Fine-grained Financial Opinion Mining: A Survey and Research Agenda

Abstract

Opinion mining is a prevalent research issue in many domains. In the financial domain, however, it is still in the early stages. Most of the researches on this topic only focus on the coarse-grained market sentiment analysis, i.e., 2-way classification for bullish/bearish. Thanks to the recent financial technology (FinTech) development, some interdisciplinary researchers start to involve in the in-depth analysis of investors’ opinions. In this position paper, we first define the financial opinions from both coarse-grained and fine-grained points of views, and then provide an overview on the issues already tackled. In addition to listing research issues of the existing topics, we further propose a road map of fine-grained financial opinion mining for future researches, and point out several challenges yet to explore. Moreover, we provide possible directions to deal with the proposed research issues.

1 Introduction

Dealing with the data in the financial domain is one of the hot research directions in the artificial intelligence (AI) community. Following the recent trend of financial technology (FinTech), several workshops are held in conjunction with major conferences such as FinNLP Chen et al. (2019e), ECONLP Hahn et al. (2019), FNP Mahmoud El-Haj et al. (2019), and DSMM Burdick et al. (2019). This reflects the increasing interest of the AI researchers in financial and economic domains. The special track in IJCAI-2020, AI in FinTech, also evidences this phenomenon.

Recently, more and more interdisciplinary cooperation between finance and computer science, and interesting research results are published. Some works Sedinkina et al. (2019); Qin and Yang (2019); Yang et al. (2020) introduce the earning conference call, which is one of the important meetings for announcing the news of a company, to the natural language processing (NLP) community. Some works Maia et al. (2018); Chen et al. (2019a) pay their attention to financial social media data, and propose novel tasks for in-depth investigations. These works indicate the trend of fine-grained opinion mining in the financial domain.

When mentioning the opinion in Finance, bullish/bearish comes into most people’s minds. However, the market sentiment of the financial instrument is just one kind of opinions in the financial industry. As other industries such as manufacturing and textiles have many kinds of products, there are also a lot of products in the financial industry. Financial service is also a major business of many financial companies, especially, in the recent FinTech trend. For instance, many commercial banks focus on the business of both loan and credit card. Although many issues could be explored in the financial domain, most researchers in the AI and the NLP communities only focus on the market sentiment of the financial instrument. In this paper, we sort out several research issues that can broaden the research topics in the AI community.

This paper is aimed at providing an overview of where we are in fine-grained financial opinion mining and helping the community to understand where we should be in the future. For understanding the past and the present works, we discuss the components of the financial opinions one-by-one with related works. During the discussion, we will point out some possible research issues. For the future research directions, we mainly focus on illustrating the unexplored challenges. We provide a research agenda with the directed graphs toward financial opinions.

At beginning, some concepts need to be declared. Firstly, market profits are rather aleatory, so that they cannot be used as labels of opinions, and those studies focusing on constructing end-to-end models for market movement prediction Hu et al. (2018); Feng et al. (2019) will not be included in this paper. Secondly, news articles describing the events do not contain opinions. Thus, those studies analyzing the events in news articles Zheng et al. (2019) will not be covered by this paper. Thirdly, following the investigations of previous works Loughran and McDonald (2009); Chen et al. (2018a, 2020), general sentiment (positive/negative) are different from market sentiment (bullish/bearish).

This paper is organized as follows. Section 2 compares this paper with previous surveys. Section 3 provides careful definitions of coarse-grained and fine-grained financial opinions. Section 4 lists the existing tasks and points out critical research issues. Section 5 proposes novel extension tasks of financial opinion mining. Section 6 provides potential directions for the extension tasks. Finally, Section 7 concludes remarks.

2 Related Work

Pang and Lee Pang et al. (2008) and Liu Liu (2015) provide a general overview of sentiment analysis and opinion mining. Then the overview and survey papers related to opinion mining in the general domain are updated every year Pradhan et al. (2016); Abirami and Gayathri (2017); Hussein (2018); Tedmori and Awajan (2019). Most of the works focus on the opinions on social media platforms Kharde and Sonawane (2016); Li et al. (2019); Soong et al. (2019). Some works focus on specific topics such as product review Jebaseeli and Kirubakaran (2012) and reputation evaluation Chiranjeevi et al. (2019). Although Kumar and Ravi Kumar and Ravi (2016) provide a survey on text mining in finance, few of the previous work provides an arrangement of opinion mining in finance. In this paper, we will formulate the financial opinion mining task and illustrate a big picture of this research area.

Although some previous surveys have paid their attention to text mining in finance Das and others (2014); Fisher et al. (2016), they show less solicitude for opinion mining, and only mention a few coarse-grained financial opinion mining tasks. In order to provide an in-depth look at the recent trend—fine-grained financial opinion mining, this paper mainly focuses on the issues of fine-grained financial opinion mining and proposes a road map for the future research.

