holdouts would rather sell to the government at in and withdraw from the market. In fact, must equal , as stated in part (ii). To explain why, consider a simple case of DSE with ; that is, every firm with sells to the government in . (The proof treats all cases.) First of all, we must have , or no firm would ever sell only in since it would be strictly better to sell to the government in and withdraw from the market in . Suppose next . Then, by the indifference of type , we have

Since (by buyers’ break-even condition), we then have , or equivalently, . If a buyer offers a price , all types will sell to the deviating buyer because . Furthermore, the highest type that sells to the market over two periods will be determined by , or equivalently, . By definition of , however, we have , so the deviating buyer can make a profit, a contradiction.

The high price for the non-recipients in in turn incentivizes high-type firms to hold out, validating the premise of the DSE. More interestingly, the high price is not just enjoyed by the holdouts but also by the market sellers. This feature keeps the bailout stigma from spreading to the market sellers. Quite the contrary, their good reputation “propped up” by the holdouts mitigates the stigma suffered by the bailout recipients. This can be seen in the above no-arbitrage equation. Substituting in that equation yields : the bailout recipients enjoy the same price in the market as the price that prevails in the market. This is why, unlike SSE, the laissez-faire price can be supported for both market as well as for the markets.242424Several steps are needed to arrive at this conclusion. First, since the buyers must break even, the observation earlier implies that the average types of bailout recipients and market sellers must be identical and thus equal to . This, together with the fact that the marginal type must be indifferent to selling in both periods versus selling only in one period gives rise to , the condition that defines the laissez-faire cutoff in (1). It now follows immediately that . In a nutshell, the high-type firms’ holdout decision keeps bailout stigma from freezing the markets. Although the government offer does not boost the private market offer as in Tirole (2012)’s static setup, it does not suppress the market offer, unlike in SSE.

The above discussions lead to the following key observation.

Corollary 1.

Each DSE is equivalent to an equilibrium under secret bailout (described in Theorem 2) in total volume of asset sales—and thus in total investments undertaken by firms. The total volume of asset sales in any DSE exceeds that in SSE.

Proof.

See Appendix A.4.∎

One interesting, and perhaps surprising, implication of this result is that delays in the effect of a bailout should not be viewed as a policy failure, at least when compared to the secret bailout benchmark. Take a possible equilibrium where is very low; in fact, one can show that can be supported if is not too high (again such an equilibrium arises due to a large mass of high type firms holding out in ). In such an equilibrium, it may appear at that bailouts have no impact, since trading and investment activity have not changed after the government offer. The impression would be that government purchases “crowded out” private purchases, since a positive measure of firms with sell to the government at a higher price than , the price they would have sold at in the absence of bailouts. Indeed, in the wake of the Great Recession, such a sentiment prevailed following the apparent lack of response by banks to the first wave of stimulation policies.252525In fact, as pointed out by Bolton et al. (2009), LIBOR-OIS spreads did not decrease following the implementation of the Fed’s emergency lending programs (such as the PDCF and the TSLF) during the 2007 – 2009 Great Recession. Bolton et al. (2011) also argued that the public liquidity programs, if implemented at a bad timing, will only crowd out the private liquidity supplied from the financial market. As can be seen, our theory provides a different perspective on the same phenomenon.

However, our result suggests that holdout by high-type firms is a blessing in disguise. The presence of these holdout firms is precisely what leads the market to make attractive offers to those that did not accept the bailout. Indistinguishable from these holdout firms, those that actually sold to the market in also receive attractive offers, thus overcoming the adverse selection endemic to the problem. The alleviation of adverse selection for these firms in turn creates “collateral benefits” to those that accept the bailout, since no arbitrage means that they can also overcome stigma. Consequently, the increase in trade volume in more than makes up for the initial under-response, when compared with SSE.

