Modality for Scenario Analysis and Maximum Likelihood Allocation

Abstract

We study the variability of a risk from the statistical viewpoint of multimodality of the conditional loss distribution given that the aggregate loss equals an exogenously provided capital. This conditional distribution serves as a building block for calculating risk allocations such as the Euler capital allocation of Value-at-Risk. A superlevel set of this conditional distribution can be interpreted as a set of severe and plausible stress scenarios the given capital is supposed to cover. We show that various distributional properties of this conditional distribution, such as modality, dependence and tail behavior, are inherited from those of the underlying joint loss distribution. Among these properties, we find that modality of the conditional distribution is an important feature in risk assessment related to the variety of risky scenarios likely to occur in a stressed situation. Under unimodality, we introduce a novel risk allocation method called maximum likelihood allocation (MLA), defined as the mode of the conditional distribution given the total capital. Under multimodality, a single vector of allocations can be less sound. To overcome this issue, we investigate the so-called multimodalty adjustment to increase the soundness of risk allocations. Properties of the conditional distribution, MLA and multimodality adjustment are demonstrated in numerical experiments. In particular, we observe that negative dependence among losses typically leads to multimodality, and thus a higher multimodality adjustment can be required.

JEL classification: C02, G32

Keywords: Risk allocation, Scenario analysis, Variability measure, Conditional distribution, Unimodality, Mode

1 Introduction

Risk allocation concerns the quantification of the risk of each unit of a portfolio. For a -dimensional portfolio of risks or losses represented by an -valued random vector , , the overall loss is covered by a total capital , which is typically determined as for a risk measure . The Euler principle, proposed in Tasche, (1995), is one of the most well-known rules of risk allocation. It is economically justified, for example, in Tasche, (1995) and Kalkbrener, (2005), and the derived allocated capital is also known as the Aumann-Shapley value (Aumann and Shapley,, 2015) in cooperative game theory; see Denault, (2001).

The Euler principle is applicable when the total capital is determined by a risk measure via . However, as pointed out by Asimit et al., (2019), the total capital in practice may not always coincide with the risk measure itself but includes various adjustments such as stress scenarios and liquidity adjustments. In such cases, the capital does not possess the original meaning as a risk measure and the formula under the Euler principle is not straightforwardly applicable. In addition, there are situations when the total capital is given exogenously as a constant; see Laeven and Goovaerts, (2004). For the case when the total capital is regarded as a constant, various allocation methods have been proposed in the literature. One of the main streams found, for example, in Laeven and Goovaerts, (2004) and Dhaene et al., (2012), is to derive an allocation as a minimizer of some loss function over a set of allocations . Another method is to find a confidence level for which the corresponding risk measure coincides with , and then allocate by regarding it as measured by a risk measure. For example, if Value-at-Risk (VaR) or Expected Shortfall (ES) are chosen as risk measures, confidence levels are first found such that or, respectively, hold for a given total capital . After performing this procedure, the Euler principle becomes applicable and the resulting allocated capital of to the th risk is or, respectively, ; see Section 2.1 for details.

Although these methods provide plausible risk allocations, they sometimes ignore important distributional properties of related to the soundness of risk allocations and to risky scenarios expected to be covered by the allocated capitals. As we will see in Section 2.2, most allocation methods provide the homogeneous allocation when is exchangeable in the sense that for any permutation of . This homogeneous allocation can be sound when the conditional distribution of in a stressed situation is unimodal with the mode since this homogeneous allocation covers the risky scenario most likely to occur in a stressed situation. On the other hand, the same allocation is derived when the conditional distribution in a stressed situation is multimodal and is supposed to cover multiple risky scenarios on average. In this multimodal case, the homogeneous allocation can be less sound than in the former unimodal case since multiple risky scenarios are hidden in a single vector of allocations. Therefore, the soundness of risk allocations depends on the distributional properties of the conditional distribution of in a stressed situation. In the multimodal case, imposing a multimodality loading to the capital can be required to take the variability of scenarios into account.

In this paper, we study the variability of a risk from the statistical viewpoint of multimodality of the conditional distribution of given . Since takes values in , this random vector serves as a building block for deriving risk allocations. For example, the Euler allocation of , , arises as the expectation of with . In addition, we show in Section 2.2 that a superlevel set of can be regarded as a set of severe and plausible stress scenarios the given capital is supposed to cover. Based on the motivation provided there, we investigate distributional properties of in Section 3. We show that unimodality, dependence and tail behavior of are typically inherited from those of the underlying unconditional loss , respectively. Moreover, we demonstrate in Section 5.2 that negative dependence among typically leads to multimodality of . These observations can be useful to detect the hidden risk of multimodality in risk allocation. The properties of studied in this paper are of potential importance in simulation and statistical inference of using Markov chain Monte Carlo (MCMC) methods for efficiently simulating the distribution of interest; see Remark 2 and Appendix F.

We also propose a novel risk allocation method termed maximum likelihood allocation (MLA), which is defined as the mode of assuming that it is unimodal. Besides the mean (which leads to the Euler allocation of VaR), the mode is also an important summary statistics of . It can be interpreted as the risky scenario most likely to occur in the stressed situation . By searching for the global mode of , possibly multiple local modes can be detected. As explained in Section 2.2, this procedure of detecting multimodality is beneficial for evaluating the soundness of risk allocations, for discovering hidden multiple scenarios likely to occur in the stressed situation and for constructing more flexible risk allocations by weighting important scenarios. In Section 4.1 we present a definition and properties of MLA expected to hold for a risk allocation. In Section 4.2 we introduce the so-called multimodality adjustment to increase the soundness of risk allocations when is multimodal. The multimodality adjustment can be regarded as a measure of variability of the underlying risk; see Furman and Landsman, (2006) and Furman et al., (2017) for studies of variability measures of tail risk. MLA and multimodality-adjusted allocated capitals are estimated and compared with Euler allocations in numerical experiments in Section 5. Concluding remarks are given in Section 6 and all proofs can be found in Appendix A.

2 Preliminaries

2.1 A brief introduction to capital allocation

On a standard atomless probability space , let , be a -dimensional random vector with joint distribution function with margins and a copula . Furthermore, let and denote by its distribution function. If and have densities, we denote them by and , respectively, with marginal densities of and copula density . The variable is interpreted as loss of the th asset, business line, economic entity and so on, of the portfolio in a fixed period of time. Similarly, is regarded as the aggregate risk of the portfolio . Positive values of and are understood as losses and negative values are interpreted as profits.

The amount of total capital required to cover the risk of the portfolio is often determined as where is a risk measure, that is, a map from a set of random variables to a real number. Examples of risk measures include Value-at-Risk (VaR) at confidence level defined by

for a random variable on and its distribution function , and Expected Shortfall (ES) at confidence level , also known as Conditional VaR, Tail VaR and Average VaR, defined by

provided that .

Once the total capital is determined as , it is decomposed into real numbers such that the full allocation property

| (1) |

holds. The set of all possible allocations is denoted by

If for a positive homogeneous risk measure , the so-called Euler principle determines the th allocated capital by

provided that the partial derivative exists; see Tasche, (2001) for more details on the differentiability argument. The Euler principle leads to the VaR contributions and ES contributions given by

| (2) |

and

| (3) |

respectively.

We consider the case when the capital is an exogenously given constant . Our proposed risk allocation introduced in Section 4 is based on the conditional distribution

| (4) |

The conditional distribution (4) is degenerate and its first components determine the last one via . Therefore, it suffices to consider the -dimensional marginal distribution . Note that throughout this paper, the ′-notation is used to denote quantities related to this non-degenerate distribution in dimensions and should not be confused with matrix transposition for which we will use the ⊤-symbol. Assuming that and admit densities, also has a density and is given by

| (5) |

where the last equality follows from an affine transformation with unit Jacobian.

2.2 A motivating example

The distribution of is a primary subject in this paper. In this section, we provide a motivating example for investigating this distribution from the viewpoint of risk alloation.

