We describe a procedure to perform approximate inference on the

achieved signal-noise ratio of the Markowitz portfolio under Gaussian i.i.d. returns.

The procedure relies on a statistic similar to the Sharpe Ratio Information

Criterion. [8]

Testing indicates the procedure is somewhat conservative, but

otherwise works well for reasonable values of sample and asset universe sizes.

We adapt the procedure to deal with generalizations of the portfolio optimization problem.

1 Introduction

For a universe of assets,

we consider the portfolio optimization problem

(1)

Here is the expected return and is the covariance of returns.

This problem is solved by the Markowitz portfolio, defined as

(2)

and any positive multiple thereof.

In practice the parameters and are unknown and must be estimated from the data.

The estimation of parameters is known to deterioriate the quality of the

portfolio. [7]

The signal-noise ratio of the Markowitz portfolio, its mean divided by its volatility, is subject to a

fundamental bound. [10, 2]

While inference on the population parameters follows from classical statistics

via the connection to Hotelling’s , little is known about performing

inference on the signal-noise ratio achieved by the Markowitz portfolio.

Paulsen and Söhl described the Sharpe Ratio Information Criterion (SRIC),

which is an approximately unbiased estimator for this quantity. [8]

Some asymptotic confidence intervals have also been described, but these

require unreasonably large sample sizes. [9]

Here we fill this gap, describing confidence intervals very similar

to the SRIC and using the same approximation.

Practical construction of these bounds requires one to estimate the population

effect size.

In practice this causes the confidence intervals to be slightly conservative.

2 The Procedure

Assume you observe returns on assets,

which are independently drawn from a Gaussian distribution

.

The population Markowitz portfolio is .

The signal-noise ratio of this portfolio is .

Given observations of returns,

one typically estimates the population parameters via

(3)

(4)

The (sample) Markowitz portfolio is .

The achieved signal-noise ratio of is defined as

(5)

It is an unobservable random quantity that we wish to perform inference on.

The Sharpe ratio of is defined as

(6)

We note that is the familiar Hotelling’s statistic,

which is usually prescribed to perform inference on , but

can be used to perform inference on .

[1, 11]

The Sharpe Ratio Information Criterion is defined as

[8]

(7)

Under the simplifying approximation

(8)

the SRIC is unbiased for the achieved signal-noise ratio:

(9)

Note this only holds for , but it is simple to express

when .

Inspired by the SRIC, we seek a constant such that

Under the approximation we also have .

We note that for Gaussian returns, we can write

where

Thus

Now because

If we want this condition to hold with probability we should set

(12)

where is the quantile of the non-central chi-square distribution

with degrees of freedom and non-centrality parameter .

Checking coverage

Before proceeding, we check whether use of Approximation 8

leads to a degradation in coverage of a confidence interval implied by Inequality 10.

We draw days of returns from the -variate normal distribution.

For a fixed value of , we perform

simulations of computing and , computing a

one-sided confidence bound and measuring the empirical rate of type I errors.

We then let vary from 50 to days;

we let vary from 2 to 16;

we let vary from to , where we assume

252 days per year.

We compute the lower confidence limit on using knowledge of the

actual to construct .

For practical inference this would

have to be estimated, but here we are only testing conditions for which the

approximation is close enough for purposes of inference.

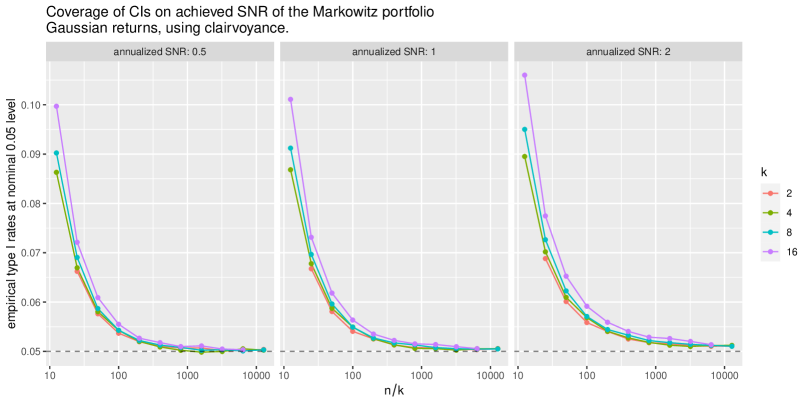

Figure 1: The empirical type I rate, over 1,000,000 simulations, of a one-sided confidence bound for are shown for a nominal type I rate of . The daily returns are drawn from multivariate normal distribution with varying , , and . Type I rates are plotted versus to indicate the requisite aspect ratio to achieve near nominal coverage.