To an outsider observer, bailouts could very well be seen as “working” mysteriously here. Paradoxically, the policy invigorates the market by allowing high-type firms to send a strong signal on their financial strength by “rejecting” the bailout offer. This indirect signaling creates the desired stimulation effect later. As Corollary 1 suggests, the opportunity to “reject” a bailout turns out to be more profitable than “accepting” one.

To establish the existence of DSE, it is necessary to check that buyers in each period do not have an incentive to deviate from the prescribed equilibrium strategies on every equilibrium path. Just as with SSE, it is difficult to check these “no-deviation-by-buyers” conditions.262626Online Appendix LABEL:Asec:DS presents these necessary conditions and show them to be sufficient for equilibrium. Nevertheless, the equilibrium exists for a sufficiently large , as stated in Theorem 4. For example, the equilibrium always exists under the uniform distribution, as we show in Section III.C.

Corollary 1 also shows that, if a leads to a DSE under the transparent bailout, it yields the same total volume of trade as under a secret bailout. From this, one may conclude that bailout stigma is not of economic concern in a DSE. However, there are two caveats to this conclusion. First, there is a possibility of multiple equilibria, as we show in the next section. That is, the same may also support an SSE, which is clearly undesirable to a policy maker, as discussed previously. In order to avoid the selection of such an equilibrium, a policy maker may have to raise beyond the lower bound identified in Theorem 3-(iii). This, together with Theorems 4, suggests that a delayed equilibrium can be uniquely implemented by an offer . Second, a delay in and of itself may be undesirable for reasons not modeled in our theory. For instance, prompt revitalization of economic activities often has external benefits for the rest of the economy. In particular, if we consider financial institutions investing in the rest of the economy, a prompt restoration of their activities will have a positive spillover effect, and from this perspective delayed stimulation can be harmful. For these reasons, one may view the delay itself as a cost of stigma.

While it is difficult to find direct evidence on our equilibria, what transpired in the aftermath of the 2007–2009 Great Recession are somewhat consistent with our DSE. For instance, firms outright rejected rescue offers made by the government ostensibly to signal their financial strength, as mentioned in the introduction. In particular, our theory suggests that firms with high-quality assets are more likely to hold out when bailout terms are more generous (recall the difference between SSE and DSE.) Indeed, there is some evidence that firms with high-quality assets participated less in programs that were more generous. Krishnamurthy et al. (2014) find that, during the Great Recession, dealer banks with a large share of agency collaterals (i.e., collaterals guaranteed by the US government) rarely participated in the Primary Dealer Credit Facility (PDCF) despite their favorable funding rates, although they did participate in the Term Securities Lending Facility (TSLF) along with banks with a large share of non-agency collaterals (i.e., collaterals not guaranteed by the US government).

Remark 2 (The “full” freeze case: ).

We have so far implicitly assumed , for ease of exposition. But our equilibrium characterizations from Theorems 3 and 4 extend even to the case of ; that is, when the market would freeze completely absent any bailout. In this case, our characterizations imply that , and this leads to existence of a unique equilibrium. Given , the equilibrium admits a threshold such that types sell to the government in but do not sell in , and types hold out in but sell in at price , where satisfies . Types sell in neither period. One can think of this as a form of DSE: a bailout does not revive market in but induces delayed trading in . In keeping with Corollary 1, the equilibrium induces the same trade volume as a secret bailout would.

III.C Uniform Distribution Example

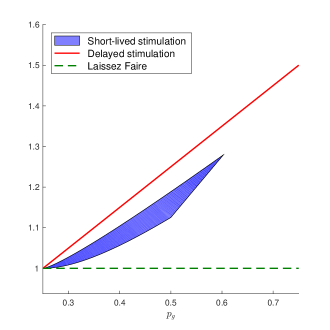

To gain a better understanding about the two types of equilibria and their possible coexistence, it is useful to exhibit them in full detail for some concrete parameter values. Assume uniform distribution , along with and . We choose these parameter values for the sake of exposition, as shown in Figure 9 below. However, the qualitative results shown in Figure 9 hold more generally for (so that ) and .

