S. Somin, G. Gordon, A .Pentland, E. Shmueli and Y. Altshuler

11institutetext: MIT Media Lab, Cambridge, MA, USA

11email: shaharso@media.mit.edu

22institutetext: Industrial Engineering Department, Tel Aviv University, Israel

33institutetext: Endor Ltd.

ERC20 Transactions over Ethereum Blockchain: Network Analysis and Predictions

Abstract

Following the birth of Bitcoin and the introduction of the Ethereum ERC20 protocol a decade ago, recent years have witnessed a growing number of cryptographic tokens that are being introduced by researchers, private sector companies and NGOs. The ubiquitous of such Blockchain based cryptocurrencies give birth to a new kind of rising economy, which presents great difficulties to modeling its dynamics using conventional semantic properties. Our work presents the analysis of the dynamical properties of the ERC20 protocol compliant crypto-coins’ trading data using a network theory prism. We examine the dynamics of ERC20 based networks over time by analyzing a meta-parameter of the network — the power of its degree distribution. Our analysis demonstrates that this parameter can be modeled as an under-damped harmonic oscillator over time, enabling a year forward of network parameters predictions.

1 Introduction

Blockchain technology, which has been known by mostly small technological circles up until recently, is bursting throughout the globe, with a potential economic and social impact that could fundamentally alter traditional financial and social structures. Launched in July 2015 [1], the Ethereum Blockchain is a public ledger that keeps publicly accessible records of all Ethereum related transactions. The ability of the Ethereum Blockchain to store not only ownership, similarly to the Bitcoin Blockchain, but also execution code, in the form of ”Smart Contracts”, has recently led to the creation of an immense number of new types of ”tokens”, based on the Ethereum ERC20 protocol.

Apart from providing full data of prices, volumes and holders distribution, the ERC20 transactional data also presents the monetary activity of anonymous individuals, which is otherwise scarce and hard to obtain due to confidentiality and privacy control. Thereby, this ERC20 digital ecosystem intrinsically provides a rare opportunity to analyze and model financial behavior in an evolving market over a long period of time. Specifically, understanding the governing forces upon this emerging economy, and in turn being able to perform accurate predictions of the economy’s state are fundamental, as this market is becoming increasingly relevant to the traditional financial world.

In this work we aim to broaden our comprehension of the dynamics this financial ecosystem undergoes, from a network theory perspective. Specifically, we first demonstrate how the dynamics of the degree distribution’s power parameter can be modeled by an under-damped oscillator with zero-mean Gaussian noise. In turn, this analytical model enables us to predict network’s dynamics, reliably predicting a whole year forward in time.

2 Background and Related Work

Blockchain’s ability to process transactions in a trust-less environment, apart from trading its official cryptocurrency, the Ether, presents the most prominent framework for the execution of ”Smart Contracts” [2]. Smart Contracts are computer programs, formalizing digital agreements, automatically enforced to execute any predefined conditions using the consensus mechanism of the Blockchain, without relying on a trusted authority. They empower developers to create diverse applications in a Turing Complete Programming Language, executed on the decentralized Blockchain platform, enabling the execution of any contractual agreement and enforcing its performance.

Moreover, Smart Contracts allow companies or entrepreneurs to create their own proprietary tokens on top of the Blockchain protocol [3]. These tokens are often pre-mined and sold to the public through Initial Coin Offerings (ICO) in exchange of Ether, other crypto-currencies, or Fiat Money. The issuance and auctioning of dedicated tokens assist the venture to crowd-fund their project’s development, and in return, the ICO tokens grant contributors with a redeemable for products or services the issuer commits to supply thereafter, as well as the opportunity to gain from their possible value increase due to the project’s success. The most widely used token standard is Ethereum’s ERC20 (representing Ethereum Request for Comment), issued in 2015. The protocol defines technical specifications giving developers the ability to program how new tokens will function within the Ethereum ecosystem.

There has been a surge in recent years in the attempt to model social dynamics via statistical physics tools [4], ranging from opinion dynamics, through crowd behaviors to language dynamics. The physical tools used are also varied, ranging from Ising models [5] to topology analysis [4]. More specifically, previous studies have implemented physics-based approaches to the analysis of economic markets. Econophysics have attempted to describe the dynamical nature of the economy with different, and increasingly sophisticated physical models. Frisch [6], who started this trend, has suggested to use a damped oscillator model to the economy post wars or disasters, with the assumption that there is an equilibrium state that has been perturbed. Since then, many new models have been suggested, ranging from quantum mechanical models [7, 8] to chaos theory [9, 10]. However, all of these models have attempted to describe the economy, represented by a singular value, e.g. stock market prices, whereas the underlying network of the economy has not been addressed.

