Tensor Factor Model Estimation by Iterative Projection

Supplementary Material to “Tensor Factor Model Estimation by Iterative Projection”

Abstract

Tensor time series, which is a time series consisting of tensorial observations, has become ubiquitous. It typically exhibits high dimensionality. One approach for dimension reduction is to use a factor model structure, in a form similar to Tucker tensor decomposition, except that the time dimension is treated as a dynamic process with a time dependent structure. In this paper we introduce two approaches to estimate such a tensor factor model by using iterative orthogonal projections of the original tensor time series. These approaches extend the existing estimation procedures and improve the estimation accuracy and convergence rate significantly as proven in our theoretical investigation. Our algorithms are similar to the higher order orthogonal projection method for tensor decomposition, but with significant differences due to the need to unfold tensors in the iterations and the use of autocorrelation. Consequently, our analysis is significantly different from the existing ones. Computational and statistical lower bounds are derived to prove the optimality of the sample size requirement and convergence rate for the proposed methods. Simulation study is conducted to further illustrate the statistical properties of these estimators.

keywords:

[class=MSC2020]keywords:

, , , and

1 Introduction

Motivated by a diverse range of modern scientific applications, analysis of tensors, or multi-dimensional arrays, has emerged as one of the most important and active research areas in statistics, computer science, and machine learning. Large tensors are encountered in genomics (Alter and Golub, 2005, Omberg, Golub and Alter, 2007), neuroimaging analysis (Zhou, Li and Zhu, 2013, Sun and Li, 2017), recommender systems (Bi, Qu and Shen, 2018), computer vision (Liu et al., 2012), community detection (Anandkumar et al., 2014), among others. High-order tensors often bring about high dimensionality and impose significant computational challenges. For example, functional MRI produces a time series of 3-dimensional brain images, typically consisting of hundreds of thousands of voxels observed over time. Previous work has developed various tensor-based methods for independent and identically distributed (i.i.d.) tensor data or tensor data with i.i.d. noise. However, as far as we know, the statistical framework for general tensor time series data was not well studied in the literature.

Factor analysis is one of the most useful tools for understanding common dependence among multi-dimensional outputs. Over the past decades, vector factor models have been extensively studied in the statistics and economics communities. For instance, Chamberlain and Rothschild (1983), Bai and Ng (2002), Stock and Watson (2002) and Bai (2003) developed the static factor model using principal component analysis (PCA). They assumed that the common factors must have impact on most of the time series, and weak serial dependence is allowed for the idiosyncratic noise process. Fan, Liao and Mincheva (2011, 2013), Fan, Liu and Wang (2018) established large covariance matrix estimation based on the static factor model. The static factor model has been further extended to the dynamic factor model in Forni et al. (2000). The latent factors are assumed to follow a time series process, which is commonly taken to be a vector autoregressive process. Fan, Liao and Wang (2016) studied semi-parametric factor models through projected principal component analysis. Pena and Box (1987), Pan and Yao (2008), Lam, Yao and Bathia (2011) and Lam and Yao (2012) adopted another type of factor model. They assumed that the latent factors capture all dynamics of the observed process, and thus the idiosyncratic noise process has no serial dependence. We will adopt this approach. We note that the factor process may have complex dynamic behavior, resulting in complex dynamics of the observed tensor, even with white additive noise process. Of course, when all the dynamics of the observed tensor process are ‘forced’ to be included in the signal process induced by the factor process, situations may arise in which some factors are ‘weak’ (or have impact on a small portion of the observed series in the tensor). This leads us to consider the ‘signal strength’ in our investigation.

Although there have been significant efforts in developing methodologies and theories for vector factor models, there is a paucity of literature on matrix- or tensor-valued time series. Wang, Liu and Chen (2019) proposed a matrix factor model for matrix-valued time series, which explores the matrix structure. Chen, Tsay and Chen (2020) established a general framework for incorporating domain and prior knowledge in the matrix factor model through linear constraints. Chen and Chen (2019) applied the matrix factor model to the dynamic transport network. Chen and Fan (2021) developed an inferential theory of the matrix factor model under a different setting from that in Wang, Liu and Chen (2019) .

Recently, Chen, Yang and Zhang (2021) introduced a factor approach for analyzing high dimensional dynamic tensor time series in the form

| (1.1) |

where are the observed tensor time series, and are the corresponding signal and noise components of , respectively. The goal is to estimate the unknown signal tensor from the tensor time series data. Following Lam and Yao (2012), it is assumed that the signal tensor accommodates all dynamics, making the idiosyncratic noise uncorrelated (white) across time. It is further assumed that lives in a lower dimensional space and has certain multilinear decomposition. Specifically, we assume that satisfies a Tucker-type decomposition and model (1.1) can be written as

| (1.2) |

where is the deterministic loading matrix of size and , and the core tensor itself is a latent tensor factor process of dimension . Here the -mode product of with a matrix , denoted as , is an order -tensor of size such that

The core tensor is usually much smaller than in dimension. This structure provides an effective dimension reduction, as all the comovements of individual time series in are driven by . Without loss of generality, assume that is of rank . It should be noted that vector and matrix factor models can be viewed as special cases of our model since a vector time series is a tensor time series composed of a single fiber (), and a matrix times series is one composed of a single slice ().

Chen, Yang and Zhang (2021) proposed two estimation procedures, namely TOPUP and TIPUP, for estimating the column space spanned by the loading matrix , for . The two procedures are based on different auto-cross-product operations of the observed tensors to accumulate information, but they both utilize the assumption that the noise and are uncorrelated. The convergence rates of their estimators critically depend on , a potentially very large number as , are large. Often a large , the length of the time series, is required for accurate estimation of the loading spaces.

In this paper we propose extensions of the TOPUP and TIPUP procedures, motivated by the following observation. Suppose that the loading matrices are orthonormal with , and we are given . Let

Then (1.2) leads to

| (1.3) |

where is a tensor. Since , is a much smaller tensor than . Under proper conditions on the combined noise tensor , the estimation of the loading space of based on can be made significantly more accurate, as the convergence rate now depends on rather than .

Of course, in practice we do not know . Similar to backfitting algorithms, we propose an iterative algorithm. With a proper initial value, we iteratively estimate the loading space of at iteration based on

using the estimate obtained in the previous iteration and the estimate , obtained in the current iteration. Our theoretical investigation shows that the iterative procedures for estimating can achieve the convergence rate as if all are known and we indeed observe that follows model (1.3). We call the procedure iTOPUP and iTIPUP, based on the matrix unfolding mechanism used, corresponding to TOPUP and TIPUP procedures. To be more specific, our algorithms have two steps: (i) We first use the estimated column space of factor loading matrices of TOPUP (resp. TIPUP) to construct the initial estimate of factor loading spaces; (ii) We then iteratively perform matrix unfolding of the auto-cross-moments of much smaller tensors to obtain the final estimators.

We note that the iterative procedure is related to higher order orthogonal iteration (HOOI) that has been widely studied in the literature; see, e.g., De Lathauwer, De Moor and Vandewalle (2000), Sheehan and Saad (2007), Liu et al. (2014), Zhang and Xia (2018), among others. However, most of the existing works are not designed for tensor time series. They do not consider the special role of the time mode nor the covariance structure in the time direction. Typically HOOI treats the signal part as fixed or deterministic. In this paper we treat the signal as dynamic in the sense that the core tensor in (1.2) is dynamic and the relationship between and the lagged is of interest. Our setting requires special treatment although each iteration of our iterative procedures also consists of power up and orthogonal projection operations. While HOOI applies the SVD directly to the matrix unfolding of the iteratively projected data, in our approach the SVD is applied to the matrix unfolding of the outer- and inner-auto-cross-product of the iteratively projected data, respectively in iTOPUP and iTIPUP. Although the iTOPUP algorithm proposed here can be reformulated as a twist of HOOI on the auto-cross-moment tensor, the iTIPUP algorithm is different and cannot be recast equivalently as HOOI. More importantly, the theoretical analysis and theoretical properties of the estimators are fundamentally different from those of HOOI, due to the dynamic structure of tensor time series and the need to use the auto-cross-product operation between the SVD and data projection in each iteration. Different concentration inequalities are derived to study the performance bounds.

In this paper, we establish upper bounds on the estimation errors for both the iTOPUP and the iTIPUP, which are much sharper than the respective theoretical guarantees for TOPUP and TIPUP, demonstrating the benefits of using iterative projection. It is also shown that the number of iterations needed for convergence is of order no greater than . We mainly focus on the cases where the tensor dimensions are large and of similar order. We also cover the cases where the ranks of the tensor factor process increase with the dimensions of the tensor time series.

Chen, Yang and Zhang (2021) showed that the TIPUP has a faster convergence rate in estimation error than the TOPUP, under a mild condition on the level of signal cancellation. In contrast, the theoretically guaranteed rate of convergence for the iTOPUP in this paper is of the same order or even faster than that for the iTIPUP under certain regularity conditions. Our results also suggest an interesting phenomenon. Using the iterative procedures, we find that the increase in either dimension or sample size can improve the estimation of the factor loading space of the tensor factor model with the tensor order . We believe that such a super convergence rate is new in the literature. Specifically, under proper regularity conditions, the convergence rate of the iterative procedures for estimating the space of is , where , while the existing rate for non-iterative procedures is for the vector factor model (Lam, Yao and Bathia, 2011) and the matrix/tensor factor models (Wang, Liu and Chen, 2019, Chen, Yang and Zhang, 2021). While the increase in the dimensions () does not improve the performance of the non-iterative estimators, it significantly improves that of the proposed iterative estimators.

In addition, we establish the computational lower bound for the estimation of the loading spaces of tensor factor models under the hardness assumption of certain instances of hypergraphic planted clique detection problem. It shows that the sample size requirement (or signal to noise ratio condition) needed for using the TIPUP estimate as the initial values for the iterative procedures is unavoidable for any computationally manageable estimation procedure to achieve consistency, although the iterative procedures have faster convergence rates. Moreover, we provide a statistical lower bound which matches the rates of convergence of our iterative procedures under proper conditions.

Related work. We close this section by highlighting several recent papers on related topics. First, we draw attention to the work of Foster (1996), Fan, Liao and Wang (2016) and Chen et al. (2020). Chen et al. (2020) adopts a spectral initialization plus an iterative refinement step estimating procedure, so that our methods are related to theirs. However, due to the differences in problem setting and model assumptions, their estimation procedures, performance bounds and analytic techniques are all significantly different from ours. Foster (1996), Fan, Liao and Wang (2016) use the projection to the space spanned by the sieve bases without iteration. Rogers, Li and Russell (2013) assumes the tensor factor model in (1.2), with an additional specific AR structure on the dynamic of the factor process. The additional model structure led to an EM type of estimation approach, quite different from the approach we develop here. Wang, Zheng and Li (2021) concerns low rank tensor AR model and uses a nuclear norm penalty to enforce the low rank structure and optimization algorithms for estimation, again quite different from our approach.

