Loss aversion and the welfare ranking of policy interventions††thanks: The authors are grateful to Pedro Carneiro, Dan Hamermesh, Hide Ichimura, Radosław Kurek, Essie Maasoumi, Piotr Miłoś, Magne Mogstad, Jim Powell, João Santos Silva, Tiemen Woutersen, and seminar participants at the University of Chicago, University of Wisconsin-Madison, USC, MSU, University of Montreal, University of California Berkeley, University of Arizona, 28th annual meeting of the Midwest Econometrics Group, 35th Meeting of the Canadian Econometric Study Group, and the 3rd edition of the Rio-Sao Paulo Econometrics Workshop for useful comments and discussions regarding this paper. Martyna Kobus acknowledges the support of the National Science Centre, Poland, the grant no. 2020/39/B/HS4/03131. Marta Schoch provided excellent research assistance. Computer programs to replicate the numerical analyses are available from the authors. This work was made possible by the facilities of the Shared Hierarchical Academic Research Computing Network (SHARCNET:www.sharcnet.ca) and Compute/Calcul Canada. All the remaining errors are ours.

Abstract

This paper develops theoretical criteria and econometric methods to rank policy interventions in terms of welfare when individuals are loss-averse. Our new criterion for “loss aversion-sensitive dominance” defines a weak partial ordering of the distributions of policy-induced gains and losses. It applies to the class of welfare functions which model individual preferences with non-decreasing and loss-averse attitudes towards changes in outcomes. We also develop new semiparametric statistical methods to test loss aversion-sensitive dominance in practice, using nonparametric plug-in estimates; these allow inference to be conducted through a special resampling procedure. Since point-identification of the distribution of policy-induced gains and losses may require strong assumptions, we extend our comparison criteria, test statistics, and resampling procedures to the partially-identified case. We illustrate our methods with a simple empirical application to the welfare comparison of alternative income support programs in the US.

Keywords: Welfare, Loss Aversion, Policy Evaluation, Stochastic Ordering, Directional Differentiability

JEL codes: C12, C14, I30

We suffer more, … when we fall from a better to a worse situation, than we ever enjoy when we rise from a worse to a better.

Adam Smith, The Theory of Moral Sentiments

1 Introduction

Policy interventions often generate heterogeneous effects, giving rise to gains and losses to different individuals and sectors of society. Classically, the welfare ranking of policy interventions, conducted under the Rawlsian principle of the “veil of ignorance”, has deemed such gains and losses irrelevant: all policies that produce the same marginal distribution of outcomes should be considered equivalent for the purpose of welfare analysis. (Atkinson, 1970; Roemer, 1998; Sen, 2000). However, more recent approaches have focused precisely on how different individuals are affected by a given policy (Heckman and Smith, 1998; Carneiro, Hansen, and Heckman, 2001). Our paper relates to this latter approach and focuses on an important characteristic of the individual valuation of policy-induced effects: loss aversion.666Loss aversion is a well established empirical regularity, documented in a wide variety of contexts (Kahneman and Tversky, 1979; Samuelson and Zeckhauser, 1988; Tversky and Kahneman, 1991; Rabin and Thaler, 2001; Rick, 2011)

There are two main reasons why loss aversion can be important for the welfare ranking of policy interventions. First, as shown in Carneiro, Hansen, and Heckman (2001), the individual gains and losses caused by a policy have important political economy consequences. Public support for that policy, and for the authorities that implement it, depends on the balance of gains and losses experienced and valued by different individuals in the electorate. In this context, there is mounting empirical evidence indicating that the electorate often exhibits loss aversion. This aversion to losses among constituents, in turn, drives the actions of policy makers, as documented in situations as diverse as government support to the steel industry in US trade policy, and President Trump’s attempted repeal of the Affordable Care Act (Freund and Özden, 2008; Alesina and Passarelli, 2019).

Second, political economy aside, there are important situations where policy makers have strong normative reasons for incorporating loss-aversion in their own welfare ranking of public policies. This has been proposed in a range of fields. In a recent example, Eyal (2020) shows that the Hippocratic principle of “first, do no harm” has led US and EU policy makers to delay the development of Covid-19 vaccines by rejecting human challenge trials, that involve purposefully infecting a small number of vaccine trial volunteers. In this situation, policy makers placed more weight on the potential harm to a small number of volunteers, than on the vast potential benefits of accelerating the availability of a vaccine to large swathes of the population. Similarly, in the context of minimum wage legislation, Mankiw (2014) proposes that policy makers should be loss-averse in their approach to policy evaluation and adopt a “first, do no harm” principle: “As I see it, the minimum wage and the Affordable Care Act are cases in point. Noble as they are in aspiration, they fail the do-no harm test. An increase in the minimum wage would disrupt some deals that workers and employers have made voluntarily”. Along the same lines, in the context of development economics, scholars such as Easterly (2009) have proposed a “first, do no harm” approach to foreign aid interventions in developing countries.

In this paper, we extend the toolkit available for the evaluation of policy interventions in contexts where it is sensible to incorporate loss-aversion in the welfare ranking of policy interventions. We are not proposing that all policies should be ranked under loss aversion sensitive criteria. Instead, we provide a methodology for conducting such a ranking in cases where aversion to losses is likely to be important. As discussed above, this may be the case either because policy makers are genuinely loss-averse, or because they know that the individuals exposed to the policy are so, and this leads them to incorporate loss aversion in policy ranking. To this end, our paper develops new testable criteria and econometric methods to rank distributions of individual policy effects, from a welfare standpoint, incorporating loss aversion. We make two main contributions to the literature.

Our first contribution is to propose loss aversion-sensitive criteria for the welfare ranking of policies. We adopt the standard welfare function approach (Atkinson, 1970): alternative policies are compared based on a welfare ranking, where social welfare is an additively separable and symmetric function of individuals’ outcomes. It is well established that, for non-decreasing utility functions, this is equivalent to first-order stochastic dominance (FOSD) over distributions of policy outcomes. Analogously, our ranking is based on social value functions, which are additively separable and symmetric functions of individual gains and losses. We show that the social value function ranking with non-decreasing and loss-averse value functions (Tversky and Kahneman, 1991) is equivalent to a new concept we call loss aversion-sensitive dominance (LASD) over distributions of policy-induced gains and losses. FOSD requires that the cumulative distribution function of the dominated distribution lies everywhere above the cumulative distribution of the dominant distribution. In contrast, under LASD, the dominated cumulative distribution function must lie sufficiently above the dominant distribution function for losses such that the probability of potential losses cannot be compensated by a higher probability for potential gains. This is a consequence of loss-aversion. Except for the special case of a status quo policy (i.e. a policy of no change) where FOSD and LASD coincide, generally, as we show, LASD can be used to compare policies that are indistinguishable for FOSD.777The literature on stochastic dominance is vast and spans economics and mathematics - we refer the reader to, e.g., Shaked and Shanthikumar (1994) and Levy (2016) for a review. When dominance curves cross, higher order or inverse stochastic dominance criteria have been proposed. The former involves conditions on higher (typically third and fourth) order derivatives of utility function (e.g. Fishburn (1980), Chew (1983) to which Eeckhoudt and Schlesinger (2006) provided interesting interpretation, whereas the latter is related to the rank-dependent theory originally proposed by Weymark (1981) and Yaari (1987, 1988), where social welfare functions are weighted averages of ordered outcomes with weights decreasing with the rank of the outcome (see Aaberge, Havnes, and Mogstad (2018) for a recent refinement of this theory).

The LASD criterion relies on gains and losses, which under standard identification conditions can be considered treatment effects. It is well known that the point identification of the distribution of treatment effects may require implausible theoretical restrictions such as rank invariance of potential outcomes (Heckman, Smith, and Clements, 1997). We thus extend our LASD criteria to a partially-identified setting and establish a sufficient condition to rank alternative policies under partial identification of the distributions of their effects. We use Makarov bounds (Makarov, 1982; Rüschendorf, 1982; Frank, Nelsen, and Schweizer, 1987) to bound the distribution of treatment effects when the joint pre and post-policy outcome distribution is unknown. This provides a testable criterion that can be used in practice, since the marginal distribution functions from samples observed under various treatments can usually be identified and Makarov bounds only rely on marginal information for their identification.

