Pattern graphs: a graphical approach to nonmonotone missing data

Abstract

We introduce the concept of pattern graphs–directed acyclic graphs representing how response patterns are associated. A pattern graph represents an identifying restriction that is nonparametrically identified/saturated and is often a missing not at random restriction. We introduce a selection model and a pattern mixture model formulations using the pattern graphs and show that they are equivalent. A pattern graph leads to an inverse probability weighting estimator as well as an imputation-based estimator. We also study the semi-parametric efficiency theory and derive a multiply-robust estimator using pattern graphs.

keywords:

[class=MSC]keywords:

journalname

Yen-Chi Chen111yenchic@uw.edu

Department of Statistics

University of Washington

1 Introduction

Missing data problems are prevalent in modern scientific research (Little and Rubin, 2002; Molenberghs et al., 2014). Based on the intrinsic constraints of missing/response patterns, these problems can be categorized into monotone and nonmonotone missing data problems. In the case of monotone missing data, the missingness of variables is ordered in such a way that if a variable is missing, all following variables are missing. This occurs in a scenario in which individuals drop out of a study, which is common in longitudinal studies (Diggle et al., 2002).

In the case of nonmonotone missing data, the missingness is not necessarily monotone, and the missingness of one variable does not necessarily place constraints on the missingness of any other variables. There have been several attempts to use the missing at random (MAR) restriction/assumption in this case (Robins, 1997; Robins and Gill, 1997; Sun and Tchetgen Tchetgen, 2018). However, the resulting inverse probability weighting (IPW) estimator may not be stable (Sun and Tchetgen Tchetgen, 2018), and the MAR restriction is not easy to interpret in nonmonotone cases (Robins and Gill, 1997; Linero, 2017). Therefore, several attempts have been made to use missing not at random (MNAR) restrictions which are interpretable. For instance, Shpitser (2016); Sadinle and Reiter (2017); Malinsky et al. (2019) proposed a non-self-censoring/itemwise conditionally independent nonresponse restriction, Little (1993a) and Tchetgen et al. (2018) considered a complete-case missing value (CCMV) restriction, and Linero (2017) introduced the transformed-observed-data restriction. However, each study proposed only one MNAR restriction to handle data, and it remains unclear how to construct a general class of identifying restrictions for nonmonotone missing data.

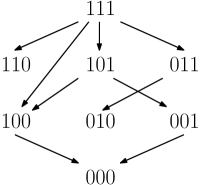

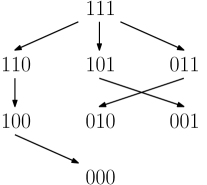

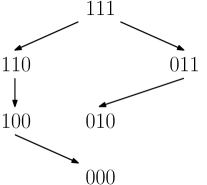

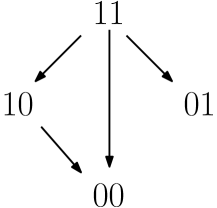

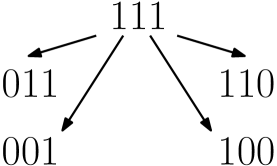

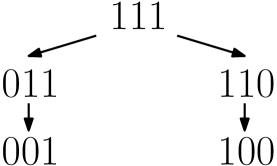

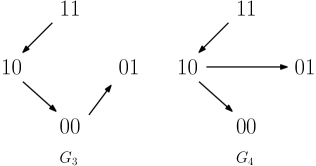

In this paper, we introduce a graphical approach to constructing identifying restrictions for nonmonotone missing data problems. This graphical approach defines an identifying restriction using a graph of response patterns; thus, the resulting graph is called a pattern graph. Formally, a pattern graph is a directed graph where nodes are possible response patterns and whose edges/arrows represent the relationship between the selection probability of patterns (also known as the missing data mechanism in Little and Rubin 2002). A pattern graph represents an identifying restriction placing conditions on the unobserved part of data, and is always nonparametrically identified/saturated (Theorem 3; Robins et al. 2000); that is, it does not contradict the observed data. In general, the identifying restriction of a pattern graph is an MNAR restriction. Figure 1 provides examples of pattern graphs when three variables may be missing, and a response pattern is described by a binary vector (e.g., signifies that for a variable , and are observed and is missing). Different pattern graphs correspond to different identifying restrictions, so pattern graphs define a large class of identifying restrictions. It should be emphasized that a pattern graph is not a conventional graphical model.

Main results. The main results of this paper can be summarized as follows:

Related work. The CCMV restriction (Little, 1993a; Tchetgen et al., 2018) can be represented by a pattern graph. In monotone missing data problems, the available-case missing value restriction (Molenberghs et al., 1998) and the neighboring-case missing value restriction (Thijs et al., 2002) and some donor-based identifying restrictions (Chen and Sadinle, 2019) can also be represented by pattern graphs. There have been studies that utilize graphs to analyze missing data. Mohan et al. (2013); Mohan and Pearl (2014); Tian (2015); Mohan and Pearl (2018); Bhattacharya et al. (2020); Nabi et al. (2020) proposed methods to test missing data assumptions under graphical model frameworks. Shpitser et al. (2015); Shpitser (2016); Sadinle and Reiter (2017); Malinsky et al. (2019) proposed a non-self censoring graph that leads to an identifying restriction under the MNAR scenario. However, it should again be emphasized that pattern graphs are different from graphical models; thus, our graphical approach is very different from the above-mentioned studies.

Outline. In Section 2, we formally introduce the concept of (regular) pattern graphs and describe how they represent an identifying restriction. We discuss strategies for constructing an estimator under a pattern graph in Section 3. We discuss potential future work in Section 4. In the supplementary materials (Chen, 2020), we present a sensitivity procedure in Appendix A, a study on the equivalence class in Appendix B, and an application to a real data in Appendix C. Technical assumptions and proofs are provided in Appendix J and K.

2 Pattern graph and identification

Let be a vector of the study variables of interest and be a binary vector representing the response pattern. Variable signifies that variable is observed. Let be the pattern corresponding to the completely observed case and be the reverse (flipping and ) of pattern . We use the notation . For example, suppose that , then , and . Table 1 presents an example of data with missing entries and the corresponding pattern indicator . Both and are random vectors from a joint distribution with a probability density function (PDF) , and we denote as the support of random variable . For a binary vector , we use to denote the number of non-zero elements.

| ID | ||||

| 001 | 5 | 1.3 | * | 110 |

| 002 | 6 | * | 1.1 | 101 |

| 003 | * | * | 1.0 | 001 |

| 004 | 5 | * | * | 100 |

| 005 | 2 | 2.1 | 0.8 | 111 |

Let be the collection of all possible response patterns, i.e., . A pattern graph is a directed graph , where each vertex represents a response pattern (vertex/node set ), and the directed edge represents associations of the distribution of across different patterns. Figure 1 provides examples of pattern graphs. Later we will give a precise definition of how a pattern graph factorizes the underlying distribution. The joint distribution of is called the full-data distribution and identifying the full-data distribution is a key topic in missing data problems.

When we equip the pattern set with a graph , we can define the notion of parents and children in the graph. For two patterns , if there is an arrow , we say that is a parent of and is a child of . Let denote the parents of pattern/node . A pattern/node is called a source if it has no parent.

For two patterns , we say that if for all and there is at least one element such that . For instance, and ; however, cannot be compared with or . An immediate result from the above ordering is that when , the observed variables in pattern are also observed in pattern .

A pattern graph is called a regular pattern graph if it satisfies the following conditions:

-

(G1)

Pattern is the only source in .

-

(G2)

If there is an arrow from pattern to (i.e., ), then .

Figure 1 presents three examples of regular pattern graphs when there are three variables subject to missingness. The first two panels are regular pattern graphs when all eight response patterns are possible, and the last panel displays a regular pattern graph when only six patterns are possible.

