Vayanos, Georghiou, Yu

Robust Optimization with Decision-Dependent Information Discovery

Robust Optimization with

Decision-Dependent Information Discovery

Phebe Vayanos \AFFUniversity of Southern California, Center for Artificial Intelligence in Society, \EMAILphebe.vayanos@usc.edu \AUTHORAngelos Georghiou \AFFUniversity of Cyprus, Department of Business and Public Administration, \EMAILgeorghiou.angelos@ucy.ac.cy \AUTHORHan Yu \AFFUniversity of Southern California, Center for Artificial Intelligence in Society, \EMAILhyu376@usc.edu

Robust optimization (RO) is a popular paradigm for modeling and solving two- and multi-stage decision-making problems affected by uncertainty. In many real-world applications, such as R&D project selection, production planning, or preference elicitation for product or policy recommendations, the time of information discovery is decision-dependent and the uncertain parameters only become observable after an often costly investment. Yet, most of the literature on robust optimization assumes that the uncertain parameters can be observed for free and that the sequence in which they are revealed is independent of the decision-maker’s actions. To fill this gap in the practicability of RO, we consider two- and multi-stage robust optimization problems in which part of the decision variables control the time of information discovery. Thus, information available at any given time is decision-dependent and can be discovered (at least in part) by making strategic exploratory investments in previous stages. We propose a novel dynamic formulation of the problem and prove its correctness. We leverage our model to provide a solution method inspired from the -adaptability approximation, whereby candidate strategies for each decision stage are chosen here-and-now and, at the beginning of each period, the best of these strategies is selected after the uncertain parameters that were chosen to be observed are revealed. We reformulate the problem as a finite mixed-integer (resp. bilinear) program if none (resp. some of the) decision variables are real-valued. This finite program is solvable with off-the-shelf solvers. We generalize our approach to the minimization of piecewise linear convex functions. We demonstrate the effectiveness of our method in terms of interpretability, optimality, and speed on synthetic instances of the Pandora box problem, the preference elicitation problem with real-valued recommendations, the best box problem, and the R&D project portfolio optimization problem. Finally, we evaluate it on an instance of the active preference elicitation problem used to recommend kidney allocation policies to policy-makers at the United Network for Organ Sharing based on real data from the U.S. Kidney Allocation System.

robust optimization, endogenous uncertainty, decision-dependent information discovery, Pandora box problem, R&D project portfolio selection, preference elicitation, kidney allocation.

1 Introduction

1.1 Background & Motivation

Over the last two decades, robust optimization has emerged as a popular approach for decision-making under uncertainty in both single- and multi-stage settings, see e.g., Ben-Tal et al. (2009), Ben-Tal and Nemirovski (2000), Ben-Tal and Nemirovski (1999), Ben-Tal and Nemirovski (1998), Bertsimas et al. (2004), Bertsimas and Sim (2004), Ben-Tal et al. (2004), Bertsimas et al. (2011), Zhen et al. (2018), Vayanos et al. (2012), Bertsimas and Goyal (2012), Xu and Burer (2018). In multi-stage models, the uncertain parameters are revealed sequentially as time progresses and the decisions are allowed to depend on all the information made available in the past. Mathematically, decisions are modeled as functions of the history of observations, thus capturing the adaptive and non-anticipative nature of the decision process.

Most models and solution approaches in multi-stage robust optimization are tailored to problems where the uncertain parameters are exogenous, being independent of the decision-maker’s actions. In particular, they assume that uncertainties can be observed for free and that the sequence in which they are revealed cannot be influenced by the decision-maker. Yet, these assumptions fail to hold in many real-world applications where the time of information discovery is decision-dependent and the uncertain parameters only become observable after an often costly investment. Mathematically, some binary measurement (or observation) decisions control the time of information discovery and the non-anticipativity requirements depend upon these decisions, severely complicating solution.

1.1.1 Motivating Applications.

We now detail several applications areas where the time of revelation of the uncertain parameters is decision-dependent.

R&D Project Portfolio Optimization.

Research and development firms typically maintain long pipelines of candidate projects whose returns are uncertain, see Solak et al. (2010). For each project, the firm can decide whether and when to start it and the amount of resources to be allocated to it. The return of each project will only be revealed once the project is completed. Thus, project start times and resource allocation decisions impact the time of information discovery in this problem.

Clinical Trial Planning.

Pharmaceutical companies typically maintain long R&D pipelines of candidate drugs, see e.g., Colvin and Maravelias (2008). Before any drug can reach the marketplace it needs to pass a number of costly clinical trials whose outcome (success/failure) is uncertain and will only be revealed after the trial is completed. Thus, the decisions to proceed with a trial control the time of information discovery in this problem.

Offshore Oilfield Exploitation.

Offshore oilfields consist of several reservoirs of oil whose volume and initial deliverability (maximum initial extraction rate) are uncertain, see e.g., Jonsbråten (1998), Goel and Grossman (2004), and Vayanos et al. (2011). While seismic surveys can help estimate these parameters, current technology is not sufficiently advanced to obtain accurate estimates. In fact, the volume and deliverability of each reservoir only become precisely known if a very expensive oil platform is built at the site and the drilling process is initiated. Thus, the decisions to build a platform and drill into a reservoir control the time of information discovery in this problem.

Production Planning.

Manufacturing companies can typically produce a large number of different items. For each type of item, they can decide whether and how much to produce to satisfy their demand given that certain items are substitutable, see e.g. Jonsbråten et al. (1998). The production cost of each item type is unknown and will only be revealed if the company chooses to produce the item. Thus, the decisions to produce a particular type of item control the time of information discovery in this problem.

Active Preference Elicitation.

Preference elicitation refers to the problem of developing a decision support system capable of generating recommendations to a user, thus assisting in decision making. In active preference elicitation, one can ask users a (typically limited) number of questions from a potentially large set before making a recommendation, see e.g., Vayanos et al. (2021). The answers to the questions are initially unknown and will only be revealed if the particular question is asked. Thus, the choices of questions to ask control the time of information discovery in this problem.

1.2 Literature Review

Decision-Dependent Information Discovery.

Our paper relates to research on optimization problems affected by uncertain parameters whose time of revelation is decision-dependent and which originates in the literature on stochastic programming. The vast majority of these works assumes that the uncertain parameters are discretely distributed. In such cases, the decision process can be modeled by means of a finite scenario tree whose branching structure depends on the binary measurement decisions that determine the time of information discovery. This research began with the works of Jonsbråten et al. (1998) and Jonsbråten (1998). Jonsbråten et al. (1998) consider the case where all measurement decisions are made in the first stage and propose a solution approach based on an implicit enumeration algorithm. Jonsbråten (1998) generalizes this enumeration-based framework to the case where measurement decisions are made over time. More recently, Goel and Grossman (2004) showed that stochastic programs with discretely distributed uncertain parameters whose time of revelation is decision-dependent can be formulated as deterministic mixed-binary programs whose size is exponential in the number of endogenous uncertain parameters. To help deal with the “curse of dimensionality,” they propose to precommit all measurement decisions, i.e., to approximate them by here-and-now decisions, and to solve the multi-stage problem using either a decomposition technique or a folding horizon approach. Later, Goel and Grossman (2006), Goel et al. (2006), and Colvin and Maravelias (2010) propose optimization-based solution techniques that truly account for the adaptive nature of the measurement decisions and that rely on branch-and-bound and branch-and-cut approaches, respectively. Accordingly, Colvin and Maravelias (2010) and Gupta and Grossmann (2011) have proposed iterative solution schemes based on relaxations of the non-anticipativity constraints for the measurement variables. Our paper most closely relates to the work of Vayanos et al. (2011), wherein the authors investigate two- and multi-stage stochastic and robust programs with decision-dependent information discovery that involve continuously distributed uncertain parameters. They propose a decision-rule based approximation approach that relies on a prepartitioning of the support of the uncertain parameters. Since this approach applies in our context, we will benchmark against it in our experiments.

Robust Optimization with Decision-Dependent Uncertainty Sets.

Our work also relates to the literature on robust optimization with uncertainty sets parameterized by the decisions. Such problems capture the ability of the decision-maker to influence the set of possible realizations of the uncertain parameters and have been investigated by Spacey et al. (2012), Nohadani and Sharma (2018), Nohadani and Roy (2017), Zhang et al. (2017), and Bertsimas and Vayanos (2017). These models do not apply in our context since they do not capture the ability of the decision-maker to influence the information available. In particular, the problems investigated by Spacey et al. (2012), Nohadani and Sharma (2018), and Nohadani and Roy (2017) are all single-stage, while problems with decision-dependent information discovery are inherently sequential in nature.