Network science, however, has exceedingly contributed to multiple and diverse scientific disciplines in the past two decades, by examining exactly diverse network related parameters. Applying network analysis and graph theory have assisted in revealing the structure and dynamics of complex systems by representing them as networks, including social networks [11, 12, 13], computer communication networks [14], biological systems [15], transportation [16, 17], IOT [18], emergency detection [19] and financial trading systems [20, 21, 22].

Most of the research conducted in the Blockchain world, was concentrated in Bitcoin, spreading from theoretical foundations [23], security and fraud [24, 25] to some comprehensive research in network analysis [26, 27, 28]. The world of Smart contracts has recently inspired research in aspects of design patterns, applications and security [29, 30, 31, 32], policy towards ICOs has also been studied [3]. Some preliminary results examining network theory’s applicability to ERC20 tokens has been made in [33, 34], specifically by validating that this financial ecosystem, when considered as a network of interactions, adheres to key network theory principles, such as power-law degree distribution.

In this paper we aim to examine how this prominent field can enhance the understanding of the underlying structure of the ERC20 tokens trading data, model it’s stabilization process as a network over time and achieve predictive abilities.

3 Methodology

3.1 Power-Law Fit

The degree distribution of a given graph is plotted on a double logarithmic scale, over 20 logarithmically spaced bins, between the minimal and maximal degrees of relevant graph. We’ve selected splitting the data along 20 bins, in order to accomodate both small networks, having small sets of vertices and consequently possibly small degree sequences, and also large networks obtaining much larger variance of the degree set.

Several approaches are known in literature for fitting the power law distribution to a linear model in the double logarithmic scale and for estimating its goodness-of-fit, see for example [35]. In this paper, we have chosen to fit the bins’ heights to a Linear Model, using ordinary Least Squares Regression, while considering all binned data points, and not only their tail. We further chose to verify the goodness-of-fit of the power-law model to the degree distribution by calculating the coefficient of determination of the fit, i.e its , computed as follows:

| (1) |

where are the degree distribution values, are the modeled degrees by the fitted power-law model, and is the means of the empirical degree distributions: . A different methodology for estimating ERC20 network values and their goodness-of-fit can be found in [36].

3.2 Oscillation Dynamics

We consider the ERC20 system as a social physical system and thus use physical models to analyze it. We hypothesize that the ERC20 system behaves as a dynamical system approaching its equilibrium state, which can be modeled as a damped harmonics oscillator.

A harmonic oscillator is a system acted upon by a force negatively proportional to its perturbation from its equilibrium state. Physical systems that are modeled in this way are springs and swings. Systems that also experience a velocity-dependent friction-like force, e.g. air resistance, are modeled by a damped harmonic oscillator. The dynamical equation for these models is:

| (2) |

where is the perturbation from equilibrium, is the mass, is the spring constant and is the viscous damping coefficient. The resonant frequency of the system is defined as and represents the oscillation of an undamped system. One can define the damping ratio as which represents how strong the damping is, compared to the resonant frequency, such that an over-damped system does not oscillate, but exponentially converges to the equilibrium state, whereas an under-damped system oscillates with a modified frequency during its exponential convergence. The case of critically damped system is an important one in physics, but does not relate to the analysis presented below.

Given an under-damped oscillator, the dynamics of the system can be described by the following function:

| (3) |

Here is the phase of the oscillation and is the equilibrium state.

In this paper, we will use the under-damped oscillator in order to model the dynamics of the ERC20 network meta-parameter and extract the parameters of its dynamics.

4 Results

In this work we analyze the dynamics of ERC20 tokens’ trading over the Ethereum Blockchain. We obtain the ERC20 transactions using the methodology thoroughly explained in [34]. We have retrieved all ERC20 tokens transactions spreading between February 2016 and June 2018, resulting in token trades, performed by unique wallets, trading token addresses.

During the examined timespan of years of ERC20 transactions, the economy keeps evolving and changing its dynamics. Not only does the rising public interest in Blockchain and tokens induce an exponential growth in transactions’ volume, but the traded tokens in this economy change as well, as new tokens are established and others lose their impact and decay. A thorough discussion of the dynamics of the economical properties of the ERC20 economy was conducted in [36].

4.1 Temporal Dynamics: The Oscillating Network Model

This apparent volatile nature of ERC20 ecosystem leads us to examine its network characteristics along time. We therefore apply temporal graph analysis to a sliding window of weekly graphs. Namely, we define a weekly transactions graph based on ERC20 trading activity during a week as follows:

Definition 4.1.

The weekly transactions graph for a given day , is the directed graph constructed from all trading transactions over any ERC20 token, made during the time period . The set of vertices consists of all wallets trading during that period:

| (4) |

and the set of edges is defined as:

| (5) |

Over the examined period of 2.5 years, we construct 1000 such weekly transactions graphs, using daily rolling windows, each containing one week of transactional data. As seen in [33] the incoming and outgoing degree distributions of clearly adhere to a power-law model.

