Microeconometrics with Partial Identification

Abstract

This chapter reviews the microeconometrics literature on partial identification, focusing on the developments of the last thirty years. The topics presented illustrate that the available data combined with credible maintained assumptions may yield much information about a parameter of interest, even if they do not reveal it exactly. Special attention is devoted to discussing the challenges associated with, and some of the solutions put forward to, (1) obtain a tractable characterization of the values for the parameters of interest which are observationally equivalent, given the available data and maintained assumptions; (2) estimate this set of values; (3) conduct test of hypotheses and make confidence statements. The chapter reviews advances in partial identification analysis both as applied to learning (functionals of) probability distributions that are well-defined in the absence of models, as well as to learning parameters that are well-defined only in the context of particular models. A simple organizing principle is highlighted: the source of the identification problem can often be traced to a collection of random variables that are consistent with the available data and maintained assumptions. This collection may be part of the observed data or be a model implication. In either case, it can be formalized as a random set. Random set theory is then used as a mathematical framework to unify a number of special results and produce a general methodology to carry out partial identification analysis.

1 Introduction

1.1 Why Partial Identification?

Knowing the population distribution that data are drawn from, what can one learn about a parameter of interest? It has long been understood that assumptions about the data generating process (DGP) play a crucial role in answering this identification question at the core of all empirical research. Inevitably, assumptions brought to bear enjoy a varying degree of credibility. Some are rooted in economic theory (e.g., optimizing behavior) or in information available to the researcher on the DGP (e.g., randomization mechanisms). These assumptions can be argued to be highly credible. Others are driven by concerns for tractability and the desire to answer the identification question with a certain level of precision (e.g., functional form and distributional assumptions). These are arguably less credible.

Early on, Koopmans and Reiersol (1950) highlighted the importance of imposing restrictions based on prior knowledge of the phenomenon under analysis and some criteria of simplicity, but not for the purpose of identifiability of a parameter that the researcher happens to be interested in, stating (p. 169): “One might regard problems of identifiability as a necessary part of the specification problem. We would consider such a classification acceptable, provided the temptation to specify models in such a way as to produce identifiability of relevant characteristics is resisted.”

Much work, spanning multiple fields, has been devoted to putting forward strategies to carry out empirical research while relaxing distributional, functional form, or behavioral assumptions. One example, embodied in the research program on semiparameteric and nonparametric methods, is to characterize sufficient sets of assumptions, that exclude many suspect ones –sometimes as many as possible– to guarantee that point identification of specific economically interesting parameters attains. This literature is reviewed in, e.g., Matzkin (2007, 2013), and is not discussed here.

Another example, embodied in the research program on Bayesian model uncertainty, is to specify multiple models (i.e., multiple sets of assumptions), put a prior on the parameters of each model and on each model, embed the various separate models within one large hierarchical mixture model, and obtain model posterior probabilities which can be used for a variety of inferences and decisions. This literature is reviewed in, e.g., Wasserman (2000) and Clyde and George (2004), and is not discussed here.

The approach considered here fixes a set of assumptions and a parameter of interest a priori, in the spirit of Koopmans and Reiersol (1950), and asks what can be learned about that parameter given the available data, recognizing that even partial information can be illuminating for empirical research, while enjoying wider credibility thanks to the weaker assumptions imposed. The bounding methods at the core of this approach appeared in the literature nearly a century ago. Arguably, the first exemplar that leverages economic reasoning is given by the work of Marschak and Andrews (1944). They provided bounds on Cobb-Douglas production functions in models of supply and demand, building on optimization principles and restrictions from microeconomic theory. Leamer (1981) revisited their analysis to obtain bounds on the elasticities of demand and supply in a linear simultaneous equations system with uncorrelated errors. The first exemplars that do not rely on specific economic models appear in Gini (1921), Frisch (1934), and Reiersol (1941), who bounded the coefficient of a simple linear regression in the presence of measurement error. These results were extended to the general linear regression model with errors in all variables by Klepper and Leamer (1984) and Leamer (1987).

This chapter surveys some of the methods proposed over the last thirty years in the microeconometrics literature to further this approach. These methods belong to the systematic program on partial identification analysis started with Manski (1989, 1990, 1995, 2003, 2007a, 2013b) and developed by several authors since the early 1990s. Within this program, the focus shifts from points to sets: the researcher aims to learn what is the set of values for the parameters of interest that can generate the same distribution of observables as the one in the data, for some DGP consistent with the maintained assumptions. In other words, the focus is on the set of observationally equivalent values, which henceforth I refer to as the parameters’ sharp identification region. In the partial identification paradigm, empirical analysis begins with characterizing this set using the data alone. This is a nonparametric approach that dispenses with all assumptions, except basic restrictions on the sampling process such that the distribution of the observable variables can be learned as data accumulate. In subsequent steps, one incorporates additional assumptions into the analysis, reporting how each assumption (or set of assumptions) affects what one can learn about the parameters of interest, i.e., how it modifies and possibly shrinks the sharp identification region. Point identification may result from the process of increasingly strengthening the maintained assumptions, but it is not the goal in itself. Rather, the objective is to make transparent the relative role played by the data and the assumptions in shaping the inference that one draws.

There are several strands of independent, but thematically related literatures that are not discussed in this chapter. As a consequence, many relevant contributions are left out of the presentation and the references. One example is the literature in finance. Hansen and Jagannathan (1991) developed nonparametric bounds for the admissible set for means and standard deviations of intertemporal marginal rates of substitution (IMRS) of consumers. The bounds were developed exploiting the condition, satisfied in many finance models, that the equilibrium price of any traded security equals the expectation (conditioned on current information) of the product’s future payoff and the IMRS of any consumer.111 Hansen and Jagannathan (1991) deduce a duality relation with the mean variance theory of Markowitz (1952) and Fama (1996), but the relation does not apply to the sharp bounds they derive. In the Arbitrage Pricing Model (Ross, 1976), bounds on extensions of existing pricing functions, consistent with the absence of arbitrage opportunities, were considered by Harrison and Kreps (1979) and Kreps (1981). Luttmer (1996) extended the analysis to economies with frictions. Hansen, Heaton, and Luttmer (1995) developed econometric tools to estimate the regions, to assess asset pricing models, and to provide nonparametric characterizations of asset pricing anomalies. Earlier on, the existence of volatility bounds on IMRSs were noted by Shiller (1982) and Hansen (1982a). The bounding arguments that build on the minimum-volatility frontier for stochastic discount factors proposed by Hansen and Jagannathan (1991) have become a litmus test to detect anomalies in asset pricing models (see, e.g. Shiller, 2003, p. 89). I refer to the textbook presentations in (Ljungqvist and Sargent, 2004, Chapter 13) and (Cochrane, 2005, Chapters 5 and 21), and the review articles by Ferson (2003) and Campbell (2014), for a careful presentation of this literature.

In macroeconomics, Faust (1998), Canova and De Nicolo (2002), and Uhlig (2005) proposed bounds for impulse response functions in sign-restricted structural vector autoregression models, and carried out Bayesian inference with a non-informative prior for the non-identified parameters. I refer to (Kilian and Lütkepohl, 2017, Chapter 13) for a careful presentation of this literature.

