Correlating Lévy processes with Self-Decomposability: Applications to Energy Markets ††thanks: The views, opinions, positions or strategies expressed in this work are those of the authors and do not represent the views, opinions and strategies of, and should not be attributed to E.ON SE.

Abstract

Based on the concept of self-decomposability, we extend some recent multivariate Lévy models built using multivariate subordination with the aim of capturing situations in which a sudden event in one market is propagated onto related markets after a certain stochastic time delay.

Consequently, we study the properties of such processes, derive closed form expressions for the characteristic function and detail how a Monte Carlo scheme can be easily implemented.

We illustrate the applicability of our approach in the context of gas and power Energy markets focusing on the calibration and on the pricing of spread options written on different underlying assets using simulations techniques.

Keywords: Multivariate Lévy Processes, Self-Decomposability, Monte Carlo, FFT, Energy Markets, Spread Options.

1 Introduction

During the last decades a lot of efforts have been done to go beyond the Black and Scholes [3] framework in Financial Modelling. The Black-Scholes (BS) formula is widely used by practitioners but its limits are well-known. Over the years a lot of researchers - Merton [21], Madan and Seneta [20] and Heston [15] among others - have proposed more sophisticated models to overcome its limitations. Nevertheless, their focus is mainly on the single asset modelling framework.

If a multi-asset market has to be considered one has to take care about modeling the dependence structure and this can be a tricky task. One mainly comes up against three issues:

-

•

How to extend a univariate model to a multivariate setting preserving mathematical tractability?

-

•

How to calibrate this model?

-

•

Which techniques can be used for derivatives pricing?

Beyond the Gaussian world, some choices have been proposed to model dependence in the context of Lévy processes. Among others, Cont and Tankov [9], Cherubini et al. [8], Panov and Samarin [22] and Panov and Sirotkin [23] have discussed the use of Lévy copulas or Lévy series representation. Unfortunately, these approaches, especially Lévy copulas, are difficult to handle mathematically and are often hard to calibrate.

In this study we address the three issues above in the context of multi-dimensional processes, that are at least marginally Lévy, using multivariate subordination. To this end, several approaches are available in the literature, for instance Barndorff-Nielsen et al. [2] or Luciano and Schoutens [18] use a common subordinator. In particular, in a series of papers Semeraro [28], Luciano and Semeraro [19], Ballotta and Bonfiglioli [1], Buchmann et al. [4] and Buchmann et al. [5] have proposed models based on subordination to introduce dependence between Lévy process. The common idea of these papers is to define multivariate processes that are the sum of an independent process and a common one. For example Ballotta and Bonfiglioli [1] define a multivariate process in the following way:

where , , are independent Lévy processes. In a financial market, one can see the common process as a systemic risk, whereas the independent processes can be considered as an idiosyncratic component. The model has a simple economical interpretation and it is mathematically tractable.

The assumption that the systemic risk is a driven by a common process simplify the modeling approach but on the other hand, specially in illiquid markets, can be too narrow. Indeed, cases in which we observe delays in market reactions are not so rare. Sometimes a general event has an effect on a market but others related markets could not immediately react. Anyway, it can happen that, as the time goes on, other related markets can be influenced from such an event. As matter of fact we observe a sort of “delay in the propagation of the information” across markets and its clear that such a situation is not taken in account by the existing models.

The aim of this paper is to use the notion of sd, following the approach proposed by Cufaro Petroni and Sabino [11], to extend previous existing models presented by Semeraro [28], Luciano and Semeraro [19] and Ballotta and Bonfiglioli [1] so that the “delay in innovations propagation” effect is considered. This last feature can be captured by simply adding one parameter to the approaches mentioned above without implying a remarkable model complication. From a mathematical point of view it is also worthwhile observing that our model goes beyond the mathematical generalization of the original ones provided by Buchmann et al. [4] and Buchmann et al. [5]: the authors analyze the case where the subordinator is sd. As it will be clear from the sequel, the -reminder part of the subordinator process is infinitely divisible but not sd.

Looking at calibration issue, general techniques, such as Non-Linear-Least-Square (NLLS) or Generalized Method of Moments (GMM), can be adapted to our case, leading to a two-step calibration method as the one presented by Ballotta and Bonfiglioli [1].

