ownRelevant publications by the applicant

On a computationally-scalable sparse formulation of the multidimensional and non-stationary maximum entropy principle

Abstract

Data-driven modelling and computational predictions based on maximum entropy principle (MaxEnt-principle) aim at finding as-simple-as-possible - but not simpler then necessary - models that allow to avoid the data overfitting problem. We derive a multivariate non-parametric and non-stationary formulation of the MaxEnt-principle and show that its solution can be approximated through a numerical maximisation of the sparse constrained optimization problem with regularization. Application of the resulting algorithm to popular financial benchmarks reveals memoryless models allowing for simple and qualitative descriptions of the major stock market indexes data. We compare the obtained MaxEnt-models to the heteroschedastic models from the computational econometrics (GARCH, GARCH-GJR, MS-GARCH, GARCH-PML4) in terms of the model fit, complexity and prediction quality. We compare the resulting model log-likelihoods, the values of the Bayesian Information Criterion, posterior model probabilities, the quality of the data autocorrelation function fits as well as the Value-at-Risk prediction quality. We show that all of the considered seven major financial benchmark time series (DJI, SPX, FTSE, STOXX, SMI, HSI and N225) are better described by conditionally memoryless MaxEnt-models with nonstationary regime-switching than by the common econometric models with finite memory. This analysis also reveals a sparse network of statistically-significant temporal relations for the positive and negative latent variance changes among different markets. The code is provided for open access.

Acknowledgement

The authors thank Michael Rockinger (HEC Lausanne) for providing the code for PML4 parameter estimator we used for comparison. This work was funded by the Swiss National Research Foundation (Project 140829) and DFG SPP 1114 (Mercator Fellowship of Illia Horenko).

Maximum Entropy principle (MaxEnt-principle) was originally introduced in physics and information theory to search for least-biased probabilistic data descriptions that match certain statistical properties of the data, e.g. the data distribution moments (Jaynes (1957)). The MaxEnt-principle implies that the most unbiased distribution for the data is the one that admits the most uncertainty, measured in terms of entropy. Depending on the constraints imposed in the entropy maximisation problem, different parametric probability distributions that can be described by this principle are Gaussian, Exponential, Laplace, Cauchy, Chi-squared and Gamma distributions, among others. This MaxEnt-based probabilistic modelling approach has been successfully applied to many problems ranging from biology (Phillips et al. (2006), Mora et al. (2010)) and natural language processing (Berger et al. (1996), Nigam et al. (1999)) to applications from economics and finance (Zellner and Highfield (1988), Wu (2003)).

In contrast to the parametric MaxEnt-modelling, where the particular parametric distribution models (Gaussian, Exponential, etc.) are dependent on the fixed finite set of constant parameters, computation of nonparametric Maximum Entropy densities even in one dimension is not a trivial task, as was previously discussed in Agmon et al. (1979), Mead and Papanicolaou (1984) and in Holly et al. (2011). In Marchenko et al. (2018) a systematic mathematical derivation for a non-stationary extension of the non-parametric MaxEnt-methodology for one-dimensional time series problems was introduced. This BV-Entropy framework imposes a mild bounded-variation (BV) assumption on the time dependence of the non-stationary moments of the underlying non-stationary probability distribution function (p.d.f.). In Marchenko et al. (2018) it was shown that the original ill-posed non-stationary MaxEnt-principle - formulated as an entropy maximisation problem with time-dependent moment constraints - can be sharply bounded from below via a well-posed and computationally-scalable maximisation problem. This lower-bound problem appeared to be a nonparametric regime-switching entropy maximisation problem with locally-stationary regimes, subject to -constraints on the regime-specific vectors of moments and to a BV-constraint for the latent regime transitions. The linear BV-constraint happens to bound from above with the maximal number of regime switches - and controls the persistence of the obtained MaxEnt regime transition models. It was also shown that the optimal values of and can be estimated deploying common model selection criteria like the Bayesian Information Criterion (BIC).

However, this model formulation is confined to one-dimensional time series analysis problems only. A direct extension of this one-dimensional BV-Entropy methodology to multiple dimensions is hampered by the curse of dimension and the overfitting problems: linear growth in the number of problem dimension will results in the exponential growth in the number of the underlying mulivariate MaxEnt-parameters that have to be determined from the data statistics. In many practical applications - for example in economics and finance - there is only one historical realisation of the process that is available, with no possibility to obtain other sampling realisations from some "model". For every particular dimension at every particular time there is only one data point available. This means that a completely nonparametric approach to statistical analysis of such a data leads to ill-posed problems (Härdle (1990)).

In the following, we describe a computational algorithm achieving a sparse multidimensional extensions of the one dimensional BV-Entropy model from (Marchenko et al. (2018)), where the coupling between the individual 1D entropy maximisation problems will be achieved through a sparsifying regularization constraint that controls appropriate function space distances (, or BV) between the individual latent factors.

