Double Debiased Machine Learning Nonparametric Inference with Continuous Treatments

(first version: February 2019) )

Abstract

We propose a doubly robust inference method for causal effects of continuous treatment variables, under unconfoundedness and with nonparametric or high-dimensional nuisance functions. Our double debiased machine learning (DML) estimators for the average dose-response function (or the average structural function) and the partial effects are asymptotically normal with nonparametric convergence rates. The first-step estimators for the nuisance conditional expectation function and the conditional density can be nonparametric or ML methods. Utilizing a kernel-based doubly robust moment function and cross-fitting, we give high-level conditions under which the nuisance function estimators do not affect the first-order large sample distribution of the DML estimators. We provide sufficient low-level conditions for kernel, series, and deep neural networks. We justify the use of kernel to localize the continuous treatment at a given value by the Gateaux derivative. We implement various ML methods in Monte Carlo simulations and an empirical application on a job training program evaluation.

Keywords: Average structural function, cross-fitting, dose-response function, doubly robust.

JEL Classification: C14, C21, C55

1 Introduction

We propose a nonparametric inference method for continuous treatment or structural effects, under the unconfoundedness assumption and in the presence of nonparametric nuisance functions. We focus on the heterogenous effect with respect to the continuous treatment or policy variable . To identify the causal effects, it is plausible to have a large number of the control variables that is randomly assigned conditional on. To achieve doubly robust inference and to employ machine learning (ML) methods, we use a double debiased ML approach that combines a doubly robust moment function and cross-fitting.

We consider a nonparametric and model-free outcome equation . No functional form assumption is imposed on the unobserved disturbances , such as restrictions on dimensionality, monotonicity, or separability. The potential outcome is indexed by the hypothetical treatment value . The object of interest is the average dose-response function as a function of , defined as the expected value of the potential outcome across observations with the observed and unobserved heterogeneity , i.e. . It is also known as the average structural function in nonseparable models in Blundell and Powell (2003). The well-studied average treatment effect of switching from treatment to is . We allow the continuous treatment to be multi-dimensional and hence capture the unrestricted heterogenous effects with respect to the multivariate treatment variables. We define the partial (or marginal) effect of the first component of the continuous variable at to be the partial derivative . In program evaluation, the average dose response function shows how participants’ labor market outcomes vary with the length of exposure to a job training program. In demand analysis when contains price and income, the average structural function can be the Engel curve. The partial effect reveals the average price elasticity at given values of price and income. Other examples include the efficacy of political advertisements on campaign contributions in Fong et al. (2018), the effect of nurse staffing on hospital readmissions penalties in Kennedy et al. (2017), etc.

We are among the first to apply the double debiased ML approach to inference on the average structural function and the partial effect of continuous variables, to our knowledge. They are non-regular nonparametric objects that cannot be estimated at a root- convergence rate. We propose a kernel-based double debiased machine learning (DML) estimator that utilizes a doubly robust moment function and cross-fitting via sample-splitting. The DML estimator uses the moment function

| (1.1) |

where the conditional expectation function and the conditional density is also known as the generalized propensity score (GPS). A kernel weights observation with treatment value around in a distance of . The number of such observations shrinks as the bandwidth vanishes with the sample size . A -fold cross-fitting splits the sample into subsamples. The nuisance function estimators for and use observations in the other subsamples that do not contain the observation . The DML estimator averages over the subsamples. Then we estimate the partial effect by a numerical differentiation.

The doubly robust moment function in equation (1.1) has appeared in Kallus and Zhou (2018) without asymptotic theory and has been extensively studied in Su et al. (2019) for Lasso-type estimators. We utilize cross-fitting and provide high-level and low-level conditions that facilitate a variety of nonparametric and ML methods. As each ML method has its strengths and weaknesses depending on the data generating process and applications, flexible employment of various nuisance function estimators is desirable. High-dimensional control variables can be accommodated via the nuisance function estimators; for example, Lasso allows the dimension of to grow with the sample size. Importantly our inference theory for the proposed DML estimator allows one of the nuisance functions to be misspecified. The doubly robust inference is useful, especially when the nuisance functions are estimated under a parametric model or sparsity approximation as Lasso.

We show that the proposed kernel-based DML estimators are asymptotically normal and provide high-level conditions under which the nuisance function estimators for and do not affect the first-order asymptotic distribution. Specifically the high-level conditions on the convergence rates use a partial norm that fixes the treatment value at , in contrast to the standard norm that integrates over the joint distribution of , i.e. the root-mean-square rate. We further give low-level conditions for nonparametric kernel, series estimators, and the deep neural networks in Farrell et al. (2021b) that is widely popular in industrial applications. These results on the convergence rates of the nuisance function estimators are new to the literature.

Furthermore, we propose a Simulated DML (SDML) estimator that replaces in (1.1) with where a simulated variable localizes the realized treatment values around the target value . Introducing such a local variation enables the standard convergence rate of the nuisance function estimator that is available for nonparametric kernel and series estimators, as well as recent ML estimators, such as Lasso in (Bickel et al., 2009), neural networks in (Chen and White, 1999; Schmidt-Hieber, 2020; Farrell et al., 2021b), random forests in (Syrgkanis and Zampetakis, 2020), and empirical rate for boosting in Luo and Spindler (2016), as discussed in Chernozhukov et al. (2018) (CCDDHNR, hereafter) and Chernozhukov et al. (2022a).222 We are grateful to Whitney Newey for the idea of simulating from the probability density function . This result is valuable, as the SDML estimator readily allows for a wider class of ML methods.

In addition, we propose generic ML estimators for the reciprocal of the conditional density when and for when respectively, which may be of independent interest. We also propose a data-driven bandwidth to consistently estimate the optimal bandwidth that minimizes the asymptotic mean squared error.

We aim for a tractable inference procedure that is flexible to employ

nonparametric or ML nuisance function estimators and delivers a reliable distributional approximation in practice.

Toward that end, the DML method contains two key ingredients: a doubly robust moment function and cross-fitting.

The doubly robust moment function reduces sensitivity in estimating with respect to nuisance parameters.333

The double robustness usually refers to consistency of the estimator even if either one of the two nuisance functions is misspecified.

The rapidly growing ML literature has utilized the double robustness

to reduce regularization and modeling biases in estimating the nuisance functions by ML or nonparametric methods;

for example, Belloni

et al. (2014), Farrell (2015), Belloni et al. (2017), Farrell

et al. (2021b), Chernozhukov et al. (2022), CCDDHNR, Rothe and

Firpo (2019), and references therein.

Cross-fitting further removes bias induced by overfitting and achieves stochastic equicontinuity without strong entropy conditions.444

CCDDHNR point out that the commonly used results in empirical process theory, such as Donsker properties, could break down in high-dimensional settings.

For example, Belloni et al. (2017) show how cross-fitting weakens the entropy condition and hence the sparsity assumption on nuisance Lasso estimator.

The benefit of cross-fitting is further investigated by Wager and

Athey (2018) for heterogeneous causal effects, Newey and

Robins (2018) for double cross-fitting, and Cattaneo and

Jansson (2019) for cross-fitting bootstrap.

Related literature: Our work builds on the results for semiparametric models in Ichimura and

Newey (2022), Chernozhukov et al. (2022), and CCDDHNR and extends the literature to nonparametric continuous treatment/structural effects.

Note that the doubly robust estimator for a binary/multivalued treatment replaces the kernel with the indicator function in equation (1.1) and has been widely studied, especially in the recent ML literature.

We show that the advantageous properties of the DML estimator for the binary treatment carry over to the continuous treatments case.

Our DML estimator utilizes the kernel function for the continuous treatments of fixed low dimension and averages out the covariates .

While our kernel-based estimator appears to be a simple modification of the binary treatment case in practice,

we show that one important distinct feature of non-regular nonparametric parameters is that

the Gateaux derivative and the Riesz representer are not unique, depending on how we approximate the continuous treatment distribution approaching a point mass.

And the kernel function is a natural choice for localization at .

Neyman orthogonality holds as ((Neyman, 1959)).

Therefore we provide a foundational justification for the proposed kernel-based DML estimator , relative to alternative approaches, such as Kennedy

et al. (2017) and Semenova and

Chernozhukov (2020); see also van der

Laan et al. (2018).

Furthermore,

our estimator is doubly robust in the sense that our inference theory is valid, i.e. the asymptotic distribution is the same, if either one of the nuisance functions or is misspecified, as in Kennedy

et al. (2017) and Takatsu and

Westling (2023).

This is a stronger result than the usual doubly robustness on the consistency of the estimator.

When one nuisance function is misspecified, we require the other nuisance function to be estimated consistently at a convergence rate faster than , which is the convergence rate of .

In contrast, the DML estimators in the semiparametric model of CCDDHNR converge at a regular root- rate,

so their inference theory does not allow this doubly robust property.

