Convergence and inference for mixed Poisson random sums

Abstract

In this paper we obtain the limit distribution for partial sums with a random number of terms following a class of mixed Poisson distributions. The resulting weak limit is a mixing between a normal distribution and an exponential family, which we call by normal exponential family (NEF) laws. A new stability concept is introduced and a relationship between -stable distributions and NEF laws is established. We propose estimation of the parameters of the NEF models through the method of moments and also by the maximum likelihood method, which is performed via an Expectation-Maximization algorithm. Monte Carlo simulation studies are addressed to check the performance of the proposed estimators and an empirical illustration on financial market is presented.

Keywords: EM-algorithm; Mixed Poisson distribution; Stability; Weak convergence.

1 Introduction

One of the most important and beautiful theorems in probability theory is the Central Limit Theorem, which lays down the convergence in distribution of the partial sum (properly normalized) of i.i.d. random variables with finite second moment to a normal distribution. This can be seen as a characterization of the normal distribution as the weak limit of such sums. A natural variant of this problem is placed when the number of terms in the sum is random. For instance, counting processes are of fundamental importance in the theory of probability and statistics. A comprehensive account for this topic is given in [11]. One of the earliest counting models is the compound Poisson process defined as

| (1) |

where is a Poisson process with rate , , and is a sequence of random variables independent of the Poisson process. Applications of the random summation (1) include risk theory, biology, queuing theory and finance; for instance, see [8], [22] and [23]. For fixed , it can be shown that the random summation given in (1), when properly normalized, converges weakly to the standard normal distribution as .

Another important quantity is the geometric random summation defined as

where is a geometric random variable with probability function and is a sequence of i.i.d. random variables independent of , for . Geometric summation has a wide range of applications such as risk theory, modeling financial asset returns, insurance mathematics and others, as discussed in [13].

In [24] it is shown that if is a positive random variable with finite mean, then converges weakly to an exponential distribution as . If the are symmetric with and finite second moment, then there exists such that converges weakly to a Laplace distribution when . If has an asymmetric distribution, it is possible to show that the geometric summation properly normalized converges in distribution to the asymmetric Laplace distribution. These last two results and their proofs can be found in [18].

The purpose of the present paper is to study the random summation with mixed Poisson number of terms. For a review about mixed Poisson distributions see [14]. In [10] it is shown that the mixed Poisson (MP) random sum converges weakly to a scale mixture of normal distributions (see [28] for a definition of such mixture) by assuming that the sequence is i.i.d. (with and ) and that there exists such that . This last assumption is necessary since the main interest in that paper is to find a Berry-Eessen type bound for the weak convergence. The study of accuracy for the convergence of MP random sums is also considered in [16], [15] and [26]. Limit theorems for random summations with a negative binomial or generalized negative binomial (which are MP distributions) number of terms, with applications to real practical situations, are addressed in [6], [27] and [17].

Our chief goal in this paper is to explore mixed Poisson random summations under different assumptions compared to those in previous works in the literature, since our aims here are also different. We assume that the number of terms follows the MP class of distributions proposed in [4] and [5]. This class contains the negative binomial and Poisson inverse-Gaussian distributions as particular cases. Further, we assume that the sequence is i.i.d. with non-null mean and finite second moment. We do not require more than finite second moment, in contrast to the work in [10]. Under these conditions, we show that the weak limit of a MP random sum belongs to a class of normal variance-mean mixtures (see [2] for a definition of this kind of distribution) driven by a latent exponential family. We call this new class of distributions by normal-exponential family (in short NEF). In particular, this class contains the normal inverse-Gaussian (NIG) distribution introduced in [2] as a special case. Therefore, this provides a new characterization for the NIG law.

Another contribution of this paper is the introduction of the new mixed Poisson stability concept, which includes the geometric stability (see [19, 21]) as a particular case. We also provide a theorem establishing a relationship between our proposed MP stability and the -stable distributions.

The statistical contribution of our paper is the inferential study on the limiting class of distributions, which is of practical interest. We propose estimation of the parameters of the NEF models through the method of moments and also by the maximum likelihood method, which is performed via an Expectation-Maximization (EM) algorithm (see [7]).

The paper is organized in the following manner. In Section 2 we show that the mixed Poisson random sums converges weakly, under some mild conditions, to a normal variance-mean mixture. Further, we define a new concept called mixed Poisson stability, which generalizes the well-known geometric stability. Properties of the limiting class of NEF distributions are explored in Section 3. Inferential aspects of the NEF models are addressed in Section 4. In Section 5 we present Monte Carlo simulations to check the finite-sample behavior of the proposed estimators. A real data application is presented in Section 6.

2 Weak convergence and stability

In this section we provide the main probabilistic results of the paper. To do this, we first present some preliminaries about the mixed Poisson distributions considered here. Then, we establish the weak convergence for mixed Poisson summations and based on this we introduce a new stability concept.

2.1 Weak limit of mixed Poisson random sums

A mixed Poisson distribution is a generalization of the Poisson distribution which is constructed as follows.

Definition 2.1.

Let be a strictly positive random variable with distribution function , where denotes a parameter associated to . We will later assume belongs to a particular exponential family of distributions. Let Poisson , for . In this case we say that follows a mixed Poisson distribution. Its probability function assumes the form

For instance, if is assumed to be gamma or inverse-Gaussian distributed, then is negative binomial or Poisson inverse-Gaussian distributed, respectively.

We consider the class of mixed Poisson distributions introduced in [5], which is defined by assuming that is a continuous positive random variable belonging to the exponential family of distributions. This family was also considered in a survival analysis context in [4]. We assume that there exist a -finite measure such that the probability density function (pdf) of with respect to is

| (2) |

where is continuous, three times differentiable and is such that and . In this case, and . For more details about this class of distributions we refer the reader to [5].

From now on we adopt the following notation: for any random variable we write for its characteristic function (). We write for belonging to the exponential family and , making clear the mixture distribution involved; we also denote when the latent variable is not important for the discussion in question. Let , where as before and when . Throughout the text will always be a sequence of random variables independent of .

Before we can state our main result we need an extra observation. In [25] the author provides a characterization of the exponential familty with a single natural parameter in terms of its characteristic function. In that paper, belongs to this family if there exists a -finite measure such that the pdf of with respect to is of the form

| (3) |

where is the support of the distribution. The following theorem appears in [25] and plays an important role in this paper.

Theorem 2.1 (Sampson, A.R.).

Let be a family of random variables such that (3) holds and . Then for the characteristic function of exists and is given by

where is the analytic extension to the complex plane of .

We are ready to state the main result of this section.

Theorem 2.2.

Let , a sequence of i.i.d. random variables with and . There exist numbers and such that

where is a random variable with

| (4) |

Proof.

First note that (2) can be written in the form of (3) by taking . It follows from Theorem 2.1 that the of is given by

| (5) |

From (5), we immediately obtain that

| (6) |

The Tower Property of conditional expectations gives

Let denote the probability generating function of . Then, we use (6) to obtain

Taking and applying L’Hôpital’s rule twice (in the second-order derivative we are using the assumption of finite variance of of the sequence ) we obtain

∎

A special case of Theorem 2.2 is obtained when the sequence of random variables has null-mean.

Corollary 2.3.

Let , a sequence of i.i.d. random variables with and . Then, , for .

Before we move on to more theoretical results, let us present a few examples.

Example 1.

If has negative binomial distribution with parameters and , then and . From Theorem 2.2, it follows that

This is the of an asymmetric Laplace distribution with parameters and , denoted here by . In other words, as .

In Example 1, we have that the density function of can be expressed in terms of the parameterization given in [18],

where is the skewness parameter.

Example 2.

We say a random variable has normal inverse-Gaussian distribution with parameters , , and , and write , if its is given by

See [2] for more details on this distribution. Now, if has Poisson inverse-Gaussian distribution with parameters and (), then and . Using again Theorem 2.2, we get

This is the of a random variable with normal inverse-Gaussian distribution with parameters , , and . Therefore, as .

The above examples provide characterizations for the Laplace and NIG distributions as weak limits of properly normalized mixed Poisson random sums.

2.2 Mixed Poisson-stability

In this section we introduce the notion of a stable mixed Poisson distribution. Our aim is to characterize such a distribution in terms of its . We start with the following definition.

Definition 2.2.

A random variable is said to be mixed Poisson stable (MP-stable) with respect to the summation scheme, if there exist a sequence of random variables , a mixed Poisson random variable independent of all , and constants , such that

| (7) |

when . If , we say is strictly mixed Poisson stable.

One of the most important objects in the theory of stable laws is the description of domains of attraction of stable laws. The definition of a domain of attraction is as follows.

Definition 2.3.

Let be a sequence of random variables with distribution function and let be the partial sums. We say that belongs to the domain of attraction of a (non-degenerate) distribution if there exist normalizing sequences () and such that

We denote .

It turns out that possesses a domain of attraction if, and only if, is a stable distribution (see Theorem 3.1, Chapter 9 in [12]). The following theorem gives a characterization of MP-stable distributions in terms of its .

Theorem 2.4.