Our second contribution is to develop statistical inference procedures to practically test the loss averse-sensitive dominance condition using sample data. We develop statistical tests for both point-identified and partially-identified distributions of outcomes. The test procedures are designed to assess, uniformly over the two outcome distributions, whether one treatment dominates another in terms of the LASD criterion. Specifically, we suggest Kolmogorov-Smirnov and Cramér-von Mises test statistics that are applied to nonparametric plug-in estimates of the LASD criterion mentioned above. Inference for these statistics uses specially tailored resampling procedures. We show that our procedures control the size of tests for all probability distributions that satisfy the null hypothesis. Our tests are related to the literature on inference for stochastic dominance represented by, e.g., Linton, Song, and Whang (2010); Linton, Maasoumi, and Whang (2005); Barrett and Donald (2003) and references cited therein. Linton, Maasoumi, and Whang (2005) is an important contribution because in addition to developing tests for stochastic dominance of arbitrary order, they propose a Prospect Theory stochastic dominance test. Their test is intended for inferring dominance among a different family of value functions than ours, namely, the focus is on risk loving for gains and risk aversion for losses (i.e. so called S-shapedness, Kahneman and Tversky (1979)), but not on loss aversion. We contribute to the literature by developing tests for loss averse-sensitive dominance, which are an alternative to standard stochastic dominance tests. Our tests widen the variety of comparisons available to empirical researchers to other criteria that encode important qualitative features of agent preferences.

The LASD criterion results in a functional inequality that depends on marginal distribution functions, and we adapt existing techniques from the literature on testing functional inequalities to test for LASD. However, in comparison with stochastic dominance tests, verifying LASD with sample data presents technical challenges for both the point- and partially-identified cases. The criterion that implies LASD of one distribution over another is more complex than the standard FOSD criterion, and hence requires a significant extension of existing procedures to justify the use of inference about loss averse-sensitive dominance with a nonparametric plug-in estimator of the LASD criterion.

In particular, the problem with using existing stochastic dominance techniques is that the mapping of distribution functions to a testable criterion is nonlinear and ill-behaved. A dominance test inherently requires uniform comparisons be made, and tractable analysis of its distribution demands regularity, in the form of differentiability, of the map between the space of distribution functions and the space of criterion functions. However, the map from pairs of distribution functions to the LASD criterion function is not differentiable. Despite this complication, we show that supremum- or -norm statistics applied to this function are just regular enough that, with some care, resampling can be used to conduct inference.

For practical implementation, we propose an inference procedure that combines standard resampling with an estimate of the way that test statistics depend on underlying data distributions, building on recent results from Fang and Santos (2019). We contribute to the literature on directionally differentiable test statistics with a new test for LASD. Recent contributions to this literature include, among others, Hong and Li (2018); Chetverikov, Santos, and Shaikh (2018); Cho and White (2018); Christensen and Connault (2019); Fang and Santos (2019); Cattaneo, Jansson, and Nagasawa (2020) and Masten and Poirier (2020).

When distributions are only partially identified by bounds, the situation is more challenging. The current state of the literature on Makarov bounds focuses on pointwise inference for bound functions (see, e.g., Fan and Park (2010, 2012), Fan, Guerre, and Zhu (2017), and Firpo and Ridder (2008, 2019)). However, the LASD criterion requires a uniform comparison of bound functions, and the map from distribution functions to Makarov bound functions is also not smooth. Fortunately the problem has a similar solution to the point-identified LASD test. The resulting - and supremum-norm statistics allow us to conduct inference for LASD in the partially identified case using functions that bound the relevant CDFs. The details are included in the online Supplemental Appendix.

We illustrate the practical use of our proposed criteria and tests with a very simple empirical application using data from Bitler, Gelbach, and Hoynes (2006). This aims at exemplifying the use of our approach, rather than developing a fully fledged empirical investigation. We show that, in the case of a policy with gainers and losers, the use of our loss aversion-sensitive evaluation criteria may lead to a ranking of policy interventions that differs from that obtained when their outcomes are compared using stochastic dominance.

The rest of the paper is organized as follows. Section 2 presents the basic definitions and notation and defines loss aversion-sensitive dominance. Section 3 develops testable criteria for loss aversion-sensitive dominance. Section 4 proposes statistical inference methods for LASD using sample observations. Section 5 illustrates our methodology using a very simple empirical application that uses data from the experimental evaluation of a well-known welfare policy reform in the US. Section 6 concludes. Our first appendix includes auxiliary results and definitions; our second one collects proof of the results in the paper.

2 Loss aversion-sensitive dominance

In this section, we propose a novel dominance relation for ordering policies under the assumption that social decision makers consider the distribution of individual gains and losses under different policy scenarios. We call this criterion Loss Aversion-Sensitive Dominance (LASD).

Consider a random variable with cumulative distribution function . Let be the set of cumulative distribution functions with bounded support . We maintain the assumption throughout that . The bounded support assumption is made to avoid technical conditions on tails of distribution functions. The aim of this paper is to provide theoretical criteria and econometric methods to rank policy interventions under LASD. The decision maker’s goal is to compare policies and using the distribution functions of and , labeled and . Because the random variables and represent gains and losses due to the enactment of policies and , they represent a change between agents’ pre-treatment and post-treatment outcomes. To this end, let and represent an agent’s potential outcome under the status quo, treatment or treatment , so that we may write and . We assume that the variables have marginal distribution functions .

It may be assumed that are identified, or that only are identified. The former case is related to a point-identified model, and the latter to a partially-identified one. Theoretical results for both situations are shown here. Inference for the first situation is considered in this paper, while partially-identified inference results under the second situation are considered in the online Supplemental Appendix.

For example, in the empirical illustration considered in Section 5, we observe quarterly household income before the enactment of a new welfare program, which we assume to represent realizations of . Next, we observe income for some households under a continuation of the old program, identifying those as realizations of , and income for other households under a new welfare program, labeling those observations as realizations. If policymakers are interested in how one household’s earnings evolve over time either by staying with the old program or switching to the new program, then the levels of and are not of primary interest, rather the changes represented by and are (and given the longitudinal nature of our data, it is natural to assume that and are identified). Our tests, detailed in Section 4, use the null hypothesis that a household exhibiting loss-aversion would prefer to switch to the new welfare program, and search for evidence to the contrary.

The decision maker has preferences over (not ) that are represented via a continuous function.

Definition 2.1 (Social Value Function (SVF)).

Suppose random variable has CDF and let denote the following social value function

| (1) |

where is called a value function.888Formally speaking we have but we suppress the subscript for expositional brevity.

The social value function defined above is the value assigned to the distribution of by a social planner that uses the value function to convert gains and losses into a measure of well-being (Gajdos and Weymark, 2012). This value function does not have to coincide with any individual’s in the population: as mentioned in the Introduction, the social planner is averse to individual losses either because individuals are loss-averse themselves (political economy motivation), or because she holds normative views that imply her loss aversion towards . In either case, will exhibit loss-aversion, i.e. there is asymmetry in the valuation of gains and losses, where losses are weighed more heavily than gains of equal magnitude. Furthermore, assigns negative value to losses and positive value to gains and is non-decreasing. These properties are formally listed in the next definition.999This standard interpretation of the social welfare function can be further extended. For example, individuals may be uncertain about their counterfactual outcome and form an expectation of given . Then we write . Denoting a new value function , i.e. an expected value for a given , is as in Definition 2.1.,101010An interesting direction for future research is to axiomatize the class of social value functions and possibly develop measures of loss aversion based on this class. Some inspiration for axiomatization may come from the inequality and poverty measurement literature. For example, ratio scale invariance (i.e. proportional changes to the units in which gains and losses are measured do not matter), may be a powerful axiom in obtaining a specific functional form.

Definition 2.2 (Properties of the value function).

The value function is differentiable and satisfies:

-

1.

Disutility of losses and utility of gains: for all , and for all .

-

2.

Non-decreasing: for all .

-

3.

Loss-averse: for all .

The properties in Definition 2.2 are typically assumed in Prospect Theory together with the additional requirement of S-shapedness of value function, which we do not consider (see, e.g., p. 279 of Kahneman and Tversky (1979)). Assumptions 1 and 2 are standard monotone increasing conditions. Assumption 3 expresses the idea that “losses loom larger than corresponding gains” and is a widely accepted definition of loss aversion (Tversky and Kahneman, 1992, p.303). It is a stronger condition than the one considered by Kahneman and Tversky (1979).

The following form of will be useful in subsequent definitions and results.

Proposition 2.3.

Suppose that and is differentiable. Then

| (2) |

Assume that the decision maker’s social value function depends on which satisfies Definition 2.2, and she wishes to compare random variables and which represent gains and losses under two policies labeled and . The decision maker prefers over if she evaluates as better than using her SVF — specifically, is preferred to if and only if , where is defined in Definition 2.1. Please note that is preferred to for every that is described by Definition 2.2. This is what makes dominance conditions robust criteria for comparing distributions. This idea is formalized below.

