A Generalization of the Savage-Dickey Density Ratio for Testing Equality and Order Constrained Hypotheses

Abstract

The Savage-Dickey density ratio is a specific expression of the Bayes factor when testing a precise (equality constrained) hypothesis against an unrestricted alternative. The expression greatly simplifies the computation of the Bayes factor at the cost of assuming a specific form of the prior under the precise hypothesis as a function of the unrestricted prior. A generalization was proposed by Verdinelli and Wasserman (1995) such that the priors can be freely specified under both hypotheses while keeping the computational advantage. This paper presents an extension of this generalization when the hypothesis has equality as well as order constraints on the parameters of interest. The methodology is used for a constrained multivariate test using the JZS Bayes factor and a constrained hypothesis test under the multinomial model.

Keywords: Bayes factors, constrained hypotheses, constrained multivariate Bayesian test, constrained multinomial models.

1 Introduction

The Savage-Dickey density ratio (Dickey, \APACyear1971) is a special expression of the Bayes factor, the Bayesian measure of statistical evidence between two statistical hypotheses in light of the observed data (Jeffreys, \APACyear1961; Kass \BBA Raftery, \APACyear1995). The Savage-Dickey density ratio is relatively easy to compute from Markov chain Monte Carlo (MCMC) output without requiring the marginal likelihoods under the hypotheses. Consider a test of a normal mean with unknown variance , versus , with independent observations , for . The indices ‘’ and ‘’ refer to a constrained hypothesis and an unconstrained hypothesis111The test can equivalently be formulated as a test of versus as has zero probability under when using a continuous prior for . The formulation is used however to make it explicit that the constrained hypothesis is nested in the unconstrained hypothesis .. Denote the priors for the unknown parameters under and by and , respectively, which reflect which values for the parameters are likely before observing the data. Under we consider a unit information prior and a conjugate inverse gamma prior for the nuisance parameter, say, (the exact choice of the hyperparameters does not qualitatively affect the argument; see also Verdinelli \BBA Wasserman, \APACyear1995, for example). The marginal prior for under then follows a Cauchy distribution (equivalent to a Student distribution with 1 degree of freedom) centered at with a scale parameter of 1. The marginal posterior for under , , also has a Student distribution. When the prior for the nuisance parameter under equals the conditional prior for under given the restriction under , i.e., , the Bayes factor for against can then be written as the Savage-Dickey density ratio: the ratio of the unconstrained posterior and unconstrained prior density evaluated at the constrained null value under (Dickey, \APACyear1971), i.e.,

where denotes the likelihood of the data given the normal mean and variance , and and denote the marginal likelihoods under and , respectively. For the current problem we would thus need to divide the posterior distribution of under evaluated at by the prior Cauchy distribution at , which both have analytic expressions. Note, of course, that the same expression would be obtained by deriving the marginal likelihoods which also have analytic expressions in this scenario. For more complex statistical models with more nuisance parameters, for which the marginal likelihoods would not have analytic expressions, the Savage-Dickey density ratio is particularly useful as we only need to compute the ratio of the unconstrained posterior and the unconstrained prior evaluated at the constrained null value, which are generally easy to obtain, e.g., using MCMC output.

Despite its computational convenience, a limitation of the Savage-Dickey density ratio is that it only holds for a specific form of the prior for the nuisance parameters under the restricted model which is completely determined by the prior under the unrestricted model. This imposed prior under the restricted model may not always have a desirable interpretation. For example, in order for the Savage-Dickey ratio to hold in the above example, the prior for the population variance under equals . This prior under is more concentrated around smaller values for than under as can be seen from the prior modes for under and which are and , respectively. This is contradictory however because the sample variance for will always be smaller under when the mean is unrestricted. Therefore the Savage-Dickey density ratio should be used with care. For discussions on the Savage-Dickey density ratio, see Marin \BBA Robert (\APACyear2010) and Heck (\APACyear2020). For discussions on priors for the nuisance parameters, see Consonni \BBA Veronese (\APACyear2008).

To retain the computational convenience of the Savage-Dickey density ratio, while allowing researchers to freely specify the prior for the nuisance parameters under the restricted model, Verdinelli \BBA Wasserman (\APACyear1995) proposed a generalization. In a multivariate setting when testing a vector of key parameters , i.e., , where r is a vector of constants, against an unconstrained alternative, unconstrained, with nuisance parameters , where the priors under and are denoted by and , respectively, the multivariate generalized Savage-Dickey density ratio is given by

| (1) |

where the expectation is taken over the conditional posterior under the unconstrained model, . As can be seen, the generalization is equal to the original Savage Dickey density ratio (the first factor on the right hand side of (1)) multiplied with a correction factor based on the ratio of the freely chosen prior for the nuisance parameters, , and the imposed prior for the nuisance parameters under the Savage-Dickey density ratio, . In the above example, one might want to use the same marginal prior for the nuisance parameter under as under , i.e., .

