Reliable Frequency Regulation through Vehicle-to-Grid:

Encoding Legislation with Robust Constraints

Dirk Lauinger1, François Vuille2, Daniel Kuhn3

1Massachusetts Institute of Technology, lauinger@mit.edu

2Etat de Vaud, francois.vuille@vaud.ch

3Ecole polytechnique fédérale de Lausanne, daniel.kuhn@epfl.ch

Problem definition: Vehicle-to-grid increases the low utilization rate of privately owned electric vehicles by making their batteries available to electricity grids. We formulate a robust optimization problem that maximizes a vehicle owner’s expected profit from selling primary frequency regulation to the grid and guarantees that market commitments are met at all times for all frequency deviation trajectories in a functional uncertainty set that encodes applicable legislation. Faithfully modeling the energy conversion losses during battery charging and discharging renders this optimization problem non-convex. Methodology/results: By exploiting a total unimodularity property of the uncertainty set and an exact linear decision rule reformulation, we prove that this non-convex robust optimization problem with functional uncertainties is equivalent to a tractable linear program. Through extensive numerical experiments using real-world data, we quantify the economic value of vehicle-to-grid and elucidate the financial incentives of vehicle owners, aggregators, equipment manufacturers, and regulators. Managerial implications: We find that the prevailing penalties for non-delivery of promised regulation power are too low to incentivize vehicle owners to honor the delivery guarantees given to grid operators.

1 Introduction

Replacing internal combustion engine vehicles with electric vehicles reduces urban air pollution and mitigates climate change if electricity is generated from renewable sources (Sperling, 1994). In general, privately owned vehicles are a vastly underutilized resource. Vehicle usage data collected by the US Federal Highway Administration (2017) shows that on an average day over % of all privately owned vehicles are parked at any one time—even during peak rush hour. Since electricity grids require storage capacity to integrate increasing amounts of intermittent wind and solar power, electric vehicle owners could capitalize on their batteries by offering storage to the electricity grid when their vehicles are parked. Kempton and Letendre (1997) term this idea vehicle-to-grid.

Réseau de transport d’électricité (RTE), Europe’s largest transmission system operator, expects to need an additional flexible generation and electricity storage capacity of GW to GW by 2035. This corresponds to % to % of the total French electricity generation capacity in 2017 (RTE RTE; RTE). If electric vehicles were to provide some of this flexibility, then the vehicles and the electricity grid could share the costs of electric vehicle batteries. Kempton and Tomić (2005) and Noel et al. (2019) have identified primary frequency regulation, also known as frequency containment reserves, as one of the most profitable flexibility services for vehicle-to-grid. Electric vehicles that provide this service must maintain a continuous power flow to the vehicle battery that is proportional to the deviation of the instantaneous grid frequency from its nominal value (e.g., 50Hz in Europe). As primary frequency regulation is the first flexibility service used to stabilize the electricity network after disturbances (Rebours et al., 2007), its provision must be highly reliable. However, RTE (RTE) questions the reliability of vehicle-to-grid. The European Commission (2017) addressed this concern by defining a minimum level of reliability that electric vehicles and other providers of frequency regulation must guarantee. Specifically, it demands that providers must be able to deliver regulation power for all frequency deviation trajectories with certain characteristics.

Adopting the perspective of a vehicle owner, we formulate an optimization model to determine the bidding strategy on the regulation market that maximizes the expected profit from selling primary frequency regulation to the transmission system operator under the reliability constraints imposed by the European Commission. These constraints must hold robustly for all frequency deviation trajectories in an uncertainty set consistent with applicable legislation. As these trajectories constitute continuous-time functions, we are confronted with a robust optimization problem with functional uncertainties. Moreover, the impossibility of simultaneously charging and discharging the battery—which amounts to dissipating energy through conversion losses and could be profitable when the battery is full and there is a reward for down-regulation (see, e.g., (Taylor, 2015, p. 84))—renders the optimization problem non-convex. The main theoretical contribution of this paper is to show that the resulting non-convex robust optimization problem with functional uncertainties is equivalent to a tractable linear program. Specifically, this paper makes the following methodological contributions to robust optimization (see Ben-Tal et al. (2009) for a textbook introduction).

-

•

We introduce new uncertainty sets in function spaces that capture those frequency deviation trajectories for which regulation providers must be able to deliver all promised regulation power. These uncertainty sets are reminiscent of the budget uncertainty sets by Bertsimas and Sim (2004) in finite-dimensional spaces, and their construction is inspired by EU legislation.

-

•

By leveraging a total unimodularity property of the proposed uncertainty sets and an exact linear decision rule reformulation, we prove that the worst-case frequency deviation scenarios in all (convex or non-convex) robust constraints of the vehicle owner’s optimization problem can be found by solving continuous linear programs, which can be viewed as variants of the so-called separated continuous linear programs introduced by Anderson et al. (1983).

-

•

By demonstrating that all these continuous linear programs are solved by piecewise constant frequency deviation trajectories, we show that the robust optimization problem with functional uncertainties is equivalent to a robust optimization problem in discrete time. In doing so, we use more direct proof techniques than Pullan (1995), who derived sufficient conditions under which the solutions of separated continuous linear programs are piecewise constant.

-

•

The robust optimization problem obtained by time discretization is still non-convex. Using the structural properties of its (discretized) uncertainty sets and of its objective and constraint functions, however, we can prove that it is equivalent to a linear robust optimization problem that can be reformulated as a tractable linear program via standard techniques.

To our best knowledge, robust optimization models with uncertainty sets embedded in function spaces have so far only been considered in the context of robust control, where the primary goal is to develop algorithms for evaluating conservative approximations (Houska, 2011), and in the context of robust continuous linear programming, where the primary goal is to reduce robust to non-robust continuous linear programs, which can be addressed with existing algorithms (Ghate, 2020). In contrast, we study here a non-convex robust optimization problem with functional uncertainties that admits a lossless time discretization and can be reformulated exactly as a tractable linear program. Remarkably, the state-of-the-art methods for solving the deterministic counterparts of this robust optimization problem are based on methods from mixed-integer linear programming. To our best knowledge, we thus describe the first class of practically relevant mixed-integer linear programs that simplify to standard linear programs through robustification.

As the emerging linear programs are amenable to efficient numerical solution, we are able to perform extensive numerical experiments based on real-world data pertaining to the French electricity system. We define the value of vehicle-to-grid as the profit from selling primary frequency regulation relative to a baseline scenario in which the vehicle owner does not offer grid services. As our optimization model faithfully captures effective legislation, it enables us to quantify the true value of vehicle-to-grid. This capability is relevant for understanding the economic incentives of different stakeholders such as vehicle owners, aggregators, equipment manufacturers, and regulators. The model developed in this paper enables us to assess how the value of vehicle-to-grid depends on the penalties for non-delivery of promised regulation power, the size of the uncertainty set, and the vehicle’s battery and charger. We thus contribute to the growing operations management literature on vehicle-to-grid (Broneske and Wozabal, 2017; Mak, 2020; Zhang et al., 2021; Qi et al., 2022). The main insights drawn from our computational experiments can be summarized as follows.

-

•

Based on 2016–2019 data, we show that the value of vehicle-to-grid attainable with a bidding strategy that is guaranteed to satisfy all reliability requirements is around € per year and vehicle. Earlier studies based on anticipative bidding strategies have estimated this value to be four times higher (Codani et al., 2015; Borne, 2019).

- •

-

•

We show that the value of vehicle-to-grid saturates at daily plug times above 15 hours. Thus, maximal profits from frequency regulation can be reaped even if the vehicle is disconnected from the grid up to 9 hours per day. This means that vehicle owners still enjoy considerable flexibility as to when to drive, which could help to promote the adoption of vehicle-to-grid.

-

•

We formulate an optimization problem for a vehicle aggregator that allows for asymmetric bids of individual vehicles and show that this problem also admits an exact linear programming reformulation. In practical terms, we find that allowing for asymmetric bids can increase the profits from frequency regulation by up to 40% for a fleet of electric vehicles with bidirectional and unidirectional chargers.

