33institutetext: J.N. Silva 44institutetext: Deparment of Economics, São Paulo State University (UNESP), 14800-901 Araraquara, SP, Brazil

55institutetext: M.A. Bertella 66institutetext: Deparment of Economics, São Paulo State University (UNESP), 14800-901 Araraquara, SP, Brazil

77institutetext: E. Brigatti 88institutetext: Instituto de Física, Universidade Federal do Rio de Janeiro, Av. Athos da Silveira Ramos, 149, Cidade Universitária, 21941-972, Rio de Janeiro, RJ, Brazil

88email: edgardo@if.ufrj.br

The leverage effect and other stylized facts displayed by Bitcoin returns

Abstract

In this paper, we explore some stylized facts of the Bitcoin market using the BTC-USD exchange rate time series of historical intraday data from 2013 to 2020. Bitcoin presents some very peculiar idiosyncrasies, like the absence of macroeconomic fundamentals or connections with underlying assets or benchmarks, an asymmetry between demand and supply and the presence of inefficiency in the form of strong arbitrage opportunity. Nevertheless, all these elements seem to be marginal in the definition of the structural statistical properties of this virtual financial asset, which result to be analogous to general individual stocks or indices. In contrast, we find some clear differences, compared to fiat money exchange rates time series, in the values of the linear autocorrelation and, more surprisingly, in the presence of the leverage effect. We also explore the dynamics of correlations, monitoring the shifts in the evolution of the Bitcoin market. This analysis is able to distinguish between two different regimes: a stochastic process with weaker memory signatures and closer to Gaussianity between the Mt. Gox incident and the late 2015, and a dynamics with relevant correlations and strong deviations from Gaussianity before and after this interval.

Keywords:

Fluctuation phenomena Random processes Noise Brownian motion1 Introduction

A cryptocurrency is a digital currency that can theoretically perform all the three functions of money, namely, medium of exchange, unit of account and store of value. Until now, the spread of this type of money is still in its infancy, despite its considerable numbers: it is estimated that today there are about 5,000 cryptocurrencies with a market capitalization of the order of US$240 billions CoinMarketCap2020 . The first and most important cryptocurrency to date is Bitcoin. It was developed in 2008 and diffused in a paper assigned using the pseudonym of Satoshi Nakamoto Nakamoto2008 . Bitcoin is an open source, peer-to-peer currency, and does not depend on monetary or governmental authority. Its invention is revolutionary given that there is no need to have an agent like a bank to effect the transaction, only the two parties involved: the payer and the receiver of the debt. All transactions carried out are stored in a public register called blockchain so that future transactions are unable to use the previously spent Bitcoins. Note that transactions on the Bitcoin network are not made in another fiat currency but they are made in Bitcoins. Thus, in addition to being a completely decentralized network, it is a virtual currency, where its value is defined in a market, such as the dollar, euro, swiss franc, etc. As its use has been quite restricted, many economists still do not consider it as currency, as it lacks at least one of its typical functions. In fact, Baur et al. BAUR2018 notes that, for the period from 2011 to 2013, most Bitcoins were used as a portfolio asset (value store) and not as a currency (medium of exchange). In fact, most of the demand as a store of value has been directed towards Bitcoin due to the credibility and predictability of its supply and resilience demonstrated during its short existence. The Bitcoin supply will increase around 1% per year for the next 25 years Ammous2018 , whereas the main currencies, like US dollar and Euro, will rise much more than that, specially if the quantitative easing remains as one of the main tools of Central Banks monetary policy. Although Bitcoin has not fulfilled all the three functions of money, it is possible that Bitcoin will continue to draw more interest as a store of value and to play a broader position as a medium of exchange. However, we can not say the same for other cryptocurrencies, which, as a store of value or a unit of account, do not seem to offer any advantages and thus are unlikely to attract interest as a medium of exchange. For instance, Ether, the second largest virtual currency by total market cap, has an annual growth rate much higher than Bitcoin (an estimated average of around 5% between 2020 and 2049) and the Ethereum Foundation (the entity behind this currency) has a discretionary power to change the issuance of Ether Ammous2018 . A presence of a clear and credible commitment to a monetary issuance policy similar to that of Bitcoin lacks to other cryptocurrencies (Ether, Dogecoin, and so forth) and this seems to be one of the main reasons of Bitcoin success. The only digital currency that can credibly show a degree of severe adherence to its issuance timetable is Bitcoin, which gives assured protection to future holders. In sum, the inflexible supply of digital currencies and their volatile demand make them unreliable for use as unit of account. Only Bitcoin may be able to act as a store of value due to its strict dedication to low supply expansion, convincingly supported by the distributed protocol of the network and a reliable proof of the lack of any entity capable of modifying the supply timeline. Centrally managed governance over other digital currencies and the application of tokens with unique purposes render them unable to perform monetary functions.

Empirical studies BAUR2018 ; LIU2018 ; bariviera ; URQUHART2019 show that Bitcoin and other cryptocurrencies generally present time series characterized by the following simple descriptive statistics: high returns, high volatility, important skewness and high kurtosis. Moreover, some return autocorrelations and a changing behavior of the Hurst exponent has been detected.

The study of autocorrelations and its connection with the presence of short or long range memory is a particularly interesting topic because of its relation with the efficient market hypothesis (EMH). This idea implies determining whether asset prices fully reflect all available information fama . If so, it means that any new information is revealed entirely in its price. The question here is to know what kind of information might be taken into consideration for a market to be considered efficient. The most widely used version of EMH is the semi-strong: prices accurately reflect all publicly known information. Under this version, there is no cheap or expensive asset: the current price is always its best estimate. This definition implies that the knowledge of past prices is useless to predict future prices, which leads us to the weak version of EMH: historical prices have no relevance to predict prices. From a statistical viewpoint, this means that asset prices or returns cannot present long range memories, since they would allow a riskless profitable trading strategy. Finally, there is the strong version of EMH: the prices accurately reflect all the information (public and private). While the first two forms of market efficiency, weak and semi-strong, have numerous advocates, there is a general perception that the strong version is difficult to empirically validate.

