Understanding Global Feature Contributions With Additive Importance Measures

Abstract

Understanding the inner workings of complex machine learning models is a long-standing problem and most recent research has focused on local interpretability. To assess the role of individual input features in a global sense, we explore the perspective of defining feature importance through the predictive power associated with each feature. We introduce two notions of predictive power (model-based and universal) and formalize this approach with a framework of additive importance measures, which unifies numerous methods in the literature. We then propose SAGE, a model-agnostic method that quantifies predictive power while accounting for feature interactions. Our experiments show that SAGE can be calculated efficiently and that it assigns more accurate importance values than other methods.

1 Introduction

Our limited understanding of the inner workings of complex models is a long-standing problem that impedes machine learning adoption in many domains. Most recent research has addressed this by focusing on local interpretability, which explains a model’s individual predictions (e.g., the role of each feature in a patient’s diagnosis) [27, 32, 36, 40]. However, in some cases users require knowledge of a feature’s global importance to understand its role across an entire dataset.

In this work we seek to understand how much models rely on each feature overall, which is often referred to as the problem of global feature importance. The problem is open to many interpretations [5, 17, 24, 26, 29], and we present the idea of defining feature importance as the amount of predictive power that a feature contributes. This raises the challenge of handling feature interactions, because features contribute different amounts of information when introduced in isolation versus into a larger set of features. We aim to provide a solution that accounts for these complex interactions.

We begin by presenting the framework of additive importance measures, a view that unifies numerous methods that define feature importance in terms of predictive power (Section 2). We then present a new tool for calculating feature importance, SAGE,111http://github.com/iancovert/sage/ a model-agnostic approach to summarizing a model’s dependence on each feature while accounting for complex interactions (Section 3). Our work makes the following contributions:

-

1.

We derive SAGE by applying the Shapley value to a function that represents the predictive power contained in subsets of features. Many desirable properties result from this approach, including invariance to invertible feature transformations and a relationship with SHAP [27].

-

2.

We introduce a framework of additive importance measures that lets us unify many existing methods in the literature. We show that these methods all define feature importance in terms of predictive power, but that only SAGE does so while properly accounting for feature interactions.

-

3.

To manage tractability challenges with SAGE, we propose an efficient sampling-based approximation that is significantly faster than a naive calculation via local SHAP values. Our approach also provides uncertainty estimates and permits automatic convergence detection.

Our experiments compare SAGE to several baselines and demonstrate that SAGE’s feature importance values are more representative of the predictive power associated with each feature. We also show that when a model’s performance is unexpectedly poor, SAGE can help identify corrupted features.

2 Unifying Global Feature Importance Methods

We introduce two notions of predictive power for subsets of features and then discuss our unifying framework of additive importance measures.

2.1 Predictive Power of Feature Subsets

Consider a supervised learning task where a model is used to predict the response variable given an input , where consists of individual features . We use uppercase symbols (e.g., ) to denote random variables and lowercase symbols (e.g., ) to denote values.

The notion of feature importance is open to different interpretations, but we take the perspective that a feature’s importance should correspond to how much predictive power it provides to the model. Although is trained using all the features, we can examine its performance when it is given access to subsets of features for different , where . We can then define “important” features as those whose absence degrades ’s performance. As a convention for evaluating when deprived of the features , we define the restricted model as

| (1) |

so that missing features are marginalized out using the conditional distribution . Two special cases are and , which respectively correspond to the mean prediction and the full model prediction . This approach is common in recent work [1, 27] and is necessary for later connections with mutual information (Supplement A).

Using this convention for accommodating subsets of features, we can now measure how much ’s performance degrades when features are removed. Given a loss function , the population risk for is defined as where the expectation is taken over the data distribution . To define predictive power as a quantity that increases with model accuracy, we consider the reduction in risk over the mean prediction and define the function as follows:

| (2) |

The domain is the power set , the left term is the loss achieved with the mean prediction , and the right term is the loss achieved using the features . The function quantifies the amount of predictive power derives from the features , and we generally expect that including more features in will make larger. While provides a model-based notion of predictive power, we also introduce a notion of universal predictive power. For this, we define the function as the reduction in risk from when using an optimal model:

| (3) |

The left term is the loss from an optimal constant prediction and the right term is the loss for an optimal model from the class of all functions (e.g., the Bayes classifier). Intuitively, represents the maximum predictive power that could hypothetically be derived from . Since is typically trained using empirical risk minimization [42], the model-based predictive power provides an approximation to and the two coincide in certain cases where is optimal (Supplement B).

