Dependence in elliptical partial correlation graphs

Abstract.

The Gaussian model equips strong properties that facilitate studying and interpreting graphical models. Specifically it reduces conditional independence and the study of positive association to determining partial correlations and their signs. When Gaussianity does not hold partial correlation graphs are a useful relaxation of graphical models, but it is not clear what information they contain (besides the obvious lack of linear association). We study elliptical and transelliptical distributions as middle-ground between the Gaussian and other families that are more flexible but either do not embed strong properties or do not lead to simple interpretation. We characterize the meaning of zero partial correlations in the elliptical family and transelliptical copula models and show that it retains much of the dependence structure from the Gaussian case. Regarding positive dependence, we prove impossibility results to learn (trans)elliptical graphical models, including that an elliptical distribution that is multivariate totally positive of order two for all dimensions must be essentially Gaussian. We then show how to interpret positive partial correlations as a relaxation, and obtain important properties related to faithfulness and Simpson’s paradox. We illustrate the transelliptical model potential to study tail dependence in S&P500 data, and of positivity to improve regularized inference.

Key words and phrases:

Partial correlation graph, elliptical distribution, transelliptical distribution, copula, graphical models, multivariate total positivity.2010 Mathematics Subject Classification:

62H05,62H20,62H221. Introduction

Several papers study graphical models for elliptical and transelliptical distributions in the standard (Finegold & Drton,, 2009; Vogel & Fried,, 2011) and high-dimensional settings (Barber & Kolar,, 2018; Bilodeau,, 2014; Liu et al.,, 2012b; Zhao & Liu,, 2014). These models found applications in many fields, such as finance and biology (Behrouzi & Wit,, 2019; Stephens,, 2013; Vinciotti & Hashem,, 2013), and (implicitly) wherever Gaussian graphical models were used but the underlying distribution is likely to depart from normality, e.g. be heavy-tailed or asymmetric. In the elliptical setting the usual definition of graphical models mimics the Gaussian case — the model is given by zeros in the inverse covariance, or equivalently, by vanishing partial correlations. Despite this being a reasonable relaxation, the corresponding partial correlation graph (PG) cannot be interpreted in terms of conditional independence, since outside of the normal case no elliptical distributions allow for conditional independence (c.f. Proposition 2.5). It is therefore unclear what type of dependence information is embedded by the PG.

For general distributions partial correlations inform only about linear dependence. Missing edges in the PG must then be interpreted with great care and, in some cases, they can fail to capture interesting dependence information. For example, in an aircraft data set from Bowman & Foster, (1993), we can model dependence between the speed of an airplane and its wingspan. Although the sample correlation is negligible, more flexible dependence tests reveal that the variables are strongly related; see e.g. Székely & Rizzo, (2009). The reason is that for very fast (military) airplanes there is a negative dependence between speed and wingspan, while this dependence is positive for regular aircrafts.

The main theme of this paper is that for (trans)elliptical distributions there is significantly more information in the partial correlation graph beyond presence/absence of linear dependence. We introduce definitions and notation to aid the exposition.

Definition 1.1.

A random vector has an elliptical distribution if there exists and a positive semi-definite matrix such that the characteristic function of is of the form for some . We write making in this notation implicit.

Important examples include the multivariate normal, Laplace and multivariate t-distributions. Elliptical graphical models have been extended to transelliptical distributions (also known as elliptical copulas or meta-elliptical distributions, Fang et al., (2002); Liu et al., (2012b)).

Definition 1.2.

A random vector has a transelliptical distribution with parameters if for some fixed strictly increasing functions . We write , making in this notation implicit.

Here the additional challenge is that is unknown. An elegant approach to learning partial correlations relies on directly estimating the correlation matrix of without actually learning ; see Liu et al., (2012b); Lindskog et al., (2003), and then proceed as in the elliptical case (Section 3.3).

Throughout we assume that is positive definite and denote , the set of vertices by , by the vector obtained by removing from , and by the vector obtained by removing from . Given denote by and the subvectors of and with coordinates in and by the corresponding subblock of with rows in and columns in . The partial correlation between is

| (1) |

and so if and only if . Finally, we denote that are independent by .

The usual interpretation of PGs in elliptical distributions is that — since the conditional expectation is linear in and the conditional correlation is equal to the partial correlation — the condition implies that are conditionally uncorrelated. That is, zero partial correlation implies zero conditional correlation. As we show in Theorem 3.4 something much stronger is true. It is possible to fully characterize the PG in elliptical distributions:

The partial correlation if and only if for every function for which the covariance exists.

A similar characterization extends to transelliptical distributions. The usual interpretation of is that are conditionally uncorrelated given , which is not very interesting, since is unknown. We show in Theorem 3.5 that equivalently for any , provided the covariance exists. In particular, , a more explicit dependence information in terms of . We also show in Proposition 3.9 yet another equivalent interpretation, namely that if and only if conditional Kendall’s tau correlation between and being zero for all strictly increasing .

These findings are practically relevant. Recall that two variables and with general distribution are independent if and only if for all functions we have ; see e.g. (Feller,, 1971, page 136). That is, if and only if there is no way to transform and such that the new variables are correlated. Our characterization of has an analogous interpretation, in elliptical families there is no way to transform such that the new variable is correlated with . This rules out situations like the aircraft example above where speed is correlated with a non-linear function of wingspan.

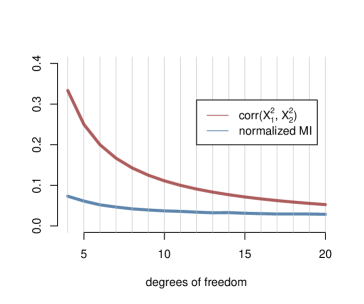

Further, interpreting can be important in applications, given that elliptical and transelliptical models are a popular tool to capture second-order or tail dependencies. Even though such dependencies can be practically significant. As an example, let and consider as a simple measure of marginal tail (or second-order) dependence. In the special sub-family of elliptical distributions defined by scale mixtures of normals (c.f. Section 2), it is possible to show

| (2) |

where if and only if is Gaussian. This measure is minimized for , then , which can be non-negligible, e.g. for the t-distribution with degrees of freedom. Figure 1 shows this quantity and, for comparison, also the normalized mutual information (a standard measure of deviation from independence). Both measures converge to zero as but this convergence is slow. Similarly, one may measure conditional tail dependence via

| (3) |

where the right-hand side follows from Proposition 2.1 below. When the conditional tail dependence is . See Section 5 for further discussion and an illustration on stock market data.