2.2.1 Soundness of risk allocations

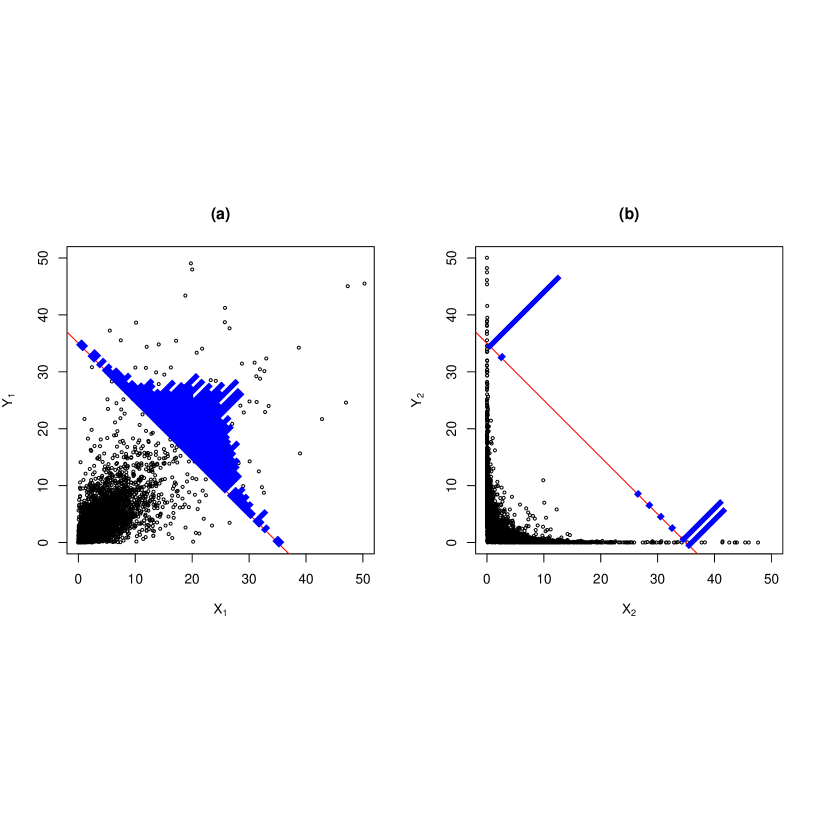

Consider two bivariate risks (a) and (b) such that all of and identically follow Pareto distributions with shape parameter 3 and scale parameter 5, and and have Student copulas and , respectively, where is the degrees of freedom parameter and and are the correlation parameters. Suppose that the exogenously given total capital equals . By exchangeability of the risk models (a) and (b), most allocation rules provide the homogeneous allocation in both cases (a) and (b). For instance, if is regarded as VaR or ES at some confidence levels and is allocated according to the Euler principle, then both VaR and ES contributions lead to homogeneous allocations. As we see in Figure 1, however, the conditional distributions of and of on the set of allocations differ substantially. Positive dependence among and prevents the two random variables from moving in opposite directions under the constraint , which results in unimodality of the conditional distribution on . On the other hand, negative dependence among and allows them to move in opposite directions, which leads to bimodality of the conditional distribution. From the viewpoint of risk management, the homogeneous allocation seems to be a more sound capital allocation in Case (a) because it covers the most likely risky scenario. In Case (b), the two risky scenarios around the corners and occur equally likely and the allocation can be understood as an average of these scenarios. However, the likelihood around is quite small and a single vector of the equal allocation obscures the two distinct risky scenarios. Moreover, either of or is likely to suffer a large amount of loss if is reserved as capital. Consequently, the soundness of the allocated capital depends on the modality of the conditional loss distribution, and multiple risky scenarios can be hidden in a single vector of risk allocations

Remark 1 (Multimodality and variability).

Models (a) and (b) may not be directly comparable since the total capital for Model (b) is typically smaller than that for Model (a). However, the variability of a risk under Model (b) is larger than under Model (a) in the sense that a wider variety of scenarios are likely to occur under Model (b) than under Model (a). Therefore, if the total capital does not incorporate the variability of a risk, an adjustment of may be required to take the multimodality of scenarios into account.

2.2.2 Stress testing of risk allocations

Inspecting modes of can also be regarded as a stress test of risk allocations. Breuer et al., (2018) requires stress scenarios to be severe and plausible. We define the scenario set with a level of plausibility by where is the density function of assuming that it exists. Among the scenario set , the set can be regarded as the set of the most severe scenarios the given total capital can cover. Using the convention , , the set leads to the superlevel set of with level since

Throughout the paper, the superlevel set of is treated as a set of stress scenarios. In particular, the modes of are the most severe and plausible scenarios that can cover since they attain the highest level of plausibility among the stress scenarios. Unimodality of (see Definition 1 for its formal definition) implies that there exists one representative stress scenario the total capital can cover, and thus the mode can be a sound risk allocation covering the risky scenario most likely to occur. On the other hand, multimodality of means that there are multiple distinct stress scenarios that are severe and plausible, and thus it may not be sufficient to only focus on a single scenario without identifying the other ones.

Remark 2 (Simulation of with MCMC methods).

Another motivation for investigating distributional properties of is an efficient simulation of this conditional distribution. This is a challenging task in general since there is no general and tractable sampling method known for . Although samples from can be generated by first simulating and then extracting those satisfying the constraint , the probability is zero, and thus such samples virtually never exist when admits a density. A potential remedy for this problem is to modify the conditioning set to for a small so that . However, this modification distorts the distribution of and the resulting estimates of risk allocations suffer from inevitable biases. To overcome this issue, Koike and Minami, (2019) and Koike and Hofert, (2020) proposed MCMC methods for exact simulation from . Although MCMC methods improve sample efficiency and the resulting estimates are unbiased, their performance highly depends on distributional properties of , in particular on its modality and tail behavior; see Appendix F for more details. From this viewpoint, investigating properties of is of potential importance to construct efficient MCMC methods for simulating .

3 Properties of the conditional distribution given a constant sum

In Section 2.2, we showed that the conditional distribution of given a constant sum plays an important role in risk allocations. With this motivation in mind, we study the support, modality, dependence and tail behavior of in this section. As introduced in Section 2.1, we consider the -dimensional random vector for to avoid the degeneracy of .

3.1 Support of

We start with the support of . Assuming that admits a density , Equation (5) implies that

Therefore, if are supported on , then . Another typical case is when for some , which implies that are bounded from below, that is, -almost surely (a.s.), for . In this case, the support of is given by

| (6) |

If , that is, when models the nonnegative part of losses, then the closure of (6) is known as the -simplex. Since the set in (6) is bounded, simulation of can be more straightforward than in the former case when . For instance, an independent Metropolis-Hastings (MH) algorithm can be applied by first generating a sample uniformly on the set in (6) and then replacing the current state with the new state with probability .

3.2 in the elliptical case

Elliptical distributions are important exceptions for which the distribution of can be derived explicitly. See Chapter 6 of McNeil et al., (2015) for applications of elliptical distributions to risk management. Throughout this work, the set of all positive definite matrices is denoted as . The characteristic function of a random vector is given by , . If a function is such that is a -dimensional characteristic function, then is called a characteristic generator; see Fang, (2018) for details. Let denote the class of all characteristic generators. A -dimensional random vector is said to have an elliptical distribution, denoted by , if its characteristic function can be expressed as

for a location vector , dispersion matrix and a characteristic generator . When an elliptical distribution admits a density function, it is of the form

for some normalizing constant and a density generator satisfying

see Fang, (2018). We omit the second argument and write when it can be ignored.

In the following proposition we derive the distribution of provided that .

Proposition 1 (Ellipticality of ).

Suppose . Then follows an elliptical distribution for some characteristic generator ,

| (7) |

where and are the first -components of and , respectively, is the principal submatrix of deleting the th row and column, and . Furthermore, if admits a density with density generator , then admits a density with density generator

| (8) |

Note that the characteristic generator of is in general different from that of ; see the proof in Appendix A. By Proposition 1, ellipticality is preserved under conditioning and thus a change of the shape of the distribution as observed in Figure 1 (b) does not occur when is elliptical. The capital is typically much larger than the mean of the total loss in practice. Therefore, by (8), the density generator is typically the tail part of the generator . Moreover, the location vector typically increases in proportion to the sum of covariances . As a consequence, more (less) capital is assigned to losses which are positively (negatively) correlated with the other losses. On the other hand, the dispersion matrix decreases in proportion to the term and the reduction depends on the variance of the sum.

Example 1 (Student distribution).

A -dimensional Student distribution is an elliptical distribution with density generator

| (9) |

where is the degrees of freedom parameter. It is known, for example, from Roth, (2012) and Ding, (2016) that the conditional distribution of the Student distribution is again Student . We can check this closedness property with Proposition 1. By (8), the random variable follows an elliptical distribution with density generator (up to a constant) given by

for which the corresponding distribution is known as the Pearson type distribution; see Schmidt, (2002). In fact, this distribution reduces to a -dimensional Student distribution since

and the multiplier can be absorbed by redefining the dispersion matrix as for . Consequently, follows . Since the degrees of freedom of increases by , has slightly lighter tails than .