3 Financial Opinion Definition

In this paper, we separate the financial opinions into two parts: (1) investor’s opinion, i.e., the opinion about financial instruments and (2) customer’s opinion, i.e., the opinion about the financial product or financial service. As we mentioned in Section 1, market sentiment and general sentiment are different, and the previous works Loughran and McDonald (2009); Chen et al. (2018a, 2020) already evidence this claim. Therefore, when discussing the investor’s opinion, the sentiment is the market sentiment. On the other hand, when discussing the opinion of a financial product or a financial service, the sentiment denotes the general sentiment. Based on these two opinion types, we define the opinions by both coarse-grained and fine-grained viewpoints.

3.1 Coarse-grained Financial Opinion

As the opinion mining task in other domains, the coarse-grained financial opinions can be separated into two (bullish/bearish or positive/negative) or three (bullish/bearish/neutral or positive/negative/neutral) classes, and each opinion related to one target entity. In most cases, the opinion holder and the publishing time are given. All of the above information can construct a 4-tuple to represent a coarse-grained opinion:

,

where denotes the target entity, denotes the sentiment, denotes the opinion holder, and denotes the publishing time.

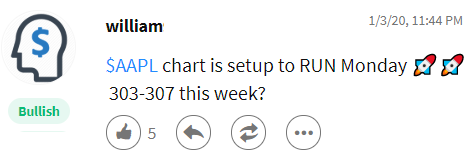

Figure 1 shows an example on one of the famous financial social media platforms, StockTwit111https://stocktwits.com. The 4-tuple of this tweet is

($AAPL, Bullish, william, 1/3/20 11:44PM)

Because all essential terms are provided by the platform and users, researchers can easily collect lots of labeled data from the platform. Therefore, many previous works adopt this dataset to construct a market sentiment lexicon for financial social media Oliveira et al. (2016); Li and Shah (2017); Chen et al. (2018a), and lots of previous works use the labels to test their sentiment analysis models. Renault Renault (2019) provides a comparison between different models on the financial social media data.

Few works involve in mining the opinions of the products and the service from customers in the financial domain, although these are also very important for financial institutions. For example, customer satisfaction and customer service quality are the focuses in the financial domain Potluri et al. (2016); Ali and Raza (2017); Tomar and Tomar (2019). Capturing the opinions from customers’ discussion on the online forum is a possible direction for evaluating customer satisfaction and customer service quality. On the other hand, the opinions of the products can also provide cues for improving the next product. For example, in the discussion of a credit card forum, the reply like (E1) shows the opinion on the credit card, called FlyGo.

Example (E1):

Because the cashback of FlyGo was canceled, I cut it directly.

The 4-tuple of this reply is

(FlyGo, Negative, CREA, 12/31/19 21:04)

Based on the above issues, we list the following research questions:

(RQ1) How to identify the opinions toward a specific product or a specific service in financial industry from the online forums or social media platforms?

(RQ2) To what extent the opinions on the online forums impact customer satisfaction or the sales of the products?

(RQ3) What can or cannot be transferred from the existing opinion mining task in other domains to financial domain?

3.2 Fine-grained Financial Opinion

In this section, we add the related components one-by-one to define the fine-grained financial opinion. The first one is the aspect of the opinion. Still, we start from the investor’s opinion. Taking the tweet in Figure 1 as an example, the analysis aspect is technical analysis, because the analysis is based on the price chart. Thus, we extend the 4-tuple to a 5-tuple as follows:

,

where denotes the analysis aspect. Maia et al. Maia et al. (2018) and our previous work Chen et al. (2019b) provide datasets for extracting the analysis aspect of the investors.

The other important component is the degree of sentiment. Adding the degree of sentiment () to the 5-tuple, we get a 6-tuple as follows:

Some works in other domains extend the sentiment into five classes based on the strongness Balikas et al. (2017); Akhtar et al. (2019). In the financial domain, Cortis et al. Cortis et al. (2017) label the degree of sentiment into the range between 1 and 1.

A fine-grained customer’s opinion can also be shown as a 6-tuple. With this definition and the five-class degree setting, we can extend (E1) to:

(FlyGo, Negative, CREA, 12/31/19 21:04, cashback, 5)

Since few works discus the customer’s opinion, the following research questions are still unexplored:

(RQ4) How to define the aspects for the financial products and financial services?

(RQ5) What kind of evaluation method is proper for the customer’s opinions?

In the example in Figure 1, the investor claim that the price of $AAPL will in the range of 303 to 307 in the coming trading days (one week). In this case, a financial opinion can be extended to a 7-tuple:

,

where denotes the set of investor’s claims. Note that a big difference exists between the investor’s claim and the customer’s claim. Different from customers, who provide their opinions based on the experience of using a product or the service in the past, investors provide their opinions for future events based on their analysis. In our previous work Chen et al. (2019a), we analyze five kinds of investor’s claims, which contain the price information. We will detail it in Section 4. Here raises a research question:

(RQ6) How to detect the claims related to the financial opinion?

