Extending Deep Reinforcement Learning Frameworks in Cryptocurrency Market Making

Abstract

There has been a recent surge in interest in the application of artificial intelligence to automated trading. Reinforcement learning has been applied to single- and multi-instrument use cases, such as market making or portfolio management. This paper proposes a new approach to framing cryptocurrency market making as a reinforcement learning challenge by introducing an event-based environment wherein an event is defined as a change in price greater or less than a given threshold, as opposed to by tick or time-based events (e.g., every minute, hour, day, etc.). Two policy-based agents are trained to learn a market making trading strategy using eight days of training data and evaluate their performance using 30 days of testing data. Limit order book data recorded from Bitmex is used to validate this approach, which demonstrates improved profit and stability compared to a time-based approach for both agents when using a simple multi-layer perceptron neural network for function approximation and seven different reward functions.

Keywords: reinforcement learning, limit order book, market making, cryptocurrencies

1 Introduction

Applying quantitative methods to market making is a longstanding interest of the quantitative finance community. Over the past decade, researchers have applied stochastic, statistical and machine learning techniques to automate market making. These approaches often use limit order book (LOB) data to train a model to make a prediction about future price movements, generally for the purpose of maintaining the optimal inventory and quotes (i.e., posted bid and ask orders at the exchange) for the market maker. These models are typically trained using the most granular form of event-driven data, level II/III tick data, where an event is defined as an incoming order received by the exchange (e.g., new, cancel, or modify). Alternatively, an event can be defined as a time interval (e.g., every n seconds, minutes, hours, etc.). Every time an event occurs, these models have the opportunity to react (e.g., adjust their quotes), thereby indirectly managing inventory by increasing or decreasing the likelihood of posted order execution.

Tick-based approaches make assumptions about latency and executions, which may impact the capability of a model to translate simulated results into real-world performance. Researchers attempt to address this challenge in different ways, such as creating simulation rules around market impact, execution rates, and priority of LOB queues [1, 2, 3, 4, 5]. We propose an alternative approach to address this challenge: Fundamentally change the mindset of strategy creation for automated market making from latency-sensitive to intelligent strategies using deep reinforcement learning (DRL) with time- and price-based event environments.

This paper applies DRL to create an intelligent market making strategy, extending the DRL Market Making (DRLMM) framework set forth in our previous work [6], which used time-based event environments. The reinforcement learning framework follows a Markov Decision Process (MDP), where an agent interacts with an environment over discrete time steps , observes a state space , takes an action guided by a policy , and receives a reward . The policy is a probability distribution mapping state spaces to action spaces . The agent’s interactions with the environment continues until a terminal state is reached. The return is the total accumulated return from time step with discount factor . The goal of the agent is to maximize the expected return from each state [7].

Although reinforcement learning has seen many recent successes across various domains [8, 9, 10], the success of its application in automated trading is highly dependent on the reward function (i.e., feedback signal) [11, 12, 13]. Previous research [6] proposed a framework for deep reinforcement learning as applied to cryptocurrency market making (DRLMM) and demonstrated its capability to generalize across different currency pairs. The focus of this paper is to extend the research of previous work by evaluating how seven different reward functions impact the agent’s trading strategy, and to introduce a new framework for DRLMM using price-based events.

This paper is structured as follows: section 1, introduction; section 2, related research; section 3, contributions in this paper; section 4, overview of the seven reward functions; section 5, overview of time- and price-based event-driven environments; section 6, our experiment design and methodology; section 7 results and analysis; and section 8, conclusion and future work.

2 Related Work

The earliest approaches of applying model-free reinforcement learning to automated trading consist of training an agent to learn a directional single-instrument trading strategy using low-resolution price data and policy methods [11, 12, 13, 14]. These approaches find risk-based reward functions, such as Downside Deviation Ratio or Differential Sharpe Ratio, generate more stable out-of-sample results than using actual profit and loss.

More recently, researchers have applied reinforcement learning methods to market making. [3] created a framework using value-based model-free methods with high-resolution LOB data from equity markets. Under this framework, an agent takes a step through the environment every time a new tick event occurs. They proposed a novel reward function, which dampens the change in unrealized profit and loss asymmetrically, discouraging the agent from speculation. Although their agent demonstrates stable out-of-sample results, assumptions about latency and executions in the simulator make it unclear how effectively the trained agent would perform in live trading environments. [15] proposed a hierarchical reinforcement learning architecture, where a macro agent views low-resolution data and generates trade signals, and a micro agent accesses the LOB and is responsible for order execution. Under this approach, the macro agent takes a step through the environment with time-based events using one-minute time intervals; the micro agent interacts with its environment in ten-second intervals. Although the agent outperformed their baseline, the lack of inventory constraints on the agent makes the results uncertain for live trading.

Previous work [6] proposed a new framework for applying deep reinforcement learning to cryptocurrency market making. The approach consists of using a time-based event approach with one-second snapshots of LOB data (including derived statistics from order and trade flow imbalances and indicators) to train policy-based model-free actor-critic algorithms. The performance of two reward functions were compared on Bitcoin, Ether and Litecoin data from Coinbase exchange. The framework’s ability to generalize was demonstrated by applying trained agents to make markets in different currency pairs profitably. This paper extends previous work through comparing five additional reward functions, and introduce a new approach for the DRLMM framework using price-based events.

3 Contributions

The main contributions of this paper are as follows:

-

1.

Analysis of seven reward functions : We extend previous work, apply the DRLMM framework to more reward functions and evaluate the impact on the agent’s market making strategy. The reward function definitions are explained in section 4.

-

2.

Price-based event environment : We propose a new approach to defining an event in the agent’s environment and compare this approach to our original time-based environment framework. The price-based event approach is explained in section 5.

4 Reward Functions

The reward function serves as a feedback signal to the agent and therefore directly impacts the agent’s trading strategy in a significant way. There are seven reward functions described in this section, which are categorized as profit-and-loss (PnL), goal-oriented, and risk-based approaches. These seven reward functions provide a wide range of feedback signals to the agent, from frequent to sparse.

When calculating realized PnL, orders are netted in FIFO order and presented in percentage terms, opposed to dollar value, to ensure compatibility if applied to different instruments (all simulation rules are set forth in section 6.3.3).

4.1 PnL-based Rewards

Unrealized PnL

The agent’s unrealized PnL provides the agent with a continuous feedback signal (assuming the agent is trading actively and maintains inventory). This reward function is calculated by multiplying the agent’s inventory count by the percentage change in midpoint price for time step . Note, inventory count is an integer, because the agent trades with equally sized orders (see section 6.3.3 for the comprehensive list of trading rules in our environment).

| (1) |

where and is the total count of executed orders held in inventory and is the maximum permitted inventory. In our experiment, we set , meaning the agent can execute and hold 10 trades (of equal quantity).

Unrealized PnL with Realized Fills

The unrealized PnL with realized fills reward function (referred to as positional PnL in our previous work) is similar to , but includes any realized gains or losses obtained between time steps and . This reward function provides the agent with a continuous feedback signal, as well as larger sparse rewards (assuming the agent is trading actively and maintains inventory).

| (2) |

where and is the average entry price and is the average exit price of the executed order(s) between time steps and for or sides.