The paper is organized as follows. Section 2.1 introduces basic notation and preliminaries of tensor analysis. We present the tensor factor model and the iTOPUP and iTIPUP procedures in Sections 2.2 and 2.3. Theoretical properties of the iTOPUP and iTIPUP are investigated in Section 3. Section 4 provides a brief summary. Numerical comparison of our iterative procedures and other methods, and all technical details are relegated to the Supplementary Material.

2 Tensor Factor Model by Orthogonal Iteration

2.1 Notation and preliminaries for tensor analysis

Throughout this paper, for a vector , define , . For a matrix , write the SVD as , where , with the singular values in descending order. The matrix spectral norm is denoted as Let (resp. ) be the smallest (resp. largest) nontrivial singular value of . For two sequences of real numbers and , write (resp. ) if there exists a constant such that (resp. ) for all sufficiently large , and write if . Write (resp. ) if there exist a constant such that (resp. ). Denote and . We use to denote generic constants, whose actual values may vary from line to line.

For any two matrices with orthonormal columns, say, and , suppose the singular values of are . A natural measure of distance between the column spaces of and is then

| (2.1) |

which equals to the sine of the largest principle angle between the column spaces of and .

For any two matrices , denote the Kronecker product as . For any two tensors , denote the tensor product as , such that

Let be the vectorization of matrices and tensors. The mode- unfolding (or matricization) is defined as , which maps a tensor to a matrix where . For example, if , then

For tensor , the Hilbert Schmidt norm is defined as

For a matrix, the Hilbert Schmidt norm is just the Frobenius norm. Define the tensor operator norm for an order-4 tensor ,

where and .

2.2 Tensor factor model

Again, we consider as in (1.2)

Without loss of generality, assume that is of rank . is not necessarily orthonormal, which is different from the classical Tucker decomposition (Tucker, 1966). Model (1.2) is unchanged if we replace by for any invertible matrix . Although are not uniquely determined, the factor loading space, that is, the linear space spanned by the columns of , is uniquely defined. Denote the orthogonal projection to the column space of as

| (2.2) |

where is the left singular matrix in the SVD . We use to represent the factor loading space of . Thus, our objective is to estimate .

The canonical representation of the tensor times series (1.2) is written as

where the diagonal and right singular matrices of are absorbed into the canonical core tensor . In this canonical form, the loading matrices are identifiable up to a rotation in general and up to a permutation and sign changes of the columns of when the singular values are all distinct in the population version of the TOPUP or TIPUP methods, as we describe in Section 2.3 below. In what follows, we may identify the tensor time series in its canonical form, i.e. , without explicit declaration.

We do not impose any specific structure for the dynamics of the core tensor factor process beyond the independence between the core process and the noise process, and we do not require any additional structure on the correlation among different time series fibers of the noise process . Because of this generality, our estimator is based on the tensor version of the lagged sample cross product , , where

| (2.3) |

which is an order- tensor. The population version of this tensor autocovariance is

Because for all ,

with the notation and for all .

2.3 Estimating procedures

In this paper, we consider iterative estimation procedures to achieve sharper convergence rates than the TOPUP and TIPUP procedures proposed in Chen, Yang and Zhang (2021). We start with a quick description of their procedures as they serve as the starting point of our proposed iTOPUP and iTIPUP procedures. Note that the procedure in Chen and Chen (2019) and Wang, Liu and Chen (2019) is the non-iterative TOPUP.

(i). Time series Outer-Product Unfolding Procedure (TOPUP):

Let be the sample autocovariance of the data as in (2.3). Define

| (2.4) |

as a matrix, where , and is a predetermined positive integer. Here we note that is a function mapping a tensor time series to a matrix. In , the information from different time lags is accumulated, which is useful especially when the sample size is small. A relatively small is typically used, since the autocorrelation is often at its strongest with small time lags. See Remark 3.8.

The TOPUP method performs SVD of (2.4) to obtain the truncated left singular matrices

where LSVDm stands for the left singular matrix composed of the first left singular vectors corresponding to the largest singular values. Here we emphasize that is treated as an operator that maps a tensor data set to a matrix of columns. It will be applied to different transformed data sets. On the other hand, is treated as fixed, based on the given under study. Note that LSVD can be obtained using eigen decomposition as well. For simplicity, we write

| (2.5) |

where is the mode- rank. Again, we emphasize that takes input of a tensor time series of length with the target mode- having dimension and rank , and produces an output matrix of size as the estimate of the mode- loading matrix .

By (1.2) and (2.3), the expectation of (2.4) satisfies

| (2.6) | |||

so that the TOPUP is expected to be consistent in estimating the column space of .

(ii). Time series Inner-Product Unfolding Procedure (TIPUP):

Similar to (2.4), define a matrix as

| (2.7) |

which replaces the tensor product by the inner product through (2.3) in (2.4). The TIPUP method performs SVD:

for . Again, is treated as an operator. For simplicity, we write

| (2.8) |

where is the mode- rank. Note that

where is an order- tensor with elements , , , , . Here, is defined as an inner product summation over all indices other than .

(iii). iTOPUP and iTIPUP: Next we describe a generic iterative procedure under the motivation described in Section 1. Its pseudo-code is provided in Algorithm 1. It incorporates two estimators/operators UINIT and UITER that map a tensor time series to an estimate of the loading matrix. The UTOPUP and UTIPUP operators in (2.5) and (2.8) are examples of such operators.

When we use the UTOPUP operator (2.5) for both UINIT and UITER in Algorithm 1, it will be called iTOPUP procedure. Similarly, iTIPUP uses UTIPUP operator (2.8) for both UINIT and UITER. Besides these two versions, we may also use UTIPUP for UINIT and UTOPUP for UITER, named as TIPUP-iTOPUP. Similarly, TOPUP-iTIPUP uses UTOPUP as UINIT and UTIPUP as UITER. These variants are sometimes useful, because TOPUP and TIPUP have different theoretical properties as the initializer or for iteration, as we will discuss in Section 3. Other estimators of the loading spaces based on the tensor time series can also be used in place of UINIT and UITER, such as the conventional high order SVD for tensor decomposition, which we refer to as Unfolding Procedure (UP), that simply performs SVD of the matricization along the appropriate mode of the order tensor with time dimension as the additional -th mode.

Remark 2.1.

While Algorithm 1 resembles an HOOI-type iteration of the orthogonal projection and singular matrix estimation methods, the proposed iTOPUP and iTIPUP are significantly different from HOOI which iterates the operations of

| orthogonal projection matrix unfolding SVD. |

In both iTOPUP and iTIPUP, each iteration carries out the operations

| (2.10) |

As the outer product is taken with TOPUPk in (2.4), its orthogonal projection and autocovariance operations are exchangeable, so that we can write

as long as the HOOI is modified by applying to both mode and mode in the projection operation and leaving alone the -th mode in the lags throughout. However, for iTIPUP, the orthogonal projection and autocovariance operations in (2.10) are not exchangeable as the projections are sandwiched inside the autocovariance. Needless to say, the analysis of iTOPUP and iTIPUP is much more difficult than the conventional HOOI with iid assumption due to the involvement of the autocovarinace operations in the time-axis in the iterations.

Remark 2.2 (Rank determination).

Here the estimators are constructed with given ranks , though in theoretical analysis they are allowed to diverge. In practice, existing procedures for rank determination in the vector factor model, including the information criteria approach (Bai and Ng, 2002, 2007, Hallin and Liška, 2007) and ratio of eigenvalues approach (Lam and Yao, 2012, Ahn and Horenstein, 2013) can be extended to the tensor factor model by treating tensors as -dimensional vectors, .

3 Theoretical Properties

In this section we present some theoretical properties of the iterative procedures. We first present the additional notations needed for the discussion, then the error bounds for the iterative estimators under a minimum condition on the error process in the model. These error bounds are quite general and cover many different models. To help decipher the general results, we then present two concrete models (or still general sets of assumptions) of the signal process of the model, under which we will be able to obtain simpler and more explicit convergence rates.

3.1 Notations

We introduce some notations first. Let . Define , , and . Define order-4 tensors

| (3.1) | ||||

with from the SVD . We view as the canonical version of the auto-covariance of the factor process. The noiseless version of the matrix TOPUPk in (2.4) is

| (3.2) |

with . The canonical factor version of (3.2) is with . Similarly define

| (3.3) | ||||

The noiseless version of (2.7) is

| (3.4) |

and its canonical factor version is . Let be the -th singular value of the noiseless version of the TOPUPk matrix,

The signal strength for iTOPUP can be characterized as

| (3.5) |

Similarly, let

The signal strength for iTIPUP can be characterized as

| (3.6) |

We note that by (3.3) and the Cauchy-Schwarz inequality,

3.2 General error bounds

Our general error bounds for the proposed iTOPUP and iTIPUP are established under the following assumption for the error process.

Assumption 1.

The error process are independent Gaussian tensors conditionally on the factor process . In addition, there exists some constant , such that

Assumption 1 is used by Chen, Yang and Zhang (2021) for the theoretical investigation of the non-iterative TIPUP and TOPUP, and is similar to those on the noise imposed in Lam, Yao and Bathia (2011), Lam and Yao (2012). The normality assumption, which ensures fast convergence rates in our analysis, is imposed for technical convenience. It accommodates general patterns of dependence among individual time series fibers, but also allows a presentation of the main results with manageable analytical complexity. In fact, direct extension is visible in our analysis under the sub-Gaussian and even more general tail probability conditions. Under Assumption 1 the magnitude of the noise can be measured by the dimension before the projection and by the rank after the projection. The main theorems (Theorems 3.1, 3.2 and 3.3) in this section are based on this assumption on the noise alone, and cover all thereafter discussed settings of the signal .

Let us first study the behavior of iTOPUP procedure. By Chen, Yang and Zhang (2021), the risk of the TOPUP estimator for , the initialization of iTOPUP, is no larger than a constant times

| (3.7) | ||||

where and . The aim of iTOPUP is to achieve dimension reduction by projecting the data in other modes of the tensor time series from to , . Ideally (e.g. when the true projection matrices are used), this would reduce the above rate in (3.7) to

| (3.8) | ||||

by replacing all with , . However, because the iteration uses the estimated of total dimension , our analysis also involves the following additional error term,

| (3.9) |

The following theorem provides conditions under which the ideal rate is indeed achieved.

Theorem 3.1.