Beyond vehicle-to-grid, this paper contributes to the literature on the optimal usage of energy storage assets. The value of a storage asset is usually identified with the profit that can be generated through arbitrage by trading the stored commodity on spot or forward markets. Unlike traditional centralized storage assets, decentralized storage assets such as electric vehicles are usually connected to distribution rather than transmission grids. This means that they face retail and not wholesale electricity prices. While wholesale prices are determined by market mechanisms and thus stochastic, retail prices are often regulated and thus deterministic. Another major difference is that it may take several days to fully charge or discharge centralized storage assets such as hydropower plants, whereas the batteries of electric vehicles can be fully charged and discharged in just a few hours. A daily planning horizon is therefore sufficient for optimizing their usage. In addition, typical vehicle owners can anticipate their driving needs at most one day in advance. One can thus solve the storage management problem in a receding horizon fashion.

The state-of-charge of a vehicle battery depends non-linearly on the power in- and outflows, which leads to non-convex optimization models. If the battery is merely used for arbitrage and market prices are non-negative, then these optimization models admit exact convex relaxations. Conversely, if the battery is used for frequency regulation or if market prices can fall below zero, then a non-convex constraint is needed to prevent the models from dissipating energy by simultaneously charging and discharging the battery (Zhou et al., 2016). If energy conversion losses are negligible and the battery state-of-charge is thus linear in the power flows, then one can model the provision of frequency regulation through adjustable uncertainty sets. Such an approach has been proposed by Zhang et al. (2017) for frequency regulation with building appliances. A stochastic dynamic programming scheme for optimizing the charging and discharging policy of an electric vehicle with linear battery dynamics is proposed by Donadee and Ilić (2014). If energy conversion losses are significant, however, one may still approximate the state-of-charge by a linear decision rule of the uncertain frequency deviations (Warrington et al., 2013). Sortomme and El-Sharkawi (2012) study a similar model under the assumption of perfect foresight.

In practice, several hundreds or thousands of electric vehicles must be aggregated to be able to bid enough reserve power to qualify for participation in the frequency regulation market. Guille and Gross (2009), Han et al. (2010), Wenzel et al. (2018) and Zhang et al. (2021) develop frameworks for controlling the batteries of aggregated vehicles, while the design of contracts between aggregators and vehicle owners is examined by Han et al. (2011) and Broneske and Wozabal (2017). The policy implications for the market entry of electric vehicle aggregators are investigated by Borne et al. (2018). Yet the study of vehicle-to-grid schemes for individual vehicles remains relevant because they constitute important building blocks for aggregation schemes and because they still pose many challenges—especially when it comes to faithfully modeling all major sources of uncertainty.

The model developed in this paper is most closely related to the discrete-time robust optimization models by Yao et al. (2017) and Namor et al. (2019), which capture the uncertainty of the frequency deviations through simplicial uncertainty sets that cover all empirical frequency deviation scenarios. However, these uncertainty sets may fail to include unseen future frequency deviation scenarios and are inconsistent with applicable EU legislation. While Yao et al. (2017) disregard energy conversion losses, Namor et al. (2019) account for them heuristically and test the resulting charging and discharging policies experimentally on a real battery. Heuristics are also common in pilot projects that demonstrate the use of vehicle-to-grid for frequency regulation (Vandael et al., 2013, 2020).

The model proposed in this paper relies on three simplifying assumptions that we justify below.

Our first key assumption is that the provision of frequency regulation has no negative impact on battery lifetime—even though the fear of battery degradation has been identified as a major obstacle to the widespread adoption of vehicle-to-grid (Lauinger et al., 2017). To justify this assumption, we point out that the impact of vehicle-to-grid on battery longevity is not yet well understood. In fact, Dubarry et al. (2017) claim that such degradation is severe, while Uddin et al. (2017) claim that vehicle-to-grid may actually extend battery lifetime. In (Uddin et al., 2018), the authors of these two studies reconcile their contradictory findings by concluding that the impact of vehicle-to-grid depends on the operating conditions of the battery, such as its temperature and variations in its state-of-charge. We further justify our no-degradation assumption by restricting the battery state-of-charge to lie within 20% and 80% of the nominal battery capacity. Thompson (2018) suggests these restrictions as a rule of thumb for extending the lifetime of common lithium-ion batteries, and Sweda et al. (2017) adopt similar rules to optimize recharging policies of electric vehicles. Models that account for battery degradation are studied by He et al. (2016) and Carpentier et al. (2019).

Our second key assumption is that vehicle owners can specify time and energy windows for their driving needs one day in advance. This assumption makes sense for commuters who adhere to predictable daily routines, for example.

The third key assumption is that the vehicle owners are price takers who influence neither the market prices nor the grid frequency. This assumption is reasonable because one vehicle may cover at most several kilowatts of the 700 megawatts required for frequency regulation in France. A model of a regulation provider influencing the grid frequency is described by Mercier et al. (2009).

The paper proceeds as follows. Section 2 formulates the vehicle owner’s decision problem as a non-convex robust program with functional uncertainties. In Sections 3 and 4 we reformulate this problem as a non-convex robust program with vectorial uncertainties and even as a tractable linear program, respectively. In Appendix B, we extend these results to an aggregator who manages a fleet of electric vehicles. Numerical experiments are discussed in Section 5, and policy insights are distilled in Section 6. All proofs are relegated to the online supplement.

Notation.

All random variables are designated by tilde signs. Their realizations are denoted by the same symbols without tildes. Vectors and matrices are denoted by lowercase and uppercase boldface letters, respectively. For any , we define and such that . The intersection of a set with is denoted by . For any closed intervals , we define as the space of all Riemann integrable functions , and we denote the intersection of a set with as .

2 Problem Description

Consider an electric vehicle whose state at any time is characterized by the amount of energy stored in its battery and the instantaneous power consumption for driving . We require that is never smaller than and never larger than . To mitigate battery degradation, we set these limits to 20% and 80% of the nominal battery capacity, respectively. The battery interacts with the power grid through a bidirectional charger with charging efficiency and discharging efficiency , where an efficiency of corresponds to a lossless energy conversion between the grid and the battery. The charger is further characterized by its maximum power consumption from the grid and its maximum power provision to the grid . The power the battery can charge or discharge is therefore limited by and , respectively. Note that and depend on the charger to which the vehicle is connected at time . When the vehicle is not connected to any charger, e.g., when it is driving, then both and must vanish. A stationary battery can be modeled by setting and keeping and constant for all .

In order to charge the battery at time , the vehicle owner may buy power from the local utility at a known time-varying price as is the case under dynamic pricing schemes or day/night tariffs. In addition, she may also use the vehicle battery to earn extra revenue by providing primary frequency regulation, which can be viewed as an insurance bought by the transmission system operator (TSO) to balance unforeseen mismatches of electricity demand and supply in real time (Glover et al., 2010). If there is more supply than demand, the frequency of the power grid rises. Conversely, if there is more demand than supply, the frequency falls. A battery owner offering regulation power at time is obliged to change her nominal power consumption from the grid by , where quantifies the normalized deviation of the instantaneous grid frequency from its nominal value (Gestionnaire du Réseau de Transport d’Electricité, 2009). Formally, we have

where is a threshold beyond which all promised regulation power must be delivered.

The TSO contracts frequency regulation as an insurance over a prescribed planning horizon of length , e.g., one day. The planning horizon is subdivided into trading intervals for all , where . In the French electricity market, for example, the length of a trading interval is minutes. The TSO requests the vehicle owner to announce the market decisions and before the beginning of the planning horizon, e.g., one day ahead at noon (RTE RTE). These decisions need to be piecewise constant over the trading intervals. The TSO compensates the vehicle owner for the frequency regulation made available at the availability price and charges her for the increase in her power consumption at the delivery price as laid out by French market rules. Note that this charge becomes negative (i.e., it becomes a remuneration) if is negative. In summary, the vehicle owner’s total cost over the planning horizon amounts to

The impact of providing frequency regulation on the battery state-of-charge depends on how the vehicle owner adjusts the power consumed from and the power injected into the grid to achieve the desired net power consumption . The most energy-efficient way is to avoid unnecessary energy conversion losses resulting from simultaneously charging and discharging. Sometimes, however, such losses can be attractive, for example if the battery is almost full and receives a request for down-regulation (). Zhou et al. (2016) show that energy losses can also be attractive when electricity prices are negative. Since common chargers are not able to simultaneously charge and discharge, we forbid this option and set the charging rate to

| (1a) | |||

| and the discharging rate to | |||

| (1b) | |||

Remark 1.

