A critical overview of privacy-preserving approaches

for collaborative forecasting

Abstract

Cooperation between different data owners may lead to an improvement in forecast quality – for instance by benefiting from spatial-temporal dependencies in geographically distributed time series. Due to business competitive factors and personal data protection questions, said data owners might be unwilling to share their data, which increases the interest in collaborative privacy-preserving forecasting. This paper analyses the state-of-the-art and unveils several shortcomings of existing methods in guaranteeing data privacy when employing Vector Autoregressive (VAR) models. The methods are divided into three groups: data transformation, secure multi-party computations, and decomposition methods. The analysis shows that state-of-the-art techniques have limitations in preserving data privacy, such as (i) the necessary trade-off between privacy and forecasting accuracy, empirically evaluated through simulation and real-world experiment based on solar data; (ii) the iterative model fitting processes which reveal data after a number of iterations.

keywords:

Vector autoregression , Forecasting , Time series , Privacy-preserving , ADMM1 Introduction

The progress of the internet-of-things (IoT) and big data technologies is fostering a disruptive evolution in the development of innovative data analytics methods and algorithms. This also yields ideal conditions for data-driven services (from descriptive to prescriptive analysis), in which the accessibility to large volumes of data is a fundamental requirement. In this sense, the combination of data from different owners can provide valuable information for end-users and increase their competitiveness.

In order to combine data coming from different sources, several statistical approaches have emerged. For example, in time series collaborative forecasting, the Vector Autoregressive (VAR) model has been widely used to forecast variables that may have different data owners. In the energy sector, the VAR model is deemed appropriate to update very short-term forecasts (e.g., from 15 minutes to 6 hours ahead) with recent data, thus taking advantage of geographically distributed data collected from sensors (e.g., anemometer, pyranometer) and/or wind turbines and solar power inverters [Tastu et al., 2013, Bessa et al., 2015a]. The VAR model can also be used in short-term electricity price forecasting [Ziel & Weron, 2018]. Furthermore, the large number of potential data owners favors the estimation of the VAR model’s coefficients by applying distributed optimization algorithms. The Alternating Direction Method of Multipliers (ADMM) is a widely used convex optimization technique; see Boyd et al. [2011]. The combination of the VAR model and ADMM can be used jointly for collaborative forecasting [Cavalcante et al., 2017], which consists of collecting and combining information from diverse owners. The collaborative forecasting methods require sharing data or coefficients, depending on the structure of the data, and may or may not be focused on data privacy. This process is also called federated learning [Yang et al., 2019].

Some other examples of collaborative forecasting include: (a) forecasting and inventory control in supply chains, in which the benefits of various types of information-sharing options are investigated [Aviv, 2003, 2007]; (b) forecasting traffic flow data (i.e. speeds) among different locations [Ravi & Al-Deek, 2009]; (c) forecasting retail prices of a specific product at every outlet by using historical retail prices of the product at a target outlet and at competing outlets [Ahmad et al., 2016]. The VAR model is the simplest collaborative model but, conceptually, a collaborative forecasting model for time series does not need to be a VAR. Furthermore, it is possible to extend the VAR model to include exogenous information (see Nicholson et al. [2017] for more details) and to model non-linear relationships with past values (e.g. Li & Genton [2009] extend the additive model structure to a multivariate setting).

Setting aside the significant potential of the VAR model for collaborative forecasting, the concerns with the privacy of personal and commercially sensitive data comprise a critical barrier and require privacy-preserving algorithmic solutions for estimating the coefficients of the model.

A confidentiality breach occurs when third parties recover the data provided in confidence without consent. The leaking of a single record from the dataset may have a different impact according to the nature of the data. For example, in medical data where each record represents a different patient, it could lead to the disclosure of all the details about said patient. On the other hand, concerning renewable energy generation time series, knowing that 30 MWh was produced in a given hour does not provide very relevant information to a competitor. Hereafter, the term confidentiality breach designates the reconstruction of the entire dataset by another party.

These concerns with data confidentiality motivated the research to handle confidential data in methods such as linear regression and classification problems [Du et al., 2004], ridge linear regression [Karr et al., 2009], logistic regression [Wu et al., 2012], survival analysis [Lu et al., 2015], aggregated statistics for time series data [Jia et al., 2014], etc. Aggregated statistics consist of aggregating a set of time series data through a specific function, such as the average (e.g., average amount of daily exercise), sum, minimum or maximum. However, certain literature approaches identified confidentiality breaches, showing that the statistical methods developed to protect data privacy should be analyzed to confirm their robustness and that additional research may be required to address overlooked limitations [Fienberg et al., 2009]. Furthermore, the application of these methodologies to the VAR model needs to be carefully analyzed, since the target variables are the time series of each data owner, and the covariates are the lags of the same time series, meaning that both target and covariates share a large proportion of values.

The simplest solution would be having the data owners agreeing on a commonly trusted entity (or a central node), capable of gathering private data, solving the associated model’s fitting problem on behalf of the data owners, and then returning the results [Pinson, 2016]. However, in many cases, the data owners are unwilling to share their data even with a trusted central node. This has also motivated the development of data markets to monetize data and promote data sharing [Agarwal et al., 2019], which can be driven by blockchain and smart contracts technology [Kurtulmus & Daniel, 2018].

Another possibility would be to apply differential privacy mechanisms, which consist in adding properly calibrated noise to an algorithm (e.g., adding noise to the coefficients estimated during each iteration of the fitting procedure) or to the data itself. Differential privacy is not an algorithm, but a rigorous definition of privacy that is useful for quantifying and bounding privacy loss (i.e., how much original data a party can recover when receiving data protected with added noise) [Dwork & Smith, 2009]. It requires computations insensitive to changes in any particular record or intermediate computations, thereby restricting data leaks through the results – this is elaborated in A. While computationally efficient and popular, these techniques invariably degrade the predictive performance of the model [Yang et al., 2019] and are not very effective, as this paper shows.

The present paper conducts a review of the state-of-the-art in statistical methods for collaborative forecasting with privacy-preserving approaches. This work is not restricted to a simple overview of the existing methods and it performs a critical evaluation of said methods, from a mathematical and numerical point of view, namely when applied to the VAR model. The major contribution to the literature is to show gaps and downsides of current methods and to present insights for further improvements towards fully privacy-preserving VAR forecasting methods.

In this work, we analyze the existing state-of-the-art privacy-preserving techniques, dividing them into the following groups:

-

1.

Data transformation methods: each data owner transforms their data before the model’s fitting process, by adding randomness to the original data in such a way that high accuracy and privacy can be achieved at the end of the fitting process. The statistical method is independent of the transformation function and it is applied to the transformed data.

-

2.

Secure multi-party computation protocols: the encryption of the data occurs while fitting the statistical model (i.e. intermediate calculations of an iterative process) and data owners are required to conjointly compute a function over their data with protocols for secure matrix operations. A protocol consists of a set of rules that determine how data owners must operate to determine said function. These rules establish the calculations assigned to each data owner, what information should be shared among them, in addition to the conditions necessary for the adequate implementation of said calculations.

-

3.

Decomposition-based methods: the optimization problem is decomposed into sub-problems allowing each data owner to fit their model’s coefficients separately.

The remaining of the paper is organized as follows: Section 2 describes the state-of-the-art for collaborative forecasting with privacy-preserving; Section 3 describes the VAR model as well as coefficients estimators, and performs a critical evaluation of the state-of-the-art methods when applied to the VAR model (solar energy time series data are used in the numerical analysis). Section 4 focuses on the discussion and comparison of the presented approaches, while the conclusions are presented in Section 5.

2 Privacy-preserving Approaches

For notation purposes, vectors and matrices are denoted by bold small and capital letters, e.g. and , respectively. The vector represents a column vector with dimension, where are scalars, . The column-wise joining of vectors and matrices is indicated by and , respectively.

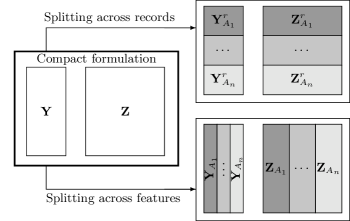

Furthermore, is the covariate matrix and is the target matrix, considering data owners. The values , and are the number of records, covariates and target variables, respectively. When considering collaborative forecasting models, different divisions of the data may be considered. Figure 1 shows the most common one, i.e.

-

1.

Data split by records: the data owners, represented as , observe the same features for different groups of samples, e.g. different timestamps in the case of time series. is split into and into , such that ;

-

2.