The generalization in (1) was not derived when the constrained hypothesis contains order (or one-sided) constraints in addition to equality constraints, say, . Scientific theories however are very often formulated with combinations of equality and order constraints (Hoijtink, \APACyear2011). In repeated measures studies for instance, theory may suggest a specific ordering of the measurement means (de Jong \BOthers., \APACyear2017) or measurement variances (Böing-Messing \BBA Mulder, \APACyear2020), in a regression model theory may suggest that a certain set of predictor variables have zero effects, while other variables are expected to have a positive or a negative effects (Mulder \BBA Olsson-Collentine, \APACyear2019), or order constraints may be formulated on regression effects (Haaf \BBA Rouder, \APACyear2017) or intraclass correlations (Mulder \BBA Fox, \APACyear2019) in multilevel models. The goal of the current paper is therefore to show the generalization of the Savage-Dickey density ratio in (1) for a constrained hypothesis with equality and order constraints on certain key parameters. This is shown in Section 2, where the generalization is related to existing special cases of the Bayes factor. Section 3 presents two applications of Bayesian constrained hypothesis testing under two statistical models: A multivariate Bayesian test for standardized effects under the multivariate normal model using a novel extension of the JZS Bayes factor (Rouder \BOthers., \APACyear2009), and a constrained hypothesis test on the cell probabilities under a multinomial model. The paper ends with some short concluding remarks in Section 4.

2 Extending the Savage-Dickey density ratio

Lemma 1 presents our main result.

Lemma 1

Consider a constrained statistical model, , where the parameters are fixed with equality constraints, i.e., , and order (or one-sided) constraints are formulated on the parameters , i.e., , with (unconstrained) nuisance parameters , and an alternative unconstrained model , where are unrestricted. If we denote the priors under and according to and , respectively, then the Bayes factor of model against model given a data set y can be expressed as

| (2) |

where the expectation is taken over the conditional posterior of given under , i.e., , and denotes the “completed” prior under the completed constrained hypothesis where the one-sided constraints are omitted, i.e., , such that , is the indicator function which equals 1 if holds, and 0 otherwise, and denotes the prior probability of under the completed prior under .

Proof: Appendix A.

Remark 1

Note that in the special case where

so that the completed prior under is equal to , then (2) results in the known generalization of the Savage-Dickey density ratio of the Bayes factor for an equality and order hypothesis against an unconstrained alternative,

| (3) |

This expression has been reported in Mulder \BBA Gelissen (\APACyear2018), for example.

Remark 2

Remark 3

The importance of the “completed” prior where the one-sided constraints are omitted was also highlighted by Pericchi \BOthers. (\APACyear2008) for intrinsic Bayes factors.

Lemma 1 shows which four ingredients need to be computed in order to obtain the Bayes factor of a constrained hypothesis against an unconstrained alternative. The computation of these four ingredients can be done in different ways across different statistical models. To give readers more insights about the computational aspects, the next section shows the application of the result under two different statistical models: the multivariate normal model for multivariate continuous data and the multinomial model for categorical data.

3 Applications

3.1 A multivariate test using the JZS Bayes factor

The Cauchy prior for standardized effects is becoming increasingly popular for Bayes factor testing in the social and behavioral sciences (Rouder \BOthers., \APACyear2009, \APACyear2012; Rouder \BBA Morey, \APACyear2015). This Bayes factor is based on key contributions by Jeffreys (\APACyear1961), Zellner \BBA Siow (\APACyear1980), and Liang \BOthers. (\APACyear2008), and is therefore also referred to as the JZS Bayes factor. Here we extend this to a Bayesian multivariate test under the multivariate normal model, and show how to compute the Bayes factor for testing a hypothesis with equality and order constraints on the standardized effects using Lemma 1. Note that this test differs from multivariate tests on multiple coefficients using a multivariate Cauchy prior under univariate linear regression models (Rouder \BBA Morey, \APACyear2015; Heck, \APACyear2020) as we consider a model with a multivariate outcome variable.

Let a multivariate dependent variable of dimensions, , follow a multivariate normal distribution, i.e., , for . To explicitly model the standardized effects, we reparameterize the model according to

| (4) |

where are the unknown standardized effects, and is the lower triangular Cholesky factor of the unknown covariance matrix , such that . The model in (4) is a generalization of the univariate model considered by Rouder \BOthers. (\APACyear2009), .

As a motivating example we consider the bivariate data set () presented in Larocque \BBA Labarre (\APACyear2004), where contains the cell count differences of CD45RA T and CD45RO T cells of HIV-positive newborn infants (Sleasman \BOthers., \APACyear1999). We are interested in testing whether the standardized effects of the cell count differences of the two cell types are equal and positive, i.e.,

The sample means were and the estimated covariance matrix equalled .

Extending the prior proposed by Rouder \BOthers. (\APACyear2009) to the multivariate normal model, we set an unconstrained Cauchy prior on under and the Jeffreys prior for the covariance matrix:

A diagonal prior scale matrix is set for given by , with . This prior implies that standardized effects of about 0.5 are likely under . Under the constrained hypothesis the free parameters are the common standardized effect, say, , and the error covariance matrix, . We set a univariate Cauchy prior for with scale truncated in , and the Jeffreys prior for , i.e.,

where denotes the completed prior, and 2 serves as a normalizing constant for the completed prior as . As has a similar interpretation as and under , the prior scale is also set to .

By applying the following linear transformation on the standardized effects,

| (5) |

the model can equivalently be written as , and the hypotheses can be written as

Note here that corresponds to the common standardized effect under . The prior for under follows a bivariate Cauchy distribution with scale matrix .

