Quickest Detection of Ecological Regimes for Natural Resource Management

Abstract

We study the stochastic dynamics of natural resources under the threat of ecological regime shifts.

We establish a Pareto optimal framework of regime shift detection under uncertainty that minimizes the delay with which economic agents become aware of the shift. We integrate ecosystem surveillance in the formation of optimal resource extraction policies.

We fully solve the case of a profit-maximizing monopolist and provide the conditions that determine whether anticipating detection of an adverse regime shift can lead to an aggressive or a precautionary extraction policy, depending on the interaction between market and environmental parameters. We compare the monopolist’s policy under detection to a social planner’s.

We apply our framework to the case of the Cantareira water reservoir in São Paulo, Brazil, and study the events that led to its depletion and the consequent water supply crisis.

JEL Codes:

Q20, Q57, D81, D42

Keywords: Regime shifts, Natural resources, Quickest detection, Uncertainty.

1 Introduction

The dynamic management of natural resources requires making decisions under ecological uncertainty, defined by Pindyck (2002) as uncertainty over the evolution of the relevant ecosystem. Stochastic bio-economic models traditionally capture this uncertainty by describing environmental fluctuations as idiosyncratic shocks affecting the stock of natural resources. Another way ecological uncertainty can manifest itself, particularly for renewable resources, is by means of regime shifts, broadly identifiable as abrupt changes in the structure of the resource ecosystem such as the underlying population dynamics or the resource’s ability to regenerate (Biggs et al., 2009). Regime shifts can cause substantial changes in the provision of ecosystem services, and can have significant impacts on both economic systems and the well-being of populations (Stern, 2006). Their occurrence has been extensively documented as a consequence of both natural and anthropogenic factors such as climate change and environmental overexploitation. Recent examples can be found in the logged tropical rainforests in parts of Asia, South America and Africa which have become more fire-prone leading to a regime shift towards exotic fire-promoting grasslands (Lindenmayer et al., 2011), or in the human-induced regime change in the Baltic Sea from cod to sprat and herring as dominant species in the fish population (Österblom et al., 2007).

There is an extensive literature studying the impact of stochasticity on renewable resource extraction and harvesting activities, dating from Pindyck (1984 and 1987) and Reed (1988) up to Saphores (2003), Alvarez and Koskela (2007) and Springborn and Sanchirico (2013). An emerging literature focuses on resource management under potential regime shifts, intended as structural changes in ecosystem dynamics: Polasky et al. (2011) shows how the threat of a regime shift can yield a precautionary extraction policy. Ren and Polasky (2014), Baggio and Fackler (2016), de Zeeuw and He (2017), Costello et al. (2019), Arvaniti et al. (2019), Crépin and Nævdal (2020), Kvamsdal (2022), Patto and Rosa (2022) and Nkuiya and Diekert (2023) extend the analysis to endogeneity, reversibility and observability of the regime shift. Sakamoto (2014) and Diekert (2017) explicitly consider a strategic environment and show how the potential occurrence of a catastrophic regime shift can facilitate cooperation between competing economic agents.

The main challenge in responding optimally to a regime shift is precisely the dual nature of the ecological uncertainty that economic agents face: the exact moment at which the shift occurs is unknown ex ante, and it is often not an easy feat to immediately disentangle structural changes in the ecosystem from idiosyncratic environmental fluctuations. This problem is further amplified by the fact that ecosystems are in constant evolution, and multiple large-scale changes to their structure are often caused or accelerated by economic activity. Barrett (2013) shows how uncertainty over tipping points’ thresholds, rather than uncertainty over consequences, can cause coordination between economic agents to collapse. Crépin et al. (2012) highlight the importance of adaptive resource management in understanding the likelihood of regime shifts and their consequent impacts on human well-being.

The primary contribution of the paper is the integration of environmental surveillance and regime shift detection in a model of natural resource extraction. Environmental monitoring is a common practice in real-world resource management: for example, the Norwegian company Aker BioMarine, a global krill monopoly, uses drones to collect, process and transmit density and distribution on the krill biomass.111https://www.akerbiomarine.com/news/aker-biomarine-pioneering-machine-learning-for-operational-decision-making

Additionally, water utilities such as Aguas Andinas in Chile (a private water monopoly), Anglian Water in the UK and American Water in the USA are increasingly reliant on remote sensing techniques for monitoring, prediction and control of algae blooms in real time.222https://www.lgsonic.com/aguas-andinas-pirque-mega-ponds/;

https://www.aquatechtrade.com/news/surface-water/3-utility-case-studies-on-treating-algal-blooms/

These techniques, combined with in situ measurements, constitute some of the most effective ways for efficient management and controlled exploitation of natural resources.

In ecology, using real-time remote sensing data is increasingly common, especially with indicators of approaching thresholds or impending collapse in ecosystems (Batt

et al., 2013; Carpenter

et al., 2014).

Our framework is therefore particularly relevant as it sheds light on how firms operate within modern-day resource markets, in which monitoring resource stocks takes an increasingly central role as drastic ecosystem changes become more frequent.

The surveillance and detection of regime shifts can substantially alter constraints and incentives faced by economic agents who extract natural resources. In this paper we first characterize the losses stemming from the ecological uncertainty of regime shifts, which manifest in the delay with which the agents become aware of their occurrence. Minimizing this delay requires the agents to be able to detect the presence of a regime shift in the quickest time possible. The problem involves the search for a way to deduce the occurrence of a general change in the drift of the controlled stochastic process that drives the natural resource evolution, and is formulated as an optimal stopping problem. This class of problems are known as quickest detection problems.333For further details we refer to Poor and Hadjiliadis (2008) and Tartakovsky et al. (2014) Originated in the Brownian disorder literature pioneered by Shiryaev (1963, 1996), detection methods have found multiple applications throughout the statistical and econometric literature, from Krämer et al. (1988) and Ploberger and Krämer (1992) to Horváth and Trapani (2022). Building on Moustakides (2004)’s work on drift changes in martingales, we present a framework with general controlled Itô diffusions that minimizes the efficiency loss caused by incomplete observability of the environmental conditions in which agents operate. To our knowledge, ours is the first paper to integrate these results in a continuous-time optimization problem in economics, and particularly in the regime shifts and renewable resources literature. More importantly, we show Pareto optimality of our framework for any resource-extracting economic agent.

In order to understand the impact of anticipating a regime shift on the agents’ incentives, and especially within our framework of quickest detection, it is of importance to include in the analysis the structure of the market in which a firm operates. We therefore integrate the surveillance procedure in the maximization problem of a resource-extracting monopolist, such that the firm maximizes its profits with respect to the resource dynamics over a time horizon determined by the detection time. A novel insight of our framework is that in expectation of detecting an adverse regime shift, a monopolist can pursue both: an aggressive or precautionary extraction policy, depending on the interplay between the environmental parameters (the ability of the resource to regenerate, the variance of the environmental fluctuations) and the firm-related ones (demand elasticity, extraction costs, detection time). Post-detection of the ecological regime change, the monopolist unequivocally decreases its stationary extraction rate. We then introduce a useful benchmark of the competitive extraction policy, allowing us to compare the extraction decisions of both a monopolist and social planner when implementing detection. While the anticipation of an adverse regime shift may lead the monopolist to adopt an aggressive policy, the social planner always pursues a precautionary extraction path. These results shed an important light on the responses of different economic agents to ecological uncertainty.

We then apply our framework to the case of the Cantareira water reservoir, a large-scale system of interconnected reservoirs which serves the Metropolitan Area of of São Paulo in Brazil. The reservoir is managed by Companhia de Saneamento Básico do Estado de São Paulo (SABESP), a water and waste management company acting as a semi-public natural monopoly. In early 2013, the reservoir’s stored water volume began decreasing sharply and by July 2014 its operational capacity was depleted, leaving a densely populated area inhabited by more than 25 million people in a devastating water crisis. Using daily data on reservoir volume, water pumping, rainfall and river inflows, we show how the depletion was caused by a catastrophic regime shift in the reservoir dynamics, and estimate the structural parameters pre- and post-shift via particle filtering. We find that the implementation of our detection procedure could have allowed the water monopolist to detect its occurrence more than six months ahead of the delayed time at which it changed its pumping policy. We further show counterfactual evidence of how adjusting the policy at the detection time could have substantially delayed depletion, if not avoided it altogether, and therefore could have drastically dampened the severe impact of the water supply crisis on the population.

The remainder of the paper is structured as follows. Section 2.1 formalizes the resource dynamics, sets up the detection procedure and shows its Pareto optimality. Section 2.2 solves the monopolist’s maximization problem within different scenarios. Section 2.3 explores the characteristics of the solution to the firm’s problem, shows the different policy responses to an adverse regime shift and compares the monopolist to a social planner. Section 3 presents the application of our framework to the case of the Cantareira water reservoir, and section 4 concludes.

2 The Model

2.1 Resource dynamics, regime shifts and quickest detection

We start by modeling the stochastic dynamics of a renewable resource extracted by an economic agent. Let be the resource stock available at time , which behaves according to the stochastic differential equation (SDE)

| (1) |

where is the extraction policy, is the intensity of noise in the evolution of the resource stock, is the process that drives the resource growth and . Finally, is the standard Brownian motion in the filtered probability space . The processes are adapted to the same filtration , and satisfy the standard requirements for existence and uniqueness of a weak solution for (1).444See Oksendal (2013) for all further details.

In order to capture the regime shift that the resource dynamics can undergo, we describe two alternative scenarios faced by the agent: one in which the resource evolves according to equation (1), and an alternate one in which the stock’s ability to regenerate (the drift) changes. This is consistent with Polasky et al. (2011), who define regime shift as a change in the system dynamics such as the intrinsic growth rate or the carrying capacity of the resource. The evolution for the resource stock then becomes

| (2) |

where is the change in resource growth, also adapted to . If , the growth rate of the resource is reduced and it undergoes a negative (adverse) regime shift, and vice versa. The regime shift can be made dependent on antecedent factors and we can write , where is the information set the agent has when it starts monitoring the resource stock. By antecedent factors we imply any process adapted to the filtration , which does not vary during the surveillance period and contributes to the knowledge the agent has at on the magnitude of the regime shift . The set can be constructed to include any early warning signals available at which can signal the likelihood and magnitude of regime shift, such as “critical slowing-down” (Scheffer et al., 2009) and self-organized spatial patterns (Rietkerk et al., 2004). Such indicators are key features of coupled human-environment systems (Boettiger and Hastings, 2012; Bauch et al., 2016). Furthermore, can include information on the agent’s extraction policy adopted before the initial observation time, allowing us to study a framework in which past extraction activity can determine future changes in resource growth.

We therefore want to study the scenario in which at a given change point in time , which is happening with certainty but at time unknown, the SDE driving the resource stock will switch between drifts:

| (3) |

Note that since the occurrence of is certain, the question faced by the agent is not if a regime shift will occur but rather when. The agent now faces two sources of uncertainty when choosing the extraction policy that maximizes its profits. The first source is given by the Brownian motion calibrated by the diffusion coefficient , which represents the fluctuations inherent to the natural randomness of environmental conditions. The second source is the uncertainty over the timing of the shift, at which the resource’s drift changes from to . Whilst being unknown to the agent ex ante, the change point would be immediately inferable in absence of fluctuations. In presence of fluctuations, however, the agent needs to be able to distinguish the structural change in the drift from idiosyncratic noise.

We now need to establish from a decision maker’s perspective the importance of adjusting to a regime shift in the ecosystem as quickly as possible. Why should an economic agent undertake any supplementary analysis in order to infer whether the regime shift has actually occurred? Let us formalize this point. The extraction policy is chosen by the agent according to a specific criterion . From Section 2.2 onwards, we will assume the agent to be a monopolist firm that follows a profit-maximizing criterion but this framework can be applied to any optimizing economic decision maker.555This criterion is only assumed to be bounded, continuous and differentiable at least once with respect to every argument. More precisely, we require to be Lipschitz continuous. For a social planner, this criterion would be expressed in terms of welfare, for a risk-averse individual it would be in terms of utility drawn from resource use. The pre-regime shift extraction policy is optimal, in the sense that it is chosen by the agent such that it maximizes their expected discounted criterion within a given time horizon i.e.

where is the non-empty set of Markovian admissible controls in feedback form such that for all , and is the discount rate. For now, we only posit the policy exists and is progressively measurable with respect to .