There is a small yet rapidly growing literature on employing the DML approach for non-regular nonparametric infinite-dimesional objects. Hsu et al. (2022) propose a test for monotonicity of . Chernozhukov et al. (2022b), Semenova and Chernozhukov (2020), Fan et al. (2021), and Zimmert and Lechner (2019) study the conditional average binary treatment effect for a low-dimensional subset of . Bonvini and Kennedy (2022) use higher-order influence functions to achieve a faster convergence rate. Despite the advantageous theoretical properties, we note potential drawbacks of the DML approach: Double robustness often requires additional nuisance function estimation, such as the conditional density in the Riesz representer, which could introduce additional variation and implementation complication. Cross-fitting could result in a small effective sample size. For example, the Monte Carlo simulations in Fan et al. (2021) show that cross-fitting does not improve the finite-sample performance for Lasso-type estimation.

Our paper adds to the literature on continuous treatment effects estimation. In low-dimensional settings, see Imbens (2000), Hirano and Imbens (2004), Flores (2007), and Lee (2018) for examples of a class of regression estimators . Galvao and Wang (2015) and Hsu et al. (2020) study a class of inverse probability weighting estimators. The empirical applications in Flores et al. (2012) and Kluve et al. (2012) focus on semiparametric results. We extend this literature to a DML framework that enables ML methods for nonparametric inference in practice.

A main contribution of this paper is a formal inference theory for the fully nonparametric causal effects of continuous variables. To uncover the causal effect of the continuous variable on , our nonparametric nonseparable model can be compared to the partially linear model in Robinson (1988) that specifies the homogenous effect by and hence is a semiparametric problem. The important partially linear model has many applications and is one of the leading examples in the recent ML literature, where the nuisance function can be high-dimensional and estimated by a ML method.555 See Chernozhukov et al. (2018) and references therein. Demirer et al. (2019) and Oprescu et al. (2019) extend to more general functional forms. Cattaneo et al. (2018a), Cattaneo et al. (2018b), Cattaneo et al. (2019), and Farrell et al. (2021a) propose different approaches. Another semiparametric parameter of interest is the weighted average of or over a range of treatment values , such as the average derivative that summarizes certain aggregate effects (Powell et al., 1989) and the bound of the average welfare effect in Chernozhukov et al. (2019). In contrast, our average structural function and the partial effect capture the fully nonparametric heterogenous effects of .

The paper proceeds as follows. Section 2 introduces the framework and estimation procedure. Section 3 presents the asymptotic theory of the DML estimators and low-level conditions for various nuisance function estimators. Section 4 introduces the Simulated DML estimator. Section 5 demonstrates the usefulness of our DML estimator with various ML methods in Monte Carlo simulations and an empirical example on the Job Corps program evaluation. All the proofs are in the Appendix. Additional results, such as uniform inference theory, are in the online supplementary appendix.

2 Setup and estimation

Let be an i.i.d. sample from from a population with a cumulative distribution function (CDF) . Consider a set of treatment values of interest to be an interior of the support of .

Assumption 2.1

(a) (Conditional independence)

and are independent conditional on ;

(b) (Common support)

for some positive constant ;

(c) and are three-times differentiable with respect to with all three derivatives being bounded uniformly over ;

(d) and its derivatives with respect to are bounded uniformly over .

The commonly used identifying Assumption 2.1(a) based on observational data (also known as unconfoundedness, selection on observables, or ignorability) assumes that conditional on observables, the treatment variable is as good as randomly assigned, or conditionally exogenous.

Define the product kernel as , where is the component of and the kernel function satisfies Assumption 2.2. Denote the roughness of as and .

Assumption 2.2 (Kernel)

The second-order symmetric kernel function is bounded differentiable, i.e. , , and . For some finite positive constants , and for some , for .

Assumption 2.2 is standard in nonparametric kernel estimation and holds for commonly used kernel functions, such as Epanechnikov and Gaussian. By Assumptions 2.1-2.2 and the same reasoning for the binary treatment, it is straightforward to show the identification,

| (2.2) | ||||

| (2.3) |

for .666For identification, we only need

for (2.2) and additionally and to be continuous in for (2.3).

Such standard identifying conditions are weaker than Assumption 2.1 used for the inference theory. The expression in equation (2.2) motivates the class of regression-based (or imputation) estimators, while equation (2.3) motivates the class of inverse probability weighting estimators; see Section S2.1 in the online supplementary appendix for further discussion.

Now we introduce the double debiased machine learning estimator.

Estimation procedure:

-

Step 1.

(Cross-fitting) For some fixed , randomly partition the observation indices into distinct groups , , such that the sample size of each group is the largest integer smaller than . For each , the estimators for and for use observations not in and satisfy Assumption 2.3 below.

-

Step 2.

(Double robustness) Define the double debiased ML (DML) estimator as

(2.4) -

Step 3.

(Partial effect) Let and , where is a positive sequence converging to zero as . We estimate the partial effect of the first component of the continuous treatment by .

The number of folds in cross-fitting is not random and typically small, such as five or ten in practice; see, e.g. Section 5.1 or CCDDHNR. When there is no sample splitting (), and use all observations in the full sample. Then the DML estimator in (2.4) is the doubly robust estimator considered in Kallus and Zhou (2018) and Su et al. (2019).

Our inference theory requires the estimators and in Step 1 to satisfy Assumption 2.3 below. We define the partial norm for any as and , where the joint distribution is evaluated at a fixed value of equal to .

Assumption 2.3

There exist functions and that

are three-times differentiable with respect to with all

three derivatives being bounded uniformly over ,

for some positive constant , and satisfy the following:

for each and for any ,

(a) and

,

(b) ;

(c) Either or .

The nuisance function estimators and converge to some fixed functions and respectively in the sense of Assumption 2.3(a)(b). Assumption 2.3(c) allows one of the nuisance functions to be misspecified, or requires at least one of the nuisance function estimators to be consistent. Assumption 2.3(b) and (c) imply that if one nuisance function is misspecified, then the other needs to be estimated consistently at a convergence rate faster than . This is the cost of our doubly robust inference. Specifically, if , then . So Assumption 2.3(b) requires . On the other hand, if , then we require . Kennedy et al. (2017) show such double robustness using a stronger uniform norm for a local linear estimation.

In Section 3.1, we provide sufficient low-level conditions for Assumption 2.3 when the nuisance function estimators are kernel estimators, series, and the deep neural networks in Farrell et al. (2021b). The partial convergence rate also appears in Kennedy et al. (2017), the conditional average treatment effect in Fan et al. (2021), and covariate adjustments in regression discontinuity designs in Noack et al. (2021).

Remark 2.1

Consider the binary treatment effect in CCDDHNR as a heuristic example of a regular parameter that can be estimated at the regular -rate. When , Assumption 2.3 suggests that the corresponding condition on the propensity score estimator would be , which is not feasible. Therefore we conjecture that the inference theory of the DML estimators for the regular estimands in the semiparametric models of CCDDHNR cannot allow for misspecification of the nuisance functions. In contrast, the DML estimator for the non-regular estimand here allows for doubly robust inference. Tan (2020) develops doubly robust inference for the average binary treatment effect by carefully chosen loss functions to estimate the nuisance functions.

Remark 2.2 (Common support)

Assumption 2.1(b) implies that we need to observe sufficient individuals in the population who can find a match sharing the same value of the control variable and receiving the counterfactual value . An analogous assumption in the binary treatment case is that the propensity score is bounded away from zero, e.g. Hirano et al. (2003). Although the common support assumption is standard, we note that it should be made with care in practice and is strong especially with many control variables. For the binary treatment case, Khan and Tamer (2010) study extensively irregular identification and inverse weight estimation, when the propensity score can be close to zero as a small denominator. For the continuous treatment case, the convergence rate of might similarly be affected if the generalized propensity score can be close to zero. We believe that this interesting extension is beyond the scope of the paper and is worthy of a separate research project. See also Su et al. (2019) for a related discussion. Another possible approach to relaxing Assumption 2.1(b) is to define the object of interest by a common support via fixed trimming, e.g. Lee (2018).

Remark 2.3 (Kernel localization)

We discuss the construction of the doubly robust moment function (1.1) by Gateaux derivative and a local Riesz representer; details are in Section S2 in the online supplementary appendix. From the literature on estimating regular parameters, the Gateaux derivative is fundamental to construct estimators with desired properties, such as bias reduction and double robustness in Carone et al. (2018) and Ichimura and Newey (2022). The partial mean is a marginal integration over the conditional distribution of given and the marginal distribution of , fixing the value of at . As a result, the Gateaux derivative and the Riesz representer depend on the choice of the distribution that belongs to a family of distributions approaching a point mass at as . We construct the locally robust estimator based on the influence function derived by the Gateaux derivative, so the asymptotic distribution of depends on the choice of that is the kernel function . Moreover, to construct the DML estimator of a linear functional of that preserves the good properties, the corresponding moment function is simply the linear functional of the moment function of . To our best knowledge, this is the first explicit calculation of Gateaux derivative for such a non-regular nonparametric parameter. Alternatively Kennedy et al. (2017) construct a “pseudo-outcome” that is motivated from the doubly robust and efficient influence function of the regular semiparametric parameter . Then they locally regress the pseudo-outcome on at using a kernel to estimate . Semenova and Chernozhukov (2020) illustrate in an example to estimate by the best linear projection of an “orthogonal signal of the outcome” which is the same “pseudo-outcome” proposed by Kennedy et al. (2017).

A second motivation of the moment function is adding to the influence function of the regression (or imputation) estimator the adjustment term from a kernel-based estimator under the low-dimensional case when the dimension of is fixed. A series estimator yields a different adjustment. These distinct features of continuous treatments are in contrast to the regular binary treatment case, where different nonparametric nuisance function estimators result in the same efficient influence function.

