The Murphy Decomposition and the Calibration-Resolution Principle: A New Perspective on Forecast Evaluation††thanks: Acknowledgements: I thank Uwe Hassler and Patrick Schmidt for helpful comments. Earlier versions of this paper were presented at DAGStat 2019 in Munich and the International Symposium on Forecasting 2019 in Thessaloniki.

Abstract

I provide a unifying perspective on forecast evaluation, characterizing accurate forecasts of all types, from simple point to complete probabilistic forecasts, in terms of two fundamental underlying properties, autocalibration and resolution, which can be interpreted as describing a lack of systematic mistakes and a high information content. This “calibration-resolution principle” gives a new insight into the nature of forecasting and generalizes the famous sharpness principle by Gneiting et al. (2007) from probabilistic to all types of forecasts. It amongst others exposes the shortcomings of several widely used forecast evaluation methods. The principle is based on a fully general version of the Murphy decomposition of loss functions, which I provide. Special cases of this decomposition are well-known and widely used in meteorology.

Besides using the decomposition in this new theoretical way, after having introduced it and the underlying properties in a proper theoretical framework, accompanied by an illustrative example, I also employ it in its classical sense as a forecast evaluation method as the meteorologists do: As such, it unveils the driving forces behind forecast errors and complements classical forecast evaluation methods. I discuss estimation of the decomposition via kernel regression and then apply it to popular economic forecasts. Analysis of mean forecasts from the US Survey of Professional Forecasters and quantile forecasts derived from Bank of England fan charts indeed yield interesting new insights and highlight the potential of the method.

Keywords: Autocalibration; Resolution; Sharpness Principle; Survey of Professional Forecasters; Bank of England Fan Charts

1 Introduction

High-quality forecasts are the basis for sound decision-making. Probabilistic forecasts, i.e. forecasts of the full distribution of the variable of interest, give the complete picture and have become increasingly popular in recent years (see e.g. Gneiting and Katzfuss (2014)), but are often difficult to obtain. Point forecasts transport a limited amount of information, but are easier to construct and are still the most widely issued type of forecast in many disciplines. Interval forecasts provide a good compromise between the two. No matter of what type the forecasts are, forecast evaluation plays a crucial role in the provision of good forecasts, detecting the strengths and weaknesses of forecasters or forecasting methods and guiding them towards possible improvements.

The standard method for evaluating the most common types of forecasts, namely mean and median forecasts, is the measurement of their accuracy via a suitable loss function. In contrast to that, traditional methods for the evaluation of quantile or interval forecasts are tests of unconditional or conditional exceedance or coverage (see e.g. Christoffersen (1998)), which are tests of optimality relative to some information set.111Optimality tests are also common for other types of forecasts, (see e.g. Elliott and Timmermann (2016, chapter 15)), for example mean forecasts, but certainly not the main method of evaluation. For probabilistic forecasts, a widely used traditional method of evaluation is the assessment of uniformity of the probability integral transform [PIT] (see e.g. Dawid (1984) or Diebold et al. (1998)).

Taking a general perspective on forecast evaluation, in seminal work, Gneiting and Ranjan (2013) and Gneiting and Raftery (2007) advocate the evaluation of all types of forecasts via suitable loss functions, namely consistent scoring functions for point forecasts and proper scoring rules for probabilistic forecasts. In other words, they put forward the assessment of forecast accuracy as the base of forecast evaluation for all types of forecasts and stress the importance of the use of loss functions appropriate for the respective type.

Focusing on the evaluation of probabilistic forecasts, in a related paper Gneiting et al. (2007) criticize the sole use of the PIT for evaluating such forecasts and conjecture the so-called sharpness principle, stating that good probabilistic forecasts should maximize sharpness, i.e. concentration of the predictive distribution, subject to calibration, and thereby characterizing accurate forecasts in terms of fundamental underlying properties. Tsyplakov (2011) later proves the principle after specifying that the required notion of calibration is autocalibration. However, while considering the principle as very interesting from a theoretical point of view, he puts into question its practical usefulness as its applicability relies on the forecasts being perfectly autocalibrated. Nevertheless, the sharpness principle has been very influential for the theory and practice of the evaluation of probabilistic forecasts over the last years.

Accompanying this principle by diagnostic tools for the evaluation of calibration and sharpness and again advocating the use of proper scoring rules, Gneiting et al. (2007) strive to set up a general framework for probabilistic forecasts in the tradition of Murphy and Winkler (1987), who proposed a general framework for the evaluation of point forecasts. Murphy and Winkler (1987) emphasized the analysis of features of the joint distribution of forecasts and observations to complement predictive accuracy assessment to gain deeper insights into the strengths and weaknesses of forecasting methods and to finally improve them.222Note that they had mainly probability forecasts of binary events and categorical variables and mean forecasts in mind and not the more complicated quantile, interval or distributional forecasts, for which Gneiting and Ranjan (2013) and Gneiting and Raftery (2007) had to stress years later that the base of forecast evaluation should be the measurement of predictive accuracy. The article shaped the meteorological forecast evaluation (or verification as it is called there) literature, which still uses partly quite different methods than statisticians or econometricians, putting a larger emphasis on properties of the joint distribution of forecasts and observations or on conditional distributions of one given the other (see e.g. Wilks (2011) or Jolliffe and Stephenson (2012) for overviews).

In this work I on the one hand provide a generalization of the sharpness principle by characterizing the accuracy of all types of forecasts, including point forecasts, by underlying theoretical properties and discuss implications of this. On the other hand, I show that the use and the advancement of forecast evaluation methods from the meteorological literature, which emphasize the use of such underlying properties in the spirit of Murphy and Winkler (1987), are beneficial also for other disciplines by applications to popular economic forecasts.

Both of this is based on a fully general version of the Murphy decomposition from meteorology, which decomposes the forecasting loss into three components: Uncertainty, representing the variation in the outcome variable, resolution, which describes the ability of the forecasts to distinguish between different outcomes, and mis(auto)calibration. (Auto)calibration refers to the statistical consistency between forecasts and observations. Resolution can also be interpreted as measuring the informational content of the forecasts and autocalibration as freedom from systematic forecasting mistakes. The decomposition was originally proposed by Murphy (1973) for the case of a probability forecast for a binary event using the Brier score as a loss function. This original version of the decomposition has been vividly used in meteorology as a forecast evaluation method (see again e.g. Wilks (2011) or Jolliffe and Stephenson (2012)) and has also spread to other disciplines like psychology (see e.g. Slovic et al. (1977) or Koriat et al. (1980)). In the statistical and econometric forecast evaluation literature, the decomposition is not very well known, see Diebold and Lopez (1996) and Elliott and Timmermann (2016) for two exceptions in the form of a handbook article and a book respectively. To the best of my knowledge the only two papers from statistics or econometrics that apply the decomposition (to economic data) are Galbraith and van Norden (2012) and Lahiri and Wang (2013). Despite presenting very interesting results, these papers are limited to probability forecasts for binary events and it is certainly of interest to analyze decompositions for other types of forecasts like mean forecasts of continuous variables, quantile or interval forecasts or even full distributional forecasts. The meteorological literature has progressed in this direction: Focussing on a specific loss function, Murphy (1996) introduces the decomposition for the case of mean forecasts and quadratic loss, Hersbach (2000) introduces it for distributional forecasts and the continuous ranked probability score, Tödter and Ahrens (2012) introduce it for variants of the logarithmic score and Bentzien and Friederichs (2014) introduce it for quantile forecasts and the quantile score. Aiming at more general classes of loss functions, Broecker (2009) treats proper scoring rules for discrete distributional forecasts and Ehm and Ovcharov (2017) treat consistent scoring functions. I provide the fully general version of the decomposition, which captures all types of forecasts that can be evaluated by a consistent scoring function or a proper scoring rule.

While the Murphy decomposition has only been used empirically so far, i.e. as a forecast evaluation method, in the first part of the paper I use it in a theoretical way. I point out that it yields a generalization of the influential sharpness principle by Gneiting et al. (2007) to all types of forecasts, which I call the “calibration-resolution principle” and show that the sharpness principle indeed arises as a special case for autocalibrated probabilistic forecasts. The new principle thus on the one hand solves the above-mentioned problem that the sharpness principle is only applicable for autocalibrated forecasts, which could be even more severe as Tsyplakov (2011) thought due to a possible trade-off between maximizing resolution and minimizing miscalibration that a forecaster could often face in practice as I argue. On the other hand point forecasts are captured by the new principle, too. The calibration-resolution principle characterizes accurate forecasts in terms of two fundamental underlying properties, gives us a better understanding of the nature of forecasting and a new way to think about what it means to construct accurate forecasts, namely jointly maximizing information content and minimizing systematic mistakes.