About derivative pricing, since chf’s are know in closed form, methods based on Fourier transform, as the ones presented by Hurd and Zhou [16], Pellegrino [24] and Caldana and Fusai [6], can be applied. Moreover standard numerical schemes for path simulations can be adapted to our model, leading to numerical pricing techniques based on Monte Carlo simulations.

The article is organized as follow: in Section 2 we give the basic notions that we need in the sequel and we point up an economic interpretation of proposed modeling framework. In Sections 3 we detail how to extend the models of Semeraro [28], Luciano and Semeraro [19] and Ballotta and Bonfiglioli [1] using sd subordinators, whereas in Section 4 we briefly outline avaiable calibration and pricing techniques, we calibrate these models on Power and Gas Forward markets and we price spread options. Section 5 concludes the paper. All proofs are given in Appendix A.

2 Preliminaries

In this section we introduce the fundamental concepts we need in the sequel: sd laws and Brownian subordination. We look at sd as a natural way to generate correlated rv and we use this notion to build dependent stochastic processes in continuous time. We define increasing dependent stochastic processes and we use the subordination technique to build dependent subordinated Brownian Motions (BM). We refer to Cont and Tankov [9], Sato [27] and Cufaro Petroni [10] for the details.

We recall that a law with probability density (pdf) and characteristic function (chf) is said to be self-decomposable (sd) (see Sato [27] or Cufaro Petroni [10]) when for every we can find another law with pdf and chf such that

| (1) |

We will accordingly say that a random variable (rv) with pdf and chf is sd when its law is sd: looking at the definition, this means that for every we can always find two independent rv’s, (with the same law of ) and (here called -remainder), with pdf and chf such that

| (2) |

It is easy to see that plays the role of correlation coefficient between and : from here follows the idea is to build stochastic Lévy processes starting from rv with sd laws. To this end, it is well-known that if a law is sd then is infinitely divisible (id) and for a given the law of is uniquely determined and id (see Sato [27, Proposition 15.5]).

Since the laws of and have id laws then we can construct the associated Lévy process (Cont and Tankov [9, Proposition 3.1]).

Other important concepts are the notions of subordinators, that are almost surely non-decreasing Lévy processes, and Brownian subordination

(see Cont and Tankov [9]). One can use a non-decreasing Lévy process, called subordinator, to time-change a Lévy process obtaining a new one (Cont and Tankov [9, Theorem 4.2]). If the time-change is done on a BM this operation is then called Brownian subordination.

Definition 2.1.

Consider a probability space , and . Let be a BM and let be a subordinator. A subordinated BM with drift is defined as:

| (3) |

If is -a.s. non-negative random variables with sd law we can build sd subordinators as follows

Definition 2.2 (Self-decomposable subordinators).

Let and be -a.s. non-negative rv with sd laws and define and as Lévy processes such that and . sd subordinators are defined as:

| (4) |

Note that the process defined in (4) is a Lévy process because it is a linear combination of two Lévy processes (Cont and Tankov [9, Theorem 4.1]).

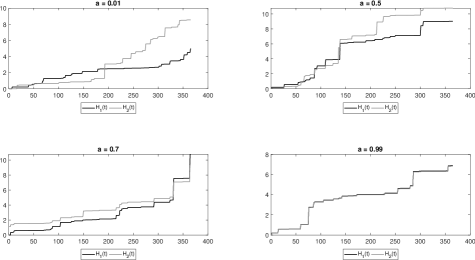

The construction proposed by Equation (4) has a clear financial interpretation. Stochastic times processes “run together” with a stochastic delay, given by the parameter and by the term , one with respect to the other. In Figure 1 different paths of the process are shown, varying the parameter : for fixed the difference between and can be viewed as stochastic delay. Roughly speaking one can observe if then and are essentially indistinguishable.

This construction provides us a powerful tool to model those markets in which, whenever an event occurs in one of them, the effect on the other ones is not immediate but it occurs with a certain time delay. Observe that the parameter is the only parameter we have to add to include this feature in our model and this do not leads to a significant model complication.

The former construction can be extended to the case .

Define , by setting:

where .

In next sections we extend some recently proposed multivariate Lévy models using the sd subordinator . Hereafter, for the sake of notational simplicity, we consider only the case with .

3 Model extensions with Self-Decomposability

In this section we extend the models presented by Semeraro [28], Luciano and Semeraro [19] and Ballotta and Bonfiglioli [1] using sd subordinators introduced in Section 2.