Asymmetrical Unrealized PnL with Realized Fills

The asymmetrical unrealized PnL with realized fills reward function is similar to , but removes any upside unrealized PnL to discourage price speculation and adds a small rebate (i.e., half the spread) whenever an open order is executed to promote the use of limit orders. This reward function is provides both immediate and sparse feedback to the agent (assuming the agent is trading actively and maintains inventory). Our implementation is similar to [3]’s asymmetrically dampened PnL function, but includes the realized gains from the current time step , which improved our agent’s performance in volatile cryptocurrency markets.

| (3) |

where is the number of matched (i.e., executed) orders multiplied by half the spread in percentage terms, and is a constant value used for dampening. In our experiment, we set to 0.35.

Asymmetrical Unrealized PnL with Realized Fills and Ceiling

The asymmetrical unrealized PnL with realized fills and gains ceiling reward function can be though of as an extension of , where we add a cap on the realized upside gains and remove the half-spread rebate on executed limit orders. The intended effect is that is discouraged from long inventory holding periods and price speculation due to the ceiling and asymmetrical dampening. Like , this reward function provides both immediate and sparse feedback to the agent.

| (4) |

where is the effective ceiling on time step realized gains. In our experiment, we set to twice the market order transaction fee.

Realized PnL Change

The change in realized PnL provides the agent with a sparse feedback signal since values are only generated at the end of a round-trip trade. The reward is calculated by taking the difference in realized PnL values between time step and .

| (5) |

where is the agent’s realized PnL at time step and previous time step .

4.2 Goal-based Rewards

Trade Completion

The trade completion reward function provides a goal-oriented feedback signal, where a reward is generated if a objective is obtained or missed. Moreover, if the realized PnL is greater (or less) than a predefined threshold , the reward is 1 (or -1) otherwise, if is in between the thresholds, the actual realized PnL in percentage terms is the reward. Using this approach, the agent is encouraged to open and close positions with a targeted profit-to-loss ratio, and is not rewarded for longer term price speculation.

| (6) |

where is a constant used for the multiplier and is a constant used for the threshold. In our experiment, we set to 2 and to the market order transaction fee.

4.3 Risk-based Rewards

Differential Sharpe Ratio

The differential sharpe ratio provides the agent with a risk adjusted continuous feedback signal (assuming the agent is trading actively and maintains inventory). Originally proposed [11] more than 20 years ago, this reward function is the online version of the well known Sharpe Ratio, but can be calculated cheaply with O(1) time complexity, thereby making it the more practical choice for training agents using high-resolution data sets.

| (7) |

where and and and and is a constant value. In our experiment, we use (as described in section 4.1) for and set to 0.01.

5 Event-driven Environments

When applying reinforcement learning to financial time series, the typical approach to framing the MDP is to have the agent take a step through the environment using a time-based interval. Depending on the trading strategy, the interval of time can be anywhere from seconds to days. For market making, the typical approach is to use tick events (e.g., new, cancel or modify order) as the catalyst for an agent to interact with its environment. The tick-based approach differs from a time-based approach in that the events are irregularly spaced in time, and occur in much greater frequency (more than a magnitude). Although tick-based strategies can yield very impressive results in research, external factors (e.g., partial executions, latency, risk checks, etc.) could limit their practicality in live trading environments. We address the challenge by proposing the use of price-based events for market making trading strategies, which partially removes the dependency on these assumptions, enabling the deep reinforcement algorithms to learn non-linear market dynamics across multiple time steps (i.e., not latency-sensitive).

5.1 Time-based Events

The time-based approach to event-driven environments consists of sampling the data at periodic intervals evenly spaced in time (e.g., every second, minute, day, etc.). This approach is the most intuitive for trading strategies, since market data is easily available in this format. This experiment takes snapshots of the LOB (and other inputs in our feature space) using one-second time intervals to reduce the number of events in one trading day from millions to 86,400 (the number of seconds in a 24-hour trading day), resulting in less clock time required to train our agent.

5.2 Price-based Events

The price-based approach to event-driven environments consists of an event being defined as a change in midpoint price greater or less than a threshold . Following this approach, our data set is further down-sampled from its original form of one-second time intervals into significantly fewer price change events that are irregularly spaced in time, thereby decreasing the amount of time required to train the agent per episode (i.e., one trading day). In this experiment, the minimum threshold is set to one basis point (i.e., 0.01%) and use the one-second LOB snapshot data (as described in section 5.1) as the underlying data set.

6 Experiment

In this section, the design and methodology aspects of the experiment are set forth.

6.1 Environment Design

6.1.1 Observation Space

The agent’s observation space is represented by a combination of LOB data from the first 20 rows, order and trade flow imbalances, indicators, and other hand-crafted indicators. For each observation, we include 100 window lags. The observation space implementation specifications are detailed in the appendix (section A.2).

It is worth noting that in previous work [6], the non-stationary feature price level distances to midpoint is included in the agent’s observation space; however, this feature does not inform the agent when using Bitmex data. This is likely due to the tick size at Bitmex being relatively large (0.50) compared to Coinbase exchange (0.01). As a result, the distances of price levels to the midpoint remain unchanged for 99.99% of the time at Bitmex.

6.1.2 Action Space

The agent action space consists of 17 possible actions. The idea is that the agent can take four general actions: no action, symmetrically quote prices, asymmetrically skew quoted prices, or flatten the entire inventory. The action space is outlined in Table 1.

| Action ID | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bid | 0 | 0 | 0 | 4 | 4 | 4 | 4 | 9 | 9 | 9 | 9 | 14 | 14 | 14 | 14 |