Assume the sequence is according to Definition 2.2 and that its distribution function satisfies for some -stable distribution . Then, is PM-stable if and only if its is of the form

| (8) |

where is the of some -stable distribution.

Proof.

By Lévy’s Continuity Theorem, the convergence in Expression (7) holds if and only if

| (9) |

where . Since is invertible (which follows by the continuity assumption), (so the function is monotone increasing) and ), it follows that (9) is equivalent to

We can take the limit above with instead of ; can be seen as a subsequence. In this case, letting and , it follows that

Since the on the left hand side of is the of

and , it follows that is the of some -stable distribution (see Chapter 9 in [12] for example). Since

we have the sufficiency part of the theorem.

Conversely, if (8) holds, then is the of some -stable distribution. Therefore, there exist a random variable , an sequence of random variables and real sequences and such that

| (11) |

Denote the ch.f. of and by and , respectively. Let , . Then, the weak limit in (11) is equivalent to

From [9], we have that the above limit implies that

Since by hypothesis

we obtain that

which is equivalent to

The above limit gives Equation (9) with instead of . This completes the proof of the desired result. ∎

We now apply Theorem 2.4 to three cases of interest.

Example 3.

Take with . In this case with probability function

Also, we have and . Apply Theorem 2.4 to deduce that a random variable is NB-stable if and only if

| (12) |

where is the of some -stable distribution.

We emphasize that Theorem 2.4 generalizes Proposition 1 in [21]. To obtain their result it is enough to take in Example 3.

Example 4.

Example 5.

Consider with . In this case with probability function

where is the modified Bessel function of the third kind; see [1]. Also, we have , . Applying Theorem 2.4 we obtain that is PIG-stable if and only if , where is the of some -stable distribution.

For instance, by taking the of a normal distribution with mean and variance , that is , it follows that , which is the of the distribution. In other words, the normal inverse-Gaussian distribution is PIG-stable.

3 Properties of the limiting distribution

In this section we obtain statistical properties of the limiting class of distributions arising from Theorem 2.2 with (4). The main result here is the stochastic representation of these distributions as a normal mean-variance mixture [3] with latent effect belonging to an exponential family. We emphasize that this class of normal exponential family (NEF) mixture distributions is new in the literature.

Proposition 3.1.

Let be a random variable with (4). Then satisfies the following stochastic representation:

where and are independent and ‘’ stands for equality in distribution.

Proof.

Since we rely on an Expectation-Maximization algorithm to estimate the parameters of the class of normal mean-variance mixture distributions, the stochastic representation given in the previous proposition plays an important role in this paper. Furthermore, this representation enables us to find explicit forms for the corresponding density function as stated in the following proposition (which proof follows directly and therefore it is omitted) and examples.

Proposition 3.2.

Let with and independent, , and . The density function of is given by

| (13) |

for .

Example 6.

Let with independent of , , and . In this case, we use , and in Equation (13) to obtain

| (14) |

where is the modified Bessel function of the third kind. This function satisfies the property , for . Using this fact and replacing in Equation (14), we obtain the probability density function of the Asymmetric Laplace distribution.

Example 7.

Example 8.

Consider following a generalized hyperbolic secant distribution with dispersion parameter ; for more details on this distribution see [5]. In this case, the density function of , for , can be expressed by

where .