Demonstrating that the principle can foster our understanding of forecast evaluation in general, I consider some widely-used traditional forecast evaluation methods, e.g. the PIT or the assessment of conditional and unconditional exceedance or coverage, some of which have already been criticized in the literature (see e.g. Hamill (2001), Gneiting et al. (2007), Holzmann and Eulert (2014) or Nolde and Ziegel (2017)). From the angle of the calibration-resolution principle I point out that all of these methods assess some form of calibration, but do not capture the information content of the forecasts, resulting in an incomplete evaluation if used as a sole evaluation method. Furthermore, I discuss the relationship between optimality testing and calibration.

Before introducing the calibration-resolution principle and drawing conclusions from it in the third section of this paper, I set up the basic framework and carefully introduce autocalibration and resolution in the second section: I pay special attention to explicitly modelling the time series and information structure and to introducing the concept of resolution, which is hardly known outside of the meteorological literature. Furthermore, I provide two justifications for interpreting resolution as a measure of information content: I firstly show that if the information contained in a forecast is larger than the one contained in another forecast, resolution is higher for that forecast. Secondly, I derive a generalization of the total variance formula, where resolution equals the term which generalizes the explained part of the variance. To illustrate the ideas behind autocalibration and especially resolution and to make clear which dimensions of forecast quality they capture and how they complement each other, I use a theoretical example comprising several stylized versions of forecasters, which builds on an example from Gneiting et al. (2007). This example also illustrates the Murphy decomposition and enriches the discussion of the sharpness and the calibration-resolution principle.

In the fourth section, I use the Murphy decomposition in the (at least for meteorologists) classical way, as a forecast evaluation method, and highlight its potential as a complement to standard forecast evaluation techniques usually applied in statistics and econometrics due to the new insights it yields by applying it to popular examples of economic forecasts. The decomposition unveils the driving forces behind forecast errors, showing whether they are mainly caused by systematic mistakes or a lack of information content and where improvements are needed. It also monitors the fall in information content with rising forecast horizon and uncovers the forecast horizon up to which the forecasts contain usual information at all, giving hints on the limits of forecastability.

At the beginning of the fourth section I discuss estimation of the decomposition terms, for which conditional functionals of the predictive distribution given the forecasts, e.g. conditional quantiles or the conditional expectation have to be estimated. I concentrate on point forecasts here as for probabilistic forecasts conditioning variables are high-dimensional and the estimation is in general problematic due to the curse of dimensionality. While the meteorologists use naive methods based on binning, I employ local linear kernel regressions, where the suitable consistent scoring functions should be used as the respective regression loss functions, e.g. for estimating conditional means least-squares kernel regression and for estimating conditional quantiles quantile regression are the right choices. Note that Galbraith and van Norden (2011) use local constant kernel regressions for estimating conditional probabilities of a binary event in a similar context.

