Helena Ferreira

Universidade da Beira Interior, Centro de Matemática e Aplicações (CMA-UBI), Avenida Marquês d’Avila e Bolama, 6200-001 Covilhã, Portugal, helenaf@ubi.ptMarta Ferreira

Center of Mathematics of Minho University, Center for Computational and Stochastic Mathematics of University of Lisbon,

Center of Statistics and Applications of University of Lisbon, Portugal, msferreira@math.uminho.pt

Abstract

We define a multivariate medial correlation coefficient that extends the probabilistic interpretation and properties of Blomqvist’s coefficient, incorporates multivariate marginal dependencies and it preserves a stronger multivariate concordance relation. We determine the maximum and minimum values attainable and illustrate the results in some models. We end with an application on real datasets.

Let us consider that is a real random vector, over the probability space , with continuous marginal distribution functions , , and let represent the corresponding uniformized vector, that is, , .

The medial correlation coefficient of , which we will represent by or , is defined by

(1)

The coefficient introduced by Blomqvist ([1]), has its value in and compares the propensity for the margins of to take both values above or both values below their respective medians, with the propensity for the occurrence of the contrary event.

Since

(2)

and

(3)

if and , , represent the copula and the survival copula of ( Nelsen [8]), respectively, we can say that

(4)

and

(5)

The bivariate medial correlation coefficient enables to compare on

with on

or to compare on with on .

The medial correlation coefficient can be related to other summary measures of dependence in , or in , such as Spearman’s or Kendall’s ( Nelsen [8], Joe [3], Lebedev [6] and references therein).

Two bivariate vectors and , or their copulas, can be partially ordered by punctually comparing their copulas. We say that is less concordant than , and we write for that , if , , or equivalent, if , (Nelsen [8]).

Thus, from the representations (4) or (5), we verify that

(6)

In addition to the increasing with concordance ordering, the bivariate medial correlation coefficient satisfies other properties that shape the definition of measure of concordance according to Scarsini ([9]).

Considering the product and minimum copulas, respectively, and

, , we have , , and we can also represent by

(7)

For a random vector with dimension , if we think about generalizing (1) to we definitely loose:

(i) interpretation as a measure of propensity for all margins to exceed their respective medians or all margins to be below their medians, and

(ii) information about the behaviour of on , , where for or values of and for the others.

On the other hand, any generalization of in the multivariate context must preserve at least the property (i) and also verify

(iii) and .

The proposals of Nelsen ([7]), Úbeda-Flores ([13]) and Schmid and Schmidt ([10]) manage to keep (i) and (iii) above.

Starting from the multivariate version of (5), , rescaled by considering the quotient between its distance to the corresponding value for and the maximum value of that distance,

Úbeda-Flores ([13]) proposes the extension of (4) in

(12)

also rescaled by considering the quotient between its distance to the corresponding value for and the maximum value of that distance. In this way, we obtain the following generalization of , which we will denote by and where represents the vector of suitable size and coordinates all equal to :

Reasoning in an equivalent way about (7), Schmid and Schmidt ([10]) propose

(17)

finding again the expression of Úbeda-Flores ([13]). In addition to this extension, Schmid and Schmidt ([10]) make a detailed study of a function resulting from a rescaling of , , putting emphasis on the tail regions of the copula which determine the degree of large co-movements between the marginal random variables.

In order to keep (i), (ii) and (iii), we have Joe’s sophisticated proposal ([4]) with an axiomatic on linear combinations of and , , , where denotes the j-th reflection of , that is, the vector . Joe’s axiomatic definition allows for various extensions of , including those mentioned above and the arithmetic mean of

, .

The extensions referred for increase with the multivariate concordance (Joe [5]). We say that is less concordant than , or is less concordant than , and in this case we write , when we have

(19)

for . In the case of the two conditions are equivalent, as we have already mentioned.

The above proposed generalizations start from extensions of the representations of bivariate in terms of copulas, considering the corresponding multivariate copulas.

The proposal that we will make, in the next section, for a multivariate correlation coefficient starts from a generalization of the probabilistic interpretation of the definition (1) and satisfies almost all the desirable properties for a multivariate concordance measure (Taylor [11],[12]). It preserves a stronger multivariate concordance relation that we introduce in section 4. We present several representations for , we demonstrate the main properties, relate it to the previously mentioned coefficients and illustrate with examples and applications.

