Abstract

Let denote , where , is a sequence of integers such that and , and is the order statistics of iid random variables with regularly varying upper tail. The estimator is an extension of the Hill estimator. We investigate the asymptotic properties of and both for fixed and for . We prove strong consistency and asymptotic normality under appropriate assumptions. Applied to real data we find that for larger the estimator is less sensitive to the change in than the Hill estimator.

Keywords: tail index; Hill estimator; residual estimator;

regular variation

MSC2010: 62G32, 60F05

Limit laws for the norms of extremal samples

Péter Kevei111 kevei@math.u-szeged.hu, Lillian Oluoch222 oluoch@math.u-szeged.hu, and László Viharos333 viharos@math.u-szeged.hu

Bolyai Institute, University of Szeged

Aradi vértanúk tere 1, 6720, Szeged, Hungary

1 Introduction

Let be iid random variables with common distribution function , . For each , let denote the order statistics of the sample . Assume that

where is a slowly varying function at infinity and . This is equivalent to the condition

| (1) |

where , , stands for the quantile function, and is a slowly varying function at 0. For introduce the notation

| (2) |

In what follows we always assume that is a sequence of integers such that and .

As a special case for we obtain the well-known Hill estimator of the tail index introduced by Hill in 1975 [14]. For the estimator was suggested by Dekkers et al. [10], where they proved that a.s. or in probability, depending on the assumptions on , and they proved asymptotic normality of the estimator as well. Segers [18] considered more general estimators of the form

for a nice class of functions , called residual estimators. Segers proved weak consistency and asymptotic normality under general conditions. More recently, Ciuperca and Mercadier [5] investigated weighted version of (2) and obtained weak consistency and asymptotic normality for the estimator.

To the best of our knowledge the possibility was not considered before. The estimate of the tail index

can be considered as as the limit law for the norm of the extremal sample. In this direction Schlather [17] and Bogachev [4] proved limit theorems for norms of iid samples.

In the present paper we investigate the asymptotic properties of and both for fixed and for . In Sections 2 and 3 is fixed, while it tends to infinity in Section 4. In Theorem 2.3 we prove strong consistency of the estimator for fixed . Strong consistency was only obtained by Dekkers et al. [10] for and , thus our result is new for general . Asymptotic normality is treated in Section 3. In this direction very general results was obtained by Segers [18] for residual estimators. However, our assumptions in Theorem 3.4 on the slowly varying function are weaker than in Theorem 4.5 in [18]. In Section 4 we obtain weak consistency and asymptotic normality when . Section 5 contains the simulation results and data analysis. Here we show that for larger values of the estimator is not so sensitive to the choice of , which is a critical property in applications. We demonstrate this property on the well-known dataset of Danish fire insurance claims, see Resnick [16] and Embrechts et al. [12, Example 6.2.9]. The technical proofs are gathered together in Section 6.

2 Consistency

In what follows, are iid uniform random variables, and stands for the order statistics. To ease notation we frequently suppress the dependence on and simply write . According to the well-known quantile representation, we have

which implies that in (2) can be written as

| (3) |

In what follows we use this representation. Therefore, to understand the behavior of first we have to handle uniform random variables. In the following , , stands for the usual gamma function.

Lemma 2.1.

For any sequence such that and , we have

Proof.

One only has to notice that the sequence has the distribution as , where are iid uniform random variables. Noting that , the statement follows from the law of large numbers. ∎

We note that the representation above immediately implies the asymptotic normality

with .

For the almost sure version we need some assumption on .

Lemma 2.2.

Assume that for some , and . Then

First we show strong consistency for . Our assumption on the sequence is the same as in Theorem 2.1 in [10]. This is not far from the optimal condition , which was obtained by Deheuvels et al. [9].

Theorem 2.3.

Assume that (1) holds and , for some . Then a.s., that is for fixed the estimator is strongly consistent.

Weak consistency holds under weaker assumption on . The following result is a special case of Theorem 2.1 in [18], and it follows from representation (3) and from the law of large numbers.

Theorem 2.4.

Assume that (1) holds, and the sequence is such that , . Then , that is for fixed the estimator is weakly consistent.

3 Asymptotic normality

To prove asymptotic normality we use that in representation (3) the summands are independent and identically distributed conditioned on . Indeed, conditioned on

| (4) |

where are iid uniform random variables, independent of , and stands for the order statistics of , , .