A regular pattern graph has several interesting properties. (G1) implies that the fully observed pattern is the only common ancestor of all patterns except for . Moreover, if is a parent of , then observed variables in must be observed in (due to (G2)). In a sense, this means that a parent pattern is more informative than its child. Condition (G2) implies the following condition:

-

(DAG)

is a directed acyclic graph (DAG).

Namely, a regular pattern graph is a DAG. In Appendix B, we demonstrate that replacing (G2) with (DAG) still leads to an identifiable full-data distribution.

2.1 Pattern graph and selection odds models

A common approach for the missing data problems is the selection model (Little and Rubin, 2002), in which we factorize the full-data density function as

and attempt to identify both quantities. Here, we focus on modeling the selection probability due to its role in constructing an IPW estimator. To illustrate this, suppose that we are interested in estimating a parameter of interest that is defined by a mean function, i.e., Using simple algebra, it can be shown that

which suggests that we can construct an IPW estimator if we know the propensity score .

To associate a pattern graph with the missing data mechanism, we consider the selection odds (Robins et al., 2000) between a pattern against its parents : . Formally, the selection odds model of factorizes with respect to pattern graph if

| (1) |

Namely, we assume that the (conditional) odds of a pattern against its parents depend only on the observed entries. Note that assumption (G2) in the regular pattern graph assumption implies that for any parent nodes of , variable is observed. Thus, factorization in terms of the selection odds implies that the selection odds are identifiable. From equation (1), it can be seen that the corresponding restriction is an MNAR restriction in general. Equation (1) is related to the MAR restriction in a more involved way (see Section 4 for a detailed discussion).

Let be the odds based on the variable . Equation (1) can be written as

| (2) |

Namely, the probability of observing pattern is the summation of the probability of observing any of its parents multiplied by the observable odds. Later in Proposition 3, we provide another interpretation of equation (1) using the path selection. A useful property of graph factorization is that the propensity score is identifiable, as described in the following theorem.

Theorem 1

Assume that the selection odds model of factorizes with respect to a regular pattern graph . Define

for each and . Then is identifiable and has the following recursive-form:

The identifiability follows from the induction. is clearly identifiable, and we recursively deduce the identifiability of from . Assumption (G2) guarantees that this recursive procedure is possible. Note that with an identifiable , we can identify and . Thus, the full-data density is identifiable.

Example 1 (Conditional MAR)

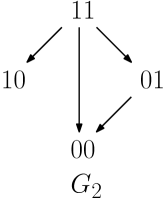

Consider the scenario in which we have a longitudinal variable with three time points, i.e., In addition, we have another study variable that is observed once at the baseline. The total study variable . Variable is subject to monotone missingness (dropout), and variable may also be missing. There are a total of six possible patterns in this case, as illustrated in the left panel of Figure 2. We use the variable to denote the dropout time and to denote the response indicator of variable . Suppose that we use the regular pattern graph as in the left panel of Figure 2. This graph implies the following assumptions on and (see Appendix D in Chen 2020 for the derivation):

The first two equations present the conditional MAR restriction, i.e., we have MAR of given and the observed . The third equation describes how the missing data mechanism of occurs. The graph provides a simple way to jointly model the dropout time and the missingness of variable .

Selection odds factorization provides an alternative interpretation of the missing data mechanism using the concept of path selection. A (directed) path , is the collection of ordered patterns

such that there is an arrow from to in the graph. A path from to refers to a path where initial node and the end node . Let

and operationally define . If there exists a path from to , we call an ancestor (pattern) of . With the above notation, we have the following decomposition.

Proposition 2

Assume that the selection odds model of factorizes with respect to a regular pattern graph . Then

| (3) | ||||

Proposition 3 presents an interesting interpretation of the selection odds model. Define to be a path-specific score. It can be seen that and by the first equality in Proposition 3. Thus, can be interpreted as the probability of selecting path from . The second equality can be written as

which implies that the probability of observing pattern is the summation of all path-specific probabilities corresponding to paths ending at .

Because every path starts from , a path can be interpreted as a scenario in which the missingness occurs (from a fully observed case). A path is randomly selected with a probability of , and missingness occurs sequentially as the elements in . So the last element in is the observed pattern. Therefore, the probability of observing a particular pattern is the summation of the probabilities of all possible paths that end at . The choice of a graph is a means of incorporating our scientific knowledge of the underlying missing data mechanism; in Section C, we provide a data example to illustrate this concept.

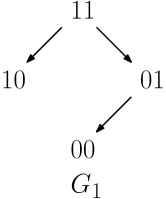

Example 2

Consider the pattern graph in the right panel of Figure 2, where it is generated by two variables and four patterns and has four arrows , and . There are five paths (including ):

and each corresponds to probability

Each path represents a possible scenario that generates the response pattern. Since the probability must sum to , we obtain

which agrees with Theorem 1. The probability of observing patterns and are and , respectively. Pattern occurs with a probability of

The first component represents scenario , i.e., the individual directly drops both variables. The other component corresponds to scenario , i.e., variable is missing first, and then variable is missing. Therefore, the paths in the pattern graph represent possible hidden scenarios that generate a response pattern.

Remark 3

Robins and Gill (1997) proposed a randomized monotone missing (RMM) process to construct a class of MAR assumptions for the nonmonotone missing data problems that also admits a graph representation on how the missingness of one variable is associated with others. This method may look similar to ours; however, the two ideas (RMM and pattern graphs) are very different. First, RMM constructs a MAR assumption, whereas pattern graphs are generally MNAR (generalizations of RMM to MNAR can be found in Robins 1997 and Robins et al. 2000). Second, each node in the RMM graph is a variable, whereas each node in a pattern graph is a response pattern. Third, in the next section, we demonstrate that the selection odds model in a pattern graph has an equivalent pattern mixture model representation; however,t it is unclear whether the RMM process has a desirable pattern mixture model representation or not.

2.2 Pattern graph and pattern mixture models

Another common strategy for handling missing data is pattern mixture models (Little, 1993b), which factorize

The above factorization provides a clear separation between observed and unobserved quantities. The first part, , is called the extrapolation density (Little, 1993b), which corresponds to the distribution of unobserved entries given the observed entries. This part cannot be inferred from the data without making additional assumptions. The latter part, , is called the observed-data distribution, which characterizes the distribution of the observed entries and can be estimated from the data without any identifying assumptions.

An interesting insight is that different response patterns provide information on different variables. Thus, we can associate an extrapolation density to the observed parts of another pattern. This motivates us to consider a graphical approach to factorize the distribution using pattern mixture models.

Formally, the pattern mixture model of factorizes with respect to a pattern graph if

| (5) |

Equation (5) states that the extrapolation density of pattern can be identified by its parent(s). Namely, we model the unobserved part of pattern using the information from its parents. This is a reasonable choice because condition (G2) implies that a parent pattern is more informative than its child pattern. Pattern mixture model factorization leads to the following identifiability property.

Theorem 3

Assume that the pattern mixture model of factorizes with respect to a regular pattern graph , then is nonparametrically identifiable/saturated.

Theorem 3 states that graph factorization using pattern mixture models implies a nonparametrically identifiable full-data distribution. Namely, the implied observed distribution of coincides with the observed-data distribution that generates our data for patterns such that . Thus, the identifying restriction derived from the graph never contradicts the observed data (Robins et al., 2000). Nonparametric identification is also known as nonparametric saturation or just-identification in Robins (1997); Vansteelandt et al. (2006); Daniels and Hogan (2008); Hoonhout and Ridder (2018).

Thus far, we have discussed two different methods of associating a pattern graph to a full-data distributions. The following theorem states that they are equivalent under the positivity condition ( for all and ).

Theorem 4

If is a regular pattern graph and for all and , then the following two statements are equivalent:

-

•

The selection odds model of factorizes with respect to .

-

•

The pattern mixture model of factorizes with respect to .

With Theorem 4, we can interpret the graph factorization using either the selection odds model or the pattern mixture model, both of which lead to the same full-data distribution. Because of Theorem 4, when we say factorizes with respect to , this factorization may be interpreted using the selection odds model or pattern mixture model. Note that this equivalence is not surprising, as Robins et al. (2000) demonstrated that certain classes of selection odds models and pattern mixture models are equivalent. Theorem 4 shows that the identifying restrictions from pattern graphs form another class of restrictions with this elegant property.

