Distributional Random Forests: Heterogeneity Adjustment and Multivariate Distributional Regression

Abstract

Random Forest (Breiman, 2001) is a successful and widely used regression and classification algorithm. Part of its appeal and reason for its versatility is its (implicit) construction of a kernel-type weighting function on training data, which can also be used for targets other than the original mean estimation. We propose a novel forest construction for multivariate responses based on their joint conditional distribution, independent of the estimation target and the data model. It uses a new splitting criterion based on the MMD distributional metric, which is suitable for detecting heterogeneity in multivariate distributions. The induced weights define an estimate of the full conditional distribution, which in turn can be used for arbitrary and potentially complicated targets of interest. The method is very versatile and convenient to use, as we illustrate on a wide range of examples. The code is available as Python and R packages drf.

Keywords: causality, distributional regression, fairness, Maximal Mean Discrepancy, Random Forests, two-sample testing

1 Introduction

In practice, one often encounters heterogeneous data, whose distribution is not constant, but depends on certain covariates. For example, data can be collected from several different sources, its distribution might differ across certain subpopulations or it could even change with time, etc. Inferring valid conclusions about a certain target of interest from such data can be very challenging as many different aspects of the distribution could potentially change. As an example, in medical studies, the effectiveness of a certain treatment might not be constant throughout the population but depend on certain patient characteristics such as age, race, gender, or medical history. Another issue could be that different patient groups were not equally likely to receive the same treatment in the observed data.

Obviously, pooling all available data together can result in invalid conclusions. On the other hand, if for a given test point of interest one only considers similar training data points, i.e. a small homogeneous subpopulation, one may end up with too few samples for accurate statistical estimation. In this paper, we propose a method based on the Random Forest algorithm (Breiman, 2001) which in a data-adaptive way determines for any given test point which training data points are relevant for it. This in turn can be used for drawing valid conclusions or for accurately estimating any quantity of interest.

Let be a multivariate random variable representing the data of interest, but whose joint distribution is heterogeneous and depends on some subset of a potentially large number of covariates . Throughout the paper, vector quantities are denoted in bold. We aim to estimate a certain target object that depends on the conditional distribution , where is an arbitrary point in . The estimation target can range from simple quantities, such as the conditional expectations (Breiman, 2001) or quantiles (Meinshausen, 2006) for some function , to some more complicated aspects of the conditional distribution , such as conditional copulas or conditional independence measures. Given the observed data , the most straightforward way of estimating nonparametrically would be to consider only the data points in some neighborhood around , e.g. by considering the nearest neighbors according to some metric. However, such methods typically suffer from the curse of dimensionality even when is only moderately large: for a reasonably small neighborhood, such that the distribution is close to the distribution , the number of training data points contained in will be very small, thus making the accurate estimation of the target difficult. The same phenomenon occurs with other methods which locally weight the training observations such as kernel methods (Silverman, 1986), local MLE (Fan et al., 1998) or weighted regression (Cleveland, 1979) even for the relatively simple problem of estimating the conditional mean for fairly small . For that reason, more importance should be given to the training data points for which the response distribution at point is similar to the target distribution , even if is not necessarily close to in every component.

In this paper, we propose the Distributional Random Forest (DRF) algorithm which estimates the multivariate conditional distribution in a locally adaptive fashion. This is done by repeatedly dividing the data points in the spirit of the Random Forest algorithm (Breiman, 2001): at each step, we split the data points into two groups based on some feature in such a way that the distribution of for which , for some level , differs the most compared to the distribution of when , according to some distributional metric. One can use any multivariate two-sample test statistic, provided it can detect a wide variety of distributional changes. As the default choice, we propose a criterion based on the Maximal Mean Discrepancy (MMD) statistic (Gretton et al., 2007a) with many interesting properties. This splitting procedure partitions the data such that the distribution of the multivariate response in the resulting leaf nodes is as homogeneous as possible, thus defining neighborhoods of relevant training data points for every . Repeating this many times with randomization induces a weighting function as in Lin and Jeon (2002, 2006), described in detail in Section 2, which quantifies the relevance of each training data point for a given test point . The conditional distribution is then estimated by an empirical distribution determined by these weights (Meinshausen, 2006). This construction is data-adaptive as it assigns more weight to the training points that are closer to the test point in the components which are more relevant for the distribution of .

Our forest construction does not depend on the estimation target , but it rather estimates the conditional distribution directly and the induced forest weights can be used to estimate in a second step. This approach has several advantages. First, only one DRF fit is required to obtain estimates of many different targets, which has a big computational advantage. Furthermore, since those estimates are obtained from the same forest fit, they are mutually compatible. For example, if the conditional correlation matrix is estimated componentwise using some other method, the resulting matrix might not be positive semidefinite, and as another example, the CDF estimates might not be monotone in , see Figure 6. Finally, it could be extremely difficult to tailor forest construction to some complex targets . The induced weighting function can thus be used not only for obtaining simple distributional aspects such as, for example, the conditional quantiles, conditional correlations, or joint conditional probability statements, but also to obtain more complex objectives, such as conditional independence tests (Zhang et al., 2011), heterogeneous regression (see also Section 4.4 for more details) (Künzel et al., 2019; Wager and Athey, 2018) or semiparametric estimation by fitting a parametric model for , having nonparametrically adjusted for (Bickel et al., 1993). Representation of the conditional distribution via the weighting function has a great potential for applications in causality such as causal effect estimation or as a way of implementing do-calculus (Pearl, 2009) for finite samples, as we discuss in Section 4.4.

Therefore, DRF is used in two steps: in the first step, we obtain the weighting function describing the conditional distribution in a target- and model-free way, which is then used as an input for the second step. Even if the method used in the second step does not directly support weighting of the training data points, one can easily resample the data set with the sampling probabilities equal to . This two-step approach is visualized in the following diagram:

1.1 Related work and our contribution

Several adaptations of the Random Forest algorithm have been proposed for targets beyond the original one of the univariate conditional mean : for survival analysis (Hothorn et al., 2006), conditional quantiles (Meinshausen, 2006), density estimation (Pospisil and Lee, 2018), CDF estimation (Hothorn and Zeileis, 2021) or heterogeneous treatment effects (Wager and Athey, 2018). Almost all such methods use the weights induced by the forest, as described in Section 2, rather than averaging the estimates obtained per tree. This view of Random Forests as a powerful adaptive nearest neighbor method is well known and dates back to Lin and Jeon (2002, 2006). It was first used for targets beyond the conditional mean in Meinshausen (2006), where the original forest construction with univariate was used (Breiman, 2001). However, the univariate response setting considered there severely restricts the number of interesting targets and DRF can thus be viewed as an important generalization of this approach to the multivariate setting.

In order to be able to perform certain tasks or to achieve a better accuracy, many forest-based methods adapt the forest construction by using a custom splitting criterion tailored to their specific target, instead of relying on the standard CART criterion. In Zeileis et al. (2008) and Hothorn and Zeileis (2021), a parametric model for the response is assumed and recursive splitting is performed based on a permutation test which uses the user-provided score functions. Similarly, Athey et al. (2019) estimate certain univariate targets for which there exist corresponding score functions defining the local estimating equations. The data is split so that the estimates of the target in resulting child nodes differ the most. This is different, though, to the target-free splitting criterion of DRF, which splits so that the distribution of in child nodes is as different as possible.

Since the splitting step is extensively used in the algorithm, its complexity is crucial for the overall computational efficiency of the method, and one often needs to resort to approximating the splitting criterion (Pospisil and Lee, 2018; Athey et al., 2019) to obtain good computational run time. We propose a splitting criterion based on a fast random approximation of the MMD statistic (Gretton et al., 2012a; Zhao and Meng, 2015), which is commonly used in practice for two-sample testing as it is able to detect any change in the multivariate distribution of with good power (Gretton et al., 2007a). DRF with the MMD splitting criterion also has interesting theoretical properties as shown in Section 3 below.

The multivariate response case has not received much attention in the Random Forest literature. Most of the existing forest-based methods focus on either a univariate response or on a certain univariate target . One interesting line of work considers density estimation (Pospisil and Lee, 2018) and uses aggregation of the CART criteria for different response transformations. Another approach (Kocev et al., 2007; Segal and Xiao, 2011; Ishwaran and Kogalur, 2022) is based on aggregating standard univariate CART splitting criteria for and targets only the conditional mean of the responses, a task which could also be solved by separate regression fits for each . In order to capture any change in the distribution of the multivariate response , one needs to not only consider the marginal distributions for each component , but also to determine whether their dependence structure changes, see e.g. Figure 8.

There is an increasing number of methods that nonparametrically estimate the joint multivariate conditional distribution in the statistics and machine learning literature. In addition to a few simple classical methods such as -nearest neighbors and kernel regression, there exist methods based on normalizing flows such as Inverse Autoregressive Flow (Kingma et al., 2016) or Masked Autoregressive Flow (Papamakarios et al., 2017) and also conditional variants of several popular generative models such as Conditional Generative Adversarial Networks (Mirza and Osindero, 2014) or Conditional Variational Autoencoder (Sohn et al., 2015). The focus of these methods is more on the settings with large response dimension and small covariate dimension , such as image or text generation. Another interesting and related line of research focuses on estimating the conditional mean embedding (CME), as described e.g., in Song et al. (2009); Muandet et al. (2017); Song et al. (2013); Park and Muandet (2020), rather than estimating the conditional distribution directly. CMEs generalize the concept of embedding (marginal) probability distributions into a Reproducing Kernel Hilbert Space (RKHS) to the conditional case. Interestingly, DRF with the MMD-based splitting criterion can also be viewed as a method for estimating the CME, as discussed in Section 3 below. This viewpoint provides a natural connection between the Random Forest and kernel embedding literature. A comparison of DRF with the methods for distributional estimation listed above can be found in Section 4.1.

Our contribution, resulting in the proposal of the Distributional Random Forest (DRF), can be summarized as follows: First, we introduce the idea of forest construction based on sequential multivariate two-sample test statistics. It does not depend on a particular estimation target and is completely nonparametric, which makes its implementation and usage very simple and universal. Not only does it not require additional user input such as the log-likelihoods or score functions, but it can be used even for complicated targets for which there is no obvious forest construction. Furthermore, it has a computational advantage as only a single forest fit is needed for producing estimates of many different targets that are additionally compatible with each other. Second, we propose an MMD-based splitting criterion with good statistical and computational properties, for which we also derive interesting theoretical results in Section 3. It underpins our implementation, which we provide as R and Python packages drf. Finally, we show on a broad range of examples in Section 4 how many different statistical estimation problems, some of which not being easily tractable by existing forest-based methods, can be cast to our framework, thus illustrating the usefulness and versatility of DRF.

2 Method

In this section we describe the details of the Distributional Random Forest (DRF) algorithm. We closely follow the implementations of the grf (Athey et al., 2019) and ranger (Wright and Ziegler, 2017) R-packages. A detailed description of the method and its implementation and the corresponding pseudocode can be found in the Appendix A.

2.1 Forest Building

The trees are grown recursively in a model-free and target-free way as follows: For every parent node , we determine how to best split it into two child nodes of the form and , where the variable is one of the randomly chosen splitting candidates and denotes its level based on which we perform the splitting. The split is chosen such that we maximize a certain (multivariate) two-sample test statistic

| (1) |

which measures the difference of the empirical distributions of the data in the two resulting child nodes and . Therefore, in each step we select the candidate predictor which seems to affect the distribution of the most, as measured by the metric . Intuitively, in this way we ensure that the distribution of the data points in every leaf of the resulting tree is as homogeneous as possible, which helps mitigate the bias caused by pooling the heterogeneous data together. A related idea can be found in GRF (Athey et al., 2019), where one attempts to split the data so that the resulting estimates and , obtained respectively from data points in and , differ the most:

| (2) |

where we write and are defined analogously.

One could construct the forest using any metric for empirical distributions. However, in order to have a good accuracy of the overall method, the corresponding two-sample test using needs to have a good power for detecting any kind of change in distribution, which is a difficult task in general, especially for multivariate data (Bai and Saranadasa, 1996; Székely and Rizzo, 2004). Another very important aspect of the choice of distributional metric is the computational efficiency; one needs to be able to sequentially compute the values of for every possible split very fast for the overall algorithm to be computationally feasible, even for moderately large data sets. Below, we propose a splitting criterion based on the MMD two-sample test statistic (Gretton et al., 2007a) which has both good statistical and computational properties.

In contrast to other forest-based methods, we do not use any information about our estimation target in order to find the best split of the data, which comes with a certain trade-off. On one hand, it is sensible that tailoring the splitting criterion to the target should improve the estimation accuracy; for example, some predictors might affect the conditional distribution of , but not necessarily the estimation target and splitting on such predictors unnecessarily reduces the number of training points used for estimating . On the other hand, our approach has multiple benefits: it is easier to use as it does not require any user input such as the likelihood or score functions and it can also be used for very complicated targets for which one could not easily adapt the splitting criterion. Furthermore, only one DRF fit is necessary for producing estimates of many different targets, which has both computational advantage and the practical advantage that the resulting estimates are mutually compatible (see e.g. Figure 5).

