Abstract

A local projection model is defined by a set of linear regressions

that account for the associations between exogenous variables and

an endogenous variable observed at different time points. While it

is standard practice to separately estimate individual regressions

using the ordinary least squares estimator, some recent studies treat

a local projection model as a multivariate regression with correlated

errors, i.e., seemingly unrelated regressions, and propose Bayesian

and non-Bayesian methods to improve the estimation accuracy. However,

it is not clear how and when this way of treatment of local projection

models is justified. The primary purpose of this paper is to fill

this gap by showing that the likelihood of local projection models

can be analytically derived from a stationary vector moving average

process. By means of numerical experiments, we confirm that this treatment

of local projections is tenable for finite samples.

1 Introduction

Local projections (LPs) (Jordà, 2005) are linear regressions

that project observations of an endogenous variable at different time

periods, , onto exogenous variables observed

at period , :

|

|

|

(1) |

where is a coefficient vector

and is a residual.

may include an intercept, preidentified structural shocks, the lags

of the endogenous variables up to period , and other controls.

LPs are mainly employed for impulse response analysis. When the th

element of , denoted by , is a

preidentified structural shock, a sequence of the corresponding coefficients

is interpreted as an impulse response function, namely,

|

|

|

Because of their flexibility and robustness to model misspecification,

LPs are extensively applied to investigate the economic dynamics (e.g.,

Ramey2016a and cited therein). In this paper, we refer

to a set of LPs for the same endogenous variable (1)

as an LP model and statistical analysis using an LP model as the LP

method.

The LP method is intrinsically different from conventional approaches

to time series modeling. Standard time series models, such as the

vector autoregressive (VAR) model and its variants, are designed to

approximate the data generating process (DGP). In contrast, the LP

method does not explicitly assume the DGP and directly captures the

associations between the exogenous variables

and the endogenous variable observed at different time points ,

.

It is standard practice to separately estimate LPs (1)

using the ordinary least squares (OLS) estimator, while Tanaka (2020)

and El-Shagi (2019) estimate an LP model as a multivariate regression

with correlated residuals, i.e., seemingly unrelated regressions (SUR)

(Zellner, 1962). Tanaka (2020) and El-Shagi (2019)

treat response variables for different projection horizons as correlated

but different variables and estimate an LP model as a multivariate

regression model where a vector of the responses

are regressed on the covariates :

|

|

|

(2) |

|

|

|

|

|

|

Tanaka (2020) assumes that the residuals of an LP model are

distributed according to a multivariate normal distribution with the

covariance matrix , ,

where denotes

a multivariate normal distribution with mean and

covariance matrix . Thus, the (conditional) distribution

of is specified as

|

|

|

(3) |

which leads to the following likelihood:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where

denotes the probability density function of a multivariate normal

distribution with mean and covariance matrix

evaluated at . Tanaka (2020) considers Bayesian

inference of LP models based on this likelihood. El-Shagi (2019)

estimates LP models in a similar way to a feasible generalized least-squares

estimation of an SUR model, where the quadratic loss function that

he employs is closely related to the previously described likelihood

(1). Tanaka (2020) and El-Shagi (2019)

propose a Bayesian approach and a non-Bayesian approach to improve

the estimation of accuracy using a tailored prior and a penalty term,

respectively.

Whereas Tanaka (2020) and El-Shagi (2019) show that their

statistical approaches perform well by means of simulation studies,

they do not explicitly discuss how and when the likelihood of the

LP models that they utilize (1) is justified.

The primary focus of this paper is to fill this gap. We suggest that

their SUR-like treatment of LP models is statistically valid by showing

that the likelihood (1) can be analytically

derived from a stationary vector moving average (VMA) process with

the normality assumption.

Lusompa (2019) proposes Bayesian and non-Bayesian methods to

estimate LPs. Unlike the SUR-like treatment in Tanaka (2020)

and El-Shagi (2019), his approach requires estimation of all

the LPs for endogenous variables, i.e., the whole system of LPs; thus,

it is computationally demanding. Specifically, his Bayesian method

is not practical when the number of endogenous variables and/or the

number of projection horizons is large. In most situations, it is

not necessary to examine all the LPs because analysts’ attention is

limited to coefficients that represent impulse responses of interest.