| Ask | 4 | 9 | 14 | 0 | 4 | 9 | 14 | 0 | 4 | 9 | 14 | 0 | 4 | 9 | 14 |

| Action 1 | No action | ||||||||||||||

| Action 17 | Market order with size | ||||||||||||||

6.1.3 Function Approximator

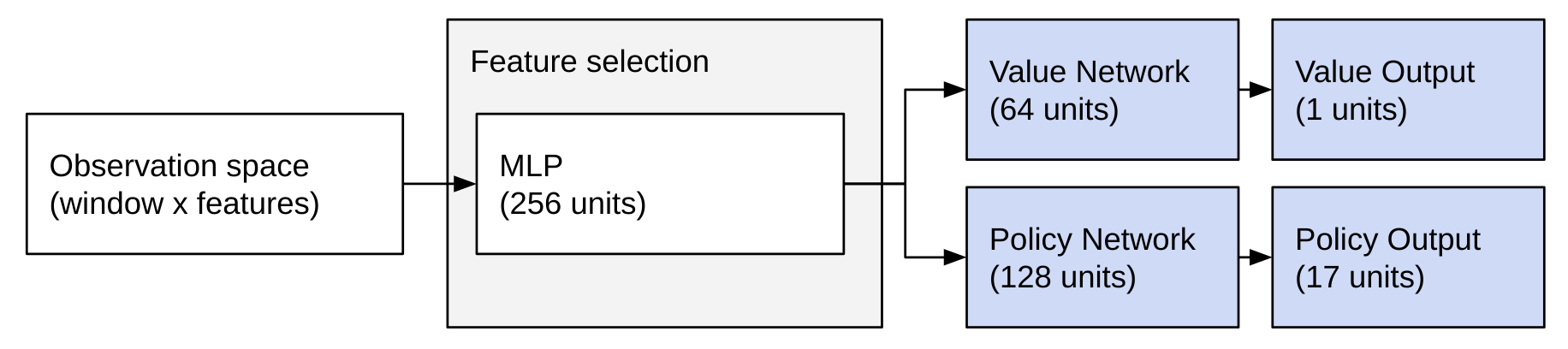

The function approximator is a multilayer perceptron (MLP), which is a forward feed artificial neural network. The architecture of our implementation consists of 3-layer network with a single shared layer for feature extraction, followed by separate actor and critic networks. ReLu activations are used in every hidden layer.

6.1.4 Reward Functions

We implement seven different reward functions, as outlined in section 4.

6.2 Agents

Two advanced policy-based model-free algorithms are used as market making agents: Advantage Actor-Critic (A2C) and Proximal Policy Optimization (PPO). We use the Stable Baselines [16] implementation for the algorithms. Since both algorithms run on multiple processes, they require nearly the same amount of clock time to train. The same policy network architectures (figure 1) are used across all experiments, and parameter settings are listed in the appendix (section A.1).

6.2.1 Advantage Actor-Critic (A2C)

The A2C is an on-policy model-free actor-critic algorithm that is part of policy-based class of RL algorithms. It interacts with the environment asynchronously while maintaining a policy and estimate of the value function , and synchronously updates parameters using a GPU, opposed to its off-policy asynchronous update counterpart A3C [17]. A2C learns good and bad actions through calculating the advantage of a particular action for a given state. The advantage is the difference between the action-value and state value . The A2C algorithm also uses k-step returns to update both policy and value-function, which results in more stable learning than a vanilla policy gradient, which uses 1-step returns. These features, asynchronous training and k-step returns, make A2C a strong fit for its application to market making, which relies on noisy high-resolution LOB data.

The A2C update is calculated as

| (8) |

where is the estimate of the advantage function given by , where can vary by an upper bound [17].

6.2.2 Proximal Policy Optimization (PPO)

The PPO is an on-policy model-free actor-critic algorithm is part of policy-based class of RL algorithms, even though the policy is indirectly updated through a surrogate function. Like the A2C algorithm, it interacts with the environment asynchronously, makes synchronous parameter updates , and uses k-step returns. However, unlike A2C, PPO uses Generalized Advantage Estimation (GAE) to reduce the bias of advantages [18] and indirectly optimizes the policy through a clipped surrogate function that represents the difference between the new policy after the most recent update and the old policy before the most recent update [19]. This surrogate function removes the incentive for a new policy to depart from the old policy, thereby increasing learning stability. These features, asynchronous training, k-step returns, and surrogate function, make PPO a strong fit for its application to market making, which relies on noisy high-resolution LOB data.

The PPO Clip update is calculated as

| (9) |

where is a hyperparameter constant [19].

6.3 Methodology

6.3.1 Data Collection

LOB data for cryptocurrencies is free to access via WebSocket, but not readily downloadable from exchanges, and therefore requires recording. The data set for this experiment was recorded using Level II tick and trade data from Bitmex exchange111https://www.bitmex.com/ and persisted into an Arctic TickStore222https://github.com/man-group/arctic for storage.

Unlike previous work, where we replayed recorded data to reconstruct the data set, in this experiment we recorded the LOB snapshots in real-time using one-second time intervals. This approach has two main advantages over replaying tick data. First, the computational burden is significantly reduced (millions of tick events per trading day) in setting up the experiment, since the LOB no longer needs to be reconstructed to create LOB snapshot data. Second, the data feed is more reflective of a production trading system. However, this approach introduced a small amount of latency into the snapshot intervals (less than 1 millisecond), resulting in approximately 86,390 snapshots per a 24 hour trading day, opposed to the actual number of seconds (86,400). We export the recorded data to compressed CSV files, segregated by trading date using UTC timezone; each file is approximately 160Mb in size before compression.

6.3.2 Data Processing

Since LOB data cannot be used for machine learning without preprocessing, it is necessary to apply a normalization technique to the raw data set. In this experiment, the data set was normalized using the approach described by [20, 6], which transforms the LOB from non-stationary into a stationary feature set, then uses the previous three trading days to fit and -score normalize the current trading day’s values, and in which data point is standard deviations from the mean . After normalizing the data set, outliers (values less than -10 or greater than 10) are clipped.

| (10) |

6.3.3 Simulation Rules

The environment follows a set of rules to ensure the simulation as realistic as possible.

Episode

An episode is defined as a 24-hour trading day, using coordinated universal time (UTC) to segregate trading days. At the end of an episode, the agent is required to flatten its entire inventory as a risk control.

Transaction Fees

Transaction fees for orders are included and are deducted from the realized profit and loss when an order is completed. We use a maker rebate of 0.025% and taker fee of 0.075%, which corresponds to Bitmex’s fee schedule at the time of the experiment. The maker-taker fee structure is crucial to the success of our agent’s market making trading strategy.

Risk Limits

The agent is permitted to open one order per side (e.g., bid and ask) at a given moment, and can hold up to ten executed orders (i.e., inventory maximum ) in its inventory . All orders placed by the agent are equal in size . There are no stop losses imposed on agents.

Position Netting

If the agent has an open long (short) position and fills an open short (long) order, the existing long (short) position is netted, and the position’s realized profit and loss is calculated in FIFO order. PnL is calculated in percentage terms.

Executions

Each time a new order is opened by the agent, the dollar value (e.g., price quantity) of the order’s price-level at the time step is captured by our simulator, and only reduced when there are buy (sell) transactions at or above (below) the ask (bid). Only after the LOB price-level queue is depleted, can the agent’s order begin to be executed. This environment rule is necessary to help simulate more realistic results. Additionally, the agent can modify an existing open order, even if it is partially filled, to a new price and reset its priority in the price-level queue. Once the order is filled completely, the average execution price is used for profit and loss calculations and the agent must wait until the next environment step to select an action (such as replenishing the filled order in the order book).

Slippage

If the agent selects decides to flatten its inventory, we account for market impact by applying a fixed slippage percentage to each transaction individually and recursively (e.g., ), where is 0.01% and is linked to order direction. We noticed adding slippage to the flatten all action encouraged the agent to use limit orders more frequently.

6.3.4 Training and Testing

The market-making agents (A2C and PPO) are trained on 8 days of data (December 27th, 2019 to January 3rd, 2020) and tested on 30 days of data (January 4th to February 3rd, 2020) using perpetual Bitcoin data (instrument: XBTUSD). Each trading day consists of 86,390 snapshots, which reflects roughly one snapshot per second in a 24-hour market (slightly less due to latency in our Python implementation, as noted in section 6.3.1). Each agent’s performance is evaluated on daily and cumulative returns.