3.1 Extension of Semeraro’s Model

The first model we extend using sd subordinators was proposed by Semeraro [28].

Definition 3.1 (sd-Semeraro Model).

Let be independent subordinators, and , be sd subordinators defined in Equation (4), independent of . Define the subordinator

| (5) |

with . Let , , be standard independent BM’s and let subordinators as is (5). Define the subordinated BM with drift as:

| (6) |

Observe that the “delay in time effect” appears at the level of subordinators and it is given by the couple .

The joint chf of the process defined in (6) has a nice closed expression.

Proposition 3.1 (Characteristic Function).

The joint chf of the process at time defined in (6) is given by:

| (7) |

Note.

Starting from the explicit expression of the chf one can easily compute the linear correlation coefficient at time .

Proposition 3.2 (Correlation).

The correlation at time is given by:

| (8) |

We observe that the value of correlation is lower than the one obtained by Semeraro [28]. This is obvious from an intuitive point of view: in the original model the author modeled the systemic risk component using a common subordinator whilst we use two processes, . On the other hand, as observed before, if then and are indistinguishable and we retrieve the value of correlation obtained by Semeraro [28].

3.1.1 2D - Variance-Gamma

So far we analyzed the general model without assuming a particular form for the law of any of the processes involved. Gamma rv’s have sd law then they are suitable candidates for our construction. Assuming that has Gamma law (with a specific parameters choice) we extend Semeraro’s model for the Variance Gamma process using sd-subordinators.

We recall that a Gamma rv has a density (pdf) and chf given by:

| (9) |

with . It is well-known that if then and if and are independent, then . Now set in (6):

and noting that we have

Remembering that we have the following conditions:

| (10) | |||

| (11) |

Note.

If we request condition (10), we have that:

and so the parameter is somehow redundant and we can assume .

We get the same conclusion observing that, in Equation (8), we fit only the variance of : for this reason assuming is not restrictive.

Corollary 3.3.

Corollary 3.4.

Linear correlation coefficient in 2D Variance-Gamma case is given by:

3.2 Extension of Semeraro-Luciano’s Model

The model presented by Luciano and Semeraro [19], which was developed in order to catch those correlation levels in log-returns that the model proposed by Semeraro [28] is not able to get (see Wallmeier and Diethelm [29]), can be extended in a similar way to what we showed in Section 3.1.

Definition 3.2 (sd-Luciano and Semeraro’s model).

Let , subordinators and let and two sd subordinators independent from . Define the following process:

| (13) |

where and are independent BM’s whereas

and is independent from and .

Here too the chf has a nice closed expression.

Proposition 3.5 (Characteristic Function).

The joint chf of the process at time defined in (13) is given by:

where and

Following the technique proposed for the proof of Proposition 3.2 one can show the following:

Proposition 3.6 (Correlation).

The correlation at time , is given by:

| (14) |

All considerations about correlation coefficient and chf we pointed out in Section 3.1 are still valid.

3.2.1 2D - Variance-Gamma

Here too it’s possible to build a 2D-Variance Gamma process by choosing

We have that:

and, imposing conditions (10) and (11), we have get and, consequently, for . Following the same argument of Section 3.1.1, expressions of linear correlation coefficient and the chf for the 2D Variance Gamma case can be derived.

Corollary 3.7.

Linear correlation coefficient in 2D Variance-Gamma case is given by:

3.3 Extension of Ballotta-Bonfiglioli’s Model

The construction technique of dependent Lévy processes proposed by Ballotta and Bonfiglioli [1] is slightly different from what we have seen so far. The dependence between processes is not introduced on subordinators, as in the previous case, but two subordinated BMof the same type are added together. Some convolution conditions on parameters guarantee that the resulting process is of the same type of the summed ones. This model, as the previous ones, can be extended using sd subordinators.

Definition 3.3 (sd-Ballotta and Bonfiglioli’s model).

Let and be sd subordinators as in (4) and define:

| (15) |

where:

-

•

is a subordinated Brownian motion with parameters , where is the drift, is the diffusion and is the variance of the subordinator. We state the two independent subordinators of with . We have that:

-

•

and are given by:

(16) where and are independent Brownian motions and and .

The following Lemma will help to derive the chf of the process.