The left panel (a) of Figure 9 depicts the set of threshold types supported in SSE for various bailout terms . The corresponding threshold type for DSE is , as indicated by the straight red line. The right panel (b) of Figure 9 depicts the total volume of trade induced by SSE (blue area) and DSE (red line) for differing levels of .

This explicit example leads us to several interesting observations. First, as can be seen clearly by the blue area, for a range of ’s, there is a continuum of SSE that induce different threshold values of for each in that range. Note also that SSE exist for , but do not exist when is sufficiently high. Specifically, SSE exist only for , which is well below the upper bound identified in Theorem 3-(iii). Although not shown in the figure, typically multiple DSE exist, but all of them induce the same threshold and the same total trade volume, as formally stated in Theorem 4.

Second, both types of equilibria coexist for a range of bailout offers, as can be seen in the figure. This multiplicity reflects the endogenous nature of equilibrium belief formation. Given a , suppose a large measure of high-type firms accept a bailout but boycott the market to avoid stigma. This causes buyers to adjust down their offers in the market, in turn validating the firms’ decision not to hold out in . An SSE then arises. By contrast, if a large measure of high-type firms hold out in for the same , then buyers in make high offers to attract them, which in turn validates their decision to hold out, leading to a DSE.

Third, as can be seen from Figure 9-(b), the effect of bailout can be discontinuous with respect to the terms of bailout. Suppose the policy maker raises the bailout term starting from a low value close to . At first, an SSE may arise. As rises past , however, SSE disappear. Instead, the market shifts to a DSE, characterized by an increase in trade volume at a delay. As mentioned before, one policy implication is that the policy maker may need to choose an attractive bailout offer ( in this example) in order to avoid the selection of less desirable SSE.

Lastly, despite the stigma, a bailout with boosts overall trade regardless of the types of equilibria selected. As shown in Figure 9-(b), the total trade volume in SSE is strictly higher than , the total trade volume in the benchmark without bailout. This suggests that the positive effect of bailout on asset trading in —that is, every type sells in —outweighs the negative effect of stigma on asset trading in . Further, as can be seen in Figure 9-(b), the total trade volume in SSE tends to increase with , so a more generous bailout tends to have a higher stimulation effect.

IV Cost of Bailouts and the Optimal Bailout Policy

So far, we have abstracted from the cost of bailouts, which is nevertheless a crucial element of policy debates. In this section, we evaluate the effect of bailout programs while explicitly accounting for the cost of bailouts. To model the cost, we follow the literature (Tirole (2012), Chiu and Koeppl (2016)) and assume that raising a dollar of public funds in use for the asset purchase program costs the society dollars, where represents the deadweight loss of raising public funds, such as distortionary taxation. While a budget deficit entails social cost, we assume that a budget surplus does not contribute to any direct social welfare. This is in keeping with the primary purpose of government intervention here, which is to bail out distressed firms and to support socially desirable projects, and not to profit from the intervention itself.272727 This could be further justified by the assumption that profits from asset purchase are not easily converted to fund other government projects. If a budget surplus generates the commensurate welfare benefit— per dollar—, the results below are still valid as long as .

To evaluate the welfare of an equilibrium resulting from government bailouts, we adopt a mechanism design perspective. In so doing, we allow for the policy maker to offer a menu of (arbitrarily numerous) bailout programs, not just a single purchase offer, and to adopt any information policy with regard to the identities of the firms that accept the programs. Offering multiple bailout programs is realistic and policy relevant. During the Great Recession, numerous programs were introduced to help out financially distressed firms, which varied in bailout terms and generosity. Similarly, information is an important tool for the policy maker; the policy maker may craft the disclosure policy to fine-tune the degree to which the identity of a bailout recipient is revealed to the market.