The other characteristic of the investor’s opinion is that the market information of the financial instruments (the target entity) is very important for understanding the investor’s opinion. For example, the closing price of a financial instrument is given every day, and it can provide a base for evaluating the degree of sentiment. For instance, 303 and 307 in Figure 1 cannot provide any information if we do not compare it with the closing price of $AAPL. When the closing price 297.32 is given, we can, therefore, infer the degree of sentiment as [1.91%, 3.26%] by a simple calculation. The degree of sentiment acquired via this approach is more rational than those labels from 1 to 1 by the intuition of annotators in the previous work Cortis et al. (2017). This kind of information not only provides the degree of sentiment but also implies the sentiment toward the target financial instrument. Now the 7-tuple is extended to 8-tuple as follows:

,

where denotes the market information set of target entity before publishing time. The other research question is raised below:

(RQ7) How to align the information in the investor’s claims to the market information of the target entity?

In most of opinion mining tasks, the opinions do not have the validity period. However, since the financial market changes all the time, the investor’s opinions do have a validity period, even the opinions of professional stock analysts are the same. Most of the analysis reports of professional analysts set the validity period within one year even shorter. Therefore, an investor’s opinion can be represented as a 9-tuple:

,

where denotes the validity period. Taking the instance in Figure 1 as an example, the opinion is transferred into:

($AAPL, Bullish, william, 1/3/20 11:44PM, 1/6/20–1/10/20 (this week), technical analysis, [1.91%, 3.26%], {Price Target: [303,307]}, {Closing Price: 297.32})

The aforementioned lead to:

(RQ8) How long is the validity period of the investor’s opinions?

(RQ9) Comparing with coarse-grained opinions, how much informativeness is increased for the downside tasks after capturing fine-grained opinions?

4 Current Financial Opinion Mining Tasks

Although the opinion mining in the financial domain, the investor’s opinions mainly, has been discussed for a long time, there are few benchmark datasets for reproducing the experimental results and making the extended researches. In this section, we focus on sorting out the existing datasets of different tasks and the related state-of-the-art models, and further discuss the potential research questions. Again, the datasets or task setting adopting market profit as labels such as StockNet Xu and Cohen (2018) will not be included, because these works do not capture any individual opinions.

4.1 Tasks and Datasets

Detecting the components in the opinion 9-tuple (7-tuple) defined in Section 3 is the challenge that has already been explored. For the investor’s sentiment, several works Li and Shah (2017); Chen et al. (2018a), adopt the labeled data from StockTwits directly, and do not publish the datasets for future research. Therefore, these works are not comparable. The dataset in Semeval-2017 task 5 Cortis et al. (2017) extends the investor’s sentiment into the range from 1 to 1. Total 2,499 financial tweets collected from Twitter and StockTwits are labeled by three annotators. Jiang et al. Jiang et al. (2017) perform the best with an ensemble model composed of support vector regression, XGBoost, AdaBoost, and bagging regressor.

For the aspect of the fine-grained investor’s opinion, FiQA dataset Maia et al. (2018) provides 774 annotated tweets, and there are 4,847 annotated tweets in NumAttach dataset Chen et al. (2019b). E et al. E. et al. (2018) perform the best in FiQA dataset with an attention-based LSTM model. Since the annotation in NumAttach is used as the auxiliary task Chen et al. (2019b), the performance on aspect detection is not yet explored.

Like the example in Figure 1, numerals are informative in the financial data. However, the meanings of numerals are various. In order to understand the fine-grained meaning of the numerals, we propose a taxonomy for the numerals in financial data, FinNum Chen et al. (2018b). There are five kinds of numerals related to investor’s opinions, including price target, buying price, selling price, support price-level, and resistance price-level. The informativeness and usefulness of these fine-grained opinions are already discussed in our previous work Chen et al. (2019a). The FinNum dataset provides 8,868 annotations on the numeral information on financial tweets. This dataset can be used for detecting the numeral components in the investor’s opinions. Wang et al. Wang et al. (2019) adopt BERT Devlin et al. (2019) in this dataset, and gain the state-of-the-art performance.

The named entity recognition (NER) may not be a challenging task in financial data, because there are finite financial instruments. As shown in Figure 1, the target entity ($AAPL) is marked by the writer. However, the linking between the opinion and the target entity is a challenge. When analyzing the paragraph-level or document-level description, there may exist more than one financial instrument or financial product. In the NumAttach dataset Chen et al. (2019b), we show that even a tweet may mention more than one financial instrument. There are 7,984 annotations for the linking between the target entity and the fine-grained opinion.