Robust Optimization with Binary Adaptive Variables.

Two-stage, and to a lesser extent also multi-stage, robust binary optimization problems have received considerable attention in the recent years. One stream of works proposes to restrict the functional form of the recourse decisions to functions of benign complexity, see Bertsimas and Dunn (2017) and Bertsimas and Georghiou (2015, 2018). A second stream of work relies on partitioning the uncertainty set into finite sets and applying constant decision rules on each partition, see Vayanos et al. (2011), Bertsimas and Dunning (2016), Postek and Den Hertog (2016), Bertsimas and Vayanos (2017). The last stream of work investigates the so-called -adaptability counterpart of two-stage problems, see Bertsimas and Caramanis (2010), Hanasusanto et al. (2015), Subramanyam et al. (2020), Chassein et al. (2019), and Rahmattalabi et al. (2019). In this approach, candidate policies are chosen here-and-now and the best of these policies is selected after the uncertain parameters are revealed. Most of these papers assume that the uncertain parameters are exogenous in the sense that they are independent of the decision-maker’s actions. Our paper most closely relates to the works of Bertsimas and Caramanis (2010) and Hanasusanto et al. (2015). It generalizes and subsumes the approach from Hanasusanto et al. (2015) to problems with decision-dependent information discovery, to multi-stage problems, and to problems with piecewise linear convex objective.

Stochastic Probing.

Our paper also fits in a line of work on stochastic probing in the computer science literature, see Gupta et al. (2016, 2017) and Singla (2018). Here, the problem consists of a set of elements with uncertain value whose distribution is known but whose realization becomes observable only after the element is probed. However, probing is costly (incurs a cost or consumes budget) and irrevocable and the goal is to choose the set of elements to probe and the order in which to probe them to maximize profit (e.g., the value of the item with the highest value that has been probed). Concrete examples include the best box problem and the Pandora box problem, see e.g., Singla (2018). The techniques presented in this stream of work do not apply to the case where the distributions are unknown, to general optimization problems with decision-dependent information discovery, nor to problems with general, potentially uncertain, constraints.

Worst-Case Regret Optimization.

Finally, our work relates to two-stage worst-case absolute regret minimization problems, see e.g., Assavapokee et al. (2008b, a), Zhang (2011), Jiang et al. (2013), Ng (2013), Chen et al. (2014), Ning and You (2018), and Poursoltani and Delage (2019). To the best of our knowledge, our paper is the first to investigate worst-case regret minimization problems in the presence of uncertain parameters whose time of revelation is decision-dependent.

1.3 Proposed Approach and Contributions

We now summarize our approach and main contributions in this paper:

-

(a)

We consider general two- and multi-stage robust optimization problems with decision-dependent information discovery. These encompass as special cases the R&D project portfolio optimization problem, the Pandora box problem (which can be used to model job candidate selection and house hunting, among others), the active preference elicitation problem, and many more. To the best of our knowledge, only one other paper in the literature studies such problems in the robust optimization setting. We propose novel “min-max-min-max-…-min-max” reformulations of these problems and prove correctness of our formulations. These reformulations unlock new approximate (and potentially also exact) solution approaches for addressing problems with decision-dependent information discovery.

-

(b)

We leverage our new reformulations to propose a solution approach based on the -adaptability approximation, wherein candidate strategies are chosen here-and-now and the best of these strategies is selected after the uncertain parameters that were chosen to be observed are revealed. This approximation allows us to control the trade-off between complexity and solution quality by tuning a single design parameter, . We propose practicable reformulations of the -adaptability counterpart of problems with decision-dependent information discovery in the form of moderately sized finite programs solvable with off-the shelf solvers. These programs can be written equivalently as mixed-binary linear programs if all decision-variables are binary. Our reformulations subsume those from the literature that apply only to two-stage problems with exogenous uncertain parameters.

-

(c)

We generalize the -adaptability approximation scheme to multi-stage problems and to problems with piecewise linear convex objective function. The piecewise linear convex objective enables us, among others, to address worst-case absolute regret minimization problems. These generalizations and associated algorithm that we provide apply also to problems with exogenous uncertain parameters.

-

(d)

We perform a wide array of experiments on the R&D project portfolio selection problem, the preference elicitation problem with real-valued recommendations, the best box selection problem, Pandora’s box problem, and the preference elicitation problem. We show that our proposed approach outperforms the state-of-the-art in the literature in terms of interpretability, optimality, and speed. Indeed, our approach reduces the number of subsets in the recourse strategy by a factor of 3, improves the quality of the returned solution by a factor of 1.9, and results in an 8.5 speed-up. We perform a case study showcasing the benefits of our approach on real data from the U.S. Kidney Allocation System (KAS) to recommend policies that meet the needs of policy-makers at the Organ Procurement and Transplantation Network (OPTN) and the United Network for Organ Sharing (UNOS), the lead agency in charge of allocating organs for transplantation in the United States.111See https://www.srtr.org, https://optn.transplant.hrsa.gov, and https://unos.org.

1.4 Organization of the Paper and Notation

The paper is organized as follows. Sections 2 and 3 introduce two-stage robust optimization problems with exogenous uncertainty and with decision-dependent information discovery (DDID), respectively. In particular, Section 3 introduces our novel formulation. Section 4 proposes reformulations of the -adaptability counterparts of problems with DDID as finite programs solvable with off-the-shelf solvers. Section 5 generalizes the -adaptability approximation to problems with piecewise linear convex objective and proposes an efficient solution procedure. Section 6 generalizes the -adaptability approximation to multi-stage problems. Section 7 presents computational results on synthetic instances of the two-stage R&D project portfolio optimization problem, the two-stage best box selection problem, and the multi-stage Pandora’s box problem. Finally, Section 8 formulates the preference elicitation problem for learning the preferences of policy-makers at the OPTN/UNOS as a two-stage robust problem with decision-dependent information discovery, and presents numerical results on real data from the U.S. Kidney Allocation System. The proofs of all statements can be found in the Electronic Companion to the paper. Proposed extensions to our methods, algorithms, and speed-up strategies are also deferred to the Electronic Companion.

Notation.

Throughout this paper, vectors (matrices) are denoted by boldface lowercase (uppercase) letters. The th element of a vector () is denoted by . Scalars are denoted by lowercase letters, e.g., or . For a matrix , we let denote the th row of , written as a column vector. We let denote the space of all functions from to . Accordingly, we denote by the spaces of all functions from to . Given two vectors of equal length, , , we let denote the Hadamard product of the vectors, i.e., their element-wise product. With a slight abuse of notation, we may use the maximum and minimum operators even when the optimum may not be attained; in such cases, the operators should be understood as suprema and infima, respectively. We use the convention that a decision is feasible for a minimization problem if and only if it attains an objective that is . Finally, for a logical expression , we define the indicator function as if is true and 0 otherwise.

2 Two-Stage RO with Exogenous Uncertainty

To motivate our formulation from Section 3, we introduce two equivalent models of two-stage robust optimization with exogenous uncertainty from the literature and discuss their relative merits.

In two-stage robust optimization with exogenous uncertainty, first-stage (or here-and-now) decisions are made today, before any of the uncertain parameters are observed. Subsequently, all of the uncertain parameters are revealed. Finally, once the realization of has become available, second-stage (or wait-and-see) decisions are selected. We assume that the uncertainty set is a non-empty bounded polyhedron expressible as for some matrix and vector . As the decisions are selected after the uncertain parameters are revealed, they are allowed to adapt or adjust to the realization of . In the literature, there are two formulations of generic two-stage robust problem with exogenous uncertainty: they differ in the way in which the ability of to adapt to is modeled.

Decision Rule Formulation.

In the first model, one optimizes today over both the here-and-now decisions and over recourse actions to be taken in each realization of . The decision is modeled as a function (or decision rule) of that is selected today, along with . Under this paradigm, a two-stage linear robust problem with exogenous uncertainty is expressible as:

| (1) |

where , , , , and . We assume that the objective function and right hand-sides are linear in . We can account for affine dependencies on by introducing an auxiliary uncertain parameter restricted to equal unity.

Min-Max-Min Formulation.