Example 4 (Complete-case missing value restriction)

The CCMV restriction (Little, 1993a) is an assumption in pattern mixture models. It requires that

| (6) |

for all pattern . The corresponding pattern graph is a graph where every node (except the node of ) has only one parent: the completely-observed case; namely, for all . The left panel in Figure 3 presents an example of the pattern graph of CCMV. Using Theorem 4 and the selection odds model, equation (6) is equivalent to

| (7) |

which is the key formulation in Tchetgen et al. (2018) that establishes a multiply-robust estimator.

Remark 5 (Transform-observed-data restriction)

Linero (2017) proposed a transform-observed-data restriction that is related to a particular pattern graph under a special case. Consider a three-variable scenario in which only five patterns are available , and there are two paths of arrows: and . The right panel of Figure 3 displays this graph. The first path implies and , which further implies , which is a requirement of the transform-observed-data restriction in this case. Similarly, the other path implies which is another requirement of the transform-observed-data restriction.

Remark 6 (Monotone missing data problem)

Suppose that the missingness is monotone; then, the pattern graph reduces to special cases of the interior family (Thijs et al., 2002) and donor-based identifying restriction (Chen and Sadinle, 2019). In particular, the parent set is the donor set of the dropout time The available-case missing value restriction (Molenberghs et al., 1998) corresponds to the pattern graph with , i.e., the graph with all possible arrows/edges. The neighboring-case missing value restriction (Thijs et al., 2002) is the pattern graph with .

3 Estimation with pattern graphs

In this section, we present several strategies for estimating the parameter of interest using the pattern graph. Here, we consider the parameter of interest that can be written in the form , where is a known function. Note that all analyses can be applied to the case of estimating equations.

With a slight abuse of notation, the observed data are written as IID random elements

where denote the response pattern of each observation and denotes the observed variables of the -th individual and denotes the vector of study variables of the -th individual. Note that not every entry of is observed; we only observe , while is missing.

3.1 Inverse probability weighting

The parameter of interest can be written as

This formulation implies that as long as we can estimate , we can construct a consistent estimator of via the concept of IPW.

From Theorem 1, the propensity score can be expressed as

By the above recursive property, an estimator of leads to an estimator of and . The odds

can be estimated by comparing the distribution of patterns with patterns . This can be achieved by constructing a generative binary classifier (Friedman et al., 2001) such that label refers to and label refers to or by a regression function with the same binary outcome and the feature/covariate is . In Example J.19 of Appendix J, we describe a logistic regression approach to estimate .

Suppose that we have an estimator of the propensity score. Then, we can estimate using the IPW approach as follows:

As an example, suppose that we estimate by placing parametric models over the odds, i.e.,

where is the estimated parameter of the selection odds . We can estimate the selection odds using a maximum likelihood approach or moment-based approach. With the estimated selection odds, we estimate the propensity score using the recursive relation. Let be the set of the estimated parameters.

Theorem 5

Assume (L1-4) in Appendix J and that the selection odds model of factorizes with respect to a regular pattern graph . Then is a consistent estimator and satisfies

for some .

Theorem 5 shows the asymptotic normality of the IPW estimator and can be used to construct a confidence interval. A traditional approach is to obtain a sandwich estimator of and use it with the normal score to construct a confidence interval. However, the actual form of is complex because patterns are correlated based on the graph structure and there is no simple way to disentangle them. Thus, we recommend using the bootstrap approach (Efron, 1979; Efron and Tibshirani, 1994) to construct a confidence interval. This can be acheived without knowing the form of . Note that the bootstrap method often requires a third moment condition of the score (Hall, 2013); for smooth parametric models such as logistic regression with a bounded covariates, this condition holds.

We can rewrite the IPW estimator as

So the quantity behaves like a score from pattern on observation .

3.1.1 Recursive computation

Although the IPW estimator has desirable properties, the propensity score does not have a simple closed form; therefore, the computation of Equation (3) is not easy. To resolve this problem, we provide a computationally friendly approach to evaluate (or its estimator ) using the recursive relation in Theorem 1.

From Theorem 1, ; thus, it is only necessary to compute . The recursive form in Theorem 1,

demonstrates that we can compute recursively.

Algorithm 1 summarizes the procedure for computing . We first compute cases where . Having computed , we can easily compute because only depend on and each . Thus, by sequentially computing (noting that )

we obtain every , which then leads to .

Suppose that evaluating takes units of operations; then, total cost of evaluating using Algorithm 1 is units, where is the number of parents of node . However, if we use equation (3), the total cost is , where is the number of vertices in the path. It can be seen that and the number of parents can be much smaller than the total number of paths. Therefore, Algorithm 1 is much more efficient than directly using equation (3).

3.2 Regression adjustments

We can rewrite the parameter of interest as

Thus, if we have an estimator for every , we can estimate using the regression adjustment approach

In Appendix F.2, we demonstrate that a Monte Carlo approximation of this estimator is the imputation-based estimator (Little and Rubin, 2002; Rubin, 2004; Tsiatis, 2007).

Regression adjustment is feasible because the regression function is identifiable. To see this, using the PMM factorization in equation (5),

and is identifiable due to Theorem 3.

In practice, we first estimate using a parametric model for every . With this, we then estimate . Note that we can use a nonparametric density estimator as well, but it often suffers from the curse of dimensionality.

For pattern , let be the parameter of the model . Namely,

We can estimate via the maximum likelihood estimator (MLE). Let be the MLE. We model it in this way to avoid model conflicts; see Appendix F.1 in the supplementary material (Chen, 2020) for more details. Let be the collection of all parameters in the model, let be the corresponding parameter space, and let be the MLE. The regression function is then estimated by

Note that in the above expression, the expression of the estimator depends on the entire set of parameters , but actually only depends on the parameter belonging to its ancestor. We express it using to simplify the notation.

Theorem 6

Assume (R1-3) in Appendix J and that the pattern mixture model of factorizes with respect to a regular pattern graph . Then is a consistent estimator and satisfies

for some .

Theorem 6 shows that if the density estimators are consistent, the resulting regression adjustment estimator is asymptotically normal. Similar to the IPW estimator, this provides a way to construct a confidence interval using the bootstrap. In Appendix F.2, we describe a Monte Carlo approach to compute . In addition, we show that when the pattern graph is a tree graph, there may be a closed form of the regression adjustment estimator; thus,o we do not need a numerical procedure (Appendix I).

3.3 Semi-parametric estimators

We now study the semi-parametric theory of the pattern graph and propose an efficient estimator. We start with a derivation of the efficient influence function (EIF) of . For any pattern , recall that denotes all paths from to and is the collection of all paths.

By Theorem 1 and equation (4), the inverse of the propensity score can be written as

Thus, the IPW formulation can be decomposed as

| (8) | ||||

For a path and an element , we define

| (9) | ||||

where

| (10) | ||||

| (11) |

The following proposition demonstrates that is the EIF of ; therefore, we obtain a closed form of the EIF of .

Theorem 7 (Efficient influence function)

Suppose that the selection odds model of factorizes with respect to a regular pattern graph and . The EIF of is

Thus, the EIF of is

Theorem 7 provides an analytical form of the EIF of both and a pathwise version of it. Theorem 7 also illustrates how a pattern graph informs the construction of the EIF. In Appendix H, we derive the expression of the EIF of Example 2. A key element in the EIF is the function defined in equation (10). In what follows, we describe how is associated with the regression adjustment estimator in Section 3.2.

Proposition 8 (Relation to regression adjustment)

Let denote the ancestors of including itself. For , let be the collection of all paths from to . Then

-

1.

Function is identifiable from

-

2.

, where is the regression function defined in Section 3.2;

-

3.