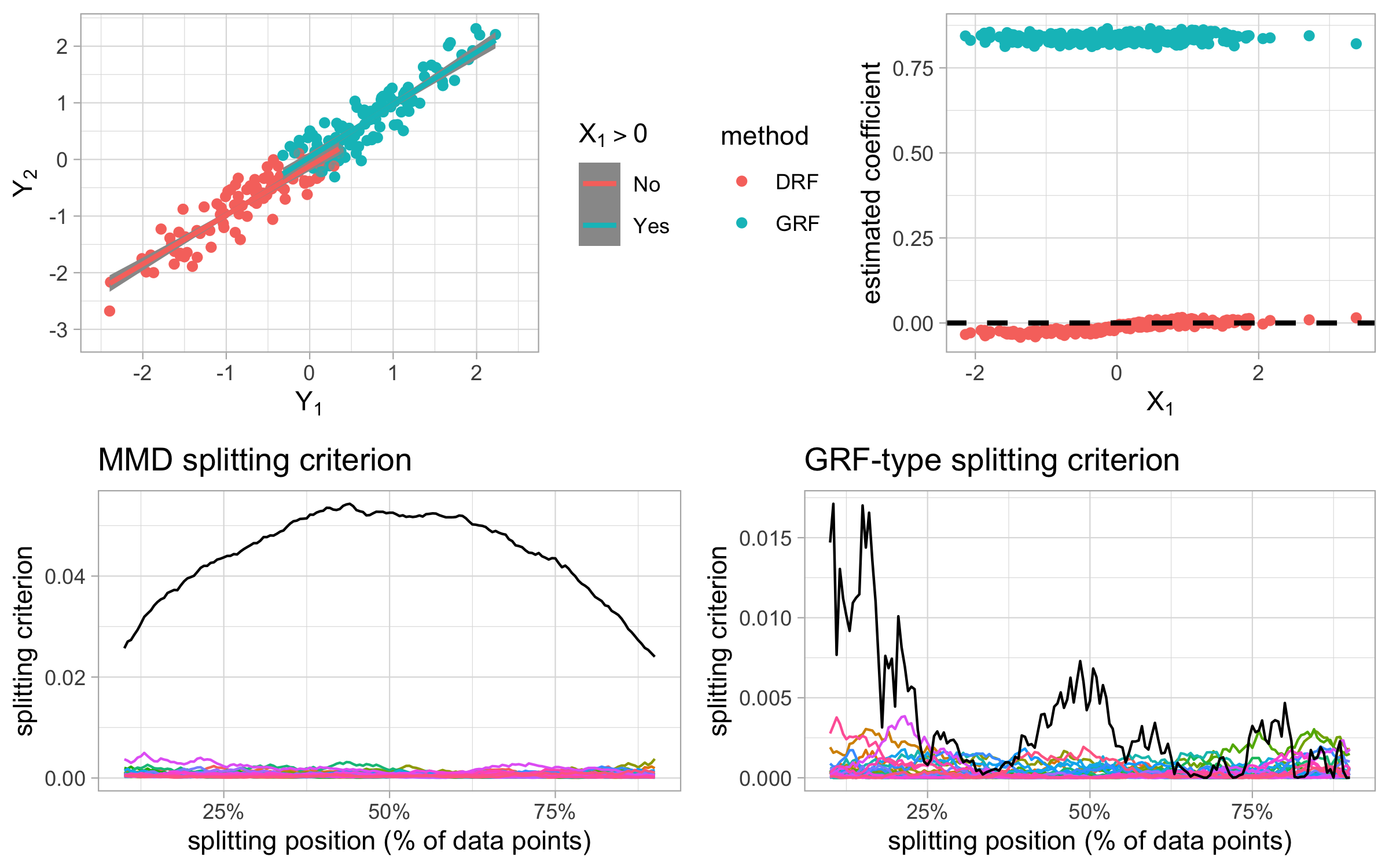

Interestingly, sometimes it could even be beneficial to split based on a predictor which does not affect the target of estimation, but which affects the conditional distribution. This is illustrated by the following toy example. Suppose that for a bivariate response we are interested in estimating the slope of the linear regression of on conditionally on predictors , i.e. our target is . This is one of the main use cases for GRF and its variant which estimates this target is called Causal Forest (Wager and Athey, 2018; Athey et al., 2019). Let us assume that the data has the following distribution:

| (3) |

i.e. affects only the mean of the responses, while the other predictors have no effect. In Figure 1 we illustrate the distribution of the data when , together with the DRF and GRF splitting criteria. The true value of the target is , but when is not too big, the slope estimates on pooled data will be closer to . Therefore, the difference of and between the induced slope estimates for a candidate split, which is used for splitting criterion (2) of GRF, might not be large enough for us to decide to split on , or the resulting split might be too unbalanced. This results in worse forest estimates for this toy example, see Figure 1.

2.2 Weighting Function

Having constructed our forest, just as the standard Random Forest (Breiman, 2001) can be viewed as the weighted nearest neighbor method (Lin and Jeon, 2002), we can use the induced weighting function to estimate the conditional distribution at any given test point and thus any other quantity of interest . This approach is commonly used in various forest-based methods for obtaining predictions, see e.g., Hothorn and Zeileis (2021); Pospisil and Lee (2018); Athey et al. (2019).

Suppose that we have built trees . Let be the set of the training data points which end up in the same leaf as in the tree . The weighting function is defined as the average of the corresponding weighting functions per tree (Lin and Jeon, 2006):

| (4) |

The weights are positive and add up to : . In the case of equally sized leaf nodes, the assigned weight to a training point is proportional to the number of trees where the test point and end up in the same leaf node. This shows that forest-based methods can in general be viewed as adaptive nearest neighbor methods. The sets of DRF will contain data points such that is close to , thus removing bias due to heterogeneity of caused by . On the other hand, since the trees are constructed randomly and are thus fairly independent (Breiman, 2001), the leaf sets will be different enough so that the induced weights are not concentrated on a small set of data points, which would lead to high estimation variance. Such good bias-variance tradeoff properties of forest-based methods are also implied by their asymptotic properties (Biau, 2012; Wager, 2014), even though this is a still active area of research and not much can be shown rigorously.

One can estimate the conditional distribution from the weighting function by using the corresponding empirical distribution:

| (5) |

where is the point mass at .

Two-step approach using weights.

The weighting function can directly be used for any target in a second step and not just for estimating the conditional distribution. For example, the estimated conditional joint CDF is given by

| (6) |

It is important to point out that using the induced weighting function for locally weighted estimation is different than the approach of averaging the noisy estimates obtained per tree (Wager and Athey, 2018), originally used in standard Random Forests (Breiman, 2001). Even though the two approaches are equivalent for conditional mean estimation, the former approach is often much more efficient for more complex targets (Athey et al., 2019), since the number of data points in a single leaf is very small, leading to large variance of the estimates.

For the univariate response, the idea of using the induced weights for estimating targets different than the original target of conditional mean considered in Breiman (2001) dates back to Quantile Regression Forests (QRF) (Meinshausen, 2006), where a lot of emphasis is put on the quantile estimation, as the number of interesting targets is quite limited in the univariate setting. In the multivariate case, on the other hand, many interesting quantities such as, for example, conditional quantiles, conditional correlations or various conditional probability statements can easily be directly estimated from the weights.

By using the weights as an input for some other method, we can accomplish some more complicated objectives, such as conditional independence testing, causal effect estimation, semiparametric learning, time series prediction or tail-index estimation in extreme value analysis. As an example, suppose that our data come from a certain parametric model, where the parameter is not constant, but depends on instead, i.e. , see also Zeileis et al. (2008). One can then estimate the parameter by using weighted maximum likelihood estimation:

Another example is heterogeneous regression, where we are interested in the regression fit of an outcome on certain predicting variables conditionally on some event . This can be achieved by weighted regression of on , where the weights assigned to each data point are obtained from DRF with the multivariate response and predictors , for an illustration see Section 4.4.

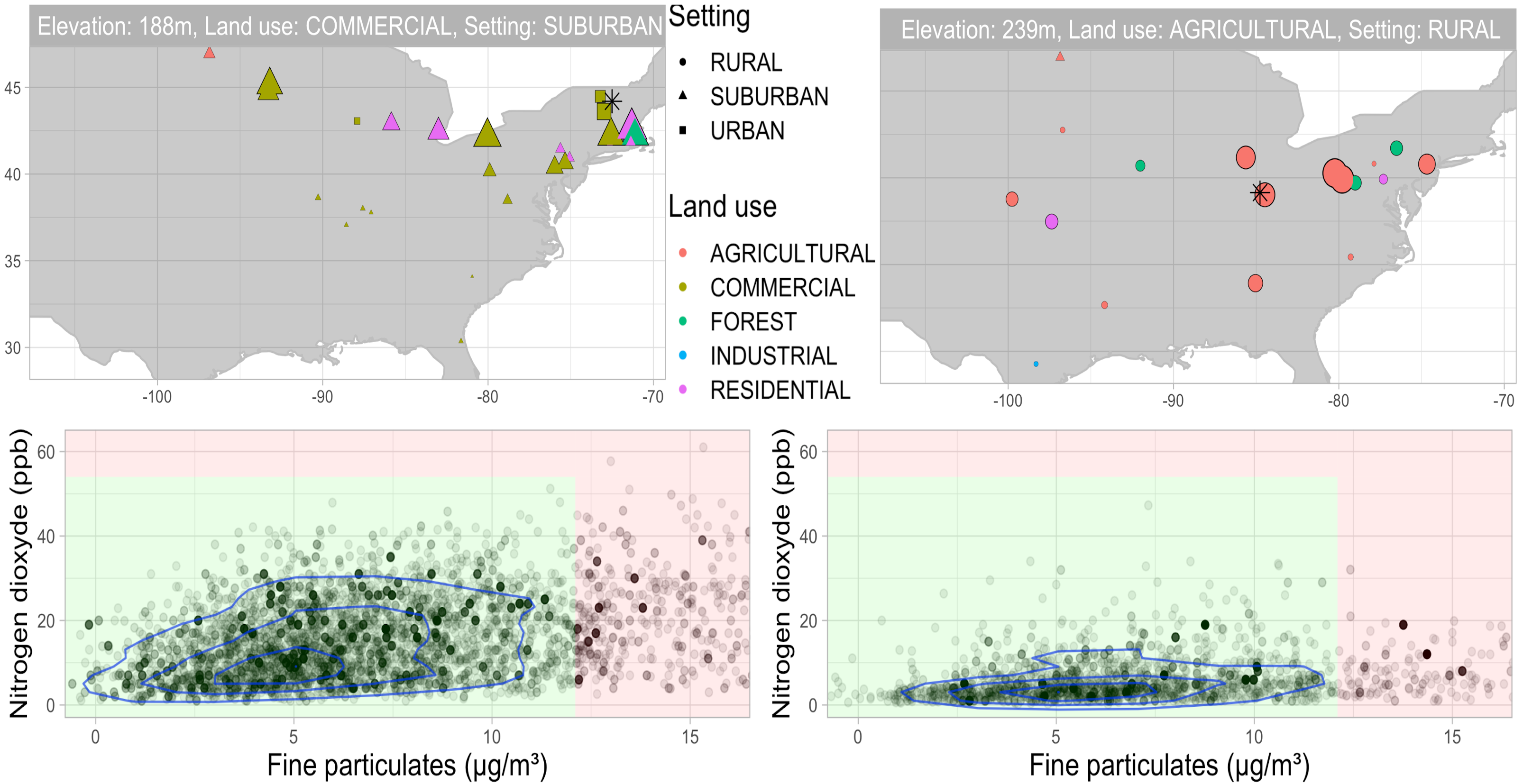

The weighting function of DRF is illustrated on the air quality data in Figure 2. Five years () of air pollution measurements were obtained from the US Environmental Protection Agency (EPA) website. Six main air pollutants (nitrogen dioxide (NO2), carbon monoxide (CO), sulphur dioxide (SO2), ozone (O3) and coarse and fine particulate matter (PM and PM)) that form the air quality index (AQI) were measured at many different measuring sites in the US for which we know the longitude, latitude, elevation, location setting (rural, urban, suburban) and how the land is used within a mile radius. Suppose we would want to know the distribution of the pollutant measurements at some new, unobserved, measurement site. We train DRF with the measurements (intraday maximum) of the two pollutants PM and NO2 as the responses, and the site longitude, latitude, elevation, land use and location settings as the predictors and choose two decommissioned measurement sites as test points. For each test point we obtain the weights to all training measurements. We further combine the weights for all measurements corresponding to the same site. The top row illustrates for a given test site, whose characteristics are indicated in the plot title, how much weight in total is assigned to the measurements from a specific training site. We see that the important sites share many characteristics with the test site and that DRF determines the relevance of each characteristic in a data-adaptive way. The bottom row shows the corresponding estimates of the joint conditional distribution of the pollutants (we choose of them for visualization purposes), where the transparency of each training point reflects the assigned weight. One can clearly see how the estimated pollution levels are larger for the suburban site than for the rural site. The forest weights can be used, for example, for estimating the joint density (whose contours can be seen in the plot) or for estimating the probability that the AQI is below a certain value by summing the weights in the corresponding region of space.