If one would be testing the hypotheses with the Savage-Dickey density ratio in (3), it is easy to show that the implied prior for under (i.e., the conditional unconstrained prior for given under ) follows a Student distribution with 2 degrees of freedom with a scale parameter of ; thus assuming that standardized effects of 0.25 are likely under . As was discussed earlier, there is no logical reason why the common standardized effect under the restricted hypothesis is expected to be smaller than the standardized effects under a priori.

The JSZ Bayes factor for this constrained testing problem using Lemma 1 based on the actual Cauchy priors for the standardized effects can be computed using MCMC output from a sampler under , which is described in Appendix B. The R code for the computation is given in Appendix C.1. The four key quantifies in (2) are computed as follows:

-

•

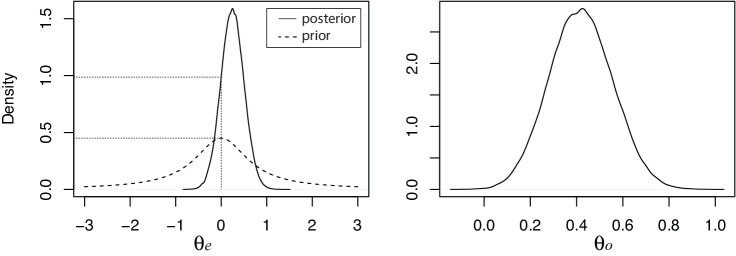

As the unconstrained marginal prior for follows a Cauchy distribution with scale (Figure 1, left panel, dashed line), the prior density equals .

-

•

The estimated marginal posterior for under follows from MCMC output. The estimated posterior for is plotted in Figure 1 (left panel, solid line). This yields .

-

•

As the completed prior for under follows a distribution that is centered at zero, the prior probability equals .

-

•

As the priors for the covariance matrices cancel out in the fraction, the expected value can be written as under the conditional posterior for given under . Appendix B also shows how to get posterior draws from under given . The estimated posterior is displayed in Figure 1 (right panel). A Monte Carlo estimate can then be used to compute the expectation, which yields 1.098799.

Application of Lemma 1 then yields a Bayes factor for against of . Thus there is 4.8 times more evidence in the data for equal and positive standardized count differences than for the unconstrained alternative hypothesis. Assuming equal prior probabilities for and this would yield posterior probabilities of and . Thus there is mild evidence for relative to . In order to draw clearer conclusions more data would need to be collected.

3.2 Constrained hypothesis testing under the multinomial model

When analyzing categorical data using a multinomial model, researchers are often interested in testing the relationships between the probabilities of the different cells (Robertson, \APACyear1978; Klugkist \BOthers., \APACyear2010; Heck \BBA Davis-Stober, \APACyear2019). As an example we consider an experiment for testing the Mendelian inheritance theory discussed by Robertson (\APACyear1978). A total of 556 peas coming from crosses of plants from round yellow seeds and plants from wrinkled green seeds were divided in four categories. The cell probabilities for these categories are contained in the vector , where denotes the probability that a pea resulting from such a mating is round and yellow; denotes the probability that it is wrinkled and yellow; denotes the probability that it is round and green; and denotes the probability that it is wrinkled and green. The Mendelian theory states that is largest, followed by and which are assumed to be equal, and is expected to be smallest. This can be summarized as . In particular the theory dictates that the four probabilities are proportional to 9, 3, 3, and 1, respectively. We translate this to a completed prior under such that its means satisfy . This can be achieved via a Dirichlet prior under an alternative parameterization, , with . The cell probabilities under are then defined by , which then follow a specific scaled Dirichlet distribution, which we denote by SDirichlet222This specific scaled Dirichlet distribution has probability density function , with , where is the multivariate beta function.. The prior for the cell probabilities under is then a truncation of this scaled Dirichlet distribution truncated under . The Mendelian hypothesis can equivalently be formulated on the transformed parameters so that , as in Lemma 1. It is easier however to compute the four quantities in (2) via the untransformed parameters as will be shown below.

The Mendelian hypothesis will be tested against an unconstrained alternative which does not make any assumptions about the relationships between the cell probabilities. A uniform prior on the simplex will be used under the alternative, i.e., . The observed frequencies in the four respective categories were equal to 315, 101, 108, and 32.

The R code for the computation of the Bayes factor of against can be found in Appendix C.2.

-

•

The unconstrained marginal prior density at can be estimated from a sample of where is sampled from the unconstrained Dirichlet prior, resulting in .

-

•

Similarly, the unconstrained marginal posterior density at can be obtained by sampling from the unconstrained Dirichlet posterior, resulting in .

-

•

The prior probability under can be obtained by first sampling , then transforming the prior draws according to , and taking the proportion of draws satisfying the constraints , where denotes the -th draw, for .

-

•

To get draws from the conditional distribution given when under , we can sample transformed parameters , and compute . This can be used to obtain draws from the conditional posterior for given under by setting . The expectation in (2) can then be computed as the arithmetic mean of based on a sufficiently large sample. This yields an estimate of 10.50881.