Suppose Assumption 1 holds. Let and , , and be as in (2.2), (3.1), (3.3) and (3.5) respectively. Let with the in (3.7), with the in (3.8), and with the in (3.9). Let with the -step estimator in the iTOPUP algorithm. Then, the following statements hold for a certain numerical constant and a constant depending on only: When

| (3.10) |

with a constant , it holds simultaneously for all and that

| (3.11) |

in an event with probability at least . In particular, after at most iterations,

| (3.12) |

Remark 3.1.

The essence of our analysis of iTOPUP is that under (3.10), each iteration is a contraction of the error in the estimation of in a small neighborhood of it. The upper bound (3.11) for the error of the -step estimator is comprised of two terms respectively corresponding to the cumulative iteration error and the contracted error of the initial estimator. Of course, after sufficiently large number of iterations, the first term would dominate the second as in (3.12).

Remark 3.2.

The constant is taken in (3.10) to guarantee sufficient accuracy of the initialization of iTOPUP in the following sense:

| (3.13) |

with at least probability . The consistency of the non-iterative TOPUP estimator requires (Chen, Yang and Zhang, 2021). However, here we do not require the TOPUP estimator as the initial value to be consistent. For (3.11) to hold, the TOPUP estimator is only required to be sufficiently close to the ground truth as in (3.13).

Remark 3.3.

It is relatively easy to verify that the first part of (3.10) implies the second part under many circumstances, including when are of the same order, are of the same order, and (). In Zhang and Xia (2018), condition is imposed to control the complexity of the estimated in HOOI although their error bound is sharp and their model is very different. In Corollaries 3.1 and 3.3 below, we prove that the second part of (3.10) follows from the first part respectively in a general fixed rank model and a general diverging rank model. In fact typically so that the second part of (3.10) provides a non-asymptotic lower bound for the in (3.11), allowing . In Corollary 3.1 below, is taken in (3.10) to give (3.12) in one iteration when dominates .

Remark 3.4.

When the loading matrices and the TOPUP version of the matrix unfolding of the auto-covariance of all have bounded condition numbers and average squared entries of magnitude 1, , and are all of the order poly. In this case, Theorem 3.1 just requires poly for the initialization to achieve through iteration the fast convergence rate poly. See Corollary 3.3 for details. This is in sharp contrast to the results of traditional factor analysis which requires to consistently estimate the loading spaces. The main reason is that the other tensor modes provide additional information and in certain sense serve as additional samples. Roughly speaking, we have totally observations in the tensor time series to estimate the parameters in the projection to the column space of the loading matrix , where in the above “regular” case.

Now, let us consider the statistical performance of iTIPUP procedure. Again, by Chen, Yang and Zhang (2021) the TIPUP risk in the estimation of is bounded by

| (3.14) |

with , and the aim of iTIPUP is to achieve the ideal rate

| (3.15) |

through dimension reduction, where . As in the case of iTOPUP, our error bound for iTIPUP involves the additional error term

| (3.16) |

The following theorem, which allows the ranks to grow to infinity as well as when , provides sufficient conditions to guarantee the ideal convergence rate for iTIPUP.

Theorem 3.2.

Suppose Assumption 1 holds. Let , and be as in (2.2), (3.3) and (3.6) respectively. Let , and

with in (3.14), in (3.15) and in (3.16). Let with the -step estimator in iTIPUP algorithm. Then, the following statements hold for a certain numerical constant and a constant depending on only: When

| (3.17) |

with a constant , it holds simultaneously for all and that

| (3.18) |

in an event with probability at least . In particular, after at most iterations,

| (3.19) |

We briefly discuss the conditions and conclusions of Theorem 3.2 as the details are parallel to the remarks below Theorme 3.1. By (3.3), (3.6) and the Cauchy-Schwarz inequality, , so that the first condition in (3.17) guarantees a sufficiently small , which implies a sufficiently small error in the initialization of iTIPUP by (3.14). The second condition in (3.17) again has two terms respectively reflecting the ideal rate after dimension reduction by the true in the estimation of and the extra cost of estimating . The upper bound (3.18) for the error of the -step estimator is also comprised of two terms representing the cumulative iteration error and contracted initialization error. In Corollary 3.2 below with fixed , the smallest is taken in (3.17) to achieve (3.19) in one iteration when dominates . Moreover, Theorem 3.2 allows diverging ranks and convergence rate poly under proper conditions as discussed in Remark 3.4.

As discussed in Section 2.3, we can mix the TOPUP and TIPUP operations for the initiation and iterative operations in Algorithm 1. For example, the proof of Theorems 3.1 yields the following error bound for the mixed TIPUP-iTOPUP algorithm.

Theorem 3.3.

Assumption 1 holds. Let , and be as in Theorem 3.1 and be as in Theorem 3.2. Let with being the -step estimator in the TIPUP-iTOPUP algorithm. Then, the following statement holds for a certain numerical constant and a constant depending on only: When

| (3.20) |

with a constant , it holds in an event with probability at least that simultaneously for all and

We omit the statement of an analogous error bound for the TOPUP-iTIPUP algorithm.

3.3 Fixed rank factor process

In this section we provide the convergence rate when the dimensions of the factors , or equivalently the ranks of the signal process , , are fixed, and the auto-cross-outer-product of the factor process is ergodic. Formally, we impose the following additional assumption.

Assumption 2.

The ranks are fixed. The factor process is weakly stationary and its auto-cross-outer-product process is ergodic in the sense of

where the elements of are all finite. In addition, the condition numbers of () are bounded. Furthermore, assume that is fixed, and

(i) (TOPUP related): is of rank for .

(ii) (TIPUP related): is of rank for .

Under Assumption 2, the factor process has a fixed expected auto-cross-moment tensor with fixed dimensions. The assumption that the condition numbers of () are bounded corresponds to the pervasive condition (e.g., Stock and Watson (2002), Bai (2003)). It ensures that all the singular values of are of the same order. Such conditions are commonly imposed in factor analysis.

As our methods are based on auto-cross-moment at nonzero lags, we do not need to assume any specific model for the latent process , except some rank conditions in Assumption 2(i) and (ii). Since the columns of are linear combinations of those of and and have the same rank, Assumption 2(ii) implies Assumption 2(i).

In order to provide a more concrete understanding of Assumption 2(i) and (ii), consider the case of and . We write the factor process , and the stationary auto-cross-moments . Hence is a matrix, with columns being . Since is a sum of many semi-positive definite matrices, if any one of these matrices is full rank, then is of rank . Hence Assumption 2(i) is relatively easy to fulfill. On the other hand, Assumption 2(ii) is quite different. First, the condition is imposed on the canonical form of the model as the inner product in TIPUP related procedures behaves differently. Let , and ). Then . As may be positive or negative for different , the summation is subject to potential signal cancellation for . Assumption 2(ii) ensures that there is no complete signal cancellation that makes the rank of less than . While the signal cancellation rarely causes the rank deficiency, the resulting loss of efficiency may still have an impact on the finite sample performance as our simulation results demonstrate. Of course complete signal cancellation is less likely with larger .

Corollary 3.1.

Corollary 3.1 asserts that, in order to recover the factor loading space for , the signal to noise ratio needs to satisfy as in (3.21), and the ideal rate (3.22) can be achieved in one iteration. The ideal rate is much sharper than the convergence rate of the non-iterative TOPUP in Chen, Yang and Zhang (2021).

The following corollary is a simplified version of Theorem 3.2 under Assumption 2(ii), which excludes severe signal cancellation in iTIPUP.

Corollary 3.2.

Compared with the results in Corollary 3.1 for iTOPUP, the achieved ideal rate (3.24) is the same. However, the signal-to-noise ratio requirement (3.23) is weaker but Assumption 2(ii) is stronger in Corollary 3.2 for iTIPUP. Again, the ideal rate is much sharper than the convergence rate of the non-iterative TIPUP in Chen, Yang and Zhang (2021).

3.4 Diverging ranks

The main theorems in Subsection 3.2 allow for the case where the dimensions of the core factor, , diverge as the dimensions of the observed tensor grow to infinity. The following assumption provides a concrete set of conditions that can be used to provide some insights of the properties of iTOPUP and iTIPUP in such scenarios.

Assumption 3.

For a certain ,

and with probability approaching one.

For the singular values, two scenarios are considered.

(i) (TOPUP related): There exist some constants and such that with probability approaching one (as ) , for all .

(ii) (TIPUP related):

There exist some constants , and such that with probability approaching one (as ), for all .

Assumption 3 is similar to the signal strength condition of Lam and Yao (2012), and the pervasive condition on the factor loadings (e.g., Stock and Watson (2002) and Bai (2003)). It is more general than Assumption 2 in the sense that it allows to diverge and the latent process does not have to be weakly stationary.

We take as measures of the strength of the signal process . They roughly indicate how much information is contained in the signals compared with the amount of noise, with respect to the dimensions and ranks, and . In this sense, they reflect the signal to noise ratio. When , the factors are called strong factors; otherwise, the factors are called weak factors.

Remark 3.5 (Signal Strength and the index ).

We note that , and that and when the data is in general position, where is treated as a matrix. Thus, if is the signal-to-noise ratio, then the condition holds when is the order of the effective rank of and the condition holds when is the order of the effective rank of . Because the signal has elements at each , the assumption says that the squared ratio of the elements and the noise level is averaged over time and space. Thus, the factor is called strong when . In view of (1.1) and (1.2), , so that we may have weaker factor with when the loading matrices are sparse or have some relatively small singular components. We note that by Cauchy-Schwarz, the signal-to-noise ratio conditions also imply and respectively.

Remark 3.6 (Assumption 3(i) and the role of ).

In fact, for TOPUP, Assumption 3(i) holds when (a) and (b) all the nonzero singular values of are of the same order. Because by the condition on the signal-to-noise ratio, we must have , and can be viewed as the order of average auto-correlation over lags . For and , the factor process in the canonical form is , and is the time average cross product between the factor fibers and . Thus, the first condition (a) means .

Remark 3.7 (Assumption 3(ii), the role of and signal cancellation).

The points parallel to those in Remark 3.6 are applicable to TIPUP, but with one caveat: Beyond the average auto-correlation, an additional discount is needed to take into account the impact of possible signal cancellation with TIPUP and its iteration. For and , , and the summation inside the square is subject to signal cancellation for since the auto-cross-moment can have different signs. The additional parameter measures the severity of signal cancellation in the TIPUP related procedures. For example, when the majority of are of the same sign for most of , it would be reasonable to assume . When behave like independent mean zero variables, would be close to . And when all the signals cancel out by the summation over . In the case of fixed , the convergence rate depends on whether (severe signal cancellation) or not.

Remark 3.8 (The role of ).