Definition 2.4 (Loss Aversion-Sensitive Dominance).

Let and have distribution functions respectively labeled . If for all value functions that satisfy Definition 2.2, we say that dominates in terms of Loss Aversion-Sensitive Dominance, or LASD for short, and we write .

In the next section we relate this theoretical definition to a more concrete condition that depends on the cumulative distribution functions of the outcome distributions, and .

3 Testable criteria for loss aversion-sensitive dominance

In this section we formulate testable conditions for evaluating distributions of gains and losses in practice. We propose criteria that indicate whether one distribution of gains and losses dominates another in the sense described in Definition 2.4.

Recall that and represent an outcome before or after a policy takes effect, while and represent a change from a pre-policy state to an outcome under a policy. The challenge of comparing variables and is well known in the treatment effects literature: because and are defined by differences between the , and depend on the joint distribution of , which may not be observable without restrictions imposed by an economic model. In subsection 3.1 we abstract from specific identification conditions and discusses LASD under the assumption that and are identified. In subsection 3.2 we work with a partially identified case where only the marginal distribution functions , and are identified and no restrictions are made to identify and .

3.1 The case of point-identified distributions

The LASD concept in Definition 2.4 requires that one distribution is preferred to another over a class of social value functions and is difficult to test directly. The following result relates the LASD concept to a criterion which depends only on marginal distribution functions and orders and according to the class of SVFs allowed in Definition 2.2. In this section we assume that are point identified. This may result from a variety of econometric restrictions that deliver identification and are the subject of a large literature.

Theorem 3.1.

Suppose that . The following are equivalent:

-

1.

.

-

2.

For all , and satisfy

(3) -

3.

For all , and simultaneously satisfy

(4) and

(5)

Theorem 3.1 provides two different conditions that can be used to verify whether one distribution of gains and losses dominates the other in the LASD sense.111111LASD is a partial order. Over losses, (4) is a partial order because FOSD is a partial order. For the tail condition (5) checking transitivity we have , and . If then and using it in (5) gives anti-symmetry. These criteria compare the outcome distributions by examining how the distribution functions assign probabilities to gains and losses of all possible magnitudes. The particular way that they make a comparison is related to the relative importance of gains and losses. Consider condition (3). For the distribution of to be dominated, its distribution function must lie above the distribution of for losses. can be dominated by in the LASD sense even when gains under do not dominate for gains — that is, when for some — as long as this lack of dominance in gains is compensated by sufficient dominance of over in the losses region. This is a consequence of the asymmetric treatment of gains and losses. Conditions (4) and (5) jointly express the same idea, but they help to understand how gains and losses are treated asymmetrically in condition (3). In the losses region, condition (4) is a standard FOSD condition. This is a consequence of loss aversion; note that in the extreme case where only losses matter, we would have (4). In the gains region, dominance has to be sufficiently large so that under , the probability of gains minus the probability of losses (of magnitude or larger) is no smaller than the corresponding difference for .121212We leave 1s on both sides of inequality (5) for this interpretation to be more evident. Inequality (3) combines the two inequalities represented by (4) and (5) into a single equation.

It is interesting to note that LASD has one property in common with FOSD, namely, a higher mean is a necessary condition for both types of dominance. This follows directly from Definitions 2.1 and 2.2 by using .

Lemma 3.2.

If then .

Note that FOSD cannot rank two distributions that have the same mean — that is, if and , then . This is not the case for LASD, as the next example demonstrates. Therefore, for example, equation (3) may still be used to differentiate between two distributions with the same average effect.

Example 3.3.

Consider the family of uniform distributions on indexed by and denote the corresponding member distribution functions . The family of such distributions have mean zero and whenever . Indeed, note that

and thus for any which is loss-averse (see Definition 2.2) we have

It is important to note that LASD is a concept that is specialized to the comparison of distributions that represent gains and losses. Standard FOSD is typically applied to the distribution of outcomes in levels without regard to whether the outcomes resulted from gains or losses of agents relative to a pre-policy state — in our notation, and are typically compared with FOSD, instead of and . FOSD applied to post-policy levels may or may not coincide with LASD applied to changes. This means that even when a strong condition such as FOSD holds for final outcomes, if one took into account how agents value gains and losses it may turn out that the dominant distribution is no longer a preferred outcome. One could apply the FOSD rule to compare distributions of income changes, which implies LASD applied to changes, because FOSD applies to a broader class of value functions. However, this type of comparison would ignore agents’ loss aversion, the important qualitative feature that LASD accounts for. The following example shows that the analysis of outcomes in levels using FOSD need not correspond to any LASD ordering of outcomes in changes.

Example 3.4.

Let represent outcomes before policies or . Suppose is distributed uniformly over . Policy assigns post-policy outcomes depending on the realized according to the schedule

Therefore the distribution of is , . Meanwhile, policy maintains the status quo: with probability 1.

Distributions and are the same, thus FOSD holds between and . However, there is no loss aversion-sensitive dominance between and . Indeed, we can find two value functions that fulfill the conditions of Definition 2.4 but order and differently. For example, take . Then . Next let . Then .

In the previous example, policy left pre-treatment outcomes unchanged, or in other words, maintained a status quo condition — we had . Suppose generally that has a distribution that is degenerate at . Then for all and for all . We define this as a status quo policy distribution, labelled . When comparison is between a distribution and , LASD and standard FOSD are equivalent. The distribution that dominates is necessarily only gains.

Corollary 3.5.

Suppose that and . Then .

3.2 The case of partially-identified distributions

In many situations of interest the cumulative distribution functions of gains and losses, and , are not point identified without a model of the relationship between and . However, the marginal distributions of outcomes in levels under different policies, represented by the variables , and , may be identified. Without information on the dependence between potential outcomes, we can still make some more circumscribed statements with regard to dominance based on bounds for the distribution functions. This section studies the LASD dominance criterion to the case that distribution functions and are only partially identified.

A number of authors have considered functions that bound the distribution functions and . Taking as an example, Makarov bounds (Makarov, 1982; Rüschendorf, 1982; Frank, Nelsen, and Schweizer, 1987) are two functions and that satisfy for all , depend only on the marginal distribution functions and and are pointwise sharp — for any fixed there exist some and such that the resulting has a distribution function at that is equal one of or . Williamson and Downs (1990) provide convenient definitions for these bound functions. For any two distribution functions , define

For convenience define the policy-specific bound functions for , and all , which depend on the marginal CDFs and , by

| (6) | ||||

| (7) | ||||

Using these definitions we obtain a sufficient and a necessary condition for LASD when only bound functions of the treatment effects distribution functions are observable. The next theorem formalizes the result.

Theorem 3.6.

Theorem 3.6 is an analog of Theorem 3.1 and shows what effect the loss of point identification has on the relationship between dominance and conditions on the CDFs. In particular, one loses a simple “if and only if” characterization that depends on CDFs. Instead, LASD implies a necessary condition using some bound functions, while a different sufficient condition using other bound functions implies LASD. Inference using the necessary condition shown in Theorem 3.6 is discussed in the online Supplemental Appendix. We remark that there may exist other features of the joint data distribution that do not depend only on pointwise features of the CDFs of changes and would result in a necessary and sufficient condition for LASD under partial identification. That is an interesting open question but is beyond the scope of this paper.

When the comparison is with the status quo distribution, the partially identified conditions simplify. Corollary 3.7 below shows what can be learned about LASD from bound functions in the partially identified case.

4 Inferring loss aversion-sensitive dominance

In this section we propose statistical inference methods for the loss aversion-sensitive dominance (LASD) criterion discussed in previous sections. We consider the null and alternative hypotheses

| (10) | ||||

Under the null hypothesis (10) policy dominates in the LASD sense, similar to much of the literature on stochastic dominance. It is a simplification of the hypotheses considered for several potential policies discussed in Linton, Maasoumi, and Whang (2005), who test whether one policy is maximal, and the techniques developed below could be extended to compare several policies in the same way in a straightforward manner.131313Linton, Maasoumi, and Whang (2005) consider a test for Prospect Theory by testing whether the integral of one CDF dominates the other. This paper considers a different approach in which we impose loss aversion on the value function, and then derive testable conditions on the CDFs. The null hypothesis above represents the assumption that policy is preferred by agents in the LASD sense. Rejection of the null implies that there is significant evidence for ambiguity in the ordering of the policies by LASD. Unfortunately, a drawback of the proposed procedure is that rejection of the null does not inform one about which sort of value function results in a rejection. Strong orderings of policies can result in more information, although they constrain by construction, and such exploration is left for future research.141414There is also another strand of literature that develops methods to estimate the optimal treatment assignment policy that maximizes a social welfare function. Recent developments can be found in Manski (2004), Dehejia (2005), Hirano and Porter (2009), Stoye (2009), Bhattacharya and Dupas (2012), Tetenov (2012), Kitagawa and Tetenov (2018, 2019), among others. These papers focus on the decision-theoretic properties and procedures that map empirical data into treatment choices. In this literature, our paper is most closely related to Kasy (2016), which focuses on welfare rankings of policies rather than optimal policy choice.