4.2 Further Research Questions

Since constructing a domain-specific dataset are costly, there are few benchmark datasets in financial opinion mining. That also shows the chance for future research. For example, the validity period detection and the fine-grained customer’s opinion are not discussed yet.

Most of the previous works Bollen and Mao (2011); Valencia et al. (2019) adopt market movement prediction as the downside task of capturing investor’s sentiment, and coarsely use the averaged sentiment score from all investors. However, Wang et al. Wang et al. (2015) indicate that the top investors, ranking by their history performances, on social media platforms can achieve 75% accuracy on market movement prediction. For reference, the accuracy of the recent market movement prediction model Feng et al. (2019) is in the range of [53.05%, 57.20%]. Besides, as the opinions in other domains, with the financing incentive, some opinions may not be worthy of trust such as spam review. In the financial domain, the exaggerate information Chen et al. (2019c) may influence the market, and the opinions with the exaggerate information may also be doubtful. Therefore, detecting the doubtful opinions are also an open issue. The above discussion arises the following research questions:

(RQ10) How to evaluate the quality of the investor’s opinions?

(RQ11) What kinds of opinions are influential in finance?

(RQ12) What kinds of opinions are worth to truth in finance?

5 Road Map of Future Research Issues

5.1 Argument Mining in Finance

Argument mining is one of the focused topics in the AI community recently. Cabrio and Villata Cabrio and Villata (2018) and Lawrence and Reed Lawrence and Reed (2019) provide the surveys to the recent development of argument mining. Please refer to their survey for details. In our view, it can be considered as the next stage of fine-grained financial opinion mining. Previous works and the above sections only focus on extracting the opinions of the investors or customers. In this section, we discuss the importance of mining the premises and evaluating the rationales of a financial opinion.

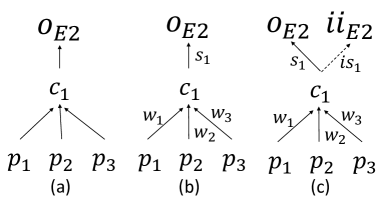

In order to clarify the tasks, we use a passage (E2) selected from professional analysis as an example. The target entity of (E2) is TSMC, and there are one fact (F1), three premises (P1-3), and one claim (C1) in (E2).

Example (E2):

(F1) The overall revenue of semiconductor industry 10–11/2018 is in line with expectations. As (P1) the company’s leading-edge in high-end process production continues to increase, coupled with (P2) Globalfoundries’ withdrawal from competition and (P3) inconsistencies in Intel’s process conversion, we estimate that (C1) TSMC’s revenue in 4Q18 will approximate to 9.35 billion US dollars.

The first challenge of in-depth opinion analysis is that detecting the opinion and the rationales, i.e., the claim and the premise. In the financial market, the investors debate on different financial instruments every day with different stances, bullish or bearish. It just likes the situations where the debaters discuss different topics on the affirmative and negative sides. In order to analyze the claims and the premises of the investors, the detection task is necessary.

Aiming to make the AI models becomes explainable, AI scientists strive for having proof and evidence for the models’ predictions. However, in the financial opinion mining field, people use all kinds of opinions directly without asking the reasons. For example, should we give the same weight to the tweet “$TSMC Goooooo!” and (E2) when analyzing the investors’ opinions? In most of the previous works, their weights are the same. It shows that there is still room for future researches.

One of the further research issues after claim and premise detection is relation linking. In a narrative of an opinion, investors or customers may propose more than one claim with several premises. After predicting the relationship, an opinion can be transformed into a graph as shown in Figure 2 (a). Now, the claim set of an opinion may contain several premise, set .

5.2 Quality Evaluation

After extracting the claims and the premises of an opinion, we can evaluate the opinion quality based on the extracted results. Taking Figure 2 (b) for illustration, we can first evaluate the rationality of the premises, and we will get the rationality scores () of the premises. We can further add up the rationality scores as the strength score () of the claim. Then we can get the opinion quality () by accumulating the strength scores, and now an opinion can be represented as a 10-tuple or 8-tuple:

In summary, this section provides a possible direction for (RQ10) in Section 4.2. That is, we can evaluate the opinions based on their claims and premises.

5.3 Inferring Implicit Influence

Different from other argument mining tasks, with the nature in the financial domain, we can infer the implicit influence (abbreviated as hereafter) from an opinion. That is, the bullish opinion of certain financial instruments could be bearish information of the other financial instrument, and vise versa. This is also an issue of financial product/service. We illustrate the implicit influence of (E2) in Figure 2 (c). The claim (C1) in the example (E2) may also influence the other company in the semiconductor industry. Therefore, we can infer the implicit influence () based on the influence score(). The implicit influence can be represented as a 10-tuple as an opinion.

