Inject Machine Learning into Significance Test for Misspecified Linear Models

Abstract

Due to its strong interpretability, linear regression is widely used in social science, from which significance test provides the significance level of models or coefficients in the traditional statistical inference. However, linear regression methods rely on the linear assumptions of the ground truth function, which do not necessarily hold in practice. As a result, even for simple non-linear cases, linear regression may fail to report the correct significance level.

In this paper, we present a simple and effective assumption-free method for linear approximation in both linear and non-linear scenarios. First, we apply a machine learning method to fit the ground truth function on the training set and calculate its linear approximation. Afterward, we get the estimator by adding adjustments based on the validation set. We prove the concentration inequalities and asymptotic properties of our estimator, which leads to the corresponding significance test. Experimental results show that our estimator significantly outperforms linear regression for non-linear ground truth functions, indicating that our estimator might be a better tool for the significance test.

1 Introduction

Linear regression is commonly used in practice because it can provide explanations for important features by significance test, but the required linear assumptions (e.g. linearity and normality) on the ground truth function are easily violated in practice (Osborne and Waters, 2002; Casson and Farmer, 2014). This problem is critical: when linear assumptions are violated, one may ignore important features or focus on unimportant features due to the fake significance level. One potential solution is considering all kinds of ground truth functions by removing the linear assumption, but this triggers another problem: since there are numerous types of non-linear functions, how can we learn the feature importance without knowing the exact type of the ground truth function?

The answer is simply applying linear regression to the unknown non-linear ground truth functions, i.e. using misspecified linear models (Fahrmexr, 1990; Hainmueller and Hazlett, 2014; Grünwald et al., 2017; Markiewicz and Puntanen, 2019). Apart from the fake significance level, misspecified linear models can also address other problems of linear regression, such as bias, inefficiency, and incorrect inferences (e.g. King and Zeng (2006)). Indeed, as we will show in Section 5, traditional significance test based on linear regression fails even for the simple non-linear ground truth functions like square function.

The most common approach for misspecification is introducing high-order terms and interactions (e.g. Friedrich (1982); Brambor et al. (2006)), but this only works for the prescribed types and usually cannot find the correct functional form. Another line of work (White, 1980; Berk et al., 2013; MacKinnon and White, 1985; Buja et al., 2015; Bachoc et al., 2020) tries to do the significance test directly based on the least square estimation, and derive the consistent estimators of its variance. The downside of this approach is that the corresponding estimators contain inevitable system errors and bias due to wrong model selections (see Section 5.2).

In this work, we introduce machine learning methods into the misspecified linear models, where we do not need to know the correct functional form and also effectively avoid system errors. We first use a machine learning method to fit the ground truth function in the training step and estimate the corresponding linear approximation. Afterward, we correct the mistakes made by the machine learning methods in the validation step. We show a positive correlation between the performance of the underlying machine learning method and the performance of our new estimator (see Theorem 1). Moreover, we prove the concentration inequalities (see Theorem 2) and asymptotic properties (see Theorem 3) of the newly proposed estimator, which can be further applied into the significance test.

Several experiments are conducted to show that this newly proposed estimator works well in both non-linear and linear scenarios. Especially, our newly proposed estimator can significantly outperform the traditional linear regression (see Table 2) when considering the Kolmogorov-Smirnov statistic in the non-linear scenarios (square function). This indicates that we make fewer mistakes in the significance test. For example, as we will show in Section 5.3, in the non-linear scenario, our method makes mistakes with probability , while for the traditional linear regression, the number is .

2 Related Work

The research on misspecified linear models can be broadly divided into Conformal Prediction, which focuses on the inference of prediction, and Parameter Inference, which focuses on the inference of the linear approximation parameter of ground truth function.

Conformal Prediction is a framework pioneered by Law (2006), which uses past experience to determine precise levels of confidence in new predictions. Conformal prediction (Shafer and Vovk, 2008; Papadopoulos et al., 2014; Barber et al., 2019; Cauchois et al., 2020; Zeni et al., 2020) mainly focuses on the confidence interval for predictions, so it cannot provide explanations for feature importance. Our work can be regarded as a parallel line of conformal prediction that focuses on the assumption-free parameter estimation confidence interval.

Parameter Inference can be dated back to White (1980); MacKinnon and White (1985), where sandwich-type estimators for variance are proposed. Furthermore, Buja et al. (2015) introduce M-of-N Bootstrap techniques to improve the estimation of variance. Hainmueller and Hazlett (2014) reduce this misspecification bias from a kernel-based point of view. Some other techniques, e.g. LASSO (Lee et al., 2016), least angle regression (Taylor et al., 2014) are introduced in the post-selection inference. And some works (Rinaldo et al., 2016; Bühlmann et al., 2015) focus on a high-dimensonal reversions. More discussions can be found in Berk et al. (2013); Bachoc et al. (2020). However, this line of works relies on the direct misspecification of linear models, which means system errors are inevitable when the ground-truth function is non-linear. Furthermore, this type of estimator based on the least square estimation contains much bias, which will be further discussed in Section 5.2. In this paper, we use a machine learning based estimator instead of least square estimation, which contains less bias as we will see later in Section 5.2.

3 Preliminaries

In this section, we define the basic notations, starting from the definition of function norm and function distance.

Definition 1 (Function Norm and Function Distance)

Given a functional family defined on domain , for any and a probability distribution on with density , the function -norm of with respect to is defined as

When the context is clear, we simply use instead. Moreover, the function distance between and is defined as

Based on function distance, we can define the least square linear approximation, or simply linear approximation.