We consider tests for this null hypothesis given sample data observed under two different identification assumptions. We start with the case where one can directly observe samples and which represent agents’ gains and losses, or in other words, we simply assume that the distribution functions of and are point-identified and their distribution functions can be estimated using the empirical distribution functions from two samples. Next we extend these results to the partially-identified case where no assumption about the joint distribution of potential outcomes under either treatment is made. In this case, we assume that three samples are observable, , and , representing outcomes under a control or pre-policy state and outcomes under policies and . Then tests are based on plug-in estimates for bounds for and .

We consider distribution functions as members of the space of bounded functions on the support , denoted , equipped with the supremum norm, defined for by . For real numbers let . Given a sequence of bounded functions and limiting random element we write to denote weak convergence in in the sense of Hoffman-Jørgensen (van der Vaart and Wellner, 1996).

4.1 Inferring dominance from point identified treatment distributions

In this subsection we suppose that the pair of marginal distribution functions is identified. In the Online Supplemental Appendix C, we provide results extending the dominance tests to the case that distribution functions and are only partially identified.

4.1.1 Test statistics

To implement a test of the hypotheses (10) we employ the results of Theorem 3.1 to construct maps of into criterion functions that are used to detect deviations from the hypothesis . Specifically, recalling that , for the point-identified case we examine maps and , defined for each by

| (11) |

and

| (12) |

Functions and are designed so that large positive values will indicate a violation of the null. Taking as an example, Theorem 3.1 states that if and only if for all , so tests can be constructed by looking for where becomes significantly positive. We will refer to as maps from pairs of distribution functions to another function space, and also refer to them as functions.

The hypotheses (10) can be rewritten in two equivalent forms, depending on whether one uses or to transform distribution functions: letting be an evaluation set, we have

| (13) | ||||

and

| (14) | ||||

In the second set of hypotheses is a two-dimensional vector of zeros and inequalities are taken coordinate-wise.

The next step in testing the hypotheses (13) and (14) is to estimate and . Let denote the pair of marginal empirical distribution functions, that is, for . These are well-behaved estimators of the components of . Letting , standard empirical process theory shows that converges weakly to a Gaussian process under weak assumptions (van der Vaart, 1998, Example 19.6). In order to conduct inference for loss aversion-sensitive dominance, we use plug-in estimators for . See Remark B.1 in Appendix D for details on the computation of these functions.

In order to detect when is significantly positive, we consider statistics based on a one-sided supremum norm or a one-sided norm over . Kolmogorov-Smirnov (i.e., supremum norm) type statistics are

| (15) | ||||

| (16) |

Meanwhile Cramér-von Mises (or norm) test statistics are defined by

| (17) | ||||

| (18) |

Because all the CDFs used in these statistics belong to , distributions with bounded support, the integrands in the statistics are square-integrable.

4.1.2 Limiting distributions

We wish to establish the limiting distributions of and , for , under the null hypothesis . Two challenges arise when considering these test statistics. First, the form of the null hypothesis as a functional inequality to be tested uniformly over is a source of irregularity. Let the joint probability distribution of be denoted by . Because the null hypothesis, , is a functional weak inequality the asymptotic distributions of the test statistics and may depend on features of . This is referred to as non-uniformity in in (Linton, Song, and Whang, 2010; Andrews and Shi, 2013), and requires attention when resampling.

Second, due to the pointwise maximum function in its definition, is too irregular as a map from the data to the space of bounded functions to establish a limiting distribution for the empirical process using conventional statistical techniques. In contrast, is a linear map of , which implies that has a well-behaved limiting distribution in .151515The issues of a general lack of differentiability of functions arrived at by marginal optimization and a solution for inference based on directly characterizing the behavior of test statistics applied to such functions are studied in more generality in Firpo, Galvao, and Parker (2019). However, we highlight that the tests described here are extensions of the results of that paper and are specifically tailored to this application.

Despite the above challenges, we show that and (for ) have well-behaved asymptotic distributions, and furthermore, that the limiting random variables satisfy and . This is an important result because it is the foundation for applying bootstrap techniques for inference. Before stating the formal assumptions and asymptotic properties of the tests, we discuss the two difficulties mentioned above in more detail.

The limiting distributions of and statistics depend on features of . Let be the set of distributions such that . These are distributions with marginal distribution functions such that for all . To discuss the relationship between these sets of distributions and test statistics, we relabel the two coordinates of the function as

| (19) |

and

| (20) |

When , both and for all .

More detail is required about the behavior of the two coordinate functions to determine the limiting distributions of and statistics. For -norm statistics and , we define the following relevant subdomains of , which collect the arguments in the interior of where or are equal to zero:

| (21) | ||||

| (22) |

Denote as the set of where or at least one coordinate of equals for probability distribution . As will be seen below, is the same for both the and functions, and when it is non-empty, test statistics have a nondegenerate distribution. Following Linton, Song, and Whang (2010), we call the contact set for the distribution . Given the above definitions, under the null hypothesis we can write

On the other hand, the supremum-norm statistics and need a different family of sets, namely the sets of -maximizers of and . For any and , let

| (23) |

An important subset of are those for which test statistics have nontrivial limiting distributions under the null hypothesis — that is, not degenerate at 0, which occurs when there is some such that (note that there are no such that when ). Define to be the set of all such that . If then and because the distribution satisfies the null hypothesis, strictly dominates everywhere and the criterion functions are strictly negative over . When , test statistics have asymptotic distributions that are degenerate at zero because test statistics will detect that policy is strictly better that over all of . When , is zero over and test statistics have a nontrivial asymptotic distribution over . Thus, when , the asymptotic behavior of test statistics depends on whether or . Note that when , we have (that is, nonstochastic convergence in the sense of Painlevé-Kuratowski, see, e.g., Rockafellar and Wets (1998, p. 111)) for whichever coordinate function actually achieves the maximal value zero.

The second challenge for testing is related to the scaled difference as grows large. Hadamard differentiability is an analytic tool used to establish the asymptotic distribution of nonlinear maps of the empirical process. Definition D.1 in Appendix D provides a precise statement of the concept. When a map is Hadamard differentiable — for example , which is linear as a map from to and is thus trivially differentiable — the functional delta method can be applied to describe its asymptotic behavior as a transformed empirical process, and a chain rule makes the analysis of compositions of several Hadamard-differentiable maps tractable. Also, the Hadamard differentiability of a map implies resampling is consistent when this map is applied to the resampled empirical process (van der Vaart, 1998, Theorem 23.9) — so, for example, the distribution of resampled criterion processes is a consistent estimate of the asymptotic distribution of in the space . On the other hand, consider the map. The pointwise Hadamard directional derivative of at a given in direction is

| (24) |

This map, thought of as a map between function spaces, and , is not differentiable because the scaled differences converge to the above derivative at each point , but may not converge uniformly in . Despite the lack of differentiability of the map , we show in Lemma D.3 in Appendix D that the maps and are Hadamard directionally differentiable, which implies these maps are just regular enough that existing statistical methods can be applied to their analysis. Later in this section we apply the resampling technique recently developed in Fang and Santos (2019) along with this directional differentiability to describe hypothesis tests using or .

Having discussed the difficulties in the relationship between distributions and test statistics, we turn to assumptions on the observations. In order to conduct inference using either or we make the following assumptions.

-

A1

The observations and are iid samples and independent of each other and are continuously distributed with marginal distribution functions and respectively.

-

A2

Let the sample sizes and increase in such a way that as , where for . Define .

Under these assumptions we establish the asymptotic properties of the test statistics under the null and fixed alternatives. Under the above assumptions, there is a Gaussian process such that . We denote each coordinate process and , and for convenience define two transformed processes: for each let

| (25) | ||||

| (26) |

These will be used in the theorem below.

Theorem 4.1.

Theorem 4.1 derives the asymptotic properties of the proposed test statistics. Parts 1 and 2 establish the weak limits of and for when the null hypothesis is true. Recall that when , , which is why terms are absent in the first part of the theorem. Remarkably, the test statistics using and criterion processes have the same asymptotic behavior despite the different appearances of the underlying processes and the irregularity of . Part 3 shows that the statistics are asymptotically degenerate at zero when the contact set is empty, that is, when lies on the interior of the null region. Part 4 shows that the test statistics diverge when data comes from any distribution that does not satisfy the null hypothesis.