When operating a vehicle fleet, some vehicles could charge while others discharge, which suggests that the regulation profits achievable with vehicles may exceed the regulation profit of a single vehicle multiplied by . In this paper, we focus on the case .

The power exchanged with the grid and the power needed for driving determine the battery state-of-charge at any time via the integral equation

| (2) |

where represents the state-of-charge at time .

At the time when the vehicle owner needs to choose and report the market commitments and , she has no knowledge of the uncertain future frequency deviations and the delivery prices at time . In addition, she has no means to predict the battery state-of-charge at the beginning of the planning horizon, which depends on market commitments chosen on the previous day and on the uncertain frequency deviations to be revealed until time . By contrast, the availability prices for can be assumed to be known at the planning time. In practice, these prices are determined by an auction. As the vehicle owner bids an offer curve expressing as a function of for any , it is as if the availability prices were known upfront (the bidding process is described at https://www.entsoe.eu/network_codes/eb/fcr/). Next, we describe the information that is available about the uncertain problem parameters , , and .

We first discuss the uncertainty in the frequency deviations, which limits the amount of reserve power that can be sold on the market. Indeed, the vehicle owner must ensure that the battery state-of-charge will never drop below or exceed when the TSO requests down-regulation () or up-regulation (), respectively, for a prescribed set of conceivable frequency deviation scenarios. Otherwise, the vehicle owner may not be able to honor her market commitments, in which case the TSO may charge a penalty or even ban her from the market.

The TSO defines under what conditions regulation providers must be able to deliver the promised regulation power, keeping in mind that extreme frequency deviations are uncommon. Indeed, between 2015 and 2018 the frequency deviation has never attained its theoretical maximum of or its theoretical minimum of in the French market. In the following, we thus assume that the vehicle owner needs to guarantee the delivery of regulation power only for frequency deviation scenarios within the uncertainty set

parametrized by the duration of a regulation cycle and the duration of an activation period. Throughout this paper, we assume that . By focusing on frequency deviation scenarios in , one stipulates that consecutive extreme frequency deviations can occur at most over one activation period within each regulation cycle. The activation ratio can thus be interpreted as the percentage of time during which the vehicle owner must be able to deliver all committed reserve power.

Remark 2.

Note that the uncertainty set grows with and shrinks with .

Besides displaying favorable computational properties, the uncertainty set has conceptual appeal because it formalizes the delivery guarantee rules prescribed by the European Commission (2017, art. 156(10, 13b)). These rules stipulate that the “minimum activation period to be ensured by [frequency regulation] providers [is not to be] greater than or smaller than minutes.” This guideline prompts us to set minutes. The EU further demands that regulation providers “shall ensure the recovery of [their] energy reservoirs as soon as possible, within hours after the end of the alert state.” This means that for hours after the end of an alert state in which the regulation provider delivered frequency regulation, she will not have to deliver any additional frequency regulation, even if new alert states occur during this time. The law defines an “alert state” as a state of normal operating conditions in which prespecified contingencies may lead to abnormal operating conditions but does not specify its duration. We conservatively consider a duration equal to the activation period, which maximizes the size of the uncertainty set. In fact, to be consistent, the worst-case alert state should be at least as long as the minimum activation period. The regulation cycle is then equal in duration to the worst-case alert state plus the hour break from delivering frequency regulation. As the uncertainty set shrinks with , considering the alert state to last as long as the activation period does indeed maximize the uncertainty set. Thus, we set hours.

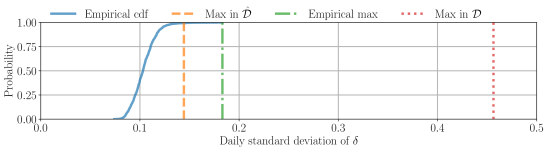

In the following, we compare the empirical distribution of the daily variance of between the years 2017 and 2019 with the maximum variance that can be achieved by any hypothetical frequency deviation scenario for a planning horizon of one day. By slight abuse of notation, we define the variance of a frequency deviation scenario with respect to zero as . This is justified because the TSO protects the system against unforeseen demand and supply fluctuations, which means that the frequency deviations should be unbiased and thus vanish on average. Indeed, the empirical frequency deviations have an average of . Figure 1 shows that if day, minutes, and hours, then the maximum standard deviation of any exceeds the maximum empirical standard deviation by a factor of . Thus, contains extreme frequency deviation scenarios with unrealistically high variance. The optimization model developed below not only involves the conservative uncertainty set compatible with the guidelines of the European Commission but also a smaller uncertainty set

parametrized by and . This uncertainty set contains only frequency deviation scenarios that are likely to materialize under normal operating conditions. Note that is obtained from by inflating to and shrinking to . By Remark 2, we may thus conclude that is indeed a subset of . While the pessimistic uncertainty set is used to enforce the stringent delivery guarantees imposed by the European Commission, the more optimistic uncertainty set is used to model a softer reachability guarantee for the terminal state-of-charge. In the numerical experiments we will set day and minutes. One can show that the variance of all frequency deviation scenarios in is therefore bounded above by . Empirically, this threshold exceeds the variance of the frequency deviation on of all days in the years from 2017 to 2018.

Next, we discuss the uncertainty in the initial battery state-of-charge . Recall that is uncertain at the time when and are chosen because it depends on how much regulation energy must be provided until the beginning of the planning horizon. This quantity depends itself on uncertain frequency deviations that have not yet been revealed. We assume that the vehicle owner constructs two confidence intervals and for , either taking into account all frequency deviations under which she must imperatively be able to deliver regulation power or only those frequency deviations that are likely to occur under normal operating conditions.

The only assumption we make about the uncertainty in the delivery price is that the vehicle owner can reliably estimate the expected regulation price .

We are now ready to formalize the vehicle owner’s decision problem for selecting the market decisions and . The primary objective is to minimize the expected cost

| (3) |

while ensuring that and are robustly feasible across all frequency deviation scenarios and initial battery states . Mathematically, the charging rate , the discharging rate , and the battery state-of-charge must therefore satisfy the robust constraints

As the vehicle owner continues to use the vehicle for driving and for offering grid services after the end of the planning horizon, the battery should end up in a state that is “conducive to satisfactory future operations” (Yeh, 1985, p. 1798). Consequently, the vehicle owner aims to steer to a desirable state-of-charge . We assume that the cost-to-go of any is quantified by a convex and piecewise affine value function determined by for all . As and are uncertain, the terminal state-of-charge is also uncertain. To trade off present versus future costs, it is therefore reasonable to minimize in view of the worst of all scenarios and . This can be achieved by adding the term to the objective function (3).

In summary, the vehicle owner’s decision problem can be cast as the following robust optimization problem with continuous (functional) uncertain parameters,

| (R) |

where denotes the set of all functions in that are constant on the trading intervals. Using the conservative uncertainty sets and in the constraints ensures that the delivery guarantee dictated by the European Commission can be fulfilled. Failing to fulfill this guarantee might lead to exclusion from the regulation market. In contrast, there are no drastic consequences of reaching an undesirable state-of-charge at time . Hence, we use the less conservative uncertainty sets and in the objective function to steer the terminal state-of-charge toward a desirable value under all reasonably likely frequency deviation scenarios. The use of different uncertainty sets in the same model has previously been proposed in robust portfolio insurance problems (Zymler et al., 2011).

One can show that the function is concave in the decision variables and ; see Propostion 1 in the online supplement. Upper bounds on this function thus constitute non-convex constraints. This implies that (R) represents a non-convex robust optimization problem with functional uncertain parameters. In general, such problems are severely intractable.

Remark 3 (Uncertain driving patterns).

Although model (R) assumes deterministic driving patterns, it readily extends to uncertain driving times and distances. If it is only known that the vehicle will drive at some time within a prespecified interval, then the vehicle owner must not plan on exchanging any electricity with the grid during that interval. Similarly, if it is only known that the vehicle will drive some distance within a certain range, then the vehicle owner must plan with the low end of the range for the constraint on the maximum state-of-charge and with the high end of the range for the constraint on the minimum state-of-charge. The worst-case driving times and distances are thus independent of the vehicle owner’s decisions and can be determined ex-ante.

Remark 4 (Traditional charging stations).