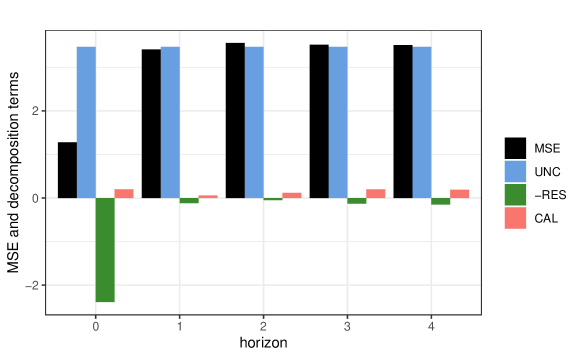

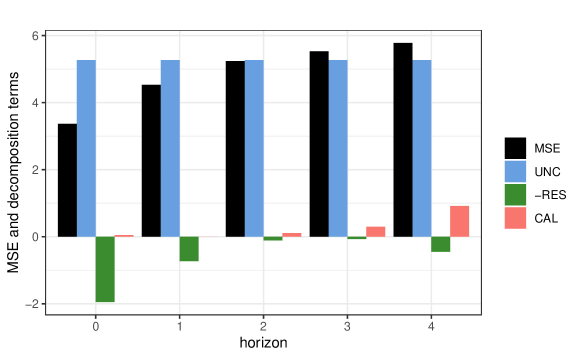

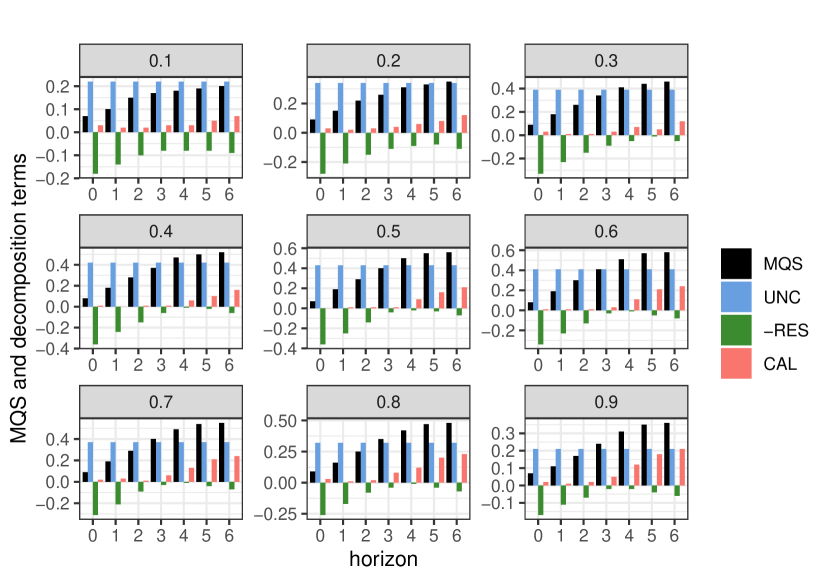

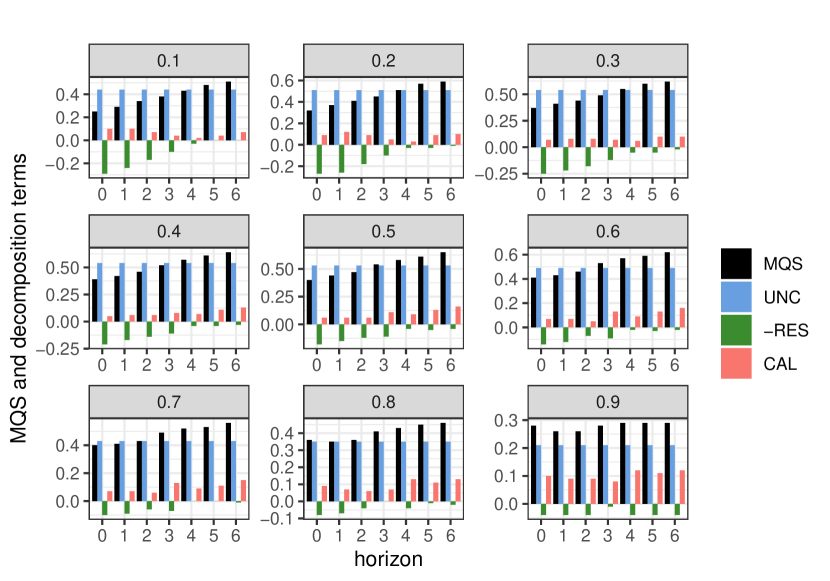

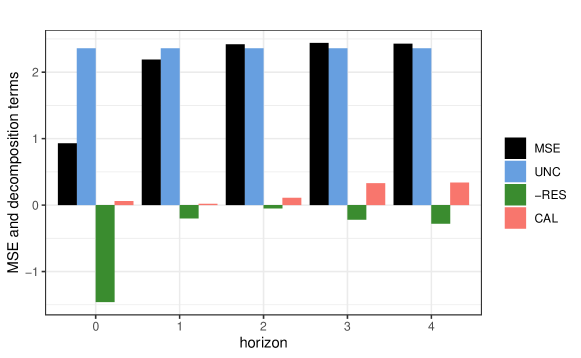

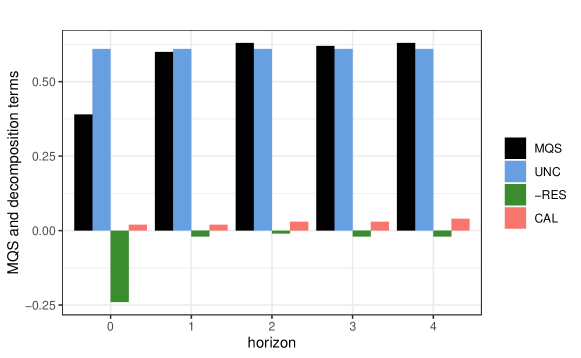

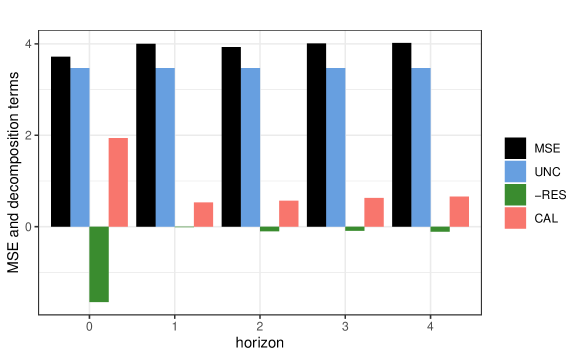

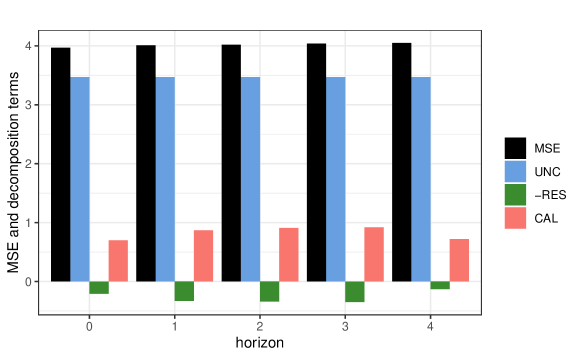

Subsequently I apply the general form of the decomposition to economic forecasts for the first time. The applications are to mean forecasts of inflation and GDP growth from the US Survey of Professional Forecasters [SPF] and to quantile forecasts obtained from the probabilistic inflation and GDP growth forecasts issued by the Bank of England [BoE]. The former show no signs of miscalibration and I can trace back their huge drop in performance from nowcasts to one-quarter-ahead forecasts to a lack of resolution. Despite the lack of resolution, they clearly outperform the classical benchmark in the form of autoregressive [AR] models, hinting to the inherent difficulty of this forecasting problem.

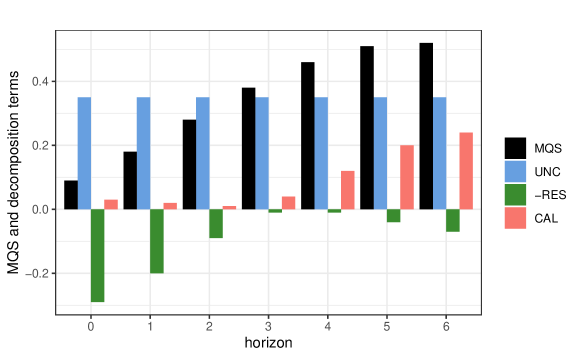

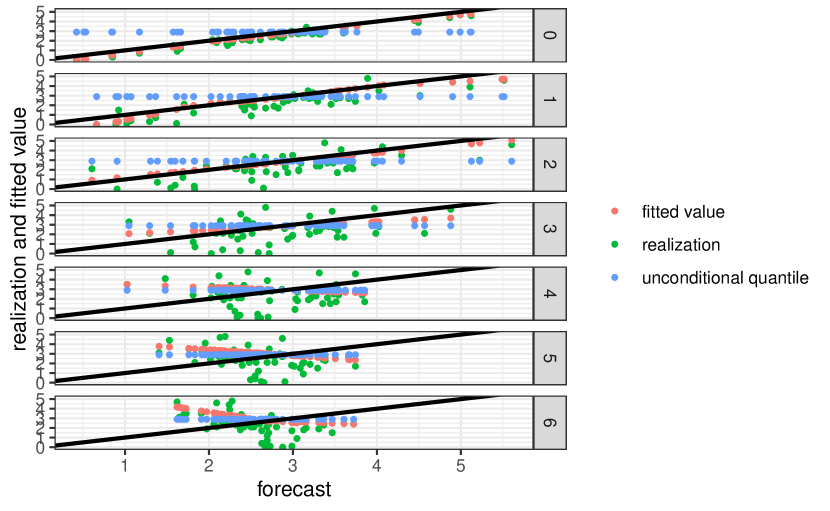

The BoE’s probabilistic forecasts, which I evaluate over a range of quantiles, show a diverse pattern in terms of the decomposition with multiple interesting insights: For both variables at most quantiles there is considerable resolution for the shorter forecast horizons, which gradually declines towards zero and often a rise in miscalibration from then on. Furthermore, substantial differences between the quantiles can be observed, where the forecasts are better at the lower parts of the distribution and deteriorate towards the upper parts. However, the inflation forecasts contain much more information content and (as is analyzed in Pohle (2020a)) clearly outperform relevant benchmarks, while the GDP growth forecasts are sometimes outperformed by a benchmark, namely the quantile autoregressive [QAR] model, indicating potential for improvement.

The fifth section sketches ideas for future research and forecast evaluation practice and concludes. The appendix contains in four parts proofs, calculations for the illustrative example used throughout the paper, details on robustness checks and benchmark forecasts and details on the probabilistic forecasts issued by the BoE and how to calculate quantiles from them.

2 Fundamentals, Autocalibration and Resolution

Even though forecast accuracy, characterized by closeness between forecasts and observations in terms of a suitable loss function, is the primary criterion for evaluating forecasts, many other properties that characterize good forecasts exist. Examining those properties may yield valuable additional insights and lead to improved and in turn more accurate forecasts as Murphy and Winkler (1987) stress in their influential paper. Due to the influence of this paper on the meteorological forecast evaluation literature, such fundamental properties as (auto)calibration and resolution are widely used there, but hardly known in other disciplines. In this section I thus introduce these two properties, justify their use and illustrate them by a theoretical example. While they are very interesting for forecast evaluation on their own right, the next section demonstrates via the so-called calibration-resolution principle that they are intimately related to forecast accuracy, which makes them even more relevant. To set the stage for the rest of the paper I first introduce the basic setup, review relevant classes of loss functions and the concepts of entropy and divergence.

2.1 Basic Setup

In a time series or sequential prediction problem a forecaster tries to predict a variable of interest over one or several forecasting horizons given certain information in every period. All other variables which may contain relevant information concerning are summarized in the possibly very large vector . The forecaster’s target may be to forecast the whole distribution of , then he is called a probabilistic forecaster, or some functional of it, e.g. the mean or a certain quantile.

To make the sequential nature of the problem and the information structure explicit, consider the real-valued time series and . Denote the -algebra containing all the information at time , i.e. , the -algebra generated by the history of and . A forecaster who tries to predict periods into the future at time has access to a certain information set . may be continuous or discrete (with the important binary special case) random variables.

A probabilistic forecaster trying to predict with a forecast horizon issues a forecast distribution or predictive distribution , which is his or her best guess of the true distribution of based on the given information contained in , . The goal of a forecaster in general is to predict a functional of , which he or she does by reporting the respective functional of his or her forecast distribution . Most often a point forecast is required, e.g. a mean forecast with target functional or a quantile forecast, where the functional is a certain quantile , . The functionals could be set-valued as e.g. in the case of quantiles of discrete distributions, but to streamline the discussion we assume unique functionals, noting that non-unique ones can be easily accounted for. The forecast targets may also be prediction intervals or histogram-type forecasts, which lead to vector-valued functionals, or of course the whole distribution.333As mentioned in the introduction, probability forecasts of a binary event do also frequently appear. Here, is a binary random variable and the goal is thus to forecast the parameter of a Bernoulli distribution, which is at the same time the expected value and characterizes the whole distribution, i.e. in this important special case the forecast is a point forecast and a distributional forecast at the same time. In all these cases, I will use the notation , no matter if maps to the real numbers, a vector of real numbers or (for a probabilistic forecaster) to a density function or back to the distribution function itself. Furthermore, to simplify notation, I denote the forecast, no matter of what type it is, as . This leads to a sequence of forecasts . The information contained in the forecast is represented by , the -algebra generated by it.

Note that even though I talk about a time series prediction problem here, cross-sectional forecasting problems are of course nested as a special case. The theory and methods laid out in this paper can be fruitfully applied to such problems, even a very large vector of explanatory variables poses no problems, but on the contrary could make the results obtained even more interesting.

2.2 Loss Functions

The goal of forecast evaluation is to assess the quality of forecasts, which may have been obtained by any forecasting method, be it model-based or not. An indispensable step in the forecast evaluation process is measuring forecast accuracy via a suitable loss function. Loss functions also play a fundamental role in this paper. Thus, I review the relevant classes now.

In the statistical forecast evaluation literature, a loss function mapping a realized forecast-observation pair onto the real numbers is called a scoring function if is a point forecast, i.e. if the underlying functional is one-dimensional, and a scoring rule if is a distributional or an interval forecast (see e.g. Gneiting and Raftery (2007), Gneiting (2011) and Gneiting and Katzfuss (2014)). I define the loss functions as nonnegative and negatively oriented as is common in the literature. The forecaster’s aim thus is to minimize , the expected score conditional on the given information set by choosing the forecast . A scoring function is called consistent or a scoring rule proper for the functional if this functional of the true conditional distribution of the outcome variable minimizes the expected score given the available information, formally if

for all forecasts , which are constructed on the basis of this information, i.e. which are -measurable, and strictly consistent or proper if equality holds only for . This requirement makes sure that the forecaster has no incentive to deviate from his true beliefs to possibly improve the score and is maintained throughout the rest of the paper.

