Halting Time is Predictable for Large Models:

A Universality Property and Average-case Analysis

Abstract

Average-case analysis computes the complexity of an algorithm averaged over all possible inputs. Compared to worst-case analysis, it is more representative of the typical behavior of an algorithm, but remains largely unexplored in optimization. One difficulty is that the analysis can depend on the probability distribution of the inputs to the model. However, we show that this is not the case for a class of large-scale problems trained with first-order methods including random least squares and one-hidden layer neural networks with random weights. In fact, the halting time exhibits a universality property: it is independent of the probability distribution. With this barrier for average-case analysis removed, we provide the first explicit average-case convergence rates showing a tighter complexity not captured by traditional worst-case analysis. Finally, numerical simulations suggest this universality property holds for a more general class of algorithms and problems.

Key words. universality, random matrix theory, optimization

AMS Subject Classification. 60B20, 90C06, 90C25, 65K10, 68T07

1 Introduction

Traditional worst-case analysis of optimization algorithms provides complexity bounds for any input, no matter how unlikely (Nemirovski, 1995; Nesterov, 2004). It gives convergence guarantees, but the bounds are not always representative of the typical runtime of an algorithm. In contrast, average-case analysis gives sharper runtime estimates when some or all of its inputs are random. This is often paired with concentration bounds that quantify the spread of those estimates. In this way, it is more representative of the typical behavior.

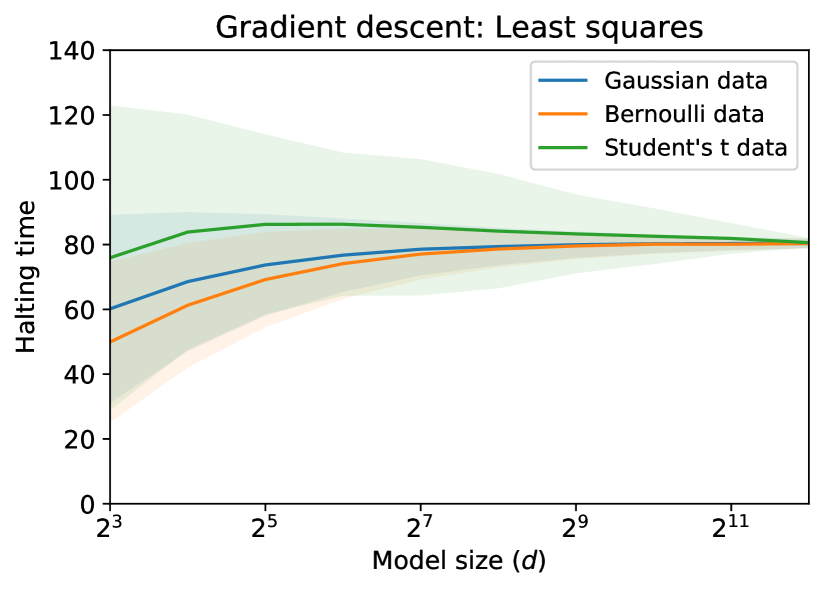

Yet, average-case analysis is rarely used in optimization because the complexity of algorithms is assumed to depend on the specific probability distribution of the inputs. Surprisingly, simulations reveal this is not the case for large-scale problems (see Figure 1).

We show that almost all instances of high-dimensional data are indistinguishable to first-order algorithms. Particularly, the halting time, i.e. the number of iterations to reach a given accuracy, for any first-order method converges to a deterministic value which is independent of the input distribution (see Figure 1). Since the halting time is deterministic, the empirical complexity coincides almost surely with the average-case rates.

[notespar,

caption = Comparison of convergence guarantees for non-strongly convex objectives in terms of asymptotic behavior of as problem size and iteration are large in the isotropic features model. The average-case guarantees are strictly faster than the traditional worst-case and adversarial rates. Furthermore, the traditional worst-case complexity bounds depend on the distance to the optimum which under our constant signal-to-noise model, grows as the problem size, or dimension, , increases. The ‘without noise’ setting refers to the case when the targets equal with the signal and the ‘noisy’ setting when the targets follow a generative model but are corrupted by noise, that is, , where is a noise vector. The rates are stated in terms of an absolute constant , the amount of signal and noise , the ratio of number of features to samples , and the maximum and minimum eigenvalues. Denote the maximum value of the squared Bessel function of the first kind over . See Section 1.2 and 5 for derivations and definitions of terms such as non-strongly convex., captionskip=2ex,

label=tab:comparison_worst_avg_cvx,

pos =ht!

]clll\tnote[1]In the noisy setting, we lower bounded by (see Lemma 5.1) to the worst-case complexity bound provided in Taylor et al. (2017, Section 4.1.3). \tnote[2]Nesterov (2004); Beck and Teboulle (2009)

\tnote[3]Nesterov (2012) \tnote[4]Adversarial model maximizes the norm of the gradient subject to a fixed condition number (see Section 1.2). \tnote[5]When noise is added, the convergence rates are dominated by the term with in (4).

Method

Non-strongly cvx

w/o noise

Non-strongly cvx

w/ noise\tmark[5]

Gradient descent (GD)

Worst\tmark[1]

Adversarial\tmark[4]

Average

Nesterov

accelerated method \tmark[2]

Worst \tmark[3]

Adversarial

Average

[notespar, caption = Comparison of convergence guarantees for strongly convex objectives in terms of asymptotic behavior of as problem size and iteration are large in the isotropic features model. Average-case matches the worst-case asymptotic guarantees multiplied by an additional polynomial correction term (green). This polynomial term has little effect on the complexity compared to the linear rate. However as the matrix becomes ill-conditioned , the polynomial correction starts to dominate the average-case complexity. Indeed this shows that the support of the spectrum does not fully determine the rate. Many eigenvalues contribute meaningfully to the average-rate.

See Section 5 for derivations and Table LABEL:tab:comparison_worst_avg_cvx for definition of terms in the rates.,

label= tab:comparison_worst_avg_str_cvx,

captionskip=2ex,

pos = ht!

]cll\tnote[1]Taylor et al. (2017, Section 4.1.3)

Method Strongly cvx w/ noise

Gradient descent (GD)

Worst\tmark[1]

Average

Polyak

(Polyak, 1964)

Worst

Average

Nesterov accelerated method

(Nesterov, 2004)

Worst

Average

Notation.

We write vectors in lowercase boldface () and matrices in uppercase boldface (). The norm gives the usual Euclidean -norm and is the usual operator-2 norm. Given a matrix , the largest eigenvalue of is and its smallest eigenvalue is . A sequence of random variables converges in probability to , indicated by , if for any , . In other words, the probability that is far from goes to as increases. Probability measures are denoted by and their densities by . We say a sequence of random measures converges to weakly in probability if for any bounded continuous function , we have in probability.

All stochastic quantities defined hereafter live on a probability space denoted by with probability measure and the -algebra containing subsets of . A random variable (vector) is a measurable map from to respectively. Let be a random variable mapping into the Borel -algebra and the set . We use the standard shorthand for the event .

1.1 Main results

In this paper, we analyze the halting time and develop the first explicit average-case analysis for first-order methods on quadratic objectives. Quadratic objective functions are rich enough to reproduce the dynamics that arise in more complex models, yet simple enough to be understood in closed form. Quadratic models are receiving renewed interest in the machine learning community as recent advances have shown that over-parameterized models, including neural networks, have training dynamics similar to those of quadratic problems (Jacot et al., 2018; Novak et al., 2019; Arora et al., 2019; Chizat et al., 2019).

The precise form of the quadratic problem we consider is

| (1) |

where is the data matrix, is the signal vector 111The signal is not the same as the vector for which the iterates of the algorithm are converging to as ., and is a source of noise. All of these inputs will possibly be random and the target is produced by a generative model corrupted by noise. We refer to the noiseless (without noise) setting when and the noisy setting as .

We work in the following setting: Both the number of features and data dimension grow to infinity while tends to a fixed . We use to denote the magnitude of the noise. For intuition, we implicitly define to measure the strength of the signal222The definition of in Assumption 1 does not imply that . However the precise definition of and this intuitive one yield similar magnitudes and both are generated from similar quantities. ; we make the definition of precise in Assumption 1 of Section 2, one of two assumptions fundamental to this work. Throughout, the signal-to-noise ratio in is held constant as the problem size grows. Moreover, we assume that the data matrix is independent of both the signal, , and noise Note this, together with the generative model, allows for some amount of dependence between and the target We will also assume that has a well-defined limiting spectral density, denoted by , as (see Assumption 2 of Section 2).