Definition 2 (Linear Approximation)

For a given function , its least square linear approximation is defined as

where is the linear functional family.

The traditional linear regression uses a single dataset to compute the parameters, but our method splits the dataset into two parts, a training set, and a validation set, as defined below.

Definition 3 (Training and Validation Set)

Given a dataset , we randomly split into training set and validation set , where , , and , .

In some scenarios, we may have additional unlabeled data points, therefore in total data points. Usually, unlabeled data are easier to get than labeled data, which can be used to calculating the linear approximation of the machine learning model, and help to improve the estimation of . As we will discuss in Section 5, our analysis still applies without unlabeled data, given that the machine learning model is the linear form, and is estimated from only the validation set. But more unlabeled data could help enrich the patterns of our choices for machine learning models.

In order to evaluate the performance of our model on the population distribution, we need to estimate the upper and lower bounds of a given function (will be defined later).

Definition 4 (Upper and Lower Bounds)

Given a function defined on , the upper and lower bounds of is

Similarly, given a dataset , where , the empirical lower bound and empirical upper bound of on set is defined by

While and are hard to get, we may assume that is at least loosely bounded.

Assumption 1

Given a loss function defined on , we assume .

Notice that for linear regression, Assumption 1 usually holds, as we may assume that the domain of input is bounded, and the weight is also bounded. After applying proper scaling, we get .

As we will see in Theorem 1, our analysis depends on , and smaller gives more accurate estimations. If Assumption 1 holds, we immediately have . However, with additional prior knowledge on and , we may get tighter bounds of using Bayesian methods, as discussed in Lemma 1.

Lemma 1 (Tighter Estimation on )

Given a validation dataset where data points are randomly sampled from , and a function defined on with bounds and where and are unknown, and . Let , and assume the prior , where represents uniform distribution. For any , if , we have

where are the empirical bounds of on set .

Assumption 2 (Concentration of Explanatory Variables)

Let be a random vector in , and assume that there exists a constant , such that

almost surely.

Assumption 3 (Bounded Second Moment)

Let be a random vector in , and assume is invertible. Denote and . We assume that

In the following statements, we always use all data, including labeled and unlabeled data, to estimate , leading to the estimator .

4 Estimation

In this section, we study the problem of linear approximation of the oracle model , based on a machine learning framework. Specifically, we show the following: a) how the performance of our machine learning model affects the linear approximation estimator. b) after adding a bias term (we call it the residual term), one can get an estimator with better guarantees. c) how to run the hypothesis test (coefficient significance) based on the asymptotic distribution of our estimator. We defer all the proofs to Appendix A.

4.1 Approach Based on MSE

In this subsection, we study the relationship between the linear approximation functions and given that is close to . We use mean squared error (MSE) to measure the performance of machine learning models.

Theorem 1 (Performance of Machine Learning Models)

For , given oracle model and machine learning model , where their linear approximations are and , respectively. The labeled data is randomly split following Definition 3. Denote the loss function as , the population loss is then . Under Assumption 3, for any , the following inequality holds :

where , is the sample loss defined on validation set.

Remark: Theorem 1 shows that controls the approximation quality of and , which depends on both the validation set size and the validation loss. In other words, if the machine learning model generalizes well, we get good estimations of and .

The term depends on , which is bounded by based on Assumption 1. Although this term shrinks as the validation set grows, below we show that it can be bounded more accurately using Lemma 1.

Corollary 1

Under the assumptions of Lemma 1 and Theorem 1, by replacing in Lemma 1 by loss function and plugging it into Theorem 1, we have

where

Intuitively, using (the best linear approximation of ) to approximate seems to the optimal choice. However, as we will show below, this is not true, as may contain bias in the linear setting.

4.2 Filling the Bias

In this subsection, we will jump out of the restrictions of MSE, and improve our estimation by adding a bias term. We first present Lemma 2 that focuses on the estimation of the second-moment matrix of explanatory variables .

Lemma 2 (The Second Moment Concentration)

By adding a small bias, we can derive the following Theorem 2, which mainly focuses on the coordinate wise bound. Here we denote as the feature of , and as the row of matrix .

Theorem 2 (Adding a bias term)

For , given oracle model and machine learning model , where the linear approximation is and , respectively. The labeled data is randomly split based on Definition 3. Assume that Assumption 2 and Assumption 3 hold. Denote . Then, for any , the following inequality holds :

where is the realization of defined on validation set.

Notice that is the total number of data. The first term in the bound is because we use samples in the validation set to estimate the population. A tighter bound requires smaller fluctuation for (which is ) and more samples in validation set (). The second term is because we use to replace . A smaller condition number and a larger help tighten the bound.

Similar to Corollary 1, we can use and to replace and under additional assumptions, see below.

Corollary 2

Therefore, we should use as the new estimator. Recall the bound in Theorem 1 (denoted as ) and the bound in Theorem 2 (denoted as ). We can see that as goes to zero, while , where denote the average sample loss. This means that cannot be arbitrarily similar to given a fixed machine learning model even if we have infinite data for validation. That is to say, although Theorem 1 contains the frequently-used MSE as a measure, it causes some natural bias. And Theorem 2 filled this bias by adding a correction term.

Furthermore, as the standard practice in statistics, we will derive the asymptotic property of in Section 4.3.

