Non-concave expected utility optimization with uncertain time horizon

Abstract

We consider an expected utility maximization problem where the utility function is not necessarily concave and the time horizon is uncertain. We establish a necessary and sufficient condition for the optimality for general non-concave utility function in a complete financial market. We show that the general concavification approach of the utility function to deal with non-concavity, while being still applicable when the time horizon is a stopping time with respect to the financial market filtration, leads to sub-optimality when the time horizon is independent of the financial risk, and hence can not be directly applied. For the latter case, we suggest a recursive procedure which is based on the dynamic programming principle. We illustrate our findings by carrying out a multi-period numerical analysis for optimal investment problem under a convex option compensation scheme with random time horizon. We observe that the distribution of the non-concave portfolio in both certain and uncertain random time horizon is right-skewed with a long right tail, indicating that the investor expects frequent small losses and a few large gains from the investment. While the (certain) average time horizon portfolio at a premature stopping date is unimodal, the random time horizon portfolio is multimodal distributed which provides the investor a certain flexibility of switching between the local maximizers, depending on the market performance. The multimodal structure with multiple peaks of different heights can be explained by the concavification procedure, whereas the distribution of the time horizon has significant impact on the amplitude between the modes.

1 Introduction

A classical problem in optimal control theory and mathematical finance is to maximize the expected reward or utility over all admissible terminal positions (portfolios) starting with an initial investment in the time horizon , where is given upfront and the objective (utility) function is a concave. Such a utility maximization problem in a continuous-time setting dates back to Merton [19] with the underlying stochastic processes representing a financial market. Merton’s pioneering work has been extended in several directions e.g. by assuming more general structures of preferences, by incorporating additional randomness to the underlying risk processes, or by including a risk constraint to the optimization problem, see among many others e.g. Biagini [5], Wong et al. [26], or Karatzas et al. [17] for a broad discussion.

In this work, we investigate an extension of the Merton problem to the case where the utility function is not necessarily concave and the time horizon is random.

Let us briefly mention some of the most relevant literature. Most optimal control-type problems have a fixed known time horizon. However, in reality such a natural fixed maturity does not exist and instead exogenous or endogenous events determine the end of the optimal control/optimal investment problem. An early paper by Yaari [27] looks at the investment problem of an individual with an uncertain time of death in a simplified case with purely deterministic investment opportunities. Yaari’s paper is extended to discrete-time settings with multiple risky assets. Optimal life-cycle consumption and investment is studied by Merton [19], where the time horizon uncertainty is reflected by the first jump of an independent Poisson process with constant intensity. Richard [23] solves in closed-form an optimal portfolio choice problem with an uncertain time of death and the presence of life insurance. In these works, the time horizon uncertainty can be treated as additional discount factor and closed-form solution can be provided by using dynamic programming principle for concave utility functions. A more complete setting for concave utility maximization with a continuous time horizon distribution in a complete financial market has been studied in Blanchet et al. [10]. Bouchard and Pham [11] investigate a concave utility maximization in an incomplete market with general uncertain time horizon structure. All the mentioned works leave the case where the objective utility is not necessarily concave e.g. [13] as an open problem. To the best of our knowledge, the non-concave utility maximization problem under random time horizon has not yet been investigated.

The literature of non-concave optimization with certain time horizon is vast, see for instance Aumann and Perles [2], Basak and Makarov [3], Bensoussan et al. [4], Bichuch and Sturm [8], Carassus and Pham [12], Carpenter [13], Chen et al. [14], Larsen [18], Reichlin [22], Rieger [24] and Ross[25]. For non-concave optimization with constraints see Nguyen and Stadje [20] or Dai et al. [15]. In these works in the finance and the OR literature the non-concavity arises typically from non-linear, option-type managerial compensations. Such remuneration schemes have been seen in industry as one way to overcome potential principal-agent issues and are supposed to align the incentives of managers with the ones of owners.

Another important application of non-concave investment problem relate to participating insurance contracts which have been extensively used in European and non-European life insurance markets, see the references provided in the introduction. Typically, to buy a participating insurance policy, the policyholder pays a lump sum premium upfront and the capital saved is invested in a self-financing way, subject to annual interest, where the insurance company offers a (minimal) guarantee. An example is given by so called “flexibility rider contract” which have gained popularity recently due to the current low interest rate development where the decision variable is the riskiness of the investment pool, see [14] and the references within.

In positive economic developments, the policyholder receives a surplus, while in case of bad economic developments, the insurance company carries the loss. Hence, a participating insurance contract may be regarded as an option-type financial instrument, leading to a non-concave utility function. In such a context our work to the best of our knowledge is the first one which is able to include the randomness of the lifetime into the investment problem (instead of simply assuming a fixed pre-specified time-horizon).

As we aim to obtain some explicit result in the illustration section, we extensively consider the option compensation problem in [13] where the utility function admits only one concavification interval but with a random time horizon which has a discrete distribution on the universal time interval . We remark that our results can be extended to settings with a continuous distribution time horizon.

Our contribution is fourth-fold. First, we show that when the time horizon is a stopping time with respect to the financial market filtration, the general approach of concavificiation techniques as described in [24] to deal with non-concavity can be applied. This is an extension of the result in [13], complementing the result in [11] (Proposition 4.3) to random time horizons in complete markets. Second, when is independent of the financial risk and the market is therefore incomplete, we establish necessary and sufficient conditions for the optimality for general utility functions. Third, also for the case where is independent of the financial risk, we show that optimizing the concavified version of the utility function will lead to sub-optimality with a potentially significant expected utility loss and suggest a recursive procedure which is based on the dynamic programming principle to solve the optimization problem in this situation. Fourth, we illustrate our finding by carrying out a multiple period numerical analysis for the non-concave option compensation problem with random time horizon thoroughly exploring the effect of randomness on managerial compensation schemes and participing insurance contracts. This is computationally challenging because the optimal multiplier obtained by the concavified problem in one period is a random variable that depends on the market realizations at the end of the previous period.