Since the 1980s, EMH has been questioned and the analysis of the presence of long memory in financial time series has become an important topic, with papers presenting some empirical evidences of long memory noFama , and others challenging it okFama . Several studies have been done to draw some conclusion about the efficiency of Bitcoin, however without a definitive one (see bariviera ; Bartos2015 ; Urquhart2016 ; Nadarajah2017 ; Dimitrova2019 ; Nan2019 among others). Bartos Bartos2015 analyses the effects of public announcements on Bitcoin price concluding for a positive answer. Therefore, its price seems to follow the EMH. Urquhart Urquhart2016 , through several tests, finds that Bitcoin market is inefficient, but when he splits into two subsample periods, he finds that the Bitcoin may be in a process towards efficiency. Nadarajah and Chu Nadarajah2017 show, through eight different tests, that Bitcoin satisfies the EMH. Dimitrova et al. Dimitrova2019 conclude that, although the self-similarity exponent of the BTC-USD price series is different than 0.5, this result is not due to the presence of significant memory but to its underlying distribution. Bariviera et al. bariviera analyze the behavior of long memory of returns from 2011 until 2017, using the Hurst’s exponent. They show a persistent behavior from 2011 until 2014, whereas the series is more informational efficient since 2014. Finally, Nan and Kaizoji Nan2019 study the Bitcoin market efficiency in terms of the Bitcoin exchange rate and conclude that the weak and semi-strong form of market efficiency of the USD/EUR Bitcoin exchange rate holds in the long run concerning the spot, futures, and forward FX markets.

These analysis are of particular relevance since the common sense speaks about inefficiency of the cryptocurrency market. Arbitrage opportunity are evident, as the price may present an enormous spread among the different platforms used for buying and selling the cryptocurrency. Moreover, Bitcoin price is not driven by macro-financial indicators, a fact that can generate more sensitivity on information flows in market affecting the supply and demand interaction. For these reasons, a natural question that emerges is whether these inefficiencies can be tracked in the Bitcoin historical time series, either in the form of a clear long memory, or in more subtle temporal structures present in the data.

With this aim, our work will try to systematically characterize the empirical properties of the returns of the Bitcoin time series, highlighting the most relevant stylized facts cont ; cont2 present in these data. Among them, we will describe the heavy tails of the distribution of returns, and the autocorrelations of some nonlinear functions of returns. These features have been studied in recent works with similar or different approaches. A comparison with these previous results will be unfolded in the Sections 4 and 5 of the paper. The important novelty of our work is the clear characterization of the presence of the leverage effect in Bitcoin, and, more in general, in an exchange rate return, by measuring the realized volatilities in intraday data. A comparison of all the examined stylized facts with well known features already detected in the time series of the exchange rate of fiat currencies, which are among the most liquid assets in the world, could shed light on the real impact that inefficiencies can have on the statistical properties of the temporal dynamics of a general financial asset.

This approach will be used also for characterizing the time varying behavior of the evolution of Bitcoin returns (Section 4.2). In this way we will explore the possibility of using some of these statistical features as empirical indicators or signals for monitoring the shifts in the evolution of the Bitcoin market. This analysis will show some interesting aspects related to how important events and publicly announced information can affect the prices of cryptocurrencies.

2 Data

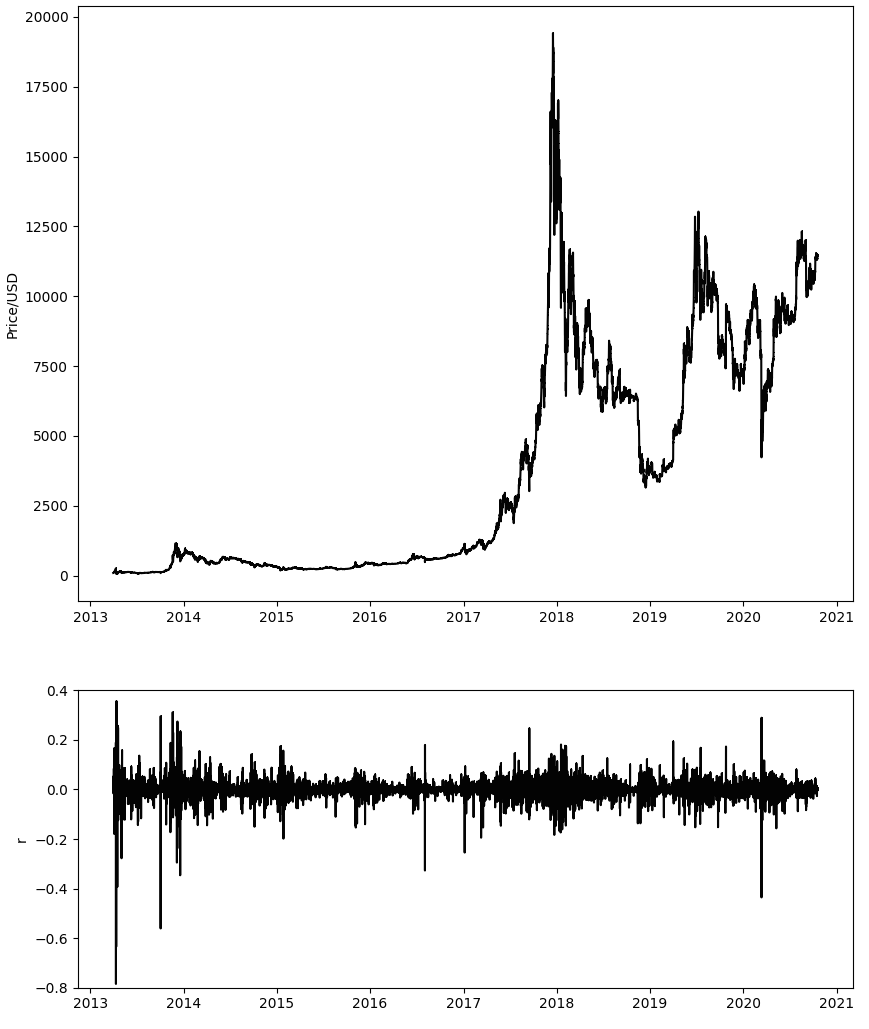

We examine the time series of the price of Bitcoin, expressed in US dollars, from 31/3/2013 to 19/10/2020, with a sampling time interval of 5 hours,

which corresponds to a series of 13246 elements (see Fig. 1).

We leave out earlier periods due to low market liquidity.

Data are extracted from the site Bitcoincharts BitChar and are representing the

Bitcoin price from the Bitstamp exchange market platform.

Note that Bitcoin price, in the considered period, can depend strongly

on the platform used for trading.

At high frequencies, data directly downloaded from Bitcoincharts do not present regular

time intervals of sampling. For this reason, we realize a resampling of the series with intervals of 5 hours. This resampled time series presents a good statistical quality.