In each experiment, agents are trained for one million environment steps and episodes restart at a random step in the environment to prevent deterministic learning. The time-based environment takes advantage of action repeats, enabling agents to accelerate learning; we use five action repeats in our experiment, which results in up to approximately 17,000 agent interactions with the environment per episode. The price-based environment does not use action repeats, since the number of interactions with the environment is already reduced to approximately 5,000 instances per episode. It is important to note that during action repeats or between price events, the agent’s action is only performed once and not repeated; all subsequent repeats in the environment consist of taking “no action,” thereby avoid performing illogical repetitive actions multiple times in a row, such as flattening the entire inventory, or re-posting orders to the same price and losing LOB queue priority. All the experiment parameters are outlined in the appendix (section A.1).

| Feature Sets | ||||

|---|---|---|---|---|

| Combination | LOB Quantity | Order Flow | LOB Imbalances | Indicators |

| Set 1 | ✓ | ✓ | ✓ | ✓ |

| Set 2 | ✓ | ✓ | ||

| Set 3 | ✓ | ✓ | ✓ | |

| Set 4 | ✓ | ✓ | ||

| Set 5 | ✓ | ✓ | ✓ | |

| Set 6 | ✓ | ✓ | ||

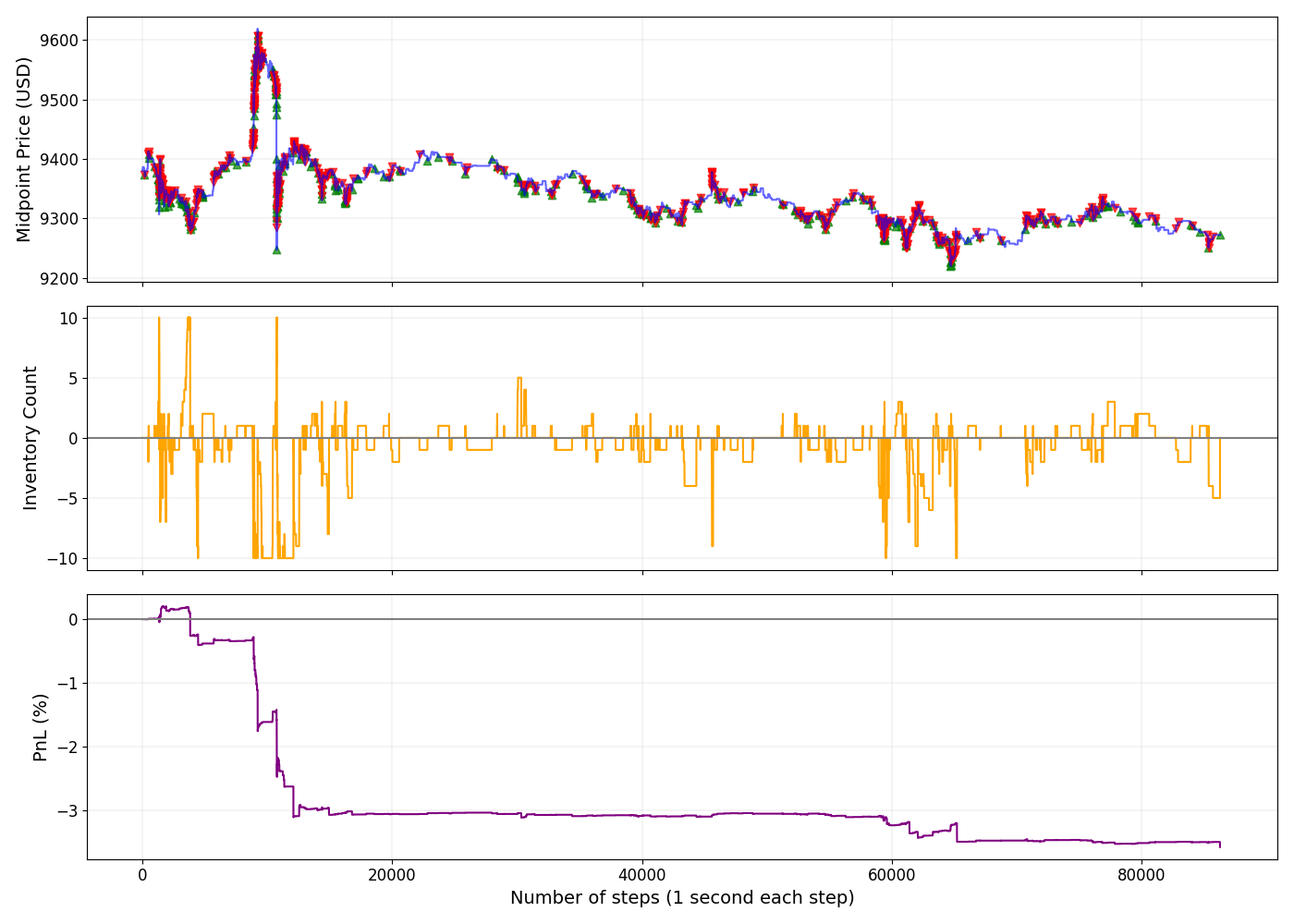

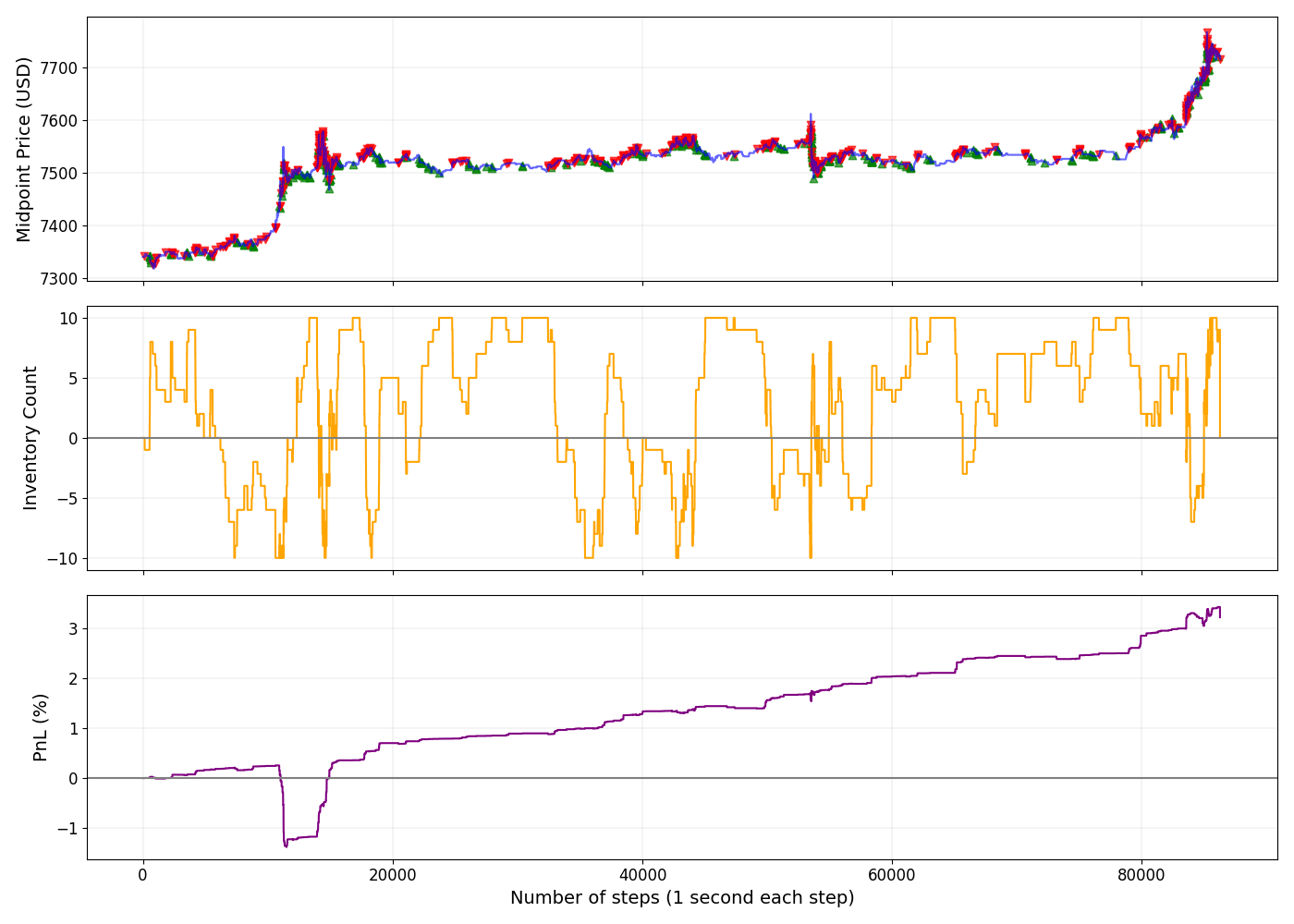

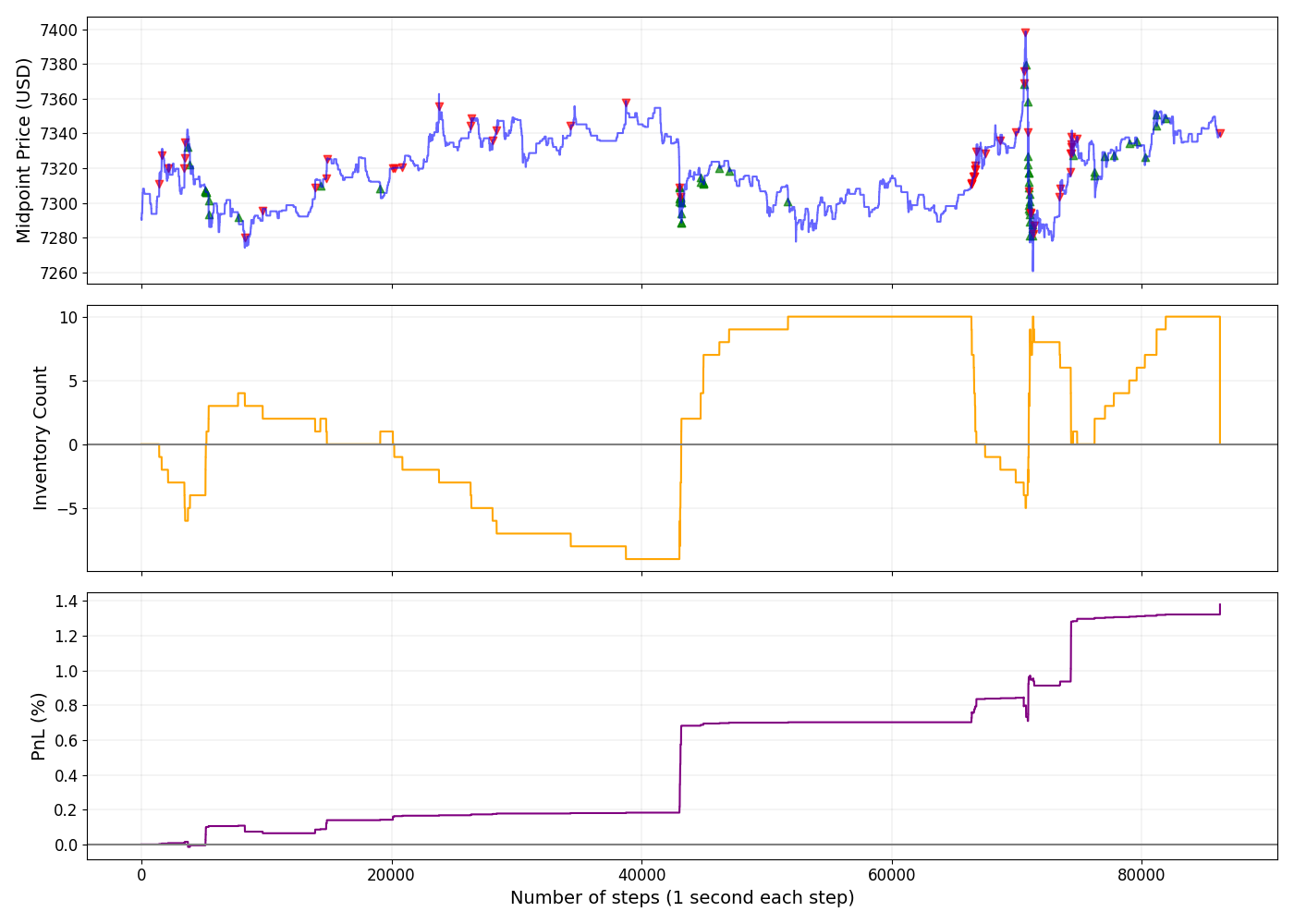

7 Results

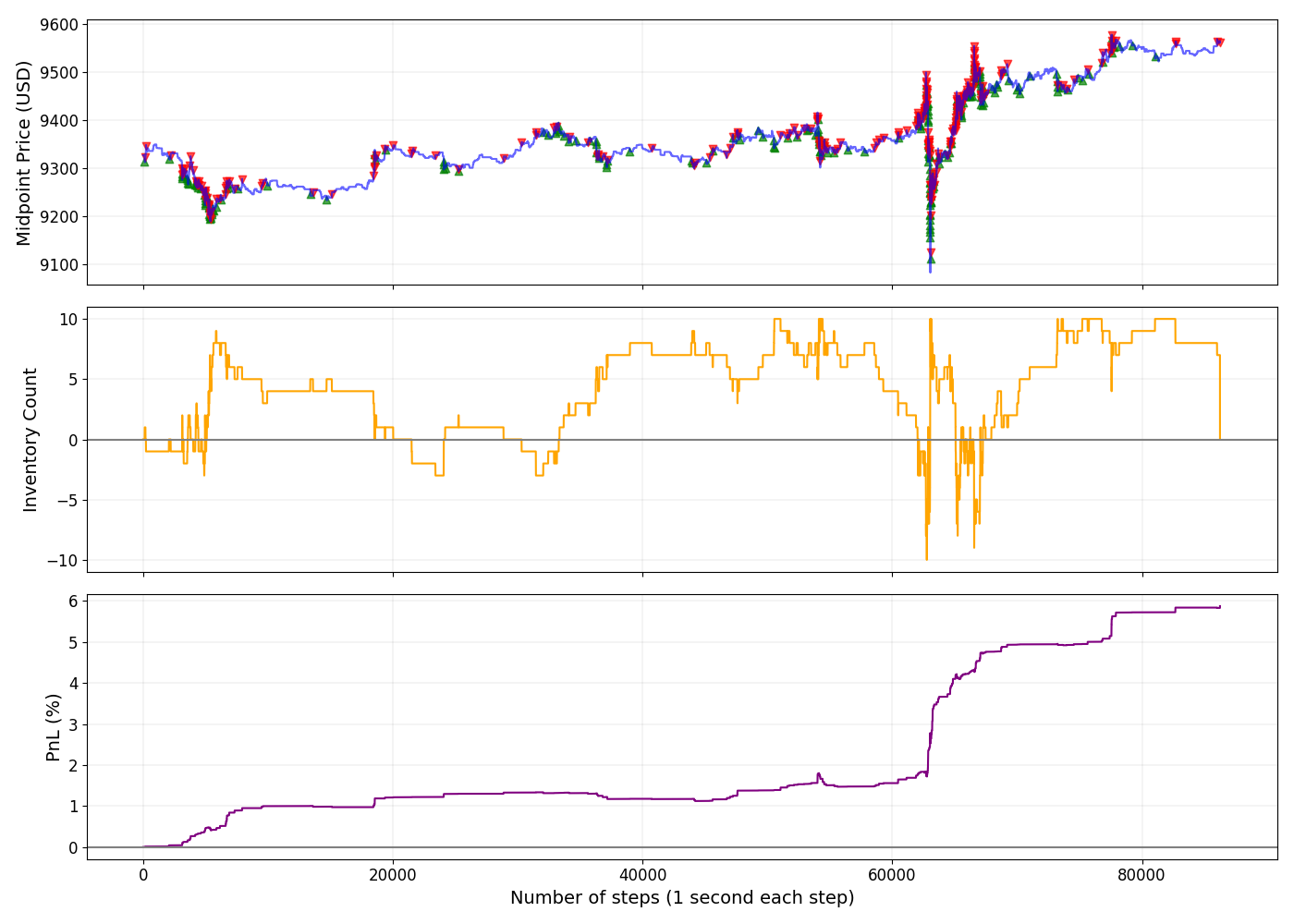

In this section, the performance of each agent (PPO and A2C) are compared using the cumulative return (in percentage) including transaction costs from the out-of-sample tests. Our benchmark is a simple buy-and-hold strategy, where we assume Bitcoin is purchased on the first day of the out-of-sample data and sold on the last day, for a total holding period of 30333 Not including January 14th, 2020 due to a