Thus, confirming the statistical validity of the SUR-like treatment

of LPs in Tanaka (2020) and El-Shagi (2019), which is

more parsimonious than that of Lusompa (2019), has practical

importance.

We discuss the relationship between a VMA process and the SUR-like

likelihood of an LP model in two steps. First, we develop the entire

system of LPs from a stationary VMA process with normality assumption

(Section 2). Second, we define an LP model as a sub-system of the

entire system of LPs and derive its probabilistic representation,

i.e., the likelihood (Section 3). We see that the covariance matrix

of the residuals of an LP model can be represented as a (matrix-valued)

function of the parameters of the VMA process and that it is non-diagonal,

full rank, and symmetric positive definite. Therefore, the likelihood

of an LP model can be specified as in SUR. By means of numerical experiments,

we show that the derived representation of the residual covariance

matrix can be accurately estimated using the OLS estimator and Bayesian

Markov chain Monte Carlo method (Section 4). Therefore, the SUR-like

treatment of LP models is tenable for finite samples.

2 From VMA Process to Entire System of LPs

This section derives an entire system of LPs that corresponds to the

underlying DGP specified by a VMA process. We assume that data

are generated from an th-order stationary VMA process:

|

|

|

(5) |

where

is an -dimensional vector of endogenous variables,

is an -dimensional vector of structural shocks that are distributed

according to a multivariate normal distribution with covariance matrix

, and

is an -by- VMA coefficient matrix. Without loss of generality,

intercepts are omitted. The process is not assumed to be fundamental;

thus, our discussion applies not only to VAR processes but also to

more general multivariate time series. The identification of structural

shocks is beyond the scope of this paper; impulse responses can be

estimated only when the shocks are exogenous or identified before

inference.

An horizon LP is defined by a projection of

onto the lags of the endogenous variables, :

|

|

|

(6) |

where denotes

the orthogonal projection of onto

and

is an -dimensional vector of the LP residuals. The orthogonal

projection

is specified by the linear projection ,

where is an -by- LP

coefficient matrix whose -element is denoted by

.

Each LP is posed as

|

|

|

In the following section, we refer to this representation of LPs (or

equivalently (6)) as the entire system

of LPs, in distinction from an LP model for a specific endogenous

variable, such as (1) and (2).

Although multivariate time series data are considered, an LP model

is not a typical time series model. The purpose of the model is to

directly examine the relationship between variables measured at different

time points, not to recover the underlying DGP.

The construction of the likelihood of LP models is different from

that of the standard multivariate time series models. For instance,

if the VMA process (5) has a VAR representation,

the likelihood of the VAR model is written generically in the following

form:

|

|

|

where denotes a set of parameters that specify

the VAR model. Contrastingly, the likelihood of the LP representation

of the VMA process (6) is specified as

|

|

|

where denotes a set of parameters that specify

the entire system of LPs. As shown in Jordà (2005), when the

true DGP is a VAR process, the LP coefficients ,

, are parametrized by the coefficients that specify the

VAR process.

The residuals of the entire system of LPs

have autocorrelations. Lusompa (2019) shows that the process

of is known: for ,

|

|

|

where is an -dimensional

vector of serially uncorrelated residuals. In the population, it follows

that

|

|

|

|

|

|

|

|

|

|

The residuals are written as

|

|

|

|

|

(7) |

for .

3 From Entire System of LPs to LP model

An LP model for the th endogenous variable is defined by extracting

a portion of the LPs, or a sub-system, from the remainder of the entire

system:

|

|

|

|

|

|

where

is a vector containing the element of the th row of .

This sub-system is summarized in an analogous fashion to (2):

for ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The likelihood of the sub-system is structured as

|

|

|

|

|

|

|

|

|

|

|

|

|

This expression corresponds to (1).