Our first contribution is a framework to analyze the average-case complexity of gradient-based methods in the described setting. Our framework highlights how the algorithm, signal and noise levels interact with each other to produce different average-case convergence guarantees. The culmination of this framework is the average-case convergence rates for first-order methods (see Tables LABEL:tab:comparison_worst_avg_cvx and LABEL:tab:comparison_worst_avg_str_cvx).

Our framework is broad enough to facilitate multiple perspectives on average-case analysis. Our motivating and central application is the fully-average-case, in which we assume that all inputs are random. The quintessential random data model is isotropic features. This supposes the entries of are i.i.d. random variables with zero mean, equal variance, and bounded fourth moments, that is, for all . In a celebrated theorem of Marčenko and Pastur (1967), the spectrum of converges to a compactly supported measure as the problem size grows without any further assumptions on the distribution of the entries of . This limiting spectral distribution is known as the Marčenko-Pastur law:

| (2) |

However, our framework is built to be vastly more general. To start, the framework covers a fully-average-case analysis with other data models, such as the one-hidden layer network with random weights and the correlated features model (see Section 2.2). More to the point, this framework also allows for a type of semi-average-case analysis, in which only is taken to be random. When we do this and then choose in such a way as to maximize the halting time, we call this the adversarial average-case. See Section 1.2 for further details and motivations.

We now discuss the contents of this framework in detail, which is to say we survey how Assumptions 1 and 2 combine to show the halting time is concentrated and deterministic. The first step is to express the conditional expectation of the gradient at the -th iterate as a sum of expected traces of polynomials in the matrix (c.f. Proposition 4.3):

| (3) |

The polynomial , known as the residual polynomial, is a -th degree polynomial associated with the gradient-based algorithm. This tool of associating each algorithm with polynomials is a classic technique in numerical iterative methods for solving linear systems (Flanders and Shortley, 1950; Golub and Varga, 1961; Fischer, 1996; Rutishauser, 1959). Such polynomials are used to prove convergence of some of the most celebrated algorithms like the conjugate gradient method (Hestenes and Stiefel, 1952). Explicit expressions of the residual polynomials for Nesterov’s accelerated methods (Nesterov, 2004; Beck and Teboulle, 2009), both convex and strongly convex, as well as, gradient descent and Polyak’s momemtum (a.k.a Heavy-ball) (Polyak, 1964) are derived in Section 3. These polynomials may be of independent interest.

The result in (3) gives an exact expression for the expected gradient depending only on traces of powers of , which in turn can be expressed in terms of its eigenvalues. Our second main assumption (Assumption 2) then ensures that these traces converge to integrals against the spectral density In summary, the squared gradient norm concentrates to a deterministic quantity, 333 In many situations this deterministic quantity is in fact the limiting expectation of the squared-norm of the gradient. However, under the assumptions that we are using, this does not immediately follow. It is however always the limit of the median of the squared-norm of the gradient.444Technically, there is no need to assume the measure has a density – the theorem holds just as well for any limiting spectral measure . In fact, a version of this theorem can be formulated at finite just as well, thus dispensing entirely with Assumption 2 – c.f. Proposition 4.3. :

Theorem 1.1 (Concentration of the gradient).

Notably, the deterministic value for which the gradient concentrates around depends only on through its eigenvalues.

The concentration of the norm of the gradient above yields a candidate for the limiting value of the halting time, or the first time the gradient falls below some predefined . We define this candidate for the halting time from and we denote the halting time , by

| (5) |

We note that the deterministic value is, by definition, the average complexity of the first-order algorithm. This leads to our second main result that states the almost sure convergence of the halting time to a constant value.

Theorem 1.2 (Halting time universality).

A result of this form previously appeared in Deift and Trogdon (2020) for the conjugate gradient method.

1.1.1 Extension beyond least squares, ridge regression

One extension of Theorems 1.1 and 1.2 to other objective functions is the ridge regression problem or -regularization, that is, we consider a problem of the form

| (7) |

As discussed above, we assume that is (possibly random) data matrix, is an unobserved signal vector, and is a noise vector. We make the same assumptions on the limiting spectral measure of , the ratio of features to samples, that is, tends to some fixed as , and the magnitude of the noise . In addition to the independence assumption between the data matrix and the signal and , we add that the signal and the initialization are also independent of each other with magnitudes and (see Assumption 3 for precise statement). The constant is the ridge regression parameter.

The addition of the -regularizer to the least squares problem alters the Hessian of the least squares by adding a multiple of the identity. Therefore the matrix and its eigenvalues play the role of and its eigenvalue in Theorem 1.1. The result is the following theorem.

Theorem 1.3 (Concentration of the gradient for ridge regression).

Here is the limiting spectral density of . The limiting gradient (8) decomposes into three terms which highlight the effects of initialization, signal, and noise. This is unlike the two terms in (4) which illustrate the noise and signal/initialization effects. The extra term in (8) only adds to the magnitude of the gradient due to the independence between the signal and initialization. We also note that the matrix always has eigenvalues bounded away from even in the limit as . As such, we expect linear convergence. By defining the right-hand side of (8) to be , it follows that Theorem 1.2 holds under Assumption 3 in replace of Assumption 1. For additional discussion see Section 4.4.

1.2 Comparison between average and worst-case

The average-case analysis we develop in this paper is effective in the large problem size limit, whereas worst-case analysis is performed for a fixed matrix size. This implies that there are potentially dimension-dependent quantities which must be addressed when making a comparison.

For example, all the first-order methods considered here converge linearly for the finite-dimensional least squares problem: the rate is determined by the gap between the smallest nonzero eigenvalue of the matrix and . However this could very well be meaningless in the context of a high-dimensional problem, as this gap becomes vanishingly small as the problem size grows.

In the context of the isotropic features model, when the ratio of features to samples is this is precisely what occurs: the smallest eigenvalues tend to as the matrix size grows. In contrast, when is bounded away from , the least squares problem in (1) has a dimension-independent lower bound on the Hessian which holds with overwhelming probability, (c.f. Figure 2). However, for the comparison we do here, there is another dimension-dependent quantity which will have a greater impact on the worst-case bounds.

Before continuing, we remark on some terminology we will use throughout the paper. While for any realization of the least squares problem the Hessian is almost surely positive definite, as problem size grows, the matrix can become ill-conditioned, that is, the smallest eigenvalues tend to as when . Consequently, the computational complexity of first-order algorithms as exhibit rates similar to non-strongly convex problems. On the other hand, when is bounded away from , the gap between the smallest nonzero eigenvalue of and 0 results in first order methods having complexity rates similar to strongly convex problems. We use this terminology, non-strongly convex and strongly convex, in Tables LABEL:tab:comparison_worst_avg_cvx and LABEL:tab:comparison_worst_avg_str_cvx to distinguish the different convergence behaviors when and resp. and for worst-case complexity comparisons.

Worst-case rates and the distance to optimality.

Typical worst-case upper bounds for first-order algorithms depend on the distance to optimality, . For example, let us consider gradient descent (GD). Tight worst-case bounds for GD in the strongly convex and convex setting (Taylor et al., 2017), respectively, are

where is the solution to (1) found by the algorithm, i.e, the iterates of the algorithm converge .

To formulate a comparison between the fully-average-case rates, where follows isotropic features, and the worst-case rates, we must make an estimate of this distance to optimality . In the noiseless setting , the expectation of is a constant multiple of . In particular, it is independent of the dimension. Similarly when we have dimension-independent-strong-convexity, even with noisy targets , the distance to the optimum is well-behaved and is a constant involving and . Hence, a direct comparison between worst and average-case is relatively simple.

For the ill-conditioned case when , the situation is more complicated with noisy targets. To maintain a fixed and finite signal-to-noise ratio, the distance to optimality will behave like ; that is, it is dimension-dependent.555Precisely, we show that is tight (see Section 5, Lemma 5.1). So the worst-case rates have a dimension-dependent constant whereas the average-case rates are dimension-independent. This dimension-dependent term can be see in the last column of Table LABEL:tab:comparison_worst_avg_cvx. Conversely, if one desires to make constant across dimensions using a generative model with noise, one is forced to scale to go to zero as , thus reducing the full generative model to the noiseless regime.

Adversarial model.

As mentioned above, the comparison with existing worst-case bounds is problematic due to dimension-dependent factors. To overcome this, we consider the following adversarial model. First, we assume a noisy generative model for (Assumption 1 holds). Next, our adversary chooses the matrix without knowledge of to maximize the norm of the gradient subject to the constraint that the convex hull of the eigenvalues of equals . For comparison to the average-case analysis with isotropic features, we would choose to be the endpoints of the Marčenko-Pastur law. In light of Theorem 1.1, the adversarial model seeks to solve the constrained optimization problem

| (9) |

We call this expression the adversarial average-case guarantee.