3.3 Unimodality of

Next we study the modality of . Among various definitions of unimodality considered in the literature, we adopt those defined based on the superlevel set

where is a density on which is assumed to be bounded for simplicity so that exists. By definition, is a decreasing set, that is, for . We also write for if has density . A set is called star-shaped about if, for any , the line segment from to is in .

Definition 1 (Concepts of unimodality).

For a bounded density function on , we call the mode set of for . If then we call the mode of . Furthermore, is said to be weakly unimodal if is connected, star unimodal about the center if is star-shaped about and convex unimodal if is convex, for all . Finally, is said to be multimodal if is not connected for some .

From Definition 1, convex unimodality implies star unimodality and star unimodality implies weak unimodality. Other notions of unimodality, such as block unimodality, linear unimodality, monotone unimodality, -unimodality, orthounimodality and Khinchin’s unimodality are not introduced in this paper due to their intractability for our purpose; see Dharmadhikari and Joag-Dev, (1988) for a comprehensive discussion on unimodality. As mentioned in Section 2.2, can be understood as a plausible scenario set with being the level of plausibility. In addition, can be regarded as a set of severe and plausible stress scenarios the total capital is supposed to cover. From these interpretations, we believe that the notion of unimodality should describe tractability of these scenario sets, such as connectivity and convexity. The superlevel set can also be important when is simulated with MCMC methods since the ratio of levels of is a primary quantity of interest for such methods. MCMC methods are required to be specifically designed when is not connected since in this case a Markov chain needs to traverse distinct regions to simulate samples from the entire space.

Note that uniqueness of the maximum of a density , that is, the mode set of being a singleton for , is an important but different concept of unimodality from those in Definition 1. In fact, uniqueness of the maximum may not be an appropriate concept of unimodality when the relationship between and is of interest. This is because the uniqueness of the maximum of is equivalent to that of on the restricted domain via (5), and thus the uniqueness of the maximum of on the entire support does not provide any information on the shape of on unless the mode of on is in .

The following proposition reveals some relationships between unimodality of and that of .

Proposition 2 (Unimodality of ).

-

1.

Suppose admits a density with density generator . If is decreasing on , then is convex unimodal. Furthermore, if the equation of has a unique solution , then has the mode .

-

2.

If is convex unimodal, then is convex unimodal.

Unlike convex unimodality, neither weak unimodality nor star unimodality of implies any of the unimodality concepts of introduced in Definition 1. To provide a counterexample, we introduce the following class of distributions.

Definition 2 (Homothetic density).

A -dimensional random vector is said to have a homothetic density, denoted by , with a location parameter , shape set and a scaling function if admits a density satisfying

for some continuous and decreasing function and a bounded and star-shaped set around such that

| (10) |

where denotes the Lebesgue measure on .

Note that Condition (10) is required to ensure that . To see this, we have

Homothetic distributions arise from -spherical distributions (Osiewalski,, 1993) where the superlevel sets are determined as balls in the -norm, and also arise from a further generalized class of distributions called the -spherical distributions (Fernandez et al.,, 1995). Examples of homothetic distributions include skew-normal distributions and rotund-exponential distributions; see Balkema and Nolde, (2010). It is straightforward to check that is star unimodal about if is star-shaped about , and convex unimodal if is convex.

Suppose for a convex set . Then is convex unimodal and so is by Proposition 2 Part 2. For this homothetic distribution, the superlevel set of embedded in has the following representation

that is, the superlevel set embedded in is a collection of the projected points of intersected with the upper half space onto .

The following example shows that neither weak unimodality nor star unimodality of implies any of the unimodality concepts introduced in Definition 1 for .

Example 2.

Consider where and . is star-shaped (and thus connected) around and is a decreasing function. Furthermore, the pair of satisfies Condition (10) since

Suppose that the total capital is given by . For , we have and thus . Therefore, , which is neither star-shaped nor even connected.

Next we study marginal properties of unimodality. In general, even if is convex unimodal, it does not imply any unimodality for its marginal distributions; see Balkema and Nolde, (2010, Example A.3.) for a counterexample. The following example shows that marginal unimodality also does not imply joint unimodality.

Example 3 (Marginal unimodality does not imply joint unimodality).

Consider the following bivariate density

which has the convex unimodal marginal densities

However, is neither convex nor star-shaped.

Joint unimodality implies marginal unimodality for certain classes of distributions. As is shown in Balkema and Nolde, (2010), -spherical distributions form a subclass of homothetic densities for which unimodality is preserved under marginalization. This property also holds for the class of -concave densities, which is also closed under the operation ; see Appendix B for details.

3.4 Dependence of and its modality

The dependence structure of is typically described in terms of the dependence among and for . For instance, when , Proposition 1 yields

where and is the correlation coefficient of . Beyond the elliptical case, various dependence concepts, in particular the total positivity and its related order of , are investigated in Appendix C.

In this section, we investigate the modality of under extremal dependence of . The following example shows that is degenerate and thus unimodal when is comonotone.

Example 4 ( under comonotonicity).

Suppose is a comonotone random vector with continuous and strictly increasing margins , that is, for some . Under continuity and strict increasingness of , their quantile functions , , are continuous and strictly increasing. Therefore, the equation of has a unique solution . Moreover, it holds that

since

This example can be understood as an extreme case where positive dependence (comonotonicity) implies unimodality of , which takes on one point with probability .

When has negative dependence, a wider variety of distributions, possibly multimodal ones, arise as compared with the positive dependent case. We demonstrate this phenomenon in the following example.

Example 5 ( under extreme negative dependence).

Let and for a continuous distribution function supported on such that is radially symmetric about in the sense that . For define by

Then for all . Since the conditional radial symmetry of implies that , it holds that

Therefore, and . The body of and the tail of are mutually exclusive in the sense that . Similarly . In the tail, and are comonotone in the sense that on . In the body, and are countermonotone in the sense that on . Since on and on , we have that

and thus that

Consequently, has the homogeneous marginal distribution and a countermonotone copula . Therefore, multimodality of appears when, for example, has a bimodal distribution on the body ; see Remark 3 for a more concrete example.

Remark 3 (Extension to with complete mixability).

Example 5 for constructing based on countermonotonicity can be extended to the multivariate case . Let and for a continuous distribution function supported on such that the conditional distribution is -completely mixable with center for , that is, there exists a -dimensional random vector called the -complete mix such that , , and a.s. Such a random vector exists, for example, when admits a decreasing density with ; see Wang and Wang, (2011, Corollary 2.9.). Define by for being the -complete mix of , , , and , and are independent of each other. Then one can check that . Moreover, since

and a.s. Consequently, a.s. and thus is the -complete mix of . To construct a multimodal one can choose as an equally weighted mixture of three Dirichlet distributions , and for . This mixture is a -complete mix since it has homogeneous marginal distributions and a constant sum. Moreover, has non-connected superlevel sets when, for example, and , and thus is multimodal.

3.5 Tail behavior of

In this section we study the tail behavior of through its density. Since boundedness of from below leads to a bounded support of as shown in Section 3.1, we focus on the case when is supported on . In this case, the support of is and thus there are orthants to be considered. Hereafter we consider tail behavior only in the first orthant since tails on the other orthants can be discussed similarly. We study the following limiting behaviors of the ratio of densities.

Definition 3 (Multivariate regular and rapid variations of a density).

Let be a -dimensional random vector with a density .

-

1.

is called multivariate regularly varying with limit function (at and on the first orthant), denoted by MRV(), if

(11) provided the limit function exists.

-

2.

is called multivariate rapidly varying (at and on the first orthant), denoted by MRV if,

Note that we adopt the definitions of regular and rapid variations of densities for their potential application to MCMC methods where the ratio of target densities at any two points is of interest; see Appendix F. Taking in (11) leads to the standard definition of regular variation introduced, for example, in Resnick, (2007). Regular variation is typically described in terms of probability measures or their survival functions, and these concepts of variations are connected to regular variation of densities through Resnick, (2007, Theorem 6.4.).

The following proposition states that one can find a limit function for based on that of through the auxiliary random vector .

Proposition 3 (Multivariate regular and rapid variations of ).

-

1.

Assume that is MRV(). Then is MRV() with limit function

-

2.

If is MRV(), then is MRV().

The sufficient conditions in Proposition 3 are straightforward to check since does not depend on the sum , and the joint distribution of can be specified through its marginal distributions and copula. The margins of are , , and , and the copula of is the distribution function of where is the copula of . This enables one to find a limit function for ; see, for example, Li, (2013) and Joe and Li, (2019).