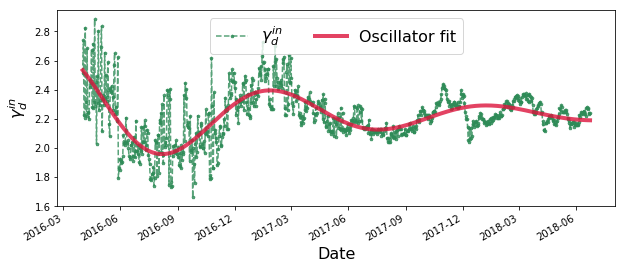

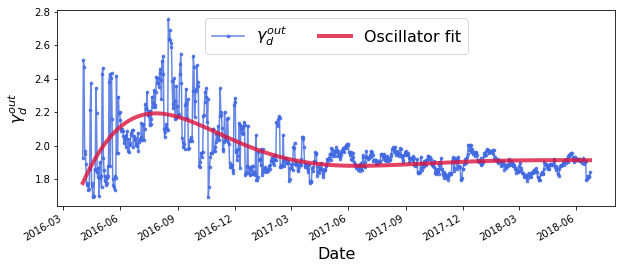

Next, we turn to model the degree distribution over time, as captured by its associated values. We postulate that any network of human related transactions, has a characteristic stable state, in the form of and , to which the network strives to converge:

Empirical observations of both and coincide with this hypothesis, as can be seen in Fig. 1, and can be efficiently modeled as an Harmonic Under-Damped Oscillator, formally :

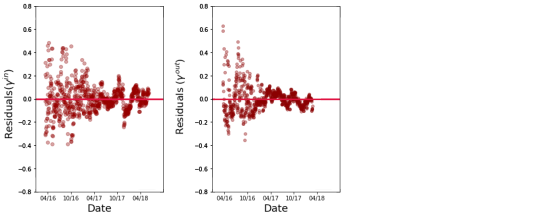

In order to examine how well the Oscillator model describes and models the dynamics of the degree distribution along time, we explore the residuals from the fit, i.e the deviations of the dependent variable, , from the fitted oscillator for each day, :

| (6) |

Fig. 2 presents the residuals of the oscillator fit for both and . These demonstrate a symmetrical dispersion around a zero mean, proving the validity of modeling the empirical data using an under-damped oscillator. The residual plots against time further exhibit another interesting phenomena, presenting a decreasing standard deviation of the residuals values along time.

The under-damped oscillator model can be considered as an extension of the regular single-parameter model, which suggested as a constant stable state, to a new model governed by five parameters: (i) representing the exponential decay, (ii) standing for the angular frequency, (iii) for the stable state to which the system converges, (iv) representing the maximal amplitude of the oscillation and (v) for the phase shift. The parameters of fitted oscillators to and , and correspondingly, are presented in Table 1 and Table 2.

| Type | (days) | ||||

|---|---|---|---|---|---|

| -0.77 | 2.96 | 1.91 | 530.2 | 0.577 | |

| 0.39 | 2.23 | 2.23 | 341.1 | 0.152 |

| Type | (days) | (days) | ||

|---|---|---|---|---|

| 146.3 | 649.1 | |||

| 356.6 | 345.6 |

As part of this novel approach to modeling the network’s consolidation process, one should further note that the amplitude of the under-damped oscillator is governed by:

| (7) |

The latter enables establishing the time at which the network has reached a stabilization of , formally:

Definition 4.2.

Let be the directed graph based on all transactions made during , trading any of the ERC20 tokens, for a given . Let denote the power of the associated degree distribution of , whose dynamics modeled by an oscillator . We define the ’ stabilization time of the network’ w.r.t to be the time when the amplitude of reaches at most of the initial amplitude, observed as time :

| (8) |

This, in turn, enables us to establish the time required for the network to reach stabilization, in both aspects of and . For instance, using the fitted parameters of the under-damped oscillator depicted in Table 1, one can verify that a 70% stabilization occurs after 430 days for :

Using . presents the same stabilization after merely 177 days:

where .

4.2 The Oscillating Network Model: Predictive Ability

Once the modeling of the ERC20 network dynamics by an under-damped oscillator is established, it can be also used for predictive purposes. With this objective in mind, we fit partial observations to an oscillator model, considering data restricted by date, in order to predict future dynamics, formally defined as :

Definition 4.3.

Let stand for the minimal date available in our dataset, April 1st, 2016. Given any time-stamp , we define to be the partial oscillator model, representing the under-damped oscillator model fitted to values between and . The parameters characterizing are denoted by and .

