When to sell an asset amid anxiety about drawdowns

Abstract

We consider risk averse investors with different levels of anxiety about asset price drawdowns. The latter is defined as the distance of the current price away from its best performance since inception. These drawdowns can increase either continuously or by jumps, and will contribute towards the investor’s overall impatience when breaching the investor’s private tolerance level. We investigate the unusual reactions of investors when aiming to sell an asset under such adverse market conditions. Mathematically, we study the optimal stopping of the utility of an asset sale with a random discounting that captures the investor’s overall impatience. The random discounting is given by the cumulative amount of time spent by the drawdowns in an undesirable high region, fine tuned by the investor’s personal tolerance and anxiety about drawdowns. We prove that in addition to the traditional take-profit sales, the real-life employed stop-loss orders and trailing stops may become part of the optimal selling strategy, depending on different personal characteristics. This paper thus provides insights on the effect of anxiety and its distinction with traditional risk aversion on decision making.

keywords:

[class=MSC]keywords:

math.PR/00000000 \startlocaldefs \endlocaldefs

t3Corresponding author.

1 Introduction

There are many economic, financial and psychological (behavioural) reasons that drive investors to panic when their asset prices experience a relatively large fall or have a relatively low value for a significant amount of time. This often results in the assets being sold at a lower than anticipated price. A common scenario, that leads investors to such decisions, is financial markets acting contrary to an investor’s expectation for a lot longer than their investment capital can hold out. Another scenario is when asset prices remain at low levels, supervisors of traders grow impatient and ask “How much longer do we have to carry this trade before it profits?”. One can also consider the case of Commodity Trading Advisors who determine various rules for the magnitude and duration of their client accounts’ drawdowns. These can be accounts that are shut down either when certain drawdowns are breached or after small long-lasting drawdowns (see, e.g. [4] for more details). In all these examples, investors are driven to liquidate assets at undesirable low prices.

This phenomenon of “selling low” is also evident in financial markets through the extensive use of traditional stop-loss and trailing stop orders placed by investors. Stop-loss orders are usually placed to minimise risks associated with trading accounts, to bound losses or to protect profits, and they have a fixed value.111See [10] for a recent empirical study stressing the importance of stop-loss orders and their usefulness for reducing investors’ disposition effect. Trailing stops serve a similar purpose, but contrary to stop-loss orders, they automatically follow price movements, e.g. the asset’s best historical performance. Even though such strategies sell a “losing” investment without guaranteeing that this is better than holding onto the assets, they are frequently used in practice mainly due to investors’ anxiety of incurring further losses. Besides their aforementioned purpose, placing trailing stop orders has the additional benefit of allowing investors to focus on multiple open positions at the same time, thanks to their special self-adjustment feature (see [11] for a study of trailing stop strategies, their optimal value, duration and distribution of gains). Recently, the use of these strategies was also studied in various mathematical frameworks. For instance, the optimal combination of an up-crossing target price and a stop-loss, chosen from a specific given set, was studied in [36] under a switching geometric Brownian motion model. An investigation in [17] under a drifted Brownian motion showed that the possibility of a negative drift also suggests the use of combinations of such strategies. Moreover, buying and selling strategies with exogenous trailing stops were considered in conjunction with take-profit orders in [22] under diffusion models. In practice, such stop-loss and trailing stop orders are available for use on stock, option and futures exchanges.

Although trailing stops and stop-loss orders have been widely used, there is no quantitative model that can explain the rationale behind such practices. In all aforementioned studies [36, 17, 22, 37], the use of trailing stops is exogenously imposed. On the other hand, Russian options and their extensions (see e.g. [34]) involve the use of trailing stops, but as in regret theory, their objective is to protect against drawdowns, and is not concerned about the utility realised from an asset sale. The purpose of this paper is thus to provide a framework that rationalises the use of these types of orders from the perspective of selling an asset. In particular, we neither impose any exogenous hard constraints on the set of selling strategies, nor do we have a reward that involves the running maximum of the asset’s price. In such case, a traditional take-profit sale is usually optimal. However, we demonstrate in the present paper that, the use of stop-loss and trailing stop strategies naturally arises from the growing “anxiety” of the investor, as the asset price’s performance remains at undesirable levels. A decision making process affected by (asset price) path-dependence can also be found, via the so-called history-dependent risk aversion models, in [7] and references therein. Contrary to our work, the path-dependence affects directly the risk aversion in these models, e.g. it is incorporated in a state-dependent risk aversion coefficient of utility functions as in (1.4). Our model can be seen as an expansion of this class of path-dependent risk aversion studies in the novel direction that we rigorously present in the sequel.

To fix ideas, consider a financial market with a risky asset whose price process is modelled by a spectrally negative Lévy process on a filtered probability space . Empirical evidence suggests that such a financial market model, allowing for negative asset price jumps, is appropriate in various settings, such as equity, fixed income and credit risk (see [3] and [26] among others). In order to model the aforementioned anxiety of investors, consider also the best performance of the asset , where is the running maximum process associated with , given by . Namely, the best performance until time is the maximum between the highest price of the asset during the time interval and the constant . The latter represents the “starting maximum” of the asset price and can be interpreted as the highest asset price over some previous time period , for some .

We model the driving concern of investors with an “impatience” clock, when the asset price remains at relatively low levels for a significant amount of time. Specifically, for any fixed constant , we construct an (impatience) Omega clock, which measures the amount of time that is below its running maximum by a pre-specified level :

| (1.1) |

In other words, it measures the amount of time that the drawdowns of the logarithm of the asset price , away from its best performance , exceed a tolerance level . The extent of the investors’ impatience is tuned by the value of the anxiety rate . Then, the investor is faced with a random penalisation in the form of discounting driven by (1.1). Under the aforementioned impatience mechanism, the investor is looking for the optimal selling strategy in order to maximise the utility from selling the asset at time . Mathematically, the investor aims at solving the following optimal stopping problem:

| (1.2) |

where is the set of all -stopping times , is the increasing process

| (1.3) |

with being the investor’s original discount rate and is either a constant relative risk aversion (CRRA) or a risk-neutral utility function. Specifically, by fixing a relative risk aversion coefficient , we define , for , by

| (1.4) |

Note that, when , by scaling we also obtain the revenue from selling the asset with price net of the transaction cost .

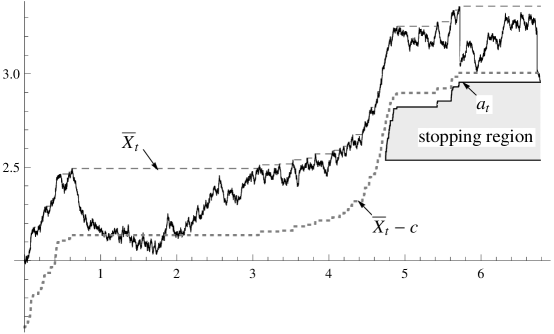

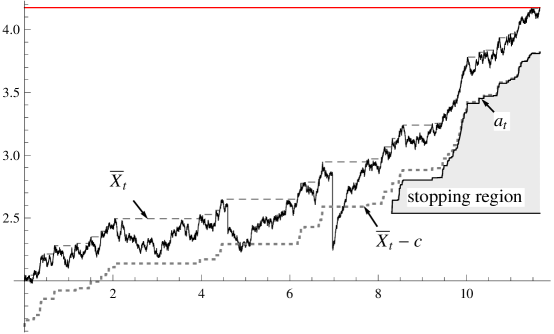

Intuitively, a large anxiety rate implies a strong penalisation of each unit of time, that the asset price’s drawdown breaches the investor’s tolerance level . This will naturally demand selling the asset sooner, and in some occasions, this sale may even happen with a loss, if its price does not go up quickly. Indeed, our analysis captures this phenomenon by proving that traditional stop-loss type strategies are optimal either when investors have a high tolerance level for drawdowns, but severe anxiety when these asset price drawdowns occur, see Theorem 2.4 (also Figure 3); or when investors have severe anxiety and a low drawdown tolerance, see Theorem 2.6 (also Figures 4). Furthermore, in the latter class of investors with severe anxiety even about small drawdowns, we prove that trailing stop type strategies also become part of the optimal strategy, see Theorem 2.6 (also Figures 4–6). Overall, through the study of problem (1.2), this paper manages to answer the following (qualitative and quantitative) question: “what are the individual tolerance and anxiety characteristics of an investor that may result in an optimal use of trailing stop and stop-loss type strategies?”. Our results on the optimal selling strategy are robust with respect to the choice of utility function. Their qualitative nature remains the same and they only change quantitatively when tuning the risk aversion coefficient . On the other hand, irrespective of the risk aversion of investors, the absence of severe anxiety always produces take-profit selling strategies (see Section 2.1). Thus, our novel results are mainly driven by anxiety, a risk factor which is not captured by traditional risk aversion.

Drawdown is widely used as a path-dependent risk indicator (see, e.g. [37]) and has been often used as a constraint for portfolio optimisation. The growth optimal portfolio under exogenous drawdown constraints is explicitly constructed for diffusion models in [12, 5]. Their strategy entails continuous buying and selling of risky assets, in order to meet the hard constraint on drawdowns. In particular, the portfolio will be 100% invested in the risk-free asset once the drawdown reaches their pre-specified tolerance level. In contrast, our framework only imposes a soft drawdown constraint, in that breaching the investor’s drawdown tolerance does not automatically trigger a sale of the risky asset. Additionally, our investment is irreversible and indivisible, thus the investor’s objective is to find the optimal timing of a sale instead of the continuous rebalancing of the holding position.