Our other main contributions relate to PGs in settings where one wishes to study positive forms of association. Two standard ways to define positive dependence are via the notions of multivariate total positivity of order two () and conditionally increasing (CI, Section 4). Although these concepts are different, in the Gaussian case they are equivalent and reduce to constraining partial correlations to be non-negative. It is less clear how to interpret these concepts in general elliptical families. A first contribution is showing several impossibility results: within the elliptical family with at least one partial correlation zero there exist no conditionally increasing distributions (other than the Normal) implying the same result for distributions. That is, if one wants remove edges in the PG with an additional positive dependence structure, one cannot rely on the standard notions of positive dependence.

A natural relaxation is to learn a PG under the constraint that , as proposed by Agrawal et al., (2019). We refer to this strategy as positive partial correlation graphs (PPG). We contribute to understanding how should one interpret missing edges in the PPG, and to characterizing embedded positivity properties such as the positive correlation of each with any increasing function of the vector . In Section 5 we illustrate how positivity constraints induce a type of regularization that can help improve inference relative to other standard forms of regularization, such as graphical LASSO, specifically attaining a higher log-likelihood with a sparser graph. This is meant as a testimony that our theoretical results have practical relevance. For further examples in risk modelling see Abdous et al., (2005); Rüschendorf & Witting, (2017), and in psychology see Epskamp & Fried, (2018); Lauritzen et al., (2019b), for example.

This paper also contributes to recent research aimed at understanding multivariate total positivity in a wide variety of contexts; see, for example, Fallat et al., (2017); Lauritzen et al., (2019a, b); Robeva et al., (2018); Slawski & Hein, (2015). We provide in Theorem 4.16 a complete characterization of elliptical distributions in terms of their density generator. In Theorem 4.19 this characterisation is used to show a remarkable result: a density generator may induce a -variate distribution for each if and only if the underlying distribution is essentially Gaussian.

The paper is organized as follows. In Section 2 we review basic results on elliptical distributions. In Section 3 we characterize partial correlation graphs for elliptical and transelliptical distributions, giving a refined understanding of their encoded dependence information, and how one should interpret zero partial correlations. In Section 4 we study positive elliptical distributions and their alternative characterizations. In Section 5 we illustrate our main results with examples.

In the rest of the article we employ the convention where the letter is reserved for elliptical random variables, is reserved for transelliptical random variables, is reserved for Gaussian random variables and for general random variables. The letter is reserved for the monotone functions defining transelliptical distributions as in Definition 1.2, and denote general functions, and denotes probability density functions.

2. Elliptical distributions

We review some elliptical distribution results; for more information see Fang, (2018) or Kelker, (1970), for example.

2.1. Stochastic representation

If then admits the representation

| (4) |

where denotes the square root of the positive-definite , is an arbitrary random variable, is uniformly distributed on the unit -dimensional sphere, and . Elementary arguments show that, if , then and if then . Throughout this paper we assume that .

There is a useful representation equivalent to (4) in terms of normal variables. Let with . Then is a mean zero Gaussian variable with covariance . From (4) it follows that

| (5) |

where and . In general is not independent of . The special case corresponds to the scale mixture of normals sub-family, which includes most popular elliptical distributions. The normal distribution corresponds to . If for then has a multivariate t-distribution with parameter . If we get the multivariate Cauchy, and if the multivariate Laplace distribution. Equivalently, scale mixture of normals can be defined as the marginal distribution of associated to when , and follows an arbitrary continuous distribution.

The elliptical family is closed under taking margins and under conditioning.

Proposition 2.1.

Let be any split of into subvectors and . Then

-

(i)

,

-

(ii)

, where and

For the proof see, for example, (Fang,, 2018, Theorem 2.18). The conditional mean has the same form as in the Gaussian case, where above can be replaced by (a scalar multiple of ). Moreover, the conditional correlations are the normalized entries of (the partial correlations ), and do not depend on the value of the conditioning variable ; see also Lemma 2.3 below.

2.2. Characterization of Gaussianity within the elliptical family

If is Gaussian then each marginal distribution and each conditional distribution is Gaussian. Moreover, the conditional covariances do not depend on the conditioning variable and independence is equivalent to zero correlations. These properties characterize the Gaussian distribution in the class of elliptical distributions. We recall these basic results.

Lemma 2.2 (Lemma 4 and 8 in Kelker, (1970)).

Let . If is Gaussian for some then is Gaussian. Further, if given is Gaussian for some then is Gaussian.

We noted earlier that conditional correlations do not depend on the conditioning variable. For conditional covariances this is only true in the Gaussian case.

Lemma 2.3 (Theorem 7 in Kelker, (1970)).

Let . The conditional covariance of given is independent of if and only if is Gaussian.

The standard definition of graphical models uses density factorizations that link to conditional independence through the Hammersley-Clifford theorem (Lauritzen,, 1996). However, it is not possible to define conditional independence in the elliptical family outside of the Gaussian case. The next two characterizations are the most consequential for this article.

Lemma 2.4 (Lemma 5 in Kelker, (1970)).

Let . If is a diagonal matrix, then the components of are independent if and only if has a normal distribution.

Proposition 2.5 (Theorem 3 in Baba et al., (2004)).

Suppose that and for some and . Then is Gaussian.

3. Graphs for (trans)elliptical distributions

3.1. Partial correlation graph and dependence

By Proposition 2.5 it is not possible to do structural learning in (non-normal) elliptical graphical models, under the conditional independence definition. It is then natural to look for relaxations that may be useful from the modelling point of view. A common strategy is to define graphs based on zeroes in the inverse covariance matrix, mimicking the Gaussian case; see Vogel & Fried, (2011).

Definition 3.1.

The partial correlation graph (PG) is the graph over vertex set with an edge between if and only if .

Equivalently, if and only if the partial correlation . In general, does not imply conditional independence but only linear independence. The aim of this section is to understand what additional information does the PG carry in elliptical distributions. Proposition 2.1 and standard matrix algebra give

| (6) |

hence if and only if does not depend on . This immediately gives the following standard result.