2.1 Conditional density estimation

We propose an estimator for the reciprocal of the generalized propensity score (GPS), i.e. , when . The estimator avoids plugging in a small estimate in the denominator, and the estimate is positive by construction. When , we propose an estimator for the GPS. We can use various nonparametric and ML methods designed for the conditional expectation. We provide a root-mean-square convergence rate. In Section 3.1, we demonstrate these generic GPS estimators using the deep neural networks in Farrell et al. (2021b) and show how Assumption 2.3 can be verified.

The theory of ML methods in estimating the conditional density is less developed compared with estimating the conditional expectation. Alternative estimators for estimating the GPS can be the kernel density estimator, the artificial neural networks in Chen and White (1999), the Lasso methods in Su et al. (2019) and Belloni et al. (2019), or the series cross-validated method in Zhang (2022).

It is known that for any CDF , for . So . Inspired by the idea in Koenker (1994), we estimate by a numerical differentiation estimator, labelled as ReGPS,

| (ReGPS) |

where is a positive sequence vanishing as grows and . By a standard algebra, the conditional CDF , where is the CDF of a standard normal random variable and is a bandwidth sequence vanishing as grows. Let be a generic estimator of the conditional expectation for an outcome variable . Then we estimate by with a transformed outcome variable of , . The conditional -quantile function is estimated by the generalized inverse function . When is continuous in , is strictly increasing. Then the resulting estimator .

Denote the standard root-mean-square norm, or the norm, of a random vector with distribution as for a random variable .

Lemma 2.1 (ReGPS)

Consider an estimator of , denoted as , which is continuous in and satisfies for a sequence of constants . Assume to be three-times differentiable with respect to with all three derivatives being bounded uniformly over . Then the ReGPS estimator satisfies and .

Assumption 2.3 specifies the root-mean-square convergence rate of our conditional density estimator. Thus as long as the root-mean-square convergence rate of a ML method () for the conditional expectation function is available, Assumption 2.3 can be satisfied with a suitable bandwidth and . Then we are able to use such a ML method to estimate the conditional density, as illustrated in Section 3.1.

Note that estimates the conditional quantile function. The ReGPS estimator inverses the CDF estimate and allows to apply various ML methods for conditional expectation functions. Alternatively we can estimate the conditional quantile function directly by a -penalized quantile regression; for example, the conditional density function estimation in Belloni et al. (2019).

When , we propose a direct estimator for the conditional density function by

| (MultiGPS) |

labelled as MultiGPS, where the bandwidth is a positive sequence vanishing as grows, the product kernel . We can choose to be the Gaussian kernel.777A possible drawback of MultiGPS is that the estimate could be negative or small in finite samples. We may adopt the trimming/flooring approaches to addressing this concern in the literature. For example, following Hsu et al. (2020), we can use the estimate for some positive sequence .

Lemma 2.2 (MultiGPS)

Consider an estimator of , denoted as

, which satisfies

for a sequence of constants and .

Let satisfy Assumption 2.2 with in place of and with an unbounded support.

Assume to be three-times differentiable with respect to with all three derivatives being bounded uniformly over .

Then the MultiGPS estimator satisfies

and

for .

Further assume for a sequence of constants . Then and .

3 Asymptotic theory

We present the asymptotically linear representation and asymptotic normality. We provide low-level conditions for estimating the nuisance functions by the deep neural networks in Farrell et al. (2021b) in Section 3.1. Conditions for kernel and series estimators are in Section S3.2 in the online supplementary appendix. Section 3.2 provides sufficient rate conditions using the standard norm.

Let denote the th partial derivative of a generic function with respect to , and .

Theorem 3.1 (Asymptotic normality)

Further let and its derivatives with respect to be bounded uniformly over .

Let .

Then ,

where

and

.

Note that the second part in the influence function888 For our non-regular parameters, we borrow the terminology “influence function” in estimating a regular parameter that is -estimable. An influence function gives the first-order asymptotic effect of a single observation on the estimator. The estimator is asymptotically equivalent to a sample average of the influence function. See Hampel (1974) and Ichimura and Newey (2022), for example. in (3.5) and hence does not contribute to the first-order asymptotic variance . We keep these smaller-order terms to show that the nuisance function estimators have no first-order influence on the asymptotic distribution of . This is in contrast to the binary treatment case where is replaced by in , so converges at a root- rate. Then the second part in (3.5) is of first-order for a binary treatment, resulting in the well-studied efficient influence function in estimating the binary treatment effect in Hahn (1998).

Theorem 3.1 is fundamental for inference, such as constructing confidence intervals and the optimal bandwidth that minimizes the asymptotic mean squared error. We propose an estimator for the leading bias , inspired by the idea in Powell and Stoker (1996). Let the notation be explicit on the bandwidth and

with a pre-specified fixed scaling parameter . Theorem 3.2 below shows the consistency of under Assumption 3.4(d).

We can estimate the asymptotic variance by the sample variance of the estimated influence function , where . Then we propose a data-driven bandwidth to consistently estimate the optimal bandwidth that minimizes the asymptotic mean squared error (AMSE) given in Theorem 3.2.

Assumption 3.4

For each and for any , (a) , (b) , , and ; (c) and its derivatives with respect to are bounded uniformly over and ; (d) and . for .

Theorem 3.2 (AMSE optimal bandwidth for )

Assumption 3.4(a)-(c) are for the consistency of . The condition (a) strengthens Assumption 2.3(a), and (b) is mild boundedness conditions that are implied when and are bounded uniformly. In practice, we may use different Step 1 estimators in and due to different high-level conditions.

A common approach is to choose an undersmoothing bandwidth smaller than such that the bias is first-order asymptotically negligible, i.e. . Then we can construct the usual point-wise confidence interval , where is the CDF of . Alternatively, we may consider a further bias correction to allow for a wider range of bandwidth choice so that we may implement in practice. Specifically we may use the above bias estimator and account for its variation in the asymptotic theory of the bias-corrected estimator . Calonico et al. (2018) show that the AMSE optimal bandwidth of the original estimator is feasible in different contexts. Takatsu and Westling (2023) develop such robust bias-corrected inference for the local linear estimator in Kennedy et al. (2017).

Next we present the asymptotic theory for .

Theorem 3.3 (Partial effect)

The conditions (a) and (b) in Theorem 3.3 strengthen Assumption 2.3 for and imply that cannot be too small and depends on the precision of the nuisance function estimators. The bias is due to misspecifying one of the nuisance functions and is zero when both nuisance functions are correctly specified or estimated by nonparametric methods.

We propose a data-driven bandwidth to consistently estimate the optimal bandwidth that minimizes the AMSE given in Theorem 3.4. Following the same procedure for , let and . In practice, we may choose , where , such that the conditions in Theorem 3.3 are satisfied.

Theorem 3.4 (AMSE optimal bandwidth for )

3.1 Nuisance function estimators

We show that the high-level conditions on the convergence rates in Assumption 2.3 are attainable by the nonparametric and ML methods: kernel, series, and the deep neural networks in Farrell et al. (2021b), where the dimension of the control variables is fixed. Lasso methods have been extensively studied in Su et al. (2019), Sasaki and Ura (2021), and Sasaki et al. (2021), where can grow with . These ML methods require different low-level conditions, such as dimensionality, smoothness, and tuning parameters.

Consider the conditional density estimator MultiGPS given in Section 2.1 for example. By Lemma 2.2, Assumption 2.3(b) requires

Therefore, we need to obtain the partial convergence rate and the standard convergence rate .

We seek theoretical results, such as the above rate conditions, for insights on selection of the tuning parameters in practice that is challenging and under-developed in the ML literature. We may use the optimal choices for the nuisance function estimators, as they do not affect the first-order asymptotics. A common method is cross-validation. We may choose the optimal rates for the bandwidths for and that respectively minimize and , which might be available in the literature. Similarly we can derive the optimal .

Next we propose a deep MLP-ReLU network kernel estimator for (labelled as Kernel NN) and derive its convergence rate. We illustrate the low-level conditions of conventional kernel and series estimators in Section S3 in the online supplementary appendix, as the calculations are rather standard. These results on the convergence rates for neural networks and series are new and non-trivial extensions of existing results in the literature.

We consider the deep neural networks in Farrell et al. (2021b) (FLM, hereafter) that use the fully connected feedforward neural networks (multilayer perceptron, or MLP) and the nonsmooth rectified linear units (ReLU) activation function. We propose a deep MLP-ReLU network kernel estimator for . The proposed estimator serves the purpose to conveniently apply the convergence rate given in FLM to obtain the convergence rate. So we can deliver valid asymptotic inference for and following deep learning. In this section, we closely follow the notations in FLM for easy reference, by slightly abusing our notations.

We consider a kernel-weighted loss function for any ,

where a product kernel with a kernel function and a positive sequence of bandwidth vanishing as grows. We define the deep MLP-ReLU network kernel estimator for any as

| (3.7) |

where is the MLP class, is an absolute constant, and depending on collects the weights and constants over all nodes. We refer the details of the MLP-ReLU network estimators to FLM. Then we obtain .