The main distinction between worst-case and adversarial average-case is that traditional worst-case maximizes the gradient over all inputs – both targets and data matrix . This leads to dimension–dependent complexity, as there are usually exceptional target vectors that are heavily dependent on the data matrix (such as those built from extremal singular vectors of ) and cause the algorithm to perform exceptionally slowly.

In contrast, the adversarial average-case keeps the randomness of the target while maximizing over the data matrix . This is a more meaningful worst-case comparison: for example, in the setting of linear regression, the response and measurements of the independent variables are typically generated through different means and have different and independent sources of noise (see for example (Walpole and Myers, 1989, Example 10.1). Hence the independence of the noise intervenes to limit how truly bad the data matrix can be. Furthermore, the complexity of the adversarial average-case is dimension-independent. Table LABEL:tab:comparison_worst_avg_cvx shows these adversarial complexities for non-strongly convex objectives (1). Similar results can also be derived for strongly convex objectives but are omitted for brevity.

Comparison with adversarial and worst-case complexities.

By construction, the average-case convergence rates are at least as good as the worst-case and adversarial guarantees. The average-case complexity in the convex, noiseless setting () for Nesterov’s accelerated method (convex) (Nesterov, 2004; Beck and Teboulle, 2009) and gradient descent (GD) are an order of magnitude faster in than the worst case rates (see Table LABEL:tab:comparison_worst_avg_cvx, first column). It may appear at first glance (Table LABEL:tab:comparison_worst_avg_cvx) that there is a discrepancy between the average-case and exact worst-case rate when and noisy setting (). As noted in the previous section, the worst-case rates have dimension-dependent constants. Provided the dimension is bigger than the iteration counter ( for GD and for Nesterov), the average complexity indeed yields a faster rate of convergence. Average-case is always strictly better than adversarial rates (see Table LABEL:tab:comparison_worst_avg_cvx). This improvement in the average rate indeed highlights that the support of the spectrum does not fully determine the rate. Many eigenvalues contribute meaningfully to the average rate. Hence, our results are not and cannot be purely explained by the support of the spectrum.

The average-case complexity in the strongly convex case matches the worst-case guarantees multiplied by an additional polynomial correction term (green in Table LABEL:tab:comparison_worst_avg_str_cvx). This polynomial term has little effect on the complexity compared to the linear rate. However as the matrix becomes ill-conditioned , the polynomial correction starts to dominate the average-case complexity. The sublinear rates in Table LABEL:tab:comparison_worst_avg_cvx show this effect and it accounts for the improved average-case rates.

Our average-case rates accurately predict the empirical convergence observed in simulations, in contrast to the worst-case rates (see Figure 3). Although our rates only hold on average, surprisingly, even a single instance of GD exactly matches the theoretical predictions. Moreover, the noisy non-strongly convex worst-case is highly unpredictable due to the instability in across runs. As such, the worst-case analysis is not representative of typical behavior (see Figure 3).

These theoretical results are supported by simulations and empirically extended to other models, such as logistic regression, as well as other algorithms, such as stochastic gradient descent (SGD) (see Section 6). This suggests that this universality property holds for a wider class of problems.

Related work.

The average-case analysis has a long history in computer science and numerical analysis. Often it is used to justify the superior performance of algorithms as compared with their worst-case bounds such as Quicksort (sorting) (Hoare, 1962) and the simplex method in linear programming, see for example (Spielman and Teng, 2004; Smale, 1983; Borgwardt, 1986; Todd, 1991) and references therein. Despite this rich history, it is challenging to transfer these ideas into continuous optimization due to the ill-defined notion of a typical continuous optimization problem. Recently Pedregosa and Scieur (2020); Lacotte and Pilanci (2020) derived a framework for average-case analysis of gradient-based methods and developed optimal algorithms with respect to the average-case. The class of problems they consider is a special case of (1) with vanishing noise. We use a similar framework – extending the results to all first-order methods and noisy quadratics while also providing concentration and explicit average-case convergence guarantees.

A natural criticism of a simple average-case analysis is that the complexity is data model dependent and thus it only has predictive power for a small subset of real world phenomena. Because of this, it becomes important to show that any modeling choices made in defining the data ensemble have limited effect. Paquette and Trogdon (2020) showed that the halting time for conjugate gradient becomes deterministic as the dimension grows and it exhibits a universality property, that is, for a class of sample covariance matrices, the halting times are identical (see also Deift and Trogdon (2020)). It is conjectured that this property holds in greater generality – for more distributions and more algorithms (Deift et al., 2014; Deift and Trogdon, 2018)). In Sagun et al. (2017), empirical evidence confirms this for neural networks and spin glass models. Our paper is in the same spirit as these– definitively answering the question that all first-order methods share this universality property for the halting time on quadratic problems.

This work is inspired by research in numerical linear algebra that uses random matrix theory to quantify the “probability of difficulty” and “typical behavior” of numerical algorithms (Demmel, 1988). For many numerical linear algebra algorithms, one can place a random matrix as an input and analyze the algorithm’s performance. It is used to help explain the success of algorithms and heuristics that could not be well understand through traditional worst-case analysis. Numerical algorithms such as the QR (Pfrang et al., 2014), Gaussian elimination (Sankar et al., 2006; Trefethen and Schreiber, 1990), and other matrix factorization algorithms, for example, symmetric triadiagonalization and bidiagonalization (Edelman and Rao, 2005) have had their performances analyzed under random matrix inputs (typically Gaussian matrices). In Deift and Trogdon (2019), an empirical study extended these results beyond Gaussian matrices and showed that the halting time for a many numerical algorithms were independent of the random input matrix for a large class of matrix ensembles. This universality result eventually was proven for the conjugate gradient method (Paquette and Trogdon, 2020; Deift and Trogdon, 2020).

An alternative approach to explaining successes of numerical algorithms, introduced in (Spielman and Teng, 2004), is smoothed analysis. Smoothed analysis is a hybrid of worst-case and average-case analysis. Here one randomly perturbs the worst-case input and computes the maximum expected value of a measure for the performance of an algorithm. It has been used, for example, to successful analyze linear programming (Spielman and Teng, 2004), semi-definite programs (Bhojanapalli et al., 2018), and conjugate gradient (Menon and Trogdon, 2016). In this work, we instead focus on the random matrix approach to analyze first-order methods on optimization problems.

Our work draws heavily upon classical polynomial based iterative methods. Originally designed for the Chebyshev iterative method (Flanders and Shortley, 1950; Golub and Varga, 1961), the polynomial approach for analyzing algorithms was instrumental in proving worst-case complexity for the celebrated conjugate gradient method (Hestenes and Stiefel, 1952). For us, the polynomial approach gives an explicit equation relating the eigenvalues of the data matrix to the iterates which, in turn, allows the application of random matrix theory.

The remainder of the article is structured as follows: in Section 2 we introduce the full mathematical model under investigation including some examples of data models. Section 3 discusses the relationship between polynomials and optimization. Our main results are then described and proven in Section 4. Section 5 details the computations involved in the average-case analysis, the proofs of which are deferred to the appendix. The article concludes on showing some numerical simulations in Section 6.

2 Problem setting

In this paper, we develop an average-case analysis for first-order methods on quadratic problems of the form

| (10) |

where is a (possibly random) matrix (discussed in the next subsection), is an unobserved signal vector, and is a noise vector.

2.1 Data matrix, noise, signal, and initialization assumptions

Throughout the paper we make the following assumptions.

Assumption 1 (Initialization, signal, and noise).

The initial vector , the signal , and noise vector are independent of and satisfy the following conditions:

-

1.

The entries of are i.i.d. random variables and there exist constants such that for

(11) -

2.

The entries of the noise vector are i.i.d. random variables satisfying the following for and for some constants

(12)

Assumption 1 encompasses the setting where the signal is random and the algorithm is initialized at . But it is more general. Starting farther from the signal requires more iterations to converge. Hence, intuitively, (11) restricts the distance of the algorithm’s initialization to the signal so that it remains constant across problem sizes. The unbiased initialization about the signal, put another way, says the initialization is rotationally-invariantly distributed about the signal (see Figure 4).

Assumption 1 arises as a result of preserving a constant signal-to-noise ratio in the generative model. Such generative models with this scaling have been used in numerous works (Mei and Montanari, 2019; Hastie et al., 2019).

Tools from random matrix theory.