Data split by features: the data owners observe different features of the same records. , , such that , , with and ;

This section summarizes state-of-the-art approaches to deal with privacy-preserving collaborative forecasting methods. Section 2.1 describes the methods that ensure confidentiality by transforming the data. Section 2.2 presents and analyzes the secure multi-party protocols. Section 2.3 describes the decomposition-based methods.

2.1 Data Transformation Methods

Data transformation methods use operator to transform the data matrix into . Then, the problem is solved in the transformed domain. A common method of masking sensitive data is adding or multiplying it by perturbation matrices. In additive randomization, random noise is added to the data in order to mask the values of records. Consequently, the more masked the data becomes, the more secure it will be, as long as the differential privacy definition is respected (see A). However, the use of randomized data implies the deterioration of the estimated statistical models, and the estimated coefficients of said data should be close to the estimated coefficients after using original data [Zhou et al., 2009].

Concerning multiplicative randomization, it enables changing the dimensions of the data by multiplying it by random perturbation matrices. If the perturbation matrix multiplies the original data on the left (pre-multiplication), i.e. , then it is possible to change the number of records; otherwise, if multiplies on the right (post-multiplication), i.e. , it is possible to modify the number of features. Hence, it is possible to change both dimensions by applying both pre and post-multiplication by perturbation matrices.

2.1.1 Single Data Owner

The use of linear algebra to mask the data is a common practice in recent outsourcing approaches, in which a data owner resorts to the cloud to fit their model’s coefficients, without sharing confidential data. For example, in Ma et al. [2017] the coefficients that optimize the linear regression model

| (1) |

with covariate matrix , target variable , coefficient vector and error vector , are estimated through the regularized least squares estimate for the ridge linear regression, with penalization term ,

| (2) |

In order to compute via a cloud server, the authors consider that

| (3) |

where and , , . Then, the masked matrices and are sent to the server which computes

| (4) |

where , , and are randomly generated matrices, , . Finally, the data owner receives and recovers the original coefficients by computing .

Data normalization is also a data transformation approach that masks data by transforming the original features into a new range through the use of a mathematical function. There are many methods for data normalization, the most important ones being -score and min-max normalization [Jain & Bhandare, 2011], which are useful when the actual minimum and maximum values of the features are unknown. However, in many applications, these values are either known or publicly available, and normalized values still encompass commercially valuable information.

As to time series data, other approaches for data randomization make use of the Fourier and wavelet transforms. The Fourier transform allows representing periodic time series as a linear combination of sinusoidal components (sine and cosine). In Papadimitriou et al. [2007], each data owner generates a noise time series by: (i) adding Gaussian noise to relevant coefficients, or (ii) disrupting each sinusoidal component by randomly changing its magnitude and phase. Similarly, the wavelet transform represents the time series as a combination of functions (e.g. the Mexican hat or the Poisson wavelets), and randomness can be introduced by adding random noise to the coefficients [Papadimitriou et al., 2007]. However, there are no privacy guarantees since noise does not respect any formal definition such as differential privacy.

2.1.2 Multiple Data Owners

The task of masking data is even more challenging when dealing with different data owners, since it is crucial to ensure that the transformations that data owners make to their data preserve the real relationship between the variables or the time series.

Usually, for generalized linear models (linear regression model, logistic regression model, among others), where data owners observe the same features, i.e. data is split by records as illustrated in Figure 1, each data owner , can individually multiply their covariate matrix and target variable by a random matrix (with a jointly defined value), providing to the competitors [Mangasarian, 2012, Yu et al., 2008], which allows pre-multiplying the original data,

by , since

| (5) |

The same holds for the multiplication , . This definition of is possible because when multiplying and , the -th column of only multiplies the -th row of . For some statistical learning algorithms, a property of such matrix is the orthogonality, i.e. . Model fitting is then performed with this new representation of the data, which preserves the solution to the problem. This is true in the linear regression model because the multivariate least squares estimate for the linear regression model with covariate matrix and target variable is

| (6) |

which is also the multivariate least squares estimate for the coefficients of a linear regression considering data matrices and , respectively. Despite this property, the application in LASSO regression does not guarantee that the sparsity of the coefficients is preserved and a careful analysis is necessary to ensure the correct estimation of the model [Zhou et al., 2009]. Liu et al. [2008] discuss attacks based on prior knowledge, in which a data owner estimates by knowing a small collection of original data records. Furthermore, when considering the linear regression model for which and , i.e. data is split by features, it is not possible to define a matrix and then privately compute and , because as explained, the -th column of multiplies the -th row of , which, in this case, consists of data coming from different owners.

Similarly, if the data owners observe different features, a linear programming problem can be solved in a way that each individual data owner multiplies their data by a private random matrix (with a jointly defined value ) and, then, shares [Mangasarian, 2011], , which is equivalent to post-multiplying the original dataset by , which represents the joining of , through row-wise operation. However, the obtained solution is in a different space, and it needs to be recovered by multiplying it by the corresponding . For the linear regression, which models the relationship between the covariates and the target , this algorithm corresponds to solving a linear regression that models the relationship between and , i.e. the solution is given by

| (7) |

where and are shared matrices. Two private matrices , are required to transform the data, since the number of columns for and is different ( and values are jointly defined). The problem is that the multivariate least squares estimate for (7) is given by

| (8) |

which implies that this transformation does not preserve the coefficients of the linear regression considering data matrices and , respectively, and therefore and would have to be shared.

Generally, data transformation is performed through the generation of random matrices that pre- or post-multiply the private data. However, there are other techniques through which data is transformed with matrices defined according to the data itself, as is the case with Principal Component Analysis (PCA). PCA is a widely used statistical procedure for reducing the dimension of data, by applying an orthogonal transformation that retains as much of the data variance as possible. Considering the matrix of the eigenvectors of the covariance matrix , , PCA allows representing the data by variables performing , where are the first columns of , . For the data split by records, Dwork et al. [2014] suggest a differential private PCA, assuming that each data owner takes a random sample of the fitting records to form the covariate matrix. In order to protect the covariance matrix, one can add Gaussian noise to this matrix (determined without sensible data sharing), leading to the computation of the principal directions of the noisy covariance matrix. To finalize the process, the data owners multiply the sensible data by said principal directions before feeding it into the model fitting. Nevertheless, the application to collaborative linear regression with data split by features would require sharing the data when computing the matrix, since is divided by rows. Furthermore, as explained in (7) and (8), it is difficult to recover the original linear regression model by performing the estimation of the coefficients using transformed covariates and target matrices, through post-multiplication by random matrices.

Regarding the data normalization techniques mentioned above, Zhu et al. [2015] assume that data owners mask their data by using -score normalization, followed by the sum of random noise (from Uniform or Gaussian distributions), allowing a greater control on their data, which is then shared with a recommendation system that fits the model. However, the noise does not meet the differential privacy definition (see A).

For data collected by different sensors (e.g., smart meters and mobile users) it is common to proceed to the aggregation of data through privacy-preserving techniques. For instance, by adding carefully calibrated Laplacian noise to each time series [Fan & Xiong, 2014, Soria-Comas et al., 2017]. The addition of noise to the data is an appealing technique given its easy application. However, even if this noise meets the definition of differential privacy, there is no guarantee that the resulting model will perform well.

2.2 Secure Multi-party Computation Protocols

In secure multi-party computation, the intermediate calculations required by the fitting algorithms, which require data owners to jointly compute a function over their data, are performed through protocols for secure operations, such as matrix addition or multiplication (discussed in Section 2.2.1). In these approaches, the encryption of the data occurs while fitting the model (discussed in Section 2.2.2), instead of as a pre-processing step such as in the data transformation methods from the previous section.

2.2.1 Linear Algebra-based Protocols

The simplest secure multi-party computation protocols are based on linear algebra and address the problems where matrix operations with confidential data are necessary. Du et al. [2004] propose secure protocols for product and inverse of the sum , for any two private matrices and with appropriate dimensions. The aim is to fit a (ridge) linear regression between two data owners, who observe different covariates but share the target variable. Essentially, the protocol transforms the product of matrices, , , into a sum of matrices, , which are equally secret, . However, since the estimate of the coefficients for linear regression with covariate matrix and target matrix is

| (9) |

the protocol is used to perform the computation of such that

| (10) |

which requires the definition of an protocol to compute

| (11) |

For the protocol, , , there are two different formulations, according to the existence, or not, of a third entity. In cases where only two data owners perform the protocol, a random matrix is jointly generated and the protocol achieves the following results, by dividing the and into two matrices with the same dimensions

| (14) | ||||

| (15) |

where and represent the left and right part of , and and designate the top and bottom part of , respectively. In this case,

| (16) |

is derived by the first data owner, and

| (17) |

by the second one. Otherwise, a third entity is assumed to generate random matrices and , such that

| (18) |

which are sent to the first and second data owners, respectively, , , . In this case, the data owners start by trading the matrices and , then the second data owner randomly generates a matrix and sends

| (19) |

to the first data owner, in such a way that, at the end of the protocol, the first data owner keeps the information

| (20) |

and the second keeps (since the sum of with is ).