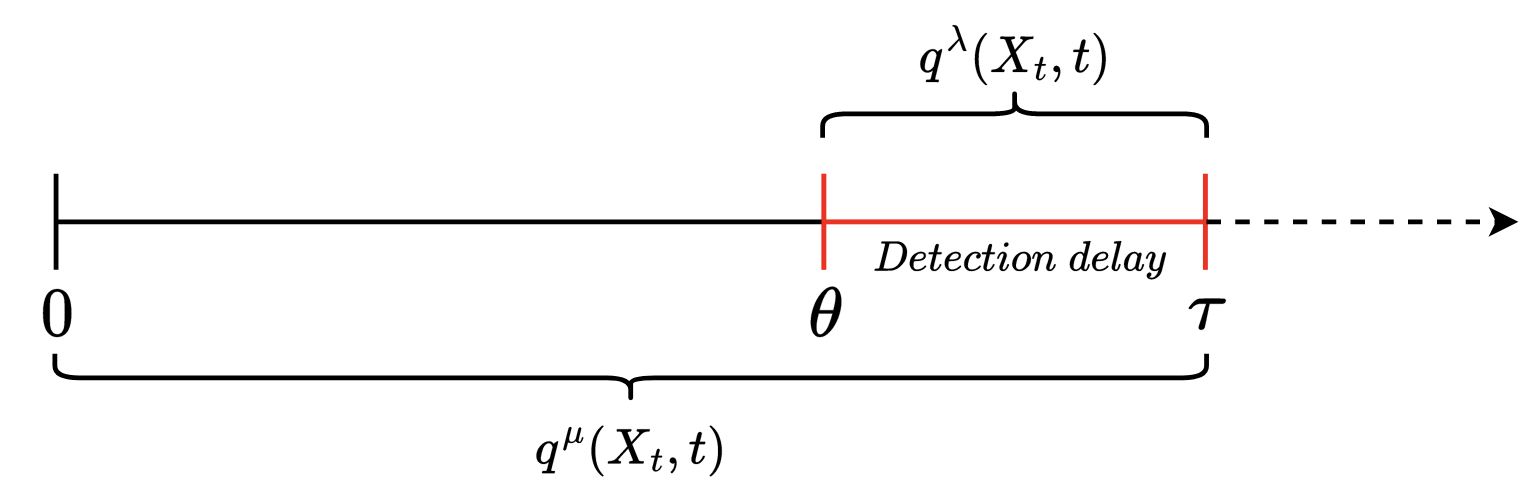

Let us now assume that the regime shift occurs in the dynamics of as shown in (3) but the agent only realizes the occurrence of the shift at , thus with a delay . This implies that there exists an extraction policy in the time interval that achieves the supremum of the discounted criterion function, i.e. s.t. . Because of this delay, the agent will continue to extract according to the policy that achieves the supremum of the optimization problem constrained by the pre-regime shift resource dynamics . The agent, therefore, will incur a loss expressed in the same unit as the criterion (utility/welfare/profits) which is increasing in the detection delay.

The rationale is intuitive: the losses are generated by the fact that the agent chooses its extraction policy by maximizing a criterion which hinges upon the continuous observation of the evolution of the resource as given by (3). If the changepoint was observable, the agent would immediately adjust extraction in order to adapt to the post-shift resource growth . On the contrary, if the agent realizes the occurrence of the regime shift with a delay at and only then adjusts extraction, within the time interval the agent is de facto extracting a “wrong” quantity that is optimal for the pre-shift problem but sub-optimal for the post-shift one. Figure 1 presents a schematic representation of this phenomenon. In Appendix A.1 we prove that this loss is increasing in the length of the delay and characterize explicitly the stochastic dynamics of the loss function in terms of the gradients of the Hamilton-Jacobi-Bellman equations associated to the respective optimization problems.

The problem now involves the minimization of the delay , which implies finding a strategy to detect the change in drift of in the quickest time possible via sequential observations, as seen in (3). In order to solve this problem the agent searches for a “rule” (an optimal stopping time) adapted to the filtration , at which one can conclude the change point has been reached and the regime shift has occurred. As delays are costly, this search requires the optimization of the tradeoff between two measures, one being the delay between the time a change occurs and it is detected i.e. , and the other being a measure of the frequency of false alarms for events of the type . The agent minimizes the worst possible detection delay over all possible realizations of paths of before the change and over all possible change points . This problem is formalized as

| (4) |

This class of problems is usually comprised of three elements: a controlled stochastic process under observation (the evolution of the renewable resource), an unknown change point at which the properties of the process change (a regime shift), and a decision maker observing the process. In this search there has to be an expected “time to first false alarm”, which represents the minimum time that the agent is willing to wait before reassessing its decisions when no shift is yet detected. This is to include in the process the fact that the signal (the change in the drift due to a regime shift) can be drowned in a noisy environment that does not allow for its detection within a “reasonable” time frame. This constraint has been formalized by Shiryaev (1963) and Lorden (1971) in the following way:

| (5) |

for when the regime shift is a constant , and a divergence-type criterion by Moustakides (2004) for a general time-varying regime shift.

The procedure to determine is given by adapting the results of Moustakides (2004) to our framework (3) first via a transformation of the diffusion coefficient and then a change of probability measure, both shown in detail in Appendix A.2. The stopping time that solves (4) is given by:

| (6) |

where is given by

| (7) |

where

in which any primitive of the function may be used. The process is the logarithm of the Radon-Nikodym derivative between the probability measure post-regime shift and the measure pre-regime shift of the process , and is the probability measure under which is a martingale. The false alarm constraint faced by the agent is given by

| (8) |

and the threshold is set such that it solves is unique for each choice of , and the constraint (8) is binding with equality.

Shiryaev (1963) studied the simplified scenario of the so-called “Brownian disorder” for a Brownian motion with constant diffusion coefficient and at the drift changes to . Note how (8) essentially reduces to (5) for constant and . Adapting this case to our framework, which will be of relevance in our subsequent applications, the optimal stopping time under the constraint (5) is given by (6) where now one has

| (9) |

under the martingale measure for the pre-regime shift resource stock . The threshold is the solution of the equation . Furthermore, the expected delay of detection is given by

| (10) |

The detection procedure involves observing the process given by the resource stock’s log-likelihood ratio (the Radon-Nikodym derivative) of the resource dynamics under the two regimes, and comparing it to its minimum.666Note that we are under the measure . If the two regimes are very similar (for example, if is very small in the constant diffusion coefficient case), then the Radon-Nikodym derivative between the two measures will often be close to unity. In this case the process , which is known as a cumulative sum (CUSUM) process, will remain close to zero. This implies that unless the diffusion coefficient is very small, it will take longer on average to detect the presence of such a small drift change. On the other hand, if the two regimes are substantially different, then one should be able to detect the change faster. At the stopping time the agent will detect the change in drift, which is the change from a -martingale to a -sub/supermartingale.

Constraints (5) and (8) may not appear intuitive but can be understood in the context of costly false alarms i.e. if a negligible regime shift is expected the agent would be willing to tolerate for longer the uncertainty on . For a small , the difference between the pre- and post-shift problems is negligible and therefore so is the loss incurred within the delay. In either case, is decided ex ante by the agent and it can be interpreted as a measure of tolerance to ecological uncertainty. Additionally, can also be a measure of the “quality” of the detection system as it bounds the expected delay in the detection under a false alarm, i.e. the minimum waiting time the agent faces when (the change point never occurs) before reassessing extraction decisions. This quantity depends on the ex ante information the agent has on the magnitude of the regime shift, as well as early warning signals on the proximity of structural changes. The effective time period in which the agent optimizes is therefore between and the final time given by a combination of and i.e. the expected time to first reassessment plus the delay of detection. The “tolerance” is chosen by the agent, however, is a random variable. Since the agent knows the average delay time of detection it can assume as time horizon the sum of the expectations of both change-point and delay, which is equivalent to taking an ex ante time interval . In the baseline detection case the agent has a uniform/uninformative prior on the time of the regime shift .777Bayesian extensions of quickest detection problems that include prior beliefs on the change point time have been studied, among others, by Gapeev and Shiryaev (2013): we leave the complex yet important application of these methods to our framework for future research.

Monitoring continuously the resource stock can be a costly procedure. However, obtaining a constant stream of data on is already required in order for the agent to calculate its optimal extraction policy in (3). This cost can be included straightforwardly in the criterion and once included, the added costs of undertaking the detection procedure are negligible. On the other hand, the loss the agent incurs in not implementing the procedure is non-zero and increasing in the delay. Implementing a detection procedure that minimizes the delay, and therefore our framework, is Pareto optimal.

2.2 The resource-extracting monopolist’s problem

We now focus on the relevant scenario for our application. The firm’s detection strategy presented in the previous section applies to a very general framework. The strategy takes the optimal extraction policy as given, as well as known to the agent (i.e. is -adapted). In this section we study what is the optimal extraction policy of an agent that wants to implement the detection procedure in its decision-making process. In order to obtain a tractable form for the optimal we assume the dynamics of the resource stock to follow a controlled geometric Brownian motion, which is Eq. (3) with as resource growth, as regime shift and as diffusion coefficient, where . The detection problem is now a detection of a regime shift yielding a change in the growth rate of the (uncontrolled) resource stock from to . The first question that we need to address is how can the detection procedure be integrated in this framework, and what are its implications for the firm’s extraction decisions.

The risk-neutral monopolist faces an isoelastic inverse demand function of the form and with a marginal cost function defined as , where .888Cost functions of this form also allow us to flexibly model a natural monopoly, as the technical definition of a natural monopoly is that the cost function is subadditive. That is, . Hence it is always cheaper to produce units of output using a single firm than using two or more firms. Lastly, the specific choice of for the marginal cost exponent is necessary to obtain a quasi-explicit solution. For a discussion of this cost function in a resource extraction setting we refer to Pindyck (1987). The extraction rate is chosen by the firm in order to maximize the expected value of the sum of discounted profits under the resource dynamics (3), and the profit function takes the form

| (11) |

We assume a profit function depending on both the stock level and the extracted quantity which implies a marginal cost function linear in extraction, rather than the stock level, and no fixed operating costs. This assumption can be relaxed at the expense of an optimal extraction function only available in numerical form.

The simplest way of modeling a regime shift is to assume that the shift occurs only once and there are only two periods, pre-shift and post-shift. The firm’s problem therefore reads:

| s.t. | ||||

and the extraction policy exists among the class of admissible Markov controls . A natural boundary condition of this problem is .

Here the firm assumes a constant the second period.

The solution to this problem is presented in the following Proposition:

Proposition 1. The extraction policy that solves the monopolist’s problem (2.2) is given by:

| (13) |

where for is the solution to the ordinary differential equation

| (14) |

equipped with the boundary condition , where is a constant that solves the equation

| (15) |

and for . The resource rent for the monopolist is given by

| (16) |

which is the value of a marginal unit of in situ stock.

Proof: See Appendix A.3, where we show how the monopolist’s value function can be characterized as a viscosity solution of the Hamilton-Jacobi-Bellman equation associated with the optimization problem (2.2).999The optimal extraction policy is therefore a weak solution of (2.2). Note that is the optimal extraction rate for a stationary problem (i.e. when ) when there is no detection procedure put into place, and the firm never realizes the occurrence of a regime shift, and identifies , the extraction rate of the stationary problem post-shift.

Sakamoto (2014) highlights that ecological shifts are better modeled as open-ended processes in which several regime shifts can occur. For example, Hare and Mantua (2000) show that the aquatic ecosystem in the North Pacific Ocean has experienced multiple regime shifts for the past forty years. Within an open-ended, multi-regime setting, the firm detects subsequent regime changes throughout successive periods. It is however unlikely that the firm knows the magnitude of the regime shifts beyond the one it is currently detecting. This issue is especially present if the regime shift magnitude depends on the amount extracted or the state of the resource. The way the firm’s problem is therefore set up is that in each period the firm will undergo the detection procedure for the regime shift . Once the regime shift is detected the firm will update the set using all available information at such as the stock level or the total extraction up to and form expectations on the magnitude of the next regime shift thus restarting the detection process. The stochastic control problem of the firm will therefore read:

| s.t. | ||||

where are the different periods, Here , since in the first period the growth rate of the resource stock is , and are the subsequent periods and relative changes in resource growth. Here we formalize the structure of the firm’s extraction decisions in a sequential manner. Once solved, this problem will yield a piecewise continuous control. The key issue in this sequential formulation is that the firm does not know at the entire sequence of regime shifts , but rather only the one that it is trying to detect. After each detection the firm updates its set and constructs expectations on the magnitude of the next regime shift and the next detection time . The firm’s optimal extraction policy is presented in the following Proposition.

Proposition 2. The extraction policy that solves the monopolist’s problem (2.2) is a sequence of the optimal policies for each time period . The optimal policy for each period is given by:

| (18) |

where is the solution to the ordinary differential equation

| (19) |

equipped with the boundary condition , where is a constant that solves the equation

| (20) |

Proof: See Appendix A.3.