Random matrix theory studies properties of matrices (most notably, statistics of matrix eigenvalues) whose entries are random variables. We refer the reader to (Bai and Silverstein, 2010; Tao, 2012) for a more thorough introduction. Many important statistics of random matrix theory can be expressed as functionals on the eigenvalues of a matrix (e.g., determinants and traces). Let be the eigenvalues of and define the empirical spectral measure (ESM), , as

| (13) |

where is a Dirac delta function, i.e., a function equal to except at and whose integral over the entire real line is equal to one. The empirical spectral measure puts a uniform weight on each of the eigenvalues of . When is random, this becomes a random measure. A main interest in random matrix theory is to characterize the behavior of the empirical spectral measure as the dimension of the matrix tends to infinity.

Because the ESM is a well-studied object for many random matrix ensembles, we state the following assumption on the ESM for the data matrix, . In Section 2.2, we review practical scenarios in which this is verified.

Assumption 2 (Data matrix).

Let be a (possibly random) matrix such that the number of features, , tends to infinity proportionally to the size of the data set, , so that . Let with eigenvalues and let denote the Dirac delta with mass at . We make the following assumptions on the eigenvalue distribution of this matrix:

-

1.

The ESM converges weakly in probability to a deterministic measure with compact support,

(14) -

2.

The largest eigenvalue of converges in probability to the largest element in the support of . In particular, if denotes the top edge of the support of then

(15) -

3.

(Required provided the algorithm uses the smallest eigenvalue) The smallest eigenvalue of converges in probability to the smallest, non-zero element in the support of . In particular, if denotes the bottom edge of the support of then

(16)

2.2 Examples of data distributions.

In this section we review three examples of data-generating distributions that verify Assumption 2: a model with isotropic features, a correlated features model, and a one-hidden layer neural network with random weights. Numerous works studying the spectrum of the Hessian on neural networks have found that this spectrum shares many characteristics with the limiting spectral distributions discussed below including compact support, a concentration of eigenvalues near , and a stable top eigenvalue (Dauphin et al., 2014; Papyan, 2018; Sagun et al., 2016; Behrooz et al., 2019). In fact, the work of Martin and Mahoney (2018) directly compares the Hessians of deep neural networks at various stages in training with the Marčenko-Pastur density, that is, the limiting spectral density for the isotropic features model.

Isotropic features.

We will now elaborate on the well developed theory surrounding the isotropic features model (see (2) and the text just above it). In particular, parts 2 and 3 of Assumption 2 on the convergence of the largest and smallest eigenvalues is well known:

Lemma 2.1 (Isotropic features).

(Bai and Silverstein (2010, Theorem 5.8)) Suppose the matrix is generated using the isotropic features model. The largest and smallest eigenvalue of , and , resp., converge in probability to and resp. where is the top edge of the support of the Marčenko-Pastur measure and is the bottom edge of the support of the Marčenko-Pastur measure.

In addition, the isotropic features model is sufficiently random that it is possible to weaken Assumption 1 and still derive for it the conclusion of Theorem 1.1. In particular, we may let be defined as

| (17) |

for any deterministic sequences of vectors and from the -dimensional and the -dimensional spheres, respectively, multiplied by the signal strength and noise . Then, under the further moment assumption on that for any

| (18) |

it is a consequence of (Knowles and Yin, 2017, Theorem 3.6,3.7), that

| (19) |

This implies that for the isotropic features model under the stronger assumption for the data matrix (18), but the weaker target assumption (17), we obtain the same complexity results presented in Tables LABEL:tab:comparison_worst_avg_cvx and LABEL:tab:comparison_worst_avg_str_cvx. See also (Paquette and Trogdon, 2020, Corollary 5.12) in which a central limit theorem for the gradient is derived under these same assumptions

Correlated features.

In this model, one takes a random matrix generated from the isotropic features model and a symmetric positive definite correlation matrix . One then defines the correlated features model by

This makes the normalized sample covariance matrix of samples of a -dimensional random vector with covariance structure

Under the assumption that the empirical spectral measure of converges to a measure and that the norm of is uniformly bounded, it is consequence of Bai and Silverstein (1999, 1998) (see also the discussions in Bai and Silverstein (2004); Knowles and Yin (2017); Hachem et al. (2016)) that Assumption 2 holds. Unlike in isotropic features, the limiting spectral measure is not known explicitly, but is instead only characterized (in general) through a fixed-point equation describing its Stieltjes transform.

One-hidden layer network with random weights.

In this model, the entries of are the result of a matrix multiplication composed with a (potentially non-linear) activation function :

| (20) |

The entries of and are i.i.d. with zero mean, isotropic variances and , and light tails, that is, there exists constants and such that for any

| (21) |

Although stronger than bounded fourth moments, this assumption holds for any sub-Gaussian random variables (e.g., Gaussian, Bernoulli, etc). As in the previous case to study the large dimensional limit, we assume that the different dimensions grow at comparable rates given by and . This model encompasses two-layer neural networks with a squared loss, where the first layer has random weights and the second layer’s weights are given by the regression coefficients . In this case, problem (10) becomes

| (22) |

The model was introduced by (Rahimi and Recht, 2008) as a randomized approach for scaling kernel methods to large datasets, and has seen a surge in interest in recent years as a way to study the generalization properties of neural networks (Hastie et al., 2019; Mei and Montanari, 2019; Pennington and Worah, 2017; Louart et al., 2018; Liao and Couillet, 2018).

The most important difference between this model and the isotropic features is the existence of a potentially non-linear activation function . We assume to be entire with a growth condition and have zero Gaussian-mean,

| (23) |

The additional growth condition on the function is precisely given as there exists positive constants such that for any and any

| (24) |

Here is the th derivative of . This growth condition is verified for common activation functions such as the sigmoid and the softplus , a smoothed approximation to the ReLU. The Gaussian mean assumption (23) can always be satisfied by incorporating a translation into the activation function.

Benigni and Péché (2019) recently showed that the empirical spectral measure and largest eigenvalue of converge to a deterministic measure and largest element in the support, respectively. This implies that this model, like the isotropic features one, verifies Assumption 2. However, contrary to the isotropic features model, the limiting measure does not have an explicit expression, except for some specific instances of in which it is known to coincide with the Marčenko-Pastur distribution.

Lemma 2.2 (One-hidden layer network).

(Benigni and Péché (2019, Theorems 2.2 and 5.1)) Suppose the matrix is generated using the random features model. Then there exists a deterministic compactly supported measure such that weakly in probability. Moreover where is the top edge of the support of .

[notespar,

caption = Residual Polynomials. Summary of the residual polynomials associated with the methods discussed in this paper. is the -th Chebyshev polynomial of the first kind, is -th Chebyshev polynomial of the second kind, and is the -th Legendre polynomial. Derivations of these polynomials can be found in Appendix A. In light of Proposition 3.1, an explicit expression for the polynomial is enough to determine the polynomial . ,

label = table:polynomials,

captionskip=2ex,

pos =!t

]l c l\tnote[1](Nesterov, 2004; Beck and Teboulle, 2009) \tnote[2](Polyak, 1964) \tnote[3](Nesterov, 2004)

Methods Polynomial Parameters

Gradient Descent

Nesterov (cvx) \tmark[1]

Polyak \tmark[2]

Nesterov

(Strongly cvx) \tmark[3]

,

3 From optimization to polynomials

In this section, we look at the classical connection between optimization algorithms, iterative methods, and polynomials (Flanders and Shortley, 1950; Golub and Varga, 1961; Fischer, 1996; Rutishauser, 1959). While the idea of analyzing optimization algorithms from the perspective of polynomials is well-established, many modern algorithms, such as the celebrated Nesterov accelerated gradient (Nesterov, 2004), use alternative approaches to prove convergence.

This connection between polynomials and optimization methods will be crucial to proving the average-case guarantees in Tables LABEL:tab:comparison_worst_avg_cvx and LABEL:tab:comparison_worst_avg_str_cvx. To exploit this connection, we will construct the residual polynomials associated with the considered methods and we prove novel facts which may be of independent interest. For example, the polynomials associated with Nesterov’s method provides an alternative explanation to the ODE in (Su et al., 2016).

Throughout the paper, we consider only gradient-based methods, algorithms which can be written as a linear combination of the previous gradients and the initial iterate.

Definition 3.1 (Gradient-based method).

An optimization algorithm is called a gradient-based method if each update of the algorithm can be written as a linear combination of the previous iterate and previous gradients. In other words, if every update is of the form

| (25) |

for some scalar values that can potentially depend continuously on and .