In sum the Bayes factor of the Mendelian hypothesis against the noninformative unconstrained alternative is equal to . This can be interpreted as relatively strong evidence for the Mendelian hypothesis against an unconstrained alternative based on the observed data.

Finally note that by using probability calculus it can be shown that the first two ingredients have analytic solutions as the marginal probability density at under , when , is equal to . In the above calculation, numerical estimates were used to give readers more insights how to obtain these quantities when analytic expressions are unavailable.

4 Concluding remarks

As Bayes factors are becoming increasingly popular to test hypotheses with equality as well as order constraints on the parameters of interest, more flexible and fast estimation methods to acquire these Bayes factors are needed. The generalization of the Savage-Dickey density ratio that was presented in this paper will be a useful contribution for this purpose. The expression allows one to compute Bayes factors in a straightforward manner from MCMC output while being able to freely specify the priors for the free parameters under the competing hypotheses. The applicability of the proposed methodology was illustrated in a constrained multivariate test using a novel extension of the JSZ Bayes factor to the multivariate normal model and in a constrained hypothesis test under the multinomial model.

Acknowledgements

The authors would like to thank Florian Böing-Messing for helpful discussions at an early stage of the paper, and the editor and three anonymous reviewers for constructive feedback which improved the readability of the manuscript. The first author is supported by an ERC Starting Grant (758791).

Appendix A Proof of Lemma 1

As the constrained model is nested in the unconstrained model , the likelihood under can be written as the truncation of the unconstrained likelihood, i.e., . The result in Lemma 1 then follows via the following steps,

which completes the proof. Note that in the third step the indicator function, , was omitted as the integrand is integrated over the subspace where . In the second last step, the completed version of the constrained hypothesis has the order constraints omitted, i.e., , with completed prior , such that .

Appendix B MCMC sampler for the multivariate Student test

-

1.

Drawing the standardized effects . It is well-known that a multivariate Cauchy prior of dimensions can be written as a Multivariate normal distribution with an inverse Wishart mixing distribution on the normal covariance matrix with degrees of freedom, i.e.,

Thus the conditional prior for given the auxiliary parameter matrix follows a distribution. Consequently, as , the conditional posterior of follows a multivariate normal posterior,

where are the sample means of , for .

-

2.

Drawing the auxiliary covariance matrix . The conditional posterior for only depends on the standardized effects and it follows an inverse Wishart distribution,

-

3.

Drawing the error covariance matrix . The conditional posterior for the covariance matrix does not follow a known distribution. For this reason we use a random walk (e.g., Gelman \BOthers., \APACyear2004) for sampling the separate elements of .

The sampler under the unconstrained model while restricting () is very similar except that the prior for is now univariate Cauchy and is a scalar, and thus the conditional posterior for is univariate normal , where is the mean of . Also note that the inverse Wishart distribution in Step 2 is now for a covariance matrix which is equivalent to an inverse gamma distribution.

Appendix C R code for empirical analyses

C.1 R code for multivariate test in Section 3.1

library(mvtnorm)

library(Matrix)

# computing the unconstrained marginal prior density at \theta_e=0:

priorE <- dcauchy(0, location = 0, scale = sqrt(.5))

# computing the unconstrained marginal posterior density at \theta_e=0:

# read data

Y <- t(matrix(c(242,1708,569,569,270,757,-25,499,309,231,22,338,-42,26,

-233,119,206,163,-106,-186,55,54,85,48,30,50,194,525,-87,-110,159,148,

29,102,89,364,-9,36,158,234,76,122,15,24,3,36,93,71,160,44,66,128,180,

155,237,85,105,76,16,6,167,364,-10,-18,-61,-21,-7,-2,15,32,160,188),

nrow=2))

set.seed(123)

#dimension

p <- ncol(Y)

nums <- p*(p+1)/2

n <- nrow(Y)

#initial parameter values based on burn-in period

delta <- c(.5,.2)

Sigma <- matrix(c(2,2,2,11),2,2) * 10**4

L <- t(chol(Sigma))

Phi <- diag(p)

#selection of unique elements in \Sigma

lowerSigma <- lower.tri(Sigma,diag=TRUE)

welklower <- which(lowerSigma)

# tranformation matrix

Trans <- matrix(c(1,0,-1,1),ncol=2)

#prior hyperparameters

S0 <- diag(p) * .5**2

# random walk sd’s for the elements of \Sigma to have an

# efficient acceptance probability based on burn-in period.

sdstep <- c(9,13,48) * 10**3

#store draws

numdraws <- 1e5

storeDelta <- matrix(0,nrow=numdraws,ncol=p)

storeSigma <- storePhi <- array(0,dim=c(numdraws,p,p))

#draws from stationary distribution

for(s in 1:numdraws){

#draw delta

deltaMean <- c(apply(Y%*%t(solve(L)),2,mean))

SigmaDelta <- solve(n*diag(p) + solve(Phi))

muDelta <- c(SigmaDelta%*%deltaMean*n)

delta <- c(rmvnorm(1,mean=muDelta,sigma=SigmaDelta))

#draw Phi

Phi <- solve(rWishart(1,df=p+1,Sigma=solve(S0 + delta%*%t(delta)))[,,1])

#draw Sigma using MH

for(sig in 1:nums){

welknu <- welklower[sig]

step1 <- rnorm(1,sd=sdstep[sig])