In the second model, only is selected today and the recourse decisions are optimized explicitly, in a dynamic fashion, after nature is done making a decision. Under this model, a two-stage robust problem with exogenous uncertainty is expressible as:

| (2) |

Problems (1) and (2) are equivalent, see e.g., Shapiro (2017). However, each of them has proved successful in different contexts. Problem (1) has been the building block of most of the literature on the decision rule approximation, see Section 1. Problem (2) has enabled the advent and tremendous success of the -adaptability approximation approach to two-stage robust problems with binary recourse, see Bertsimas and Caramanis (2010), Hanasusanto et al. (2015). It has also facilitated the development of algorithms and efficient solution schemes, see e.g., Zeng and Zhao (2013), Ayoub and Poss (2016), and Bertsimas and Shtern (2018).

3 Two-Stage RO with Decision-Dependent Information Discovery

In this section, we describe two-stage robust optimization problems with decision-dependent information discovery (DDID) and propose an entirely new modeling framework for studying such problems. This framework underpins our ability to generalize the popular -adaptability approximation approach from the literature to problems affected by uncertain parameters whose time of revelation is decision-dependent, see Sections 4.1 and 4.2.

3.1 Problem Description

In two-stage robust optimization with DDID, the uncertain parameters do not necessarily become observed (for free) between the first and second decision-stages. Instead, some (typically costly) first stage decisions control the time of information discovery in the problem: they decide whether (and which of) the uncertain parameters will be revealed before the wait-and-see decisions are selected. If the decision-maker chooses to not observe some of the uncertain parameters, then those parameters will still be uncertain at the time when the decision is selected, and will only be allowed to depend on the portion of the uncertain parameters that have been revealed. On the other hand, if the decision-maker chooses to observe all of the uncertain parameters, then there will be no uncertainty in the problem at the time when is selected, and will be allowed to depend on all uncertain parameters.

In order to allow for endogenous uncertainty, we introduce a here-and-now binary measurement (or observation) decision vector of the same dimension as whose th element is 1 if and only if we choose to observe between the first and second decision stages. In the presence of such endogenous uncertain parameters, the recourse decisions are selected after the portion of uncertain parameters that was chosen to be observed is revealed. In particular, must be constant in (i.e., robust to) those uncertain parameters that remain unobserved at the second decision-stage. The requirement that only depend on the uncertain parameters that have been revealed at the time it is chosen is termed non-anticipativity. In the presence of uncertain parameters whose time of revelation is decision-dependent, this requirement translates to decision-dependent non-anticipativity constraints.

3.2 Decision Rule Formulation

In the literature and to the best of our knowledge, two-stage robust optimization problems with DDID have been formulated (in a manner paralleling Problem (1)) by letting the recourse decisions be functions of and requiring that those functions be constant in if , see Vayanos et al. (2011). Under this (decision rule based) modeling paradigm, generic two-stage robust optimization problems with decision-dependent information discovery take the form

| (3) |

where , , , and the remaining data elements are as in Problem (1). The set can encode requirements on the measurement decisions. For example, it can enforce that a given uncertain parameter may only be observed if another uncertain parameter has been observed using . Accordingly, it can postulate that the total number of uncertain parameters that are observed does not exceed a certain budget using . If only some (or all) of the uncertain parameters have a time of information discovery that is exogenous, our models and solution approaches can be used by restricting the observation decisions to equal 1 (resp. 0) for each exogenous uncertain parameter that is (resp. is not) observed between the first and second decision stages. These restrictions can be conveniently added as constraints to the set . The last constraint in the problem is a decision-dependent non-anticipativity constraint: it ensures that the function is constant in the uncertain parameters that remain unobserved at the second stage. Indeed, the identity evaluates to true only if the elements of and that were observed are indistinguishable, in which case the decisions taken in scenarios and must be equal. We omit joint (first stage) constraints on and to minimize notational overhead but emphasize that our approach remains applicable in their presence.

Note that Problem (3) generalizes Problem (1). Indeed, if we set , , and in Problem (3), we recover Problem (1). In addition, it generalizes the single-stage robust problem: if we set in Problem (3), all uncertain parameters are revealed after the second stage so that the second stage decisions are forced to be static (i.e., constant in ).

To the best of our knowledge, the only approach in the literature for (approximately) solving problems of type (3) is presented in Vayanos et al. (2011) and relies on a decision rule approximation. The authors propose to approximate the binary (resp. continuous) wait-and-see decisions by functions that are piecewise constant (resp. piecewise linear) on a pre-selected partition of the uncertainty set of the form where and represent breakpoints along the axis. Unfortunately, as the following example illustrates, this approach is highly sensitive to the choice of breakpoint configuration.

Example 3.1

Consider the following instance of Problem (3)

| (4) |

where . The inequality constraints in the problem combined with the requirement that be binary imply that we must have (resp. 0) whenever (resp. ). Thus, from the decision-dependent non-anticipativity constraints, the only feasible choice for is . It is easy to show that if and if we uniformly partition each axis iteratively in 2, 3, 4, etc. subsets, then 1999 breakpoints along each direction will need to be introduced before reaching a feasible (and thus optimal) solution. The associated problem will involve over binary decision variables and constraints. In contrast, as will become clear later on, our proposed solution approach with approximation parameter will be optimal in this case.\Halmos

3.3 Proposed Min-Max-Min-Max Formulation

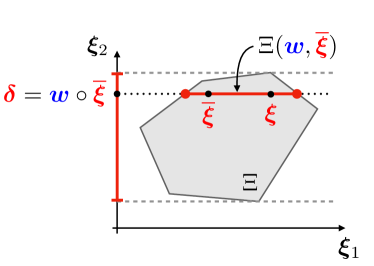

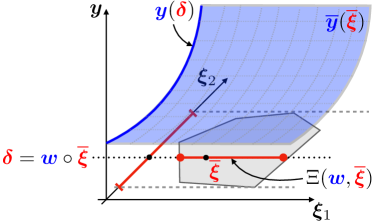

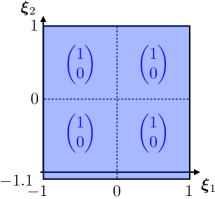

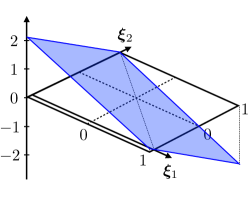

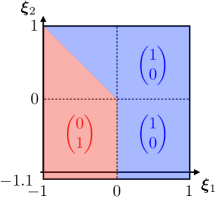

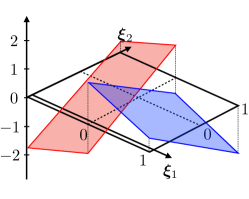

Motivated by the success of formulation (2) as the starting point to solve two-stage robust optimization problems with exogenous uncertainty, we derive an analogous dynamic formulation for the case of endogenous uncertainties. In particular, we build a robust optimization problem in which the sequence of problems solved by each of the decision-maker and nature in turn is captured explicitly. The idea is as follows. Initially, the decision-maker selects and . Subsequently, nature commits to a realization of the uncertain parameters from the set . Then, the decision-maker selects a recourse action that needs to be robust to those elements of the uncertain vector that they have not observed, i.e., for which . Indeed, the decision may have to be taken under uncertainty if there is some such that , in which case not all of the uncertain parameters have been revealed when is selected. Indeed, after is selected, nature is free to choose any realization of that is compatible with the original choice in the sense that for all such that . This model captures the notion that, after has been selected, nature is still free to choose the elements that have not been observed, provided it does so in a way that is consistent with those parameters that have been observed. Mathematically, given the measurement decisions and the observation , nature can select any element from the set

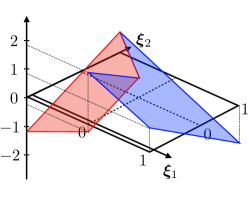

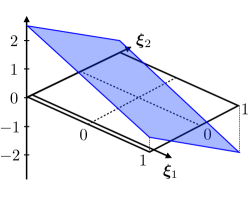

Note in particular that if , then and there is no uncertainty when is chosen. Accordingly, if , then and has no knowledge of any of the elements of . The realizations , , and the sets and are all illustrated on Figure 1.

Based on the above notation, we propose the following generic formulation of a two-stage robust optimization problem with decision-dependent information discovery:

| () |

Note that, at the time when is selected, some elements of are still uncertain. The choice of thus needs to be robust to the choice of those uncertain parameters that remain to be revealed. In particular, the constraints need to be satisfied for all choices of . Accordingly, is chosen so as to minimize the worst-case possible cost when is valued in the set .

Problems (3) and () are equivalent in a sense made precise in the following theorem.