Proposition 3.2.

Let . Then if and only if , or equivalently, and depend on only.

Our first main results offer a stronger characterization for elliptical distributions. Lemma 3.3 relates to marginal covariances, and immediately gives Theorem 3.4 on conditional covariances.

Lemma 3.3.

Let and . Then if and only if for any function for which the covariance exists.

Proof..

Without loss of generality assume . By the law of total expectation

where the expectation is computed with respect to the marginal distribution of . The expression inside the expectation is almost surely zero with respect to this distribution. Indeed, by Proposition 2.1,

which is zero because . ∎

Theorem 3.4.

Let . Then if and only if for any function for which this covariance exists.

Proof..

Lemma 3.3 and Theorem 3.4 are if and only if statements, that is, they characterize the presence of zero marginal and partial correlations (respectively). In particular, Theorem 3.4 characterizes the meaning of elliptical PGs: if are conditionally uncorrelated then so are and any function of . For instance, there is no linear association between and higher-order moments associated to , , etc.

The most commonly used elliptical distributions in applications of partial correlation graphs are scale mixture of normals. Our interest in general elliptical distributions is motivated by semi-parametric techniques related to copula models given by transelliptical distributions, which we now discuss in more detail.

3.2. Transelliptical distributions

Recall that has a transelliptical distribution, denoted , if and only if for strictly increasing deterministic functions . If is Gaussian (nonparanormal sub-family) the PG gives conditional independence on and so it is highly interpretable (Liu et al.,, 2012a). More generally, a missing edge in the PG means that , but this interpretation is not very interesting given that is unknown and simply refers to linear conditional independence between the latent . The focus should be directly on the dependence structure of .

Our second main result shows that a weaker version of Theorem 3.4 holds for transelliptical distributions.

Theorem 3.5.

Suppose . Then if and only if the conditional covariance is zero for every function for which the covariance exists.

Proof..

Let . Suppose that for all , taking gives . Since each is a strictly monotone fixed function, it is bijective. It follows that and generate the same -field giving that . Vanishing of this conditional covariance is equivalent to . To prove the reverse implication, note that

where the second equality follows from Theorem 3.4. ∎

Theorem 3.5 helps interpret the PG as follows. If then is conditionally uncorrelated with any function of . Hence learning a single element within (rather than the whole ) describes (local) aspects of conditional dependence of on (and functions thereof). Taking to be the identity function in Theorem 3.5 we get the following result.

Corollary 3.6.

Suppose . If then for some strictly increasing function .

3.3. Rank correlations

Theorem 3.5 is an if and only if statement, hence it fully characterizes the meaning of PG in transelliptical distributions using covariances between any function of and latent . Kendall’s tau gives an interesting alternative characterization that can be interpreted without any reference to .

Let be a continuous random vector and be an independent copy. Kendall’s tau for is

In elliptically-distributed the following beautiful result relates Pearson correlations with Kendall’s tau.

Lemma 3.7 (Lindskog et al., (2003)).

If then

Let , so that . Since Kendall’s tau is invariant under strictly increasing transformations,

Thus and one can learn the correlation matrix of from the observations of without learning simply by estimating and using the above formula that deterministically relates with .

Below is another basic corollary of Lemma 3.7 and the fact that Kendall’s tau is invariant under monotone transformations.

Proposition 3.8.

If then if and only if for all strictly increasing functions . Moreover, if and only if for all strictly increasing .

Define conditional Kendall’s correlation as

| (7) |

where is an independent copy of from the conditional distribution given . If then, by Lemma 3.7 applied to the conditional distribution of given , we have that

| (8) |

Proposition 3.9.

Let . Then if and only if for all strictly increasing , or equivalently, .

Proof..

The last equivalence follows from invariance of under strictly monotone transformations. Let . Suppose for all strictly increasing , then , since Kendall’s tau is invariant to monotone transformations, which by Lemma 3.7 applied to the conditional distribution of given implies that (c.f. Proposition 2.1), or equivalently, . To prove the reverse implication, suppose that , then, by Lemma 3.7, and hence for all strictly increasing . ∎

4. Positive dependence in elliptical distributions

In this section we study PGs in elliptical distributions when one imposes positive dependence. We begin by recalling two important notions of multivariate positive dependence. We show that neither of them is meaningful to learn structure in elliptical PGs. This leads to relaxations given by elliptical distributions whose partial correlations are all nonnegative, which we refer to as positive partial correlation graph (PPG). We then complement the interpretation of PPGs offered by the characterizations in Section 3 by studying positive dependence properties embedded within PPGs.

4.1. Positive dependence

Let be a -variate continuous random vector with density function .

Definition 4.1.

A random vector (or its density function ) is multivariate totally positive of order two () if and only if

| (9) |

where is the coordinatewise minimum and the coordinatewise maximum of and .

Definition 4.2.

is conditionally increasing (CI) if for every and the conditional expectation is an increasing function of for every increasing function .

Proposition 4.3.

If is /CI then each marginal distribution is /CI. If is /CI then each conditional distribution is /CI.

The proof for the marginal distribution for CI follows from the definition. For the property it relies on smart combinatorial arguments; see Karlin & Rinott, (1980). The statement for conditional distributions follows from the definitions.

Another well-known result is that these positivity notions are strictly related, and closed under monotone transforms; see Theorem 3.3 and Proposition 3.5 in Müller & Scarsini, (2001) as well as Proposition 3.1 in Fallat et al., (2017).

Theorem 4.4.

If a random vector is then it is conditionally increasing.

Proposition 4.5.

Let where are strictly increasing. Then is CI is CI. Also is is .

In the Gaussian case both condition (9) and CI simplify to an explicit constraint on the inverse covariance . A symmetric positive definite matrix is called an M-matrix if for all . Denote the set of inverses of M-matrices by . Directly from (1), if and only if all partial correlations are nonnegative.

Proposition 4.6 (Proposition 3.6 in Müller & Scarsini, (2001)).

Suppose is a Gaussian vector with covariance then

4.2. Positive elliptical distributions

We first show in Theorem 4.8 that the positive dependence notions reviewed in Section 4.2 are not useful in our elliptical setting. If has any zeroes then cannot be CI (hence neither , from Theorem 4.4) unless is Gaussian. The same impossibility result applies to transelliptical families (outside the nonparanormal sub-family). As a consequence, it is not possible to learn structure (remove edges) of a non-normal elliptical graphical model under these positivity constraints.