The resulting algorithm (further referred to as a TV-Entropy) allows a computationally-tractable search for the most unbiased multivariate time-dependent distribution of the data, minimizing the optimal number of the locally-stationary hidden regimes and sparsifying their time-persistent regime-switching dynamic and the regime-specific distribution parameter vectors. Then, we illustrate its performance and compare it to common approaches on the test model system (a regime-switching Gaussian, Figure 1). Finally, we apply this algorithm and the common GARCH tools to a set of seven popular financial stock market indexes and show that these simpler memoryless maximum entropy models of volatility outperform the popular heteroschedastic methods with finite memory for all of the benchmarks considered (Figures 2-3, Table 2).

Method

We start with -dimensional multivariate time series data , and on a closed interval . The goal is to find the most descriptive and least complex model for these data. We will first assume that is conditionally independent in time, and would like to estimate its unknown marginal time-dependent probability densities . In the context of the Maximum Entropy principle, the density can be identified by solving an optimization problem which consists of finding a time-dependent density function with the maximal entropy among all distribution functions that match the data in first sample moments at all of the given time instances in the dimension . There is a long tradition in statistics and econometrics adopting inference methodologies based on matching sample moments (Generalized Method of Moments (GMM) estimation, Hansen (1982)). Moreover, Maximum Entropy methods are often invoked in multinomial choice problems (Ggolan et al. (1996), Manski and McFadden (1981)). Maximisation of the expected entropy with respect to a time-dependent multivariate probability density (where the expectation is taken over the time and the dimension ) can be written as:

| (1) |

subject to

| (2) |

and are time- and dimension-dependent sample moments. Then, the optimal can be derived by computing first-order optimality conditions of the corresponding optimization problem (1-2), providing the following formulation

| (3) | |||

| (4) | |||

| (5) |

where are unknown time-dependent parameters (Lagrange multipliers) of maximum entropy distributions. One way to compute would be to maximize the log-likelihood function based on the obtained densities , i.e.,

| (6) | |||

| (7) |

The first-order optimality conditions of the problem [6] are equivalent to the conditions [3]-[5], therefore maximizing the criterion in [6] are the optimal values of the maximum entropy densities parameters in [3]-[5].

In the realistic applications when only one historical realization sequence is available, there is no straightforward solution to the nonstationary problem [6], as at each time instance we have much more parameters than we have observed data. To solve this problem, we are going to introduce two following assumptions.

Assumption 1: Total variation (a TV norm) of the MaxEnt parameters is bounded, i.e.

| (8) |

Assumption 2: There exist distinct sets of parameters and (with and for all ), such that for any and vector can be expressed as a convex linear combination

| (9) |

Assumptions 1 and 2 introduce sparsity on the across time and space indices and . Very importantly, these assumptions do not rely on any ordering in the space dimension. Indeed, in many practical applications, e.g., in economics and finance a natural ordering across assets, institutions, markets etc. does not exist. On a practical side, for real financial data these assumptions will be fulfilled automatically if one sets both constants and to be large enough (for example, setting always fulfills Assumption 2). In the practical applications the aim will be in finding the computationally-scalable lower bound estimates of these constants. Substituting condition [9] in [8], getting use of the Jensen’s inequality and inserting into [6] the obtained inequality constraint as the penalty-term of the Karush-Kuhn-Tucker leads to the following lower-bound approximation of the MaxEnt-problem [6]:

| (10) | |||

| (11) |

A solution of the obtained lower-bound problem is an approximation to the solution of the original nonstationary ill-posed Maximum Entropy problem [1]. The optimization criteria in [10] is nonlinear and nonconvex - implying that the problem can have more than one locally-optimal solution. However, there are three properties of this optimization problem formulation that can be exploited numerically: (i) when is kept fixed, [10]-[11] becomes a uniquely-solvable linear programming (LP) problem w.r.t. - and can be solved very efficiently by means of common LP-tools (e.g., with the simplex method); (ii) if , solving [10]-[11] becomes equivalent to solving independent one-dimensional non-stationary entropy maximisation problems from the BV-Entropy method in Marchenko et al. (2018); (iii) algebraic structure of the term containing is similar to the LASSO-regularization formulation very popular in machine learning (Tibshirani (1996)), increasing will result in increasing the sparsity of and in penalizing the temporal and cross-sectional variations in - making the obtained MaxEntropy model approximations more simple, sparse and persistent across dimensions and in time. For a numerical solution of the problem [10]-[11] with a fixed set of parameters and we will adapt the subspace algorithms introduced in Horenko (2010a, b) (that were further developed in Gerber and Horenko (2015); Pospíšil et al. (2018)): to get the best possible use of the algebraic structure in [10]-[11], resulting algorithms should iterate between two distinct optimization problems, where the problem [10]-[11] is solved w.r.t. (for a current fixed values of ) and in the following step - w.r.t. (for current fixed values of ). The -optimization step will involve independent solution of regularized stationary Maximum Entropy problems. As a result, an iterative procedure would converge monotonically to a local maximum solution of the problem [10]-[11]. This procedure - further referred to as TV-Entropy - should be repeated for different combinations of the input parameters , (from some pre-defined discrete sets) - and common model discrimination tools like Akaike Information Criterion (Burnham and Anderson (2003)), cross-validation (Kohavi (1995)) or the bootstrap (Burnham and Anderson (2003), Kohavi (1995)) will be deployed to identify the most optimal combination of - hopefully small - parameters , .