To sum, this section points out a research issue as follows:

(RQ13) How to infer the implicit influence embedded in an opinion?

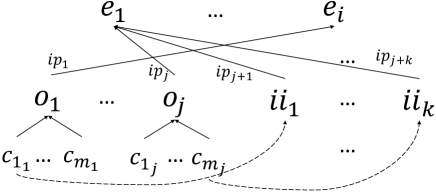

5.4 Retrieval and Summarization

Now, we complete the fine-grained opinion mining task on individual opinions. The next stage is to compare the opinions and provide a global view of certain financial instruments/products/services. We provide a directed graph in Figure 3. Here, we use the case in financial instruments as an example. Image that we are in the world with financial instruments (), investors’ opinions () with implicit influences (), and each investors’ opinion has claims. Each opinion node and implicit influence node have their own influence power () toward certain financial instruments. Now, an opinion can be shown as an 11-tuple or 9-tuple:

Based on the thought, some research questions emerge:

(RQ14) How to evaluate the influence power of an opinion?

(RQ15) What is the relationship between the influence power and other components?

Leveraging to the opinion 11-tuple and 9-tuple, we can retrieve the opinions based on different kinds of queries. For example, we can sort out the top 5 influential opinions of TSMC, which may be useful for analyzing the sales on June 2020 based on in the opinion 11-tuple.

With the directed graph between the entities and the opinion 11-tuple (9-tuple), we can prune the graph based on different components. We can only adopt the opinions that may influence our analysis of the target entity, or those are important to downside tasks.

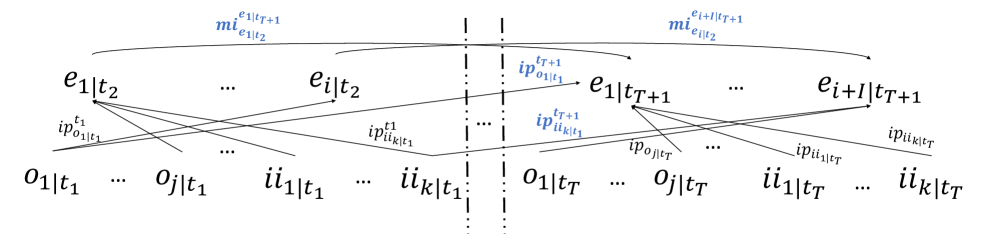

5.5 Tracing in Time Series

When analyzing financial data, time is one of the most important components that should be considered. Till now, we only discuss the opinion at a certain time, i.e., . However, the opinion at time will not influence the status of the target entity at time . As shown in Figure 4, the opinion at () may influence at time (), and is the influence power of to . Therefore, time is the condition of , and the toward different entities at different time can be shown as a set . Now, an opinion can be shown as follows:

With the concept of time series, there are three kinds of opinions may exist in time : (1) the new opinion in time , (2) the opinion in time continuing to exist in time , i.e, has not passed yet, and (3) the opinion in time changing at time . The opinion may be changed due to other opinions in time . That is, there exists an interaction between the opinions, and here arises the other research question:

(RQ16) How to evaluate or capture the interaction between the opinions?

The last interaction that we should consider is the one between , i.e., the entities. The status of at time may influence the status of itself at time and the status of other entities at time . The influence between entities is denoted as , market influence. It can be linked to the research question in the microeconomics field. Now, the overall picture from a financial opinion to the target entity is complete.

6 Blueprint — Solutions and Directions

6.1 Component Extraction

As we already showed, an opinion can be represented as an 11-tuple or a 9-tuple. We can obtain some of the components in the 11-tuple (9-tuple) via information extraction techniques. Because of many named entities, including , , , and , the NER task is the first step that we should consider. For the target entity, as shown in Figure 1, investors (both professional analysts in the institution and individual investors) have idioms for the target entity such as the ticker of the financial instruments (AAPL US EQUITY) on the Bloomberg Terminal and the cashtag ($AAPL) on StockTwits. For financial products or services, the number of entities is finite. Therefore, extracting the target entity may not be a challenge when dealing with financial textual data.

The identification of time expressions is more tackleable now. However, since a time expression may have different meanings, disambiguating the validity period could remain a challenging task. In the FinNum shared task Chen et al. (2019d), participants provide several useful features for understanding numeral information. That may be useful for inspiring future researches.

6.2 Relations of Components

Some components could be inferred based on other components. We list some examples as follows. The sentiment () and the degree of sentiment () could be deduced from the comparison between market information () and the fine-grained claims () such as price target. The opinion quality () could be analyzed based on the strength of the claims (). The influence power () could be a function of the opinion holder () and the opinion quality (). For example, the tweet of Donald John Trump, the president of the United States, may have a higher than that of a common person. The implicit influence () is also an interesting and complex research issue. We may need to leverage the ontologies such as the Financial Industry Business Ontology (FIBO)222https://spec.edmcouncil.org/fibo/index.html to construct the knowledge graph of the financial domain to deal with this issue.

