Robust Multiple Stopping — A Pathwise Duality Approach

Abstract

We develop a method to solve, theoretically and numerically, general optimal stopping problems. Our general setting allows for multiple exercise rights, i.e., optimal multiple stopping, for a robust evaluation that accounts for model uncertainty, and for general reward processes driven by multi-dimensional jump-diffusions. Our approach relies on first establishing robust martingale dual representation results for the multiple stopping problem that satisfy appealing pathwise optimality (i.e., almost sure) properties. Next, we exploit these theoretical results to develop upper and lower bounds that, as we formally show, not only converge to the true solution asymptotically, but also constitute genuine pre-limiting upper and lower bounds. We illustrate the applicability of our approach in a few examples and analyze the impact of model uncertainty on optimal multiple stopping strategies.

Keywords: Optimal stopping; Multiple stopping;

Robustness; Model uncertainty; Ambiguity;

Pathwise duality; -expectations; BSDEs; Regression.

AMS 2010 Subject Classification: Primary: 49L20; 60G40; 62L15;

Secondary: 91B06; 91B16.

OR/MS Classification: Dynamic programming/optimal control: Models;

Dynamic programming/optimal control: Applications;

Decision analysis: Risk.

1 Introduction

In this paper we analyze general optimal stopping problems of the following form:

| (1.1) |

where is a family of stopping time vectors, is a number of exercise rights, is a fixed time horizon, is a family of probabilistic models, and is a general -adapted reward process. (The operator is to be understood as if it applies to an uncountable family of random variables.) The optimal stopping problem (1.1) features generality along three dimensions: (i) it allows for optimal multiple stopping (when ), (ii) it allows for a robust evaluation that explicitly takes probabilistic model uncertainty (ambiguity) into account (when is not a singleton), and (iii) it allows for general reward processes that will be driven by multi-dimensional jump-diffusion processes. The process is referred to as the upper Snell envelope of due to exercise rights after the seminal work of Snell [76]. Problems of this type, or special cases thereof, occur naturally in a wide variety of applications in probability, operations research, economics and finance.

Our aim is to develop upper and lower bounds on that satisfy several desirable properties. We achieve this by first establishing suitable martingale dual representations for problem (1.1) that can be viewed as significant generalizations of the classical additive dual representations for standard (i.e., as opposed to robust) optimal stopping problems, developed independently by Rogers [66] and Haugh and Kogan [46] (see also the early Davis and Karatzas [33]) and their extension to standard multiple stopping problems in Schoenmakers [72]. (A multiplicative dual representation for standard optimal stopping problems was proposed by Jamshidian [48].) Our dual representations take the form of an infimum over (robust) martingales, with no appearance of stopping times.

An appealing feature—both theoretically and for numerical stability—of the dual representations we establish is their pathwise optimality, i.e., their almost sure property. Already when these results are new and of independent interest for robust optimal single stopping. They are developed here in the general setting of robust optimal multiple stopping (1.1). The almost sure nature of the dual representations suggests that finding a ‘good’ martingale that is ‘close’ to a ‘surely optimal’ martingale will yield tight and nearly constant upper bounds. The target can be the unique (robust) Doob martingale, to be constructed from an approximation to the upper Snell envelope or, more generally, a martingale for which the dual representation’s infimum is attained and the almost sure property is satisfied. While this phenomenon of tightness and constancy is known in the case of standard, non-robust single stopping problems (i.e., when and , see Rogers [67] and Schoenmakers, Zhang and Huang [73]), we will analyze it in our general setting of robust stopping. We will show in particular that a low (vanishing in probability) robust variance implies a tight (converging in ) approximation. The mathematical details of these results are delicate.

These new theoretical results justify and enable us to next develop a numerically implementable method to obtain upper and lower bounds to with desirable properties. Our lower bound, derived from the proposed exercise strategy, will, as we formally show, not only converge to the optimal solution asymptotically but also be ‘biased low’ at the pre-limiting level in a Brownian-Poisson filtration. This is not the case for the initially proposed upper bound: it converges to the true solution but is not in general ‘biased high’. We therefore also develop a second upper bound that as we prove both converges to the true solution asymptotically and is biased high in a Brownian-Poisson filtration. It is based on a Lipschitzian -approximation, with a Lipschitz constant that we explicitly derive, and a suitable (reversed) application of Jensen’s inequality. We will refer to this second upper bound as our genuine upper bound. The computational complexity of both upper bounds is only linear in the number of exercise rights, and our method does not require nested simulation.

We provide extensive numerical examples, including single and multiple stopping problems, univariate and multivariate stochastic drivers, increasing and decreasing reward functions, and pure diffusion and jump-diffusion models, to illustrate the applicability and generality of our approach. They demonstrate that our approach yields tight upper and lower bounds that, due to almost sure properties, moreover have low standard errors. They also analyze the impact of multiple vs. single stopping rights and reveal that employing a robust evaluation that takes ambiguity into account is highly relevant for optimal stopping, especially in the presence of multiple exercise rights.

Embedded in a Brownian-Poisson filtration, the problems we analyze are naturally represented as stopping problems with respect to -expectations (Peng [61, 62]), leading to backward stochastic differential equations (BSDEs). Hence, we explicitly construct novel genuine upper and lower bounds to BSDE solutions with positively homogeneous convex drivers in a Brownian-Poisson filtration, as a development of independent interest. Bender, Schweizer and Zhuo [17], when analyzing solutions to discrete-time (reflected) BSEs rather than the continuous-time BSDEs we consider, develop upper and lower bounds applying techniques different from the techniques we employ. Bender, Gärtner and Schweizer [18] construct Monte Carlo upper and lower bounds for a class of discrete-time stochastic dynamic programs which includes discretizations of multiple stopping problems. Our genuine upper and lower bounds apply directly to our original continuous-time problem. Our genuine lower bound takes advantage of an almost sure property of a ‘second kind’ that we formally establish in order to reduce its variance—‘second kind’ to distinguish it from the additive dual representation’s almost sure property. This almost sure property entails that the difference between the BSDEs terminal condition and the associated (robust) martingale is constant almost surely. Our genuine upper bound for the continuous-time problem is based on forward simulation of an approximate BSDE solution. The construction is somewhat related to the a posteriori criterion for error evaluation introduced in Bender and Steiner [15] in a Brownian filtration, and developed here to obtain explicit genuine upper bounds for BSDEs in a Brownian-Poisson filtration.

The development of numerically implementable methods to obtain approximations to problems of the type (1.1) but with a singleton (no ambiguity), (single stopping), and with multi-dimensional but satisfying strong conditions, started with the regression-based Monte Carlo methods of Carriere [28] and Longstaff and Schwartz [55]; see also Tsitsiklis and Van Roy [79] and Clément, Lamberton and Protter [31]. These methods yield lower bounds to by approximating the optimal stopping time using regression and are commonly referred to as “primal” approaches. An important example of a non-regression based primal approach is the stochastic mesh method of Broadie and Glasserman [22] (see, for further details, Glasserman [42] and also Belomestny, Kaledin and Schoenmakers [14]). “Dual” algorithms that exploit additive dual representations to numerically compute upper bounds were first proposed by Andersen and Broadie [2] in the standard single stopping problem and were further developed by e.g., Belomestny, Bender and Schoenmakers [11] to allow for non-nested simulation. While primal methods rely in a sense on constructing an appropriate stopping time, dual methods rely on constructing an appropriate martingale. Brown, Smith and Sun [23] in an innovative paper enlarge the information on which an exercise decision may depend in dual optimization, yielding tight upper bounds.

Model uncertainty, and the distinction between risk and ambiguity, has received much attention in recent years. Under the Bayesian paradigm, as adopted in Savage’s [71] subjective expected utility model, this distinction is, in a sense, nullified, through subjective probabilities resulting from a subjective prior probability over probabilistic models that quantifies model uncertainty. A popular approach beyond the Bayesian paradigm is provided by the multiple priors model of Gilboa and Schmeidler [41], which is a decision-theoretic formalization of the classical Waldian maxmin decision rule (Wald [80]; see also Huber [47]) and experimentally motivated by the Ellsberg [37] paradox. These models are intimately related to coherent, convex and entropy convex measures of risk in financial risk measurement (Föllmer and Schied [38, 39], Frittelli and Rosazza Gianin [40], Ruszczyński and Shapiro [68, 69], and Laeven and Stadje [52]). They explicitly recognize that probabilistic models may be misspecified and are often referred to as robust approaches (Hansen and Sargent [45]). The literature on robust single stopping theory is rapidly growing; it includes Riedel [64], Krätschmer and Schoenmakers [50], Bayraktar, Karatzas and Yao [6], Bayraktar and Yao [7], Cheng and Riedel [29], Øksendal, Sulem and Zhang [60], Belomestny and Krätschmer [12, 13], Bayraktar and Yao [8, 9, 10], Ekren, Touzi, and Zhang [36], Matoussi, Piozin, and Possamaï [57], Matoussi, Possamaï, and Zhou [58], and Nutz and Zhang [59]. However, numerically implementable methods to solve general optimal stopping problems of the form (1.1) have not been well-developed as yet. Krätschmer et al. [51] propose a numerically implementable method for single stopping problems under uncertainty in drift and jump intensity. Their approach is dual but not path-wise, i.e., it does not rely on a dual representation with the appealing almost sure property, and cannot handle multiple stopping problems.