Sigma0 <- matrix(0,p,p)

Sigma0[lowerSigma] <- Sigma[lowerSigma]

Sigma0[welknu] <- Sigma0[welknu] + step1

Sigma_can <- Sigma0 + t(Sigma0) - diag(diag(Sigma0))

if(min(eigen(Sigma_can)$values) > .000001){

#the candidate is positive definite

L_can <- t(chol(Sigma_can))

#acceptance probability

R_MH <- exp( sum(dmvnorm(Y,mean=c(L_can%*%delta),sigma=Sigma_can,

log=TRUE)) - (p+1)/2*log(det(Sigma_can)) -

sum(dmvnorm(Y,mean=c(L%*%delta),sigma=Sigma,log=TRUE)) +

(p+1)/2*log(det(Sigma)) )

if(runif(1) < R_MH){

#accept draw

Sigma <- Sigma_can

L <- t(chol(Sigma))

}

}

}

storeDelta[s,] <- delta

storeSigma[s,,] <- Sigma

storePhi[s,,] <- Phi

}

drawsE <- storeDelta[,1] - storeDelta[,2]

denspost <- density(drawsE)

df <- approxfun(denspost)

postE <- df(0)

# Figure 1 (left panel)

plot(denspost,xlim=c(-3,3),main="",xlab="theta_e")

seq1 <- seq(-3,3,length=1e3)

lines(seq1,dcauchy(seq1,scale=sqrt(.5)),lty=2)

# computing the prior probability of \theta_o>0 under H_c:

priorO <- 1 - pcauchy(0, location = 0, scale = .5)

# computing the expectation of the ratio of the priors

# from a posterior sample under H_c given \theta_e = 0

# initialization

set.seed(123)

p1 <- 1

p <- ncol(Y)

nums <- p*(p+1)/2

n <- nrow(Y)

S0 <- diag(1)*.25**2

# initial parameter values based on burn-in period

delta <- .55

Phi <- matrix(1)

Sigma <- matrix(c(23,22,22,89),nrow=2) * 10**3

L <- t(chol(Sigma))

# random walk sd’s for the elements of \Sigma to have an

# efficient acceptance probability based on burn-in period.

sdstep1 <- c(10,15,48) * 10**3

lowerSigma <- lower.tri(Sigma,diag=TRUE)

welklower <- which(lowerSigma)

# store draws

numdraws <- 1e5

storeDelta1 <- matrix(0,nrow=numdraws,ncol=1)

storePhi1 <- array(0,dim=c(numdraws,p1,p1))

storeSigma1 <- array(0,dim=c(numdraws,p,p))

for(s in 1:numdraws){

#draw delta

deltaMean <- mean(c(apply(Y%*%t(solve(L)),2,mean)))

SigmaDelta <- solve(2*n*diag(p1) + solve(Phi))

muDelta <- c(SigmaDelta%*%deltaMean*2*n)

delta <- c(rmvnorm(1,mean=muDelta,sigma=SigmaDelta))

#draw Phi

Phi <- solve(rWishart(1,df=p1+1,Sigma=solve(S0 +

delta%*%t(delta)))[,,1])

#draw Sigma using MH

deltavec <- rep(delta,2)

for(sig in 1:nums){

welknu <- welklower[sig]

step1 <- rnorm(1,sd=sdstep1[sig])

Sigma0 <- matrix(0,p,p)

Sigma0[lowerSigma] <- Sigma0[lowerSigma] + Sigma[lowerSigma]

Sigma0[welknu] <- Sigma0[welknu] + step1

Sigma_can <- Sigma0 + t(Sigma0) - diag(diag(Sigma0))

if(min(eigen(Sigma_can)$values) > .000001 ){

#the candidate is positive definite

L_can <- t(chol(Sigma_can))

#dit zou sneller kunnen via onafhankelijke univariate normals

R_MH <- exp( sum(dmvnorm(Y,mean=c(L_can%*%deltavec),

sigma=Sigma_can,log=TRUE)) - (p+1)/2*log(det(Sigma_can)) -

sum(dmvnorm(Y,mean=c(L%*%deltavec),sigma=Sigma,log=TRUE))

+ (p+1)/2*log(det(Sigma)) )

if(runif(1) < R_MH){

#accept draw

Sigma <- Sigma_can

L <- t(chol(Sigma))

}

}

}

storeDelta1[s,] <- delta

storePhi1[s,,] <- Phi

storeSigma1[s,,] <- Sigma

}

expratio <- mean(dcauchy(c(storeDelta1),scale=.5) /

dcauchy(c(storeDelta1),scale=.25)

* (c(storeDelta1)>0))

# Figure 1, right panel

plot(density(c(storeDelta1)),main="",xlab="theta_o")

# computation of the Bayes factor

Bcu <- postE / (priorE * priorO) * expratio

C.2 R code for multinomial model in Section 3.2

library(MCMCpack)

set.seed(123)

# computing the unconstrained marginal prior density at \theta_e=0:

uncpriorsample <- rdirichlet(n=1e7, alpha=c(1,1,1,1))

densprior <- density(uncpriorsample[,2]-uncpriorsample[,3])

df <- approxfun(densprior)

priorE <- df(0)

remove(uncpriorsample)