The irreversible sale of a real asset which is indivisible, at a time chosen by the investor, is a classical topic in the optimal stopping literature. Optimal timing of an asset sale such that an expected utility is maximised was studied in [14] under an exponential utility and in [15] under a CRRA utility (see also [16]) in a diffusion framework. The problem under a risk neutral utility, which is simply given by the revenue from the sale, namely the value of the asset net of the transaction cost at the selling time , was studied in [27] in a general Lévy model.222See also [30, Example 3.5] for a specific geometric Lévy process and [29, Example 10.2.2] for a geometric Brownian motion The optimal sale of an asset under a utility given by the asset price scaled by its running maximum was studied in [8] in a geometric Brownian motion model. All aforementioned studies are performed either with a constant discount rate or without discounting. The study of the above optimal stopping problem with a random (stochastic path-dependent) discount rate and exponential Lévy asset price models was developed in [35]. There, a risk neutral utility was considered, in a simplified version of the problem formulated in (1.2), namely

| (1.5) |

where instead of the original Omega clock (1.1), a “level Omega clock” was used to define , given by the occupation time

| (1.6) |

This “level Omega clock” measures the amount of time when is below this fixed pre-specified level . Above, is the expectation under , which is the law of given that . A European-type equivalent to the problem (1.5) was considered under a risk-neutral utility by [23] under a geometric Brownian motion model, which he named a step option. The American version of this option under the same model and utility and a finite maturity time was recently considered by [6].

Part of our analysis builds on the results obtained in Theorems 4.2 and 4.3 for the problem (1.5), which generalises [35, Theorems 2.4 and 2.5] to the class of CRRA utility functions. To be more precise, we show that the original optimal stopping problem (1.2) reduces to its simplified version (1.5) for specific ranges of parameter values and certain levels of asset price best performance. However, our problem (1.2) is two-dimensional with state space process , which makes the rest of the analysis significantly harder. In particular, the optimal exercise boundaries will be proved to be the first entry times of the first component process in intervals with boundaries, which are functions of the second component process . We manage to obtain analytical solutions in all possible cases. This is achieved via a guess-and-verify approach, as well as the complete characterisation of the solution to a highly non-linear ordinary differential equation. In mathematical terms, this paper contributes to the literature of explicitly solvable two-dimensional optimal stopping problems in Lévy models (see [20], [21], [31] among others).

The remaining paper is structured as follows. In Section 2, we present preliminaries for spectrally negative Lévy models and standing assumptions. We introduce the concepts of mild and severe anxiety in Section 2.1 and then present our main results and economic insights in Section 2.2: Theorem 2.2 (investors with mild anxiety), Theorem 2.4 and Theorem 2.6 (investors with severe anxiety). Figures 2, 3 and 4 respectively illustrate numerically the optimal strategies when the log price is given by a compound Poisson jump process plus a Brownian motion with drift. We also simulate our results in Figures 5 and 6, which demonstrate two possible scenarios faced by an investor with severe anxiety and a small drawdown tolerance. The remaining sections are devoted to proving the main results. In particular, we bound the value function (1.2) from above and below in Section 3 and show its connection with the simpler version of the problem (1.5). In Section 4, we fully solve the problem (1.5) and completely characterise all optimal strategies. Then, we prove the main results of this paper in Section 5. Some useful facts on scale functions of spectrally negative Lévy processes are reviewed in Appendix A.

2 Model and main results

We consider a filtered probability space on which we define the logarithm of the asset price (log price) to be a spectrally negative Lévy process. Here is the augmented natural filtration of . We denote by the Lévy triplet of , and by its Laplace exponent, i.e.

for every . Here, the Lévy measure is supported on satisfying , is atom-less and has a (weakly) monotone density , i.e. is non-increasing in and

This condition is weaker than the standard one of the tail measure either having a completely monotone density or being log-convex. Examples of processes that satisfy the condition include spectrally negative -stable process, spectrally negative CGMY model and spectrally negative hyper-exponential model.

We assume that the discount rate , which is equivalent to the discounted asset price being a super-martingale. For any given , the equation has at least one positive solution, and we denote the largest one by . Notice that implies that . Finally, the -scale function is a function vanishing on , continuous on , with a Laplace transform given by

We assume that for all , which is guaranteed if (see e.g. [18, Theorem 3.10]).333However, is not a necessary condition for . For instance, a spectrally negative -stable process with satisfies this condition without a Gaussian component. The -scale function is closely related to the first passage times of the spectrally negative Lévy process , which are defined by 444Notice also that the assumption implies

In Appendix A we list a handful of useful properties and identities of -scale functions.

2.1 Two degrees of anxiety

As seen in [35], the optimal selling strategy, for problem (1.5) with a risk neutral utility, is largely affected by the investor’s own anxiety rate . To extend the arguments there to a general CRRA utility and eventually to our objective (1.2), we introduce the concept of mild anxiety and severe anxiety, after conducting some preliminary analysis of problem (1.5).

We focus on the case of , because the corner case of logarithmic utility can be obtained from the isoelastic utility in the limit .

Our preliminary approach is inspired by the optimality of threshold type strategies [25]. We first consider the benchmark case of no anxiety, i.e. . In this case, we always discount at rate . Given that

| (2.1) |

is strictly increasing over , we know from [25, Theorem 2.2] (see also footnote 4) that problem (1.5) is solved by a take-profit (up-crossing) selling strategy when the log price reaches the target

With anxiety, i.e. , we consider the function given by

| (2.2) |

where is defined by

| (2.3) |

The function is continuous everywhere with one possible discontinuity at 0. It is known from [35, Lemma 4.2] that is strictly decreasing over , with limits and . Moreover, following similar analysis to [35], we know that is strictly increasing over with a lower limit , and is ultimately increasing over for sufficiently large, with an upper limit . Thus, one can unambiguously define (the largest local minimum of )

Notably, constant is either non-negative, or .

In case , the function is non-decreasing over , so for any fixed , the mapping

| (2.4) |

is also non-decreasing. By [25, Theorem 2.2] and Lemma A.2 (see also footnote 4), we immediately know that (1.5) is also solved by a take-profit selling strategy, regardless of the risk tolerance level . In this case, the selling target log price is given by 555The definition of holds for any value of .

| (2.5) |

Equivalently, is the largest root over , which is simply when , to equation

| (2.6) |

Because of the qualitative similarity of this type of optimal strategy with that under no anxiety (i.e. ), we henceforth refer to the case of as the case of mild anxiety.

The remaining case, when , is referred to as the case of severe anxiety. In this case, contrary to the previous mild one, an investor may choose an additional stop-loss type strategy to “cut the loss” depending on the risk tolerance level , which is a phenomenon already documented in [35] under a risk neutral utility 666We shall see that such distinction still exists for our generalised problem (1.5) (see Section 4) and our main objective (1.2) (see main results in Section 2.2 below).. Furthermore, the representation of candidate threshold as the largest root to (2.6) does not always hold under severe anxiety. Specifically, only if

| (2.7) |

can we identify as the largest root over to (2.6). If , of (2.5) is simply equal to .

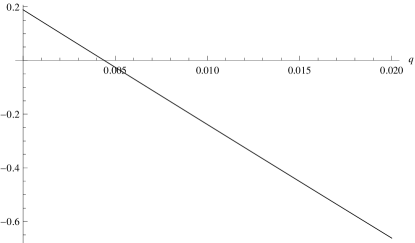

We close this subsection by providing a convenient criterion that distinguishes severe from mild anxiety: when the tail jump measure of the Lévy process, denoted by (for ), either has a completely monotone density or is log-convex, then following similar arguments as in [35, Lemma 2.6], one can show that

| (2.8) |

Figure 1 plots as a function of , illustrating the relationship between mild anxiety () and small , as well as severe anxiety () and large .

2.2 Main results

In this section we present our main result, the value function and the optimal selling strategy for problem (1.2), when the investor has either mild (i.e. ) or severe (i.e. ) anxiety.

To begin, we note that the optimal stopping of reward with a constant discounting rate , is solved by a take-profit selling strategy with target log price

| (2.9) |

and the value function is given by

| (2.10) |

Function is smooth everywhere off the set , and is continuously differentiable over . These results follow from [25, Theorem 2.2] together with the increasing property of mapping (2.1) as we replace discount rate by .

Define also the log price threshold

| (2.11) |

By the monotonicity of over , we know that .

2.2.1 Investors with mild anxiety

In the first result of this section, we present the properties of two types of take-profit sale targets from (2.5) or from (2.11), which can be attained either before or after the asset price improves its best performance , respectively.

Lemma 2.1.

The optimality of the above selling strategies is given in the following result and is proved in Section 5.1 via the use of variational inequalities (see the beginning of Section 5) and the results obtained in the subsequent Sections 3 and 4.1.

Theorem 2.2.

Theorem 2.2 asserts that an investor with mild anxiety does not behave so differently from an investor with no anxiety () when facing problem (1.2). The optimal strategy is always given by a take-profit sale. However, observe that the two regions of the value function (2.12), when , are not communicating. The optimal selling target thus depends explicitly on the past, through the asset’s historical best performance at the price . To be more precise:

-

(i)

When the starting maximum log price is lower than the target , the investor should hold onto the asset and sell it once its log price reaches the threshold ;

-

(ii)

When the starting maximum log price is already higher than the target , then the investor is less patient about adverse movements of the asset price, hence lowers the optimal selling target to the log price .