3 Stylized facts: definitions and methods

Empirical properties of traditional financial assets

have been characterized by a set of regularities and general tendencies known as “stylized facts” cont ; cont2 .

This term was introduced by the economist N. Kaldor,

who pointed out the importance of highlighting

broad and robust tendencies of statistical dataset, by ignoring individual details Kaldor .

In finance, stylized facts are usually formulated in terms of statistical properties of the time series of asset returns which present a character of universality, being

present in different scenarios and

common to a wide variety of markets, instruments and time periods.

Their identification could be helpful for

validating the approaches used to study financial data and

for establishing empirical based models

in order to produce reliable forecasts.

Among the different stylized facts recently recorded, in this article we will consider a set of facts

presents in the time series of the returns of a single asset and now widely accepted.

In table 1 we present a synthetic representation of

these stylized facts and in the following

we explain in details the methods used for their analysis.

| Stylized Fact | Definiton | Implications |

|---|---|---|

| Heavy tails | Distribution of returns | Finite second moment |

| displays a power-law tail | (fundamental for risk | |

| (tail index ). Increasing | management and | |

| , the distribution | portfolio optimization) | |

| approaches a Normal one. | ||

| Absence of linear | Autocorrelations of returns | Possible evidence |

| autocorrelations | are insignificant, except for | for the efficient market |

| very small intraday scale | hypothesis | |

| Persistence in | Autocorrelation of absolute | Long-range |

| absolute returns | returns decays as a power-law | dependence |

| Volatility | Different measures of | High-volatility tends |

| clustering | volatility display persistence | to cluster in time |

| Leverage effect | Volatility are negatively | Volatility increases |

| correlated with returns | with negative shocks |

As usual, the characterization of stylized facts is realized using the return of the price series , defined as:

| (1) |

where is the price at time and is the considered sampling time interval (for our series, corresponds to 5 hours).

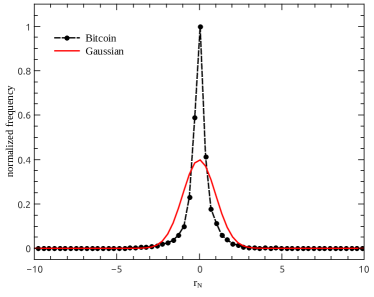

As a first step, we study the distribution of returns,

with the aim of characterizing the expected presence

of heavy tails cont ; cont2 .

The non-Gaussian shape of the distribution of price changes

is a well known character when sufficient small sampling time intervals are considered.

It can be quantified looking at the kurtosis of the distribution.

More interesting is the description of the

behavior of the tail of the distribution.

Based on some general empirical results

for foreign exchange markets and for stock markets guillame ; gabaix ,

the tail can be characterized using a power-law distribution.

For a better comparison with similar works present in the literature,

the distribution of the price change is defined using

a normalized return: ,

where is the mean value of the returns and

the standard deviation estimated over the whole time series.

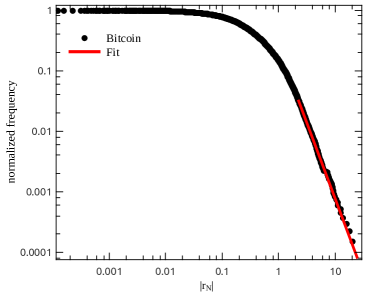

We estimate the power-law exponent (tail index) of the cumulated distribution

using the Maximum Likelihood estimate (see, for example power1 ).

As usual, we use only the data larger than

the smallest value for which the power-law behaviour holds ().

This lower bound on the power-law behaviour is estimated

following an approach proposed by Clauset et al. power3 :

we select the value that makes the probability distribution of the measured

data and the best-fit power-law model as similar as possible above .

We continue our analysis studying the dependence and memory properties of the time series. We analyse the autocorrelation function:

| (2) |

where is the Pearson’s correlation between the two variables.

In liquid markets this linear autocorrelation function is

expected to reach zero in a few minutes, with really faster decays in the most liquid ones, like

the foreign exchange markets corr2 ; corr .

This fact has been often cited for supporting the efficient market hypothesis fama .

In addition, we tested the autocorrelation present in our time series with a non-parametric measure, by using the Spearman’s rank-order correlation spearman .

The Spearman’s correlation between two variables is equal to the Pearson’s correlation between the rank values of those two variables. In our case, the Spearman’s autocorrelation function corresponds to: .

More details can be found in Lehmann .

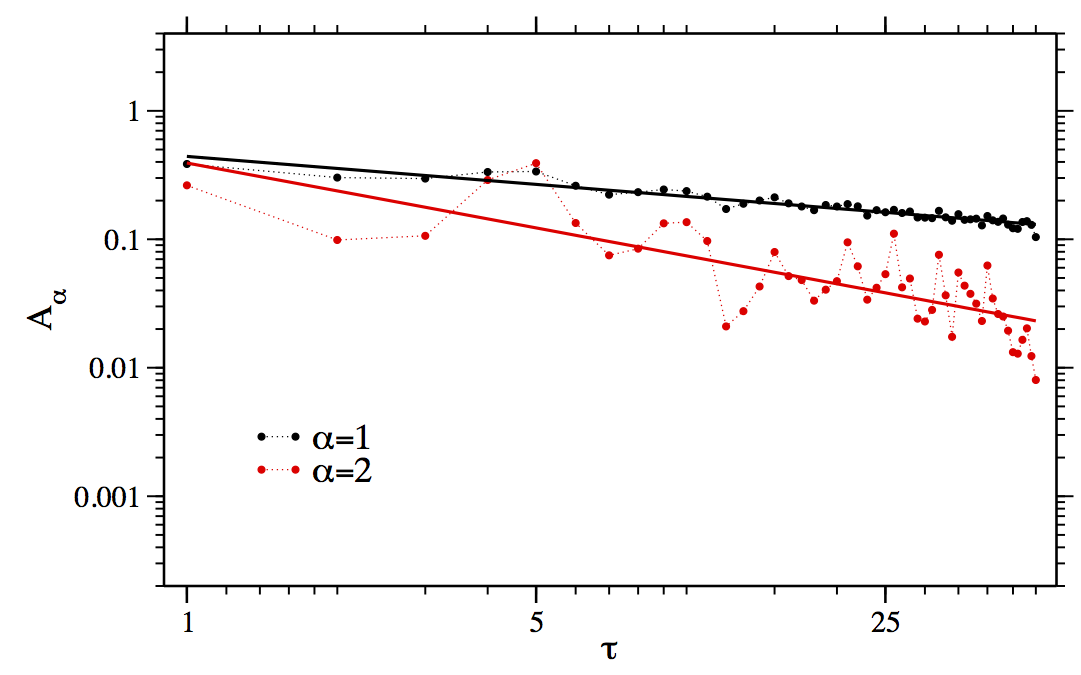

For assuring the independence of the elements of the time series not only the linear autocorrelation, but any nonlinear function of returns should present no autocorrelation. This property is not satisfied by financial time series. Absolute and squared returns show important positive autocorrelations, a fact generated by the tendency of large price variations to be followed by large price variations (volatility clustering). For this reason we will analyse the autocorrelation functions of powers of absolute returns:

| (3) |

considering the case with and . The first one generally presents the highest correlations, and the second one is commonly used for measuring volatility clustering.