Finally, the protocol considers two steps, where . Initially, the matrix is jointly converted to using two random matrices, and , which are only known to the second data owner to prevent the first one from learning matrix , . The results of are known only by the first data owner who can conduct the inverse computation . In the following step, the data owners jointly remove and and get . Both steps can be achieved by applying the protocol. Although these protocols prove to be an efficient technique to solve problems with a shared target variable, one cannot say the same when is private, as further elaborated in Subsection 3.3.2.

Another example of secure protocols for producing private matrices can be found in Karr et al. [2009]; they are applied to data from multiple owners who observe different covariates and target features – which are also assumed to be secret. The proposed protocol allows two data owners, with correspondent data matrix and , , , to perform the multiplication by: (i) first data owner generates , , such that

| (21) |

where is the -th column of matrix, and , and then sends to the second owner; (ii) the second data owner computes and shares it, and (iii) the first data owner performs

| (22) |

without the possibility of recovering , since the . To generate , Karr et al. [2009] suggest selecting columns from the matrix, computed by decomposition of the private matrix , and excluding the first columns. Furthermore, the authors define the optimal value for according to the number of linearly independent equations (represented by NLIE) on the other data owner’s data. The second data owner obtains (providing values, since ) and receives , knowing that (which contains values), i.e.

| (23) |

Similarly, the first data owner receives (providing values) and (providing values since and ), i.e.

| (24) |

Karr et al. [2009] determines the optimal value for by assuming that both data owners equally share NLIE, so that none of the agents benefit from the order assumed when running the protocol, i.e.

| (25) |

which allows to obtain the optimal value .

An advantage to this approach, when compared to the one proposed by Du et al. [2004], is that is simply generated by the first data owner, while the invertible matrix proposed by Du et al. [2004] needs to be agreed upon by both parties, which entails substantial communication costs when the number of records is high.

2.2.2 Homomorphic Cryptography-based Protocols

The use of homomorphic encryption was successfully introduced in model fitting and it works by encrypting the original values in such a way that the application of arithmetic operations in the public space does not compromise the encryption. Homomorphic encryption ensures that, after the decryption stage (in the private space), the resulting values correspond to the ones obtained by operating on the original data. Consequently, homomorphic encryption is especially responsive and engaging to privacy-preserving applications. As an example, the Paillier homomorphic encryption scheme defines that (i) two integer values encrypted with the same public key may be multiplied together to give encryption of the sum of the values, and (ii) an encrypted value may be taken to some power, yielding encryption of the product of the values. Hall et al. [2011] proposed a secure protocol for summing and multiplying real numbers by extending the Paillier encryption, aiming to perform matrix products required to solve linear regression, for data divided by features or records.

Equally based in Paillier encryption, the work of Nikolaenko et al. [2013] introduces two parties that correctly perform their tasks without teaming up to discover private data: a crypto-service provider (i.e., a party that provides software or hardware-based encryption and decryption services) and an evaluator (i.e., a party who runs the learning algorithm), in order to perform a secure linear regression for data split by records. Similarly, Chen et al. [2018] use Paillier and ElGamal encryptions to fit the coefficients of ridge linear regression, also including these entities. In both works, the use of the crypto-service provider is prompted by assuming that the evaluator does not corrupt its computation in producing an incorrect result. Two conditions are required to ensure that there will be no confidentiality breaches: the crypto-service provider must publish the system keys correctly, and there can be no collusion between the evaluator and the crypto-service provider. The data could be reconstructed if the crypto-service provider supplies correct keys to a curious evaluator. For data divided by features, the work of Gascón et al. [2017] extends the approach of Nikolaenko et al. [2013] by designing a secure multi/two-party inner product.

Jia et al. [2018] explore a privacy-preserving data classification scheme with a support vector machine, thus ensuring that the data owners can successfully conduct data classification without exposing their learned models to the “tester”, while the “testers” keep their data private. For example, a hospital (owner) can create a model to learn the relation between a set of features and the existence of a disease, and another hospital (tester) can use this model to obtain a forecasting value, without any knowledge about the model. The method is supported by cryptography-based protocols for secure computation of multivariate polynomial functions but, unfortunately, this only works for data split by records.

Li & Cao [2012] addresses the privacy-preserving computation of the sum and the minimum of multiple time series collected by different data owners, by combining homomorphic encryption and a novel key management technique to support large data dimensions. These statistics with a privacy-preserving solution for individual user data are quite useful to explore mobile sensing in different applications such as environmental monitoring (e.g., average level of air pollution in an area), traffic monitoring (e.g., highest moving speed during rush hour), healthcare (e.g., number of users infected by a flu), etc. Liu et al. [2018] and Li et al. [2018] explored similar approaches, based on Paillier or ElGamal encryption, namely concerning the application in smart grids. However, the estimation of models such as the linear regression model also requires protocols for the secure product of matrices.

Homomorphic cryptography was further explored to solve secure linear programming problems through intermediate steps of the simplex method, which optimizes the problem by using slack variables, tableaus, and pivot variables [Hoogh, 2012]. The author observed that the proposed protocols are still unviable to solve linear programming problems, having numerous variables and constraints, which are quite reasonable in practice.

Aono et al. [2017] perform a combination of homomorphic cryptography with differential privacy, in order to deal with data split by records. Summarily, if data is split by records, as illustrated in Figure 1, each -th data owner observes the covariates and target variable , . Then and are computed and Laplacian noise is added to them. This information is encrypted and sent to the cloud server, which works on the encrypted domain, summing all the matrices received. Finally, the server provides the result of this sum to a client who decrypts it and obtains relevant information to perform the linear regression, i.e. , , etc. However, noise addition can result in a poor estimation of the coefficients, limiting the performance of the model. Furthermore, this is not valid when data is divided by features, because and .

In summary, the cryptography-based methods are usually robust to confidentiality breaches but may require a third party for keys generation, as well as external entities to perform the computations in the encrypted domain. Furthermore, the high computational complexity is a challenge when dealing with real applications [Hoogh, 2012, Zhao et al., 2019, Tran & Hu, 2019].

2.3 Decomposition-based Methods

In decomposition-based methods, problems are solved by breaking them up into smaller sub-problems and solving each separately, either in parallel or in sequence. Consequently, private data is naturally distributed between the data owners. However, this natural division requires sharing of intermediate information. For that reason, some approaches combine decomposition-based methods with data transformation or homomorphic cryptography-based methods; but in this paper’s case, a special emphasis will be given to these methods in separate.

2.3.1 ADMM Method

The ADMM is a powerful algorithm that circumvents problems without a closed-form solution, such as the LASSO regression, and it has proved to be efficient and well suited for distributed convex optimization, in particular for large-scale statistical problems [Boyd et al., 2011]. Let be a convex forecast error function, between the true values and the forecasted values given by the model using a set of covariates and coefficients , and a convex regularization function. The ADMM method [Boyd et al., 2011] solves the optimization problem

| (26) |

by splitting into two variables ( and ),

| (27) |

and using the corresponding augmented Lagrangian function formulated with dual variable ,

| (28) |

The quadratic term provides theoretical convergence guarantees because it is strongly convex. This implies mild assumptions on the objective function. Even if the original objective function is convex, augmented Lagrangian is strictly convex (in some cases strongly convex) [Boyd et al., 2011].

The ADMM solution is estimated by the following iterative system,

| (29) |

For data split by records, the consensus problem splits primal variables and separately optimizes the decomposable cost function for all the data owners under the global consensus constraints. Considering that the sub-matrix of corresponds to the local data of the th data owner, the coefficients are given by

| (30) | ||||

where . In this case, measures the error between the true values and the forecasted values given by the model .

For data split by features, the sharing problem splits into , and into . Auxiliary are introduced for the -th data owner based on and . In such case, the sharing problem is formulated based on the decomposable cost function and . Then, are given by

| (31) | ||||

where . In this case, is related to the error between the true values and the forecasted values given by the model .

Undeniably, ADMM provides a desirable formulation for parallel computing [Dai et al., 2018]. However, it is not possible to ensure continuous privacy, since ADMM requires intermediate calculations, allowing the most curious competitors to recover the data at the end of some iterations by solving non-linear equation systems [Bessa et al., 2018]. An ADMM-based distributed LASSO algorithm, in which each data owner only communicates with its neighbor to protect data privacy, is described in Mateos et al. [2010], with applications in signal processing and wireless communications. Unfortunately, this approach is only valid for the cases where data is distributed by records.