2.2 Additive Importance Measures

In certain very simple cases, features contribute predictive power in an additive manner. This means that we have for all subsets such that . In these situations, we can define ’s importance as the predictive power it contributes, or . However, a feature’s contribution is generally not additive because it depends on which features are already present.

We therefore propose a class of additive importance measures that includes any method whose scores can be understood as performance gains associated with each feature. This framework lets us unify numerous methods that either explicitly or implicitly define feature importance in terms of predictive power. The class of methods is defined as follows.

Definition 1.

Additive importance measures are methods that assign importance scores to features and for which there exists a constant so that the additive function

provides a proxy for the predictive power of feature subsets, i.e., .

For methods in this class, approximates up to a constant value by summing the values for each included feature . Each can be viewed as the performance gain associated with , which provides a measure of its importance for the prediction task. Although our definition focuses on methods that approximate the universal predictive power , we also include methods that approximate model-based predictive power because these implicitly approximate .

The function exhibits non-additive behavior for most prediction problems, so the proxy often cannot perfectly represent each feature’s contribution to the predictive power. Although a crude approximation may provide users with some insight, closer approximations give a more accurate sense of each feature’s importance. Next, we show that several existing methods manage this challenge by providing high quality approximations in specific regions of the domain .

2.3 Existing Additive Importance Measures

Our framework of additive importance measures unifies numerous methods in the feature importance literature. These methods can be divided into three categories, representing the parts of the domain in which the additive proxy models or most accurately. Supplement G provides a table that summarizes the methods in each category.

The first category of methods characterize predictive power when no more than one feature is excluded, and they provide an additive function that accurately approximates or in the subdomain . The canonical method for this is a feature ablation study where, in addition to a model trained on all features, separate models are trained with individual features excluded [2, 16, 22]. Importance values are then assigned based on the degradation in performance, according to the formula

| (4) |

A natural choice for in this case is , because then and approximate and , respectively.

Several other methods provide similar notions of feature importance using a single model . Permutation tests measure performance degradation when each column of the data is permuted [5]. Since permutation tests break feature dependencies, one variation suggests using a conditional permutation scheme [38]. Finally, in a method we refer to as “mean importance,” performance degradation is measured after mean imputing individual features [34]. Although these methods take slightly different approaches, they all approximate either or when at most one feature is excluded.

The second category of methods describe when no more than one feature is included, providing an additive function that accurately describes in the subdomain . Methods in this category model the bivariate association between and to quantify ’s stand-alone predictive power. Bivariate association is commonly studied in fields such as computational biology (e.g., [25]) and is widely used to identify sensitive features [33]. As an example, the squared correlation is equivalent to the variance explained by a univariate linear model. More generally, one can measure the performance of univariate models trained to predict given [14]. Given a model for each feature , the importance values are calculated with the formula

| (5) |

A natural choice for the constant is in this case, because with these scores we see that and that approximates .

The two previous categories of methods provide imperfect notions of feature importance because they do not account for feature interactions. For example, two perfectly correlated features with significant predictive power would both be deemed unimportant by a feature ablation study, and two complementary features would have their importance underestimated by univariate models. The third category of methods addresses these issues by considering all feature subsets .

Methods in the third category account for complex feature interactions by modeling across its entire domain . These methods therefore supersede the two other categories, which either exclude or include individual features. Our method, SAGE, belongs to this category, and we show that SAGE assigns scores by modeling optimally via a weighted least squares objective (Section 3.2).

3 Shapley Additive Global Importance

We now introduce our method, Shapley additive global importance (SAGE), for quantifying a model’s dependence on each feature. We present SAGE as an application of the game-theoretic Shapley value to and then examine its properties, including how it can be understood as an additive importance measure. Finally, we propose a practical sampling-based approximation algorithm.

3.1 Shapley Values for Credit Allocation

Recall that the function describes the amount of predictive power that a model derives from subsets of features . We define feature importance via to quantify how critical each feature is for to make accurate predictions. It is natural to view as a cooperative game, representing the profit (predictive power) when each player (feature) participates (is available to the model). Research in game theory has extensively analyzed credit allocation for cooperative games, so we apply a game theoretic solution known as the Shapley value [35].

Shapley values are the unique credit allocation scheme that satisfies a set of fairness axioms. For any cooperative game (such as or ) we may want the scores assigned to each player to satisfy the following desirable properties:

-

1.