The following proposition shows that the limit function is determined by the density generator in the elliptical case.

Proposition 4 (Multivariate regular and rapid variations for elliptical distribution).

Assume admits a density with density generator continuous on .

-

1.

If is regularly varying in the sense that

then is MRV() with

-

2.

If is rapidly varying in the sense that

then is MRV().

Example 6 (Normal and Student distributions).

The multivariate Normal distribution has a rapidly varying density generator , and thus its corresponding conditional distribution is also rapidly varying by Proposition 4 Part 2. Next, suppose follows a -dimensional Student distribution with degrees of freedom . Its density generator (9) is regularly varying with limit function

Consequently, by Proposition 4 Part 1, is regularly varying with limit function

where is an Euclidean norm on .

4 Maximum likelihood allocation and multimodality adjustment

In this section we investigate how the modality of can be incorporated in risk management. Under unimodality, the mode of is regarded as the most likely stress scenario covered by the given total capital . This mode is defined to be a maximum likelihood allocation (MLA) in Section 4.1.1, and its properties are studied in Section 4.1.2. Under multimodality of , a single vector of allocations may obscure multiple risky scenarios as seen in Section 2.2. To overcome this issue, we introduce the so-called multimodality adjustment in Section 4.2 to utilize the knowledge of multimodality of and to increase the soundness of risk allocations.

4.1 Maximum likelihood allocation

4.1.1 Definition and assumptions on MLA

We denote by the set of all -dimensional random vectors such that and admit density functions, and that the function has a unique maximum. For , admits a density through (5), and has a unique maximum attained by the mode of . By Proposition 2, elliptical random vectors with continuous and decreasing density generators form a subclass of . Although some exchangeable random vectors possessing negative dependence, such as Model (b) in Section 2.2, may not be included in , we believe that most loss models used in risk management practice are contained in . As explained in Section 3.3, uniqueness of the mode of and its unimodality are different concepts, and thus the class contains multimodal random vectors in the sense that the density has multiple local maximizers (we call them the local modes of ; see Definition 8 for their formal definitions). Nevertheless, in this section we focus only on the unique global maximizer of (not on local ones) since unimodal distributions are the primary object to apply the MLA to. The multimodal case will then be revisited in Section 4.2. As we will demonstrate in Section 5, multimodality can be detected by searching for the modes of .

In the following we define the unique mode of as a risk allocation of .

Definition 4 (Maximum likelihood allocation).

For and , the maximum likelihood allocation (MLA) on a set is defined by

provided the function has a unique maximum. When , we call it the maximum likelihood allocation.

By (5), MLA of on can be equivalently formulated as

4.1.2 Properties of MLA

We now investigate properties of MLA as a risk allocation principle. For desirable properties of risk allocation in the case when the capital is exogenously given as a constant, see Maume-Deschamps et al., (2016). By construction, always satisfies the full allocation property (1). The following proposition summarizes other desirable properties of MLA.

Proposition 5 (Properties of MLA).

Suppose and .

-

1.

Translation invariance: for .

-

2.

Positive homogeneity: for .

-

3.

Symmetry: For , , let be a -dimensional random vector such that , and , . If , then , where is the th component of for .

-

4.

Continuity: Suppose have densities and for respectively. If is uniformly continuous and bounded for and weakly, then .

Translation invariance states that a sure loss requires the same amount of risk allocation and the rest of the total capital is allocated to the random loss . Positive homogeneity means that, for a proportion , 100% of the loss requires 100% of the total capital and the resulting MLA of is 100% of the allocation of to . Symmetry implies that, if exchanging two units does not change the distribution of the joint loss, then equal amounts of capitals are allocated to them. Finally, continuity ensures that if MLA is calculated based on an estimated model of , then this estimate of MLA is close to the true MLA. Note that the assumption that , , and belong to is esssential so that the MLAs of , , and are well-defined.

Next we discuss properties that need to be considered separately.

-

1.

RORAC compatibility and core compatibility:

RORAC compatibility and core compatibility are important properties of risk allocations since either of them characterizes Euler allocation; see Tasche, (1995) and Denault, (2001). However, the definitions of these properties are not meaningful when is exogenously given as a constant. Moreover, similar constraints as in core compatibility can be additionally imposed on so that the resulting MLA is core-compatible; see Appendix F.2 for details. -

2.

Riskless asset:

The riskless asset condition requires the sure loss a.s. for to be covered by the amount of allocated capital . This property needs to be considered separately since in this case does not admit a density. Suppose that a.s. for and that admits a density . Since(12) any realization of satisfies and the likelihood of is quantified through the value of the density . According to this discussion, a natural extension of the definition of MLA to such a random vector is

(13) which is compatible with the riskless asset property.

- 3.

4.1.3 Discussion on MLA

We now discuss whether MLA is an appropriate risk allocation principle, and also compare MLA with Euler allocation. Here we define Euler allocation by , which are VaR contributions (2) with for some confidence level . As shown in Proposition 5, MLA possesses properties naturally required as an allocation such as translation invariance, positive homogeneity and riskless asset. Euler allocation also satisfies these properties since for (translation invariance), for (positive homogeneity) and the riskless asset property holds by taking expectation on the both sides of the first equality in (12). See Appendix D for properties that neither MLA nor Euler allocation satisfy. Note that by Proposition 1 and Proposition 2 Part 1, Euler and maximum likelihood allocations coincide when is elliptically distributed. Therefore, the economic justifications of Euler allocation, such as RORAC compatibility and core-compatibility, also hold for MLA when is elliptical. Moreover, through the process of estimating a MLA, one can detect multimodality of and discover hidden risky scenarios based on which one can evaluate the soundness of risk allocations. On the other hand, the main disadvantage of MLA compared with Euler allocation is that estimating modes becomes more difficult than estimating a mean as the dimension of the portfolio becomes larger. Furthermore, MLA is not well-defined for distributions whose is not a single point. Finally, MLA may ignore the behavior of other than its mode. Considering these aspects, we believe that MLA itself may not be an appropriate risk allocation principle, but its estimation procedure is beneficial for discovering hidden multiple scenarios likely to occur in the stressed situation , for assessing the soundness of risk allocations in stress testing applications, and eventually for constructing more sound risk allocations based on multiple scenarios as we will consider in Section 4.2.

4.2 Multimodality adjustment of risk allocations

Multiple local modes of can be discovered in the process of estimating MLAs. In this section, we discuss how to utilize the local modes, and introduce the so-called multimodality adjustment to increase the soundness of risk allocations under multimodality of .

4.2.1 Definition of multimodality adjustment

Suppose that scenarios are found with corresponding probability weights such that . A typical choice of the scenario set is the set of local modes of (assumed to be a finite set), or possibly those belonging to a superlevel set at a certain level of plausibility. The probability weight typically represents the likelihood of the scenario to occur, for instance, . Moreover, experts’ assessments of the impact of the loss on the portfolio can also be incorporated. Multimodality adjustment is then defined as follows.

Definition 5 (Multimodality adjustment of risk allocations).

Let be the number of scenarios, be the set of scenarios where for any such that , and be the associated probability weights such that . Then the multimodality-adjusted allocated capital is defined by

| (14) |

where is the baseline allocation, is the matrix of multimodality loading parameters, for and for . We call the second term of (14) the multimodality adjustment.

Unlike MLA, the multimodality-adjusted allocated capital can be well-defined even if the global mode of is not unique. The capital (14) consists of the baseline allocation and the additional loading to cover the variability of scenarios. The baseline allocation is understood as an allocated capital before adjustment of multimodality. Therefore, in (14) can be replaced by Euler allocation if one requires its economic justification such as RORAC compatibility and core-compatibility. To explain the multimodality adjustment, suppose that the scenario occurs with probability . Under this scenario, the portfolio incurs the loss (or profit) . When , the actual amount of loss contributes to the multimodality adjustment . However, this choice of is too conservative, and smaller values of are typically more reasonable since both and sum up to and thus losses of some units imply profits of others. Therefore, losses of some units can be compensated by the profits of other units, and the multimodality loading parameter can be determined by such risk mitigation or a corresponding insurance contract.