2.3 Distributional Metric

In order to determine the best split of a parent node , i.e. such that the distributions of the responses in the resulting child nodes and differ the most, one needs a good distributional metric (see Equation (1)) which can detect change in distribution of the response when additionally conditioning on an event . Testing equality of distributions from the corresponding samples is an old problem in statistics, called two-sample testing problem. For univariate data, many good tests exist such as Wilcoxon rank test (Wilcoxon, 1946), Welch’s t-test (Welch, 1947), Wasserstein two-sample testing (Ramdas et al., 2017), Kolmogorov-Smirnov test (Massey Jr, 1951) and many others, but obtaining an efficient test for multivariate distributions has proven to be quite challenging due to the curse of dimensionality (Friedman and Rafsky, 1979; Baringhaus and Franz, 2004).

Additional requirement for the choice of distributional metric used for data splitting is that it needs to be computationally very efficient as splitting is used extensively in the algorithm. If we construct trees from data points and in each node we consider mtry candidate variables for splitting, the complexity of the standard Random Forest algorithm (Breiman, 2001) in the univariate case is provided our splits are balanced. It uses the CART splitting criterion, given by:

| (7) |

where and is defined analogously. This criterion has an advantage that not only it can be computed in complexity, but this can be done for all possible splits as cutoff level varies, since updating the splitting criterion when moving a single training data point from one child node to the other requires only computational steps (most easily seen by rewriting the CART criterion as in (13)).

If the time complexity of evaluating the DRF splitting criterion (1) for a single splitting candidate and all cutoffs of interest (usually taken to range over all possible values) is at least for some , say for some function , then by solving the recursive relation we obtain that the overall complexity of the method is given by (Akra and Bazzi, 1998), which can be unfeasible even for moderately large if grows too fast.

The problem of sequential two-sample testing is also central to the field of change-point detection (Wolfe and Schechtman, 1984; Brodsky and Darkhovsky, 2013), with the slight difference that in the change-point problems the distribution is assumed to change abruptly at certain points in time, whereas for our forest construction we only are interested in finding the best split of the form and the conditional distribution usually changes gradually with . The testing power and the computational feasibility of the method play a big role in change-point detection as well. However, the state-of-the-art change-point detection algorithms (Li et al., 2019; Matteson and James, 2014) are often too slow for our purpose as sequential testing is done times for forest construction, much more frequently than in change-point problems.

2.3.1 MMD splitting criterion

Even though DRF could in theory be constructed with any distributional metric , as a default choice we propose splitting criterion based on the Maximum Mean Discrepancy (MMD) statistic (Gretton et al., 2007a). Let be the RKHS of real-valued functions on induced by some positive-definite kernel , and let be the corresponding feature map satisfying that .

The MMD statistic for kernel and two samples and is given by:

| (8) |

MMD compares the similarities, described by the kernel , within each sample with the similarities across samples and is commonly used in practice for two-sample testing. It is based on the idea that one can assign to each distribution its embedding into the RKHS , which is the unique element of given by

| (9) |

The MMD two-sample statistic (8) can then equivalently be written as the squared distance between the embeddings of the empirical distributions with respect to the RKHS norm :

| (10) |

recalling that is the point mass at .

As the sample sizes and grow, the MMD statistic (10) converges to its population version, which is the squared RKHS distance between the corresponding embeddings of the data-generating distributions of and . Since the embedding map is injective for a characteristic kernel , we see that MMD is able to detect any difference in the distribution. Even though the power of the MMD two sample test also deteriorates as the data dimensionality grows, since the testing problem becomes intrinsically harder (Ramdas et al., 2015), it still has good empirical power compared to other multivariate two-sample tests for a wide range of (Gretton et al., 2012a).

Fast random splitting criterion approximation.

The complexity for computing from (8) is nevertheless too large for many applications. For that reason, several fast approximations of MMD have been suggested in the literature (Gretton et al., 2012a, b; Zaremba et al., 2013; Chwialkowski et al., 2015; Jitkrittum et al., 2016). As already mentioned, the complexity of the distributional metric used for DRF is crucial for the overall method to be computationally efficient, since the splitting step is used extensively in the forest construction. We therefore propose splitting based on an MMD statistic computed with an approximate kernel , which is also a fast random approximation of the original MMD statistic (Zhao and Meng, 2015).

Bochner’s theorem (see e.g. Wendland (2004, Theorem 6.6)) gives us that any bounded shift-invariant kernel can be written as

| (11) |

i.e. as a Fourier transform of some measure . Therefore, by randomly sampling the frequency vectors from normalized , we can approximate our kernel by another kernel (up to a scaling factor) as follows:

where we define as the kernel function with the feature map given by

which is a random vector consisting of the Fourier features (Rahimi and Recht, 2008). Such kernel approximations are frequently used in practice for computational efficiency (Rahimi and Recht, 2009; Le et al., 2013). As a default choice of we take the Gaussian kernel with bandwidth , since in this case we have a convenient expression for the measure and we sample . The bandwidth is chosen as the median pairwise distance between all training responses , commonly referred to as the ’median heuristic’ (Gretton et al., 2012c).

From the representation of MMD via the distribution embeddings (10), we can obtain that MMD two-sample test statistic using the approximate kernel is given by

Interestingly, is not only an MMD statistic on its own, but can also be viewed as a random approximation of the original MMD statistic (8) using kernel ; by using the kernel representation (11), it can be written as

Finally, our DRF splitting criterion (1) is then taken to be the (scaled) MMD statistic with the approximate random kernel used instead of , which can thus be conveniently written as:

| (12) |

where we recall that and are defined analogously. The additional scaling factor in (12) occurs naturally and compensates the increased variance of the test statistic for unbalanced splits; it also appears in the GRF (2) and CART (see representation (13)) splitting criteria.

The main advantage of the splitting criterion based on is that by using the representation (1) it can be easily computed for every possible splitting level in complexity, whereas the MMD statistic using kernel would require computational steps, which makes the overall complexity of the algorithm instead of much slower .

We do not use the same approximate random kernel for different splits; for every parent node we resample the frequency vectors defining the corresponding feature map . Using different at each node might help to better detect different distributional changes. Furthermore, having different random kernels for each node agrees well with the randomness of the Random Forests and helps making the trees more independent. Since the MMD statistic used for our splitting criterion is not only an approximation of , but is itself an MMD statistic, it inherits good power for detecting any difference in distribution of in the child nodes for moderately large data dimensionality , even when is reasonably small. One could even consider changing the number of random Fourier features at different levels of the tree, as varies, but for simplicity we take it to be fixed.

Relationship to CART.

There is some similarity of our MMD-based splitting criterion (12) with the standard variance reduction CART splitting criterion (7) when , which can be rewritten as:

| (13) |

The derivation can be found in Appendix B. From this representation, we see that the CART splitting criterion (7) is also equivalent to the GRF splitting criterion (2) when our target is the univariate conditional mean which is estimated for and by the sample means and . Therefore, as it compares the means of the univariate response in the child nodes, the CART criterion can only detect changes in the response mean well, which is sufficient for prediction of from , but might not be suitable for more complex targets. Similarly, for multivariate applications, aggregating the marginal CART criteria (Kocev et al., 2007; Segal and Xiao, 2011) across different components of the response can only detect changes in the means of their marginal distributions. However, it is possible in the multivariate case that the pairwise correlations or the variances of the responses change, while the marginal means stay (almost) constant. For an illustration on simulated data, see Figure 7. Additionally, aggregating the splitting criteria over components of the response can reduce the signal size if only the distribution of a few components change. Our MMD-based splitting criterion (12) is able to avoid such difficulties as it implicitly inspects all aspects of the multivariate response distribution.

If one takes a trivial kernel with the identity feature map , the distributional embedding (9) is given by and thus the corresponding splitting criterion based on (10) is exactly equal to the CART splitting criterion (7), which can be seen from its equivalent representation (13). Interestingly, Theorem 3.1 in Section 3 shows that the MMD splitting criterion with general kernel can also be viewed as the abstract version of the CART criterion in the RKHS corresponding to (Fan et al., 2010), with the response variable being the feature map . Therefore, DRF with the MMD splitting criterion can also be viewed as a forest-based method for estimation of the conditional embedding, which further justifies the proposed method. In Section 3 below, we use this relationship to derive interesting theoretical properties of DRF with the MMD splitting criterion.

3 Theoretical Results

In this section we first use the properties of the kernel mean embedding in order to relate DRF with the MMD splitting criterion to an abstract version of the standard Random Forest with the CART splitting criterion (Breiman, 2001), where the response is taking values in the corresponding RKHS. This representation reveals that DRF with the MMD splitting criterion can be viewed as a Random Forest estimator of the conditional mean embedding (CME) (Park and Muandet, 2020), similarly as the standard Random Forest estimates the conditional mean. This relationship is further exploited to adapt the existing theoretical results from the Random Forest literature to show that our estimate (5) of the conditional distribution of the response is consistent with respect to the MMD metric for probability measures and with a good rate. Finally, we show that this implies consistency of the induced DRF estimates for a range interesting targets , such as conditional CDFs or quantiles. The proofs of all results can be found in the Appendix B.

3.1 Casting DRF as a Random Forest in an RKHS

Recalling the notation from above, let be the Reproducing kernel Hilbert space induced by the positive definite kernel and let be its corresponding feature map. The kernel embedding function maps any bounded signed Borel measure on to an element defined by

| (14) |

see also (9). Boundedness of ensures that is indeed defined on all of , while continuity of ensures that is separable (Hsing and Eubank, 2015).

By considering the kernel embedding and using its linearity, the embedding of the distributional estimate of DRF (5) can be written as the average of the embeddings of the empirical distributions of in the leaves containing over all trees:

| (15) |

This is analogous to the prediction of the response for the standard univariate Random Forest, but where we average the embeddings instead of the response values themselves.

Furthermore, one can relate the MMD splitting criterion to the original CART criterion (7), which measures the mean squared prediction error for splitting a certain parent node into children and . On one hand, from Equation (13) we see that the CART criterion also measures the squared distance between the response averages and in the child nodes, but on the other hand, Equation (10) shows that the MMD splitting criterion measures the RKHS distance between the embeddings of the empirical response distributions in and . This is summarized in the following theorem, which not only shows that the MMD splitting criterion can be viewed as the abstract CART criterion in the RKHS (Fan et al., 2010), but also that DRF with the MMD splitting criterion can be viewed asymptotically as a greedy minimization of the average squared MMD distance between our estimate and the truth :

theoremMMDCART For any split of a parent node into child nodes and , let denote the resulting estimate of the distribution when . Then the MMD splitting criterion can be viewed as the version of the CART criterion (7) on :

Moreover, for any node and any fixed distributional estimator , we have:

where is a deterministic term not depending on the estimates .

In conclusion, from the above results we see that by applying the kernel embedding (14), we can shift the perspective to the RKHS and view DRF as the analogue of the original Random Forest for estimation of the CME in an abstract Hilbert space . Like some traditional CME estimators (Song et al., 2009, 2013; Muandet et al., 2017; Park and Muandet, 2020) it is also of the form

| (16) |

It can be shown that, since DRF produces nonnegative weights that sum to one in (16), there is one-to-one correspondence between the resulting estimate in and the empirical probability distribution in . Thus DRF can be seen as a CME estimator through (16), or directly as an estimator for the conditional distribution through (5). By contrast, other CME estimators of the form (16) have weights that are unconstrained and can be negative. Finding an appropriate distribution on for a given mean-embedding (sometimes referred to as “distributional inverse image problem”, see e.g. McCalman et al. (2013); Muandet et al. (2017)) is not straightforward in general. For certain tasks, such as sampling from the estimated conditional distribution or obtaining the plug-in estimates of some target functionals , this is crucial.

3.2 Convergence of Conditional Distribution Estimates

As we have seen, DRF can be viewed as the abstract version of the standard Random Forest when the response takes value in an RKHS. In principle, one could thus derive properties of DRF by adapting any existing theoretical result from the literature to the RKHS case. However, a lot of care is needed for making the results rigorous in this abstract setup, as many useful properties of need not hold for infinite-dimensional . This section is inspired by the results from Wager and Athey (2018).

We suppose that the forest construction satisfies the following properties, which significantly facilitate the theoretical considerations of the method and ensure that our forest estimator is well behaved, as stated in Wager and Athey (2018):

-

(P1)

(Data sampling) The bootstrap sampling with replacement, usually used in forest-based methods, is replaced by a subsampling step, where for each tree we choose a random subset of size out of training data points. We consider going to infinity with , with the rate specified below.

-

(P2)

(Honesty) The data used for constructing each tree is split into two partOn the pitfalls of Gaussian scoring for causal discoverys; the first is used for determining the splits and the second for populating the leaves and thus for estimating the response.

-

(P3)

(-regularity) Each split leaves at least a fraction of the available training sample on each side. Moreover, the trees are grown until every leaf contains between and observations, for some fixed tuning parameter .

-

(P4)

(Symmetry) The (randomized) output of a tree does not depend on the ordering of the training samples.