In this constellation, is incremented on a daily basis, starting from April 28th, 2016, resulting in a set of partial oscillator models, each fitted to values occurring between :

The initial parameters values and their corresponding upper and lower bounds, as supplied to the oscillator model in the fitting process, are depicted in Table 3.

| Type | (days) | ||||

|---|---|---|---|---|---|

| initial values | 0.5 | 2.1 | 365 | 0.25 | |

| initial values | -0.5 | 1.9 | 365 | 0.5 | |

| Bounds | [-1, 1] | [0, ] | [1, 3] | [1, 700] | [0.001, 0.999] |

We start by examining the stabilization process of the partial models’ parameters. In order to smoothen their dynamics, we calculate a -days rolling mean over each parameter, retrieved from consecutive partial oscillator fits. Formally:

Definition 4.4.

given a time-stamp and given an oscillator’s property such that:

| (9) |

We define the mean and standard deviation of w.r.t to as follows:

| (10) | |||

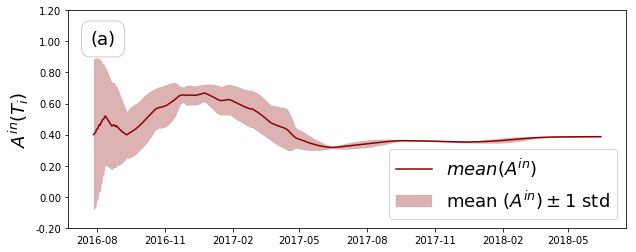

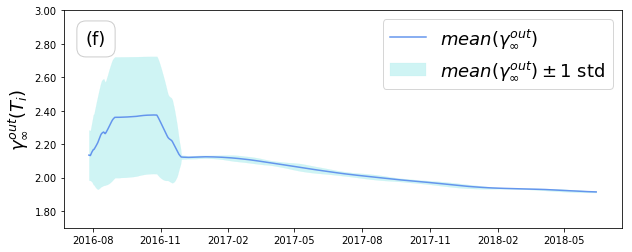

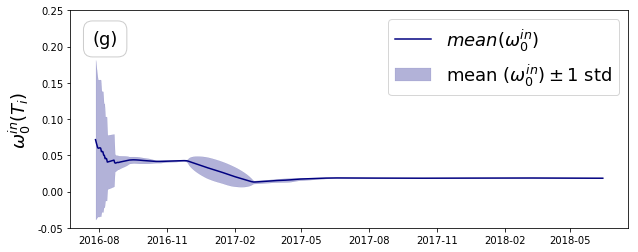

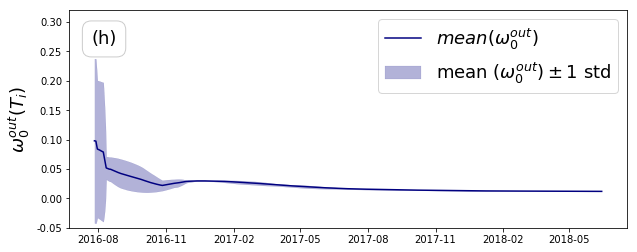

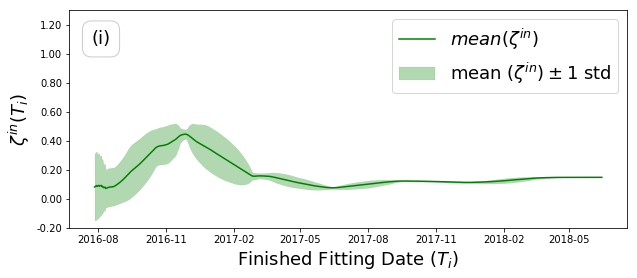

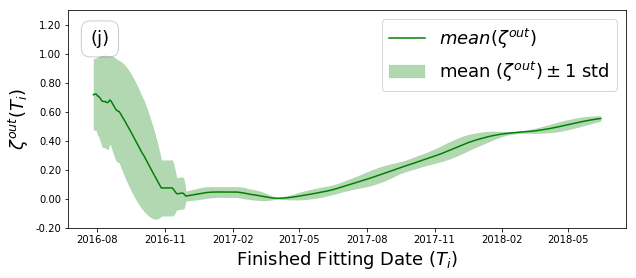

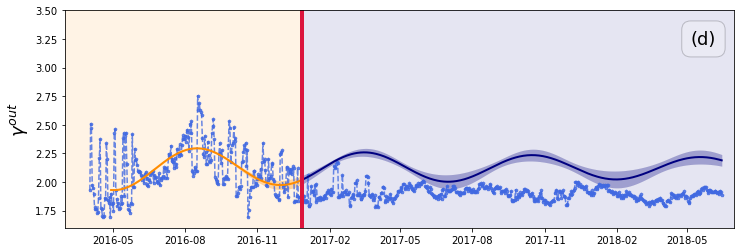

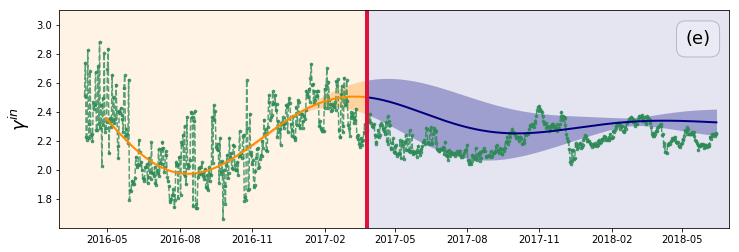

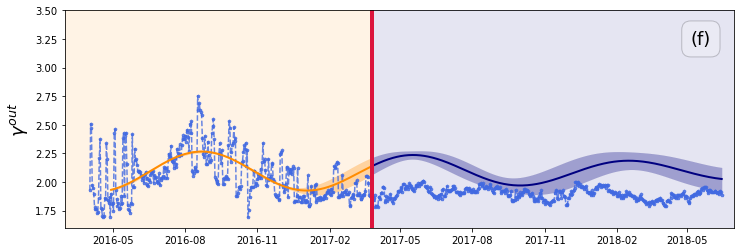

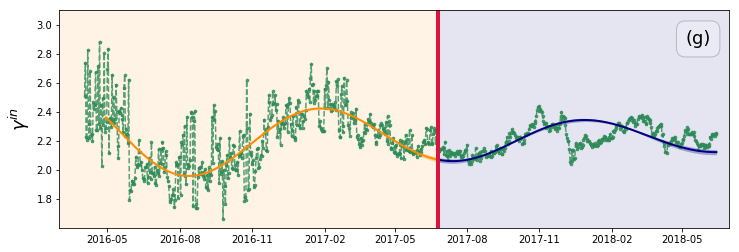