The multiple stopping problem can be viewed as nested single stopping problems, where the decision-maker first chooses between stopping at time on the one hand, thus collecting the reward and entering into a new contract with exercise rights, and retaining exercise rights on the other hand, and so on. Multiple exercise rights occur naturally in many applications across various fields. For example, in environmental economics, a swing option gives the investor the right to change his purchased energy quantity a number of times per time period; in finance, a flexible interest rate cap gives the investor the right to exercise at each interest rate reset date a number of times over the life of the contract; and in insurance, a partial surrender option provides a payoff to the policyholder each time he partially surrenders his life insurance contract; see e.g., Carmona and Dayanik [24] and Carmona and Touzi [25] and the references therein. Kobylanski, Quenez and Rouy-Mironescu [49] analyze the standard multiple stopping problem (without ambiguity) allowing the payoff to be a general functional of an ordered sequence of stopping times. Bender, Schoenmakers and Zhang [16] develop a dual approach to generalized multiple stopping problems with respect to standard conditional expectations that is intimately related to the information relaxation approach of Brown, Smith and Sun [23]. A primal-dual algorithm for standard multiple stopping with respect to standard conditional expectations in the context of flexible interest rate caps has been proposed in Balder, Mahayni and Schoenmakers [4].

As an important application, our approach may be used for robust no-arbitrage pricing (Hansen and Jagannathan [44], Cochrane and Saá-Requejo [32]) of American-style derivatives with possibly multiple exercise rights, via superhedging. This entails a significant advancement of the standard approach, where in a usually incomplete market the corresponding stopping problem is solved with respect to an arbitrarily chosen (local equivalent martingale) measure. Our results can also be applied to indifference valuation (seller’s perspective; Carmona [26], Laeven and Stadje [53]) of general optimally stopped reward processes under the multiple priors model. Another application is that of robust risk measurement (Ben-Tal and Nemirovski [19], Bertsimas and Brown [20], Föllmer and Schied [39]) to determine e.g., the risk capital required to cover optimally stopped reward processes.

The remainder of this paper is organized as follows. In Section 2 we recall some basic notions, establish some general properties, introduce the robust optimal multiple stopping problem, and provide some examples. In Section 3, we present our pathwise dual representations and establish our results on surely optimal (robust) martingales. In Section 4, we outline a general primal-dual algorithm and prove its convergence. Section 5 presents explicit upper and lower bounds in a Brownian-Poisson filtration. Section 6 provides extensive numerical results. All proofs and several auxiliary results are in the Online Appendix.

2 Robust Optimal Multiple Stopping

2.1 Basic Notions and General Properties

We start by considering a general stochastic setup. We let be a filtered probability space and let be a linear subspace of with . We further assume that has a lattice structure, i.e., is closed under the operations (min) and (max), and that contains all indicator functions . ((In)equalities between random variables are understood in the -almost sure sense, often without explicit mention.)

To represent preferences, we consider a family of mappings ,

It is referred to as a monotone, regular, recursive, conditional translation invariant dynamic monetary utility functional, henceforth DMU for short, if it satisfies the following conditions:

-

(C1)

for all with and (monotonicity).

-

(C2)

for all , and (regularity).

-

(C3)

for all (recursiveness).

-

(C4)

for all with and (conditional translation invariance).

As additional properties we consider:

-

(P1)

for all and (subadditivity).

-

(P2)

(sensitivity).

-

(P3)

for all and (positive homogeneity).

Conditions (C1)–(C4) will always be assumed. In the sequel, we will mention explicitly which of the properties (P1)–(P3) is required. Properties (P1) and (P2) also entail the implication ; see Lemma A.1 in Appendix A.1. DMUs that satisfy (P1)–(P3), in addition to (C1)–(C4), take the form of robust, or worst case, expectations and have been widely used in applied probability, operations research, economics and finance; see the references in the Introduction and Section 2.3 below.

In this paper, we will frequently use the following implications of (C2) and (C4):

-

(C5)

for all (normalization).

-

(C6)

for all with and (-invariance).

Let be the set of adapted processes such that . A process is said to be a -martingale if

| (2.1) |

We present two auxiliary lemmas. The first lemma provides a generalization of Doob’s optional sampling theorem towards our setup:

Lemma 2.1

(Doob) Suppose satisfies (C1)–(C4). Then, for any -martingale and any stopping time , , it holds that

Due to the next lemma, the properties of recursiveness (C3) and conditional translation invariance (C4) carry over to stopping times, as we will exploit later:

Lemma 2.2

Let satisfy (C1)–(C4), and let be fixed. Consider, for any stopping time , , the functional

Then, acts from , and

-

(i)

satisfies ;

-

(ii)

.

2.2 The Stopping Problem

Consider a fixed adapted reward, or (discounted) cash-flow, process and a DMU decision-maker with exercise rights that have to be exercised at different exercise dates. For each fixed and , , let be the family of stopping vectors such that and for all , . The decision-maker faces the following robust optimal multiple stopping problem:

| (2.2) |

for a DMU functional that satisfies (C1)–(C4). (We note that problem (2.2) is even slightly more general than problem (1.1), which arises when additionally (P1)–(P3) are satisfied.) Henceforth, we write (and ) instead of (and ) for convenience, understanding that they apply to an uncountable family of random variables. For a clean formulation of the multiple stopping problem (2.2), we extend the cash-flow process by setting and , for . That is, the subset of rights , , not exercised by time become valueless. Hence, for any -martingale , , .

When , the single stopping problem

| (2.3) |

occurs as a special case, where the family of stopping times takes values in the set .

The multiple stopping problem can be viewed as nested single stopping problems with only a single exercise right. Indeed, setting , is the upper Snell envelope of due to a single exercise right. Then, for multiple exercise rights , can be viewed as the upper Snell envelope of the process

due to only a single exercise right.

Let us denote the set of -martingales with by . There exists a unique -martingale and a non-decreasing predictable such that

| (2.4) |

which represents the -Doob decomposition of . It is easy to verify that, for ,

| (2.5) |

Henceforth, the -martingale will often be referred to as the -Doob martingale and we often suppress its superscript to simplify notation.

2.3 Examples

We provide the following examples in which specific versions of the robust optimal multiple stopping problem of the general form (2.2) occur naturally:

-

(A.)

No-arbitrage pricing: Let be the set of local equivalent martingale measures. (Only if markets are complete is a singleton, i.e., .) Then, the superhedging price of a contract with exercise rights and associated payoff is given by

Many different approaches to no-arbitrage pricing have been proposed in the literature; see, e.g., the good-deal bounds of Cochrane and Saá-Requejo [32], Hansen and Jagannathan [44] and Björk and Slinko [21], or the acceptable opportunities of Carr, Geman and Madan [27]. All these approaches yield prices of the form

where .

Prototypical situations leading to single and multiple stopping problems in economics and finance are the pricing and exercising of American-style, Bermudan-style, and swing options. American options give the holder the right to exercise the option (once) on any preferred trading day before expiration. Different from American options, Bermudan options prescribe a set of trading days on which the option can be exercised (once). Swing options, more generally, give the holder the right to exercise the option multiple times, at a pre-specified set of exercise dates. With exercise rights, exercised at , the payoff equals for a cash-flow process . Swing options are particularly popular in energy markets to manage the risk of fluctuations in oil, gas, or electricity prices.

-

(B.)

Indifference valuation—the seller’s perspective: Suppose that the seller of a contract has a max-min utility functional of the form

for a family of probabilistic models (i.e., priors) and adopts a utility indifference valuation approach (Carmona [26], Laeven and Stadje [53]). Then, the value of a contract with exercise rights and associated payoff is determined from the indifference relation

Hence,

-

(C.)

Robust risk measurement: Suppose that is a robust, or worst case, expectation, that is,

(2.6) for a family of probabilistic models . In financial risk measurement, (2.6) is referred to as a coherent risk measure and as a set of generalized scenarios (Artzner et al. [3] and Föllmer and Schied [39]); see also Ben-Tal and Nemirovski [19] for the intimately connected robust optimization paradigm. It determines the minimal amount of risk capital required to be added to the financial position to make it ‘safe’ from the viewpoint of the regulatory authority. Applications of coherent risk measures and generalized scenarios to decision and optimization include Lesnevski, Nelson and Staum [54], Bertsimas and Brown [20], Choi, Ruszczyński and Zhao [30], Philpott, de Matos and Finardi [63] and Tekaya, Shapiro, Soares and da Costa [78]. Assume now that is a payout obligation (i.e., liability) at time , where is a stopping time, due to e.g., a flexible interest rate cap in interest rate markets or a partial surrender option in life insurance to be paid to a policyholder who decides to partially surrender his insurance contract. Then, the required amount of risk capital due to stopping rights is given by

3 Pathwise Duality

3.1 Pathwise Dual Representation

The following theorem establishes our pathwise (i.e., almost sure) additive dual representation for general multiple stopping problems of the form (2.2).