Model (R) assumes that the vehicle exclusively connects to the grid through smart charging stations, which enable the vehicle to provide regulation power with or without the option of discharging into the grid. Traditional charging stations may not offer the option of providing frequency regulation. We can model such charging stations by adding the constraint for all , where if the vehicle is not connected to a smart charger at time and otherwise, which is always an upper bound on .

3 Time Discretization

In order to derive a lossless time discretization of the frequency deviation scenarios in problem (R), we assume from now on that the power demand for driving and the maximum charge and discharge power of the vehicle charger remain constant over the trading intervals. This assumption is justified because a vehicle that is both driving and parking in the same trading interval cannot offer constant market bids and is therefore unable to participate in the electricity market. Although the power demand for driving may fluctuate wildly, the battery state-of-charge cannot increase while the vehicle is driving, and therefore the power consumption for driving can be averaged over trading intervals without loss of generality. Note that we do not assume the frequency deviation scenarios to remain constant over the trading intervals. In practice may fluctuate on time scales of the order of milliseconds, and averaging out the frequency deviations across a trading interval could result in a dangerous oversimplification of reality. This phenomenon is illustrated in the following example.

Example 1 (Risks of ignoring intra-period fluctuations).

As the market decisions and , the power demand and the charging limits and are piecewise constant, one might be tempted to replace the frequency deviation signal with a piecewise constant signal obtained by averaging over the trading intervals. As we will see, however, averaging relaxes the battery state-of-charge constraints. Decisions and that are infeasible under the true signal may therefore appear to be feasible under the averaged signal. Hence, replacing the true signal with the averaged signal could make it impossible for the vehicle owner to honor her market commitments. As a simple example, assume that and are constant and that the true frequency deviation signal averages to 0 over the first trading interval , that is, . The left chart of Figure 2 visualizes two such signals, which display a small and a high total variation and are denoted by and , respectively. The constant signal equal to their (vanishing) average over is denoted by . If reflects reality but is incorrectly replaced with , we are led to believe that the state-of-charge will remain constant at . In reality, however, the battery dissipates the amount of energy over the first trading interval, where , and the state-of-charge temporarily rises above by . If reflects reality, on the other hand, then the repeated charging and discharging of the battery still dissipates energy. See the right chart of Figure 2 for a visualization. While scenario is contrived for maximum impact, scenario rapidly fluctuates around 0 and thus captures a stylized fact that one would expect to see in reality. This example suggests that finding the minimum or the maximum of the state-of-charge over the entire planning horizon and over all signals should be non-trivial because intra-period fluctuations do matter. As a further complication, note that the constraints of the uncertainty set couple the frequency deviations across time.

We will now argue that, in spite of Example 1, and can be restricted to contain only piecewise constant frequency deviation signals without relaxing problem (R). To formalize the reasoning about piecewise constant functions, we introduce a lifting operator that maps any vector to a piecewise constant function with pieces defined through if , . We also introduce the adjoint operator that maps any function to a -dimensional vector defined through for all . Note that and are indeed adjoint to each other because for all and . Mathematically, we impose from now on the following assumption.

Assumption 1.

The functions , and are piecewise constant, that is, there exist such that , and .

Next, we introduce a discretized uncertainty set

reminiscent of , where and count the trading intervals within a regulation cycle and an activation period, respectively. Similarly, we define a smaller discretized uncertainty set reminiscent of , which is obtained from by replacing with and with . In the remainder we impose the following divisibility assumption.

Assumption 2.

The parameters , , and are (positive) multiplies of .

Recall that and characterize the delivery guarantees of frequency regulation bids, while characterizes the granularity of the market bids. In principle, is unrelated to and . Assumption 2 improves the tractability of model R and comes at hardly any loss of generality. If the assumption does not hold but , , and are rational, it can be enforced by reducing to the greatest common divisor of , , and the original , and by introducing linear coupling constraints that will ensure piecewise constant market decisions over the original trading intervals.

Next, we define the finite-dimensional feasible set . As contains only piecewise constant functions, we have . We further define the cost function , which is linear in and . In addition, for any we define the function

| (4) |

which represents the battery state-of-charge at the end of period under the assumption that both the market bids and the frequency deviations are piecewise constant.

We are now ready to define the discrete-time counterpart of the robust optimization problem (R).

| (RK) |

Unlike the original problem (R), the discrete-time counterpart (RK) constitutes a standard robust optimization problem that involves only finite-dimensional uncertain parameters. For this reason, there is hope that is easier to solve than .

The equivalence of (R) and (RK) is perhaps surprising in view of Example 1. It means that the worst-case frequency deviation scenarios are piecewise constant even though intra-period fluctuations matter. Theorem 1 is proved by showing that the four robust constraints in (R) with functional uncertainties are equivalent to the corresponding robust constraints in (RK) with vectorial uncertainties and that the worst-case terminal cost functions in (R) and (RK) coincide. For example, the equivalence of the first (second) robust constraints in (R) and (RK) follows from the observation that, for any fixed , the left hand side of the first (second) constraint in (R) is maximized by a scenario with (), which exists by the definition of . The last two robust constraints in (R) are nonlocal as they depend on the entire frequency deviation scenario and not only on its value at a particular time. Thus, they are significantly more intricate. The robust upper bound on the state-of-charge can be reformulated as an upper bound on . Thanks to the properties of the state-of-charge and the uncertainty set, one can then show that the maximum over must be attained at for some and that for any such the state-of-charge can be expressed as an integral of against a piecewise constant function. Thus, averaging across the trading intervals has no impact on the state-of-charge, which in turn allows us to focus on piecewise constant scenarios without restricting generality. The robust lower bound on the state-of-charge in (R) can be reformulated as a lower bound on , which appears to be intractable because the optimization problem over minimizes a concave function over a convex feasible set and is therefore non-convex. Classical robust optimization provides no general recipe for handling such constraints even if the uncertain parameters are finite-dimensional, and state-of-the-art research settles for deriving approximations (Roos et al., 2020). By exploiting a continuous total unimodularity property of the uncertainty set facilitated by Assumption 2, we first prove that the minimum of over is attained by a frequency deviation trajectory that takes only values in . Next, we demonstrate that there exists an affine function of that matches for all trajectories valued in and for all . In the language of robust optimization, the state-of-charge can be viewed as an analysis variable that adapts to the uncertainty , and the corresponding affine function constitutes a decision rule approximating . Decision rule approximations almost invariably introduce approximation errors (Ben-Tal et al., 2009, § 14). However, the affine decision rule proposed here is error-free because it coincides with for all scenarios valued in that may attain the worst case in . Using this decision rule in an elaborate sensitivity analysis, we can finally prove that the minimum over must be attained at for some and that for any such the state-of-charge can be expressed as an integral of against a piecewise constant function. Thus, we may focus again on piecewise constant scenarios without restricting generality. The full proof of Theorem 1 can be found in the online supplement.

The new robust optimization techniques developed to prove Theorem 1 are of independent interest as they provide exact tractable reformulations for certain adjustable robust optimization problems with functional or vectorial uncertain parameters, where the embedded optimization problems over the uncertainty realizations are non-convex. We also note that the embedded optimization problems over in problem (R) can be viewed as variants of the so-called separated continuous linear programs introduced by Anderson et al. (1983). The proof of Theorem 1 shows that these problems are solved by piecewise constant frequency deviation scenarios that can be computed efficiently, thereby extending the purely existential results by Pullan (1995).

Even though the non-convex robust optimization problem (R) with functional uncertainty admits a lossless time discretization, its discrete-time counterpart (RK) still constitutes a non-convex robust optimization problem and thus appears to be hard. In the next section, however, we will show that (R) can be reformulated as a tractable linear program by exploiting its structural properties.

4 Linear Programming Reformulation

In order to establish the tractability of the non-convex robust optimization problem (R), it is useful to reformulate its time discretization (RK) as the following linear robust optimization problem, where all constraint functions are bilinear in the decision variables and the uncertain parameters.

| (R) |

Here, is used as a shorthand for the reduction in the battery state-of-charge resulting from first charging and then discharging one unit of energy as seen from the grid. In addition, we set , and .