-

(P5)

(Random-split) At every split point, the probability that the split occurs along the feature is bounded below by , for some and for all .

The validity of the above properties are easily ensured by the forest construction used.

From Equation (15), the prediction of DRF for a given test point can be viewed as an element of . If we denote the -th training observation by , then by (15) we estimate the embedding of the true conditional distribution by the average of the corresponding estimates per tree:

where is a random subset of of size chosen for constructing the -th tree and is a random variable capturing all randomness in growing , such as the choice of the splitting candidates. denotes the output of a single tree: i.e. the average of the terms over all data points contained in the leaf of the tree constructed from and .

Since one can take the number of trees to be arbitrarily large, we consider an “idealized” version of our estimator, as done in Wager and Athey (2017), which we denote as :

| (17) |

where the sum is taken over all possible subsets of .We have that as , while keeping the other variables constant, and thus we assume for simplicity that those two quantities are the same.

Our main result shows that, under similar assumptions as in Wager and Athey (2017), the embedding of our conditional distribution estimator consistently estimates with respect to the RKHS norm with a certain rate:

theoremconsistency Suppose that our forest construction satisfies properties (P1)–(P5). Assume additionally that is a bounded and continuous kernel and that we have a random design with independent and identically distributed on with a density bounded away from and infinity. If the subsample size is of order for some , the mapping

is Lipschitz and , we obtain the consistency w.r.t. the RKHS norm:

| (18) |

for .

Remark 1

The rate in (18) is analogous to the one from Wager and Athey (2018), who used it further to derive the asymptotic normality of the Random Forest estimator in . Unfortunately, this alone is not enough to establish asymptotic normality of as an element of . To do so, one needs to prove a functional central limit theorem with a Gaussian limiting process in the Hilbert space . This then allows to deduce asymptotic normality of smooth real-valued functionals. We will provide the detailed derivations in future work.

3.3 Convergence of the Induced Estimates

The above result shows that DRF estimate converges fast to the truth in the MMD distance, i.e. the RKHS distance between the corresponding embeddings. Even though this is interesting on its own, ultimately we want to relate this result to estimation of certain distributional targets

For any , we have that the DRF estimate of the target equals the dot product in the RKHS:

where we recall the weighting function induced by the forest (4). Therefore, the consistency result (18) in Theorem 3.2 directly implies that

| (19) |

i.e. that the DRF consistently estimates the targets of the form , for . From (18) we also obtain the rate of convergence when :

for as in Theorem 3.2. When is continuous, it is well known that all elements of are continuous, see e.g. Hsing and Eubank (2015). Under certain assumptions on the kernel and its input space, holding for several popular kernels, (e.g. the Gaussian kernel) (Sriperumbudur, 2016), we can generalize the convergence result (19) to any bounded and continuous function , as the convergence of measures in the MMD metric will also imply their weak convergence, i.e. metrizes weak convergence (Sriperumbudur, 2016; Simon-Gabriel and Schölkopf, 2018; Simon-Gabriel et al., 2020):

Corollary 2

Assume that one of the following two sets of conditions holds:

-

(a)

The kernel is bounded, (jointly) continuous and has

(20) Moreover, is vanishing at infinity, for all .

-

(b)

The kernel is bounded, shift-invariant, (jointly) continuous and in the Bochner representation in (11) is supported on all of . Moreover, takes its values almost surely in a closed and bounded subset of .

Then, under the conditions of Theorem 3.2, we have for any bounded and continuous function that DRF consistently estimates the target for any :

Recalling the Portmanteau Lemma on separable metric spaces, see e.g. Dudley (2002, Chapter 11), this has several other interesting consequences, such as the consistency of CDF and quantile estimates; Let be the conditional CDF of and for any index , let be the conditional CDF of and its generalized inverse, i.e. the quantile function. Let and be the corresponding DRF estimates via weighting function (6). Then we have the following result:

Corollary 3

Under the conditions of Corollary 2, for any , we have

for all points of continuity and of and respectively.

4 Applications and Numerical Experiments

The goal of this section is to demonstrate the versatility and applicability of DRF for many practical problems. We show that DRF can be used not only as an estimator of the multivariate conditional distribution, but also as a two-step method to easily obtain out-of-the box estimators for various, and potentially complex, targets .

Our main focus lies on the more complicated targets which cannot be that straightforwardly approached by conventional methods. However, we also illustrate the usage of DRF for certain applications for which there already exist several well-established methods. Whenever possible in such cases, we compare the performance of DRF with the specialized, task-specific methods to show that, despite its generality, there is at most a very small loss of precision. However, we should point out that for many targets such as, that can not be written in a form of a conditional mean or a conditional quantile, for example, conditional correlation, direct comparison of the accuracy is not possible for real data, since no suitable loss function exists and the ground truth is unknown. Finally, we show that, in addition to directly estimating certain targets, DRF can also be a very useful tool for many different applications, such as causality and fairness.

Detailed descriptions of all competing methods, data sets and the corresponding analyses can be found in Appendix C, and some additional simulations can be found in the Appendix D.

4.1 Estimation of Conditional Multivariate Distributions

In order to provide good estimates for any target , our method needs to estimate the conditional multivariate distribution well. Therefore, we first investigate here the accuracy of the DRF estimate (5) of the full conditional distribution and compare its performance with the performance of several existing methods.

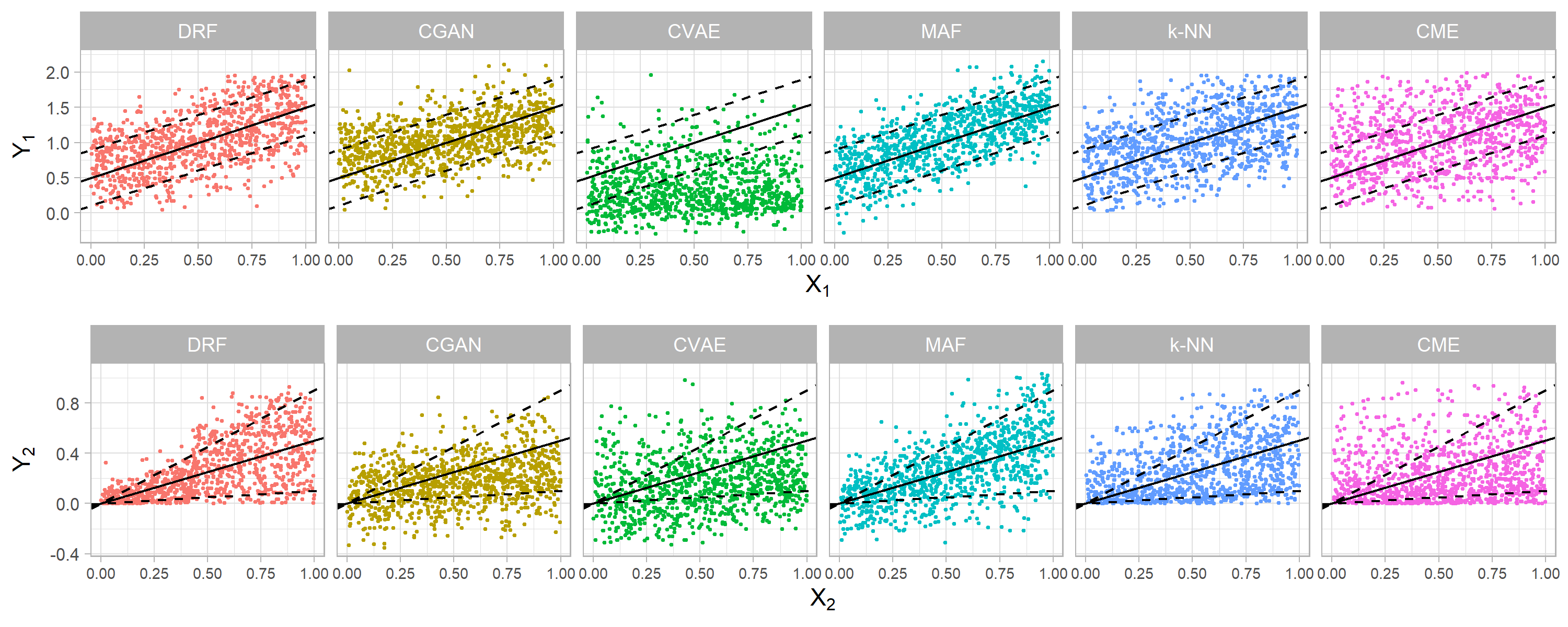

In addition to a few simple methods such as the -nearest neighbors or the kernel regression, which locally weight the training points, we also consider the CME estimator of Park and Muandet (2020) and several advanced machine learning methods such as the Conditional Generative Adversarial Network (CGAN) (Mirza and Osindero, 2014; Aggarwal et al., 2019), Conditional Variational Autoencoder (CVAE) (Sohn et al., 2015) and Masked Autoregressive Flow (Papamakarios et al., 2017). It is worth mentioning that the focus in the machine learning literature has been more on applications where is very large (e.g. pixels of an image) and is very small (such as image labels). Even though some methods do not provide the estimated conditional distribution in a form as simple as DRF, one is still able to sample from the estimated distribution and thus perform any subsequent analysis and make fair comparisons between the methods. For the CME estimator we simply set the negative weights to zero and renormalize, such that the weights are nonnegative and sum to one.

We first illustrate the estimated distributions by the above methods on a toy example where and

| (21) |

In the above example affects the mean of , whereas affects the both mean and variance of , and have no impact. The results can be seen in Figure 3. We see that, unlike some other methods, DRF is able to balance the importance of the predictors and and thus to estimate the distributions of and well.

One can do a more extensive comparison on a collection of real data sets. We use the benchmark data sets from the multi-target regression literature (Tsoumakas et al., 2011) together with some additional ones created from the data sets described throughout this paper. The performance of DRF is compared with the performance of other existing methods for nonparametric estimation of multivariate distributions by using the Negative Log Predictive Density (NLPD) loss, which evaluates the logarithm of the induced multivariate density estimate (Quinonero-Candela et al., 2005). As the number of test points grows to infinity, NLPD loss becomes equivalent to the average KL divergence between the estimated and the true conditional distribution and is thus able to capture how well one estimates the whole distribution, instead of only its mean.

In addition to the methods mentioned above, we also include some methods that are intended only for mean prediction, by assuming that the distribution of the response around its mean is homogeneous, i.e. that the conditional distribution does not depend on . This is fitted by regressing each component of separately on and using the pooled residuals. We consider the standard nonparametric regression methods such as Random Forest (Breiman, 2001), XGBoost (Chen and Guestrin, 2016), and Deep Neural Networks (Goodfellow et al., 2016).

| jura | slump | wq | enb | atp1d | atp7d | scpf | sf1 | sf2 | copula | wage | births1 | births2 | air | |

| 359 | 103 | 1K | 768 | 337 | 296 | 143 | 323 | 1K | 5K | 10K | 10K | 10K | 10K | |

| 15 | 7 | 16 | 8 | 370 | 370 | 8 | 21 | 22 | 10 | 73 | 23 | 24 | 15 | |

| 3 | 3 | 14 | 2 | 6 | 6 | 3 | 3 | 6 | 2 | 2 | 2 | 4 | 6 | |

| DRF | 3.9 | 4.0 | 22.5 | 2.1 | 7.3 | 7.0 | 2.0 | -24.2 | -24.3 | 2.8 | 2.8 | 2.5 | 4.2 | 8.5 |

| CGAN | 10.8 | 5.3 | 27.3 | 3.5 | 10.4 | 363 | 4.8 | 9.8 | 21.1 | 5.8 | 360 | 2.4 | 1K | 11.8 |

| CVAE | 4.8 | 37.8 | 36.8 | 2.6 | 1K | 1K | 108.8 | 8.6 | 1K | 2.9 | 1K | 1K | 49.7 | 9.6 |

| MAF | 4.6 | 4.5 | 23.9 | 3.0 | 8.0 | 8.1 | 2.6 | 4.7 | 3.8 | 2.9 | 3.0 | 2.5 | 1K | 8.5 |

| k-NN | 4.5 | 5.0 | 23.4 | 2.4 | 8.8 | 8.6 | 4.1 | -22.4 | -19.7 | 2.9 | 2.8 | 2.7 | 4.4 | 8.8 |

| kernel | 4.1 | 4.2 | 23.0 | 2.0 | 6.6 | 7.1 | 2.9 | -23.0 | -20.6 | 2.8 | 2.9 | 2.6 | 4.3 | 8.4 |

| RF | 7.1 | 12.1 | 35.2 | 5.7 | 12.7 | 13.3 | 16.7 | 3.9 | 2.2 | 5.8 | 6.1 | 5.0 | 8.3 | 13.9 |

| XGBoost | 11.4 | 38.3 | 25.9 | 3.0 | 1K | 1K | 1K | 0.3 | 1.6 | 3.5 | 2.9 | 1K | 1K | 12.8 |

| DNN | 4.0 | 4.2 | 23.3 | 2.6 | 8.6 | 8.7 | 2.6 | 2.3 | 2.2 | 2.9 | 3.0 | 2.6 | 5.4 | 8.6 |

| CME | 3.2 | 4.9 | 23.2 | 2.9 | 8.5 | 8.4 | 2.5 | -24.4 | -24.3 | 2.8 | 3.5 | 3.8 | 15.2 | 8.8 |

The results are shown in Table 1. We see that DRF performs well for a wide range of sample size and problem dimensionality, especially in problems where is large and is moderately big. It does so without the need for any tuning or involved numerical optimization.