Theorem 3.1

Suppose satisfies (C1)–(C4) and is subadditive (P1). Then, for any adapted process and each fixed ,

-

(i)

we have the dual representation

(3.1) -

(ii)

the dual representation’s infimum is attained:

(3.2) -

(iii)

if in addition is sensitive (P2), we have the pathwise dual representation

(3.3)

where the -martingales satisfy

| (3.4) |

and is the upper Snell envelope due to exercise rights, satisfying the Bellman principle,

| (3.5) |

Already when , Theorem 3.1 is new and of significant independent interest. In this case it simplifies to:

Corollary 3.2

Suppose satisfies (C1)–(C4) and (P1). Then, for any adapted process and each fixed , we have the dual representation

| (3.6) | ||||

| (3.7) |

where is the -Doob martingale in Eqn. (2.4). If in addition is sensitive (P2), we have the almost sure property:

| (3.8) |

Remark 3.3

We note that the single stopping problem also admits an alternative but non-pathwise additive dual representation for functionals satisfying (C1)–(C4); see Proposition A.2 in the Appendix. In Theorem 3.1 and Corollary 3.2, the subadditivity property (P1) of is required, and exploited through application of Lemma B.1 in the proof of Theorem 3.1. A dual representation theorem in the spirit of Theorem 3.1 and Corollary 3.2 without assuming (P1) seems not possible to us.

3.2 Surely Optimal -Martingales

The -Doob martingale in Eqn. (2.4) plays a special role in the set of -martingales as its appearance in Corollary 3.2, Eqn. (3.7) (and indirect appearance in Theorem 3.1, (ii)) confirms. In our numerically implementable method developed and applied in Sections 4–6 we rely on the -Doob martingale. From a theoretical perspective, however, and as a general justification of our pathwise dual, martingale-based approach, we develop in this section several results on so-called surely optimal -martingales. To achieve this, we generalize the concept of standard surely optimal martingales (see Schoenmakers, Zhang and Huang [73] in the context of standard conditional expectations and optimal single stopping problems) to subadditive DMU functionals. The results in this section show formally that if a general -martingale—not necessarily the -Doob martingale—induces ‘small’ (robust) variance, then the associated bounds obtained from the dual representation can be expected to be ‘tight’ and nearly constant.

Our results on surely optimal -martingales can also serve as a diagnostic device to assess the quality of the estimated -Doob martingale, derived from an (input) approximation to the upper Snell envelope. If the (robust) variance the estimate induces fails to be small, then it must be far from the -Doob martingale. If, on the other hand, this variance is small, then the estimate will be close to an optimal -martingale (attaining the dual representation’s infimum), even though not necessarily close to the -Doob martingale.

For ease of exposition, we focus attention first on optimal single stopping problems. The next theorem generalizes the analogous key measurability result for standard conditional expectations and optimal single stopping problems to DMU functionals satisfying (C1)–(C4) and (P1).

Theorem 3.4

Let be the upper Snell envelope of the cash-flow process with respect to a subadditive DMU functional satisfying (C1)–(C4) and (P1) as in Corollary 3.2 and let be a -martingale. Then, for any ,

The following lemma will later allow for a generalization of the results in this section to multiple stopping.

Lemma 3.5

Let , , and be as in Theorem 3.4. Then, for any fixed ,

hence is a -Doob martingale increment. (Note the strict first inequality under the max operator.) Thus, in particular, if for every then is the -Doob martingale.

Let us define the conditional -variance as follows:

| (3.9) |

It admits a conditional Chebyshev inequality, exploited in the proof of Theorem 3.8 below, as follows:

Proposition 3.6

Assume (C1)–(C4). If is positively homogeneous (P3), then

| (3.10) |

Next, we state the following lemma:

Lemma 3.7

Assume (C1)–(C4). Let be subadditive (P1) and sensitive (P2). Then,

By virtue of Lemma 3.7, Theorem 3.4 implies that if a -martingale is such that, for some , the conditional -variance

is zero a.s., then a.s. In that case, we say that the -martingale is surely optimal at . (Note that, in particular, the -Doob martingale in (2.4) is surely optimal.)

We then present a stability result for -martingales that are, in loose terms, ‘close’ to be surely optimal, in the sense that the conditional -variance is ‘small’. In particular, for a sequence of -martingales that induces vanishing conditional -variance, we establish weak conditions guaranteeing that the corresponding upper bounds converge to the upper Snell envelope (in ), even though the sequence of -martingales itself does not necessarily converge.

Theorem 3.8

Assume (C1)–(C4). Let be subadditive (P1) and positively homogeneous (P3). Suppose that

If, in addition, for every and every there exists such that

| (3.11) |

then

Note that, if , (3.11) boils down to a standard uniform integrability condition. More generally, we have the following:

Proposition 3.9

Assume (C1)–(C4). Let be subadditive (P1) and positively homogeneous (P3). If, for some ,

then satisfies (3.11).

Under an additional Lipschitz continuity condition, Theorem 3.8 may be readily applied as follows. Let us assume that, for some number ,

| (3.12) |

with In particular, if (3.12) holds for , one obviously has

| (3.13) |

where . That is, if we achieve in an algorithm that , and the are standard uniformly integrable, i.e.,

then on the one hand,

i.e., the satisfy the notion of -uniform integrability, and on the other hand we have due to (3.13) that

Then, Theorem 3.8 implies that

Theorem 3.10

Assume (C1)–(C4) and (P1). Let us define for a set of -martingales , ,

with (Note the strict first inequality under the max operator.) Then it holds that

Remark 3.11

Without doubt it is also possible to derive a version of Theorem 3.8 for the multiple stopping setting. However, as our algorithm in Section 4 below aims at approximative construction of -Doob martingale increments associated with the upper Snell envelopes of the generalized cash-flows

| (3.14) |

respectively, rather than approximative construction of merely surely optimal -martingales, we refrain from such an analysis.

4 A General Primal-Dual Pseudo Algorithm

In this section, we develop a primal-dual pseudo algorithm for robust multiple stopping (henceforth called algorithm for short). Our treatment in this section applies to DMUs satisfying (C1)–(C4), (P1) and weak continuity conditions, and to general reward processes in a Markovian environment; in particular, our treatment in this section is not restricted to -expectations. The following lemma will serve as a cornerstone in our construction.

Lemma 4.1

Let satisfy (C1)–(C4), (P1) and be Lipschitz continuous in the sense of (3.12) for . Furthermore, let , , and let be a -martingale increment, that is, for , , such that

| (4.1) | ||||

Then,

Corollary 4.2

Let be an already constructed approximation to a random variable . Furthermore, let , the -martingale increment , and be as in Lemma 4.1, such that

Then,

Guided by Lemma 4.1 and Corollary 4.2, we now develop a primal-dual algorithm in the context of a Markovian underlying process with state space , possibly in continuous time, that is monitored at the exercise dates as . As usual, we assume that is the -field generated (directly or, as in the next section, indirectly) by the process up to exercise date . Furthermore, we assume that the cash-flows are of the form

where , , are given nonnegative payoff functions such that . Note that, due to the Bellman principle (3.5), can be seen as the upper Snell envelope corresponding to the generalized cash-flow

| (4.2) |

due to a single exercise right, where the so-called continuation functions exist by Markovianity. We also assume to have a set of Monte Carlo simulated training trajectories

We proceed in the following steps:

-

1.

Initialize , for .

-

2.

Suppose that, for a particular with :

(i) we have constructed a set of (approximate) continuation functions , hence an (approximate) continuation value process (for up to exercise times) of the form(ii) we have constructed a (true) -martingale ; and

(iii) we have constructed, on each trajectory , a path(4.3) (4.6) as an approximation to .

-

3.

Now construct, using these trajectories, a subsequent (true) -martingale , a subsequent set of continuation functions , , and subsequent trajectories , (as approximations to and , respectively) such that (4.3) holds for . To this end, we carry out the following backward procedure, or “backward subroutine”, at level :

-

–

As initialization, set . (We also set .)

-

–

Suppose that, for , the values , , the set of -martingale increments (which is empty if ), and the continuation function have been constructed.

-

–

Then construct, according to the regression subroutine in Section 4.1 below, a continuation function , a -martingale increment with , and set , for

(4.7)

-

–

Proceeding this way:

-

(a.)

Working forward from thus yields a family of continuation functions and a family of (true) -martingales , respectively:

-

(b.)