We numerically show that under an uncertain time horizon which imposes a new randomness that cannot be fully hedged by only using the available financial instruments, the concavified problem strategy is super-optimal and leads to an expected utility loss. In addition, due to concavification, the distribution of the wealth at exiting times of the non-concave optimization problems is right-skewed with a long right tail, indicating that the investor can expect frequent small losses and a few large gains from the investment. Intuitively, a positively skewed distribution of investment returns is generally desirable by the agent with option-liked compensation payoff because there is some probability to gain huge profits that can cover all the frequent small losses. Under the premature exiting risk, the wealth at an exiting time exhibits a bimodal distribution with peaks of different heights. The bimodal structure can be explained by the concavification procedure whereas the distribution of the exiting time has significant impact on the amplitude between the two modes. When the concavified utility at an exiting time is affine in many open intervals, the corresponding wealth is intuitively expected to be of multimodal distribution.

The remainder of the paper is organized as follows: First, we describe a specific complete financial market setting and introduce the uncertain investment time in Section 2. We present our necessary and sufficient condition for optimality for non-concave general utility functions in Section 3. We show that the concavification technique is not applicable in a non-concave setting with random time horizon which induces additional risk to the financial market, and derive a dynamic programming principle for such a non-concave optimization with uncertain time horizon in Section 4. In Section 5, we investigate the case of power utility and perform a numerical study for non-concave optimization with time horizon uncertainty. We study the case when the time horizon is a stopping time with respect to the financial market filtration in Section 6. Finally, Section 7 summarizes our main results.

2 Financial market and the optimal investment problem

Let with be the maximal time span of the economy and is -dimensional Brownian motion in a probability space .

2.1 The financial market

For the market setup, we assume that the prices of risky assets are modelled as a geometric Brownian motion, i.e.,

where the superscript denotes the -th entry of the corresponding vector or the entry in the -th row and -th colomn of a matrix and we use the subscript to denote the time index . We use the notation and for the corresponding vector or matrix, respectively. Additionally to these risky assets, we consider a bond , given by , where denotes the (deterministic) interest rate. The information in the market is captured by the augmented filtration generated by the Brownian motion, satisfying the usual conditions and is trivial. We assume that the coefficients , are bounded and deterministic and the volatility is bounded, deterministic, invertible with bounded inverse .

In this arbitrage-free financial market, there exists a unique equivalent martingale measure with Radon-Nikodym density as the solution of , where . Further we define . By Itô’s formula and

We consider the economy in the usual frictionless setting, where stocks and bonds are infinitely divisible and there are no market frictions, no transaction costs etc. Additional to the financial market setting, we consider a random time-horizon , where is a positive discrete random variable independent of . In particular, is not an -stopping time. Let with being the -algebra generated by . Define . can be extended to by defining for any . We note that any -martingale is also an -martingale.

2.2 Utility function

In the sequel we consider a general not necessarily concave utility function which is non-constant, increasing, continuous, has left- and right-hand side derivatives and satisfies the growth condition

| (2.1) |

We set for to avoid ambiguity and define . We do not assume that is concave or strictly increasing. In a concave setting, Equation (2.1) is equivalent to , which is part of the Inada condition. We note that Equation (2.1) and the assumption imply that there exists a concave function that dominates , i.e., . The following result explains why we can consider -predictable, instead of -predictable investment strategies.

Lemma 2.1

Suppose that . Then there exists a strategy :

Proof. Denote by for . Prop. 2.11 in [1] yields that the -predictable process can be expressed as where is -predictable and is a random function. Set . Then

This entails that and the lemma follows.

2.3 Admissible strategy

We consider an investor putting the amount in each risky asset at time . By considering a self-financing portfolio, the amount is invested in the bond. We use the notation for the wealth process at time , developed from an initial capital

at time under a self-financing strategy where denotes the amount invested in asset . Then evolves according to the stochastic differential equation

| (2.2) |

We call a portfolio admissible, if is progressively measurable w.r.t. , locally square-integrable, i.e., a.s., and the associated wealth process is non-negative. By Girsanov’s theorem as long as is locally square-integrable is always a local martingale. For the set of admissible portfolios with initial capital at time , we use the notation

| (2.3) |

We define as the discounted portfolio process.

3 Non-concave optimization problem with random time horizon

Assume that the agent evaluates his investment performance at times with respect to the weights , , and , with . Let be the set of all portfolios in that are progressively measurable with respect to , locally square-integrable with non-negative associated wealth process. In our complete financial market setup, we consider the problem

| (3.1) |

where the second equality holds by Lemma 2.1. Define

| (3.2) |

where by convention . Note that for , we have Furthermore, it is clear that the strategy

is locally square integrable. Denote by the corresponding wealth process (which is equal to at time for ). Note that is a non-negative local martingale (hence a supermartingale). We say that the supermartingale is generated by the -tuple .

The optimization problem (3.1) can be restated in the following way

| (3.3) |

Define

| (3.4) |

By continuity the supremum and infimum are attained so that is the smallest of the function . Below, denotes the right-hand side derivative of . The following result provides a sufficient condition for optimality of the optimization problem (3.3).

Theorem 3.1

Let . Suppose that there is an adapted process with such that the process generated by the -tuple is a martingale and is a constant. Then, solves the optimization problem (3.3).