(Efficiency) They sum to the total improvement over the empty set, .

-

2.

(Symmetry) If two players always make equal contributions, or for all , then .

-

3.

(Dummy) If a player makes zero contribution, or for all , then .

-

4.

(Monotonicity) If for two games and a player always make greater contributions to than , or for all , then .

-

5.

(Linearity) The game , which is a linear combination of multiple games , has scores given by .

The Shapley values are the unique credit allocation scheme that satisfies properties 1-5 [35], and they are given by the expression:

| (6) |

The expression above shows that each Shapley value is a weighted average of the incremental changes from adding to subsets . For SAGE, we propose assigning feature importance using the Shapley values of our model-based predictive power, or for , which we refer to as SAGE values.

SAGE values satisfy many intuitive and desirable properties, arising both from the properties of Shapley values and from how is defined. These properties include:

-

1.

Due to the efficiency property, SAGE values sum to ’s total predictive power. In other words, we have .

-

2.

Due to the symmetry property, pairs of features with a deterministic relationship (e.g., perfect correlation) always have equal importance. To see this, remark that for all , so that .

-

3.

Due to the dummy property, we have if is conditionally independent of given all possible subsets of features . However, features may receive non-zero importance even if they are not used by (which in some cases may be desirable).

-

4.

Due to the monotonicity property, if we have two response variables with models and we have for all , so that contributes more predictive power for than for , then the SAGE values satisfy .

-

5.

Due to the linearity property, SAGE values are the expectation of per-instance SHAP values applied to the model loss [26]. By this, we mean the Shapley values of the game

In other words, the SAGE values are given by . These values were used in prior work, but they were not analyzed in depth and are costly to calculate via many local explanations [26].

-

6.

Due to our definition of , SAGE values are invariant to invertible mappings of the features. More precisely, if we apply an invertible function to a feature and define , and we then use a model that applies the inverse to before , then the SAGE values of the new model under the new data distribution are unchanged. For example, SAGE values do not depend on whether a model uses gene counts or log gene counts.

Finally, SAGE values have an elegant interpretation when the loss function is cross entropy or mean squared error (MSE) and the model is optimal. With cross entropy loss, the optimal model (the Bayes classifier) predicts the conditional distribution and the predictive power is , where denotes mutual information. The SAGE values are then given by:

| (7) |

The expression above represents a weighted average of the conditional mutual information, i.e., the reduction in uncertainty for when incorporating into different subsets . An analogous result arises in the MSE case, and in both cases the SAGE values satisfy (Supplement C). Through this we see that although SAGE is a tool for model interpretation, it can also provide insight into intrinsic relationships in the data when applied with optimal models.

3.2 SAGE as an Additive Importance Measure

Though it not immediately obvious, SAGE is an additive importance measure (Section 2). Prior work has shown that Shapley values (Eq. 6) can be understood as the solution to a weighted least squares problem [6, 27]. From these findings, we see that SAGE provides an additive approximation to with , where are optimal coefficients for the following problem:

| (8) |

Understanding SAGE values in this way reveals that SAGE attempts to represent across its entire domain, modeling it optimally in a weighted least squares sense. Although the weights are perhaps not intuitive, this is the unique weighting scheme that leads to SAGE’s desirable properties.

Using this interpretation of Shapley values, we observe that two more existing methods can be categorized as additive importance measures. The mean SHAP value of the loss [26] and Shapley Net Effects for linear models [24] are both similar to SAGE, but they involve more expensive calculations (explaining every individual prediction, or fitting an exponential number of linear models).

3.3 Practical SAGE Approximation

We now consider how to calculate SAGE values efficiently. Obtaining these values is challenging because (i) there are an exponential number of subsets and (ii) evaluating a restricted model requires a Monte Carlo estimate with sampled from . Like previous methods that use Shapley values, we sidestep the inherent exponential complexity using an approximation algorithm [9, 20, 27, 39].

We address the first challenge by sampling random subsets of features , and the second by sampling from its marginal distribution. To efficiently generate subsets of features from the appropriate distribution, we enumerate over random permutations of the indices , similar to Štrumbelj and Kononenko [20]. Prior work has used sampling from the marginal distribution in a similar manner [27], but doing so alters some of SAGE’s properties to align less with the information value of each feature and more with the model’s mechanism. Supplement D describes the SAGE sampling algorithm (Algorithm 1) and the changes to its properties in more detail.