The necessity of giving a clear directive to the forecaster in form of a statistical functional and to evaluate these forecasts by a suitable consistent scoring function is stressed e.g. by Gneiting (2011). A functional is called elicitable if there exists a scoring function that is strictly consistent for it (see Lambert et al. (2008) for details). All functionals that are used in this paper are elicitable. A prominent example of a non-elicitable functional is the mode (see Heinrich (2013)). Note that usually (infinitely) many consistent scoring functions exist for the same functional (see e.g. Ehm et al. (2016) for details).

The most prominent example for a consistent scoring function is certainly the squared error for mean forecasts,

| (1) |

A consistent scoring function for quantile forecasts is the check function well-known from quantile regression applied to the forecast error, also called quantile score:

| (2) |

A popular example for a proper scoring rule is the logarithmic score: Given a forecast in the form of a density , i.e. , the logarithmic score is

The accuracy of a forecaster or a forecasting method is measured by the expected score or loss

For the example of the squared error expected loss amounts to the mean squared (forecast) error

For the quantile and the logarithmic score expected loss is represented by the mean quantile score,

and the mean logarithmic score,

respectively.

Throughout the paper, I will tacitly assume that the expected loss and the other measures of fundamental properties of forecasts and and of the process itself , which are defined below in terms of expectations over loss functions or differences of loss functions, exist, i.e. that the loss functions and the joint distributions of forecasts and observations are sufficiently well-behaved, and that they are constant over time, i.e. that the bivariate time series of forecasts and observations fulfils a suitable form of stationarity to guarantee constancy of the occurring unconditional and conditional functionals and showing up later in these terms.

2.3 Entropy and Divergence

To define measures of (mis)autocalibration and resolution and to write down the Murphy decomposition for general loss functions, a general measure of uncertainty for a random variable and a distance measure between a real number (which can be interpreted as a forecast of for our purposes) and a functional of , , using consistent scoring functions and proper scoring rules are needed. The generalized entropy and divergence (see Gneiting and Raftery (2007) and references therein) are suitable for this purpose.

For a random variable with distribution function the generalized entropy is defined as

It measures the expected score achieved by the ideal forecast ,555More details on the definition of ideal forecasts follow in the next subsection. i.e. the minimal achievable expected score. It generalizes the classical entropy from information theory as well as the variance and serves as a measure of the inherent uncertainty in : For a distributional forecast in the form of a density function and the logarithmic score as proper scoring rule the classical entropy arises and for a mean forecast with the squared error as a consistent scoring function the variance arises.

For a forecast of the divergence between this forecast and the ideal forecast is defined as666Note that divergence is not a metric, lacking symmetry and the triangle inequality.

It is the expected difference in scores achieved by and the optimal forecast. By the definition of consistent scoring functions or proper scoring rules respectively divergence is nonnegative. For the logarithmic score, the Kullback-Leibler divergence arises as a special case and for the squared error, the squared bias comes up.

The expected score of can trivially be decomposed into entropy and divergence, leading to a generalized bias-variance decomposition for the forecasts of the random variable , which expresses the expected score as the uncertainty in plus deviations of from the ideal forecast:

| (3) |

2.4 Autocalibration

Calibration describes the statistical compatibility between forecasts and observations. Different notions of calibration exist in the statistical literature, for recent work classifying them and clarifying their relationship see Gneiting and Ranjan (2013) and Tsyplakov (2014).

Ideally calibrated or ideal forecasts are constructed from the true conditional distribution, i.e. a forecast is ideal relative to the information set if

holds (see e.g. Gneiting and Ranjan (2013) and Tsyplakov (2014)).

As it is usually difficult to reconstruct the exact information available to the forecaster, a more practicable approach is to condition on , the information contained in the forecasts themselves, instead of on :777Note that I use the usual shorthand notation to denote

Definition 1 (Autocalibration, see Tsyplakov (2011) and Gneiting and Ranjan (2013)).

Forecasts that are ideal with respect to the information contained in themselves,

are called autocalibrated.

Of course is generally a richer information set, , and may contain some relevant information that has been overlooked by the forecaster. Nevertheless, in practice this is very hard to assess. Furthermore, ideal calibration implies autocalibration and thus if we detect deviations from autocalibration, the forecasts are not ideally calibrated. In the meteorological literature, autocalibration is simply known as calibration or reliability and is routinely assessed, especially for binary probability forecasts. As will become clear throughout the paper, autocalibration appears naturally within the context of the sharpness principle conjectured by Gneiting et al. (2007) and in the Murphy decomposition. The notion of calibration from the statistical and meteorological literature is closely related to the notion of forecast optimality from the econometric literature (see e.g. Elliott and Timmermann (2016, chapter 15) for an overview). Forecast optimality is essentially equivalent to ideal calibration and the popular Mincer-Zarnowitz regression (see Mincer and Zarnowitz (1969)) well-known and widely used in economic forecast evaluation (implicitly) assesses autocalibration of mean forecasts, . Other related, but weaker forms of calibration as marginal and probabilistic calibration exist (see again Gneiting and Ranjan (2013) or Tsyplakov (2014)).

A natural measure to assess deviations from autocalibration is what I naturally call the conditional divergence between the forecast and the autocalibrated forecast :

where I define

as the conditional entropy, which is disussed in more detail below.

An overall measure of mis(auto)calibration is the expectation of this conditional divergence:

Definition 2 (Miscalibration).

The overall measure of miscalibration is defined as

Special cases of have appeared in the literature, see the overview of previous work on special cases of the Murphy decomposition in the introduction. The same holds true for the measure of resolution introduced below. is nonnegative due to consistency of scoring functions or propriety of scoring rules respectively and equals zero for autocalibrated forecasts. Note that the first representation of containing the conditional divergence is more useful in terms of theoretical interpretation, while the second term, where the law of iterated expectations has been applied to get rid of the conditioning is more useful in terms of estimation and will be used later on for that purpose. In the example of the squared error, just measures the expected squared conditional bias

In addition to calculating the overall measure of miscalibration , miscalibration can also be assessed in detail over the whole range of forecast values. This is best done graphically (at least for point forecasts) by what is called a reliability diagram or calibration plot in meteorology for the special case of binary probability forecasts (see e.g. Wilks (2011, chapter 7)), where observed event frequencies are plotted against binned forecasted event probabilities. The generalization to mean or other point forecasts is straightforward by plotting the estimated conditional functionals against the possible values of the forecasts . For autocalibrated forecasts the graph is on the diagonal as holds and for miscalibrated forecasts the miscalibration pattern is illustrated by the deviations from the diagonal.

Assessing autocalibration over the range of values of may uncover systematic mistakes in the forecasts, which could make a correction of these mistakes possible in the future. This process is called recalibration in meteorology. If for example the inflation outcomes averaged to three percent whenever a forecaster forecasted two percent for the mean, this would mean to just always add one percent to his forecasts in these cases to recalibrate him or her. As easy as recalibration sounds in theory, in practice this would require exactly knowing the systematic mistakes, e.g. the estimation error and deviations from the true model. Of course this knowledge about the joint distribution of forecasts and observations could be observed over time, but this is probably done by very few forecasters and additional real-world problems like structural change may complicate matters. As will be illustrated in the empirical part of the paper, especially for other distributional features than the mean, it may be difficult to construct autocalibrated forecasts and diverse patterns and large values of miscalibration can be observed in practice.

To assess autocalibration in practice, first the conditional functionals , e.g. , have to be estimated. Estimation methods will be discussed in section 4 of this paper.

Example (Part 1: Introducing the Stylized Forecasters).

As the notions of autocalibration and especially resolution are not widely known in statistics, we use a theoretical example to illustrate the different aspects of forecast quality that they capture. This example builds on an example that has been used by Hamill (2001) and Gneiting et al. (2007) in a related context and is expanded here: In a two-step procedure, first the random variable is drawn and then realizes independently. This example resembles a situation frequently occurring in practice, where information about the mean of a random variable is known in advance and can be used for forecasting.888Such a situation could for instance arise if the underlying process was a stationary process (without intercept) and knowing here would mean knowing the process, the value of the parameter and the past of the process. Consider the following probabilistic forecasters for the random variable at hand,

The first one is a very important reference forecaster, namely the unconditional forecaster, who does not have any knowledge about and consequently issues the unconditional distribution of , , as his predictive distribution. The second one is the informed forecaster, who does know and thus issues as forecast distribution. The third one is the sign-reversed forecaster, who issues , thus knows , but makes the systematic mistake of reversing its sign. Observing exact information on the underlying process like the value of in our example may not be all that realistic and should rather be an exception than the rule in practice due to measurement error, model misspecification or estimation error. Certainly more realistic is that the forecaster has access to some noisy information. Thus I introduce as the fourth forecaster the noisily informed forecaster as he or she does not observe , but a noisy version of it, namely , where is independent of and , and issues as his predictive distribution. Table 1 gives an overview of the four different stylized forecasters and their predictive distributions. Two more forecasters, which are represented in the last two rows, will be added to the example soon.

| Forecaster | |

|---|---|

| Unconditional () | |

| Informed () | |

| Sign-Reversed () | |

| Noisily Informed () | |

| Recalibrated () | |

| Perfect () |

Example (Part 2: Assessing Autocalibration).