dropped WebSocket connection consecutive trading days. Although the train-test split of data sets was selected based on data availability and not empirically, the out-of-sample data set coincidentally captures a volatile upward month long trend in January 2020, which enables the benchmark to generate a 16.25%††footnotemark: return during this period.

The best result obtained from our agents is a 17.61%††footnotemark: return over this same period, using reward function Trade Completion , A2C algorithm, and feature combination Set 3 for the observation space. Although the A2C algorithm outperformed the PPO agent in terms of greatest return and number of profitable experiments, it is interesting that no clear trends emerged for the best observation space combination, or reward function (other than what does not work).

It is worth noting that on January 19, 2020, the price of Bitcoin sold off more than 5% in less than 200 seconds, and all experiments (agents, reward functions, and observation space combinations) incurred significant losses ranging between 5% and 10% as a result of the rapid price drop; if this trading day were excluded, many more experiments would have yielded positive results. All experiment results are outlined in tables 3 and 4.

7.1 Reward Functions

We evaluated seven different reward functions across a combination of features in the observation space, A2C and PPO reinforcement learning algorithms, and time- and price-based event environments. Each reward function resulted in the agent learning a different approach to trading and maintaining its inventory.

7.1.1 PnL-based rewards

Reward functions where realized gains are not incorporated in the function’s feedback signal tended to result in nearsighted trading behavior. For example, the unrealized profit-and-loss function encouraged the agent to use market orders (e.g., action 17 - flatten inventory) often and executed many trades with short holding periods, resulting in consistent losses due to transaction costs.