The EIF of pattern , , can be written as

Suppose that we have a collection of models , where is the underlying parameters. By Proposition 8, we can identify using these models, leading to without any knowledge of the selection odds. This insight leads to the construction of a semi-parametric estimator in the next section.

In addition, Theorem 7 and Proposition 8 provide two equivalent expressions of the EIF. The first one is a path expression:

while the second is an ancestor expression:

where is defined in Proposition 8. The path expression provides insight into how each path’s information contributes to the efficiency of a node, whereas the ancestor expression demonstrates how an ancestor improves the efficiency of its descendent. Moreover, the path expression provides a clear picture of the multiple robustness property (Section 3.3.2) while the ancestor expression leads to a simpler numerical procedure (Algorithm 2), which is a mild modification of the regression adjustment.

3.3.1 Construction of semi-parametric estimators

With the EIF, we can derive a semi-parametric estimator. Since our derivation of EIF is based on the IPW approach, the linear form of the semi-parametric estimator is the IPW added to the augmentation from the EIF, i.e.,

It can be seen that . We use the path expression in the following derivation, as it leads to an elegant multiple robustness property (see next section).

Let be the estimated selection odds and let be the estimated density used in the regression adjustment method. By Proposition 8, the collection implies the collection , where . In addition, let be the estimated selection odds of pattern .

With these estimators, we estimate the EIF by

and construct the semi-parametric estimator

| (12) | ||||

The semi-parametric estimator contains an IPW component and an augmentation component, so it is an augmented IPW estimator (see Appendix G for more details). Semi-parametric theory ensures that this estimator is the most efficient estimator when both the selection odds and the regression functions are correctly specified. Algorithm 2 provides a Monte Carlo procedure to compute the semi-parametric estimator, which is a combination of the recursive algorithm in Algorithm 1 and the multiple imputation in Algorithm 4 in the supplementary materials. The key is to use the ancestor expression, which leads to a simpler form of the semi-parametric estimator. Note that similar to the regression adjustment estimator, if the pattern graph is a tree graph, we can avoid using Algorithm 2 to compute the estimator; see Appendix I.

3.3.2 Multiple robustness

In many scenarios, a semi-parametric estimator often exhibits a double robustness or multiple robustness property (Robins et al., 2000; Tsiatis, 2007; Seaman and Vansteelandt, 2018). We demonstrate that our semi-parametric estimator in equation (12) also enjoys a multiple robustness property. Here, we assume that the parameters and Note that equation (12) can be factorized as

We demonstrate the multiple robustness properties of each component . Note that we let and denote the correct selection odds and regression function for each and each path , respectively.

Theorem 9 (Multiple robustness)

Suppose that the selection odds model of factorizes with respect to a regular pattern graph and . Let be a response pattern. For a path , if either or for each , then

Using the fact that , it is evident that if we can consistently estimate for each , we can estimate consistently.

Let be the case where the selection odds of pattern is correctly specified. For and , let be the case where is correctly specified. Theorem 9 shows that under the intersection of models

the quantity leads to a consistent estimator of , i.e.,

Thus, to estimate , we must select a model in

| (13) |

If our model falls within , we have This describes the multiple robustness property of the semi-parametric estimator in equation (12).

4 Discussion

In this paper, we, introduce the concept of pattern graphs and use it to represent an identifying restriction for missing data problems. Pattern graphs provide a new way to construct identifying restrictions. We demonstrate that pattern graphs can be interpreted using a selection odds model or pattern mixture model. In addition, we propose various estimators using different modeling strategies and study statistical and computational properties with a pattern graph. The theories developed in Section 3.3 demonstrate the elegant association between the semi-parametric theory and pattern graphs. We believe that the pattern graph approach can provide a new direction in missing data research. Below, we discuss possible future directions that arevworth pursuing.

-

•

Choice of pattern graph. In this paper, we mainly focus on the theoretical analysis of pattern graphs and assume that a pattern graph is given. In practice, determining how to select a pattern graph is an open problem. Since a pattern graph leads to an identifying restriction, it should be chosen based on background knowledge of how missingness occurs. In Appendix C, we provide a data analysis example and attempt to choose a pattern graph based on prior knowledge of the data generating process. In this particular example, we use the path selection interpretation of pattern graphs (Proposition 3 and related discussion) to select a plausible pattern graph. Although this approach is reasonable for this particular data, it may not apply to other problems. We plan to develop a general principle for selecting a pattern graph in future work.

-

•

Inference with multiple restrictions. Although a pattern graph may be derived from scientific knowledge, sometimes there may be uncertainties regarding the graph to be used. As a result, there may be a set of possible graphs that are reasonable. In this scenario, determining how to perform statistical inference is an open question. One possible solution is to derive a nonparametric bound (Manski, 1990; Horowitz and Manski, 2000) or an uncertainty interval (Vansteelandt et al., 2006) in which we compute an estimator of each graph and use the range of these estimators as an interval estimate. Alternatively, one can consider a Bayesian approach that assigns a prior distribution over possible graphs and derives the posterior distribution of the parameter of interest. The posterior mean behaves like a Bayesian model averaging estimator (Hoeting et al., 1999), and the posterior distribution includes uncertainties from both estimation and graphs.

-

•

MAR and conditional independence. The MAR restriction can be written as a pattern graph with . It is not a regular pattern graph; however, it still leads to a uniquely identified full-data distribution (Gill et al., 1997). This implies that pattern graphs that are not DAGs may still lead to an identifying restriction. Pattern graph factorization implies the following conditional independence:

(14) for each . When , this is equivalent to the MAR restriction. The choice of is equivalent to the choice of the parents, which may provide a way to study identifying restrictions beyond acyclic pattern graphs. Thus, studying the conditions on that lead to an identifiable full-data distribution is a future direction that is worth pursuing.

Acknowledgement

We thank Adrian Dobra, Mathias Drton, Mauricio Sadinle, Daniel Suen, Thomas Richardson for very helpful comments on the paper. This work is partially supported by NSF grant DMS 1810960 and DMS - 195278 and NIH grant U01 AG016976.

Appendix A Sensitivity analysis

Sensitivity analysis is a common task in handling missing data (Little et al., 2012). It aims to analyze the effect of perturbing an identifying restriction on the final estimate, and also serves as a means of incorporating the uncertainties of the identifying restriction into the inference. Here, we introduce three approaches for sensitivity analysis based on pattern graphs.

A.1 Perturbing selection odds

The first approach involves perturbing the selection odds model. Using the concept of exponential tilting (Kim and Yu, 2011; Shao and Wang, 2016; Zhao et al., 2017), the selection odds model in equation (1) can be perturbed as

where is a given vector that controls the amount of perturbation. If we set , this reduces to the usual graph factorization.

When we use a logistic regression model, the exponential tilting approach leads to an elegant form of the selection odds:

| (15) |

where and . Thus, computing the estimator of the propensity score is simple: we modify Algorithm 1 by replacing by , where . The recursive computation approach in Algorithm 1 can be easily adapted to this case. Appendix C.1 provides a data example of this concept.

A.2 Perturbing pattern mixture models

Alternatively, we can perturb the PMMs. From equation (5), the graph factorization of a PMM implies that

and we use the exponential tilting again to perturb it as

| (16) |

Again, implies that there is no perturbation, which is the case where graph factorization is assumed to be correct.

Interestingly, perturbations on selection odds and on PMMs are the same, as illustrated by the following theorem.

Theorem 10

Let be a response pattern and be any function of the unobserved entries and for all and . Then the assumption

is equivalent to the assumption

Theorem 10 demonstrates that a perturbation on the selection odds is the same as a perturbation on the PMMs. This result is not limited to the exponential tilting approach: any other perturbation, as long as the perturbation is only on unobserved variables, will lead to the same result.

As mentioned before, we generally use the multiple imputation procedure to compute an estimator when a PMM factorization is used. This procedure must be modified when using the sensitivity analysis of equation (16). If is bounded and with a known upper bound such that , we can then modify Algorithm 4 by combining it with rejection sampling. We change steps 2-4 in Algorithm 4 to the following two steps:

2.4’ If , return to 2-2; otherwise draw .