4.2 Estimation of Statistical Functionals

Because DRF represents the estimated conditional distribution in a convenient form by using weights , a plug-in estimator of many common real-valued statistical functionals can be easily constructed from .

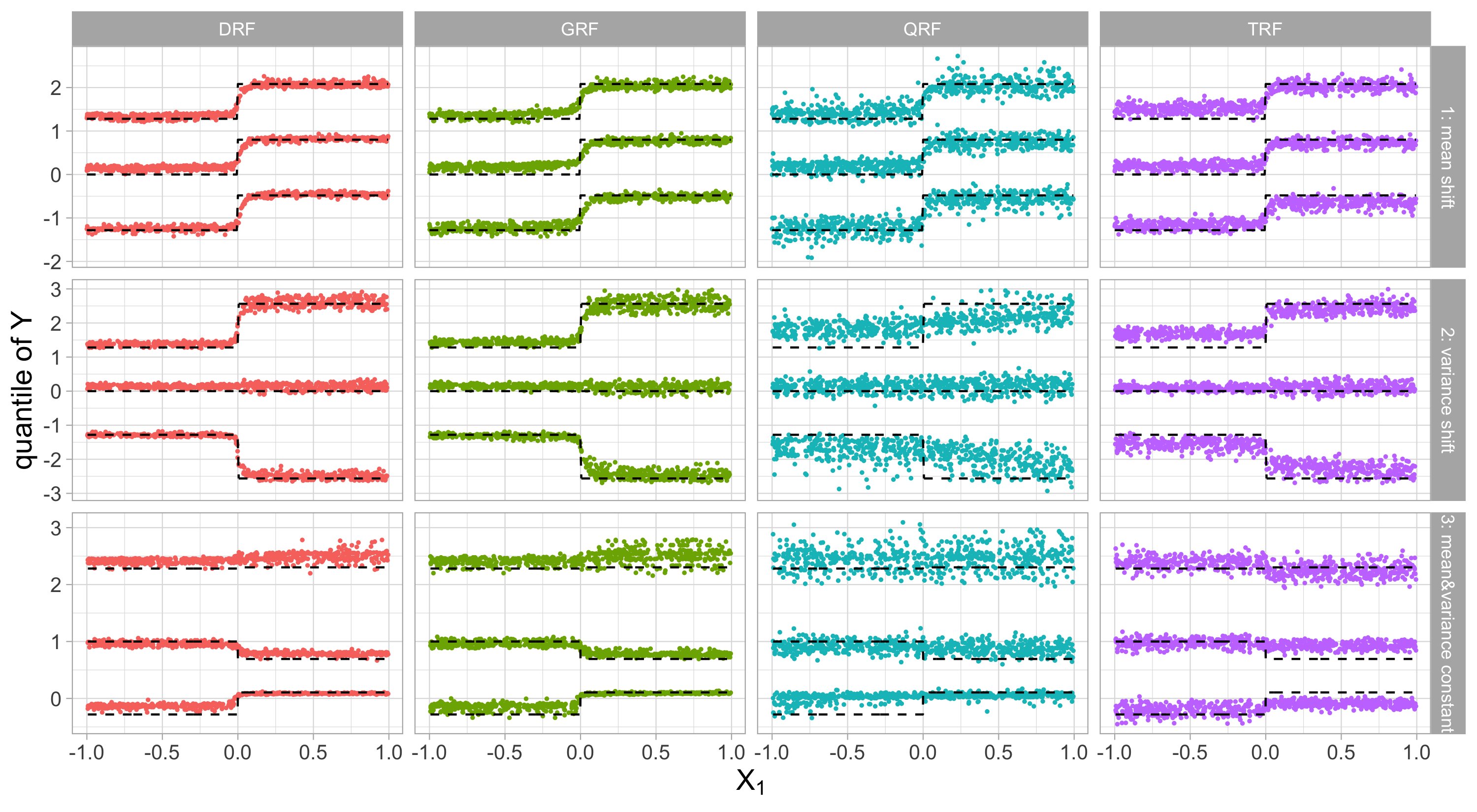

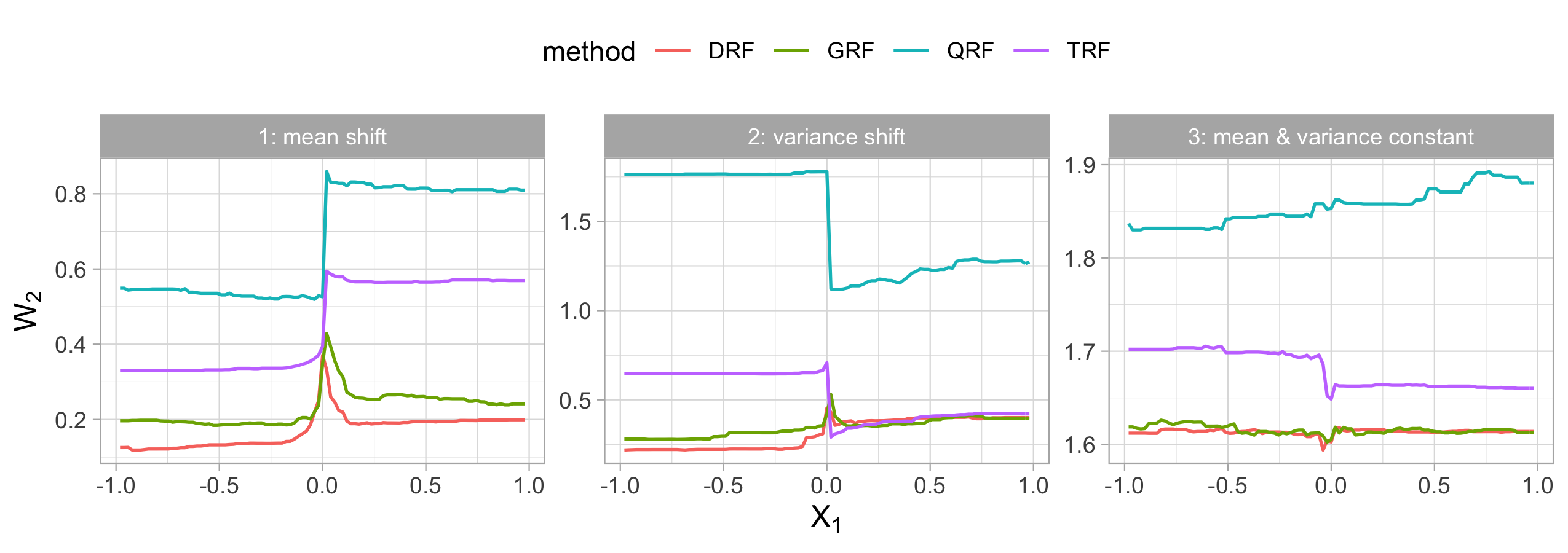

We first investigate the performance for the classical problem of univariate quantile estimation on simulated data. We consider the following three data generating mechanisms with and :

-

•

Scenario 1: (mean shift based on )

-

•

Scenario 2: (variance shift based on )

-

•

Scenario 3: (distribution shift based on , constant mean and variance)

The first two scenarios correspond exactly to the examples given in Athey et al. (2019).

In Figure 4 we can see the corresponding estimates of the conditional quantiles for DRF, Quantile Regression Forest (QRF) (Meinshausen, 2006), which uses the same forest construction with CART splitting criterion as the original Random Forest (Breiman, 2001) but estimates the quantiles from the induced weighting function, Generalized Random Forests (GRF) (Athey et al., 2019) with a splitting criterion specifically designed for quantile estimation and Transformation Forests (TRF) (Hothorn and Zeileis, 2021). We see that DRF is performing very well even compared to methods that are specifically tailored to quantile estimation.

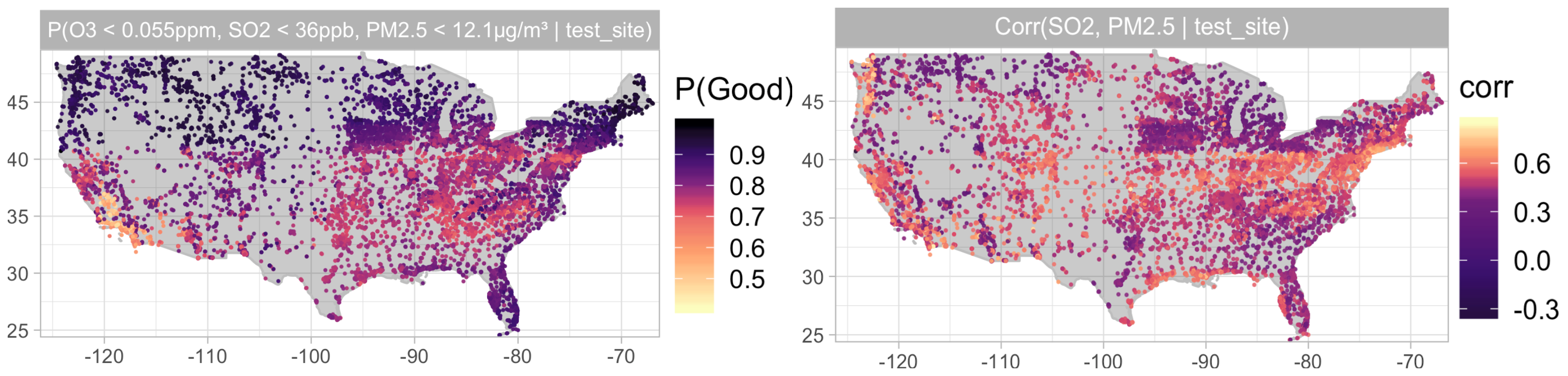

The multivariate setting is however more interesting, as one can use DRF to compute much more interesting statistical functionals . We illustrate this in Figure 5 for the air quality data set, described in Section 2.2. The left plot shows one value of the estimated multivariate CDF, specifically the estimated probability of the event that the air quality index (AQI) is at most at a given test site. This corresponds to the ”Good” category and means that the amount of every air pollutant is below a certain threshold determined by the EPA. Such probability estimates can be easily obtained by summing the weights of the training points belonging to the event of interest. For both plots in Figures 2 and 5, we train the single DRF with the same set of predictor variables and take the three pollutants O3, SO2 and PM as the responses. In this way we still have training data from many different sites.

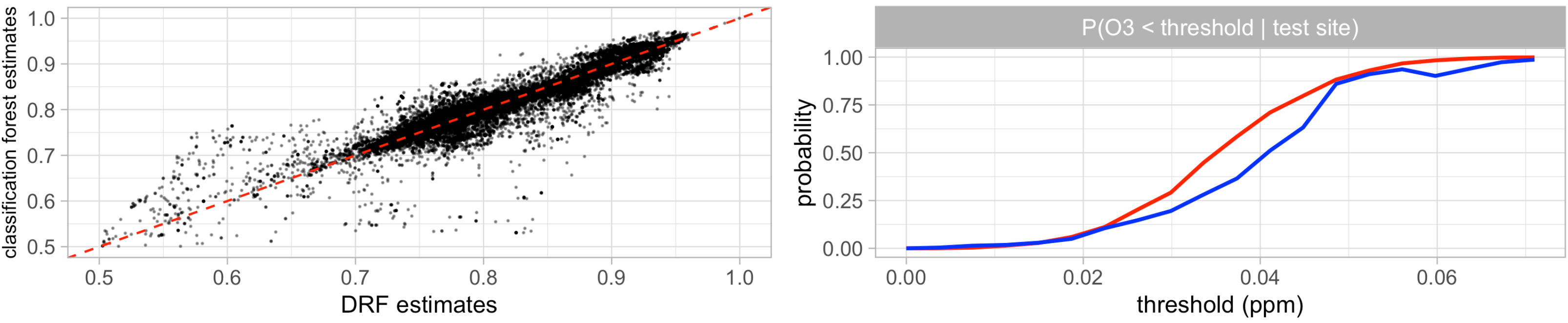

In order to investigate the accuracy of the conditional CDF obtained by DRF, we compare the estimated probabilities with estimates of the standard univariate classification forest (Breiman, 2001) with the response . In the left plot of Figure 6, we can see that the DRF estimates of the (also visualized in Figure 5) are quite similar to the estimates of the classification forest predicting the outcome . Furthermore, the cross-entropy loss evaluated on the held-out measurements equals and respectively, showing almost no loss of precision. In general, estimating the simple functionals from the weights provided by DRF comes usually at a small to no loss compared to the classical methods specifically designed for this task.

In addition to the classical functionals in the form of an expectation or a quantile for some function , which can also be computed by solving the corresponding one-dimensional problems, additional interesting statistical functionals with intrinsically multivariate nature that are not that simple to estimate directly are accessible by DRF, such as, for example, the conditional correlations . As an illustration, the estimated correlation of the sulfur dioxide () and fine particulate matter (PM2.5) is shown in the right plot of Figure 5. The plot reveals also that the local correlation in many big cities is slightly larger than in its surroundings, which can be explained by the fact that the industrial production directly affects the levels of both pollutants.