Reward functions where the feedback signal is sparse tended to result in speculative trading behavior. For example, the change in realized profit function encouraged the agent to hold positions for an extended period, regardless if the agent had large unrealized gains or drawdown.

Reward functions where the feedback signal is dampened asymmetrically tended to result in tactical trading while failing to exploit large price movements. For example, the asymmetrical unrealized PnL with realized fills function discouraged the agent holding a position for an extended period of time into a price jump, either resulting in closing out a position too early and foregoing profits, or closing out a position during a transitory drawdown period. These types of reward functions are very sensitive to the dampening factor , and the value 0.35 yielded the most stable out-of-sample performance through a grid search.

7.1.2 Goal-oriented rewards

The Trade Completion reward function tended to result in more active trading and inventory management. For example, agent does not hold positions for speculation and quickly closes positions as they approach the upper and lower boundaries of the reward function curve.

7.1.3 Risk-based rewards

The Differential Sharpe Ratio reward function produced inconsistent results, and appears to be very sensitive to experiment settings. For example, in some experiments the agents learned very stable trading strategies, while unable to learn at all in other experiments (even with different random seeds). Additionally, in certain market conditions the agents were able to learn how to exploit price jumps, while making nonsensical decisions in other market regimes. It is possible that this reward function could have better performance with a thorough parameter grid search.