It could now be of relevance to model a “full information” scenario in which there is a finite number of subsequent regime shifts , and the firm knows their magnitude at . This problem now reads as follows:

| s.t. | ||||

where we note that now the expectation in the criterion is evaluated at time . The solution of this problem is presented in the following Proposition:

Proposition 3: The optimal policy for the monopolist facing the sequential problem (2.2) under full information of the sequence has the same form as (18) and (19), but the time-varying policies are determined by boundary conditions obtained by backward induction:

| (22) |

Proof: See Appendix A.3.

It can be easily seen that the two-period, one regime shift problem (2.2) is equivalent to the full information problem (2.2) over two periods, by simply noting that in this case at (now the only change point) the boundary condition is , which is precisely the boundary condition of Proposition 1.

Since in every scenario the optimal extraction policy is linear in and the regime shift enters log-linearly at each , the optimally controlled resource stock process expressed in growth rates is equivalent to a Brownian disorder problem. It is therefore clear that one can implement detection procedure with constant parameters described in Section 2.1 by applying it to the process

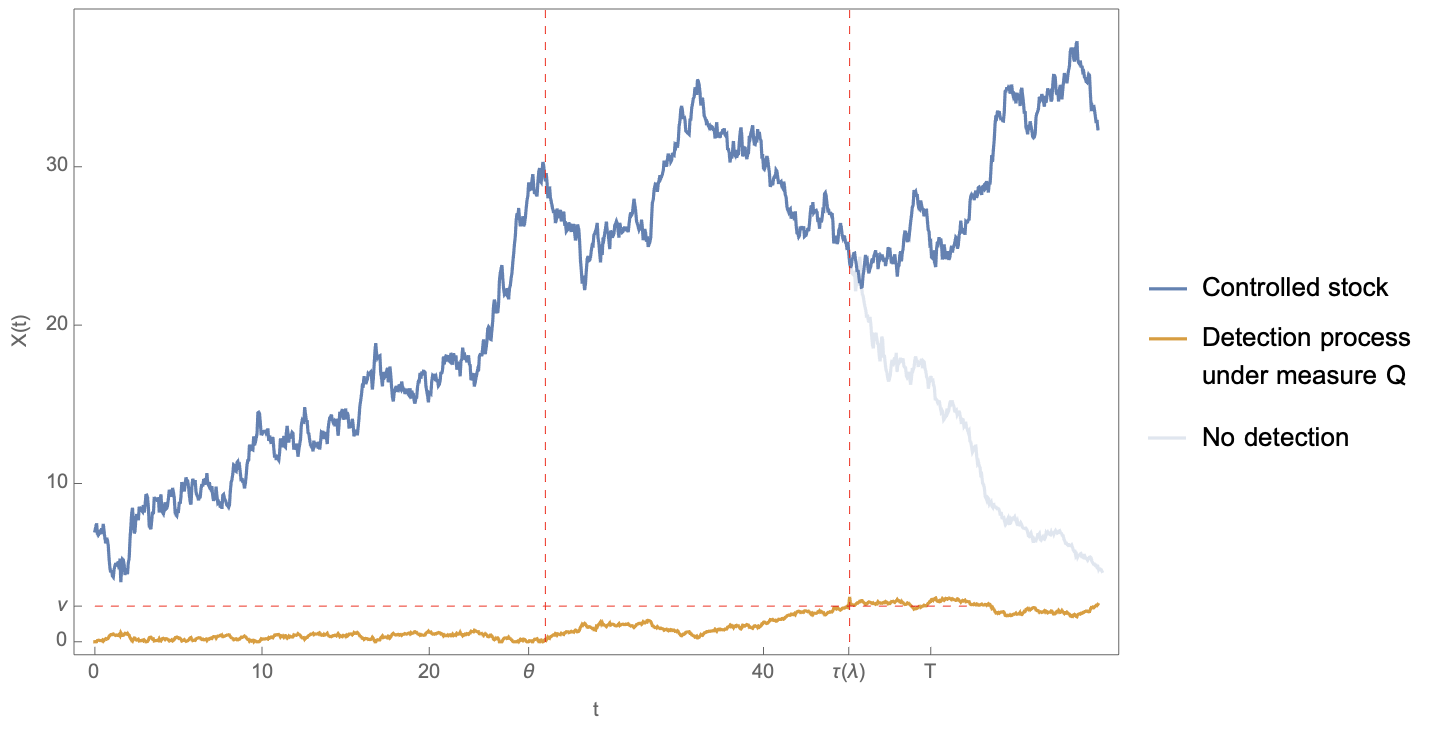

in each period , under a change of measure such that the pre-shift process is a martingale. Figure 2 shows a simulation of the detection procedure where the resource stock is hit by an adverse regime shift at , which is subsequently detected successfully by the firm at time , which occurs when the Q-CUSUM process hits the threshold . From the figure one can see how the delay in detection can yield resource over-extraction, since the “real” growth rate of the resource stock shifts to at , but the monopolist continues to apply an extraction policy which does not account for this change. Once the regime shift is detected at , the extraction policy is updated and the resource stock is extracted optimally once again. Additionally, Figure 2 shows the counterfactual dynamics of the resource stock in absence of the detection procedure where the firm continues to apply the “wrong” extraction policy yielding a substantially lower stock level.

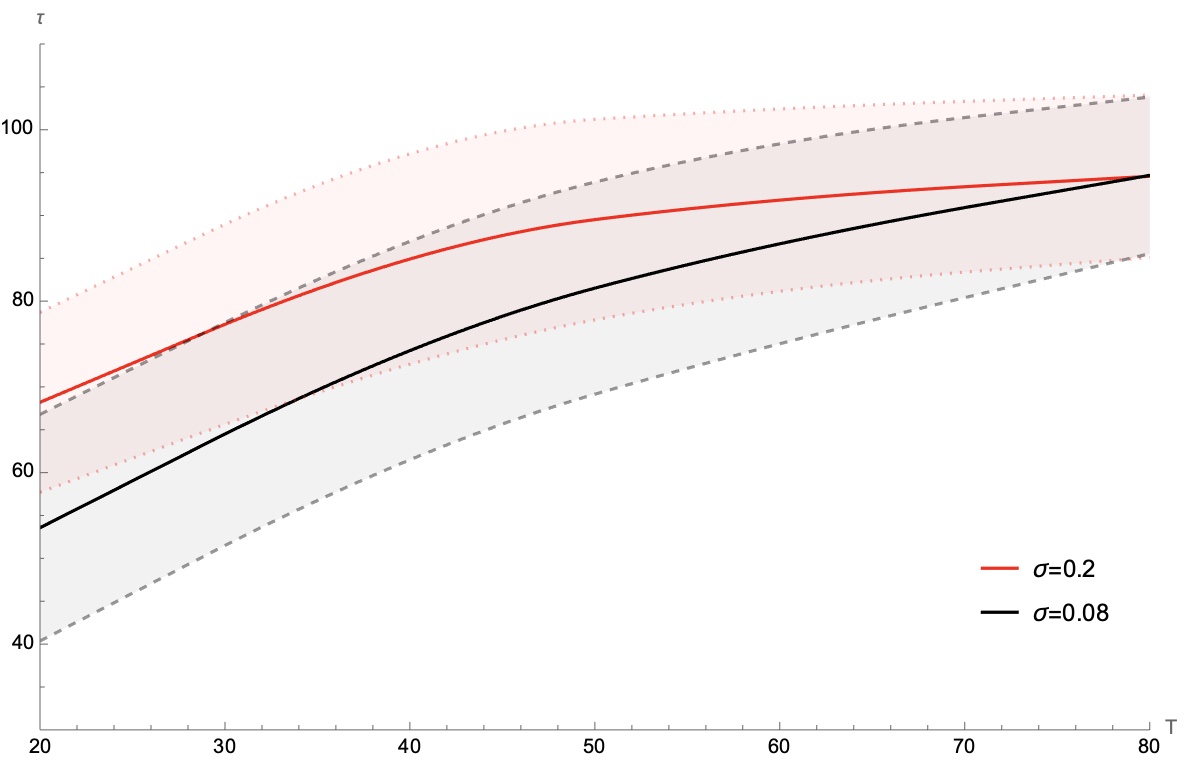

The choice of , mean time to the first false alarm, is left for the firm to choose based on its information set , and is therefore arbitrary. It is however a relevant parameter in our framework as it regulates the threshold at which the process (7) triggers the detection, and consequently sets the time horizon in which the firm operates. It is therefore important to understand the effect of varying on both resource and extraction dynamics, and establish a set of criteria for its choice. Figure 3 shows how the choice of has a concave effect on the detection time. The thick lines in Figure 3 presents Monte Carlo estimates of the average detection time, as well as its 95% confidence band, using the same parameters as Figure 2 except for two different choices of . The variance of the log-normal fluctuations is a key parameter for detection as it is inversely proportional to the expectation of the detection time , and thus directly affects the firm horizon. These estimates are obtained via varying on a grid between 20 and 100, and for each point running 200 simulations of the optimally controlled with relative extraction , as given by (13) evaluated with its respective -dependent time horizon and boundary conditions. The regime shift occurs at for each value of on the grid, which is equivalent to assuming uniform priors on . One can see that whilst is increasing in , its sensitivity is limited and drops drastically for large for all levels of . This result is robust to varying parametric choices.

The time at which the regime changes is unknown: the firm therefore will use the expected detection time (10) and the expected false alarm as a “maximal delay” estimate, in order to evaluate the boundary conditions and simultaneously undertake the detection procedure. If the threshold is reached before the expected detection time , then the firm switches to the subsequent period with the modified drift since the regime shift has been detected. It is also possible to introduce the stopping time itself as the final time, , thus directly joining real-time detection and firm optimization. This choice would leave the properties of the model unchanged, as it can be shown with standard arguments that the value function of the real-time problem can be rewritten as an infinite-time version of the value function of the problem (2.2) with a stochastic discount factor :

in the augmented state space , where is the solution of

The problem is more involved but the form of the extraction policy remains unchanged and at each detection time the firm will switch to the next period. As our specification is equivalent to uniform priors on the unobservable change point and this distribution is unaffected by within-period firm choices, the problem only involves the well-known distributional properties of running minima. We leave a more comprehensive exploration of this aspect, especially for when the occurrence of or the firms’ priors are influenced by the actions of economic agents, for future research.

2.3 Response to adverse regime shifts

Having established the optimal policy in the previous section we can now study the effects of detection of an adverse regime shift on the firm’s extraction decisions. We choose to focus on and the two-period, one shift case shown in Proposition 1 since this scenario is a good fit for our empirical application, and because we deem adverse shifts to be of greater real-world relevance. All that follows holds when and there are multiple subsequent regime shifts.

The first insight that can be drawn is straightforward and consistent with the existing literature: one can show with a simple geometric argument that the solution of (15) decreases in . i.e. . This implies that an adverse regime shift unequivocally decreases the post-detection stationary extraction rate . To see this effect more clearly assume the scenario of no extraction costs which yields

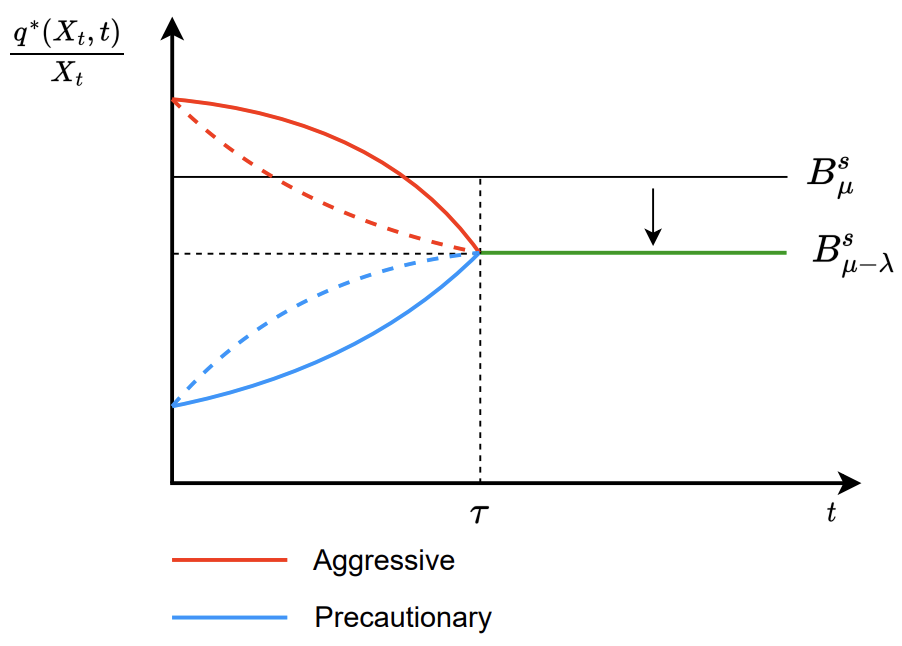

which clearly decreases as increases. This mechanism is illustrated in Figure 4, where is the counterfactual stationary rate if the detection procedure was not put in place and/or if the firm was unaware of the regime shift.