In microeconomic theory, bounds were derived from inequalities resulting as necessary and sufficient conditions that data on an individual’s choice need to satisfy in order to be consistent with optimizing behavior, as in the research pioneered by Samuelson (1938) and advanced early on by Houthakker (1950) and Richter (1966). Afriat (1967) and Varian (1982) extended this research program to revealed preference extrapolation. Notably, in this work no stochastic terms enter the analysis. Block and Marschak (1960), Marschak (1960), Hall (1973), McFadden (1975), Falmagne (1978), and McFadden and Richter (1991), extended revealed preference arguments to random utility models, and obtained bounds on the distributions of preferences. I refer to the survey articles by Crawford and De Rock (2014) and (Blundell, 2019, Chapter XXX in this Volume) for a careful presentation of this literature.

A complementary approach to partial identification is given by sensitivity analysis, advocated for in different ways by, e.g., Gilstein and Leamer (1983), Rosenbaum and Rubin (1983), Leamer (1985), Rosenbaum (1995), Imbens (2003), and others. Within this approach, the analysis begins with a fully parametric model that point identifies the parameter of interest. One then reports the set of values for this parameter that result when the more suspicious assumptions are relaxed.

Related literatures, not discussed in this chapter, abound also outside Economics. For example, in probability theory, Hoeffding (1940) and Fréchet (1951) put forward bounds on the joint distributions of random variables, and Makarov (1981), Rüschendorf (1982), and Frank, Nelsen, and Schweizer (1987) on the sum of random variables, when only marginal distributions are observed. The literature on probability bounds is discussed in the textbook by (Shorack and Wellner, 2009, Appendix A). Addressing problems faced in economics, sociology, epidemiology, geography, history, political science, and more, Duncan and Davis (1953) derived bounds on correlations among variables measured at the individual level based on observable correlations among variables measured at the aggregate level. The so called ecological inference problem they studied, and the associated literature, is discussed in the survey article by Cho and Manski (2009) and references therein.

1.2 Goals and Structure of this Chapter

To carry out econometric analysis with partial identification, one needs: (1) computationally feasible characterizations of the parameters’ sharp identification region; (2) methods to estimate this region; and (3) methods to test hypotheses and construct confidence sets. The goal of this chapter is to provide insights into the challenges posed by each of these desiderata, and into some of their solutions. In order to discuss the partial identification literature in microeconometrics with some level of detail while keeping this chapter to a manageable length, I focus on a selection of papers and not on a complete survey of the literature. As a consequence, many relevant contributions are left out of the presentation and the references. I also do not discuss the important but separate topic of statistical decisions in the presence of partial identification, for which I refer to the textbook treatments in Manski (2005, 2007a) and to the review by (Hirano and Porter, 2019, Chapter XXX in this Volume).

The presumption in identification analysis that the distribution from which the data are drawn is known allows one to keep separate the identification question from the distinct question of statistical inference from a finite sample. I use the same separation in this chapter. I assume solid knowledge of the topics covered in first year Economics PhD courses in econometrics and microeconomic theory.

I begin in Section 2 with the analysis of what can be learned about features of probability distributions that are well defined in the absence of an economic model, such as moments, quantiles, cumulative distribution functions, etc., when one faces measurement problems. Specifically, I focus on cases where the data is incomplete, either due to selectively observed data or to interval measurements. I refer to Manski (1995, 2003, 2007a) for textbook treatments of many other cases. I lay out formally the maintained assumptions for several examples, and then discuss in detail what is the source of the identification problem. I conclude with providing tractable characterizations of what can be learned about the parameters of interest, with formal proofs. I show that even in simple problems, great care may be needed to obtain the sharp identification region. It is often easier to characterize an outer region, i.e., a collection of values for the parameter of interest that contains the sharp one but may contain also additional values. Outer regions are useful because of their simplicity and because in certain applications they may suffice to answer questions of great interest, e.g., whether a policy intervention has a nonnegative effect. However, compared to the sharp identification region they may afford the researcher less useful predictions, and a lower ability to test for misspecification, because they do not harness all the information in the observed data and maintained assumptions.

In Section 3 I use the same approach to study what can be learned about features of parameters of structural econometric models when the model is incomplete (Tamer, 2003; Haile and Tamer, 2003; Ciliberto and Tamer, 2009). Specifically, I discuss single agent discrete choice models under a variety of challenging situations (interval measured as well as endogenous explanatory variables; unobserved as well as counterfactual choice sets); finite discrete games with multiple equilibria; auction models under weak assumptions on bidding behavior; and network formation models. Again I formally derive sharp identification regions for several examples.

I conclude each of these sections with a brief discussion of further theoretical advances and empirical applications that is meant to give a sense of the breadth of the approach, but not to be exhaustive. I refer to the recent survey by Ho and Rosen (2017) for a thorough discussion of empirical applications of partial identification methods.

In Section 4 I discuss finite sample inference. I limit myself to highlighting the challenges that one faces for consistent estimation when the identified object is a set, and several coverage notions and requirements that have been proposed over the last 20 years. I refer to the recent survey by Canay and Shaikh (2017) for a thorough discussion of methods to tests hypotheses and build confidence sets in moment inequality models.

In Section 5 I discuss the distinction between refutable and non-refutable assumptions, and how model misspecification may be detectable in the presence of the former, even within the partial identification paradigm. I then highlight certain challenges that model misspecification presents for the interpretation of sharp identification (as well as outer) regions, and for the construction of confidence sets.

In Section 6 I highlight that while most of the sharp identification regions characterized in Section 2 can be easily computed, many of the ones in Section 3 are more challenging. This is because the latter are obtained as level sets of criterion functions in moderately dimensional spaces, and tracing out these level sets or their boundaries is a non-trivial computational problem. In Section 7 I conclude providing some considerations on what I view as open questions for future research.

1.3 Random Set Theory as a Tool for Partial Identification Analysis

Throughout Sections 2 and 3, a simple organizing principle for much of partial identification analysis emerges. The cause of the identification problems discussed can be traced back to a collection of random variables that are consistent with the available data and maintained assumptions. For the problems studied in Section 2, this set is often a simple function of the observed variables. The incompleteness of the data stems from the fact that instead of observing the singleton variables of interest, one observes set-valued variables to which these belong, but one has no information on their exact value within the sets. For the problems studied in Section 3, the collection of random variables consistent with the maintained assumptions comprises what the model predicts for the endogenous variable(s). The incompleteness of the model stems from the fact that instead of making a singleton prediction for the variable(s) of interest, the model makes multiple predictions but does not specify how one is chosen.

The central role of set-valued objects, both stochastic and nonstochastic, in partial identification renders random set theory a natural toolkit to aid the analysis.222The first idea of a general random set in the form of a region that depends on chance appears in Kolmogorov (1950), originally published in 1933. For another early example where confidence regions are explicitly described as random sets, see (Haavelmo, 1944, p. 67). The role of random sets in this chapter is different. This theory originates in the seminal contributions of Choquet (1953/54), Aumann (1965), and Debreu (1967), with the first self contained treatment of the theory given by Matheron (1975). I refer to Molchanov (2017) for a textbook presentation, and to Molchanov and Molinari (2014, 2018) for a treatment focusing on its applications in econometrics.

Beresteanu and Molinari (2008) introduce the use of random set theory in econometrics to carry out identification analysis and statistical inference with incomplete data. Beresteanu, Molchanov, and Molinari (2011, 2012) propose it to characterize sharp identification regions both with incomplete data and with incomplete models. Galichon and Henry (2011) propose the use of optimal transportation methods that in some applications deliver the same characterizations as the random set methods. I do not discuss optimal transportation methods in this chapter, but refer to Galichon (2016) for a thorough treatment.