4.3 Asymptotic Properties

In this section, we study the asymptotic property of estimator , which gives us tighter and more practical guarantees. In the following analysis, we assume that . This is without loss of generality because otherwise we can directly use to estimate without any loss.

Theorem 3 (Asymptotic Properties)

Given oracle model and machine learning model , with its corresponding linear approximation , , respectively. The labeled data is randomly split based on Definition 3. Denote , and assume are bounded111This usually holds in practice as long as are all bounded., then under Assumption 3 , the following asymptotic property of holds:

where represents normal distribution, , , .

Remark: Traditional asymptotic analysis is usually based on the assumptions for the ground truth function, but our analysis does not need such assumptions and instead relies on the training-validation framework. For example, in the traditional analysis, the claim that follows normal distribution is based on the assumption that the ground truth function is linear, and also the label noise follows a well-defined distribution.

Now we can do the hypothesis test based on the asymptotic property of , including model test and coefficient test under significance level . The details can be found in Appendix B.

5 Experiments

In this section, we conduct experiments of the significance test derived in Section 4.3. We will show that our method works in both linear and non-linear scenarios, while the traditional linear regression fails in non-linear scenarios even in a simple square case. Due to space limitations, we show linear scenarios in Appendix D. More experimental details could be found in Appendix C. For each statistic, we repeat experiments 6 times and compute its confidence interval of its mean.

We choose two types of machine learning models: a three-layer Neural Network (labeled as Ours(NN)) and a Linear-form model (labeled as Ours(L)), respectively. Note that Ours(L) does not need unlabeled data, while Ours(NN) needs unlabeled data to calculate the linear approximation of machine learning methods.

5.1 Metrics

Two metrics are considered here, focusing on the correctness and efficiency, respectively.

Correctness is shown by the Kolmogorov-Smirnov statistic, which is defined in Equation 1. Kolmogorov-Smirnov statistic measures how close the simulation results and theoretical results are. Smaller Kolmogorov-Smirnov statistic is better.

| (1) |

where is the empirical CDF in simulation, and is the theoretical CDF.

Efficiency is shown by the average standard deviation () of the estimators. Efficiency measures how much uncertainty the new estimators have. Since we have removed the requirements of linear assumptions, more uncertainty appears in our newly proposed method. A smaller means that we have more confidence in our estimators.

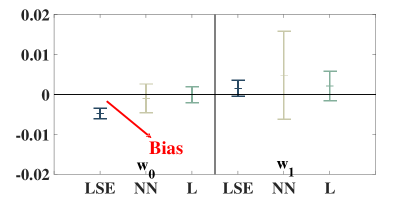

5.2 Unbiasedness

First of all, we would show that the traditional estimators based on least squares (LSE) contain more bias (see also (Rinaldo et al., 2016)), including the linear regression methods and the estimators proposed in White (1980); MacKinnon and White (1985); Lee et al. (2016); Taylor et al. (2014); Bühlmann et al. (2015); Bachoc et al. (2020), etc.

| LSE-based Estimator | Ours(NN) | Ours(L) | |

|---|---|---|---|

| -0.0048 () | -0.0010 () | -0.0001 () | |

| 0.0015 () | 0.0048 () | 0.0021 () |

We test a simple square case, where , our aim is to estimate its linear approximation. We repeat the simulation 1000 times, and each time we calculate the mean of the estimators. Note that for better showing the bias, we use a smaller dataset (see Appendix C.2). Table 1 shows the difference between simulation results and the theoretical parameter with their confidence interval.

Figure 1 shows that the traditional LSE-based estimators on are biased, where the confidence interval of bias does not contain . Our proposed methods can outperform these LSE-based methods because the newly proposed methods have a smaller bias. For simplification, we compare our proposed methods with only linear regression on their correctness and efficiency in Section 5.3, since linear regression is most widely used among these LSE-based methods in practice.

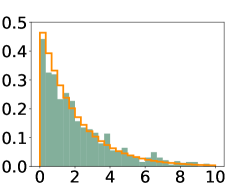

5.3 Non-linear Scenarios

In this section, we focus on the performance of the linear regression method and our newly proposed method under a non-linear scenario. We focus on a simple non-linear ground truth model, which is