However, our central question asks how a firm responds to the prospect of a regime shift detection. The extraction policy implemented by the firm anticipating the regime shift at is determined by the sign of the right-hand side of (14) as it dictates whether its solution reaches the required final state at the boundary via a higher or lower extraction path. A novel insight of our framework is that the presence of detection can generate both extraction policies, depending on the interplay between the environmental parameters (the ability of the resource to regenerate, the variance of the environmental fluctuations) and the firm-related ones (demand elasticity, extraction costs, detection time). A precautionary policy is defined as one where the firm decreases resource extraction when compared to and reaches the post-detection stationary policy from below. On the contrary an aggressive policy is where the firm increases extraction greater than and reaches from above. A pre-detection policy is aggressive if the gradient of the solution of (14) is positive. A necessary condition is given by

| (23) |

which is more likely to hold for larger adverse regime shifts. This condition, however, is not sufficient. What is required is that the \sayexponential term, the first term on the right-hand side of (14) that contains all the environmental parameters, changes sign and dominates the second term which is a “power” term.101010Note that for the degenerate case of (no demand) condition (23) is sufficient. On the other hand, the firm pursues a precautionary extraction policy when (23) is reversed, or if the condition holds but does not meet the sufficiency criterion. Both extraction policies are illustrated in Figure 4. The curvature of the pre-detection policy in either scenario is determined by the parametric values of the problem in (14). Although the dashed lines represent cases which can occur within a smaller parametric space, the solid lines are the most likely combinations to be observed.

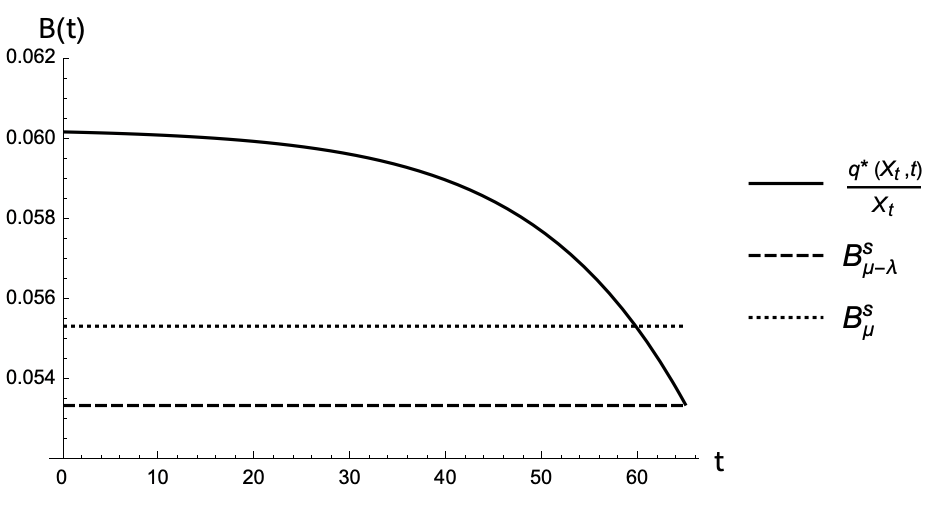

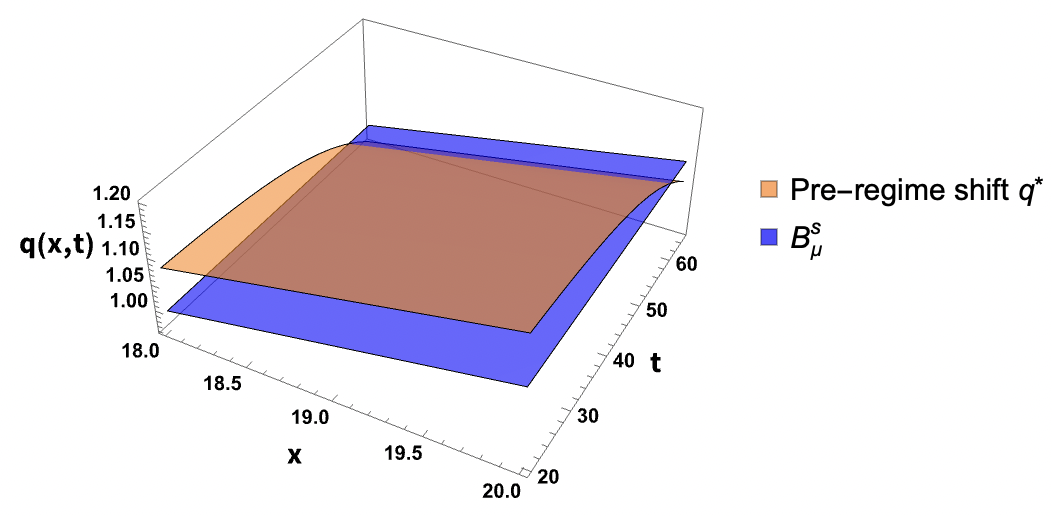

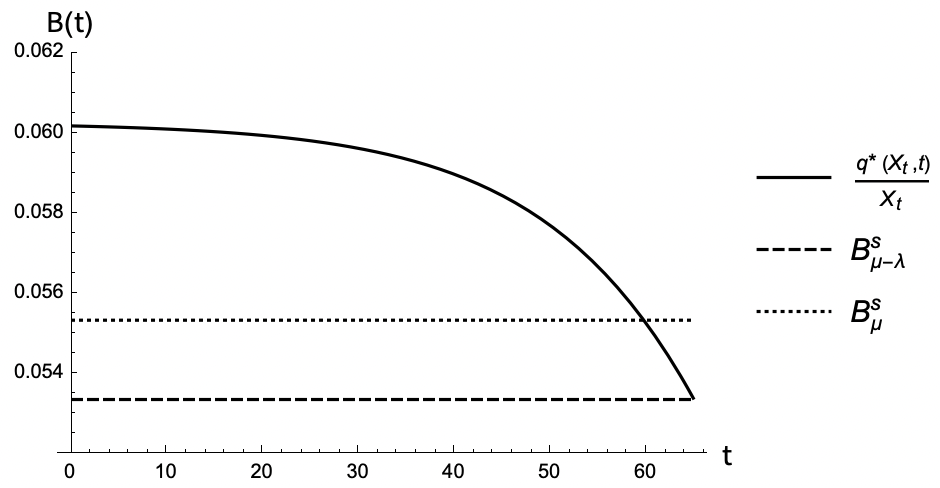

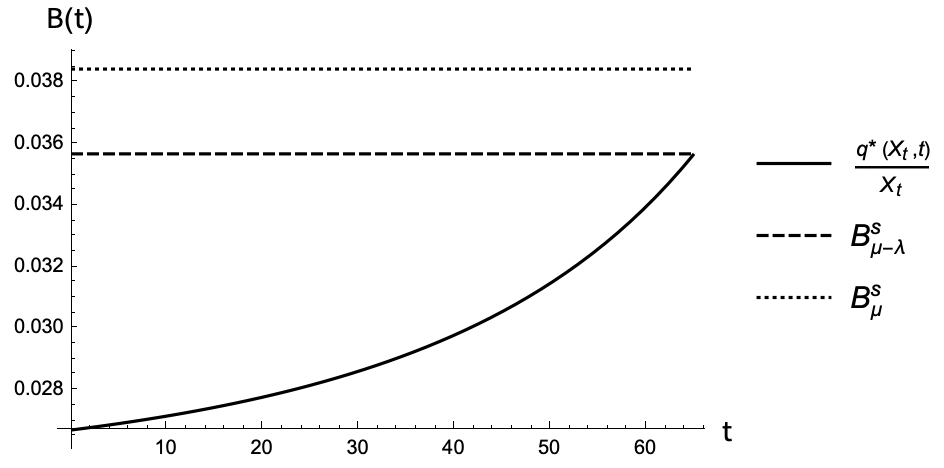

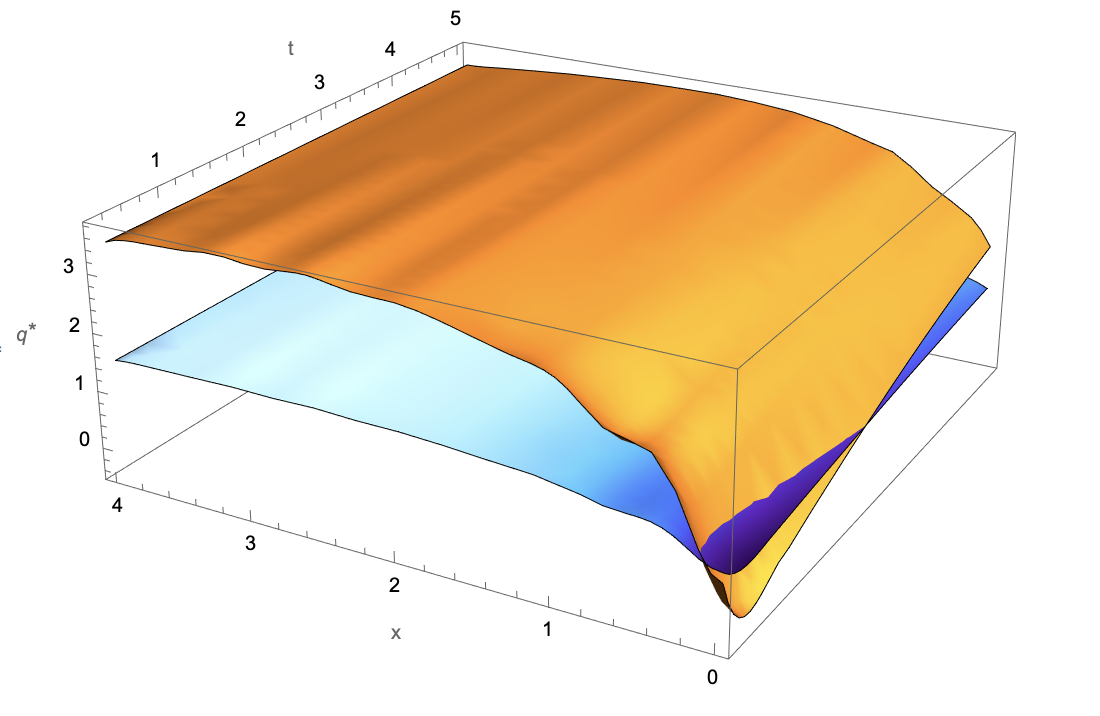

Figure 5 presents a numerical illustration of the emergence of an aggressive extraction path pursued by a firm pre-detection. Suppose an ecosystem with a growth rate of 15% () undergoes a regime shift of magnitude . In Figure 5(a) the solid line charts the pre-detection optimal extraction rate of a monopolist up until , obtained by calibrating . The resource extraction policy put in place in anticipation of an adverse regime shift is higher than the dotted line representing the counterfactual stationary policy i.e. if the detection procedure was not implemented and/or the firm was operating in the absence of the knowledge of a regime change. The dashed line is the new post-detection stationary policy which is lower than . The point at which the pre-detection extraction equals the post detection stationary extraction is the boundary condition given by . Figure 5(b) represents the above mechanics in a three-dimensional plot where the orange shaded region depicts the evolution of the firm’s optimal extraction policies prior to the regime shift detection and the blue shaded region shows .