2.5’ If , then update ; otherwise return to 2-1.

Step 2.5’ states that with a probability of , we accept this proposal. This additional rejection-acceptance step rescales the density so that we are indeed sampling from (16). Note that it is possible to modify the algorithm using Markov chain Monte Carlo (MCMC; Liu 2008); however, the computational cost of MCMC would be enormous, as we would have to perform it for every observation.

A.3 Perturbing the graph

In addition to performing sensitivity analysis on the selection odds and pattern mixture models, we can consider perturbing the graph. Before we proceed, we provide description of the number of identifying restrictions that can be represented by regular pattern graphs. Let be the total number of distinct graphs that satisfy (G1-2) when there are variables subject to missingness.

Proposition 11

If all study variables in are subject to missingness, then there are

distinct graphs satisfying conditions (G1-2) .

The first few values of are as follows:

Proposition 11 demonstrates that the collection of regular pattern graphs is a rich class. It contains an astronomical number of identifying restrictions when only four variables are subject to missingness. Given the richness of this class, we can examine the effect of perturbing the graph on the final estimate.

Here, we formally describe our perturbation of a graph. Suppose that is the graph used in our original analysis that leads to an estimate . We wish to know how changes if we slightly perturb . A simple perturbation is by using graph such that and differ by only one edge.

Let be a graph satisfying (G1-2). We define to be the collection of graphs such that

where represents the case in which the two graphs only differ by one edge (arrow). Namely, is the collection of graphs satisfying (G1-2) and only differ from by one edge (arrow). The class can be decomposed into

where

Namely, is the collection of graphs with one more edge than , whereas is the collection of graphs with one less edge than .

The following proposition provides an explicit characterization of and .

Proposition 12

Assume that is a regular pattern graph. Let be vertices of . We define to be the graph where edge is added and to be the graph where edge is removed. Then

Proposition 12 provides a simple description of the possible perturbed graphs from . is the collection of graphs in which we add an arrow from a potential parent (the set is the potential parent of ). In other words, the constraint of is that the added edge must preserve the partial order among patterns. The set is the collection of graphs in which we drop one parent if there are at least two possible parents. Namely, the constraint of is that we can only remove an arrow if it is not the only arrow pointing toward a pattern. Given graph , finding these two sets is straightforward: the first one can be obtained by enumerating all possible edges that are not yet presented in . To find all graphs in , we identify all arrows pointing to a node with multiple parents; each arrow represent a graph in .

Appendix B Acyclic pattern graphs and equivalence classes

In this section, we investigate the scenario of relaxing the regular pattern graph conditions (G1-2). A pattern graph is called an acyclic pattern graph if it satisfies (G1) and (DAG). An acyclic pattern graph also leads to an identifying restriction.

Theorem 13

For a pattern graph that satisfies (G1) and (DAG) and for all and , the following holds:

-

1.

The selection odds model and pattern mixture model factorizations are equivalent.

-

2.

Graph factorization leads to an identifiable full-data distribution.

Namely, Theorem 13 states that if we replace the descending property (G2; implies ) by the DAG condition (DAG), graph factorization still defines an identifying restriction. This is not a surprising result because using PMM factorization, as long as the source is identifiable (i.e., is estimatable), its children and all descendants are identifiable. Although an acyclic pattern graph defines an identifying restriction, it may be difficult to interpret the implied restriction.

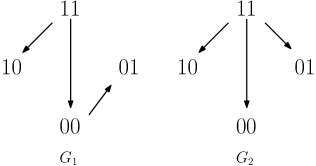

Two graphs are equivalent if the implied full-data distributions are the same. An equivalence class is a collection of graphs that are all equivalent. This idea is similar to the Markov equivalence class in graphical model literature (Andersson et al., 1997; Gillispie and Perlman, 2002; Ali et al., 2009). Figure 4 presents four examples of acyclic pattern graphs (note that is also a regular pattern graph), and they form two equivalence classes: are equivalent and are equivalent. Although is not a regular pattern graph, it represents the same full-data distribution as a regular pattern graph . Thus, some acyclic pattern graphs are equivalent to regular pattern graphs. However, there are cases in which acyclic pattern graphs are different from regular pattern graphs. Graphs form another equivalent class, but there is no regular pattern graph in the same class.

The example in Figure 4 motivates us to investigate graphical criteria leading to the equivalence of two acyclic pattern graphs. The following theorem provides a graphical criterion for this purpose.

Theorem 14

Let be an acyclic pattern graph and be two patterns such that . Graph is equivalent to graph if the following conditions hold:

-

1.

(blocking) All paths from to intersect .

-

2.

(uninformative) For any pattern that is on a path from to , .

Theorem 14 provides a graphical criterion for how to construct an equivalent graph. It also provides a sufficient condition for the equivalence of two graphs. The two equivalence classes in Figure 4 can be obtained by applying Theorem 14. This theorem states that if we can identify a pattern such that blocks all paths from the source to (blocking condition) and all descendants on a path from to do not provide any information on the missing variables of (uninformative condition), then we can remove all arrows to and replace them with an arrow from to .

Appendix C Data Analysis

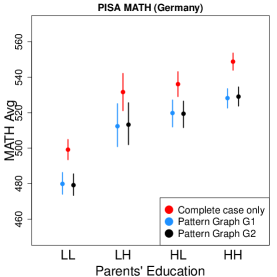

To demonstrate the applicability of pattern graphs, we use the Programme for International Student Assessment (PISA) data from the year 2009222The data can be obtained from http://www.oecd.org/pisa/data/pisa2009database-downloadabledata.htm. We focus on Germany (country code: 276) as there is a higher proportion of missing entries for Germany’s students. There are a total of 4,979 students in Germany’s dataset. We consider the following three study variables: MATH: the plausible score of mathematics, FA: whether the father has higher education or not, MA, whether the mother has higher education or not. There are five plausible scores of mathematics (due to five different item response models to balance the fact that students may be taking different exams), and we use their average. Variables FA and MA are binary variables (we use H/L to avoid confusion with the response indicator) such that H represents yes (with a college degree or higher) and L represents no. Missingness occurs in the variables FA and MA while the mathematics scores are always observed. Note that the original data contains finer categories for educational level of the father/mother; if any of them are missing, we treat variable as missing. The distribution of missingness is presented in Table 2.

| 11 | 10 | 01 | 00 | |

|---|---|---|---|---|

| 3282 | 230 | 340 | 1126 | |

| Proportion |

Here, we present a possible approach of choosing a pattern graph using prior knowledge of the data. Variables FA and MA are collected by a questionnaire before a student takes the exam. Suppose that the question asking about the father’s education precedes asking about the mother’s education. In addition, suppose that if a student chooses to report FA and moves to the question about the mother’s education, he or she will not change his/her mind to remove the value of FA.

Before we ask a student a question, there is an answer to that question. Thus, every individual starts with a response pattern in the beginning. When we ask the first question (the father’s education level), the student may answer it or not. If the student answers it, the pattern remains and the student moves to the second question. If the student does not answer it, then the pattern becomes and the student moves to the second question. Before asking the second question, the response pattern is . If the student answers the second question, then the pattern remains ; however, if the student does not answer it, the pattern becomes . To sum up, there are four possible scenarios and each can be represented by a particular path:

| Answer FA and then answer MA | |||

| Answer FA and then not answer MA | |||

| Not answer FA but then answer MA | |||

| Not answer FA and then not answer MA | |||

The notation denotes the decision of whether to answer one question; becomes an arrow in a DAG when . The only exception is the scenario in which ; in this case, we denote it as . We do not have the arrow because the decision to report FA precedes the decision to report MA. Using the path selection interpretation, the graph in Figure 6 is a reasonable pattern graph that contains all these scenarios. Now, if we include a new scenario in which the individual can skip any questions about the parents’ education at the same time, this corresponds to the path , so the graph in Figure 6 is a plausible pattern graph in this case. Although the above procedure provides a simple and perhaps interpretable way to select a pattern graph, it should be emphasized that this procedure is merely a tool for selecting a plausible pattern graph and is not a model of the mechanism of how an individual responds to the questions.