An upper bound for the solution to the robust multiple stopping problem at due to exercise rights is now given by (cf. Theorem 3.1, (ii)):

(4.8) which needs to be estimated by a separate (Monte Carlo) procedure.

-

(c.)

A lower bound for the solution to the robust multiple stopping problem at due to exercise rights may next be obtained from the family of stopping times

(4.9) via a (Monte Carlo) estimation of:

(4.10)

4.1 Regression Subroutine

Let there be given a collection of ‘elementary’ -martingale increments , with and , that is,

and a collection of basis functions . We assume that the set of -martingale increments

is -dense among the -measurable square-integrable random variables such that . We then solve, in view of Lemma 4.1 and Corollary 4.2, for fixed and and the least squares problem

| MSE | ||||

| (4.11) |

where we used vector notation and . For the algorithm to converge, it is actually sufficient that the MSE above converges to zero as for our choice of and . We will suppress the superscripts and whenever there is no ambiguity. We set

4.2 Convergence Theorem

We state the following theorem:

Theorem 4.3

Let be subadditive (P1) and Lipschitz continuous in the sense of (3.12) for . We set and denote by , and the functions constructed in the algorithm above. Then,

| (4.12) |

| (4.13) |

| (4.14) |

for all and . Furthermore,

4.3 Complexity

At first sight, the path-wise maximum in (4.8) would require the evaluation of terms. Fortunately, due to following proposition, it only requires evaluations.

Proposition 4.4

Define, for and

and naturally , . Then,

| (4.15) |

Thus, the evaluation of (4.8) may be described as follows:

Recursive evaluation of (4.8)

-

1.

Initialize for

-

2.

Suppose that, for and for , the construction of has been conducted;

-

3.

Backward subroutine: Initialize . When has been constructed for , compute via (4.15).

5 Explicit Construction in a Brownian-Poisson Filtration

In the sequel, we assume that we have a completed continuous-time filtration on a filtered probability space generated by a -dimensional standard (i.e., zero mean and unit variance) Brownian motion and a -dimensional Poisson process with arrival intensity . As usual, we define the compensated counterpart of as . The components of the processes and are assumed to be independent. The stochastic drivers and generate the underlying Markovian adapted reward process with state space of Section 4.

Furthermore, we assume that satisfies (the continuous-time analogs of) (C1)–(C4) and (P1)–(P3). This means, in particular, that is a coherent risk measure. By classical duality results (e.g., Föllmer and Schied [39]), the robust multiple stopping problem at time is then given by

| (5.1) |

with our family of stopping vectors, and a closed convex set of probability measures absolutely continuous with respect to and satisfying a stability assumption. In such a continuous-time setting, it is known that every recursive coherent risk measure can be identified with a solution to a backwards stochastic differential equation (BSDE) also called a -expectation, modulo a compactness assumption; see Section 5.1 for the precise definitions and results. Exploiting our algorithm presented in Section 4, this section constructs explicit upper and lower bounds to with desirable properties.

5.1 Bellman’s Principle, the Set of Priors, and BSDE drivers

A probability measure change from to an absolutely continuous measure admits an explicit representation in our Brownian-Poisson setting. Consider the Radon-Nikodym derivative

As is well-known, has the Doléans-Dade exponential form

| (5.2) |

where is a predictable, -valued, stochastic drift, and is a positive, predictable, -valued process with , which jointly uniquely characterize . From Girsanov’s theorem, we know that is a standard Brownian motion under while the process has arrival intensity . In particular, the reference model corresponds to and . The stochastic drift may be given the interpretation of a drift in the diffusive component that is misspecified to be absent by the reference model . Similarly, represents a deviation from the misspecified arrival intensity under .

In our dynamic setting, with DMU evaluations satisfying the continuous-time analogs of (C1)–(C4) and (P1)–(P3), time-consistency of choice under uncertainty is satisfied as it is equivalent to recursiveness or Bellman’s dynamic programming principle. Time-consistency of a dynamic evaluation requires—according to its usual definition, also referred to as ‘strong’ time-consistency—that whenever , . That is, if is preferred over , in each state of nature at time , then the same preference necessarily applies prior to time ; see e.g., Riedel [65], Ruszczyński and Shapiro [69], Shapiro, Dentcheva and Ruszczyński [74], Chapter 6, Ruszczyński [70] and Shapiro [75]. Indeed, requiring recursiveness or Bellman’s dynamic programming principle is equivalent to requiring time-consistency for , , which is, in turn, equivalent to the set of priors being -stable; see Delbaen [34]. More formally, the following statements are equivalent (see Lemma 11.11 of Föllmer and Schied [39] for the equivalence (i)–(ii), Delbaen [34] and Delbaen, Peng and Rosazza Gianin [35] for (ii)–(iii) in a Brownian setting, and Tang and Wei [77] and Laeven and Stadje [53] for (ii)–(iii) in a general semi-martingale setting):

-

(i)

is recursive, i.e., satisfies Bellman’s dynamic programming principle for every , , and bounded .

-

(ii)

is time-consistent over bounded rewards.

-

(iii)

There exists a closed, convex, set-valued predictable mapping taking values in such that

As in our continuous-time Brownian-Poisson setting recursiveness (C3) is equivalent to (iii), we assume henceforth:

-

(A1)

with is compact.

We note that (A1) also implies that is recursive and time-consistent over square-integrable rewards.

For , and , and satisfying Assumption (A1), let us define a function via Fenchel’s duality:

| (5.3) |

One easily verifies that is convex, positively homogeneous and Lipschitz continuous. Then, from Krätschmer et al. [51], we have the following statement, which is essentially (with (A1)) equivalent to (i)–(iii) above:

-

(iv)

For every , there exists a unique square-integrable predictable such that

In particular, there exists a unique square-integrable predictable such that

| (5.4) |

Furthermore, for , the in (5.4) recover—and later allow to practically compute—the -Doob martingale as follows (cf. Eqns. (2.4)–(2.5)):

| (5.5) |

Here, should be interpreted as exercise dates and as the continuous embedding.

Because , by (iv), for ,

| (5.6) |

Eqn. (5.4) is referred to as a backward stochastic differential equation (BSDE). Formally, given a terminal payoff and a function , referred to as a driver, the solution to the corresponding BSDE is a triple of square-integrable and suitably measurable processes that satisfies

The solution is often referred to as a (conditional) -expectation; see, e.g., Peng [62].

As a means of illustrating the generality of our setup given by (5.1) with (A1) we provide a few examples.

Example 5.1

-

(1.)

Ball scenarios: Consider a decision-maker endowed with a set of priors constituting a small ball environment surrounding all deemed equally plausible. Then,

and . Suppose without losing generality that . Then, from (5.3), in explicit form, .

-

(2.)

Discrete scenarios: Imagine a decision-maker who considers, at each time , finite-dimensional families and , , with all elements deemed equally plausible. Then,

and , with the convex hull. We can assume that without losing generality, upon redefining the reference measure. Furthermore, .

To obtain genuine upper and lower bounds to the optimal solution of the stopping problem (5.1), we henceforth impose the following additional assumption:

-

(A2)

and we can simulate i.i.d. copies of .

Once, we have constructed a ‘good’ family of -martingales , we are faced with the computation of in (4.8). An important advantage of this dual approach for numerical stability is that we have, in fact, the pathwise dual representation

Indeed, we will obtain an estimate with ‘low’ variance provided the -martingale is ‘good’. Furthermore, to obtain a lower bound we employ in (4.10). By the results discussed in this subsection, for a square-integrable payoff , has a representation of the form

| (5.7) | ||||

| (5.8) |

Let us now first consider the question of how to explicitly obtain a ‘good’ family of -martingales in our Brownian-Poisson filtration with (C1)–(C4), (P1)–(P3) and (A1)–(A2). Next, we develop in Sections 5.3 and 5.4 explicit genuine lower and upper bounds.

5.2 Parameterization of the -Martingale Increments

As in Section 4, we assume that is an -adapted -dimensional underlying Markovian process, now in a Brownian-Poisson filtration, and that our cash-flow process has a structure of the form , such that . We further assume that the resulting random variables are square integrable.

We are going to construct a -martingale backwardly. To this end, we consider, between two exercise dates and , the (fine) grid , where with . We also define

and sometimes use the notation , where the are simply the enumerated . For our numerical schemes we always assume that Assumption (A2) is in place, next to (A1). In particular, we can also simulate i.i.d. copies of the .

We formally initialize . Suppose that for some (fixed) , an approximation to the upper Snell envelope and the set of -martingale increments have been constructed. Then, we carry out the following loop. For , we initialize . Now, if , , has been constructed, we solve the piecewise linear minimization problem

| (5.9) |

for certain basis functions , , and , , and trajectories. Alternatively to (5.2), we can solve

| (5.10) |

which has a closed-form solution.