The chf of the process defined in (15) is given by the following Proposition.

Proposition 3.9 (Characteristic Function).

The chf of the process at time defined in (15) is given by:

| (17) |

where and and is the Hadamard product.

Note.

As in the precious models it is easy to verify that:

which is the chf obtained by Ballotta and Bonfiglioli [1].

Even then, the correlation coefficient of the process can be obtained.

Proposition 3.10.

The correlation coefficient at time of the process defined in (15) is given by:

| (18) |

3.3.1 Convolution Conditions

It’s easy to show that, if and , are subordinated BM’s with subordinators from the same family, then is a subordinated process of the same type of and if the following Ballotta and Bonfiglioli [1] style convolution conditions hold:

| (19) |

and

| (20) |

Relation (19) holds because and have the same law and so they have the same variance . It is easy to check that if Equations (20) are satisfied then:

3.3.2 2D - Variance-Gamma

We can construct a 2D - Variance-Gamma using Gamma subordinators as follows.

-

•

Let be a Gamma subordinator and set .

-

•

Let be a subordinated BM (with drift and diffusion ) obtained using the Gamma subordinator .

-

•

Let be a subordinated BM (with drift and diffusion ) obtained using a Gamma subordinator .

-

•

Set

We obtain that , , where respect convolution conditions (20).

The joint chf can be easly derived using (17) and remembering the expression of the chf of a rv:

Applying Proposition 3.10 one can derive the correlation coefficient of the 2D - Variance-Gamma process which has the following expression:

4 Financial Application

So far we derived the theoretical modeling framework and we showed how to build correlated Lévy processes using sd subordinators. In this section we show a real application of models presented in Section 3 to energy markets. Many standard techniques for market modeling, calibration, paths simulation and pricing can be adapted to our case.

Similar to what already done in Cont and Tankov [9], we model energy forward markets by defining exponential Lévy processes using the process derived in Section 3. The forward price at time can be defined as follow:

| (21) |

where is the drift correction that leads us to work under a risk-neutral probability measure. Non-arbitrage conditions can be obtained setting:

| (22) |

where is the characteristic exponent of the process .

In order to calibrate our model we use a two steps calibration procedure, as the one proposed by Luciano and Semeraro [19]. It is worthwhile noticing that marginal distributions don’t depend on the parameters we use to model dependence structures. Then, if we observe in the market quoted vanilla products we can obtain the marginal parameter vector solving the following:

| (23) |

where are model prices.

Once we fit we have to calibrate dependence structure. Generally derivatives written on multiple underlying assets are not very liquid: for this reason the dependence parameters vector is estimated fitting the correlation matrix on historical data. Theoretical correlation matrix can be computed using the closed form expression for linear correlation coefficients derived in Section 3.

In the first step we used a NLLS approach combined with the FFT method proposed by Carr and Madan [7] (the version proposed by Lewis [17] leads to similar results), whereas in the second step both NLLS and GMM method can be used: in our experiments we adopted the first one.

An observant reader would point out that 2D-Variance Gamma processes can be easily simulated by using standard techniques presented, for example, in Devroye [14] and Cont and Tankov [9]. The only arising difficulty is the simulation of processes. Cufaro Petroni and Sabino [11, 12] have shown that the -remainder of a Gamma distribution can be exactly simulated by taking:

where

denote a Polya or negative binomial distribution and denotes an exponential distribution. Using this result a simulation scheme can be derived and a Monte Carlo algorithm for pricing purposing developed.

One can argue that, alternatively to MC schemes, since the chf’s of the log-process are known in closed form, Fourier methods can be adopted. Different techniques based on Fourier Transform are available for pricing, and some of them can be used in a multivariate contest (see for example Hurd and Zhou [16], Pellegrino [24] and Caldana and Fusai [6]). In this section we used the method proposed by Caldana and Fusai [6] which gives a good approximation for spread-options prices and it’s simpler to implement than the one proposed by Hurd and Zhou [16], because it requires only one Fourier inversion.

The remaining part of the section is split into two branches:

in the first one we apply our models to the German and French power forward markets, whereas in the second part we focus on German power forward market and to natural gas forward market.

We have chosen those markets because, in the first case we deal with markets that are strongly correlated due to the configuration of European electricity network, whereas in the second case, the correlation between markets is still positive, since natural gas can be used to produce electricity, but it’s not as strong as in the former case. This gives us the opportunity to test our models for different level of correlations.