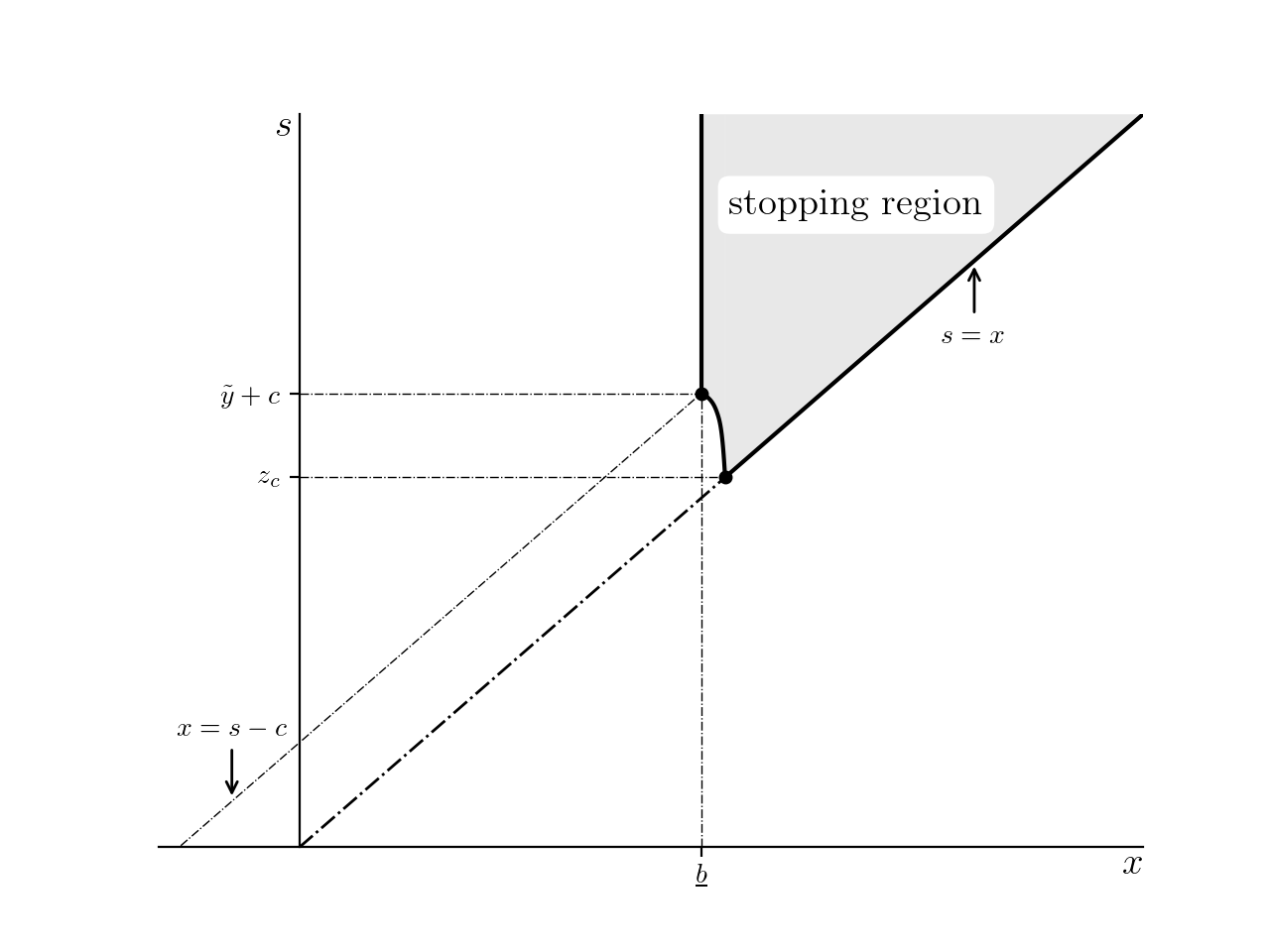

2.2.2 Investors with severe anxiety

In this case, i.e. when , the structure of the optimal selling strategy for problem (1.2) changes as the investor’s tolerance level varies. In order to define the critical regions of -values, we firstly need to specify two values and that are closely related to variational inequalities and martingale methods associated to the optimality of take-profit selling strategies. To formalise the following results, consider the function

| (2.13) |

Following similar analysis to [35], one can show that is continuous and strictly decreasing over , and satisfies . Thus, we can define

| (2.14) |

Moreover, we define another critical log price threshold , given by

| (2.15) |

In the following lemma, we present the properties of three types of take-profit sale targets. On the one hand, from (2.11) that can be attained after the asset price improves its best performance . On the other hand, from (2.5) or the novel , which is also associated with a stop-loss type sale target , that can be attained before the asset price improves its best performance .

Lemma 2.3.

If , then

-

(i).

the function of (2.5) is continuous and strictly decreasing over ;

-

(ii).

we have and ;

-

(iii).

by defining the positive 777Positivity of is due to . constant

(2.16) we have for all that .

-

(iv).

for any , let be defined as

(2.17) where is the negative set of the function indexed by :

(2.18) with given in (A.3). Then and are respectively strictly increasing/decreasing continuous functions on , and satisfy

(2.19)

We differentiate investors with severe anxiety into two types: the ones with a high and the others with a low tolerance for asset price drawdowns, based on whether the investor’s drawdown tolerance level or not. Here is the constant defined in (2.16).

The optimality of the above selling strategies for the former class of investors is given in the following result. This is proved in Section 5.2 via the use of variational inequalities (see the beginning of Section 5) and the results obtained in the subsequent Sections 3 and 4.2.

Theorem 2.4.

The difference in the degree of investor’s anxiety in Theorems 2.2 and 2.4 results in the optimal strategies having different structures when .

-

(i)

If the initial maximum log price is strictly lower than , then it is optimal to hold onto the asset and sell it once its log price reaches threshold . In this case, the investor essentially behaves in the same way as an investor with mild anxiety.

-

(ii)

If the best performance of the asset is higher than , the investor with severe anxiety may need to complement the take-profit sale with an additional stop-loss type sale to “cut the loss”.