Over the last ten years, random set methods have been used to unify a number of specific results in partial identification, and to produce a general methodology for identification analysis that dispenses completely with case-by-case distinctions. In particular, as I show throughout the chapter, the methods allow for simple and tractable characterizations of sharp identification regions. The collection of these results establishes that indeed this is a useful tool to carry out econometrics with partial identification, as exemplified by its prominent role both in this chapter and in Chapter XXX in this Volume by Chesher and Rosen (2019), which focuses on general classes of instrumental variable models. The random sets approach complements the more traditional one, based on mathematical tools for (single valued) random vectors, that proved extremely productive since the beginning of the research program in partial identification.

This chapter shows that to fruitfully apply random set theory for identification and inference, the econometrician needs to carry out three fundamental steps. First, she needs to define the random closed set that is relevant for the problem under consideration using all information given by the available data and maintained assumptions. This is a delicate task, but one that is typically carried out in identification analysis regardless of whether random set theory is applied. Indeed, throughout the chapter I highlight how relevant random closed sets were characterized in partial identification analysis since the early 1990s, albeit the connection to the theory of random sets was not made. As a second step, the econometrician needs to determine how the observable random variables relate to the random closed set. Often, one of two cases occurs: either the observable variables determine a random set to which the unobservable variable of interest belongs with probability one, as in incomplete data scenarios; or the (expectation of the) (un)observable variable belongs to (the expectation of) a random set determined by the model, as in incomplete model scenarios. Finally, the econometrician needs to determine which tool from random set theory should be utilized. To date, new applications of random set theory to econometrics have fruitfully exploited (Aumann) expectations and their support functions, (Choquet) capacity functionals, and laws of large numbers and central limit theorems for random sets. Appendix A reports basic definitions from random set theory of these concepts, as well as some useful theorems. The chapter explains in detail through applications to important identification problems how these steps can be carried out.

| Nonatomic probability space | |

| Euclidean space equipped with the Euclidean norm | |

| Collection of closed, open, and compact subsets of (respectively) | |

| Unit sphere in | |

| Unit ball in | |

| Convex hull and closure of a set (respectively), and cardinality of a finite set | |

| Random vectors | |

| Realizations of random vectors or deterministic vectors | |

| Random sets | |

| Realizations of random sets or deterministic sets | |

| Unobserved random variables (heterogeneity) | |

| Parameter space, data generating value for the parameter vector, and a generic element of | |

| Joint distribution of all variables (observable and unobservable) | |

| Joint distribution of the observable variables | |

| Joint distribution whose features one wants to learn | |

| A joint distribution of observed variables implied by the model | |

| Quantile function at level for a random variable distributed | |

| Expectation operator associated with distribution | |

| Capacity functional of random set | |

| Containment functional of random set | |

| Convergence in probability, convergence almost surely, and weak convergence (respectively) | |

| and have the same distribution | |

| Statistical independence between random variables and | |

| Inner product between vectors and , | |

| Family of utility functions and one of its elements | |

| Criterion function that aggregates violations of the population moment inequalities | |

| Criterion function that aggregates violations of the sample moment inequalities | |

| Sharp identification region of the functional in square brackets (a function of ) | |

| An outer region of the functional in square brackets (a function of ) |

1.4 Notation

This chapter employs consistent notation that is summarized in Table 1.1. Some important conventions are as follows: denotes outcome variables, denote explanatory variables, and denotes instrumental variables (i.e., variables that satisfy some form of independence with the outcome or with the unobservable variables, possibly conditional on ).

I denote by the joint distribution of all observable variables. Identification analysis is carried out using the information contained in this distribution, and finite sample inference is carried out under the presumption that one draws a random sample of size from . I denote by the joint distribution whose features the researcher wants to learn. If were identified given the observed data (e.g., if it were a marginal of ), point identification of the parameter or functional of interest would attain. I denote by the joint distribution of all variables, observable and unobservable ones; both and can be obtained from it. In the context of structural models, I denote by a distribution for the observable variables that is consistent with the model. I note that model incompleteness typically implies that is not unique. I let denote the sharp identification region of the functional in square brackets, and an outer region. In both cases, the regions are indexed by , because they depend on the distribution of the observed data.

2 Partial Identification of Probability Distributions

The literature reviewed in this chapter starts with the analysis of what can be learned about functionals of probability distributions that are well-defined in the absence of a model. The approach is nonparametric, and it is typically constructive, in the sense that it leads to “plug-in” formulae for the bounds on the functionals of interest.

2.1 Selectively Observed Data

As in Manski (1989), suppose that a researcher is interested in learning the probability that an individual who is homeless at a given date has a home six months later. Here the population of interest is the people who are homeless at the initial date, and the outcome of interest is an indicator of whether the individual has a home six months later (so that ) or remains homeless (so that ). A random sample of homeless individuals is interviewed at the initial date, so that individual background attributes are observed, but six months later only a subset of the individuals originally sampled can be located. In other words, attrition from the sample creates a selection problem whereby is observed only for a subset of the population. Let be an indicator of whether the individual can be located (hence ) or not (hence ). The question is what can the researcher learn about , with the distribution of ? Manski (1989) showed that is not point identified in the absence of additional assumptions, but informative nonparametric bounds on this quantity can be obtained. In this section I review his approach, and discuss several important extensions of his original idea.

Throughout the chapter, I formally state the structure of the problem under study as an “Identification Problem”, and then provide a solution, either in the form of a sharp identification region, or of an outer region. To set the stage, and at the cost of some repetition, I do the same here, slightly generalizing the question stated in the previous paragraph.

Identification Problem 2.1 (Conditional Expectation of Selectively Observed Data):

Let and be, respectively, an outcome variable and a vector of covariates with support and respectively, with a compact set. Let . Suppose that the researcher observes a random sample of realizations of and, in addition, observes the realization of when . Hence, the observed data is . Let be a measurable function that attains its lower and upper bounds and , and assume that . Let be such that , .333The bounds and the values at which they are attained may differ for different functions . In the absence of additional information, what can the researcher learn about , with the distribution of ?

Manski’s analysis of this problem begins with a simple application of the law of total probability, that yields

| (2.1) |

Equation (2.1) lends a simple but powerful anatomy of the selection problem. While and can be learned from the observable distribution , under the maintained assumptions the sampling process reveals nothing about . Hence, is not point identified.

If one were to assume exogenous selection (or data missing at random conditional on ), i.e., , point identification would obtain. However, that assumption is non-refutable and it is well known that it may fail in applications.444Section 5 discusses the consequences of model misspecification (with respect to refutable assumptions). Let denote the space of all probability measures with support in . The unknown functional vector is . What the researcher can learn, in the absence of additional restrictions on , is the region of observationally equivalent distributions for , and the associated set of expectations taken with respect to these distributions.

Theorem SIR-2.1 (Conditional Expectations of Selectively Observed Data):

Proof.

Due to the discussion following equation (2.1), the collection of observationally equivalent distribution functions for is

| (2.3) |

Next, observe that the lower bound in equation (2.2) is achieved by integrating against the distribution that results when places probability one on . The upper bound is achieved by integrating against the distribution that results when places probability one on . Both are contained in the set in equation (2.3). ∎

These are the worst case bounds, so called because assumptions free and therefore representing the widest possible range of values for the parameter of interest that are consistent with the observed data. A simple “plug-in” estimator for replaces all unknown quantities in (2.2) with consistent estimators, obtained, e.g., by kernel or sieve regression. I return to consistent estimation of partially identified parameters in Section 4. Here I emphasize that identification problems are fundamentally distinct from finite sample inference problems. The latter are typically reduced as sample size increase (because, e.g., the variance of the estimator becomes smaller). The former do not improve, unless a different and better type of data is collected, e.g. with a smaller prevalence of missing data (see Dominitz and Manski, 2017, for a discussion).