2 Motivation for the multivariate medial correlation coefficient

For , , , with continuous marginal distributions and , we define

(21)

where and are the notations for the maximum and minimum operators, respectively.

When further clarification is needed, we write and .

Inequalities between vectors are understood by corresponding inequalities between homologous coordinates. By we understand the subvector of with margins in and represents the family of subsets of .

Let’s fix disjoint and in . The propensity for margins of and margins of simultaneously taking values below the respective medians or simultaneously values above the respective medians is evaluated by , that is, the probability of taking values in . If we want to compare this probability with the probability of taking values in , we can do it briefly by calculating the coefficients

(25)

and

(29)

Let us make some comments about

(31)

(i) The expressions (25), (29) and (31) have as a particular case, if we take and .

If , and we consider that and , then (31) is equal to , which can be rescaled in order to obtain the proposal of Úbeda-Flores ([13]) and Schmid and Schmidt ([10]).

(ii) Since is defined as an average of bivariate coefficients, it can be estimated by the methods available for the bivariate context (Blomqvist [1], Schmid and Schmidt [10] and references therein).

(iii) If we have and if then , where denotes the cardinality of . This value becomes null if and only if or .

(iv) A linear combination of , , takes into account the bivariate dependencies in , but if we consider some function of the coefficients , with , for some family containing sets with more than one element, then we will be incorporating multivariate marginal dependencies.

The definition we propose, in the next section, for a multivariate medial correlation coefficient, will be based on the bivariate coefficients , , incorporating the dependency between each margin and , .

Our proposal contains, as a particular case, the Blomqvist bivariate coefficient, extends the probabilistic interpretation (1), takes values in , becoming null naturally when and taking the maximum value when . The rest of the properties we proved allow us to consider it a measure for a multivariate concordance relation stronger than concordance order.

3 A multivariate medial correlation coefficient

Definition 3.1.

The multivariate medial correlation coefficient of the vector with dimension , or of its copula , is defined as

(32)

where

(33)

Below we present some representations of that will be useful to clarify their properties and interpretation. The following

reinforces the idea that compares the propensity of each margin to agree with the remaining margins together, , and the propensity to disagree with them, when they are all above or all below their respective medians.

In the following, we establish relationships between and the generalizations referred to in the introduction.

By applying the definition (15) of , we conclude from the representation ( that

That fits Joe’s representation (3.1.1) ([4]) with , and the remaining weights equal to zero.

Note that in the -dimensional case, the multivariate medial correlation coefficient satisfies

(52)

Thus, in the -dimensional case equals and hence allows a different view on Blomqvist’s discussed in Úbeda-Flores ([13]).

We refer the properties of in the next section and end this one with three examples.

Example 3.1.

Consider , with , that is, is the product of two Marshall-Olkin survival copulas ([5]).

It holds that

(56)

Therefore,

(58)

In the case of the result agrees with what we expect, since in this case the margins of are independent. The expression obtained can be related to and

through

(62)

We verify that increases with and , generalizing what we already knew to

and . Therefore increases with the concordance of .

Example 3.2.

Let us consider that has a trivariate Gumbel copula , with .

It holds that

(64)

and

(66)

Therefore, we obtain , coincident with , .

With simple calculations we can also conclude that

and that

which corresponds to the verification in this example of a transition property that we present in the next section.

Before we present the general expression of the multivariate correlation coefficient for a Gumbel distribution of dimension , let’s also calculate it specifically for .

We have

(68)

and

(70)

Then

These results for , calculated directly, can also be obtained from the following general result.

If is even, we have

(considering that a sum with the initial value of the counter greater than the final one is null) and if is odd, we have

The third example also serves as a motivation for one of the properties in the next section, on the best lower limit of .

Example 3.3.

Consider of dimension such that . Then

(76)

It follows that and if, in particular , then .

4 Properties of the multivariate medial correlation coefficient

Since the coefficients , , take values in , the proposed coefficient takes values in the same range, being null for . The maximum value is attainable when and the minimum attainable value is equal to . In fact, from the representation (45), we verify that takes the minimum value when and , what happens when, for example, for some pair and for each , analogously to what we saw in the example 3.3.