The concept of differential privacy was also explored in ADMM by introducing randomization when computing the primal variables, i.e. during the iterative process, each data owner estimates the corresponding coefficients and perturbs them by adding random noise [Zhang & Zhu, 2017]. However, these local randomization mechanisms can result in a non-convergent algorithm with poor performance even under moderate privacy guarantees. To address these concerns, Huang et al. [2019] use an approximate augmented Lagrangian function and Gaussian mechanisms with time-varying variance. Nevertheless, noise addition is not enough to guarantee privacy, as a competitor can potentially use the results from all iterations to perform inference [Zhang et al., 2018].

Zhang et al. [2019] have recently combined a variant of ADMM with homomorphic encryption namely in cases where data is divided by records. As referred by the authors, the incorporation of the proposed mechanism in decentralized optimization under data divided by features is quite difficult. Whereas the algorithm for data split by records the algorithm only requires sharing the coefficients, the exchange of coefficients in data split by features is not enough, since each data owner observes different features. The division by features requires the local estimation of by using information related to , and , meaning that, for each new iteration, an th data owner shares new values, instead of (from ), .

For data split by features, Zhang & Wang [2018] propose a probabilistic forecasting method combining ridge linear quantile regression and ADMM. The output is a set of quantiles instead of a unique value (usually the expected value). In this case, the ADMM is applied to split the corresponding optimization problem into sub-problems, which are solved by each data owner, assuming that all the data owners communicate with a central node in an iterative process, providing intermediate results instead of private data. In fact, the authors claimed that the paper describes how wind power probabilistic forecasting with off-site information could be achieved in a privacy-preserving and distributed fashion. However, the authors did not conduct an in-depth analysis of the method, as will be shown in Section 3. Furthermore, this method assumes that the central node knows the target matrix.

2.3.2 Newton-Raphson Method

ADMM is becoming a standard technique in recent research about distributed computing in statistical learning, but it is not the only one. For generalized linear models, the distributed optimization for model’s fitting has been efficiently achieved through the Newton-Raphson method, which minimizes a twice differentiable forecast error function , between the true values and the forecasted values given by the model using a set of covariates , including lags of . is the coefficient matrix, which is updated iteratively. The estimate for at iteration , represented by , is given by

| (32) |

where and are the gradient and Hessian of , respectively. With certain properties, convergence to a certain global minima can be guaranteed [Nocedal & Wright, 2006]: (i) is continuously differentiable, and (ii) is convex.

In order to enable distributed optimization, and are required to be decomposable over multiple data owners, i.e. these functions can be rewritten as the sum of functions that depend exclusively on local data from each data owner. Slavkovic et al. [2007] proposes a secure logistic regression approach for data split by records and features by using secure multi-party computation protocols during the Newton-Raphson method iterations. However, and although distributed computing is feasible, there is no sufficient guarantee of data privacy, because it is an iterative process; even though an iteration cannot reveal private information, sufficient iterations can: in a logistic regression with data split by features, for each iteration the data owners exchange the matrix , making it possible to recover the local data at the end of some iterations [Fienberg et al., 2009].

An example of an earlier promising work – combining logistic regression with the Newton-Raphson method for data distributed by records – was the Grid binary LOgistic REgression (GLORE) framework [Wu et al., 2012]. The GLORE model is based on model sharing instead of patient-level data, which has motivated subsequent improvements, some of which continue to suffer from confidentiality breaches on intermediate results and other ones resorting to protocols for matrix addition and multiplication. Later, Li et al. [2015] explored the issue concerning Newton-Raphson over data distributed by features, considering the existence of a server – that receives the transformed data and computes the intermediate results, returning them to each data owner. In order to avoid the disclosure of local data while obtaining an accurate global solution, the authors apply the kernel trick to obtain the global linear matrix, computed using dot products of local records (), which can be used to solve the dual problem for logistic regression. However, the authors identified a technical challenge in scaling up the model when the sample size is large, since each record requires a parameter.

2.3.3 Gradient-Descent Methods

Different gradient-descent methods have also been explored, aiming to minimize a forecast error function , between the true values and the forecasted values given by the model using a set of covariates , including lags of . The coefficient matrix is updated iteratively such that the estimate at iteration , , is given by

| (33) |

where is the learning rate; it allows the parallel computation when the optimization function is decomposable. A common error function is the multivariate least squared error,

| (34) |

With certain properties, convergence to a certain global minima can be guaranteed [Nesterov, 1998]: (i) is convex, (ii) is Lipschitz continuous with constant , i.e. for any , ,

| (35) |

and (iii) .

Han et al. [2010] proposed a privacy-preserving linear regression for data distributed over features (with shared ) by combining distributed gradient-descent with secure protocols, based on pre- or post-multiplication of the data by random private matrices. In the work of Song et al. [2013], differential privacy is introduced by adding random noise in the updates,

| (36) |

When this iterative process uses a few samples (or even a single sample) randomly selected, rather than the entire data, the process is known as stochastic gradient descent (SGD). The authors argue that the trade-off between performance and privacy is most pronounced when smaller batches are used.

3 Collaborative Forecasting with VAR: Privacy Analysis

This section presents a privacy analysis focused on the VAR model, a model for the analysis of multivariate time series and collaborative forecasting. It is not only used for forecasting tasks in different domains (and with significant improvements over univariate autoregressive models), but also for structural inference where the main objective is exploring certain assumptions about the causal structure of the data [Toda & Phillips, 1993]. A variant with the Least Absolute Shrinkage and Selection Operator (LASSO) regularization is also covered. The critical evaluation of the methods described in Section 2 is conducted from a mathematical and numerical point of view in Section 3.3. The solar energy time series dataset and R scripts are published in the online appendages to this paper (see B).

3.1 VAR Model Formulation

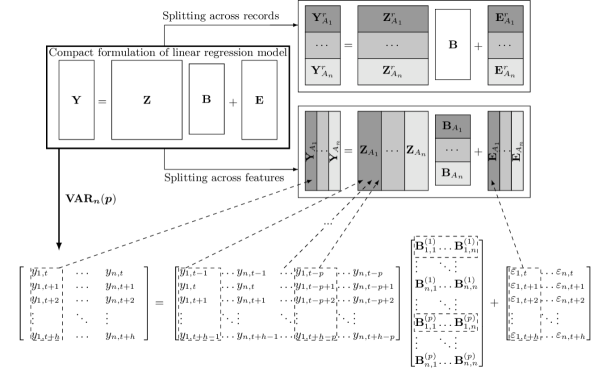

Let be an -dimensional multivariate time series, where is the number of data owners. Then, follows a VAR model with lags, represented as , when the following relationship holds

| (37) |

for , where is the constant intercept (row) vector, ; represents the coefficient matrix at lag , , and the coefficient associated with lag of time series (to estimate time series ) is positioned at of , for ; and , , indicates a white noise vector that is independent and identically distributed with mean zero and nonsingular covariance matrix. By simplification, is assumed to follow a centered process, , i.e., as a vector of zeros of appropriate dimension. A compact representation of a model reads as

| (38) |

where

are obtained by joining the vectors row-wise, and defining, respectively, the response matrix, the coefficient matrix, the covariate matrix and the error matrix, with .

Notice that the VAR formulation adopted in this paper is not the usual because a large proportion of the literature in privacy-preserving techniques derives from the standard linear regression problem, in which each row is a record and each column is a feature.

Notwithstanding the high potential of the VAR model for collaborative forecasting, namely by linearly combining time series from the different data owners, data privacy or confidentiality issues might hinder this approach. For instance, renewable energy companies, competing in the same electricity market, will never share their electrical energy production data, even if this leads to a forecast error improvement in all individual forecasts.

For classical linear regression models, there are several techniques for estimating coefficients without sharing private information. However, in the VAR model, the data is divided by features (Figure 2) and the variables to be forecasted are also covariates, which is challenging for privacy-preserving techniques (especially because it is also necessary to protect the data matrix , as illustrated in Figure 3). In the remaining of the paper, and represent the target and covariate matrix for the -th data owner, respectively, when defining a VAR model. Therefore, the covariates and target matrices are obtained by joining the individual matrices column-wise, i.e. and . For distributed computation, the coefficient matrix of data owner is denoted by .