Even if one were to forsake structural learning and focus on the fully dense graph with no missing edges, it is not possible to find /CI transelliptical distributions, except in very restrictive cases. For example, Proposition 4.9 shows that there are no /CI t-distributions. We defer a deeper analysis to Section 4.3, where we fully characterize the elliptical class and show that it is highly restrictive, particularly as grows.

We conclude the current section by defining positive transelliptical distributions to be those for which for all (equivalently, being an M-matrix, following upon Agrawal et al., (2019)) and showing basic properties such as closedness under margins, conditionals and increasing transforms. We also give properties important for inference, such as positivity of partial correlations given any conditioning set, partial faithfulness and that Simpson’s paradox cannot occur.

Remark 4.7.

Suppose . From (6) it follows that is an M-matrix if and only if for every the conditional expectation is increasing in . Note that, if is CI then must be increasing in and so, in particular, for all . This shows that nonnegativity of all partial correlations is a necessary condition for to be CI and so also for to be .

Theorem 4.8.

Suppose that and is CI. If has a zero entry then is Gaussian. Further, suppose that and is CI. Let , if has a zero entry then is Gaussian.

Proof..

Let be CI and suppose . By Proposition 3.2, the conditional covariance is zero. Since is CI, by Proposition 4.3, the conditional distribution of given is also CI. It is well known that CI distributions are also associated; c.f. Colangelo et al., (2005). By Corollary 3 in Newman, (1984) applied to this conditional distribution we get that implies . From Proposition 2.5 we know that the latter is only possible if is Gaussian. Consider now . From Proposition 4.5, is CI and, since is elliptical, by the first part of the proof, must be Gaussian. ∎

Zeros in the inverse covariance matrix are not the only obstacle for the CI property.

Proposition 4.9.

If has a multivariate t-distribution then is not CI.

Proof..

Since both the CI property and -distribution are closed under taking margins, it is enough to show that no bivariate t-distribution is conditionally increasing. Suppose has bivariate t-distribution with degrees of freedom. Without loss of generality assume that the mean is zero and that the scale matrix satisfies , . By Remark 4.7, necessarily . Moreover, if the statement follows from Theorem 4.8 so assume . The conditional distribution of given is a t-Student distribution with degrees of freedom, , and scale parameter

(c.f. Section 5 in Roth, (2012)). To show that is not CI we provide an increasing function for which is not increasing in . Let , so that , where is the conditional cumulative distribution function (c.d.f.). Using the formula (Johnson et al.,, 1994, (28.4a)) for the c.d.f. of the t-Student distribution, if (or equiv. ), we express in terms of the incomplete beta function

where

Using the definition of the incomplete beta function in terms of the beta function we get that for a positive constant and

Since the integral above is strictly increasing in , to show that is not increasing, it is enough to show that is not an increasing function for . But direct calculations show

showing that is strictly decreasing for all in some neighborhood of . ∎

Proposition 3.3, Rüschendorf & Witting, (2017) states that for an elliptical distribution if and only if is CI. Unfortunately, this result is not true as illustrated both by Theorem 4.8 and Proposition 4.9.

Our results show that the CI/ properties are too restrictive in connection with PGs. As a natural alternative, we study the following relaxation proposed by Agrawal et al., (2019).

Definition 4.10.

An elliptically distributed is positive if for all (equiv. ). A transelliptically distributed is positive if the distribution of is positive elliptical.

From Remark 4.7 this notion of positivity is weaker than both and CI. Similarly, positivity does not imply association: for example if is an M-matrix with a zero entry, then it is positive but not associated in general unless Gaussian. Thus, positive elliptical distributions satisfy a fairly weak notion of positive dependence, that is also simple and useful in applied modelling.

We first collect basic properties of this family of distributions.

Proposition 4.11.

If has a positive (trans)elliptical distribution then the same is true for each marginal and each conditional distribution. Positive transelliptical distributions are also closed under strictly increasing transformations.

Proof..

If then, by Proposition 2.1, for every , . If then by Johnson & Smith, (2011), Corollary 2.3.2. Similarly, then by Johnson & Smith, (2011), Corollary 2.3.1, proving that the conditional distribution of given is a positive elliptical distribution. The same argument after replacing with works for transelliptical distributions. The last statement follows directly from the definition of transelliptical distributions. ∎

The next proposition shows that positive elliptical distributions retain some strong properties of Gaussian distributions.

Proposition 4.12.

If has a positive elliptical distribution then for all and the conditional mean is an increasing function of . Moreover, for any two and it holds that

and

Proof..

These results are well known for Gaussian distributions; c.f. Fallat et al., (2017). It is convenient to translate them to equivalent statements in terms of ; c.f. (Drton et al.,, 2009, Proposition 3.1.13). The statement about the conditional mean and the first statement about conditional correlations follow from the fact that -matrices are closed under taking principal submatrices; c.f. Johnson & Smith, (2011), Corollary 2.3.2. In consequence, for all and it holds that . The last part states that if for some then for every . This statement is given in (Johnson & Smith,, 2011, Theorem 3.3). ∎

These properties are pivotal in the interpretation and application of the classical positive dependence measures. Briefly, the first part says that for positive elliptical distributions conditional correlations are non-negative, regardless of what subset of variables one conditions upon. The second part says that if a covariance conditional on is 0, then it remains 0 when conditioning upon larger sets. In particular, zero marginal correlation implies zero partial correlation, hence Simpson’s paradox cannot occur.

The following result offers an extension of Theorem 3.4 to the positive case.

Proposition 4.13.

If where then for every , any increasing function , and any conditioning set .

Proof..

Let . By the law of total expectation

where we denote . Denote , which is an M-matrix by Johnson & Smith, (2011), Corollary 2.3.2. Using that is an M-matrix, expression (6) gives that all entries in the vector are non-negative, hence is a non-decreasing function of . Further, note that for any fixed we can write as a function of only. Denote this function by . We thus have

where now both and are nondecreasing functions of . By Property 3 in Esary et al., (1967) it follows that .

∎

Remark 4.14.

Consider a multivariate function . Given then is an increasing function of only , hence we may write

the right-hand side following from Proposition 4.13.