It is straightforward to verify that the second term in (10) can alternatively be formulated as a set of two linear inequality constraints:

| (12) | |||

| (13) |

where , with being the global TV-constant defined in (8). This formulation allows a separate handling of constraints for the regime-switching and for the MaxEnt parameters with two separate sets of constraining variables and . In contrast, the Tykhonov-like formulation (10-11) allows a joint simultaneous control for all of the variables by means of a single constraining variable .

Results

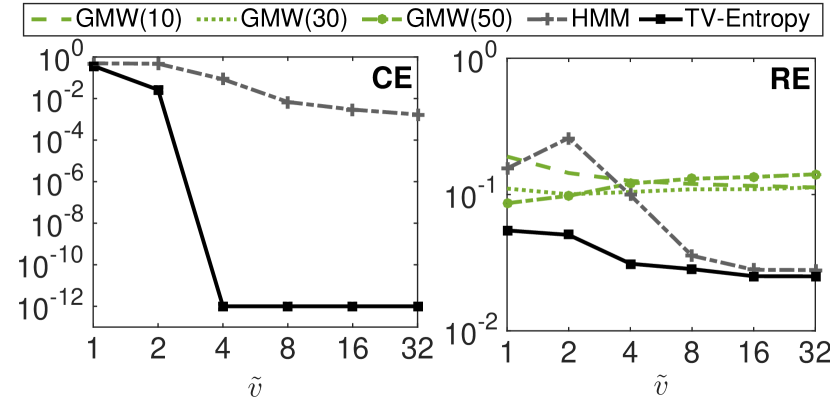

First, we illustrate an application of the TV-Entropy methodology introduced above and its comparison to the common regime identification methods like HMM and the adaptive Gaussian Moving Window (GMW) in a study with artificial simulated data. For this simulated data study we use the model system proposed in Marchenko et al. (2018): we generate multiple samples from the regime-switching model with two Gaussian regimes, i.e., , where with , . For each value of we generate 100 samples with 1000 points. The regime switching weights are discrete and satisfy the convexity constraints in [11], imposing only one active regime at time . There are three regime transitions in data-generating process that occur every 250 points. The time-dependent variance signal can then be computed as . This test system is designed to be favorable for HMM and GMW - since their common variants rely on the Gaussianity assumption for the realizations. The TV-Entropy models were estimated with two regimes, six density regime parameters and number of regime switches. We used 10 annealing steps for estimating both TV-Entropy and HMM models. The corresponding optimal parameters were chosen using BIC criteria. For GMW model we used bandwidth value to obtain various levels of persistence. As demonstrated in Figure 1, TV-Entropy outperforms these common models in data classification and reconstruction of the variance signal used in data-generating process.

| Stationary and without | Nonstationary and with | |

|---|---|---|

| regime transitions | regime transitions | |

| Parametric | GARCH/GARCH-GJR | MS-GARCH |

| Semi/Nonparametric | GARCH-PML4 | TV-Entropy |

In the following empirical study we compare the performance of the TV-Entropy approach [10]-[11] to different popular variants of GARCH models (Table LABEL:tab:models). For the sake of simplicity, we will start with . For a comparison with common econometric models we use a classic GARCH111With this abbreviation we refer to GARCH(1,1) model. model with normally distributed innovations (Bollerslev (1986)) and a GARCH-PML4 model that uses Maximum Entropy principle to achieve the less-restrictive description of the density (Holly et al. (2011)). Additionally, we employ GARCH-GJR model that incorporates the asymmetric influence of positive and negative news on volatility (Glosten et al. (1993)) and the MS-GARCH model that assumes the presence of several hidden GARCH regimes in data with the regime transitions governed by a Markov chain (Bauwens et al. (2014)).