6.3 Entity Status Evaluation and Prediction

Analyzing the status of is the final purpose of analyzing opinions. The status of could be the credit cards in circulation, the sales of the insurance, the quality of the customer service, the price of the stock, or the market information of any financial instrument/product/service. In Figure 3, we show that the current status of the entity can be formulated by the opinions related to it. This information could be used for evaluating the current reputation of the entity. As shown in Figure 4, it could also be the cue for predicting the future status of the entity.

Based on the discussions in this paper, we suggest the researchers interested in this field pay more attention to completing the opinion 11-tuple (9-tuple) and the proposed graph of financial opinions, and further provide an in-depth analysis of the relations between the target entities and the components. In this way, comparing with constructing an end-to-end model and focusing on the accuracy, things will become explainable and more rational.

7 Conclusion

This position paper provides a definition of fine-grained financial opinion and proposes the comprehensive directed graphs for real-world interaction between financial opinions and entities. In addition to a survey of the existing datasets and tasks, this paper indicates 16 research questions for future works and provide feasible research directions for them. We also indicate the important but untackled challenges in fine-grained financial opinion mining. Our intent is to depict a big picture for researchers who involve in expediting the development of this topic.

References

- Abirami and Gayathri [2017] AM Abirami and V Gayathri. A survey on sentiment analysis methods and approach. In ICoAC, pages 72–76. IEEE, 2017.

- Akhtar et al. [2019] Shad Akhtar, Deepanway Ghosal, Asif Ekbal, Pushpak Bhattacharyya, and Sadao Kurohashi. All-in-one: Emotion, sentiment and intensity prediction using a multi-task ensemble framework. IEEE Transactions on Affective Computing, 2019.

- Ali and Raza [2017] Muhammad Ali and Syed Ali Raza. Service quality perception and customer satisfaction in islamic banks of pakistan: the modified servqual model. Total Quality Management & Business Excellence, 28(5-6):559–577, 2017.

- Balikas et al. [2017] Georgios Balikas, Simon Moura, and Massih-Reza Amini. Multitask learning for fine-grained twitter sentiment analysis. In SIGIR, pages 1005–1008. ACM, 2017.

- Bollen and Mao [2011] Johan Bollen and Huina Mao. Twitter mood as a stock market predictor. Computer, 44(10):91–94, 2011.

- Burdick et al. [2019] Doug Burdick, Rajasekar Krishnamurthy, and Louiqa Raschid, editors. DSMM’19: Proceedings of the 5th Workshop on Data Science for Macro-Modeling with Financial and Economic Datasets, New York, NY, USA, 2019. ACM.

- Cabrio and Villata [2018] Elena Cabrio and Serena Villata. Five years of argument mining: a data-driven analysis. In IJCAI, pages 5427–5433, 2018.

- Chen et al. [2018a] Chung-Chi Chen, Hen-Hsen Huang, and Hsin-Hsi Chen. Ntusd-fin: a market sentiment dictionary for financial social media data applications. In FNP, 2018.

- Chen et al. [2018b] Chung-Chi Chen, Hen-Hsen Huang, Yow-Ting Shiue, and Hsin-Hsi Chen. Numeral understanding in financial tweets for fine-grained crowd-based forecasting. In WI, pages 136–143. IEEE, 2018.

- Chen et al. [2019a] Chung-Chi Chen, Hen-Hsen Huang, and Hsin-Hsi Chen. Crowd view: converting investors’ opinions into indicators. In IJCAI, 2019.

- Chen et al. [2019b] Chung-Chi Chen, Hen-Hsen Huang, and Hsin-Hsi Chen. Numeral attachment with auxiliary tasks. In SIGIR, pages 1161–1164. ACM, 2019.

- Chen et al. [2019c] Chung-Chi Chen, Hen-Hsen Huang, Hiroya Takamura, and Hsin-Hsi Chen. Numeracy-600K: Learning numeracy for detecting exaggerated information in market comments. In ACL, pages 6307–6313, Florence, Italy, July 2019. Association for Computational Linguistics.

- Chen et al. [2019d] Chung-Chi Chen, Hen-Hsen Huang, Hiroya Takamura, and Hsin-Hsi Chen. Overview of the ntcir-14 finnum task: Fine-grained numeral understanding in financial social media data. In NTCIR, pages 19–27, 2019.

- Chen et al. [2019e] Chung-Chi Chen, Hen-Hsen Huang, Hiroya Takamura, and Hsin-Hsi Chen, editors. Proceedings of the First Workshop on Financial Technology and Natural Language Processing, Macao, China, August 2019.