While being fully general in these two dimensions, in keeping with our baseline model, we maintain the following assumptions: (a) the government programs are offered only in ; (b) the programs consist of a menu of asset purchase offers such that for all , for some arbitrarily high level , so that offered prices are at least as attractive as the laissez-faire price;282828Recall that the assumption that government offers take the form of asset purchase programs is without loss, given that the investment returns are not pledgeable. and (c) there is no rationing, meaning any (eligible) firms may choose any program made available by the government.

Formally, we represent the equilibrium outcome of a bailout policy by a pair of mappings, , where is a type- firm’s total asset sale across the two periods and is the total transfer it receives across the two periods in equilibrium. Naturally, there exist and transfer functions and of , measurable with respect to , such that . This transfer includes payment from both the government (if the firm accepts a bailout) and private buyers (if it sells to the market in either period). The fact that is nonfractional reflects the no-rationing assumption mentioned earlier. We can view these mappings as a direct mechanism that implements a social choice as a function of report on the firm’s type .

For the mechanism to represent an equilibrium outcome, it must satisfy incentive compatibility and participation constraints. It is worth emphasizing that these constraints are required only for the total two-period allocation and transfers . In general, depending on the information the policy maker makes available about the recipients of bailout programs in , further incentive constraints may be necessary for firms’ payoffs. By ignoring these additional constraints, we focus only on the necessary incentive constraints that must hold regardless of the information policy. In this sense, we allow for a fully general information policy.292929 The preceding observation already implies that total secrecy, which would obviate the need for additional incentive constraints for , is at least weakly optimal. This follows from the standard insight in mechanism design: secrecy, or “no information,” is tantamount to the pooling of incentive constraints across states, which relaxes the incentive constraints by requiring them to hold only on average rather than state by state. Given our incentive and participation constraints, one can invoke the celebrated revenue equivalence or envelope theorem to characterize the welfare of a particular equilibrium via the trade volume and a payoff for a reference type (e.g., the highest type) induced by the equilibrium. However, the additional constraints (a) and (b) make the standard method inapplicable. The following characterization, which reflects (a) and (b), is crucial for our analysis.

Lemma 2.

Fix any equilibrium outcome in which a positive measure of firms accept some government bailout program. Then,

- (i)

-

the total trade satisfies

(3) for some and ; and

- (ii)

-

the social welfare is:

(4) for some payoff accruing to the highest-type ().

Proof.

See Appendix A.5. ∎

Part (i) reflects the standard monotonicity condition necessary for incentive compatibility, in the presence of single crossing, as was the case with Lemma 1. The fact that the equilibrium trade volume takes a particularly simple form follows from (c), that is, the lack of rationing. The crucial part is that —or for all . This property, which reveals a fundamental limit to the effect of trade stimulation, follows from (a). Recall from Theorems 3 and 4 that both types of equilibria in Section III also exhibit the same limit; the claim here is that the limit applies even when the government offers a menu of bailout programs. Lastly, the fact that , which follows from (b), simply means that the government will never gain from suppressing the trade below the laissez-faire level.

Part (ii) shows that the welfare under a general bailout equilibrium consists of three terms. The first term, , is simply the value of a type- asset; recall that each firm owns 2 units of such an asset, and its value does not depend on the eventual owner of that asset. The second term describes the social welfare associated with inducing a trade for a type- firm. Sale of an asset by a type -firm yields social benefit of , the return to the project enabled by the sale. Meanwhile, it creates a budget shortfall of , which inflicts a cost of to society.303030 To check the marginal budget shortfall caused by a sale by the type- firm, note that where we used the envelope theorem to substitute for . Intuitively, the inverse hazard term, , is the incentive cost that is required to induce type- firm to sell an additional unit of its asset: since any sale by type can be mimicked by all lower types, these types must be paid rents to prevent their mimicking. The project return acts as an incentive for sale, and thus mitigates the budget shortfall and saves the subsidy needed to induce a sale. Finally, a rent of accrues to the highest-type () firm (namely, above its asset value ) and adds to the budget shortfall, inflicting a social cost of .313131By the standard envelope theorem reasoning, any rent enjoyed by the highest type is enjoyed by “all” firm types. Effectively, such a rent amounts to a pure cash transfer. Even though we do not formally include pure subsidy as a possible policy tool, our model implicitly allows for such a possibility. Evidently, pure subsidy is never optimal here as it is dominated by asset purchase which entails a lower deficit.