Denote the derivative of a function as , where and .

Assumption 3.5 (DNN)

(a) For any , the second derivatives of and with respect to are bounded and continuous uniformly over ; (b) are continuously distributed with support for fixed ,999To simplify exposition, is assumed to be continuous, but discrete variables with a fixed number of supporting points are allowed. Theorem 1 in Farrell et al. (2021a) find that the rate only depends on the dimension of the continuously distributed components. and for an absolute constant , ; (c) For and some finite positive constant , ; (d) for some finite positive constant .

Assumption 9(a) is due to the kernel weight in the loss function. Assumption 9(b)-(d) collect assumptions for applying Theorem 1 in FLM. Detailed discussion on these assumptions is referred to FLM. As discussed in FLM, it is standard in nonparametric analysis to assume the true function to be estimated is bounded. The choice of may be arbitrarily large and is simply a formalization of the requirement that the optimizer is not allowed to diverge on the function level in the sup-norm sense. For practical implementation, we do not impose such bound. But there is a practice for rescaling the output variable which is generally dependent on the activation function being used, e.g. the domain of the activation function. A common practice for variable transformation is standardization (subtracting mean and dividing by standard deviation) or scaling to a specific range by an affine transformation (generally chosen between 0 and 1).

Theorem 3.5 (DNN)

Let be the deep MLP-ReLU network kernel estimator defined by (3.7). Let Assumption 9 hold. Let satisfy Assumption 2.2 with in place of and with a bounded support. Let width and depth . Then for any , with probability approaching one as , for a constant independent of , which may depend on , , and other fixed constants.

We can apply deep neural networks to the GPS estimation proposed in Section 2.1. The ReGPS estimator can use the MLP estimator in FLM with the unweighted loss function:

| (3.8) |

The MultiGPS estimator can use :

| (3.9) |

Lemma 3.3 (Theorem 1 in FLM)

Let be continuously distributed with support for fixed . Let width and depth . Let .

-

(a)

For defined by (3.8), assume (A) for some finite positive constant . Let . Then .

- (b)

We are ready to show that Assumption 2.3 is attainable by the MLP-ReLU network estimators.

Take the MultiGPS estimator in (3.9) for example, with for simplicity.

Assumption 2.3(b) is

by Theorem 3.5, Lemmas 2.2 and 3.3.

Assumption 2.3(a) is implied by and .

When , Assumption 2.3(a) holds by letting , and (ii) holds by letting smoothness .

FLM discuss the same condition for the average treatment effect of a binary treatment variable.

Similarly we note that this condition is not minimal but is sufficient to justify the practical use of the MLP-ReLU network estimators for valid inference on the average structural function and the partial effect of continuous treatments by our approach.

3.2 Standard norm rate

We provide sufficient rate conditions using the standard norm in Assumption 3.6 to replace the partial norm in Assumption 2.3. Let the norm be . We do not need to modify the rate condition on , as it equivalently uses the standard norm for a given . The cost of the more commonly used norm is losing the doubly robust inference and stricter regularity conditions.

Assumption 3.6

There exists a function that is three-times differentiable with respect to with all three derivatives being bounded uniformly over , for some positive constant , and satisfies the following: for each and for any , (a) and ; (b) ; (c) . (d) is twice differentiable with respective to with two derivatives being bounded uniformly over .

Corollary 3.1

Note that the rate condition Assumption 3.6(b) is the same rate condition for the regular semiparametric models in CCDDHNR and Chernozhukov et al. (2022a), e.g. is replaced with the propensity score for a discrete treatment. We discuss the cost and implications of Assumption 3.6 based on the standard norm. First under Assumption 3.6, the inference theory cannot allow to be misspecified, while can be misspecified. Second, the convergence rates are faster than those required in Assumption 2.3. To learn intuition on the rate condition (a), we utilize the bounded kernel in the DML estimator, resulting in a penalty in the loose bound . Third, the bandwidth choice is more restrictive. Assumption 3.6(c) implies undersmoothing, i.e. the leading bias of is first-order ignorable by .

For a specific example, consider to be FLM’s estimator for the conditional expectation function , i.e. using the unweighted loss function . FLM provide the corresponding convergence rate with the smoothness defined in Assumption 9(c). We need that is stronger than , as discussed in Section 3.1. Moreover comparing the rate conditions in Assumption 2.3(b) and Assumption 3.6(b) for , we can show that using the partial norm results in a tighter bound by with , and .

4 Simulated DML estimator

We introduce Simulated DML estimator that enables the high-level rate conditions based on the standard norm, rather than the partial norm, and also permits the doubly robust inference. Following the estimation procedure given in Section 2, Step 1 computes the nuisance function estimators and . In Step 2, let where are i.i.d. draws from with replacement, for , , and is a positive sequence converging to zero as . The Simulated DML (SDML) estimator is defined as

The corresponding partial effect estimator as in Step 3.

To get intuition, the SDML estimator uses rather than as in that fixes the treatment value at the target . The simulated localizes the realized treatment values around . Introducing such local variation enables the standard rate of . Specifically defined above follows the empirical distribution function of , denoted as . Therefore follows a CDF conditional on the sample , .

Assumption 4.7 gives the high-level conditions on the nuisance function estimators.

Assumption 4.7

There exist functions and that are three-times differentiable with respect to with all three derivatives being bounded uniformly over such that for each and for , (a) and ; (b) ; (c) ; (d) Either or .

Theorem 4.6 (SDML-Asymptotic normality)

Assumption 4.7(a) strengthens the consistency condition in Assumption 2.3(a) with a penalty . Interestingly when , the rate condition (b) , which is the same rate condition for the regular semiparametric models in CCDDHNR and Chernozhukov et al. (2022a). Assumption 4.7(c) is a boundedness condition that is implied if is uniformly bounded; for example, deep neural networks in FLM for a uniformly bounded . Specifically, FLM provide the corresponding convergence rate and illustrate its usefulness for semiparametric inference on the average treatment effect of a binary treatment. We could use this rate to verify the high-level conditions in Assumption 4.7 for the SDML estimator or Assumption 3.6 for the DML estimator as discussed in Section 3.2.

We can estimate the AMSE optimal bandwidth given in Theorem 3.2 by the SDML approach. We can estimate the leading bias by with a pre-specified positive scaling parameter . We can estimate the asymptotic variance by , where . Then a data-driven bandwidth . Theorem 4.7 below shows the consistency of , , and , under Assumption 4.8 that is modified from Assumption 3.4.

Assumption 4.8

For each and for any , (a) , (b) , , and ; (c) is bounded uniformly over ; (d) and .

Theorem 4.7 (SDML-AMSE optimal bandwidth)

We can similarly obatin the asymptotic theory for .

5 Numerical examples

This section provides numerical examples of Monte Carlo simulations and an empirical illustration. The estimation procedure of the proposed DML estimator is described in Section 2. To estimate the first-step conditional expectation function and the conditional density by MultiGPS as described in Section 2.1, we employ three methods: Lasso, the deep neural networks (NN) based on Farrell et al. (2021b), and the Kernel NN proposed in Section 3.1. We implement our DML estimator with these algorithms respectively. Note that Lasso assumes certain sparsity specifications and NN is a nonparametric method. Our doubly robust inference theory allows one of the first-step functions to be misspecified. Software we develop is available at https://github.com/KColangelo/Double-ML-Continuous-Treatment. Section S1 in the online supplementary appendix provides the implementation details and additional results of ReGPS.

5.1 Simulation study

We consider the data-generating process: , ,

where , , the -entry for and for for , and is the CDF of . Thus this is a nonseparable model and the potential outcome . The parameters of interest are the average dose response function and the partial effect at , i.e. and .

We compare estimations with cross-fitting and without cross-fitting, and with a range of bandwidths to demonstrate robustness to bandwidth choice. We consider sample size and the number of subsamples used for cross-fitting . We use the second-order Epanechnikov kernel with bandwidth . For the MultiGPS estimator described in Section 2.1, we choose bandwidth . Let the bandwidth for a constant and the standard deviation of . We computed the AMSE-optimal bandwidth given in Theorem 3.2 that has the corresponding . Thus using some undersmoothing bandwidth with , the 95% confidence interval is asymptotically valid, where the standard error () is computed using the sample analogue of the estimated influence function, as described in Section 3.

Table 1 reports the results based on 1,000 Monte Carlo replications. Under no cross-fitting (), the confidence intervals generally have lower coverage rates and the bias is larger than under cross-fitting. The estimators using NN and Kernel NN perform well in the case of fivefold cross-fitting, with coverage rates (Cov.) near the nominal 95%, especially in a smaller sample size . Intuitively Kernel NN estimates the conditional expectation function locally at , resulting in a smaller effective sample size than the full sample size used by NN. Therefore NN may outperform Kernel NN in small samples. The coverage rate and bias are improved the most for NN and Kernel NN with cross-fitting, but only marginally for Lasso. Cross-fitting should improve our estimation in the case that the machine learning algorithm is over-fitting. Given that cross-fitting does not improve Lasso, it might suggest that Lasso does not have a severe over-fitting problem for this data-generating process.