With a given pattern graph, we study the students’ average math scores under different parents’ education levels (FA, MA). Figure 6 presents the results using both (blue) and (black), and the result using a complete-case only (red) as a reference. We use the IPW estimator with a logistic regression model for the selection odds and compute the uncertainty using the (empirical) bootstrap. The intervals are 95% confidence intervals. We observe that both and produce very similar results, and the complete-case analysis indicate a higher average score across all groups. Note that using both and in the analysis can be viewed as a sensitivity analysis in which we perturb the underlying mechanism (graphs) to investigate the effect on the final estimate.

C.1 Sensitivity analysis on PISA data

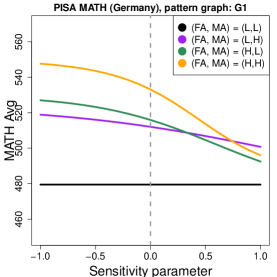

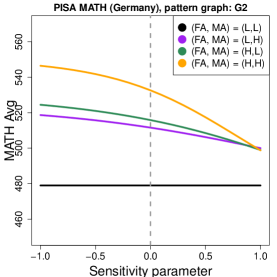

For completeness of analysis, we perform a simple sensitivity analysis on the PISA data by the exponential tilting approach introduced in Section A. We use the same sensitivity parameter for all patterns and all values, i.e., every element of in equation (15) is identical. Note that because only FA and MA are subject to missingness, the sensitivity parameter only applies to these two variables.

Figure 7 presents the average math score when we vary the sensitivity parameter in both graphs and . In both panels, we observe that group is unaffected by the sensitivity parameter. This is because when both FA and MA are L (the binary representation of L is and H is ), the sensitivity parameter does not affect any odds ( when ). Group is strongly influenced by the sensitivity parameter because both variables are non-zero; thus, the effect is strongest. In most cases (except case ), we see a decreasing trend. This can be understood by comparing it to the complete-case analysis (red dots in Figure 6). When we only use complete data, all values are higher than pattern graphs. A small value (negatively large) of the sensitivity parameter provides low selection odds in the graph, leading to a result that is similar to the complete-case analysis. This is why a decreasing trend is observed.

Appendix D Derivation of Example 1 (conditional MAR)

Recall that in Example 1, and is the response indicator of and are the response indicators of and is the dropout time. Let be the response indicator of . For two patterns we use the notation to denote or .

We present the result for the case in which is observed. The case in which is unobserved can be derived in a similar manner.

Case . In the case of observing , the selection odds model implies

Dividing both sides by , we obtain

Using the fact that , we have

so , which further implies

the conditional MAR of given .

Case . The selection odds model implies that

Dividing both sides by , we obtain

The case of also implies that

Thus, using the equality again, we have

Using , the above equality becomes

which implies . Using the fact that

we conclude that , which proves the case of .

Note that is a trivial case and is thus omitted. Therefore, the above analysis demonstrates that the graph in Example 1 implies

The case of unobserved can be derived in a similar manner by replacing by and removing all conditioning on . Thus, we also have

Note that the graph in Example 1 can be generalized to cases in which there are more time points. The pattern graph will correspond to similar conditional MAR assumptions.

Appendix E Computation: logistic regression

In Theorem 1, a key quantity for the IPW estimator is and Proposition 3 presents a simple form for . With logistic regression, we can further express in an elegant way.

Proposition 15

Using the path selection interpretation in Section 2.1, each path contributes the amount of to , thus, the quantity can be interpreted as a path-specific parameter in the logistic regression model. The intuition behind this is that the augmented parameter has the following useful property:

As a result, using the form of simplifies the representation.

Example 8

Consider an example in which we have three study variables and a total of four possible patterns: (the third variable is always observed). Suppose that there are four arrows: , , . In this case,

For a vector of study variables , and the corresponding , and the parameters are

Thus, only depends on the last variable, which implies

The other two cases are very simple: . With these quantities, we can compute

If we have estimators for each , the estimated propensity score is

Appendix F More about regression adjustment

F.1 Model congeniality

The parametric model in regression adjustment is constructed from modeling the observed-data distribution first and then deriving the model on the conditional expectation (regression function). One may wonder whether we can directly start with a model on the conditional expectation, i.e., make a parametric model for each . We do not recommend this approach because these models may not be variationally independent. For instance, suppose that pattern is a parent of pattern . Then, the regression model and regression model are linked via the following equality:

The quantity can be further written as

Thus, and are associated. If we do not specify them properly, the two models may conflict with each other.

F.2 Imputation algorithm of PMMs

Despite the power of Theorem 6, the regression adjustment estimator is generally not easy to compute. A major challenge is that the conditional expectation often does not have a simple form. Here we propose to compute the expectation using a Monte Carlo approach. For a given , we generate many values of as follows:

and then approximate the expectation using

We perform this approximation for every observation, and then obtain our final estimator as

| (17) | ||||

where

is an estimator using a completely imputed dataset. Namely, the Monte Carlo approximated estimator combines several individually imputed estimators; thus, it is essentially a multiple imputation estimator (Little and Rubin, 2002; Rubin, 2004; Tsiatis, 2007).

To compute the regression adjustment estimator, we must be able to sample from . However, sampling from may be difficult. Here, we provide a simple procedure to sample from the estimated extrapolation density with access to only (i) sampling from and (ii) evaluating the function .

Algorithm 3 is a simple approach that imputes missing entries of an observation. The output is an observation with a smaller number of missing entries (there may still be missing entries after executing Algorithm 3 once). Suppose that the input response pattern is and Algorithm 3 imputes some missing entries, making it a new response pattern . Then, we can treat this observation as if it was an observation with response pattern and apply Algorithm 3 again to impute more missing entries. By repeatedly executing Algorithm 3 until no missingness remains, we impute all missing entries of this observation. Note that this algorithm is based on equation (25) in the proof of Theorem 3.

Appendix G Improving efficiency by augmentation

It is known from semi-parametric theory that the IPW estimator may not be efficient, and it is possible to improve the efficiency by augmenting it with additional quantities (Tsiatis, 2007). We propose to augment it by the form

| (18) |

where is a pattern -specific function of variable . This augmentation is inspired by the following equality

Therefore, the augmented inverse probability weighting (AIPW) estimator

| (19) | ||||

is an unbiased estimator of . The semi-parametric estimator in Section 3.3 is an AIPW estimator.

To investigate the augmentation of equation (19), let

be the collection of all possible augmentations leading to an unbiased estimator and

| (20) | ||||

be the augmentation via equation (19).

Proposition G.17.

Assume that factorizes with respect to a regular pattern graph and for all . Then

Proposition G.17 presents a powerful result–the augmentation in the form of spans the entire augmentation space. Therefore, any augmented IPW estimator can be written in the form of equation (19). Alternatively, one can interpret this proposition as stating that a typical element orthogonal to the observed data tangent space can be expressed via the augmentation in equation (20).

Remark G.18 (Another representation of augmentations).

A common augmentation (Tsiatis, 2007; Tchetgen et al., 2018) is in the form of

A notable fact is that this augmentation is the same as equation (19) if the pattern graph is constructed using for all . Namely, this is the augmentation from the CCMV restriction (Tchetgen et al., 2018). Although this is a valid augmentation (see Lemma K.35), the optimal may not have a simple form due to the fact that the odds depend on every variable in . As a result, we commend to construct the augmentation using equation (20).

Appendix H An example of efficient influence function

Here, we provide a closed form expression of the EIF of Example 2 (based on the pattern graph of right panel of Figure 2) in the main document. There are a total of four patterns: and four edges .

For each , the collection of paths is

The corresponding regression function is

One can observe that which is a property that used in the part 3 of the proof of Proposition 8. Note that so is merely a constant.