Proof. Let which is a constant by assumption. Then for any for any by construction the process is a non-negative local martingale. Let be the corresponding localizing sequence. Then

Passing to the limit and using Fatou’s lemma yields

| (3.5) |

The process defines a density process of a probability measure as it is a martingale with initial value equal to 1. Due to the construction of it can be observed that . Therefore, we obtain

For any admissible we have

where we have used (3.5) in the last step. This implies the optimality of .

We now seek for a necessary condition for optimality. The following is the main theorem of this section which generalizes results by Blanchet et al. [10] to non-concave settings. Let be the right-hand side derivative of . We need the following assumption.

Assumption 1

We assume that is an optimal solution to Problem (3.3) such that for some , that is a square integrable martingale (instead of only a local martingale), and that with being a decreasing function with and

If (concave hull) for all for an and if is bounded on , we can choose . Denote by the set of all such that is not differentiable in and is a non-zero set for a . Note that, since is not defined on the negative half-line, is in particular not differentiable in . Denote the set of all with for at least one by , and let be its complement. In other words, the set contains at most scenarios with portfolio outcomes at a where the utility function is differentiable.

Theorem 3.2

Proof. If is a zero-set the theorem is obvious. So assume . Consider an admissible (non-negative) portfolio with terminal value of the form such that is a martingale. In particular, we consider a portfolio which at time agrees with on . We define for the functions and by and We denote the right-hand side derivative of a continuous function by and the left-hand side derivative by . Of course, in points where the function is differentiable both limits coincide and the “” and “” may be omitted, respectively. Note that is admissible so that is integrable. For we have . We calculate

Denote if and else. Under Assumption 1 we obtain

We know that the function attains its maximum at , since is the optimal solution by assumption. Hence, Thus,

Integration by parts yields

since by definition on and is differentiable for for each so that Hence,

| (3.6) |

We note that this equality holds for any admissible which is equal on , such that is a martingale. Define Thus, which is equivalent to

| (3.7) |

The theorem would follow if we can show that is constant on . Since

we have Hence, (3.7) implies

| (3.8) |

with . By Lemma 3.3 this entails that

| (3.9) |

for any bounded with satisfying on .

Now if or on we have that on and we are done (since and therefore, must be constant on ). On the other hand. if then

where the first equation holds as the wealth process is non-negative and by the definition of , since is not differentiable at For we can define Then on . Choose such that . Then by (3.9)

Hence, and thus , since By the definition of above this entails that is constant. To obtain the representation of , we recall our definition (for ) from the very beginning of this proof.

Lemma 3.3

for any -measurable bounded with satisfying on .

Proof. Note that (3.8) implies that

for any -measurable such that and is bounded. (Since this implies by Assumption 1 and the martingale representation theorem on that there exists a corresponding admissible with such that is a martingale.) In particular, for any bounded being -measurable such that and . By definition the wealth process, , is non-negative. By multiplying below with the positive constant , we see in particular that we must have

| (3.10) |

for all bounded -measurable with , such that on for a , and bounded by else. Since was arbitrary, (3.10) holds actually for any bounded -measurable with and on for some . Finally, suppose that an -measurable bounded satisfies if , and . Then define

with chosen such that . The existence of if is small is guaranteed by the intermediate value theorem. If we exclude the case that , then as . Furthermore, on so that satisfies (3.10). Hence,

4 Dynamic programming approach with random time horizon

Concavification has been widely applied to solve non-concave optimization problems, see e.g. [8, 12, 13, 14, 18, 22, 24, 25, 20] in various settings where the time horizon is fixed and the market is complete. The concavification argument is based on the fact that concavified hall strictly dominates the initial function only in a union of finite number of open intervals and is affine in this union. The key idea is that in order to gain more expected utility, it is possible to put all the expensive states to the left points of these intervals in the concavification region, keeping the budget constraint unchanged.

In this section, we show that the concavification technique may no longer be applicable in settings with a random time horizon. Furthermore, we derive a dynamic programming principle for such a non-concave optimization.

We will start with the following useful lemma, where with a slight abuse of notation we write instead of .

Lemma 4.1

Let have the same distribution as conditioned on and independent of . Then we have

Proof. Let Y be bounded and -measurable. By Jeulin (2006), Lemma 4.4 for some -measurable random variable and some family of -measurable random variables . Let have the same distribution as conditioned on and independent of . Then we have

from which the lemma follows by the definition of a conditional expectation.

Let have the same distribution as conditioned on . Let us define

and . We want to find . Below we show that follows the usual dynamic programming principle.

Proposition 4.2 (Dynamic Programming)

For any , we have

Proof. It is

We are now in a position to show that contrary to the case with a certain time horizon, concavifying the utility function is not applicable when the investment horizon is random. In other words, replacing with in the optimization (3.1) leads to a super-optimal strategy. To this end, we need to investigate smoothness and concavity of the value function of the certain time horizon optimization problem

| (4.1) |

Smoothness and concavity of the value function has been also studied in [6] by working on the dual control problem and the dual HJB equation under the following assumption which we in the sequel will make as well §§§It is shown in [7] that the continuity assumption of can be dropped under a Hölder continuity condition (Theorem 4.2) by using the comparison principle of PDEs for the dual control problem.:

Assumption (H): , and is strictly increasing and for some constant and .

Proposition 4.3

Under Assumption (H), the value function of Problem (4.1) is strictly concave and strictly increasing and in . Furthermore, , and for some positive constant and satisfies the Inada’s condition at zero and infinity.