In the following section, we show that the residuals of the sub-system

are distributed according to a multivariate distribution, ,

where is a symmetric positive definite matrix,

and that the distribution of

is specified as

|

|

|

(9) |

This expression is a mirror image of (3). We

analytically derive the covariance of the residuals of the sub-system

as a matrix-valued

function of the parameters of the LP coefficients for the th endogenous

variable and the covariance of the structural shocks ,

which shows that is proper as a covariance matrix

because it is full rank, symmetric, and positive definite. For readers’

convenience, the correspondence between the notations in the SUR-like

treatment of an LP model (1) and the

VMA process is summarized in Table 1.

From (7), using the LP coefficients

and the structural shocks, the residuals can be rewritten as follows:

|

|

|

|

|

|

|

|

|

|

Let denote an -dimensional vector of

zeros, where the th element is replaced by one. The residuals

are arranged as

|

|

|

|

|

|

|

|

|

|

The covariance of

is represented using the LP coefficients and the covariance matrix

of the structural shocks as

|

|

|

(14) |

|

|

|

(15) |

This expression implies that is non-diagonal,

full rank, and symmetric positive definite. Thus,

is properly defined as a covariance matrix, and the distribution of

can be written

in the form of (9).

Given , the likelihood

of this sub-system is independent from the VMA coefficients for the

remainder of the whole system (6), because

does not

contain the LP coefficients for the remaining endogenous variables,

namely, ,

; . Therefore, to recover the LP

coefficients from the data, it is sufficient to estimate the sub-system.

The likelihood (3) is specified as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

There is a correspondence between this likelihood presentation and

the SUR-like likelihood (1).

From the foregoing analysis, we confirm that the probabilistic representations

of an LP model in (9), and thus, (3)

are justifiable when the true DGP is a stationary VMA process with

the normality assumption and that the likelihood of an LP model based

on the SUR-like treatment (1), which

is applied in Tanaka (2020), is statistically valid.

Lusompa (2019) proposes a Bayesian method to estimate the entire

system of LPs (6). His posterior simulation

algorithm consists of two steps. First, the horizon 0 LP, which is

equivalent to a VAR model, is estimated. Second, for each draw, the

remaining coefficients are simulated from the conditional posteriors

sequentially for . This algorithm is computationally

demanding, because all the coefficient matrices of the entire system

are inferred. In most situations, the analyst’s focus is limited to

a small portion of these matrices, e.g., coefficients that represent

impulse responses of interest. Thus, inference about the whole system

is unnecessary. As long as structural shocks of interest are identified

before inference, the SUR-like treatment of LPs is advantageous to

the approach of Lusompa (2019).

4 Numerical Illustration

By numerical experiments, we investigate the small-sample performance

of non-Bayesian and Bayesian approaches in the inference of an LP

model. Synthetic data are generated from the following VMA process:

|

|

|

We fix , , , and . Our focus is inference

of the responses of the second element of to

the first element of , which is exogenous to

the system. A covariate vector includes

lags of and an intercept. The parameters for

the synthetic data are randomly generated. Let denote

the -element of The

first element of is a preidentified structural

shock ; thus, all the first rows of

are zero. A sequence of the -elements of ,

which is denoted by ,

represents the impulse responses of interest. The elements of

are specified as

|

|

|

where is a parameter that controls the shape of the impulse response

function. We fix . The diagonal elements of

are uniformly sampled from the unit interval, .

The second to third rows of are set to

,

where each entry of is independently generated

from the standard normal distribution. The covariance matrix of

is specified by .

is simulated from an inverse gamma distribution

with a shape parameter of 1 and scale parameter of 1, while

is simulated from an inverse Wishart distribution with scale matrix

and degrees of freedom.

First, we consider a feasible generalized least-squares estimator,

as discussed in El-Shagi (2019). In the first step,

is estimated using the OLS estimator,

|

|

|

where

and .

Second, is estimated based on the OLS residuals,

|

|

|

The second-step estimate of is obtained using

. The system might be re-estimated iteratively.