Many constraint-based structure learning algorithms, like the PC algorithm (Spirtes et al.,, 2000), rely on the assumption that the dependence structure in the data-generating distribution reflects faithfully the graph. We say that the distribution of is faithful to a graph if we have that if and only if the subset of vertices separates vertices and in , for any . In words, any independence obtained by conditioning on subsets is reflected in the graph. Under faithfulness one can consistently learn the underlying graph from data by conditioning on potentially smaller subsets than the full set of vertices, and benefit from simpler computation. One may extend this definition to partial correlation graphs (Spirtes et al.,, 2000): the distribution of is linearly faithful to an undirected graph if we have that if and only if separates and in . Bühlmann et al., (2010) proposed a related convenient notion unrelated to any particular graph: the distribution of is partially faithful if we have that for any implies that . Using partial faithfulness Bühlmann et al., (2010) developed a simplified version of the PC algorithm that is computationally feasible even with thousands of variables and was reported to be competitive to standard penalty-based approaches. An important property of positive elliptical distributions is given by the following result.

Proposition 4.15.

Every positive elliptical distribution is partially faithful.

Proof..

The proof follows from Proposition 4.12. ∎

4.3. Characterisation of elliptical distributions

We finish our discussion of positive dependence for elliptical distributions with a complete characterization of distributions. In this section we assume that admits a density with respect to the Lebesgue measure. In this case the density necessarily takes the form

| (10) |

where is a nonnegative function (that may depend on ) called the density generator.

Proposition 1.2 in Abdous et al., (2005) gives a necessary and sufficient condition for bivariate elliptical distributions to be . With a bit of matrix algebra their proof generalizes.

Theorem 4.16.

Suppose has a -dimensional elliptical distribution with partial correlations and suppose admits a twice differentiable density function with the density generator for . Let and let . Then is if and only if for all ; implies for all ; and

| (11) |

for all . In particular, .

Proof..

Without loss of generality assume has mean zero and satisfies . In this case for all . If admits a strictly positive and twice differentiable density function then is if and only if for every

This result, found for example in Bach, (2019) can be proved by elementary means, for example, by applying a second-order mean value theorem (Theorem 9.40 in Rudin, (1964)). In our case so is if and only if for every

| (12) |

Basic calculus gives and

If we perform a change of coordinates to and constrained by and . We extend it to the whole by mapping to and . In the new coordinate system, condition (12) holds if and only if for all

| (13) |

Taking such that (which includes the case), (13) implies that for all , which gives the first condition. If and , (13) cannot hold for all unless , which gives the second condition in the theorem. Now suppose is such that then (13) becomes

| (14) |

To study the bounds on subject to we define the Lagrangian

Denote and . The Lagrangian condition can be then reduced to and

Multiplying both sides by we get

All stationary points must then satisfy . The maximal value of subject to is obtained at a point where . The value of can be found by noting that

where is the vector of ones. Since , . In a similar way we show that the minimal value of is . This gives that (14) is equivalent to

This inequality must be satisfied for every . However the functions and are increasing for and so and . Thus we arrive at (11).

Now suppose that is such that ; implies that ; and (11) holds for all . By reversing the argument above we conclude that (13) holds for all . For all the remaining this inequality also holds because then both sides are equal to zero. However, as we argued before (13) holds for all if and only if is . This concludes our proof. ∎

We illustrate Theorem 4.16 with two examples.

Example 4.17.

By Proposition 4.9, if has a t-distribution then is not conditionally increasing and so, in particular, it is not . Theorem 4.16 provides an easy way to see this. For the d-dimensional t-distribution with degrees of freedom . Since , condition (11) requires that

must be satisfied for all . Taking the limits shows that this is impossible irrespective of . Similarly, in the case of a zero-mean multivariate Laplace distribution the density generator is , where and is the modified Bessel function of the second kind. Irrespective of , and so Laplace distributions are never by the last part of Theorem 4.16.

Example 4.18.

Consider a d-dimensional with generator , i.e. density . This defines a special type of Kotz type distributions; see Fang, (2018) (Section 3.2) and in our case we have

From Theorem 4.16, if ( has thinner-than-Normal tails) then holds if and only if , and similarly if (thicker-than-Normal tails) then also holds if and only if . If then cannot be .

The constraints on possible in Example 4.18 did not take into account one more important aspect of the problem, namely that is a positive definite matrix. To illustrate this, suppose that all off-diagonal entries of are equal, that is, for all . Such is positive definite if and only if . In Example 4.18 this gives an upper bound on that interplays with the lower bound . These two bounds define a non-empty set if and only if . If this holds for any . If this holds if and only if

Note that unless (the Gaussian case), this condition cannot hold for all .

It is remarkable that this simple example generalizes and yields the following characterization of elliptical families with a fixed density generator that contain distributions.

Theorem 4.19.

Consider the family of all elliptical distributions with density generator and let . Then, there exists a scale matrix parameter such that the density (10) is if and only if ; implies ; and

for all .

Proof..

Let and . First suppose that for some the underlying elliptical distribution is . By Theorem 4.16 it follows that and whenever . Assume without loss that is normalized to have ones on the diagonal so that for . The fact that partial correlations must be necessarily nonnegative follows from Remark 4.7. Since is an M-matrix, by Proposition 6.1 in Lauritzen et al., (2019a) we can shrink each off-diagonal entry towards zero preserving positive-definitedness. In particular, the matrix obtained from by replacing each off-diagonal entry with , where , must be positive definite. This matrix is positive definite if and only if , which gives an upper bound on on the top of the two upper bounds implied by Theorem 4.16, namely, and (use the fact that by the last part of Theorem 4.16). The intersection of these three constraints is non-empty if and only if . In other words, and , which finished the proof of one implication.

Now suppose and whenever . If, in addition, the third condition in the theorem is satisfied then and . Let be a matrix with ones on the diagonal and on the remaining entries. If then is positive definite. If then and . Since and we can always find close enough to so that

By Theorem 4.16 the corresponding distribution is . ∎

To illustrate this result consider the elliptically symmetric logistic distribution as defined in Fang, (2018), Section 3.5. The density generator satisfies

Theorem 4.16 gives that a bivariate logistic distribution is if and only if . However, if , Theorem 4.19 implies that there are no distributions of this form.