To state the result, we need some notation. Introduce the variable for

| (5) |

where is uniform, and . Define

and the corresponding limiting quantities

Note that the quantities , , , depend on the parameter . However, since the value is fixed, to ease notation we suppress in the following.

Central limit theorem with random centering was obtained in Theorem 4.1 in [18]. Next, we spell out this result in our case. In the special case we obtain Theorem 1.6 by Csörgő and Mason [6]. The key observation in the proof is the representation (4).

Theorem 3.1.

To obtain asymptotic normality for the estimator, i.e. to change the random centering to , we have to show that

Since in probability, this is the same as the deterministic convergence

see the proof of Theorem 3.4 for the precise version. In case of the Hill estimator Csörgő and Viharos [7] obtained optimal conditions under which the random centralization in Theorem 3.1 can be replaced by the deterministic one . For general residual estimator this was obtained in Theorem 4.2 in [18]. In Theorem 4.5 in [18] conditions were obtained which assures that the random centering can be replaced by the limit . However, in Theorem 4.5 in [18] the slowly varying function belongs to the de Haan class , see the definitions below. Our assumptions are weaker.

We need second order conditions on the slowly varying function . First assume that

| (6) |

where is a regularly varying function such that

| (7) |

In Proposition 3.3 we assume less stringent conditions on , however in this case it is easier to obtain the rate of convergence.

In the following two propositions we allow at certain rate, which we assume in the next section.

Proposition 3.2.

Now we turn to more general conditions on the slowly varying function . We still need some kind of weak second order condition. Assume that there is a regularly varying function for which (7) holds, and a Borel set with positive measure, such that

| (9) |

By Theorem 3.1.4 in Bingham et al. [3] condition (9) implies that the limsup in (9) is finite uniformly on any compact set of . However, in general, uniformity cannot be extended to . Put , . Introduce the notation

and for

| (10) |

Note that the weaker conditions on imply more restrictive conditions on , when .

Proposition 3.3.

Note that if is fixed then and we obtain the same bound as in Proposition 3.2.

We emphasize that we do not need exact second-order asymptotics for , only bounds. In particular, if belongs to the de Haan class (defined at 0) then the conditions (9) and (7) holds; see Appendix B in de Haan and Ferreira [8], or Chapter 3 in Bingham et al. [3]. Therefore, even in the special case , i.e. for the Hill estimator, our next result is a generalization of Theorem 3.1 in [10]. The conditions in Theorem 4.5 in [18] are also more restrictive.

Proof.

The theorem is an immediate consequence of Theorem 3.1 and Proposition 3.3. Indeed, by Proposition 3.3

By the assumption , while the last two factors tends to 1, since and are regularly varying and .

The central limit theorem for follows from the previous result using the delta method, see Agresti [1, Section 14.1]. ∎

4 Asymptotics for large

In this section we assume that tends to infinity at a certain rate. First we determine the asymptotic behavior of the moments as .

Lemma 4.1.

For any there is a and such that for ,

Proof.

First note that if is a nonnegative random variable for which for any then for any

This implies that for any and there exist such that for

| (12) |

Using the Potter bounds (see (28)) and (12), for any and there exists , and such that for ,

Together with an analogous lower bound, the statement follows. ∎

Recall (5). Let be iid random variables, and put

The following results are analogous to Theorems 2.1 and 2.2 by Bogachev [4]. The main difficulty in our setup is the additional parameter , in which we need some kind of uniformity. For the sequence let

| (13) |

Note that in (13) means that increases at most logarithmically. To obtain a weak law of a large numbers we need that .

Proposition 4.2.

If then there exists such that uniformly for as

that is for any

For the central limit theorem we need further restriction on . In the iid case treated by Bogachev the condition is sharp in the sense that for non-Gaussian stable limit theorem holds, see [4, Theorem 2.4].

Proposition 4.3.

If then uniformly on for some small enough

that is for any

where is the standard normal distribution function.

As a consequence we obtain the following.

Theorem 4.4.

Assume that , , and . Let denote

| (14) |

If then

Furthermore, for

Note that both the centering and the norming is random. To change to deterministic values and further assumptions are needed. Recall in (14).

Theorem 4.5.

Proof.

First note that in probability, and since and are regularly varying functions can be changed to .

Similarly, it is possible to obtain law of large numbers and central limit theorem under the conditions of Proposition 3.3. We do not go into further details.

Next we translate the previous result for our estimator.

Theorem 4.6.

Assume that , , and . If then

If then

Furthermore, under the conditions of Theorem 4.5, deterministic centering and norming works, i.e.

| (16) |

Proof.