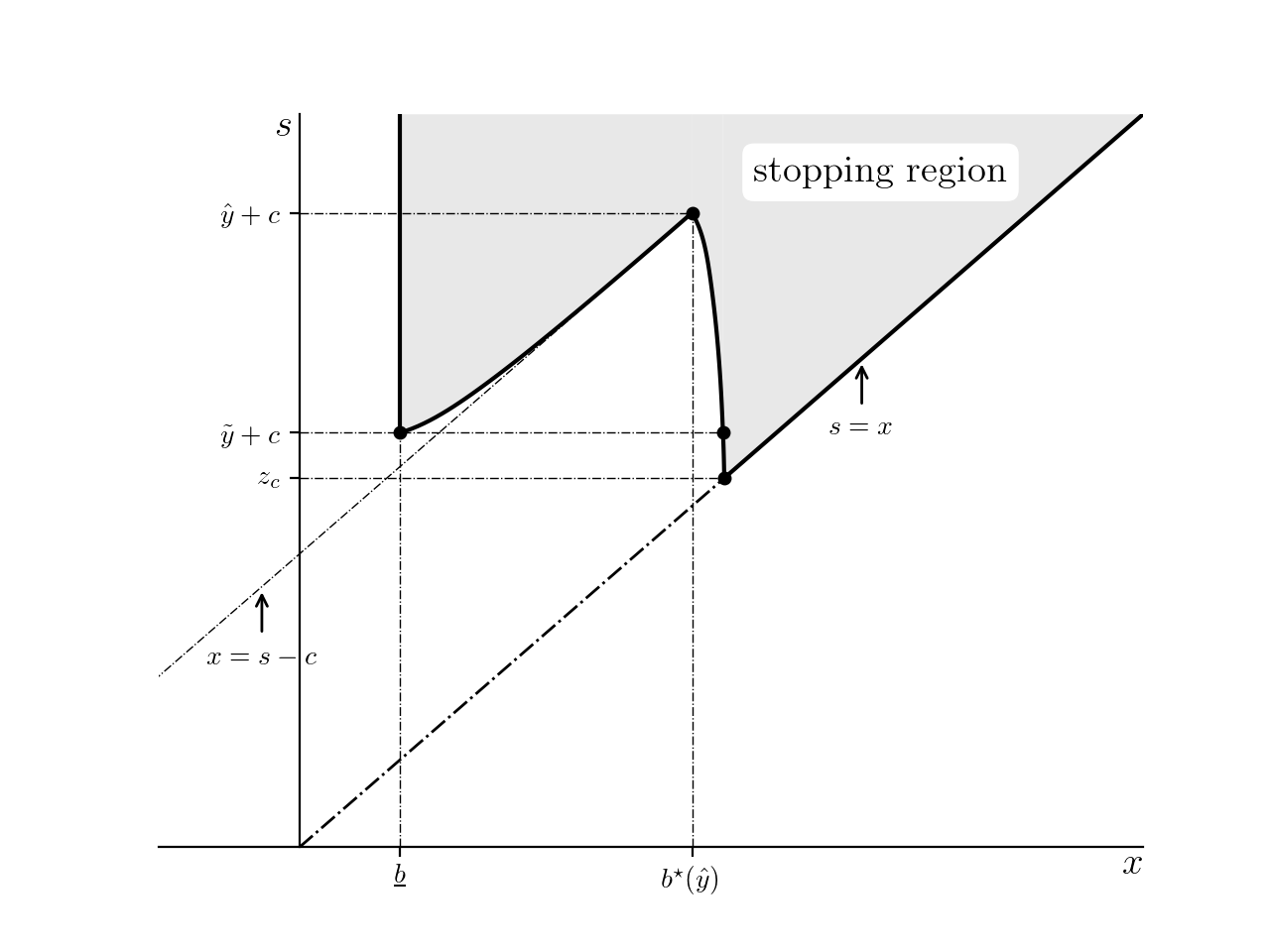

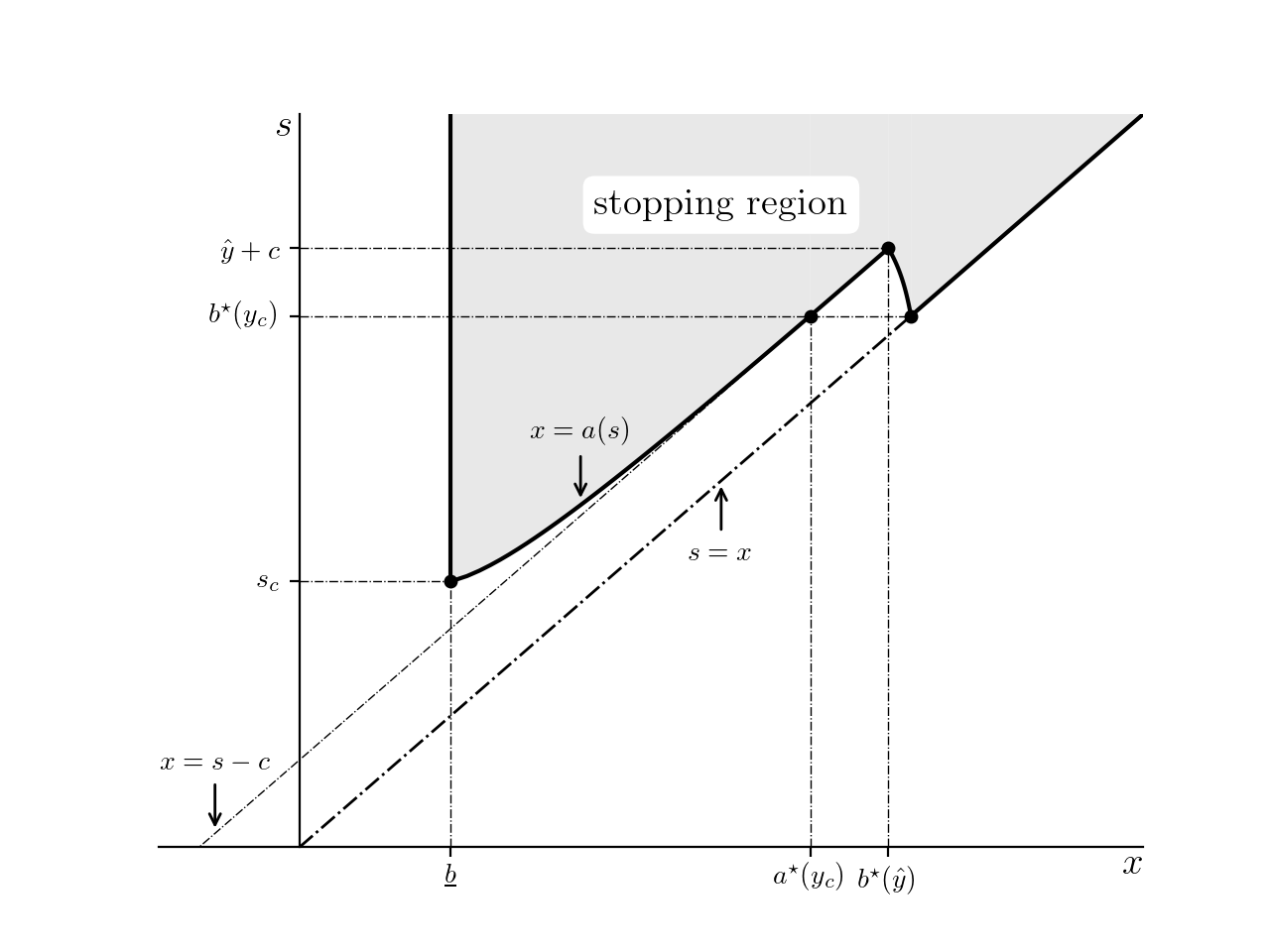

Finally, we treat the type of investors with severe anxiety, who are concerned also about asset price drawdowns with size smaller than . By fixing a , and using the continuity, monotonicity of over , and its limits in (2.19), we may define a threshold as the unique root over to equation

| (2.21) |

By construction we know that . We shall see that the optimal selling strategy involves a combination of the take-profit sale at the target log price , in conjunction with a trailing-stop type sale, with the barrier given by the solution to a first order non-linear ordinary differential equation (ODE). We provide the complete characterisation of this solution in the following lemma.

Lemma 2.5.

The optimality of the selling strategies presented in Lemma 2.3 together with the aforementioned trailing stop type sale target, is given below for this class of investors. This is proved in Section 5.2 via the use of variational inequalities (see the beginning of Section 5) and the results obtained in the subsequent Sections 3 and 4.2.

Theorem 2.6.

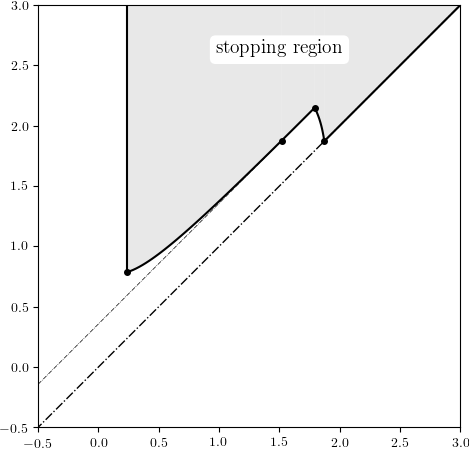

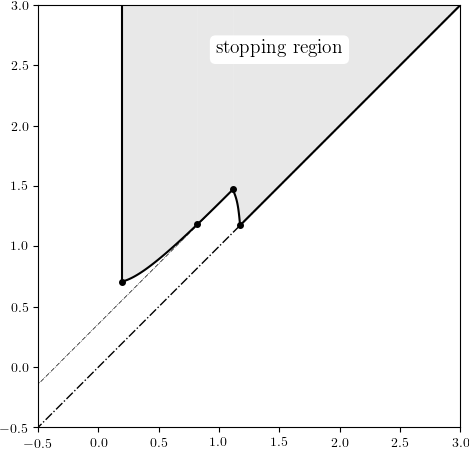

Contrary to Theorems 2.2 and 2.4, we observe that the regions of the value function communicate in Theorem 2.6. If an investor with severe anxiety has a low tolerance for drawdowns, then the optimal selling strategy may involve some holding period of no trade, and some period when a fixed take-profit target is set up together with a sequence of protective, adaptive stop-loss orders. To be more precise:

-

(i)

When the starting maximum log price is lower than , the investor should hold onto the asset until its log price reaches (no trade region).

-

(ii)

If the maximum log price is at least , but lower than , the investor should set up a take-profit target log price , while also consider to (optimally) sell the asset when the log price jumps down to the interval . The latter strategy is precisely a generalised trailing stop, where the stochastic floor increases along with the running maximum (see also [22]).

-

(iii)

If the trailing stop order is not activated as continuously increases towards the take-profit target log price , it will be optimal to sell the asset once reaches .

-

(iv)

As an independent case, not communicating with the aforementioned ones (i)–(iii), when the starting maximum log price is higher than , we obtain similar economic insights as in the severe anxiety with high drawdown tolerance, since the optimal selling strategy is realised either at a traditional take-profit sale, before a new maximum is established, or at a stop-loss type order.

Remark 2.7.

It is worth mentioning that, when setting a trailing stop type order, there is a possibility that the asset log price jumps downwards from the interval to the interval . In this case, we proved that it is optimal for the investor not to sell the asset, but rather be patient by waiting until to sell (this is also true for all aforementioned cases under severe anxiety that require the use of a stop-loss type strategy). This reflects the additional protection sought by investors in financial markets through a trailing stop (resp., stop-loss) with a limit. The purpose is to secure a price only when the asset price experiences a drawdown from its peak that crosses the trailing stop (resp., stop-loss) threshold but not the limit. We can further interpret this result as missing out on selling the asset after a relatively big price jump, since the asset has already lost enough value that it “costs” nothing to wait for some more time until the log price recovers to .

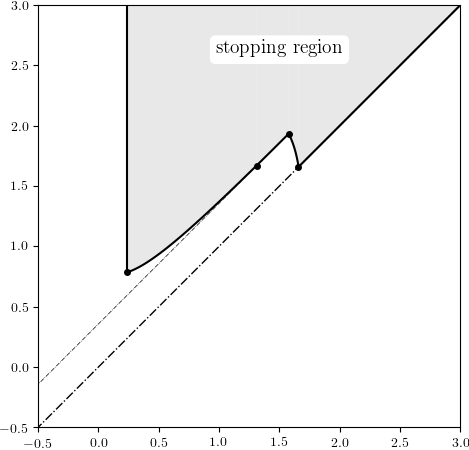

In order to illustrate the optimal selling strategy proposed in Theorem 2.6, we present two numerical case studies for identical assets: In Figure 5, the asset is optimally sold at time at the trailing stop threshold , protecting some of the “profits” from holding this asset, whose value rose significantly from the initial log price ; in Figure 6, the trailing stop is never activated (even though it is set up at some point), so the investor sells the asset at the take-profit threshold .

Remark 2.8.

We comment here that the rationale behind the consideration of the ODE (2.22) is the imposition of Neumann condition on the value of the optimal selling strategy at the diagonal of the two-dimensional state space. Different from the majority of existing literature on optimal stopping problems involving the maximum process, we do have a boundary condition at for the ODE, which helps us to obtain a unique solution as the candidate down-crossing sell order. When such a boundary condition is not available, an appropriate (unique) candidate must be chosen from the set of infinitely many solutions of the ODE, by relying on various different methods; e.g. using the transversality condition (see [13], [34], among others), or the maximality principle from [32] (see [28] for diffusion models, [21] for Lévy models, among others).

2.3 Comparative statics

Given that the structure of the stopping region is explicitly determined by model parameters via equations of differentiable functions, we know that the optimal stopping boundaries are continuous in and . It is easy to see that the set of optimal selling regions shrinks with the investor’s tolerance level for asset price drawdowns and increases with the anxiety rate about these drawdowns. Namely, when decreases or when increases, investors should become more proactive and (optimally) sell their asset at lower profit-taking and/or higher stop-loss/trailing stop targets. These results can also be proved independently of the theory developed in Section 2.2, directly via the expression of the value function in (1.2). In particular, the result for is given in Proposition 3.1 in Section 3.1 below, while one can similarly prove the monotonicity with respect to from (1.3) and (1.1), by observing that is non-decreasing.888Here, we used the notation to stress the dependence of the Omega clock on the parameter .

We can further prove that the set of optimal selling strategies for investors with mild anxiety (cf. Theorem 2.2 in Section 2.2.1) is strictly increasing with the investors’ risk aversion coefficient . In particular, we prove in Lemma B.1 that the mappings , and are all strictly decreasing, whenever they are defined (cf. Section 2.2).999Here, we used the notation , and to stress the dependence of these take-profit selling targets on the parameter . Therefore, more risk averse investors should be more proactive and (optimally) sell their asset at lower profit-taking targets.