For the popular case of mean forecasts evaluated by the squared error, I calculate the measure of miscalibration for the four forecasters, thus the expected squared conditional bias. The last column of table 2 contains these values, while the second column repeats the mean forecasts already contained in table 1 for convenience. Details on the calculations can be found in appendix B. The unconditional and the informed forecaster have a miscalibration of 0 as they are autocalibrated and make no systematic mistakes. Whenever they report a forecast , the expected outcome given that forecast equals the forecast. Obviously, the unconditional forecasts are not very informative as they do not vary, but this is not captured by calibration. The sign-reversed forecaster makes huge systematic mistakes, which leads to a miscalibration of 4. The noisy mean forecasts have a conditional bias of for each value of , leading to a miscalibration of . The bias and miscalibration rise with the strength of the noise as expected.

Continuing the example I also present the values of miscalibration for the case of full distributional forecasts in the form of densities evaluated by the logarithmic score in the last column of table 3. They are qualitatively similar, capturing the same observations as the assessment of the mean forecasts just described. This is as expected since the miscalibration of the sign-reversed forecaster is only caused by the conditionally biased mean forecast and the miscalibration of the noisily informed forecaster is caused by a miscalibrated mean and variance. The other two forecasters show no miscalibration at all.

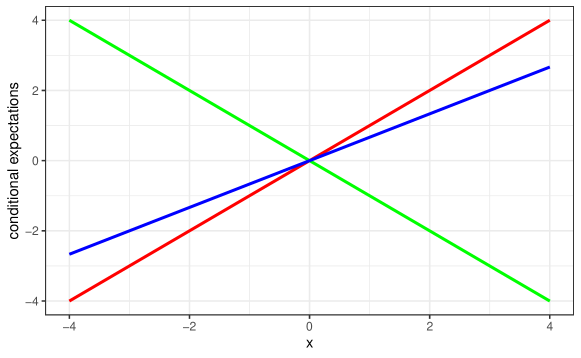

The calibration diagram for the example in the case of mean forecasts is plotted in figure 1 for a selected value of the noise variance of . For the calibrated forecasters, i.e. the unconditional and the informed forecaster (), the graph is on the diagonal and for the noisily informed () and the sign-reversed () forecaster the miscalibration pattern is illustrated by the deviations from the diagonal. Of course, in practice the miscalibration pattern can be much more diverse than in this stylized example as will be illustrated in the empirical part of the paper.

In this stylized example it is easy to correct the systematic mistakes of the miscalibrated forecasters by recalibration, e.g. by simply correcting for the conditional bias in the example of the mean forecasts. The noisily informed forecaster could be recalibrated by changing the mean forecast to , which can be interpreted as a linear combination between the unconditional mean (which is 0 in this case) and the noisy conditional mean and puts less weight on the latter the noisier it is. As the noisily informed forecaster also has a miscalibrated variance of 1 not accounting for the noise, the variance also changes for what I name the recalibrated forecaster, who thus issues the distributional forecast .

2.5 Resolution

While calibration assesses if the information contained in the forecasts is ideally used or if the forecasts contain systematic mistakes, it does not evaluate if this information is valuable and leads to useful forecasts. Resolution in turn measures exactly this, the ability of forecasts to discriminate between outcome values or, in other words, the information content of the forecasts. The unconditional forecaster from the example is perfectly autocalibrated, but his forecasts are constant and thus not able to discriminate between subsequent outcome values, i.e. not informative. The sign-reversed and the noisily informed forecaster in turn are not autocalibrated, but their forecasts contain some valuable information about the outcome, this is captured by resolution. It can be defined as the expected conditional divergence between the unconditional forecast and the autocalibrated forecast:

Definition 3.

Resolution is defined as

As above, the conditional divergence involved is defined as follows:

Note that again, as for , the first representation of in definition 3 will be used in the theoretical part due to its good interpretability and the second term for the estimation later on. Resolution measures how much closer the autocalibrated forecasts , i.e. the ideal forecasts given the information contained in , are to the outcomes than the unconditional forecasts not using this information. It thus measures the useful additional variability in the functional of the distribution function of the outcome variable that can be generated by conditioning on the forecasts or the amount of information contained in them. Due to consistency of scoring functions or propriety of scoring rules respectively is nonnegative as well. A value of zero means that there is no valuable information contained in the forecasts as the unconditional forecasts not using this information are as good.

To justify the use of resolution and its interpretation as a measure of information content, I provide two theoretical results: The first result ensures that resolution really does what it is supposed to do, i.e. that it is higher for a forecast containing more information.

Proposition 1.

For two forecasts and with it holds that , with equality only if almost surely.

Proof.

See appendix A. ∎

The second result is a generalization of the total variance formula

For the case of the squared error loss, resolution equals

i.e. the part of the variance of , which is explained by . This interpretation is justified by the total variance formula. I derive a suitable generalization of this formula, such that the interpretation of resolution as the part of the uncertainty in , in the general case represented by the entropy , which is explained by the forecasts , remains valid:

Proposition 2 (Total Entropy Formula).

The total entropy formula holds:

Proof.

See appendix A. ∎

The total entropy formula shows that the entropy of decomposes into resolution and a further term, . The term , which has already been defined above as conditional entropy, and which, following the naming for a special case of it from information theory, can also fittingly be called equivocation of about , measures the uncertainty about that remains given the knowledge of . For the squared error, the equivocation is equal to the second part of the conditional variance formula, the unexplained part of the variance , the variance of that cannot be explained by or that remains given . Thus, as in the famous special case, the total entropy in can be decomposed in a part that can be explained by , the resolution , and in a part that remains unexplained, the expected conditional entropy .

As the information content of forecasts has barely been touched upon in statistics and econometrics so far,999Even in meteorology, where resolution is often used for forecast evaluation via the Murphy decomposition, I am neither aware of an in-depth discussion of its merits as a fundamental property of good forecasts on its own nor of theoretical justifications as I provide here. with noteworthy exceptions being Holzmann and Eulert (2014), the two aforementioned papers for the binary case (Galbraith and van Norden (2012), Lahiri and Wang (2013)) and the literature on content or predictability horizons (see Galbraith and Tkacz (2007), Isiklar and Lahiri (2007) or Diebold and Kilian (2001) and Breitung and Knüppel (2018) for more recent work), I will sketch some of the possible benefits of analyzing information content and especially resolution for forecast evaluation already here before they are illustrated using real-world examples in the empirical part of the paper.

A first and obvious use of resolution lies in comparing the information content of different forecasts or forecasting methods, for example univariate against multivariate model-based forecasts or model-based against survey forecasts.

A second use that rather judges the absolute usefulness of forecasts is analyzing resolution over the forecasting horizon , where the information content usually decreases with and often reaches zero rather quickly, making them as useful in terms of information content as the unconditional forecasts . Here it is instructive to normalize the resolution by the entropy, , which leads to a measure of information content, predictability or of variation explained lying between zero and one analogous to the from least-squares regression.101010 Consider again the example of an AR(1) process . For the optimal mean forecasts , this measure equals . In practice a plot of this measure against the forecast horizon is useful.

It is natural to compare forecasts against an unconditional benchmark (as resolution does) to assess information content or predictability. Actually, Clements and Hendry (1998, chapter 2) define a random variable as unpredictable with respect to an information set if the conditional equals the unconditional distribution, . The definition of resolution is in line with this definition.

The literature on content or predictability horizons mentioned above tries to assess information content as well and strives to find the maximum horizon up to which forecasts contain information about the variable of interest or up to which it is predictable. The used measure there is the quotient between the loss of short-term forecasts and unconditional forecasts (or long-term forecasts, which converge to unconditional forecasts). This is a similar approach to the one sketched above, but, as will become clear in the next section, the effects of miscalibration may disguise these results and they should be reassessed in terms of the more exact measure that we propose, namely (normalized) resolution. As this literature concentrates mainly on mean forecasts, it is certainly a path for future research and very easy by our approach to check more generally for predictability with respect to other features of the distribution. For example, there could be predictability in outer quantiles of stock returns in contrast to the unpredictability at the median or mean.