If no firm accepts a government program in equilibrium, then the outcome is the same as the no-bailout benchmark described in Section II. The resulting trade rule is still described by (3) with , and the associated welfare is accurately characterized by (4).323232In that case, the budget shortfall reduces to zero, so the terms multiplied by vanish. See footnote 30.

Inspecting the welfare objective in (4), it is immediate that the rents accruing to the highest type serves no purpose; they only entail social cost without stimulating any trade. Hence, the optimal policy has ; this is accomplished by limiting the generosity of offers. In light of Lemma 2, the mechanism design problem is therefore reduced to finding two cutoffs and that solve:

subject to:

The optimal solution depends on the cost of public fund, in particular, whether it is less than a threshold .

Theorem 5.

The following characterizes the optimal bailout policy.

- (i)

-

The uniquely optimal outcome is characterized by a trade rule in (3) with cutoffs and , where , with no rents accruing to the highest type.333333Here, the “unique” optimality means that any equilibrium outcome where differs from for a positive measure of ’s is strictly welfare dominated by , where is the transfer rule implementing with zero rents accruing to the highest type.

- (ii)

-

If , then the optimal outcome is implemented by no intervention; and if , then it is implemented by a secret bailout or, equivalently, a delayed-stimulation equilibrium under a single purchase offer of

- (iii)

-

The short-lived stimulation equilibrium is strictly suboptimal.

- (iv)

-

A menu of multiple transparent bailout offers is strictly suboptimal as long as positive measures of firms accept distinct bailout offers in equilibrium.

Proof.

See Appendix A.6. ∎

Theorem 5 summarizes several broad lessons learned from our general mechanism design analysis. Parts (i) and (ii) of the theorem suggest that the best possible outcome that the government can achieve with its bailout policy can be achieved by a single bailout offer made in total secrecy. A transparent bailout that leads to the delayed-stimulation equilibrium can also achieve the same outcome, but the possible multiplicity of equilibria complicates the problem, as we discuss below.

First, the optimality of total secrecy means that even if the government can design its information policy with regard to firms’ acceptance of the offers without any constraints, it can never do strictly better than keeping the market in the dark about the identities of the bailout recipients. This follows from the fact that the information revelation and separation of types exacerbate adverse selection and market unraveling (recall footnote 29). In light of Corollary 1, this means that the optimum can be attained by the DSE under transparency, which is important in practice given the difficulty of maintaining secrecy. In particular, this implies that the SSE is strictly worse, as stated in part (iii). Note that this conclusion is not a priori obvious from Corollary 1, since for any DSE associated with , an SSE with some suitably chosen may implement the same total volume of trade. What part (iii) suggests is that even when such an offer exists, it would require a strictly higher deficit on the part of the government and therefore a strictly higher social cost. Intuitively, a more severe stigma arising from that equilibrium requires a larger deficit to support the same level of stimulation. Admittedly, the bailout offer that implements the optimal outcome under a DSE may also admit a less desirable SSE. To avoid this situation, the policy maker may need to raise the offer even further to a level for which the latter type of equilibrium is no longer possible, although this may not implement the optimal policy. This result is also consistent with the Fed’s decision to lower the interest rate charged to the banks borrowing from the Discount Window in the early phase of the Great Recession.