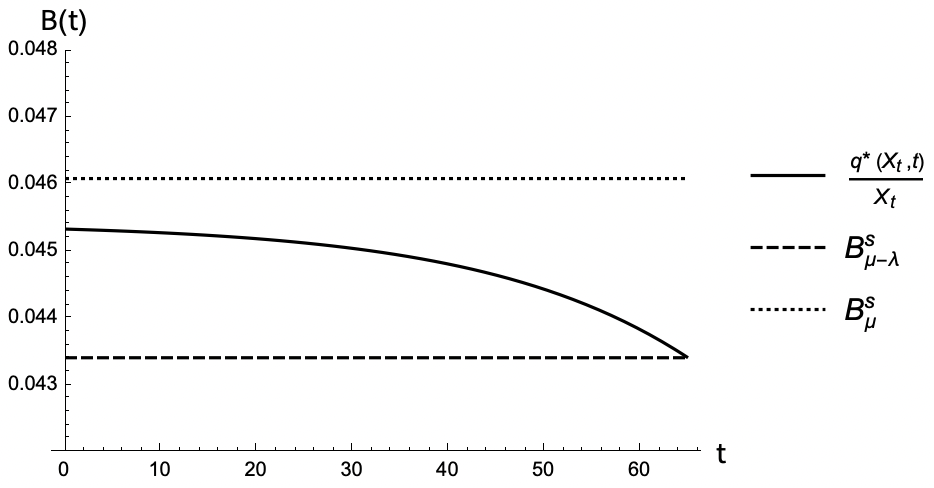

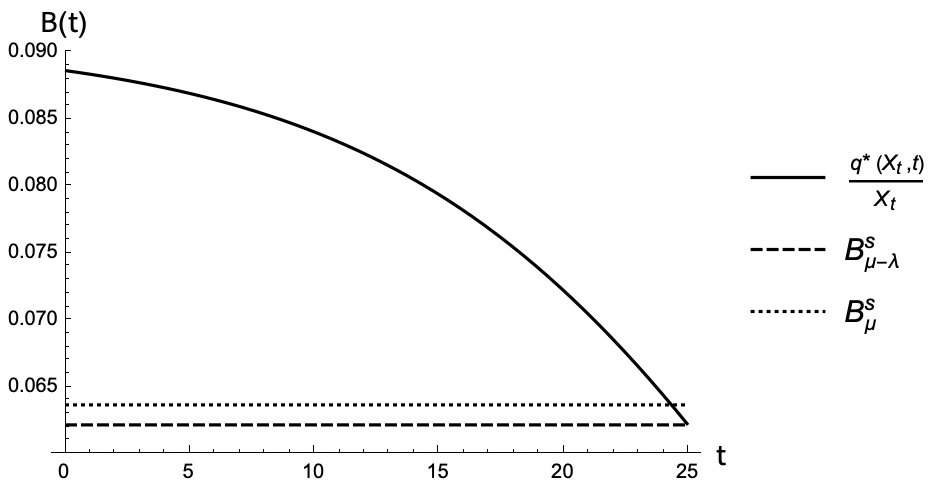

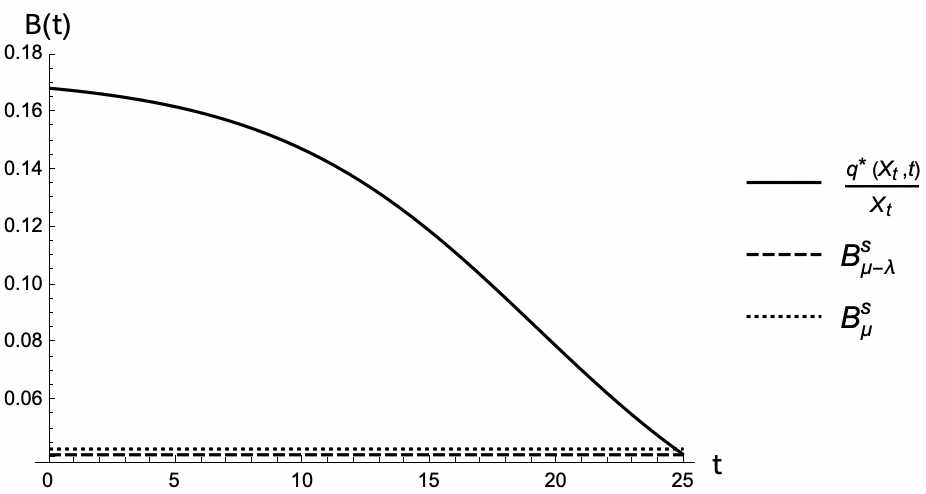

We now examine the role of demand elasticity. It is easy to show that the derivative with respect to of the right-hand side of (23) is given by , which implies that an increasingly elastic demand will switch the firm’s response to an anticipated adverse regime shift from aggressive to precautionary. Figure 6 illustrates this mechanism numerically using three different magnitudes of . A more elastic demand increases the marginal cost and because is convex in resource stock, a negative regime shift increases the expected extraction costs (on average) over time, which creates an incentive to extract faster. Nevertheless, this is dominated by the increase in value of the in situ resource stock due to higher demand elasticity, leading to a higher resource rent thus switching the pre-detection extraction policy from aggressive to precautionary. However, note that the right-hand side of the inequality in (23) for large limits to the discount rate , which implies that if the initial drift is negative and the resource is already heading towards collapse, the switch to precautionary never happens even with a highly elastic demand. This is illustrated in Figure 7 where the resource drift is and one can observe that the pre-shift detection policy continues to be aggressive. This is because the total value of the in situ stock of the resource is a concave function of the stock and that value is reduced by a negative drift thus incentivizing the firm to speed up extraction. This combined with higher costs reduces the value of the marginal in situ unit and results in the firm continuing to pursue an aggressive extraction policy.

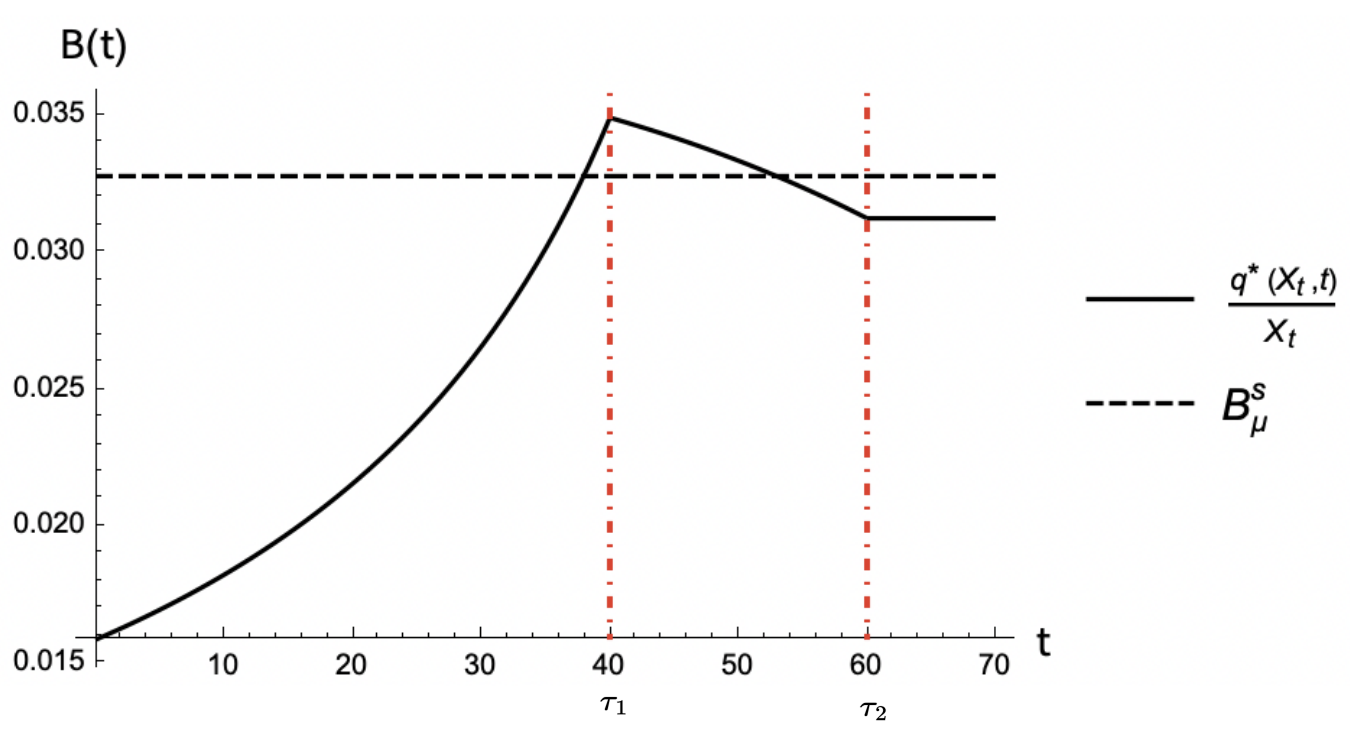

Figure 8 illustrates the case of a monopolist with full information detecting multiple regime shifts as discussed in Proposition 3. Suppose an ecosystem with a growth rate of 15% () undergoes two regime shift of magnitude and . In Figure 8 the solid line shows the evolution of the optimal extraction path of a monopolist for the detection times and obtained by calibrating , and the dashed line represents the counterfactual stationary policy . We find that in anticipating the detection of multiple adverse changes in the resource dynamics, the monopolist can in fact switch from precautionary to aggressive extraction as seen in the interval and vice versa as seen in .

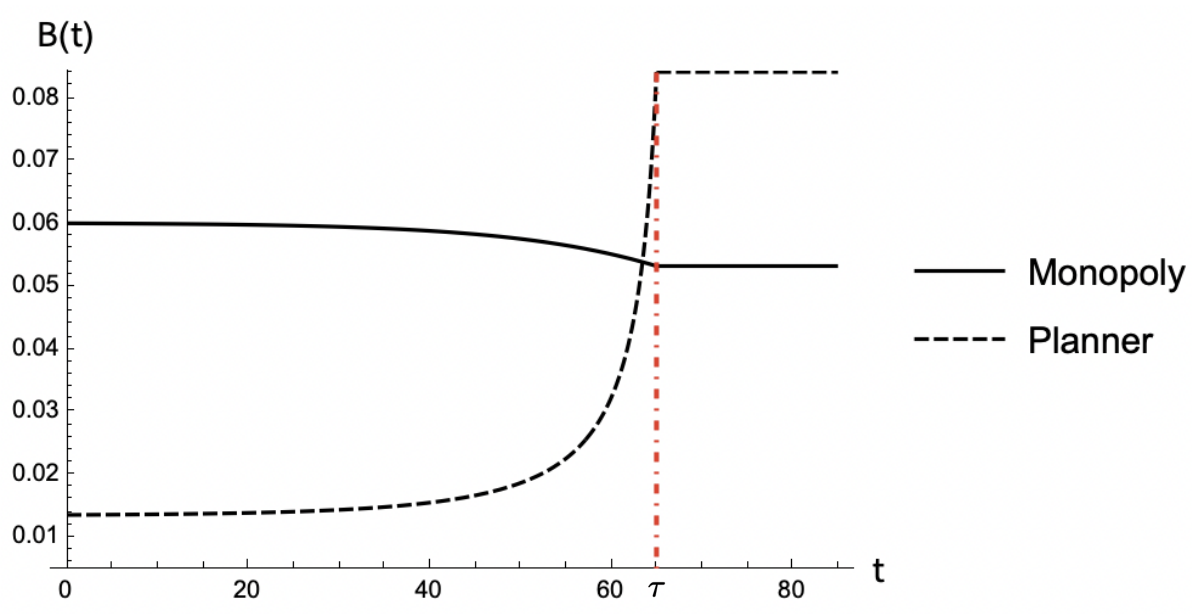

As a useful benchmark, let us discuss the case of a competitive extraction path and compare it to the monopolist’s optimal policy. It is well known that in the absence of externalities the competitive equilibrium is welfare maximizing, i.e. it yields the same aggregate extraction trajectory as that which maximizes the expected value of the sum over time of discounted net surplus. This scenario allows us to study how a social planner would respond to the prospect of a regime shift detection. We assume every agent has the same information set in the formation of the expectation , so that all agents “compete” perfectly on detection as well. The criterion used by the planner is given by:

for all admissible policies . We solve this scenario and present all details in Appendix A.4. Figure 9 illustrates the evolution of the pre- and post-detection extraction policies of a monopolist and a social planner. Note that the post-detection stationary extraction rate for the planner is higher than the monopolist, which is consistent with the fact that the quantity produced by a monopoly is below the socially efficient level leading to the famous suggestion of the monopolist being \saythe conservationist’s best friend (Hotelling, 1931; Solow, 1974). However, while the anticipation of an adverse regime shift leads the monopolist to adopt an aggressive policy, on the contrary the social planner pursues a precautionary extraction path. This result sheds an important light on understanding how a monopolist may respond to ecological uncertainty compared to society’s preference.

Lastly, we present an extension of our framework in Appendix A.5 where we solve numerically the HJB for the monopolist’s problem under linear demand and resource dynamics driven by a Brownian motion with constant diffusion parameter and a periodic drift to represent seasonality. We find that the scenario presented, which is similar to the one we study in our empirical application, yields similar results as the ones presented in this section.

3 Empirical application: catastrophic regime shift in the Cantareira water reservoir

The main piece of evidence motivating our paper is that ecological regime shifts are indeed often observed in the dynamics of renewable resources. A scenario in particular that captures well the essence of our framework is the case of one of the world’s largest water reservoirs, the Cantareira system. The Cantareira reservoir is an ensemble of six reservoirs connected by channels and pipelines serving the Metropolitan Area of São Paulo (MASP) in Brazil, which is one of the largest metropolitan areas in the world. The Cantareira system is managed by Companhia de Saneamento Básico do Estado de São Paulo (SABESP), a water and waste management company acting as a semi-public natural monopoly.