(Manski, 2003, Section 1.3) shows that the proof of Theorem SIR-2.1 can be extended to obtain the smallest and largest points in the sharp identification region of any parameter that respects stochastic dominance.555 Recall that a probability distribution stochastically dominates if for all . A real-valued functional respects stochastic dominance if whenever stochastically dominates . This is especially useful to bound the quantiles of . For any given , let . Then the smallest and largest admissible values for the -quantile of are, respectively,

The lower bound on is informative only if , and the upper bound is informative only if . By comparison, for any value of , and are generically informative if, respectively, and , regardless of the range of .

Stoye (2010) further extends partial identification analysis to the study of spread parameters in the presence of missing data (as well as interval data, data combinations, and other applications). These parameters include ones that respect second order stochastic dominance, such as the variance, the Gini coefficient, and other inequality measures, as well as other measures of dispersion which do not respect second order stochastic dominance, such as interquartile range and ratio.666 Earlier related work includes, e.g., Gastwirth (1972) and Cowell (1991), who obtain worst case bounds on the sample Gini coefficient under the assumption that one knows the income bracket but not the exact income of every household. Stoye shows that the sharp identification region for these parameters can be obtained by fixing the mean or quantile of the variable of interest at a specific value within its sharp identification region, and deriving a distribution consistent with this value which is “compressed” with respect to the ones which bound the cumulative distribution function (CDF) of the variable of interest, and one which is “dispersed” with respect to them. Heuristically, the compressed distribution minimizes spread, while the dispersed one maximizes it (the sense in which this optimization occurs is formally defined in the paper). The intuition for this is that a compressed CDF is first below and then above any non-compressed one; a dispersed CDF is first above and then below any non-dispersed one. Second-stage optimization over the possible values of the mean or the quantile delivers unconstrained bounds. The main results of the paper are sharp identification regions for the expectation and variance, for the median and interquartile ratio, and for many other combinations of parameters.

Key Insight 2.1 (Identification is not a binary event):

Identification Problem 2.1 is mathematically simple, but it puts forward a new approach to empirical research. The traditional approach aims at finding a sufficient (possibly minimal) set of assumptions guaranteeing point identification of parameters, viewing identification as an “all or nothing” notion, where either the functional of interest can be learned exactly or nothing of value can be learned. The partial identification approach pioneered by Manski (1989) points out that much can be learned from combination of data and assumptions that restrict the functionals of interest to a set of observationally equivalent values, even if this set is not a singleton. Along the way, Manski (1989) points out that in Identification Problem 2.1 the observed outcome is the singleton when , and the set when . This is a random closed set, see Definition A.1. I return to this connection in Section 2.3.

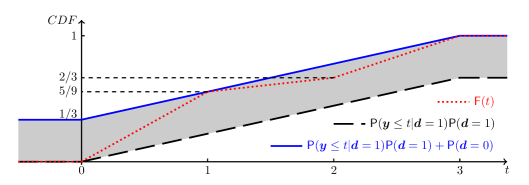

Despite how transparent the framework in Identification Problem 2.1 is, important subtleties arise even in this seemingly simple context. For a given , consider the function , with the indicator function taking the value one if the logical condition in parentheses holds and zero otherwise. Then equation (2.2) yields pointwise-sharp bounds on the CDF of at any fixed :

| (2.4) |

Yet, the collection of CDFs that belong to the band defined by (2.4) is not the sharp identification region for the CDF of . Rather, it constitutes an outer region, as originally pointed out by (Manski, 1994, p. 149 and note 2).

Theorem OR-2.1 (Cumulative Distribution Function of Selectively Observed Data):

Let denote the collection of cumulative distribution functions on . Then, under the assumptions in Identification Problem 2.1,

| (2.5) |

is an outer region for the CDF of .

Proof.

Any admissible CDF for belongs to the family of functions in equation (2.5). However, the bound in equation (2.5) does not impose the restriction that for any ,

| (2.6) |

This restriction is implied by the maintained assumptions, but is not necessarily satisfied by all CDFs in , as illustrated in the following simple example. ∎

Example 2.1.

Omit for simplicity, let , and let

The bounding functions and associated tube from the inequalities in (2.4) are depicted in Figure 2.1. Consider the cumulative distribution function

| (2.12) |

For each , lies in the tube defined by equation (2.4). However, it cannot be the CDF of , because , directly contradicting equation (2.6).

How can one characterize the sharp identification region for the CDF of under the assumptions in Identification Problem 2.1? In general, there is not a single answer to this question: different methodologies can be used. Here I use results in (Manski, 2003, Corollary 1.3.1) and (Molchanov and Molinari, 2018, Theorem 2.25), which yield an alternative characterization of that translates directly into a characterization of .777Whereas Manski (1994) is very clear that the collection of CDFs in (2.4) is an outer region for the CDF of , and Manski (2003) provides the sharp characterization in (2.13), (Manski, 2007a, p. 39) does not state all the requirements that characterize .

Theorem SIR-2.2 (Conditional Distribution and CDF of Selectively Observed Data):

Given , let denote the probability that distribution assigns to set conditional on , with . Under the assumptions in Identification Problem 2.1,

| (2.13) |

where is measurable. If is countable,

| (2.14) |

If is a bounded interval,

| (2.15) |

Proof.

The characterization in (2.13) follows from equation (2.3), observing that if as defined in equation (2.3), then there exists a distribution such that . Hence, by construction , . Conversely, if one has , , one can define . The resulting is a probability measure, and hence as defined in equation (2.3). When is countable, if it follows that for any ,

| (2.16) |

The result in equation (2.15) is proven in (Molchanov and Molinari, 2018, Theorem 2.25) using elements of random set theory, to which I return in Section 2.3. Using elements of random set theory it is also possible to show that the characterization in (2.13) requires only to check the inequalities for the compact subsets of . ∎

This section provides sharp identification regions and outer regions for a variety of functionals of interest. The computational complexity of these characterizations varies widely. Sharp bounds on parameters that respect stochastic dominance only require computing the parameters with respect to two probability distributions. An outer region on the CDF can be obtained by evaluating all tail probabilities of a certain distribution. A sharp identification region on the CDF requires evaluating the probability that a certain distribution assigns to all intervals. I return to computational challenges in partial identification in Section 6.

2.2 Treatment Effects with and without Instrumental Variables

The discussion of partial identification of probability distributions of selectively observed data naturally leads to the question of its implications for program evaluation. The literature on program evaluation is vast. The purpose of this section is exclusively to show how the ideas presented in Section 2.1 can be applied to learn features of treatment effects of interest, when no assumptions are imposed on treatment selection and outcomes. I also provide examples of assumptions that can be used to tighten the bounds. To keep this chapter to a manageable length, I discuss only partial identification of the average response to a treatment and of the average treatment effect (ATE). There are many different parameters that received much interest in the literature. Examples include the local average treatment effect of Imbens and Angrist (1994) and the marginal treatment effect of Heckman and Vytlacil (1999, 2001, 2005). For thorough discussions of the literature on program evaluation, I refer to the textbook treatments in Manski (1995, 2003, 2007a) and Imbens and Rubin (2015), to the Handbook chapters by Heckman and Vytlacil (2007a, b) and Abbring and Heckman (2007), and to the review articles by Imbens and Wooldridge (2009) and Mogstad and Torgovitsky (2018).