Remark 5.2

We note that in the case the filtration is generated by a one-dimensional process (either a Brownian motion or a Poisson process), the minimization problem (5.2) corresponds to a linear programming problem. This is seen as follows. As is a coherent risk measure, it follows that is positively homogeneous. Thus, there exist such that . Hence, the function

is convex as . (The reason is that is linear on its negative part.) Thus, the minimization problem (5.2) is convex. Because any piecewise linear function that is convex can be written as a supremum of finitely many linear functions, the minimization problem can be expressed as a linear programming problem.

Next, define

and similarly. We set

We then obtain the desired -martingale increments by defining

| (5.11) |

In the end, when we have arrived at , we define and according to Eqn. (4.7). This way, we have recursively constructed the parameterized space of -martingale increments. The following proposition establishes convergence of our construction.

Proposition 5.3

The -martingale increments constructed in (5.11) are dense in and, in particular,

5.3 Converging Genuine Lower Bound

This subsection develops an explicit lower bound that converges to the upper Snell envelope asymptotically and constitutes a genuine (biased low) lower bound at the pre-limiting level. Consider (5.8) with and constructed by (4.9). From e.g., Barrieu and El Karoui [5], we know that the supremum in (5.7) is attained in

| (5.12) |

where denotes the Doleans-Dade exponential, and denotes the mapping of subdifferentials of the convex driver . We shall exploit this to compute the lower bound numerically. For simplicity, assume that is differentiable. (If that is not satisfied, then our approach may still be applied by considering elements in the subgradient.)

Let , simulate paths , and for , and also consider (the true, non-simulated) , and . Then, define and construct

using least squares Monte Carlo regression as described in Section 5.2 with basis functions and terminal condition given by . (Henceforth, we suppress in the notation.) Furthermore, define and construct, using new i.i.d. simulations,

and moreover the partial derivatives

Next, define i.i.d. simulations of the measure via the Radon-Nikodym derivative

Finally, set

| (5.13) |

with , , simulated copies of constructed by applying the numerical scheme of Section 5.2.

Recall from (4.10) that gives a lower bound to the upper Snell envelope. Thus, it follows from (5.7), (5.12), and the definition of that

| (5.14) |

That is, our estimator (5.13) constitutes a genuine lower bound. This means that, on average, we indeed obtain a lower bound to the optimal solution given by the upper Snell envelope. Furthermore, as a consequence of Proposition 5.3 and Theorem 4.3, the lower bound converges to the optimal solution.

Summarizing succinctly: given a time grid , our explicit numerical construction of the lower bound consists of the following steps:

-

(1.)

Select basis functions and run Monte Carlo simulations to determine and . To describe their evolution, it is sufficient to store the corresponding , and . [(BSDE 1).]

-

(2.)

Use , and to estimate . Select basis functions and run Monte Carlo simulations to determine using the estimated as terminal condition. To describe the evolution of this process it is sufficient to store the corresponding and . [(BSDE 2).]

-

(3.)

With and at hand from Step (2.), simulate copies of . Furthermore, with , and at hand from Step (1.), simulate copies of . Using (5.13), a genuine lower bound to the upper Snell envelope is then obtained.

Note that the Monte Carlo simulations are done consecutively and are not nested, so that the total computation time depends only on . We summarize the results of this subsection in the following theorem:

Theorem 5.4

The estimator defined in (5.13) is a genuine lower bound to the upper Snell envelope, i.e., . Furthermore, converges to as , , , and tend to infinity and tends to zero, i.e.,

5.3.1 Subtracting the associated -martingale in Eqn. (5.13): Reducing the variance while not inducing a bias

Let be approximations of the ‘true’ solution to the BSDE with terminal condition . Denote by a probability measure defined by

| (5.15) |

By (5.7), yields a lower bound to . (If the and were exact, then and .)

The following proposition will help to reduce the variation in our numerical scheme.

Proposition 5.5

Let be the -martingale defined by

Then, subtracting the -martingale from the terminal condition does not induce a bias, i.e.,

We finally note that if we would have that from Eqn. (5.12), then, by the definition of , were constant a.s. Hence, if is approximately , then is approximately constant. More formally, if converges to in , we have that

where the convergence should be understood in . In particular, if in , then as .

Inspired by this theoretical result, which may be referred to as an almost sure property of a second kind to distinguish it from the additive dual representation’s almost sure property, we will in our numerical analysis subtract the associated -martingale from the right-hand side of Eqn. (5.13) when computing the genuine lower bound: it will reduce the variance without inducing a bias.

5.4 Converging Approximate and Genuine Upper Bounds

This subsection develops an explicit approximate upper bound that converges to the upper Snell envelope asymptotically, and an explicit genuine upper bound that not only converges to the upper Snell envelope but is also biased high at the pre-limiting level. To obtain an upper bound with Theorem 3.1, we set

Since we cannot compute exactly, we approximate, in view of (4.8), the terminal condition by the -martingale constructed in Section 5.2, i.e., we set

Next, we define

Clearly, the terminal condition depends only on . Next, note that, for every , we have that is a function of , and, for every , only depends on , , and where both of the latter are independent of . From this we may conclude that is a Markov process on the time grid .

Next, we solve numerically the BSDE (5.8) with . To do so we will consider an approximation scheme. We can simulate paths of the adapted process

for . To compute the BSDE with terminal condition , let be the number of basis functions in the least squares Monte Carlo regression. Employing the algorithm described in Section 5.2, we can construct the coefficients , and , and processes

| (5.16) |

Note that by applying Proposition 5.3 and Theorem 4.3 twice we may conclude that, in ,

| (5.17) |

In particular, constitutes a converging approximate upper bound to the upper Snell envelope. From now on we assume that we have already estimated , and .

Next, let us develop a genuine upper bound. It is well-known that under assumption (A1), the functional is Lipschitz continuous (cf. Peng [61]). Define

| (5.18) |

Then, by Theorem 3.1 and the Lipschitz continuity of , we have that

| (5.19) |

for a Lipschitz constant analyzed later. We will exploit inequality (5.4) to develop our genuine upper bound. By Proposition 5.3 and Theorem 4.3, converges to , converges to in and converges to zero, as , , and tend to infinity and tends to zero.

For , simulate i.i.d. copies of through

Next, using (5.4), simulate i.i.d. copies of . (Recall that , and are already available.) Then, (5.4) suggests to estimate the upper bound by

Note that is an unbiased estimator of . However, taking the square root of an estimator gives rise to a possible downward bias. If we wish to eliminate the downward bias, we need to elaborate a little further, as follows. We simulate independent . Then we set

| (5.20) |

Since

thus defined is biased high. Note that the first equality follows from independence and the inequality is due to a suitable (reversed) application of Jensen’s inequality. As before, as a consequence of Proposition 5.3 and Theorem 4.3, we have that converges to as , , , and tend to infinity and tends to zero.

Summarizing succinctly: given a time grid , our explicit numerical construction of the upper bound consists of the following steps:

-

(1.)

Select basis functions and run Monte Carlo simulations to determine and . To describe their evolution, it is sufficient to store the corresponding , and . [(BSDE 1).]

-

(2.)

, and give rise to a terminal condition and a Markov process defined above. Select basis functions and run Monte Carlo simulations to calculate as the solution to the corresponding BSEs with the Markov process and terminal condition . Store the corresponding , and . [(BSDE 2).]

- (3.)

Note again that the Monte Carlo simulations are done consecutively and are not nested, so that the total computation time depends only on . We summarize the results of this subsection in the following theorem:

Theorem 5.6

We finally state the following proposition on the precise Lipschitz constant appearing in (5.4).

Proposition 5.7

Let and be square-integrable terminal conditions and denote by and the associated BSDE solutions. Then,

| (5.21) |

where and with the Lipschitz constant of the driver .

6 Numerical Examples

In this section we analyze our approach in numerical examples, including single and multiple stopping, univariate and multivariate stochastic drivers, increasing and decreasing reward functions, and pure diffusion and jump-diffusion models. As a general observation, we recall that the computational complexity of the numerically implementable method proposed in this paper is linear in the number of exercise rights and that it does not require nested simulation.

6.1 Single Stopping: Bermudan Option in a Diffusion Model

The first example studied in this subsection is the pricing problem for a Bermudan-style option in a single risky asset Black-Scholes model with dividends in the presence of ambiguity. This example goes back to Andersen and Broadie [2] in a setting without ambiguity, which can serve as a benchmark case. Throughout this subsection, we consider the dynamics , , with and , where is the price of asset at time . Following this literature, we assume that there is a risk-free interest rate of , and that the option’s underlying is a single dividend-paying stock with constant volatility and dividend rate , resulting in a risk-neutral drift of . The first product we study is a call option with strike price and maturity . The stock price at time 0 is varied between . Exercise dates are specified as , , i.e., there are 9 intermediate exercise dates, and the trivial ones at time and at maturity. We allow for ambiguity in the drift and consider , ; cf. Example 5.1.