Examples of gradient-based methods include momentum methods (Polyak, 1964), accelerated methods (Nesterov, 2004; Beck and Teboulle, 2009), and gradient descent. Now given any gradient-based method, we can associate to the method residual polynomials and iteration polynomials which are polynomials of degree , precisely as followed.

Proposition 3.1 (Polynomials and gradient-based methods).

Consider a gradient-based method with coefficients that depend continuously on and . Define the sequence of polynomials recursively by

| (26) |

These polynomials and are referred to as the residual and iteration polynomials respectively. We express the difference between the iterate at step and in terms of these polynomials:

| (27) |

Proof.

We will prove the result by induction. For , the claimed result holds trivially. We assume it holds up to iteration and we will prove it holds for . To show this, we will use the following equivalent form of the gradient , which follows from the definition of . Using this and the definition of gradient-based method, we have:

where in the second identity we have used the induction hypothesis and in the last one the recursive definition of . ∎

3.1 Examples of residual polynomials.

Motivated by the identity linking the error and the residual polynomial in Proposition 3.1, we derive the residual polynomials for some well-known optimization methods. Some of these residual polynomials are known but some, like Nesterov’s accelerated methods, appear to be new.

Gradient descent.

Nesterov’s accelerated method.

Nesterov’s accelerated method (Nesterov, 2004) and its variant FISTA (Beck and Teboulle, 2009) generate iterates on (10) satisfying the recurrence

| (30) |

with initial vector and . Unrolling the recurrence, we can obtain an explicit formula for the corresponding polynomials

| (31) |

We derive the polynomials explicitly in Appendix A.1. When (strongly convex), the polynomial is given by

| (32) |

where and the Chebyshev polynomials of the 1st and 2nd-kind respectively. When the smallest eigenvalue of is equal to (non-strongly convex setting) the polynomial is given by

| (33) |

where are the Legendre polynomials.

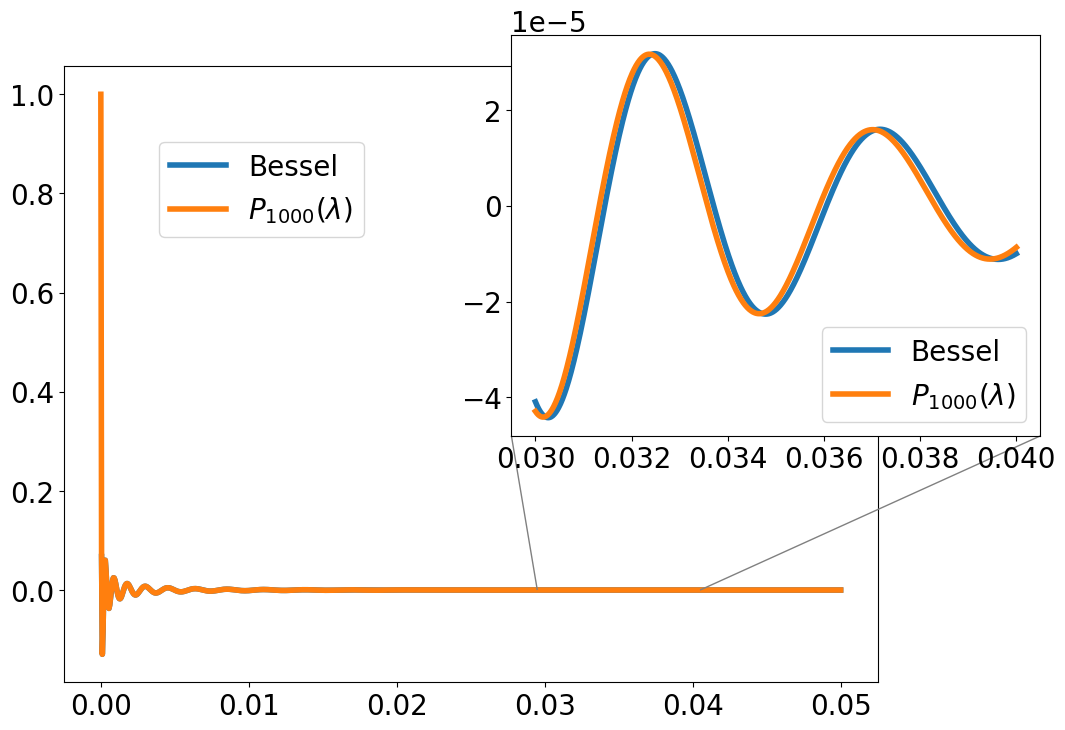

Working directly with the polynomial in (33) will prove difficult. As such, we derive an asymptotic expression for this polynomial. Nesterov’s polynomial satisfies in a sufficiently strong sense

| (34) |

where is the Bessel function of the first kind. A derivation of this can be found in Appendix A.1.2. Let . Then the recurrence in (31) becomes a discrete approximation to the initial value problem

which bears a strong resemblance to the differential equation model for Nesterov’s accelerated method in (Su et al., 2016). The solution to this initial value problem is . Our result in (34), not derived using this differential equation, yields an even tighter result for Nesterov’s accelerated method by including the exponential.

Polyak momentum algorithm.

We aim to derive the residual polynomials for the Polyak momentum algorithm (a.k.a Heavy-ball method) (Polyak, 1964). The Polyak momentum algorithm takes as arguments the largest and smallest eigenvalues of and iterates as follows

| (35) |

Using these initial conditions, the residual polynomials for Polyak momentum satisfy

| (36) |

By recognizing this three-term recurrence as Chebyshev polynomials, we can derive an explicit representation for namely

| (37) |

3.2 Properties of residual polynomials

In the following sections, it will be convenient to know some general properties of residual polynomials. Particularly, the polynomials, and are uniformly bounded in and that these polynomials goes to zero on some fixed support . The importance of these facts are twofold. First, these polynomials appear in the formula for the expected gradient, Theorem 1.1. Second, we use the boundedness and convergence properties in the proof of halting time universality, Theorem 1.2. If one a priori knows an explicit expression for these polynomials, then these properties are easily deduced. However when such an expression does not exist, we still can conclude these properties hold provided that the algorithm is convergent.

Definition 3.2 (Convergent algorithms).

We say a gradient-based method is (strongly) convergent if for every matrix such that and any vectors and , we have that the sequence of iterates generated by the algorithm starting at satisfies as and there exists constants depending on and such that

| (38) |

where in the optimum of (10).

Remark 3.1 (Minimal norm solutions).

For any gradient-based method, the iterates generated by the algorithm on the least squares problem (10) satisfy . If the algorithm converges to some and we have that , then the solution is independent of the algorithm in the following sense

| (39) |

In particular when , the optimum is the minimal norm solution. See e.g., Gunasekar et al. (2018); Wilson et al. (2017) and references therein.

Remark 3.2.

All the algorithms discussed in Section 3.1 are convergent.

The following lemma shows that convergent algorithms have residual polynomials which go to as on compact subsets of the positive real line. In essence if optimality measures go to zero, then so must the residual polynomial.

Lemma 3.1 (Convergent algorithms Residual polynomials ).

Suppose the algorithm is a (strongly) convergent gradient-based method. Fix positive constants for a convergent algorithm and constants if one has a strongly convergent algorithm. The residual polynomial, , for the algorithm satisfies

Proof.

Suppose we consider the noiseless setting where in the generative model so that . Fix a constant and define the following matrix and vectors

| (40) |

A simple computation shows that . Because the method is (strongly) convergent, the algorithm converges for these choices of and . Moreover, we know that and by Proposition 3.1, the vector . Therefore we have that

| (41) |

Similarly, we consider the same matrix as in (40) but instead a pure noise setting,

| (42) |

As before, the matrix . By Proposition 3.1, the iterates as . With this, the gradient equals

Here, again, we used Proposition 3.1. A (strongly) convergent method has the following

| (43) |

This completes the result. ∎

The following lemma shows that the residual polynomials are uniformly bounded over on any compact subset of the positive real line.

Lemma 3.2 (Convergent algorithms boundedness of ).

Suppose is a (strongly) convergent algorithm with residual polynomial . Under the assumptions of Lemma 3.1,

for some constants .

Proof.

Suppose we consider the noiseless setting in the generative model (10) so that . It then follows that where is the optimum. A simple computation using Proposition 3.1 shows that for all

| (44) | ||||

Next consider the matrix and vectors and as in (40) with the initial iterate . We consider cases: suppose . Fix a constant . It follows from our choice of , , , and that the vector and by (44) that

| (45) |

The solution set if and otherwise it equals if . From Remark 3.1, we have that and thus we deduce that

In both cases, we have that . Therefore using the boundedness assumption (38) and the expression for the gradient in (41), we have that

Here we used that the distance to the optimum and the polynomial in (45) is bounded on a compact set.