Using standard notation (e.g., Neyman, 1923), let be an individual-specific response function, with a finite set of mutually exclusive and exhaustive treatments, and let denote the individual’s received treatment (taking its realizations in ).888Here the treatment response is a function only of the (scalar) treatment received by the given individual, an assumption known as stable unit treatment value assumption (Rubin, 1978). The researcher observes data , with the outcome corresponding to the received treatment , and a vector of covariates. The outcome for is counterfactual, and hence can be conceptualized as missing. Therefore, we are in the framework of Identification Problem 2.1 and all the results from Section 2.1 apply in this context too, subject to adjustments in notation.999Beresteanu, Molchanov, and Molinari (2012) and (Molchanov and Molinari, 2018, Section 2.5) provide a characterization of the sharp identification region for the joint distribution of . For example, using Theorem SIR-2.1,

| (2.17) |

where , . If and/or , these worst case bounds are informative. When both are infinite, the data is uninformative in the absence of additional restrictions.

If the researcher is interested in an Average Treatment Effect (ATE), e.g.

with , sharp worst case bounds on this quantity can be obtained as follows. First, observe that the empirical evidence reveals and , but is uninformative about , . Each of the latter quantities (the expectations of and conditional on different realizations of and ) can take any value in . Hence, the sharp lower bound on the ATE is obtained by subtracting the upper bound on from the lower bound on . The sharp upper bound on the ATE is obtained by subtracting the lower bound on from the upper bound on . The resulting bounds have width equal to , and hence are informative only if both and . As the largest logically possible value for the ATE (in the absence of information from data) cannot be larger than , and the smallest cannot be smaller than , the sharp bounds on the ATE always cover zero.

Key Insight 2.2:

How should one think about the finding on the size of the worst case bounds on the ATE? On the one hand, if both and the bounds are informative, because they are a strict subset of the ATE’s possible realizations. On the other hand, they reveal that the data alone are silent on the sign of the ATE. This means that assumptions play a crucial role in delivering stronger conclusions about this policy relevant parameter. The partial identification approach to empirical research recommends that as assumptions are added to the analysis, one systematically reports how each contributes to shrinking the bounds, making transparent their role in shaping inference.

What assumptions may researchers bring to bear to learn more about treatment effects of interest? The literature has provided a wide array of well motivated and useful restrictions. Here I consider two examples. The first one entails shape restrictions on the treatment response function, leaving selection unrestricted. Manski (1997b) obtains bounds on treatment effects under the assumption that the response functions are monotone, semi-monotone, or concave-monotone. These restrictions are motivated by economic theory, where it is commonly presumed, e.g., that demand functions are downward sloping and supply functions are upward sloping. Let the set be ordered in terms of degree of intensity. Then Manski’s monotone treatment response assumption requires that

Under this assumption, one has a sharp characterization of what can be learned about :

| (2.18) |

Hence, the sharp bounds on are (Manski, 1997b, Proposition M1)

| (2.19) |

This finding highlights some important facts. Under the monotone treatment response assumption, the bounds on are obtained using information from all pairs (given ), while the bounds in (2.17) only use the information provided by pairs for which (given ). As a consequence, the bounds in (2.19) are informative even if , whereas the worst case bounds are not.

Concerning the ATE with , under monotone treatment response its lower bound is zero, and its upper bound is obtained by subtracting the lower bound on from the upper bound on , where both bounds are obtained as in (2.19) (Manski, 1997b, Proposition M2).

The second example of assumptions used to tighten worst case bounds is that of exclusion restrictions, as in, e.g., Manski (1990). Suppose the researcher observes a random variable , taking its realizations in , such that101010Stronger exclusion restrictions include statistical independence of the response function at each with : -a.s.; and statistical independence of the entire response function with : -a.s. Examples of partial identification analysis under these conditions can be found in Balke and Pearl (1997), Manski (2003), Kitagawa (2009), Beresteanu, Molchanov, and Molinari (2012), Machado, Shaikh, and Vytlacil (2018), and many others.

| (2.20) |

This assumption is treatment-specific, and requires that the treatment response to is mean independent with . It is easy to show that under the assumption in (2.20), the bounds on become

| (2.21) |

These are called intersection bounds because they are obtained as follows. Given and , one uses (2.17) to obtain sharp bounds on . Due to the mean independence assumption in (2.20), must belong to each of these bounds -a.s., hence to their intersection. The expression in (2.21) follows. If the instrument affects the probability of being selected into treatment, or the average outcome for the subpopulation receiving treatment , the bounds on shrink. If the bounds are empty, the mean independence assumption can be refuted (see Section 5 for a discussion of misspecification in partial identification). Manski and Pepper (2000, 2009) generalize the notion of instrumental variable to monotone instrumental variable, and show how these can be used to obtain tighter bounds on treatment effect parameters.111111See (Chesher and Rosen, 2019, Chapter XXX in this Volume) for further discussion. They also show how shape restrictions and exclusion restrictions can jointly further tighten the bounds. Manski (2013a) generalizes these findings to the case where treatment response may have social interactions – that is, each individual’s outcome depends on the treatment received by all other individuals.

2.3 Interval Data

Identification Problem 2.1, as well as the treatment evaluation problem in Section 2.2, is an instance of the more general question of what can be learned about (functionals of) probability distributions of interest, in the presence of interval valued outcome and/or covariate data. Such data have become commonplace in Economics. For example, since the early 1990s the Health and Retirement Study collects income data from survey respondents in the form of brackets, with degenerate (singleton) intervals for individuals who opt to fully reveal their income (see, e.g., Juster and Suzman, 1995). Due to concerns for privacy, public use tax data are recorded as the number of tax payers which belong to each of a finite number of cells (see, e.g., Picketty, 2005). The Occupational Employment Statistics (OES) program at the Bureau of Labor Statistics (Bureau of Labor Statistics, 2018) collects wage data from employers as intervals, and uses these data to construct estimates for wage and salary workers in more than 800 detailed occupations. Manski and Molinari (2010) and Giustinelli, Manski, and Molinari (2019b) document the extensive prevalence of rounding in survey responses to probabilistic expectation questions, and propose to use a person’s response pattern across different questions to infer his rounding practice, the result being interpretation of reported numerical values as interval data. Other instances abound. Here I focus first on the case of interval outcome data.

Identification Problem 2.2 (Interval Outcome Data):

Assume that in addition to being compact, either is countable or , with and . Let be observable random variables and be an unobservable random variable whose distribution (or features thereof) is of interest, with . Suppose that are such that .121212In Identification Problem 2.1 the observable variables are , and are determined as follows: , . For the analysis in Section 2.2, the data is and , . Hence, by construction. In the absence of additional information, what can the researcher learn about features of , the conditional distribution of given ?

It is immediate to obtain the sharp identification region

As in the previous section, it is also easy to obtain sharp bounds on parameters that respect stochastic dominance, and pointwise-sharp bounds on the CDF of at any fixed :

| (2.22) |

In this case too, however, as in Theorem OR-2.1, the tube of CDFs satisfying equation (2.22) for all is an outer region for the CDF of , rather than its sharp identification region. Indeed, also in this context it is easy to construct examples similar to Example 2.1.

How can one characterize the sharp identification region for the probability distribution of when one observes and assumes ? Again, there is not a single answer to this question. Depending on the specific problem at hand, e.g., the specifics of the interval data and whether is assumed discrete or continuous, different methods can be applied. I use random set theory to provide a characterization of . Let

Then is a random closed set according to Definition A.1.131313For a proof of this statement, see (Molchanov and Molinari, 2018, Example 1.11). The requirement can be equivalently expressed as

| (2.23) |

Equation (2.23), together with knowledge of , exhausts all the information in the data and maintained assumptions. In order to harness such information to characterize the set of observationally equivalent probability distributions for , one can leverage a result due to Artstein (1983) (and Norberg, 1992), reported in Theorem A.1 in Appendix A, which allows one to translate (2.23) into a collection of conditional moment inequalities. Specifically, let denote the space of all probability measures with support in .