Theorem 3.2

The optimal objective values of Problems (3) and () are equal. Moreover, the following statements hold true:

The parameter in item (i) of the theorem above is introduced to ensure that the decision rule defined on is non-anticipative. Indeed, if for any given and , there are many optimal solutions to problem

the decision rule defined on through

may not be constant in those parameters that remain unobserved. We note of course that other tie-breaking mechanisms could be used to build a non-anticipative solution. For example, we may select, among all optimal solutions, the one that is lexicographically first.

The theorem above is the main result that enables us to generalize the -adaptability approximation scheme to two-stage robust problems with decision-dependent information discovery and binary recourse. In Electronic Companion 12, we show that for any given choice of here-and-now decisions, the set of parameters for which a particular wait-and-see decision is optimal may be non closed and non-convex and that the optimal value of the problem may not be attained. This result is expected from the analysis in Hanasusanto et al. (2015), since Problem () generalizes Problem (2). Our example illustrates that this may be the case even if a portion of the uncertain parameters remain unobserved in the second stage.

Two-stage robust optimization problems with decision-dependent information discovery have a huge modeling power, see Sections 1, 7, and 8. Yet, as illustrated by the preceding discussion, they pose several theoretical and practical challenges. As we will see in the following sections, whether we are or not able to reformulate the the -adaptability counterpart of the problem exactly as a finite program solvable with off-the-shelf solvers depends on the absence or presence of uncertainty in the constraints. When in presence of constraint uncertainty, we can always compute an arbitrarily tight outer (lower bound) approximation, see Section 4.2.

4 -Adaptability for Problems with DDID

Instead of solving Problem () directly, we approximate it through its -adaptability counterpart,

| () |

where . In this problem, candidate policies are chosen here-and-now, that is before (the portion of uncertain parameters that we chose to observe) is revealed. Once becomes known, the best of those policies among all those that are robustly feasible (in view of uncertainty in the uncertain parameters that are still unknown) is implemented. If all policies are infeasible for some , then we interpret the maximum and minimum in () as supremum and infimum, that is, the -adaptability problem evaluates to . Problem () is a conservative approximation to program (). Moreover, if and , then the two problems are equivalent. In practice, we hope that a moderate number of candidate policies will be sufficient to obtain a (near) optimal solution to ().

The Price of Usability.

We note that Problem () is interesting in its own right. Indeed, in problems where usability is important (e.g., if workers need to be trained to follow diverse contingency plans depending on the realization ), Problem () may be an attractive alternative to Problem (). In such settings, the loss in optimality incurred due to passing from Problem () to Problem () can be thought of as the price of usability. For example, consider an emergency response planning problem where, in the first stage, a small number of helicopters can be used to survey affected areas and, in the second stage, and in response to the observed state of the areas surveyed, deployment of emergency response teams is decided. In practice, to avoid having to train teams in a large number of plans (yielding significant operational challenges), only a moderate number of response plans may be allowed. The importance of interpretability/usability has been previously noted by e.g., Koç and Morton (2015), McCarthy et al. (2018), Bertsimas et al. (2019), and Aghaei et al. (2019, 2021).

Remark 4.1

If , , and , then is optimal in Problem and thus , implying that Problem reduces to Problem (2) and Problem () reduces to the -adaptability counterpart of Problem (2).

Relative to the problems studied by Bertsimas and Caramanis (2010) and Hanasusanto et al. (2015), Problem () presents several challenges. First, the second stage problem in () is a robust (as opposed to deterministic) optimization problem. Second, the uncertainty sets involved in the maximization tasks of this robust problem are decision-dependent. While Problem () appears to be significantly more complicated than its exogenous counterpart, it can be converted to an equivalent min-max-min problem by lifting the space of the uncertainty set as show in the following lemma that is instrumental in our analysis.

Lemma 4.2

For any fixed , the subvector in the definition of represents the uncertainty scenario that “nature” will choose if the decision-maker acts according to decisions in the first stage and according to policy in the second stage. The set collects, for each , all feasible choices that nature can take if the decision-maker acts according to and then in the first and second stages, respectively. Thus, in Problem (5), the decision-maker first selects , , and , . Subsequently, nature commits to the portion of observed uncertain parameters and to a choice , , associated with each candidate policy . Finally, the decision-maker chooses one of the candidate policies.

In what follows, we provide insights into the theoretical and computational properties of the -adaptability counterpart to two-stage robust problems with DDID and with binary recourse.

Remark 4.3

We note that the results in Section 3 generalize fully to cases where the objective and constraint functions are continuous (not necessarily linear) in , , and . Moreover, all of the ideas in our paper generalize to the case where the technology and recourse matrices, and , depend on . We do not discuss these cases in detail so as to minimize notational overhead.

4.1 -Adaptability for Problems with Objective Uncertainty

In this section, we focus our attention on the case where uncertain parameters only appear in the objective of Problem () and where the recourse decisions are binary, being expressible as

| () |

where , . We study the -adaptability counterpart of Problem () given by

| () |

Applying Lemma 6, we are able to write Problem () equivalently as

| (7) |

where is defined as in Lemma 6. In the absence of uncertainty in the constraints, the constraints in the -adaptability problem can be moved to the first stage, as summarized by the following observation.

Observation 1

The -adaptability counterpart of the two-stage robust optimization problem with decision-dependent information discovery, Problem (), is equivalent to

| (8) |

where is as defined in Equation (6).

Note that for all , the set is non-empty and bounded. Thus, is feasible in Problem (8) if for all , whereas to be feasible in Problem (7) (and accordingly in Problem ()), it need only satisfy for some . Thus, a triplet feasible in (7) (and thus in ()) need not be feasible in Problem (8). However, the proof of Observation 1, provides a way to construct a feasible solution for Problem (8) from a feasible solution to Problem (7) that achieves the same optimal value.

Lemma 6 and Observation 1 are key to reformulating Problem () as a finite program. They also enable us to analyze the complexity of evaluating the objective function of the -adaptability problem under a fixed decision. Indeed, from Problem (8), it can be seen that for any fixed choice , the objective value of () can be evaluated by solving a linear program (LP) obtained by writing (8) in epigraph form. We formalize this result in the following.

Observation 2

In Observation 2, we showed that for any fixed , , , and , the objective function in Problem () can be evaluated by means of a polynomially sized LP. By dualizing this LP , we can obtain an equivalent reformulation of Problem () in the form of a bilinear problem.

Although Problem () is generally non-convex (bilinear), there exist several techniques in the literature for solving such problems exactly. In fact, this is an extremely active area of research, see e.g., Tsoukalas and Mitsos (2014) and Gupte et al. (2017). Moreover, problems of the form () can now be solved with state-of-the-art off-the-shelf solvers like Gurobi. Indeed, Gurobi recently released its 9th version that can tackle non-convex quadratic programs.222See e.g., https://www.gurobi.com/documentation/9.0/refman/nonconvex.html If and , the bilinear terms in the formulation above can be linearized using standard techniques and we can obtain an equivalent reformulation of Problem () in the form of an MBLP.

Corollary 4.5

We emphasize that the size of the MBLP in Corollary 4.5 is polynomial in the size of the input data for the -adaptability problem (). Note that, contrary to Hanasusanto et al. (2015), we require that . This is to ensure that we are able to linearize the bilinear terms involving the variables that arise from the dualization step. We note that formulation (9) and its equivalent MBLP can be augmented with symmetry breaking constraints to speed-up solution, see Section 11.1 for details.

Remark 4.6

Most MBLP solvers333See e.g., https://www.ibm.com/analytics/cplex-optimizer and https://www.gurobi.com/. allow reformulating the bilinear terms without the use of “big-” constants, which are known to suffer from numerical instability. These include, for example, so-called SOS or IfThen constraints.

4.2 -Adaptability for Problems with Constraint Uncertainty

The starting point of our analysis is the reformulation of Problem () as the min-max-min problem (5). Unfortunately, this problem is generally hard as testified by the following theorem.

Theorem 4.7

Evaluating the objective of Problem (5) if is not fixed is strongly NP-hard.

We reformulate Problem (5) equivalently by shifting the second-stage constraints from the objective function to the definition of the uncertainty set. We thus replace with a family of uncertainty sets parameterized by a vector .

Proposition 4.8

The -adaptability problem with decision-dependent information discovery, Problem (5), is equivalent to

| (10) |

where , is the number of second-stage constraints in Problem (), and the uncertainty sets , , are defined as

where, for convenience, we have suppressed the dependence of on and , .