4.2.2 Properties of the multimodality adjustment

Next we study properties of . For certain choices of and , the capital can be shown to satisfy translation invariance, positive homogeneity, riskless asset and symmetry; see Appendix E for details. In the remainder of this section, we will verify that measures the risk of multimodality from various viewpoints. First, if , then and thus the multimodality adjustment is zero. Second, suppose that and for . Then if and only if for all and such that . Therefore, under multimodality, the multimodality adjustment is zero if and only if losses of some units of the portfolio are completely compensated by profits of others. Finally, is increasing with respect to the variability of the set of scenarios, which can be understood as a degree of multimodality. To see this, suppose that for some , and denote by the discrete random vector taking points with probabilities . Then the multimodality-adjusted allocated capital (14) can be written as

| (15) |

Variability of the set of scenarios can then be compared by the so-called convex order of . For two -valued random variables and , is said to be larger than in the convex order, denoted as , if for all convex functions provided the expectations exist; see Shaked and Shanthikumar, (2007) for a comprehensive reference. Roughly speaking, convex order compares the variability of random variables and shows more variability than if ; for instance, implies , , , and for all . Therefore, for two sets of scenarios and with associated probabilities and , if one shows more variability than the other in the sense that the corresponding discrete random variables satisfy for some , then it holds that .

Remark 4 (Multimodality adjustment for general sets of scenarios).

Representation (15) bears structural resemblance to Gini shortfall allocations introduced in Furman et al., (2017), and (15) indicates a possible extension of the multimodality adjustment to the case when the set of scenarios is not finite. For instance, by taking and , (15) can be interpreted as multimodality-adjusted Euler allocations of Expected Shortfall since (15) yields

where is the Euler allocation of as derived in (3).

We end this section with a remark on the case when multiple measures or models are considered as different scenarios and how to incorporate these scenarios into multimodality-adjusted allocated capitals.

Remark 5 (Multimodality adjustment for different measures).

A single model of a risk may not be sufficient to manage the risk due to changes of an economic situation or due to model uncertainty. For a further risk assessment, it may be useful to consider multiple measures where is a probability measure on and is the distribution function of under for . These multiple measures can be incorporated into the scenario analysis by, for example, considering the (componentwise) maximum of the multimodality-adjusted allocated capitals calculated based on for , or considering their mixture with respect to probabilities where is associated to the scenario determined, for example, proportionally to the sample size available for the distribution .

5 Numerical experiments

In this section we conduct an empirical and simulation study to compute Euler and maximum likelihood allocations, and compare them for various models. Simulation of the conditional distribution given a constant sum is in general challenging. Throughout this section, we adopt (crude) Monte Carlo (MC) method to simulate according to which unconditional samples from are first generated and those falling in the region for a sufficiently small are then extracted. The extracted samples are standardized via so that their componentwise sum equals . Finally the standardized samples are used as pseudo-samples from . See Appendix F.1 for the potential bias produced by this method, and more sophisticated simulation approaches of based on MCMC methods. All experiments are run on a MacBook Air with 1.4 GHz Intel Core i5 processor and 4 GB 1600 MHz of DDR3 RAM.

5.1 Empirical study

In this section we estimate MLA nonparametrically for real financial data. We consider daily log-returns of the stock indices FTSE , S&P 500 and DJI from January 2, 1990 to March 25, 2004, which contains days and thus log-returns. We consider two portfolios (a) and (b) . For each portfolio, we aim at allocating the capital based on the conditional loss distribution at time given the history up to and including time . Taking into account the stylized facts of stock returns listed in Chapter 3 of McNeil et al., (2015) (such as unimodality, heavy-tailedness and volatility clusters), we adopt a copula-GARCH model with marginal skew- innovations (ST-GARCH; see, for example, Jondeau and Rockinger, (2006) and Huang et al., (2009)). We utilize a GARCH model with skew- innovations with degrees of freedom and skewness parameter for the th marginal time series. That is, within a fixed time period , the th return series follows

where , , and follows a skew- distribution with density given by

| (16) |

where is the density function of a Student distribution with degrees of freedom and a skewness parameter with corresponding to the standard symmetric case; see Fernández and Steel, (1998) for more details. The copula among the stationary process , denoted as , is estimated nonparametrically. Under this model, the joint distribution of the returns has marginal distributions ST, , and a copula , where ST is a skew- distribution with density with defined in (16). Parameters of the ST-GARCH(1,1) models are estimated with the maximum likelihood method; the results are summarized in Table 1.

| SE | ||||||

|---|---|---|---|---|---|---|

| SE | ||||||

| SE | ||||||

| SE |

For each case of (a) and (b) , we estimate the Euler allocation and MLA by a resampling method. After extracting the marginal standardized residuals, we build their pseudo-observations as a pseudo-sample from . We then generate samples of size by resampling with replacement. The samples from are then marginally transformed by skew- distributions with parameters specified as in Table 1. From these samples of , we extract the subsamples falling in the region where . These samples are then standardized via . Scatter plots of the first two components of these samples are shown in Figure 2.

The 3712 data points lead to 354 and 558 samples from and on , respectively. Based on these conditional samples, we estimate the Euler allocation and the MLA, that is, the mode of provided it is unique. The (possibly multiple) modes were estimated by the function kms (kernel mean shift clustering, proposed by Fukunaga and Hostetler,, 1975) of the R package ks; see Carreira-Perpinán, (2015) and Chen et al., (2016) for details and for other methods of estimating modes. For the computational times, computing MLAs took 0.35 seconds in Case (a) and 0.43 seconds in Case (b) whereas, in both cases, the Euler allocations were computed almost instantly. As was expected from the ellipticality of the scatter plots in Figure 2, the unique mode was discovered in each case. The first two components of the two allocations are pointed out in Figure 2.

Next, we estimate the standard errors of the Euler and maximum likelihood allocations using the bootstrap method. We compute the Euler allocation, MLA and their standard errors based on the number of samples of size resampled from the original data with replacement. The results are summarized in Table 2.

| Estimator | Standard error | |||||

|---|---|---|---|---|---|---|

| 0.378 | 0.338 | 0.285 | 0.019 | 0.022 | 0.038 | |

| 0.367 | 0.365 | 0.268 | 0.019 | 0.024 | 0.041 | |

| 0.345 | 0.248 | 0.903 | 0.037 | 0.039 | 0.015 | |

| 0.371 | 0.280 | 0.909 | 0.040 | 0.039 | 0.013 | |

In Figure 2 we can observe that compared with Case (a) the distribution in Case (b) is more spread out and losses take larger absolute values. If the samples are regarded as stressed scenarios, the scenario set in Case (b) contains a wider variety of scenarios than in Case (a) since both of positive and negative losses can appear in Case (b) whereas most realizations are positive in Case (a). Nevertheless, as is observed from Table 2, in both cases the Euler allocation and the MLA are close to each other also in terms of standard errors. This observation does not conflict with the stylized fact that the joint log-returns nearly follow an elliptical distribution, and thus the mean (Euler allocation) of coincides with its mode; see Proposition 1 and Proposition 2 Part 1.

5.2 Simulation study

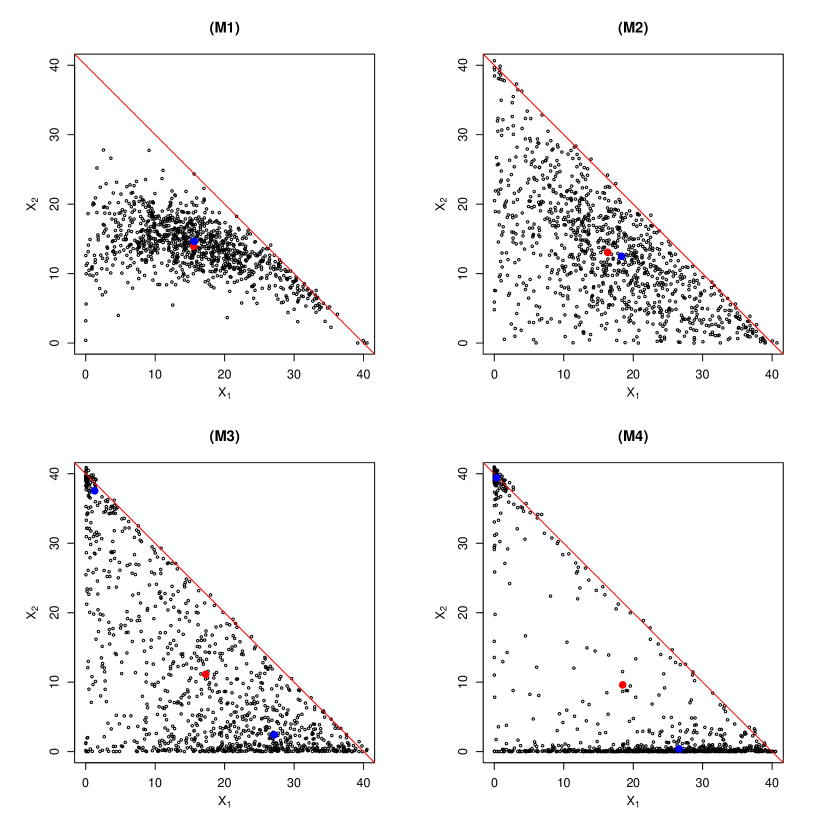

In this section, we consider four models, referred to as (M1), (M2), (M3) and (M4), respectively, with and having the same marginal distributions , and (where denotes the Pareto distribution with shape parameter and scale parameter ) but different copulas with degrees of freedom and dispersion matrices

| (17) |

respectively. For these parametric models, we first simulate samples from the unconditional distribution and then extract subsamples falling in the region with and . These pseudo samples from are shown in Figure 3. The red point in the figure represents the Euler allocation and the blue points are the (local) modes, which are estimated similarly as in Section 5.1.