The validity of this approach hinges critically on the precision of

. The parameters

and are generated

once and are fixed throughout the experiment, while the structural

shocks are randomly generated for

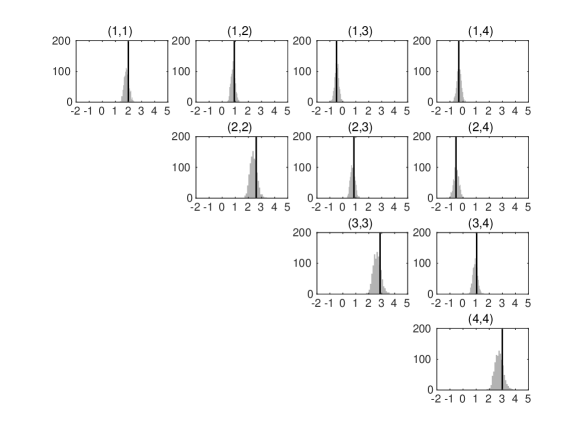

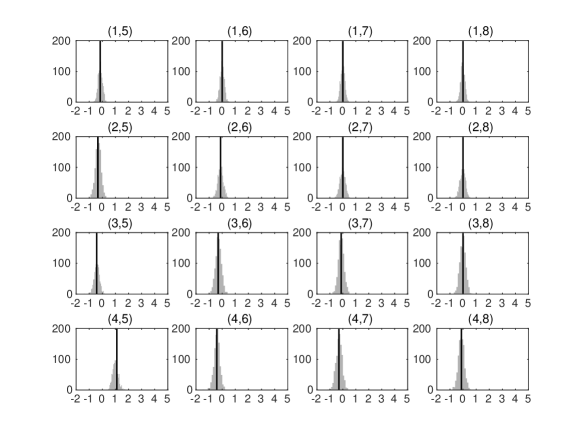

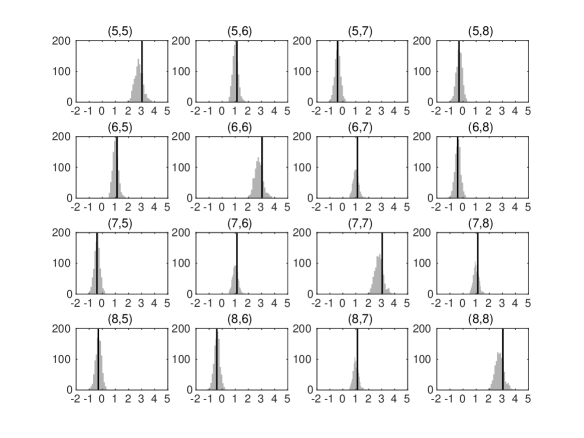

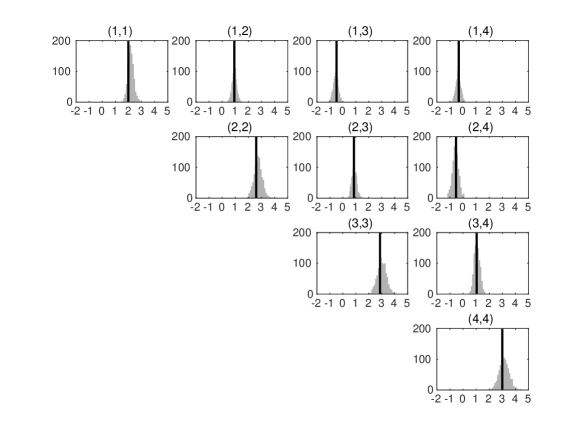

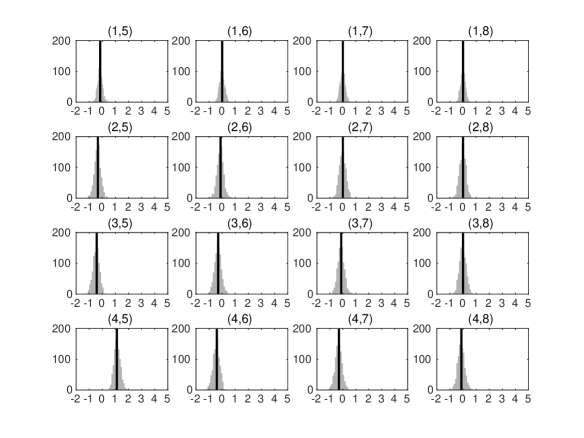

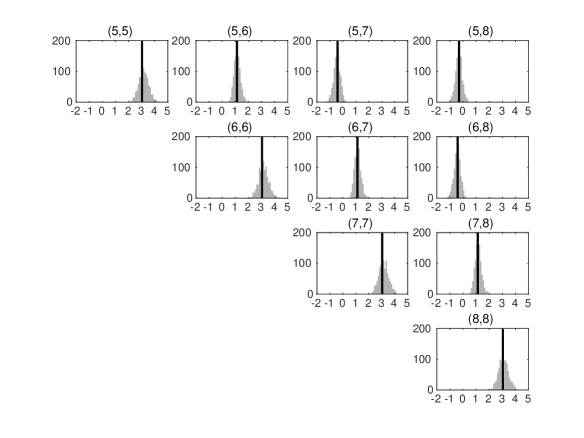

each trial. Figures 1–3 compare

for 1,000 synthetic data with the true value of

given by (14) and (15). Vertical

lines denote the true values, and the histograms represent the OLS

estimates of for different data. As evident

from these figures, can be consistently estimated

based on the OLS residuals. Figure 4 shows histograms of the estimates

of . We see that

can be estimated by the OLS estimator.

Next, in a similar vein, we consider the Bayesian inference of an

LP model. To minimize the influence of priors on the posterior, we