The three BSDEs—-martingale, lower, and upper bounds—are solved with two sets of simulations. We consider one set of simulations with trajectories and time steps for the initial -martingale BSDE, and a second set of simulations with trajectories and time steps for the BSDEs associated with the lower and upper bounds. The number of basis functions is always 52 for and 52 for . These are , , where the are percent quantiles of estimated from the trajectories in the initial run of least squares Monte Carlo. Thus, we approximate all unknown functions by linear splines. Notice that this function basis is not problem-dependent and that its precision can be controlled by the chosen grid of quantiles. Numerically, this basis works much better in our experiments than a locally linear approximation, which would also include the discontinuous terms . In all our numerical experiments, the implementation of the regression is based on (5.2).

For the evaluation of the lower bound, we draw a new sample with a larger number of trajectories. For the evaluation of the upper bound, we need a very fine time discretization to obtain a small ‘tracking error’, defined as ; cf. (5.20). We need, however, fewer trajectories, because the pathwise dual representation leads to a very small variance, as expected from the theoretical results in Section 3.2. We thus choose the number of trajectories to be and increase the number of time steps by a factor 100 to . Here, we do not run new regressions but simply repeat each set of coefficients 100 times. This device of increasing the time discretization and extrapolating regression coefficients is due to Belomestny, Bender, Schoenmakers [11], in a standard stopping setting without ambiguity. However, due to the additional non-linearity from the BSDE, it is not sufficient in our setting to just run the regressions at exercise times only; we need them at our fine grid .

Tables 3–3 summarize lower and upper bounds for different degrees of ambiguity () and different values of the initial stock price (). The first four columns display lower bounds along with their standard errors. Here, “LB without M” is the lower bound in Eqn. (5.13) without subtraction of the -martingale, while “LB” is the definitive lower bound that subtracts the -martingale, as discussed in Section 5.3.1. As the results confirm, subtraction of the -martingale leads to a substantial variance reduction. The next three columns correspond to the upper bound. Here, is the solution to the upper bound BSDE, i.e., the approximate upper bound, “TE” is the tracking error defined above, and “UB” combines the two to obtain the genuine upper bound in Eqn. (5.20). The final two columns display the mean of together with its standard error. The point here is to illustrate that having only trajectories in the upper bound simulation is already sufficient, since the terminal condition has a (very) small variance. In general, we observe that the gaps between LB on the one hand and and UB on the other hand are (very) small. When (i.e., in the no-ambiguity case), we can compare our results to benchmark values, e.g., from Andersen and Broadie [2]. With , the true value is 7.98. This should be compared to our genuine lower bound of 7.98, our approximate upper bound of 8.00, and our genuine upper bound of 8.07, corresponding to gaps of 0.2% and 1.0% of the option value, respectively.

| LB without M | s.e. | LB | s.e. | TE | UB | s.e. | |||

|---|---|---|---|---|---|---|---|---|---|

| 10 | 5.4901 | 0.0197 | 5.4635 | 0.0107 | 5.4833 | 0.0843 | 5.5689 | 5.4679 | 0.0026 |

| 30 | 4.7384 | 0.0158 | 4.7161 | 0.0096 | 4.7326 | 0.0836 | 4.8163 | 4.7184 | 0.0025 |

| 100 | 4.5005 | 0.0147 | 4.4795 | 0.0093 | 4.4962 | 0.0812 | 4.5775 | 4.4830 | 0.0025 |

| 300 | 4.4349 | 0.0144 | 4.4143 | 0.0092 | 4.4310 | 0.0806 | 4.5116 | 4.4180 | 0.0024 |

| 4.4121 | 0.0143 | 4.3917 | 0.0092 | 4.4084 | 0.0804 | 4.4888 | 4.3955 | 0.0024 | |

| 4.4030 | 0.0142 | 4.3827 | 0.0092 | 4.3997 | 0.0803 | 4.4800 | 4.3868 | 0.0024 | |

| 4.4024 | 0.0142 | 4.3821 | 0.0092 | 4.3987 | 0.0803 | 4.4790 | 4.3859 | 0.0024 |

| LB without M | s.e. | LB | s.e. | TE | UB | s.e. | |||

|---|---|---|---|---|---|---|---|---|---|

| 10 | 9.4387 | 0.0244 | 9.4069 | 0.0143 | 9.4331 | 0.0721 | 9.5063 | 9.4110 | 0.0021 |

| 30 | 8.4419 | 0.0199 | 8.4161 | 0.0132 | 8.4445 | 0.0700 | 8.5146 | 8.4232 | 0.0020 |

| 100 | 8.1305 | 0.0186 | 8.1068 | 0.0129 | 8.1316 | 0.0678 | 8.1994 | 8.1113 | 0.0019 |

| 300 | 8.0426 | 0.0183 | 8.0195 | 0.0128 | 8.0450 | 0.0678 | 8.1127 | 8.0249 | 0.0019 |

| 8.0152 | 0.0182 | 7.9923 | 0.0128 | 8.0150 | 0.0678 | 8.0828 | 7.9949 | 0.0019 | |

| 8.0039 | 0.0181 | 7.9811 | 0.0127 | 8.0034 | 0.0678 | 8.0712 | 7.9833 | 0.0019 | |

| 8.0030 | 0.0181 | 7.9802 | 0.0127 | 8.0022 | 0.0678 | 8.0699 | 7.9821 | 0.0019 |

| LB without M | s.e. | LB | s.e. | TE | UB | s.e. | |||

|---|---|---|---|---|---|---|---|---|---|

| 10 | 14.7691 | 0.0279 | 14.7380 | 0.0179 | 14.7718 | 0.0682 | 14.8411 | 14.7460 | 0.0020 |

| 30 | 13.6662 | 0.0228 | 13.6414 | 0.0166 | 13.6814 | 0.0669 | 13.7484 | 13.6570 | 0.0019 |

| 100 | 13.3221 | 0.0214 | 13.2994 | 0.0163 | 13.3400 | 0.0658 | 13.4058 | 13.3164 | 0.0019 |

| 300 | 13.2257 | 0.0211 | 13.2037 | 0.0162 | 13.2459 | 0.0658 | 13.3116 | 13.2225 | 0.0019 |

| 13.1924 | 0.0209 | 13.1706 | 0.0162 | 13.2133 | 0.0657 | 13.2790 | 13.1900 | 0.0019 | |

| 13.1791 | 0.0209 | 13.1574 | 0.0162 | 13.2007 | 0.0657 | 13.2664 | 13.1775 | 0.0019 | |

| 13.1774 | 0.0209 | 13.1556 | 0.0162 | 13.1994 | 0.0657 | 13.2650 | 13.1761 | 0.0019 |

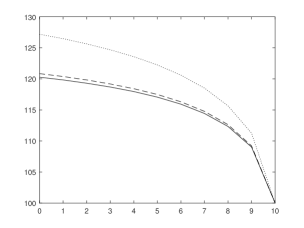

In Figure 1 we analyze exercise boundaries. These boundaries are theoretically independent of the starting values of . In order to obtain accurate exercise boundaries already for early time points, we need to make sure that the simulated trajectories are sufficiently spread out over the entire time span from to and are not concentrated around a fixed value of close to time . To this end, we start simulating trajectories at time and set the drift of to zero over the interval . Moreover, we double the number of basis functions by choosing a finer grid of quantiles, and double the number of trajectories to , to account for the fact that we now have a wider space over which we approximate.

In the left panel of Figure 1, we plot the threshold value that the stock price has to exceed to make stopping optimal (i.e., the continuation value), for different degrees of ambiguity (), as a function of the exercise dates. The solid line depicts exercise boundaries without ambiguity (), while the dashed line corresponds to and the dotted line corresponds to . In all cases, continuation values increase as we move away from the no-ambiguity case (). Thus, with more ambiguity, the decision-maker stops later. Intuitively, for a call option’s payoff function, the possibility of a (prosperous) deviation from the reference model which accumulates over time makes the option more valuable at later dates. Hence, the decision-maker will stop later.

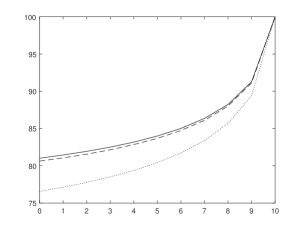

A similar pattern emerges when we replace the call option payoff function by a put option, with strike price and . To make exercise decisions non-trivial, we set the dividend rate equal to zero in this case, all else equal. Table 4 and Figure 1 (right panel) display the corresponding price bounds and exercise boundaries. For the put option, contrary to for the call option, exercise becomes optimal when the stock price falls below the exercise boundaries in the right panel of Figure 1. Similar to the call option, with more ambiguity, the decision-maker stops later. In this case, the possibility of an unfavorable deviation from the reference model that accumulates over time makes the option more valuable at later dates.

| LB without M | s.e. | LB | s.e. | TE | UB | s.e. | |||

|---|---|---|---|---|---|---|---|---|---|

Next, we consider a two-dimensional version of this example. We suppose that there are two risky assets and , which are assumed to be independent and identically distributed with the same dynamics as the single dividend-paying stock in the univariate case. The payoff function we consider is a max-call, that is, stopping at time yields a reward of . We set and , and allow for eleven equidistant exercise opportunities including and , as before. All other problem parameters and specifications remain the same.