The decay of these autocorrelation functions

are usually well described by a power law (see power ):

.

For and the coefficient

, as reported in power2 .

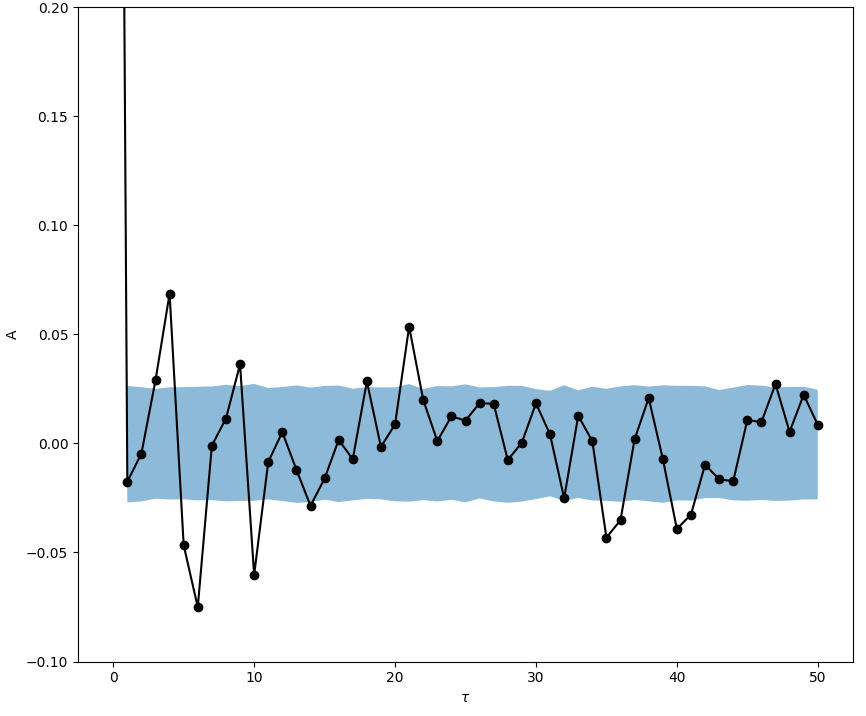

Finally, we measure the correlation of returns with subsequent squared returns:

| (4) |

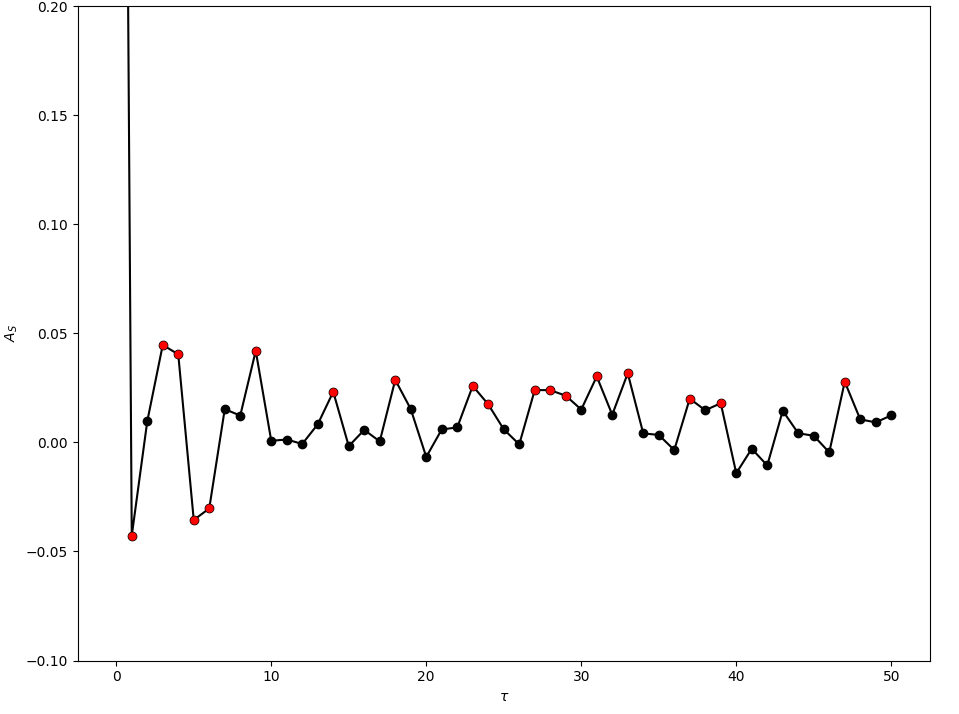

It was shown empirically that this measure generally starts from a negative value for and it grows towards zero corr2 ; leverage0 , suggesting that negative returns generate a rise in volatility. This negative correlation of volatility with returns is usually named “leverage effect”.