with no randomness . Its linear approach can be theoretically calculated by

Our aim is to estimate . Thus the hypothesis test can be written as

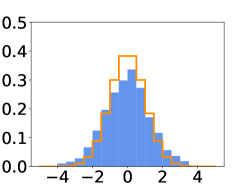

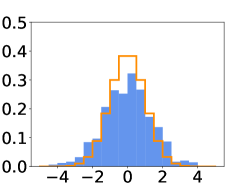

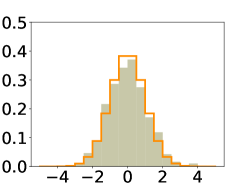

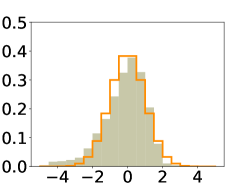

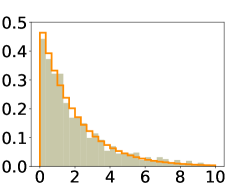

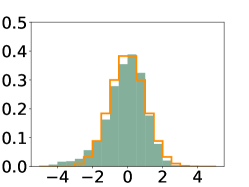

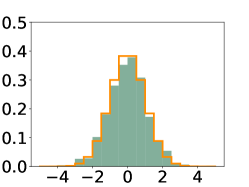

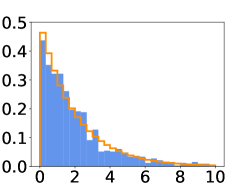

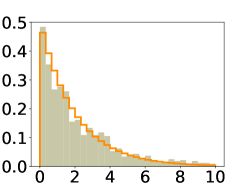

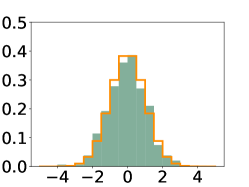

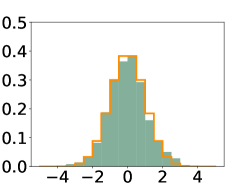

We repeat the simulation 1000 times, each time we calculate the statistic and plot them in Figure 2. We also plot its theoretical distribution, which helps visualize how far the simulation results and theoretical results are. It is visualized in Figure 2 that traditional linear regression fails in even a simple square case, while our new estimator works well. We choose one group of the six here to show the figure.

The phenomenon shown in Figure 2 leads to a fake significance test results! This fake fat-tailed distribution will make more variables determined to be significant incorrectly. For instance, when we set significance level as (which means that the parameter can be determined incorrectly with probability around 0.05), is determined incorrectly in linear regression (LSE) with probability , while Ours(L) with probability . We repeat the experiments six times, and the brackets show a confidence interval. The results of Ours(L) make the significance test more accurate.

We further show its confidence interval for correctness in Table 2 quantitatively, where our newly proposed estimators work better. More details about Table 2 are shown in Appendix E.

| normal () | normal () | ||

|---|---|---|---|

| Linear Reg | 0.1150 () | 0.0635 () | 0.0715 () |

| Ours(NN) | 0.0679 () | 0.0326 () | 0.0650 () |

| Ours(L) | 0.0810 () | 0.0489 () | 0.0276 () |

We compare the efficiency of Ours(NN) and Ours(L) in Table 3 with its confidence interval. Note that since linear regression returns a wrong asymptotic efficiency, it is not listed here.

| Ours(NN) | 0.0214() | 0.0593() |

|---|---|---|

| Ours(L) | 0.0328() | 0.0604 () |

6 Conclusion

In this paper, we propose a new estimator for the linear coefficient that works well in both linear and non-linear cases. Unlike traditional statistical inference methods, machine learning models are introduced to the significance test process. For future work, our new framework may be extended to the more general statistical inference scenarios (e.g. high-dimensional settings), and it will be interesting to show how machine learning models affect the efficiency of our estimator.

Broader Impact

Compared with the traditional significance test, our new methods output a more precise significance level (or p-value) when linear assumptions do not hold. Moreover, with small efficiency loss, one can better extract the relationship between explanatory variables and response variables. Therefore, our estimator might be a better tool for the significance test.

Acknowledgments and Disclosure of Funding

We are grateful to Yang Bai, Chenwei Wu for helpful comments on an early draft of this paper. This work has been partially supported by Shanghai Qi Zhi Institute, Zhongguancun Haihua Institute for Frontier Information Technology, the Institute for Guo Qiang Tsinghua University (2019GQG1002), and Beijing Academy of Artificial Intelligence.

References

- Bachoc et al. [2020] François Bachoc, David Preinerstorfer, Lukas Steinberger, et al. Uniformly valid confidence intervals post-model-selection. The Annals of Statistics, 48(1):440–463, 2020.

- Barber et al. [2019] Rina Foygel Barber, Emmanuel J Candes, Aaditya Ramdas, and Ryan J Tibshirani. Conformal prediction under covariate shift. arXiv: Methodology, 2019.

- Berk et al. [2013] Richard Berk, Lawrence Brown, Andreas Buja, Kai Zhang, Linda Zhao, et al. Valid post-selection inference. The Annals of Statistics, 41(2):802–837, 2013.

- Brambor et al. [2006] Thomas Brambor, William Roberts Clark, and Matt Golder. Understanding interaction models: Improving empirical analyses. Political analysis, 14(1):63–82, 2006.

- Bühlmann et al. [2015] Peter Bühlmann, Sara van de Geer, et al. High-dimensional inference in misspecified linear models. Electronic Journal of Statistics, 9(1):1449–1473, 2015.

- Buja et al. [2015] Andreas Buja, Richard A Berk, Lawrence D Brown, Edward I George, Emil Pitkin, Mikhail Traskin, Linda Zhao, and Kai Zhang. Models as approximations-a conspiracy of random regressors and model deviations against classical inference in regression. Statistical Science, page 1, 2015.

- Casson and Farmer [2014] Robert J Casson and Lachlan DM Farmer. Understanding and checking the assumptions of linear regression: a primer for medical researchers. Clinical & experimental ophthalmology, 42(6):590–596, 2014.

- Cauchois et al. [2020] Maxime Cauchois, Suyash Gupta, and John Duchi. Knowing what you know: valid confidence sets in multiclass and multilabel prediction. arXiv e-prints, page arXiv:2004.10181, April 2020.

- Fahrmexr [1990] Ludwig Fahrmexr. Maximum likelihood estimation in misspecified generalized linear models. Statistics, 21(4):487–502, 1990.

- Friedrich [1982] Robert J Friedrich. In defense of multiplicative terms in multiple regression equations. American Journal of Political Science, pages 797–833, 1982.