As benchmark problems we considered the daily percentage log-returns time series of the seven major world market indexes: DJI, SPX, FTSE, STOXX, SMI, HSI and N225222DJI (The Dow Jones Industrial Average Index, USA), SPX (The Standard & Poor’s 500 index, USA US), FTSE (The Financial Times Stock Exchange 100 Index, UK), STOXX (EURO STOXX 50 Index, EU), SMI (The Swiss Market Index, CH), HSI (The Hang Seng Index, HK/CN) and N225 (The Nikkei Stock Average Index, JP).. The data is available in the Oxford-Man Institute’s ”realised library” Gerd et al. (2009)333The dataset and the source code used in numerical experiments are available at https://github.com/Ganna85/TV-Entropy. The sample size and some related statistics of all considered samples are gathered in Table 2. All considered samples are not normally distributed 444For the normal distribution the skewness and kurtosis should be equal to zero and four respectively.. High kurtosis points to the presence of the fat tails in data and non-zero skewness suggests the asymmetry in the distribution of the returns. These properties are consistent with stylized facts often found in empirical data.

| Index | T | skewness | kurtosis |

|---|---|---|---|

| DJI | 2864 | 0.08 | 10.96 |

| SPX | 2862 | -0.08 | 10.11 |

| FTSE | 2878 | -0.09 | 6.81 |

| STOXX | 2896 | -0.12 | 7.61 |

| SMI | 2875 | 0.03 | 9.26 |

| HSI | 2603 | 0.13 | 16.38 |

| N225 | 2773 | -0.41 | 13.30 |

To reduce the number of estimation routines needed to obtain the optimal parameters of the TV-Entropy, we split the estimation procedure into two stages. First, models are estimated for all combinations of the input parameters outlined in Table 3 without -regularization of the regime parameters. The optimal number of the regimes () and transitions upper bound () for each data set are chosen based on minimal BIC value.

| K | N | |||

|---|---|---|---|---|

| {1,2,3,4} | {1,2,3,,50} | 10 | 6 | + |

Next, in order to identify the optimal number of local parameters needed to describe data in each of the regimes, we estimate TV-Entropy models with various values of -regularization bounds, while keeping the number of hidden regimes and transitions fixed according to their optimal values (,) obtained at the previous step. The range of bounds is data-dependent and varies across samples. To choose the appropriate range for each sample we analyze the corresponding unregularized solution.

| Index | |||

|---|---|---|---|

| DJI | 3 | 21 | [6,6,4] |

| SPX | 3 | 18 | [6,6,4] |

| FTSE | 4 | 12 | [6,6,6,6] |

| STOXX | 3 | 16 | [6,6,4] |

| SMI | 3 | 19 | [6,6,4] |

| HSI | 3 | 8 | [6,4,4] |

| N225 | 3 | 11 | [6,6,4] |

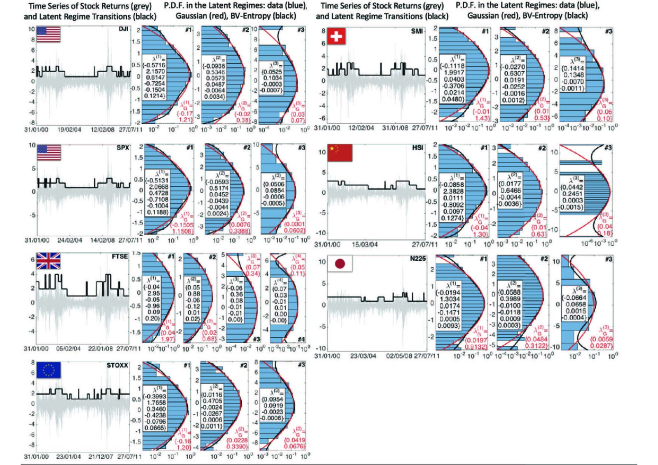

As shown in Table 4, the application of the TV-Entropy model reveals three hidden regimes in all of the considered benchmarks, with an exception of the FTSE index data, where the four-regime model is identified as mBIC-optimal. The obtained regime-switching dynamic appears to be persistent for all of the considered benchmarks. Particularly, the highest number of regime transitions allowed per regime is 21 in the case of DJI and the lowest number is 8 in the case of HSI. Using regularizaion lead to identification of simpler models with respect to the number of regime parameters needed to describe the data. In all samples, except FTSE, we were able to eliminate irrelevant parameters, as reflected in the values of of Table 4 representing the optimal number of the parameters in each regime. The corresponding regime densities with reduced parameters (shown in Figure 2) can be interpreted as curved exponential distributions. For the interpretation of the results it is important to note that integration domain is finite and rescaled to [-1 1] interval at the time of estimation. This approach allows us to resolve integrability issues otherwise present in fitting densities with Maximum Entropy. Apart from the Maximum Entropy distributions estimated by the method (in black), we fit the Gaussian densities to the data in each regime (in red). As shown in the Table 2, the unconditional densities of all seven datasets are skewed with heavy tails. As seen from the comparison, the nonparametric TV-Entropy densities provide a better fit for fat tails and asymmetry exhibited by the underlying densities, compared to the Gaussian distribution function555The Gaussian density is fully described with two moments (e.g., the mean and the variance) and it corresponds to the Maximum Entropy distribution with first two moments constraints (=2).. This effect is most prominent in the regimes where the data points contributing to heavy mass at the tails are observed (for instance regime of HSI in Figure 2).