After having found out that a forecasting method has a low resolution or resolution quickly drops over the forecasting horizon, it is natural to look for the reasons for that, which are certainly hard to analyze empirically. Theoretically, one may categorize these reasons as follows: Are the forecasting methods or the forecasters bad (do they not use the information available to them properly), is their information limited or is the variable not predictable at all? In terms of the our theoretical framework, this may be cast as follows: A low resolution of forecasts may arise due to a bad use of the given information, which would mean that the forecaster did not consider valuable information contained in . It may also be that he or she made proper use of the given information , but lacks information, i.e. some valuable information contained in is not available to him or her. Finally, it may be the case that he or she has access to all or almost all of the information contained in , but the information is not useful in predicting , making unpredictable. Certainly, this is an interesting direction for future research, but requires a detailed knowledge of the forecasting method under analysis and the respective information structure.

Example (Part 3: Resolution).

The values for the resolution of the different stylized forecasters can be found in the second to last columns of table 2 for the mean forecasts and squared error loss and of table 3 for the density forecasts and logarithmic loss. Details on the calculations can again be found in appendix B. In both cases the unconditional forecaster has a resolution of zero as his constant forecasts are not able to discriminate between the outcomes at all. The informed forecaster has the maximum attainable resolution of 1 or respectively as he perfectly knows , the outcome of the first step of the example, and the outcome of the second step, , is unpredictable. Thus, the informed forecaster can be seen as a reference case that cannot be improved upon in terms of resolution as he possesses the maximum available information. The same holds true for the sign-reversed forecaster, whose forecasts include the same information and who thus has the same resolution, but of course does not use it efficiently and is hence heavily miscalibrated at the same time.

However, in reality it is difficult or often impossible to assess what the maximum available information is and what part of the variation in the outcome is unpredictable as a not even remotely comprehensible amount of variables may influence the outcome. Thus, such a reference will usually not be available in practice. A reference forecaster that is always available, even though imaginary and not realistic, is the omniscient forecaster, who has the gift of foresight, hence knows the outcome in advance (even the unpredictable part of the outcome) and issues a degenerate distribution as his probabilistic forecast, i.e. , and consequently as a forecast for the expected value. The resolution of the omniscient forecaster is equal to the entropy of , , which represents a usually unattainable upper bound for resolution. In the case of the squared error the resolution of the omniscient forecaster is thus equal to as he knows not only the outcome of , but also of .

The noisily informed forecaster as well as his or her recalibrated version have a resolution of and respectively, which falls with the amount of noise, always lying between the resolutions of the informed and the unconditional forecaster, which are the limiting cases for moving towards zero or infinity.

3 The Murphy Decomposition, the Calibration-Resolution and the Sharpness Principle

In the last section I discussed desirable properties of forecasts, focusing mainly on accuracy, autocalibration and resolution. The question naturally comes up if different approaches to forecast evaluation arise from using different properties, which in turn may yield to different results and recommendations. This section answers this question and shows that assessing forecast accuracy and jointly assessing autocalibration and resolution are two sides of the same coin complementing each other perfectly instead of being mutually exclusive approaches to forecast evaluation. I first introduce the generalized Murphy decomposition, then deduce the calibration-resolution principle from it and touch upon some of its implications: Amongst others I point out that it generalizes the sharpness principle and then assess some widely used forecast evaluation methods from its perspective.

3.1 The Murphy Decomposition and the Calibration-Resolution Principle

As laid out in the introduction, after having been proposed by Murphy (1973) for the special case of probability forecasts for a binary event and having been applied frequently in meteorology as a forecast evaluation method, the Murphy decomposition has been proposed for other types of forecasts and for general classes of loss functions by meteorologists. I provide a fully general version of the decomposition.

Proposition 3 (Murphy Decomposition).

For a consistent scoring function or a proper scoring rule it holds that:

where I call the unconditional entropy uncertainty, .

Proof.

See appendix A. ∎

Besides the mechanical and simple version of the proof in the appendix, I sketch a very instructive version here, which involves amongst others a general form of the Sanders decomposition (see Sanders (1963)), a predecessor of the Murphy decomposition, which is related in multiple ways to the sharpness principle: I first apply the decomposition from equation 3 of the expected score into an entropy and a divergence term to the random variable and the forecasts to decompose the conditional expected score into a conditional entropy term and the divergence between and , which measures miscalibration:

Taking unconditional expectations, the second term just yields the measure of miscalibration and I arrive at the fully general version of the decomposition introduced by Sanders (1963) for the Brier score:

| (4) |

The first term, , was called sharpness by Sanders and is also often referred to as refinement in the meteorological literature (see e.g. Jolliffe and Stephenson (2012)). Since Gneiting et al. (2007) the term sharpness is used in a more narrow sense as will be explained in the next subsection. Murphy (1973) refined this decomposition by decomposing the first term again. This is easily achieved here in the general case by applying the total entropy formula from proposition 2.

For the example of the squared error, the Murphy decomposition simplifies and looks as follows:

| (5) |

The Murphy decomposition partitions the expected score of the forecasts into three components: The first one is the unconditional entropy of , which represents the uncertainty in the variable of interest and does not depend on the forecasts. By definition, this term equals the score obtained by the functional of the unconditional distribution of , ,

The second component, resolution, enters the decomposition negatively and represents the part of the uncertainty in that can be explained by the forecasts, i.e. it reduces the expected score by that amount compared to the unconditional forecast. The resulting difference , i.e. the expected conditional entropy or expected equivocation of about , represents the minimal achievable score given the information contained in , i.e. the score achieved by autocalibrated forecasts. For miscalibrated forecasts, the expected score rises by their amount of miscalibration, , which is the third component.

What I name the calibration-resolution principle is an immediate consequence of the generalized Murphy decomposition, but has profound consequences for forecast evaluation as I will discuss throughout the remainder of this section.

Corollary 1 (Calibration-Resolution Principle).

When constructing forecasts maximizing forecast accuracy, i.e. minimizing expected loss , is equivalent to jointly minimizing miscalibration and maximizing resolution .

The calibration-resolution principle as a characterization of forecast accuracy in terms of two underlying properties provides an alternative interpretation and a deeper understanding of what constructing accurate forecasts means and has many implications for the theory and practice of forecast evaluation: It provides a further justification for the accuracy-measurement approach by consistent scoring functions or proper scoring rules put forward by Tilmann Gneiting and his coauthors. Furthermore, it generalizes the sharpness principle conjectured by Gneiting et al. (2007) for probabilistic forecasts to all types of forecasts as will be discussed in detail in the next subsection. The sharpness principle reshaped the field probabilistic forecasting and of probabilistic forecast evaluation by providing a deeper understanding of what a good probabilistic forecast is and which methods are suitable to judge that. The calibration-resolution principle provides such a general perspective for all types of forecasts (including the important case of point forecasts), i.e. for forecasting in general. As a consequence it may e.g. provide a clearer understanding of the relationships of formerly seemingly unrelated forecast evaluation methods and uncover the drawbacks of several widely used evaluation methods, most often their lack of an assessment of informational content, just as the sharpness principle uncovered the drawbacks of the PIT for the evaluation of probabilistic forecasts. This will be discussed in the subsection after the next. While the calibration-resolution principle makes clear that evaluating forecasts by assessing their accuracy and by analyzing autocalibration and resolution are two sides of the same coin in the sense of leading to results that are in line with each other, it is nevertheless very interesting to flip the coin and to complement average loss by an analysis of autocalibration and resolution: Autocalibration and resolution are not only interesting in their own right as has been laid out in the previous section, but this will also uncover the driving forces of forecasting loss, i.e. show if a lack of information content or systematic mistakes or a combination of both are responsible for low accuracy, and where improvements are needed. Thus, the use of the Murphy decomposition as a forecast evaluation method will be the topic of the next section. The example with the stylized forecasters already gives a preview to that.

Example (Part 4: The Murphy Decomposition).