The elements of vector in Proposition 4.8 encode which second-stage policies are feasible for the parameter realizations . Indeed, recall that can be viewed as the recourse action that nature will take if the decision-maker acts according to in response to seeing . Thus, policy is feasible in Problem (5) (and thus in Problem ()) if . On the other hand, policy violates the -th constraint in Problem (5) if . Thus, if , this implies that the -th constraint in () is violated for some and therefore is not feasible in (). Note that, in contrast to the case with exogenous uncertainty discussed by Hanasusanto et al. (2016), if and only if policy is robustly feasible in ().

Having brought Problem () to the form (10), it now presents a similar structure to a problem with objective uncertainty (see Section 4.1) with the caveats that the problem involves multiple uncertainty sets that are also open. Next, we employ closed inner approximations of the sets that are parameterized by a scalar :

| () |

where the uncertainty sets are defined as

Using this definition, we next reformulate the approximate Problem () equivalently as an MBLP.

Theorem 4.9

The approximate problem () is equivalent to the mixed binary bilinear program

| (11) |

where , and denote the sets for which the decision satisfies or violates the second-stage constraints in Problem (10), respectively.

As in the case of objective uncertainty, if and , then Problem (11) is equivalent an MBLP involving a suitably chosen “big-” constant. Similar to the robust counterpart resulting from the decision rule approximation proposed in Vayanos et al. (2011), Problem (11) presents a number of constraints and decision variables that is exponential in the approximation parameter, in this case . Relative to the prepartitioning approach from Vayanos et al. (2011), our method does however present a number of distinct advantages. First, the trade-off between approximation quality and computational tractability is controlled using a single design parameter; in contrast, in the prepartitioning approach, the number of design parameters equals the number of observable uncertain parameters. Second, as we increase , the quality of the approximation improves in our case, whereas increasing the number of breakpoints along a given direction does not necessarily yield to improvements in the prepartitioning approach. Finally, to identify breakpoint configurations resulting in low optimality gap, a large number of optimization problems need to be solved.

Remark 4.10

Theorem 4.9 directly generalizes to instances of Problem () where the technology and recourse matrices , , and depend on . Indeed, it suffices to absorb the coefficients of any uncertain terms in , , and in the right-hand side matrix .

Observation 4

Suppose that we are only in the presence of exogenous uncertainty, i.e., , , and . Then, Problem (11) reduces to the MBLP formulation of the K-adaptability problem with constraint uncertainty and with only exogenous uncertain parameters from Hanasusanto et al. (2015). In particular, in the case of constraint uncertainty, Hanasusanto et al. (2015) also require that the first stage variables be binary.

5 The Case of Piecewise Linear Convex Objective

In this section, we investigate two-stage robust optimization problems with DDID and objective uncertainty where the objective function is given as the maximum of finitely many linear functions.

5.1 Problem Formulation

A piecewise linear convex objective function can be written compactly as the maximum of finitely many linear functions of and , being expressible as

| (12) |

where , , and , , . A two-stage robust optimization problem with DDID, objective function given by (12), and objective uncertainty is then expressible as

| () |

Note that, as in Section 4.1, our framework remains applicable in the presence of joint deterministic constraints on the first and second stage variables. We omit these to minimize notational overhead.

5.2 -Adaptability Approximation & MBLP Reformulation

The -adaptability counterpart of Problem () reads

| () |

We begin this reformulation by the following lemma, which parallels Lemma 6, and shows that we can exchange the order of the inner min and max in formulation (), by indexing by .

Theorem 5.2

Albeit Problem (14) is an MBLP, it presents an exponential number of decision variables and constraints making it difficult to solve directly using off-the-shelf solvers even when is only moderately large (). In the remainder of this section, we exploit the specific structure of Problem () to solve its -adaptability counterpart exactly by reformulating it as an MBLP that presents an attractive structure amenable to decomposition techniques.

5.3 “Column-and-Constraint Generation” Algorithm

Column-and-constraint generation techniques are a popular approach for addressing problems that possess an exponential number of decision variables and constraints while presenting a decomposable structure, see e.g., Fischetti and Vigo (1997), Löbel (1998), Valério De Carvalho (1999), Mamer and McBride (2000), Feillet et al. (2010), Sadykov and Vanderbeck (2011), Zeng and Zhao (2013), Muter et al. (2013), and Muter et al. (2018). We propose a new column-and-constraint generation algorithm to solve the -adaptability counterpart () based on its reformulation (14). The key idea is to decompose the problem into a relaxed master problem and a series of subproblems indexed by . The master problem initially only involves the first stage constraints and a single auxiliary MBLP is used to iteratively identify indices for which the solution to the relaxed master problem becomes infeasible when plugged into subproblem . Constraints associated with infeasible subproblems are added to the master problem and the procedure continues until convergence. We detail this procedure in Electronic Companion 9 where we also show that certain classes of two-stage robust optimization problems that seek to minimize the “worst-case absolute regret” criterion can be written in the form (). In Section 8, we leverage the column and constraint generation algorithm and this observation to solve an active preference elicitation problem that seeks to recommend kidney allocation policies with least possible worst-case regret.

6 The Multi-Stage Case with Objective Uncertainty

We now show that many of our results generalize to the multi-stage case. To this end, we propose a novel formulation of multi-stage robust optimization problems with DDID. This formulation will enable us to generalize the -adaptability approximation approach to the multi-stage setting.

6.1 Multi-Stage Robust Optimization with Exogenous Uncertainty

In the literature, and similar to the two-stage case, there are (broadly speaking) two formulations of a generic multi-stage robust optimization problem with exogenous uncertainty over the planning horizon . These differ in the way in which the ability for the time decisions to adapt to the history of observed parameter realizations is modeled.

Decision Rule Formulation.

In the first model, one optimizes today over all recourse actions that will be taken in each realization of . Under this modeling paradigm, a multi-stage robust optimization problem with exogenous uncertainty is expressible as

| (15) |

where , , and . The fixed binary vector represents the information base at time , i.e., it encodes the information revealed up to (and including) time . Thus, if and only if has been observed at some time . As information cannot be forgotten, it holds that for all . The last constraint in Problem (15) ensures that the decisions , , are non-anticipative: it stipulates that can only depend on those parameters that have been observed up to and including time .

Dynamic Formulation.

In the second model, the recourse decisions are optimized explicitly after nature is done making a decision. Under this modeling paradigm, a generic multi-stage robust problem with exogenous uncertainty is expressible as:

| (16) |

where This set stipulates that, given the information base for time and the associated uncertainty vector , nature can select any vector at time whose elements associated with parameters it chose prior to time do not change (i.e., are equal to the corresponding elements chosen in the past).

We state the following theorem without proof.

6.2 Multi-Stage Robust Optimization with DDID

In this section, we investigate a variant of Problem (15) (and accordingly (16)) that enjoys much greater modeling flexibility since the time of information discovery (i.e., the information base) is kept flexible. Thus, we interpret the information base as a decision variable, which is allowed to depend on . The set may incorporate constraints stipulating, for example, that a specific uncertain parameter can only be observed after a certain stage or that an uncertain parameter can only be observed if another one has, etc. We assume that a cost is incurred for including uncertain parameters in the information base (equivalently, for observing uncertain parameters) and that the observation decisions also impact the constraints through the additional term , where . As before, we propose two equivalent models for multi-stage robust problems with DDID which differ in the way the ability for the time decisions to depend on the history of parameter realizations is modeled.

Decision Rule Formulation.

In the first model, one optimizes today over all recourse actions and that will be taken in each realization of . Under this modeling paradigm, a multi-stage robust optimization problem with decision-dependent information discovery, originally proposed in Vayanos et al. (2011), reads

| (17) |

where for all and is given and encodes the information available at the beginning of the planning horizon. The above formulation can be used to model problems involving also some exogenous uncertain parameters by restricting to equal either 1 or 0 for all depending on whether or not the exogenous uncertain parameter is observed on or before time . These restrictions can be conveniently added as constraints to the sets .

Dynamic Formulation.

In the second model, the recourse decisions and are optimized explicitly after nature is done selecting the parameters we have chosen to observe in the past. Under this modeling paradigm, a generic multi-stage robust problem with DDID is expressible as:

| () |

Similarly to the exogenous case, it can be shown that the two models above are equivalent.

Theorem 6.2

Problems (17) and () are equivalent.