In Figure 1 we plot the empirical type I rate at the nominal

0.05 level of the confidence bound.

The main takeaway from this experiment is that the bound gives near-nominal

coverage when or so.

2.1 Practical Inference

One can construct one- or two-sided confidence intervals from Inequality 10 when is known.

However, it is unknown in practice, and the constant is sufficiently sensitive to it.

To practically perform inference, there are two obvious routes: one is to

jointly perform inference on on ;

the other is to estimate and plug it in when constructing .

For the joint estimation procedure, for some ,

construct a upper bound on .

That confidence bound can be described implicitly via the connection

to the non-central distribution:

to find the one-sided confidence intervals with

coverage , find

(13)

where is the CDF of the non-central

-distribution with

non-centrality parameter and and degrees of freedom.

This method requires computational inversion of the CDF function.

Then compute

The bound then should

have type I rate at most .

However, since this is a joint confidence bound the bound on will be

somewhat conservative.

Another approach, which does not have guaranteed coverage, is to

estimate from the data, and plug in that value in the computation of

.

We can perform this estimation using standard techniques,

again via the connection of Hotelling’s to the distribution.

Kubokawa, Robert and Saleh described improved methods for estimating

the non-centrality parameter given an observation of a non-central

statistic. [6].

They described the following estimators for the non-centrality parameter,

which is in our case:

(14)

They note that is the Uniform Minimum Variance Unbiased Estimator (UMVUE) of .

However, it can be negative.

The estimators are non-negative, and dominate in having

lower expected squared error.

Thus the suggested procedure is to compute

then use the bound .

In practice this bound seems to give slightly less conservative coverage than

the joint bound described above.

It is not clear how to find a coverage guarantee for this bound.

The quantities and are not independent,

and their asymptotic correlation is , which is only slowly shrinking. [9]

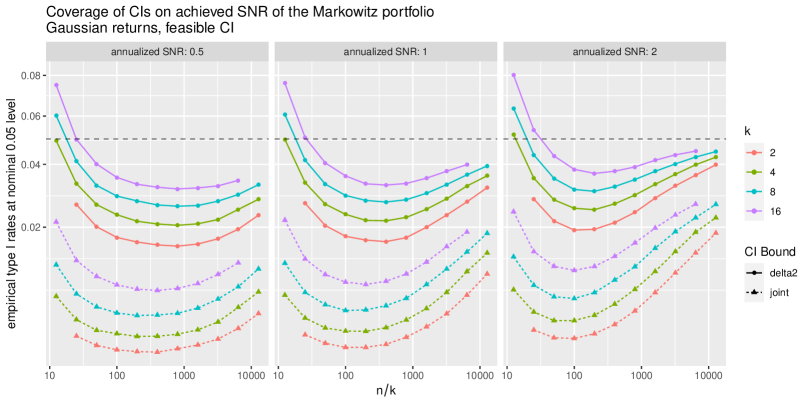

Feasible CI Coverage

We reconsider the experiments above but compute feasible confidence bounds.

We use both the simultaneous CI approach with ;

and plug in to construct the bound.

In Figure 2, we plot the empirical type I rate for both of these bounds

versus , with facets for .

We see that the plug-in estimator has coverage closer to the nominal rate.

Both bounds have issues when is not sufficiently large, a problem stemming

from the poor quality of the approximation , and which was seen above.

However, here we see closer to nominal coverage for larger for both methods.

It is not clear how the coverage will behave for larger , though

that seems like an unlikely problem in practice.

Figure 2: The empirical type I rate, over 1,000,000 simulations, of two feasible one-sided confidence bounds for are shown for a nominal type I rate of . The daily returns are drawn from multivariate normal distribution with varying , , and . The axis is drawn in square root scale to show detail.