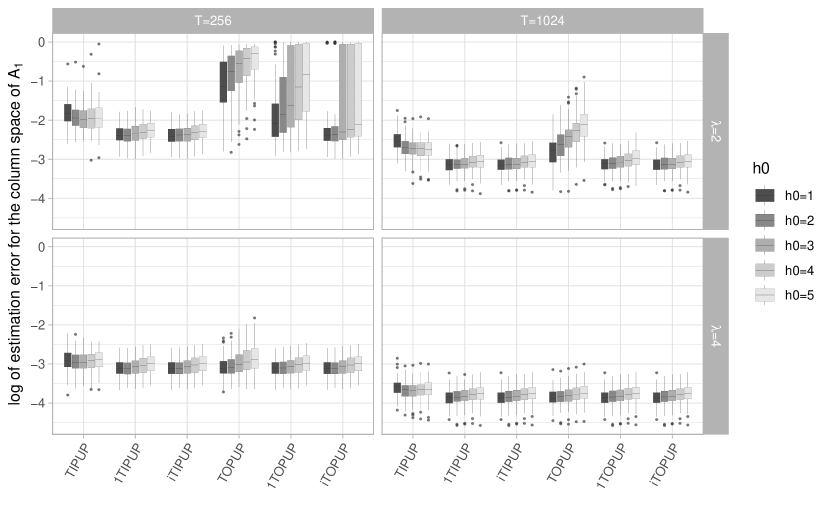

The selection of is a relative minor problem in practice though very complex to analyze. Theoretically it suffices to use an with of the right order, so that choosing a somewhat large would not harm the convergence rate for the proposed methods. In practice a small (less than 3) is often sufficient. The impact of the choice of on the signal and noise depends on the autocorrelation of the factor process, as well as the loading matrices. For example, if the factor process is of very short memory (e.g. an MA(1) process), including any lag only introduces noise to TOPUPk in (2.4) and TIPUPk in (2.7) without enhancing the signal. On the other hand, including an extra lag is the most simple and effective way to prevent signal cancellation with iTIPUP, as discussed in the previous remark. Increasing includes more non-negative terms in the signal strength , hence potentially reducing the chance of severe signal cancellation. The simulation results presented in the supplementary material provide some empirical behavior of choosing different . While the choice of will affect the assumptions, in practice we may compare the patterns of estimated singular values under different lag values in iTOPUP and iTIPUP to evaluate the benefit of taking a larger . See also the simulation study.

We describe below the convergence rate of iTOPUP in terms of , and under Assumption 3(i) when the dimensions of the core factor are allowed to diverge.

Corollary 3.3.

Suppose Assumptions 1 and 3(i) hold. Let , and . Suppose that for a sufficiently large not depending on ,

| (3.25) |

Then, after iterations, we have the following upper bounds for iTOPUP,

| (3.26) |

Moreover, (3.26) holds after at most iterations, if any one of the following three conditions holds in addition to (3.25): (i) () are of the same order, (ii) () are of the same order, (iii) () are of the same order.

Note that the second part of Corollary 3.3 says that when the condition is right, iTOPUP algorithm only needs a small number of iterations to converge, as is typically very small. The noise level does not appear directly in the rate since it is incorporated in the signal to noise ratio in the tensor form in Assumption 3. In Corollary 3.3, we show that as long as the sample size satisfies (3.25), the iTOPUP achieves consistent estimation under regularity conditions. To digest (3.25), consider that the growth rate of is much slower than and the factors are strong with . Then (3.25) becomes .

The advantage of using index is to link the convergence rates of the estimated factor loading space explicitly to the strength of factors. It is clear that the stronger the factors are, the faster the convergence rate is. Moreover, the stronger the factors are, the smaller the sample size is required.

When the ranks () also diverge and there is no severe signal cancellation in iTIPUP, we have the following convergence rate for iTIPUP under Assumption 3(ii).

Corollary 3.4.

Suppose Assumptions 1 and 3(ii) hold. Let and . Suppose that for a sufficiently large not depending on ,

| (3.27) |

Then, after at most iterations, the iTIPUP estimator satisfies

| (3.28) |

Moreover, (3.28) holds after at most iterations, if any one of the following three conditions holds in addition to condition (3.27), (i) () are of the same order, (ii) () are of the same order, (iii) () are of the same order.

When the average auto-correlation is of unit order and the signal cancellation for TIPUP has no impact on the order of the signal ( and respectively), Corollary 3.4 requires the sampling rate and provides the convergence rate . For examples, gives the rate when and , and the sample size requirement can be written as when regardless of . Thus, the side condition involving in the second part of (3.17) is absorbed into the other components of (3.17).

Corollary 3.3 and Corollary 3.4 offer comparison of the iTOPUP and iTIPUP when the ranks diverge from two perspectives: sample size requirements and convergence rates. The lower bounds on in (3.25) in Corollary 3.3 and (3.27) in Corollary 3.4 provide the sample complexity of the iTOPUP and iTIPUP respectively. In the case that the growth rate of is much slower than and the factors are strong with , the required sample size of the iTIPUP reduces to , where and . By comparing with the comment after Corollary 3.3, where the sample size requirement for the iTOPUP is when , it can be seen that the sample complexity for the iTIPUP is smaller, if is a small constant. From the perspective of convergence rate, let us compare (3.26) in Corollary 3.3 and (3.28) in Corollary 3.4. When ranks diverge, iTIPUP is slower than iTOPUP if and faster if , no matter how strong the factor is or what values take. As expected, the convergence rate is slower in the presence of weak factors. See the simulation for more empirical evidence.

Corollary 3.5.

Suppose Assumptions 1 and 3 hold. Let and . Suppose that for a sufficiently large not depending on ,

| (3.29) |

Then, after at most iterations, the TIPUP-iTOPUP estimator satisfies

Moreover, the above error bound holds after at most iterations, if any one of the following three conditions holds in addition to condition (3.29), (i) () are of the same order, (ii) () are of the same order, (iii) () are of the same order.

3.5 Comparisons

3.5.1 Comparison between the non-iterative procedures and iterative procedures

Theorems 3.1 and 3.2 show that the convergence rates of the non-iterative estimators TOPUP and TIPUP can be improved by their iterative counterparts. Particularly, when the dimensions for the factor process are fixed and the respective signal strength conditions are fulfilled, the proposed iTOPUP and iTIPUP just need one-iteration to achieve the much sharper ideal rate in (3.8) and in (3.15), compared with the rate (3.7) of TOPUP and (3.14) of TIPUP derived in Chen, Yang and Zhang (2021), respectively. The improvement is achieved through replacing the much larger by , via orthogonal projection. When the factors are strong with and the factor dimensions are fixed, the non-iterative TOPUP-based estimators of Lam, Yao and Bathia (2011) for the vector factor model, Wang, Liu and Chen (2019) for the matrix factor and Chen, Yang and Zhang (2021) for tensor factor models all have the same convergence rate for estimating the loading space. In comparison, the convergence rate of both iterative estimators, iTOPUP and iTIPUP (when there is no severe signal cancellation, with bounded ), is much sharper. Intuitively, when the signal is strong, the orthogonal projection operation helps to consolidate signals while potentially averaging out the noises, when the projection reduces the dimension of the mode- unfolded matrix from for the tensor to for the projected tensor , resulting in the improvement by a factor of in the convergence rate.

3.5.2 Comparison between iTIPUP and iTOPUP

The inner product operation in (2.7) for TIPUP-related procedures enjoys significant amount of noise cancellation comparing to the outer product operation in (2.4) for TOPUP-related procedures. Compared with iTOPUP, the benefit of noise cancellation of the iTIPUP procedure is still visible through the reduction of in (3.8) to in (3.15) in the ideal rates. However, this post-iteration benefit is much less pronounced compared with the reduction of in (3.7) for TOPUP to in (3.14) for TIPUP in the non-iterative rates. Meanwhile, the potential for signal cancellation in the TIPUP related schemes persists as and are unchanged between the initial and ideal rates. We note that the signal strength can be viewed as and in Theorems 3.1 and 3.2 respectively for TOPUP/iTOPUP and TIPUP/iTIPUP, and that severe signal cancellation can be expressed as . When are allowed to diverge to infinity, the impact of signal cancellation is expressed in terms of in Assumption 3: The iTOPUP has a faster rate than the iTIPUP when and slower rate when , in view of Corollary 3.3 and 3.4. In Corollaries 3.1 and 3.2, iTOPUP and iTIPUP have the same convergence rate because Corollary 3.2 assumes that signal cancellation does not change convergence rate.

Our results seem to suggest that the mixed TIPUP-iTOPUP procedure would strike a good balance between the benefit of noise cancellation (e.g. smaller for consistency) and the potential danger of signal cancellation (e.g. ) for the following four reasons: (1) The benefit of noise cancellation is much larger in the initialization, in term of , in view of the rates in (3.7) and in (3.14). (2) The first part of condition (3.20) for TIPUP-iTOPUP is weaker than the first part of condition (3.17) for TIPUP-iTIPUP. (3) The signal strength of the stronger TOPUP form is retained in the rate after iTOPUP iteration. (4) As we will prove in Section 3.6, the sample size requirement for the TIPUP initialization is optimal in the sense that it matches a computational lower bound under suitable conditions. Our simulation results support this recommendation, especially for relatively small . Of course if the sample size qualitatively justifies the condition in (3.10) and/or if a possible signal cancellation is a significant concern, the TOPUP initiation should be used.

3.5.3 Comparison with HOOI

The signal to noise ratio (SNR) condition, or equivalently the sample size requirement, is mainly used to ensure that the initial estimator has sufficiently small estimation error. Thus, the performance of iterative procedures is measured by both the SNR requirement and the error rate achieved. Consider fixed in the fixed rank case with and . In the fixed signal model where is fixed and deterministic in (1.1), applying HOOI to the average of would require SNR to achieve the loss of the order according to Zhang and Xia (2018), where is viewed as the noise level for HOOI as it is the standard deviation of each element of the average tensor. In terms of the auto-crossproducts, taking the average over roughly amounts to taking the average of all lagged products between and , . However, in the tensor factor model (1.1) where the signal part is random and serial correlated, the average is taken only over lagged products for each . Thus, while the rate of the average of the signal-by-noise crossproducts in the factor model is heuristically expected to match that of HOOI at noise level , the rate of the average of the noise-by-noise crossproducts in the factor model is expected to only match that of HOOI with noise level . In Corollary 3.2, the contribution of the noise-by-noise crossproducts dominates the initial estimation error as the SNR requirement in (3.23) matches that of HOOI with noise level ; at the same time the contribution of the signal-by-noise crossproducts dominates the estimation error after iteration as the rate in (3.24) matches that of HOOI with noise level . Thus, if there is no severe signal cancellation, the signal to noise ratio requirement and convergence rate for iTIPUP and TIPIP-iTOPUP in the factor model are both comparable with those of HOOI in the simpler fixed signal setting, but the rate match is achieved in very different and subtle ways. We prove that this insight is intrinsic as the rates in (3.23) and (3.24) are both optimal according to the computational and statistical lower bounds in the following subsection.