As shown in Table 5, the memoryless TV-Entropy model outperformed all of the finite-memory GARCH models across all seven benchmarks w.r.t. the log-likelihood and the BIC values. The highest log-likelihood value suggests the superior fit, while the lowest BIC value suggests the best balance between the fit and the complexity among all the considered models. As demonstrated by the posterior probabilities inferred from Schwartz weights [Burnham and Anderson (2003)], the difference in BIC values is highly significant. These results indicate that the assumption of finite autoregressive memory imposed by the GARCH models is redundant for all of the considered time series data, once nonstationary regime switches are taken into account.

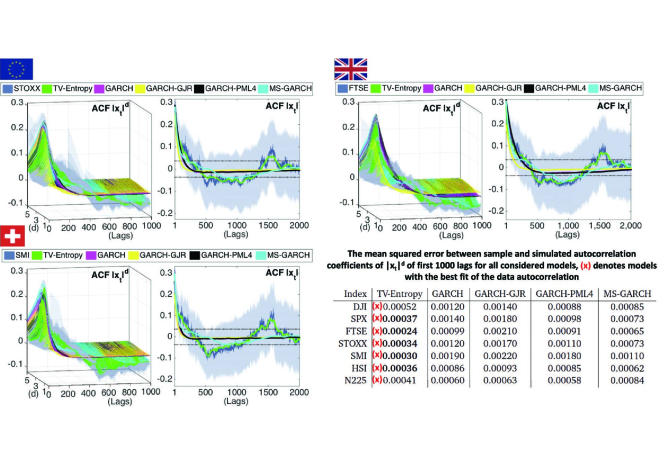

One of the central arguments for using the GARCH models is based on their ability to fit the autocorrelation function of as a function of lag times and exponents (Ding et al. (1993)). As was shown in Ding et al. (1993), there is little to no auto-correlation in daily returns. The highest auto-correlation is observed in the absolute returns and it is significant even at very large lags, suggesting a presence of autoregressive memory in the data. In the following we commence a simulation study where we draw 1000 samples from all previously obtained optimal models. We then compute the mean values of autocorrelation coefficients at each lag and compare them to the auto-correlation coefficients obtained on a real data. Specifically, we analyze the auto-correlation function of as a function of and a lag as shown in the left panels of Figure 3 for SMI, FTSE and STOXX index data. The summary of results for all of the considered indexes are shown in the lower-right panel of the Figure 3. Consistently with Ding et al. (1993), the highest serial correlation is observed around the value for all of the considered benchmarks. As can be seen from Figure 3, even at the very large lags there is a significant serial correlation as the values of the coefficients lay outside the confidence intervals (light grey) constructed under the null-hypothesis that the obtained series are completely random. Results from Figure 3 demonstrate that the simpler, conditionally memoryless TV-Entropy models (green) provide the closest approximation of the sample autocorrelation function (grey), as compared to all of the considered GARCH models.

Next, all of the obtained models will be used to produce volatility forecasts and, consequently, the 1-day-ahead Value-at-Risk (VaR) forecasts. We compare the online VaR prediction quality for the considered methods and benchmarks. Once we observe the new data point we confirm or correct the assigned regime value using the optimal parameters obtained during the in-sample estimation. To compare the quality of the VaR forecasts, we commence the unconditional coverage test Kupiec (1995). As shown in Table 6, there is no particular model that would be clearly preferred for all of the considered assets. However, since the results are not statistically-distinguishable (the confidence intervals are overlapping), it can be concluded that the conditionally memoryless TV-Entropy - relying on fewer tuneable model parameters - is a good alternative to the traditional GARCH models in forecasting 1-day-ahead VaR.