The computational times required for calculating MLAs were (in seconds) (M1) 18.96, (M2) 11.72, (M3) 15.94, and (M4) 22.76 whereas the Euler allocations were computed almost instantly for all the cases. Compared with the results in Section 5.1, we observe that the computational time required to calculate MLA increases more rapidly than the Euler allocation does as the sample size increases.

In Figure 3 we can observe that the conditional distribution is more concentrated under positive dependence (Model (M1) and (M2)) and it is more dispersed under negative dependence (Model (M4)). Regarding the samples as stressed scenarios, the sets for Model (M3) and (M4) are more worrisome than those for Model (M1) and (M2) since (M3) and (M4) contain two distinct scenarios, one around the first axis and another around the upper-left corner of the plot region, both of which are likely to occur in the stressed situation . Unimodality of the conditional distribution for Model (M1) and (M2) leads to closer Euler allocation and MLA. For Model (M1) and (M2), the choice of Euler allocation and MLA does not significantly change the resulting allocation. On the other hand, for Model (M3) and (M4), the conditional distributions are multimodal, and thus a more careful decision making may be required.

| Estimator | Standard error | |||||

| (M1) Pareto + copula: strong positive dependence | ||||||

| 15.549 | 13.889 | 10.562 | 0.336 | 0.157 | 0.288 | |

| 15.849 | 14.434 | 9.718 | 0.482 | 0.213 | 0.356 | |

| (M2) Pareto + copula: positive dependence | ||||||

| 16.228 | 13.042 | 10.562 | 0.399 | 0.355 | 0.288 | |

| 17.689 | 12.481 | 9.830 | 0.759 | 0.663 | 0.475 | |

| (M3) Pareto + copula: no correlation | ||||||

| 17.479 | 11.368 | 10.562 | 0.517 | 0.530 | 0.288 | |

| 25.678 | 3.107 | 11.215 | 1.185 | 0.278 | 1.205 | |

| 2.639 | 35.275 | 2.086 | 0.973 | 1.306 | 0.424 | |

| (M4) Pareto + copula: negative dependence | ||||||

| 19.062 | 9.272 | 10.562 | 0.556 | 0.614 | 0.288 | |

| 28.353 | 0.684 | 10.962 | 2.125 | 1.646 | 2.154 | |

| 0.710 | 38.385 | 0.905 | 1.719 | 3.537 | 2.705 | |

To investigate the standard errors of the estimators, we compute the estimates of Euler allocation and (local) modes of times for each model. For each repetition, we simulate samples from so that there are samples in the region . The estimates and standard errors are computed based on the 100 replications and the results are summarized in Table 3. We can again see that for Models (M1) and (M2) the mode of is unique and the two allocations are close. On the other hand, for Models (M3) and (M4) where the conditional distributions are multimodal, the standard errors of the (local) modes are higher than those of the Euler allocation.

In the end, we compute the multimodality-adjusted allocated capitals (14) for (M3) and (M4). In each case, the parameters are specified as , and with , where and for (M3), and and for (M4). For both (M3) and (M4), the first and third units incur losses when occurs, and the second unit incurs a large loss when happens. The probability weights of the scenarios are given by for (M3) and for (M4). The two scenarios and are almost equally likely to occur for (M3), and the second scenario is more likely to occur for (M4). Based on and , the baseline allocations are given by for (M3) and for (M4). As seen in Table 3, these allocations are not quite close to the Euler allocations since is calculated based only on the two points and in .

On computing the multimodality adjustments, we consider two cases when or Euler allocations are used as baseline allocations. If is the baseline allocation, the average loss in the multimodality adjustment is given by for (M3) and for (M4). If Euler allocation is used as a baseline allocation, the average loss is given by for (M3) and for (M4). In all cases, the average loss incurred in the second unit is larger than those in the first and third units since the second unit incurs a large loss when the second scenario occurs. Moreover, for (M4), the probability that the scenario occurs is higher than that of the first scenario . Therefore, the analysis of the modes of reveals that a large multimodality adjustment should be applied to to increase the soundness of risk allocations.

6 Conclusion

Motivated from stress testing of risk allocations, we investigated properties of the conditional distribution of given the sum constraint , and also introduced the novel risk allocation method called maximum likelihood allocation (MLA). The superlevel set of can be regarded as a set of stressed (severe and plausible) scenarios, and the modality of can be interpreted as a variety of risky scenarios, which turned out to be an important feature in risk assessment related to the soundness of risk allocations. We then studied modality, dependence and tail behavior of , most of which are inherited from those of the unconditional loss . We then investigated how to incorporate the knowledge of the modality of for more sound risk management. Under unimodality, we defined MLA as a mode of , and studied its properties as a risk allocation principle, such as translation invariance and positive homogeneity. Under multimodality, we considered the so-called multimodality adjustment to increase the soundness of risk allocations based on the multiple modes. Euler allocation and MLA were then compared in numerical experiments. Through the experiments, we demonstrated that is typically unimodal, and Euler allocation and MLA lead to close values when possesses positive dependence. On the other hand, when the losses are negatively dependent, multimodality is likely to occur, and searching for the modes of is beneficial for discovering hidden risky scenarios, evaluating the soundness of risk allocations, and eventually increasing the soundness of risk allocations by imposing the multimodality adjustment.

Although we empirically observed the relationship between multimodality of and negative dependence of , this relationship requires further theoretical investigation. Another aspect of future research is to study more distributional properties, such as tail dependence and measures of concordance, of especially without assuming the existence of a density. Unlike Euler allocations, estimation of MLAs is not a straightforward problem in general but various methods are known for estimating modes of multivariate distributions. For applying the MLA principle in practice, efficient estimation methods of the modes of multivariate distributions in high dimensions need to be explored further. An economic justification of the MLA principle is also an interesting direction for future research. In addition, an extension of the multimodality adjustment to general sets of scenarios is another avenue to explore since the multimodality adjustment proposed in this paper relies on the assumption that the set of scenarios is finite. In the end, efficient simulation approaches of may need to rely on MCMC methods as introduced in Appendix F, and further investigation is required to assess how beneficial the distributional properties proven in this paper are to construct efficient MCMC methods since the performance of MCMC methods typically depends on tail-heaviness and modality of the target distribution.

Funding

This research was funded by NSERC through Discovery Grant RGPIN-5010-2015.

Declaration of interests

Declarations of interest: none.

Acknowledgments

We would like to thank the editor and three anonymous referees for their insightful comments on our manuscript.

References

- Asimit et al., (2019) Asimit, V., Peng, L., Wang, R., and Yu, A. (2019). An efficient approach to quantile capital allocation and sensitivity analysis. Mathematical Finance, 29(4):1131–1156.

- Aumann and Shapley, (2015) Aumann, R. J. and Shapley, L. S. (2015). Values of non-atomic games. Princeton University Press, Princeton, New Jersey.

- Balkema and Nolde, (2010) Balkema, G. and Nolde, N. (2010). Asymptotic independence for unimodal densities. Advances in Applied Probability, 42(2):411–432.

- Breuer et al., (2018) Breuer, T., Jandacka, M., Rheinberger, K., and Summer, M. (2018). How to find plausible, severe, and useful stress scenarios. Eighteenth issue (September 2009) of the International Journal of Central Banking.

- Carreira-Perpinán, (2015) Carreira-Perpinán, M. A. (2015). A review of mean-shift algorithms for clustering. arXiv preprint arXiv:1503.00687.

- Chen et al., (2016) Chen, Y.-C., Genovese, C. R., Wasserman, L., et al. (2016). A comprehensive approach to mode clustering. Electronic Journal of Statistics, 10(1):210–241.