# computing the unconstrained marginal posterior density at \theta_e=0:

uncpostsample <- rdirichlet(n=1e7, alpha=c(1+315,1+101,1+108,1+32))

denspost <- density(uncpostsample[,2]-uncpostsample[,3])

df <- approxfun(denspost)

postE <- df(0)

remove(uncpostsample)

# computing the prior probability of \theta_o>0 under H_c:

priorsample1 <- rdirichlet(n=1e7,alph=c(9,6,1))

priorsample1[,2] <- priorsample1[,2]/2

priorO <- mean(priorsample1[,1] > priorsample1[,2] &

priorsample1[,2] > priorsample1[,3])

remove(priorsample1)

# computing the expectation of the ratio of priors:

# first define probability density for (gamma1,gamma2)

SDirichlet <- function(gamma1,gamma2,alpha1,alpha2,alpha3){

alphavec <- c(alpha1,alpha2,alpha3)

B1 <- exp(sum(lgamma(alphavec)) - lgamma(sum(alphavec)))

return(

2^alpha2 / B1 * gamma1^(alpha1-1) * gamma2^(alpha2-1) *

(1-gamma1-2*gamma2)^(alpha3-1)

)

}

condpostsample <- rdirichlet(n=1e7, alpha=c(316,210,33))

condpostsample[,2] <- condpostsample[,2]/2

expratio <- mean(SDirichlet(condpostsample[,1],condpostsample[,2],9,6,1) /

SDirichlet(condpostsample[,1],condpostsample[,2],1,1,1) *

(condpostsample[,1]>condpostsample[,2] &

condpostsample[,2]>condpostsample[,3])

)

remove(condpostsample)

# computing the Bayes factor of $H_c$ against $H_u$:

Bcu <- postE/(priorE*priorO)*expratio

References

- Böing-Messing \BBA Mulder (\APACyear2020) \APACinsertmetastarBoingMessing2020{APACrefauthors}Böing-Messing, F.\BCBT \BBA Mulder, J. \APACrefYearMonthDay2020. \BBOQ\APACrefatitleBayes Factors for Testing Order Constraints on Variances of Dependent Outcomes Bayes factors for testing order constraints on variances of dependent outcomes.\BBCQ \APACjournalVolNumPagesThe American Statistician1-10. {APACrefDOI} \doi10.1080/00031305.2020.1715257 \PrintBackRefs\CurrentBib

- Consonni \BBA Veronese (\APACyear2008) \APACinsertmetastarConsonniVeronese2008{APACrefauthors}Consonni, G.\BCBT \BBA Veronese, P. \APACrefYearMonthDay2008. \BBOQ\APACrefatitleCompatibility of Prior Specifications Across Linear Models Compatibility of prior specifications across linear models.\BBCQ \APACjournalVolNumPagesStatistical Science23332–353. \PrintBackRefs\CurrentBib

- de Jong \BOthers. (\APACyear2017) \APACinsertmetastarDeJong:2017{APACrefauthors}de Jong, J., Rigotti, T.\BCBL \BBA Mulder, J. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleOne after the other: Effects of sequence patterns of breached and overfulfilled obligations One after the other: Effects of sequence patterns of breached and overfulfilled obligations.\BBCQ \APACjournalVolNumPagesEuropean Journal of Work and Organizational Psychology26337–355. \PrintBackRefs\CurrentBib

- Dickey (\APACyear1971) \APACinsertmetastarDickey:1971{APACrefauthors}Dickey, J. \APACrefYearMonthDay1971. \BBOQ\APACrefatitleThe weighted likelihood ratio, linear hypotheses on normal location parameters The weighted likelihood ratio, linear hypotheses on normal location parameters.\BBCQ \APACjournalVolNumPagesThe Annals of Statistics42204–223. \PrintBackRefs\CurrentBib

- Gelman \BOthers. (\APACyear2004) \APACinsertmetastarGelman{APACrefauthors}Gelman, A., Carlin, J\BPBIB., Stern, H\BPBIS.\BCBL \BBA Rubin, D\BPBIB. \APACrefYear2004. \APACrefbtitleBayesian Data Analysis Bayesian data analysis (\PrintOrdinalSecond \BEd). \APACaddressPublisherLondon: Chapman & Hall. \PrintBackRefs\CurrentBib

- Haaf \BBA Rouder (\APACyear2017) \APACinsertmetastarHaaf{APACrefauthors}Haaf, J.\BCBT \BBA Rouder, J. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleDeveloping constraint in Bayesian mixed models Developing constraint in Bayesian mixed models.\BBCQ \APACjournalVolNumPagesPsychological Methods22779?798. {APACrefDOI} \doi10.1037/met0000156 \PrintBackRefs\CurrentBib

- Heck (\APACyear2020) \APACinsertmetastarHeck:2020{APACrefauthors}Heck, D. \APACrefYearMonthDay2020. \BBOQ\APACrefatitleA caveat on the Savage-Dickey density ratio: The case of computing Bayes factors for regression parameters A caveat on the Savage-Dickey density ratio: The case of computing Bayes factors for regression parameters.\BBCQ \APACjournalVolNumPagesBritish Journal of Mathematical and Statistical Psychology. {APACrefDOI} \doi10.1111/bmsp.12150 \PrintBackRefs\CurrentBib