3.6 Computational and statistical lower bounds

In this subsection, we focus on the typical factor model setting that the condition numbers of are bounded and ranks are fixed. We shall prove that under the computational hardness assumption, the signal to noise ratio condition (3.23) imposed on iTIPUP (also TIPUP-iTOPUP) in Corollary 3.2 is unavoidable for computationally feasible estimators to be consistent. To be specific, we show that, if the signal to noise ratio condition is violated, then any computationally efficient and consistent estimator of the loading spaces leads to a computationally efficient and statistically consistent test for the Hypergraphic Planted Clique Detection problem in a regime where it is believed to be computationally intractable. In addition, we establish a statistical lower bound on the minimax risk of the estimators.

Hypergraphic Planted Clique. An -hypergraph is a natural extension of regular graph, where and each hyper-edge is represented by an unordered group of different vertices (), denoted as . Given a -hypergraph its adjacency tensor is defined as

We denote by the Erdős–Rényi -hypergraph on vertices where each hyper-edge is drawn independently with probability , by a random clique of size where the members are uniformly sampled from and is composed of all with , and by the random graph generated by first sampling independently and and then adding all the edges in to the set of edges in . The Hypergraphic Planted Clique (HPC) detection problem of parameter refers to testing the following hypotheses:

| (3.30) |

If , the above HPC detection becomes the traditional planted clique (PC) detection problem. When , many computationally efficient algorithms have been developed for PC detection; see, Alon, Krivelevich and Sudakov (1998), Feige and Krauthgamer (2000), Feige and Ron (2010), Ames and Vavasis (2011), Dekel, Gurel-Gurevich and Peres (2014), Deshpande and Montanari (2015), Feldman et al. (2017), among others. However, it has been widely conjectured that when , the PC detection problem cannot be solved in randomized polynomial time, which is referred to as the hardness conjecture. Computational lower bounds in several statistical problems have been established by assuming the hardness conjecture of PC detection, including sparse PCA (Berthet and Rigollet, 2013a, b, Wang, Berthet and Samworth, 2016), sparse CCA (Gao, Ma and Zhou, 2017), submatrix detection (Ma and Wu, 2015, Cai, Liang and Rakhlin, 2017), community detection (Hajek, Wu and Xu, 2015), etc.

Recently, motivated by tensor data analysis, hardness conjecture for HPC detection problem has been proposed; see, for example, Zhang and Xia (2018), Brennan and Bresler (2020), Luo and Zhang (2022, 2020), Pananjady and Samworth (2022). Similar to the PC detection, they hypothesized that when with , the HPC detection problem (3.30) cannot be solved by any randomized polynomial-time algorithm. Formally, the conjectured hardness of the HPC detection problem can be stated as follows.

Hypothesis I (HPC detection).

Consider the HPC detection problem (3.30) and suppose is a fixed integer. If

| (3.31) |

for any sequence of polynomial-time tests ,

Evidence supporting this hypothesis has been provided in Zhang and Xia (2018), Luo and Zhang (2022). This version of the hypothesis is similar to the one in Berthet and Rigollet (2013a), Ma and Wu (2015), Gao, Ma and Zhou (2017) for the PC detection problem.

For simplicity, we especially consider the one-factor model (1.2) with being a mean 0 univariate series,

| (3.32) |

where , for , and . The probability space we consider in this subsection is

| (3.33) | ||||

The computational lower bound over is then presented as below.

Theorem 3.4.

Suppose that Hypothesis I holds for some and for all . If, for some ,

| (3.34) |

then for any randomized polynomial-time estimators , ,

| (3.35) |

where and .

Comparing (3.34) with (3.23), we see that the signal to noise ratio condition (3.23) cannot be improved upon by a factor of with polynomial time complexity for any .

Remark 3.9.

Theorem 3.4 illustrates the computational hardness for factor loading spaces estimation under the typical factor model setting that the condition numbers of are bounded and ranks are fixed, and suggests the use of TIPUP initialization with proper fixed as it attains the computational lower bound under the typical factor model setting.

Next, we establish the statistical lower bound for the tensor factor model problem. Again, we consider the probability space (3.33).

Theorem 3.5.

Suppose and as for all . Then there exists a universal constant such that for sufficiently large,

| (3.36) |

for all , where and .

4 Summary

In this paper we propose new estimation procedures for tensor factor model via iterative projection, and focus on two procedures: iTOPUP and iTIPUP. Theoretical analysis shows the asymptotic properties of the estimators. Simulation study presented in the supplementary material illustrates the finite sample properties of the estimators. While theoretical results are obtained under very general conditions, concrete specific cases are considered. In particular, under the typical factor model setting where the condition numbers of are bounded and the ranks are fixed, the proposed iterative procedures, iTOPUP method and iTIPUP method (with no severe signal cancellation) lead to a convergence rate under strong factors settings due to information pooling of the orthogonal projection of the other dimensions. This rate is much sharper than the existing rate in the recent literature for non-iterative estimators for vector, matrix and tensor factor models. It implies that the accuracy can be improved by increasing the dimensions, and consistent estimation of the loading spaces can be achieved even with a fixed finite sample size . This is in sharp contrast to the folklore based on the existing literature that only the sample size helps the estimation of the loading matrices in factor models. The proposed iterative estimation methods not only preserve the tensor structure, but also result in sharper convergence rate in the estimation of factor loading space.

The iterative procedure requires two operators, one for initialization and one for iteration. Under certain conditions of the signal to noise ratio (or the sample size requirement), we only need the initial estimator to have sufficiently small estimation errors but not the consistency of the initial estimator. Often, one iteration is sufficient. In more complicated general cases, at most iterations are needed to achieve the ideal rate of convergence. Based on the theoretical results and empirical evidence, we suggest to use iTOPUP for iteration when the ranks are small. In terms of initiation, the computational lower bound shows that the signal to noise ratio condition derived from TIPUP initialization is unavoidable for any computationally feasible estimation procedure to achieve consistency, while that from TOPUP initialization is not optimal. Based on this result, we suggest the use of TIPUP initialization. Of course, this should be done with precaution against potential signal cancellation, for example by using a slightly large as our empirical results show. By examination of the patterns of estimated singular values under different lag values , using iTOPUP and iTIPUP, it is possible to detect signal cancellation, which has significant impact on iTIPUP estimators.

The proposed iterative procedure is similar to HOOI algorithms in spirit, but the detailed operations and the theoretical challenges are significantly different.

Acknowledgements

We would like to thank the Editor, the Associate Editor and the anonymous referees for their detailed reviews, which helped to improve the paper substantially.

Yuefeng Han’s research is supported in part by National Science Foundation grant IIS-1741390. Rong Chen’s research is supported in part by National Science Foundation grants DMS-1737857, IIS-1741390, CCF-1934924 and DMS-2027855. Dan Yang’s research is supported in part by NSF grant IIS-1741390, Hong Kong grant GRF 17301620 and Hong Kong grant CRF C7162-20GF. Cun-Hui Zhang’s research is supported in part by NSF grants DMS-1721495, IIS-1741390 and CCF-1934924.

References

- Ahn and Horenstein (2013) {barticle}[author] \bauthor\bsnmAhn, \bfnmSeung C\binitsS. C. and \bauthor\bsnmHorenstein, \bfnmAlex R\binitsA. R. (\byear2013). \btitleEigenvalue ratio test for the number of factors. \bjournalEconometrica \bvolume81 \bpages1203–1227. \endbibitem

- Alon, Krivelevich and Sudakov (1998) {barticle}[author] \bauthor\bsnmAlon, \bfnmNoga\binitsN., \bauthor\bsnmKrivelevich, \bfnmMichael\binitsM. and \bauthor\bsnmSudakov, \bfnmBenny\binitsB. (\byear1998). \btitleFinding a large hidden clique in a random graph. \bjournalRandom Structures & Algorithms \bvolume13 \bpages457–466. \endbibitem

- Alter and Golub (2005) {barticle}[author] \bauthor\bsnmAlter, \bfnmOrly\binitsO. and \bauthor\bsnmGolub, \bfnmGene H\binitsG. H. (\byear2005). \btitleReconstructing the pathways of a cellular system from genome-scale signals by using matrix and tensor computations. \bjournalProceedings of the National Academy of Sciences \bvolume102 \bpages17559–17564. \endbibitem

- Ames and Vavasis (2011) {barticle}[author] \bauthor\bsnmAmes, \bfnmBrendan PW\binitsB. P. and \bauthor\bsnmVavasis, \bfnmStephen A\binitsS. A. (\byear2011). \btitleNuclear norm minimization for the planted clique and biclique problems. \bjournalMathematical Programming \bvolume129 \bpages69–89. \endbibitem

- Anandkumar et al. (2014) {barticle}[author] \bauthor\bsnmAnandkumar, \bfnmAnimashree\binitsA., \bauthor\bsnmGe, \bfnmRong\binitsR., \bauthor\bsnmHsu, \bfnmDaniel\binitsD. and \bauthor\bsnmKakade, \bfnmSham M\binitsS. M. (\byear2014). \btitleA tensor approach to learning mixed membership community models. \bjournalThe Journal of Machine Learning Research \bvolume15 \bpages2239–2312. \endbibitem

- Bai (2003) {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. (\byear2003). \btitleInferential theory for factor models of large dimensions. \bjournalEconometrica \bvolume71 \bpages135–171. \endbibitem

- Bai and Ng (2002) {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. and \bauthor\bsnmNg, \bfnmSerena\binitsS. (\byear2002). \btitleDetermining the number of factors in approximate factor models. \bjournalEconometrica \bvolume70 \bpages191–221. \endbibitem

- Bai and Ng (2007) {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. and \bauthor\bsnmNg, \bfnmSerena\binitsS. (\byear2007). \btitleDetermining the number of primitive shocks in factor models. \bjournalJournal of Business & Economic Statistics \bvolume25 \bpages52–60. \endbibitem

- Berthet and Rigollet (2013a) {binproceedings}[author] \bauthor\bsnmBerthet, \bfnmQuentin\binitsQ. and \bauthor\bsnmRigollet, \bfnmPhilippe\binitsP. (\byear2013a). \btitleComplexity theoretic lower bounds for sparse principal component detection. In \bbooktitleConference on Learning Theory \bpages1046–1066. \bpublisherPMLR. \endbibitem