Our analytical results in Section 2.2 allow also for a numerical study of comparative statics with respect to general model parameter configurations, including cases of severe anxiety. To set up a numerical study for comparative statics of the risk-aversion coefficient , volatility and jump distribution intensity , we consider an asset with log price process given by a compound Poisson jump process plus a Brownian motion with drift. Namely, we consider an asset price model with Laplace exponent

| (2.24) |

within seven model parameter configurations, as shown in Table 1 below.

| Configuration | ||||||

|---|---|---|---|---|---|---|

| Benchmark | 0.2 | 4 | 0.18 | 1 | 0.25 | 0.3568 |

| Smaller | 0.2 | 4 | 0.18 | 1 | 0.3568 | |

| Larger | 0.2 | 4 | 0.18 | 1 | 0.3568 | |

| Smaller | 4 | 0.18 | 1 | 0.25 | 0.3568 | |

| Larger | 4 | 0.18 | 1 | 0.25 | 0.3568 | |

| Smaller | 0.2 | 0.18 | 1 | 0.25 | 0.3568 | |

| Larger | 0.2 | 0.18 | 1 | 0.25 | 0.3568 |

| Configuration | ||||

|---|---|---|---|---|

| Benchmark | 0.2277 | 1.2793 | 0.7331 | 1.5593 |

| Smaller | 0.2349 | 1.8713 | 0.7851 | 2.1489 |

| Larger | 0.2211 | 1.0160 | 0.6966 | 1.3012 |

| Smaller | 0.1792 | 1.1204 | 0.6950 | 1.4358 |

| Larger | 0.2987 | 1.5807 | 0.7964 | 1.8416 |

| Smaller | 0.2221 | 0.8555 | 0.6788 | 1.2123 |

| Larger | 0.2341 | 1.6568 | 0.7838 | 1.9333 |

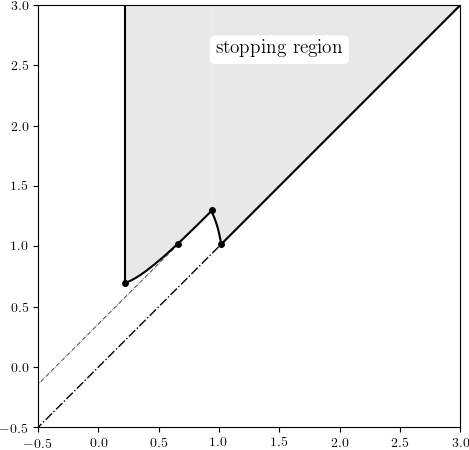

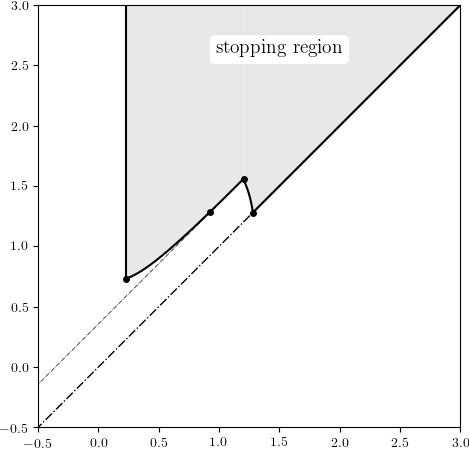

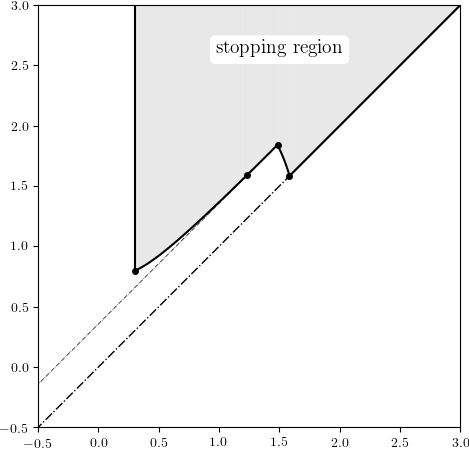

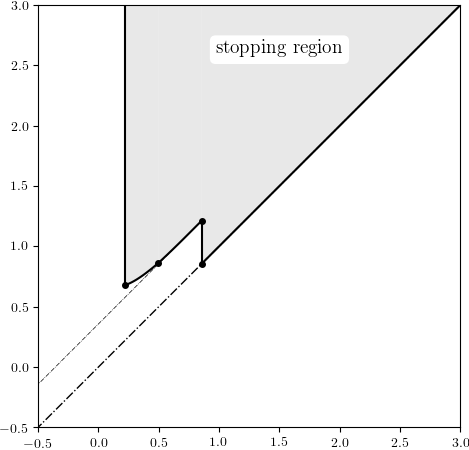

We illustrate in Figure 7 the optimal stopping regions for investors with severe anxiety and low drawdown tolerance (cf. Theorem 2.6), when perturbing their risk aversion coefficient , the log price’s volatility , or the intensity of the jumps’ exponential distribution according to the configurations in Table 1. The key selling thresholds for each case are also shown in Table 2 complementing the illustrations in Figure 7.

One can observe from Figure 7 and Table 2 that: the set of selling strategies appears to grow (resp., shrink) with respect to (resp., and ) also in the case of severe anxiety; the changes in the trailing stop , stop-loss and take-profit targets, whenever they exist for each fixed , are relatively minor under all parameters examined, compared to the resulting changes in the take-profit target , which are much more significant. In summary,

-

1.

for both degrees of anxiety, the more risk averse investors tend to be more proactive and (optimally) sell their asset at lower profit-taking and/or higher stop-loss (or trailing stop) targets.

-

2.

in cases of severe anxiety, the more volatile the asset price, the longer investors wait before (optimally) selling their asset, as it is widely understood that options tend to gain value when volatility increases;

-

3.

in cases of severe anxiety, the higher the intensity of the exponential distribution, the smaller the size of negative jumps tends to be, hence the investors wait longer before (optimally) selling their asset.

3 Bounds for the value function

Fixing any tolerance level , we denote by the “stopping region” of log prices. This contains all the states of price and maximum price at which the investor should (optimally) sell the asset. By the general theory of optimal stopping for Markov processes (see, e.g. [33, Ch. I, Sec. 2.2]), we define

As the first step of determining the value function of (1.2), we derive a lower and an upper bound. We also provide bounds for the stopping region , which will be useful in proofs in later sections.

3.1 Lower bound for and upper bound for

For any , it is easily seen from (1.3) and (1.1) that holds for all . Therefore, the value of (1.2) is always bounded from below by , the optimal expected value of utility discounted at rate .

Proposition 3.1.

For any ,

and

Proof.

For any fixed , and any stopping time , we have on the event that, the following inequalities

hold true (-a.s.). Taking expectations 101010Note that the -component is actually redundant when the objective function does not involve the running maximum. and the suprema over all stopping times , we obtain in view of the definition (2.10) of that

The bound for follows immediately. ∎

3.2 Upper bound for and lower bound for

Consider the value function of (1.5), i.e. optimal expected value of utility with discounting . We define the optimal stopping region of problem (1.5), (see, e.g. [33, Ch. I, Sec. 2.2]) by

| (3.2) |

Problem (1.5) can be considered as a simplified version of the original problem (1.2), when the discount factor does not update with the running maximum . Specifically, for any fixed and , the continuous additive functional is almost surely dominated from above by under . Thus, the value function of (1.2) is always bounded from above by the value of (1.5) when .

Proposition 3.2.

Proof.

We only need to prove that the equality in (3.3) holds if and only if . But the latter condition means that it is optimal to stop in problem (1.5) before the asset log price reaches . This is equivalent to the running maximum remaining constant, equal to , in which case the value of the same strategy for problem (1.2) under is the same as . Therefore, the optimal value for problem (1.2) is no less than . This completes the proof. ∎

In the next section, we focus on solving for the upper bound .

4 Cracking problem (1.5) with value function

This section is concerned with the study of problem (1.5), which servers as a cornerstone in the analysis of problem (1.2). Recall that, the case of risk neutral utility has already been treated in [35, Theorem 2.4, Theorem 2.5].

Proposition 4.1.

The value function of (1.5) satisfies the following properties:

-

(i)

is strictly increasing and continuous in over , and is non-increasing and continuous in over ;

-

(ii)

if there exists a constant , then and ;

-

(iii)

the optimal stopping region is a union of disjoint closed intervals and there is at most one component that lies in .

Proof.

For any , we know from

that

Hence, by the dominated convergence theorem, one can repeat the steps used in the proof of [35, Proposition 3.1] to prove and . The claim in the first half of follows from the fact that is continuous in over ; the second half of the claim in can be proved in the same way as in [35, Proposition A.1]. ∎

We recall that, if or and , the candidate up-crossing selling threshold of (2.5), is actually the largest root to (2.6). By the monotone property of we know that is strictly decreasing. Moreover, Proposition 4.1(i) also implies that if for all in some interval with nonempty interior, then is continuous and non-increasing in over . Proposition 4.1(ii)–(iii) imply that there are three possibilities for the stopping region: does not include , or , or for some .

In what follows, we study the problem (1.5) separately in the two cases of mild (i.e. ) and severe (i.e. ) anxiety (see Section 2.1). The following results generalise [35, Theorem 2.4, Theorem 2.5] to the case of risk averse investors.

4.1 Investors with mild anxiety

Theorem 4.2.

Proof.

The expression for has already been proved in the preliminary analysis of Section 2.1, which also implies the form of in view of Lemma A.2. The expression of for follows from equations (2.6) and (2.9), using the fact that for all . Also, Proposition 4.1 and succeeding discussions imply the continuity and non-increasing property of over .

To prove the strictly decreasing property of over , suppose that there exist such that , aiming for a contradiction. Then, we must have for all . However, it is easily seen that

which is a contradiction. Hence, must be strictly decreasing over . ∎

4.2 Investors with severe anxiety

Theorem 4.3.

For an investor with severe anxiety (i.e. ), we have and . The optimal stopping region and the value function for problem (1.5) are given as follows:

-

(a)

if , then , while if , then . The value function is given by (4.1);

- (b)

-

(c)

if , then and .

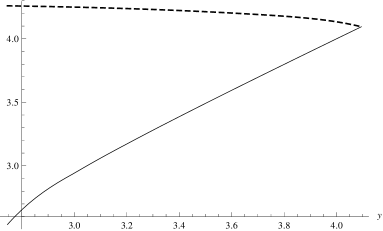

Overall, the function is continuous and strictly increasing over , with and , while the mapping

is continuous and strictly decreasing, with ; (see Figure 8(a) for a plot of and ).

Proof.

Construction of the critical -value from (2.7). In view of equation (2.4), the fact that is a local minimum of and the monotonicity

which follows from being strictly decreasing on (see [35, Lemma 4.2]), we conclude that there exists such that , which is given by the expression (2.7). For any , the value does not identify with a root of (2.6) and a candidate up-crossing threshold for problem (1.5). We thus focus on the values of .