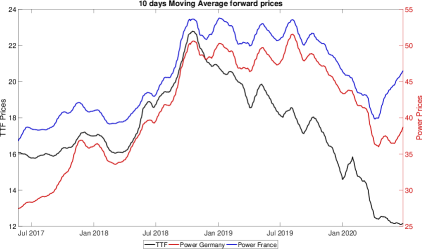

Moreover, as can be observed by Figure 2, due to the structure of European electricity grid, power markets usually react “in the same way at the same time” whereas a delay between power markets and natural gas market is more likely. Then we expect a value for the parameter very close to one between forward power markets and a lower value when we consider forward power and natural gas markets.

For the sake of concision we use the following notation:

-

•

(SSD): sd-Semeraro’s model presented in Section 3.1.

-

•

(LSSD): sd-Luciano and Semeraro’s model presented in Section 3.2.

-

•

(BBSD): sd-Ballotta and Bonfiglioli’s model presented in Section 3.3.

In our experiments we price spread options on future prices, denoted , whose payoff is given by:

It customary to reserve the name Cross-Border or Spark-Spread option if the futures are relative to power or gas markets, respectively. In all our experiments we use the MC technique with simulations and the Fourier-based method proposed by Caldana and Fusai [6].

4.1 Application to German and French Power Markets

In order to calibrate our model we need both derivatives contracts written on forward and historical time series of forward quotations. The data-set111Data Source: www.eex.com. we relied upon is composed as follow:

-

•

Forward quotations from 25 April 2017 to 12 November 2018 of Calendar 2019 power forward. A Forward Calendar 2019 contract is a contract between two counterparts to buy or sell a specific volume of energy in MWh at fixed price for all the hours of 2019. Calendar power forward in German and France are stated respectively with DEBY and F7BY.

-

•

Call Options on power forward 2019 quotations for both countries with settlement date 12 November 2018. We used strikes in a range of around the settlement price of the Forward contract, i.e. we exclude deep ITM and OTM options.

-

•

We assume risk-free rate .

-

•

The historical correlation between markets is .

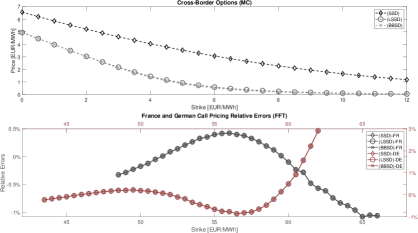

From Table 4 we see that all models provide the same set of marginal parameters. In the lower box of Figure 3 we report the percentage error defined as:

We can observe this error is really small, varying : our model is able to replicate market prices and therefore can be used for pricing purposes.

If we look at the fitted correlation the situation is slightly different. The SSD model presented in Section 3.1 fits a correlation that is roughly zero. For this reason the model is not recommendable for Cross-Border option pricing because it overestimates the derivative price as we can see from the upper picture in Figure 3. The LSSD model of Section 3.2 is better than the previous one and the fitted correlation is very close to the one observed in the market as we can see from Table 4. For this reason the LSSD model can be used to price Cross-Border options. The BBSD model derived by in Section 3.3 provides an even better fitting of market correlation. We conclude that the BBSD model is the best one for the valuation of Cross-Border options. A comparison between models can be found in the upper part of Figure 3: option prices provided by the BBSD model are the lowest ones due to the highest value of fitted correlation.

One additional consideration is needed: we note that, as we expected, for all models, the fitted value for the sd parameters is very close to one. This is not a surprise because German and France forward markets are so strictly correlated that whenever an event occurs in a market it has an immediate impact on the other one. As mentioned before, if we obtain the original models of Semeraro [28], Luciano and Semeraro [19] and Ballotta and Bonfiglioli [1]. For this reason, for Cross Border options, there’s not an essential difference between original models and the extended ones.