Example.

5 Simulation study

We provide simulation study for our estimators. Note that for we obtain the usual Hill estimator. In Theorem 5.1 Segers [18] proved the optimality of the Hill estimator among residual estimators. We also see from Theorem 4.6 that the asymptotic variance increases with . However, in practical situation higher values turns out to be useful as we show below.

In the simulations below and we repeated the simulations times. In all the figures the mean and mean squared error (MSE) are calculated for different values of and .

In Table 1 we see that the Hill estimator is the best in the strict Pareto model. In this case . However, in practice it is very unusual to encounter data which fit to a nice distribution everywhere. It is more common that the large values fit to a Pareto-type distribution, while the smaller values behave as a light-tailed distribution. Consider the quantile function

| (18) |

which is a mixture of an exponential and a strict Pareto quantile. The parameter of the exponential is chosen such that is continuous. Table 2 contains the simulation results for . In this simple model we already see the advantage of larger values. Note that the Hill estimator is very sensitive to the change of for those values where the quantile function changes. Indeed, for we basically have a sample from a strict Pareto distribution, and for those values the Hill estimator is the best. For we already see the exponential part of the sample, and the Hill estimator changes drastically (from 0.98 to 0.76), while for the change is not as large (from 0.92 to 0.88).

| mean | |||

|---|---|---|---|

| 0.9964 | 1.0001 | 1.0007 | |

| 0.9458 | 0.9878 | 0.9942 | |

| 0.7508 | 0.8946 | 0.9300 |

| MSE | |||

|---|---|---|---|

| 0.1022 | 0.0194 | 0.0100 | |

| 0.1086 | 0.0229 | 0.0121 | |

| 0.1531 | 0.0512 | 0.0343 |

| mean | |||||

|---|---|---|---|---|---|

| 1.0039 | 0.9968 | 1.0021 | 0.9790 | 0.7654 | |

| 0.6663 | 0.7469 | 0.8260 | 0.9238 | 0.8836 | |

| 0.4387 | 0.5175 | 0.6009 | 0.7430 | 0.7480 |

| MSE | |||||

|---|---|---|---|---|---|

| 0.1981 | 0.1039 | 0.0493 | 0.0112 | 0.0593 | |

| 0.2241 | 0.1529 | 0.0967 | 0.0348 | 0.0344 | |

| 0.3663 | 0.2799 | 0.2011 | 0.0947 | 0.0883 |

Next, we further add a nonconstant slowly varying function to the quantile. A logarithmic factor in the tail of the random variable cannot be detected, but it makes significantly more difficult to determine the underlying index of regular variation. We modify the construction in (18) and consider the quantile function

| (19) |

Note again that the function is continuous. We see from the simulation results in Table 3 that in this setup the estimators with larger values work much better than the Hill estimator. These estimators are not so sensitive for the change in the nature of the quantile function.