employ a flat prior for , ,

and a scale-invariant Jeffreys prior for , .

Posterior draws are simulated using a Gibbs sampler, and the conditionals

are specified as

|

|

|

|

|

|

|

|

|

|

|

|

where denotes an inverse

Wishart distribution with degrees of freedom and scale matrix

. We generate 11,000 draws and use the last 10,000

draws for the posterior analysis. All the chains in the experiments

passed the Geweke (1992) test at the 5 percent level. Figures

5–7 contain histograms of the posterior mean estimates

of . As with the OLS estimator, the posterior

means of are distributed around the true values.

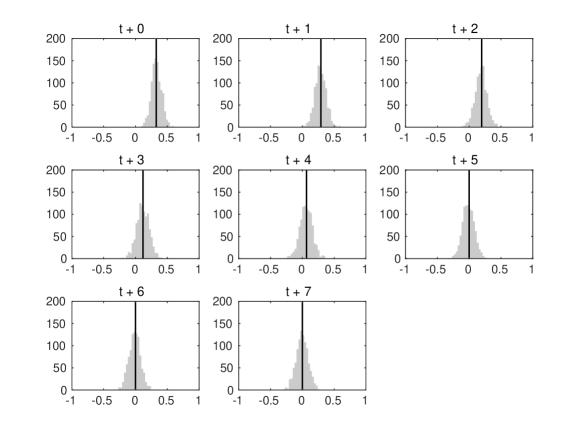

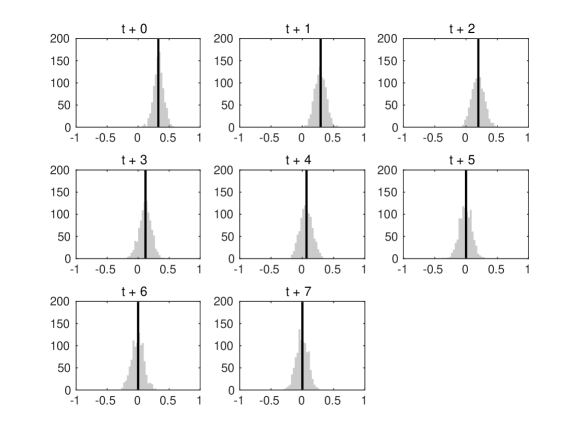

Figure 8 depicts histograms of the posterior mean estimates of the

impulse responses of interest. The estimated impulse responses are

distributed around the true values. Therefore, Bayesian analysis based

on the SUR-like treatment of LP models is tenable for finite samples.