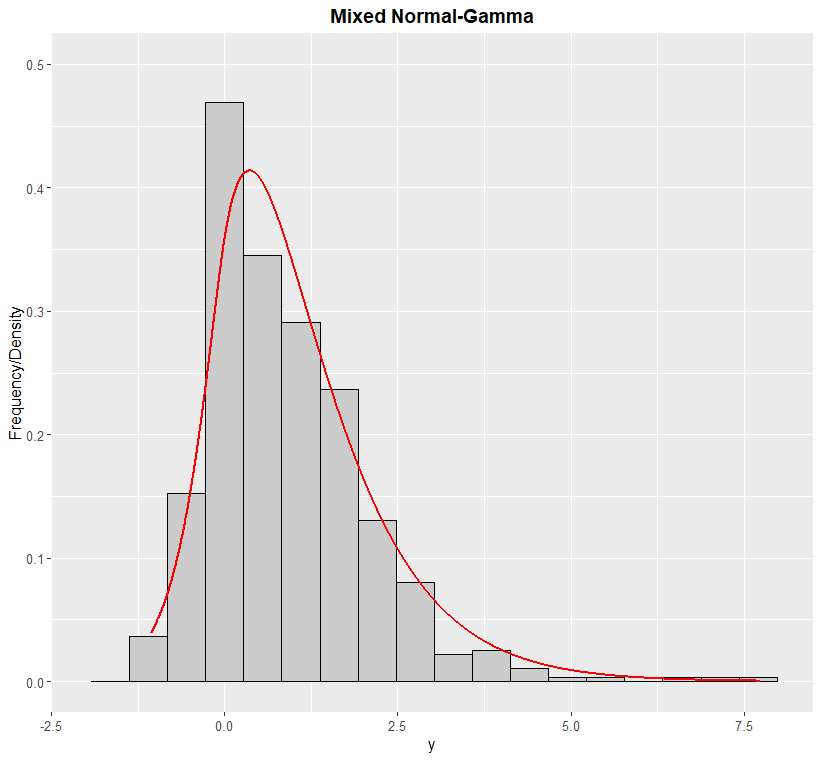

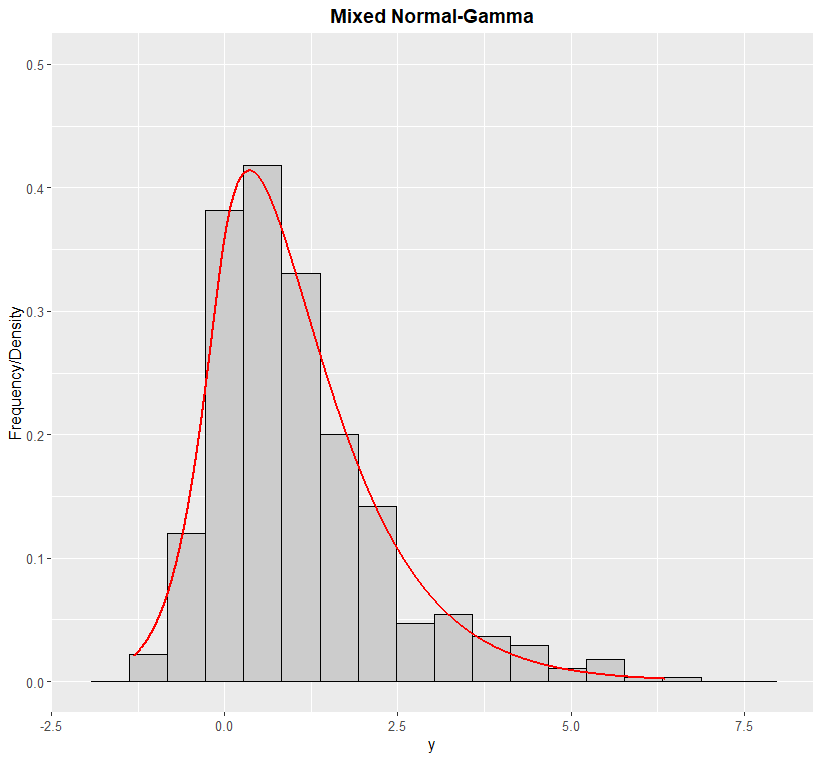

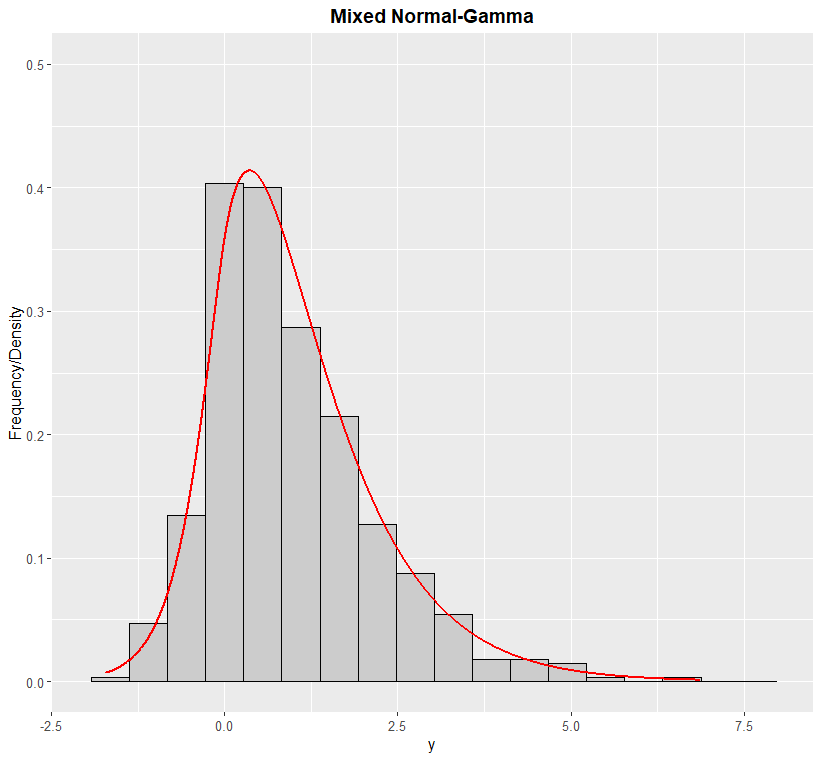

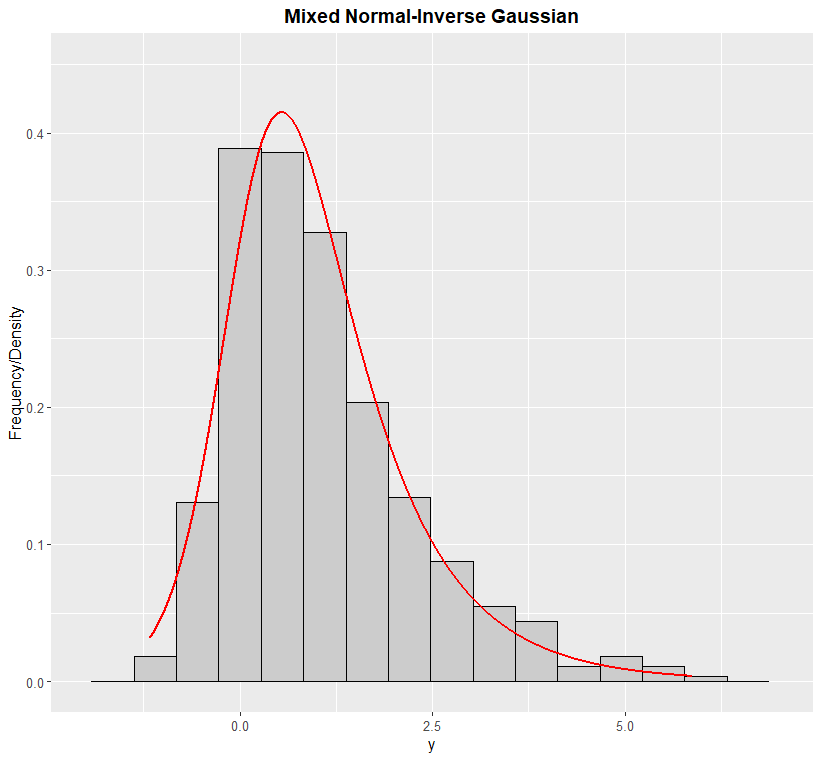

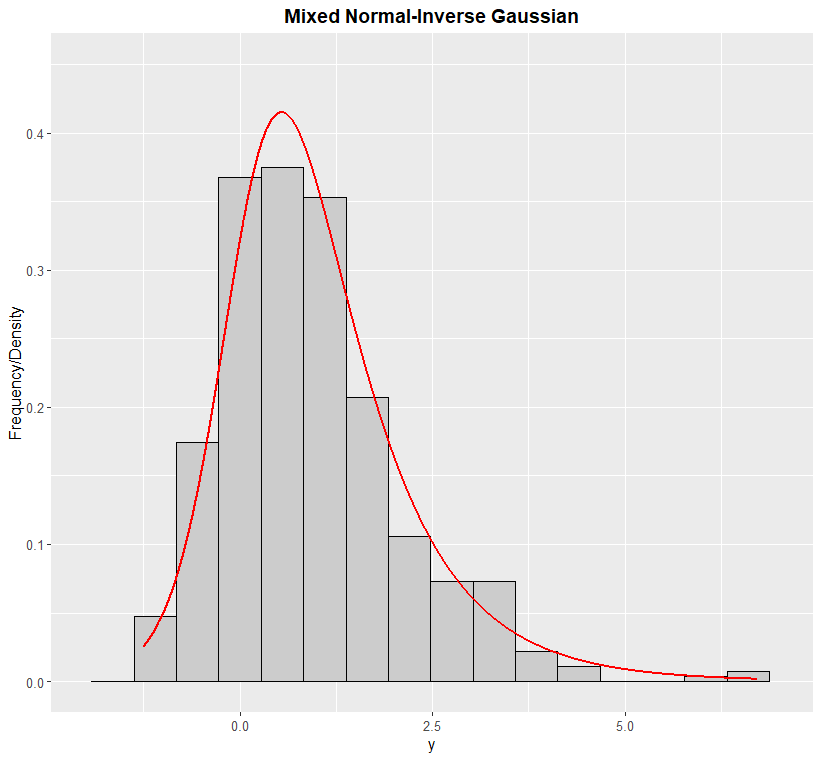

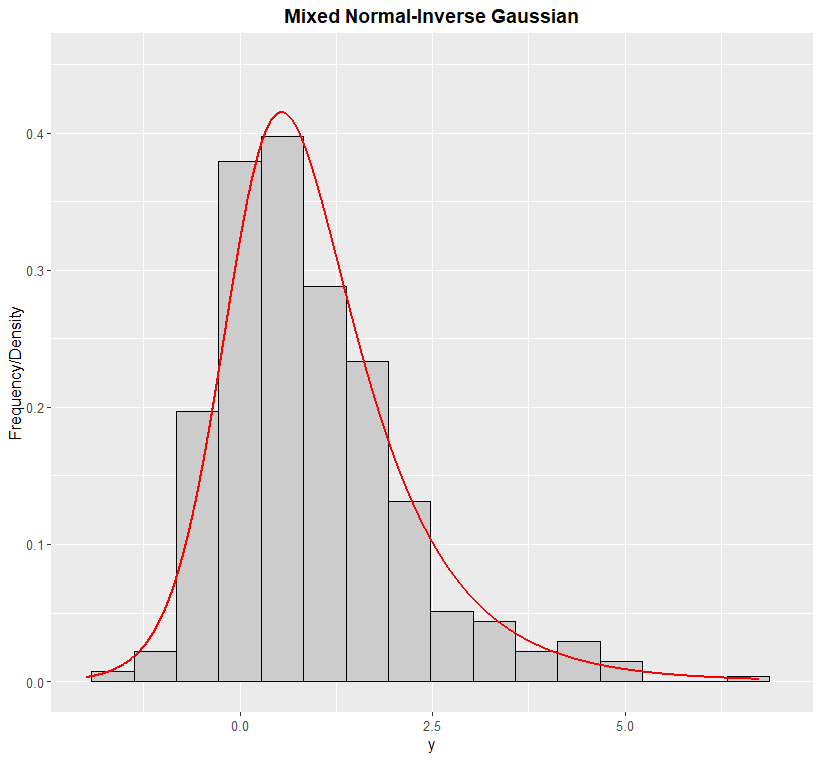

We conclude this section with a numerical illustration of the weak convergence obtained in Theorem 2.2 through a small Monte Carlo simulation. We generate random samples (500 replicas) from the partial sums with and number of terms; we set and . The sequence is generated from the exponential distribution with mean equal to 1 (in this case ). Figures 1 and 2 show the histograms of the generated random samples with the curve of the corresponding density function for the NB and PIG cases, respectively. As expected, we observe a good agreement between the histograms and the theoretical densities as increases, which is according Theorem 2.2.

4 Inference for NEF laws

In this section we discuss estimation of the parameters of the limiting class of normal-exponential family laws obtained in Section 2. We consider the method of moments and maximum likelihood estimation via Expectation-Maximization algorithm. Throughout this section, denotes a random sample (i.i.d.) from the NEF distribution and stands for the sample size.

4.1 Method of moments

Let . By using the characteristic function of the NEF distributions given in Proposition 2.2, we see that the first four cumulants of are given by

| (16) | ||||

where and are the third and forth derivatives of the function . The skewness coefficient and the excess of kurtosis, denoted respectively by and , can be obtained from the well-known relationships

| (17) |

The following examples give explicit expressions for the first four cumulants for some special cases of the NEF class of distributions.

Example 9.

Example 10.

Now consider . Then, for and . We have that follows a NIG distribution with parameters , and . Its central moments and cumulants are given by

Example 11.

For the case , it follows that for and . We have that follows a normal-generalized hyperbolic secant distribution. Its central moments and cumulants are given by

Let us discuss the estimation procedure. Since we have three parameters, we need three equations to estimate them. We use the three first moments and its respective empirical quantities to do this job, where and . The theoretical moments can be obtained from the cumulants by using the relationships , and .

By equating theoretical moments with their empirical quantities, the method of moments (MM) estimators are obtained as the solution of the following system of non-linear equations:

The solution of the above system of equations, denoted by , and , is the MM estimator and is given explicitly by

where is the admissible solution of the quadratic equation

A potential problem of the MM estimators is that estimates can lie outside of the parameter space, specially under small sample sizes. When admissible MM estimates are available, they also can be used as initial guesses for the EM-algorithm, as discussed in the sequence.

4.2 Expectation-Maximization algorithm

In this section we obtain the Expectation-Maximization (EM) algorithm to find the maximum likelihood estimators for the parameters of the model. From the stochastic representation of the NEF laws, we can use as the latent variable to construct such estimation algorithm.

Consider the complete data , where are observable variables with respective latent effects . Let be the parameter vector.