2.2 Hedged Portfolios

Now we generalize the portfolio problem of Equation 1 to add a hedging constraint.

So consider the constrained portfolio optimization problem on assets,

(15)

where is an matrix of rank , and,

as previously, , are the mean vector and covariance matrix,

is the risk-free rate, and is a risk ‘budget’.

We can interpret

the constraint as stating that the covariance of the returns of

a feasible portfolio with the returns of a portfolio whose weights are in

a given row of shall equal zero. In the garden variety application of this problem, consists of

rows of the identity matrix; in this case, feasible portfolios are hedged with respect

to the assets selected by (although they may hold some position in the hedged assets).

We use “hedged” to mean a portfolio with zero covariance

against some other portfolio(s).

The

solution to this problem, via the Lagrange multiplier technique,

is

When , the unique solution is found by setting so that the risk budget is an equality.

Note that, up to scaling, is the unconstrained optimal

portfolio, and thus the imposition of the constraint only changes

the unconstrained portfolio in assets corresponding to columns of containing non-zero elements. In the garden variety application where

is a single row of the identity matrix, the imposition of the

constraint only changes the holdings in the asset to be hedged (modulo

changes in the leading constant to satisfy the risk budget).

The squared signal-noise ratio of the optimal portfolio we write as

(16)

The sample optimal portfolio is given by

The squared Sharpe ratio of this portfolio is

(17)

The achieved signal-noise ratio of this portfolio is

(18)

Define:

Giri showed that conditional on observing ,

(19)

where is the non-central -distribution

with , degrees of freedom and non-centrality parameter

. [giri1964likelihood, 11]

Now we apply Approximation 8, and complete the square as we did in the unhedged case, to find that

where

Now note that the matrix

is idempotent with rank .

Thus a quadratic form in follows a non-central distribution111n.b. the standard definition of

non-centrality parameter in the time Graybill and Marsaglia wrote their paper is different from the one we use today by a factor of

. with degrees of freedom equal to the rank of . [10.2307/2237227, Theorem 2]

Thus

Then, as in the unhedged case, we have

(20)

if we let

To perform feasible inference one will need to estimate .

Again this will be via the connection to a non-central -distribution, Equation 19.

One can either find an upper quantile directly, or use a KRS-type estimator, which

for the hedged case are

(21)

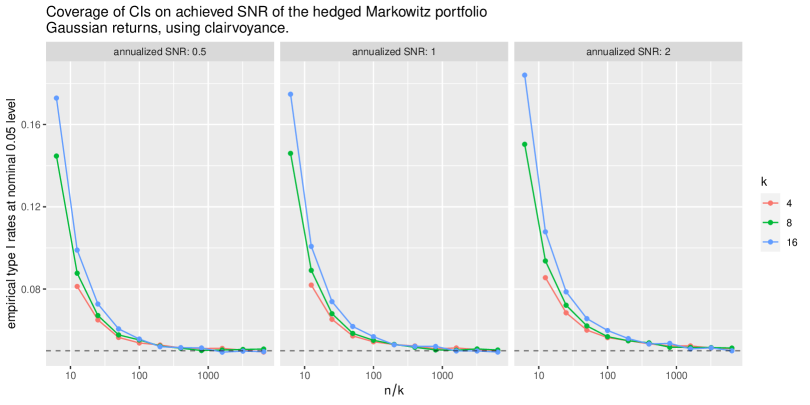

Checking coverage

As in the unhedged case, we first perform simulations where the population parameter is known,

to assess the effects of Approximation 8.

In our simulations, we set , and let be the first rows of the identity matrix.

We set and .

We perform simulations for different values of , and ,

computing for the hedged portfolio, as well as and .

We compute the lower 0.05 bound using knowledge of and compute the empirical type I rate

over the simulations, which we plot versus in Figure 3.

Again we see that the nominal type I rate is nearly achieved when or so.

Figure 3: The empirical type I rate, over 100,000 simulations, of a one-sided confidence bound for are shown for the hedged portfolio problem. We set and take . The SNR in the facet titles refers to .