6.3 -Adaptability for Multi-Stage Problems with DDID

We henceforth propose to approximate Problem () with its -adaptability counterpart, whereby candidate policies are selected here-and-now (for each time period) and the best of these policies is selected, in an adaptive fashion, at each stage. To streamline presentation, we focus on the case where Problem () presents only objective uncertainty. Thus, the -adaptability counterpart of the multi-stage robust problem () with DDID is expressible as

| () |

where we have defined for all with if and only if is observed at the beginning of the planning horizon and, as in the two-stage case, we have moved the deterministic constraints to the first stage. We note that using the same value of to approximate the decisions in all periods is without loss of generality and is used to minimize notational overhead. In our experiments in Section 7, we allow for different choices of for each .

Observation 5

6.4 Reformulation as a Mixed Binary Linear Program

In Observation 5, we showed that for any fixed , , , and , the objective function in Problem () can be evaluated by means of an exponentially sized LP. By dualizing this LP and linearizing the resulting bilinear terms, we can obtain an equivalent reformulation of Problem () in the form of a mixed-binary linear program.

Theorem 6.3

7 Computational Studies on Stylized Instances

We investigate the performance of our approach on a variety of robust optimization problems with decision-dependent information discovery. We solve these problems with our proposed methods discussed in Sections 4.1, 4.2, and 6. To speed-up computation, for the two-stage problems, we employ a conservative greedy heuristic that uses the solution to problems with smaller to solve problems with larger more efficiently, see Section 11.2. This strategy enables us to solve many random instances of problems with large approximation parameters (up to ). In all our experiments, we compare our method to the state-of-the-art prepartitioning approach from Vayanos et al. (2011) using the ROC ++ platform, see Vayanos et al. (2020). All of our experiments are performed on the High Performance Computing Cluster of our university. Each job is allotted 64GB of RAM, 16 cores, and a 2.6GHz Xeon processor. All optimization problems are solved using Gurobi v9.0.1. In Sections 7.1 and 7.3, a total time limit of 7,200 seconds is allowed to solve each instance cumulatively across all values of for the -adaptability problem and across all breakpoint configurations for the prepartitioning approach. In Section 7.4, a time limit of 7,200 seconds is imposed on each instance solved. In all our experiments, we set and .

7.1 Two-stage Robust Best Box Selection (Objective Uncertainty)

The first problem we study is a robust variant of the best box selection problem, see e.g., Gupta et al. (2016, 2017) for results on the stochastic version. In this problem, an agent must select one out of boxes, indexed in the set , each of which contains a prize. The value of the prize in each box is unknown and will only be revealed if the box is opened. Opening box incurs a cost . In the first stage, the agent can decide whether to open each box which we indicate with the decision variables . Thus, if and only if is observed between the first and second decision stages. The total budget available to open boxes is . In the second stage, the agent can choose one of the opened boxes to keep, which we indicate with the decision variable , , earning its prize. We assume that the value of box is expressible as , where corresponds to the nominal value of the prize of box , are risk factors, and collects the factor loadings associated with the value of box . The goal of the agent is to select the boxes to open (first stage decisions) and the box to keep (second stage decision) to maximize the worst-case value of the box kept. The Best Box Selection problem has numerous applications, for example in house purchasing or in candidate interviewing, see e.g., Singla (2018). With the notation above, the problem can be expressed as a two-stage robust optimization problem with decision-dependent information discovery of the form () as

| (18) |

where .

We evaluate the performance of our approach on 100 randomly generated instances of Problem (18) with risk factors: 20 instances for each . In these instances, is drawn uniformly at random from the box , we let , and . The matrix is sampled uniformly at random from the box . Our computational results across those instances are summarized in Table 1. From the table, we observe that with the proposed -adaptability approach, all instances (even those involving boxes) solved to optimality with an average solver time no greater than 15.6 seconds across all problem sizes. In contrast, the average solver time of the prepartitioning approach exceeded 475 seconds for boxes and equaled 7028 seconds for boxes, with only 70.1% of the problems associated with all breakpoint configurations solving within the allotted time on average. In addition, the quality of the best solution identified by the proposed -adaptability solution consistently outperformed that of the best prepartitioning solution. For example, an average improvement of over 148% over the static solution was exhibited for the -adaptability method for , while the prepartitioning solution only resulted in a 128% improvement. Finally, we note that the smallest value of needed to achieve saturation in the optimal value of the problem was consistently smaller that the number of subsets needed to obtain the best possible solution in the prepartitioning method, resulting in more interpratable solutions for our proposed approach. For example, for boxes, a value of is sufficient to yield a 177.4% improvement in optimal value while an average of 8.2 subsets are needed in the prepartitioning approach to achieve a 164.3% improvement.

| Adapt. | , | , | , | , | , | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| -adaptability | 100%/0.0%/0s | 100%/0.0%/0s | 100%/0.0%/0s | 100%/0.0%/0.1s | 100%/0.0%/0s | |||||||||||

| 100%/153.9%/0s | 100%/115.6%/0s | 100%/116.9%/1s | 100%/110.5%/1s | 100%/87.3%/1s | ||||||||||||

| 100%/177.4%/0s | 100%/147.2%/0s | 100%/150.1%/1s | 100%/135.5%/3s | 100%/113.9%/3s | ||||||||||||

| 100%/177.4%/0s | 100%/156.0%/1s | 100%/159.4%/2s | 100%/145.8%/8s | 100%/122.6%/7s | ||||||||||||

| 100%/177.4%/1s | 100%/159.0%/1s | 100%/164.0%/3s | 100%/148.3%/9s | 100%/126.2%/8s | ||||||||||||

| 100%/177.4%/1s | 100%/159.0%/2s | 100%/164.0%/3s | 100%/148.3%/9s | 100%/126.2%/9s | ||||||||||||

| 100%/177.4%/1s | 100%/159.0%/2s | 100%/164.0%/3s | 100%/148.3%/10s | 100%/126.2%/10s | ||||||||||||

| 100%/177.4%/1s | 100%/159.0%/3s | 100%/164.0%/4s | 100%/148.3%/12s | 100%/126.2%/12s | ||||||||||||

| 100%/177.4%/1s | 100%/159.0%/3s | 100%/164.0%/5s | 100%/148.3%/13s | 100%/126.2%/14s | ||||||||||||

| 100%/177.4%/2s | 100%/159.0%/3s | 100%/164.0%/5s | 100%/148.3%/15s | 100%/126.2%/16s | ||||||||||||

|

Preparti-tioning |

10 subsets |

|

|

|

|

|

7.2 Preference Elicitation with Real-Valued Recommendations (Real Decisions)

The second problem we consider is a robust active preference elicitation problem where user preferences can be elicited by asking them “how much” they like any particular item and where real-valued quantities of multiple items can be recommended after preferences are elicited, see Vayanos et al. (2021) for a variant where pairwise comparison queries are used instead.

The building blocks of our framework are candidate items which we index in the set . We let be the feature vector of item . We assume that user preferences are cardinal and model them by means of a linear utility function. Specifically, we assume that the utility of item is given by , where are independent identically distributed and is a vector of (unknown) utility function coefficients supported in the set . These assumptions are standard in the literature, see e.g., Bertsimas and O’Hair (2013) and Boutilier et al. (2004). Before making recommendations, the system has the opportunity to make queries to the user. Each query is based on one of the candidate items: if query is chosen, the user is asked “On a scale from 0 to 1, where 1 is the most anyone could like an item and 0 is the least anyone could like an item, how much do you like policy ?” We denote by the answer to query . After the answers to these queries are observed, the system can select out of the items to recommend and the quantity , , of those items to recommend. The goal of the recommender system is to select queries the answers to which will enable the system to recommend a set of items in quantities resulting in greatest possible worst-case utility.