Construction of the critical -value from (2.15). In view of the above, for any fixed , the up-crossing threshold of (2.5) satisfies . By employing the techniques leading to [35, Proposition 4.7] in our setting, we know that the positive function given by (4.1) satisfies:

-

1.

the process is a super-martingale;

-

2.

the process is a martingale;

-

3.

for all and .

Combining these properties with the classical verification method (see, e.g. proofs of theorems in [1, Section 6]), we can establish the optimality of the selling strategy by finally proving that for all , or equivalently

Recall that for all . Since is strictly increasing for , we know that

| (4.3) |

Hence, for all . However, since (2.4) can have more than one solution, (4.3) implies that may not be always increasing over , in which case it admits at least one local maximum in this region. Also, for every fixed and , given that and are both decreasing over and (see [35, Lemma 4.2]), we get

thus the function is strictly increasing over . This yields that the largest local maximum of (which must be in ) is also increasing in and we can define , which is equivalent to the definition (2.15), in view of the expression (4.1) of .

For (and ), since is a local minimum of , we know that for all sufficiently small , we have , so . This implies that for all in a sufficiently small left neighborhood of . Hence, we conclude that .

Proof of part . By the construction of , we know that for any fixed ,

which implies that the selling strategy is optimal for all .

If , we may also conclude that the candidate value function of (4.1) is the true value function. Moreover, by the above properties of , we know that there exists a point satisfying

Essentially, is a second point (other than ) where the value function smoothly touches the reward function . Then for all sufficiently small , will be the optimal up-crossing threshold, so is also a stationary point of and solves . By Proposition 4.1(iii), we may further conclude that , thus

In view of the above, we conclude that there is only one such and with .

Construction of the critical -value from (2.14) and proof of part . In order to show that the value function is given by for all sufficiently large , we adopt the method of proof through variational inequalities (see e.g. [30] or [35, Lemma 4.10] for the same problem under risk neutral utility). Using the explicit expression of in (2.10), one can easily see that from (2.13) for any , where is the infinitesimal generator of . Precisely, for all functions , is given by

Given that for all , we know that defined by (2.14) is the smallest -value such that is super-harmonic with respect to the discount rate . It follows that and for all , which proves part . Since , we may conclude that .

Proof of part . The analysis in part (a), the fact that is increasing in and the above observation (see also (2.14)) that , dictates the consideration of the following pasting points, for all :

| (4.4) |

In fact, using Proposition 4.1(ii), we may conclude that . Hence, for any , we have

| (4.5) |

Using the results from Lemma A.2 and [35, Proposition 4.12], we can rewrite (4.5), using defined in (2.13), as

| (4.6) |

In view of this explicit formula, one can easily see that the mapping is in . By exploiting the optimality of and and similar arguments to the proof of [35, Proposition 4.13], we can show that the smooth fit condition always holds for , while it holds for only when has unbounded variation. Using the above smoothness at the log prices and together with (4.5)–(4.2), we can show that the optimal pair , from (4.4) necessarily solves the following system:

where is given by (2.18). The rest of the proof, including showing that takes the form (4.2) and , from (4.4) are given by (2.17), is identical to the one for [35, Theorem 2.5(iv)], hence is omitted for brevity.

5 Proofs of the main results

In this section, we shall prove that the solution to the problem (1.2), takes the forms presented in Theorems 2.2, 2.4 and 2.6. Our main verification approach is through the Hamilton-Jacobi-Bellman equation. Specifically, suppose that we can find a function in (resp., ) if has paths of unbounded (resp., bounded) variation, for some , such that and is super-harmonic. That is, satisfies the variational inequality

| (5.1) |

with boundary condition

| (5.2) |

Using these properties of together with the Itô-Lévy lemma and the compensation formula, we know that is the value function of the problem (1.2) for this tolerance level .

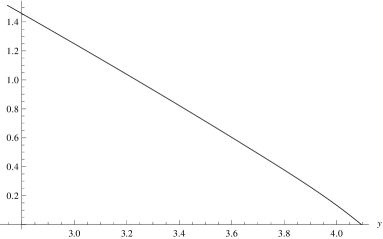

Before we move on to the individual proofs, we define the mapping

| (5.3) |

where and are given by (2.5) and (2.17). From Theorems 4.2 and 4.3, we know that function is strictly decreasing over its domain, with a range equal to . A plot of is shown in Figure 8(b).

5.1 Investors with mild anxiety

Proof of Lemma 2.1.

Proof of Theorem 2.2.

Proof of part for . We know from Theorem 4.2 under the case of , that the optimal stopping region for problem (1.5) is the half-line . On the other hand, Proposition 3.2 asserts that

It is thus natural to consider the critical -value, such that , namely,

| (5.4) |

where is defined by (5.3). By the construction of we know that

In fact, using (2.2) and (2.5), one can obtain an explicit expression for :

| (5.5) |

Therefore, we can define as the -value determined by (5.4), which is given by (2.11). Taking into account the definition and expression of in (2.11), we observe from the monotonicity of in (cf. Theorem 4.2) that

Hence by Proposition 3.2, we know that for any such that , where admits the expression (4.1). The result follows by finally observing that, for all , we have

Proof of part for . For the remaining case, we prove that it is optimal to wait until the process reaches the point , i.e. to sell at . The value of such strategy, denoted by , is given by

| (5.6) | ||||

thanks to the strong Markov property of . Using the Neumann boundary condition , as we expect the process to reflect at the diagonal of the state space until it reaches the point , we obtain from (5.6) that

| (5.7) |

Notice that, the positive function given by the right-hand side of (2.12) is precisely . Then by construction, it is easily seen that the mapping is continuous over , is over for each fixed , and it satisfies the Neumann condition (5.2) for all . In addition, one can show that the Neumann condition also holds at by respectively computing the left and the right derivative with respect to . Hence, it remains to show that solves the variational inequality (5.1) for all .

We first prove that the inequalities involving the infinitesimal generator hold. To this end, we fix and by using the definition of from (5.6) and similar arguments to Section 4 of [2], we know that

| (5.8) |

In order to finish the proof, we show in the sequel that the inequalities involving the dominance of over the intrinsic value hold as well. To that end, for , we define

Taking the partial derivative of with respect to yields that

| (5.9) |

Considering that is strictly increasing over when , together with the fact that and from (2.11) and (5.5), respectively, solve the equation (2.4), we conclude that

It follows that is strictly increasing over , for any fixed . Hence, for all . Furthermore, we notice from the expression (5.7) of that

| (5.10) |

Taking the derivative of the above with respect to and using (2.11) yields that

In view of , which follows straightforwardly from (5.10) for , we thus obtain

which implies that

| (5.11) |

5.2 Investors with severe anxiety

Proof of Lemma 2.3.

Proof of Theorem 2.4.

Construction of from (2.16). Recall from Theorem 4.3, under , that the optimal strategy for the simplified problem (1.5) changes qualitatively when the value is less or greater than the key level . Naturally, one may consider the tolerance level associated with through the definition

| (5.12) |

which is equivalent to the definition in (2.16). By the construction of we know that is uniquely defined and positive.

Proof of part for . Following the same reasoning as in Section 5.1, we consider the critical -value satisfying the properties in (5.4) and thus solving . By the construction of ,

| (5.13) |

However, in this case, we can further conclude from the monotonicity of , the assumption , the definition (5.12) of and the fact that that

Thus, by Theorem 4.3.(a), we can define the critical -value as with given explicitly by (5.5), yielding that is indeed given by (2.11) in this case as well. Moreover, recall from Theorem 4.3.(a) that, the optimal stopping region for problem (1.5) is given by

In both cases, using the monotonicity of in (cf. Theorem 4.3), it is straightforward to see that

Hence, by Proposition 3.2 we know that for any such that , where admits the expressions in Theorem 4.3 for . The result follows by the straightforward observation that the Neumann condition (5.2) holds for all (see e.g. Section 5.1 for similar arguments).

Proof of part for . For the remaining case, we prove that it is optimal to wait until the process reaches the point . Notice that the positive function given by the right-hand side of (2.20) identifies with from (5.6) (see also (5.7)), and the proof follows similar arguments as the ones in the proof for Theorem 2.2. Therefore, the only non-trivial task, before establishing the optimality of , is to prove the dominance of over the intrinsic value . We examine below the ratio for .

When , we know that is non-monotone anymore, hence we cannot draw any conclusions from the partial derivative (5.9) of . To this end, we employ a different technique than in the proof of Theorem 2.2. We begin by noticing that for , we have by (2.11) and (5.5) that , thus

| (5.14) |

Therefore, in light of Theorem 4.3.(a), we have

Then, we take the partial derivative of the expression (5.7) of with respect to , for ,

due to the fact that is strictly decreasing on (cf. [35, Lemma 4.2]). We therefore have

In light of (5.14) and Theorem 4.3.(a) for , we know from the above and (4.1) that

Finally, we comment that the only possibility for is realised when the two inequalities above are equalities. In particular, this can only occur when either , or when and (see Theorem 4.3.(a) for ). ∎

Proof of Lemma 2.5.

The existence and the uniqueness of the solution follow from classical results for nonlinear ODEs. To show the other properties, let , and let be the slope field of (2.22), i.e.

Then satisfies the ordinary differential equation

By equation (A.4), we see that for , which occurs whenever , for some , we get

since by its definition (2.18). Hence, for such values of , we have

| (5.15) |

However, from (2.21) we have , thus we get in this case that . Therefore, the inequality for all (see (2.14)) yields that

| (5.16) |

On the other hand, following the proof of [35, Lemma 4.9] one can show that is decreasing and continuous over , with limit

| (5.17) |

Therefore,

| (5.18) | ||||

where the last equality follows from (5.17). From (5.15), (5.16) and (5.18) we know that

| for all such that , we have . |

Thus, if there exists such that , then for all . However, notice that

which is a contradiction. Therefore, such an cannot exist and the only possibility is , i.e. , as long as and is well-defined.

In the final part of the proof, we use the aforementioned property of , in order to examine the behaviour of when , which also implies that . Then, for any fixed and all ,

Combining all the above with the probabilistic meaning of in Lemma A.1, we conclude that for all , as long as . We now define

Notice that . Thus, from the monotonicity of we know that . We complete the proof by showing that . Arguing by contradiction, we suppose that , which implies that is well-defined at and . However, it follows from the established fact , that , which is indeed a contradiction. ∎

Proof of Theorem 2.6.