The proof of Theorem 2 critically relies on the exact affine decision rule approximation discovered in the proof of Theorem 1. Note that the linear robust optimization problem (R) still appears to be difficult because each robust constraint must hold for all frequency deviation scenarios in an uncountable uncertainty set or and therefore corresponds to a continuum of ordinary linear constraints. Fortunately, standard robust optimization theory (Ben-Tal et al., 2004; Bertsimas and Sim, 2004) allows us to reformulate (R) as the tractable linear program

| (R) |

where and .

The conversion of the robust optimization problem (R) to the linear program (R) comes at the expense of introducing dual variables. Overall, the linear program (R) involves variables and constraints, that is, its size scales quadratically with . In conjunction, Theorems 1–3 imply that the non-convex robust optimization problem (R) with continuous uncertain parameters can be reduced without any loss to the tractable linear program (R), which is amenable to efficient numerical solution with state-of-the-art linear programming solvers.

Remark 5 (Robustification reduces complexity).

A striking property of the robust optimization model (R) is that it is much easier to solve than the underlying deterministic model, which would assume precise knowledge of the frequency deviation scenario . Indeed, the textbook formulation of the deterministic model requires continuous decision variables to represent and and a binary decision variable to model their complementarity for every (Taylor, 2015, p. 85). This results in a large-scale mixed-integer linear program even if is discretized. In contrast, the robust optimization model (R) is equivalent to the tractable linear program (R). To our best knowledge, we have thus discovered the first practically interesting class of optimization problems that become dramatically easier through robustification. Since the uncertainty set can be seen as a continuous-time version of a classical budget uncertainty set (Bertsimas and Sim, 2004; Bandi and Bertsimas, 2012), we hypothesize that our approach applies to other robust optimization problem with continuous-time budget uncertainty sets. Budget uncertainty sets are very popular in classical robust optimization, and we suspect that there are similarly many applications for robust optimization with functional uncertainties.

Remark 6 (Futility of solving a multistage model).

The proposed model (R) looks only one day ahead and accounts for the future usage of the vehicle only through the cost-to-go function , which depends on the terminal state-of-charge estimates. The basic model (R) can readily be extended to a robust dynamic program that looks days into the future. The cost-to-go functions of this dynamic program can be shown to be convex and piecewise affine. In addition, it is possible to construct tight convex piecewise affine bounds on these cost-to-go functions by solving a series of linear programs. Numerically, we find that the added value of solving a dynamic model that looks days into the future is negligible, probably because electric vehicles can usually fully recharge overnight. We emphasize, however, that the robust optimization models and techniques developed in this paper may also be useful to optimize the operation of other energy storage devices that are characterized by slower dynamics and therefore necessitate a proper multi-stage approach.

5 Numerical Experiments

In the following, we first describe how the vehicle owner’s decision problem is parametrized from data, and we explain the backtesting procedure that is used to assess the performance of a given bidding strategy. Next, we present numerical results and discuss policy implications. All experiments are run on an Intel i7-6700 CPU with GHz clock speed and GB of RAM. All linear programs are solved with GUROBI using its PYTHON interface. In order to ensure the reproducibility of our experiments, we provide links to all data sources and make our code available at www.github.com/lauinger/reliable-frequency-regulation-through-vehicle-to-grid.

5.1 Model Parametrization

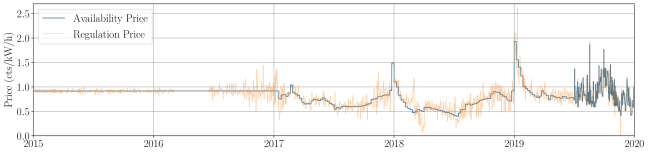

Our experiments are based on availability and delivery prices as well as frequency measurements from the French transmission system. There have been two policy changes in frequency regulation since 2015. While the availability prices were historically kept constant throughout the year, they change on a weekly basis since mid-January 2017 and on a daily basis since July 2019. At this point, the pricing mechanism also changed from a pay-as-bid auction to a clearing price auction. The average availability price over all years from 2015 to 2019 amounts to cts/kWh, but the yearly average decreased in 2017 and 2018, and increased again in 2019 to pre-2017 levels. For all practical purposes we may assume that the expected regulation price coincides with the availability price because the realized regulation price oscillates rapidly around the availability price due to intra-day fluctuations of the frequency-adjusted delivery prices; see Figure 7 in Appendix A. In fact, empirically averages to € over all 10s intervals from 2015 to 2019. We further identify the utility prices with the residential electricity prices charged by Electricité de France (EDF), the largest European electricity provider. These prices exhibit six different levels corresponding to peak- and off-peak hours on high, medium and low price days. High price days can occur exclusively on work days between November and March, whereas medium price days can occur on all days except Sundays. Low-price days can occur year-round. The peak hours are defined as the hours from 6 am to 10 pm on work days, and all the other hours are designated as off-peak hours. The prices corresponding to each type of day and hour are regulated and published in the official French government bulletin. From 2015 to 2019, these prices have not changed more than three times per year. On each day, RTE announces the next day’s price levels by 10:30 am. The average utility price over the years 2015 to 2019 amounts to cts/kWh, exceeding the average availability price by an order of magnitude.

When simulating the impact of the market decisions on the battery state-of-charge, it is important to track the frequency signal with a high time resolution. In fact, the European Commission (2017) requires regulation providers to adjust the power flow between the battery and the grid every ten seconds to ensure that it closely matches for all . We thus use a sampling rate of mHz when simulating the impact of the market decisions on the battery state-of-charge.

The vehicle data is summarized in Table 1 in Appendix A. The chosen parameter values are representative for commercially available midrange vehicle-to-grid-capable electric vehicles such as the 2018 Nissan Leaf. We assume that the vehicle owner reserves the time windows from 7 am to 9 am and from 5 pm to 7 pm on workdays and from 8 am to 8 pm on weekends and public holidays for driving. At all other times, the car is connected to a bidirectional charging station. We also assume that the car travels about 27km per day, which could be easily covered within one hour. However, it makes sense to reserve extended time slots for driving because vehicle owners may not be able to (nor wish to) pinpoint the exact driving times one day in advance.

5.2 Backtesting Procedure and Baseline Strategy

In our experiments, we assess the performance of different bidding strategies over different test datasets covering one of the years between 2015 and 2019. A bidding strategy is any procedure that computes on each day at noon a pair of market decisions and for the following day. We call a strategy non-anticipative if it determines the market decisions using only information observed in the past. In addition, we call a strategy feasible if it allows the vehicle owner to honor all market commitments for all frequency deviation scenarios within the uncertainty set .

To measure the profit generated by a particular strategy over one year of test data, we use the following backtesting procedure. On each day at noon we compute the market decisions for the following day. We then use the actual frequency deviation data between noon and midnight and the market decisions for the current day to calculate the true battery state-of-charge at midnight. Next, we use the frequency deviation data of the following day to calculate the revenue from selling regulation power to the TSO, which is subtracted from the cost of buying electricity for charging the battery. If the strategy is infeasible and the vehicle owner is not able to deliver all promised regulation power even though the realized frequency deviation trajectory falls within the uncertainty set , then she pays a penalty. The penalty at time is set to , where denotes the maximum amount of regulation power that could have been offered without risking an infeasibility, and the penalty factor ranges from to , e.g., RTE (RTE) sets . Repeated offenses may even lead to market exclusion. For simplicity, in each experiment we either assume that the vehicle owner pays a penalty corresponding to a fixed value of for every offense or is excluded from the regulation market directly upon the first offense. If the battery is depleted during a trip, any missing energy needed for driving is acquired at a high price from a public fast charging station. We assume that accounts for the price of energy as well as for the opportunity cost of the time lost in driving to the charging station and waiting to be serviced. In our experiments we set either to 0.75€ /kWh (which corresponds to typical energy prices offered by the European fast charging network Ionity), to 7.5€ /kWh or to 75€ /kWh. The procedure described above is repeated on each day, and the resulting daily profits are accumulated over the entire test dataset.

Our baseline strategy is to determine the next day’s market decisions by solving the robust optimization problem (R) with terminal cost function , where the calibration of and is described below. Thus, (R) is equivalent to an instance of the linear program (R). This problem is updated on each day because the driving pattern as well as the market prices and change, and because the uncertainty sets and for the state-of-charge at midnight depend on the state-of-charge at noon and on the market commitments between noon and midnight that were chosen one day earlier. The baseline strategy is feasible thanks to the robust constraints in (R), which ensure that regulation power can be provided for all frequency deviation scenarios in .