To formulate the preference elicitation problem mathematically we let , , denote the decision to pose query , i.e., to observe before making a recommendation. Thus, The set of possible realizations of is given by

where the normalization of ensures that has the correct interpretation and, in the spirit of modern robust optimization, see e.g., Lorca and Sun (2016), we assume that is valued in the set where is a user-specified budget of uncertainty parameter. Once the answers to the queries are observed, the recommender system may select the quantity of each item to recommend which we encode with decisions . We let indicate if item is recommended and require that the quantity of items recommended equals 1. Thus,

With this notation, the preference elicitation problem is expressible as

| () |

A conservative solution to Problem () can be obtained using the -adaptability approximation scheme discussed in Section 4.1, by solving the bilinear reformulation (9).

| Adapt. | , , | , , | , , | , , | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| -adaptability | 100%/0.0%/2s | 100%/0.0%/4s | 100%/0.0%/7s | 100%/0.0%/25s | |||||||||

| 100%/14.0%/8s | 100%/28.2%/15s | 100%/35.7%/22.7s | 100%/41.7%/48s | ||||||||||

| 100%/15.2%/22s | 100%/29.0%/92s | 100%/42.6%/406.8s | 100%/52.2%/232s | ||||||||||

| 100%/15.5%/44s | 100%/29.4%/221s | 100%/43.5%/1396s | 90%/53.1%/2425s | ||||||||||

| 100%/15.9%/75s | 100%/29.4%/434s | 90%/43.9%/3352s | 70%/53.3%/4839s | ||||||||||

| 100%/16.1%/117s | 100%/29.6%/779s | 65%/44.2%/5050s | 25%/53.3%/6295s | ||||||||||

| 100%/16.6%/172s | 100%/29.8%/1279s | 35%/44.3%/6221s | 15%/53.3%/6761s | ||||||||||

| 100%/16.7%/226s | 100%/30.0%/1973s | 20%/44.4%/6594s | 10%/53.3%/7035s | ||||||||||

| 100%/17.3%/294s | 95%/30.0%/2970s | 5%/44.4%/6941s | 5%/53.3%/7167s | ||||||||||

| 100%/17.3%/375s | 85%/30.0%/4031s | 5%/44.4%/7056s | 0%/53.3%/7200s | ||||||||||

|

Preparti-tioning |

10 subsets |

|

|

|

|

We evaluate the performance of our approach on 80 randomly generated instances of Problem (): 20 instances for each . In these instances, , , and , , are drawn uniformly at random from the box . Our computational results across these instances are summarized in Table 2. From the table, we observe that on average the optimal value of our proposed -adaptability method (across all ) is greater than that of the best optimal value of the prepartitioning method (across all breakpoint configurations). For example, for the setting, -adaptability yields an average improvement in optimal value of relative to the static solution, whereas prepartitioning only results in an average improvement of in the best case. In addition, the solutions obtained by the -adaptability approach in the same time needed to solve for all breakpoint configurations (or to reach the time limit) in the prepartitioning approach are of far better quality. For example, the prepartitioning approach always reached the 7200 seconds time limit for instances of size with an associated average improvement in optimal value of . In contrast, within just 15 seconds on average, the -adaptability approach results in an improvement of in optimal value on average over the same instances. Finally, and similar to our results on the best box problem in Section 7.1, the average value of needed to achieve a solution of quality comparable to that of the best prepartitioning approach is a lot smaller than the number of subsets needed in prepartitioning, implying that -adaptability has more attractive interpretability properties. For example, for , 8.9 subsets are needed by prepartitioning to yield a 16.0% improvement in optimal value whereas is sufficient for our method to yield an improvement of 35.7%.

7.3 Robust R&D Project Portfolio Optimization (Constraint Uncertainty)

The third problem we investigate is a robust variant of the R&D project portfolio optimization problem, see e.g., Solak et al. (2010) for a solution approach on the stochastic version. In this problem, an R&D firm has a pipeline of candidate projects indexed in the set that it can invest in. The return of each project is uncertain and will only be revealed if the firm chooses to undertake the project. The firm can decide to undertake each project in year one, indicated by decision , in the following year, indicated by decision , or not at all. Thus, if and only if is observed between the first and second years. If the firm chooses to undertake the investment in the second year, it will only realize a known fraction of the return. Undertaking project incurs an unknown cost that will only be revealed if the firm chooses to undertake the project. The total budget available to invest in projects across the two years is . We assume that the return and cost of project are expressible as and where and corresponds to the nominal return and cost for project , respectively, are risk factors, and the vectors and collect the factor loadings for the return and cost of project , respectively. With this notation, the R&D project portfolio optimization problem is expressible as a two-stage robust optimization problem with decision-dependent information discovery of the form () as

| (19) |

where

We evaluate the performance of our approach on 100 randomly generated instances of Problem (19): 20 instances for each . In these instances, , is drawn uniformly at random from the box , and we let and . The elements of and are uniformly distributed in the interval . Our computational results across these instances are summarized in Table 3. From the table, we observe that on average the optimal value of our proposed -adaptability method (across all ) is greater than that of the best optimal value of the prepartitioning method (across all breakpoint configurations). For example, for the setting, -adaptability yields an average improvement in optimal value of relative to the static solution, whereas prepartitioning only results in an average improvement of in the best case. In addition, the solutions obtained by the -adaptability approach in the same time needed to solve for all breakpoint configurations (or to reach the time limit) in the prepartitioning approach are of far better quality. For example, the prepartitioning approach needed 5771 seconds on average to solve instances of size with an associated average improvement in optimal value of . In contrast, within just 1814 seconds on average, the -adaptability approach results in an improvement of in optimal value on average over the same instances. Finally, and similar to our results on the best box problem in Section 7.1, the average value of needed to achieve a solution of quality comparable to that of the best prepartitioning approach is a lot smaller than the number of subsets needed in prepartitioning, implying that -adaptability has more attractive interpretability properties. For example, for , 8.2 subsets are needed by prepartitioning to yield a 35.4% improvement in optimal value whereas is sufficient for our method to yield an improvement of 46.2%.

| Adapt. | , | , | , | , | , | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| -adaptability | 100%/0.0%/0s | 100%/0.0%/0s | 100%/0.0%/1s | 100%/0.0%/15s | 100%/0.0%/39s | |||||||||||

| 100%/40.8%/1s | 100%/32.7%/2s | 100%/32.2%/12s | 100%/31.0%/264s | 100%/31.9%/1915s | ||||||||||||

| 100%/81.1%/1s | 100%/46.2%/6s | 100%/50.6%/55s | 90%/43.9%/1543s | 50%/42.8%/5633s | ||||||||||||

| 100%/102.6%/3s | 100%/52.2%/22s | 100%/59.4%/323s | 70%/51.9%/3959s | 0%/44.6%/7200s | ||||||||||||

| 100%/109.2%/5s | 100%/57.1%/103s | 100%/65.7%/1814s | 20%/56.6%/6661s | 0%/44.6%/7200s | ||||||||||||

| 100%/110.5%/10s | 100%/59.4%/435s | 40%/67.6%/6321s | 0%/56.6%/7200s | 0%/44.6%/7200s | ||||||||||||

| 100%/110.7%/43s | 100%/62.5%/1835s | 5%/67.8%/7122s | 0%/56.6%/7200s | 0%/44.6%/7200s | ||||||||||||

| 100%/114.5%/32s | 60%/66.6%/5319s | 0%/67.8%/7200s | 0%/56.6%/7200s | 0%/44.6%/7200s | ||||||||||||

| 100%/117.5%/100s | 10%/66.9%/6955s | 0%/67.8%/7200s | 0%/56.6%/7200s | 0%/44.6%/7200s | ||||||||||||

| 100%/118.6%/301s | 0%/66.9%/7200s | 0%/67.8%/7200s | 0%/56.6%/7200s | 0%/44.6%/7200s | ||||||||||||

|

Preparti-tioning |

10 subsets |

|

|

|

|

|

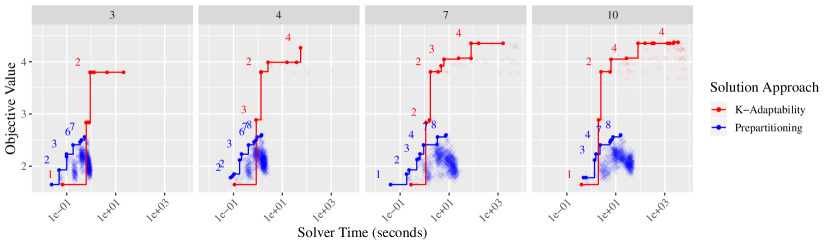

7.4 Multi-Stage Robust Pandora Box (Multi-Stage Objective Uncertainty)

The fourth problem we investigate is a robust variant of the multi-stage Pandora Box problem, see e.g., Doval (2018) and Singla (2018) for the stochastic setting. This problem is similar to best box selection, see Section 7.1, however opening boxes incurs a cost in the objective and no budget constraint is imposed. The planning horizon consists of periods indexed in the set . At the beginning of each period , the agent can select one box to open out of available boxes indexed in the set , each of which contains a prize. We let indicate if box has been opened on or before time . The value of the prize in each box is unknown at the beginning of the planning horizon and is only observable at time if the box has been opened before time . Thus, the decisions to open the boxes control the time of information discovery in this problem. Opening box incurs a cost . If the agent chooses to not open a box at some time , they may alternatively choose to keep one of the previously opened boxes, earning its prize. We let indicate the choice to keep box at time . Throughout the planning horizon, the agent may keep at most one box. The goal of the agent is to select whether and when to open each box to maximize the worst-case value of the box they choose to keep less the total cost of opening boxes. We assume that , where denotes the nominal value of box , are risk factors, and the vectors , , collect the factor loadings for the value of box . With this notation, Pandora’s Box problem is expressible as a multi-stage robust optimization problem with decision-dependent information discovery of the form () as

| (20) |

where , , and . The first set of constraints ensures that if a box has been kept in the past, no box can be opened. The second set of constraints guarantees that exactly one of the open boxes is kept.