Proof. By Theorem 4.1 in [22] the concavification argument can be applied and can be replaced by its concave hull . By assumption, is increasing and concave and it follows that is strictly increasing, in and satifies the growth condition by applying Theorem 3.8 in [6]. An inspection of the proof of Theorem 3.8 together with Lemma 3.6 [6] also confirms that satisfies the Inada condition at and infinity.

Proposition 4.4

Assume that Assumption (H) holds and the concavification region contains an interval for some ¶¶¶This assumption is satisfied in the option compensation problem with power utility, see Section 5.2. Define Then .

Proof. By the dynamic programming principle it is sufficient to show that on a non-zero set

Let us remark that in our complete market setting, the market price density is atomless and is continuous by assumption. In particular, by Proposition 4.3 and the concavification techniques in the certain maturity case (see Section 5 of [22]), the last period value function is given by

which is strictly increasing and strictly concave and . Therefore,

It can be observed that for an

It then follows

with . The strict inequality above holds because is not affine on the set and is strictly concave on an interval for some due to Inada’s condition at zero of (see Lemma 8.3). Hence, by a Merton-Lagrange-type analysis, takes values with positive probability in a non-zero set where .

It follows from Proposition 4.4 that concavification techniques (as for instance in [22]) cannot be directly applied to when the time horizon is random. The non-concave optimization in this case can however still be solved by a recursive procedure which is established by Proposition 4.2. This will be explicitly illustrated in the next section.

5 Example for power utility function

In this section, we illustrate our main results established in the previous sections. In particular, we consider for a discrete random variable, i.e., there are times and probabilities for with such that for For simplicity, we assume that and are constant and we choose a power (CRRA) utility, i.e.,

| (5.1) |

5.1 Concave optimization with power utility

Note first that since is strictly concave we have that . By Theorem 3.1, we need to find an adapted process with such that the process generated by the -tuple is a martingale and is a constant. As shown below, for such a CRRA utility function we can find a which is deterministic, in particular, is a constant.

Proposition 5.1

For power utility defined in (5.1), the optimal solution generated by the -tuple , where

and . Furthermore, the optimal investment strategy is the Merton strategy, i.e. the optimal fraction of wealth invested in the risky asset at time is given by which is independent of the distribution of the stopping time.

Proof. We try to find the optimal solution generated by the -tuple , where , are deterministically chosen such that the martingale condition is fulfilled. By Lemma 8.1 and the martingale condition we have for

which yields

Hence,

Using Itô’s formula it can be checked directly that which is the classical Merton strategy.

Hence, in the concave optimization problem the optimal portfolio selection is not affected by the presence of an uncertain time horizon, even though the value function is not identical to the one corresponding to the standard fixed-horizon case. This result can be considered as a confirmation of Merton [19] and Richard [23] and is aligned with the findings in [10, 11].

5.2 Non-concave optimization: recursive solution

We consider the special choice of a non-concave objective function as in (5.2), i.e., for given and :

| (5.2) |

where , with . We remark that although in almost all optimal control problems considered in the literature a fixed known time horizon is assumed, in reality a fixed maturity is typically not naturally given and the target date itself instead is often of random-type. Hence, the problem considered in this chapter fits to all option type managerial compensation problems, for which in the case of a non-random time horizon there is already a rich literature in the finance & OR literature going back to [13, 25].

Besides option type managearial compensation payoffs of the form (5.2) arise naturally for instance in flexibility rider insurance products which at the end of the life time of the policy holder, pay out a guarantee plus a particpation rate the latter depending on the returns in the stock market. In these products, the policy holder is allowed to influence the investment decision of the life insurance product. An example for such producs are in France for instance the life insurance products AXA Twin Star, in Germany the Swiss Life Champion and in the US, for example, Allianz Index Advanta, see [14] and the references within. In this case , , are the participation rate, the guarantee and the threshold for the participation, respectively.

By Proposition 4.4, a concavification procedure cannot be directly applied and we will solve the optimization by a recursive procedure. For comparison purpose, we introduce the concave envelope given by

| (5.3) | ||||

where . As in [20, 13], is defined by the following concavification equation:

| (5.4) |

Note that dominates with equality for and . Now, we are able to define the function by

| (5.5) |

where is the inverse of . We note that is the generalized inverse function of in the sense that

In our last period we already know so that the problem can be treated as a static non-concave EU maximization problem.

Given , the wealth level at time , the optimal terminal wealth of the conditional static problem is given by

| (5.6) |

where is -measurable and defined by the budget constraint , see [13, 20, 25]. The optimal wealth process is given by the following lemma:

Lemma 5.2

Given a realized wealth level at time , the optimal wealth process on is given by , where

| (5.7) |

where satisfies the budget constraint at time , denotes the cumulative distribution function of the standard normal distribution and

| (5.8) |

Note that the wealth process , expressed as a functional of the product , depends on the wealth level at time , , as the multiplier is characterized by the budget equation at time .

Lemma 5.3

The indirect value function is given by

| (5.9) |

Proposition 5.4

is a globally strictly concave function and its first two derivatives are given by

| (5.10) |

The inverse of marginal indirect value function is given by

| (5.11) |

Proof. By differentiating the budget constraint

we obtain , where

Similarly, by differentiating (5.9) we obtain that

Note that from (5.8) we have for any ,

| (5.12) |

By direct calculation, we can represent as

| (5.13) |

By applying (5.12) with and we obtain

It follows that

| (5.14) |

and

| (5.15) |

The bracket in (5.13) can be expressed as

From (5.2) we have

and

This implies that due to the concavification equation (5.4). Hence, The above derivation also shows that (5.11) defines the inverse of

For a power utility function, it is straightforward to compute the optimal investment strategy in the period given the wealth level at time , see e.g. [13, 20]. Having determined the indirect utility function at time , we now represent the optimization problem as

| (5.16) |

Note that (5.16) is expressed as a non-concave optimization problem in a complete market. To solve it we look at its static version

| (5.17) |

subject to the usual budget constraint , where are concave functions defined by

| (5.18) |

Since in the last period the problem becomes static, the solution of the non-concave optimization (5.17) is given by maximizing the concavified target function. Let be the corresponding inverse marginal utilities. The optimal wealth at is given by the following expression.