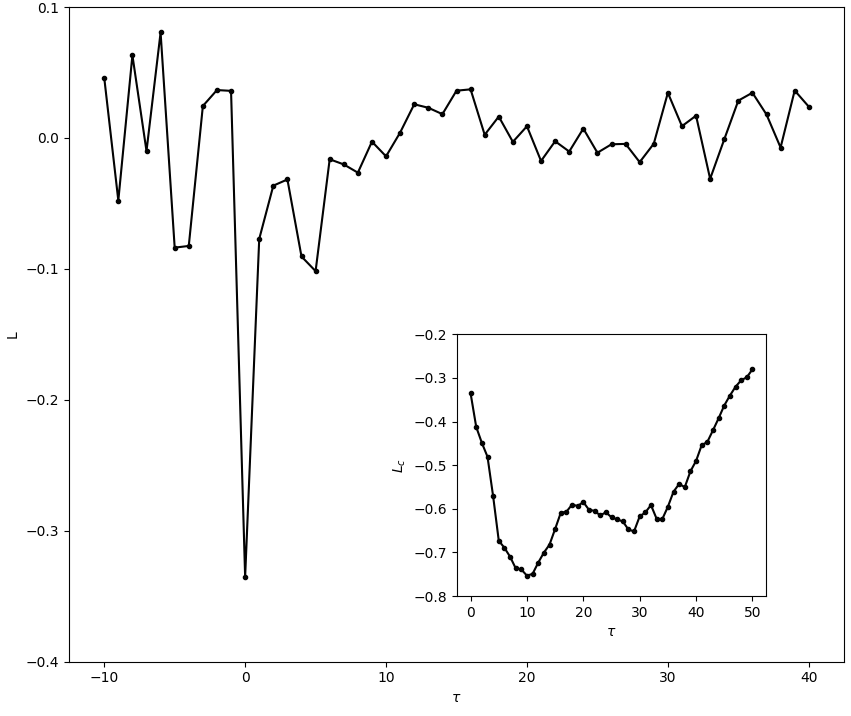

We introduce a simple way for characterizing the presence of the leverage effect in our time series, defining a critical correlation time , which estimates the temporal scale over which the leverage effect (anticorrelation) is relevant. This critical time corresponds to the smallest value of where crosses zero. We can easily estimate calculating the cumulative leverage . Note that, if the time series presents the leverage effect, is negative and is a convex function with a well defined minimum. In this case is the value where reaches the minimum io . In fact, at this lag time the leverage vanishes and the volatility no more exercises a negative influence on the return. If is not clearly negative and does not present a convex shape the leverage effect is not present.

4 Results

4.1 General results

An inspection of simple descriptive statistics of the considered time series gives a Standard Deviation value of 0.032, a Skewness of -2.93 and a Kurtosis of 72.64. These results are consistent with previous results appeared in the literature bariviera which, in relation to other traditional currencies, pointed out an extreme high value of the volatility, with a difference of one order of magnitude and comparable values for higher moments.

In Fig. 2 we present the Bitcoin distribution of the normalized returns , with its obvious non-Gaussian shape. The estimation of the tail index of the cumulated distribution of the absolute value of the normalized returns gives a value of , in good correspondence with the ones measured for the spot intra-daily foreign exchange markets guillame and for stock markets gabaix , where the power law estimation presented exponents close to 3.

In Fig. 3 we displayed the results relative to the values of the linear autocorrelations for our dataset. For the Pearson’s autocorrelation, as the empirical observations are clearly not Gaussian, the significance levels are estimated comparing the correlation function to the 1-/99-percentiles of a generated ensemble of randomized data. In this case, the results show that the linear autocorrelations are close to be negligible. Anyway, we can detect some values slightly above the significance level. Also the Spearman’s autocorrelations present statistical significant values, in particular for . Spearman autocorrelations are smaller than the Pearson ones. This is probably due to important observations present in the tails of the distributions which positively impact the Pearson’s correlation. Our general findings in the measure of the autocorrelation function are consonant with some previous studies bariviera , in particular with the work of Urquhart Urquhart2016 which showed some antipersistent behaviors dependent on the sampling period.

The analysis of the behaviour of the absolute and squared returns for the Bitcoin time series follows the behaviour already recorded for other financial assets. In fact, it presents important positive autocorrelations which decay with a power-law. The exponents of the best fitted functions are for and for . This second value is larger than expected, which corresponds to a faster decay in relation to the behaviour reported in power2 .

The measurement of the volatility-return correlation shows that the values are not significantly different from zero for , whereas they are significant and negative for . This behaviour is consistent with the so-called leverage effect (see Fig. 5). It follows that the cumulated function is a clear convex function, and reaches the minimum for , which delineates a correlation with a decay time slightly longer than 2 days. Leverage effect has been previously detected for individual stocks and stock indices leverage0 ; leverage , with a typical decay time of about 50 days for stocks and 10 days for indices. It is interesting to note that our result is particularly visible. In fact, it does not need to rely on an averaging procedure, as for individual stocks, and the negative correlation is larger than the one usually seen in stock indices. In general, it is common to find empirical studies which present evidence of leverage in stock markets. In contrast, for foreign exchange returns the typical assumption is the absence of such phenomenon Hull , as suggested by a large amount of empirical evidences NoLeverage .