With this, the EIF of each path is

where signifies or . The function is the summation of all these terms.

Appendix I Tree graph

In this section, we discuss a particularly interesting family of pattern graphs called tree graphs. We demonstrate that for this family, if the observed-data distribution is Gaussian for all and the parameter of interest is a simple function, then we can avoid the use of Monte Carlo approach in the regression adjustment estimator and the semi-parametric estimator.

A tree graph is a pattern graph such that for all patterns , . Namely, every node has only one parent, so it looks like a tree with the unique source . We use to denote the collection of all tree graphs. One can easily see that the pattern graph corresponding to the CCMV restriction is a tree graph.

Since every node in a tree graph has only one parent, the selection odds have an elegant expression. Specifically, supposing that is the parent of , we have

| (21) |

With this, we now demonstrate that if the pattern graph and is a (multivariate) normal density, the function may have a closed form, so by property 2 of Proposition 8, function has a closed form.

Without loss of generality, consider a path

By equation (21) and , we have

Thus, if functional is a simple function such as for some fixed ), the quantity is a linear function of and parameters of this function are determined by the mean and covariance of because of Gaussian assumption. By iteratively applying this fact, we conclude that is a linear function of and the parameters of this function are determined by the coefficients of Gaussians on path . Moreover, using property 2 of Proposition 8, we also obtain a closed form of the function . In this case, we do not need to use any numerical methods to compute .

Appendix J Technical assumptions

J.1 Assumptions of IPW estimators

Let be any parameter value, where is the total parameter space. To obtain the asymptotic normality of the IPW estimator, we assume the following conditions:

-

(L1)

there exists such that

for all and and .

-

(L2)

there exists in the interior of such that and

for some for all .

-

(L3)

for every , the class is a Donsker class.

-

(L4)

for every , the differentiation of with respect to , , exists and for a ball for some .

Assumption (L1) avoids the scenario that the selection odds diverge. The second assumption (L2) requires that the model is correctly specified and the estimator is asymptotic normal and the implied estimated odds converges in norm. The Donsker condition (L3) is a common condition that many parametric models satisfy; see Example 19.7 in van der Vaart (1998) for a sufficient condition on the parametric family. The bounded integral condition (L4) is relatively weak after assuming (L2) and (L3). The quantity is essentially a score equation so this assumption requires that the score equation exists and has a finite norm.

Example J.19 (Logistic regression).

Here, we discuss a special case of modeling the selection odds via logistic regression. For each , the logistic regression models the selection odds as

| (22) |

where is the coefficient vector and is the vector including as the first variable. We include in so the intercept is the first element of can be estimated by applying a logistic regression for the pattern against the pattern . Now we discuss conditions (L1-4) in Theorem 1 under the logistic regression model. (L1) holds if the support of study variable is (elementwise) bounded. The second condition holds if the logistic regression model correctly describes the selection odds. The asymptotic normality follows from the regular conditions of a logistic regression model. The Donsker class condition (L3) holds for the logistic regression model with a bounded study variable. Condition (L4) also holds when is bounded and the true parameter is away from boundary because of . Note that the logistic regression has a special computational benefit, as described in Appendix E.

J.2 Assumptions of RA estimators

The regression adjustment estimator has asymptotic normality under the following conditions:

-

(R1)

There exists such that the true conditional density for every .

-

(R2)

For every , the class

is a Donsker class.

-

(R3)

For every , is bounded twice-differentiable and

(R1) requires that the parametric model is correct, which is common for establishing the asymptotic normality centering at the true parameter. The Donsker class condition in (R2) is a common assumption to establish a uniform central limit theorem of a likelihood estimator (see Chapter 19 of van der Vaart 1998). In general, if the parametric model is sufficiently smooth and the statistical functional is smooth such as being a linear functional (van der Vaart, 1998), we have this condition. Condition (R3) is a consistency condition–we need to be a consistent estimator of in the sense that the implied regression function converges in norm and has asymptotic normality.

Appendix K Proofs

Proof K.20 ( of Theorem 1).

We first prove the closed form of and the recursive form of . Because , it is easy to see that

which is the closed form of . For the recursive form, a direct computation shows that

For the identifiability, we use the proof by induction. We will show that each is identifiable so is identifiable. Since , it is immediately identifiable. For with , they only have one parent: so is identifiable.

Now we assume that is identifiable for all , and we consider a pattern such that . We will show that is also identifiable. By the recursive form,

Assumption (G2) implies that any must satisfies so . The assumption of induction implies that is identifiable. Thus, both and are identifiable, which implies that is identifiable. By induction, is identifiable for all and is identifiable.

Proof K.21 ( of Proposition 3).

Recall from Theorem 1 that

so proving equation (23) is equivalent to proving

| (24) |

We prove this by induction from . It is easy to see that when and , this result holds.

We now assume that the statement holds for any pattern with . Consider the pattern such that . By induction and assumption (G2), any parent pattern of must satisfy equation (24).

Due to the construction of a path (from to ), any path can be written as

where for some except for the case where . Suppose that , then there is only one path that corresponds to the parent pattern being , and this path contributes in the right-hand-sided of equation (24) the amount of . With the above insight, we can rewrite the right-hand-side of equation (24) as

Proof K.22 ( of Theorem 3).

We prove this by induction from patterns with . We first prove that it identifies the joint distribution . The case of is trivially true since everything is identifiable under this case.

For , they only have one parent and recall from equation (5),

This implies

Clearly, is identifiable so is identifiable.

Now we assume that is identifiable for all and consider a pattern with . Equation (5) implies that the extrapolation density

| (25) | ||||

Since is a parent of , condition (G2) implies that so is identifiable. Also, by the assumption of induction, is identifiable for Thus, is identifiable, which proves the result.

Since equation (5) only places conditions on the extrapolation densities, it is easy to see that the resulting full-data distribution is nonparametrically identifiable.

Proof K.23 ( of Theorem 4).

This proof consists of a sequence of “if and only if” statements. We start with the selection odds model:

The left-hand-side equals whereas the right-hand-side equals . So the selection odds model is equivalent to

which is what the pattern mixture model factorization refers to.

Before proceeding to the proof of Theorem 5, we introduce some notations from the empirical process theory. For a function , we write

and the empirical version of it

Although may not be fully observed when , the indicator function has an appealing feature that

so the IPW estimator can be written as

where . Note that when the model is correct, the parameter of interest

where is true parameter value.

Proof K.24 ( of Theorem 5).

Using the notation of the empirical process, we can rewrite the difference as

Thus, we only need to show that both (I) and (II) have asymptotic normality. Note that formally we need to show that the asymptotic correlation between (I) and (II) is not -1, but this is clearly the case so we ignore this step. We analyze (I) and (II) separately.

Part (I): The asymptotic normality is based on Theorem 19.24 of van der Vaart (1998) that this quantity is asymptotically the same as the case if we replace by when we have the following:

-

(C1)

and

-

(C2)

the class is a Donsker class.

Thus, we will show both conditions in this proof.

Condition (C1). A direct computation shows that

Thus,

where is the number of elements in and is some constant. So a sufficient condition to (C1) is

| (26) |

for each .

From the likelihood condition (L2), we have . Namely, we have the desired weighted convergence result of . To convert this into , we use the proof by induction. It is easy to see that when , this holds trivially because . Suppose for a pattern , the convergence holds for all its parents , i.e.,

for all . By Theorem 1,

Quantity : The boundedness assumption of in (L1) implies that for some constant so is uniformly bounded. As a result,

by assumption (L2).

Quantity : Assumption (L1) implies that is uniformly bounded so

by the induction assumption and are some constant.

Therefore, both and converges in the weighted sense, which implies that

so condition (C1) holds.

Condition (C2). The derivation of this property follows from a similar idea as condition (C1) that we start with and then and finally . The Donsker class follows because is a uniformly bounded Donsker class. The multiplication of uniformly bounded Donsker class is still a Donsker class (see, e.g., Example 2.10.8 of van der Vaart and Wellner 1996). Thus, the class is a uniformly bounded Donsker class.