- Grünwald et al. [2017] Peter Grünwald, Thijs Van Ommen, et al. Inconsistency of bayesian inference for misspecified linear models, and a proposal for repairing it. Bayesian Analysis, 12(4):1069–1103, 2017.

- Hainmueller and Hazlett [2014] Jens Hainmueller and Chad Hazlett. Kernel regularized least squares: Reducing misspecification bias with a flexible and interpretable machine learning approach. Political Analysis, 22(2):143–168, 2014.

- King and Zeng [2006] Gary King and Langche Zeng. The dangers of extreme counterfactuals. Political Analysis, 14(2):131–159, 2006.

- Law [2006] James Law. Review of "algorithmic learning in a random world by vovk, gammerman and shafer", springer, 2005, ISBN: 0-387-00152-2. SIGACT News, 37(4):38–40, 2006.

- Lee et al. [2016] Jason D Lee, Dennis L Sun, Yuekai Sun, Jonathan E Taylor, et al. Exact post-selection inference, with application to the lasso. The Annals of Statistics, 44(3):907–927, 2016.

- MacKinnon and White [1985] James G MacKinnon and Halbert White. Some heteroskedasticity-consistent covariance matrix estimators with improved finite sample properties. Journal of econometrics, 29(3):305–325, 1985.

- Markiewicz and Puntanen [2019] Augustyn Markiewicz and Simo Puntanen. Linear prediction sufficiency in the misspecified linear model. Communications in Statistics-Theory and Methods, pages 1–20, 2019.

- Osborne and Waters [2002] Jason W Osborne and Elaine Waters. Four assumptions of multiple regression that researchers should always test. Practical Assessment, Research, and Evaluation, 8(1):2, 2002.

- Papadopoulos et al. [2014] Harris Papadopoulos, Vladimir Vovk, and Alex J. Gammerman. Regression conformal prediction with nearest neighbours. CoRR, abs/1401.3880, 2014.

- Rinaldo et al. [2016] Alessandro Rinaldo, Larry Wasserman, Max G’Sell, and Jing Lei. Bootstrapping and sample splitting for high-dimensional, assumption-free inference. arXiv preprint arXiv:1611.05401, 2016.

- Shafer and Vovk [2008] Glenn Shafer and Vladimir Vovk. A tutorial on conformal prediction. J. Mach. Learn. Res., 9:371–421, 2008.

- Taylor et al. [2014] Jonathan Taylor, Richard Lockhart, Ryan J Tibshirani, and Robert Tibshirani. Exact post-selection inference for forward stepwise and least angle regression. arXiv preprint arXiv:1401.3889, 7:10–1, 2014.

- Vershynin [2018] Roman Vershynin. High-Dimensional Probability: An Introduction with Applications in Data Science. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, 2018.

- White [1980] Halbert White. Using least squares to approximate unknown regression functions. International Economic Review, pages 149–170, 1980.

- Zeni et al. [2020] Gianluca Zeni, Matteo Fontana, and Simone Vantini. Conformal prediction: a unified review of theory and new challenges. arXiv preprint arXiv:2005.07972, 2020.

Appendix A Proofs

A.1 The Proof of Lemma 1

This proof is mainly based on Bayesian Estimation, where we have the prior information that .

For a given , we have

The first equation is due to its definition. The second equation is because the probability is zero when . Denote . By setting , we have

We slightly enlarger with , which leads to the results that

The proof is done.

A.2 The Proof of Theorem 1

In this section, we will prove Theorem 1. Before the proof, we propose Lemma 3 first, which focuses on why we need to split the datasets into the training set and the validation set.

Lemma 3 (Independence Lemma)

If and are independent random variables, and is a fixed function which is independent of and , then is independent of .

Proof 1 (Proof of Lemma 3)

The proof directly follows the definition of independence of random variables.

| (2) | ||||

where , is the corresponding measurable sets which is decided by and , . The second equality follows the independence of and . By definition, is independent of . The proof is done.

Corollary 3 (Random Split of Datasets)

Given i.i.d. data which is randomly split into training data and test data . If we use to train a machine learning model , then for two independent samples , , and loss of sample , is independent of .

It should be noted that is trained by , thus is independent of samples in the validation set. That is why the dataset needs to be randomly split. Armed with Corollary 3, we can go on to finish the proof.

We split the proof into two parts. In Lemma 4, we give an approximation measure for the machine learning model . In Lemma 5, we will prove that the linear approximations of two close functions are also close. In this part, we use MSE to measure how the machine learning model approaches ground truth functions.

Lemma 4 (Approximation measure for )

Given an i.i.d. dataset which is split into training set and validation set , where . Suppose we use MSE () as our loss, and the sample loss is denoted as , the population loss is denoted as . Then for a given , we have

Namely, , .

Note that Lemma 4 gives an measure for , which is a probabilistic upper bound. And the results also show a trade-off between training set and validation set. If more data are split into training set, decreases theoretically. If more data are split into validation set, decreases theoretically.

Proof 2 (Proof of Lemma 4)

The key of the proof is Hoeffding’s inequality, which states that given a series of bounded random variables , and , if , then for any , we have

Plug the bound of loss into this inequality. By setting , it holds that

Finally, notice that

The proof is done.

The next Lemma 5 shows that when the distance of two functions is bounded, the distance of their linear approximation is also bounded.

Lemma 5

Given oracle model and machine learning model , where their linear approximation is , , respectively, where is a linear function family. Given , if , then

where d is the dimension of .