The second implication of part (ii) is that it does not pay the policymakers to offer multiple bailout programs. Indeed, part (iv) shows that doing so under full transparency is strictly suboptimal in any equilibrium in which firms self-select into multiple programs. This finding does not necessarily contradict the approach taken by the US government in the wake of Great Recession. The plethora of bailout programs rolled out by the government targeted different segments of the financial market and the broader economy, whereas part (iv) concerns the multiplicity of programs targeting the same segment of the economy. One example of the latter case is the coexistence of the Discount Window (DW) and the Term Auction Facility (TAF), both of which targeted depository institutions. Our result suggests that the Fed could have improved the efficacy of the public liquidity provision if it had chosen either DW (at a very low borrowing rate) or TAF alone, but not both. Running both programs could have worsened the overall perception of not only the banks using the DW facility, but also the TAF users and the banks that did not participate in either program. Put differently, it is never desirable to offer a menu of multiple programs solely for the purpose of eliciting firms’ types. Doing so backfires by compounding the incentive constraints. The multiplicity of programs leads to more separation of firm types, which exacerbates adverse selection and market freeze.

V Related Literature

While the broad theme of this paper is related to an extensive literature on the benefits and costs of government intervention in distressed banks,343434The primary rationale for intervention is to prevent the contagion of bank runs whether it stems from depositor panic (Diamond and Dybvig (1983)), contractual linkages in bank lending (Allen and Gale (2000)), or aggregate liquidity shortages (Diamond and Rajan (2005), Diamond and Rajan (2012)). The costs of anticipated bailouts due to the time-inconsistency of the policy are discussed by, among others, Stern and Feldman (2004); the optimal response to the time inconsistency problem is studied in Green (2010), Chari and Kehoe (2016), and Keister (2016). our work is most closely related to Philippon and Skreta (2012) and Tirole (2012), who focus on adverse selection in asset markets as a primary reason for government intervention.353535Regarding the optimal form of bailouts, Philippon and Skreta (2012) show that optimal interventions involve the use of debt instruments when adverse selection is the main issue. With additional moral hazard but limits on pledgeable income, Tirole (2012) justifies asset purchases. When there is debt overhang due to lack of capital, Philippon and Schnabl (2013) find that optimal interventions take the form of capital injection in exchange for preferred stock and warrants. During the US subprime crisis, the Emergency Economic Stabilization Act (EESA) initially granted the Secretary of the Treasury authority to purchase or insure troubled assets owned by financial institutions. However, the Capital Purchase Program under the TARP switched to capital injection against preferred stock and warrants. As mentioned previously, these studies do not explicitly study the dynamic consequence of receiving a bailout—the focus of the current study. Even though these papers recognize that relatively low types accept bailouts, this does not translate into an adverse effect on subsequent financing in their models. Our dynamic model captures not only how bailout stigma affects firms’ financing behavior but also how the stigma fundamentally alters the role of a bailout. In particular, our most striking takeaway is the ability of firms to favorably signal their type by “refusing” an attractive bailout offer, which has no analogue in these or other antecedent studies.

Banks’ reputational concerns are explicitly considered in Ennis and Weinberg (2013), La’O (2014), Chari et al. (2014), Ennis (2019), and Hu and Zhang (2021). In Ennis and Weinberg (2013), to meet their short-term liquidity needs, banks with high-quality assets use interbank lending while those with low-quality assets use the discount window. The resulting discount window stigma is reflected in the subsequent pricing of assets. In La’O (2014), financially strong banks use the Federal Reserve’s Term Auction Facility since winning the auction at a premium signals financial strength, which protects them from predatory trading. Hu and Zhang (2021) study the banks’ choice between the Discount Window and Term Auction Facility (TAF) where funds are immediately available from the Discount Window, albeit entailing a stigma, whereas TAF releases funds with delay. They show how banks self-select themselves into different programs. The main focus in Chari et al. (2014) is on how reputational concerns in secondary loan markets can result in persistent adverse selection. Since all three studies consider discrete types of banks and there is no government bailout, their results are not directly comparable to ours. Ennis (2019) extends Philippon and Skreta (2012) by allowing banks to borrow from the discount window before borrowing from the market, thereby formalizing the discount window stigma alluded to in Philippon and Skreta (2012). There are two main differences between Ennis (2019) and our work. First, there is only one investment opportunity in Ennis (2019), hence it does not capture the dynamics of a stimulation effect (e.g., the possibility of stimulation being either short-lived or delayed). Second, Ennis (2019) characterizes equilibria for exogenously given discount window rates, whereas we study the optimal bailout policy.