A big advantage of the target-free forest construction of DRF is that all subsequent targets are computed from same the weighting function obtained from a single forest fit. First, this is computationally more efficient, since we do not need for every target of interest to fit the method specifically tailored to it. For example, estimating the CDF with classification forests requires fitting one forest for each function value. Secondly and even more importantly, since all statistical functionals are plug-in estimates computed from the same weighting function, the obtained estimates are mathematically well-behaved and mutually compatible. For example, if we estimate by separately estimating the terms , , and , one can not in general guarantee the estimate to be in the range , but this is possible with DRF. Alternatively, the correlation or covariance matrices that are estimated entrywise are guaranteed to be positive semi-definite if one uses DRF. As an additional illustration, Figure 6 shows that the estimated (univariate) CDF using the classification forest need not be monotone due to random errors in each predicted value, which can not happen with the DRF estimates.

4.3 Conditional Copulas and Conditional Independence Testing

One can use the weighting function not only to estimate certain functionals, but also to obtain more complex objects, such as, for example, the conditional copulas. The well-known Sklar’s theorem (Sklar, 1959) implies that at a point , the conditional CDF can be represented by a CDF on , the conditional copula at , and conditional marginal CDFs for , as follows:

| (22) |

Copulas capture the dependence of the components by the joint distribution of the corresponding quantile levels of the marginal distributions: . Decomposing the full multivariate distribution to marginal distributions and the copula is a very useful technique used in many fields such as risk analysis or finance (Cherubini et al., 2004). Using DRF enables us to estimate copulas conditionally, either by fitting certain parametric model or nonparametrically, directly from the weights.

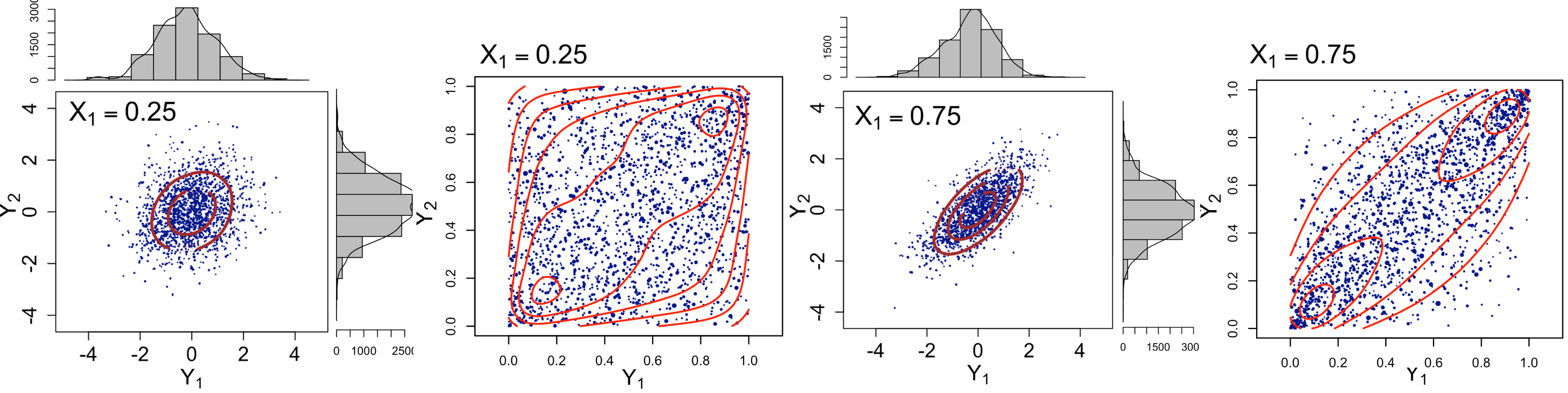

To illustrate this, consider an example where the -dimensional is generated from the equicorrelated Gaussian copula conditionally on the covariates with distribution , where and . All have a distribution marginally, but their conditional correlation for is given by . Figure 7 shows that DRF estimates the full conditional distribution at different test points quite accurately and thus we can obtain a good nonparametric estimate of the conditional copula as follows. First, for each component , we compute the corresponding marginal CDF estimate from the weights. Second, we map each response . The copula estimate is finally obtained from the weighted distribution , from which we sample the points in Figure 7 in order to visualize the copula.

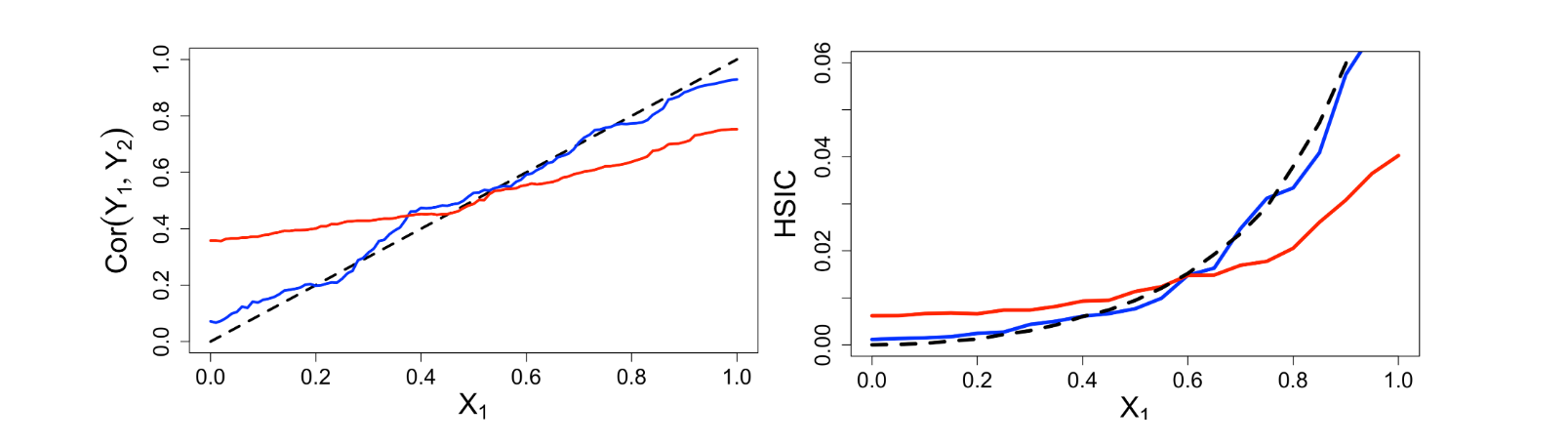

If we want to instead estimate the copula parametrically, we need to find the choice of parameters for a given model family which best matches the estimated conditional distribution, e.g. by weighted maximum likelihood estimation (MLE). For the above example, the correlation parameter of the Gaussian copula can be estimated by computing the weighted correlation with weights . The left plot in Figure 8 shows the resulting estimates of the conditional correlation obtained from , which uses the MMD splitting criterion (12) described in Section 2.3.1, and , which aggregates the marginal CART criteria (Kocev et al., 2007; Segal and Xiao, 2011). We see that is able to detect the distributional heterogeneity and provide good estimates of the conditional correlation. On the other hand, cannot detect the change in distribution of caused by that well. The distributional heterogeneity can not only occur in marginal distribution of the responses (a case extensively studied in the literature), but also in their interdependence structure described by the conditional copula , as one can see from decomposition (22). Since relies on a distributional metric for its splitting criterion, it is capable of detecting any change in distribution (Gretton et al., 2007a), whereas aggregating marginal CART criteria for in only captures the changes in the marginal means.

This is further illustrated for a related application of conditional independence testing, where we compute some dependence measure from the obtained weights. For example, we can test the independence conditionally on the event by using the Hilbert Schmidt Independence Criterion (HSIC) (Gretton et al., 2007b), which measures the difference between the joint distribution and the product of the marginal distributions. The right plot of Figure 8 shows that the estimates are quite close to the population value of the HSIC, unlike the ones obtained by .

4.4 Heterogeneous Regression and Causal Effect Estimation

In this and the following section, we illustrate that, in addition to direct estimation of certain targets, DRF can also be a useful tool for complex statistical problems and applications, such as causality.

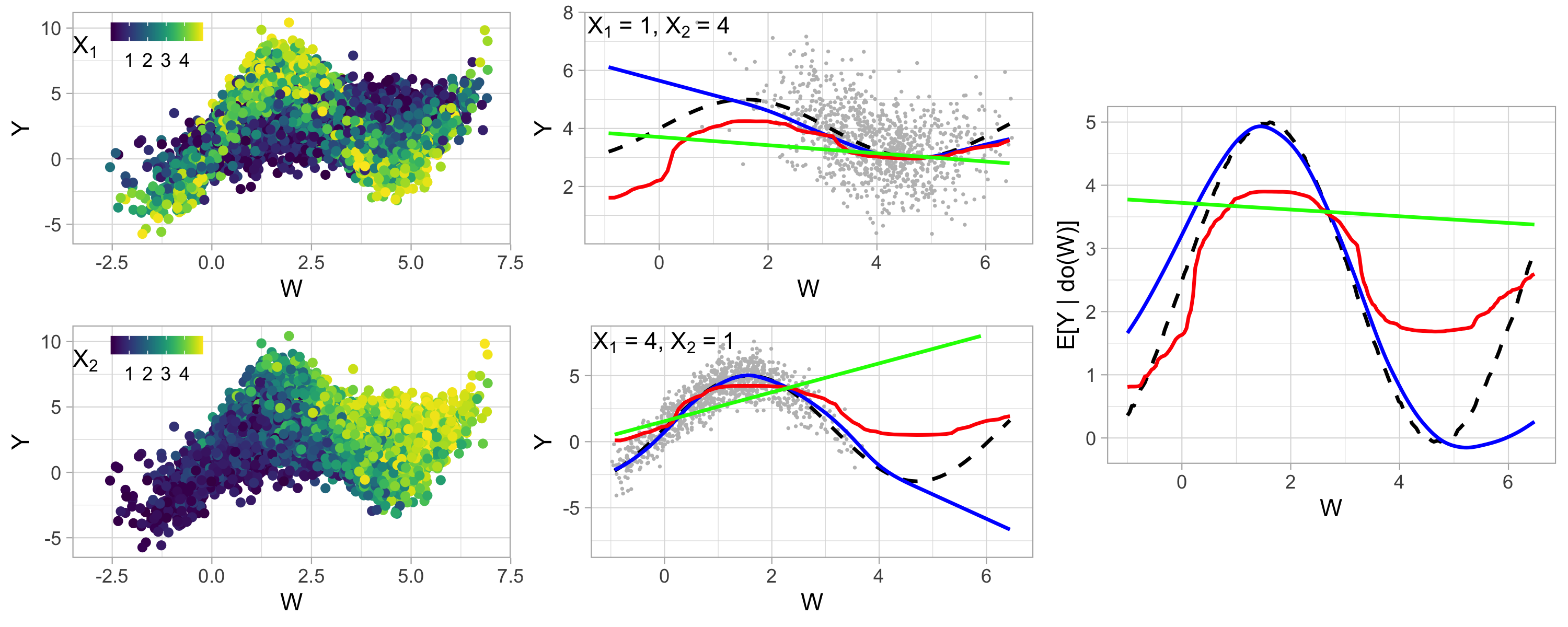

Suppose we would like to investigate the relationship between some (univariate) quantity of interest and certain predictors from heterogeneous data, where the change in distribution of can be explained by some other covariates . Very often in causality applications, is a (multivariate) treatment variable, is the outcome, which is commonly, but not necessarily, binary, and is a set of observed confounding variables for which we need to adjust if we are interested in the causal effect of on . This is illustrated by the following causal graph:

The problem of nonparametric confounding adjustment is hard; not only can the marginal distributions of and be affected by , thus inducing spurious associations due to confounding, but the way how affects can itself depend on , i.e. the treatment effect might be heterogeneous. The total causal effect can be computed by using the adjustment formula (Pearl, 2009):

| (23) |

In general, implementing do-calculus for finite samples and potentially non-discrete data might not be straightforward and comes with certain difficulties. In this case, the standard approach would be to estimate the conditional mean nonparametrically by regressing on with some method of choice and to average out the estimates over different sampled from the observed distribution of . Using DRF for this approach is not necessary, but has an advantage that one can easily estimate the full interventional distribution and not only the interventional mean .

Another way of computing the causal effect, which allows to add more structure to the problem, is explained in the following: We use DRF to first fit the forest with the multivariate response and the predictors . In this way, one can for any point of interest obtain the joint distribution of conditionally on the event and then the weights can be used as an input for some regression method for regressing on in the second step. This conditional regression fit might be of an independent interest, but it can also be used for estimating the causal effect from (23), by averaging the estimates over , where is sampled from the empirical observation of . In this way one can efficiently exploit and incorporate any prior knowledge of the relationship between and , such as, for example, monotonicity, smoothness or that it satisfies a certain parametric regression model, without imposing any assumptions on the effect of on . Furthermore, one might be able to better extrapolate to the regions of space where is small, compared to the standard approach which computes directly, by regressing on . Extrapolation is crucial for causal applications, since for computing we are interested in what would happen with when our treatment variable is set to be , regardless of the value achieved by . However, it can easily happen that for this specific combination of and there are very few observed data points, thus making the estimation of the causal effect hard (Pearl, 2009).