Now we suppose that . As above, we use the same matrix and vectors and as in (40) and, in addition, we set . In this situation, the matrix is invertible and . Hence both (45) and holds. Using the boundedness assumption on function values (38) and the expression for the function values in (44), we deduce

The result immediately follows.

∎

4 Halting time is almost deterministic

In this section we develop a framework for the average-case analysis and state a main result of this paper: the concentration of the halting time. We define the halting time as the first iteration at which the gradient falls below some predefined :

| (46) |

Our main result (Theorem 4.1) states that this halting time is predictable for almost all high-dimensional data, or more precisely,

| (47) |

Furthermore, we provide an implicit expression for this constant, otherwise known as the average complexity, and in Tables LABEL:tab:comparison_worst_avg_cvx and LABEL:tab:comparison_worst_avg_str_cvx an explicit expression under further assumptions. The rest of this section provides a proof of this result.

4.1 First-order methods as polynomials

Proposition 4.1 (Residual polynomials and gradients).

Suppose the iterates are generated from a gradient based method. Let be a sequence of polynomials defined in (26). Then the following identity exists between the iterates and its residual polynomial,

Proof.

This equality for the squared norm of the gradient is crucial for deriving average-case rates. In contrast, worst-case analysis typically uses only bounds on the norm. A difficulty with the polynomials and is that their coefficients depend on the largest and smallest eigenvalue of , and hence are random. We can remove this randomness thanks to Assumption 2, replacing and with the top (bottom) edge of the support of , denoted by and , without loss of generality.

Proposition 4.2 (Remove randomness in coefficients of polynomial).

Suppose Assumption 2 holds. Fix any -degree polynomial whose coefficients depend continuously on the largest and smallest eigenvalues of . Then the following hold

| (48) |

Proof.

Fix any . Let where be the coefficients associated with the term of degree in . For each , the continuity of implies there exists such that

| (49) |

For sufficiently large , Assumption 2 implies and . With this, we define the event We have for all sufficiently large

| (50) |

Here we used that for large . Therefore, it suffices to consider the first term in (50) and show that it is . By construction of the set , any element in satisfies both and . Hence on the event , we have the following

| (51) |

From this, we deduce that and the result immediately follows by (50). ∎

The squared norm of the gradient in (4.1) is a quadratic form. In Proposition 4.2, we removed the randomness in the coefficients of the polynomial and now we will relate this back to the squared norm of the gradient, and particularly, the quadratic form. The following lemmas state this precisely.

Lemma 4.1.

Suppose the sequences of non-negative random variables satisfy and . Then .

Proof.

Fix constants and suppose we set and . Because converges in probability, we have for sufficiently large . Define the event and decompose the space based on this set so that for large

Here we used that . For the other term, a direct application of Markov’s inequality yields

The result immediately follows. ∎

Lemma 4.2 (Remove randomness in coefficients of quadratic form).

Suppose Assumption 2 holds and let the vectors and be i.i.d. satisfying and for some constants . For any degree polynomial whose coefficients depend continuously on and , the quadratic form converges in probability

Proof.

From Lemma 4.2 and the expression for the squared norm of the gradient in (4.1), we can replace the maximum (minimum) eigenvalue in (4.1) with the top (bottom) edge of the support of , (). This followed because the vectors and satisfy and in Lemma 4.2 and the terms surrounding these vectors in (4.1) are polynomials in .

4.2 Concentration of the gradient

Having established the key equation linking the gradient to a polynomial in Proposition 4.1, we now show that for almost any large model the magnitude of the gradient after iterations converges to a deterministic value which we denote by . We recall the statement of Theorem 1.1:

Theorem. (Concentration of the gradient) Under Assumptions 1 and 2 the norm of the gradient concentrates around a deterministic value:

| (52) |

Intuitively, the value of is the expected gradient after first taking the model size to infinity. The above expression explicitly illustrates the effects of the model and the algorithm on the norm of the gradient: the signal () and noise (), the optimization algorithm which enters into the formula through the polynomial , and the model used to generate by means of the measure .

The main tool to prove Theorem 1.1 is the moment method which requires computing explicit expressions for the moments of the norm of the gradient. We summarize this in the following proposition. To ease notation in the next few propositions, we define the following matrices and vectors

| (53) |

and let be the quadratic form given by

| (54) |

Observe that the value is simply in (4.1) with replaced with .

Proposition 4.3.

Proof.

We can write any quadratic form as . Expanding the quadratic forms, the following holds

| (56) | ||||

| (ind. of and , ) | (57) | |||

| (isotropic prop. of and ) | (58) | |||

| (59) |

In the last equality, we used that .

To prove (55), we will use Chebyshev’s inequality; hence we need to compute the . First, a simple computation yields that

| (60) |

Next, we compute . By expanding out the terms in (54), we get the following

| (61) | ||||

To compute the variance of , we take (61) and subtract (60). Since this is quite a long expression, we will match up terms and compute these terms individually. First consider the terms (a) and (i) in equations (61) and (60) respectively. By expanding out the square, we get

We need each index to appear exactly twice in the above for its contribution to be non-negligible since and . There are four possible ways in which this can happen: , , , or . By the symmetry of the matrix, the last two cases are identical. Noting that and , we, consequently, get the following expression for the variance

| (62) | ||||

In the second equality, we used that and in the second inequality we can without loss of generality choose so that . Finally, we used that .

Next, we consider the terms (b) and (ii) in equations (61) and (60) respectively. Similar to the previous case, by expanding out the square, we get the following

Because of independence, isotropic variance , and mean , we need each index to appear exactly twice in the above expression in order for its contribution to be non-negligible. There are four possible ways in which this can happen: , or . As before, we have the following expression for the variance

| Var | (63) | |||

Here we can without loss of generality choose so that . Next, we compare (c) and (iii) in equation (61) and (60), respectively. We begin by expanding out (c) in equation (61) which yields

The only terms which contribute are when and . Therefore, we deduce the following

| (64) | ||||

We have now used up all the terms in (60) so the remaining terms, (d) and (e), in (61) we will show are themselves already going to as . Again expanding the term (d), we get

| (65) |

By independence and isotropic variance of and , the only terms which remain after taking expectations are the ones with and terms. Therefore, we deduce

| (66) | ||||

The only term which remains in (61) is (e). Since , the term contributes nothing to the expectation. Similarly since , the term is also zero in expectation.

Putting all the quantities (62), (63), (64), (66) together with (60) and (61), a straight forward application of Chebyshev’s inequality yields the result.

∎

The only difference between and is the coefficients of the polynomials in continuously depend on while the coefficients of depend on . The polynomials and together with Assumptions 1 and 2 ensure that all the conditions of Lemma 4.2 hold by setting and to combinations of and and the polynomials to , , and . Therefore we have so we can replace with . The proof of Proposition 4.3 shows, that conditioned on , the is and

| (67) |

Consequently, conditioned on , the squared norm of the gradient is roughly (67). So in view of this, it suffices to understand the expected traces of polynomials in . Random matrix theory studies convergence properties of the limiting distribution of high dimensional matrices, particularly the empirical spectral measure. An important tool derived from using Assumption 2 linking the ESM and the expected trace to the moments of the measure is given below.

Proposition 4.4 (Convergence of ESM).

Let be any -degree polynomial. Under Assumption 2, the following is true

Proof.

For sufficiently large , Assumption 2 says . Define the event . We construct a bounded, continuous function by

Because the function is bounded and continuous, Assumption 2 guarantees that

| (68) |

Depending on whether has occurred, we have for all sufficiently large

| (69) |

In the last line, the probability for large . Hence, we consider only the first term in (69). By construction, for any element in it is clear that . For sufficiently large , equation (68) yields

The result follows after combining with (69). ∎

Now that we have described the main components of our argument, we present a preliminary concentration result for the gradient.

Proposition 4.5.

Proof.

Recall the definitions in (53) and (54) and equation (4.1). We note that the only difference between and is that the coefficients of the polynomials in continuously depend on while the coefficients in depend on . The polynomials and together with Assumptions 1 and 2 ensure that all the conditions of Lemma 4.2 hold by setting and to combinations of and and the polynomials to , , and . Therefore we have so it suffices to prove (70) with replaced by .