The value of may not increase with the concordance of . We can verify this with an example proposed by an anonymous referee.

Consider and -dimensional vetors with copulas, respectively,

(78)

and

(80)

where denotes the countermonotonicity copula, . We have and however .

If and, for each ,

(83)

then, from proposition 3.1, (45), we can conclude that .

The verification of condition (83) together with , which can be illustrated with example 3.2, tells us that, in addition to the propensity for all margins to exceed their respective medians or all margins to be below their medians to be higher in , also the propensity for each margin to disagree with the remaining, in this sense, is lower in , reinforcing the relation .

When we have and (83) we denote this type of relation by .

The above properties on the values of the multivariate medial correlation coefficient are arranged in the following proposition.

Proposition 4.1.

The values of the multivariate medial correlation coefficient for vectors of dimension satisfy the following properties:

(i) If then .

(ii) If then .

(iii) If then .

(iv) The minimum attainable value for is .

In the proposition below we present the properties of continuity, permutation invariance, duality,

reflection symmetry and transition, which together with (i)-(iii) of the previous proposition and following Taylor [11], [12], justifies calling the proposed coefficient a measure for the concordance relation .

Proposition 4.2.

The values of the multivariate medial correlation coefficient for vectors of dimension satisfy the following properties:

(i) If converges uniformly to , , then .

(ii) The value of is invariant for permutations of the margins of .

(iii) .

(iv) .

(v) If is a -dimensional random vector such that then

Proof.

The statement of (i) can be obtained, for example, from (44).

From the representation (50) we can conclude (ii).

The representation (45) leads to (iii) and (iv).

Finally to obtain (v), let us note that, by (45), we have

The multivariate medial correlation coefficient in (32) can be estimated through the bivariate coefficients in (33). Here we consider the respective empirical counterparts. This estimation procedure has already been addressed in literature (Blomqvist [1], Schmid and Schmidt [10] and references therein).

Let , , be a random sample generated from . Consider

We are going to apply the multivariate medial correlation coefficient estimator in (92) on two datasets.

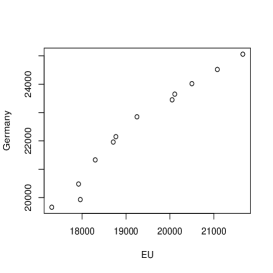

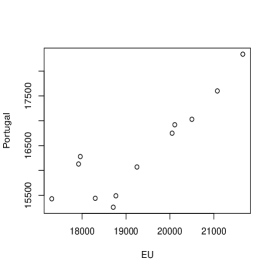

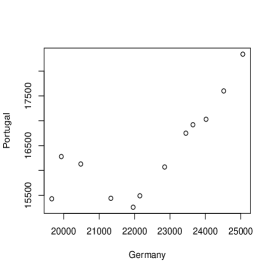

First, we consider the main GDP aggregates per capita in the European Union (EU), Germany and Portugal, available in https://ec.europa.eu/eurostat/data/database. We consider anual data from 2008 to 2019. The respective scatterplots are in Figure 1. Germany and EU seem the most correlated. The estimates of the bivariate coefficients and of the multivariate medial correlation coefficient are in Table 1. We can see that the bivariate medial correlation between Portugal and the remaining EU and Germany presents the lowest contribution to the multivariate medial correlation.

Figure 1: Anual main GDP aggregates per capita in the European Union versus Germany (left), European Union versus Portugal (center) and Germany versus Portugal (right).

Table 1: Estimates of the bivariate coefficients and of the multivariate medial correlation coefficient of the anual main GDP aggregates per capita in the European Union, Germany and Portugal, from 2008 to 2019.