7.2 Time-based Events

The time-based environments were more difficult for the agents to learn; 15 out of 84 experiments led to profitable outcomes. This is likely due to the training methodology, where agents may benefit from training for more than one million steps. That said, the time-based environment was able to achieve the highest return out of all experiments due to quicker reactions to adverse price movements with the goal-based reward function .

| Time-event: | Profit-and-Loss (%)††footnotemark: | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| A2C | PPO | |||||||||||

| Reward Function | Set 1 | Set 2 | Set 3 | Set 4 | Set 5 | Set 6 | Set 1 | Set 2 | Set 3 | Set 4 | Set 5 | Set 6 |

| UPnL | (-12.05) | (-11.67) | (-12.06) | (-24.00) | (-35.30) | (-14.83) | (-18.58) | (-29.57) | (-25.62) | (-43.95) | (-32.12) | (-56.52) |

| UPnLwF | 4.53 | (-32.97) | 11.04 | (-4.73) | 5.12 | (-22.56) | (-5.44) | (-20.34) | 1.56 | (-28.20) | (-17.37) | (-12.68) |

| Asym | (-13.09) | (-39.02) | (-35.41) | (-6.96) | 2.82 | 8.28 | (-14.00) | (-16.61) | (-13.00) | (-17.97) | (-11.57) | (-4.69) |

| AsymC | 9.30 | 5.78 | 3.91 | 1.24 | (-15.92) | (-24.71) | (-18.04) | (-15.49) | (-20.5) | 2.13 | (-13.32) | (-38.37) |

| RPnL | (-10.57) | (-36.18) | (-19.41) | (-21.71) | (-33.18) | (-26.42) | (-31.16) | (-39.70) | (-13.90) | (-8.19) | (-19.50) | (-30.56) |

| TC | (-7.22) | (-32.49) | 17.61 | (-7.83) | (-0.82) | 3.45 | (-24.88) | (-2.42) | (-18.55) | (-13.28) | (-24.53) | (-19.34) |

| DSR | (-16.55) | (-23.33) | (-0.66) | 0.18 | 9.98 | (-2.99) | (-7.55) | (-18.71) | (-6.11) | (-19.96) | (-28.43) | (-38.10) |

7.3 Price-based Events

The price-based environments were easier to learn for the agents; 23 out of 84 experiments led to profitable outcomes. This is likely due to the nature of having the agent take steps in the environment only when the price changes, therefore avoiding some noise in the LOB data. Although this environment approach did not yield the highest score, in general the agent trading patterns appeared to be more stable and less erratic during large price jumps.

| Price-event: | Profit-and-Loss (%)††footnotemark: | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| A2C | PPO | |||||||||||

| Reward Function | Set 1 | Set 2 | Set 3 | Set 4 | Set 5 | Set 6 | Set 1 | Set 2 | Set 3 | Set 4 | Set 5 | Set 6 |

| UPnL | (-31.42) | (-28.65) | (-38.74) | (-0.95) | (-0.91) | (-43.58) | (-31.74) | (-25.89) | (-21.37) | (-46.12) | (-16.72) | (-32.32) |

| UPnLwF | 8.80 | (-11.85) | (-18.37) | (-21.66) | (-8.98) | (-20.24) | (-4.61) | (-23.18) | 3.92 | (-9.92) | 3.50 | (-23.28) |

| Asym | (-27.21) | (-2.00) | (-1.66) | (-0.86) | (-14.82) | (-8.16) | (-16.04) | (-12.76) | (-15.32) | (-6.10) | (-15.78) | (-10.73) |

| AsymC | (-7.12) | (-11.58) | (-12.24) | 11.88 | (-14.98) | (-14.12) | (-19.58) | (-15.92) | (-2.08) | (-12.57) | (-8.21) | (-15.42) |

| RPnL | 2.65 | (-1.62) | 6.70 | 8.74 | 6.97 | 6.71 | (-6.29) | (-6.28) | (-13.76) | 3.60 | (-11.47) | (-28.35) |

| TC | 6.28 | 10.66 | 10.19 | 6.91 | 13.43 | 9.57 | 5.72 | (-23.71) | (-29.99) | 2.73 | 11.38 | (-16.25) |

| DSR | (-27.35) | 2.80 | 12.23 | (-1.80) | 9.73 | (-28.14) | (-14.23) | (-13.96) | (-19.67) | (-24.19) | 5.74 | (-33.25) |

8 Conclusion

In this paper, two advanced policy-based model-free reinforcement learning algorithms were trained to learn automated market making for Bitcoin using high resolution Level II tick data from Bitmex exchange. The agents learned different trading strategies from seven different reward functions and six different combinations of features for the agent’s observation space. Additionally, this paper proposes a price-based approach to defining an event in which the agent steps through the environment and demonstrates its effectiveness to solve the automated market making challenge, extending the DRLMM framework [6].

All agents were trained for one million steps across eight days of data and evaluated on 30 out-of-sample days. The A2C algorithm outperformed PPO in terms of cumulative return and number of profitable experiments. An A2C agent with goal-based reward function generated the greatest return for both time- and price-based environments.

Several observations made during the execution of this experiment could lead to fruitful future research avenues. First, a formalized methodology for training model-free reinforcement learning in context of financial time-series problem. More specifically, it would be worthwhile to explore the effects of a framework for scoring and selecting which trading days to include in the training data set (e.g., volatility, daily volume, number of price jumps, etc.). Second, with the demonstrated success of more advanced neural network architectures in the supervised learning domain [1, 21], it would be interesting to see if convolution, attention, and recurrent neural networks help the agents learn to better exploit price jumps.

ACKNOWLEDGEMENTS

Thank you to Toussaint Behaghel for reviewing the paper and providing helpful feedback and Florian Labat for suggesting the use of price-based events in reinforcement learning. Thank you to Mathieu Beucher, Sakina Ouisrani, and Badr Ghazlane for helping execute experiments and collate results.

References

- [1] Zihao Zhang, Stefan Zohren, and Stephen Roberts. Deeplob: Deep convolutional neural networks for limit order books. IEEE Transactions on Signal Processing, 67(11):3001–3012, Jun 2019.

- [2] Baron Law and Frederi Viens. Market making under a weakly consistent limit order book model. 2019.

- [3] Thomas Spooner, John Fearnley, Rahul Savani, and Andreas Koukorinis. Market making via reinforcement learning, 2018.

- [4] Maxime Morariu-Patrichi and Mikko S. Pakkanen. State-dependent hawkes processes and their application to limit order book modelling, 2018.

- [5] E. Bacry and J. F Muzy. Hawkes model for price and trades high-frequency dynamics, 2013.

- [6] Jonathan Sadighian. Deep reinforcement learning in cryptocurrency market making, 2019.

- [7] Richard S. Sutton and Andrew G. Barto. Reinforcement Learning: An Introduction. The MIT Press, second edition, 2018.

- [8] Volodymyr Mnih, Koray Kavukcuoglu, David Silver, Andrei A. Rusu, Joel Veness, Marc G. Bellemare, Alex Graves, Martin Riedmiller, Andreas K. Fidjeland, Georg Ostrovski, Stig Petersen, Charles Beattie, Amir Sadik, Ioannis Antonoglou, Helen King, Dharshan Kumaran, Daan Wierstra, Shane Legg, and Demis Hassabis. Human-level control through deep reinforcement learning. Nature, 518(7540):529–533, February 2015.

- [9] David Silver, Aja Huang, Chris J. Maddison, Arthur Guez, Laurent Sifre, George van den Driessche, Julian Schrittwieser, Ioannis Antonoglou, Veda Panneershelvam, Marc Lanctot, Sander Dieleman, Dominik Grewe, John Nham, Nal Kalchbrenner, Ilya Sutskever, Timothy Lillicrap, Madeleine Leach, Koray Kavukcuoglu, Thore Graepel, and Demis Hassabis. Mastering the game of Go with deep neural networks and tree search. Nature, 529(7587):484–489, jan 2016.