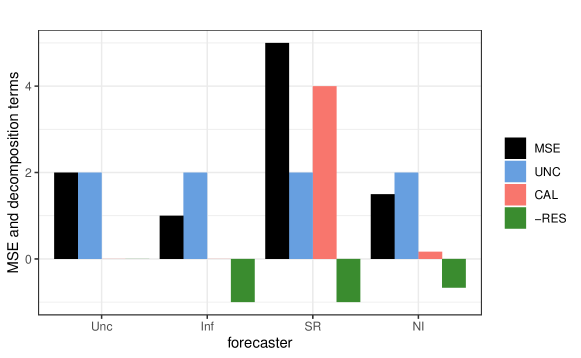

For the mean forecasts of the stylized forecasters evaluated by squared error loss, the full decomposition is shown in table 2. The uncertainty in the fourth column is of course constant over all forecasters and the resolution and miscalibration in the last two columns have already been discussed in the previous section. They lead to an expected loss or in this case as depicted in the third column. As discussed above, the unconditional forecaster’s loss equals the uncertainty. The perfect forecaster has a loss of zero as his resolution equals the uncertainty, while for the more realistic informed forecaster half of the uncertainty is resolved by his forecasts, leading to a of one. The even more realistic noisily informed forecaster has a loss, which is higher by exactly the noise variance (compared to the informed forecaster) due to a drop in resolution and a rise in miscalibration caused by the noise, while the miscalibration is cured for his recalibrated version, leading to a between the informed and the noisily informed cases. The sign-reversed forecaster, even though having the same resolution as the informed forecaster, has a very high loss due to his massive miscalibration.

| Forecaster | ||||

|---|---|---|---|---|

| Unconditional () | 0 | 2 | 0 | 0 |

| Informed () | 1 | 1 | 0 | |

| Sign-Reversed () | 5 | 1 | 4 | |

| Noisily Informed () | ||||

| Recalibrated () | 1 + | 0 | ||

| Perfect () | 0 | 2 | 0 |

| Forecaster | ||||

|---|---|---|---|---|

| 0 | 0 | |||

| 0 | ||||

| 2 | ||||

| 0 | ||||

| 0 | 0 |

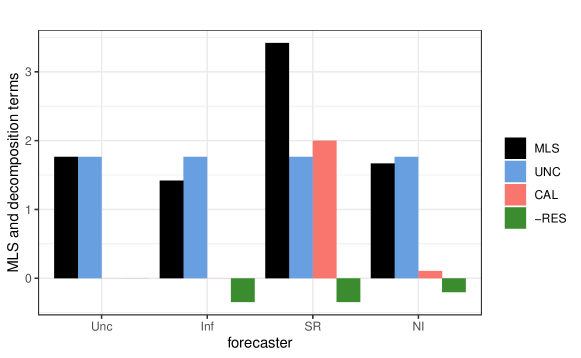

I introduce a graphical representation of the decomposition using bar charts, which facilitates a comparison of its components within and between the single forecasters. Such a plot for the first four forecasters from the example is presented in figure 2 for a noise variance of . A similar plot can also and will in the empirical applications be used to compare the development of the decomposition over the forecasting horizon . For the case of density forecasts and logarithmic loss a similar picture emerges as is illustrated in table 3 and figure 3.

3.2 The Sharpness Principle Revisited

In this subsection I review the very influential sharpness principle, discuss in which ways the calibration-resolution principle generalizes it and why these generalizations are important for the theory and practice of forecast evaluation.

Sharpness, a property of distributional forecasts popularized by Gneiting et al. (2007) refers to the concentration of the predictive distribution , i.e. more concentrated predictive distributions are sharper. Obviously, sharpness alone is not very informative as every degenerate distribution with zero variance is perfectly sharp, but may be far away from the outcomes, i.e. strongly miscalibrated.

To measure sharpness, Gneiting et al. (2007) suggest the variance of the forecast distribution, , as the classical measure of dispersion. Of course other measures of dispersion are also suitable, a natural measure fitting to the specific loss function used is of course the generalized entropy .111111Here, an expression for the random variable having the distribution is needed to denote its entropy. To obtain it, I use the famous result about the inverse probability integral transform, i.e. the fact that for a distribution function of a continuous random variable it holds that for . Note that the mean and variance of the predictive distribution, for which the shorthand notations and were used above, could also be expressed in this way as and .

In their highly influential article Gneiting et al. (2007) conjectured that good or accurate probabilistic forecasts can be characterized as maximizing sharpness subject to calibration.121212To be precise, Gneiting et al. (2007) conjectured the sharpness principle for what they call ideal forecasts, not for accurate forecasts. However, the notion of ideality they use is different to the one used in later work, which I use as well and which is relative to some information set. They define a forecast as ideal if the forecast distribution coincides with the true distribution of the outcome, which can perhaps best be understood as the distribution of conditional on the largest available information set, which I called . Thus their definition of ideality coincides with ideality with respect to in our framework. Being ideal with respect to implies being most accurate and the reverse direction is also true for strictly proper scoring rules. Thus, as the notion of ideality is not entirely precise and if understood in this way equivalent to accuracy anyway, we work with accuracy as Tsyplakov (2011) also does. They discussed several different forms of calibration, which are weaker than autocalibration, and stated the conjecture “deliberately loosely” as it was unclear which notion of calibration was needed. This so-called sharpness principle establishes a characterization of accurate forecasts via other properties, namely calibration and sharpness. This article has had a profound impact as the paradigm of maximizing sharpness subject to calibration has been widely accepted in the probabilistic forecasting literature and proper scoring rules, the use of which the article also advocates, have become increasingly popular as a forecast evaluation method.

Tsyplakov (2011) was able to prove the sharpness principle after clarifying that autocalibration is the required underlying notion of calibration:131313Note that a prior attempted proof of the sharpness principle based on different notions of calibration (see Pal (2009)) turned out to be wrong (see Pal (2010)). Within the general framework used here, the proof is easy using the Sanders decomposition from equation (4): For a probabilistic forecast in the form of e.g. a density or a distribution function, , which is autocalibrated, i.e. , the miscalibration vanishes and the expected score equals the expected conditional entropy. Further, again by autocalibration, the expected conditional entropy equals the expected sharpness (measured by the entropy of the predictive distribution),141414Note that the expected conditional entropy, i.e. the measure of sharpness, has the opposite orientation to sharpness. As no confusion should arise I will nevertheless speak of maximizing sharpness when this term is minimized in the following. i.e. in this step the more general notion of sharpness used by Sanders (1963) is reduced to the notion of sharpness used by Gneiting et al. (2007):151515Note that the first step is of course also valid for point forecasts, but the second step is not as it replaces a property of the conditional distribution of by a property of the predictive distribution only. Thus, for point forecasts, this simplification of the expected conditional entropy under autocalibration is not possible. Note however, that for the important special case of mean forecasts and quadratic loss, the interesting relationship arises.

Thus, for autocalibrated probabilistic forecasts minimizing loss is equivalent to maximizing sharpness. This is a neat characterization of probabilistic forecasts in terms of underlying properties. It also has had a major impact in terms of assessing which evaluation methods are suitable to assess probabilistic forecasts as will be discussed in more detail in the next section.

While Tsyplakov (2011, p. 5) also stressed that “the sharpness principle provides a useful insight into the essence of probabilistic forecasting”, he nevertheless pointed out that its practical use may be limited as perfectly autocalibrated forecasts are very hard to achieve. I already elaborated further on this and discussed that in practice miscalibration will rather be the rule than the exception as for example information about the underlying process will hardly ever be observed without noise due to for example model uncertainty or estimation error. I introduced the noisily informed forecaster as a stylized example for this. What is more, forecasters may often face a trade-off between using more information and risking miscalibration and not using this information to avoid possible sources of miscalibration. An example for this may be the use of a multivariate model instead of a univariate model, which probably contains more useful information about the underlying process, but is also prone to estimation error and model misspecification. In our stylized example, a forecaster may have to choose between being an unconditional or a noisily informed forecaster, i.e. between using the information on and not using it. Which choice is optimal will depend on the noise variance . This tradeoff cannot be captured by the sharpness principle, which goes along with a maximization of sharpness given perfect autocalibration.

Hence a generalization of the sharpness principle which is also applicable to miscalibrated forecasts is useful. Furthermore, a generalization to all kinds of forecasts, including point forecasts, and hence stressing the common nature of the forecasting process for point and probabilistic forecasts, is valuable. The calibration-resolution principle yields the desired generalization in both direction, stating that constructing accurate forecasts amounts to jointly minimizing systematic mistakes, i.e. mis(auto)calibration, and maximizing informational content, i.e. resolution. It replaces sharpness, a property exclusive to probabilistic forecasts, by resolution, a property suitable for all kinds of forecasts, and replaces an optimization conditional on perfect autocalibration by a joint optimization, opening up also to miscalibrated forecasts. This principle is thus an insight into the essence of (all) forecasting and of practical use.

To see that the sharpness principle really is a special case of the calibration-resolution principle, which arises for autocalibrated probabilistic forecasts, remember from above that under autocalibration the expected score, , equals the expected conditional entropy, , and that for autocalibrated probabilistic forecasts the conditional entropy equals sharpness, . Thus, in this case the following relationship holds between resolution and sharpness:

Hence, maximizing sharpness is equivalent to maximizing resolution in this case as predictive distributions contain no systematic mistakes under autocalibration and their informational content is higher the more concentrated they are.

From a theoretical point of view, there seems to be no reason to analyze sharpness anymore when evaluating probabilistic forecasts as resolution also captures miscalibrated forecasts, but in practice sharpness is much easier to assess than resolution: Sharpness is a property of the forecast distribution only and can be measured easily, while for resolution a conditional distribution of the observations given the forecasts has to be estimated, which is hard if the forecasts come in form of a full distribution as will be discussed at the beginning of the next section. Thus, sharpness still may play a crucial practical role in the evaluation of probabilistic forecasts.