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

|---|---|---|---|---|---|---|

3.2 Estimation in VAR Models

Commonly, when the number of covariates included, , is substantially smaller than the length of the time series, , the VAR model can be fitted using multivariate least squares solution given by

| (39) |

where represents both vector and matrix norms. However, in collaborative forecasting, as the number of data owners increases, as well as the number of lags, it becomes crucial to use regularization techniques, such as LASSO, in order to introduce sparsity into the coefficient matrix estimated by the model. In the standard LASSO-VAR approach (see Nicholson et al. [2017] for different variants of the LASSO regularization in the VAR model), the coefficients are given by

| (40) |

where is a scalar penalty parameter.

With the addition of the LASSO regularization term, the convex objective function in (40) becomes non-differentiable, thus limiting the variety of optimization techniques that can be employed. In this domain, ADMM (which was described in 2.3.1) is a widespread and computationally efficient technique that enables the parallel estimation for data divided by features. The ADMM formulation of the non-differentiable cost function associated to LASSO-VAR model in (40) solves the optimization problem

| (41) |

which differs from (40) by splitting into two parts ( and ). This allows splitting the objective function in two distinct objective functions, and . The augmented Lagrangian [Boyd et al., 2011] of this problem is

| (42) |

where is the dual variable and is the penalty parameter. The scaled form of this Lagrangian is

| (43) |

where is the scaled dual variable associated with the constrain . Hence, according to (29), the ADMM formulation for LASSO-VAR consists in the following iterations [Cavalcante et al., 2017],

| (44) |

Concerning the LASSO-VAR model, and since data is naturally divided by features (i.e. , and ) and the functions and are decomposable (i.e. and ), the model fitting problem (40) becomes

| (45) |

, which is rewritten as

| (46) |

, while the corresponding distributed ADMM formulation [Boyd et al., 2011, Cavalcante et al., 2017] is the one presented in the system of equations (47),

| (47a) | |||

| (47b) | |||

| (47c) |

where and , ,, , .

Although the parallel computation is an appealing property for the design of a privacy-preserving approach, ADMM is an iterative optimization process that requires intermediate calculations, thus a careful analysis is necessary to evaluate if some confidentiality breaches can occur at the end of some iterations.

3.3 Privacy Analysis

3.3.1 Data Transformation with Noise Addition

This section presents experiments with simulated data and solar energy data collected from a smart grid pilot in Portugal. The objective is to quantify the impact of data distortion (through noise addition) into the model forecasting skill.

a) Synthetic Data: An experiment has been performed to add random noise from the Gaussian distribution with zero mean and variance , Laplace distribution with zero mean and scale parameter and Uniform distribution with support , represented by , and , respectively. Synthetic data generated by VAR processes are used to measure the differences between the coefficients’ values when adding noise to the data. The simplest case considers a VAR with two data owners and two lags described by

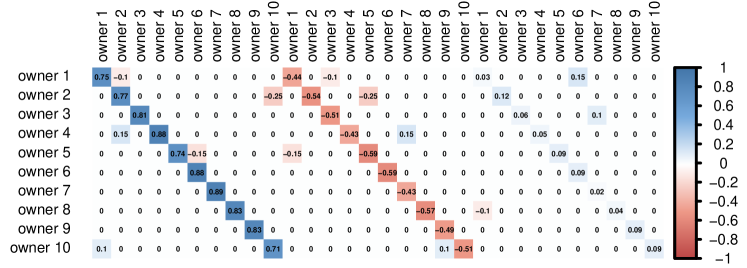

The second case includes ten data owners and three lags, introducing a high percentage of null coefficients (), with Figure 4 illustrating the considered coefficients. Since a specific configuration can generate various distinct trajectories, 100 simulations are performed for each specified VAR model, each of them with 20,000 timestamps. For both simulated datasets, the errors were assumed to follow a multivariate Normal distribution with a zero mean vector and a covariance matrix equal to the identity matrix of appropriate dimensions. Distributed ADMM (detailed in Section 2.3.1) was used to estimate the LASSO-VAR coefficients, considering two different noise characterizations, .

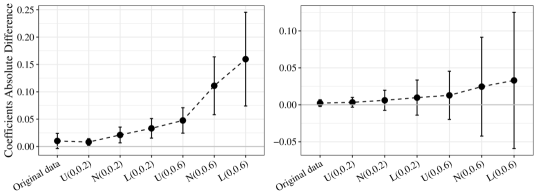

Figure 5 summarizes the mean and the standard deviation of the absolute difference between the real and estimated coefficients, for both VAR processes, from 100 simulations. The greater the noise , the greater the distortion of the estimated coefficients. Moreover, the Laplace distribution, which has desirable properties to make the data private according to the differential privacy framework, registers the greater distortion in the estimated model.

Using the original data, the ADMM solution tends to stabilize after 50 iterations, and the value of the coefficients is correctly estimated (the difference is approximately zero). Regarding the distorted time series, it converges faster, but the coefficients deviate from the real ones. In fact, adding noise contributes to decreasing the absolute value of the coefficients, i.e. the relationships between the time series become weakened.

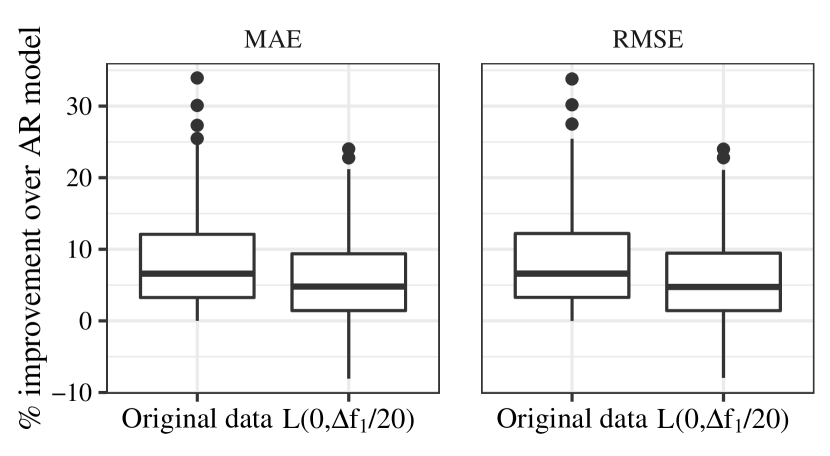

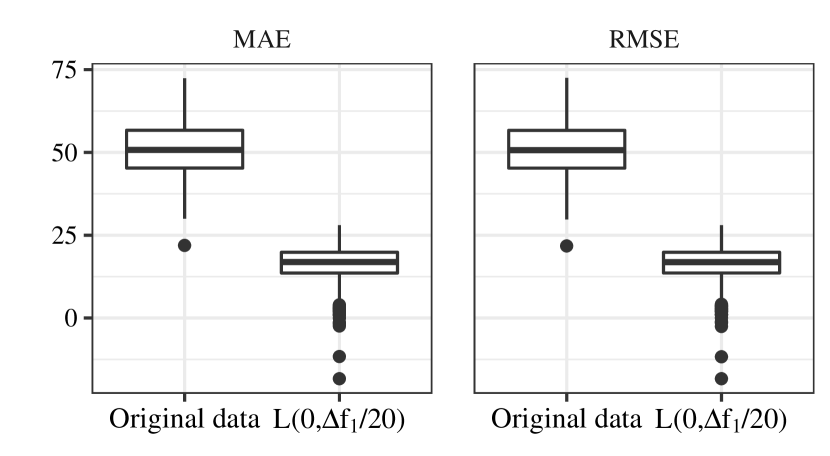

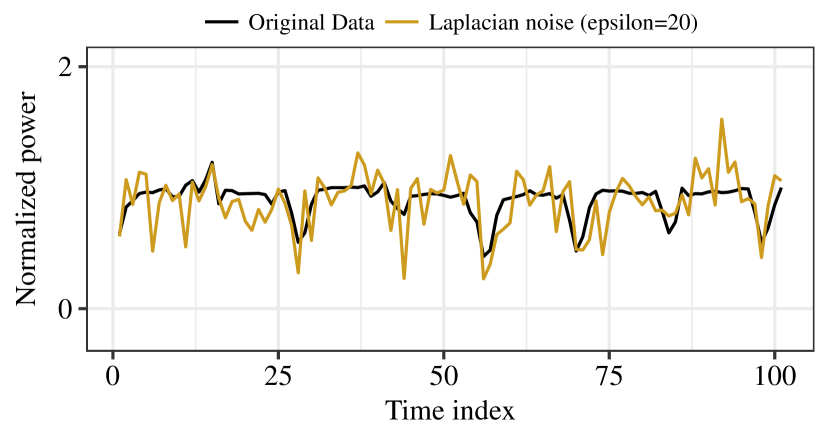

These experiments allow drawing some conclusions about the use of differential privacy. The Laplace distribution has advantageous properties, since it ensures -differential privacy when random noise follows . For the VAR with two data owners, since the observed values are in the interval . Therefore, when and when , meaning that the data still encompass much relevant information. Finally, to verify the impact of noise addition into forecasting performance, Figure 7 illustrates the improvement of each estimated VAR model (with and without noise addition) over the Autoregressive (AR) model estimated with original time series, in which collaboration is not used. This improvement is measured in terms of Mean Absolute Error (MAE) and Root Mean Squared Error (RMSE) values. Concerning the case with ten data owners, and when using data without noise, seven data owners improve their forecasting performance, which was expected from the coefficient matrix in Figure 4. When Laplacian noise is applied to the data, only one data owner (the first one) improves its forecasting skill (when compared to the AR model) by using the estimated VAR model. Even though the masked data continues to provide relevant information, the model obtained for the Laplacian noise performs worse than the AR model for the second data owner, making the VAR useless for the majority of the data owners.