In Theorems 1 and 2, we make two claims regarding the estimates from our sampling algorithm (with proofs provided in Supplement E). The first result shows that the estimates converge to the correct values when run under appropriate conditions, and the second result shows that the estimates have variance that reduces at a linear rate.

Theorem 1.

The SAGE value estimates from Algorithm 1 converge to the correct values when run with , , with an arbitrarily large dataset , and with sampling from the correct conditional distribution .

Theorem 2.

The SAGE value estimates from Algorithm 1 have variance that reduces at the rate of .

In practice the algorithm must run for a finite number of iterations, so we propose an approach to monitor the estimates’ uncertainty and detect convergence. Theorem 2 implies that for each feature there exists a constant such that the estimate after iterations has variance given by . This quantity can be estimated while running the sampling algorithm and can then be used to provide confidence intervals on the estimated values. Finally, the algorithm may be considered converged when the largest standard deviation is a sufficiently low proportion (e.g., ) of the range in the estimated values, or when the following criterion is satisfied:

| Method | Agnostic | Performance | Interactions | Missingness | Tractable |

| Linear Model Coeff. Size | ✓ | ||||

| Gini Importance | ✓ | ||||

| Number of Splits | ✓ | ||||

| Neural Network Weights | ✓ | ||||

| Aggregated Local Saliency | ✓ | ||||

| Mean Abs. SHAP | ✓ | ✓ | |||

| Feature Ablation | ✓ | ✓ | ✓ | ||

| Permutation Test | ✓ | ✓ | ✓ | ||

| Conditional Permutation Test | ✓ | ✓ | ✓ | ✓ | |

| Mean Importance | ✓ | ✓ | ✓ | ||

| Univariate Predictors | ✓ | ✓ | ✓ | ||

| Squared Correlation | ✓ | ✓ | ✓ | ||

| Shapley Net Effects | ✓ | ✓ | ✓ | ||

| Mean Loss SHAP | ✓ | ✓ | ✓ | ||

| SAGE | ✓ | ✓ | ✓ |

4 Related Work

Section 2 described prior work that was unified under the framework of additive importance measures, but there are also methods that do not fit into our framework. These are often model-specific heuristics that do not directly relate to the predictive power associated with each feature. For linear models, one heuristic is the magnitude of model coefficients [15]. For tree-based models, options include Gini importance and counting splits based on each feature [12]. And for neural networks, one can examine the magnitude of weights or aggregate local explanations [17], such as integrated gradients [40].

Shapley values have been studied extensively in game theory [35] and have been applied to machine learning for both local [7, 9, 27, 39] and global interpretability. For global interpretability, Shapley Net Effects proposed training linear models with every combination of features [24], which is similar to SAGE but often impractical due to the need for model retraining. Some work has considered applying Shapley values to function sensitivity, which is a subtly different problem than explaining the performance of machine learning models (Supplement F) [3, 29, 30, 37].

SHAP is a well-known method for local interpretability, but it has only been applied heuristically to global importance by calculating the mean absolute attribution value [27] and by using SHAP on the model loss rather than the model output [26]. SAGE draws a connection between global and local SHAP interpretability (Section 3.1), and our approach can converge hundreds or thousands of times faster than a naive calculation via SHAP because it avoids explaining individual instances in the dataset (Section 5).

5 Experiments

We now evaluate SAGE by comparing it with several baseline methods. For simplicity we only consider model-agnostic baselines, including permutation tests, mean importance, feature ablation and univariate predictors (see Section 2.3). For datasets, we used MNIST [21], a bike sharing demand dataset [10], the German credit quality dataset [23], the Portuguese bank marketing dataset [28], and a breast cancer (BRCA) subtype classification dataset [4, 41]. We used XGBoost [8] for the bike data, CatBoost [31] for the bank and credit data, regularized logistic regression for the BRCA data, and a multi-layer perceptron (MLP) for MNIST. Supplement H provides more information about each dataset, including how we selected a subset of genes to avoid overfitting with the BRCA data.