Example (Part 5: Sharpness).

In the example, the perfect forecaster is the sharpest or perfectly sharp as he or she issues a point distribution, but of course infeasible, while the informed forecaster is as sharp as is realistically possible, while still being autocalibrated, as his forecast distribution just represents the unpredictable uncertainty and has just the same variance of 1. The recalibrated forecaster is less sharp, having a variance of . The unconditional forecaster is not very sharp, having a variance of 2. The miscalibrated forecasters both have a variance of 2, but for them sharpness is not a useful measure as discussed above. If we wanted to apply the suitable measure of entropy for the loss function for probabilistic forecasts used before in the example, namely the classical entropy for log loss, this would lead to values of , where stands for the respective predictive variances just discussed, by the formula for the entropy of normally distributed random variable (see appendix B).

3.3 Traditional Forecast Evaluation Methods from the Perspective of the Calibration-Resolution Principle

The calibration-resolution principle provides a general perspective on forecast evaluation, from which the merits and drawbacks of different forecast evaluation methods can be assessed and the relationships between the methods can be clarified. In order to do this, it is important to clearly show which aspects of forecast quality are captured by certain forecast evaluation methods and which are not. This is facilitated by the use of the three fundamental properties accuracy, resolution and autocalibration and their relationship made clear by the calibration-resolution principle. Using this framework, I point out in this subsection that some widely used forecast evaluation methods do not assess informational content, but only some form of calibration, which is often even weaker than autocalibration. Furthermore, I discuss the relationship between optimality testing and the calibration-resolution principle.

Many traditional and widely used methods of forecast evaluation like the PIT for probabilistic forecasts or conditional coverage or exceedance tests for interval or quantile forecasts focus on assessing some form of calibration. Although undoubtedly being useful tools for forecast evaluation, when used exclusively without accompanying them by the calculation of a suitable loss, these methods yield an incomplete assessment of forecast quality that may leave the forecast examiner clueless or even lead to him or her being content with inferior forecasts or forecasting methods. Such a critique has been issued in recent years for some types of forecasts and the dominant evaluation methodologies used for them. The calibration-resolution principle reveals the common theme here, the lack of an assessment of the informational content, and makes fully transparent what (further) aspects of forecast quality specific methods are missing out on.

The first critique of this form regards the use of the PIT for evaluating probabilistic forecasts. When using the PIT for forecast evaluation (see Dawid (1984) and Diebold et al. (1998)), the realizations are plugged into the respective forecast distributions and the resulting series of probability integral transforms is checked for uniformity or uniformity and independence. Hamill (2001) and Gneiting et al. (2007) constructed examples for forecasts, which are obviously (conditionally) biased, but nevertheless lead to uniform PITs in their simulations. Gneiting et al. (2007) named the uniformity of the PIT probabilistic calibration, stated that this was not enough for forecasts being of a high quality and called for an additional evaluation of sharpness, i.e. this critique was the major motivation for them for coming up with the sharpness principle. Mitchell and Wallis (2011) criticized Gneiting et al. (2007) on several ends, questioning amongst others the validity of the sharpness principle and stating that in a proper time series framework and when checking for uniformity and independence (for one-step-ahead forecasts and -independence for -step-ahead forecasts) of the PIT as proposed by Diebold et al. (1998), which they call complete calibration, the relevance of these examples would break down. Even though Mitchell and Wallis make some interesting points, it is clear that even complete calibration is only a necessary condition for ideal calibration. Regarding the question what can go wrong even though forecasts are completely calibrated Tsyplakov (2011) points out that this form of calibration is only equivalent to ideal calibration if the information set of the forecaster only consists of the past of the process of interest, i.e. if , and is considerably weaker than autocalibration in realistic settings. Equipped with this knowledge, the calibration-resolution principle reveals that assessing complete calibration is not really an assessment of correct specification or optimality (called ideal calibration here) as intended by Diebold et al. (1998), but only of a weaker form of calibration and ignores the information content of the forecasts. In a related project (Pohle (2020b)) I rename the misleading term complete calibration as autoregressive calibration, come up with realistic examples with an information set generated by a bivariate process and with empirical examples, where I demonstrate that autoregressively calibrated forecasts may be very bad (i.e. inaccurate) either by a lack of information content or by systematic mistakes (deviations from autocalibration).161616Note that this also shows, where the orignial form of the sharpness principle conjectured by Gneiting et al. (2007) before the clarification of Tsyplakov (2011) and the approach to forecast evaluation proposed with it have their weaknesses: An assessment of probabilistic calibration via uniformity of the PIT or the other weak forms of calibration discussed there does not uncover many relevant types of systematic mistakes and, what is more, in this case sharpness is not equivalent to resolution and not really suitable anymore for assessing information content. This does by no means imply that the PIT is useless as it is still able to uncover systematic mistakes with respect to the information contained in its own past, but that it should not be exclusively used for evaluating probabilistic forecasts as is often done. Instead, it should be accompanied by proper scoring rules and further methods, which come closer to a real check for autocalibration. I discuss new methods going in this direction in Pohle (2020b).

In a similar fashion as the PIT has been the dominant method for evaluating probabilistic forecasts, the conditional coverage test by Christoffersen (1998) has been the dominant method for evaluating interval forecasts. It tests if the sequence of indicator functions, which describe if realizations fell into their respective prediction intervals, is , where is the desired coverage of the prediction interval (again independence should only hold for one-step-ahead forecasts, while for -step-ahead forecasts, -independence should hold). The test is closely related to the PIT and thus checks autoregressive calibration for interval forecasts, thus also ignoring information content and assessing a weaker form of calibration than autocalibration. Hence, using a suitable proper scoring rule, for example the interval score (see e.g. Gneiting and Raftery (2007)), is advisable here, as the basis for interval forecast evaluation. Complementing this by an assessment of autocalibration and resolution here is possible for interval forecasts as it is for point forecasts. They are only two-dimensional, making estimation of the decomposition terms feasible as will be discussed at the beginning of the next section. The Christoffersen test could then also complement the analysis by these two methods, but should certainly not be used on its own. The test is also often used for quantile forecasts, where the same critique applies.

As a final point in this section, I discuss the relationship between forecast optimality and the calibration-resolution principle. Forecast optimality is a crucial notion mainly in econometrics and there is a huge literature on optimality testing (see e.g. Elliott and Timmermann (2016, chapter 15) for an overview) emerging from the rational expectations literature from economics. A forecast is defined as optimal with respect to the information set and the loss function if it minimizes expected conditional loss, i.e. if

where are -measurable random variables. Thus, if is a consistent scoring function or a proper scoring rule respectively, , i.e. the notions of optimality and ideal calibration are equivalent (see also Gneiting (2011, Theorem 1)). If optimality is defined with respect to a smaller information set, this leads to weaker notions of optimality analogous to the weaker notions of calibration mentioned throughout the paper. Optimality is usually tested by checking orthogonality of forecast errors and functions of several variables from . Well-known problems arising here are that firstly the information set of the forecaster is usually unknown and secondly too big, so that it is not entirely clear against which variables to check orthogonality and after orthogonality was not rejected for a set of variables it is never clear if there are other variables which violate it. Thus, here it may be the case as well that only a weaker form of calibration than ideal calibration is tested for. Often optimality is tested against functions of the forecasts , which amounts to a test for autocalibration as e.g. in the case of the popular Mincer-Zarnowitz regression (see e.g. Mincer and Zarnowitz (1969)). Then again the information content would not be captured by the procedure. Arguing similarly for a special field of application, Nolde and Ziegel (2017) criticize traditional backtesting of risk measures, which amounts to optimality testing of these risk measures and make a case for comparative backtesting, which amounts to predictive accuracy testing and mention, referring to Holzmann and Eulert (2014), that traditional backtesting ignores the role of the informational content.

Evaluating the forecasts by resolution and autocalibration is a good complement to optimality testing as these problems do not arise there. First, the information content of the forecasts is assessed and then the optimality of the forecasts against the information contained in themselves, which is always available as is observed. Furthermore, if optimality is rejected by an optimality test, it is not clear if the deviations from optimality are large (i.e. really important or economically significant as an econometrician would say) and in which situation they occur, i.e. how the miscalibration pattern looks, and how they can be cured. An assessment of autocalibration answers these questions by providing the shape of the miscalibration pattern with respect to by analyzing the deviations of from the diagonal as explained in the previous section and also shows the size of deviations from optimality by the miscalibration . Note that in principle the miscalibration pattern and a term measuring overall miscalibration can also be estimated for larger information sets (for example adopted to the information set used in the accompanying optimality test) than , but then the estimation becomes high-dimensional, which makes it difficult as discussed in the next section.

4 The Murphy Decomposition as a Forecast Evaluation Method