{EU}

{Germany, Portugal}

0.833

{Germany}

{EU, Portugal}

0.833

0.778

{Portugal}

{EU, Germany}

0.667

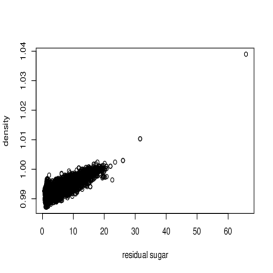

Now we consider a dataset related to white variants of the Portuguese “Vinho Verde" wine, available in http://archive.ics.uci.edu/ml/datasets/Wine+Quality. See also Cortez et al. ([2]). Our analysis focuses on variables residual sugar, density and alcohol, whose respective scatterplots are plotted in Figure 2. It is visible some negative association between alcohol and density, as well as, between alcohol and residual sugar. On the other hand, density and residual sugar are positively correlated. The estimates of the bivariate coefficients and of the multivariate medial correlation coefficient (Table 2) reflect this lack of concordance, with a larger negative bivariate coefficient between alcohol and the remaining variables.

Figure 2: Scatterplots of the variables residual sugar versus density (left), residual sugar versus alcohol (center) and density versus alcohol (right) within the wine dataset.

Table 2: Estimates of the bivariate coefficients and of the multivariate medial correlation coefficient for the variables residual sugar, density and alcohol within the wine dataset.

0.250

0.179

0

-0.429

6 Conclusion

The multivariate medial correlation coefficient that we propose extends the probabilistic interpretation and properties of the Blomqvist coefficient, it is calculable from the copula, incorporates the dependence between each margin of the vector and the vector of the remaining margins and is a measure of a strong mode of multivariate concordance.

The estimation is addressed based on bivariate inferential methodology existing in literature and we illustrate its application using real data.

The adopted approach envisages the possibility of considering other functions of bivariate coefficients envolving extremes of subvectors of , as well as the possibility of adapting the method to generalize other coefficients of bivariate dependence.

Acknowledgements

The authors thank the reviewers and the associated editor for the very important and valuable comments that contributed to the improvement of this work.

The first author was partially supported by the research unit Centre of Mathematics and Applications of University of Beira Interior

UIDB/00212/2020 - FCT (Fundação para a Ciência e a Tecnologia).

The second author was financed by Portuguese Funds through FCT - Fundação para a Ciência e a Tecnologia within the Projects UIDB/00013/2020 and UIDP/00013/2020 of Centre of Mathematics of the University of Minho, UIDB/00006/2020 of Centre of Statistics and its Applications of University of Lisbon and PTDC/MAT-STA/28243/2017.

References

[1] Blomqvist, N. (1950). On a measure of dependence between two random variables. Ann. Math. Statist. 21, 593–600.

[2] Cortez, P., Cerdeira, A., Almeida, F., Matos, T. and Reis, J. (2009). Modeling wine preferences by data mining from physicochemical properties. In Decision Support Systems, Elsevier 47(4), 547–553.

[3]Joe, H. (1997). Multivariate Models and Dependence Concepts. Chapman and Hall London.

[4]Joe, H. (1990). Multivariate Concordance. J. Multivariate Anal. 35, 12–30.

[5] Joe, H. (2015). Dependence Modeling with Copulas. Monographs on Statistics and Applied Probability 134. CRC Press, Boca Raton, FL.

[6] Lebedev, A.V. (2019). On the Interrelation between Dependence Coefficients of Bivariate Extreme Value Copulas. Markov Process. Related Fields 25, 639–648.

[7] Nelsen, R. B. (2002). Concordance and copulas: A survey, Distributions with Given Marginals and

Statistical Modelling (eds. C. Cuadras, J. Fortiana and J. A. Rodrfguez), 169 178, Kluwer Academic Publishers, Dordrecht.

[8] R. Nelsen (2006). An Introduction to Copulas. Springer, New York.

[9] Scarsini, M. (1984) On Measures of Concordance. Stochastica 8(3), 201–218.

[10] Schmid, F. and Schmidt, R. (2007). Nonparametric inference on multivariate versions of Blomqvist’s beta and related measures of tail dependence. Metrika 66, 323–354.

[11] Taylor, M. D. (2007). Multivariate measures of concordance. Ann. Inst. Statist. Math. 59(4), 789–806.

[12] Taylor, M. D. (2016). Multivariate measures of concordance for copulas and their marginals. Depend. Model. 4, 224–236

[13] Úbeda-Flores, M. (2005) Multivariate versions of Blomqvist’s beta and Spearman’s footrule. Ann. Inst. Statist. Math. 57(4), 781–788.