- Denault, (2001) Denault, M. (2001). Coherent allocation of risk capital. Journal of Risk, 4(1):1–34.

- Dhaene et al., (2012) Dhaene, J., Tsanakas, A., Valdez, E. A., and Vanduffel, S. (2012). Optimal capital allocation principles. Journal of Risk and Insurance, 79(1):1–28.

- Dharmadhikari and Joag-Dev, (1988) Dharmadhikari, S. and Joag-Dev, K. (1988). Unimodality, convexity, and applications. Elsevier.

- Ding, (2016) Ding, P. (2016). On the conditional distribution of the multivariate t distribution. The American Statistician, 70(3):293–295.

- Fang, (2018) Fang, K. W. (2018). Symmetric multivariate and related distributions. Chapman and Hall/CRC.

- Fernandez et al., (1995) Fernandez, C., Osiewalski, J., and Steel, M. F. (1995). Modeling and inference with -spherical distributions. Journal of the American Statistical Association, 90(432):1331–1340.

- Fernández and Steel, (1998) Fernández, C. and Steel, M. F. (1998). On bayesian modeling of fat tails and skewness. Journal of the American Statistical Association, 93(441):359–371.

- Fukunaga and Hostetler, (1975) Fukunaga, K. and Hostetler, L. (1975). The estimation of the gradient of a density function, with applications in pattern recognition. IEEE Transactions on information theory, 21(1):32–40.

- Furman and Landsman, (2006) Furman, E. and Landsman, Z. (2006). Tail variance premium with applications for elliptical portfolio of risks. ASTIN Bulletin: The Journal of the IAA, 36(2):433–462.

- Furman et al., (2017) Furman, E., Wang, R., and Zitikis, R. (2017). Gini-type measures of risk and variability: Gini shortfall, capital allocations, and heavy-tailed risks. Journal of Banking & Finance, 83:70–84.

- Huang et al., (2009) Huang, J.-J., Lee, K.-J., Liang, H., and Lin, W.-F. (2009). Estimating value at risk of portfolio by conditional copula-garch method. Insurance: Mathematics and economics, 45(3):315–324.

- Joe and Li, (2019) Joe, H. and Li, H. (2019). Tail densities of skew-elliptical distributions. Journal of Multivariate Analysis, 171:421–435.

- Jondeau and Rockinger, (2006) Jondeau, E. and Rockinger, M. (2006). The copula-garch model of conditional dependencies: An international stock market application. Journal of international money and finance, 25(5):827–853.

- Kalkbrener, (2005) Kalkbrener, M. (2005). An axiomatic approach to capital allocation. Mathematical Finance, 15(3):425–437.

- (21) Karlin, S. and Rinott, Y. (1980a). Classes of orderings of measures and related correlation inequalities. i. multivariate totally positive distributions. Journal of Multivariate Analysis, 10(4):467–498.

- (22) Karlin, S. and Rinott, Y. (1980b). Classes of orderings of measures and related correlation inequalities ii. multivariate reverse rule distributions. Journal of Multivariate Analysis, 10(4):499–516.

- Koike and Hofert, (2020) Koike, T. and Hofert, M. (2020). Markov chain monte carlo methods for estimating systemic risk allocations. Risks, 8(1):6.

- Koike and Minami, (2019) Koike, T. and Minami, M. (2019). Estimation of risk contributions with mcmc. Quantitative Finance, 19(9):1579–1597.

- Laeven and Goovaerts, (2004) Laeven, R. J. and Goovaerts, M. J. (2004). An optimization approach to the dynamic allocation of economic capital. Insurance: Mathematics and Economics, 35(2):299–319.

- Li, (2013) Li, H. (2013). Toward a copula theory for multivariate regular variation. In Copulae in mathematical and quantitative finance, pages 177–199. Springer.

- Maume-Deschamps et al., (2016) Maume-Deschamps, V., Rullière, D., and Said, K. (2016). On a capital allocation by minimization of some risk indicators. European Actuarial Journal, 6(1):177–196.

- McNeil et al., (2015) McNeil, A. J., Frey, R., and Embrechts, P. (2015). Quantitative risk management: Concepts, techniques and tools. Princeton University Press, Princeton.

- Müller and Stoyan, (2002) Müller, A. and Stoyan, D. (2002). Comparison methods for stochastic models and risks, volume 389. Wiley New York.

- Norkin and Roenko, (1991) Norkin, V. and Roenko, N. (1991). -concave functions and measures and their applications. Cybernetics and Systems Analysis, 27(6):860–869.

- Osiewalski, (1993) Osiewalski, J. (1993). Robust bayesian inference in lq-spherical models. Biometrika, 80(2):456–460.

- Resnick, (2007) Resnick, S. I. (2007). Heavy-tail phenomena: probabilistic and statistical modeling. Springer Science & Business Media.

- Roth, (2012) Roth, M. (2012). On the multivariate t distribution. Linköping University Electronic Press.

- Saumard and Wellner, (2014) Saumard, A. and Wellner, J. A. (2014). Log-concavity and strong log-concavity: a review. Statistics Surveys, 8:45.

- Schmidt, (2002) Schmidt, R. (2002). Tail dependence for elliptically contoured distributions. Mathematical Methods of Operations Research, 55(2):301–327.

- Shaked and Shanthikumar, (2007) Shaked, M. and Shanthikumar, J. G. (2007). Stochastic orders. Springer Science & Business Media.

- Sweeting et al., (1986) Sweeting, T. J. et al. (1986). On a converse to scheffé’s theorem. The Annals of Statistics, 14(3):1252–1256.

- Tasche, (1995) Tasche, D. (1995). Risk contributions and performance measurement. Working Paper, Techische Universität München.

- Tasche, (2001) Tasche, D. (2001). Conditional expectation as quantile derivative. arXiv preprint math/0104190.

- Wang and Wang, (2011) Wang, B. and Wang, R. (2011). The complete mixability and convex minimization problems with monotone marginal densities. Journal of Multivariate Analysis, 102(10):1344–1360.

Appendices

Appendix A Proofs

Proof of Proposition 1

Proof.

Notice that where . Therefore, the conditional distribution also follows an elliptical distribution with the location parameter and the dispersion parameter as specified in (7). The corresponding characteristic generator can be specified through Theorem 2.18 of Fang, (2018). If admits a density with density generator , then

The quadratic term reduces to

Therefore, we have that

where and as specified in (8). ∎

Proof of Proposition 2

Proof.

-

1.

By Proposition 1, follows a -dimensional elliptical distribution with location vector , dispersion matrix and density generator . Furthermore, is decreasing if is. Therefore, for ,

which is a convex set with ellipsoid as surface. Moreover, when , we have

and thus has a mode .

- 2.

∎

Proof of Proposition 3

Proof.

Let . Since the density of is written as , we have, by (5), that

Therefore, if has a limit function , then the density of satisfies

for any since . Similarly, if is MRV(), then

for any and . ∎

Proof of Proposition 4

Proof.

Proposition 1 yields that follows a -dimensional elliptical distribution with location vector , dispersion matrix and density generator . If is regularly varying, then

for any , where the third equality comes from continuity of and the fourth equality holds since . Therefore, is MRV(). For the rapidly varying case,

for any and since if and only if and if and only if for . Therefore, is rapidly varying. ∎

Proof of Proposition 5

Proof.

-

1.

Translation invariance: Let , and . Since , we have that

Therefore, uniqueness of the maximizer of implies that of , and these maximizers are related via .

-

2.

Positive homogeneity: Let , and . Since , we have that

As seen in the case of translation invariance, this equality implies that and .

-

3.

Symmetry: Without loss of generality, consider and . Let and , where is a shorthand for for . Then for and . Moreover, when , we have that and . Consequently, we have that

(19) where the third equation holds since . Now suppose that . Then two different vectors and attain the maximum of by (19). Since is obtained by the unique maximizer of , this leads to a contradiction.

-

4.

Continuity: When is uniformly continuous and bounded for , the sequence is asymptotically uniformly equicontinuous and bounded in the sense introduced in Sweeting et al., (1986). Together with the assumption that weakly, Theorem 2 of Sweeting et al., (1986) implies that pointwise and uniformly in for the uniformly continuous density of . Define for and , . By (5) and since , the maximizers of and are uniquely determined. Denote them as and . By definition of , we have that

Since converges uniformly to , it holds that

If , then two points attain the maximum of , which contradicts the uniqueness of the maximizer of . As a consequence, and thus .