The complete log-likelihood function is , where is the density function of the exponential family given in Equation (2). From now on, we assume that the function can be expressed as , with a three times differentiable function (see [5]). For the gamma case, we have that , and . By assuming , we get , and as well.

More explicitly, we obtain that the complete log-likelihood function takes the form

We now obtain the E-step and M-step of the EM algorithm with details. We denote by the estimate of the parameter vector in the th loop of the EM-algorithm.

E-step.

Here, we need to find the conditional expectation of given the observable random variables . We denote this conditinal expectation by , which assumes the form

where , and , for .

In the following, we obtain the conditional expectations above for the gamma and inverse-Gaussian cases. For simplicity of notation, the index is omitted.

Proposition 4.1.

Assume . Then, for , we have that

where , , , , is the modified Bessel function of the third kind and denotes expecation taken with respect to the distribution of .

Proof.

We have that

By using the explicit form of the normal-gamma distribution density given in Expression (14), we get

Denoting with , and and noting that the integrand above is the kernel of a GIG density function, we obtain the desired result. ∎

Example 12.

Let with and independent of each other, , and . Replacing , and in the previous proposition, we get

and

We now present explicit expressions for the conditional expectation for the NIG case.

Proposition 4.2.

Consider . Then, for , we obtain that

where , , .

Proof.

We have that

Example 13.

By considering the NIG case and applying Proposition 4.2 with , and , we obtain

M-step.

This step of the EM-algorithm consists in maximizing the function . The score function associated to this function is

The estimate of in the th loop of the EM-algorithm is obtained as the solution of the system of equations . After some algebra, we get

where is the inverse function of .

We now describe brielfy how the EM-algorithm works. As initial guess for we can take the MM estimates. Update the conditional expectations with the previous EM-estimates, denoted by , as well as the -function. Next step is to find the maximum global point of the -function, say , which is provided in closed form above. Check if some convergence criterion is satisfied, for instance , for some small . If this criterion is satisfied, the current EM-estimate is returned. Otherwise, update the previous EM-estimate by the current one and perform the above algorithm again until convergence is achieved.

The standard error of the parameter estimates can be obtained through the observed information matrix in [20], which is given by

| (18) |

The elements of this information matrix for the NEF laws are provided in the Appendix.