Regarding the numbers of trajectories and time steps in the different stages of the algorithm, we maintain the same specifications as in the univariate case. The function basis is constructed as follows. We always use the same set of 441 basis functions for and for . These consist of the constant , 20 univariate basis functions , , which only depend on , 20 univariate basis functions , , which only depend on , and all products , . The 20 univariate basis functions are constructed as in the univariate case but with a slightly coarser grid, i.e., for , we choose and where the are the percent quantiles of estimated from the trajectories in the initial run of least squares Monte Carlo. This bivariate basis of linear splines is relatively large but fairly generic, i.e., it exploits additional knowledge about the problem far less than, e.g., the -implementations in Belomestny, Bender and Schoenmakers [11] or Krätschmer et al. [51], which rely on prices of European max-call options. In principle, one could increase efficiency by including a variable selection step in the first regression.

We observe from Table 5 that the gaps between the genuine lower bound and the approximate upper bound are fairly small, corresponding to about only 0.4% of the option value. The presence of ambiguity amplifies in the multivariate setting and its impact is more pronounced than in the univariate case.

| LB without M | s.e. | LB | s.e. | s.e. | |||

|---|---|---|---|---|---|---|---|

| 10 | 16.5266 | 0.0351 | 16.5252 | 0.0196 | 16.5902 | 16.5705 | 0.0230 |

| 30 | 14.7575 | 0.0268 | 14.7513 | 0.0172 | 14.8054 | 14.7992 | 0.0216 |

| 100 | 14.1997 | 0.0246 | 14.1921 | 0.0167 | 14.2418 | 14.2365 | 0.0211 |

| 300 | 14.0434 | 0.0240 | 14.0348 | 0.0166 | 14.0861 | 14.0807 | 0.0210 |

| 13.9916 | 0.0238 | 13.9830 | 0.0165 | 14.0322 | 14.0268 | 0.0210 | |

| 13.9700 | 0.0238 | 13.9618 | 0.0165 | 14.0115 | 14.0061 | 0.0210 | |

| 13.9679 | 0.0237 | 13.9597 | 0.0165 | 14.0092 | 14.0038 | 0.0210 |

6.2 Multiple Stopping: Swing Option in a Two-Factor Jump-Diffusion Model

Supported by the accuracy and stability of our pathwise duality approach for optimal single stopping, we now proceed to multiple stopping. In this subsection, we analyze a canonical multiple stopping problem, that of swing option pricing in electricity markets, in the presence of ambiguity. For this purpose, we consider a two-factor jump-diffusion model for the electricity log-price process, which has been suggested by Hambley, Howison and Kluge [43] to be a more realistic extension of the one-factor Gaussian model proposed by Lucia and Schwartz [56] and implemented e.g., by Bender, Schoenmakers and Zhang [16].

Specifically, we assume that the electricity price at time is given by , where the two stochastic factors and are mutually independent and is a deterministic function of time that can be used to calibrate the model. The factor is Gaussian and follows the SDE

with , , and a standard Brownian motion. The jump component follows the SDE

where , is a (non-compensated) Poisson process with arrival rate , and and the (deterministic) jump size are positive constants. In the special case , this model reduces to a mean-reverting one-factor jump-diffusion model for the log-price process. For , the model combines a mean-reverting Gaussian component, like in the Lucia-Schwartz model, with occasional highly transitory spikes; see Hambley, Howison and Kluge [43] for further discussion. Using their formula (3), the processes and can be simulated forward in time without discretization error.

In our illustration, we consider a swing option contract that gives the owner the right to purchase electricity at a strike price , and consider exercise rights, in the time interval . We assume a fixed number of equidistant exercise opportunities. We set the parameters of the price process as , , , , , and . Furthermore, we set the contract parameters as , and consider 21 equidistant exercise opportunities (including one at time 0 and one at time ). We allow for varying degrees of ambiguity towards the Gaussian and the jump components of the price process and consider , ; cf. Example 5.1.

The overall numerical implementation is very similar to the previous optimal single stopping example. The three BSDEs—-martingale, lower, and upper bounds—are solved with two sets of simulations. We consider one set of simulations with trajectories and time steps for the initial -martingale BSDE and a second set of simulations with trajectories and time steps for the BSDEs associated with the lower and upper bounds. We choose the same basis functions as in the single stopping example and thus obtain 52 basis functions for and 52 for , and now also 52 basis functions for . Note that these functions depend only on but not on and . For the evaluation of the lower bound, we draw a new sample of trajectories and time steps. For the evaluation of the upper bound, we again artificially create a finer time discretization, by repeating each set of coefficients 100 times, and reduce the number of trajectories to .

Tables 7–7 and 10–13 (in the Appendix) summarize lower and upper bounds for different numbers of exercise rights, different values of and , and for different values of (i.e., without and with jump component). Upon comparing the results for one exercise right to those for multiple exercise rights, we readily observe that the impact of ambiguity is even more pronounced in the multiple stopping case.

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| LB | |||||

| s.e. | |||||

| TE | |||||

| UB |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| LB | |||||

| s.e. | |||||

| TE | |||||

| UB |

Acknowledgements. We are very grateful to Christian Bender and to seminar and conference participants at the University of Waterloo and the Lorentz Center for comments and suggestions. This research was funded in part by the Netherlands Organization for Scientific Research (NWO) under grants NWO-Vidi and NWO-Vici (Laeven) and by the DFG Excellence Cluster Math+ Berlin, project AA4-2 (Schoenmakers).

References

- [1]

- [2] Andersen, L., and Broadie, M. (2004). A primal-dual simulation algorithm for pricing multi-dimensional American options. Management Science 50, 1222–1234.

- [3] Artzner, P., Delbaen, F., Eber, J., and Heath, D. (1999). Coherent measures of risk. Mathematical Finance 9, 203–228.

- [4] Balder, S., Mahayni, A., and Schoenmakers, J. (2013). Primal-dual linear Monte Carlo algorithm for multiple stopping — An application to flexible caps. Quantitative Finance 13, 1003-–1013.

- [5] Barrieu, P., and El Karoui, N. (2009). Pricing, hedging and optimally designing derivatives via minimization of risk measures. In: Carmona, R. (ed.). Indifference Pricing: Theory and Applications. Princeton University Press, Princeton, 77–146.

- [6] Bayraktar, E., Karatzas, I., and Yao, S. (2010). Optimal stopping for dynamic convex risk measures. Illinois Journal of Mathematics 54, 1025–1067.

- [7] Bayraktar, E., and Yao, S. (2011). Optimal stopping for non-linear expectations—Part I. Stochastic Processes and their Applications 121, 185–211.

- [8] Bayraktar, E., and Yao, S. (2014). On the robust optimal stopping problem. SIAM Journal on Control and Optimization 52, 3135–3175.

- [9] Bayraktar, E., and Yao, S. (2017a). On the robust Dynkin game. The Annals of Applied Probability 27, 1702–1755.

- [10] Bayraktar, E., and Yao, S. (2017b). Optimal stopping with random maturity under nonlinear expectations. Stochastic Processes and their Applications 127, 2586–2629.

- [11] Belomestny, D., Bender, C., and Schoenmakers, J. (2009). True upper bounds for Bermudan products via non-nested Monte Carlo. Mathematical Finance 19, 53–71.

- [12] Belomestny, D., and Krätschmer, V. (2016). Optimal stopping under model uncertainty: A randomized stopping times approach. The Annals of Applied Probability 26, 1260–1295.

- [13] Belomestny, D., and Krätschmer, V. (2017). Optimal stopping under probability distortions and law invariant coherent risk measures. Mathematics of Operations Research 42, 806–833.

- [14] Belomestny, D., Kaledin, M., and Schoenmakers, J. (2020). Semi-tractability of optimal stopping problems via a weighted stochastic mesh algorithm. Mathematical Finance 30, 1591–1616.

- [15] Bender, C., and Steiner, J. (2013). A posteriori estimates for Backward SDEs. SIAM Journal of Uncertainty Quantification 1, 139–163.

- [16] Bender, C., Schoenmakers, J., and Zhang, J. (2015). Dual representations for general multiple stopping problems. Mathematical Finance 25, 339–370.

- [17] Bender, C., Schweizer, N., and Zhuo, J. (2017). A primal-dual algorithm for BSDEs. Mathematical Finance 27, 866–901.

- [18] Bender, C., Gärtner, C., and Schweizer, N. (2018). Pathwise dynamic programming. Mathematics of Operations Research 43, 965–995.

- [19] Ben-Tal, A., and Nemirovski, A. (1998). Robust convex optimization. Mathematics of Operations Research 23, 769-805.

- [20] Bertsimas, D., and Brown, D.B. (2009). Constructing uncertainty sets for robust linear optimization. Operations Research 57, 1483–1495.