Our paper is also related to studies on dynamic adverse selection in general (Inderst and Müller (2002), Janssen and Roy (2002), Moreno and Wooders (2010), Camargo and Lester (2014), Fuchs and Skrzypacz (2015)) and those with a specific focus on the role of information in particular (Hörner and Vieille (2009), Daley and Green (2012), Fuchs et al. (2016), Kim (2017)).363636Others include dynamic extensions of Spence’s signaling model with public offers (Noldeke and Van Damme (1990)), private offers (Swinkels (1999)), and private offers with additional public information such as grades (Kremer and Skrzypacz (2007)). The key insight from the first set of studies is that dynamic trading generates sorting opportunities, which are not available in the static market setting. However, each seller has only one opportunity to trade in these studies, so signaling is not an issue. The second set of studies relates to different disclosure rules and how they affect dynamic trading. For example, Hörner and Vieille (2009) and Fuchs et al. (2016) show that secrecy (private offers) tends to alleviate adverse selection but transparency (public offers) does not. Once again, each seller has only one trading opportunity in these studies. Hence, although past rejections can boost reputation, acceptance ends the game. In contrast, in our model, acceptance as well as rejection of the bailout offer work as signaling opportunities. Although our model also shows that secret bailouts weakly dominate transparent bailouts, none of these papers studies government intervention in response to market failure.

There are several empirical studies that provide evidence on stigma in the financial market. Peristiani (1998) provides early evidence on the discount window stigma. Furfine (2001, 2003) finds similar evidence from the Federal Reserve’s Special Lending Facility during the period 1999-2000 and the new discount window facility introduced in 2003. Armantier et al. (2015) utilize the Federal Reserve’s Term Auction Facility bid data from the 2007-2008 financial crisis to estimate the cost of stigma and its effect. Cassola et al. (2013) find evidence of stigma from the bidding data from the European Central Bank’s auctions of one-week loans. Krishnamurthy et al. (2014) find that in repo financing, dealer banks with higher shares of agency collateral repayments, that is, collateral (implicitly) guaranteed by the government, borrowed less from the Primary Dealer Credit Facility (PDCF) despite its attractive funding terms, which indeed supports the existence of a stigma attached to the users of the PDCF.

Finally, there is a vast literature discussing the 2008 Great Recession. Congressional Budget Office (2012) estimates the overall cost of the TARP at approximately $32 billion, the largest part of which stems from assistance to AIG and the automotive industry while capital injections to financial institutions are estimated to have yielded a net gain. For detailed assessments of the various programs in the TARP, see the Journal of Economic Perspectives (2015). See also Fleming (2012), who discusses how the various emergency liquidity facilities provided by the Federal Reserve during the 2007-2009 crisis were designed to overcome the limitations of traditional policy instruments at the time of crisis. Tong and Wei (2020) provide international evidence on the effect of unconventional interventions during 2008-2010.

VI Conclusion

The current paper has studied a dynamic model of a government bailout in which firms have a continuing need to fund their projects by selling their assets. Asymmetric information about the quality of assets gives rise to adverse selection and a concommitant market freeze, which provides a rationale for a government bailout, just as in Tirole (2012). However, in contrast to Tirole (2012), markets stigmatize bailout recipients, which jeopardizes their ability to fund subsequent projects. The presence of this bailout stigma and other dynamic incentives yields a much more complex and nuanced portrayal of how bailouts impact the economy than have been recognized in the extant literature.