Fix constants . Proposition 4.4 guarantees convergence in probability of any expected trace to a constant which depends on the polynomial and the deterministic measure . This together with the definitions of , , and yield for sufficiently large

| (71) |

We define the set for which the expected traces of the random matrices are bounded, namely,

and we observe because of (71) that the probability . The total law of probability yields the following

| (72) |

Hence it suffices to bound the first term in (72). The idea is to condition on the matrix and apply Proposition 4.3. The law of total expectation yields

| (conditioned on ) | ||||

| (Proposition 4.3) | (73) |

Here for the indicator of the event we use the notation where the indicator is if and otherwise. By construction of the event , each of the expected traces in (73) are bounded and therefore, we deduce that

By choosing sufficiently large, we can make the right hand side smaller than . The result immediately follows from (72). ∎

Proposition 4.5 reveals that for high-dimensional data the squared norm of the gradient is a polynomial in the eigenvalues of the matrix . Every eigenvalue, not just the largest or smallest, appears in this formula (70). This means that first-order methods indeed see all of the eigenvalues of the matrix , not just the top or bottom one. However, the expected trace is still a random quantity due to its dependency on the random matrix. We remove this randomness and complete the proof of Theorem 1.1 after noting that the moments of the empirical spectral measure converge in probability to a deterministic quantity, denoted by .

4.3 Halting time converges to a constant

The concentration of the norm of the gradient in (52) gives a candidate for the limiting value of the halting time . More precisely, we define this candidate for the halting time from and we recall the halting time, , as

| (74) |

We note that the deterministic value is, by definition, the average complexity of GD whereas is a random variable depending on randomness from the data, noise, signal, and initialization. This leads to our main result that states the almost sure convergence of the halting time to a constant value. We begin by showing that is well-defined.

Lemma 4.3 ( is well-defined).

Under the assumptions of Proposition 4.5, the iterates of a convergent algorithm satisfy .

Proof.

With our candidate for the limiting halting time well-defined, we show that number of iterations until equals for high-dimensional data. We state a more general result of Theorem 1.2.

Theorem 4.1 (Halting time universality).

Provided that for all , the probability of reaching in a pre-determined number of steps satisfies

If the constant for some , then the following holds

Proof.

To simplify notation, we define . First, we consider the case where for all . We are interested in bounding the following probabilities

| (75) |

We bound each of these probabilities independently; first consider in (75). For , we note that since . So we can assume that . Since , we obtain

| (76) |

Now we bound the probabilities . As is the first time falls below , we conclude that where we used that for any . Next we define the constant and we observe that for all . Fix a constant and index . Theorem 1.1 says that by making sufficiently large

Here we used that is finite for every (Lemma 4.3). Set . Then for all , we have from (76) the following

Lastly, we bound . The idea is similar to the other direction. Let be defined as above. Therefore, again by Theorem 1.1, we conclude for sufficiently large

Indeed, we used that and . This completes the proof when .

Next, we consider the second case where . Note that for all because . In this setting, we are interested in bounding

The arguments will be similar to the previous setting. Replacing the definition of above with yields that since . With this choice of , the previous argument holds and we deduce that . Next we show that . As before, we know that . By definition of , we have that . Now define . The previous argument holds with this choice of ; therefore, one has that . ∎

For large models the number of iterations to reach a nearly optimal point equals its average complexity which loosely says . The variability in the halting time goes to zero. Since the dependence in on the distribution of the data is limited to only the first two moments, almost all instances of high-dimensional data have the same limit. In Tables LABEL:tab:comparison_worst_avg_cvx and LABEL:tab:comparison_worst_avg_str_cvx, we compute the value of for various models.

4.4 Extension beyond least squares, ridge regression

In this section, we extend the results from Theorems 1.1 and 1.2 to the ridge regression problem. We leave the proofs for the reader as they follow similar techniques as the least squares problem (1). We consider the ridge regression problem of the form

| (77) |

As in Section 2, we will assume that is a (possibly random) matrix satisfying Assumption 2, is an unobserved signal vector, and is a noise vector. The constant is the ridge regression parameter. Unlike the least squares problem, the gradient of does not decompose into a term involving and . As such, we alter Assumption 1 placing an independence assumption between the initialization vector and the signal , that is,

Assumption 3 (Initialization, signal, and noise.).

The initial vector , the signal , and noise vector are independent of each other and independent of . The vectors satisfy the following conditions:

-

1.

The entries of and are i.i.d. random variables and there exists constants such that for

(78) -

2.

The entries of noise vector are i.i.d. random variables satisfying the following for and for some constants

(79)

The difference between Assumption 1 and Assumption 3 is that (78) guarantees the initial vector and the signal are independent. One relates to and by . First, the gradient of (77) is

| (80) |

where the matrix and is the identity matrix. Under Assumption 3 and 2, we derive a similar recurrence expression for the iterates of gradient-based algorithms as Proposition 3.1

Proposition 4.6 (Prop. 3.1 for ridge regression).

Consider a gradient-based method with coefficients that depend continuously on and . Define the sequence of polynomials recursively by

| (81) |

These polynomials and are referred to as the residual and iteration polynomials respectively. We express the difference between the iterate at step and in terms of these polynomials:

| (82) |

The proof of this proposition follows the same argument as in Proposition 3.1, replacing the gradient of the least squares problem (1) with the gradient for the ridge regression problem (80). The polynomials and are exactly the same as in Proposition 3.1 but applied to a different matrix instead of (see Section 3.1 for examples the polynomials and for various first-order algorithms). Given the resemblance to the least squares problem, it follows that one can relate the residual polynomial to the squared norm of the gradient.

Proposition 4.7 (Prop. 4.1 for ridge regression).

Suppose the iterates are generated from a gradient based method. Let be a sequence of polynomials defined in (81). Then the following identity exists between the iterates and its residual polynomial,

As in the least squares problem, one can replace the in the polynomial with for . Under Assumptions 2 and 3, using the same technique as in Propositions 4.3 for the least squares problem, we derive the following.

Proposition 4.8 (Prop. 4.8 for ridge regression).

We remark that we used the independence between and to obtain (83). This independence leads to two terms in the gradient corresponding to the initialization and the signal. As the polynomials , , and are polynomials in (the identity commutes with ), Proposition 4.4 still holds. Therefore, the equivalent to Theorem 1.1 for ridge regression follows (recall, Theorem 1.3 in Section 1.1.1).

5 Derivation of the worst and average-case complexity

In this section, we derive an expression for the average-case complexity in the isotropic features model. Here the empirical spectral measure converges to the Marčenko-Pastur measure (2). The average-case complexity, , is controlled by the value of the expected gradient norm in (52). Hence to analyze the average-case rate, it suffices to derive an expression for this value, .

In light of (52), we must integrate the residual polynomials in Table LABEL:table:polynomials against the Marčenko-Pastur measure. By combining Theorem 1.1 with the integrals derived in Appendix B, we obtain the average-case complexities. Apart from Nesterov’s accelerated method (convex), an exact formula for the average-case rates are obtained. In the convex setting for Nesterov, the integral is difficult to directly compute so instead we use the asymptotic polynomial in (34). Hence for Nesterov’s accelerated method (convex), we only get an asymptotic average-case rate for sufficiently large (see Appendix B). Tables LABEL:tab:comparison_worst_avg_cvx and LABEL:tab:comparison_worst_avg_str_cvx summarize the asymptotic rates where both iteration and problem size are large.

We now turn to the worst-case guarantees. We discuss below how to make the worst-case complexity comparable.

5.1 Traditional worst-case complexity

Recall, the prior discussion on the dimension-dependent constants in the typical worst-case complexity bounds. We now make this precise below.

Worst-case complexity: strongly convex and noiseless non-strongly convex regimes.

Consider GD and note the other methods will have similar analysis. Recall, the standard analytical worst-case bound for the strongly convex regime and the exact worst-case bound for the non-strongly convex setting (Taylor et al., 2017), respectively,

where is the minimal norm solution of (10). For sufficiently large , the largest and smallest eigenvalues of converge in probability to and respectively. These are the top and bottom edge of the Marčenko-Pastur distribution. We also note in the noiseless setting . Hence by Assumption 1 and , on average, . Moreover when the matrix is nonsingular, as in the strongly convex setting, the optimum does not grow as dimension increases despite the noise. As a sequence of random variables in , is tight. From these observations we derive the worst-case complexities.

Worst-case complexity: noisy non-strongly convex regime.

While discussing the worst-case complexity in Section 1.2, we noted a discrepancy in the noisy, non-strongly convex regime between the average rate and the exact worst complexity. For instance, the exact worst complexity for gradient descent (GD) (Taylor et al., 2017) is

| (85) |

For sufficiently large , the largest eigenvalue of converges a.s. to , the top edge of the support of . Hence, to derive worst-case complexity bounds, it suffices to understand the behavior of the distance to the optimum.