These methods seem robust to bandwidth choice under cross-fitting. Overall these results demonstrate consistency with the theoretical results of this paper, confirming the usefulness of cross-fitting for ML methods.

| Lasso | Neural Network | Kernel Neural Network | ||||||||

| L | c | Bias | RMSE | Cov. | Bias | RMSE | Cov. | Bias | RMSE | Cov. |

| 1 | 0.75 | 0.003 | 0.110 | 0.936 | 0.063 | 0.113 | 0.887 | 0.036 | 0.124 | 0.597 |

| 1.00 | 0.008 | 0.100 | 0.935 | 0.064 | 0.108 | 0.890 | 0.037 | 0.111 | 0.689 | |

| 1.25 | 0.016 | 0.094 | 0.937 | 0.067 | 0.109 | 0.859 | 0.044 | 0.105 | 0.748 | |

| 1.50 | 0.025 | 0.091 | 0.925 | 0.077 | 0.112 | 0.840 | 0.051 | 0.103 | 0.778 | |

| 5 | 0.75 | 0.001 | 0.111 | 0.936 | -0.025 | 0.143 | 0.946 | 0.003 | 0.146 | 0.959 |

| 1.00 | 0.008 | 0.100 | 0.936 | -0.014 | 0.122 | 0.947 | 0.009 | 0.122 | 0.965 | |

| 1.25 | 0.016 | 0.094 | 0.936 | -0.007 | 0.109 | 0.967 | 0.018 | 0.108 | 0.968 | |

| 1.50 | 0.025 | 0.092 | 0.925 | 0.002 | 0.100 | 0.969 | 0.029 | 0.102 | 0.956 | |

| 1 | 0.75 | 0.003 | 0.040 | 0.955 | 0.002 | 0.035 | 0.961 | 0.004 | 0.042 | 0.851 |

| 1.00 | 0.005 | 0.036 | 0.956 | 0.005 | 0.032 | 0.957 | 0.006 | 0.037 | 0.885 | |

| 1.25 | 0.008 | 0.034 | 0.954 | 0.009 | 0.032 | 0.937 | 0.010 | 0.035 | 0.895 | |

| 1.50 | 0.012 | 0.033 | 0.944 | 0.014 | 0.032 | 0.918 | 0.014 | 0.034 | 0.899 | |

| 5 | 0.75 | 0.001 | 0.060 | 0.949 | 0.012 | 0.044 | 0.956 | 0.002 | 0.044 | 0.948 |

| 1.00 | 0.005 | 0.036 | 0.953 | 0.014 | 0.039 | 0.948 | 0.006 | 0.039 | 0.950 | |

| 1.25 | 0.008 | 0.034 | 0.952 | 0.018 | 0.039 | 0.916 | 0.009 | 0.036 | 0.948 | |

| 1.50 | 0.012 | 0.033 | 0.944 | 0.023 | 0.039 | 0.899 | 0.014 | 0.035 | 0.945 | |

| 1 | 0.75 | 0.107 | 0.888 | 0.978 | 0.072 | 0.717 | 0.979 | 0.276 | 1.448 | 0.512 |

| 1.00 | 0.092 | 0.588 | 0.978 | 0.077 | 0.503 | 0.981 | 0.206 | 0.943 | 0.620 | |

| 1.25 | 0.087 | 0.436 | 0.980 | 0.114 | 0.398 | 0.985 | 0.176 | 0.655 | 0.714 | |

| 1.50 | 0.088 | 0.338 | 0.979 | 0.083 | 0.312 | 0.986 | 0.140 | 0.499 | 0.784 | |

| 5 | 0.75 | 0.098 | 0.892 | 0.977 | 0.054 | 0.869 | 0.997 | 0.327 | 1.792 | 0.908 |

| 1.00 | 0.084 | 0.588 | 0.980 | 0.084 | 0.568 | 0.997 | 0.242 | 1.131 | 0.902 | |

| 1.25 | 0.077 | 0.434 | 0.979 | 0.088 | 0.426 | 0.993 | 0.206 | 0.836 | 0.897 | |

| 1.50 | 0.077 | 0.335 | 0.982 | 0.061 | 0.336 | 0.996 | 0.177 | 0.616 | 0.920 | |

| 1 | 0.75 | -0.008 | 0.527 | 0.976 | 0.018 | 0.534 | 0.957 | 0.099 | 0.664 | 0.822 |

| 1.00 | 0.005 | 0.351 | 0.985 | 0.021 | 0.348 | 0.969 | 0.105 | 0.429 | 0.880 | |

| 1.25 | 0.006 | 0.254 | 0.979 | 0.016 | 0.241 | 0.980 | 0.086 | 0.295 | 0.917 | |

| 1.50 | 0.000 | 0.200 | 0.977 | 0.017 | 0.187 | 0.983 | 0.078 | 0.230 | 0.931 | |

| 5 | 0.75 | -0.008 | 0.548 | 0.976 | 0.003 | 0.575 | 0.978 | 0.099 | 0.757 | 0.931 |

| 1.00 | 0.001 | 0.353 | 0.983 | 0.012 | 0.352 | 0.984 | 0.108 | 0.460 | 0.945 | |

| 1.25 | 0.004 | 0.254 | 0.981 | 0.007 | 0.245 | 0.989 | 0.095 | 0.319 | 0.946 | |

| 1.50 | -0.002 | 0.200 | 0.980 | 0.009 | 0.188 | 0.990 | 0.082 | 0.242 | 0.954 | |

Note: The top panel shows the results for and the bottom panel is for . : no cross-fitting. : fivefold cross-fitting. The bandwidth is , and for the AMSE-optimal bandwidth for . The nominal coverage rate (Cov.) of the confidence interval is 0.95.

5.2 Empirical illustration

We illustrate our method by re-analyzing the Job Corps program in the United States, which was conducted in the mid-1990s. The Job Corps program is the largest publicly funded job training program, which targets disadvantaged youth. The participants are exposed to different numbers of actual hours of academic and vocational training. The participants’ labor market outcomes may differ if they accumulate different amounts of human capital acquired through different lengths of exposure. We estimate the average dose response functions to investigate the relationship between employment and the length of exposure to academic and vocational training. As our analysis builds on Flores et al. (2012), Hsu et al. (2020), and Lee (2018), we refer the readers to the reference therein for further details of Job Corps.

We use the same dataset in Hsu

et al. (2020).

We consider the outcome variable () to be the proportion of weeks employed in the second year following the program assignment.

The continuous treatment variable () is the total hours spent in academic and vocational training in the first year.

We follow the literature to assume the conditional independence Assumption 2.1(a), meaning that selection into different levels of the treatment is random, conditional on a rich set of observed covariates, denoted by .

The identifying Assumption 2.1 is indirectly assessed in Flores et al. (2012).

Our sample consists of 4,024 individuals who completed at least 40 hours (one week) of academic and vocational training.

There are 40 covariates measured at the baseline survey.

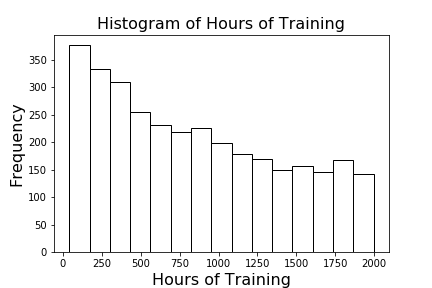

In the online supplementary appendix, Figure S1 shows the distribution of by a histogram, and Table S2 provides brief descriptive statistics.

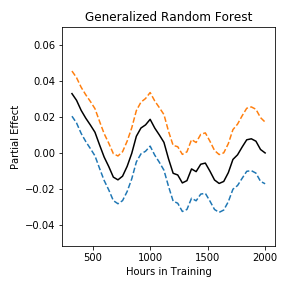

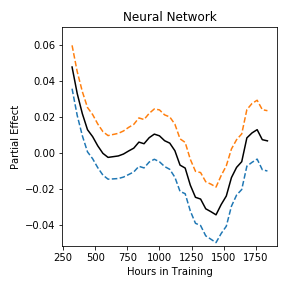

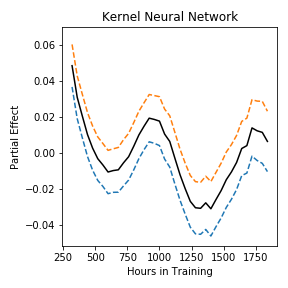

Implementation details: We estimate the average dose response function and partial effect by the proposed DML estimator with fivefold cross-fitting.

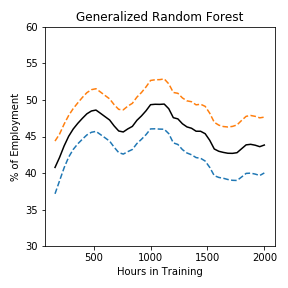

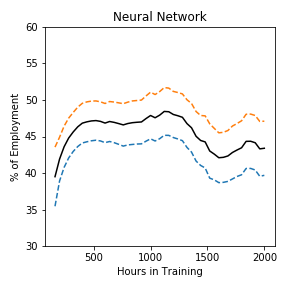

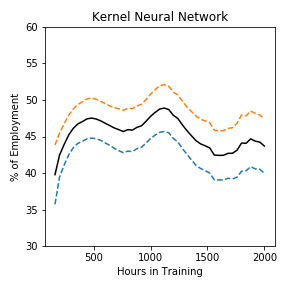

We implement three DML estimators: Lasso, the generalized random forests in Athey

et al. (2019), the neural networks (NN) based on Farrell

et al. (2021b),

and the Kernel NN proposed in Section 3.1. The parameters for these methods are selected as described in Section S1 in the online supplementary appendix.