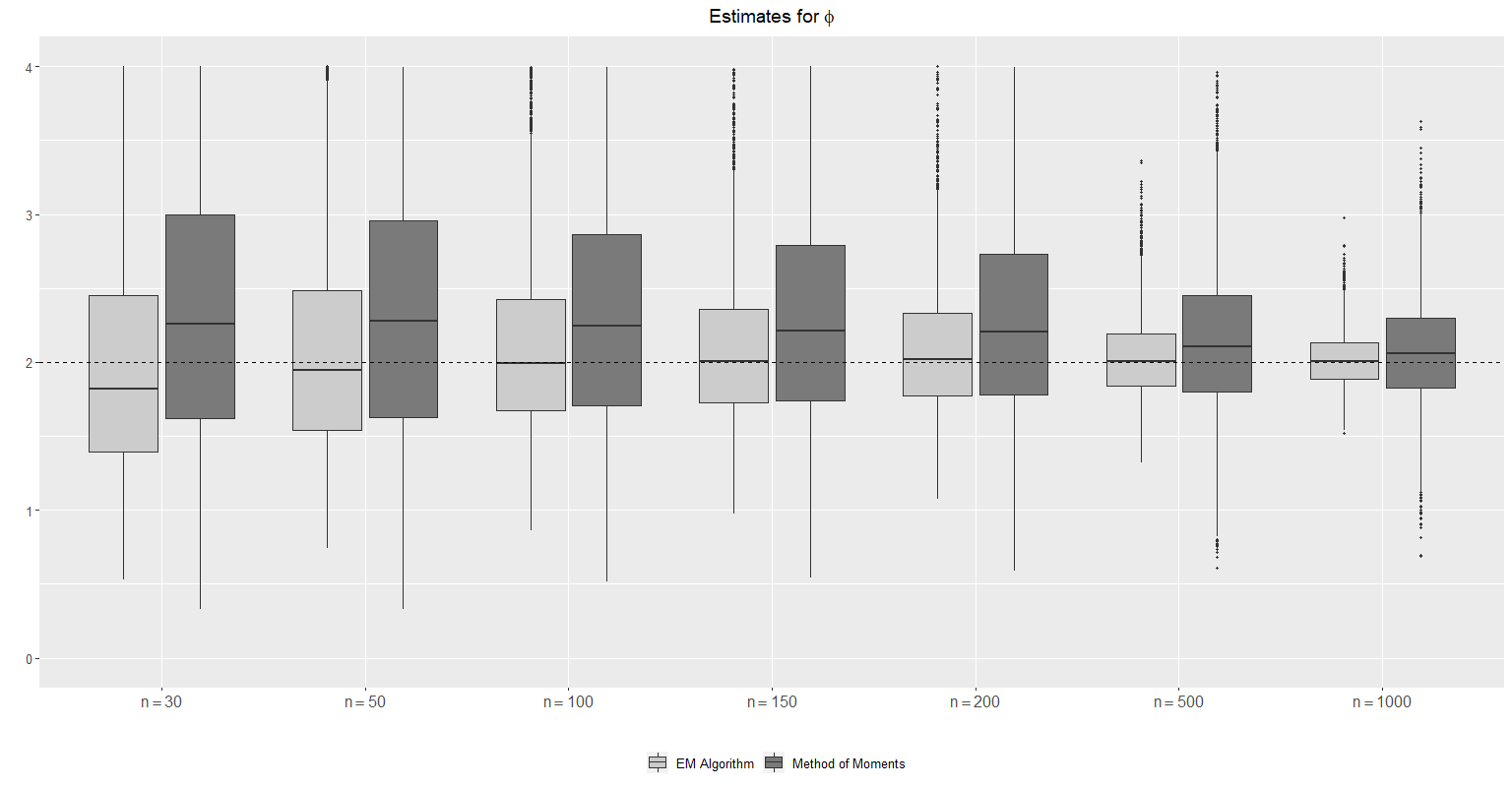

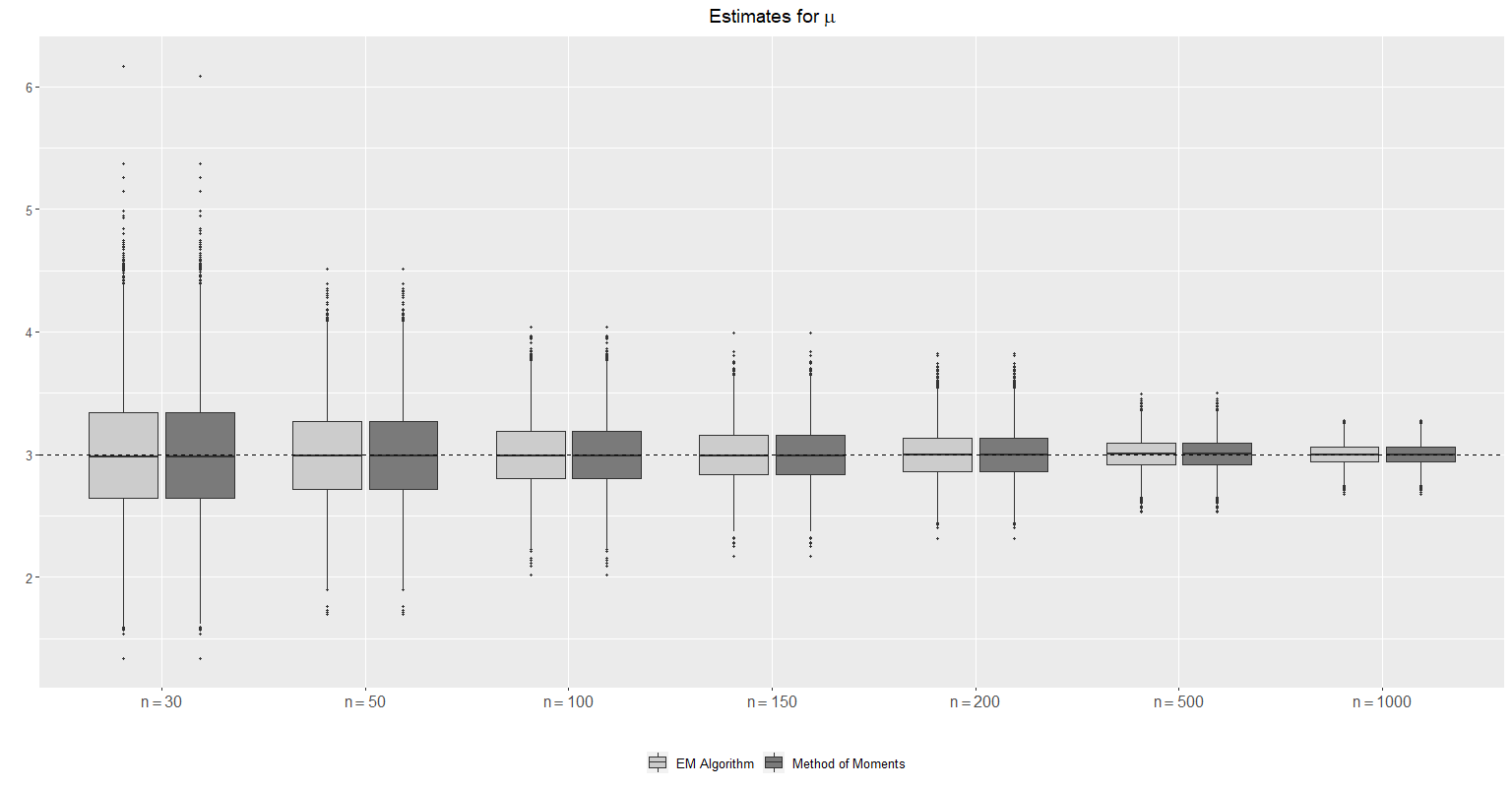

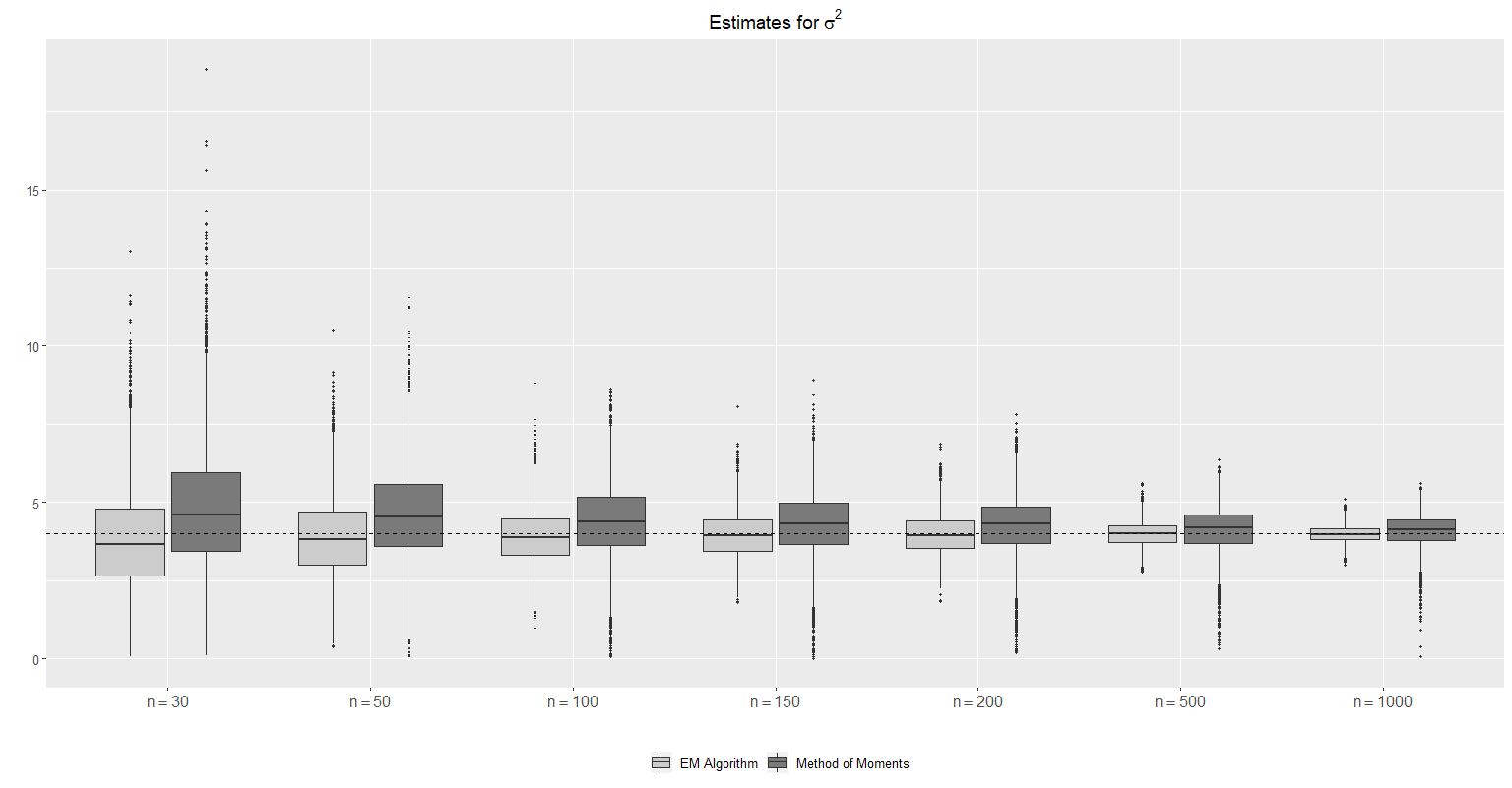

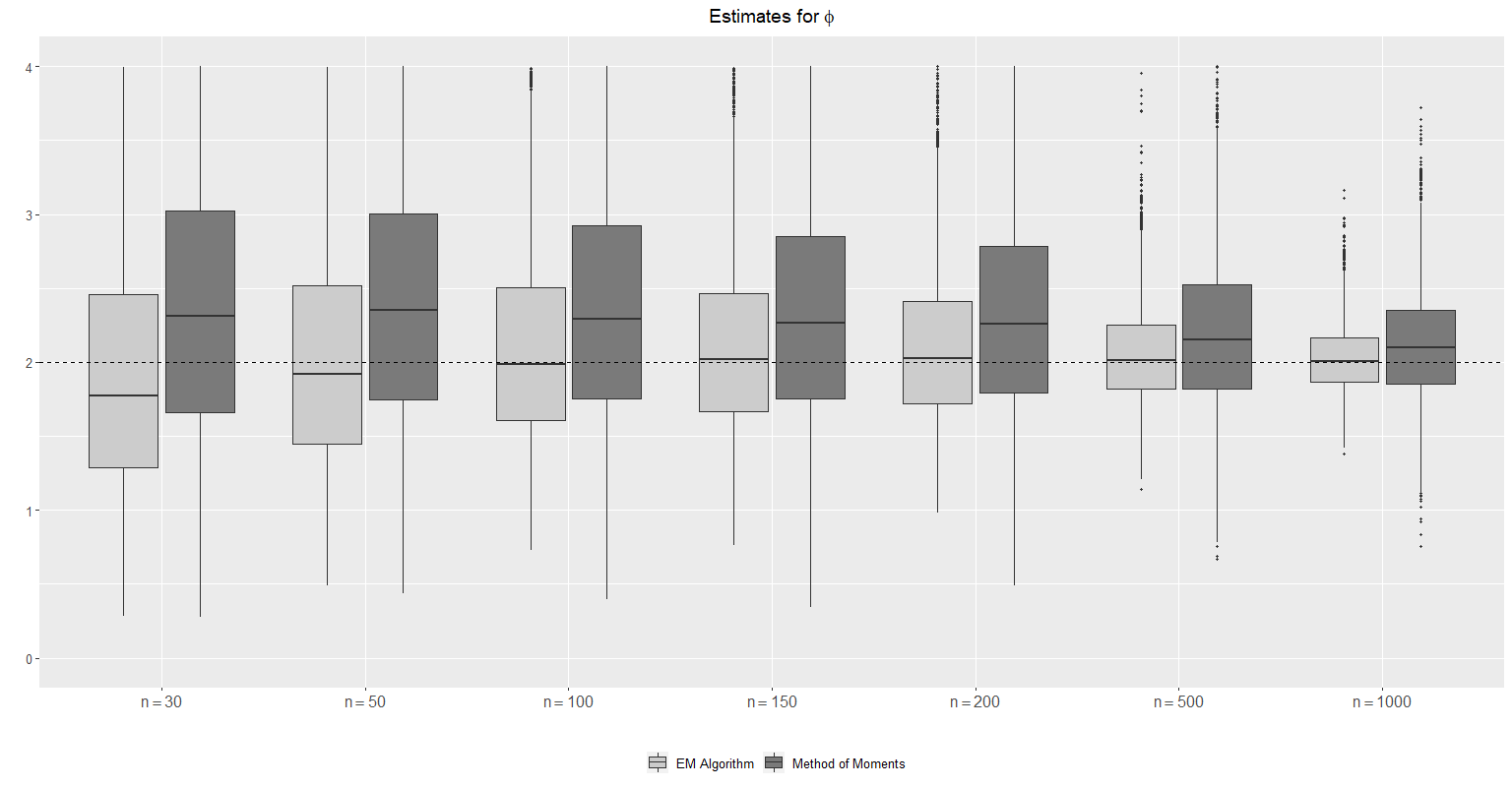

5 Simulation

In this section we present a small Monte Carlo study for comparing the performance of the EM-algorithm and the method of moments for estimating the parameters of the NEF laws. We also check the estimation of the standard errors obtained from the observed information matrix via EM-algorithm.