The parameters and are kept constant throughout each backtest. Specifically, we set € /kWh for some and kWh for some . Considering a larger search space did not lead to significantly better out-of-sample performance. Every tuple encodes a different bidding strategy. Given a training dataset comprising one year of frequency measurements and market prices, we compute the cumulative profit of each strategy via the backtesting procedure outlined above, and we choose the tuple that corresponds to the winning strategy. This strategy is non-anticipative if the year of the training dataset precedes the year of the test dataset. Perhaps surprisingly, we find that from 2017 onward, anticipative parameter tuning has no advantage over non-anticipative tuning. From now on, we thus tune and non-anticipatively using the year of training data immediately prior to the test dataset.

5.3 Experiments: Set-up, Results and Discussion

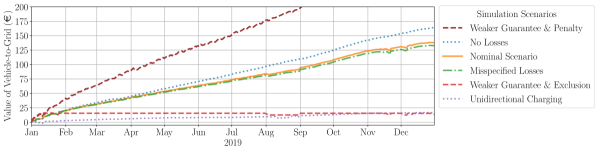

In the remainder, we distinguish six different simulation scenarios. The nominal scenario uses the parameters of Table 1 in Appendix A for both training and testing. All other scenarios are based on slightly modified parameters. Specifically, we consider a lossless energy conversion scenario, which trains and tests the baseline strategy under the assumption that . A variant of this scenario assumes lossless energy conversion in training but tests the resulting strategy under the nominal values of and . We also consider two scenarios with weaker robustness guarantees that replace the uncertainty set in the training phase with its subset . The resulting bidding strategy can be infeasible because it may fail to provide the legally required amount of reserve power. The two scenarios do not differ in training but impose different sanctions for infeasibilities in testing. In the first of the two scenarios the vehicle owner is immediately excluded from the reserve market upon the first infeasibility, thus loosing the opportunity to earn money by offering grid services for the rest of the year. In the second scenario, the vehicle owner is penalized by with for energy that is missing for frequency regulation (see also Section 5.2) and by € /kWh for energy that is missing for driving. Finally, we consider a scenario in which the vehicle is only equipped with a unidirectional charger, that is, we set . Thus, the vehicle is unable to feed power back into the grid. Requests for up-regulation ( can therefore only be satisfied by consuming less energy, which is possible only if .

Figure 3 visualizes the value of vehicle-to-grid in 2019 as a function of time for each of the six simulation scenarios. We first observe that the value of vehicle-to-grid in the lossless energy conversion scenario amounts to 165€ at the end of the year and thus significantly exceeds the respective value of 138€ in the nominal scenario. Using a perfectly efficient vehicle charger would thus have boosted the value of vehicle-to-grid by % in 2019. This is not surprising because a perfect charger prevents costly energy conversion losses. Note also that the scenario with misspecified efficiency parameters results in almost the same value of vehicle-to-grid as the nominal scenario, which suggests that misrepresenting or in training has a negligible effect on the test performance. However, the underlying bidding strategy is not guaranteed to be feasible because it neglects energy conversion losses. Even though this strategy happens to remain feasible throughout 2019, it bears the risk of financial penalties or market exclusion. The two bidding strategies with weakened robustness guarantees initially reap high profits by aggressively participating in the reserve market, but they already fail in the first half of January to fulfill all market commitments. If infeasibilities are sanctioned by market exclusion, the cumulative excess profit thus remains flat after this incident. If infeasibilities lead to financial penalties, on the other hand, the cumulative excess profit drops sharply below zero near the incident but recovers quickly and then continues to grow steadily. As only a few other mild infeasibilities occur in 2019, the end-of-year excess profit of this aggressive bidding strategy still piles up to 296€ , which is more than twice the excess profit in the nominal scenario. We conclude that the current level of financial penalties is too low to deter vehicle owners from making promises they cannot honor. Finally, with a unidirectional charger, the 2019 value of vehicle-to-grid falls to € , which is only % of the respective value with a bidirectional charger. This is not too surprising given that the unidirectional vehicle can only offer as much frequency regulation as the power it buys from the utility, which is all the up-regulation it could ever provide.

In terms of battery usage, the nominal vehicle underwent 66.5 charging cycles for driving and an additional 18.9 charging cycles for frequency regulation in 2019, which suggests increased battery degradation. However, when delivering frequency regulation the standard deviation of the state-of-charge from its midpoint of 50% reduced from 9.5 percentage points to 7.9 percentage points, which is generally thought to benefit battery longevity.

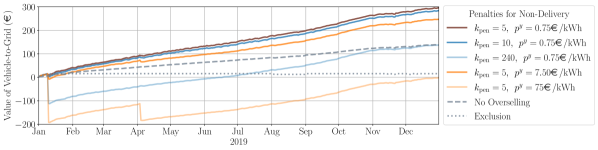

As the bidding strategy with a weakened robustness guarantee can earn high profits when infringements of the EU delivery guarantee incur only financial penalties, we carry out an additional experiment to analyze the impact of the penalty parameters and on the value of vehicle-to-grid; see Figure 4. We observe that for € /kWh, doubling the penalty factor to decreases the value of vehicle-to-grid by only % to € . An additional calculation reveals that the TSO would have to set in order push the value of vehicle-to-grid below that attained in the basline scenario, which fulfills the EU delivery guarantee. On the other hand, for , a tenfold increase of to € /kWh decreases the value of vehicle-to-grid by % to € , and an additional tenfold increase of to € /kWh pushes the value of vehicle-to-grid below zero. Increasing from € /kWh to € /kWh also reduces the number of days on which the vehicle owner does not have enough energy to drive from 7 to 2.

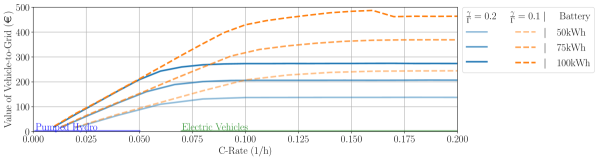

In the next experiment we investigate how the value of vehicle-to-grid depends on the activation ratio and the battery’s size and charge rate (C-rate). The C-rate is defined as the ratio of the charger power and the battery size, and thus it expresses the percentage of the battery’s total capacity that can be charged within one hour. Figure 5 shows that the value of vehicle-to-grid increases with the C-rate up to a saturation point that is insensitive to the battery size but decreases with the activation ratio. In the saturation regime, the value of vehicle-to-grid increases with the battery size. Typical electric vehicles can be fully charged overnight, within about 8 hours. The corresponding C-rate of falls within the saturation regime for both investigated activation ratios of and . This observation has two implications. First, for typical electric vehicles the value of vehicle-to-grid cannot be increased by increasing the charger power (and thereby increasing the C-rate). This insight contradicts previous studies by Kempton and Tomić (2005), Codani et al. (2015) and Borne (2019), which advocate for electric vehicles with C-rates of 1, 0.45, and 0.37, respectively. The reason for this discrepancy is that none of the previous studies faithfully account for the EU delivery guarantee. In particular, Borne (2019) allows the vehicle owner to anticipate future frequency deviations, and Codani et al. (2015) assume that the bidding strategy can be updated on an hourly basis, thereby exploiting information that is not available at the the time when the market bids are collected by the TSO (i.e., one day in advance). By underestimating the amount of energy that the vehicle owner must be able to exchange with the TSO to satisfy all future obligations on the reserve market, these studies overestimate the amount of regulation power that can be sold, which makes potent battery chargers appear more useful than they actually are. The second implication is that the activation ratio has a critical impact on the value of vehicle-to-grid. The incumbent storage providers of the European electricity grid, namely pumped-hydro storage power plants, have C-rates of about (Andrey et al., 2020), which are significantly smaller than the C-rates of electric vehicles. At such C-rates, the value of providing frequency regulation is the same for activation ratios of 0.1 and 0.2. To minimize competition from vehicle-to-grid, pumped-hydro storage operators may thus have an incentive to lobby for high activation ratios.

From the perspective of a TSO, the higher the activation ratio, the larger the uncertainty set and the lower the probability of blackouts. However, Figure 1 suggests that an activation period of minutes is already conservative. On the other hand, the larger , the harder it is for storage operators to provide regulation power, which may lead to less competition, higher market prices, and a higher total cost of frequency regulation. As the system operator is a public entity, this cost is ultimately borne by the public, and the choice of the activation ratio is a political decision.