We use the second-order Epanechnikov kernel with bandwidth . For the MultiGPS estimator, we use the Gaussian kernel with bandwidth . We compute the optimal bandwidth that minimizes an asymptotic integrated MSE. For practical implementation, consider a weight function that is the density of on a subset of the support of . The bandwidth that minimizes the asymptotic integrated MSE for an integrable weight function is , where and , following Theorem 3.2. Set equally spaced grid points over : . Following the approach given in Section 3, we estimate with and with and , for . A plug-in estimator , where and . We use and in this empirical application. We then obtain under-smoothing bandwidths that are 213.45 for Lasso, 224.36 for the generalized random forest, 223 for NN, and 225.11 for Kernel NN.

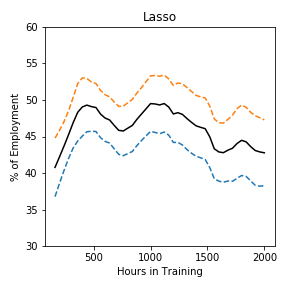

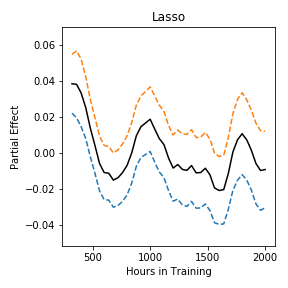

Results: Figure 1 presents the estimated average dose response function along with 95% point-wise confidence intervals. The results for the three ML nuisance function estimators have similar patterns. The estimates suggest an inverted-U relationship between the employment and the length of participation. DNN estimates appear to be the most erratic, possibly due to the smaller bandwidth compared with other estimators.

Figure 2 reports the partial effect estimates with step size (one month). Across all procedures, we see positive partial effects when hours of training are less than around 500 (three months) and negative partial effect around 1,500 hours (9 months). Taking the estimates by NN for example, with standard error and with computed based on the result of Theorem 3.3. This estimate implies that increasing the training from two months to three months increases the average proportion of weeks employed in the second year by (nearly two weeks) with .

Lee (2009) finds that the program had a negative impact on employment propensities in the short term (104 weeks since random assignments) and a positive effect in the long term (104-208 weeks). Lee (2009) considers a binary treatment variable of being in the program or not, with the outcome variable in our notations. We focus on the employment proportion in the second year following the program assignment (52-104 weeks) and estimate the heterogenous effects of the total hours spent in academic and vocational training in the first year.

The empirical practice has focused on semiparametric estimation; see Flores et al. (2012), Hsu et al. (2020), Lee (2018), for example. The semiparametric methods are subject to the risk of misspecification. Our DML estimator provides a feasible approach to implementing a fully nonparametric inference in practice.

6 Conclusion and outlook

For a future extension, our DML estimator serves as the preliminary element for policy learning and optimization with a continuous decision, following Manski (2004), Hirano and Porter (2009), Kitagawa and Tetenov (2018), Kallus and Zhou (2018), Demirer et al. (2019), Athey and Wager (2019), Farrell et al. (2021b), among others.

Another extension is robustness against multiway clustering, where the conventional cross-fitting does not ensure the independence between observations in from . We may adopt the -fold multiway cross-fitting proposed by Chiang et al. (2021) that focus on regular DML estimators as in CCDDHNR. Since the form of estimators and the proofs of asymptotic theories for our continuous treatment case are similar to those studied in Chiang et al. (2021), we expect that their proposed algorithm works for ; a formal extension is out of the scope of this paper.

When unconfoundedness is violated, we can use the control function approach in triangular simultaneous equations models by including in the covariates some estimated control variables using instrumental variables. For example, Lee (2009) studies the issue of sample selection for the wage effects of the Job Corps program. To extend our empirical application to the wage effect of the length of exposure to the program, we may follow Lee (2009) to estimate bounds on the wage effect of the continuous treatment using the excess number of individuals who are induced to be selected. A closer approach to our estimator is Das et al. (2003), who show that a nonparametric control function method accounts for both selection and endogeneity. Imbens and Newey (2009) show that the conditional independence assumption holds when the covariates include the additional control variable , the conditional distribution function of the endogenous variable given the instrumental variables . The influence function that accounts for estimating the control variables as generated regressors has derived in Corollary 2 in Lee (2015). Lee (2015) shows that the adjustment terms for the estimated control variables are of smaller order in the influence function of the final estimator, but it may be important to include them to achieve local robustness. This is a distinct feature of the average structural function of continuous treatments, as discussed in Section 3. Using such an influence function to construct the corresponding DML estimator is left for future research.

Acknowledgements

This work is not related to Kyle Colangolo’s position at Amazon, and was completed outside of the regular duties of the position. We are grateful to Max Farrell, Whitney Newey, Takuya Ura, Ted Westling, and Yichong Zhang for valuable discussion. We thank Parush Arora for assistance.

References

- Aitchison and Aitken (1976) Aitchison, J. and C. G. G. Aitken (1976). Multivariate binary discrimination by the kernel method. Biometrika 63, 413–420.

- Athey et al. (2018) Athey, S., G. W. Imbens, and S. Wager (2018). Approximate residual balancing: De-biased inference of average treatment effects in high dimensions. Journal of the Royal Statistical Society Statistical Methodology Series B 80(4).

- Athey et al. (2019) Athey, S., J. Tibshirani, and S. Wager (2019). Generalized random forests. Annals of Statistics 47(2), 1148–1178.

- Athey and Wager (2019) Athey, S. and S. Wager (2019). Efficient policy learning. arxiv:1702.02896.

- Belloni et al. (2017) Belloni, A., V. Chernozhukov, I. Fernández-Val, and C. Hansen (2017). Program evaluation and causal inference with high-dimensional data. Econometrica 85(1), 233–298.

- Belloni et al. (2014) Belloni, A., V. Chernozhukov, and C. Hansen (2014). Inference on Treatment Effects after Selection among High-Dimensional Controls. The Review of Economic Studies 81(2), 608–650.

- Belloni et al. (2019) Belloni, A., V. Chernozhukov, and K. Kato (2019). Valid post-selection inference in high-dimensional approximately sparse quantile regression models. Journal of the American Statistical Association 114(526), 749–758.

- Bickel et al. (2009) Bickel, P. J., Y. Ritov, and A. B. Tsybakov (2009). Simultaneous analysis of Lasso and Dantzig selector. Annals of Statistics 37(4), 1705–1732.

- Blundell and Powell (2003) Blundell, R. and J. L. Powell (2003). Endogeneity in nonparametric and semiparametric regression models. In L. H. M. Dewatripont and S.J.Turnovsky (Eds.), Advances in Economics and Econometrics, Theory and Applications, Eighth World Congress, Volume II. Cambridge University Press, Cambridge, U.K.

- Bonvini and Kennedy (2022) Bonvini, M. and E. H. Kennedy (2022). Fast convergence rates for dose-response estimation. arxiv:2207.11825.

- Bravo et al. (2020) Bravo, F., J. Escanciano, and I. van Keilegom (2020). Two-step semiparametric likelihood inference. Annals of Statistics 48, 1–26.

- Calonico et al. (2018) Calonico, S., M. D. Cattaneo, and M. H. Farrell (2018). On the effect of bias estimation on coverage accuracy in nonparametric inference. Journal of the American Statistical Association 113(522), 767–779.

- Carone et al. (2018) Carone, M., A. R. Luedtke, and M. J. van der Laan (2018). Toward computerized efficient estimation in infinite-dimensional models. Journal of the American Statistical Association 0(0), 1–17.

- Cattaneo (2010) Cattaneo, M. D. (2010). Efficient semiparametric estimation of multi-valued treatment effects under ignorability. Journal of Econometrics 155(2), 138–154.

- Cattaneo et al. (2020) Cattaneo, M. D., M. H. Farrell, and Y. Feng (2020). Large sample properties of partitioning-based series estimators. Annals of Statistics 48(3), 1718–1741.

- Cattaneo and Jansson (2019) Cattaneo, M. D. and M. Jansson (2019). Average density estimators: Efficiency and bootstrap consistency. arxiv:1904.09372v1.

- Cattaneo et al. (2019) Cattaneo, M. D., M. Jansson, and X. Ma (2019). Two-step estimation and inference with possibly many included covariates. Review of Economic Studies 86(3), 1095–1122.

- Cattaneo et al. (2018a) Cattaneo, M. D., M. Jansson, and W. Newey (2018a). Alternative asymptotics and the partially linear model with many regressors. Econometric Theory 34(2), 277–301.

- Cattaneo et al. (2018b) Cattaneo, M. D., M. Jansson, and W. Newey (2018b). Inference in linear regression models with many covariates and heteroscedasticity. Journal of the American Statistical Association 113(523), 1350–1361.

- Chen (2007) Chen, X. (2007). Chapter 76 Large sample sieve estimation of semi-nonparametric models. Volume 6 of Handbook of Econometrics, pp. 5549–5632. Elsevier.