Proof 3 (Proof of Lemma 5)

First, we would like to represent in a linear form. For simplification, we omit the superscript for a while.

Then we can derive an explicit representation of

Therefore, by adding the superscript, we have

| (3) |

It can be further calculated that

where the first inequality comes from the definition of matrix norm, the third inequality is due to Cauchy-Schwartz inequality, and the final equality is by the bound of functions and .

If eigenvalues of is denoted by , then

That is to say,

| (4) |

Plug Equation 4 into ,

Therefore, we have

| (5) |

The proof is done.

A.3 The Proof of Corollary 1

Corollary 1 directly follows Theorem 1. From Theorem 1 we know that

where . By Lemma 1, we use empirical bounds to replace the real bounds. That is to say, we use to replace . This operation brings loss, the probability becomes . By the following inequality, we slightly reduce the probability.

So we have, ,

The proof is done.

A.4 The Proof of Lemma 2

The key point of the proof comes from Vershynin [2018] (Page 130). They states that under the assumptions of Lemma 2, the following inequality holds

| (7) |

Therefore, under the assumption that , we have

| (8) |

The proof of Lemma 2 is done.

A.5 The Proof of Theorem 2

By denoting and , where is the residual, the result of Equation 3 can be rewritten as

Then the coefficient can be represented as

where is the row of . Denote the realization of on sample as . Since is bounded by , by using two-side Hoeffding’s inequality, we have

| (9) |

We need to further replace with , which holds that

| (10) |

The first inequality is the triangle inequality, and the second inequality is from the definition of vector norm.

The proof is done.

A.6 The Proof of Corollary 2

We mainly use to replace .

Firstly, notice that ,

We will bound by in the following. First, we know from Lemma 2 that is close to . So we have for every

| (11) |

where , .

Denote , then

The final inequality is from its definition.

Combining them together,

Moreover, we know that

where .

A.7 The Proof of Theorem 3

The key point of this proof is Slutsky’s theorem, which is stated as follows

Lemma 6 (Slutsky’s theorem)

Let and be sequence of scalar / vector / matrix random elements. If converges in distribution to a random element , and converges to a constant , then

-

•

-

•

-

•

provided that is invertible

Furthermore, consider two estimators and . The aim of Theorem 3 is to derive the asymptotic distribution of .

The main intuition is: can reach asymptotic normal distribution due to Central Limit Theorem. So we want to prove the difference of and is sufficiently small, and converges to zero in probability. By Slutsky’s Theorem, the distribution of is then asymptotic normal distribution. But notice that and share different variance (although they converge to the same constant in probability), which will be discussed later.

We first derive the asymptotic distribution of based on Central Limit Theorem. But before that, we now focus on the distribution of . By Multidimensional Central Limit Theorem, consider a series of i.i.d. random vectors , their mean converges to the normal distribution

Furthermore, can be regarded as a transformation of , with mean and variance . We also denote for simplification.

Therefore the following asymptotic property holds

| (12) |

Next we prove the asymptotic property of . Notice that the relationship between and can be stated as follows, where

First, we would like to show some bounded terms. Since is bounded, and the weights in are all bounded, then is bounded. And further we have is bounded, so is bounded. Besides, since we assume is not always zero, and are both two-sided bounded. Since and are both two-sided bounded, and are two-sided bounded.

Besides, since , are bounded, is bounded. And due to bounded , are also bounded.

We will prove this difference converges to zero in probability in the following. Consider the part first. We know that

By Lemma 2, we know that Therefore converge to in probability. . Since is bounded, converges to zero in probability.

Furthermore, since we assume is double-side bounded in probability, then is also bounded in probability. So we have

| (13) |

Next we consider . Since the sample covariance converges to population covariance in probability according to Law of Large Numbers, we have

Combining the covergence of and , by Slutsky’s theorem,

which means that . Since , are assumed to be two-side bounded, we can apply Continuous Mapping Theorem to get

Since we further assume that , are bounded in probability, we can say

| (14) |

Recall that

The proof is done.

Appendix B Significance Test

The significance test is a special type of hypothesis test in statistics, which focuses on whether a parameter is significantly different from zero. In the hypothesis test process, we first assume holds, and then derive the corresponding distribution of certain statistics. The asymptotic properties of an estimator can directly lead to the significance test. For example, we can construct asymptotic normal or asymptotic distribution based on these asymptotic properties.

The significance test can be divided into model test and coefficient test. The model test is used to determining whether a model is significantly different from a constant model, where a constant model means the model predicts each sample as a constant whatever its features are. The model test can also be regarded as the test for a set of features. The coefficient test is used to determining whether a feature can significantly affect its response variable. Usually, we first do the model test. Once the model is significant, we then do the coefficient test.

We show the model test and coefficient test under significance level as follows, where represents the true parameter, represents the estimator of , and represents the estimator of the variance of . Furthermore, is the quantile of distribution, and is the quantile of normal distribution. As in the main text, we use to represent feature of , and to represent row and of a matrix .

The following statements are all based on the asymptotic properties that

1. Model Test

-

•

If , we do not have enough confidence to reject the null hypothesis, which means the model is not significant.

-

•

If , we have enough confidence to reject the null hypothesis, which means the model is significant.

2. Coefficient Test

-

•

If , we do not have enough confidence to reject the null hypothesis, which means the coefficient is not significant.