- Berthet and Rigollet (2013b) {barticle}[author] \bauthor\bsnmBerthet, \bfnmQuentin\binitsQ. and \bauthor\bsnmRigollet, \bfnmPhilippe\binitsP. (\byear2013b). \btitleOptimal detection of sparse principal components in high dimension. \bjournalThe Annals of Statistics \bvolume41 \bpages1780–1815. \endbibitem

- Bi, Qu and Shen (2018) {barticle}[author] \bauthor\bsnmBi, \bfnmXuan\binitsX., \bauthor\bsnmQu, \bfnmAnnie\binitsA. and \bauthor\bsnmShen, \bfnmXiaotong\binitsX. (\byear2018). \btitleMultilayer tensor factorization with applications to recommender systems. \bjournalThe Annals of Statistics \bvolume46 \bpages3308–3333. \endbibitem

- Birnbaum et al. (2013) {barticle}[author] \bauthor\bsnmBirnbaum, \bfnmAharon\binitsA., \bauthor\bsnmJohnstone, \bfnmIain M\binitsI. M., \bauthor\bsnmNadler, \bfnmBoaz\binitsB. and \bauthor\bsnmPaul, \bfnmDebashis\binitsD. (\byear2013). \btitleMinimax bounds for sparse PCA with noisy high-dimensional data. \bjournalThe Annals of Statistics \bvolume41 \bpages1055. \endbibitem

- Brennan and Bresler (2020) {binproceedings}[author] \bauthor\bsnmBrennan, \bfnmMatthew\binitsM. and \bauthor\bsnmBresler, \bfnmGuy\binitsG. (\byear2020). \btitleReducibility and statistical-computational gaps from secret leakage. In \bbooktitleConference on Learning Theory \bpages648–847. \bpublisherPMLR. \endbibitem

- Cai, Liang and Rakhlin (2017) {barticle}[author] \bauthor\bsnmCai, \bfnmT Tony\binitsT. T., \bauthor\bsnmLiang, \bfnmTengyuan\binitsT. and \bauthor\bsnmRakhlin, \bfnmAlexander\binitsA. (\byear2017). \btitleComputational and statistical boundaries for submatrix localization in a large noisy matrix. \bjournalThe Annals of Statistics \bvolume45 \bpages1403–1430. \endbibitem

- Chamberlain and Rothschild (1983) {barticle}[author] \bauthor\bsnmChamberlain, \bfnmGary\binitsG. and \bauthor\bsnmRothschild, \bfnmMichael\binitsM. (\byear1983). \btitleArbitrage, factor structure, and mean-variance analysis on large asset markets. \bjournalEconometrica \bvolume51 \bpages1281–1304. \endbibitem

- Chen and Chen (2019) {barticle}[author] \bauthor\bsnmChen, \bfnmElynn Y\binitsE. Y. and \bauthor\bsnmChen, \bfnmRong\binitsR. (\byear2019). \btitleModeling dynamic transport network with matrix factor models: with an application to international trade flow. \bjournalarXiv preprint arXiv:1901.00769. \endbibitem

- Chen and Fan (2021) {barticle}[author] \bauthor\bsnmChen, \bfnmElynn Y\binitsE. Y. and \bauthor\bsnmFan, \bfnmJianqing\binitsJ. (\byear2021). \btitleStatistical inference for high-dimensional matrix-variate factor models. \bjournalJournal of the American Statistical Association \bpages1–18. \endbibitem

- Chen, Tsay and Chen (2020) {barticle}[author] \bauthor\bsnmChen, \bfnmElynn Y\binitsE. Y., \bauthor\bsnmTsay, \bfnmRuey S\binitsR. S. and \bauthor\bsnmChen, \bfnmRong\binitsR. (\byear2020). \btitleConstrained Factor Models for High-Dimensional Matrix-Variate Time Series. \bjournalJournal of the American Statistical Association \bvolume115 \bpages775-793. \endbibitem

- Chen, Yang and Zhang (2021) {barticle}[author] \bauthor\bsnmChen, \bfnmRong\binitsR., \bauthor\bsnmYang, \bfnmDan\binitsD. and \bauthor\bsnmZhang, \bfnmCun-Hui\binitsC.-H. (\byear2021). \btitleFactor models for high-dimensional tensor time series. \bjournalJournal of the American Statistical Association \bpages1–23. \endbibitem

- Chen et al. (2020) {barticle}[author] \bauthor\bsnmChen, \bfnmElynn Y\binitsE. Y., \bauthor\bsnmXia, \bfnmDong\binitsD., \bauthor\bsnmCai, \bfnmChencheng\binitsC. and \bauthor\bsnmFan, \bfnmJianqing\binitsJ. (\byear2020). \btitleSemiparametric tensor factor analysis by iteratively projected SVD. \bjournalarXiv preprint arXiv:2007.02404. \endbibitem

- De Lathauwer, De Moor and Vandewalle (2000) {barticle}[author] \bauthor\bsnmDe Lathauwer, \bfnmLieven\binitsL., \bauthor\bsnmDe Moor, \bfnmBart\binitsB. and \bauthor\bsnmVandewalle, \bfnmJoos\binitsJ. (\byear2000). \btitleOn the best rank-1 and rank-(, , …, ) approximation of higher-order tensors. \bjournalSIAM Journal on Matrix Analysis and Applications \bvolume21 \bpages1324–1342. \endbibitem

- Dekel, Gurel-Gurevich and Peres (2014) {barticle}[author] \bauthor\bsnmDekel, \bfnmYael\binitsY., \bauthor\bsnmGurel-Gurevich, \bfnmOri\binitsO. and \bauthor\bsnmPeres, \bfnmYuval\binitsY. (\byear2014). \btitleFinding hidden cliques in linear time with high probability. \bjournalCombinatorics, Probability and Computing \bvolume23 \bpages29–49. \endbibitem

- Deshpande and Montanari (2015) {barticle}[author] \bauthor\bsnmDeshpande, \bfnmYash\binitsY. and \bauthor\bsnmMontanari, \bfnmAndrea\binitsA. (\byear2015). \btitleFinding hidden cliques of size in nearly linear time. \bjournalFoundations of Computational Mathematics \bvolume15 \bpages1069–1128. \endbibitem

- Diaconis and Freedman (1980) {barticle}[author] \bauthor\bsnmDiaconis, \bfnmPersi\binitsP. and \bauthor\bsnmFreedman, \bfnmDavid\binitsD. (\byear1980). \btitleFinite exchangeable sequences. \bjournalThe Annals of Probability \bpages745–764. \endbibitem

- Fan, Liao and Mincheva (2011) {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ., \bauthor\bsnmLiao, \bfnmYuan\binitsY. and \bauthor\bsnmMincheva, \bfnmMartina\binitsM. (\byear2011). \btitleHigh dimensional covariance matrix estimation in approximate factor models. \bjournalThe Annals of Statistics \bvolume39 \bpages3320. \endbibitem

- Fan, Liao and Mincheva (2013) {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ., \bauthor\bsnmLiao, \bfnmYuan\binitsY. and \bauthor\bsnmMincheva, \bfnmMartina\binitsM. (\byear2013). \btitleLarge covariance estimation by thresholding principal orthogonal complements. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume75 \bpages603–680. \endbibitem

- Fan, Liao and Wang (2016) {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ., \bauthor\bsnmLiao, \bfnmYuan\binitsY. and \bauthor\bsnmWang, \bfnmWeichen\binitsW. (\byear2016). \btitleProjected principal component analysis in factor models. \bjournalThe Annals of Statistics \bvolume44 \bpages219–254. \endbibitem

- Fan, Liu and Wang (2018) {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ., \bauthor\bsnmLiu, \bfnmHan\binitsH. and \bauthor\bsnmWang, \bfnmWeichen\binitsW. (\byear2018). \btitleLarge covariance estimation through elliptical factor models. \bjournalThe Annals of Statistics \bvolume46 \bpages1383. \endbibitem

- Feige and Krauthgamer (2000) {barticle}[author] \bauthor\bsnmFeige, \bfnmUriel\binitsU. and \bauthor\bsnmKrauthgamer, \bfnmRobert\binitsR. (\byear2000). \btitleFinding and certifying a large hidden clique in a semirandom graph. \bjournalRandom Structures & Algorithms \bvolume16 \bpages195–208. \endbibitem

- Feige and Ron (2010) {binproceedings}[author] \bauthor\bsnmFeige, \bfnmUriel\binitsU. and \bauthor\bsnmRon, \bfnmDorit\binitsD. (\byear2010). \btitleFinding hidden cliques in linear time. In \bbooktitleDiscrete Mathematics and Theoretical Computer Science \bpages189–204. \bpublisherDiscrete Mathematics and Theoretical Computer Science. \endbibitem

- Feldman et al. (2017) {barticle}[author] \bauthor\bsnmFeldman, \bfnmVitaly\binitsV., \bauthor\bsnmGrigorescu, \bfnmElena\binitsE., \bauthor\bsnmReyzin, \bfnmLev\binitsL., \bauthor\bsnmVempala, \bfnmSantosh S\binitsS. S. and \bauthor\bsnmXiao, \bfnmYing\binitsY. (\byear2017). \btitleStatistical algorithms and a lower bound for detecting planted cliques. \bjournalJournal of the ACM (JACM) \bvolume64 \bpages1–37. \endbibitem

- Forni et al. (2000) {barticle}[author] \bauthor\bsnmForni, \bfnmMario\binitsM., \bauthor\bsnmHallin, \bfnmMarc\binitsM., \bauthor\bsnmLippi, \bfnmMarco\binitsM. and \bauthor\bsnmReichlin, \bfnmLucrezia\binitsL. (\byear2000). \btitleThe generalized dynamic-factor model: identification and estimation. \bjournalThe Review of Economics and Statistics \bvolume82 \bpages540–554. \endbibitem

- Foster (1996) {barticle}[author] \bauthor\bsnmFoster, \bfnmGrant\binitsG. (\byear1996). \btitleTime series analysis by projection. II. Tensor methods for time series analysis. \bjournalThe Astronomical Journal \bvolume111 \bpages555. \endbibitem

- Gao, Ma and Zhou (2017) {barticle}[author] \bauthor\bsnmGao, \bfnmChao\binitsC., \bauthor\bsnmMa, \bfnmZongming\binitsZ. and \bauthor\bsnmZhou, \bfnmHarrison H\binitsH. H. (\byear2017). \btitleSparse CCA: Adaptive estimation and computational barriers. \bjournalThe Annals of Statistics \bvolume45 \bpages2074–2101. \endbibitem

- Hajek, Wu and Xu (2015) {binproceedings}[author] \bauthor\bsnmHajek, \bfnmBruce\binitsB., \bauthor\bsnmWu, \bfnmYihong\binitsY. and \bauthor\bsnmXu, \bfnmJiaming\binitsJ. (\byear2015). \btitleComputational lower bounds for community detection on random graphs. In \bbooktitleConference on Learning Theory \bpages899–928. \bpublisherPMLR. \endbibitem