The limiting distributions described in Part 1 of Theorem 4.1 are not standard because the distributions of the test statistics depend on features of through the terms in each expression. Therefore, to make practical inference feasible, we suggest the use of resampling techniques below.

4.1.3 Resampling procedures for inference

The proposed test statistics have complex limiting distributions. In this subsection, we present resampling procedures to estimate the limiting distributions of both and for under the assumption that . Naive use of bootstrap data generating processes in the place of the original empirical process suffers from distortions due to discontinuities in the directional derivatives of the maps that define the distributions of the test statistics. In finite samples the plug-in estimate will not find, for example, the region where , where the derivatives exhibit discontinuous behavior. Our procedure involves making estimates of the derivatives involved in the limiting distribution and a standard exchangeable bootstrap routine, as proposed in Fang and Santos (2019).161616Given a set of weights that sum to one and are independent of , the exchangeable bootstrap measure is a randomly-weighted measure that puts mass at observed sample point for each . This encompasses, for example, the standard bootstrap, -of- bootstrap and wild bootstrap. See Section 3.6.2 of van der Vaart and Wellner (1996) for more specific details.

In order to estimate contact sets, define a sequence of constants such that and and let and . Then for statistics define estimated contact sets by

| (27) | ||||

| (28) |

When both sets are empty, replace both estimates by , as suggested in Linton, Song, and Whang (2010) to ensure nondegenerate bootstrap reference distributions. Meanwhile, for statistics define estimated -maximizer sets. For a sequence of constants such that and , let

| (29) | ||||

| (30) |

Although the null hypothesis may imply that the maximum is zero, the above formulas use the maximum of the sample analog without setting its maximum equal to zero, which is important for ensuring non-empty set estimates. Using these estimates, the distributions of and can be estimated from sample data (recall that Part 2 of Theorem 4.1 asserts that these are the same distributions as those of and ). We conducted simulation experiments to choose these parameters using a few simulated data-generating processes, which are briefly discussed in the appendix in the context of simulations that suggest that the resulting tests have correct size and good power. Scaling the estimated processes by their pointwise standard deviation functions when estimating contact sets as in Lee, Song, and Whang (2018) might result in better performance when distribution functions are evaluated near their tails, but we leave that rather complex topic for future research.

Resampling routine to estimate the distributions of and for :

-

1.

If using a Cramér-von Mises statistic, given a sequence of constants , estimate the contact sets and . If using a Kolmogorov-Smirnov statistic, given a sequence of constants , estimate the -maximizer sets of and .

Next repeat the following two steps for :

-

2.

Construct the resampled processes

using an exchangeable bootstrap.

-

3.

Calculate the resampled test statistic. Letting and satisfy , calculate

(31) or

(32)

Finally,

- 4.

The formulas in part 3 of the steps above are obtained by inserting estimated contact sets and resampled empirical processes in the place of population-level quantities into the functions shown in part 1 of Theorem 4.1.

The resampled statistics are calculated by imposing the null hypothesis and assuming that the region is the only part of the domain that provides a nondegenerate contribution to the asymptotic distribution of the statistic under the null. The two cases of each part in the maximum arise from trying to impose the null behavior on the resampled supremum norm statistics, even when it appears the null is violated based on the value of the sample statistic. A simple alternative way to conduct inference would be to assume the least-favorable null hypothesis that , and to resample using all of . However, this may result in tests with lower power (Linton, Song, and Whang, 2010) — power loss arises in situations where (strictly), so that the process is only nondegenerate on a subset, while bootstrapped processes that assume would look over all of and result in a stochastically larger bootstrap distribution than the true distribution.

The next result shows that our tests based on the resampling schemes described above have accurate size under the null hypothesis. In order to metrize weak convergence we use test functions from the set , which denotes Lipschitz functions that have constant 1 and are bounded by 1.

Theorem 4.2.

Make assumptions A1-A2 and suppose that . Let denote the sample observations. Then for , the bootstrap is consistent:

and

where and are defined in Theorem 4.1. In particular, when the resampling procedure outlined above results in asymptotically valid inference: for any , letting and ,

and

with equality when the distributions of and are strictly increasing at their -th quantiles.

The result in above theorem is stated in terms of the limiting variables and and bootstrap analogs. and , using the functional delta method, are Hadamard directional derivatives of a chain of maps from the marginal distribution functions to the real line, and the derivatives are most compactly expressed as the definitions in Theorem 4.1.

The bootstrap variables combine conventional resampling with finite-sample estimates of the maps defined in Part 1 of Theorem 4.1, which is a resampling approach proposed in Fang and Santos (2019). Their result is actually more general — it states that with a more flexible estimator , we would obtain bootstrap consistency for in the null and alternative regions. Because our focus is on testing , however, our resampling scheme, and Theorem 4.2, are done under the imposition of the null hypothesis. The resampling consistency result in Theorem 4.2 implies that our bootstrap tests have asymptotically correct size for all probability distributions in the null region, in the same sense as was stressed in Linton, Song, and Whang (2010). A formal statement showing size control over all of is given in Theorem 4.3 in Appendix D. Along with Part 4 of Theorem 4.1, Theorem 4.3 additionally implies that our tests are consistent, that is, that their power to detect violations from the null represented by fixed alternative distributions tends to one. This is because the resampling scheme produces asymptotically bounded critical values, while the test statistics diverge under the alternative.

The behavior of bootstrap tests under the null and alternatives is most easily examined using distributions local to . We consider sequences of distributions local to the null distribution such that for a mean-zero, square-integrable function , have distribution functions (where has CDF ) that satisfy

| (33) |

The behavior of the underlying empirical process under local alternatives satisfies Assumption 5 of Fang and Santos (2019) in a straightforward way (Wellner, 1992, Theorem 1).

Theorem 4.3.

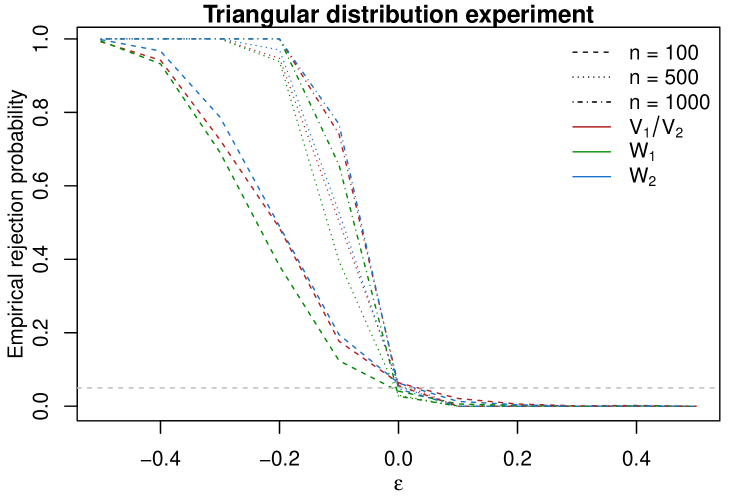

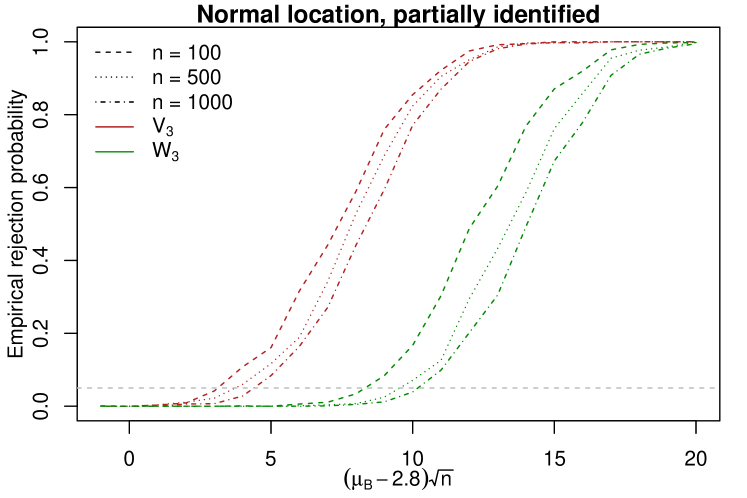

In the Supplemental Appendix we provide Monte Carlo numerical evidence of the finite sample properties of both point- and partially-identified methods. The simulations show that tests have empirical size close to the nominal, and high power against selected alternatives.