- Chen et al. (2014) Chen, X., Z. Liao, and Y. Sun (2014). Sieve inference on possibly misspecified semi-nonparametric time series models. Journal of Econometrics 178, 639–658.

- Chen and Pouzo (2015) Chen, X. and D. Pouzo (2015). Sieve wald and QLR inferences on semi/nonparametric conditional moment models. Econometrica 83(3), 1013–1079.

- Chen and White (1999) Chen, X. and H. White (1999). Improved rates and asymptotic normality for nonparametric neural network estimators. IEEE Transactions on Information Theory 45.

- Chernozhukov et al. (2018) Chernozhukov, V., D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey, and J. Robins (2018). Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal 21(1), C1–C68.

- Chernozhukov et al. (2014a) Chernozhukov, V., D. Chetverikov, and K. Kato (2014a). Anti-concentration and honest, adaptive confidence bands. Annals of Statistics 42(5), 1787–1818.

- Chernozhukov et al. (2014b) Chernozhukov, V., D. Chetverikov, and K. Kato (2014b). Gaussian approximation of suprema of empirical processes. Annals of Statistics 42(4), 1564–1597.

- Chernozhukov et al. (2022) Chernozhukov, V., J. C. Escanciano, H. Ichimura, W. K. Newey, and J. M. Robins (2022). Locally robust semiparametric estimation. Econometrica 90(4), 1501–1535.

- Chernozhukov et al. (2019) Chernozhukov, V., J. A. Hausman, and W. K. Newey (2019). Demand analysis with many prices. cemmap Working Paper, CWP59/19.

- Chernozhukov et al. (2022a) Chernozhukov, V., W. Newey, and R. Singh (2022a). Automatic debiased machine learning of causal and structural effects. Econometrica 90(3), 967–1027.

- Chernozhukov et al. (2022b) Chernozhukov, V., W. Newey, and R. Singh (2022b). Debiased machine learning of global and local parameters using regularized Riesz representers. Econometrics Journal, forthcoming.

- Chiang et al. (2021) Chiang, H. D., K. Kato, Y. Ma, and Y. Sasaki (2021). Multiway cluster robust double/debiased machine learning. Journal of Business & Economic Statistics 0(0), 1–11.

- Das et al. (2003) Das, M., W. K. Newey, and F. Vella (2003). Nonparametric estimation of sample selection models. Review of Economic Studies 70(1), 33–58.

- Demirer et al. (2019) Demirer, M., V. Syrgkanis, G. Lewis, and V. Chernozhukov (2019). Semi-parametric efficient policy learning with continuous actions. arxiv:1905.10116v1.

- Fan et al. (2021) Fan, Q., Y.-C. Hsu, R. P. Lieli, and Y. Zhang (2021). Estimation of conditional average treatment effects with high-dimensional data. Journal of Business & Economic Statistics, forthcoming.

- Farrell (2015) Farrell, M. H. (2015). Robust inference on average treatment effects with possibly more covariates than observations. Journal of Econometrics 189(1), 1–23.

- Farrell et al. (2021a) Farrell, M. H., T. Liang, and S. Misra (2021a). Deep learning for individual heterogeneity: An automatic inference framework. arxiv:2010.14694.

- Farrell et al. (2021b) Farrell, M. H., T. Liang, and S. Misra (2021b). Deep neural networks for estimation and inference. Econometrica 89(1), 181–213.

- Flores (2007) Flores, C. A. (2007). Estimation of dose-response functions and optimal doses with a continuous treatment. Working paper.

- Flores et al. (2012) Flores, C. A., A. Flores-Lagunes, A. Gonzalez, and T. C. Neumann (2012). Estimating the effects of length of exposure to instruction in a training program: The case of job corps. The Review of Economics and Statistics 94(1), 153–171.

- Fong et al. (2018) Fong, C., C. Hazlett, and K. Imai (2018). Covariate balancing propensity score for a continuous treatment: Application to the efficacy of political advertisements. The Annals of Applied Statistics 12(1), 156–177.

- Galvao and Wang (2015) Galvao, A. F. and L. Wang (2015). Uniformly semiparametric efficient estimation of treatment effects with a continuous treatment. Journal of the American Statistical Association 110(512), 1528–1542.

- Hahn (1998) Hahn, J. (1998). On the role of the propensity score in efficient semiparametric estimation of average treatment effects. Econometrica 66(2), 315–332.

- Hampel (1974) Hampel, F. R. (1974). The influence curve and its role in robust estimation. Journal of the American Statistical Association 69, 383–393.

- Hansen (2022) Hansen, B. E. (2022). Econometrics. Princeton University Press.

- Hirano and Imbens (2004) Hirano, K. and G. W. Imbens (2004). The propensity score with continuous treatments. In A. Gelman and X.-L. Meng (Eds.), Applied Bayesian Modeling and Causal Inference from Incomplete-Data Perspectives, pp. 73–84. New York: Wiley.

- Hirano et al. (2003) Hirano, K., G. W. Imbens, and G. Ridder (2003). Efficient estimation of average treatment effects using the estimated propensity score. Econometrica 71(4), 1161–1189.

- Hirano and Porter (2009) Hirano, K. and J. Porter (2009). Asymptotics for statistical treatment rules. Econometrica 77, 1683–1701.

- Hsu et al. (2020) Hsu, Y.-C., M. Huber, Y.-Y. Lee, and L. Lettry (2020). Direct and indirect effects of continuous treatments based on generalized propensity score weighting. Journal of Applied Econometrics 35(7), 814–840.

- Hsu et al. (2022) Hsu, Y.-C., M. Huber, Y.-Y. Lee, and C.-A. Liu (2022). Testing monotonicity of mean potential outcomes in a continuous treatment with high-dimensional data. arxiv:2106.04237.

- Hsu et al. (2020) Hsu, Y.-C., T.-C. Lai, and R. P. Lieli (2020). Estimation and inference for distribution and quantile functions in endogenous treatment effect models. Econometric Reviews 0(0), 1–38.

- Ichimura and Newey (2022) Ichimura, H. and W. K. Newey (2022). The influence function of semiparametric estimators. Quantitative Economics 13(1), 29–61.

- Imbens (2000) Imbens, G. (2000). The role of the propensity score in estimating dose-response functions. Biometrika 87(3), 706–710.

- Imbens and Newey (2009) Imbens, G. W. and W. K. Newey (2009). Identification and estimation of triangular simultaneous equations models without additivity. Econometrica 77(5), 1481–1512.

- Kallus and Zhou (2018) Kallus, N. and A. Zhou (2018). Policy evaluation and optimization with continuous treatments. Proceedings of the 21st International Conference on Artificial Intelligence and Statistics (AISTATS) 84, 1243–1251.

- Kennedy et al. (2017) Kennedy, E. H., Z. Ma, M. D. McHugh, and D. S. Small (2017). Nonparametric methods for doubly robust estimation of continuous treatment effects. Journal of the Royal Statistical Society: Series B 79(4), 1229–1245.

- Khan and Tamer (2010) Khan, S. and E. Tamer (2010). Irregular identification, support conditions, and inverse weight estimation. Econometrica 78(6), 2021–2042.

- Kitagawa and Tetenov (2018) Kitagawa, T. and A. Tetenov (2018). Who should be treated? empirical welfare maximization methods for treatment choice. Econometrica 86, 591–616.

- Kluve et al. (2012) Kluve, J., H. Schneider, A. Uhlendorff, and Z. Zhao (2012). Evaluating continuous training programs using the generalized propensity score. Journal of the Royal Statistical Society: Series A (Statistics in Society) 175(2), 587–617.

- Koenker (1994) Koenker, R. (1994). Confidence intervals for regression quantiles. In H. M. Mandl P. (Ed.), Asymptotic Statistics. Contributions to Statistics. Physica, Heidelberg.

- Lee (2009) Lee, D. S. (2009, 07). Training, Wages, and Sample Selection: Estimating Sharp Bounds on Treatment Effects. The Review of Economic Studies 76(3), 1071–1102.

- Lee (2015) Lee, Y.-Y. (2015). Partial mean processes with generated regressors: Continuous treatment effects and nonseparable models. Working paper.

- Lee (2018) Lee, Y.-Y. (2018). Partial mean processes with generated regressors: Continuous treatment effects and nonseparable models. arxiv:1811.00157.

- Lee and Li (2018) Lee, Y.-Y. and H.-H. Li (2018). Partial effects in binary response models using a special regressor. Economics Letters 169, 15–19.

- Luo and Spindler (2016) Luo, Y. and M. Spindler (2016). High-dimensional l2boosting: Rate of convergence. arxiv:1602.08927.

- Manski (2004) Manski, C. F. (2004). Statistical treatment rules for heterogeneous populations. Econometrica 72(4), 1221–1246.

- Newey (1994a) Newey, W. (1994a). The asymptotic variance of semiparametric estimators. Econometrica 62(6), 1349–1382.

- Newey (1994b) Newey, W. K. (1994b). Kernel estimation of partial means and a general variance estimator. Econometric Theory 10(2), 233–253.

- Newey (1997) Newey, W. K. (1997). Convergence rates and asymptotic normality for series estimators. Journal of Econometrics 79(1), 147–168.

- Newey and Robins (2018) Newey, W. K. and J. R. Robins (2018). Cross-fitting and fast remainder rates for semiparametric estimation. arxiv:1801.09138.