4.2 Running windows

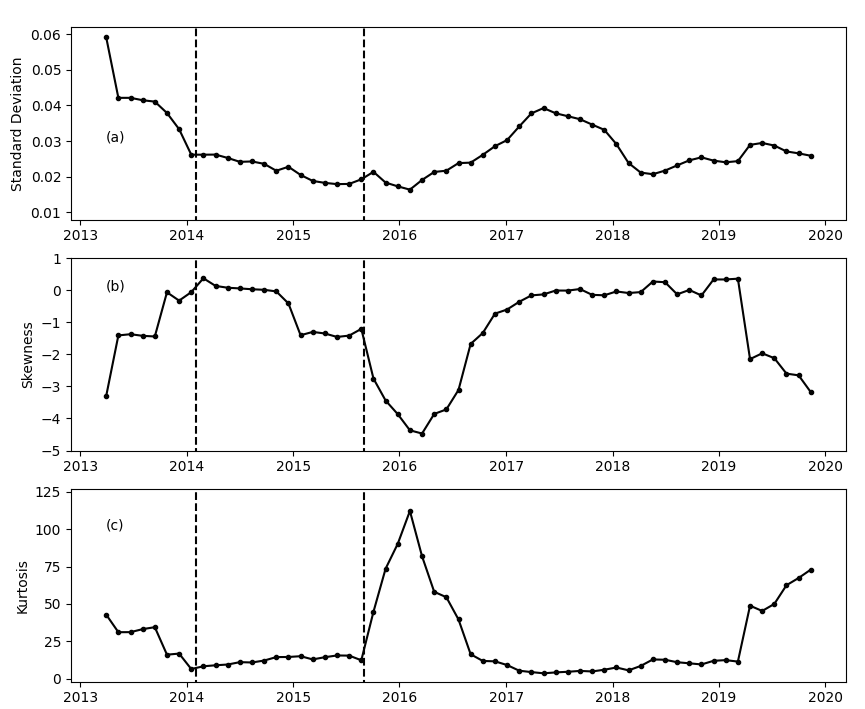

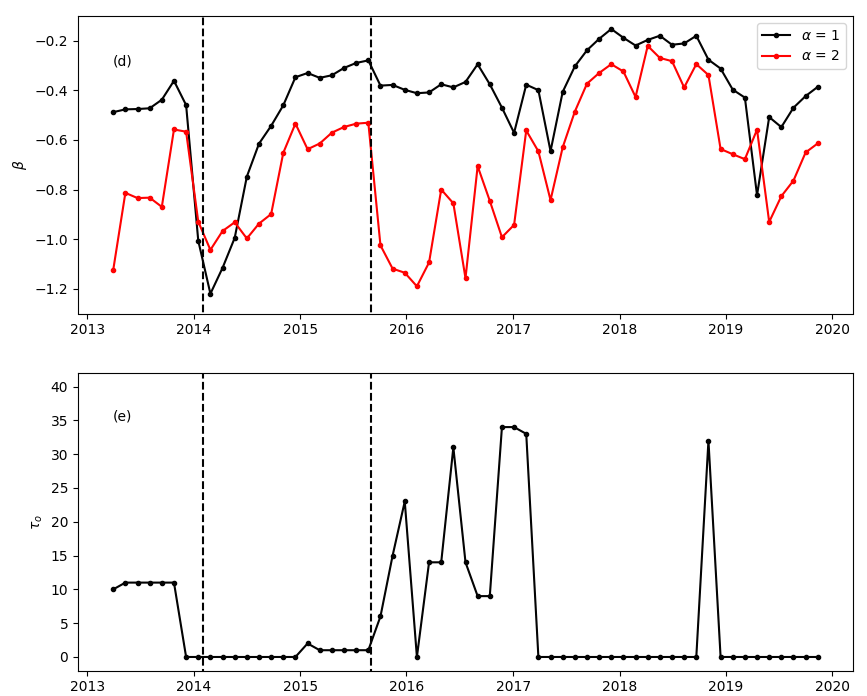

In order to describe the dynamics of correlations all along the evolution of the Bitcoin time series, we partition our dataset using sliding windows. We consider windows of 1600 data points, which correspond to less than one year. The starting points of the windows are considered as the time stamp.

By looking at the behaviour of the moments of the distribution (see Fig. 6) we can note that the volatility decreases monotonically until close to 2/2016, when it starts to grow. Around the same period there is a drop towards strong negative values of the skewness and, conversely, a peak in the value of the kurtosis.

We estimate also the values of the exponents for characterizing the autocorrelation functions of powers of the returns and the characteristic time for describing the presence of the leverage effect (see Fig. 6). By looking at these quantities it is possible to detect two clear critical moments in the time evolution of the Bitcoin market: the early 2014, which presents an abrupt rise in the leverage effect, which reaches a characteristic time of more than 7 days, followed by the disappearance of the same effect. In the same period a strong fall in the exponents of the non-linear correlations is recorded. This period follows the Mt. Gox incident when, in February 2014, this Bitcoin exchange suspended trading and closed its service MtGox .

The second critical moment is in the late 2015, and it is characterized by high values of the exponent for and the reappearance of the leverage effect (). It can be associated with the unsuccessful fork attempt of Bitcoin into Bitcoin XT in August 2015. In between these two important events, the Bitcoin history is characterized by relative small Kurtosis and Skewness.

Over the months following the early 2017 Kurtosis, Skewness and approach values close to 0. In this period, the values of the exponents are comparable to the ones reported in power2 .

5 Discussion

In this paper, we explore some stylized facts of the Bitcoin market from 2013 to 2020, using the BTC-USD exchange rate time series with a time lag of 5 hours.

We detect heavy tails in the distribution of returns, which can be characterized by a power-law. The tail index of the cumulated distribution is close to 3, a value comparable to the one displayed by foreign exchange markets and stock markets guillame ; gabaix . It is interesting to note that, using higher frequencies data, Bitcoin returns distributions with heavier tails () have been recorded begusic . Our result suggests that, at larger temporal scales, the expected exponent close to 3 is recovered.

The analysis of the behaviour of the absolute and squared returns shows important positive autocorrelations, which decay slowly as a function of the time lag, following a power-law with the exponents , for the absolute returns, and for the squared returns. These results are homologous with the behaviour found in the time series of exchange rates of fiat money. By looking at the linear autocorrelations we have observed that even if they are very close to be always negligible, as expected for the exchange rates of fiat money, we can detect some values above the significance level. This fact is consonant with some previous studies bariviera , in particular with the work of Urquhart Urquhart2016 which shows some antipersistent behaviors dependent on the sampling period. More marked differences can be found in the measurement of the volatility-return correlation, which shows a negative correlation (leverage effect) with a decay time slightly longer than 2 days. Bitcoin shows a leverage effect analogous to that of stocks and stock indices, in contrast with the negligible importance that traditional studies give to this effect in exchange rates. Our findings can be contrasted with previous results for Bitcoin time series, which claimed to have found no leverage effect absence or an inverted leverage effect inverted , and compared to a recent analysis of the conditional volatility, based on financial econometrics models, which suggested the possible existence of the effect presence . Important differences are also present in the extreme high value of the volatility, with a difference of one order of magnitude in relation to other fiat money, and the presence of a gain/loss asymmetry, a property usually present in stock prices and stock index values, but not in exchange rates, where there is a higher symmetry in up/down movements.

Bitcoin market is characterized by some very peculiar idiosyncrasies. It seems that there are no macroeconomic fundamentals for digital currencies, nor their values can be derived from an underlying asset or benchmark. The absence of macro-financial indicators should generate more sensitivity on information flows in market and affect the supply and demand interaction. Moreover, there is a clear asymmetry between a demand, strongly influenced by speculative interests, and its rigid supply. The presence of inefficiency in the form of very strong arbitrage opportunity can be easily tracked looking at the important spread among the different platforms used for buying and selling this cryptocurrency. Anyway, all these elements seem to be marginal in the definition of the structural statistical properties of this virtual financial asset, which result to be analogous to general individual stocks or indices. This fact suggests conjecturing about what determines the statistical properties of the considered stylized facts for a general financial asset. As these properties do not change in the case of the Bitcoin, they should be related more to the market and the social component shaping the price, and much less to macroeconomic aspects, or connections with underlying assets or benchmarks.

If the comparison is restricted to fiat money exchange rates time series, we can outline some clear differences in the linear autocorrelation and, most importantly, in the presence of the leverage effect, gain/loss asymmetry and the extreme high value of the volatility.