5 Empirical illustration

In this section we briefly illustrate the use of our approach using household-level data from a well-known experimental evaluation of alternative welfare programs in the state of Connecticut, documented in Bitler, Gelbach, and Hoynes (2006). Aid to Families with Dependent Children (AFDC) was one of the largest federal assistance programs in the United States between 1935 and 1996. It consisted of a means-tested income support scheme for low-income families with dependent children, administered at the state level, but funded at the federal level. Following criticism that this program discouraged labor market participation and perpetuated welfare dependency, the Clinton administration enacted the 1996 Personal Responsibility and Work Opportunity Reconciliation Act (PRWORA), requiring all US states to replace AFDC with a Temporary Assistance for Needy Families (TANF) program. TANF programs differed amongst US states and were all fundamentally different from AFDC: they included strict time limits for the receipt of benefits and, simultaneously, generous earnings disregard schemes to incentivise work.

Under the policy framework of TANF, the state of Connecticut launched its own program, called Jobs First (JF) in 1996: this included the strictest time limit and also the most generous earnings disregard of all the US states. Nonetheless, there was a transition period during which a policy experiment was conducted by the Manpower Demonstration and Research Corporation (MDRC). A random sample of approximately 5000 welfare applicants was randomly assigned to one of two groups: half of them were assigned to JF and faced its eligibility and program rules; the other half were randomly assigned to AFDC (the program that JF aimed to replace in the state of Connecticut), thereby facing AFDC eligibility and program rules.

The MDRC experimental data include rounded data on quarterly income for a pre-program assignment period and also for a post-program assignment period, thereby allowing one to quantify and compare the income gains and losses experienced by the households that were randomly assigned to JF and ADFC171717Bitler, Gelbach, and Hoynes (2006) conduct a test comparing features of households before random assignment and find that they do not differ significantly in terms of observable characteristics. We check additionally that the income distributions were the same before the experiment split households among the two policies. We use a conventional two-sided Cramér-von Mises test for the equality of distributions. The statistic was approximately and its p-value was , implying that before the experiment, the distributions are indistinguishable. Bitler, Gelbach, and Hoynes (2006) use these experimental data to compare the distribution of income between the beneficiaries of AFDC and JF. They find that while JF made the majority of individuals better-off, it also made a significant number of worse-off, especially after the JF time limit kicks in and becomes binding.181818Bitler, Gelbach, and Hoynes (2006) focus on quantile treatment effects (QTEs). If QTEs were to be used as a measure of the impact on any individual household in a welfare comparison, it would require the assumption of rank invariance across potential outcome distributions, which would be quite strong. Note that Bitler, Gelbach, and Hoynes (2006) do not make this assumption. In our simple empirical illustration we draw on Bitler, Gelbach, and Hoynes (2006) and consider “AFDC” and “JF” as our alternative policies (equivalent to policies and in the previous sections). We illustrate our methods by constructing a LASD partial order to support a policy choice between these two programs191919Although not directly relevant for our empirical illustration, it can be mentioned that the debate on the replacement of AFDC by TANF combined political economy concerns and also normative considerations about the appropriateness of policy-makers causing income losses to parts of the population. Alesina, Glaeser, and Sacerdote (2001) use the AFDC as an empirical proxy for the generosity of the welfare state in the US and show that changes to this program had the potential to sway the electorate. At the same time, normative arguments supporting policy-makers’ loss-aversion have also been put forth in this context. Peter Edelman, then a senior advisor to President Clinton, resigned in protest against this policy change, calling the replacement of ADFC by TANF a ”crucial moral litmus test”, as it risked causing important income losses to some households. and comparing it with the partial ordering that would emerge if loss aversion were not taken into consideration using conventional first order stochastic dominance (FOSD).202020Because assignment is random, we assume that the distribution functions of gains and losses under each policy, and , are point-identified by the differences in incomes before and after random assignment. Along the lines of Bitler, Gelbach, and Hoynes (2006) we make this comparison separately for the time period up until the JF time limit for the receipt of welfare benefits becomes binding and for the period after that.

5.1 JF vs AFDC: LASD ordering

To make welfare decisions in terms of gains and losses, we use data on household income changes, i.e. the difference between households’ income after exposure to the program (JF or AFDC) and before exposure to that program. We make this analysis separately for the period before the JF time limit become binding (TL) and for after that. We thus call pre-TL observations those that were made after random assignment to either of the policies (JF or AFDC) but before the time limit; we call post-TL observations those made after the JF time limit. We summarize household income (for both policies and pre/post TL periods) by averaging income over all quarters in the relevant time span.212121We explored alternative definitions of our outcome of interest such as using the final quarter within the time span; generally these led to the same results, so we will not show them for the purpose of this simple illustration. Changes in household income due to the AFDC and JF policies were defined as the natural logarithm of the average household income in all post-policy quarters (either JF or AFDC) minus the natural log of the average pre-policy quarterly household income. Thus, our analysis applies LASD to these changes in two separate periods, the pre-TL period and the post-TL one.

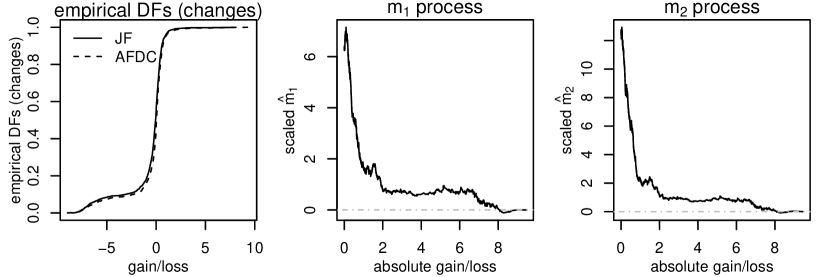

The left-hand side of Table LABEL:tab:pointIDtests shows the results of formal tests of the hypothesis (10) using statistics (Cramér-von Mises statistics applied to the empirical process).222222Results for the other test statistics are qualitatively the same. They are collected in an Online Supplemental Appendix. For the pre-time limit period we cannot reject the hypothesis that .232323For this time period we cannot even reject the null of equality in the distributions of changes in income between households assigned to JF and AFDC. However, everything changes when we make this comparison taking into account the post-time limit period. As mentioned above, after the time limit becomes binding, Bitler, Gelbach, and Hoynes (2006) show that a sizeable number of households in JF experience total income losses, as they stop receiving welfare transfers; this does not happen amongst households on ADFC, which does not have a time limit. In order to rank the distribution of income changes under JF and AFDC using LASD we test the hypothesis that . As shown in the left-hand side of Table 1, this hypothesis is rejected for every significance level, reflecting the greater weight placed on the income losses experienced by JF beneficiaries.

[botcap,caption=Tests for inferring whether the Jobs First (JF) program would be preferred to the Aid to Families with Dependent Children (AFDC). Column titles paraphrase the null hypotheses in the tests. The first column uses changes in income and the second column measures income in levels without regard to pre-policy income. 1999 bootstrap repetitions used in each test.,label=tab:pointIDtests,pos=!tbp,]lccc\FL LASD FOSD \NN \MLBefore JF time limit\NNp-value\NNAfter JF time limit\NNp-value\LL

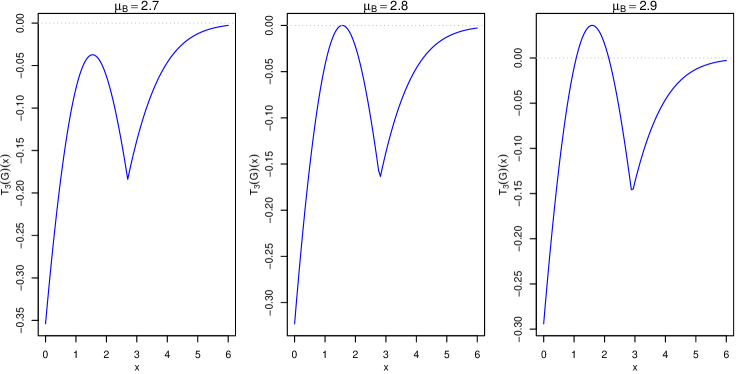

To investigate how this rejection occurs, Figure 1 displays the CDFs of gains and losses under the AFDC and JF policies around the JF time limit, then the way that the two coordinate processes compare them — when looking at the coordinates in equation (12), large positive values correspond to a rejection of the hypothesis . The positive parts of the and functions illustrated in the middle and right-hand plots of Figure 1 are squared and integrated over estimated contact sets to arrive at the test statistic in the lower left of Table LABEL:tab:pointIDtests. It can be seen in the second and third panels that the presumable reason that the JF policy does not dominate the AFDC policy using LASD is because the distribution of small gains and losses is more appealing in the AFDC program and the relation between small gains and small losses is preferable to JF.