- Neyman (1959) Neyman, J. (1959). Optimal asymptotic tests of composite statistical hypotheses. Probability and Statistics 213(57).

- Noack et al. (2021) Noack, C., T. Olma, and C. Rothe (2021). Flexible covariate adjustments in regression discontinuity designs. 2107.07942.

- Oprescu et al. (2019) Oprescu, M., V. Syrgkanis, and Z. S. Wu (2019). Orthogonal random forest for causal inference. arxiv:1806.03467v3.

- Ouyang et al. (2009) Ouyang, D., Q. Li, and J. S. Racine (2009). Nonparametric estimation of regression functions with discrete regressors. Econometric Theory 25(1), 1–42.

- Powell et al. (1989) Powell, J. L., J. H. Stock, and T. M. Stoker (1989). Semiparametric estimation of index coefficients. Econometrica 57(6), 1403–30.

- Powell and Stoker (1996) Powell, J. L. and T. M. Stoker (1996). Optimal bandwidth choice for density-weighted averages. Journal of Econometrics 75(2), 291–316.

- Robinson (1988) Robinson, P. M. (1988). Root-N-consistent semiparametric regression. Econometrica 56(4), 931–954.

- Rothe and Firpo (2019) Rothe, C. and S. Firpo (2019). Properties of doubly robust estimators when nuisance functions are estimated nonparametrically. Econometric Theory 35(5), 1048–1087.

- Sasaki and Ura (2021) Sasaki, Y. and T. Ura (2021). Estimation and inference for policy relevant treatment effects. Journal of Econometrics, forthcoming.

- Sasaki et al. (2021) Sasaki, Y., T. Ura, and Y. Zhang (2021). Unconditional quantile regression with high dimensional data. arxiv:2007.13659.

- Schmidt-Hieber (2020) Schmidt-Hieber, J. (2020). Nonparametric regression usingdeep neural networkswith reluactivation function. Annals of Statistics 48(4), 1875–1897.

- Semenova and Chernozhukov (2020) Semenova, V. and V. Chernozhukov (2020). Estimation and inference about conditional average treatment effect and other causal functions. arxiv:1702.06240v3.

- Su et al. (2019) Su, L., T. Ura, and Y. Zhang (2019). Non-separable models with high-dimensional data. Journal of Econometrics 212(2), 646–677.

- Syrgkanis and Zampetakis (2020) Syrgkanis, V. and M. Zampetakis (2020). Estimation and inference with trees and forests in high dimensions. arxiv:2007.03210.

- Takatsu and Westling (2023) Takatsu, K. and T. Westling (2023). Debiased inference for a covariate-adjusted regression function. arxiv:2210.06448.

- Tan (2020) Tan, Z. (2020). Model-assisted inference for treatment effects using regularized calibrated estimation with high-dimensional data. The Annals of Statistics 48(2), 811–837.

- van der Laan et al. (2018) van der Laan, M. J., A. Bibaut, and A. R. Luedtke (2018). CV-TMLE for nonpathwise differentiable target parameters. In M. J. van der Laan and S. Rose (Eds.), Targeted Learning in Data Science: Causal Inference for Complex Longitudinal Studies, pp. 455–481. Springer International Publishing.

- van der Vaart and Wellner (1996) van der Vaart, A. W. and J. A. Wellner (1996). Weak Convergence and Empirical Processes: with Application to Statistics. New York: Springer-Verlag.

- Wager and Athey (2018) Wager, S. and S. Athey (2018). Estimation and inference of heterogeneous treatment effects using random forests. Journal of the American Statistical Association 113(523), 1228–1242.

- Yarotsky (2017) Yarotsky, D. (2017). Error bounds for approximations with deep relu networks. Neural networks: the official journal of the International Neural Network Society 94, 103–114.

- Zhang (2022) Zhang, L. Z. (2022). Cross-validated conditional density estimation and continuous difference-in-differences models. Working paper, Department of Economics, UCLA.

- Zimmert and Lechner (2019) Zimmert, M. and M. Lechner (2019). Nonparametric estimation of causal heterogeneity under high-dimensional confounding. arxiv:1908.08779.

Appendix: Proofs of Results

Proof of Lemma 2.1: We suppress subscripts for notational ease, e.g. .

We first show that uniformly in ,

,

using integration by parts, change of variables, a Taylor series expansion, and assuming to be uniformly bounded over .

By the triangle inequality,

| (A.1) | |||

| (A.2) |

For (A.1), we focus on . Denote by construction. So . Denote the th partial derivative of the conditional -quantile function with respect to (w.r.t.) as . By the mean value theorem, with between and . So

with between and by the mean value theorem. As is assumed to be bounded above uniformly, we obtain that uniformly in , . So the term in (A.1) is uniformly in .

Next consider (A.2). By a Taylor series expansion,

with and . So . Since we assume to be uniformly bounded over , the term in (A.2) is uniformly in .

As we assume that there exists a positive constant such that ,

we obtain that uniformly in .

Proof of Lemma 2.2: By the assumptions, there exists a finite positive constant such that .

By the triangle inequality,

| (A.3) | |||

For the term in (A.3) to be , we follow the standard algebra for kernel as the arguments in the proof of Lemma 2.1.

Asymptotically linear representation of : We give an outline of deriving the asymptotically linear representation in Theorem 3.1.

Let the moment function for identification by (2.2), i.e. uniquely defines .

Let the adjustment term , where .

The doubly robust moment function , as in equation (1.1).

Let denote the observations for .

Let

and using for .

Let and .

We can write , where and .

Then

.

We show below for each .

Since is fixed and are randomly partitioned distinct subgroups, the result follows from

We decompose the remainder term for each ,

| (R1-1) | ||||

| (R1-2) | ||||

| (R1-DR) | ||||

| (R2) |

The remainder terms (R1-1) and (R1-2) are stochastic equicontinuous terms that are controlled to be by the mean-square consistency conditions in Assumption 2.3(a) and cross-fitting. The second-order remainder term (R2) is controlled by Assumption 2.3(b).

The remainder term (R1-DR) is the key to doubly robust inference. Note that in the binary treatment case when is replaced by , the term (R1-DR) is zero because is the Neyman-orthogonal influence function, under correct specification and . In our continuous treatment case, the Neyman orthogonality holds as .

We show that by a standard algebra of kernel and the assumed conditions, for any , uniformly in . We will use the same arguments in the proofs. We use change of variables , a Taylor expansion, the mean value theorem where is between and , being bounded away from zero, and the second derivatives of being bounded uniformly over to show that

| (A.4) | |||

for some positive constant , for any , uniformly over .

Our results are readily extended to include binary/multivalued treatments at the cost of notational complication, e.g. the low-dimensional setting in Cattaneo (2010).

Specifically, the frequency method replaces the kernel with an indicator function:

, where

and

.101010

There is a literature on the kernel smoothing of discrete (categorical) variables (Aitchison and

Aitken (1976), Ouyang

et al. (2009) and reference therein); such extension to smoothing discrete treatments is out of the scope of this paper.

Proof of Theorem 3.1: The statements in the following hold for , , and for all .

For (R1-DR),

in the first part .

So the first term in (R1-DR)

.

Under the conditions in Theorem 3.1, .

So when , this first term in (R1-DR) is .

When ,

this first term is by assuming

in Assumption 2.3(b)(c).

A similar argument yields the second term in (R1-DR), . When , this second term of (R1-DR) is . When , this second term of (R1-DR) is by assuming in Assumption 2.3(b)(c).

Define . By construction and independence of and for , and for . By Assumptions 2.1(b) and 2.3(a), . . The conditional Markov’s inequality implies that .

The analogous results hold for in (R1-1) and in (R1-2). In particular for (R1-2), a standard algebra using change of variables, a Taylor expansion, the mean value theorem, and Assumption 2.1 yields that

| (A.5) |

where and are between and . So by Assumption 2.3(a). The conditional Markov’s inequality implies that . Then (R1-1) and (R1-2).

For (R2),

| (A.6) |

by Cauchy-Schwartz inequality and Assumption 2.3(b), and (A.4). So (R2) follows by the conditional Markov’s and triangle inequalities.

By the triangle inequality, we obtain the asymptotically linear representation

.

For , first compute . A standard algebra for kernel as (A.4) yields

uniformly over . Thus

| (A.7) | |||

Due to the doubly robust property, (A.7) is zero. Specifically, when and , (A.7) becomes . When and , (A.7) becomes . We then obtain and .

The asymptotic variance is determined by . A standard algebra for kernel as (A.5) yields .

Asymptotic normality follows from the Lyapunov central limit theorem with the third absolute moment.

Specifically,

, by the same arguments as (A.5)

under the condition that and its first derivative w.r.t. are bounded uniformly in .

Let .

Thus the Lyapunov condition holds: .

Proof of Theorem 3.2: By Theorem 3.1, the asymptotic MSE is .

Solving the first-order condition yields the optimal bandwidth .

Given the consistency of and , the continuous mapping theorem implies

.

Below we show the consistency of and .

Consistency of : Let , where .

It suffices to show that is consistent for as , for .

Toward that end,

we show that

(I) ,

where ,

(II) ,

and (III) ,

where .