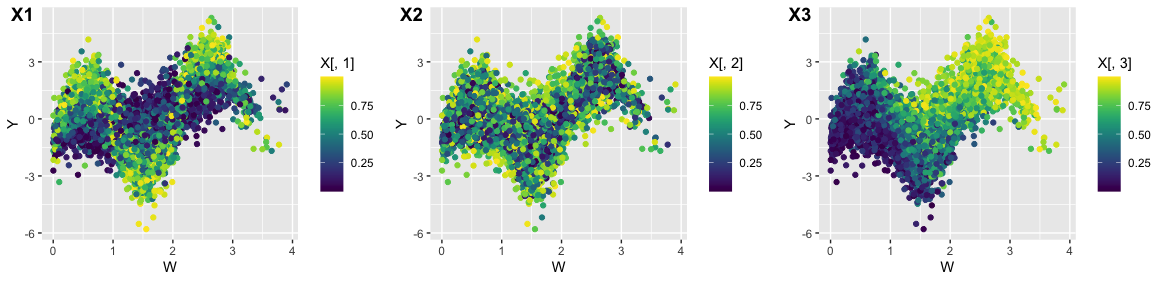

As an illustration, we consider the following synthetic data example, with continuous outcome , continuous univariate treatment , and :

| (24) |

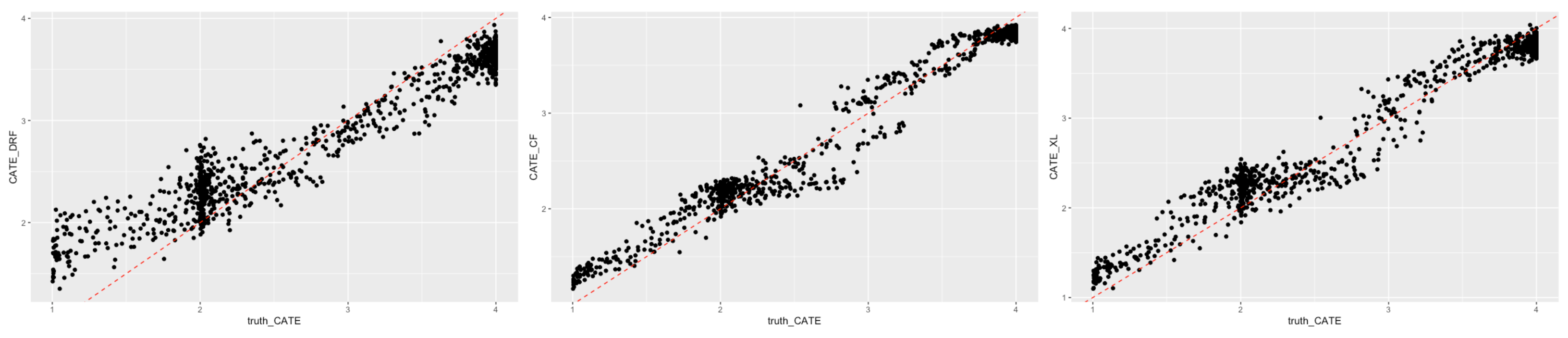

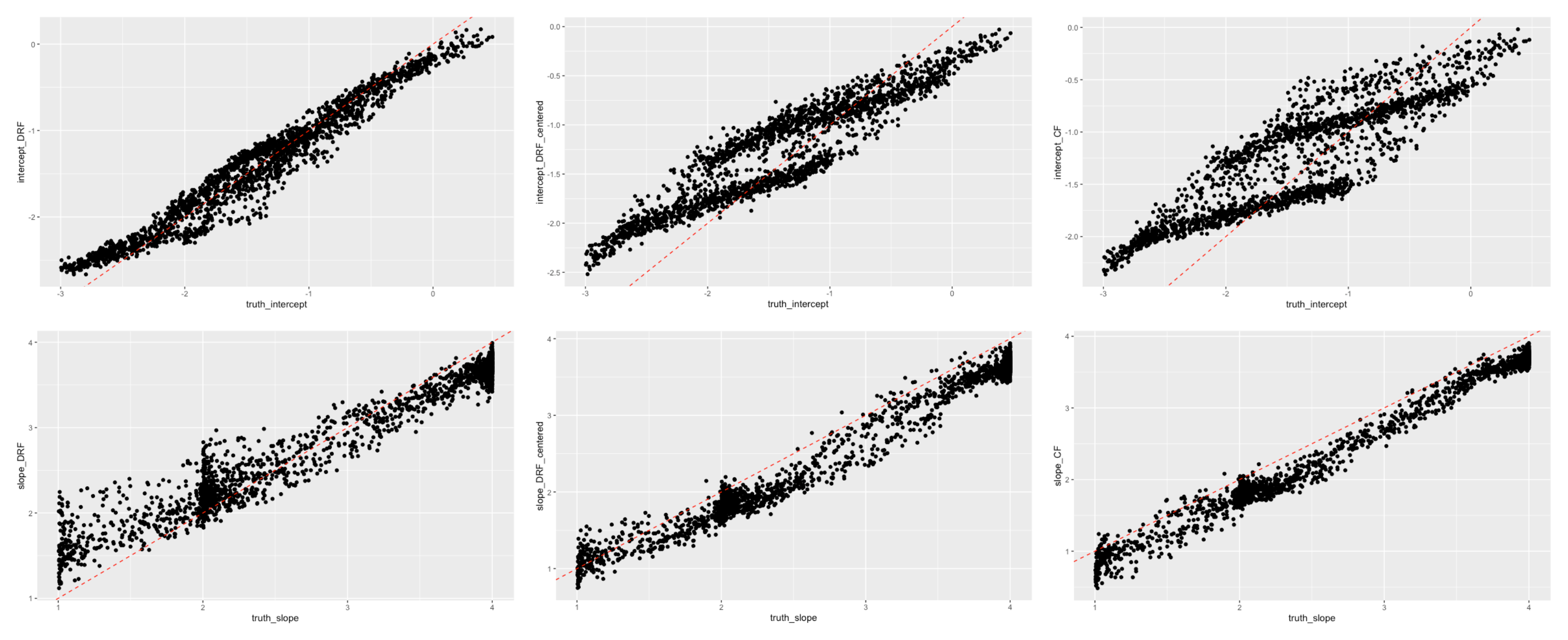

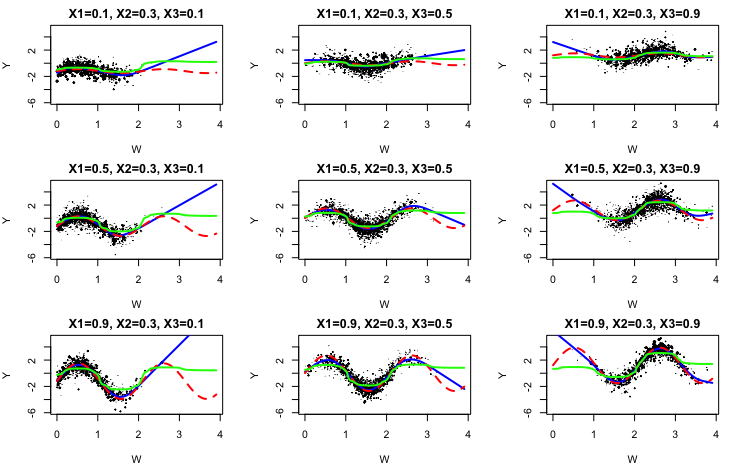

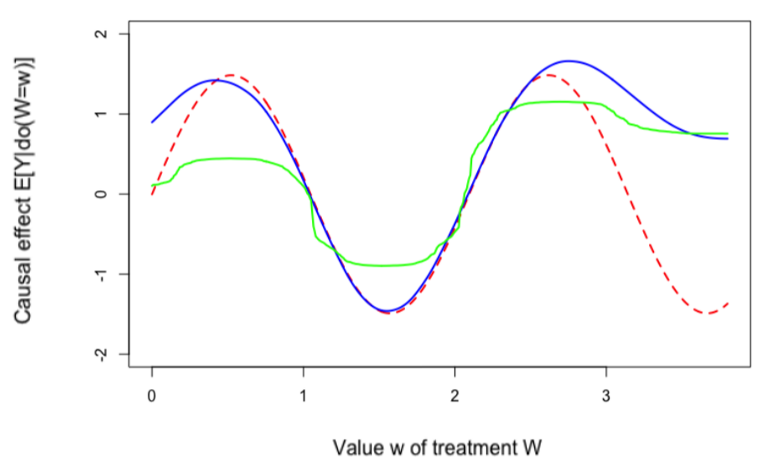

A visualization of the data can be seen on the left side of Figure 9; treatment affects nonlinearly, is a confounding variable that affects the marginal distributions of and and makes the treatment effect heterogeneous. The middle part of Figure 9 shows the conditional regression fits, i.e. the estimates of as varies and is fixed. In general, the conditional regression fit is related to the concept of the conditional average treatment effect (CATE) as it quantifies the effect of on for the subpopulation for which . We see that combination of DRF with response and predictors with the smoothing splines regression of on (blue curve) is more accurate than the estimates obtained by standard Random Forest (Breiman, 2001) with response and predictors (red curve). Furthermore, we see that the former approach can extrapolate better to regions with small number of data points, which enables us to better estimate the causal effect from (23), by averaging the corresponding estimates of over observed , as shown in the right plot of Figure 9.

There exist many successful methods in the literature for estimating the causal effects and the (conditional) average treatment effects for a wide range of settings (Abadie and Imbens, 2006; Chernozhukov et al., 2018; Wager and Athey, 2018; Künzel et al., 2019). However, some methods are not designed for the most general case and make certain modeling assumptions or are designed specifically for the (very common) case where the treatment variable is univariate or even binary. Due to its versatility, DRF can easily be used when the underlying assumptions of conventional methods are violated, when some additional structure is given in the problem or for the general, nonparametric, settings (Imbens, 2004; Ernest and Bühlmann, 2015; Kennedy et al., 2017). Appendix D contains additional comparisons with some existing methods for causal effect estimation.

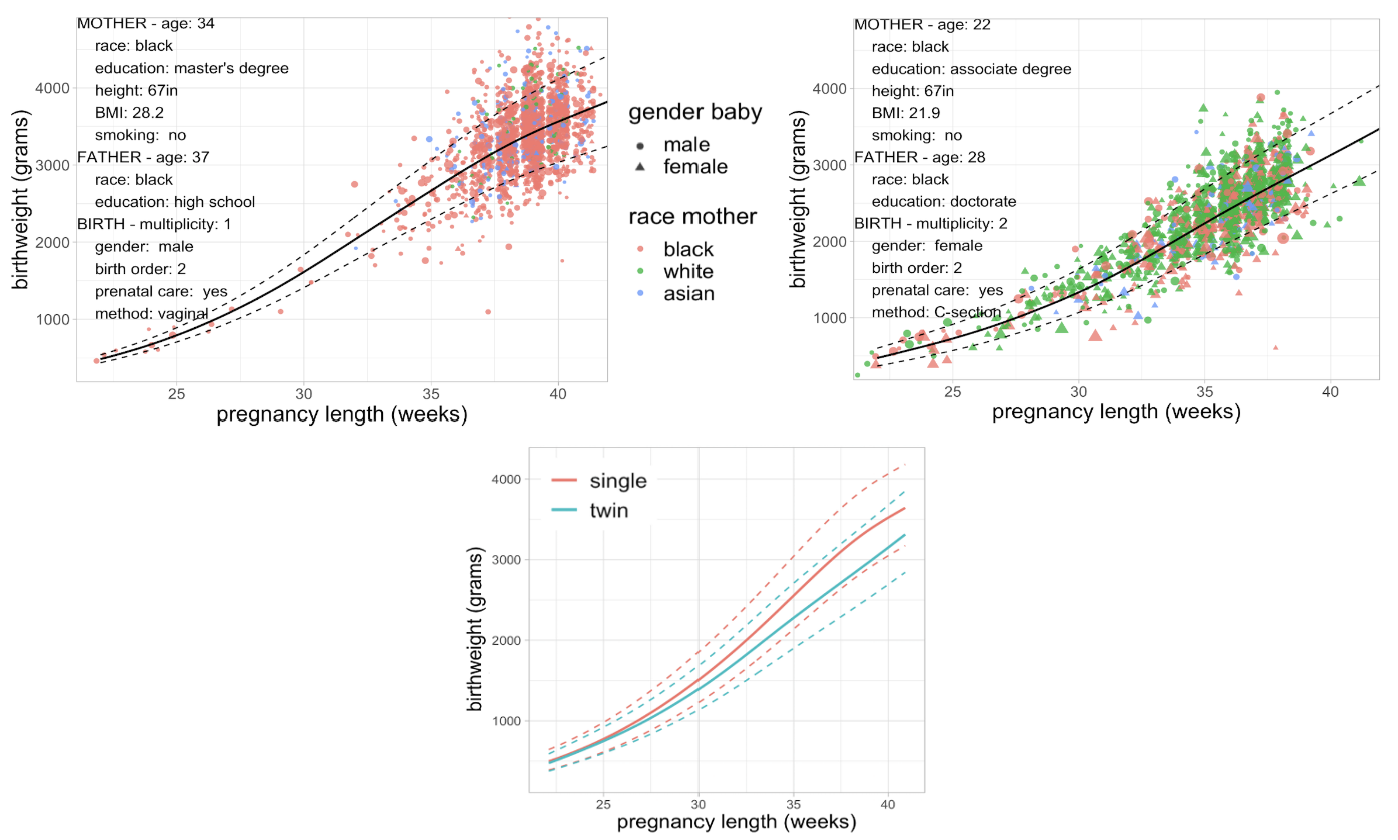

4.4.1 Births data

We further illustrate the applicability of DRF for causality-related problems on the natality data obtained from the Centers for Disease Control and Prevention (CDC) website, where we have information about all recorded births in the USA in 2018. We investigate the relationship between the pregnancy length and the birthweight, an important indicator of baby’s health. Not only is this relationship complex, but it also depends on many different factors, such as parents’ race, baby’s gender, birth multiplicity (single, twins, triplets…) etc. In the left two plots of Figure 10 one can see the estimated joint distribution of birthweight and pregnancy length conditionally on many different covariates, as indicated in the plot. The black curves denote the subsequent regression fit, based on smoothing splines. In addition to the estimate of the mean, indicated by the solid curve, we also include the estimates of the conditional - and -quantiles, indicated by dashed curves, which is very useful in practice for determining whether a baby is large or small for its gestational age. Notice how DRF assigns less importance to the mother’s race when the point of interest is a twin (middle plot), as in this case more weight is given to twin births, regardless of the race of the parents.