- Heck \BBA Davis-Stober (\APACyear2019) \APACinsertmetastarHeck:2019{APACrefauthors}Heck, D.\BCBT \BBA Davis-Stober, C. \APACrefYearMonthDay2019. \BBOQ\APACrefatitleMultinomial models with linear inequality constraints: Overview and improvements of computational methods for Bayesian inference Multinomial models with linear inequality constraints: Overview and improvements of computational methods for Bayesian inference.\BBCQ \APACjournalVolNumPagesJournal of Psychological Mathematics9170–87. \PrintBackRefs\CurrentBib

- Hoijtink (\APACyear2011) \APACinsertmetastarHoijtink:2011{APACrefauthors}Hoijtink, H. \APACrefYear2011. \APACrefbtitleInformative Hypotheses: Theory and Practice for Behavioral and Social Scientists Informative hypotheses: Theory and practice for behavioral and social scientists. \APACaddressPublisherNew York: Chapman & Hall/CRC. \PrintBackRefs\CurrentBib

- Jeffreys (\APACyear1961) \APACinsertmetastarJeffreys{APACrefauthors}Jeffreys, H. \APACrefYear1961. \APACrefbtitleTheory of Probability-3rd ed Theory of probability-3rd ed. \APACaddressPublisherNew York: Oxford University Press. \PrintBackRefs\CurrentBib

- Kass \BBA Raftery (\APACyear1995) \APACinsertmetastarKass:1995{APACrefauthors}Kass, R\BPBIE.\BCBT \BBA Raftery, A\BPBIE. \APACrefYearMonthDay1995. \BBOQ\APACrefatitleBayes Factors Bayes factors.\BBCQ \APACjournalVolNumPagesJournal of American Statistical Association90773–795. \PrintBackRefs\CurrentBib

- Klugkist \BOthers. (\APACyear2010) \APACinsertmetastarKlugkist:2010{APACrefauthors}Klugkist, I., Laudy, O.\BCBL \BBA Hoijtink, H. \APACrefYearMonthDay2010. \BBOQ\APACrefatitleBayesian evaluation of inequality and equality constrained hypotheses for contingency tables Bayesian evaluation of inequality and equality constrained hypotheses for contingency tables.\BBCQ \APACjournalVolNumPagesPsychological Methods15281–299. \PrintBackRefs\CurrentBib

- Larocque \BBA Labarre (\APACyear2004) \APACinsertmetastarLarocque2004{APACrefauthors}Larocque, D.\BCBT \BBA Labarre, M. \APACrefYearMonthDay2004. \BBOQ\APACrefatitleA Conditionally Distribution-Free Multivariate Sign Test for One-Sided Alternatives A conditionally distribution-free multivariate sign test for one-sided alternatives.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association99499–509. \PrintBackRefs\CurrentBib

- Liang \BOthers. (\APACyear2008) \APACinsertmetastarLiang:2008{APACrefauthors}Liang, F., Paulo, R., Molina, G., Clyde, M\BPBIA.\BCBL \BBA Berger, J\BPBIO. \APACrefYearMonthDay2008. \BBOQ\APACrefatitleMixtures of priors for Bayesian variable selection Mixtures of priors for Bayesian variable selection.\BBCQ \APACjournalVolNumPagesJournal of American Statistical Association103481410–423. \PrintBackRefs\CurrentBib

- Marin \BBA Robert (\APACyear2010) \APACinsertmetastarMarinRobert:2010{APACrefauthors}Marin, J\BPBIM.\BCBT \BBA Robert, C\BPBIP. \APACrefYearMonthDay2010. \BBOQ\APACrefatitleOn resolving the Savage–Dickey paradox On resolving the Savage–Dickey paradox.\BBCQ \APACjournalVolNumPagesElectronic Journal of Statistics4643–654. \PrintBackRefs\CurrentBib

- Mulder \BBA Fox (\APACyear2019) \APACinsertmetastarMulderFox:2019{APACrefauthors}Mulder, J.\BCBT \BBA Fox, J\BHBIP. \APACrefYearMonthDay2019. \BBOQ\APACrefatitleBayes factor testing of multiple intraclass correlations Bayes factor testing of multiple intraclass correlations.\BBCQ \APACjournalVolNumPagesBayesian Analysis14521–552. \PrintBackRefs\CurrentBib

- Mulder \BBA Gelissen (\APACyear2018) \APACinsertmetastarMulderGelissen:2018{APACrefauthors}Mulder, J.\BCBT \BBA Gelissen, J\BPBIP. \APACrefYearMonthDay2018. \BBOQ\APACrefatitleBayes factor testing of equality and order constraints on measures of association in social research Bayes factor testing of equality and order constraints on measures of association in social research.\BBCQ {APACrefURL} \urlhttps://arxiv.org/abs/1807.05819 \PrintBackRefs\CurrentBib