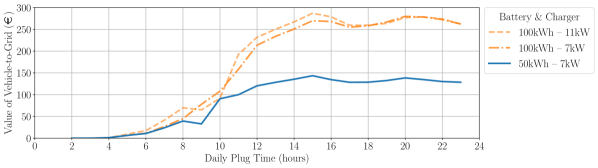

Figure 6 shows the value of vehicle-to-grid in 2019 against the daily plug time, that is, the total amount of time during which the vehicle is connected to a bidirectional charger. In this experiment, we assume that a daily plug time of means that cars are plugged from midnight to am and from pm to midnight the next day. Whenever the car is not plugged, it consumes a constant amount of power such that the total consumption over the year corresponds to a mileage of 10,000 km as in the baseline experiment. We observe that the value of vehicle-to-grid increases with the daily plug time and saturates after 15 hours at a level that scales with the battery size. Thus, a daily plug time of 15 hours suffices for offering the maximal possible amount of regulation power. Additional experiments show that for an activation ratio of 0.1 instead of 0.2, the saturation point increases to 20 hours.

6 Conclusions

We develop an optimization model for the decision problem of an electricity storage operator offering frequency regulation. To our best knowledge, this is the first model that faithfully accounts for the delivery guarantees required by the European Commission. In contrast, all existing models relax the true delivery guarantee constraints and therefore risk that the electricity storage is empty (full) when a request for up- (down-)regulation arrives. In its original formulation, our model represents a non-convex robust optimization problem with functional uncertain parameters and thus appears to be severely intractable. Indeed, the state-of-the-art methods for solving the deterministic version of this problem for a single frequency deviation scenario in discrete time rely on techniques from mixed-integer linear programming. Maybe surprisingly, however, our robust optimization problem is equivalent to a tractable linear program. This is an exact result and does not rely on any approximations. To our best knowledge, we have thus discovered the first practically interesting class of optimization problems that become significantly easier through robustification.

As our optimization model faithfully captures effective legislation, it enables us to quantify the true value of vehicle-to-grid. This capability is relevant for understanding the economic incentives of different stakeholders such as vehicle owners, aggregators, equipment manufacturers, and regulators.

As for the vehicle owners, we find that their profits from frequency regulation range from 100€ to 500€ per year under typical driving patterns. It seems unlikely that such profits are sufficient for vehicle owners to forego the freedom of using their car whenever they please to. Nevertheless, some vehicle owners may choose to participate in vehicle-to-grid for idealistic reasons such as advancing the energy transition away from fossil fuels. Our numerical results also reveal that the value of vehicle-to-grid saturates at daily plug times above 15 hours. Thus, maximal profits from frequency regulation can be reaped even if the vehicle is disconnected from the grid up to 9 hours per day. This means that vehicle owners participating in vehicle-to-grid still enjoy considerable flexibility as to when to drive, which could help to promote the adoption of vehicle-to-grid.

Our results also have ramifications for aggregators, which pool multiple vehicles to offer regulation power. Indeed, aggregators may allow vehicle owners to reserve their vehicles for up to 9 hours of driving per day without sacrificing profit. This leaves vehicle owners ample freedom and reduces the probability that they exceed their driving slots. Thus, the actual number of vehicles available for frequency regulation at any point in time closely matches its prediction. This allows aggregators to place reserve market bids with small safety margins, which ultimately lowers transaction costs. The online supplement extends our one-vehicle problem formulation to a multi-vehicle formulation.

Equipment manufacturers design and sell bidirectional vehicle chargers. Contrary to previous studies that relax the exact delivery guarantee constraints, we find that the battery size and not the charger power is limiting the profits from frequency regulation. Manufacturers thus have no incentive to produce overly powerful bidirectional chargers.

The electricity system and the society as a whole could benefit significantly from vehicle-to-grid, which harnesses the idle storage capacities of electric vehicles and thereby reduces the need for other sources of flexible electricity supply, such as gas power plants or stationary batteries. This in turn reduces the need for imports of natural gas and critical raw materials, increases the long-term security of electricity supply, and decreases greenhouse gas emissions. Regulators may therefore want to make vehicle-to-grid more attractive by prescribing the availability and delivery prices, defining appropriate delivery guarantee requirements and setting the penalties charged for non-compliance. Our results show that the vehicle owners’ profits from frequency regulation decrease with the activation ratio and that current penalties are too low to incentivize vehicle owners to respect the law. Regulators could thus make vehicle-to-grid more attractive by decreasing the activation ratio and thereby relaxing the delivery guarantee requirements. Given that the delivery guarantee in our nominal scenario is very restrictive, this would only slightly decrease the reliability of frequency regulation. If, at the same time, regulators were to increase the penalties for non-compliance, then the reliability of frequency regulation might even increase because more vehicle owners would honor their contractual obligations. Our new model can be used for finding the appropriate level of the penalty.

Acknowledgments

DL acknowledges fruitful discussions with Nadège Faul, François Colet, Wilco Burghout, Paul Codani, Olivier Borne, Emilia Suomalainen, Jaâfar Berrada, Willett Kempton, Evangelos Vrettos, Sophie Hiriart, and Pierre Guillain, and funding from the Institut VEDECOM.

References

- Anderson et al. (1983) E. J. Anderson, P. Nash, and A. F. Perold. Some properties of a class of continuous linear programs. SIAM Journal on Control and Optimization, 21(5):758–765, 1983.

- Andrey et al. (2020) C. Andrey, P. Barberi, L. Lacombe, L. van Nuffel, F. Gérard, J. Gorenstein Dedecca, K. Rademaekers, Y. El Idrissi, and M. Crenes. Study on Energy Storage – Contribution to the Security of the Electricity Supply in Europe. Publications Office of the European Union, 2020.

- Bandi and Bertsimas (2012) C. Bandi and D. Bertsimas. Tractable stochastic analysis in high dimensions via robust optimization. Mathematical Programming, Ser. B 134(1):23–70, 2012.

- Ben-Tal et al. (2004) A. Ben-Tal, A. Goryashko, E. Guslitzer, and A. Nemirovski. Adjustable robust solutions of uncertain linear programs. Mathematical Programming, Ser. A 99(2):351–376, 2004.

- Ben-Tal et al. (2009) A. Ben-Tal, L. El Ghaoui, and A. Nemirovski. Robust Optimization. Princeton University Press, 2009.

- Bertsimas and Sim (2004) D. Bertsimas and M. Sim. The price of robustness. Operations Research, 52(1):35–53, 2004.

- Bertsimas and Tsitsiklis (1997) D. Bertsimas and J. N. Tsitsiklis. Introduction to Linear Optimization. Athena Scientific, 1997.

- Borne (2019) O. Borne. Vehicle-to-Grid and Flexibility for Electricity Systems: From Technical Solutions to Design of Business Models. PhD thesis, Université Paris-Saclay, 2019.

- Borne et al. (2018) O. Borne, Y. Perez, and M. Petit. Market integration or bids granularity to enhance flexibility provision by batteries of electric vehicles. Energy Policy, 119:140–148, 2018.

- Boyd et al. (2011) S. Boyd, N. Parikh, E. Chu, B. Peleato, and J. Eckstein. Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends® in Machine learning, 3(1):1–122, 2011.

- Boyd and Vandenberghe (2004) S. P. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press, 2004.

- Broneske and Wozabal (2017) G. Broneske and D. Wozabal. How do contract parameters influence the economics of vehicle-to-grid? Manufacturing & Service Operations Management, 19(1):150–164, 2017.

- Carpentier et al. (2019) P. Carpentier, J.-P. Chancelier, M. de Lara, and T. Rigaut. Algorithms for two-time scales stochastic optimization with applications to long term management of energy storage. Preprint available from http://hal.archives-ouvertes.fr/hal-02013963, 2019.

- Codani et al. (2015) P. Codani, M. Petit, and Y. Perez. Participation of an electric vehicle fleet to primary frequency control in France. International Journal of Electric and Hybrid Vehicles, 7(3):233–249, 2015.

- Donadee and Ilić (2014) J. Donadee and M. D. Ilić. Stochastic optimization of grid to vehicle frequency regulation capacity bids. IEEE Transactions on Smart Grid, 5(2):1061–1069, 2014.