Suppose now we would like to understand how a twin birth causally affects the birthweight , but ignoring the obvious indirect effect due to shorter pregnancy length . For example, sharing of resources between the babies might have some effect on their birthweight. We additionally need to be careful to adjust for other confounding variables , such as, for example, the parents’ race, which can affect and . We assume that this is represented by the following causal graph:

In order to answer the above question, we investigate the causal quantity . Even though one cannot make such do-intervention in practice, this quantity describes the total causal effect if the birth multiplicity and the length of the pregnancy could be manipulated and thus for a fixed pregnancy length , we can see the difference in birthweight due to . We compute this quantity as above, by using DRF with subsequent regression fits, which has the advantage of better extrapolating to regions with small probability, such as long twin pregnancies (see the middle plot of Figure 10). In the right plot of Figure 10 we show the mean and quantiles of the estimated interventional distribution and we see that, as one might expect, a twin birth causes smaller birthweight on average, with the difference increasing with the length of the pregnancy.

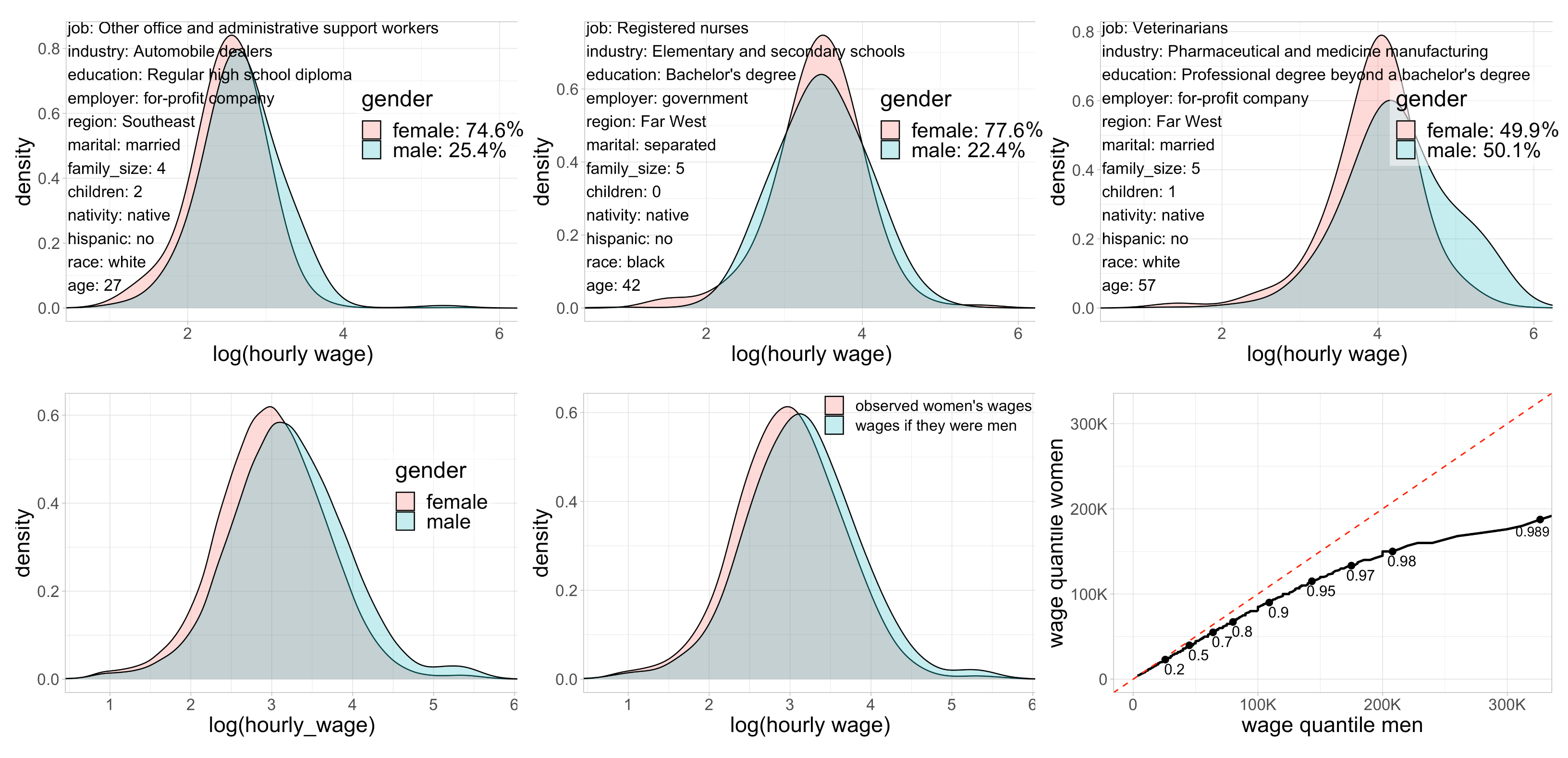

4.5 Fairness

Being able to compute different causal quantities with DRF could prove useful in a range of applications, including fairness (Kusner et al., 2017). We investigate the data on approximately million full-time employees from the 2018 American Community Survey by the US Census Bureau from which we have extracted the salary information and all covariates that might be relevant for salaries. In the bottom left plot of Figure 11 one can see the distribution of hourly salary of men and women (on the logarithmic scale). The overall salary was scaled with working hours to account for working part-time and for the fact that certain jobs have different working hours. We can see that men are paid more in general, especially for the very high salaries. The difference between the median hourly salaries, a commonly used statistic in practice, amounts for this data set.

We would like to answer whether the observed gender pay gap in the data is indeed unfair, i.e. only due to the gender, or whether it can at least in part be explained by some other factors, such as age, job type, number of children, geography, race, attained education level and many others. Hypothetically, it could be, for example, that women have a preference for jobs that are paid less, thus causing the gender pay gap.

In order to answer this question, we assume that the data is obtained from the following causal graph, where denotes the gender, the hourly wage and all other factors are denoted by :

i.e. is a source node and is a sink node in the graph. In order to determine the direct effect of the gender on wage that is not mediated by other factors, we would like to compute the distribution of the nested counterfactual , which is interpreted as the women’s wage had they been treated in same way as men by their employers for determining the salary, but without changing their propensities for other characteristics, such as the choice of occupation (Chernozhukov et al., 2013). Therefore, it can be obtained from the observed distribution as follows:

| (25) |

Put in the language of the fairness literature, it quantifies the unfairness when all variables are assumed to be resolving (Kilbertus et al., 2017), meaning that any difference in salaries directly due to factors is not viewed as gender discrimination. For example, one does not consider unfair if people with low education level get lower salaries, even if the gender distribution in this group is not balanced.

There are several ways how one can compute the distribution of from (25) with DRF. The most straightforward option is to take as the response and as predictors in order to compute the conditional distribution . However, with this approach it could happen that for predicting we also assign weight to training data points for which . This happens if in some trees we did not split on variable , which is likely, for example, if is low. Using salaries of both genders to estimate the distribution of men’s salaries might be an issue if our goal is to objectively compare how women and men are paid.

Another approach is to take as a multivariate response and as the predictors for DRF and thus obtain joint distribution of conditionally on the event . In this way we can also quantify the gender discrimination of a single individual with characteristics by comparing his/her salary to the corresponding quantile of the salary distribution of people of the opposite gender with the same characteristics (Plečko and Meinshausen, 2020). This is interesting because the distribution of salaries, and thus also the gender discrimination, can be quite different depending on other factors such as the industry sector or job type, as illustrated for a few choices of in the top row of Figure 11.

Finally, by averaging the DRF estimates of , conveniently represented via the weights, over different sampled from the distribution , we can compute the distribution of the nested counterfactual (Chernozhukov et al., 2013). In the middle panel in the bottom row of Figure 11 a noticeable difference in the means, also called natural direct effect in the causality literature (Pearl, 2009), is still visible between the observed distribution of women’s salaries and the hypothetical distribution of their salaries had they been treated as men, despite adjusting for indirect effects of the gender via covariates . By further matching the quantiles of the counterfactual distribution with the corresponding quantiles of the observed distribution of men’s salaries in the bottom right panel of Figure 11, we can also see that the adjusted gender pay gap even increases for larger salaries. Median hourly wage for women is still lower than the median wage for the hypothetical population of men with exactly the same characteristics as women, indicating that only a minor proportion of the actually observed hourly wage difference of can be explained by other demographic factors.

5 Conclusion

We have shown that DRF is a flexible, general and powerful tool, which exploits the well-known properties of the Random Forest as an adaptive nearest neighbor method via the induced weighting function. Not only does it estimate multivariate conditional distributions well, but it constructs the forest in a model- and target-free way and is thus an easy to use out-of-the-box algorithm for many, potentially complex, learning problems in a wide range of applications, including also causality and fairness, with competitive performance even for problems with existing tailored methods.

Appendix A Implementation Details

Here we present the implementation of the Distributional Random Forests (DRF) in detail. The code is available in the R-package drf and the Python package drf. The implementation is based on the implementations of the R-packages grf (Athey et al., 2019) and ranger (Wright and Ziegler, 2017). The largest difference is in the splitting criterion itself and the provided user interface. Algorithm 1 gives the pseudocode for the forest construction and computation of the weighting function .

-

•

Every tree is constructed based on a random subset of size (taken to be of the size of the training set by default) of the training data set, similar to Wager and Athey (2018). This differs from the original Random Forest algorithm (Breiman, 2001), where the bootstrap subsampling is done by drawing from the original sample with replacement.

-

•

The principle of honesty (Biau, 2012; Denil et al., 2014; Wager and Athey, 2018) is used for building the trees (line 4), whereby for each tree one first performs the splitting based on one random set of data points , and then populates the leaves with a disjoint random set of data points for determining the weighting function . This prevents overfitting, since we do not assign weight to the data points which we used to built the tree.

-

•

We borrow the method for selecting the number of candidate splitting variables from the grf package (Athey et al., 2019). This number is randomly generated as , where mtry is a tuning parameter. This differs from the original Random Forests algorithm, where the number of splitting candidates is fixed to be mtry.

-

•

The number of trees built is by default.

-

•

The factor variables in both the responses and the predictors are encoded by using the one-hot encoding, where we add an additional indicator variable for each level of some factor variable . This implies that in the building step, if we split on this indicator variable, we divide the current set of data points in the sets where and . This works well if the number of levels is not too big, since otherwise one makes very uneven splits and the dimensionality of the problem increases significantly. Handling of categorical problems is a general challenge for the forest based methods and is an area of active research (Johannemann et al., 2019). We will leave improving on this approach for the future development.

-

•

We try to enforce splits where each child has at least a fixed percentage (chosen to be as the default value) of the current number of data points. In this way we achieve balanced splits and reduce the computational time. However, we cannot enforce this if we are trying to split on the variable with only a few unique values, e.g. indicator variable for a level of some factor variable.

-

•

All components of the response are scaled for the building step (but not when we populate the leaves). This ensures that each component of the response contributes equally to the kernel values, and consequently to the MMD two-sample test statistic. Plain usage of the MMD two-sample test would scale the components of at each node. However, this approach favors always splitting on the same variables, even though their effect will diminish significantly after having split several times.

-

•

By default, in step 20 of the Algorithm 1, we use the MMD-based splitting criterion given by