Proposition 5.5

The optimal portfolio of Problem (5.17) is given by

where is defined by

| (5.19) |

and is determined such that the budget constraint is satisfied.

Before presenting the proof let us remark that (5.19) defines the linear line that is jointly tangent to the curves of and .

Proof. For and , consider the following Lagrangian

Note first that is continuous and attains maximum at , . Furthermore, it follows from (5.18) that for all and . Let . If , then . Hence is increasing in and decreasing in . So is the maximizer when . Similarly, for we observe that is increasing in and decreasing in . So is the maximizer for . It remains to consider the case . The global optimality of results from the comparison of and . To this end, consider the continuous function

Obviously , which implies that is decreasing in . Furthermore, noting that we obtain

and

because and are strictly concave. Therefore, there exists such that which gives the concavification equation (5.19). Note that is strictly positive in and strictly negative in . The global maximizer of is then given by if or by if . The existence of is not difficult to see.

5.3 Numerical illustration

We consider a classical Black-Scholes market with a risky asset and a bond and the such that We assume that , , , , , , . We carry out a recursive procedure to determine the optimal solution for the non-concave problem with random time horizon .

Our numerical illustration relies on a Monte-Carlo simulation with 50000 paths of the market price density to determine the optimal multiplier in the first period. This recursive procedure is computationally rather challenging. First, although the indirect value function of the last period can be computed in closed form in (5.9), it implicitly depends on the price density . Second, computation of the marginal utility functions , of the corresponding concavified utilities is computationally intensive as concavification requires a root search step for each value of the market price density . This is done using Brent’s method with a careful choice of the starting values. Below, we numerically test and confirm the theoretical result established in Section 5.2

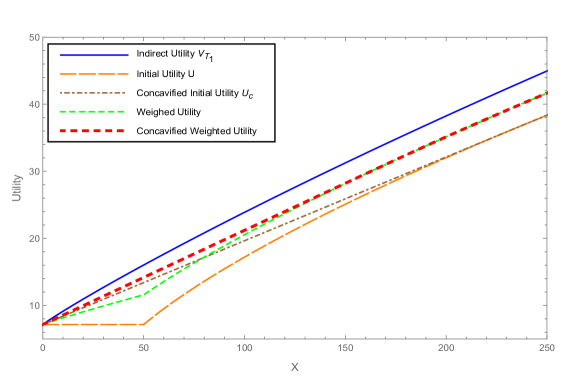

In order to test the concavity of the weighted utility at time , we plot in Figure 1 the indirect valued function at time defined in (5.9). The graph numerically confirms the result in Proposition 5.4 that is strictly concave and dominates the initial utility . In addition, the weighted utility defined by (5.16) is indeed non-concave and its concave hull is dominated by the indirect value function . This implies that having a premature stopping time before leads to lower expected utility than the solution with certain time horizon . In other words, this numerical example also confirms the result in Proposition 4.4 that optimizing the concavified version of the utility function will lead to sub-optimality.