-

•

If , we have enough confidence to reject the null hypothesis, which means the coefficient is significant.

Notice that we use instead of the true variance , so the better choice of distribution in the coefficient test is t distribution. But we still use the normal distribution for simplification, since when the number of samples is large enough, these two distributions are almost equivalent.

Appendix C Experiment Details

C.1 Experiment Settings

We will compare our proposed method with traditional Linear Regression. In linear regression, we focus on its LSE estimator, and use gradient descent to get . In our new proposed method, we first split the datasets into training set (70%) and validation set (30%) and finally get based on the trained machine learning model (see Section 4.3).

In each case, we test whether the practical asymptotic distribution meets theory. We first propose the hypothesis test

where is the true linear approximation parameter.

Remark: Here we use instead of (in Section 4.3). That is because we aim to test whether in Section 4.3, representing whether the parameter is significantly different from . And here we want to test whether the parameter is significantly different from the true parameter . They are fundamentally the same.

The asymptotic theory tells that and both reach some asymptotic distribution under (at least, we use this in practice). Namely, as Section 4.3 shows, and , where is or , and is the covariance of . We will test whether it is true in practice.

We conduct 1000 trials in each experiments. Each time, we generate a new datasets with and unlabelled data with . And then calculate with unlabelled data , but in practice we can also use together. We compute the correctness (KS statistics) and the efficiency (the average std) based on these 1000 trials.

Furthermore, we conduct each experiment repeatedly six times, and calculate the confidence interval of each statistics. This will help reduce the randomness caused in the experiments.

C.2 Experimental Settings for Unbiasedness Test

In unbiasedness test (Section 5.2), we would like to set with split rate , which means that we use 10 samples for training and 10 samples for validation. We use a smaller dataset compared with Appendix C.1 for better showing the bias. The other hyperparameters will retain as in Appendix C.1 (non-linear cases).

Each time, we calculate the mean of these 1000 trials. After repeating this experiment six times, we calculate its confidence interval. As shown in Section 5, LSE-based methods contain more biasness compared with our methods.

Appendix D Experiments Under Linear Settings

For completeness, we here show the comparison under linear scenarios. We would show that our proposed method also works in a traditional linear scenario, which is

Our aim is to estimate , which can be written as the following hypothesis test

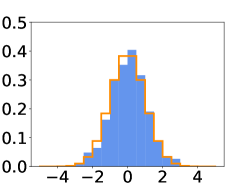

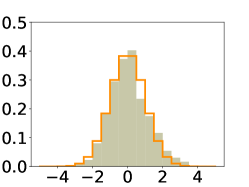

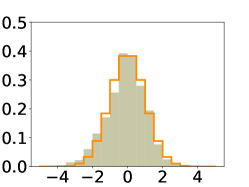

Similar to Figure 2, Figure 3 visualizes the simulation results and theoretical distribution here under linear case, and Table 4 shows the same observations quantifiably. We see that three methods can all reach the true asymptotic distribution successfully. Also, the figure here is one group of the six.

| normal () | normal () | ||

|---|---|---|---|

| Linear Reg | 0.0288() | 0.0368() | 0.0367() |

| Ours(NN) | 0.0643() | 0.0479() | 0.0427() |

| Ours(L) | 0.0474() | 0.0316() | 0.0288() |

Moreover, Table 5 shows the average standard deviation of each methods with their efficiency.

| Linear Reg | 0.0020 () | 0.0035 () |

|---|---|---|

| Ours(NN) | 0.0196() | 0.0323 () |

| Ours(L) | 0.0037() | 0.0064 () |

Appendix E Supplementary Experimental Results

For reducing the randomness in experiments, we conduct each experiment repeatedly six times. We calculate the corresponding mean and average with respect to each trial, which is used to constructing confidence interval.

The confidence interval can be calculated as

We do not show the efficiency of linear regression in main text, since it returns fake significance level, and its efficiency is shown here just for completeness. The full results are listed as follows. They corresponds to Table 1, Table 2, Table 3, Table 4, Table 5. respectively.

| Trial 1 | Trial 2 | Trial 3 | Trial 4 | Trial 5 | Trial 6 | average | std | |

|---|---|---|---|---|---|---|---|---|

| Linear Reg () | -0.1718 | -0.1714 | -0.1695 | -0.1708 | -0.1705 | -0.1747 | -0.1715 | 0.0016 |

| Linear Reg () | 1.0033 | 1.0020 | 0.9976 | 1.0021 | 0.9989 | 1.0048 | 1.0015 | 0.0025 |

| Ours(NN) () | -0.1718 | -0.1644 | -0.1681 | -0.1746 | -0.1649 | -0.1616 | -0.1676 | 0.0045 |

| Ours(NN) () | 1.0193 | 0.9911 | 1.004 | 1.0267 | 0.995 | 0.9924 | 1.0048 | 0.0137 |

| Ours(L) () | -0.1702 | -0.1673 | -0.1624 | -0.1667 | -0.1651 | -0.169 | -0.1668 | 0.0025 |

| Ours(L) () | 1.0093 | 1.0018 | 0.9958 | 1.0055 | 0.9972 | 1.0029 | 1.0021 | 0.0046 |

| Trial 1 | Trial 2 | Trial 3 | Trial 4 | Trial 5 | Trial 6 | average | std | |

|---|---|---|---|---|---|---|---|---|

| Linear Reg () | 0.1289 | 0.1119 | 0.0928 | 0.1176 | 0.1297 | 0.1090 | 0.1150 | 0.0126 |