- [10] OpenAI, :, Christopher Berner, Greg Brockman, Brooke Chan, Vicki Cheung, Przemysław Dębiak, Christy Dennison, David Farhi, Quirin Fischer, Shariq Hashme, Chris Hesse, Rafal Józefowicz, Scott Gray, Catherine Olsson, Jakub Pachocki, Michael Petrov, Henrique Pondé de Oliveira Pinto, Jonathan Raiman, Tim Salimans, Jeremy Schlatter, Jonas Schneider, Szymon Sidor, Ilya Sutskever, Jie Tang, Filip Wolski, and Susan Zhang. Dota 2 with large scale deep reinforcement learning, 2019.

- [11] Rakesh Agrawal, Paul E. Stolorz, and Gregory Piatetsky-Shapiro, editors. Proceedings of the Fourth International Conference on Knowledge Discovery and Data Mining (KDD-98), New York City, New York, USA, August 27-31, 1998. AAAI Press, 1998.

- [12] John Moody and Matthew Saffell. Reinforcement learning for trading. In Proceedings of the 1998 Conference on Advances in Neural Information Processing Systems II, pages 917–923, Cambridge, MA, USA, 1999. MIT Press.

- [13] John E. Moody and Matthew Saffell. Learning to trade via direct reinforcement. IEEE Trans. Neural Networks, 12(4):875–889, 2001.

- [14] Carl Gold. Fx trading via recurrent reinforcement learning. 2003 IEEE International Conference on Computational Intelligence for Financial Engineering, 2003. Proceedings., pages 363–370, 2003.

- [15] Yagna Patel. Optimizing market making using multi-agent reinforcement learning, 2018.

- [16] Ashley Hill, Antonin Raffin, Maximilian Ernestus, Adam Gleave, Anssi Kanervisto, Rene Traore, Prafulla Dhariwal, Christopher Hesse, Oleg Klimov, Alex Nichol, Matthias Plappert, Alec Radford, John Schulman, Szymon Sidor, and Yuhuai Wu. Stable baselines. https://github.com/hill-a/stable-baselines, 2018.

- [17] Volodymyr Mnih, Adrià Puigdomènech Badia, Mehdi Mirza, Alex Graves, Timothy P. Lillicrap, Tim Harley, David Silver, and Koray Kavukcuoglu. Asynchronous methods for deep reinforcement learning, 2016.

- [18] John Schulman, Philipp Moritz, Sergey Levine, Michael I. Jordan, and Pieter Abbeel. High-dimensional continuous control using generalized advantage estimation. CoRR, abs/1506.02438, 2015.

- [19] John Schulman, Filip Wolski, Prafulla Dhariwal, Alec Radford, and Oleg Klimov. Proximal policy optimization algorithms, 2017.

- [20] Avraam Tsantekidis, Nikolaos Passalis, Anastasios Tefas, Juho Kanniainen, Moncef Gabbouj, and Alexandros Iosifidis. Using deep learning for price prediction by exploiting stationary limit order book features, 2018.

- [21] James Wallbridge. Transformers for limit order books, 2020.

Appendix A Appendix

A.1 Agent Configurations

The parameters used to train agents in all experiments.

| # | Parameter | Value |

|---|---|---|

| 1 | Action repeats | 5 |

| 2 | Window size | 100 |

| 3 | Transaction fees | Limit -0.025% / Market 0.075% |

| 4 | Max positions | 10 |

| 5 | Gamma | 0.99 |

| 6 | Learning rate | 3e-4 |

| 7 | No. of LOB levels | 20 |

| 8 | K-steps | 256 (PPO) / 40 (A2C) |

| 9 | Training steps | 1,000,000 |

| 10 | Action space | 17 |

| 11 | Dampening | 0.35 |

| 12 | GAE | 0.97 |

| 13 | Price-event threshold | 0.01% |

| 14 | Optimizer | Adam (both A2C and PPO) |

A.2 Observation Space

As set forth in our previous work [6], the agent’s observation space is a combination of three sub-spaces: the environment state space, consisting of LOB, trade and order flow snapshots with a window size ; the agent state space, consisting of handcrafted risk and position indicators; and the agent action space, consisting of a one-hot vector of the agent’s latest action. In this experiment, is set to 100.

A.2.1 Environment State Space

LOB Quantity

The dollar value of each price level in the LOB, where is the dollar value at LOB level at time , applied to both and sides. Since we use the first 20 price levels of the LOB, this feature is represented by a vector of 40 values.

| (11) |

where is the price and is the quantity at LOB level for bid and ask sides, respectively.

LOB Imbalances

The order imbalances are represented by the cumulative dollar value for each price level in the LOB. Since we use the first 20 price levels of the LOB, this feature is represented by a vector of 20 values.

| (12) |

Order Flow

The sum of dollar values for cancel , limit , and market orders is captured between each LOB snapshot. Since we use the first 20 price levels of the LOB, this feature is represented by a vector of 120 values, 60 per each side of the LOB.

| (13) |

| (14) |

| (15) |

where is the number of units available at price at LOB level .

Trade Flow Imbalances

The Trade Flow Imbalances indicator measures the magnitude of buyer initiated and and seller initiated transactions over a given window . Since we use 3 different windows (5, 15, and 30 minutes), this feature is represented by a vector of 3 values.

| (16) |

where and .

Custom RSI

The relative strength index indicator (RSI) measures the magnitude of prices changes over a given window . This custom implementation scales the data so that it does not require normalization, even though we do use the scaled z-score values in our experiment. Since we use 3 different windows (5, 15, and 30 minutes), this feature is represented by a vector of 3 values.

| (17) |

where and and .

Spread

The spread is the difference between the best bid and best ask . This feature is represented as a scalar.

| (18) |

Change in Midpoint

The change in midpoint is the log difference in midpoint prices between time step and . This feature is represented as a scalar.

| (19) |

Reward

The reward from the environment, as described in section 4.

A.2.2 Agent State Space

Net Inventory Ratio

The agent’s net inventory ratio is the inventory count represented as a percentage of the maximum inventory . This feature is represented as a scalar.

| (20) |

Realized PnL

The agent’s realized profit-and-loss is the sum of realized and unrealized profit and losses. In this experiment, the is scaled by a scalar value , which represents the daily PnL target.

Unrealized PnL

The agent’s current unrealized PnL is the unrealized PnL across all open positions. The unrealized PnL feature is represented as a scalar, containing the net of long and short positions.

| (21) |

where is the average price of the agent’s or position and is the midpoint price at time .

Open Order Distance to Midpoint

The agent’s open limit order distance to midpoint is the distance of the agent’s open and limit orders to the midpoint price at time . The feature is represented as a vector with 2 values.

| (22) |

Order Completion Ratio

Order completion is a custom indicator that incorporates an order’s relative position in the LOB queue and partial executions relative to the order size . The feature is represented as a vector with 2 value, one per and sides.

| (23) |

Agent Action Space

The agent’s action space is included in the agent state space. It is represented by a one-hot vector over the action space outlined in table 1.