- Hallin and Liška (2007) {barticle}[author] \bauthor\bsnmHallin, \bfnmMarc\binitsM. and \bauthor\bsnmLiška, \bfnmRoman\binitsR. (\byear2007). \btitleDetermining the number of factors in the general dynamic factor model. \bjournalJournal of the American Statistical Association \bvolume102 \bpages603–617. \endbibitem

- Lam, Yao and Bathia (2011) {barticle}[author] \bauthor\bsnmLam, \bfnmClifford\binitsC., \bauthor\bsnmYao, \bfnmQiwei\binitsQ. and \bauthor\bsnmBathia, \bfnmNeil\binitsN. (\byear2011). \btitleEstimation of latent factors for high-dimensional time series. \bjournalBiometrika \bvolume98 \bpages901–918. \endbibitem

- Lam and Yao (2012) {barticle}[author] \bauthor\bsnmLam, \bfnmClifford\binitsC. and \bauthor\bsnmYao, \bfnmQiwei\binitsQ. (\byear2012). \btitleFactor modeling for high-dimensional time series: inference for the number of factors. \bjournalThe Annals of Statistics \bvolume40 \bpages694–726. \endbibitem

- Liu et al. (2012) {barticle}[author] \bauthor\bsnmLiu, \bfnmJi\binitsJ., \bauthor\bsnmMusialski, \bfnmPrzemyslaw\binitsP., \bauthor\bsnmWonka, \bfnmPeter\binitsP. and \bauthor\bsnmYe, \bfnmJieping\binitsJ. (\byear2012). \btitleTensor completion for estimating missing values in visual data. \bjournalIEEE Transactions on Pattern Analysis and Machine Intelligence \bvolume35 \bpages208–220. \endbibitem

- Liu et al. (2014) {binproceedings}[author] \bauthor\bsnmLiu, \bfnmYuanyuan\binitsY., \bauthor\bsnmShang, \bfnmFanhua\binitsF., \bauthor\bsnmFan, \bfnmWei\binitsW., \bauthor\bsnmCheng, \bfnmJames\binitsJ. and \bauthor\bsnmCheng, \bfnmHong\binitsH. (\byear2014). \btitleGeneralized higher-order orthogonal iteration for tensor decomposition and completion. In \bbooktitleAdvances in Neural Information Processing Systems \bpages1763–1771. \endbibitem

- Luo and Zhang (2020) {binproceedings}[author] \bauthor\bsnmLuo, \bfnmYuetian\binitsY. and \bauthor\bsnmZhang, \bfnmAnru R\binitsA. R. (\byear2020). \btitleOpen problem: Average-case hardness of hypergraphic planted clique detection. In \bbooktitleConference on Learning Theory \bpages3852–3856. \bpublisherPMLR. \endbibitem

- Luo and Zhang (2022) {barticle}[author] \bauthor\bsnmLuo, \bfnmYuetian\binitsY. and \bauthor\bsnmZhang, \bfnmAnru R\binitsA. R. (\byear2022). \btitleTensor clustering with planted structures: Statistical optimality and computational limits. \bjournalThe Annals of Statistics \bvolume50 \bpages584–613. \endbibitem

- Ma and Wu (2015) {barticle}[author] \bauthor\bsnmMa, \bfnmZongming\binitsZ. and \bauthor\bsnmWu, \bfnmYihong\binitsY. (\byear2015). \btitleComputational barriers in minimax submatrix detection. \bjournalThe Annals of Statistics \bvolume43 \bpages1089–1116. \endbibitem

- Omberg, Golub and Alter (2007) {barticle}[author] \bauthor\bsnmOmberg, \bfnmLarsson\binitsL., \bauthor\bsnmGolub, \bfnmGene H\binitsG. H. and \bauthor\bsnmAlter, \bfnmOrly\binitsO. (\byear2007). \btitleA tensor higher-order singular value decomposition for integrative analysis of DNA microarray data from different studies. \bjournalProceedings of the National Academy of Sciences \bvolume104 \bpages18371–18376. \endbibitem

- Pan and Yao (2008) {barticle}[author] \bauthor\bsnmPan, \bfnmJiazhu\binitsJ. and \bauthor\bsnmYao, \bfnmQiwei\binitsQ. (\byear2008). \btitleModelling multiple time series via common factors. \bjournalBiometrika \bvolume95 \bpages365–379. \endbibitem

- Pananjady and Samworth (2022) {barticle}[author] \bauthor\bsnmPananjady, \bfnmAshwin\binitsA. and \bauthor\bsnmSamworth, \bfnmRichard J\binitsR. J. (\byear2022). \btitleIsotonic regression with unknown permutations: Statistics, computation and adaptation. \bjournalThe Annals of Statistics \bvolume50 \bpages324–350. \endbibitem

- Pena and Box (1987) {barticle}[author] \bauthor\bsnmPena, \bfnmDaniel\binitsD. and \bauthor\bsnmBox, \bfnmGeorge EP\binitsG. E. (\byear1987). \btitleIdentifying a simplifying structure in time series. \bjournalJournal of the American Statistical Association \bvolume82 \bpages836–843. \endbibitem

- Rogers, Li and Russell (2013) {barticle}[author] \bauthor\bsnmRogers, \bfnmMark\binitsM., \bauthor\bsnmLi, \bfnmLei\binitsL. and \bauthor\bsnmRussell, \bfnmStuart J\binitsS. J. (\byear2013). \btitleMultilinear dynamical systems for tensor time series. \bjournalAdvances in Neural Information Processing Systems \bvolume26 \bpages2634–2642. \endbibitem

- Sheehan and Saad (2007) {binproceedings}[author] \bauthor\bsnmSheehan, \bfnmBernard N\binitsB. N. and \bauthor\bsnmSaad, \bfnmYousef\binitsY. (\byear2007). \btitleHigher order orthogonal iteration of tensors (HOOI) and its relation to PCA and GLRAM. In \bbooktitleProceedings of the 2007 SIAM International Conference on Data Mining \bpages355–365. \bpublisherSIAM. \endbibitem

- Stock and Watson (2002) {barticle}[author] \bauthor\bsnmStock, \bfnmJames H.\binitsJ. H. and \bauthor\bsnmWatson, \bfnmMark W.\binitsM. W. (\byear2002). \btitleForecasting using principal components from a large number of predictors. \bjournalJournal of the American Statistical Association \bvolume97 \bpages1167–1179. \endbibitem

- Sun and Li (2017) {barticle}[author] \bauthor\bsnmSun, \bfnmWill Wei\binitsW. W. and \bauthor\bsnmLi, \bfnmLexin\binitsL. (\byear2017). \btitleSTORE: sparse tensor response regression and neuroimaging analysis. \bjournalThe Journal of Machine Learning Research \bvolume18 \bpages4908–4944. \endbibitem

- Tucker (1966) {barticle}[author] \bauthor\bsnmTucker, \bfnmLedyard R\binitsL. R. (\byear1966). \btitleSome mathematical notes on three-mode factor analysis. \bjournalPsychometrika \bvolume31 \bpages279–311. \endbibitem

- Wang, Berthet and Samworth (2016) {barticle}[author] \bauthor\bsnmWang, \bfnmTengyao\binitsT., \bauthor\bsnmBerthet, \bfnmQuentin\binitsQ. and \bauthor\bsnmSamworth, \bfnmRichard J\binitsR. J. (\byear2016). \btitleStatistical and computational trade-offs in estimation of sparse principal components. \bjournalThe Annals of Statistics \bvolume44 \bpages1896–1930. \endbibitem

- Wang, Liu and Chen (2019) {barticle}[author] \bauthor\bsnmWang, \bfnmDong\binitsD., \bauthor\bsnmLiu, \bfnmXialu\binitsX. and \bauthor\bsnmChen, \bfnmRong\binitsR. (\byear2019). \btitleFactor models for matrix-valued high-dimensional time series. \bjournalJournal of Econometrics \bvolume208 \bpages231–248. \endbibitem

- Wang, Zheng and Li (2021) {barticle}[author] \bauthor\bsnmWang, \bfnmDi\binitsD., \bauthor\bsnmZheng, \bfnmYao\binitsY. and \bauthor\bsnmLi, \bfnmGuodong\binitsG. (\byear2021). \btitleHigh-dimensional low-rank tensor autoregressive time series modeling. \bjournalarXiv preprint arXiv:2101.04276. \endbibitem

- Wedin (1972) {barticle}[author] \bauthor\bsnmWedin, \bfnmPer-Åke\binitsP.-Å. (\byear1972). \btitlePerturbation bounds in connection with singular value decomposition. \bjournalBIT Numerical Mathematics \bvolume12 \bpages99–111. \endbibitem

- Zhang and Xia (2018) {barticle}[author] \bauthor\bsnmZhang, \bfnmAnru\binitsA. and \bauthor\bsnmXia, \bfnmDong\binitsD. (\byear2018). \btitleTensor SVD: Statistical and computational limits. \bjournalIEEE Transactions on Information Theory \bvolume64 \bpages7311–7338. \endbibitem

- Zhou, Li and Zhu (2013) {barticle}[author] \bauthor\bsnmZhou, \bfnmHua\binitsH., \bauthor\bsnmLi, \bfnmLexin\binitsL. and \bauthor\bsnmZhu, \bfnmHongtu\binitsH. (\byear2013). \btitleTensor regression with applications in neuroimaging data analysis. \bjournalJournal of the American Statistical Association \bvolume108 \bpages540–552. \endbibitem

, , , and

In this supplementary material, we shall provide simulation studies, the proofs of main results in the paper and some lemmas that are useful in proofs of the paper.

The readers are referred to Appendix A for simulation studies. The proofs of Theorems 3.2, 3.1, 3.4 and 3.5 are presented in Appendix B, C, D and E, respectively. Appendix F includes the proofs of corollaries. All technical lemmas are relegated to Appendix G.