| Index | TV-Entropy | GARCH | G-GJR | G-PML4 | MS-GARCH |

|---|---|---|---|---|---|

| DJI | -3906.43 | -4058.89 | -4000.98 | -4034.36 | -4048.55 |

| SPX | -4016.21 | -4150.95 | -4091.07 | -4128.38 | -4139.24 |

| FTSE | -3465.43 | -3580.84 | -3552.85 | -3563.42 | -3577.93 |

| STOXX | -4415.74 | -4545.38 | -4473.82 | -4528.83 | -4534.32 |

| SMI | -3496.79 | -3641.14 | -3601.21 | -3625.24 | -3631.99 |

| HSI | -3443.06 | -3522.12 | -3521.07 | -3522.29 | -3508.54 |

| N225 | -4003.36 | -4100.27 | -4080.22 | -4067.87 | -4094.51 |

| DJI | 7948.18 | 8141.66 | 8033.80 | 8108.52 | 8113.10 |

| SPX | 8167.73 | 8325.78 | 8213.99 | 8296.56 | 8294.47 |

| FTSE | 7129.99 | 7185.58 | 7137.57 | 7166.67 | 7171.86 |

| STOXX | 8966.99 | 9114.66 | 8979.52 | 9097.52 | 9084.64 |

| SMI | 7136.94 | 7306.16 | 7234.27 | 7290.30 | 7279.97 |

| HSI | 7004.08 | 7067.84 | 7073.59 | 7083.91 | 7047.08 |

| N225 | 8141.50 | 8224.32 | 8192.15 | 8175.38 | 8205.02 |

| DJI | (1.00) | (0.00) | (0.00) | (0.00) | (0.00) |

| SPX | (1.00) | (0.00) | (0.00) | (0.00) | (0.00) |

| FTSE | (0.98) | (0.00) | (0.02) | (0.00) | (0.00) |

| STOXX | (1.00) | (0.00) | (0.00) | (0.00) | (0.00) |

| SMI | (1.00) | (0.00) | (0.00) | (0.00) | (0.00) |

| HSI | (1.00) | (0.00) | (0.00) | (0.00) | (0.00) |

| N225 | (1.00) | (0.00) | (0.00) | (0.00) | (0.00) |

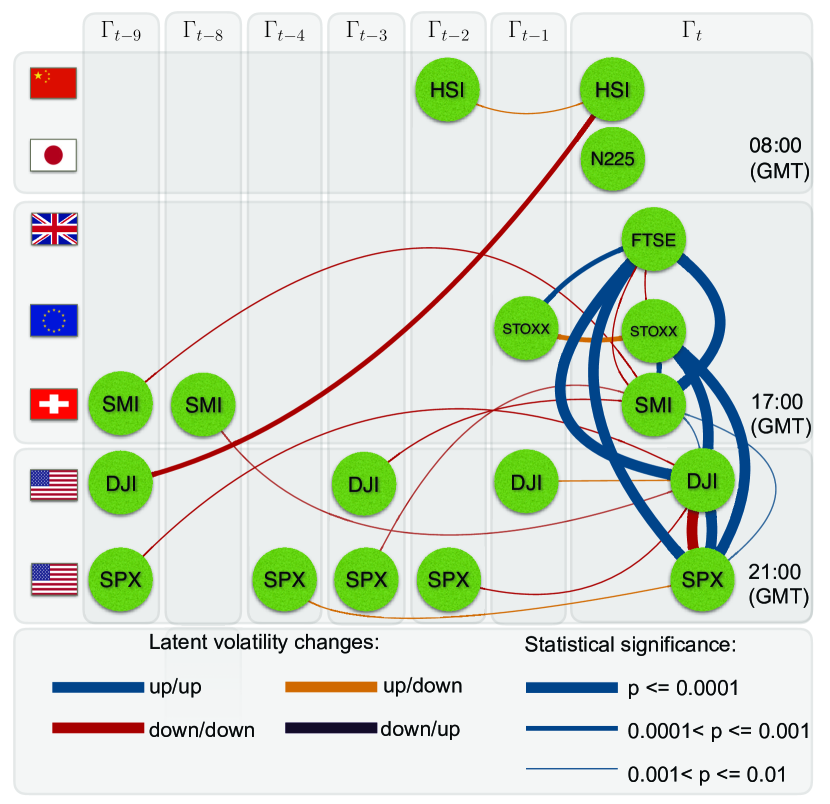

Next, we analyze the relationships between the latent volatility transitions inferred by TV-Entropy (see the left panel of Figure 2). Identified maximum entropy regimes are characterized by different volatility levels. As a result, the regime transitions are jumps indicating an increase or a decrease of the volatility level. For every considered asset we construct two distinct binary variables describing such a behavior, where zeros indicate no jump at a current time instance, and ones stand for transition to the regime with only increased (”up”) or only decreased (”down”) volatility. We then perform a pair-wise comparison of the obtained categorical time series (characterized by "up/up", "up/down", "down/up", "down/down" directions) using Fisher’s exact test (Fisher (1922)) and analyze the resulting p-values to identify the statistically-significant relations between the regime transitions. Shown in Figure 4 are only the most significant relationships () among these categorical time series of latent regime transitions. The assets in the American and in the European regions appear to be heavily connected through their latent regime transitions. These connections are mostly governed by the volatility increase on the short time scale and volatility decrease on longer time scales. As for the considered Asian markets, the inferred latent influence of the American and European markets is present but it appears to be delayed in time and driven mostly by a decrease in the latent volatility levels.

Discussion

In this work we presented a sparse extension of the nonstationary MaxEnt methodology from one to multiple dimensions, aiming at identification of the most qualitative (in terms of the loglikelihood) and the least complex (in terms of the information content and the required number of tuneable parameters) representation for multidimensional time series data.