5.2 JF vs AFDC: first order stochastic dominance ordering

What difference would it make if loss-aversion had been left out of this welfare ordering of social policies? In order to address this question we compare the welfare ordering obtained in the previous section with that obtained by ordering JF and AFDC according to first order stochastic dominance (FOSD). Using FOSD, the only relevant comparison is between the post-policy household income under JF and AFDC (household income before exposure to these policies is not material). We thus define our outcome of interest in levels, i.e. the natural log of the average household income under JF or AFDC. As before, we do this analysis separately for the two relevant time periods: before the JF time limit becomes binding and after it does.

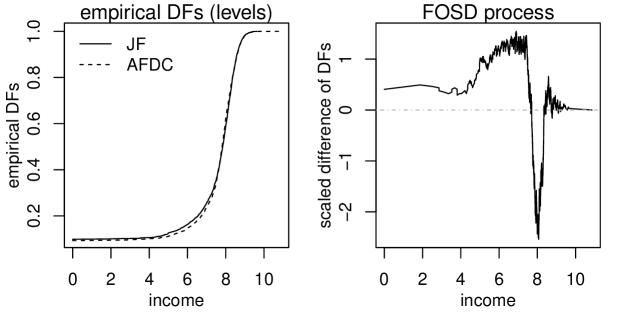

The right-hand side of Table 1 shows the result of our FOSD tests. Either way post-policy outcomes are measured, we cannot reject the null that . When measurements are made before and after exposure to the policy this is unsurprising, as prior to the JF time limit becoming binding none of the policies produces large income losses. However, even after the JF time limit becomes binding, the FOSD test still does not allow us to reject , while the LASD test would lead us to categorically reject the dominance of JF over AFDC. This simple empirical illustration shows that, in practice, the consideration of loss aversion can change the welfare ordering of social policies.

Figure 2 shows an analogous investigation into the way analysis would typically be conducted using first order stochastic dominance to compare outcomes, using contact sets as in Linton, Song, and Whang (2010). The contact set was estimated using , corresponding to the tuning parameter choice of that paper, for both the FOSD and LASD tests (the smaller sequence was used for estimating near-maximizing sets in LASD tests). The left-hand plot in the figure shows the empirical distribution functions of outcomes under each program after the JF time limit. That is, the functions are based on levels of income rather than changes in income. The scaled difference is displayed as the criterion function in the right-hand side of the panel, and the square of the positive part of this function is integrated over an estimated contact set. As the lower-right test in Table LABEL:tab:pointIDtests indicates, these differences are sometimes mildly positive, so that is occasionally below (especially at lower income levels) but the difference is not large enough to indicate a rejection of the hypothesis that , as indicated by the p-value of the test. Because outcomes are measured in levels, there is no way to measure whether they represent gains or losses for agents, and so a simple difference is used here instead of the comparison that accounts for loss aversion used with changes in income.

6 Conclusion

Public policies often result in gains for some individuals and losses for others. We define a social preference relation for distributions of gains and losses caused by a policy: loss aversion-sensitive dominance (LASD). We relate these social preferences to criteria that depend solely on distribution functions. The assumption of loss aversion can lead to a welfare ranking of policies that is different from the one that would be brought about if classic utility theory and first-order stochastic dominance were used. We then propose empirically testable conditions for LASD based on our CDF-based criterion functions. Because data may come as differences between underlying random variables, we propose a point-identified version of these conditions and also a partially identified analog. We develop inference methods to formally test LASD relations and derive the corresponding statistical properties. We show that resampling techniques, tailored to specific features of the criterion functions, can be used to conduct inference. Finally, : illustrate our LASD criterion and inference methods with a simple empirical application that uses data from a well known evaluation of a large income support policy in the US. This shows that the ranking of policy options depends crucially on whether changes or levels are used and whether or not one takes individual loss aversion into account.

Appendix

Appendix A Proof of results

A.1 Results in Section 2

Proof of Proposition 2.3.

Equation (1) implies that

| (34) |

We will now re-write the two parts of (34) using integration by parts, normalization and the fact that has bounded support i.e. there exist and such that , in which case we have and =0. For the first part of (34) we obtain

and for the second part (34) we have

Putting these two parts together yields (2). ∎

A.2 Proofs of results in Section 3

Proof of Theorem 3.1.

Notice that (3) is equivalent to both (4) and (5); in this proof we use the latter two conditions. Using Proposition 2.3 we rewrite as the equivalent condition

Rearranging terms we find this is equivalent to

or simply

This is in turn equivalent to

or

Adding to both sides we find this is equivalent to

| (35) |

Utilizing the assumptions of loss aversion and non-decreasingness given in Definition 2.2, (4) and (5) are sufficient for (35) to hold for any . Condition (5) is due to the fact that

| is equivalent to the condition | ||||

We now show that conditions (4) and (5) are also necessary by means of a contradiction to (35). To this end, assume that there exists some such that . From the fact that the distribution function is right continuous, it follows that there is a neighbourhood , , such that for all , . For arbitrarily small , consider the value function

Note that this satisfies Definition 2.2. Further, for , . Therefore

while

because for . This contradicts (35).

The second condition can be proven similarly. Assume that there exists a neighbourhood , such that for all , . Take . Using we find

while

which is a contradiction.

∎

Proof of Corollary 3.5.

Proof of Theorem 3.6.

Proof of Corollary 3.7.

Recall Corollary 3.5 implied that when is a status quo distribution, the FOSD and LASD relations are equivalent. Then implies that for all because for all . Therefore a sufficient condition for is that for all . Similarly, if , equivalent to , then it must be the case that for all , implying that as well. ∎

A.3 Results in Section 4

Proof of Theorem 4.1.

For Part 1 note that if then by definition, for some and for all , . For any such that , that set is the limit of in the Painlevé-Kurotowski sense as , because form a monotone sequence of sets and Exercise 4.3 of Rockafellar and Wets (1998) implies the limit is . Then the supremum is achieved and (in the Painlevé-Kuratowski sense) for at least one coordinate, so that suprema are taken over at least one of and and whichever coordinate satisfies this condition will contribute to the asymptotic distribution. Note that for all , . Lemma D.3 and the null hypothesis, which implies for , imply the result for and .

To show Part 2, note that is a linear map of , and assuming that for , we have that its weak limit (for whichever set is nonempty) is by Lemma D.3. Breaking into its two subsets and assuming the null hypothesis is true results in the same behavior as the supremum norm statistic from the first part (using the definition of the supremum norm in two coordinates as the maximum of the two suprema). The same reasoning holds for the statistic in Part 2.

Part 3 follows from the behavior of the test statistics over described in Lemma D.3. To show Part 4 for suppose that for some , . Then . Then

where the last convergence follows from the delta method applied to , which converges in distribution to a tight random variable. The proof for the other statistics is analogous. ∎

Proof of Theorem 4.2.

This theorem is an application of Theorems 3.2 and 3.3 of Fang and Santos (2019). Define the statistics and as maps from to the real line using and defined in equations (55) and (56) in Lemma D.3, and let their estimators be defined as in part 3 of the resampling scheme. Their Assumptions 1-3 are satisfied either by the definitions of and and Lemma D.3, the standard convergence result (van der Vaart and Wellner, 1996, Theorem 2.8.4) and the choice of bootstrap weights. We need to show that their Assumption 4 is also satisfied. Write either function as using the desired norm. Both norms satisfy a reverse triangle inequality, and using the fact that , the difference for two functions and is bounded by . The first difference is bounded by , and the second and the third are bounded by . Rewriting equations (31) and (32) as functionals of differential directions , define

and

| (37) |

Because both and are Lipschitz, Lemma S.3.6 of Fang and Santos (2019) implies we need only check that and for each fixed . This follows from the consistency of the contact set and -argmax estimators. The consistency of these estimators follow from the uniform law of large numbers for the -maximizing sets, and the tightness of the limit for the contact sets, which implies that . ∎

References

- (1)

- Aaberge, Havnes, and Mogstad (2018) Aaberge, R., T. Havnes, and M. Mogstad (2018): “Ranking Intersecting Distribution Functions,” Journal of Applied Econometrics, forthcoming.

- Alesina, Glaeser, and Sacerdote (2001) Alesina, A., E. Glaeser, and B. Sacerdote (2001): “Why Doesn’t the US Have a European-Style Welfare System,” NBER working paper 8524.