Fig. 3 depicts the stabilization process all parameters undergo along time, as advances, both for and , presenting the and along time.

The great difference between and is quite evident in this analysis as well, and is manifested through the parameters’ convergence properties. Each parameter of , the partial oscillator models for , presents not only a decreasing as progresses, manifesting the early consensus established by consecutive -s, but also a clear-cut stabilization for each of the parameters’ mean value, formulating at June 2017. This stabilization, occurring approximately a year prior to the end of our data, strongly implies the potentially extraordinary predictive abilities of the model, applied to . The parameters of the partial oscillator models for , although presenting a decreasing standard deviation along time, do not display the same converging tendency as progresses, manifested by a constant change in the parameters’ mean value along time.

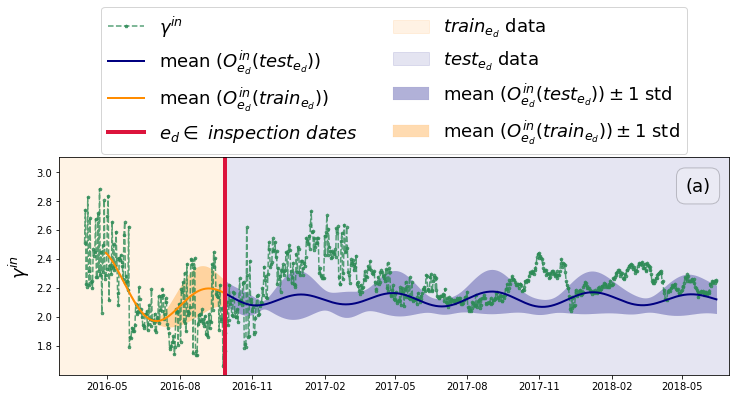

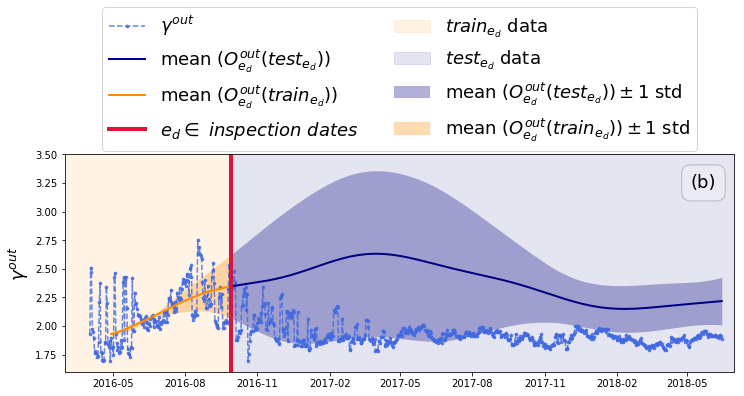

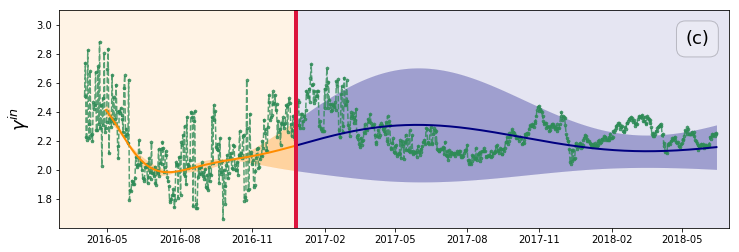

This analysis leads us to examine the predictive abilities of , and the amount of data required for fitting the oscillator’s parameters, in order to establish a stable and accurate prediction. For this purpose, we select different inspection dates, referred as :