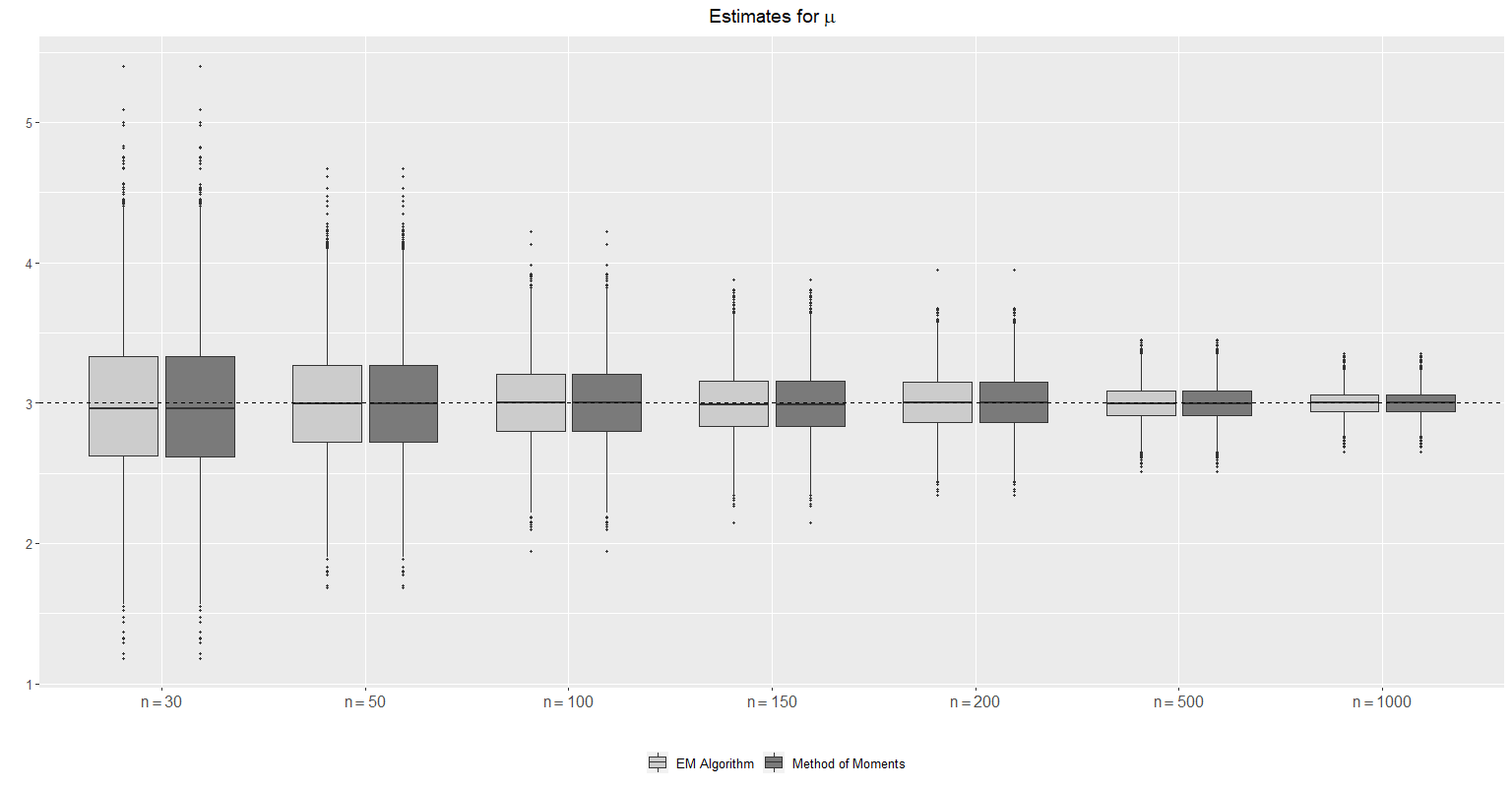

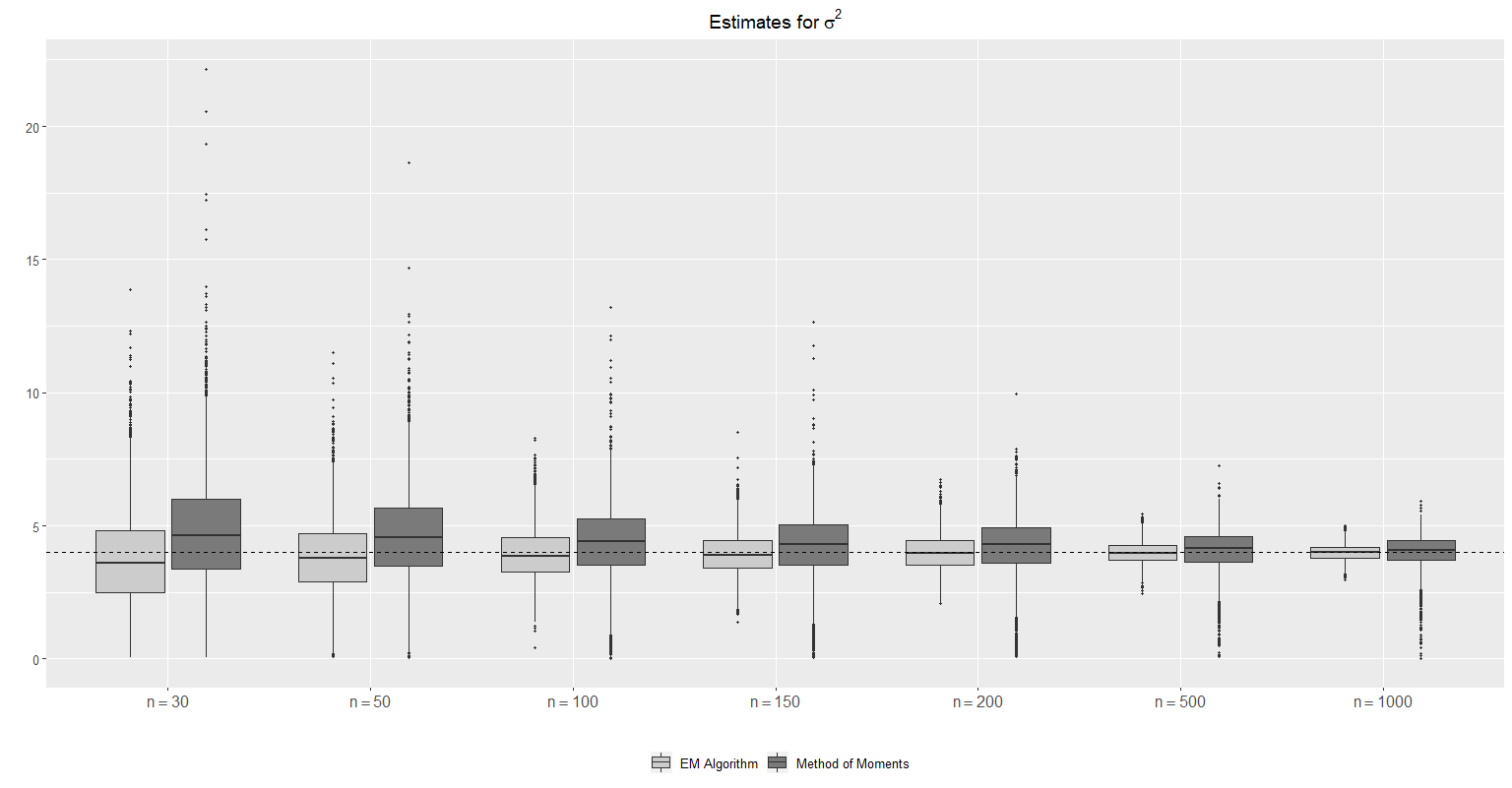

We consider the cases where data are generated from the normal-gamma and NIG distributions. To generate from these distributions, we use the stochastic representation , where independent of , which is or distributed, respectively. We set the true parameter vector and sample sizes . We run a Monte Carlo simulation with replicas. Further, we use the MM estimates as initial guesses for the EM-algorithm and consider its convergence criterion to be the one proposed in Subsection 4.2 with .

Figures 3 and 4 present boxplots of the estimates of the parameters based on the EM-algorithm and method of moments for some sample sizes under the normal gamma and NIG distributions, respectively. Overall, the bias and variance of the estimates go to 0 as the sample size increases, as expected. Let us now discuss each case with more details.

Concerning the parameter , both methods yield similar results under normal gamma and NIG assumptions. On the other hand, regarding the estimation of the parameters and , the EM-algorithm has a superior performance over the method of moments in all cases considered for both normal gamma and NIG distributions. We observe that the method of moments yields a considerable bias, even for sample sizes , in constrast with EM-approach which produces unbiased estimates even for sample sizes .

Another problem of the MM estimator is that it can produce estimates out of the parameter space. Under the normal gamma distribution, the percentages of negative estimates for and/or with sample sizes were respectively , , , , , and . The respective percentages for the NIG case were respectively , , , , , and . In these cases, the Monte Carlo replicas were discarted and new values were generated. It is worth to mention that some huge outlier estimates were yielded by the method of moments (for small sample sizes). They cannot be seen from the plots due to the scale of the boxplots, which were chosen to give a clear view of the big picture.