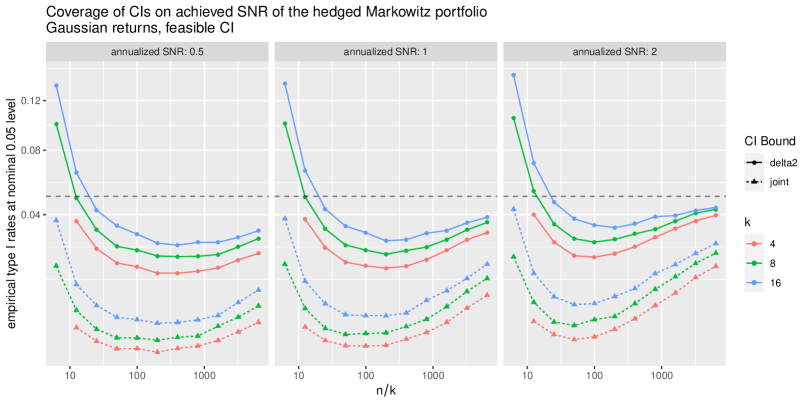

As above we analyze the data from the hedged experiments, but compute feasible confidence bounds.

We use both the simultaneous CI approach with ;

and plug in to construct the bound.

In Figure 4, we plot the empirical type I rate for both of these bounds

versus , with facets for and .

Once again, the plug-in estimator has coverage closer to the nominal rate,

and both bounds are anti-conservative when is not sufficiently large.

Figure 4: The empirical type I rate, over 100,000 simulations, of two feasible one-sided confidence bounds for are shown for a nominal type I rate of . The daily returns are drawn from multivariate normal distribution with varying , , and . The axis is drawn in square root scale to show detail.

3 Examples

Fama French 4 Factor Returns

We consider a portfolio constructed on the ‘Market’, size (SMB), value (HML)

and momentum (HMD) portfolios described by Fama and French, inter alia,

with data compiled and published by Kenneth French. [4, 3, 5]

The set consists of of data, from

1927 through 2018.917.

We observe .

From this we compute .

Plugging in for we compute a two-sided confidence bound on as

.

By comparison, via the connection to the distribution,

we compute confidence intervals on as

.

Next we consider the imposition of a constraint that the portfolio should be “hedged against the Market”.

This corresponds to and is the row of the identity matrix corresponding to the Market factor.

We compute

With , we

compute the three KRS estimators of , which all take the same value,

From this we compute a one-sided confidence bound on

to be

.

4 Discussion

Testing indicates the confidence bound exhibits closer to nominal

coverage than the known asymptotic bounds for reasonable and .

Further work should naturally focus on mitigating the effects of the

approximation , and finding a coverage guarantee

of the plug-in estimator.

We also anticipate that this confidence bound procedure can be adapted

to deal with conditional expectation models.

References

Anderson [2003]

T. W. Anderson.

An Introduction to Multivariate Statistical Analysis.

Wiley Series in Probability and Statistics. Wiley, 2003.

ISBN 9780471360919.

URL http://books.google.com/books?id=Cmm9QgAACAAJ.

Carhart [1997]

Mark M Carhart.

On persistence in mutual fund performance.

Journal of Finance, 52(1):57, 1997.

URL http://www.jstor.org/stable/2329556.

Fama and French [1992]

Eugene F. Fama and Kenneth R. French.

The cross-section of expected stock returns.

Journal of Finance, 47(2):427, 1992.

URL http://www.jstor.org/stable/2329112.

Kubokawa et al. [1993]

Tatsuya Kubokawa, C. P. Robert, and A. K. Md. E. Saleh.

Estimation of noncentrality parameters.

Canadian Journal of Statistics, 21(1):45–57, Mar 1993.

URL http://www.jstor.org/stable/3315657.

Paulsen and Söhl [2020]

Dirk Paulsen and Jakob Söhl.

Noise fit, estimation error and a Sharpe information criterion.

Quantitative Finance, 0(0):1–17, 2020.

doi: 10.1080/14697688.2020.1718746.

URL https://doi.org/10.1080/14697688.2020.1718746.

Pav [2013]

Steven E. Pav.

Asymptotic distribution of the Markowitz portfolio.

Privately Published, 2013.

URL http://arxiv.org/abs/1312.0557.