Foreign exchange rates, with their high liquidity, can be considered as a market which better supports the efficient market hypothesis. In the particular case of the Bitcoin market, the evident detection of positive autocorrelations in the absolute and squared returns and, most importantly, the presence of a clear leverage effect which can be interpreted as a sign of long-range dependence, provide evidence against the efficient market hypothesis.

The second part of our analysis explores the dynamics of correlations all along the evolution of the Bitcoin time series, by partitioning it with sliding windows of 1600 data points, which correspond to less than one year. We look at the behaviour of the moments of the distribution, the character of the slow decay of the absolute and squared returns autocorrelation functions (using the exponent) and the leverage effect (using the characteristic time ). These indicators of specific statistical characters of the time series behave particularly well as empirical signals for monitoring the shifts in the evolution of the Bitcoin market. In fact, their changes are clearly correlated to two important critical moments of the Bitcoin dynamics: the Mt. Gox incident, and the unsuccessful fork attempt of Bitcoin into Bitcoin XT in August 2015.

In the interval between these two important events, the Bitcoin history is characterized by relative small kurtosis and skewness, with absence of the leverage effect and a strong fall in the exponents of the absolute return correlations. These features generally correspond to a stochastic process with weaker memory signatures and closer to Gaussianity. In contrast, outside this region, deviation from Gaussianity (higher skewness and kurtosis) and correlations (leverage and a slower decay in the absolute return correlation) become more relevant. We can note how Mt. Gox incident was a huge strike to the Bitcoin’s credibility and reputation, which affected its price generating a shock in a moment of euphoria, which led to a stable decreasing trend. An inversion to this tendency appeared in the late 2015, with a new rise associated with an increasing popular attention. Following the work of Gerlach et al., this interval corresponds to the correction regime which follows the second Bitcoin’s long bubble, and the neutral period before the rise of the third long bubble Gerlach2019 . From these considerations, we can suppose that periods of greater interest associated to speculative activities generate stronger deviation from Gaussianity and more relevant memory effects.

Similarly, over the months following the early 2017 the absence of the leverage effect and a small skewness is registered. This behaviour occurs with exponents values comparable to the ones of mature markets. These facts suggest that the Bitcoin was approaching a maturity regime, as already pointed out by other works drozdz . Actually, in that period, important events which can be correlated with the maturation of the Bitcoin market happened: the breaking of the psychological USD barrier and the announcement and launch of Bitcoin future contracts.

From the results of our running windows analysis we can state that the considered statistical indicators behave particularly well for monitoring the evolution of the Bitcoin time series and for characterizing the regime switches in the Bitcoin market. For this reason, a future analysis based on these indicators applied to other cryptocurrencies could be able to characterize possible spill-over effects in the cryptocurrency market. This is a theme of particular interest, as already pointed out by Katsiampa et al. Katsiampa , who suggested that there are two-way shock propagation effects between Bitcoin and Ether and Bitcoin and Litecoin. In the first case, past Bitcoin shock news has a positive effect on Ether current conditional volatility, whereas prior Ether shocks have a negative impact on Bitcoin current volatility. As far as Bitcoin and Litecoin are concerned, the lagging shocks of one digital currency adversely impact the present conditional volatility of the other.

Acknowledgements.

F.N.M.S.F. acknowledges the PIBIC program of Universidade Federal do Rio de Janeiro for partial financial support. M.A.B. is grateful to Fapesp (Grant 2018/22562-4) and CNPQ (Grant 303986/2017-4 and 428433/2018-9) for their support.References

- (1) Total Market Capitalization. Available from: https://coinmarketcap.com/all/views/all/

- (2) S. Nakamoto, Bitcoin: A Peer-to-Peer Electronic Cash System (2009). Available from: https://Bitcoin.org/Bitcoin.pdf

- (3) D. G. Baur, K. Hong, A. D. Lee, Bitcoin: Medium of exchange or speculative assets? Journal of International Financial Markets, Institutions and Money, 54, 177 (2018).

- (4) S. Ammous, Can cryptocurrencies fulfil the functions of money? The Quarterly Review of Economics and Finance 70, 38-51 (2018).

- (5) Y. Liu, A. Tsyvinski, Risks and returns of cryptocurrency. Technical Report. National Bureau of Economic Research (2018).

- (6) A. F. Bariviera, M. J. Basgall, W. Hasperué, M. Naiouf, Some stylized facts of the Bitcoin market. Physica A, 484, 82 (2017).

- (7) A. Urquhart, H. Zhang, Is Bitcoin a hedge or safe haven for currencies? An intraday analysis. International Review of Financial Analysis, 63, 49 (2019).

- (8) E. F. Fama, Efficient capital markets: II. J. Finance, 46, 575 (1991).

- (9) M. T. Greene, B. D. Fielitz, Long-term dependence in common stock returns. J. Financ. Econ., 4, 339 (1977); F. Lillo, J. D. Farmer, The Long Memory of the Efficient Market. Stud. Nonlinear Dyn. Econom., 8, 1 (2004); J. T. Barkoulas, C. F. Baum, Long-term dependence in stock returns. Econ. Lett., 53, 253 (1996) ; J. Tolvi, Long memory and outliers in stock market returns. Applied Financial Economics, 13, 495 (2003) ; S. Kasman, E. Turgutlu, A. D. Ayhan, Long memory in stock returns: Evidence from the major emerging central European stock markets. Appl. Econ. Lett., 16, 1763 (2009) ; C. Cheong, Estimating the hurst parameter in financial time series via heuristic approaches. J. Appl. Stat., 37, 201 (2010).

- (10) A. W. Lo, Long-Term Memory in Stock Market Prices. Econometrica, 59, 1279 (1991); A. W. Lo, A. C. MacKinlay, Long-term memory in stock market prices. A Non-Random Walk Down Wall Street. Princeton, New Jersey: Princeton University Press (1999).

- (11) J. Bartos, Does Bitcoin follow the hypothesis of efficient market? International Journal of Economic Sciences, IV, 10 (2015).

- (12) A. Urquhart, The inefficiency of Bitcoin. Economics Letters, 148, 80 (2016).

- (13) S. Nadarajah, J. Chu, On the inefficiency of Bitcoin. Economics Letters, 150, 6 (2017).

- (14) V. Dimitrova, M. Fernández-Martínez, M. A. Sánchez-Granero, J. E. Trinidad Segovia, Some comments on Bitcoin market (in)efficiency. PLoS ONE 14, e0219243 (2019).