We evaluate the performance of our approach on 80 randomly generated instances of Problem (20) with boxes and risk factors: 20 instances for each choice of . In these instances, is drawn uniformly at random from and we let . The elements of are uniformly distributed in the interval . Our computational results across these instances are summarized in Figure 2. From the figure, it can be seen that the -adaptability approach results in solutions of far better quality than the prepartitioning approach. For example, the best average optimal value of the prepartitioning approach for the case is 2.60 whereas it is 4.27 for the -adaptability method. Moreover, solutions outperforming the best prepartitioning solution are found on average faster with the -adaptability approach. For example, in the setting , the breakpoint configuration that resulted in the best average optimal value had an average solver time of 15.9 seconds, whereas 1.9 seconds on average were needed to solve the -adaptability problem associated with the adaptability configuration that resulted in a higher optimal value on average. Finally, the solutions obtained by the -adaptability approach were consistently more interpretable than those of the prepartitioning method. In particular, across all our experiments, the cardinality of the breakpoint configuration that resulted in the best performance of the prepartitioning method was between 7 and 8 and that solution was consistently outperformed by -adaptable solutions with under 3 candidate policies.

8 Preference Elicitation to Improve the US Kidney Allocation System

In this section, we evaluate our approach on a preference elicitation and recommendation problem that explicitly captures the endogenous nature of the elicitation process.

8.1 Motivation & Problem Formulation (Piecewise Linear Convex Objective)

The motivation for our study is one of the central problems faced by policymakers at the OPTN/UNOS who must periodically make changes to the policy for prioritizing patients on the kidney transplant waiting list for scarce deceased donor kidneys. To tackle this problem, a Kidney Transplantation Committee (KTC) is appointed at the OPTN that examines the outcomes of numerous candidate policies simulated using the Kidney-Pancreas Simulated Allocation Model (KPSAM), a simulator developed by the Scientific Registry of Transplant Recipients (SRTR), see KPSAM (2015). The KTC examines the outcomes of the allocation policy alternatives along several dimensions (measures) of fairness and efficiency (e.g., number of recipients by age group, number of deaths by gender) before ultimately committing to one of the alternatives. This process was for example followed in the latest big policy change, see e.g., Wolfe et al. (2009). Since selecting one alternative (policy) over many others is a challenging task, in particular when the dimension of each alternative is large, see e.g., Toubia et al. (2003, 2004, 2007) and Boutilier et al. (2004), we propose a preference elicitation and recommendation framework for identifying a preferred policy using a moderate number of strategically chosen queries.

We formulate this problem as a variant of the active preference elicitation problem from Section 7.2 where a single item can be recommended and where we select queries that minimize worst-case regret of the recommendation. Items indexed in the set correspond to policies where the feature vector of policy collects various measures of fairness and efficiency of the policy. The problem is expressible mathematically as

| () |

where and are as in Section 7.2 and where . In this problem, the first part of the objective computes the utility of the best item to offer in hindsight, after the utilities have been observed. The second part of the objective corresponds to the worst-case utility of the item recommended when only a portion of the uncertain parameters are observed, as dictated by the vector . Problem () can be solved approximately using the -adaptability approximation scheme discussed in Section 5. Indeed, the regret in Problem () is given as the maximum of finitely many linear functions and Theorem 5.2 applies. We note that in this case . Thus, solving the -adaptability counterpart of () with recovers an optimal solution to the corresponding original problem.

8.2 Generating KAS Candidate Policies

We generate the outcomes , , of candidate policies using the KPSAM simulator which we obtained from the SRTR using a modeling window from 01/01/2010 to 12/31/2010. The candidate policies we consider are linear scoring rules that use the patient dialysis time, the life years from transplant score, the Calculated Panel Reactive Antibodies and the age of the patient. For each policy, we record outcomes, including the number of transplants overall, by age, by blood type, by race, and by gender, and the number of deaths by race and by gender. For details on the construction of the policies and for a list of outcomes, see Electronic Companion 10.

8.3 Numerical Results on KAS Candidate Policies

We evaluate the performance of our approach on the KAS policies dataset from Section 8.2. Throughout our experiments, the -adaptability counterpart of Problem () is solved using the techniques described in Section 5. To speed-up computation, we also use a heuristic adapted from Subramanyam et al. (2020) and detailed in Section 11.2. The tolerance used in the column-and-constraint generation algorithm (see Section 5.3) is . We evaluate the true worst-case regret of any given solution , which we denote by , as follows: we fix in Problem (), where we set and employ all candidate policies in the set . As before, we use the ROC ++ platform to solve the prepartitioning problem, see Vayanos et al. (2020). All of our experiments are performed using the same computing resources as in Section 7.

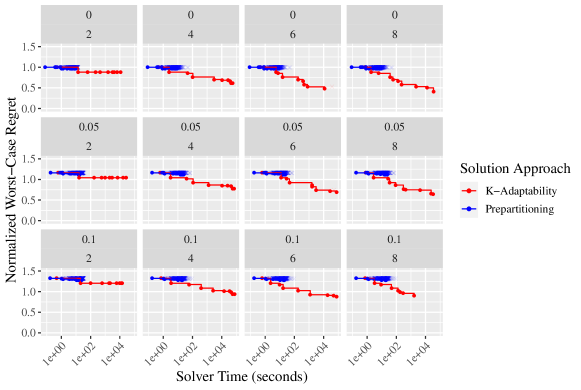

Optimality-Scalability Trade-Off.

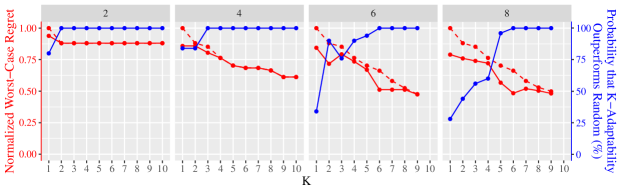

We evaluate the trade-off between computational complexity and scalability of our approach. We solve the min-max regret problems as and are varied in the sets and , respectively. The results are summarized in Figure 3. From the figure it can be seen that the -adaptability approach significantly outperforms the prepartitioning approach and static policies are very sub-optimal. In fact, the prepartitioning approach performs comparably to static policies across all settings. On the other hand, with the -adaptability approach, the normalized444To aid with interpretability, we normalize regret such that the worst-case regret when no question is asked is 1 and the worst-case regret when all questions are asked is 0. worst-case regret drops to 0.40, 0.68, and 0.9 from 1, 1.16, and 1.32, for and , respectively (for ). This experiment shows the strength of the -adaptability approach compared to the state of the art.

Performance Relative to Random Elicitation.

We evaluate the benefits of computing near-optimal queries using the -adaptability approximation approach relative to asking questions at random. We compare the true performance of a solution to the -adaptability problem, , to that of 50 questions drawn uniformly at random from the set , . The results are summarized on Figure 4. From the figure, we see that the probability that the -adaptability solution outperforms random elicitation converges to 1 as grows. We observe that, for values of greater than 5, the -adaptability solution outperforms random elicitation in over 90% of the cases.

This work was supported primarily by the Operations Engineering Program of the National Science Foundation under NSF Award No. 1763108. The authors are grateful to Miss. Qing Jin for valuable discussions on implementation issues.

References

- Aghaei et al. (2019) Aghaei S, Azizi MJ, Vayanos P (2019) Learning optimal and fair decision trees for non-discriminative decision-making. Proceedings of the 33rd AAAI Conference on Artificial Intelligence.

- Aghaei et al. (2021) Aghaei S, Gómez A, Vayanos P (2021) Strong optimal classification trees. Major revision at Operations Research, URL https://arxiv.org/abs/2002.09142.

- Assavapokee et al. (2008a) Assavapokee T, Realff MJ, Ammons JC (2008a) Min-max regret robust optimization approach on interval data uncertainty. Journal of Optimization Theory and Applications 137:297–316, ISSN 00223239, URL http://dx.doi.org/10.1007/s10957-007-9334-6.