- Chen et al. [2020] Chung-Chi Chen, Hen-Hsen Huang, and Hsin-Hsi Chen. Issues and Perspectives from 10,000 Annotated Financial Social Media Data. In Proceedings of the Twelfth International Conference on Language Resources and Evaluation (LREC 2020). European Language Resources Association (ELRA), 2020.

- Chiranjeevi et al. [2019] P Chiranjeevi, D Teja Santosh, and B Vishnuvardhan. Survey on sentiment analysis methods for reputation evaluation. In Cognitive Informatics and Soft Computing, pages 53–66. Springer, 2019.

- Cortis et al. [2017] Keith Cortis, André Freitas, Tobias Daudert, Manuela Huerlimann, Manel Zarrouk, Siegfried Handschuh, and Brian Davis. Semeval-2017 task 5: Fine-grained sentiment analysis on financial microblogs and news. In SemEval, pages 519–535, 2017.

- Das and others [2014] Sanjiv Ranjan Das et al. Text and context: Language analytics in finance. Foundations and Trends® in Finance, 2014.

- Devlin et al. [2019] Jacob Devlin, Ming-Wei Chang, Kenton Lee, and Kristina Toutanova. BERT: Pre-training of deep bidirectional transformers for language understanding. In NAACL, pages 4171–4186, Minneapolis, Minnesota, June 2019. Association for Computational Linguistics.

- E. et al. [2018] Shijia E., Li Yang, Mohan Zhang, and Yang Xiang. Aspect-based financial sentiment analysis with deep neural networks. In WWW, WWW ’18, page 1951–1954, Republic and Canton of Geneva, CHE, 2018. International World Wide Web Conferences Steering Committee.

- Feng et al. [2019] Fuli Feng, Huimin Chen, Xiangnan He, Ji Ding, Maosong Sun, and Tat-Seng Chua. Enhancing stock movement prediction with adversarial training. In IJCAI, pages 5843–5849. AAAI Press, 2019.

- Fisher et al. [2016] Ingrid E Fisher, Margaret R Garnsey, and Mark E Hughes. Natural language processing in accounting, auditing and finance: A synthesis of the literature with a roadmap for future research. Intelligent Systems in Accounting, Finance and Management, 23(3):157–214, 2016.

- Hahn et al. [2019] Udo Hahn, Véronique Hoste, and Zhu Zhang, editors. Proceedings of the Second Workshop on Economics and Natural Language Processing, Hong Kong, November 2019. ACL.

- Hu et al. [2018] Ziniu Hu, Weiqing Liu, Jiang Bian, Xuanzhe Liu, and Tie-Yan Liu. Listening to chaotic whispers: A deep learning framework for news-oriented stock trend prediction. In WSDM, pages 261–269. ACM, 2018.

- Hussein [2018] Doaa Mohey El-Din Mohamed Hussein. A survey on sentiment analysis challenges. Journal of King Saud University-Engineering Sciences, 30(4):330–338, 2018.

- Jebaseeli and Kirubakaran [2012] A Nisha Jebaseeli and E Kirubakaran. A survey on sentiment analysis of (product) reviews. International Journal of Computer Applications, 47(11), 2012.

- Jiang et al. [2017] Mengxiao Jiang, Man Lan, and Yuanbin Wu. ECNU at SemEval-2017 task 5: An ensemble of regression algorithms with effective features for fine-grained sentiment analysis in financial domain. In SemEval, pages 888–893, Vancouver, Canada, August 2017. Association for Computational Linguistics.

- Kharde and Sonawane [2016] Vishal A Kharde and SS Sonawane. Sentiment analysis of twitter data: A survey of techniques. International Journal of Computer Applications, 975:8887, 2016.

- Kumar and Ravi [2016] B Shravan Kumar and Vadlamani Ravi. A survey of the applications of text mining in financial domain. Knowledge-Based Systems, 114:128–147, 2016.

- Lawrence and Reed [2019] John Lawrence and Chris Reed. Argument mining: A survey. Computational Linguistics, pages 1–54, 2019.

- Li and Shah [2017] Quanzhi Li and Sameena Shah. Learning stock market sentiment lexicon and sentiment-oriented word vector from stocktwits. In Proceedings of the 21st Conference on Computational Natural Language Learning (CoNLL 2017), pages 301–310, 2017.

- Li et al. [2019] Zuhe Li, Yangyu Fan, Bin Jiang, Tao Lei, and Weihua Liu. A survey on sentiment analysis and opinion mining for social multimedia. Multimedia Tools and Applications, 78(6):6939–6967, 2019.

- Liu [2015] Bing Liu. Sentiment analysis: Mining opinions, sentiments, and emotions. Cambridge University Press, 2015.

- Loughran and McDonald [2009] Tim Loughran and Bill McDonald. When is a liability not a liability. Journal of Finance, forthcoming, 2009.