Theorem SIR-2.3 (Conditional Distribution of Interval-Observed Outcome Data):

Proof.

Compare equation (2.24) with equation (2.13). Under the set-up of Identification Problem 2.1, when we have and when we have . Hence, for any , .141414For , both (2.24) and (2.13) hold trivially. It follows that the characterizations in (2.24) and (2.13) are equivalent. If is countable, it is easy to show that (2.24) simplifies to (2.13) (see, e.g., Beresteanu, Molchanov, and Molinari, 2012, Proposition 2.2).

Key Insight 2.3 (Random set theory and partial identification):

The mathematical framework for the analysis of random closed sets embodied in random set theory is naturally suited to conduct identification analysis and statistical inference in partially identified models. This is because, as argued by Beresteanu and Molinari (2008) and Beresteanu, Molchanov, and Molinari (2011, 2012), lack of point identification can often be traced back to a collection of random variables that are consistent with the available data and maintained assumptions. In turn, this collection of random variables is equal to the family of selections of a properly specified random closed set, so that random set theory applies. The interval data case is a simple example that illustrates this point. More examples are given throughout this chapter. As mentioned in the Introduction, the exercise of defining the random closed set that is relevant for the problem under consideration is routinely carried out in partial identification analysis, even when random set theory is not applied. For example, in the case of treatment effect analysis with monotone response function, Manski (1997b) derived the set in the right-hand-side of (2.18), which satisfies Definition (A.1).

An attractive feature of the characterization in (2.24) is that it holds regardless of the specific assumptions on , and . Later sections in this chapter illustrate how Theorem A.1 delivers the sharp identification region in other more complex instances of partial identification of probability distributions, as well as in structural models. In Chapter XXX in this Volume, Chesher and Rosen (2019) apply Theorem A.1 to obtain sharp identification regions for functionals of interest in the important class of generalized instrumental variable models. To avoid repetitions, I do not systematically discuss that class of models in this chapter.

When addressing questions about features of in the presence of interval outcome data, an alternative approach (e.g. Tamer, 2010; Ponomareva and Tamer, 2011) looks at all (random) mixtures of . The approach is based on a random variable (a selection mechanism that picks an element of ) with values in , whose distribution conditional on is left completely unspecified. Using this random variable, one defines

| (2.26) |

The sharp identification region in Theorem SIR-2.3 can be characterized as the collection of conditional distributions of all possible random variables as defined in (2.26), given . This is because each is a (stochastic) convex combination of , hence each of these random variables satisfies . While such characterization is sharp, it can be of difficult implementation in practice, because it requires working with all possible random variables built using all possible random variables with support in . Theorem A.1 allows one to bypass the use of , and obtain directly a characterization of the sharp identification region for based on conditional moment inequalities.151515It can be shown that the collection of random variables equals the collection of measurable selections of the random closed set (see Definition A.3); see (Beresteanu, Molchanov, and Molinari, 2011, Lemma 2.1). Theorem A.1 provides a characterization of the distribution of any that satisfies a.s., based on a dominance condition that relates the distribution of to the distribution of the random set . Such dominance condition is given by the inequalities in (2.24).

Horowitz and Manski (1998, 2000) study nonparametric conditional prediction problems with missing outcome and/or missing covariate data. Their analysis shows that this problem is considerably more pernicious than the case where only outcome data are missing. For the case of interval covariate data, Manski and Tamer (2002) provide a set of sufficient conditions under which simple and elegant sharp bounds on functionals of can be obtained, even in this substantially harder identification problem. Their assumptions are listed in Identification Problem 2.3, and their result (with proof) in Theorem SIR-2.4.

Identification Problem 2.3 (Interval Covariate Data):

Let be observable random variables in and be an unobservable random variable. Suppose that , the joint distribution of , is such that: (I) ; (M) is weakly increasing in ; and (MI) . In the absence of additional information, what can the researcher learn about for given ?

Compared to the earlier discussion for the interval outcome case, here there are two additional assumptions. The monotonicity condition (M) is a simple shape restrictions, which however requires some prior knowledge about the joint distribution of . The mean independence restriction (MI) requires that if were observed, knowledge of would not affect the conditional expectation of . The assumption is not innocuous, as pointed out by the authors. For example, it may fail if censoring is endogenous.161616For the case of missing covariate data, which is a special case of interval covariate data similarly to arguments in footnote 12, Aucejo, Bugni, and Hotz (2017) show that the MI restriction implies the assumption that data is missing at random.

Theorem SIR-2.4 (Conditional Expectation with Interval-Observed Covariate Data):

Under the assumptions of Identification Problem 2.3, the sharp identification region for for given is

| (2.27) |

Proof.

The law of iterated expectations and the independence assumption yield . For all , the monotonicity assumption and the fact that -a.s. yield . Putting this together with the previous result, . Then (using again the monotonicity assumption) for any , so that the lower bound holds. The bound is weakly increasing as a function of , so that the monotonicity assumption on holds and the bound is sharp. The argument for the upper bound can be concluded similarly. ∎

Learning about functionals of naturally implies learning about predictors of . For example, yields the collection of values for the best predictor under square loss; , with the median with respect to distribution , yields the collection of values for the best predictor under absolute loss. And so on. A related but distinct problem is that of parametric conditional prediction. Often researchers specify not only a loss function for the prediction problem, but also a parametric family of predictor functions, and wish to learn the member of this family that minimizes expected loss. To avoid confusion, let me clarify that here I am not referring to a parametric assumption on the best predictor, e.g., that is a linear function of . I return to such assumptions at the end of this section. For now, in the example of linearity and square loss, I am referring to best linear prediction, i.e., best linear approximation to . (Manski, 2003, pp. 56-58) discusses what can be learned about the best linear predictor of conditional on , when only interval data on is available.

I treat first the case of interval outcome and perfectly observed covariates.

Identification Problem 2.4 (Parametric Prediction with Interval Outcome Data):

Maintain the same assumptions as in Identification Problem 2.2. Let be observable random variables and be an unobservable random variable, with . In the absence of additional information, what can the researcher learn about the best linear predictor of given ?

For simplicity suppose that is a scalar, and let denote the parameter vector of the best linear predictor of . Assume that . Combining the definition of best linear predictor with a characterization of the sharp identification region for the joint distribution of , we have that

| (2.28) |

where, using an argument similar to the one in Theorem SIR-2.3,

| (2.29) |

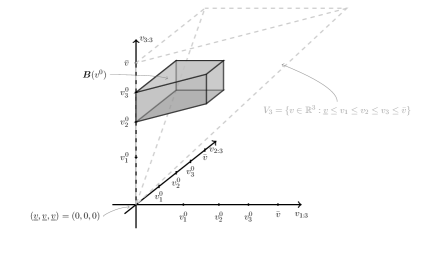

(Beresteanu and Molinari, 2008, Proposition 4.1) show that (2.28) can be re-written in an intuitive way that generalizes the well-known formula for the best linear predictor that arises when is perfectly observed. Define the random segment and the matrix as

| (2.30) |

where is the set of all measurable selections from , see Definition A.3. Then,

Theorem SIR-2.5 (Best Linear Predictor with Interval Outcome Data):

Proof.