| mean | |||||

|---|---|---|---|---|---|

| 1.5019 | 1.5516 | 1.6387 | 1.9031 | 1.2517 | |

| 0.9777 | 1.1242 | 1.2807 | 1.5962 | 1.4835 | |

| 0.6427 | 0.7760 | 0.9250 | 1.2507 | 1.2297 |

| MSE | |||||

|---|---|---|---|---|---|

| 0.6599 | 0.5325 | 0.5250 | 0.8519 | 0.0781 | |

| 0.2145 | 0.1845 | 0.2033 | 0.4061 | 0.2712 | |

| 0.2247 | 0.1396 | 0.0843 | 0.1147 | 0.0978 |

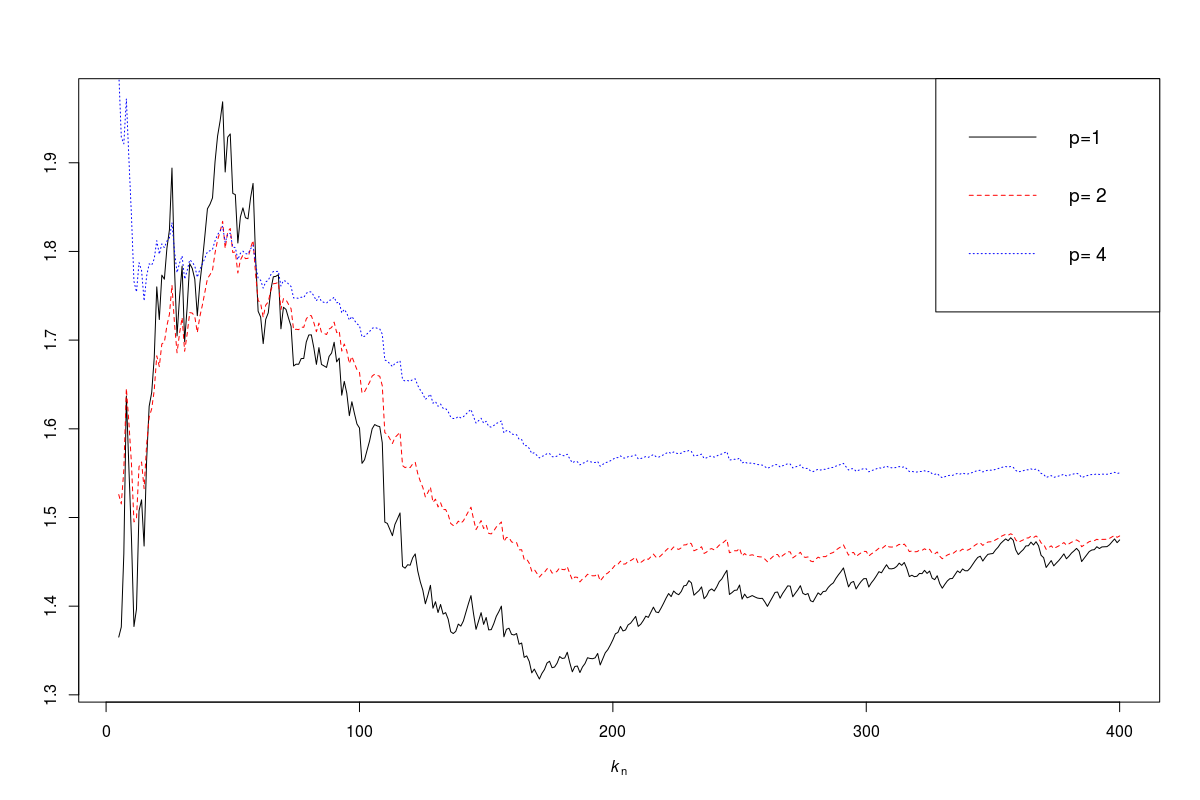

We also apply the estimator with different values to real data. We chose the data set of Danish fire insurance losses, which consists of 2167 fire losses in millions of Danish Kroner. The data set is included in the R package evir, and was analyzed in [16] and in [12, Example 6.2.9]. In Figure 1 we plotted the estimate for , i.e. we plotted against , to obtain the Hill plot in [16] for . Resnick [16] used various techniques to obtain smoother plot. In our setting larger values naturally produces smoother plots.

6 Proofs

6.1 Strong consistency

Proof of Lemma 2.2..

Let denote the empirical distribution function of the sample , , . Then, integrating by parts, we have

| (20) |

Theorem 1 by Wellner [19] implies that

| (21) |

Thus, the first term in the right-hand side of (20) tends to 0 a.s. For the second term

Again by (21)

| (22) |

For the second term, choosing , we have

| (23) |

where is a finite constant, not depending on . Using Theorem 1(ii) by Einmahl and Mason [11] we see that the last term in (23) is a.s. bounded, if , which holds if is close enough to . The first term in (23) tends to 0. From (22), (23), and (20) the statement follows. ∎

Proof of Theorem 2.3..

By the Potter bounds ([3, Theorem 1.5.6]), for any , there exist such that

| (24) |

Since , equation (21) implies a.s. Therefore, for large enough a.s.

| (25) |

6.2 Asymptotic normality

First we need two simple auxiliary lemmas.

Lemma 6.1.

For , , and we have

Proof.

Simply , with being between and . If then , thus

If then , thus for , and

While if and

∎

Lemma 6.2.

For we have

Proof.

Simple calculation gives that

∎

Proof of Proposition 3.2..

First we deal with the integral on . By (24), for any , , there is such that for ,

| (28) |

implying that uniformly on

| (29) |

Writing

we see that the first factor tends to 0 by (7) and the second factor is bounded by (6). Therefore, uniformly in

| (30) |

By (29) and (30), if (8) holds then, uniformly on ,

| (31) |

Thus,

| (32) |

Proof of Proposition 3.3..

The difference compared to the previous proof is that (6) does not hold uniformly in , which implies that the integral on has to be treated differently.