- Mulder \BBA Olsson-Collentine (\APACyear2019) \APACinsertmetastarMulderOlsson:2019{APACrefauthors}Mulder, J.\BCBT \BBA Olsson-Collentine, A. \APACrefYearMonthDay2019. \BBOQ\APACrefatitleSimple Bayesian testing of scientific expectations in linear regression models Simple Bayesian testing of scientific expectations in linear regression models.\BBCQ \APACjournalVolNumPagesBehavioral Research Methods511117–1130. {APACrefDOI} \doi10.3758/s13428-018-01196-9 \PrintBackRefs\CurrentBib

- Pericchi \BOthers. (\APACyear2008) \APACinsertmetastarPericchi:2008{APACrefauthors}Pericchi, L\BPBIR., Liu, G.\BCBL \BBA Torres, D. \APACrefYearMonthDay2008. \BBOQ\APACrefatitleObjective Bayes factors for informative hypotheses: “Completing” the informative hypothesis and “splitting” the Bayes factors Objective bayes factors for informative hypotheses: “completing” the informative hypothesis and “splitting” the bayes factors.\BBCQ \BIn H. Hoijtink, I. Klugkist\BCBL \BBA P\BPBIA. Boelen (\BEDS), \APACrefbtitleBayesian Evaluation of Informative Hypotheses Bayesian evaluation of informative hypotheses (\BPGS 131–154). \APACaddressPublisherNew York: Springer. \PrintBackRefs\CurrentBib

- Robertson (\APACyear1978) \APACinsertmetastarRobertson:1978{APACrefauthors}Robertson, T. \APACrefYearMonthDay1978. \BBOQ\APACrefatitleTesting For and Against an Order Restriction on Multinomial Parameters Testing for and against an order restriction on multinomial parameters.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association73197–202. \PrintBackRefs\CurrentBib

- Rouder \BBA Morey (\APACyear2015) \APACinsertmetastarRouder:2015{APACrefauthors}Rouder, J\BPBIN.\BCBT \BBA Morey, R\BPBID. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleDefault Bayes factors for model selection in regression Default Bayes factors for model selection in regression.\BBCQ \APACjournalVolNumPagesMultivariate Behavioral Resaerch6877–903. \PrintBackRefs\CurrentBib

- Rouder \BOthers. (\APACyear2012) \APACinsertmetastarRouder:2012{APACrefauthors}Rouder, J\BPBIN., Morey, R\BPBID., Speckman, P\BPBIL.\BCBL \BBA Province, J\BPBIM. \APACrefYearMonthDay2012. \BBOQ\APACrefatitleDefault Bayes factors for ANOVA designs Default Bayes factors for ANOVA designs.\BBCQ \APACjournalVolNumPagesJournal of Mathematical Psychology. \PrintBackRefs\CurrentBib

- Rouder \BOthers. (\APACyear2009) \APACinsertmetastarRouder:2009{APACrefauthors}Rouder, J\BPBIN., Speckman, P\BPBIL., D. Sun, R\BPBID\BPBIM.\BCBL \BBA Iverson, G. \APACrefYearMonthDay2009. \BBOQ\APACrefatitleBayesian t tests for accepting and rejecting the null hypothesis Bayesian t tests for accepting and rejecting the null hypothesis.\BBCQ \APACjournalVolNumPagesPsychonomic Bulletin & Review16225–237. \PrintBackRefs\CurrentBib

- Sleasman \BOthers. (\APACyear1999) \APACinsertmetastarSleasman{APACrefauthors}Sleasman, J\BPBIW., Nelson, R\BPBIP., Goodenow, M\BPBIM., Wilfert, D., Hutson, A., Bassler, M.\BDBLMueller, B\BPBIU. \APACrefYearMonthDay1999. \BBOQ\APACrefatitleImmunoreconstitution After Ritonavir Therapy in Children With Human Immunodeficiency Virus Infection Involves Multiple Lymphocyte Lineages Immunoreconstitution after ritonavir therapy in children with human immunodeficiency virus infection involves multiple lymphocyte lineages.\BBCQ \APACjournalVolNumPagesJournal of Pediatrics134597–606. \PrintBackRefs\CurrentBib

- Verdinelli \BBA Wasserman (\APACyear1995) \APACinsertmetastarVerdinelli:1995{APACrefauthors}Verdinelli, I.\BCBT \BBA Wasserman, L. \APACrefYearMonthDay1995. \BBOQ\APACrefatitleComputing Bayes Factors Using a Generalization of the Savage-Dickey Density Ratio Computing bayes factors using a generalization of the savage-dickey density ratio.\BBCQ \APACjournalVolNumPagesJournal of American Statistical Association90614-618. \PrintBackRefs\CurrentBib

- Zellner \BBA Siow (\APACyear1980) \APACinsertmetastarZellnerSiow1980{APACrefauthors}Zellner, A.\BCBT \BBA Siow, A. \APACrefYearMonthDay1980. \BBOQ\APACrefatitlePosterior Odds Ratios for Selected Regression Hypotheses Posterior odds ratios for selected regression hypotheses.\BBCQ \BIn J\BPBIM. Bernardo, M\BPBIH. DeGroot, D\BPBIV. Lindley\BCBL \BBA A\BPBIF\BPBIM. Smith (\BEDS), \APACrefbtitleBayesian Statistics Bayesian statistics (\BPGS 585–603). \APACaddressPublisherValenciaUniversity Press. \PrintBackRefs\CurrentBib