Let be the level defined by (2.16).

Proof of part for . By the construction of and the fact that , we conclude that the critical value from (5.13), satisfies

Using the definition (5.3) of , we know that the unique value satisfies (2.21). Recall from Theorem 4.3.(b) that, for , the optimal stopping region for problem (1.5) is given by

| (5.19) |

By the monotonicity of in (cf. Theorem 4.3), we have that,

Hence, by Proposition 3.2 we know that for any such that , where admits the expressions in Theorem 4.3 for . The result follows by the straightforward observation that the Neumann condition (5.2) holds for all (see e.g. Section 5.1 for similar arguments).

Proof of part for . We now focus on the remaining case that . As in Theorems 2.2 and 2.4, we prove that the take-profit selling strategy still constitutes part of the optimal strategy if . However, we shall prove that the optimal selling strategy is also partially given by a trailing stop type order, which requires selling the asset if its log price drops below some moving threshold that depends on the running best performance of the asset log price.

To be more precise, we define the value of the two-sided exit strategy from an interval by the asset log price process , where is such that for a fixed . In view of the equivalent expression in (3.1) of our original problem (1.2), the value of this strategy is given by

| (5.20) |

We now derive a useful renewal equation satisfied by . Since the second component of the process is constant up to time , we know that for all (-a.s.), so we can rewrite (5.20) in the form

Hence, using Lemma A.2 and [35, Proposition 4.12], we conclude that

| (5.21) |

where the non-negative function is defined in (2.18).

Optimality of the trailing stop . We now choose an appropriate threshold that maximises the value of the two-sided selling strategy for each fixed . In order to make it a reasonable candidate for the value function (see also beginning of Section 5), we invoke the principle of continuous (resp., smooth) fit for function when has bounded (resp., unbounded) variation. Specifically:

Continuous fit: If the asset log price process has paths of bounded variation, we start from the point , then by imposing continuous fit at , i.e. in (5.21), and recalling from (2.18) that, for any , we obtain

where we used (A.3) for simplification. Because (cf. Lemma A.3), the above equation is equivalent to

| (5.22) |

Smooth fit: If the asset log price process has paths of unbounded variation, then the fact that (cf. Lemma A.3) guarantees the continuous fit at . However, taking the partial derivative of (5.21) with respect to , we have

Then, Lemma A.3 asserts that , so by imposing smooth fit at , i.e. , we again obtain (5.22).

In both cases, we obtain from (5.21) and (5.22) that the threshold (if it exists) and function satisfy

| (5.23) |

Then by the above construction, it is easily seen that the mapping is continuous over , and is over for each fixed in the unbounded variation case. Also, by straightforward calculations, the function from (5.23) (defined in (5.20)) satisfies the Neumann condition (5.2) if and only if solves the ODE (2.22), where the boundary condition follows from the structure of the optimal selling region (5.19) when . Given that is always part of the continuation region of problem (1.2) (cf. Proposition 3.1), the candidate optimal threshold must satisfy , which is the final condition imposed in Lemma 2.5. Notice that, Lemma 2.5 then implies that the function is strictly increasing and there exists a unique value , such that . The above function is precisely the positive function from the right-hand side of (2.23) for .

Proof of sub-part for . In light of the above, the selling strategy in (5.20) (see also (5.23)) is a candidate only for , while for all , it is optimal to simply wait until the asset log price increases to and then follow the optimal strategy . Thus, the expression of the value function in (2.23) for all follows from similar arguments to the ones leading to (5.6)–(5.7) and their optimality in the proof of Theorem 2.4, as soon as we prove the optimality of for all .

Proof of sub-part for . Therefore, in order to complete the proof, it suffices to show that satisfies the variational inequality (5.1) for all such that .

Firstly, it is seen by construction and the definition (2.18) of , that the inequalities involving the infinitesimal generator can be straightforwardly verified, since

Hence, it remains to show in the sequel that the inequalities involving the dominance of over the intrinsic value hold as well, namely

We know from Lemma 2.5 that

We therefore focus on any fixed , for which we have , where

Using the expression of from (5.23) and the ODE (2.22) solved by , we get

Combining all of the above, we obtain that, for all and ,

where we used (A.1) and (A.2) in the second identity, while the last inequality is due to the facts that

is strictly decreasing and that (see (5.17)) . We therefore see that

| the mapping is strictly decreasing on for any fixed . | (5.24) |

We then argue by contradiction, assuming that there exists a pair for and , such that . We arrive to a contradiction in both scenarios of and . In particular, on one hand, if , then (5.24) yields that

However, combining the above with Theorem 4.3.(b) for , we get the contradiction

On the other hand, if , then we define and use again (5.24) to get the contradiction

where the last inequality follows from Lemma 2.5. In summary we conclude that

which completes the proof.∎

Appendix A Preliminaries on scale functions

A well-known fluctuation identity of spectrally negative Lévy processes (see e.g. [19, Theorem 8.1]) is given, for and , by

| (A.1) |

The following result from [24, Theorem 2] provides a generalization of the above case with deterministic discounting in (A.1) to the case with state-dependent discount rate , for some fixed .

Lemma A.1.

A related result from [35, Proposition 4.1] (see also [24, Corollary 2.(ii)] for the proof of a similar result) will also be useful.

Lemma A.2.

For any , we have

| (A.5) |

Finally, the following lemma gives the behaviour of scale functions at and ; see, e.g., [18, Lemmata 3.1, 3.2, 3.3], and [9, (3.13)].

Lemma A.3.

For any ,

Appendix B Technical results

Lemma B.1.

Proof.

Suppose that . Denote by , and , the selling strategies defined by (2.5), (2.9), under and , respectively.

We can firstly observe from the definitions (2.9) and (2.11) that both and are strictly decreasing in independently of the case under consideration (cf. Section 2.2).

Taking into account (from above) that holds, we can straightforwardly conclude from Theorems 2.2 and 2.4 that for all . In view of the inequalities

we claim that for all . To prove this by contradiction, we assume that there exists such that (this suffices as , is continuous in ). Given that solves (2.6), it follows that

However, firstly note that the function has fixed convexity in . Secondly, for any fixed , observe that is already a solution. Hence, having two more distinct roots is impossible. This is a contradiction. Therefore, we have that for all . Combining the above results, we can conclude that we eventually have for all in their common domain independently of the case under consideration (cf. Theorems 2.2 and 2.4 in Section 2.2). ∎

Acknowledgments

Neofytos Rodosthenous gratefully acknowledges support from EPSRC Grant Number EP/P017193/1.

References

- Alili and Kyprianou [2005] {barticle}[author] \bauthor\bsnmAlili, \bfnmL.\binitsL. and \bauthor\bsnmKyprianou, \bfnmA. E.\binitsA. E. (\byear2005). \btitleSome remarks on first passage of Lévy processes, the American put and pasting principles. \bjournalThe Annals of Applied Probability \bvolume15 \bpages2062–2080. \bdoi10.1214/105051605000000377 \bmrnumberMR2152253 (2006b:60078) \endbibitem

- Biffis and Kyprianou [2010] {barticle}[author] \bauthor\bsnmBiffis, \bfnmEnrico\binitsE. and \bauthor\bsnmKyprianou, \bfnmAndreas E.\binitsA. E. (\byear2010). \btitleA note on scale functions and the time value of ruin for Lévy insurance risk processes. \bjournalInsurance: Math and Economics \bvolume46 \bpages85–91. \bdoi10.1016/j.insmatheco.2009.04.005 \bmrnumber2586158 \endbibitem

- Carr and Wu [2003] {barticle}[author] \bauthor\bsnmCarr, \bfnmPeter\binitsP. and \bauthor\bsnmWu, \bfnmLiuren\binitsL. (\byear2003). \btitleThe finite moment log stable process and option pricing. \bjournalThe Journal of Finance \bvolume58 \bpages753–778. \endbibitem

- Chekhlov, Uryasev and Zabarankin [2005] {barticle}[author] \bauthor\bsnmChekhlov, \bfnmAlexei\binitsA., \bauthor\bsnmUryasev, \bfnmStanislav\binitsS. and \bauthor\bsnmZabarankin, \bfnmMichael\binitsM. (\byear2005). \btitleDrawdown measure in portfolio optimization. \bjournalInternational Journal of Theoretical and Applied Finance \bvolume8 \bpages13–58. \endbibitem

- Cvitanić and Karatzas [1995] {barticle}[author] \bauthor\bsnmCvitanić, \bfnmJ.\binitsJ. and \bauthor\bsnmKaratzas, \bfnmI.\binitsI. (\byear1995). \btitleOn portfolio optimization under drawdown constraints. \bjournalIMA Lecture Notes in Mathematical Applications \bvolume65 \bpages77-78. \endbibitem

- Detemple, Abdou and Moraux [2019] {barticle}[author] \bauthor\bsnmDetemple, \bfnmJerôme\binitsJ., \bauthor\bsnmAbdou, \bfnmSouleymane Laminou\binitsS. L. and \bauthor\bsnmMoraux, \bfnmFranck\binitsF. (\byear2019). \btitleAmerican step options. \bjournalEuropean Journal of Operational Research \bvolume282 \bpages363–385. \endbibitem

- Dillenberger and Rozen [2015] {barticle}[author] \bauthor\bsnmDillenberger, \bfnmD.\binitsD. and \bauthor\bsnmRozen, \bfnmK.\binitsK. (\byear2015). \btitleHistory-dependent risk attitude. \bjournalJournal of Economic Theory \bvolume157 \bpages445–477. \endbibitem

- du Toit and Peskir [2009] {barticle}[author] \bauthor\bparticledu \bsnmToit, \bfnmJ.\binitsJ. and \bauthor\bsnmPeskir, \bfnmG.\binitsG. (\byear2009). \btitleSelling a stock at the ultimate maximum. \bjournalThe Annals of Applied Probability \bvolume19 \bpages983-1014. \endbibitem