By Theorem 3.1.4 in [3] (translating the results from infinity to zero, by defining , )

This implies that the bound (33) on remains true and on as in (32) we have

| (34) |

6.3 Asymptotics for large

Proof of Proposition 4.2..

We follow the proof of Theorem 2.1 in [4]. Fix , and let . Using the Markov inequality, the Marcinkiewicz–Zygmund inequality (see e.g. [15, 2.6.18]), and the subadditivity we have

| (41) |

By Lemma 4.1 for any we can choose and such that for and

with . Thus, by the Stirling formula

| (42) |

As we can choose such that . Then choosing small enough we see that the right-hand side in (42) is negative, implying that the right-hand side in (41) tends to 0. ∎

Proof of Proposition 4.3..

Acknowledgements. PK’s research was partially supported by the János Bolyai Research Scholarship of the Hungarian Academy of Sciences, by the NKFIH grant FK124141, by the Ministry of Human Capacities, Hungary grant 20391-3/2018/FEKUSTRAT and by the EU-funded Hungarian grant EFOP-3.6.1-16-2016-00008. LV’s research was partially supported by the Ministry of Human Capacities, Hungary grant TUDFO/47138-1/2019-ITM.

References

- [1] A. Agresti. Categorical data analysis. Wiley Series in Probability and Statistics. Wiley-Interscience [John Wiley & Sons], New York, second edition, 2002.

- [2] P. Billingsley. Probability and measure. Wiley Series in Probability and Mathematical Statistics. John Wiley & Sons, Inc., New York, third edition, 1995. A Wiley-Interscience Publication.

- [3] N. H. Bingham, C. M. Goldie, and J. L. Teugels. Regular variation, volume 27 of Encyclopedia of Mathematics and its Applications. Cambridge University Press, Cambridge, 1989.

- [4] L. Bogachev. Limit laws for norms of IID samples with Weibull tails. J. Theoret. Probab., 19(4):849–873, 2006.

- [5] G. Ciuperca and C. Mercadier. Semi-parametric estimation for heavy tailed distributions. Extremes, 13(1):55–87, 2010.

- [6] S. Csörgő and D. M. Mason. Central limit theorems for sums of extreme values. Math. Proc. Cambridge Philos. Soc., 98(3):547–558, 1985.

- [7] S. Csörgő and L. Viharos. On the asymptotic normality of Hill’s estimator. Math. Proc. Cambridge Philos. Soc., 118(2):375–382, 1995.

- [8] L. de Haan and A. Ferreira. Extreme value theory. Springer Series in Operations Research and Financial Engineering. Springer, New York, 2006. An introduction.

- [9] P. Deheuvels, E. Haeusler, and D. M. Mason. Almost sure convergence of the Hill estimator. Math. Proc. Cambridge Philos. Soc., 104(2):371–381, 1988.

- [10] A. L. M. Dekkers, J. H. J. Einmahl, and L. de Haan. A moment estimator for the index of an extreme-value distribution. Ann. Statist., 17(4):1833–1855, 1989.

- [11] J. H. J. Einmahl and D. M. Mason. Laws of the iterated logarithm in the tails for weighted uniform empirical processes. Ann. Probab., 16(1):126–141, 1988.

- [12] P. Embrechts, C. Klüppelberg, and T. Mikosch. Modelling extremal events, volume 33 of Applications of Mathematics (New York). Springer-Verlag, Berlin, 1997. For insurance and finance.

- [13] P. Hall. On some simple estimates of an exponent of regular variation. J. Roy. Statist. Soc. Ser. B, 44(1):37–42, 1982.

- [14] B. M. Hill. A simple general approach to inference about the tail of a distribution. Ann. Statist., 3(5):1163–1174, 1975.

- [15] V. V. Petrov. Limit theorems of probability theory, volume 4 of Oxford Studies in Probability. The Clarendon Press, Oxford University Press, New York, 1995.

- [16] S. Resnick. Discussion of the Danish data on large fire insurance losses. 27(1):139–151, 1997.

- [17] M. Schlather. Limit distributions of norms of vectors of positive i.i.d. random variables. Ann. Probab., 29(2):862–881, 2001.

- [18] J. Segers. Residual estimators. J. Statist. Plann. Inference, 98(1-2):15–27, 2001.

- [19] J. A. Wellner. Limit theorems for the ratio of the empirical distribution function to the true distribution function. Z. Wahrsch. Verw. Gebiete, 45(1):73–88, 1978.