| 0.1 | 0.17661847317422547 | 0.1766184731742255 |

|---|---|---|

| 0.2 | 0.17365388191218573 | 0.1736538819121857 |

| 0.3 | 0.170919 | 0.170919 |

| 0.4 | 0.16871475448916323 | 0.16871475448916323 |

| 0.5 | 0.165183 | 0.165183 |

| 0.6 | 0.1627175838160374 | 0.1627175838160374 |

| 0.7 | 0.1598441738970805 | 0.1598441738970805 |

| 0.8 | 0.15719801306953618 | 0.15719801306953618 |

| 0.9 | 0.15428390949982979 | 0.15428390949982979 |

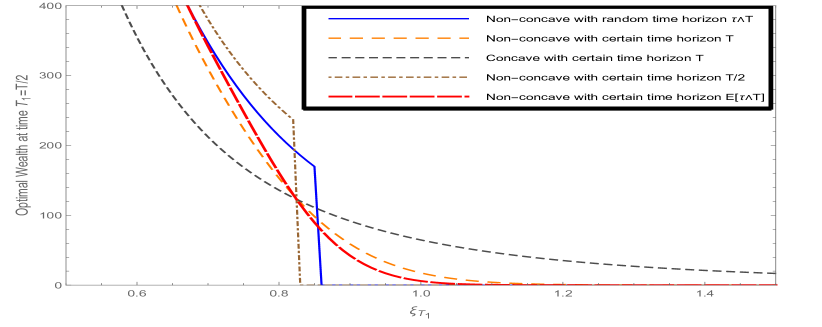

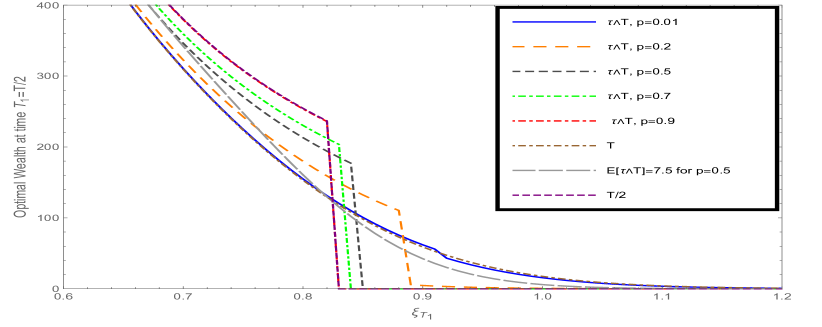

The optimal wealth at time is plotted in Figure 2(a) which exhibits an intermediate investment behavior between the non-concave problems with certain time horizon and . In particular, it is higher (resp. lower) in good market scenarios but lower (resp. higher) in bad market states than the corresponding wealth of the certain time horizon problem (resp. ). In addition, there are ranges of intermediate market states in which the uncertain time wealth can be higher and lower than that of the non-concave problem with (certain) average time horizon . As confirmed in Figure 2(b), the larger (resp. smaller) the probability of exiting at the smallest time horizon value , the riskier (resp. less risky) the investment behavior at time . Furthermore, the random horizon problem converges to the extreme cases with certain horizon and when approaches to 0 and 1 respectively.

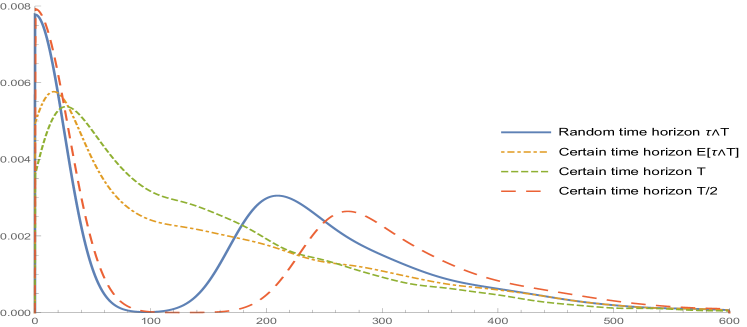

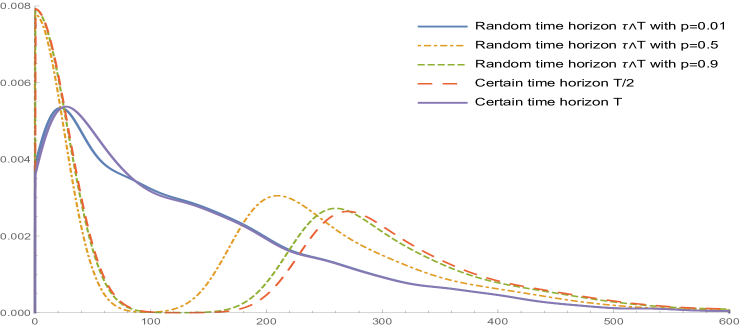

To further understand this effect, we plot in Figure 3 the estimated density of the optimal wealth at time from 5000 simulations of the market price density . It is interesting to observe that the distribution of the wealth at time of the non-concave optimization problems is right-skewed with a long right tail, indicating that the investor expects frequent small losses and a few large gains from the investment. A positively skewed distribution of investment returns is generally desirable by the agent with option-liked compensation payoff. In addition, the premature (before time ) exiting risk forces the investor to follow a portfolio that is of right-skewed and bimodal distribution with peaks of different heights. The bimodal structure can be explained by the concavification procedure at , whereas the binomial distribution of the exiting time has significant impact on the amplitude between the two modes. The higher the probability , the larger the amplitude. While the (certain) average time horizon portfolio is right-skewed and unimodal, the random time horizon portfolio, due to the option-liked compensation payoff at time , is bimodal distributed which provides the investor flexibility of switching between the two local maximizers and , depending on the market performance. If the concavified utility at time is affine in many open intervals, the corresponding wealth is intuitively expected to be of multimodal distribution. Again, when approaches to or , the wealth distribution of the random horizon problem converges to the extreme cases with certain horizon and .

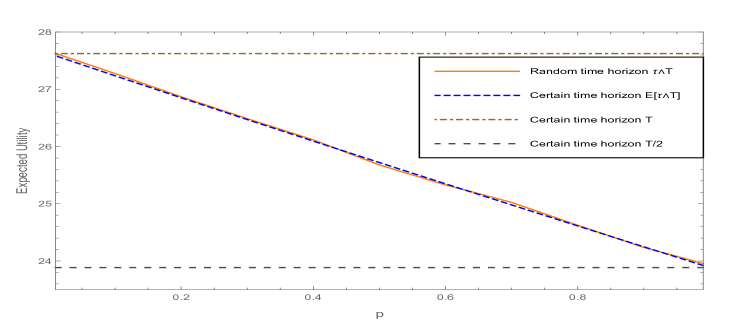

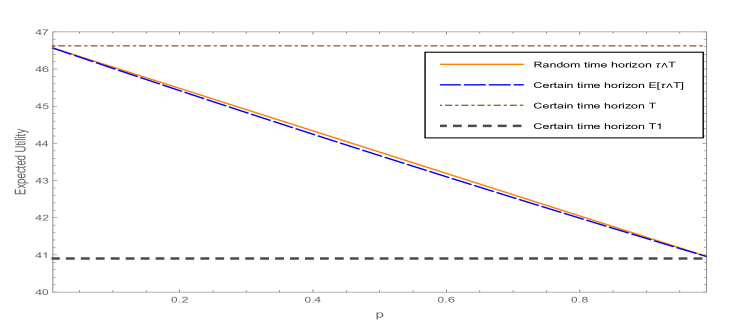

We now turn our attention to the impact of the time horizon uncertainty on the total expected utility. We first remark that in certain time horizon settings, it can numerically be shown that the value function of the concave and the non-concave problems is a convex function in the time horizon variable. Figure 4 reports the impact of exiting probability on the expected utility of the random time horizon and the certain time horizon . As shown in the right panel, the expected utility of the random horizon problem is always higher than that of the certain horizon problem, which is due to the convexity in time horizon of the value function and the fact that investment strategies for both cases with certain and uncertain horizon time horizon are identical and given by the Merton fraction (see Proposition 5.1).