| Linear Reg () | 0.0669 | 0.0602 | 0.0530 | 0.0585 | 0.0648 | 0.0774 | 0.0635 | 0.0077 |

| Linear Reg () | 0.0727 | 0.0657 | 0.0688 | 0.0583 | 0.0782 | 0.0853 | 0.0715 | 0.0087 |

| Ours(NN) () | 0.0759 | 0.0763 | 0.0649 | 0.0570 | 0.0687 | 0.0648 | 0.0679 | 0.0067 |

| Ours(NN) () | 0.0376 | 0.0343 | 0.0217 | 0.0266 | 0.0440 | 0.0314 | 0.0326 | 0.0072 |

| Ours(NN) () | 0.0702 | 0.0645 | 0.0580 | 0.0555 | 0.0756 | 0.0661 | 0.0650 | 0.0068 |

| Ours(L) () | 0.0919 | 0.0907 | 0.0688 | 0.0729 | 0.0801 | 0.0814 | 0.0810 | 0.0084 |

| Ours(L) () | 0.0461 | 0.0683 | 0.0394 | 0.0411 | 0.0526 | 0.0459 | 0.0489 | 0.0096 |

| Ours(L) () | 0.0264 | 0.0395 | 0.0228 | 0.0273 | 0.0271 | 0.0224 | 0.0276 | 0.0057 |

| Trial 1 | Trial 2 | Trial 3 | Trial 4 | Trial 5 | Trial 6 | average | std | |

|---|---|---|---|---|---|---|---|---|

| Linear Reg () | 0.0148 | 0.0148 | 0.0148 | 0.0148 | 0.0148 | 0.0147 | 0.0148 | 0.0000 |

| Linear Reg () | 0.0257 | 0.0256 | 0.0256 | 0.0256 | 0.0256 | 0.0256 | 0.0256 | 0.0000 |

| Ours(NN) () | 0.0219 | 0.0212 | 0.0210 | 0.0216 | 0.0211 | 0.0213 | 0.0214 | 0.0003 |

| Ours(NN) () | 0.0594 | 0.0574 | 0.0570 | 0.0590 | 0.0569 | 0.0661 | 0.0593 | 0.0032 |

| Ours(L) () | 0.0333 | 0.0325 | 0.0326 | 0.0331 | 0.0329 | 0.0324 | 0.0328 | 0.0003 |

| Ours(L) () | 0.0610 | 0.0600 | 0.0600 | 0.0609 | 0.0604 | 0.0600 | 0.0604 | 0.0004 |

| Trial 1 | Trial 2 | Trial 3 | Trial 4 | Trial 5 | Trial 6 | average | std | |

|---|---|---|---|---|---|---|---|---|

| Linear Reg () | 0.0234 | 0.0339 | 0.0244 | 0.0232 | 0.0248 | 0.0433 | 0.0288 | 0.0074 |

| Linear Reg () | 0.0361 | 0.0395 | 0.0380 | 0.0478 | 0.0301 | 0.0294 | 0.0368 | 0.0062 |

| Linear Reg () | 0.0429 | 0.0341 | 0.0384 | 0.0501 | 0.0278 | 0.0270 | 0.0367 | 0.0082 |

| Ours(NN) () | 0.0708 | 0.0746 | 0.0496 | 0.0727 | 0.0512 | 0.0666 | 0.0643 | 0.0101 |

| Ours(NN) () | 0.0511 | 0.0539 | 0.0519 | 0.0431 | 0.0479 | 0.0395 | 0.0479 | 0.0051 |

| Ours(NN) () | 0.0487 | 0.0412 | 0.0426 | 0.0313 | 0.0443 | 0.0479 | 0.0427 | 0.0057 |

| Ours(L) () | 0.0435 | 0.0618 | 0.0211 | 0.0657 | 0.0347 | 0.0576 | 0.0474 | 0.0159 |

| Ours(L) () | 0.0314 | 0.0250 | 0.0218 | 0.0336 | 0.0481 | 0.0295 | 0.0316 | 0.0084 |

| Ours(L) () | 0.0227 | 0.0212 | 0.0257 | 0.0263 | 0.0328 | 0.0441 | 0.0288 | 0.0078 |

| Trial 1 | Trial 2 | Trial 3 | Trial 4 | Trial 5 | Trial 6 | average | std | |

|---|---|---|---|---|---|---|---|---|

| Linear Reg () | 0.0020 | 0.0020 | 0.0020 | 0.0020 | 0.0020 | 0.0020 | 0.0020 | 0.000 |

| Linear Reg () | 0.0034 | 0.0035 | 0.0035 | 0.0035 | 0.0034 | 0.0034 | 0.0035 | 0.0001 |

| Ours(NN) () | 0.0138 | 0.0135 | 0.0136 | 0.0133 | 0.0139 | 0.0138 | 0.0137 | 0.0002 |

| Ours(NN) () | 0.0230 | 0.0225 | 0.0227 | 0.0222 | 0.0234 | 0.0228 | 0.0228 | 0.0004 |

| Ours(L) () | 0.0036 | 0.0037 | 0.0036 | 0.0036 | 0.0036 | 0.0037 | 0.0036 | 0.0000 |

| Ours(L) () | 0.0063 | 0.0063 | 0.0064 | 0.0063 | 0.0063 | 0.0063 | 0.0063 | 0.0000 |