To summarize, our results show that although there are some non-normal elliptical distributions that are , the imposed constraints can be quite severe, particularly as the dimension grows. We additionally showed that popular elliptical distributions such as the t, Laplace and most Kotz-type distributions in Example 4.18 cannot be . These findings highlight the need to define alternative measures of positive association, such as the PPGs in Section 4.2.

5. Examples

|

|

|

|

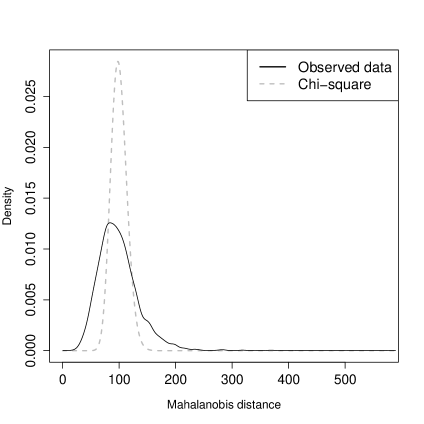

We illustrate the application of transelliptical PG and PPG and the interpretation afforded by our characterizations with S&P500 stock market data. The R code to reproduce our analyses is provided as supplementary material. We downloaded the daily log-returns of S&P500 stocks for the 10-year period ranging from 2010-04-29 to 2020-04-14 ( observations). For illustration we selected the first stocks, hence the graphical model has 4,950 potential edges. We used the R package huge (Zhao et al.,, 2012) to apply univariate transformations aimed at improving the marginal normal fit (function huge.npn). Despite these transformations, we observed departures from multivariate normality. Let the observed and transformed data matrices be and (respectively), both with zero column means and unit variances. The empirical distribution of the Mahalanobis distances , where is the sample covariance, had significantly thicker tails than the expected under multivariate normal data and (Figure 2, top left). This departure from normality motivates considering other elliptical models.

We studied the dependence structure in these data via several models. First we fit a transelliptical model to , where is estimated by first computing Kendall’s and then exploiting their connection to in Lemma 3.7. This procedure can be performed with option npn.func = "skeptic" in function huge.npn, see Liu et al., (2012b) for details. Second, we also fit an elliptical model to . In both models we estimated via graphical LASSO (Friedman et al.,, 2008), where the regularization parameter was set via the EBIC (Chen & Chen, (2008), function huge.select), in the transelliptical case using the pseudo-likelihood defined by , see Foygel & Drton, (2010). The transelliptical model is in principle more robust, in that it does not require estimating the marginal transformations. However both models provided similar results: the Spearman correlation between the estimated was 0.911, the selected PGs agreed in 93.0% of the 4,950 edges, and there were no disagreements in the signs of for any .

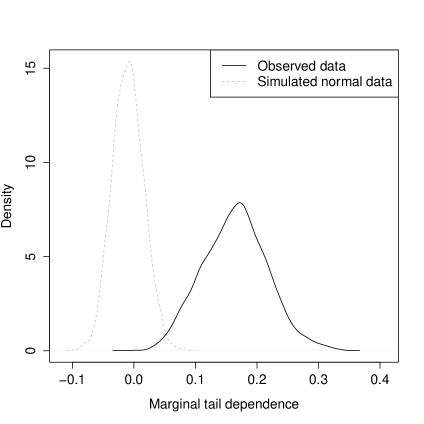

To illustrate the interpretation of the PG implied by , relative to a Gaussian graphical model, we focus on the elliptical model for . Figure 2 (bottom left) shows that the marginal tail dependence in (2) is significantly larger than the expected under normality. The magnitude of these departures is practically significant. For comparison the figure also displays estimated from simulated Normal data, with zero mean and sample covariance matching that of .

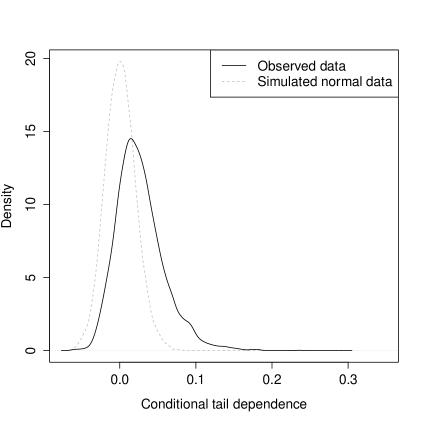

In practical terms, measures the predictability of a variable’s variance (also called volatility) from that of other variables. A natural question is what predictability remains after conditioning upon other variables, i.e. what is the conditional tail dependence in (3). To address this question for each variable pair we computed the non-parametric estimate

where , is the -th column in and the least-squares prediction given (analogously for ). These estimates were significantly larger than the expected under normality (Figure 2, bottom right). As a further check, from (3) the elliptical model (more specifically, the scale mixture of normals sub-family) predicts to be linear in . Figure 2 (top right) suggests that they are indeed roughly linearly related. Admittedly one never expects a model to describe the data perfectly, but the elliptical model appears reasonable to study volatility in these data.

The estimated partial correlation graph had 1,600 out of the 4,950 edges. Our results from Section 3 help strengthen the interpretation of the missing edges, e.g. suggests that conditional on one cannot predict the variance, asymmetry or kurtosis in linearly from . Further it also implies zero Kendall’s conditional tau between increasing transforms of and , e.g. if daily returns are not conditionally positively/negative correlated (according to Kendall’s tau) then neither are log-returns.

A quite interesting point is that among the edges the estimated partial correlations were positive for and negative for only edges. That is, the partial correlation graph was very close to being a PPG; see Agrawal et al., (2019) for a discussion why this may be frequently encountered in stock data, and Epskamp & Fried, (2018); Lauritzen et al., (2019b) for examples in Psychology. To compare the PPG fit with our earlier graphical LASSO fit we estimated the precision matrix under the constraint that is an M-matrix, using the R package mtp2 available at GitHub (Lauritzen et al.,, 2019a, Algorithm 1)111Package golazo that recently appeared on GitHub offers a more flexible and scalable way of doing this and other related computations. The relevant function is positive.golazo(S,rho=Inf), where is the sample covariance matrix. See Lauritzen & Zwiernik, (2020) for more details.. The maximized constrained log-likelihood was substantially higher than for the graphical LASSO fit ( versus ) and the graph was sparser ( versus edges), hence the EBIC (and any other model selection criteria) strongly favored the PPG model. Note that, from its Lagrangian interpretation, the graphical LASSO constrains the size . In contrast the M-matrix constraint allows for arbitrarily large , provided . That is, the graphical LASSO and the PPG constraints induce quite different regularization and the latter appears more appropriate for these S&P500 data, illustrating the potential value of positivity constraints in certain applications.