| Model | ||||||

|---|---|---|---|---|---|---|

| SSD | 0.40 | 0.61 | 0.31 | 0.32 | 0.02 | 0.02 |

| LSSD | 0.40 | 0.61 | 0.31 | 0.32 | 0.02 | 0.02 |

| BBSD | 0.40 | 0.61 | 0.31 | 0.32 | 0.02 | 0.02 |

| Parameter | Value |

|---|---|

| 41.89 | |

| 1.00 | |

| 0.99 | |

| 0.05 |

| Parameter | Value |

|---|---|

| 42.31 | |

| 1.00 | |

| 1.00 | |

| 0.99 | |

| 0.92 |

| Parameter | Value | Parameter | Value |

|---|---|---|---|

| -0.00 | 0.85 | ||

| 0.09 | 0.50 | ||

| 0.00 | 0.47 | ||

| 0.10 | 0.02 | ||

| 1.01 | 0.99 | ||

| 0.14 | 0.94 | ||

| 0.62 |

4.2 Application to Power German and TTF Gas Future Market

In this section we apply our models to the German power forward market and to the Natural Gas forward market (TTF). These two markets are positively correlated but not as strongly as power markets are.

As in the power case, data-set222Data Source: www.eex.com and www.theice.com we relied upon is the following one:

-

•

Forward quotations from 1 July 2019 to 09 September 2019 relative to the Month January 2019 for the Power Forward in Germany and the Gas TTF Forward.

-

•

Call Options on power forward January 2020 quotations for both Germany and TTF with settlement date 9 September 2019. As done before, we use strikes prices in a range of around the settlement price of the forward contract, i.e. we exclude deep ITM and OTM options.

-

•

We assume risk-free rate .

-

•

The historical correlation between log-returns is .

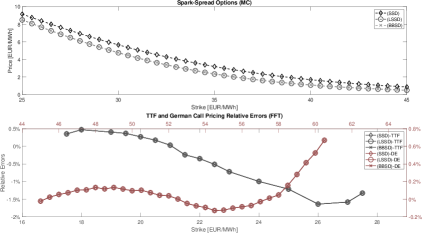

In the picture at the bottom of Figure 4 we can see that all models provide a good fitting of quoted market options because the error is very small. In Figure 4 the picture at the top shows that the SSD model overprices the Spark-Spread option due to the fact that captured correlation is close to zero. Both LSSD and BBSD models provide a lower price of the derivatives because they are able to catch the market correlation. Fitted parameters are shown in Table 8: we observe that the sd parameter is no more as close to one as it was in the forward power markets. This result is reasonable for different reasons. First of all only approximately the 25% of electricity in Germany is produce using natural gas: for this reason if natural gas prices falls the effect on electricity prices could not be immediate. Moreover, despite of what happens for electricity, natural gas can be stored. Many electricity producers subscribe swing contracts to protect against perturbations in natural gas prices. Then a sudden but temporary change in gas market prices doesn’t effect the cost of producing electricity and consequently its price. Of course if the perturbation in natural gas prices last too long, after a while one should expect to observe the perturbation in electricity prices too.

| Model | ||||||

|---|---|---|---|---|---|---|

| SSD | 0.46 | 0.24 | 0.43 | 0.33 | 0.08 | 0.05 |

| LSSD | 0.46 | 0.24 | 0.43 | 0.33 | 0.08 | 0.05 |

| BBSD | 0.46 | 0.24 | 0.43 | 0.33 | 0.08 | 0.05 |

| Parameter | Value |

|---|---|

| 12.36 | |

| 1.00 | |

| 0.99 | |

| 0.04 |

| Parameter | Value |

|---|---|

| 9.89 | |

| 1.00 | |

| 0.89 | |

| 0.90 | |

| 0.57 |

| Parameter | Value | Parameter | Value |

|---|---|---|---|

| 0.13 | 0.29 | ||

| 0.12 | 0.47 | ||

| 0.23 | 0.29 | ||

| 0.23 | 0.11 | ||

| 0.28 | 0.90 | ||

| 0.12 | 0.54 | ||

| 0.47 |

5 Conclusions and further work

Based on the concept of self-decomposability, in this paper we have presented a new method to build dependent stochastic processes that are, at least, marginally Lévy. We have developed the theoretical setting and we have shown how sd subordinators can be built starting from sd laws which are also infinitely divisible. Such processes are extremely useful if one wants to model such markets in which, whenever an event shocks one asset, after a certain random time delay, one can observe the effect spreading to the other ones. Applying this technique, we have embedded this feature inside some recent works based on multivariate subordinators presented by Semeraro [28], Luciano and Semeraro [19] and Ballotta and Bonfiglioli [1] and we have shown how explicit expressions for the chf and the correlation can be derived. These results are instrumental to design Monte Carlo schemes and Fourier techniques employed to calibrate the models to real data in energy markets and to price Cross Border and Spark Spread options. We focused on German and French power and gas forward markets and we calibrated our models using a two steps calibration technique, consisting in fitting firstly marginal parameters on quoted vanilla products and secondly, the correlation on historical realizations. Numerical experiments have shown that our proposed models can catch even extreme values of correlation between assets.