- Egami, Leung and Yamazaki [2013] {barticle}[author] \bauthor\bsnmEgami, \bfnmE.\binitsE., \bauthor\bsnmLeung, \bfnmT.\binitsT. and \bauthor\bsnmYamazaki, \bfnmK.\binitsK. (\byear2013). \btitleDefault swap games driven by spectrally negative Lévy processes. \bjournalStochastic Processes and their Applications \bvolume123 \bpages347-384. \bmrnumberMR3003355 \endbibitem

- Fischbacher, Hoffmann and Schudy [2017] {barticle}[author] \bauthor\bsnmFischbacher, \bfnmUrs\binitsU., \bauthor\bsnmHoffmann, \bfnmGerson\binitsG. and \bauthor\bsnmSchudy, \bfnmSimeon\binitsS. (\byear2017). \btitleThe causal effect of stop-loss and take-gain orders on the disposition effect. \bjournalThe Review of Financial Studies \bvolume30 \bpages2110–2129. \endbibitem

- Glynn and Iglehart [1995] {barticle}[author] \bauthor\bsnmGlynn, \bfnmP. W.\binitsP. W. and \bauthor\bsnmIglehart, \bfnmD. L.\binitsD. L. (\byear1995). \btitleTrading securities using trailing stops. \bjournalManagement Science \bvolume41 \bpages1096–1106. \endbibitem

- Grossman and Zhou [1993] {barticle}[author] \bauthor\bsnmGrossman, \bfnmS. J.\binitsS. J. and \bauthor\bsnmZhou, \bfnmZ.\binitsZ. (\byear1993). \btitleOptimal investment strategies for controlling drawdowns. \bjournalMathematical Finance \bvolume3 \bpages241-276. \endbibitem

- Guo and Zervos [2010] {barticle}[author] \bauthor\bsnmGuo, \bfnmXin\binitsX. and \bauthor\bsnmZervos, \bfnmMihail\binitsM. (\byear2010). \btitle options. \bjournalStochastic processes and their applications \bvolume120 \bpages1033–1059. \endbibitem

- Henderson [2007] {barticle}[author] \bauthor\bsnmHenderson, \bfnmV.\binitsV. (\byear2007). \btitleValuing the option to invest in an incomplete market. \bjournalMathematics and Financial Economics \bvolume1 \bpages103–128. \endbibitem

- Henderson and Hobson [2008] {barticle}[author] \bauthor\bsnmHenderson, \bfnmVicky\binitsV. and \bauthor\bsnmHobson, \bfnmDavid\binitsD. (\byear2008). \btitleAn explicit solution for an optimal stopping/optimal control problem which models an asset sale. \bjournalThe Annals of Applied Probability \bvolume18 \bpages1681–1705. \endbibitem

- Henderson, Hobson and Zeng [2018] {barticle}[author] \bauthor\bsnmHenderson, \bfnmVicky\binitsV., \bauthor\bsnmHobson, \bfnmDavid\binitsD. and \bauthor\bsnmZeng, \bfnmMatthew\binitsM. (\byear2018). \btitleCautious Stochastic Choice, Optimal Stopping and Deliberate Randomization. \bjournalWorking paper. \endbibitem

- Imkeller and Rogers [2014] {barticle}[author] \bauthor\bsnmImkeller, \bfnmNora\binitsN. and \bauthor\bsnmRogers, \bfnmLCG\binitsL. (\byear2014). \btitleTrading to stops. \bjournalSIAM Journal on Financial Mathematics \bvolume5 \bpages753–781. \endbibitem

- Kuznetsov, Kyprianou and Rivero [2013] {barticle}[author] \bauthor\bsnmKuznetsov, \bfnmA.\binitsA., \bauthor\bsnmKyprianou, \bfnmAndreas E.\binitsA. E. and \bauthor\bsnmRivero, \bfnmV.\binitsV. (\byear2013). \btitleThe theory of scale functions for spectrally negative Lévy processes. \bjournalSpringer Lecture Notes in Mathematics \bvolume2061 \bpages97-186. \bmrnumberMR3014147 \endbibitem

- Kyprianou [2006] {bbook}[author] \bauthor\bsnmKyprianou, \bfnmAndreas E.\binitsA. E. (\byear2006). \btitleIntroductory Lectures on Fluctuations of Lévy Processes with Applications. \bseriesUniversitext. \bpublisherSpringer-Verlag, \baddressBerlin. \bmrnumberMR2250061 (2008a:60003) \endbibitem

- Kyprianou and Ott [2012] {barticle}[author] \bauthor\bsnmKyprianou, \bfnmA. E.\binitsA. E. and \bauthor\bsnmOtt, \bfnmC.\binitsC. (\byear2012). \btitleSpectrally negative Lévy processes perturbed by functionals of their running supremum. \bjournalJournal of Applied Probability \bvolume49 \bpages1005–1014. \endbibitem

- Kyprianou and Ott [2014] {barticle}[author] \bauthor\bsnmKyprianou, \bfnmA. E.\binitsA. E. and \bauthor\bsnmOtt, \bfnmC.\binitsC. (\byear2014). \btitleA capped optimal stopping problem for the maximum process. \bjournalActa Applicandae Mathematicae \bvolume129 \bpages147–174. \endbibitem

- Leung and Zhang [2019] {barticle}[author] \bauthor\bsnmLeung, \bfnmT.\binitsT. and \bauthor\bsnmZhang, \bfnmH.\binitsH. (\byear2019). \btitleOptimal trading with a trailing stop. \bjournalApplied Mathematics & Optimization. \endbibitem

- Linetsky [1999] {barticle}[author] \bauthor\bsnmLinetsky, \bfnmVadim\binitsV. (\byear1999). \btitleStep options. \bjournalMathematical Finance \bvolume9 \bpages55–96. \endbibitem

- Loeffen, Renaud and Zhou [2014] {barticle}[author] \bauthor\bsnmLoeffen, \bfnmR. L.\binitsR. L., \bauthor\bsnmRenaud, \bfnmJ. F.\binitsJ. F. and \bauthor\bsnmZhou, \bfnmX.\binitsX. (\byear2014). \btitleOccupation times of intervals until first passage times for spectrally negative Lévy processes. \bjournalStochastic Processes and their Applications \bvolume124 \bpages1408-1435. \bmrnumberMR3148018 \endbibitem

- Long and Zhang [2019] {barticle}[author] \bauthor\bsnmLong, \bfnmM.\binitsM. and \bauthor\bsnmZhang, \bfnmH.\binitsH. (\byear2019). \btitleOn the optimality of threshold type strategies in single and recursive optimal stopping under Lévy models. \bjournalStochastic Processes and their Applications \bvolume129 \bpages2821-2849. \endbibitem

- Madan and Schoutens [2008] {barticle}[author] \bauthor\bsnmMadan, \bfnmDilip B\binitsD. B. and \bauthor\bsnmSchoutens, \bfnmWim\binitsW. (\byear2008). \btitleBreak on through to the single side. \bjournalJournal of Credit Risk \bvolume4 \bpages3-20. \endbibitem

- Mordecki [2002] {barticle}[author] \bauthor\bsnmMordecki, \bfnmE.\binitsE. (\byear2002). \btitleOptimal stopping and perpetual options for Lévy processes. \bjournalFinance and Stochastics \bvolume6 \bpages473-493. \bmrnumberMR1932381 (2003j:91059) \endbibitem

- Obłój [2007] {bincollection}[author] \bauthor\bsnmObłój, \bfnmJan\binitsJ. (\byear2007). \btitleThe maximality principle revisited: On certain optimal stopping problems. In \bbooktitleSéminaire de probabilités XL \bpages309–328. \bpublisherSpringer. \endbibitem

- Øksendal [2003] {bbook}[author] \bauthor\bsnmØksendal, \bfnmB.\binitsB. (\byear2003). \btitleStochastic Differential Equations: an Introduction with Applications, \bedition6th ed. \bpublisherSpringer. \endbibitem

- Øksendal and Sulem [2005] {bbook}[author] \bauthor\bsnmØksendal, \bfnmB.\binitsB. and \bauthor\bsnmSulem, \bfnmA.\binitsA. (\byear2005). \btitleApplied Stochastic Control of Jump Diffusions. \bpublisherSpringer. \endbibitem

- Ott [2013] {barticle}[author] \bauthor\bsnmOtt, \bfnmC.\binitsC. (\byear2013). \btitleOptimal stopping problems for the maximum process with upper and lower caps. \bjournalThe Annals of Applied Probability \bvolume23 \bpages2327–2356. \endbibitem

- Peskir [1998] {barticle}[author] \bauthor\bsnmPeskir, \bfnmGoran\binitsG. (\byear1998). \btitleOptimal stopping of the maximum process: The maximality principle. \bjournalAnnals of Probability \bpages1614–1640. \endbibitem

- Peskir and Shiryaev [2006] {bbook}[author] \bauthor\bsnmPeskir, \bfnmGoran\binitsG. and \bauthor\bsnmShiryaev, \bfnmAlbert\binitsA. (\byear2006). \btitleOptimal stopping and free-boundary problems. \bpublisherSpringer. \endbibitem

- Rodosthenous and Zervos [2017] {barticle}[author] \bauthor\bsnmRodosthenous, \bfnmNeofytos\binitsN. and \bauthor\bsnmZervos, \bfnmMihail\binitsM. (\byear2017). \btitleWatermark options. \bjournalFinance and Stochastics \bvolume21 \bpages157–186. \endbibitem

- Rodosthenous and Zhang [2018] {barticle}[author] \bauthor\bsnmRodosthenous, \bfnmN.\binitsN. and \bauthor\bsnmZhang, \bfnmH.\binitsH. (\byear2018). \btitleBeating the Omega clock: an optimal stopping problem with random time-horizon under spectrally negative Lévy models. \bjournalThe Annals of Applied Probability \bvolume28 \bpages2105–2140. \endbibitem

- Zhang [2001] {barticle}[author] \bauthor\bsnmZhang, \bfnmQ.\binitsQ. (\byear2001). \btitleStock trading: An optimal selling rule. \bjournalSIAM Journal on Control and Optimizatoin \bvolume40 \bpages64-87. \endbibitem

- Zhang [2018] {bbook}[author] \bauthor\bsnmZhang, \bfnmHongzhong\binitsH. (\byear2018). \btitleStochastic Drawdowns. \bpublisherWorld Scientific. \endbibitem