The left panel of Figure 4 reports the expected utility of the non-concave optimization setting. We observe a similar expected utility dominance of the uncertain time horizon problem over the certain time horizon problem when is close to and . However, this effect is hard to see for intermediate values of for the given parameters. Unlike concave problems, the optimal investment strategy of the non-concave optimization problem significantly depends on the time horizon.

Lastly, let , where is the right-hand derivative of . We now want to numerically verify that as shown in Theorem 3.2, the weighted multiplier is constant (a.s.) on the set . We remark that is a non-zero set and is not differentiable at . For the given parameters and for 50000 paths on the market price of risk, we obtain that is constant on the set , confirming the result established in Theorem 3.2. Note that this weighted multiplier coincides with the multiplier of the first period. The result is consistent when different values of are considered, see Table 1.

6 Optimal investment with an -stopping time

In this section we study the case where is an -stopping time taking values at . For simplicity, we consider again in this section the non-concave utility function defined in (5.2). We remark that the result obtained in this section can be extended to more general utilities. The optimization problem (3.1) becomes

| (6.1) |

Recall the generalized inverse marginal utility defined by (3.4). The function is not differentiable everywhere but the superdifferential may be identified with the set-valued function

| (6.2) |

Proposition 6.1

Assume that is an -stopping time taking values . Suppose furthermore that there is an adapted process with such that the process generated by is a martingale and is a constant. Then, solves the optimization problem (6.1).

Proof. Let which is a constant by assumption. Let us first show that for any we have

| (6.3) |

Indeed, by construction the process is a local martingale. Denoting the localizing sequence of stopping times of this local martingale by , we have

Using Fubini’s Theorem we obtain

The conclusion follows by passing to the limit and Fatou’s lemma.

Note that the defines a density process of a probability measure as it is a martingale with initial value equal to 1. By construction, . Therefore, by Bayes formula we obtain

| (6.4) |

For any admissible we have by (6.4) that

where we have used (6.3) in the last step. This implies the optimality of the process generated by .

We now aim to solve the non-concave optimization problem when is an -stopping time, namely

| (6.5) |

where is the non-concave utility function defined by (5.2). In particular, by applying Proposition 6.1 we prove below that Problem (6.5) can be solved by concavification arguments and the optimal wealth can be characterized by , where is the generalized inverse marginal utility function defined by (5.5) and is an adapted process. We need the following integrability condition.

Condition (C): For any , .

Below we show that under condition (C) and the assumption that the stopping time adapted to the financial market filtration, it is possible to construct an adapted process such that the process generated by the stopped -tuple is a martingale and is a constant. The result is summarized in the following proposition.

Proposition 6.2 (Non-concave problem with a stopping time horizon)

Assume that is an -stopping time taking values at and Condition (C) holds. Then, there exists an -adapted process such that the optimal wealth of Problem (6.5) is given by

and is a constant satisfying

Proof. Consider the mapping defined for by Condition (C). Since the market price density is atomless, is continuous on . Moreover, by Fatou’s lemma, (5.5) and Inada’s condition of the power utility function we obtain and . Therefore, there exists such that . Define for , and

where the superdifferential is defined by (6.2). Note that since the conditional expectation process is a non-negative martingale with initial value , almost surely corresponds to and is invertible. Thus, by construction we obtain with being a constant and the stopped-tuple is a martingale with starting value . Hence, it is an optimal solution to (6.5).

The following is aligned with Proposition 3.3 in [11] when is an -stopping time for stricly concave utility function .

Corollary 6.3 (Concave problem with a stopping time horizon)

Assume that is a strictly concave utility for which Condition (C) holds and is an -stopping time taking values at . For any , there exists such that . Moreover, there exists an adapted process such that the optimal wealth of Problem (6.5) is given by , and is a constant.

7 Conclusion

We studied a non-concave optimal investment with a random time horizon in a complete financial market setting. We established a necessary and sufficient condition for the optimality in this case for general utility functions with a random time horizon. When is independent of the financial risk, we showed that a direct concavification approach cannot be applied and suggest a recursive procedure based on the dynamic programming principle. We illustrated our finding by carrying out a multiple period numerical analysis for the non-concave option compensation problem with random time horizon. We numerically show that due to concavification, the distribution of the wealth at exiting times of the non-concave optimization problems is right-skewed with a long right tail, indicating that the investor can expect frequent small losses and a few large gains from the investment. Under the premature exiting risk, the wealth at an exiting time exhibits a bimodal distribution with peaks of different heights due to the concavification procedure and whereas the exiting time distribution has significant impact on the amplitude between the two modes.

Our work leaves several interesting directions for future work. for instance, it would be interesting to look at the case when the time horizon is correlated with the financial market information, or to investigate the problem in a general incomplete financial market like in [11]. Furthermore, our non-concave framework with random horizon might serve as an attempt to extend the results for contract design problems of term-life insurance or insurance contracts with surplus participation [14, 20] to an uncertain time horizon setting. We leave this for future work.

Acknowledgments: Thai Nguyen acknowledges the support of the Natural Sciences and Engineering Research Council of Canada [RGPIN-2021-02594].