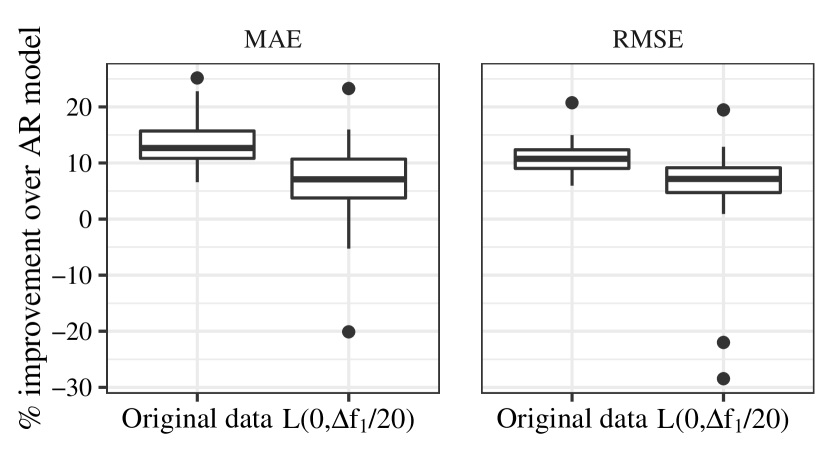

However, the results cannot be generalized for all VAR models, especially regarding the illustrated VAR, which is very close to the AR(3) model. Given that, a third experiment is proposed, in which 200 random coefficient matrices are generated for a stationary VAR and VAR following the algorithm proposed by Ansley & Kohn [1986]. Usually, the generated coefficient matrix has no null entries and the higher values are not necessarily found on diagonals. Figure 7 illustrates the improvement for each data owner when using a VAR model (with and without noise addition) over the AR model. In this case, the percentage of times the AR model performs better than the VAR model with distorted data is smaller, but the degradation of the models is still noticeable, especially in relation to the case with 10 data owners.

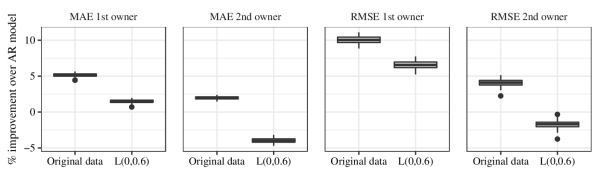

b) Real Data: The real dataset encompasses hourly time series of solar power generation from 44 micro-generation units located in Évora city (Portugal), covering the period from February 1, 2011 to March 6, 2013. As in Cavalcante & Bessa [2017], records corresponding to a solar zenith angle higher than 90∘ were removed, in order to take off nighttime hours (i.e., hours without any generation). Furthermore, and to make the time series stationary, a normalization of the solar power was applied by using a clear-sky model (see Bacher et al. [2009]) that gives an estimate of the solar power in clear sky conditions at any given time. The power generation for the next hour is modeled through the VAR model, which combines data from 44 data owners and considers 3 non-consecutive lags (1, 2 and 24h). Figure 8 (a) summarizes the improvement for the 44 PV power plants over the autoregressive model, in terms of MAE and RMSE. The quartile 25% allows concluding that MAE improves at least 10% for 33 of the 44 PV power plants, when data owners share their observed data. As to RMSE the improvement is not so significant, but is still greater than zero. Although the data obtained after Laplacian noise addition keeps its temporal dependency, as illustrated in Figure 8 (b), the corresponding VAR model is useless for 4 of the 44 data owners. When considering RMSE, 2 of the 44 data owners obtain better results by using an autoregressive model. Once again, the resulting model suffers a significant reduction in terms of forecasting capability.

3.3.2 Linear Algebra-based Protocols

Let us consider the case with two data owners. Since the multivariate least squares estimate for the VAR model with covariates and target is

| (52) | ||||

| (57) |

the data owners need to jointly compute , and .

As mentioned in the introduction of Section 2.2.1, the work of Du et al. [2004] proposes protocols for secure matrix multiplication for the situations where two data owners observe the same common target matrix and different confidential covariates. Unfortunately, without assuming a trusted third entity for generating random matrices, the proposed protocol fails when applied to the VAR model because values of the covariate matrix are included in the target matrix , which is also undisclosed. Additionally, has unique values instead of – see Figure 3.

Proposition 1

Consider the case in which two data owners, with private data and , want to estimate a VAR model without trusting a third entity, . Assume that the records are consecutive, as well as the lags. The multivariate least squares estimate for the VAR model with covariates and target requires the computation of , and .

If data owners use the protocol proposed by Du et al. [2004] for computing such matrices, then the information exchanged allows to recover data matrices.

Proof 1

As in Du et al. [2004], let us consider the case with two data owners without a third entity generating random matrices.

In order to compute both data owners define a matrix and compute its inverse . Then, the protocol defines that

requiring data owners to share and , respectively. This implies that each data owner shares values.

Similarly, the computation of implies that data owners define a matrix , and share and , respectively, providing new values. This means that Owner #2 receives and , i.e. values, and may recover which consists of values, representing a confidentiality breach. Furthermore, when considering a VAR model with lags, has unique values, meaning less values to recover. Analogously, Owner #1 may recover through the matrices shared for the computation of and .

Lastly, when considering a VAR with lags, only has values that are not in . Since, while computing , Owner #1 receives values from , a confidentiality breach can occur (in general ). In the same way, Owner #2 recovers when computing . \qed

The main disadvantage of the linear algebra-based methods is that they do not take into account that, in the VAR model, both target variables and covariates are private and that a large proportion of the covariates matrix is determined by knowing the target variables. This means that the data shared between data owners may be enough for competitors to be able to reconstruct the original data. For the method proposed by Karr et al. [2009], a consequence of such data is that the assumption may still provide a number of linearly independent equations on the other data owner’s data, which is enough for recovering their data.

3.3.3 ADMM Method and Central Node

The work of Zhang & Wang [2018] appears to be a promising approach for dealing with the problem of private data during the ADMM iterative process described by (47). Based on Zhang & Wang [2018], for each iteration , each data owner communicates their local results, , to the central node, . Then, the central node computes the intermediate matrices in (47b)-(47c) and returns the matrix to each data owner, in order to update in the next iteration, as seen in (47a). Figure 9 illustrates the methodology for the LASSO-VAR with three data owners. In this solution, there is no direct exchange of private data. However, as presented next, not only can the central node recover the original data, but also individual data owners can obtain a good estimation of the data used by the competitors.

Proposition 2

Proof 2

Using the notation of Section 3.1, each of the data owners is assumed to use the same number of lags to fit a LASSO-VAR model with a total number of records (keep in mind that , otherwise there will be more coefficients to be determined than system equations). At the end of iterations, the central node receives a total of values from each data owner , corresponding to , and does not know , corresponding to and , respectively, . Given that, the solution of the inequality

| (59) |

in , allows to infer that a confidentiality breach can occur at the end of

| (60) |

iterations, where denotes the ceiling function. Since tends to be large, tends to , which may represent a confidentiality breach if the number of iterations required for the algorithm to converge is greater than .\qed

Proposition 3

Proof 3

Without loss of generality, Owner #1 is considered the semi-trusted data owner — a semi-trusted data owner completes and shares his/her computations faithfully, but tries to learn additional information while or after the algorithm runs. For each iteration , this data owner receives the intermediate matrix , which provides values. However, Owner #1 does not know

which corresponds to values. However, since all the data owners know that and are defined by the expressions in (47b) and (47c), it is possible to perform some simplifications in which and becomes (62) and (63), respectively,

| (62) |

| (63) |

Therefore, the iterative process to find the competitors’ data proceeds as follows:

-

1.

Initialization: The central node generates , and the -th data owner generates , .

-

2.