The selected graph being a PPG strengthens its interpretation. By Proposition 4.12, the finding suggests that all possible partial correlations are positive regardless of the conditioning set, and that Simpson’s paradox does not occur in these data, i.e. stocks with zero marginal correlation also have zero partial correlation. By our earlier discussion, this implies that if marginally then is uncorrelated with higher moments of , both marginally and conditionally on . Further, the conditional expectation of can only be increasing as a function of other variables (or increasing transformations thereof), and missing edges indicate the lack of such association.

6. Discussion

When studying multivariate dependence in applications it is often convenient to strike a balance between models that equip strong theoretical properties (e.g. Gaussian, non-paranormal, and CI classes) but impose potentially restrictive conditions, and models that are more flexible but do not provide such strong characterizations and/or lead to complex interpretations. We studied a natural strategy based on the transelliptical family and partial correlation graphs, including many copula models that are popular in applications. We showed that the interpretation remains simple yet goes far beyond the regular linear dependence.

This work is also relevant in the context of Gaussian graphical models. Although the partial correlation graph in the Gaussian case translates into conditional independence statements, it is important to understand how robust is this interpretation with respect to the Gaussianity assumption. Our analysis shows that in the elliptical case a lot of this dependence information is retained. We also illustrate how simple tail dependence measures, like the one in (2), characterize the Gaussian distribution within the scale mixture of normals family and can help assess whether transelliptical class is useful to capture second-order dependence (variance) dependencies in the data.

An important part of this paper is the study of positive dependence. The notion of positivity can be quite useful in regularizing inference relative to unrestricted penalized likelihood, as we illustrated in the S&P500 example. However, we also showed that strictly speaking some standard notions of positive dependence are meaningless for structural learning in elliptical partial correlation graphs. One of our main contributions is a remarkable result that characterizes elliptical distributions and shows that becomes very restrictive in high dimensions. It is therefore important to study relaxations such as positive elliptical distributions that impose all partial correlations to be nonnegative. We showed that this family retains strong positive dependence properties that are important from the applied point of view.

In conclusion, we hope that our results help to motivate the study of other suitable relaxations of Gaussianity and positivity in graphical models, as well as strengthen the use of transelliptical graphical models in practice.

Acknowledgements

We thank Yuhao Wang, Frank Röttger, and Ludger Rüschendorf for helpful remarks. We also thank the reviewer and the AE of the first version of this manuscript for pointing to us a mistake in the original proof of Lemma 3.3 and other inaccuracies.

References

- Abdous et al., (2005) Abdous, Belkacem, Genest, Christian, & Rémillard, Bruno. 2005. Dependence properties of meta-elliptical distributions. Pages 1–15 of: Statistical Modeling and Analysis for Complex Data Problems. Springer.

- Agrawal et al., (2019) Agrawal, Raj, Roy, Uma, & Uhler, Caroline. 2019. Covariance Matrix Estimation under Total Positivity for Portfolio Selection. arXiv preprint arXiv:1909.04222.

- Baba et al., (2004) Baba, Kunihiro, Shibata, Ritei, & Sibuya, Masaaki. 2004. Partial correlation and conditional correlation as measures of conditional independence. Australian & New Zealand Journal of Statistics, 46(4), 657–664.

- Bach, (2019) Bach, Francis. 2019. Submodular functions: from discrete to continuous domains. Mathematical Programming, 175(1-2), 419–459.

- Barber & Kolar, (2018) Barber, Rina Foygel, & Kolar, Mladen. 2018. Rocket: Robust confidence intervals via Kendall’s tau for transelliptical graphical models. The Annals of Statistics, 46(6B), 3422–3450.

- Behrouzi & Wit, (2019) Behrouzi, Pariya, & Wit, Ernst C. 2019. Detecting epistatic selection with partially observed genotype data by using copula graphical models. Journal of the Royal Statistical Society: Series C (Applied Statistics), 68(1), 141–160.

- Bilodeau, (2014) Bilodeau, Martin. 2014. Graphical lassos for meta-elliptical distributions. Canadian Journal of Statistics, 42(2), 185–203.

- Bowman & Foster, (1993) Bowman, Adrian, & Foster, Peter. 1993. Density based exploration of bivariate data. Statistics and Computing, 3(4), 171–177.

- Bühlmann et al., (2010) Bühlmann, Peter, Kalisch, Markus, & Maathuis, Marloes H. 2010. Variable selection in high-dimensional linear models: partially faithful distributions and the PC-simple algorithm. Biometrika, 97(2), 261–278.

- Chen & Chen, (2008) Chen, J., & Chen, Z. 2008. Extended Bayesian information criteria for model selection with large model spaces. Biometrika, 95(3), 759–771.

- Colangelo et al., (2005) Colangelo, Antonio, Scarsini, Marco, & Shaked, Moshe. 2005. Some notions of multivariate positive dependence. Insurance: Mathematics and Economics, 37(1), 13–26.

- Drton et al., (2009) Drton, Mathias, Sturmfels, Bernd, & Sullivant, Seth. 2009. Lectures on Algebraic Statistics. Vol. 39. Birkhäuser Basel.

- Epskamp & Fried, (2018) Epskamp, Sacha, & Fried, Eiko I. 2018. A tutorial on regularized partial correlation networks. Psychological methods, 23(4), 617.

- Esary et al., (1967) Esary, James D, Proschan, Frank, & Walkup, David W. 1967. Association of random variables, with applications. Ann. Math. Stat., 38(5), 1466–1474.

- Fallat et al., (2017) Fallat, Shaun, Lauritzen, Steffen L., Sadeghi, Kayvan, Uhler, Caroline, Wermuth, Nanny, & Zwiernik, Piotr. 2017. Total positivity in Markov structures. Annals of Statistics, 45, 1152–1184.