- Dubarry et al. (2017) M. Dubarry, A. Devie, and K. McKenzie. Durability and reliability of electric vehicle batteries under electric utility grid operations: Bidirectional charging impact analysis. Journal of Power Sources, 358:39–49, 2017.

- European Commission (2017) European Commission. Commission Regulation (EU) 2017|1485 of 2 August 2017 establishing a guideline on electricity transmission system operation. Official Journal of the European Union, 60(220):1–120, 2017.

- Federal Highway Administration (2017) Federal Highway Administration. 2017 National Household Travel Survey, 2017.

- Gestionnaire du Réseau de Transport d’Electricité (2009) Gestionnaire du Réseau de Transport d’Electricité. Documentation Technique de Référence, Chapitre 4–Contribution des utilisateurs aux performances du RPT, Article 4.1–Réglage Fréquence/Puissance, 2009.

- Ghate (2020) A. Ghate. Robust continuous linear programs. Optimization Letters, 14:1627–1642, 2020.

- Glover et al. (2010) J. D. Glover, M. S. Sarma, and T. J. Overbye. Power Systems Analysis and Design. Cengage, 2010.

- Guille and Gross (2009) C. Guille and G. Gross. A conceptual framework for the vehicle-to-grid (V2G) implementation. Energy Policy, 37:4379–4390, 2009.

- Han et al. (2010) S. Han, S. Han, and K. Sezaki. Development of an optimal vehicle-to-grid aggregator for frequency regulation. IEEE Transactions on Smart Grid, 1(1):65–72, 2010.

- Han et al. (2011) S. Han, S. Han, and K. Sezaki. Estimation of achievable power capacity from plug-in electric vehicles for V2G frequency regulation: Case studies for market participation. IEEE Transactions on Smart Grid, 2:632–641, 2011.

- He et al. (2016) G. He, Q. Chen, C. Kang, P. Pinson, and Q. Xia. Optimal bidding strategy of battery storage in power markets considering performance-based regulation and battery cycle life. IEEE Transactions on Smart Grid, 7(5):2359–2367, 2016.

- Houska (2011) B. Houska. Robust Optimization of Dynamic Systems. PhD thesis, KU Leuven, 2011.

- Kempton and Letendre (1997) W. Kempton and S. E. Letendre. Electric vehicles as a new power source for electric utilities. Transportation Research Part D: Transport and Environment, 2(3):157–175, 1997.

- Kempton and Tomić (2005) W. Kempton and J. Tomić. Vehicle-to-grid power fundamentals: Calculating capacity and net revenue. Journal of Power Sources, 144(1):268–279, 2005.

- Lauinger et al. (2017) D. Lauinger, F. Vuille, and D. Kuhn. A review of the state of research on vehicle-to-grid (V2G): Progress and barriers to deployment. In European Battery, Hybrid and Fuel Cell Electric Vehicle Congress, 2017.

- Mak (2020) H.-Y. Mak. Enabling smarter cities with operations management. Manufacturing & Service Operations Management, 24(1):24–39, 2020.

- Mercier et al. (2009) P. Mercier, R. Cherkaoui, and A. Oudalov. Optimizing a battery energy storage system for frequency control application in an isolated power system. IEEE Transactions on Power Systems, 24(3):1469–1477, 2009.

- Namor et al. (2019) E. Namor, F. Sossan, R. Cherkaoui, and M. Paolone. Control of battery storage systems for the simultaneous provision of multiple services. IEEE Transactions on Smart Grid, 10(3):2799–2808, 2019.

- Nemhauser and Wolsey (1999) G. L. Nemhauser and L. A. Wolsey. Integer and Combinatorial Optimization Part III. Wiley, 1999.

- Noel et al. (2019) L. Noel, G. Z. de Rubens, J. Kester, and B. K. Sovacool. Vehicle-to-Grid: A Sociotechnical Transition Beyond Electric Mobility. Palgrave Macmillan, 2019.

- Pullan (1995) M. C. Pullan. Forms of optimal solutions for separated continuous linear programs. SIAM Journal on Control and Optimization, 33(6):1952–1977, 1995.

- Qi et al. (2022) W. Qi, M. Sha, and S. Li. When shared autonomous electric vehicles meet microgrids: Citywide energy-mobility orchestration. Manufacturing & Service Operations Management, 24(5):2389–2406, 2022.

- Rebours et al. (2007) Y. G. Rebours, D. S. Kirschen, M. Trotignon, and S. Rossignol. A survey of frequency and voltage control ancillary services–Part I: Technical features. IEEE Transactions on Power Systems, 22(1):350–357, 2007.

- Réseau de transport d’électricité (2017a) (RTE) Réseau de transport d’électricité (RTE). Règles Service Système Fréquence, 2017a.

- Réseau de transport d’électricité (2017b) (RTE) Réseau de transport d’électricité (RTE). Bilan prévisionnel de l’équilibre offre-demande d’électricité en France, 2017b.

- Réseau de transport d’électricité (2017c) (RTE) Réseau de transport d’électricité (RTE). Electricity Report 2017, 2017c.

- Roos et al. (2020) E. Roos, D. den Hertog, A. Ben-Tal, F. de Ruiter, and J. Zhen. Tractable approximation of hard uncertain convex optimization problems. Available from Optimization Online, 2020.

- Sortomme and El-Sharkawi (2012) E. Sortomme and M. A. El-Sharkawi. Optimal scheduling of vehicle-to-grid energy and ancillary services. IEEE Transactions on Smart Grid, 3(1):351–359, 2012.

- Sperling (1994) D. Sperling. Future Drive: Electric Vehicles and Sustainable Transportation. Island Press, Washington, D.C. & Covelo, California, 1994.

- Sweda et al. (2017) T. M. Sweda, I. S. Dolinskaya, and D. Klabjan. Optimal recharging policies for electric vehicles. Transportation Science, 51(2):457–479, 2017.

- Taylor (2015) J. A. Taylor. Convex Optimization of Power Systems. Cambridge University Press, 2015.

- Thompson (2018) A. Thompson. Economic implications of lithium ion battery degradation for vehicle-to-grid (V2X) services. Journal of Power Sources, 396:691–709, 2018.

- Uddin et al. (2017) K. Uddin, T. Jackson, W. D. Widanage, G. Chouchelamane, P. A. Jennings, and J. Marco. On the possibility of extending the lifetime of lithium-ion batteries through optimal V2G facilitated by an integrated vehicle and smart-grid system. Energy, 133:710–722, 2017.

- Uddin et al. (2018) K. Uddin, M. Dubarry, and M. B. Glick. The viability of vehicle-to-grid operations from a battery technology and policy perspective. Energy Policy, 113:342–347, 2018.

- Vandael et al. (2013) S. Vandael, T. Holvoet, G. Deconinck, S. Kamboj, and W. Kempton. A comparison of two GIV mechanisms for providing ancillary services at the University of Delaware. In IEEE SmartGridComm 2013 Symposium–Demand Side Management, Demand Response, Dynamic Pricing, 2013.

- Vandael et al. (2020) S. Vandael, T. Holvoet, G. Deconinck, H. Nakano, and W. Kempton. A scalable control approach for providing regulation services with grid-integrated electric vehicles. In T. Suzuki, S. Inagaki, Y. Susuki, and A. T. Tran, editors, Design and Analysis of Distributed Energy Management Systems, chapter 6, pages 107–128. Springer, 2020.

- Warrington et al. (2013) J. Warrington, P. Goulart, S. Mariethoz, and M. Morari. Policy-based reserves for power systems. IEEE Transactions on Power Systems, 20(4):4427–4437, 2013.

- Wenzel et al. (2018) G. Wenzel, M. Negrete-Pincetic, D. E. Olivares, J. MacDonald, and D. S. Callaway. Real-time charging strategies for an electric vehicle aggregator to provide ancillary services. IEEE Transactions on Smart Grid, 9(5):5141–5151, 2018.

- Yao et al. (2017) E. Yao, V. W. S. Wong, and R. Schober. Robust frequency regulation capacity scheduling algorithm for electric vehicles. IEEE Transactions on Smart Grid, 8(2):984–997, 2017.

- Yeh (1985) W. W.-G. Yeh. Reservoir management and operations models: A state-of-the-art review. Water Resources Research, 21(12):1797–1818, 1985.