Iteration #1: The central node receives and computes , returning which is returned for all data owners. At this point, Owner #1 receives values and does not know

and columns of , corresponding to values.

-

3.

Iteration #2: The central node receives and computes , returning for the data owners. At this point, only new estimations for the vectors were introduced in the system, which means more values to estimate.

As a result, at the end of iterations, Owner #1 has received corresponding to values and needs to estimate

and columns of , corresponding to . Then, the solution for the inequality

| (64) |

allows to infer that a confidentiality breach may occur at the end of

| (65) |

iterations. \qed

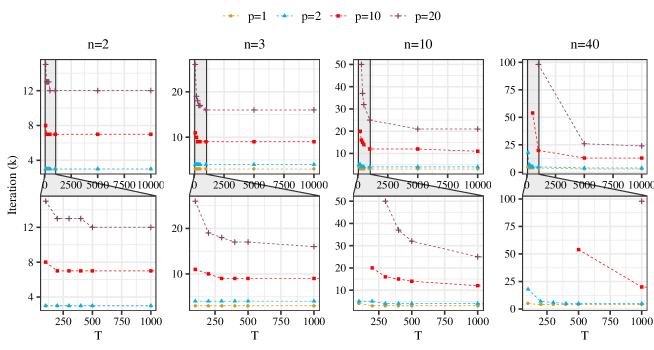

Figure 10 illustrates the value for different combinations of , , and . In general, the greater the number of records , the smaller the number of iterations necessary for confidentiality breach. That is because more information is shared during each iteration of the ADMM algorithm. On the other hand, the number of iterations until a possible confidentiality breach increases with the number of data owners (). The same is true for the number of lags ().

3.3.4 ADMM Method and Noise Mechanisms

The target matrix corresponds to the sum of private matrices , i.e.

| (66) |

where in cases where the entry (i, j) of is from -th data owner and otherwise.

Since the LASSO-VAR ADMM formulation is provided by (47), at iteration , data owners receive the intermediate matrix and then update their local solution through (47a). The combination of (62) with (66) allows to rewrite as

| (67) |

and, similarly, can be rewritten as

| (68) |

where

| (69) |

| (70) |

By analyzing (67) and (68), it is possible to verify that data owner only needs to share

| (71) |

for the computation of .

Let , , , , represent noise matrices generated according to the differential privacy framework. The noise mechanism could be introduced by

-

1.

adding noise to the data itself, i.e. replacing and by

(72) -

2.

adding noise to the estimated coefficients, i.e. replacing by

(73) -

3.

adding noise to the intermediate matrix (71),

(74)

The addition of noise to the data itself (72) was empirically analyzed in Subsection 3.3.1 and, as verified, confidentiality comes at the cost of model accuracy deterioration. The question is whether adding noise to the coefficients or intermediate matrix can ensure that data are not recovered at the end of a number of iterations.

Proposition 4

Consider noise addition in an ADMM-based framework by

Then, in both cases, a semi-trusted data owner can recover the data at the end of

| (75) |

iterations.

Proof 4

These statements are promptly deduced from the Proof presented for Proposition 3. Without loss of generality, Owner #1 is considered the semi-trusted data owner.

-

1.

Owner #1 can estimate , without distinguishing between and in (73), by recovering and . Let and , be the matrices , replacing by . Then, at iteration Owner #1 receives ( values) and does not know

which corresponds to values. As in Proposition 3, this means that, after iterations, Owner #1 has received values and needs to estimate

and columns of , corresponding to . Then, the solution for the inequality allows to infer that a confidentiality breach may occur at the end of

iterations.

-

2.

Since Owner #1 can estimate by recovering data, adding noise to the intermediate matrix reduces to the case of adding noise to the coefficients, in (i), because Owner #1 can rewrite (74) as

\qed(76)

4 Discussion

| Split by features | Split by records | ||

|---|---|---|---|

| Data Transformation | Mangasarian [2011] | Mangasarian [2012], Yu et al. [2008], Dwork et al. [2014] | |

| Secure Multi-party Computation |

Linear

Algebra |

Du et al. [2004], Karr et al. [2009], Zhu et al. [2015], Fan & Xiong [2014]*, Soria-Comas et al. [2017] | Zhu et al. [2015], Aono et al. [2017] |

| Homomorphic-cryptography | Yang et al. [2019], Hall et al. [2011], Gascón et al. [2017], Slavkovic et al. [2007] | Yang et al. [2019], Hall et al. [2011], Nikolaenko et al. [2013], Chen et al. [2018], Jia et al. [2018], Slavkovic et al. [2007] | |

| Decomposition-based Methods | Pure | Pinson [2016], Zhang & Wang [2018] | Wu et al. [2012], Lu et al. [2015], Ahmadi et al. [2010], Mateos et al. [2010] |

|

Linear

Algebra |

Li et al. [2015], Han et al. [2010] | Zhang & Zhu [2017], Huang et al. [2019], Zhang et al. [2018] | |

| Homomorphic-cryptography | Yang et al. [2019], Li & Cao [2012]*, Liu et al. [2018]*, Li et al. [2018]*, Fienberg et al. [2009], Mohassel & Zhang [2017] | Yang et al. [2019], Zhang et al. [2019], Fienberg et al. [2009], Mohassel & Zhang [2017] | |

| * secure data aggregation. | |||

Table 1 summarizes the methods from the literature. These algorithms for the privacy-preserving ought to be carefully built and consider two key components: (i) how data is distributed between data owners, and (ii) the statistical model used. The decomposition-based methods are very sensitive to data partition, while data transformation and cryptography-based methods are very sensitive to problem structure, with the exception of the differential privacy methods, which simply add random noise, from specific probability distributions, to the data itself. This property makes these methods appealing, but differential privacy usually involves a trade-off between accuracy and privacy.

Cryptography-based methods are usually more effective against confidentiality breaches, but they have some disadvantages: (i) some of them require a third-party for keys generation, as well as external entities to perform the computations in the encrypted domain; (ii) challenges in the scalability and implementation efficiency, which are mostly due to the high computational complexity and overhead of existing homomorphic encryption schemes [Hoogh, 2012, Zhao et al., 2019, Tran & Hu, 2019]. Regarding some protocols, such as secure multi-party computation through homomorphic cryptography, communication complexity grows exponentially with the number of records [Rathore et al., 2015].

Data transformation methods do not affect the computational time for training the model, since each data owner transforms his/her data before the model fitting process. The same is true for the decomposition-based methods in which data is split by data owners. The secure multi-party protocols have the disadvantage of transforming the information while fitting the statistical model, which implies a higher computational cost.

As already mentioned, the main challenge to the application of the existent privacy-preserving algorithms in the VAR model is the fact that and share a high percentage of values, not only during the fitting of the statistical model but also when using it to perform forecasts. A confidentiality breach may occur during the forecasting process if, after the model is estimated, the algorithm to maintain privacy provides the coefficient matrix for all data owners. When using the estimated model to perform forecasts, assuming that each -th data owner sends their own contribution for the time series forecasting to every other -th data owner:

-

1.

In the LASSO-VAR models with one lag, since -th data owner sends for -th data owner, the value may be directly recovered when the coefficient is known by all data owners, being the coefficient associated with lag of time series , to estimate .

-

2.

In the LASSO-VAR models with consecutive lags, the forecasting of a new timestamp only requires the introduction of one new value in the covariate matrix of the -th data owner. In other words, at the end of timestamps, the -th data owner receives the values. However, there are values that the data owner does not know about. This may represent a confidentiality breach since a semi-trusted data owner can assume different possibilities for the initial values and then generate possible trajectories.

-

3.

In the LASSO-VAR models with non-consecutive lags, , at the end of timestamps, only one new value is introduced in the covariate matrix, meaning that the model is also subject to a confidentiality breach.

Therefore, and considering the issue of data naturally split by features, it would be more advantageous to apply decomposition-based methods, since the time required for model fitting is not affected by data transformations and each data owner only has access to their own coefficients. However, with the state-of-the-art approaches, it is difficult to guarantee that these techniques can indeed offer a robust solution for data privacy when addressing data split by features. Finally, a remark about some specific business applications of VAR, where data owners know exactly some past values of the competitors. For example, consider a VAR model with lags , 2 and 24, which predicts the production of solar plants. Then, when forecasting the first sunlight hour of a day, all data owners will know that the previous lags 1 and 2 have zero production (no sunlight). Irrespective of whether the coefficients are shared or not, a confidentiality breach may occur. For these special cases, the estimated coefficients cannot be used for a long time horizon, and online learning may represent an efficient alternative.