We finish this section by presenting the estimation of the standard errors of the EM-estimates based on the information matrix given in (18). Tables 1 and 2 show the standard error of the estimates of the parameters (empirical) and the mean of the standard errors obtained from the information matrix (theoretical) for normal gamma and NIG cases, respectively, for some sample sizes. From these tables, we observe a good agreement between the empirical and the estimated theoretical standard errors, mainly for sample sizes , for both normal gamma and NIG distributions.

| Empirical | 0.5251 | 1.7598 | 6.3974 | |

| Theoretical | 0.5227 | 1.6458 | 4.9593 | |

| Empirical | 0.4144 | 1.3670 | 3.6329 | |

| Theoretical | 0.4073 | 1.2927 | 2.1497 | |

| Empirical | 0.2937 | 0.9669 | 0.8815 | |

| Theoretical | 0.2899 | 0.9242 | 0.7585 | |

| Empirical | 0.2376 | 0.7768 | 0.6010 | |

| Theoretical | 0.2368 | 0.7533 | 0.5414 | |

| Empirical | 0.2096 | 0.6723 | 0.4754 | |

| Theoretical | 0.2056 | 0.6558 | 0.4529 | |

| Empirical | 0.1313 | 0.4195 | 0.2727 | |

| Theoretical | 0.1302 | 0.4159 | 0.2658 | |

| Empirical | 0.0910 | 0.2957 | 0.1851 | |

| Theoretical | 0.0922 | 0.2948 | 0.1846 |

| Empirical | 0.5349 | 1.6942 | 21.5352 | |

| Theoretical | 0.5287 | 1.6094 | 21.2078 | |

| Empirical | 0.4067 | 1.3139 | 11.3969 | |

| Theoretical | 0.4099 | 1.2545 | 6.1186 | |

| Empirical | 0.2890 | 0.8872 | 1.2192 | |

| Theoretical | 0.2901 | 0.8849 | 0.9936 | |

| Empirical | 0.2376 | 0.7379 | 0.7910 | |

| Theoretical | 0.2374 | 0.7280 | 0.6852 | |

| Empirical | 0.2083 | 0.6385 | 0.6106 | |

| Theoretical | 0.2057 | 0.6309 | 0.5596 | |

| Empirical | 0.1325 | 0.4013 | 0.3391 | |

| Theoretical | 0.1303 | 0.4000 | 0.3266 | |

| Empirical | 0.0903 | 0.2765 | 0.2295 | |

| Theoretical | 0.0921 | 0.2827 | 0.2254 |

6 Real data application

We here apply the NEF laws and the proposed EM-algorithm in a real data to illustrate their usefulness in practical situations. We consider daily log-returns of Petrobras stock from Jan 1st 2010 to Dec 31th 2018, which consists of 2263 observations. These data can be obtained through the website https://finance.yahoo.com/. Denote being the stock price at time and the log-return, for , where denotes the sample size; in this application, . According to [27], if is the number of market transactions in an interval of time (one day, for example), with denoting the mean number of transactions, each of these transactions have an associated return, here denoted by , which are a sequence of i.i.d. random variables with finite variance. Therefore, under these assumptions, we have that . The number of daily transactions of the Petrobras stock is high due to its liquidity, in other words, the mean number of transactions is high. This justifies the modeling of these stocks through a NEF class of distributions due to Theorem 2.2.

| Model | Estimates | ||

|---|---|---|---|

| Normal | 0.0006 (0.0007) | 0.0010 (0.0001) | |

| NG | 0.0006 (0.0006) | 0.0009 (0.0001) | 1.3105 (0.1105) |

| NIG | 0.0006 (0.0006) | 0.0010 (0.0001) | 0.8201 (0.1161) |

Table 3 shows the maximum likelihood estimates of the parameters based on the normal distribution and the EM-estimates for the normal gamma and NIG models. The standard errors are also provided in this table. All models provide similar estimates for the mean and scale parameters as expected. We emphasize that the parameter controls the departure from the normal distribution. By taking , we obtain the normal law as a limiting case of the NEF class. The estimates for this parameter under both normal gamma and NIG models indicate some departure from the normal distribution.

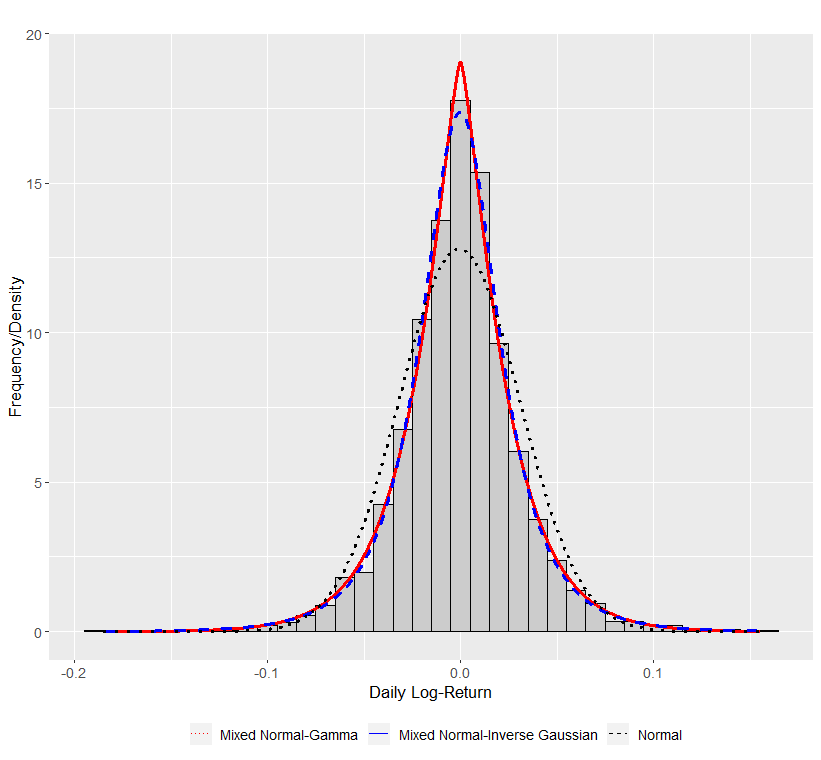

This comment is better supported by Figure 5, which provides the histogram of the data with the estimated densities of the normal, normal gamma and NIG laws. We can observe that the normal gamma and NIG densities capture well the peak, in contrast with the normal density.