∎

Appendix B Modality and -concave densities

As we saw in Section 3.3, neither joint unimodality nor marginal unimodality implies the other . However, unimodality is preserved under marginalization for some specific class of densities, so-called -concave densities. In this appendix we briefly introduce the connection between unimodality and -concavity of the conditional distribution given a constant sum.

Definition 6 (-concavity).

For , a density on is called -concave on a convex set if

where is called the generalized mean defined, by continuity, as

for , and .

Definition 6 of -concavity is based on densities and can be extended to a measure-based definition for distributions that do not admit densities; see Dharmadhikari and Joag-Dev, (1988). For , -concavity is also known as quasi-concavity and -concavity is also known as log-concavity. By definition, for , is -concave if and only if is a concave function. As shown in Dharmadhikari and Joag-Dev, (1988), the function is increasing for fixed . From this we have that -concavity of implies -concavity for . Examples of -concave densities include the skew-normal distributions (Balkema and Nolde,, 2010), Wishart distributions, Dirichlet distributions with certain range of parameters (Dharmadhikari and Joag-Dev,, 1988) and uniform distributions on a convex set in (Norkin and Roenko,, 1991).

Convex unimodality (Definition 1) is related to -concavity since a density is convex unimodal if and only if it is -concave (Dharmadhikari and Joag-Dev,, 1988). Therefore, is convex unimodal if it is -concave for some . Furthermore, it is straightforward to show that has an -concave density if has. As shown in Dharmadhikari and Joag-Dev, (1988) and Saumard and Wellner, (2014), -concavity is preserved under marginalization, convolution and weak-limit for certain ranges of . Therefore, convex unimodality can also be preserved under these operations if has the -concave the density .

Appendix C Dependence of and stochastic orders

In this appendix, we investigate the dependence, especially the total positivity and its related orders of implied by those of . To this end, we define the following concepts.

Definition 7 (Multivariate total positivity of order ).

Suppose random vectors and have densities and , respectively.

-

1.

is said to be multivariate totally positively ordered of order 2 (MTP2) if

-

2.

is said to be multivariate reverse rule of order 2 (MRR2) if

-

3.

is said to be larger than in -order, denoted as if

For examples and implied dependence properties of MTP2, MRR2 and TP2 ordered distributions, see Karlin and Rinott, 1980a and Karlin and Rinott, 1980b . The following proposition states that the MTP2, MRR2 and TP2 order of and are inherited from those of and .

Proposition 6 (MTP2, MRR2 and TP2 order of ).

Suppose and with and have densities and , respectively.

-

1.

If is MTP2 (MRR2) then is MTP2 (MRR2).

-

2.

If then .

Proof.

By (5) we have, for , that

which proves the first part on MTP2. The MRR2 and TP2 parts are shown in similar manners. ∎

The properties of MTP2 (MRR2) and TP2 order have various implications. For example, when is MTP2, then is positively associated in the sense that for all increasing functions and . If , then , that is, for all bounded and increasing functions . See Müller and Stoyan, (2002) for more implications of the MTP2, MRR2 and TP2 order.

Appendix D Fallacies in risk allocations

In this appendix we introduce two properties which intuitively hold but in general do not for the Euler and maximum likelihood allocations. For a -dimensional random vector and a real number , an allocation principle maps to such that .

-

1.

Invariance under independence:

For two integers , consider a -dimensional random vector with and a -dimensional random vector with . For , we call a risk allocation invariant under independence ifprovided that and are independent of each other. This property means that risk allocation problems of multiple portfolios independent of each other can be considered separately. This property does not hold for MLA since the maximizers of the two functions

(20) and

(21) are in general different. For example, let and and be two independent and identically distributed standard normal distributions. Then the maximum of (1) is attained at whereas that of (21) is attained at . The two vectors are not equal unless . In this example, the Euler allocation provides the same allocated capitals as MLA. Therefore, neither Euler allocation nor MLA satisfies invariance under independence.

-

2.

Additivity under convolution:

Consider two independent -dimensional random vectors and with and . For , we call an allocation additive under convolution ifNeither Euler allocation nor MLA satisfies this property. For example, let and be two independent normal random vectors for and . By Proposition 1, Equation (7) and Proposition 2 Part 1, we have that

Similarly, since , we have that and that

which is not equal to unless, for instance, . Since Euler and maximum likelihood allocations coincide under ellipticality, the same statement holds for Euler allocations.

Appendix E Further properties of the multimodality adjustment

In this section we study further properties of the multimodality adjustment introduced in Section 4.2. To clarify the relationship between , the total capital and the loss distribution of , define and to be the multimodality-adjusted allocated capitals (14) and their first term , respectively, with being the set of local modes of (assumed to be a finite set) and with . To this end, we adopt the following definition of local modes.

Definition 8 (Local modes).

For an -valued function on , is called a local mode of if there exists such that

| (22) |

where . If (22) holds for any , then is called a global mode of .

Properties of are then summarized as follows.

-

1.

Translation invariance: We show that is translation invariant in the sense that

To show this, notice that local modes of are given by , , if , , are the local modes of . Since , the probability weight assigned to the th scenario does not change from to for all . Therefore, and thus

which shows translation invariance.

-

2.

Positive homogeneity: Multimodality-adjusted allocated capitals are positive homogeneous in the sense that

This can be checked similarly as translation invariance. The local modes of are given by , , if , , are the local modes of . Moreover, the probability weight assigned to the th scenario does not change from to since for all . Therefore, and thus

which shows positive homogeneity.

-

3.

Riskless asset: Multimodality-adjusted allocated capitals satisfy the riskless asset property in the following sense. Suppose that a.s. for and that admits a density . As we discussed in Section 4.1.2, any realization of satisfies where , and the likelihood of is quantified through the density . Therefore, reasonable choices of the scenarios are such that and are local modes of . In this case, we have that and the multimodality adjustment yields

Therefore, it holds that if a.s.

-

4.

Symmetry: For a reasonable choice of , the multimodality-adjusted allocated capitals satisfy the symmetry property, that is, for , , if where is a -dimensional random vector satisfying , and for all . For any , denote by a -dimensional vector such that , and for all . To show the symmetry, suppose that is a local mode of . Then is also a local mode of since for any by , and thus satisfies (22) for some . Therefore, any element in satisfies either (1) or (2) there exists a unique element such that , , , and for all . For such a pair of indices , it holds that since and by . Therefore, if holds for all pairs of , then the symmetry holds.

The continuity property for a given and such that converges to weakly may not be straightforward to verify since a limit of multimodal distributions can be unimodal, and more generally, the number of scenarios may change in .

Appendix F Simulation of with MCMC methods

Efficient simulation of the conditional distribution of given a constant sum for is a challenging task in general. In Section 2.2 and Section 5, the constraint was replaced by for a small so that . However, this modification distorts the conditional distribution and the resulting estimates of risk allocations suffer from inevitable biases. To overcome this issue, we briefly review MCMC methods, specifically the Metropolis-Hastings (MH) algorithm, and then demonstrate their efficiency for simulating .

F.1 MCMC methods

As mentioned in Section 2.1, it suffices to simulate for . Assume that admits a density (5). We call this density the target density and denote it as . In the MCMC approach, a Markov chain is constructed such that its stationary distribution is . Constructing such a Markov chain can be achieved by the MH algorithm as we now explain. From the current state , a candidate of the next state is simulated from where , is called the proposal density satisfying the two conditions that (i) is measurable for all , and (ii) is a density function for all . The candidate is accepted, that is, , with probability where

| (23) |

and otherwise the chain stays at the current state . Calculation of the acceptance probability (23) is often possible since it does not depend on . The resulting Markov chain is shown to have as a stationary distribution and thus can be used as samples from in order to estimate Euler and maximum likelihood allocations.

An appropriate choice of is important since MCMC samples are typically positively correlated due to the acceptance-rejection procedure. To reduce positive correlation among MCMC samples, must reflect properties of , such as the shape of its support, modality and tail behavior, for maintaining high acceptance probability . First, the support of must be taken into account since a candidate outside of the support of is immediately rejected. Second, heavy-tailed target distribution requires specific design of since most standard MCMC methods such as random walk MH, independent MH, Gibbs samplers and the Hamiltonian Monte Carlo methods cannot guarantee the theoretical convergence when is heavy-tailed. Finally, multimodality of also requires to be handled specifically since the chain needs to traverse from one mode to another to sample from the entire support of .

F.2 An application of MCMC to core allocation

In this section we compute the Euler allocation and MLA on the restricted set of allocations called the (atomic) core defined by