In either representation (2.28) or (2.31), is the collection of best linear predictors for each selection of .171717Under our assumption that is a bounded interval, all the selections of are integrable. Beresteanu and Molinari (2008) consider the more general case where is not required to be bounded. Why should one bother with the representation in (2.31)? The reason is that is a convex set, as it can be evinced from representation (2.31): has almost surely convex realizations that are segments and the Aumann expectation of a convex set is convex.181818In in our example, in if is a vector and the predictor includes an intercept. Hence, it can be equivalently represented through its support function , see Definition A.5 and equation (A.2). In particular, in this example,

| (2.32) |

where .191919See (Beresteanu and Molinari, 2008, p. 808) and (Bontemps, Magnac, and Maurin, 2012, p. 1136). The characterization in (2.32) results from Theorem A.2, which yields , and the fact that equals the expression in (2.32). As I discuss in Section 4 below, because the support function fully characterizes the boundary of , (2.32) allows for a simple sample analog estimator, and for inference procedures with desirable properties. It also immediately yields sharp bounds on linear combinations of by judicious choice of .202020For example, in the case that is a scalar, sharp bounds on can be obtained by choosing and , which yield with and . Stoye (2007) and Magnac and Maurin (2008) provide the same characterization as in (2.32) using, respectively, direct optimization and the Frisch-Waugh-Lovell theorem.

A natural generalization of Identification Problem 2.4 allows for both outcome and covariate data to be interval valued.

Identification Problem 2.5 (Parametric Prediction with Interval Outcome and Covariate Data):

Maintain the same assumptions as in Identification Problem 2.4, but with unobservable. Let the researcher observe such that . Let and let be bounded. In the absence of additional information, what can the researcher learn about the best linear predictor of given ?

Abstractly, is as given in (2.28), with

replacing (2.29) by an application of Theorem A.1. While this characterization is sharp, it is cumbersome to apply in practice, see Horowitz, Manski, Ponomareva, and Stoye (2003).

On the other hand, when both and are perfectly observed, the best linear predictor is simply equal to the parameter vector that yields a mean zero prediction error that is uncorrelated with . How can this basic observation help in the case of interval data? The idea is that one can use the same insight applied to the set-valued data, and obtain as the collection of ’s for which there exists a selection , and associated prediction error , satisfying and (as shown by Beresteanu, Molchanov, and Molinari, 2011).212121Here for simplicity I suppose that both and have bounded support. Beresteanu, Molchanov, and Molinari (2011) do not make this simplifying assumption. To obtain the formal result, define the -dependent set222222Note that while is a convex set, is not.

Theorem SIR-2.6 (Best Linear Predictor with Interval Outcome and Covariate Data):

Proof.

By Theorem A.1, (up to an ordered coupling as discussed in Appendix A), if and only if the distribution of belongs to . For given , one can find such that and with if and only if the zero vector belongs to . By Theorem A.2, is a convex set and by (A.9), if and only if . The final characterization follows from (A.7). ∎

The support function is an easy to calculate convex sublinear function of , regardless of whether the variables involved are continuous or discrete. The optimization problem in (2.33), determining whether , is a convex program, hence easy to solve. See for example the CVX software by Grant and Boyd (2010). It should be noted, however, that the set itself is not necessarily convex. Hence, tracing out its boundary is non-trivial. I discuss computational challenges in partial identification in Section 6.

I conclude this section by discussing parametric regression. Manski and Tamer (2002) study identification of parametric regression models under the assumptions in Identification Problem 2.6; Theorem SIR-2.7 below reports the result. The proof is omitted because it follows immediately from the proof of Theorem SIR-2.4.

Identification Problem 2.6 (Parametric Regression with Interval Covariate Data):

Let be observable random variables in , , and let be an unobservable random variable. Assume that the joint distribution of is such that and . Suppose that , with a known function such that for each and , is weakly increasing in . In the absence of additional information, what can the researcher learn about ?

Theorem SIR-2.7 (Parametric Regression with Interval Covariate Data):

Under the Assumptions of Identification Problem 2.6, the sharp identification region for is

| (2.34) |

Aucejo, Bugni, and Hotz (2017) study Identification Problem 2.6 for the case of missing covariate data without imposing the mean independence restriction of Manski and Tamer (2002) (Assumption MI in Identification Problem 2.3). As discussed in footnote 16, restriction MI is undesirable in this context because it implies the assumption that data are missing at random. Aucejo, Bugni, and Hotz (2017) characterize under the weaker assumptions, but face the problem that this characterization is usually too complex to compute or to use for inference. They therefore provide outer regions that are easier to compute, and they show that these regions are informative and relatively easy to use.

2.4 Measurement Error and Data Combination

One of the first examples of bounding analysis appears in Frisch (1934), to assess the impact in linear regression of covariate measurement error. This analysis was substantially extended in Gilstein and Leamer (1983), Klepper and Leamer (1984), and Leamer (1987). The more recent literature in partial identification has provided important advances to learn features of probability distributions when the observed variables are error-ridden measures of the variables of interest. Here I briefly mention some of the papers in this literature, and refer to Chapter XXX in this Volume by Schennach (2019) for a thorough treatment of identification and inference with mismeasured and unobserved variables. In an influential paper, Horowitz and Manski (1995) study what can be learned about features of the distribution of in the presence of contaminated or corrupted outcome data. Whereas a contaminated sampling model assumes that data errors are statistically independent of sample realizations from the population of interest, the corrupted sampling model does not. These models are regularly used in the important literature on robust estimation (e.g., Huber, 1964, 2004; Hampel, Ronchetti, Rousseeuw, and Stahel, 2011). However, the goal of that literature is to characterize how point estimators of population parameters behave when data errors are generated in specified ways. As such, the inference problem is approached ex-ante: before collecting the data, one looks for point estimators that are not greatly affected by error. The question addressed by Horowitz and Manski (1995) is conceptually distinct. It asks what can be learned about specific population parameters ex-post, that is, after the data has been collected. For example, whereas the mean is well known not to be a robust estimator in the presence of contaminated data, Horowitz and Manski (1995) show that it can be (non-trivially) bounded provided the probability of contamination is strictly less than one. Dominitz and Sherman (2004, 2005) and Kreider and Pepper (2007, 2008) extend the results of Horowitz and Manski to allow for (partial) verification of the distribution from which the data are drawn. They apply the resulting sharp bounds to learn about school performance when the observed test scores may not be valid for all students. Molinari (2008) provides sharp bounds on the distribution of a misclassified outcome variable under an array of different assumptions on the extent and type of misclassification.