The vectors and are different when noise is added to the signal. For simplicity, we consider the setting where the matrix is invertible. Intuitively, the optimum where is the underlying random signal. Because the signal is scaled, Assumption 1 says . Therefore, the distance to the optimum is controlled by the noise which in turn is bounded by the reciprocal of the minimum eigenvalue of , namely

where is an eigenvalue-eigenvector pair corresponding to the minimum eigenvalue of . Unfortunately, the smallest eigenvalue is not well-behaved. Particularly there does not exist any scaling so that expectation of is finite and the distribution is heavy-tailed. Instead we show that this quantity grows faster than . To do so, we appeal to a theorem in (Tao and Vu, 2010), that is, we assume that all moments of the entries of the matrix are bounded, namely,

| (86) |

This bounded moment assumption is a mild assumption on the entries. For instance it includes any sub-exponential random variables. It should be noted here that under the simple isotropic features model it is clear that is dimension-dependent, but the exact dependence is more complicated. Under this condition (86), we can prove a bound, which gives the dependence on the problem size, for the growth rate of the distance to the optimum.

Lemma 5.1 (Growth of ).

Proof.

We begin by defining the constant . The matrix is invertible a.s. so without loss of generality the smallest eigenvalue of is non-zero. Here the dimensions are equal, . From (Edelman, 1988, Corollary 3.1) and (Tao and Vu, 2010, Theorem 1.3), we know that converges in distribution where we denote the smallest eigenvalue of as . It is immediately clear that also converges in distribution. By Theorem 3.2.7 in Durrett (2010), the sequence of distribution functions is tight, that is, there exists an such that

In particular, we know that

| (88) |

Another way to observe (88) is that has a density supported on (Edelman, 1988). For any -squared with -degree of freedom random variable of , there exists a constant such that

| (89) |

Let . With defined, we are now ready to prove (87). The matrix is a.s. invertible so gradient descent converges to . Next we observe that (87) is equivalent to proving

| (90) |

Plugging in the value of and using the reverse triangle inequality, we obtain

Using Markov’s inequality, we can obtain a bound on :

Consider now the event given by . The total law of probability yields

| (91) | ||||

A simple calculation gives that where the orthonormal vector is the eigenvector associated with the eigenvalue . From this, we deduce the following inequalities

Since is Gaussian and is orthonormal, we know that , a chi-squared distribution, so (89) holds and we already showed that satisfies (88). By taking , we have

The inequality in (90) immediately follows after taking the limsup of (91). ∎

Combining this lemma with the equation (85), we get with high probability that

By setting the right-hand side equal to , we get the worst-case complexity result.

5.2 Adversarial Model

Next we recall the adversarial model. Here we assume a noisy generative model for (Assumption 1). Then our adversary chooses the matrix without knowledge of in such a way that maximizes the norm of the gradient subject to the constraint that the convex hull of the eigenvalues of equals . For comparison to the average-case analysis with isotropic features, we would choose to be the endpoints of the Marčenko-Pastur law. In light of Proposition 4.3, the adversarial model seeks to solve the constrained optimization problem

| (92) |

where the largest (smallest) eigenvalue of is restricted to the upper (lower) edge of Marčenko-Pastur measure. The optimal of (92), , has all but two of its eigenvalues at

| (93) |

The other two eigenvalues must live at and in order to satisfy the constraints. The empirical spectral measure for this is exactly

Since this empirical spectral measure weakly converges to , we satisfy the conditions of Assumption 1 for these and spectral measure . Hence, Theorem 1.1 holds and the maximum expected squared norm of the gradient as the model size goes to infinity equals

| (94) | ||||

We called the above expression the adversarial average-case complexity. Table LABEL:tab:comparison_worst_avg_cvx shows these convergence guarantees. We defer the derivations to Appendix C.

Remark 5.1.

In the strongly convex setting, we omitted the adversarial average-case guarantees out of brevity. For all the algorithms, the value of occurs near or at the minimum eigenvalue . As such there is (almost) no distinction between the traditional worst-case guarantees and the adversarial guarantees.

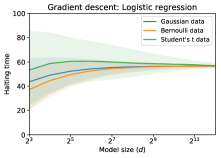

6 Numerical Simulations

To illustrate our theoretical results we report simulations using gradient descent (GD) and Nesterov’s accelerated method (convex) (Nesterov, 2004; Beck and Teboulle, 2009) on the least squares problem under the isotropic features model. We further investigate the halting time in logistic regression as well as least squares with mini-batch stochastic gradient descent (SGD). See Appendix D for details.

Setup.

The vectors and are sampled i.i.d. from the Gaussian whereas the entries of are sampled either from a standardized Gaussian, a Bernoulli distribution, or a Student’s -distribution with 5 degrees of freedom, normalized so that they all have the same mean and variance. We train the following models:

-

•

Least squares. The least squares problem minimizes the objective function . The targets, , are generated by adding a noise vector to our signal, . The entries of are sampled from a normal, , for different values of .

-

•

Logistic regression. For the logistic regression model we generate targets in the domain using where is the logistic function. The output of our model is , and the objective function is the standard cross-entropy loss:

Parameter settings.

In all simulations, the halting criterion is the number of steps until the gradient falls below , , where is chosen to be for GD and Nesterov and is for SGD. The step size for GD and Nesterov’s accelerated method is fixed to be where is the Lipschitz constant of the gradient. For least squares, . We approximate by performing 64 steps of the power iteration method on the matrix , initialized with a constant vector of norm 1. For logistic regression, we set the step size to be .

In SGD, we sample rows from the matrix . The mini-batch size parameter is a fixed fraction of the data set size , so that the comparison of halting times across model sizes is consistent. When the models are over-parametrized (), a strong growth condition (Schmidt and Le Roux, 2013) holds. This means a scaling of the GD step size can be used to ensure convergence. In the under-parametrized setting, SGD does not converge to the optimum. In this case we chose a step size such that the expected squared gradient norm at the stationary point equals the halting criterion. See Appendix D.1 for derivations.

Results and conclusions.

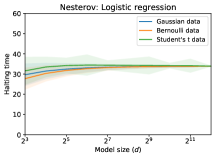

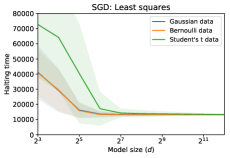

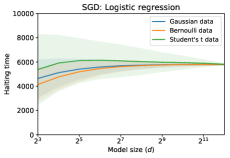

Figure 1 confirms our theoretical results: variability in the halting time decreases and the halting time converges to a deterministic quantity independent of the distribution of the data. Experimentally, the standard deviation decreased at a rate of , consistent with results in random matrix theory. For medium sized problems (), the heavy-tailed Student’s t distribution occasionally produces ill-conditioned matrices resulting in large halting times. These ill-conditioned matrices disappear as the model size grows in large part because the maximum eigenvalue becomes stable.

More interestingly, our results extend to non-quadratic functions, such as logistic regression, as well as SGD (see Figure 7). Surprisingly, we see different behaviors between logistic and least square models for smaller matrices when using SGD. Moreover, we note that the large halting times seen in the Student’s t distribution for GD on medium sized problems disappear when we instead run SGD.

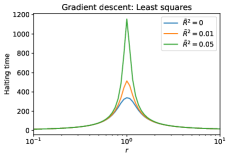

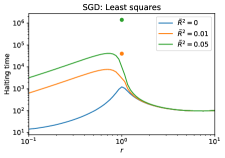

Secondly, Figure 8 evaluates the halting times dependency on the ratio . As predicted by the theory, the halting time takes its maximum value (i.e., algorithm is slowest) precisely when . For SGD different step sizes are used for the over-parametrized and under-parametrized regime resulting in an asymmetric curve and a clear discontinuity at . We leave the study of these phenomena as future work.

Acknowledgements

The authors would like to thank our colleagues Nicolas Le Roux, Ross Goroshin, Zaid Harchaoui, Damien Scieur, and Dmitriy Drusvyatskiy for their feedback on this manuscript, and Henrik Ueberschaer for providing useful random matrix theory references.

Appendix A Derivation of polynomials

In this section, we construct the residual polynomials for various popular first-order methods, including Nesterov’s accelerated gradient and and Polyak momentum.

A.1 Nesterov’s accelerated methods

Nesterov accelerated methods generate iterates using the relation

By developing the recurrence of the iterates on the least squares problem (10), we get the following three-term recurrence

with the initial vector and . Using these standard initial conditions, we deduce from Proposition 3.1 the following