- Mahmoud El-Haj et al. [2019] Mahmoud El-Haj, Paul Rayson, Steven Young, Houda Bouamor, and Sira Ferradans, editors. Proceedings of the Second Financial Narrative Processing Workshop (FNP 2019), Turku, Finland, September 2019. Linköping University Electronic Press.

- Maia et al. [2018] Macedo Maia, Siegfried Handschuh, André Freitas, Brian Davis, Ross McDermott, Manel Zarrouk, and Alexandra Balahur. Www’18 open challenge: Financial opinion mining and question answering. In WWW, pages 1941–1942. International World Wide Web Conferences Steering Committee, 2018.

- Oliveira et al. [2016] Nuno Oliveira, Paulo Cortez, and Nelson Areal. Stock market sentiment lexicon acquisition using microblogging data and statistical measures. Decision Support Systems, 85:62–73, 2016.

- Pang et al. [2008] Bo Pang, Lillian Lee, et al. Opinion mining and sentiment analysis. Foundations and Trends® in Information Retrieval, 2(1–2):1–135, 2008.

- Potluri et al. [2016] Rajasekhara Mouly Potluri, Srinivas Rao Angati, and M Srinivasa Narayana. A structural compendium on service quality and customer satisfaction: A survey of banks in india. Journal of Transnational Management, 21(1):12–28, 2016.

- Pradhan et al. [2016] Vidisha M Pradhan, Jay Vala, and Prem Balani. A survey on sentiment analysis algorithms for opinion mining. International Journal of Computer Applications, 133(9):7–11, 2016.

- Qin and Yang [2019] Yu Qin and Yi Yang. What you say and how you say it matters: Predicting stock volatility using verbal and vocal cues. In ACL, pages 390–401, Florence, Italy, July 2019. ACL.

- Renault [2019] Thomas Renault. Sentiment analysis and machine learning in finance: a comparison of methods and models on one million messages. Digital Finance, pages 1–13, 2019.

- Sedinkina et al. [2019] Marina Sedinkina, Nikolas Breitkopf, and Hinrich Schütze. Automatic domain adaptation outperforms manual domain adaptation for predicting financial outcomes. In ACL, pages 346–359, Florence, Italy, July 2019. ACL.

- Soong et al. [2019] Hoong-Cheng Soong, Norazira Binti A Jalil, Ramesh Kumar Ayyasamy, and Rehan Akbar. The essential of sentiment analysis and opinion mining in social media: Introduction and survey of the recent approaches and techniques. In ISCAIE, pages 272–277. IEEE, 2019.

- Tedmori and Awajan [2019] Sara Tedmori and Arafat Awajan. Sentiment analysis main tasks and applications: A survey. Journal of Information Processing Systems, 15(3), 2019.

- Tomar and Tomar [2019] Deepika Singh Tomar and Rohit Singh Tomar. Comparative analysis of service quality perception between public sector and private sector banks of india. In Behavioral Finance and Decision-Making Models, pages 117–138. IGI Global, 2019.

- Valencia et al. [2019] Franco Valencia, Alfonso Gómez-Espinosa, and Benjamín Valdés-Aguirre. Price movement prediction of cryptocurrencies using sentiment analysis and machine learning. Entropy, 21(6):589, 2019.

- Wang et al. [2015] Gang Wang, Tianyi Wang, Bolun Wang, Divya Sambasivan, Zengbin Zhang, Haitao Zheng, and Ben Y. Zhao. Crowds on wall street: Extracting value from collaborative investing platforms. In CSCW, CSCW ’15, page 17–30, New York, NY, USA, 2015. Association for Computing Machinery.

- Wang et al. [2019] Wei Wang, Maofu Liu, Yukun Zhang, Junyi Xiang, and Ruibin Mao. Financial numeral classification model based on bert. In Makoto P. Kato, Yiqun Liu, Noriko Kando, and Charles L. A. Clarke, editors, NII Testbeds and Community for Information Access Research, pages 193–204, Cham, 2019. Springer International Publishing.

- Xu and Cohen [2018] Yumo Xu and Shay B. Cohen. Stock movement prediction from tweets and historical prices. In ACL, pages 1970–1979, Melbourne, Australia, July 2018. Association for Computational Linguistics.

- Yang et al. [2020] Linyi Yang, Tin Lok James Ng, Barry Smyth, and Riuhai Dong. Html: Hierarchical transformer-based multi-task learning for volatility prediction. In Proceedings of The Web Conference 2020, pages 441–451, 2020.

- Zheng et al. [2019] Shun Zheng, Wei Cao, Wei Xu, and Jiang Bian. Doc2EDAG: An end-to-end document-level framework for Chinese financial event extraction. In EMNLP-IJCNLP, pages 337–346, Hong Kong, China, November 2019. ACL.