- (15) Z. Nan, T. Kaizoji, Market efficiency of the Bitcoin exchange rate: Weak and semi-strong form tests with the spot, futures and forward foreign exchange rates. International Review of Financial Analysis, 64, 273 (2019).

- (16) R. Cont, Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1, 223 (2001).

- (17) A. Chakraborti, I. M. Toke, M. Patriarca, F. Abergel, Econophysics review: I. Empirical facts, Quantitative Finance, 11, 991 (2011).

- (18) BitcoinCharts. Available from: http://Bitcoincharts.com/

- (19) N. Kaldor, Capital accumulation and economic growth. In The Theory of Capital, edited by F.A. Lutz and D.C. Hague, (Macmillan: London), pp. 177-222, (1961).

- (20) Guillaume, Dominique M., Michel M. Dacorogna, Rakhal R. Davé, Ulrich A. Muller, Richard B. Olsen, Olivier V. Pictet, From the Bird’s Eye to the Microscope: A Survey of New Stylized Facts of the Intra-Daily Foreign Exchange Markets. Finance and Stochastics, 1, 95 (1997).

- (21) X. Gabaix et al., Institutional investors and stock market volatility. The Quarterly Journal of Economics, 461 (2006).

- (22) M.E.J. Newman, Power laws, Pareto distributions and Zipf’s law. Contemporary Physics, 46, 323 (2005); A. Clauset, C. Shalizi, and M. Newman, Power-Law distributions in empirical data. SIAM Rev. 54, 661 (2009).

- (23) Clauset, A., M. Young, and K. S. Gleditsch, On the Frequency of Severe Terrorist Events. Journal of Conflict Resolution 51, 58 (2007).

- (24) A. Pagan, The econometrics of financial markets. J. Empirical Finance, 3, 15 (1996).

- (25) E. F. Fama, Efficient capital markets: a review of theory and empirical work. J. Finance, 25, 383 (1971).

- (26) C.E. Spearman, The proof and measurement of association between two things. American Journal of Psychology, 15, 72 (1904); C.E. Spearman, General intelligence, objectively determined and measured. American Journal of Psychology, 15, 201 (1904); C.E. Spearman, Correlation calculated from faulty data. British Journal of Psychology 3 271 (1910).

- (27) Lehmann E., D’Abrera H., Nonparametrics: Statistical Methods Based on Ranks. Springer, New York (2006); Y. Malevergne, D. Sornette, Extreme Financial Risks: From Dependence to Risk Management, Springer, Heidelberg (2006).

- (28) F. Comte, E. Renault, Long memory continuous time models. J. Econometrics, 73, 101 (1996); C. W. J. Granger, Z. Ding, Varieties of long memory models. J. Econometrics, 73, 61 (1996); O. V. Pictet, M. Dacorogna, U. A. Muller, R. B. Olsen, J. R. Ward, Statistical study of foreign exchange rates. J. Banking Finance, 14, 189 (1997).

- (29) Cont R., Potters M. and J.P. Bouchaud, Scaling in stock market data: stable laws and beyond. Scale Invariance and Beyond (Proc. CNRS Workshop on Scale Invariance, Les Houches, 1997) ed. Dubrulle, Graner and Sornette (Berlin: Springer); Y. Liu, P. Cizeau, M. Meyer, C. K. Peng, H. E. Stanley, Correlations in economic time series. Physica A, 245, 437 (1997).

- (30) J. P. Bouchaud, A. Matacz, M. Potters, Leverage Effect in Financial Markets: The Retarded Volatility Model. Phys. Rev. Lett. 87, 228701 (2001).

- (31) A.M. Calvão, E. Brigatti, Collective movement in alarmed animals groups: A simple model with positional forces and a limited attention field, Physica A, 520 450 (2019).

- (32) T. Bollerslev, J. Litvinova, G. Tauchen, Leverage and Volatility Feedback, Effects in High-Frequency Data. Journal of Financial Econometrics, Vol. 4, No. 3, 353 (2006); Jean-Philippe Bouchaud, Marc Potters, More stylized facts of financial markets: leverage effect and downside correlations. Physica A, 299, 60 (2001); A. Pagan, The econometrics of financial markets. J. Empirical Finance, 3, 15 (1996).

- (33) J.C. Hull, Options, Futures and Other Derivatives, 6th Ed. New Jersey: Pearson Prentice Hall (2006).

- (34) Hansen, Peter R., and Asger Lunde, A forecast comparison of volatility models: Does anything beat a garch (1, 1)? Journal of Applied Econometrics, 20, 873 (2005); Bollerslev, T., R. Y. Chou and K. F. Kroner , ARCH Modeling in Finance: A Review of Theory and Empirical Evidence, Journal of Econometrics, 52, 5 (1992).

- (35) D.K. Zuegel, What happened at MtGox? The collapse of the world’s largest Bitcoin exchange. The Stanford Review (2014). Available from: https://stanfordreview. org/what-happened-at-mtgox-the-collapse-of- the-worlds-largest-Bitcoin-exchange/.

- (36) S. Begušic, Z. Kostanjčar, E.H. Stanley, B. Podobnik, Scaling properties of extreme price fluctuations in Bitcoin markets. Physica A, 510, 400 (2018).

- (37) Chamil W. Senarathne, The Leverage Effect and Information Flow Interpretation for Speculative Bitcoin Prices: Bitcoin Volume vs ARCH Effect, European Journal of Economic Studies, 8, 77 (2019); Aviral Kumar Tiwari, Satish Kumar, Rajesh Pathak, Modelling the dynamics of Bitcoin and Litecoin: GARCH versus stochastic volatility models, Applied Economics, 51, 4073, (2019).

- (38) D. Ardia, K. Bluteau, and M. Rüede, Regime changes in Bitcoin GARCH volatility dynamics. Fin. Res. Lett. 29, 266 (2019).

- (39) J. Liu, A. Serletis, Volatility in the Cryptocurrency Market, Open Econ. Rev., 30, 779 (2019).

- (40) J.C. Gerlach, G. Demos, D. Sornette, Dissection of Bitcoin’s multiscale bubble history from January 2012 to February 2018. R. Soc. open sci. 6, 180643 (2019).

- (41) S. Drożdż et al., Bitcoin market route to maturity? Evidence from return fluctuations, temporal correlations and multiscaling effects, Chaos 28, 071101 (2018).

- (42) P. Katsiampa, S. Corbet, B. Lucey, Volatility Spillover Effects in Leading Cryptocurrencies: A BEKK-MGARCH Analysis, Finance Research Letters 29, 68 (2019).