In early 2013, the volume experienced a sharp decrease and the operational capacity of the reservoir was subsequently depleted. This depletion occurred despite the preceding rainy season being one of the heaviest recorded in recent times. At one point, the city’s main Cantareira reservoir was down to 5%, which barely covered a month’s supply of the population’s requirements. SABESP realized the critical state of the reservoir only in January 2014 and began to reduce withdrawals, but by July 2014 the operational capacity of the reservoir was depleted. Since then water withdrawal has been done by pumping of the so-called “strategic reserve” or “dead volume”, as well as starting to drill underground to extract groundwater. Dead volume pumping involves extracting the water that remains at the bottom of the reservoir, an often-criticized practice as it is considered dangerous due to the increasingly stagnant nature of the water as well as the presence of harmful elements. This shortage led to an unprecedented crisis of water supply faced by MASP in 2014, which left the 20 million inhabitants of the area at risk of catastrophic drought whose long-terms impact are still felt to this day (Sousa et al. (2022)).

Coutinho et al. (2015) study the close-to-depletion reservoir dynamics via a tipping-point transition approach. The reasons behind this catastrophic outcome have clear roots in environmental changes. The expansion of deforestation activities into the Amazon basin has increased pollution, severely reduced the upstream water sources and reduced rainfall. Some of the causes, however, can also be found in the economic decisions behind the crisis such as SABESP’s poor water management with fragile pipes and ageing infrastructures. Furthermore, during the water crisis of 2014, SABESP failed to warn their citizens about the rationing of water resources, and awarded major bonuses to its directors despite the gravity of the situation.111111https://theconversation.com/sao-paulo-water-crisis-shows-the-failure-of-public-private-partnerships-39483

This scenario is therefore an ideal test for our framework. The first question is whether a regime shift consistent with (3) actually happened. The second question is whether SABESP could have detected the regime shift by applying our framework before early 2014, which is when the firm started reacting to the rapidly depleting reservoir. If this is the case, the last question we want to ask ourselves is whether the reservoir depletion could have been avoided, or at least delayed, if SABESP would have reacted to the regime shift by adjusting its outflow policy at the detection time.

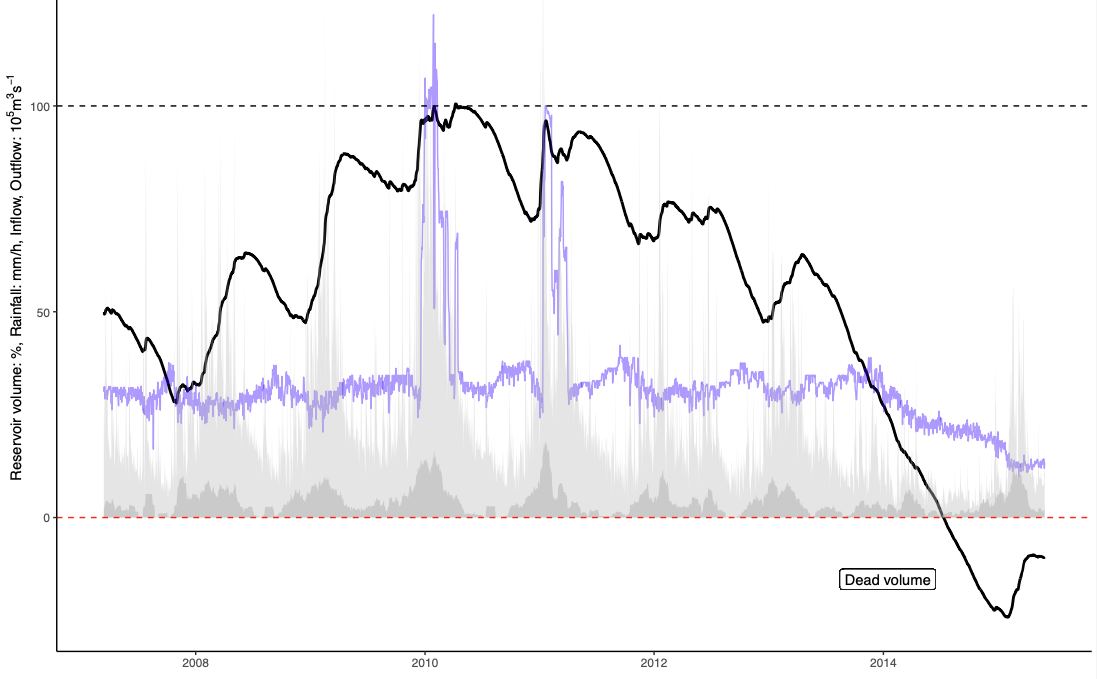

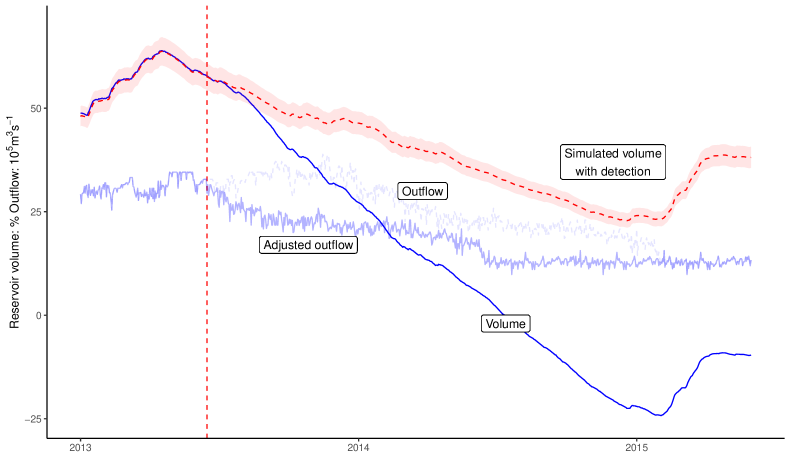

Figure 10 illustrates the reservoir dynamics. Observe that despite the inter-annual trend, a clear seasonal fluctuation is present in the rainfall (darker grey shaded region) which is reflected in the volume of stored water or the percentage of operational volume, as shown by the black line. In early 2010 and 2011 outflow (the blue line, equivalent to in our framework) had to be suddenly increased as a consequence of high river inflow, in order to allow the reservoir volume to stay within its maximum capacity. Around early 2013 the reservoir volume suddenly began a sharp decline initiated by a reduction in inflow and rainfall. In 2015 inflow and rainfall increased, but neither translated into an increase in the reservoir volume, which stabilized at a level well below the necessary operational capacity and remained persistent. This new reservoir level generated enough scarcity to plunge the region into the aforementioned water crisis. For inflow we use daily data from the rivers Jaguari, Cachoeira, Atibainha and Piva, as well as the upstream Àguas Claras reservoir, obtained from the public bulletins on SABESP’s website. The firm “extraction” is the outflow from the reservoir allowed daily by SABESP, which equals to river outflow plus the amount of water pumped to be sold for regional consumption. Rainfall is obtained as the daily precipitation levels (mm). We input inflow, rainfall and extraction and estimate the following model:

| (24) |

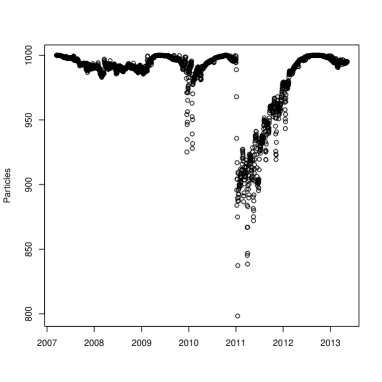

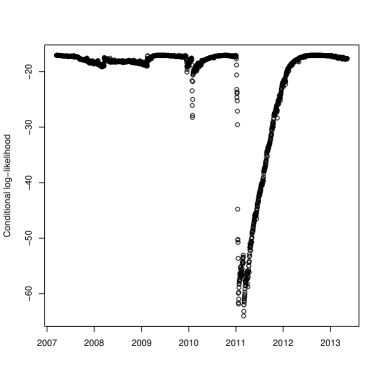

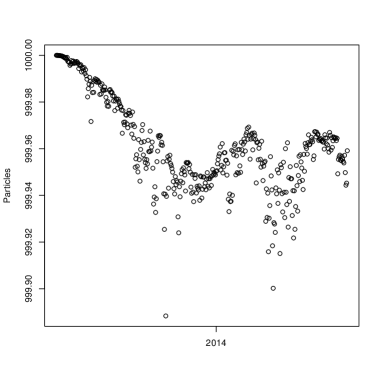

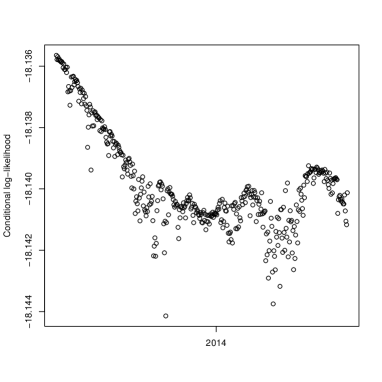

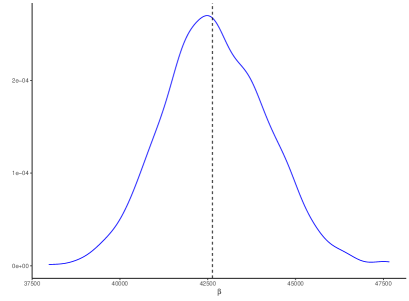

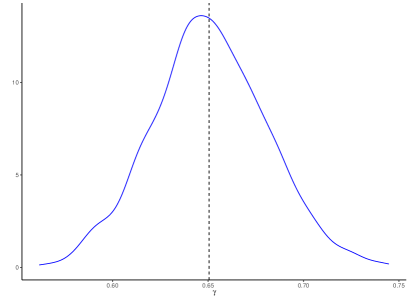

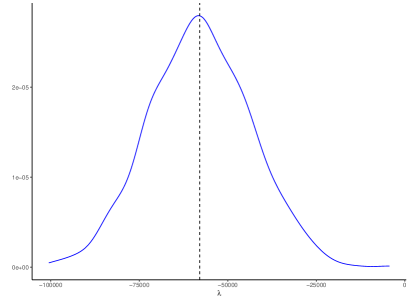

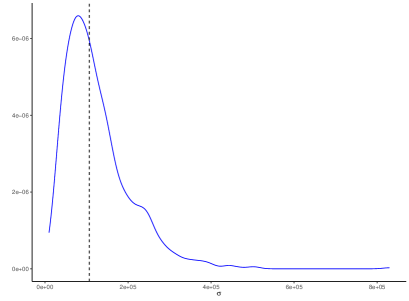

where is assumed as one day to match the daily data and is assumed to happen at the beginning of March 2013, when the reservoir volume deviated significantly from the pre-existing trends. Varying this change point in an interval of 2 months yields equivalent estimates. There is no evidence of the variance of the fluctuations being dependent on , such as in Section 2.2 and 2.3, and the drift is clearly time-dependent due to seasonalities, and therefore we estimate the model (24) with a time-dependent drift. We then estimate and by means of joint particle filtering for both state and parameters. All details on the simulation, filtering procedure and parameter estimation is reported in Appendix A.6. Table 2 reports the coefficient estimates and their standard errors of each filtered parameter distribution. Additionally, a likelihood ratio test between the model (24) and a specification with geometric fluctuations (i.e. with as noise source) yields a p-value of thus providing evidence that validates specification (24).

| (pre-shift) | 42781.41 | 0.658 | - | 202094.3 |

|---|---|---|---|---|

| (4214.25) | (0.009) | - | (38110.37) | |

| (post-shift) | 42668.86 | 0.618 | -66885.78 | 176511.4 |

| (1715.6) | (0.026) | (8552.4) | (25324.43) |

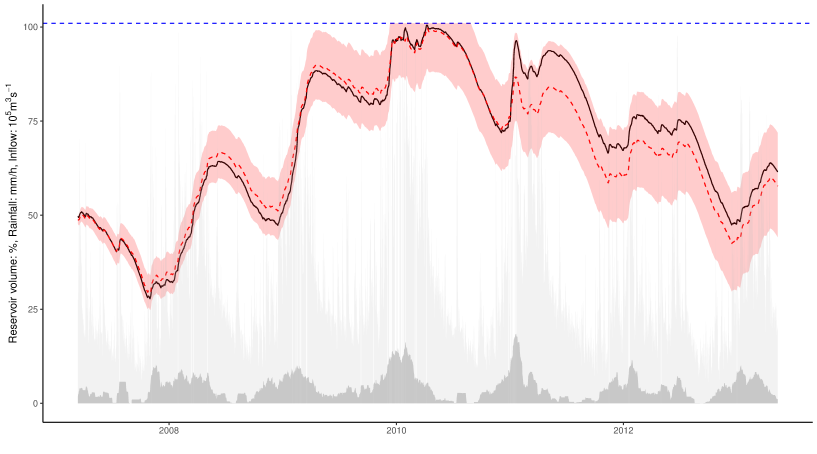

Estimation of both pre- and post-shift models show that the rainfall coefficients as well as the variance of fluctuations do not change significantly between the pre- and post-shift periods: rainfall parameters are essentially unaffected, and is the parameter that varies the most (from ca. cubic meters to ), and even though the difference is not statistically significant this change shows how the dynamics of the reservoir after the regime shift become increasingly driven by the deterministic part. This is shown in Figure 11 which plots the fitted pre- and post-shift models against the observed reservoir volume. For plotting convenience, both model fit and volume are expressed as percentages with respect to the reservoir’s capacity ranging from a maximum of to a minimum volume of below which the pumping of the dead volume is activated. The figure shows how the model estimated in (24), shown by the dashed red line, tracks well the data (solid black line) whilst remaining firmly within a 95% confidence band obtained by sampling 1000 coefficient sets from their reconstructed distributions, and running 1000 simulations for each set. The slight decay in fit in early 2011 for the pre-shift model, seen in the top panel of Figure 11, leaves open the possibility of the presence of multiple regime shifts. The bottom panel of Figure 11 shows how the post-regime model in (24) fits very well the data, as well as how the regime shift manifests by the emergence of a dominant deterministic force that drives the reservoir volume to the point where the operational capacity is exhausted.