In application to analysis of financial time series we show that one of the important distinctions between the entropy-based and the common heteroschedastic approaches used in economics and finance is an assumption about the finite autoregressive memory in the underlying data-generating process. Traditionally, the observed data is assumed to be explicitly dependent on its past realizations. In the presented application of the MaxEnt-framework we do not impose additional assumptions about memory and do not include tuneable parameters that describe it. The hypothesis that realizations are independent within the regimes, has been previously explored in Bulla and Bulla (2006) and Rydén et al. (1998) in the context of parametric HMMs, where the authors showed that proposed models can reproduce the empirical properties of daily returns, especially in the case when conditional distributions are not normally distributed. However, also these approaches impose an explicit a priori memory assumption (Markovianity) on the level of the regime-switching process, and it remains unclear whether this assumption is necessary and/or sufficient for realistic financial data. The TV-Entropy approach reveals that the volatility for all of the considered benchmarks is best described by the time-dependent persistent process, where persistence is identified through the adaptive regularization [11] of the regime-switching process and from the fact that within every regime the volatility remains stationary and i.i.d.

| Index | TV-Entropy | GARCH | G-GJR | G-PML4 | MS-GARCH |

|---|---|---|---|---|---|

| DJI | 0.044 | 0.042 | 0.043 | 0.041 | 0.043 |

| SPX | 0.045 | 0.045 | 0.047 | 0.042 | 0.046 |

| FTSE | 0.046 | 0.059 | 0.059 | 0.055 | 0.057 |

| STOXX | 0.054 | 0.052 | 0.052 | 0.048 | 0.052 |

| SMI | 0.048 | 0.049 | 0.051 | 0.047 | 0.049 |

| HSI | 0.056 | 0.054 | 0.051 | 0.054 | 0.015 |

| N225 | 0.044 | 0.047 | 0.051 | 0.044 | 0.046 |

| DJI | 0.013 | 0.018 | 0.015 | 0.014 | 0.018 |

| SPX | 0.013 | 0.017 | 0.018 | 0.014 | 0.017 |

| FTSE | 0.015 | 0.021 | 0.023 | 0.017 | 0.021 |

| STOXX | 0.015 | 0.017 | 0.022 | 0.014 | 0.017 |

| SMI | 0.014 | 0.018 | 0.019 | 0.014 | 0.016 |

| HSI | 0.017 | 0.020 | 0.019 | 0.020 | 0.003 |

| N225 | 0.013 | 0.016 | 0.017 | 0.012 | 0.019 |

Starting with the intrinsically-multivariate but ill-posed MaxEnt-formulation in the formula (1-2), we derived that introducing two (mild) Assumptions 1 and 2 its solution can be approximated from below with a well-posed solution of the sparse regularized problem (10-11). Problem (10-11) is still multivariate since the hidden regime variables change with the dimension , time and the regime . As shown in the Fig. 4, they capture the latent multivariate relation structure over different dimensions and times.

In this manuscript we analyzed seven leading world market indexes across America, Europe and Asia. We found that nonparametric TV-Entropy approach outperforms all of the considered benchmark models for in-sample analysis in terms of the log-likelihood, simplicity (the number of free parameters), the information content (BIC and the posterior model probabilities) and in terms of quality when describing the underlying autocorreltaion function behavior. The out-of-sample study indicates that TV-Entropy methodology is an effective alternative to the GARCH models for forecasting of the 1-day-ahead VaR. The TV-Entropy approach could closely reproduce serial correlation patterns found in data, especially at the large lags (unlike any of the GARCH models considered). This study indicates that the nonstationary MS-GARCH (combining GARCH with the Markovian regime transitions model) allows for a better description of the serial correlation than single regime GARCH models, but it is not able to match the data as accurately as the TV-Entropy model. Finally, Figure 4 illustrates how the regime transition processes inferred from the data allows to identify the statistically-significant temporal relations between latent volatility level transitions across different markets. In particular, these findings indicate that the negative news have a stronger short-term impact on the markets, as we observe that statistically most-significant latent connections are associated with the increase in volatility levels.

References

- Agmon et al. (1979) N. Agmon, Y. Alhassid, and R. D. Levine. An algorithm for finding the distribution of Maximal Entropy. Journal of computational physics, 30(2):250–258, 1979.

- Bauwens et al. (2014) L. Bauwens, A. Dufays, and J. V. K. Rombouts. Marginal Likelihood for Markov-switching and change-point GARCH models. Journal of Econometrics, 178:508–522, 2014.

- Berger et al. (1996) A. L Berger, V. J. Della Pietra, and S. A. Della Pietra. A Maximum Entropy approach to natural language processing. Computational linguistics, 22(1):39–71, 1996.

- Bollerslev (1986) T. Bollerslev. Generalized autoregressive conditional heteroskedasticity. Journal of econometrics, 31(3):307–327, 1986.

- Bulla and Bulla (2006) J. Bulla and I. Bulla. Stylized facts of financial time series and hidden semi-Markov models. Computational Statistics & Data Analysis, 51(4):2192–2209, 2006.