-

-

September 28th, 2016

-

-

December 27th, 2016

-

-

March 27th, 2017

-

-

June 25th, 2017

-

-

September 23rd, 2017

and analyze the predictive ability of ’ as to dynamics over the timespan.

In order to establish the confidence levels for each associated prediction, we analyze the performance of partial oscillator models for each , forming a set, we’d refer to as :

| (11) |

The mean and standard deviation of ’s prediction of for a given time are defined as:

| (12) | |||

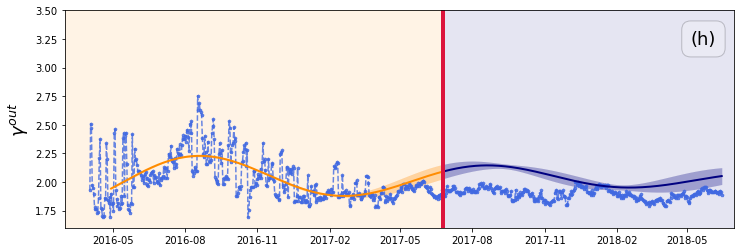

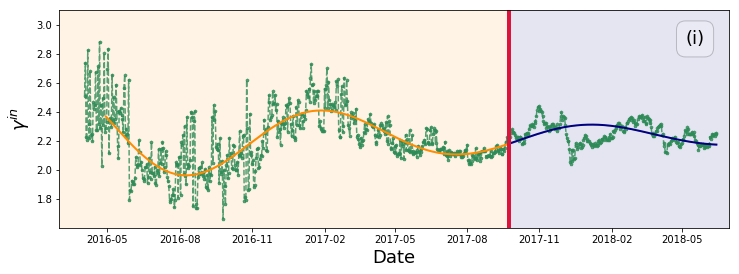

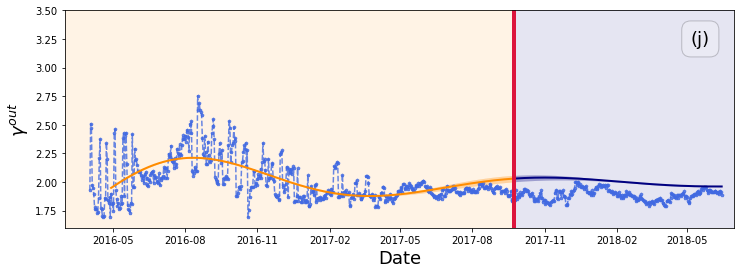

Fig. 4 depicts the predictions made for both and , presenting and along , for each of the inspection dates. The prediction analysis coincides with our parameters stabilization analysis, as predictions for stabilize as advances, until finally presenting high reliability, for predicting a whole year of data, starting from June 25, 2017. We further observe that confidence levels for the predictions increase with for both and , manifested by the decreasing standard deviation as progresses.

We note however, as was also implied by parameters stabilization process, that the predictive ability for when estimated at June 25, 2017 isn’t as strong, manifested by the evident over-estimation produced by while predicting values during . This apparent bias in the prediction of values manifests the lack of oscillations in the actual observed values, as well as an overestimation of by . This may suggest that there are other forces influencing the dynamics of , rather than just ’spring and friction’-like forces.

We further wish to analyze the ’goodness-of-fit’ of for any given , for the entire timespan. We therefore calculate the Root Mean Squared Error of each , namely:

| (13) |

where is the length of June 2018 period, measured in days.

In order to smoothen the RMSE signal, we calculate a 90-days rolling mean over the RMSE of the partial oscillator model:

| (14) | |||

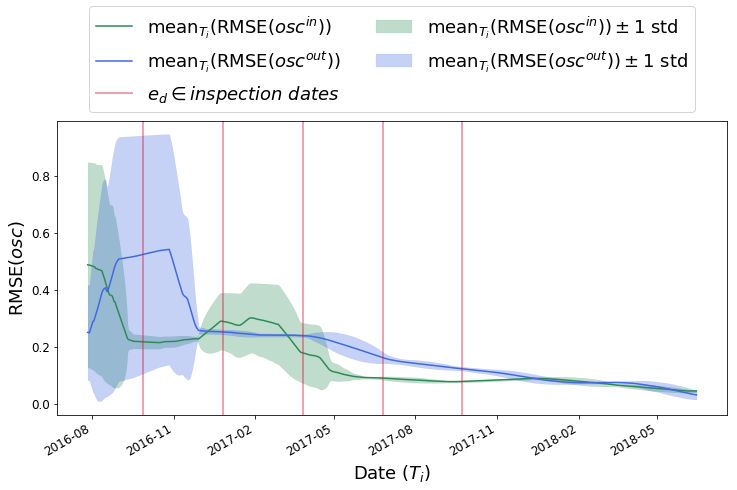

Fig. 5 depicts the Root Mean Squared Error of both and , presenting both and for predicting and along time. This analysis assists in validating that in average, has lower error values compared to along most of the examined timespan and specifically over the predictions of the last year of data, starting from June 25, 2017.

We note however that both and converge to similar RMSE values, starting from December 2017, yielding 7 months of similar and low error predictions for both and dynamics. The decreasing RMSE, and its standard deviation enhance even further the predictive abilities of the under-damped oscillator as a model of dynamics, concluding that is a better predictor compared to , as both its error rate and its confidence levels, present significant decrease earlier in time, enabling a reliable prediction of an entire year of data.

5 Discussion

In this contribution, we aimed to go beyond a static view of the ERC20 ecosystem, and explore its dynamics along time. Specifically, we have chosen to focus on the dynamics analysis of the most basic and the highly investigated network characteristic of them all, studying the development of the network’s degree distribution, manifested by its associated power, , throughout time. Inspired by macro-scale market dynamics [6, 9], which demonstrated an oscillatory stabilization process, we analyzed the exponents of in and out-degree distribution ( and ) and studied to which extent their dynamics can be modeled by an under-damped harmonic oscillator.

The goodness of fit of the oscillator model to was tested by analyzing the residuals plots, verifying they were centered around zero (see Fig. 2. Moreover, Fig. 3 (left panels) demonstrates how the fitted parameters of the oscillator model fitted to stabilize together and early, prior to the last observable oscillation in actual values. We further demonstrated the powerful predictive ability of the oscillator model for . Predicting future values based on fitting to an under-damped oscillator, Fig. 4(left-panels) shows that damped oscillations during the last year of data can be accurately and reliably predicted.

References

- [1] V. Buterin et al., “A next-generation smart contract and decentralized application platform,” white paper, 2014.

- [2] G. Wood, “Ethereum: A secure decentralised generalised transaction ledger,” Ethereum Project Yellow Paper, vol. 151, pp. 1–32, 2014.

- [3] C. Catalini and J. S. Gans, “Initial coin offerings and the value of crypto tokens,” tech. rep., National Bureau of Economic Research, 2018.

- [4] C. Castellano, S. Fortunato, and V. Loreto, “Statistical physics of social dynamics,” Reviews of modern physics, vol. 81, no. 2, p. 591, 2009.

- [5] D. Smug, D. Sornette, and P. Ashwin, “A generalized 2d-dynamical mean-field ising model with a rich set of bifurcations (inspired and applied to financial crises),” International Journal of Bifurcation and Chaos, vol. 28, no. 04, p. 1830010, 2018.

- [6] R. Frisch et al., “Propagation problems and impulse problems in dynamic economics,” 1933.

- [7] C. Ye and J. Huang, “Non-classical oscillator model for persistent fluctuations in stock markets,” Physica A: Statistical Mechanics and its Applications, vol. 387, no. 5-6, pp. 1255–1263, 2008.

- [8] C. P. Gonçalves, “Quantum financial economics—risk and returns,” Journal of Systems Science and Complexity, vol. 26, no. 2, pp. 187–200, 2013.

- [9] R. M. Goodwin, “The economy as a chaotic growth oscillator,” in The Dynamics of the Wealth of Nations, pp. 300–310, Springer, 1993.

- [10] T. Puu, Attractors, bifurcations, & chaos: Nonlinear phenomena in economics. Springer Science & Business Media, 2013.

- [11] A. Barrat, M. Barthelemy, and A. Vespignani, Dynamical processes on complex networks. Cambridge university press, 2008.

- [12] M. E. Newman, “The structure and function of complex networks,” SIAM review, vol. 45, no. 2, pp. 167–256, 2003.

- [13] M. E. Newman, “Power laws, pareto distributions and zipf’s law,” Contemporary physics, vol. 46, no. 5, pp. 323–351, 2005.

- [14] R. Pastor-Satorras and A. Vespignani, Evolution and structure of the Internet: A statistical physics approach. Cambridge University Press, 2007.

- [15] A.-L. Barabasi and Z. N. Oltvai, “Network biology: understanding the cell’s functional organization,” Nature reviews genetics, vol. 5, no. 2, p. 101, 2004.