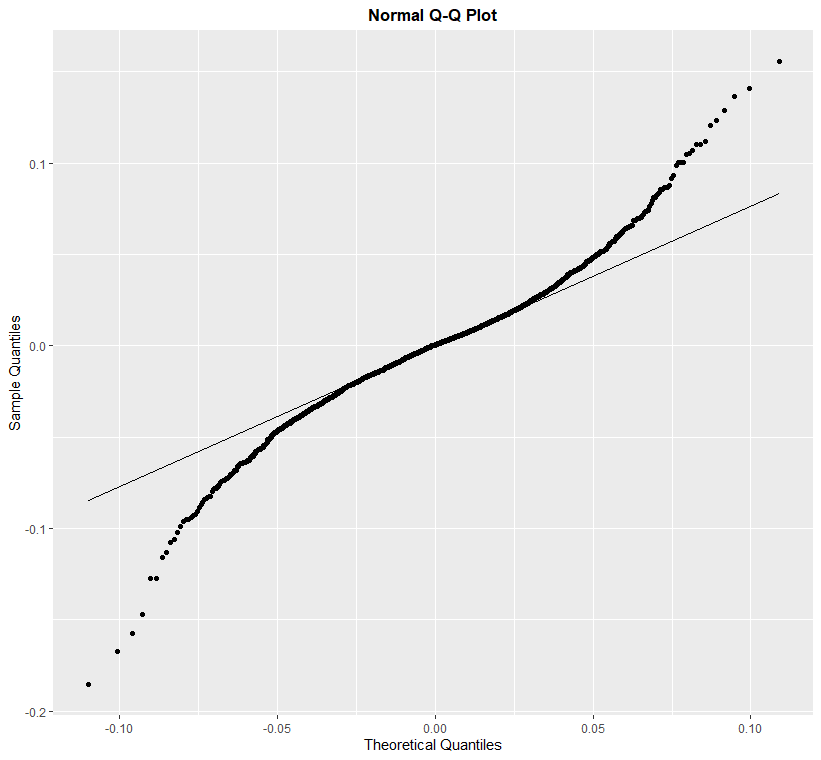

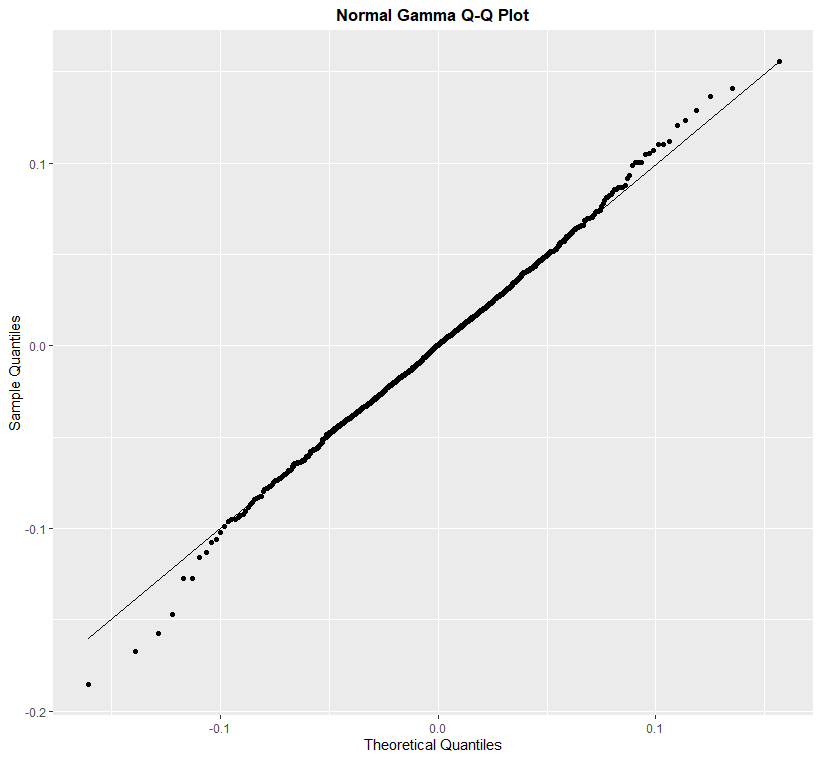

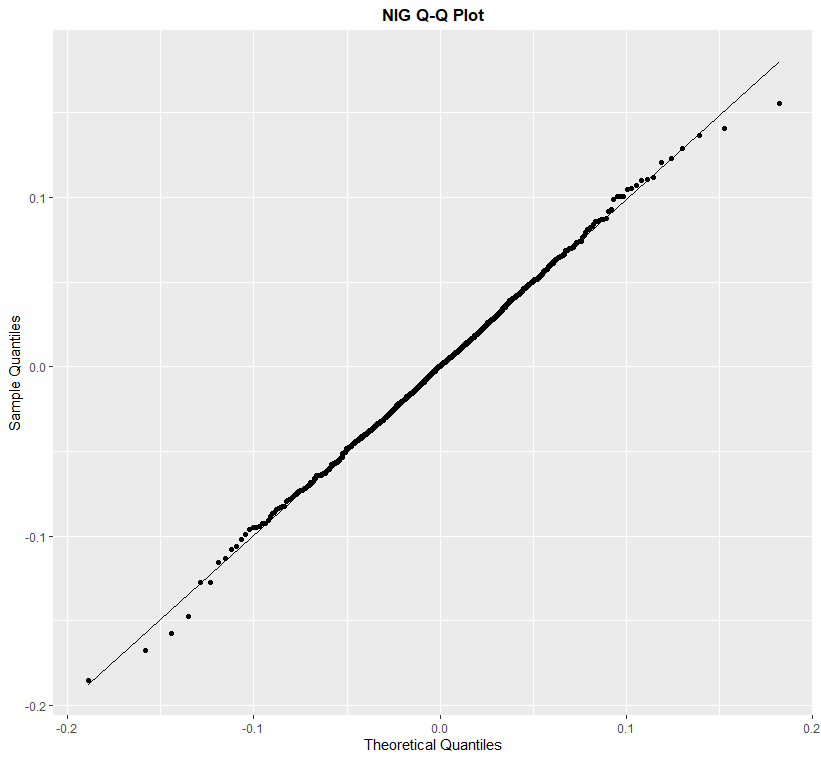

To check goodness-of-fit of the models, we consider qq-plots, which consist in plotting the empirical quantiles against the fitted ones. A well-fitted model provides a qq-plot looking like a linear function . Figure 6 exhibits the qq-plots based on the normal, NG and NIG fitted models. From this figure, we clearly observe that the normal distribution is not suitable for modeling the log-returns, which was already expected. We also notice that both NG and NIG models provide satisfactory fits, being the last one capturing better the tails. We stress that the modeling of tails is an important task in the study of financial data. For this particular dataset presented in this section, we recommend the use of the NIG law.

References

- [1] Abramowitz, M. and Stegun, I.A., Handbook of Mathematical Functions. Dover Publications, New York, 1965.

- [2] Barndorff-Nielsen, O.E., Normal inverse gaussian distributions and stochastic volatility modelling. Scandinavian Journal of Statistics. 24, 1-13, 1997.

- [3] Barndorff-Nielsen, O.E., Kent, J. Sørensen, M., Normal variance-mean mixtures and z distributions. International Statistical Review. 50, 145-159, 1982.

- [4] Barreto-Souza, W., Long-term survival models with overdispersed number of competing causes. Computational Statistics and Data Analysis. 91, 51-63, 2015.

- [5] Barreto-Souza, W. and Simas, A.B., General mixed Poisson regression models with varying dispersion. Statistics and Computing. 26, 1263-1280, 2016.

- [6] Bening, V.E. and Korolev, V.Yu., On an application of the Student distribution in the theory of probability and mathematical statistics. Theory of Probability and its Applications. 49, 377-391, 2005.

- [7] Dempster, A.P. Laird, N.M. and Rubin, D.B., Maximum likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society - Series B. 39, 1-38, 1977.

- [8] Embrechts, P., Kluppelberg, C. and Mikosch, T., Modelling Extremal Events for Insurance and Finance. Springer, Berlin, 2003.

- [9] Feller, W., An Introduction to Probability Theory and its Applications vol. 2, 2nd edition. Wiley, New York, 1971.

- [10] Gavrilenko, S.V. and Korolev, V.Yu., Convergence rate estimates for mixed Poisson random sums. Sistemy i Sredstva Informatiki. special issue, 248-257, 2006.

- [11] Gnedenko, B.V. and Korolev, V.Yu., Random Summation: Limit Theorems and Applications. Boca Raton, FL: CRC Press, 1996.

- [12] Gut, A., Probability: A Graduate Course. New York, Springer, 2013.

- [13] Kalashnikov, V., Geometric Sums: Bounds for Rare Events with Applications, Kluwer Acad. Publ., Dordrecht, 1997.

- [14] Karlis, D. and Xekalaki, E., Mixed Poisson distributions. International Statistical Review. 73, 35-58, 2005.

- [15] Korolev, V.Yu. and Dorofeeva, A., Bounds of the accuracy of the normal approximation to the distributions of random sums under relaxed moment conditions. Lithuanian Mathematical Journal. 57, 38-58, 2017.

- [16] Korolev, V.Yu. and Shevtsova, I.G., An improvement of the Berry-Esseen inequality with applications to Poisson and mixed Poisson random sums. Scandinavian Actuarial Journal. 2012, 81-105, 2012.

- [17] Korolev, V.Yu. and Zeifman, A., Generalized negative binomial distributions as mixed geometric laws and related limit theorems. Lithuanian Mathematical Journal. 59, 366-388, 2019.

- [18] Kotz, S., Kozubowski, T. and Podgorski, K, The Laplace Distribution and Generalizations: A Revisit with Applications to Communications, Economics, Engineering, and Finance. Springer, 2001.

- [19] Kozubowski, T.J. and Rachev, S.T., The theory of geometric stable distributions and its use in modeling financial data. European Journal of Operational Research. 74, 310-324, 1994.

- [20] Louis, T.A., Finding the observed information matrix when using the EM algorithm. Journal of the Royal Statistical Society - Series B. 44, 226-233, 1982.

- [21] Mittnik, S. and Rachev, S.T., Alternative multivariate stable distributions and their applications to financial modeling. In Stable Processes and Related Topics, 9-13, 1990.

- [22] Paulsen, J., Ruin models with investment income. Probability Surveys. 5, 416-434, 2008.

- [23] Puig, P. and Barquinero, J.F., An application of compound Poisson modelling to biological dosimetry. Proceedings of the Royal Society A. 467, 897-910, 2010.

- [24] Rényi, A., A characterization of the Poisson process. Translated in: P. Turan, ed., Selected Papers of Alfréd Rényi, Vol. I (Akad. Kiado, Budapest, 1976), 622-628, 1956.

- [25] Sampson, A.R., Characterizing exponential family distributions by moment generating functions. Annals of Statistics. 3, 747-753, 1975.

- [26] Shevtsova, I.G., Convergence rate estimates in the global CLT for compound mixed Poisson distributions. Theory of Probability and its Applications. 63, 72–93, 2018.

- [27] Schluter, C. and Trede, M., Weak convergence to the Student and Laplace distributions. Journal of Applied Probability. 53, 121-129, 2016.

- [28] West, M., On scale mixtures of normal distributions. Biometrika. 74, 646-648, 1987.

Appendix

Define the conditional expectations , , , , , , and , for .

The elements of the observed information matrix are given by the following expressions:

and

We now provide explicit expressions for the conditional expectations involved in the information matrix for the normal gamma and NIG cases. We omit the index to simplify the notation.

Example 14.

Let be a normal gamma distribution with parameters , , with associated latent factor . Define and . Then, we have that

and

Example 15.

For the NIG case, the conditional expectations assume the forms

and