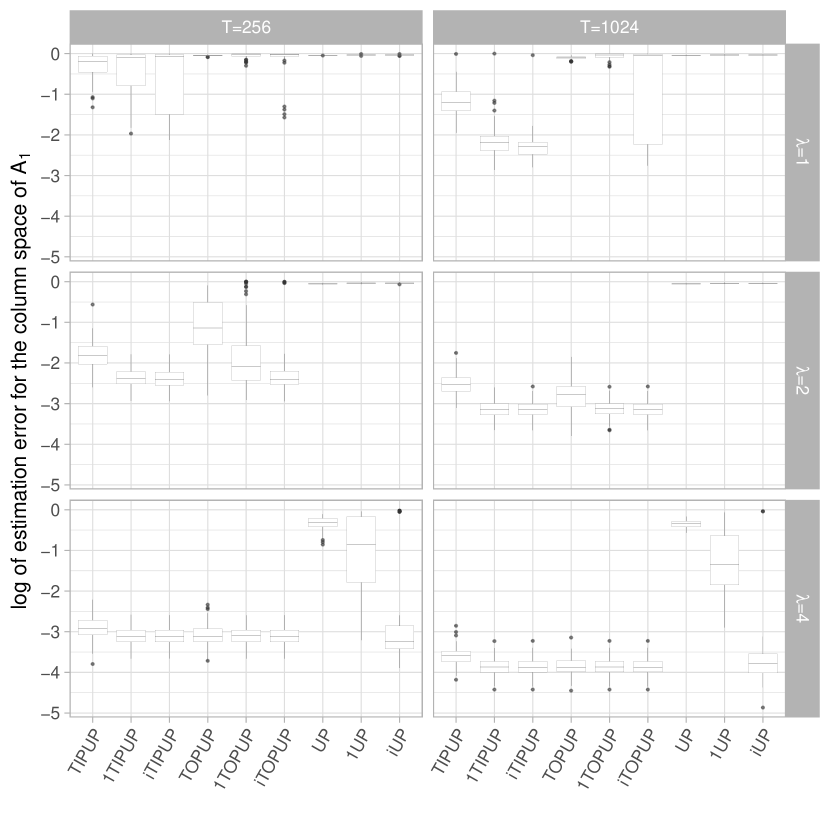

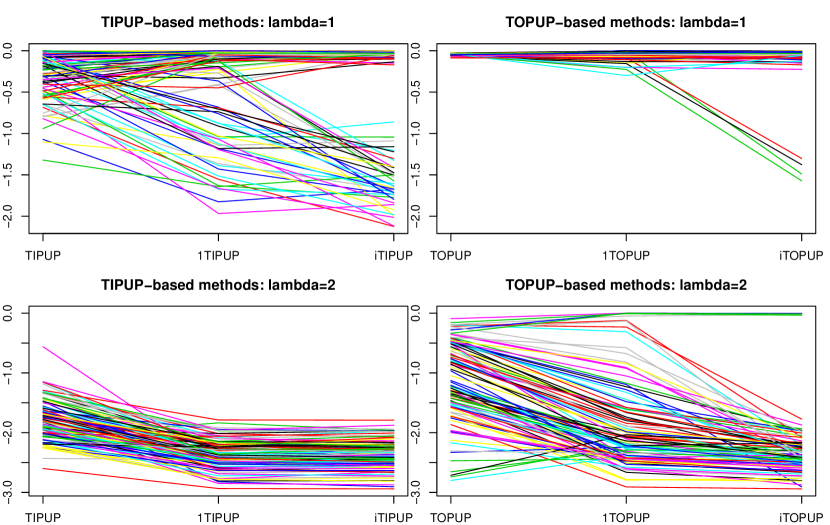

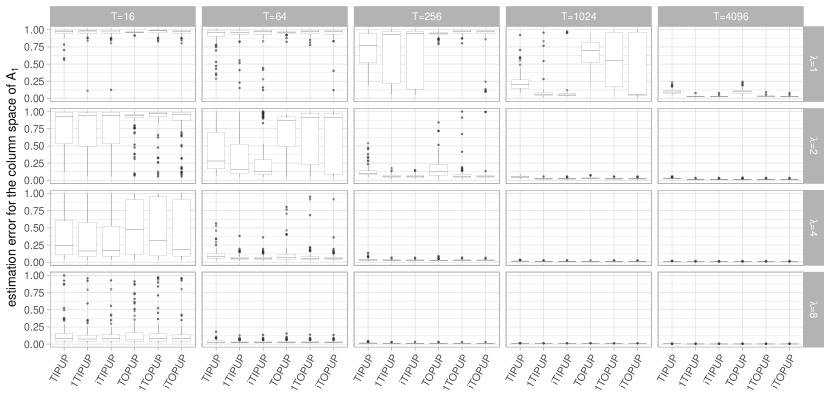

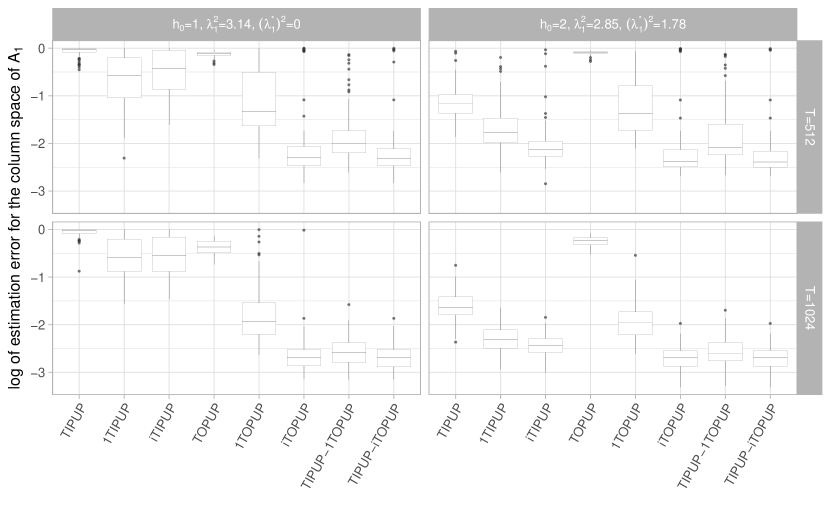

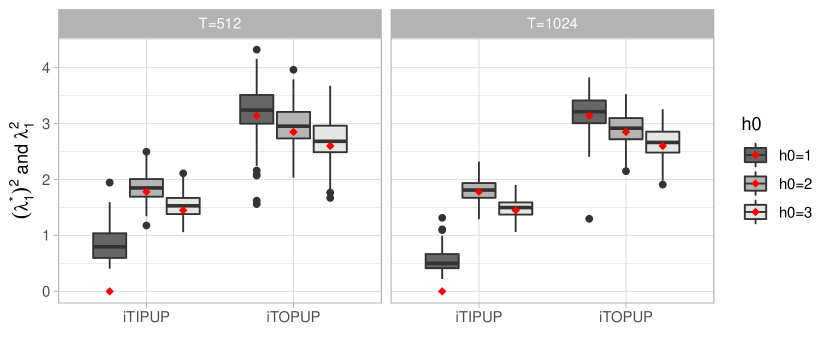

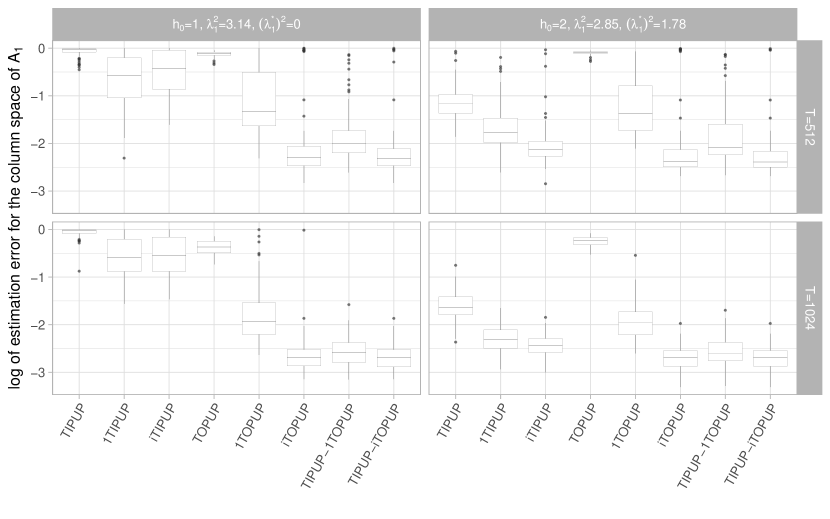

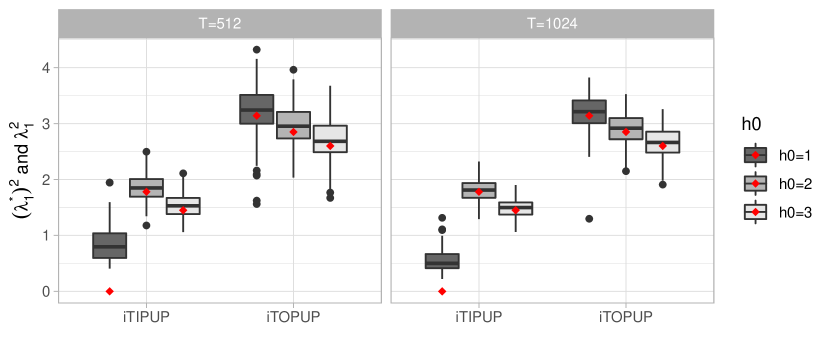

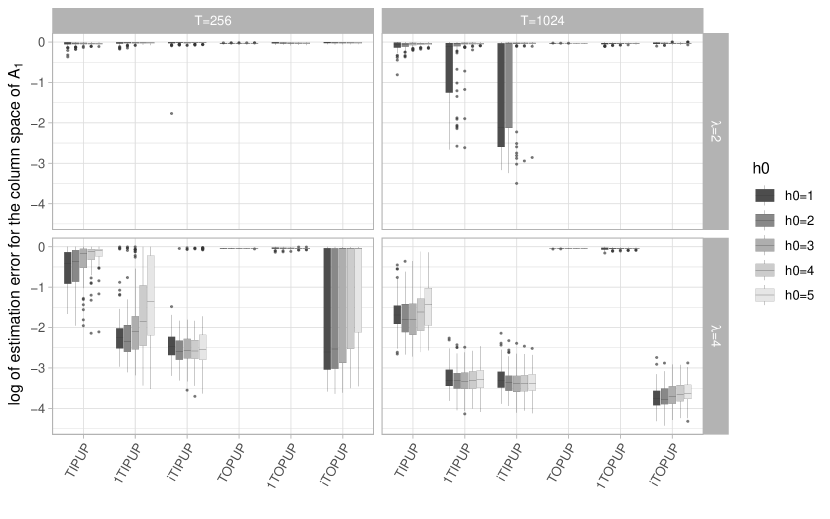

Appendix A Simulation Study

In this section, we compare the empirical performance of different procedures of estimating the loading matrices of a tensor factor model, under various simulation setups. Specifically, we consider the following procedures: the non-iterative and iterative methods, and the intermediate output from the iterative procedures when the number of iteration is 1 after initialization. If TIPUP is used as UINIT and UITER, the one step procedure will be denoted as 1TIPUP. Similarly for 1UP and 1TOPUP. We consider the following combinations of UINIT and UITER.

-

•

UP based: (i) UP, (ii) 1UP and (iii) iUP

-

•