- [16] E. Shmueli, I. Mazeh, L. Radaelli, A. S. Pentland, and Y. Altshuler, “Ride sharing: a network perspective,” in International Conference on Social Computing, Behavioral-Cultural Modeling, and Prediction, pp. 434–439, Springer, 2015.

- [17] Y. Altshuler, R. Puzis, Y. Elovici, S. Bekhor, and A. S. Pentland, “On the rationality and optimality of transportation networks defense: a network centrality approach,” Securing Transportation Systems, pp. 35–63, 2015.

- [18] Y. Altshuler, M. Fire, N. Aharony, Y. Elovici, and A. Pentland, “How many makes a crowd? on the correlation between groups’ size and the accuracy of modeling,” in International Conference on Social Computing, Behavioral-Cultural Modeling and Prediction, pp. 43–52, Springer, 2012.

- [19] Y. Altshuler, M. Fire, E. Shmueli, Y. Elovici, A. Bruckstein, A. S. Pentland, and D. Lazer, “The social amplifier—reaction of human communities to emergencies,” Journal of Statistical Physics, vol. 152, no. 3, pp. 399–418, 2013.

- [20] Y. Altshuler, W. Pan, and A. Pentland, “Trends prediction using social diffusion models,” in International Conference on Social Computing, Behavioral-Cultural Modeling and Prediction, pp. 97–104, Springer, 2012.

- [21] W. Pan, Y. Altshuler, and A. Pentland, “Decoding social influence and the wisdom of the crowd in financial trading network,” in Privacy, Security, Risk and Trust (PASSAT), 2012 International Conference on and 2012 International Confernece on Social Computing (SocialCom), pp. 203–209, IEEE, 2012.

- [22] E. Shmueli, Y. Altshuler, et al., “Temporal dynamics of scale-free networks,” in International Conference on Social Computing, Behavioral-Cultural Modeling, and Prediction, pp. 359–366, Springer, 2014.

- [23] J. Bonneau, A. Miller, J. Clark, A. Narayanan, J. A. Kroll, and E. W. Felten, “Sok: Research perspectives and challenges for bitcoin and cryptocurrencies,” in Security and Privacy (SP), 2015 IEEE Symposium on, pp. 104–121, IEEE, 2015.

- [24] S. Meiklejohn, M. Pomarole, G. Jordan, K. Levchenko, D. McCoy, G. M. Voelker, and S. Savage, “A fistful of bitcoins: characterizing payments among men with no names,” in Proceedings of the 2013 conference on Internet measurement conference, pp. 127–140, ACM, 2013.

- [25] H. Shrobe, D. L. Shrier, and A. Pentland, New Solutions for Cybersecurity. MIT Press, 2018.

- [26] D. Ron and A. Shamir, “Quantitative analysis of the full bitcoin transaction graph,” in International Conference on Financial Cryptography and Data Security, pp. 6–24, Springer, 2013.

- [27] D. D. F. Maesa, A. Marino, and L. Ricci, “Uncovering the bitcoin blockchain: an analysis of the full users graph,” in Data Science and Advanced Analytics (DSAA), 2016 IEEE International Conference on, pp. 537–546, IEEE, 2016.

- [28] M. Lischke and B. Fabian, “Analyzing the bitcoin network: The first four years,” Future Internet, vol. 8, no. 1, 2016.

- [29] M. Bartoletti and L. Pompianu, “An empirical analysis of smart contracts: platforms, applications, and design patterns,” in International Conference on Financial Cryptography and Data Security, pp. 494–509, Springer, 2017.

- [30] L. Anderson, R. Holz, A. Ponomarev, P. Rimba, and I. Weber, “New kids on the block: an analysis of modern blockchains,” arXiv preprint arXiv:1606.06530, 2016.

- [31] K. Christidis and M. Devetsikiotis, “Blockchains and smart contracts for the internet of things,” IEEE Access, vol. 4, pp. 2292–2303, 2016.

- [32] N. Atzei, M. Bartoletti, and T. Cimoli, “A survey of attacks on ethereum smart contracts (sok),” in International Conference on Principles of Security and Trust, pp. 164–186, Springer, 2017.

- [33] S. Somin, G. Gordon, and Y. Altshuler, “Network analysis of erc20 tokens trading on ethereum blockchain,” in International Conference on Complex Systems, pp. 439–450, Springer, 2018.

- [34] S. Somin, G. Gordon, and Y. Altshuler, “Social signals in the ethereum trading network,” arXiv preprint arXiv:1805.12097, 2018.

- [35] A. Clauset, C. R. Shalizi, and M. E. Newman, “Power-law distributions in empirical data,” SIAM review, vol. 51, no. 4, pp. 661–703, 2009.

- [36] S. Somin, Y. Altshuler, G. Gordon, E. Shmueli, et al., “network dynamics of a financial ecosystem,” Scientific reports, vol. 10, no. 1, pp. 1–10, 2020.