Furthermore, estimating the pre-shift model using the post-shift data results in a substantially worse fit: a likelihood ratio test between the model estimated in Table 2 and the same model without yields a p-value of which provides further evidence of the regime shift. We remain open-minded on the interpretation of what caused the emergence of : all evidence points towards a story of climate change exacerbated by deforestation around the upstream Amazon basins, leading to droughts and rising temperatures. This is captured in our framework by a deterministic force towards depletion, broadly conceivable as a reduced environmental suitability for the pre-existing volume levels of the reservoir.

| T | (detection date) | (days) | |

|---|---|---|---|

| 30 | 24.67 | 16-06-2013 | 138 |

| 100 | 25.874 | 16-06-2013 | 138 |

| 500 | 27.484 | 23-06-2013 | 145 |

| 1000 | 28.177 | 23-06-2013 | 145 |

| 5000 | 29.786 | 29-06-2013 | 151 |

| 10000 | 30.479 | 29-06-2013 | 151 |

Upon estimation of , and , we now turn to the remaining two questions of interest with respect to our framework. The first question is whether SABESP could have detected the regime shift. We therefore implement the detection procedure presented in Section 2.1 as our model shows evidence of constant diffusion and regime shift coefficients. Let us now conjecture what could have been done if SABESP had started the detection process in real time on January \nth28, 2013. This date represents the first time at which both river inflow and rainfall deviated significantly (i.e. more than twice the long-term standard deviation) from both their long-term trends for more than two weeks.121212This criterion is chosen arbitrarily: we note however that the choice of is irrelevant in terms of detection time. We prefer this criterion as it relates to a possible “early warning signal” that could have been noticed ex ante. The firm’s detection problem involves observing the running minimum/cumulative sum process over the reservoir volume under the appropriate change of measure, and detecting the presence of a regime shift once this process hits the threshold . Note that the change of measure is effectively the way to account for all observable effects of inflow and rainfall on reservoir volume, and estimate whether a new force () has emerged that transformed the “residual” fluctuations in a supermartingale.

This threshold, however, depends on the firm’s tolerance/distance to the first false alarm . In order to account for this, we undertake the detection process for the substantially different values of , which imply “tolerances” (first times to false alarm) ranging between 30 days and 27 years, representing most values SABESP could reasonably assume. Given our Monte Carlo simulations shown in Figure 3, we expect a concave effect of on the detection time : this is indeed the case. Table 2 presents the different thresholds for the detection process with varying , and the corresponding detection dates and times it would have taken for SABESP to detect the shift. The detection dates range between June \nth6 and \nth29 in 2013, more than six months before the point at which SABESP started adjusting its outflow policy.

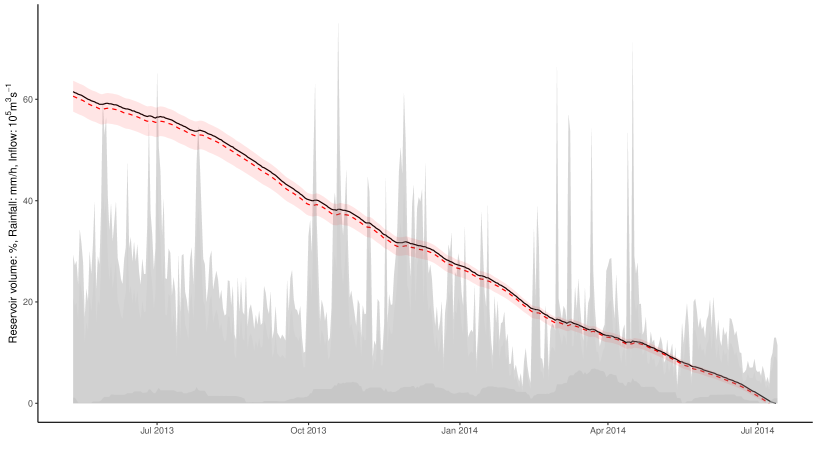

We can now address the question of whether the reservoir depletion could have been avoided, or at least delayed, if SABESP would have reacted to the regime shift by adjusting its outflow policy at the detection time. For the Cantareira reservoir, SABESP started decreasing outflow in mid-January 2014, then decreased the usable capacity limit by 18.5% on June \nth15 and by 10.7% on October \nth23. We therefore apply the equivalent outflow strategy at the average detection time (June \nth22, 2013), and obtain Monte Carlo trajectories of the model simulating 5000 trajectories keeping every other input and parameter unchanged with confidence bands obtained as before. Figure 12 shows how the simulated volume (dashed red line) remains above 25% of the maximum reservoir capacity even at times when SABESP started pumping from its strategic reserves.

It is certainly too ambitious a claim to say that the adoption of our detection framework could have avoided the water crisis. There is, however, clear evidence of how the reservoir depletion should have at least been delayed, as the regime shift that happened in 2013 could have been detected by SABESP and its outflow strategy could have been adjusted earlier. Furthermore, pumping from the dead volume could have been avoided, improving the quality of the water supplied to the population as well as saving substantial amounts of public funding poured in the company in order to tap the deepest levels of the reservoir. In a situation where every day involved rationing water for millions of people, to the point that some citizens took to drilling through their basements to reach groundwater, the adoption of our framework can help decision-makers to better understand and manage the ecosystem in which they operate.

4 Concluding Remarks

In this paper we study the stochastic dynamics of a renewable resource subject to ecological regime shifts. The occurrence of such shifts can substantially alter the constraints faced by economic agents who extract natural resources. We establish a framework of ecosystem surveillance that minimizes the efficiency loss caused by incomplete observability of the environmental conditions in which agents operate, and show Pareto optimality of our framework for any resource-extracting economic agent. We integrate the detection procedure in the maximization problem of a resource-extracting monopolist, such that the firm optimizes with respect to the resource dynamics over a time horizon determined by the detection time. We show how our framework can generate the emergence of both aggressive and precautionary extraction strategies, and compare the monopolist’s policy with that of a social planner. Finally, we apply our framework to the case of the Cantareira water reservoir, a large-scale system of interconnected reservoirs which serves the Metropolitan Area of of São Paulo in Brazil.

Our framework is of constantly increasing real-world relevance. Several natural resource firms and government organisations are adopting automated systems for high frequency monitoring of resource dynamics thus providing the potential to enhance data-driven decision making by offering larger volumes of data in near real time. However, it is important to highlight that environmental surveillance also comes with its own set of limitations and can introduce new technical, financial, and labour requirements. Even though the benefits of monitoring may be high, the lack of institutional knowledge and easy availability of technical specialists may be preventing some firms from integrating surveillance into their decision making. This trend, however, is changing as several new companies are addressing these barriers by providing straightforward affordable monitoring solutions and partnering with research organisations.131313 Companies such as LG Sonic and Aquatic Life Ltd. are leaders in providing real time in-situ water quality data, as well as meteorological, and satellite remote sensing data for water managers:

https://www.lgsonic.com/no-algae-treatment-without-real-time-data/

https://www.iisd.org/system/files/2023-06/real-time-water-quality-monitoring.pdf

To conclude, some caveats are in order. The framework we propose for the quickest detection of ecological regimes is general and optimal for any economic agent, and although a pure monopoly and perfect competition are relatively rare within resource markets, our results can be used as a first step towards richer competition structures.

Statements

Both authors declare no competing interests.

References

- Alvarez and Koskela (2007) Alvarez, L. H. and E. Koskela (2007). Optimal harvesting under resource stock and price uncertainty. Journal of Economic Dynamics and Control 31(7), 2461–2485.

- Arvaniti et al. (2019) Arvaniti, M., A.-S. Crépin, and C. K. Krishnamurthy (2019). Time-consistent resource management with regime shifts. Economics Working Paper Series 19.

- Baggio and Fackler (2016) Baggio, M. and P. L. Fackler (2016). Optimal management with reversible regime shifts. Journal of Economic Behavior & Organization 132, 124–136.

- Bardi et al. (1997) Bardi, M., I. C. Dolcetta, et al. (1997). Optimal control and viscosity solutions of Hamilton-Jacobi-Bellman equations, Volume 12. Springer.

- Barrett (2013) Barrett, S. (2013). Climate treaties and approaching catastrophes. Journal of Environmental Economics and Management 66(2), 235–250.

- Batt et al. (2013) Batt, R. D., S. R. Carpenter, J. J. Cole, M. L. Pace, and R. A. Johnson (2013). Changes in ecosystem resilience detected in automated measures of ecosystem metabolism during a whole-lake manipulation. Proceedings of the National Academy of Sciences 110(43), 17398–17403.

- Bauch et al. (2016) Bauch, C. T., R. Sigdel, J. Pharaon, and M. Anand (2016). Early warning signals of regime shifts in coupled human–environment systems. Proceedings of the National Academy of Sciences 113(51), 14560–14567.

- Biggs et al. (2009) Biggs, R., S. R. Carpenter, and W. A. Brock (2009). Turning back from the brink: Detecting an impending regime shift in time to avert it. Proceedings of the National Academy of Sciences 106(3), 826–831.

- Boettiger and Hastings (2012) Boettiger, C. and A. Hastings (2012). Quantifying limits to detection of early warning for critical transitions. Journal of the Royal Society Interface 9(75), 2527–2539.

- Carpenter et al. (2014) Carpenter, S. R., W. A. Brock, J. J. Cole, and M. L. Pace (2014). A new approach for rapid detection of nearby thresholds in ecosystem time series. Oikos 123(3), 290–297.

- Ciarlet (2002) Ciarlet, P. G. (2002). The finite element method for elliptic problems. SIAM.

- Costello et al. (2019) Costello, C., B. Nkuiya, and N. Quérou (2019). Spatial renewable resource extraction under possible regime shift. American Journal of Agricultural Economics 101(2), 507–527.

- Coutinho et al. (2015) Coutinho, R. M., R. A. Kraenkel, and P. I. Prado (2015). Catastrophic regime shift in water reservoirs and são paulo water supply crisis. PloS one 10(9), e0138278.

- Crandall and Lions (1981) Crandall, M. G. and P.-L. Lions (1981). Condition d’unicité pour les solutions généralisées des équations de Hamilton-Jacobi du premier ordre. C. R. Acad. Sci. Paris Sér. I Math. 292(3), 183–186.

- Crépin and Nævdal (2020) Crépin, A.-S. and E. Nævdal (2020). Inertia risk: Improving economic models of catastrophes. The Scandinavian Journal of Economics 122(4), 1259–1285.

- Crépin et al. (2012) Crépin, A.-S., R. Biggs, S. Polasky, M. Troell, and A. de Zeeuw (2012). Regime shifts and management. Ecological Economics 84, 15–22. The Economics of Degrowth.

- de Zeeuw and He (2017) de Zeeuw, A. and X. He (2017). Managing a renewable resource facing the risk of a regime shift in the ecological system. Resource and Energy Economics 48, 42–54.

- Diekert (2017) Diekert, F. K. (2017). Threatening thresholds? the effect of disastrous regime shifts on the non-cooperative use of environmental goods and services. Journal of Public Economics 147, 30–49.

- Fleming and Soner (2006) Fleming, W. and H. Soner (2006). Controlled Markov Processes and Viscosity Solutions. Stochastic Modelling and Applied Probability. Springer New York.

- Gapeev and Shiryaev (2013) Gapeev, P. V. and A. N. Shiryaev (2013). Bayesian quickest detection problems for some diffusion processes. Advances in Applied Probability 45(1), 164–185.

- Hadjiliadis and Moustakides (2006) Hadjiliadis, O. and V. Moustakides (2006). Optimal and asymptotically optimal cusum rules for change point detection in the brownian motion model with multiple alternatives. Theory of Probability & Its Applications 50(1), 75–85.