- Alesina and Passarelli (2019) Alesina, A., and F. Passarelli (2019): “Loss Aversion, Politics and Redistribution,” American Journal of Political Science, 63, 936–947.

- Andrews and Shi (2013) Andrews, D. W., and X. Shi (2013): “Inference Based on Conditional Moment Inequalities,” Econometrica, 81, 609–666.

- Atkinson (1970) Atkinson, A. B. (1970): “On the Measurement of Inequality,” Journal of Economic Theory, 2, 244–263.

- Barrett and Donald (2003) Barrett, G. F., and S. G. Donald (2003): “Consistent Tests for Stochastic Dominance,” Econometrica, 71, 71–104.

- Bhattacharya and Dupas (2012) Bhattacharya, D., and P. Dupas (2012): “Inferring Welfare Maximizing Treatment Assignment under Budget Constraints,” Journal of Econometrics, 167, 168–196.

- Bitler, Gelbach, and Hoynes (2006) Bitler, M. P., J. B. Gelbach, and H. W. Hoynes (2006): “What Mean Impacts Miss: Distributional Effects of Welfare Reform Experiments,” American Economic Review, 96, 988–1012.

- Boyd and Vandenberghe (2004) Boyd, S., and L. Vandenberghe (2004): Convex Optimization. Cambridge University Press, Cambridge.

- Cárcamo, Cuevas, and Rodríguez (2020) Cárcamo, J., A. Cuevas, and L.-A. Rodríguez (2020): “Directional Differentiability for Supremum-Type Functionals: Statistical Applications,” Bernoulli, 26, 2143–2175.

- Carneiro, Hansen, and Heckman (2001) Carneiro, P., K. T. Hansen, and J. J. Heckman (2001): “Removing the Veil of Ignorance in Assessing the Distributional Impacts of Social Policies,” Swedish Economic Policy Review, 8, 273–301.

- Cattaneo, Jansson, and Nagasawa (2020) Cattaneo, M. D., M. Jansson, and K. Nagasawa (2020): “Bootstrap-Based Inference for Cube Root Asymptotics,” Econometrica, 88, 2203–2219.

- Chetverikov, Santos, and Shaikh (2018) Chetverikov, D., A. Santos, and A. M. Shaikh (2018): “The Econometrics of Shape Restrictions,” Annual Review of Economics, 10, 31–63.

- Chew (1983) Chew, S. H. (1983): “A Generalization of the Quasilinear Mean with Applications to the Measurement of Income Inequality and Decision Theory Resolving the Allais Paradox,” Econometrica, 51, 1065–1092.

- Cho and White (2018) Cho, J. S., and H. White (2018): “Directionally Differentiable Econometric Models,” Econometric Theory, 34, 1101–1131.

- Christensen and Connault (2019) Christensen, T., and B. Connault (2019): “Counterfactual Sensitivity and Robustness,” Working paper.

- Dehejia (2005) Dehejia, R. (2005): “Program Evaluation as a Decision Problem,” Journal of Econometrics, 125, 141–173.

- Easterly (2009) Easterly, W. (2009): “The Burden of Proof Should Be on Interventionists – Doubt Is a Superb Reason for Inaction,” Boston Review – series Development in dangerous places.

- Eeckhoudt and Schlesinger (2006) Eeckhoudt, L., and H. Schlesinger (2006): “Putting Risk in Its Proper Place,” American Economic Review, 96, 280–289.

- Eyal (2020) Eyal, N. (2020): “Why Challenge Trials of SARS-CoV-2 Vaccines Could Be Ethical Despite Risk of Severe Adverse Events,” Ethics & Human Research.

- Fan, Guerre, and Zhu (2017) Fan, Y., E. Guerre, and D. Zhu (2017): “Partial Identification of Functionals of the Joint Distribution of “Potential Outcomes”,” Journal of Econometrics, 197, 42–59.

- Fan and Park (2010) Fan, Y., and S. S. Park (2010): “Sharp Bounds on the Distribution of Treatment Effects and Their Statistical Inference,” Econometric Theory, 26, 931–951.

- Fan and Park (2012) (2012): “Confidence Intervals for the Quantile of Treatment Effects in Randomized Experiments,” Journal of Econometrics, 167, 330–344.

- Fang and Santos (2019) Fang, Z., and A. Santos (2019): “Inference on Directionally Differentiable Functions,” Review of Economic Studies, 86, 377–412.

- Firpo, Galvao, and Parker (2019) Firpo, S., A. F. Galvao, and T. Parker (2019): “Uniform inference for value functions,” arXiv e-prints, p. arXiv:1911.10215.

- Firpo and Ridder (2008) Firpo, S., and G. Ridder (2008): “Bounds on Functionals of the Distribution of Treatment Effects,” IEPR Working Paper No. 08-09.

- Firpo and Ridder (2019) (2019): “Partial Identification of the Treatment Effect Distribution and Its Functionals,” Journal of Econometrics, 213, 210–234.

- Fishburn (1980) Fishburn, P. C. (1980): “Continua of Stochastic Dominance Relations for Unbounded Probability Distributions,” Journal of Mathematical Economics, 7, 271–285.

- Frank, Nelsen, and Schweizer (1987) Frank, M. J., R. B. Nelsen, and B. Schweizer (1987): “Best-Possible Bounds for the Distribution of a Sum — A Problem of Kolmogorov,” Probability Theory and Related Fields, 74, 199–211.

- Freund and Özden (2008) Freund, C., and c. Özden (2008): “Trade Policy and Loss Aversion,” American Economic Review, 98, 1675–1691.

- Gajdos and Weymark (2012) Gajdos, T., and J. A. Weymark (2012): “Introduction to Inequality and Risk,” Journal of Economic Theory, 147, 1313–1330.

- Heckman, Smith, and Clements (1997) Heckman, J. J., J. Smith, and N. Clements (1997): “Making the Most Out of Programme Evaluations and Social Experiments: Accounting for Heterogeneity in Programme Impacts,” Review of Economic Studies, 64, 487–535.

- Heckman and Smith (1998) Heckman, J. J., and J. A. Smith (1998): “Evaluating the Welfare State,” in Econometrics and Economic Theory in the Twentieth Century: The Ragnar Frisch Centennial Symposium, ed. by S. Strom. Cambridge University Press, New York.

- Hirano and Porter (2009) Hirano, K., and J. Porter (2009): “Asymptotics for Statistical Treatment Rules,” Econometrica, 77, 1683–1701.

- Hong and Li (2018) Hong, H., and J. Li (2018): “The Numerical Delta Method,” Journal of Econometrics, 206, 379–394.

- Kahneman and Tversky (1979) Kahneman, D., and A. Tversky (1979): “Prospect Theory: An Analysis of Decision Under Risk,” Econometrica, 47, 263–292.

- Kasy (2016) Kasy, M. (2016): “Partial Identification, Distributional Preferences, and the Welfare Ranking of Policies,” Review of Economics and Statistics, 98, 111–131.

- Kitagawa and Tetenov (2018) Kitagawa, T., and A. Tetenov (2018): “Who Should Be Treated? Empirical Welfare Maximization Methods for Treatment Choice,” Econometrica, 86, 591–616.

- Kitagawa and Tetenov (2019) (2019): “Equality-Minded Treatment Choice,” Journal of Business and Economic Statistics, forthcoming.

- Lee, Song, and Whang (2018) Lee, S., K. Song, and Y.-J. Whang (2018): “Testing For a General Class of Functional Inequalities,” Econometric Theory, 34, 1018–1064.

- Levy (2016) Levy, H. (2016): Stochastic Dominance: Investment Decision Making Under Uncertainty, 3rd edition. Springer International Publishing, Switzerland.

- Linton, Maasoumi, and Whang (2005) Linton, O., E. Maasoumi, and Y.-J. Whang (2005): “Consistent Testing for Stochastic Dominance Under General Sampling Schemes,” Review of Economic Studies, 72, 735–765.

- Linton, Song, and Whang (2010) Linton, O., K. Song, and Y.-J. Whang (2010): “An Improved Bootstrap Test of Stochastic Dominance,” Journal of Econometrics, 154, 186–202.

- Makarov (1982) Makarov, G. (1982): “Estimates for the Distribution Function of a Sum of Two Random Variables when the Marginal Distributions are Fixed,” Theory of Probability and its Applications, 26(4), 803–806.

- Mankiw (2014) Mankiw, G. (2014): “When the Scientist is also a Philosopher,” New York Times – Business.

- Manski (2004) Manski, C. F. (2004): “Statistical Treatment Rules for Heterogeneous Populations,” Econometrica, 72, 1221–1246.