The privacy issues analyzed in this paper are not restricted to the VAR model nor to point forecasting tasks. Probabilistic forecasts, using data from different data owners (or geographical locations), can be generated with splines quantile regression [Tastu et al., 2013], component-wise gradient boosting [Bessa et al., 2015b], a VAR that estimates the location parameter (mean) of data transformed by a logit-normal distribution [Dowell & Pinson, 2015], linear quantile regression with LASSO regularization [Agoua et al., 2018], among others. These are some examples of collaborative probabilistic forecasting methods. However, none of them considers the confidentiality of the data. Moreover, the method proposed by Dowell & Pinson [2015] can be influenced by the confidentiality breaches discussed thorough this paper, since the VAR model is directly used to estimate the mean of transformed data from the different data owners. On the other hand, when performing non-parametric models such as quantile regression, each quantile is estimated by solving an independent optimization problem, which means that the risk of a confidentiality breach increases with the number of quantiles being estimated. Note that quantile regression-based models may be solved through the ADMM method [Zhang et al., 2019]. However, as discussed in Section 2.3, the semi-trusted agent may collect enough information to infer the confidential data. The quantile regression method may also be estimated by applying linear programming algorithms [Agoua et al., 2018], which may be solved through homomorphic encryption, despite being computationally demanding for high-dimensional multivariate time series.

5 Conclusion

This paper presents a critical overview of the literature techniques used to handle privacy issues in collaborative forecasting methods. In addition, it also performs an analysis to their application to the VAR model. The aforementioned existing techniques are divided into three groups of approaches to guarantee privacy: data transformation, secure multi-party computation and decomposition of the optimization problem into sub-problems.

For each group, several points can be concluded. Starting with data transformation techniques, two remarks were made. The first one concerns the addition of random noise to the data. While the algorithm is simple to apply, this technique demands a trade-off between privacy and the correct estimation of the model’s parameters [Yang et al., 2019]. In our experiments, there was a clear model degradation even though the data kept its original behavior (Section 3.3.1). The second relates to the multiplication by a random matrix that is kept undisclosed. Ideally, and in what concerns data where different data owners observe different variables, this secret matrix would post-multiply data, thus enabling each data owner to generate a few lines of this matrix. However, as demonstrated in equation (8) of Section 2.1.2, this transformation does not preserve the estimated coefficients, and the reconstruction of the original model may require sharing the matrices used to encrypt the data, thus exposing the original data.

The second group of techniques, secure multi-party computations, introduce privacy in the intermediate computations by defining the protocols for addition and multiplication of the private datasets, without confidentiality breaches using either linear algebra or homomorphic encryption methods. For independent records, data confidentiality is guaranteed for (ridge) linear regression through linear algebra-based protocols; not only do records need to be independent, but some also require that the target variable is known by all data owners. These assumptions might prevent their application when covariates and target matrices share a large proportion of values – in the VAR model case, for instance. This means that shared data between agents might be enough for competitors to be able to reconstruct the data. Homomorphic cryptography methods might result in computationally demanding techniques since each dataset value has to be encrypted. The discussed protocols ensure privacy-preserving while using (ridge) linear regression if there are two entities that correctly performs the protocol without agent collusion. These entities are an external server (e.g., a cloud server) and an entity which generates the encryption keys. In some approaches, all data owners know the coefficient matrix at the end of the model estimation. This is a disadvantage when applying models in which covariates include the lags of the target variable because confidentiality breaches may occur during the forecasting phase.

Finally, the decomposition of the optimization problem into sub-problems (which can be solved in parallel) have all the desired properties for a collaborative forecasting problem, since each data owner only estimates their coefficients. A common assumption of such methods is that the objective function is decomposable. However, these approaches consist in iterative processes that require sharing intermediate results for the next update, meaning that each new iteration conveys more information about the secret datasets to the data owners, possibly breaching data confidentiality.

Acknowledgements

The research leading to this work is being carried out as part of the Smart4RES project (European Union’s Horizon 2020, No. 864337). Carla Gonçalves was supported by the Portuguese funding agency, FCT (Fundação para a Ciência e a Tecnologia), within the Ph.D. grant PD/BD/128189/2016 with financing from POCH (Operational Program of Human Capital) and the EU. The sole responsibility for the content lies with the authors. It does not necessarily reflect the opinion of the Innovation and Networks Executive Agency (INEA) or the European Commission (EC), which are not responsible for any use that may be made of the information it contains.

Appendix A Differential Privacy

Mathematically, a randomized mechanism satisfies (,)-differential privacy [Dwork & Smith, 2009] if, for every possible output of and for every pair of datasets and (differing in at most one record),

| (77) |

In practice, differential privacy can be achieved by adding random noise to some desirable function of the data , i.e

| (78) |

The (,0)-differential privacy is achieved by applying noise from Laplace distribution with scale parameter , with . A common alternative is the Gaussian distribution but, in this case, and the scale parameter which allows (,)-differential privacy is . Dwork & Smith [2009] showed that the data can be masked by considering

| (79) |

Appendix B Supplementary Data and Code

Supplementary material related to this article is available online (https://doi.org/10.25747/gywm-9457). The available material includes:

-

1.

admm_functions.R: R script with ADMM algorithm implementation.

-

2.

clear_sky_functions.R: R script to estimate clear-sky solar power generation with the model described in Bacher et al. [2009].

-

3.

coef_generator.R: R script with the functions for generating VAR model coefficients, according to the implementation in [Virolainen, 2020].

-

4.

run_experiments.R: R script with the commands for generating the results of Section 3.3.1.

-

5.

c_sky.csv: estimated clear-sky solar power generation.

-

6.

normalized_PVdata.csv: normalized (with clear-sky model) solar power time series data.

-

7.

PVdata.csv: solar power time series data.

References

- Agarwal et al. [2019] Agarwal, A., Dahleh, M., & Sarkar, T. (2019). A marketplace for data: An algorithmic solution. In Proceedings of the 2019 ACM Conference on Economics and Computation (pp. 701–726).

- Agoua et al. [2018] Agoua, X. G., Girard, R., & Kariniotakis, G. (2018). Probabilistic models for spatio-temporal photovoltaic power forecasting. IEEE Transactions on Sustainable Energy, 10, 780–789.

- Ahmad et al. [2016] Ahmad, H. W., Zilles, S., Hamilton, H. J., & Dosselmann, R. (2016). Prediction of retail prices of products using local competitors. International Journal of Business Intelligence and Data Mining, 11, 19–30.

- Ahmadi et al. [2010] Ahmadi, H., Pham, N., Ganti, R., Abdelzaher, T., Nath, S., & Han, J. (2010). Privacy-aware regression modeling of participatory sensing data. In Proceedings of the 8th ACM Conference on Embedded Networked Sensor Systems (pp. 99–112). ACM.

- Ansley & Kohn [1986] Ansley, C. F., & Kohn, R. (1986). A note on reparameterizing a vector autoregressive moving average model to enforce stationarity. Journal of Statistical Computation and Simulation, 24, 99–106.

- Aono et al. [2017] Aono, Y., Hayashi, T., Phong, L. T., & Wang, L. (2017). Input and output privacy-preserving linear regression. IEICE TRANSACTIONS on Information and Systems, 100, 2339–2347.

- Aviv [2003] Aviv, Y. (2003). A time-series framework for supply-chain inventory management. Operational Research, 51, 175–342.

- Aviv [2007] Aviv, Y. (2007). On the benefits of collaborative forecasting partnerships between retailers and manufacturers. Management Science, 53, 777–794.

- Bacher et al. [2009] Bacher, P., Madsen, H., & Nielsen, H. A. (2009). Online short-term solar power forecasting. Solar Energy, 83, 1772–1783.

- Bessa et al. [2015a] Bessa, R., Trindade, A., & Miranda, V. (2015a). Spatial-temporal solar power forecasting for smart grids. IEEE Transactions on Industrial Informatics, 11, 232–241.

- Bessa et al. [2018] Bessa, R. J., Rua, D., Abreu, C., Machado, P., Andrade, J. R., Pinto, R., Gonçalves, C., & Reis, M. (2018). Data economy for prosumers in a smart grid ecosystem. In Proceedings of the Ninth International Conference on Future Energy Systems (pp. 622–630). ACM.

- Bessa et al. [2015b] Bessa, R. J., Trindade, A., Silva, C. S., & Miranda, V. (2015b). Probabilistic solar power forecasting in smart grids using distributed information. International Journal of Electrical Power & Energy Systems, 72, 16–23.

- Boyd et al. [2011] Boyd, S., Parikh, N., Chu, E., Peleato, B., Eckstein, J. et al. (2011). Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends® in Machine learning, 3, 1–122.