Our approach, and the relative developed numerical techniques, have been applied to energy markets with two correlated underlying assets only. Nevertheless, our modeling framework is very general and can be applied to an arbitrary number of underlying assets. Moreover, such a framework can be used, for example, in equity derivatives, with an arbitrary number of stocks, or in credit risk to model a chain of defaults caused by a common market shock that propagates across markets.

On the other hand, from a more mathematical perspective some points are still open and will be the objective of future inquires. For instance, our models have Lévy margins but it is still unclear whether the couple is still a Lévy process.

In addition, although most of our results are general, we focused on sd Gamma subordinators. It will be worthwhile investigating the case of Inverse Gaussian processes, and therefore Normal Inverse Gaussian processes, in more detail, deriving for instance, an efficient Monte Carlo algorithm to simulate the relative -remainder where some intuition may come from the results in Dassios et al. [13]. Finally, a topic deserving further investigation is the time-reversal simulation of such processes in order to efficiently price other contracts like swings and storages via backward simulation as detailed in Pellegrino and Sabino [25] and Sabino [26].

Appendix A Proofs

A.1 Proof of Proposition 3.1 (See page 3.1)

Proof.

Substituting the expression of , conditioning with respect and since are independent we get:

Using the definition of we have:

and, observing that , and , are mutually independent the thesis follows. ∎

A.2 Proof of Proposition 3.2 (See page 3.2)

Proof.

We have to compute:

Substituting the expressions of and and observing that

the thesis follows from straightforward computations. ∎

A.3 Proof of Proposition 3.5 (See page 3.5)

Proof.

Rewrite as:

where:

and:

The characteristic function is given by:

| (24) |

We now compute the two last term separately. Substituting the expression of , conditioning respect and remebering that and are idependent we have:

| (25) |

Following the same approach we can compute the second term, obtaining:

Now we compute the inner expected values separately. The second inner expected value is:

For the second therm we have that, since is known:

The only unknown terms is the expected value. We have that:

A.4 Proof of Lemma 3.8 (See page 3.8)

Proof.

Replacing the definition of and we get:

We compute now the inner expected value:

The second computation of the second expected value is immediate.

For the first term we have:

Observing that and are idependent the thesis follows. ∎

A.5 Proof of Proposition 3.9 (See page 3.9)

Proof.

Replacing the expression of we have that:

Observe that, conditioning to , we have that:

This observation jointly with Lemma 3.8 complete the proof. ∎

A.6 Proof of Proposition 3.10 (See page 3.10)

References

- Ballotta and Bonfiglioli [2013] L. Ballotta and E. Bonfiglioli. Multivariate Asset Models Using Lévy Processes and Applications. The European Journal of Finance, 13(22):1320–1350, 2013.

- Barndorff-Nielsen et al. [2001] O.E. Barndorff-Nielsen, J. Pedersen, and K. Sato. Multivariate Subordination, Self-Decomposability and Stability. Advances in Applied Probability, 33(1):160–187, 2001.

- Black and Scholes [1973] F. Black and M. Scholes. The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3):637–654, 1973.

- Buchmann et al. [2017] B. Buchmann, B. Kaehler, R. Maller, and A. Szimayer. Multivariate Subordination Using Generalised Gamma Convolutions with Applications to Variance Gamma Processes and Option Pricing. Stochastic Processes and their Applications, 127(7):2208–2242, 2017.

- Buchmann et al. [2019] B. Buchmann, K. Lu, and D. Madan. Self-Decomposability of Variance Generalised Gamma Convolutions. arXiv:1712.03640 [math.PR], 2019.

- Caldana and Fusai [2016] R. Caldana and G. Fusai. A General Closed-Form Spread Option Pricing Formula. Journal of Banking & Finance, 12(37):4863–4906, 2016.

- Carr and Madan [1999] P. Carr and D.B. Madan. Option Valuation Using the Fast Fourier Transform. Journal OF Computational Finance, 2:61–73, 1999.