- Burnham and Anderson (2003) K. P. Burnham and D. R. Anderson. Model selection and multimodel inference: a practical information-theoretic approach. Springer Science & Business Media, 2003.

- Ding et al. (1993) Z. Ding, C. W. J. Granger, and R. F. Engle. A long memory property of stock market returns and a new model. Journal of empirical finance, 1(1):83–106, 1993.

- Fisher (1922) R. A. Fisher. On the interpretation of 2 from contingency tables, and the calculation of p. Journal of the Royal Statistical Society, 85(1):87–94, 1922.

- Gerber and Horenko (2015) S. Gerber and I. Horenko. Improving clustering by imposing network information. Science Advances (AAAS), 1(7):e1500163, 2015.

- Gerd et al. (2009) H. Gerd, A. Lunde, N. Shephard, and K. Sheppard. Oxford-man institute’s realized library, 2009.

- Ggolan et al. (1996) A. Ggolan, G. Judge, and J. M. Perloff. A Maximum Entropy approach to recovering information from multinomial response data. Journal of the American Statistical Association, 91(434):841–853, 1996.

- Glosten et al. (1993) L. R. Glosten, R. Jagannathan, and D. E. Runkle. On the relation between the expected value and the volatility of the nominal excess return on stocks. The journal of finance, 48(5):1779–1801, 1993.

- Hansen (1982) L. P. Hansen. Large sample properties of generalized method of moments estimators. Econometrica: Journal of the Econometric Society, pages 1029–1054, 1982.

- Härdle (1990) W. Härdle. Applied nonparametric regression. Number 19. Cambridge university press, 1990.

- Holly et al. (2011) A. Holly, A. Monfort, and M. Rockinger. Fourth order Pseudo Maximum Likelihood methods. Journal of econometrics, 162(2):278–293, 2011.

- Horenko (2010a) I. Horenko. Finite element approach to clustering of multidimensional time series. SIAM Journal on Scientific Computing, 32(1):62–83, 2010a.

- Horenko (2010b) I. Horenko. On the identification of nonstationary factor models and their application to atmospheric data analysis. Journal of the Atmospheric Sciences, 67(5):1559–1574, 2010b.

- Jaynes (1957) E. T. Jaynes. Information theory and statistical mechanics. Physical review, 106(4):620, 1957.

- Kohavi (1995) R. Kohavi. A study of cross-validation and bootstrap for accuracy estimation and model selection. In Ijcai, volume 14, pages 1137–1145. Stanford, CA, 1995.

- Kupiec (1995) P. Kupiec. Techniques for verifying the accuracy of risk measurement models. 1995.

- Manski and McFadden (1981) C. F. Manski and D. McFadden. Structural analysis of discrete data with econometric applications. MIT Press Cambridge, MA, 1981.

- Marchenko et al. (2018) G. Marchenko, P. Gagliardini, and I. Horenko. Towards a computationally tractable maximum entropy principle for nonstationary financial time series. SIAM Journal on Financial Mathematics, 9(4):1249–1285, 2018.

- Mead and Papanicolaou (1984) L. R. Mead and N. Papanicolaou. Maximum Entropy in the problem of moments. Journal of Mathematical Physics, 25(8):2404–2417, 1984.

- Mora et al. (2010) T. Mora, A. M. Walczak, W. Bialek, and C. G. Callan. Maximum Entropy models for antibody diversity. Proceedings of the National Academy of Sciences, 107(12):5405–5410, 2010.

- Nigam et al. (1999) K. Nigam, J. Lafferty, and A. McCallum. Using Maximum Entropy for text classification. In IJCAI-99 workshop on machine learning for information filtering, volume 1, pages 61–67, 1999.

- Phillips et al. (2006) S. J. Phillips, R. P. Anderson, and R. E. Schapire. Maximum Entropy Modeling of species geographic distributions. Ecological modelling, 190(3-4):231–259, 2006.

- Pospíšil et al. (2018) L. Pospíšil, P. Gagliardini, W. Sawyer, and I. Horenko. On a scalable nonparametric denoising of time series signals. Communications in Applied Mathematics and Computational Science, 13(1):107–138, 2018.

- Rydén et al. (1998) T. Rydén, T. Teräsvirta, and S. Åsbrink. Stylized facts of daily return series and the hidden Markov model. Journal of applied econometrics, pages 217–244, 1998.

- Tibshirani (1996) R. Tibshirani. Regression shrinkage and selection via the Lasso. Journal of the Royal Statistical Society. Series B (Methodological), pages 267–288, 1996.

- Wu (2003) X. Wu. Calculation of Maximum Entropy densities with application to income distribution. Journal of Econometrics, 115(2):347–354, 2003.

- Zellner and Highfield (1988) A. Zellner and R. A. Highfield. Calculation of Maximum Entropy distributions and approximation of marginal-posterior distributions. Journal of Econometrics, 37(2):195–209, 1988.