- Hare and Mantua (2000) Hare, S. R. and N. J. Mantua (2000). Empirical evidence for north pacific regime shifts in 1977 and 1989. Progress in oceanography 47(2-4), 103–145.

- Horváth and Trapani (2022) Horváth, L. and L. Trapani (2022). Changepoint detection in heteroscedastic random coefficient autoregressive models. Journal of Business & Economic Statistics 0(0), 1–15.

- Hotelling (1931) Hotelling, H. (1931). The economics of exhaustible resources. Journal of political Economy 39(2), 137–175.

- Krämer et al. (1988) Krämer, W., W. Ploberger, and R. Alt (1988). Testing for structural change in dynamic models. Econometrica 56(6), 1355–1369.

- Kvamsdal (2022) Kvamsdal, S. F. (2022). Optimal management of a renewable resource under multiple regimes. Environmental and Resource Economics, 1–19.

- Lindenmayer et al. (2011) Lindenmayer, D. B., R. J. Hobbs, G. E. Likens, C. J. Krebs, and S. C. Banks (2011). Newly discovered landscape traps produce regime shifts in wet forests. Proceedings of the National Academy of Sciences 108(38), 15887–15891.

- Liu and West (2001) Liu, J. and M. West (2001). Combined parameter and state estimation in simulation-based filtering. In Sequential Monte Carlo methods in practice, pp. 197–223. Springer.

- Lorden (1971) Lorden, G. (1971). Procedures for reacting to a change in distribution. The Annals of Mathematical Statistics, 1897–1908.

- Moustakides (2004) Moustakides, G. V. (2004). Optimality of the cusum procedure in continuous time. The Annals of Statistics 32(1), 302–315.

- Nkuiya and Diekert (2023) Nkuiya, B. and F. Diekert (2023). Stochastic growth and regime shift risk in renewable resource management. Ecological Economics 208, 107793.

- Oksendal (2013) Oksendal, B. (2013). Stochastic differential equations: an introduction with applications. Springer Science & Business Media.

- Österblom et al. (2007) Österblom, H., S. Hansson, U. Larsson, O. Hjerne, F. Wulff, R. Elmgren, and C. Folke (2007). Human-induced trophic cascades and ecological regime shifts in the baltic sea. Ecosystems 10(6), 877–889.

- Patto and Rosa (2022) Patto, J. V. and R. Rosa (2022). Adapting to frequent fires: Optimal forest management revisited. Journal of Environmental Economics and Management 111, 102570.

- Pindyck (1984) Pindyck, R. S. (1984). Uncertainty in the theory of renewable resource markets. The Review of Economic Studies 51(2), 289–303.

- Pindyck (1987) Pindyck, R. S. (1987). On monopoly power in extractive resource markets. Journal of Environmental Economics and Management 14(2), 128–142.

- Pindyck (2002) Pindyck, R. S. (2002). Optimal timing problems in environmental economics. Journal of Economic Dynamics and Control 26(9-10), 1677–1697.

- Ploberger and Krämer (1992) Ploberger, W. and W. Krämer (1992). The cusum test with ols residuals. Econometrica 60(2), 271–285.

- Polasky et al. (2011) Polasky, S., A. De Zeeuw, and F. Wagener (2011). Optimal management with potential regime shifts. Journal of Environmental Economics and management 62(2), 229–240.

- Poor and Hadjiliadis (2008) Poor, H. V. and O. Hadjiliadis (2008). Quickest detection. Cambridge University Press.

- Reed (1988) Reed, W. J. (1988). Optimal harvesting of a fishery subject to random catastrophic collapse. Mathematical Medicine and Biology: A Journal of the IMA 5(3), 215–235.

- Ren and Polasky (2014) Ren, B. and S. Polasky (2014). The optimal management of renewable resources under the risk of potential regime shift. Journal of Economic Dynamics and Control 40, 195–212.

- Rietkerk et al. (2004) Rietkerk, M., S. C. Dekker, P. C. De Ruiter, and J. van de Koppel (2004). Self-organized patchiness and catastrophic shifts in ecosystems. Science 305(5692), 1926–1929.

- Sakamoto (2014) Sakamoto, H. (2014). Dynamic resource management under the risk of regime shifts. Journal of Environmental Economics and Management 68(1), 1–19.

- Saphores (2003) Saphores, J.-D. (2003). Harvesting a renewable resource under uncertainty. Journal of Economic Dynamics and Control 28(3), 509–529.

- Scheffer et al. (2009) Scheffer, M., J. Bascompte, W. A. Brock, V. Brovkin, S. R. Carpenter, V. Dakos, H. Held, E. H. Van Nes, M. Rietkerk, and G. Sugihara (2009). Early-warning signals for critical transitions. Nature 461(7260), 53–59.

- Shiryaev (1963) Shiryaev, A. (1963). On optimum methods in quickest detection problems. Theory of Probability & Its Applications 8(1), 22–46.

- Shiryaev (1996) Shiryaev, A. (1996). Minimax optimality of the method of cumulative sums (cusum) in the case of continuous time. Russian Math. Surveys 51(4), 750–751.

- Solow (1974) Solow, R. M. (1974). The economics of resources or the resources of economics. In Classic papers in natural resource economics, pp. 257–276. Springer.

- Sousa et al. (2022) Sousa, C. O., L. V. Teixeira, and N. M. Fouto (2022). Midterm impacts of a water drought experience: evaluation of consumption changes in são paulo, brazil. Water Policy 24(1), 179–191.

- Springborn and Sanchirico (2013) Springborn, M. and J. N. Sanchirico (2013). A density projection approach for non-trivial information dynamics: Adaptive management of stochastic natural resources. Journal of Environmental Economics and Management 66(3), 609–624.

- Stern (2006) Stern, N. (2006). Review on the economics of climate change, hm treasury, uk. October. http://www. sternreview. org. uk.

- Tartakovsky et al. (2014) Tartakovsky, A., I. Nikiforov, and M. Basseville (2014). Sequential analysis: Hypothesis testing and changepoint detection. CRC Press.

Appendix A Appendix

A.1 Proof of existence of loss increasing in detection delay

Because of the delay , the firm chooses an extraction

| s.t. |

where is the non-empty set of Markovian admissible controls in feedback form such that for all and . We call this extraction policy as it assumes there has not been yet the regime shift and the optimization is undertaken under the pre-shift dynamic constraint. Define the bounded set as the supremum of the maximization problem (i.e. the total volume of maximized criterion units: profits, welfare or utils) achieved with policy over a finite period , which is a nonempty set of real numbers bounded above and below. However, the overall “real” supremum of the maximization problem, which corresponds to an observable at which the agent switches policy, is achieved by using the additive property of the supremum over bounded nonempty sets:

where is the supremum set of the problem (i.e. the maximized profits) up to under the constraint with drift generated by the optimal policy , is the supremum set of the problem between and generated by the policy under the constraint with drift and is the transition density of a diffusion . Using the dominated convergence and Fubini theorems, both suprema terms are bounded and positive for all . However, between and any admissible policy will not achieve the supremum, and . Since this is valid for any , it follows that for any . We can then write

| (25) |

where is a continuous function of and due to the feedback form of the Markovian policies and . The detection delay thus induces a loss for the agent, expressed in the same units as , which is increasing in the length of the delay itself. One can repeat the same proof as before for using as optimal and the proof is complete.

We further note that the instantaneous loss function is a function of both stock and time . Omitting arguments for clarity, its behavior in the interval is defined by the stochastic differential equation

| (26) |

under the filtration , obtained using standard Itô calculus and the optimality condition in the respective Hamilton-Jacobi-Bellman equations associated to the value function of the respective optimization problems, which read , where , the subscripts in the drift and diffusion coefficients indicate partial derivatives, and the operator is the infinitesimal generator of the controlled resource stock given by

All the extraction policy terms have the exponent in order to represent whether the policy is evaluated at the post-shift drift or not. Lastly, the terms are the solutions of the Hamilton-Jacobi-Bellman partial differential equation

for the post-shift and pre-shift problems, respectively. The terms , therefore, indicate the resource rents evaluated at the respective optimal extraction policies . The SDE starts at since (25) applies for all times. By optimality of , is a martingale while is a supermartingale. From (26) one can see that the diffusion term is proportional to , which is 0 when , and is always positive. It then follows that in almost surely.

Equation (26) has an intuitive interpretation: the deterministic part of the instantaneous loss evolves according to two differential terms. The first is the difference between the instantaneous expected change in extraction of the “theoretical” extraction policy with the suboptimal policy generated by the detection delay , expressed in units of resource rent . Intuitively, this represents why the extraction policy the agent applies in the interval is wrong: the chosen policy is optimal for a resource stock that grows deterministically as , and is applied to a resource stock that however grows at the post-shift rate .

A.2 Quickest detection of a regime shift

In the period before , the dynamics of the resource are determined by the SDE

| (27) |

under the triple . Define now the trasformation, sometimes called the Lamperti transform, given by

Under the standard conditions of existence of a solution for (27), maps one-to-one with the state space of for all and primitives of and thus this integral exists. One can then transform the original stock process in one with an unit diffusion. First, a straightforward application of Itô’s lemma to yields

Now notice that and that . We can then rewrite the previous expression as

Now, Girsanov theory tells us that the process

is a -martingale. Therefore, the process

is a -Brownian motion, where one obtains the new probability measure by . The process therefore admits the representation

and is therefore a Brownian motion under the measure . Using the same procedure as before to the post-shift resource process, the firm’s detection problem now becomes

This problem was solved by Moustakides (2004), shows that the stopping rule that solves the optimization problem (4) for a general -adapted process as regime shift, with a modified divergence-type/entropic criterion to account for a general process is given precisely by Eq.(6)

For the case of the drifted Brownian motion, notice that the Lamperti transform is simply given by and the regime shift is given by . Due to the prior information , the agent knows the magnitude of and the detection problem reverts exactly to the Brownian disorder problem studied by Shiryaev (1963 and 1996) and in the case of multiple drifts by Hadjiliadis and Moustakides (2006). The Brownian disorder is the detection of the change between a martingale and a sub/supermartingale, depending on the sign of . We apply these results directly, and refer to these papers for all details regarding the derivation of the formulas.

A.3 Proof of Proposition 1, 2 and 3

Let us prove Proposition 1 first, where the instantaneous drift is given by and the firm optimizes in where . At time the firm believes that the resource is driven by a diffusion process with the natural growth rate . At a random and unobservable time , there is an initial exogenous change, , in the resource dynamics.

Within this time interval , the value of the firm is given by

| (28) | |||||

| s.t. | |||||

where the control set is given by What we want to achieve is to show that the value function for (28) across different periods with changing drifts is a weak solution of the optimization problem (2.2). In all that follows we will use as a reference Fleming and Soner (2006). We first write the Hamilton-Jacobi-Bellman equation for this problem in terms of its infinitesimal generator. Define the set . Then is a classical solution of the optimization problem (28) if it satisfies the equation

| (29) |

where is the generator of the HJB equation. Now, define a continuous function (the Hamiltonian) such that

and consider the equation

| (30) |

Following the fundamental work by Crandall and Lions (1981), a function is a viscosity subsolution of (30) if for all

for every point which is a local maximum of . Similarly, is a viscosity supersolution of (30) if for all

for every point which is a local minimum of . The function is a viscosity solution of the equation (30) if it is both a viscosity subsolution and a viscosity supersolution. This implies that the function is a weak solution of the optimization problem (28). Let us now show that is a viscosity solution of our problem (28).

Let , let be maximized at the point and let us fix an optimal control (extraction rate) . Let be the controlled stochastic process that drives the resource stock. For every time for which , we have, using Itô’s lemma and Bellman’s principle of optimality,

This implies

for all : we can then write

This proves that is a viscosity subsolution of the problem (28). Proceeding similarly proves that is a viscosity supersolution of the problem: if attains a minimum at then for any and we can find a control such that

which implies

Proceeding equivalently as before, one shows that is a viscosity supersolution of (28). We can conclude that is a viscosity solution of (28). Note that for every time for which , since for optimality we have and is continuous and twice differentiable in , it can be easily shown that the inequalities of the definition of sub- and supersolution are satisfied with equality, which means that is also a classical solution of (29) for each . We now need to deal with the value function at each change point , and focus on the extended time interval . Given the “feasible” set , we cannot impose that the value function nor its gradient to be differentiable at at the boundary of . Following Fleming and Soner (2006), we need to impose a boundary inequality, which does not require nor the boundary to be differentiable at . This implies that the value function must be a viscosity subsolution of (28) in the time interval for all . Following the previous definitions, we must have

| (31) | |||||

for all continuous functions for which is locally maximized around . Since has to be maximized in a closed interval around , we have