- Cherubini et al. [2013] U. Cherubini, E. Luciano, and Vecchiato V. Copula Methods in Finance. Wiley Finance, 2013.

- Cont and Tankov [2003] R. Cont and P. Tankov. Financial Modelling with Jump Processes. Chapman and Hall, 2003.

- Cufaro Petroni [2008] N. Cufaro Petroni. Self-decomposability and Self-similarity: a Concise Primer. Physica A, Statistical Mechanics and its Applications, 387(7-9):1875–1894, 2008.

- Cufaro Petroni and Sabino [2020a] N. Cufaro Petroni and P. Sabino. Gamma Related Ornstein–Uhlenbeck Processes and their Simulation. available at: https://arxiv.org/abs/2003.08810, 2020a.

- Cufaro Petroni and Sabino [2020b] N. Cufaro Petroni and P. Sabino. Fast Pricing of Energy Derivatives with Mean-reverting Jump-diffusion Processes. available at: https://arxiv.org/abs/1908.03137, 2020b.

- Dassios et al. [2018] A. Dassios, Y. Qu, and H. Zhao. Exact Simulation for a Class of Tempered Stable and Related Distributions. ACM Trans. Model. Comput. Simul., 28(3), July 2018.

- Devroye [1986] L. Devroye. Non-Uniform Random Variate Generation. Springer-Verlag, 1986.

- Heston [1993] S. L. Heston. A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options. The Review of Financial Studies, 6(2):327–343, 1993.

- Hurd and Zhou [2009] T.R. Hurd and Z. Zhou. A Fourier Transform Method for Spread Option Pricing. https://arxiv.org/pdf/0902.3643.pdf, 2009.

- Lewis [2001] A. Lewis. A Simple Option Formula for General Jump-Diffusion and Other Exponential Lévy Processes. available at http://optioncity.net/pubs/ExpLevy.pdf, 2001.

- Luciano and Schoutens [2006] E. Luciano and W. Schoutens. A Multivariate Jump-driven Financial Asset Model. Quantitative Finance, 6(5):385–402, 2006. URL https://doi.org/10.1080/14697680600806275.

- Luciano and Semeraro [2010] E. Luciano and P. Semeraro. Multivariate Time Changes for Lévy Asset Models: Characterization and Calibration. Journal of Computational and Applied Mathematics, 233(1):1937–1953, 2010.

- Madan and Seneta [1990] D. B. Madan and E. Seneta. The Variance Gamma (V.G.) Model for Share Market Returns. The Journal of Business, 63(4):511–524, 1990.

- Merton [1976] R.C. Merton. Options Pricing when Underlying Shocks are Discontinuous. Journal of Financial Economics, 3:125–144, 1976.

- Panov and Samarin [2019] V. Panov and E. Samarin. Multivariate Asset-Pricing Model Based on Subordinated Stable Processes. Applied Stochastic Models in Business and Industry, 35(4):1060–1076, 2019.

- Panov and Sirotkin [2017] V. Panov and I. Sirotkin. Series Representations for Bivariate Time-Changed Lévy Models. Methodology and Computing in Applied Probability, 19:97–119, 2017.

- Pellegrino [2016] T. Pellegrino. A General Closed Form Approximation Pricing Formula for Basket and Multi-Asset Spread Options. The Journal of Mathematical Finance, 6(5):944–974, 2016.

- Pellegrino and Sabino [2015] T. Pellegrino and P. Sabino. Enhancing Least Squares Monte Carlo with Diffusion Bridges: an Application to Energy Facilities. Quantitative Finance, 15(5):761–772, 2015.

- Sabino [2020] P. Sabino. Forward or Backward Simulations? A Comparative Study. Quantitative Finance, 2020. In press.

- Sato [1999] K. Sato. Lévy Processes and Infinitely Divisible Distributions. Cambridge U.P., Cambridge, 1999.

- Semeraro [2008] P. Semeraro. A Multivariate Variance Gamma Model For Financial Applications. International Journal of Theoretical and Applied Finance, 11(1):1–18, 2008.

- Wallmeier and Diethelm [2010] M. Wallmeier and M. Diethelm. Multivariate Downside Risk: Normal Versus Variance Gamma. Available at www.ssrn.com, 2010.