- [21] Björk, T., and Slinko, I. (2006). Towards a general theory of good-deal bounds. Review of Finance 10, 221–260.

- [22] Broadie, M., and Glasserman, P. (2004). A stochastic mesh method for pricing high-dimensional American options. Journal of Computational Finance 7, 35–72.

- [23] Brown, D.B., Smith, J.E., and Sun, P. (2010). Information relaxations and duality in stochastic dynamic programs. Operations Research 58, 785–801.

- [24] Carmona, R., and Dayanik, S. (2008). Optimal multiple stopping of linear diffusions. Mathematics of Operations Research 33, 446–460.

- [25] Carmona, R., and Touzi, N. (2008). Optimal multiple stopping and valuation of swing options. Mathematical Finance 18, 239–268.

- [26] Carmona, R. (ed.) (2009). Indifference Pricing: Theory and Applications. Princeton University Press, Princeton.

- [27] Carr, P., Geman, H., and Madan, D. (2001). Pricing and hedging in incomplete markets. Journal of Financial Economics 62, 131–167.

- [28] Carriere, J. (1996). Valuation of the early-exercise price for options using simulations and nonparametric regression. Insurance: Mathematics and Economics 19, 19–30.

- [29] Cheng, X., and Riedel, F. (2013). Optimal stopping under ambiguity in continuous time. Mathematics and Financial Economics 7, 29–68.

- [30] Choi, S., Ruszczyński, A., and Zhao, Y. (2011). A multiproduct risk-averse newsvendor with law-invariant coherent measures of risk. Operations Research 59, 346–364.

- [31] Clément, E., Lamberton, D., and Protter, P. (2002). An analysis of a least squares regression method for American option pricing. Finance and Stochastics 6, 449–471.

- [32] Cochrane, J. and Saá-Requejo, J. (2000). Beyond arbitrage: Good-deal asset price bounds in incomplete markets. Journal of Political Economy 108, 79–119.

- [33] Davis, M., and Karatzas, I. (1994). A deterministic approach to optimal stopping. In: Kelly, F.P. (ed.). Probability, Statistics and Optimisation. A Tribute to Peter Whittle. Wiley, Chichester, Wiley Series in Probability and Mathematical Statistics, 455–466.

- [34] Delbaen, F. (2006). The structure of -stable sets and in particular of the set of risk neutral measures. In: Émery, M., and Yor, M. (eds.). In Memoriam Paul-André Meyer. Springer, Berlin, 215–258.

- [35] Delbaen, F., Peng, S., and Rosazza Gianin, E. (2010). Representation of the penalty term of dynamic concave utilities. Finance and Stochastics 14, 449–472.

- [36] Ekren, I., Touzi, N., and Zhang, J. (2014). Optimal stopping under nonlinear expectation. Stochastic Processes and their Applications 124, 3277–3311.

- [37] Ellsberg, D. (1961). Risk, ambiguity and the Savage axioms. Quarterly Journal of Economics 75, 643–669.

- [38] Föllmer, H., and Schied, A. (2002). Convex measures of risk and trading constraints. Finance and Stochastics 6, 429–447.

- [39] Föllmer, H., and Schied, A. (2011). Stochastic Finance. Walter de Gruyter & Co., Berlin.

- [40] Frittelli, M., and Rosazza Gianin, E. (2002). Putting order in risk measures. Journal of Banking & Finance 26, 1473–1486.

- [41] Gilboa, I., and Schmeidler, D. (1989). Maxmin expected utility with non-unique prior. Journal of Mathematical Economics 18, 141–153.

- [42] Glasserman, P. (2004). Monte Carlo Methods in Financial Engineering. Springer-Verlag, New York.

- [43] Hambly, B., Howison, S., and Kluge, T. (2009). Modelling spikes and pricing swing options in electricity markets. Quantitative Finance 9, 937–949.

- [44] Hansen, L., and Jagannathan, R. (1991). Implications of security market data for models of dynamic economies. Journal of Political Economy 99, 225–262.

- [45] Hansen, L., and Sargent, T. (2007). Robustness. Princeton University Press, Princeton.

- [46] Haugh, M., and Kogan, L. (2004). Pricing American options: A duality approach. Operations Research 52, 258–270.

- [47] Huber, P. (1981). Robust Statistics. Wiley, New York.

- [48] Jamshidian, F. (2007). The duality of optimal exercise and domineering claims: A Doob-Meyer decomposition approach to the Snell envelope. Stochastics 79, 27–60.

- [49] Kobylanski, M., Quenez, M.-C., and Rouy-Mironescu, E. (2011). Optimal multiple stopping time problem. Annals of Applied Probability 21, 1365–1399.

- [50] Krätschmer, V., and Schoenmakers, J. (2010). Representations for optimal stopping under dynamic monetary utility functionals. SIAM Journal on Financial Mathematics 1, 811–832.

- [51] Krätschmer, V., Ladkau, M., Laeven, R.J.A., Schoenmakers, J.G.M., and Stadje, M. (2018). Optimal stopping under uncertainty in drift and jump intensity. Mathematics of Operations Research 43, 1177–1209.

- [52] Laeven, R.J.A., and Stadje, M. (2013). Entropy coherent and entropy convex measures of risk. Mathematics of Operations Research 38, 265–293.

- [53] Laeven, R.J.A., and Stadje, M. (2014). Robust portfolio choice and indifference valuation. Mathematics of Operations Research 39, 1109–1141.

- [54] Lesnevski, V., Nelson, B. and Staum, J. (2007). Simulation of coherent risk measures based on generalized scenarios. Management Science 53, 1756–1769.

- [55] Longstaff, F., and Schwartz, E. (2001). Valuing American options by simulation: A simple least-squares approach. Review of Financial Studies 14, 113–147.

- [56] Lucia, J.J., and Schwartz, E.S. (2002). Electricity prices and power derivatives: Evidence from the Nordic power exchange. Review of Derivatives Research 5, 5–50.

- [57] Matoussi, A., Piozin, L., and Possamaï, D. (2014). Second-order BSDEs with general reflection and game options under uncertainty. Stochastic Processes and their Applications 124, 2281–2321.

- [58] Matoussi, A., Possamaï, D., and Zhou, C. (2013). Second order reflected backward stochastic differential equations. The Annals of Applied Probability 23, 2420–2457.

- [59] Nutz, M., and Zhang, J. (2015). Optimal stopping under adverse nonlinear expectation and related games. The Annals of Applied Probability 25, 2503–2534.

- [60] Øksendal, B., Sulem, A., and Zhang, T. (2014). Singular control and optimal stopping of SPDEs, and backward SPDEs with reflection. Mathematics of Operations Research 39, 464–486.

- [61] Peng, S. (1997). Backward SDE and related -expectations. In: El Karoui, N., and Mazliak, L. (eds.). Backward Stochastic Differential Equations. Pitman Res. Notes Math. Ser. Vol. 364, Longman, Harlow, 141–159.

- [62] Peng, S. (2004). Nonlinear Expectations, Nonlinear Evaluations and Risk Measures. Vol. 1856 of Lecture Notes in Mathematics. Springer, Berlin.

- [63] Philpott, A., de Matos, V., and Finardi, E. (2013). On solving multistage stochastic programs with coherent risk measures. Operations Research 61, 957–970.

- [64] Riedel, F. (2009). Optimal stopping with multiple priors. Econometrica 77, 857–908.

- [65] Riedel, F. (2004). Dynamic coherent risk measures. Stochastic processes and their Applications 112, 185–200.

- [66] Rogers, L.C.G. (2002). Monte Carlo valuation of American options. Mathematical Finance 12, 271–286.

- [67] Rogers, L.C.G. (2010). Dual valuation and hedging of Bermudan options. SIAM Journal on Financial Mathematics 1, 604–608.

- [68] Ruszczyński, A., and Shapiro, A. (2006). Optimization of convex risk functions. Mathematics of Operations Research 31, 433–452.

- [69] Ruszczyński, A., and Shapiro, A. (2006). Conditional risk mappings. Mathematics of Operations Research 31, 544–561.

- [70] Ruszczyński, A. (2010). Risk-averse dynamic programming for Markov decision processes. Mathematical Programming Series B 125, 235–261.

- [71] Savage, L.J. (1954). The Foundations of Statistics. Wiley, New York (2nd ed. 1972, Dover, New York).

- [72] Schoenmakers, J. (2012). A pure martingale dual for multiple stopping. Finance and Stochastics 16, 319–334.

- [73] Schoenmakers, J., Zhang, J., and Huang, J. (2013). Optimal dual martingales, their analysis and application to new algorithms for Bermudan products. SIAM Journal on Financial Mathematics 4, 86–116.

- [74] Shapiro, A., Dentcheva, D. and Ruszczyński, A. (2009). Lectures on Stochastic Programming: Modeling and Theory. SIAM, Philadelphia.