References

- [1] Aksamit, A. and Jeanblanc, M.: Enlargement of filtration with finance in view. Switzerland: Springer, (2017).

- [2] Aumann, R. J. and Perles, M.: A variational problem arising in economics, Journal of Mathematical Analysis and Applications 11, (1965), 488-503.

- [3] Basak, S. and Makarov, D.: Strategic asset allocation in money management, The Journal of Finance 69(1), (2014), 179-217.

- [4] Bensoussan, A. Cadenillas, and H. K. Koo.: Entrepreneurial decisions on effort and project with a nonconcave objective function. Mathematics of Operations Research 40(4), (2015) 902–914.

- [5] Biagini, S.: Expected Utility Maximization: Duality Methods, Encyclopedia of Quantitative Finance, (2010).

- [6] Bian, B., Miao, S., and Zheng, H.: Smooth value functions for a class of nonsmooth utility maximization problems. SIAM Journal on Financial Mathematics, 2(1), (2011), 727-747.

- [7] Bian, B., Chen, X., and Xu, Z. Q.: Utility maximization under trading constraints with discontinuous utility. SIAM Journal on Financial Mathematics, 10(1), (2019), 243-260.

- [8] Bichuch, M. and Sturm, S.: Portfolio optimization under convex incentive schemes, Finance and Stochastics 18(4), (2014), 873-915.

- [9] Blanchet-Scalliet, C., El Karoui, N. and Martellini, L.: Dynamic asset pricing theory with uncertain time-horizon, Journal of Economic Dynamics and Control 29(10), (2005), 1737-1764.

- [10] Blanchet-Scalliet, C., El Karoui, N., Jeanblanc, M. and Martellini, L.: Optimal investment decisions when time-horizon is uncertain, Journal of Mathematical Economics 44(11), (2008), 1100-1113.

- [11] Bouchard, B. and Pham, H.: Wealth-path dependent utility maximization in incomplete markets, Finance and Stochastics 8(4), (2004), 579-603.

- [12] Carassus, L. and Pham, H.: Portfolio optimization for piecewise concave criteria functions, The 8th Workshop on Stochastic Numerics, (2009).

- [13] Carpenter, J. N.: Does option compensation increase managerial risk appetite?, The Journal of Finance 55(5), (2000), 2311-2331.

- [14] Chen, A., Hieber, P. and Nguyen, T.: Constrained non-concave utility maximization: an application to life insurance contracts with guarantees, European Journal of Operational Research 273(3), (2019), 1119-1135.

- [15] Dai, M., Kou, S., Qian, S. and Wan, X.: Nonconcave Utility Maximization without the Concavification Principle, (2019). Available at SSRN: https://ssrn.com/abstract=3422276.

- [16] Dehm, C., Nguyen, N., and Stadje, M. Non-concave expected utility optimization with uncertain time horizon. arXiv preprint: https://arxiv.org/pdf/2005.13831.pdf (2021).

- [17] Karatzas, I., Lehoczky, J. P., Shreve, S. E., and Xu, G. L.: Martingale and duality methods for utility maximization in an incomplete market, SIAM Journal on Control and Optimization 29(3), (1991), 702-730.

- [18] Larsen, K.: Optimal portfolio delegation when parties have different coefficients of risk aversion, Quantitative Finance 5(5), (2005), 503-512.

- [19] Merton, R.C.: Optimal consumption and portfolio rules in continuous time, Journal of Economic Theory 3, (1971), 373-413.

- [20] Nguyen, T. and Stadje, M.: Nonconcave optimal investment with Value-at-Risk constraint: an application to life insurance contracts, SIAM Journal on Control and Optimization, 58(2), (2020), 895-936.

- [21] Pham, H.: Stochastic control under progressive enlargement of filtrations and applications to multiple defaults risk management, Stochastic Processes and their Applications 120(9), (2010), 1795-1820.

- [22] Reichlin, C.: Utility maximization with a given pricing measure when the utility is not necessarily concave, Mathematics and Financial Economics 7(4), (2013), 531-556.

- [23] Richard, S. F.: Optimal consumption, portfolio and life insurance rules for an uncertain lived individual in a continuous time model, Journal of Financial Economics 2(2), (1975), 187-203.

- [24] Rieger, M. O.: Optimal financial investments for non-concave utility functions, Economics Letters, 114(3), (2012), 239-240.

- [25] Ross S. A.: Compensation, incentives, and the duality of risk aversion and riskiness, Journal of Finance, 59 (1), (2004), 207-225.

- [26] Wong, K. C., Yam, S. C. P., and Zheng, H.: Utility-deviation-risk portfolio selection. SIAM Journal on Control and Optimization 55(3), (2017), 1819-1861.

- [27] Yaari, M. E.: Uncertain lifetime, life insurance, and the theory of the consumer, The Review of Economic Studies 32(2), (1965), 137-150.

8 Appendix

The following result can be shown directly using the lognormal distribution of :

Lemma 8.1

Let . With defined in Proposition 5.1 it holds for that

| (8.1) |

The next result provides a generalization of Lemma 8.1 when the market parameters are constant.

Lemma 8.2

Let , and let be a positive constant. With the cdf of the standard normal distribution and defined in (5.8) it holds that

| (8.2) |

Lemma 8.3

Let , be continuous, increasing functions in . Let be an open interval in the concavification region of . Assume that there exists at which coincides with the affine line

and the right derivative of the sum exists and

| (8.3) |

Then, the interval cannot be a concavification set of the sum , i.e. there exists an open interval such that for all .

Proof. We have . By continuity and (8.3) it can be seen that in a right-hand neighbourhood of , which implies that the affine line is not the concave hull of on the whole interval .