- Fang et al., (2002) Fang, Hong-Bin, Fang, Kai-Tai, & Kotz, Samuel. 2002. The meta-elliptical distributions with given marginals. Journal of Multivariate Analysis, 82(1), 1–16.

- Fang, (2018) Fang, Kai Wang. 2018. Symmetric Multivariate and Related Distributions. Chapman and Hall/CRC.

- Feller, (1971) Feller, William. 1971. An Introduction to Probability Theory and Applications. second edn. Vol. 2. New York: John Wiley & Sons.

- Finegold & Drton, (2009) Finegold, Michael A, & Drton, Mathias. 2009. Robust graphical modeling with t-distributions. Pages 169–176 of: Proceedings of the Twenty-Fifth Conference on Uncertainty in Artificial Intelligence.

- Foygel & Drton, (2010) Foygel, Rina, & Drton, Mathias. 2010. Extended Bayesian information criteria for Gaussian graphical models. Pages 604–612 of: Advances in neural information processing systems.

- Friedman et al., (2008) Friedman, Jerome, Hastie, Trevor, & Tibshirani, Robert. 2008. Sparse inverse covariance estimation with the graphical lasso. Biostatistics, 9(3), 432–441.

- Johnson & Smith, (2011) Johnson, Charles R, & Smith, Ronald L. 2011. Inverse M-matrices, II. Linear Algebra and its Applications, 435(5), 953–983.

- Johnson et al., (1994) Johnson, Norman Lloyd, Kotz, Samuel, & Balakrishnan, Narayanaswamy. 1994. Continuous Univariate Distributions. Second edn. Vol. 2. Wiley New York.

- Karlin & Rinott, (1980) Karlin, Samuel, & Rinott, Yosef. 1980. Classes of orderings of measures and related correlation inequalities. I. Multivariate totally positive distributions. J. Multiv. Anal., 10(4), 467–498.

- Kelker, (1970) Kelker, Douglas. 1970. Distribution theory of spherical distributions and a location-scale parameter generalization. Sankhyā: The Indian Journal of Statistics, Series A, 419–430.

- Lauritzen, (1996) Lauritzen, S. L. 1996. Graphical Models. Oxford, United Kingdom: Clarendon Press.

- Lauritzen & Zwiernik, (2020) Lauritzen, Steffen, & Zwiernik, Piotr. 2020. Locally associated graphical models. arXiv preprint arXiv:2008.04688.

- Lauritzen et al., (2019a) Lauritzen, Steffen, Uhler, Caroline, & Zwiernik, Piotr. 2019a. Maximum likelihood estimation in Gaussian models under total positivity. Annals of Statistics, 47(4), 1835–1863.

- Lauritzen et al., (2019b) Lauritzen, Steffen, Uhler, Caroline, & Zwiernik, Piotr. 2019b. Total positivity in exponential families with application to binary variables. To appear in the Annals of Statistics.

- Lindskog et al., (2003) Lindskog, Filip, Mcneil, Alexander, & Schmock, Uwe. 2003. Kendall’s tau for elliptical distributions. Pages 149–156 of: Credit Risk. Springer.

- Liu et al., (2012a) Liu, Han, Han, Fang, Yuan, Ming, Lafferty, John, & Wasserman, Larry. 2012a. High-dimensional semiparametric Gaussian copula graphical models. The Annals of Statistics, 40(4), 2293–2326.

- Liu et al., (2012b) Liu, Han, Han, Fang, & Zhang, Cun-hui. 2012b. Transelliptical graphical models. Pages 800–808 of: Advances in Neural Information Processing Systems.

- Müller & Scarsini, (2001) Müller, Alfred, & Scarsini, Marco. 2001. Stochastic comparison of random vectors with a common copula. Mathematics of Operations Research, 26(4), 723–740.

- Newman, (1984) Newman, Charles M. 1984. Asymptotic independence and limit theorems for positively and negatively dependent random variables. Lecture Notes-Monograph Series, 127–140.

- Robeva et al., (2018) Robeva, Elina, Sturmfels, Bernd, Tran, Ngoc, & Uhler, Caroline. 2018. Maximum Likelihood Estimation for Totally Positive Log-Concave Densities. Scandinavian Journal of Statistics.

- Roth, (2012) Roth, Michael. 2012. On the multivariate t distribution. Linköping University Electronic Press.

- Rudin, (1964) Rudin, Walter. 1964. Principles of Mathematical Analysis. Vol. 3. McGraw-hill New York.

- Rüschendorf & Witting, (2017) Rüschendorf, Ludger, & Witting, Julian. 2017. VaR bounds in models with partial dependence information on subgroups. Dependence Modeling, 5(1), 59–74.

- Slawski & Hein, (2015) Slawski, Martin, & Hein, Matthias. 2015. Estimation of positive definite M-matrices and structure learning for attractive Gaussian Markov random fields. Linear Algebra and its Applications, 473, 145–179.

- Spirtes et al., (2000) Spirtes, Peter, Glymour, Clark N, Scheines, Richard, & Heckerman, David. 2000. Causation, prediction, and search. Cambridge, MA, USA: MIT press.

- Stephens, (2013) Stephens, Matthew. 2013. A unified framework for association analysis with multiple related phenotypes. PloS one, 8(7).

- Székely & Rizzo, (2009) Székely, Gábor J, & Rizzo, Maria L. 2009. Brownian distance covariance. The Annals of Applied Statistics, 1236–1265.

- Vinciotti & Hashem, (2013) Vinciotti, Veronica, & Hashem, Hussein. 2013. Robust methods for inferring sparse network structures. Computational Statistics & Data Analysis, 67, 84–94.

- Vogel & Fried, (2011) Vogel, Daniel, & Fried, Roland. 2011. Elliptical graphical modelling. Biometrika, 98(4), 935–951.

- Zhao & Liu, (2014) Zhao, Tuo, & Liu, Han. 2014. Calibrated precision matrix estimation for high-dimensional elliptical distributions. IEEE transactions on Information Theory, 60(12), 7874–7887.

- Zhao et al., (2012) Zhao, Tuo, Liu, Han, Roeder, Kathryn, Lafferty, John, & Wasserman, Larry. 2012. The huge package for high-dimensional undirected graph estimation in R. Journal of Machine Learning Research, 13(Apr), 1059–1062.