By Theorem 1, so , which implies that is a Donsker class. So condition (C2) holds.

With condition (C1) and (C2), applying Theorem 19.24 of van der Vaart (1998) shows that the quantity (I) has asymptotic normality.

Part (II): Using the fact that , we can rewrite as

Thus, quantity (II) becomes

Thus, we only need to show that this quantity is either or has an asymptotic normality for each pattern (and at least one of them is non-zero).

Clearly, when , this quantity is 0 so we move onto the next case. For being a pattern with only one variable missing, we have , which leads to

Applying the Taylor expansion of with respect to , assumption (L4) implies that

where is the derivative with respect to . It has asymptotic normality due to assumption (L2). Note that the variance is finite because of the boundedness assumption (L1). Using the induction, one can show that for a pattern , if its parents have either asymptotic normality or equals to (but not all ), we have asymptotic normality of . Thus, the quantity in (II) converges to a normal distribution after rescaling.

Since both (I) and (II) both have asymptotic normality, also has asymptotic normality by the continuous mapping theorem, which completes the proof.

Proof K.25 ( of Theorem 6).

This proof utilizes tools from empirical process theory that are similar to the proof of Theorem 5. Let and be the empirical and probability measures of variable and pattern , respectively.

The regression adjustment estimator can be written as

where

A population version of the above quantity is

It is easy to see that the parameter of interest . Thus, if we can show that

| (27) |

for each , we have completed the proof (by the continuous mapping theorem).

To start with, we decompose the difference

Analysis of (I). By Theorem 19.24 of van der Vaart (1998) and condition (R2) and the first equality of (R3),

which has asymptotic normality.

Analysis of (II). Recall that . Using Tayloy expansion of , we can rewrite (II) as

due to the assumption on the boundedness of derivatives of and the rate of in (R3). The asymptotic normality assumption of implies the asymptotic normality of (II).

Thus, both (I) and (II) are asymptotically normal so we have the asymptotic normality of via the continuous mapping theorem, i.e., equation (27), which implies the desired result.

Proof K.26 ( of Theorem 7).

Let be a path of pattern . For a pathwise effect , it equals to

Let be the correct model, and we consider a pathwise perturbation such that satisfies .

Under the correct model , the effect is . Under the model , the effect is .

By the semi-parametric theory (see, e.g., Section 25.3 of van der Vaart 1998), the EIF is a function such that and

| (28) |

So we just need to find the proper expression of .

Our strategy is very simple. We compute and keep those terms involving the first order of and ignore anything involving since the higher-order terms varnish in the above limit.

Under the model , we have perturbed quantities and . We denote

A direct computation shows that

| (29) | ||||

Clearly, part is already in the form of an EIF so we focus on derivations of part .

Part has several components, and we can write it as

We expand the difference :

Thus, we can further write as

| (30) | ||||

Now going back to , note that we can decompose

The first part involving terms in while the second part is fixed when . Thus, we can rewrite as

Now recall that from equation (11), which appears in the first term. This, together with equation (30), implies

Comparing this expression to equation (28), we conclude that

is the EIF from and is what appears in equation (9).

Recall equation (29) that , so the EIF of the entire path is the EIF from term and the EIF of each node in , leading to

Finally, the constraint implies that we can add/subtract any constant to without affecting the fact that it satisfies equation (28). To make it the EIF, we need its mean to be . One can easily show that , so the EIF of is

and the EIF of is , which completes the proof.

Proof K.27 ( of Proposition 8).

Part 1: identification. Using the fact that

the regression function we want to identify can be decomposed as

We can always write

which is identifiable from and is a subset of (ancestors of ) when . Thus, the above equation shows that can be identifiable from

Part 2: the equality .

Part 3: the ancestor expression. The key to this proof is the following observation. For any path and a pattern , the pair can be uniquely expressed as a pattern and a path containing . Namely,

| (31) |

In the expression of right-handed-side, for a fixed , we are thinking of paths containing so any path with this property can be written in the following form:

so it can be decomposed as , and the second part (recall that is the collection of all paths from to ). Moreover, one can easily see that for each ,

| (32) |

Recall that the path-specific EIF is

and the function

One may notice that the regression function only depends on the first part of the path and is independent of the second part and

with .

Proof K.28 ( of Theorem 9).

For simplicity, we write and . Also, for abbreviatioon, we set .

Consider a pattern . It is easy to see that when is correctly specified (),

| (34) | ||||

This holds regardless of other selection odds or regression function being correct or not.

Thus, when all selection odds are correctly specified, clearly

So we consider the case where some selection odds are incorrectly specified, but the regression function is incorrectly specified.

Case 1: One selection odds is incorrectly specified. Suppose that we have only one an incorrect model for a selection odds of pattern , but all other selection odds are correct and the regression function is also correct. In this case, the quantity becomes

where

| (35) |

By equation (34), the last part has mean (correctly specified EIFs) so we obtain

So we just need to prove that the above quantity is .

For part (A), a direct computation shows that

| (36) | ||||

For the EIF part, its expectation is

The second component of is identical to in equation (36), so the summation leads to

Thus, when the selection odds of pattern is incorrectly specified, as long as the regression function is correctly specified, we still recover the true parameter.

Case 2: Two or more selection odds are incorrectly specified. We prove the case when there are two patterns that are both mis-specified. The case of more selection odds being mis-specified can be proved in a similar way. In this case, we use two incorrect selection odds and , but the corresponding regression function and are correct. In this case, becomes

Similar to the case of one selection odds being mis-specified, the component has mean so we can ignore it. So we only need to focus on the mean of term (C) and . Because of , does not involve so it is the same as equation (35). However, term involves , and it is

Using a similar derivation as in equation (36), we have

Now we compute the expectation of . Using the law of total expectation that we condition on first, one can show that

Again, the second term in the above equality (the one involving ) is identical to . So we conclude that

which is the same result as in equation (36) with replacing by . Thus, the problem reduces to Case 1: only one selection odds is mis-specified. By applying the analysis of Case 1, we conclude that

One can adapt this procedure to any number of selection odds being mis-specified. As long as the corresponding regression function is correctly specified, we recover the same pathwise effect . Thus, we conclude that for all , as long as or ,

which completes the proof.

Proof K.29 ( of Theorem 10).

The proof consists of several “if and only if” statements:

Now using the fact that

the above if and only if statement becomes

which completes the proof.

Proof K.30 ( of Proposition 11).

In non-monotone case, there are distinct missing patterns with missing variables. For a pattern with variables missing, there are totally patterns in the set that can be a parent of . Any non-empty subsets of can be a parent of so there is a total of possible parent sets of pattern .

To specify an identifying restriction, we need to specify every parent pattern, and a parent set must be a subset of . Because parent sets of different patterns can be specified independently, so the total number is

Proof K.31 ( of Proposition 12).

Case of . We first prove

and then prove the other way around. Apparently, we only add one arrow so holds. Similarly, since we are adding edges, . Also, it is straightforward that the new graph also satisfies (G1-2) so this inclusion holds.

We now turn to showing that

and implies that has one additional edge compared to . Let be the newly added arrow. Since has to satisfies (G2), it must satisfy condition and . Thus, the inclusion condition holds so the two sets are the same.

Case of . We first prove

and then derive the other direction later. Apparently, we are removing one edge so conditions and hold automatically. Also, since we are deleting an edge, the partial ordering condition (G2) holds for . All we need is to show that the resulting graph still has the unique source (condition (G1)). Because we are deleting an arrow with , so the node still has parents. Thus, this will not create any new source and the condition (G1) holds, which proves this inclusion direction.

Now we prove

Conditions and implies that we are deleting one edge so for some . Thus, we only need to show that we can only delete this edge if . Note that condition (G2) holds for the new graph so they do not provide any additional constraint. The only constraint we have is condition (G1)–we need to make sure that the deletion will not create a new source.