A completely different problem is that of data combination. Applied economists often face the problem that no single data set contains all the variables that are necessary to conduct inference on a population of interest. When this is the case, they need to integrate the information contained in different samples; for example, they might need to combine survey data with administrative data (see Ridder and Moffitt, 2007, for a survey of the econometrics of data combination). From a methodological perspective, the problem is that while the samples being combined might contain some common variables, other variables belong only to one of the samples. When the data is collected at the same aggregation level (e.g., individual level, household level, etc.), if the common variables include a unique and correctly recorded identifier of the units constituting each sample, and there is a substantial overlap of units across all samples, then exact matching of the data sets is relatively straightforward, and the combined data set provides all the relevant information to identify features of the population of interest. However, it is rather common that there is a limited overlap in the units constituting each sample, or that variables that allow identification of units are not available in one or more of the input files, or that one sample provides information at the individual or household level (e.g., survey data) while the second sample provides information at a more aggregate level (e.g., administrative data providing information at the precinct or district level). Formally, the problem is that one observes data that identify the joint distributions and , but not data that identifies the joint distribution whose features one wants to learn. The literature on statistical matching has aimed at using the common variable(s) as a bridge to create synthetic records containing (see, e.g., Okner, 1972, for an early contribution). As Sims (1972) points out, the inherent assumption at the base of statistical matching is that conditional on , and are independent. This conditional independence assumption is strong and untestable. While it does guarantee point identification of features of the conditional distributions , it often finds very little justification in practice. Early on, Duncan and Davis (1953) provided numerical illustrations on how one can bound the object of interest, when both and are binary variables. Cross and Manski (2002) provide a general analysis of the problem. They obtain bounds on the long regression , under the assumption that has finite support. They show that sharp bounds on can be obtained using the results in Horowitz and Manski (1995), thereby establishing a connection with the analysis of contaminated data. They then derive sharp identification regions for . They show that these bounds are sharp when has finite support, and Molinari and Peski (2006) establish sharpness without this restriction. Fan, Sherman, and Shum (2014) address the question of what can be learned about counterfactual distributions and treatment effects under the data scenario just described, but with replaced by , a binary indicator for the received treatment (using the notation of the previous section). In this case, the exogenous selection assumption (conditional on ) does not suffice for point identification of the objects of interest. The authors derive, however, sharp bounds on these quantities using monotone rearrangement inequalities. Pacini (2017) provides partial identification results for the coefficients in the linear projection of on .

2.5 Further Theoretical Advances and Empirical Applications

In order to discuss the partial identification approach to learning features of probability distributions in some level of detail while keeping this chapter to a manageable length, I have focused on a selection of papers. In this section I briefly mention several other excellent theoretical contributions that could be discussed more closely, as well as several papers that have applied partial identification analysis to answer important empirical questions.

While selectively observed data are commonplace in observational studies, in randomized experiments subjects are randomly placed in designated treatment groups conditional on , so that the assumption of exogenous selection is satisfied with respect to the assigned treatment. Yet, identification of some highly policy relevant parameters can remain elusive in the absence of strong assumptions. One challenge results from noncompliance, where individuals’ received treatments differs from the randomly assigned ones. Balke and Pearl (1997) derive sharp bounds on the ATE in this context, when . Even if one is interested in the intention-to-treat parameter, selectively observed data may continue to be a problem. For example, Lee (2009) studies the wage effects of the Job Corps training program, which randomly assigns eligibility to participate in the program. Individuals randomized to be eligible were not compelled to receive treatment, hence Lee (2009) focuses on the intention-to-treat effect. Because wages are only observable when individuals are employed, a selection problem persists despite the random assignment of eligibility to treatment, as employment status may be affected by the training program. Lee obtains sharp bounds on the intention-to-treat effect, through a trimming procedure that leverages results in Horowitz and Manski (1995). Molinari (2010) analyzes the problem of identification of the ATE and other treatment effects, when the received treatment is unobserved for a subset of the population. Missing treatment data may be due to item or survey nonresponse in observational studies, or noncompliance with randomly assigned treatments that are not directly monitored. She derives sharp worst case bounds leveraging results in Horowitz and Manski (1995), and she shows that these are a function of the available prior information on the distribution of missing treatments. If the response function is assumed monotone as in (2.19), she obtains informative bounds without restrictions on the distribution of missing treatments.

Even randomly assigned treatments and perfect compliance with no missing data may not suffice for point identification of all policy relevant parameters. Important examples are given by Heckman, Smith, and Clements (1997) and Manski (1997a). Heckman, Smith, and Clements show that features of the joint distribution of the potential outcomes of treatment and control, including the distribution of treatment effects impacts, cannot be point identified in the absence of strong restrictions. This is because although subjects are randomized to treatment and control, nobody’s outcome is observed under both states. Nonetheless, the authors obtain bounds for the functionals of interest. Mullahy (2018) derives related bounds on the probability that the potential outcome of one treatment is larger than that of the other treatment, and applies these results to health economics problems. Manski shows that features of outcome distributions under treatment rules in which treatment may vary within groups cannot be point identified in the absence of strong restrictions. This is because data resulting from randomized experiments with perfect compliance allow for point identification of the outcome distributions under treatment rules that assign all persons with the same to the same treatment group. However, such data only allow for partial identification of outcome distributions under rules in which treatment may vary within groups. Manski derives sharp bounds for functionals of these distributions.

Analyses of data resulting from natural experiments also face identification challenges. Hotz, Mullin, and Sanders (1997) study what can be learned about treatment effects when one uses a contaminated instrumental variable, i.e. when a mean-independence assumption holds in a population of interest, but the observed population is a mixture of the population of interest and one in which the assumption doesn’t hold. They extend the results of Horowitz and Manski (1995) to learn about the causal effect of teenage childbearing on a teen mother’s subsequent outcomes, using the natural experiment of miscarriages to form an instrumental variable for teen births. This instrument is contaminated because miscarriges may not occur randomly for a subset of the population (e.g., higher miscarriage rates are associated with smoking and drinking, and these behaviors may be correlated with the outcomes of interest).

Of course, analyses of selectively observed data present many challenges, including but not limited to the ones described in Section 2.1. Athey and Imbens (2006) generalize the difference-in-difference (DID) design to a changes-in-changes (CIC) model, where the distribution of the unobservables is allowed to vary across groups, but not overtime within groups, and the additivity and linearity assumptions of the DID are dispensed with. For the case that the outcomes have a continuous distribution, Athey and Imbens provide conditions for point identification of the entire counterfactual distribution of effects of the treatment on the treatment group as well as the distribution of effects of the treatment on the control group, without restricting how these distributions differ from each other. For the case that the outcome variables are discrete, they provide partial identification results, as well as additional conditions compared to their baseline model under which point identification attains.

Motivated by the question of whether the age-adjusted mortality rate from cancer in 2000 was lower than that in the early 1970s, Honoré and Lleras-Muney (2006) study partial identification of competing risk models (see Peterson, 1976, for earlier partial identification results). To answer this question, they need to contend with the fact that mortality rate from cardiovascular disease declined substantially over the same period of time, so that individuals that in the early 1970s might have died from cardiovascular disease before being diagnosed with cancer, do not in 2000. In this context, it is important to carry out the analysis without assuming that the underlying risks are independent. Honoré and Lleras-Muney show that bounds for the parameters of interest can be obtained as the solution to linear programming problems. The estimated bounds suggest much larger improvements in cancer mortality rates than previously estimated.

Blundell, Gosling, Ichimura, and Meghir (2007) use UK data to study changes over time in the distribution of male and female wages, and in wage inequality. Because the composition of the workforce changes over time, it is difficult to disentangle that effect from changes in the distribution of wages, given that the latter are observed only for people in the workforce. Blundell, Gosling, Ichimura, and Meghir begin their empirical analysis by reporting worst case bounds (as in Manski, 1994) on the CDF of wages conditional on covariates. They then consider various restrictions on treatment selection, e.g., a first order stochastic dominance assumption according to which people with higher wages are more likely to work, and derive tighter bounds under this assumption (and under weaker ones). Finally, they bring to bear shape restrictions. At each step of the analysis, they report the resulting bounds, thereby illuminating the role played by each assumption in shaping the inference. Chandrasekhar, Chernozhukov, Molinari, and Schrimpf (2018) provide best linear approximations to the identification region for the quantile gender wage gap using Current Population Survey repeated cross-sections data from 1975-2001, using treatment selection assumptions in the spirit of Blundell, Gosling, Ichimura, and Meghir (2007) as well as exclusion restrictions.