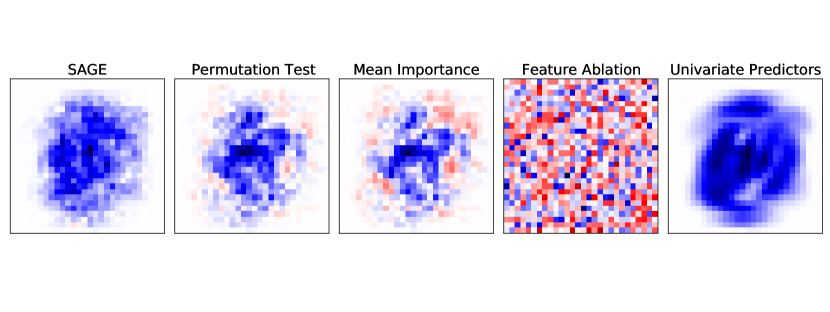

Figure 1 shows examples of global explanations generated for MNIST and BRCA. For MNIST, most methods correctly assign high importance to the central region, but permutation tests and mean importance assign noisy scores with negative importance for many pixels in the central region. Feature ablation provides meaningless scores because removing individual features has a negligible impact on retrained models. SAGE and the univariate predictors approach provide the most plausible explanations, but their differences should be analyzed using quantitative metrics (see below).

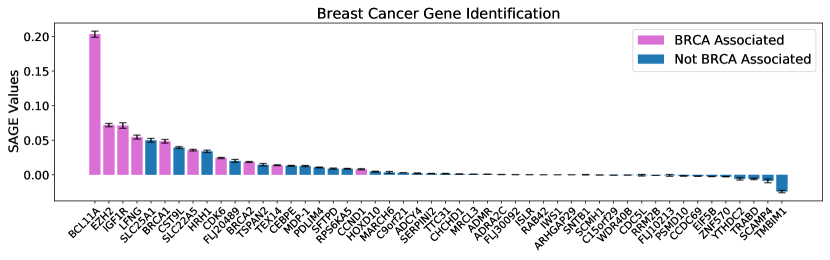

The BRCA explanation (Figure 1 bottom) shows that genes previously known to be associated with BRCA receive the highest SAGE values. The most important gene (BCL11A) has a known association with a particularly aggressive form of BRCA [19], and the BRCA1 and BRCA2 genes are also highly ranked. Among the genes not associated with BRCA, the most highly ranked gene (SLC25A1) has a documented association with lung cancer [11].

We can also compare methods through quantitative metrics. As a first experiment, we seek to measure whether the sum of a method’s importance scores is a reliable proxy for the predictive power of subsets of features. We generated several thousand feature subsets for each dataset, re-trained models for each subset, and then measured the correlation between the model loss and the total importance of the included features. Table 2 displays the results, which show that SAGE is either the best or nearly best for all datasets. Feature ablation fails for datasets with moderate numbers of features (BRCA and MNIST), but permutation tests and univariate predictors are both sometimes competitive.

| Bank Marketing | Bike Demand | Credit Quality | BRCA | MNIST | |

|---|---|---|---|---|---|

| Permutation Test | 0.9918 | 0.9798 | 0.9571 | 0.8581 | 0.4855 |

| Mean Importance | – | 0.9798 | – | 0.8490 | 0.4824 |

| Feature Ablation | 0.9779 | 0.9651 | 0.2621 | -0.0371 | -0.4536 |

| Univariate | 0.9666 | 0.9587 | 0.9542 | 0.8718 | 0.4865 |

| SAGE | 0.9937 | 0.9815 | 0.9565 | 0.8611 | 0.4868 |

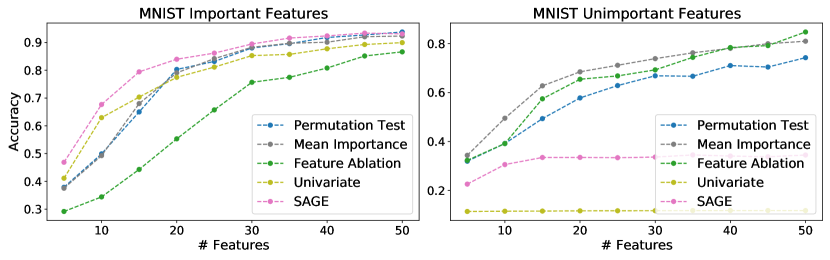

As another metric, we compared the predictive power of the highest and lowest ranked features according to each method. Figure 2 displays feature selection results on MNIST, where models are re-trained using the most (least) important features in the hopes of achieving high (low) accuracy. The results show that SAGE is most effective at identifying important features while univariate predictors are best for identifying unimportant features. Interestingly, most baselines fail to identify features with no predictive power (Figure 2 right), while SAGE performs well at both tasks.

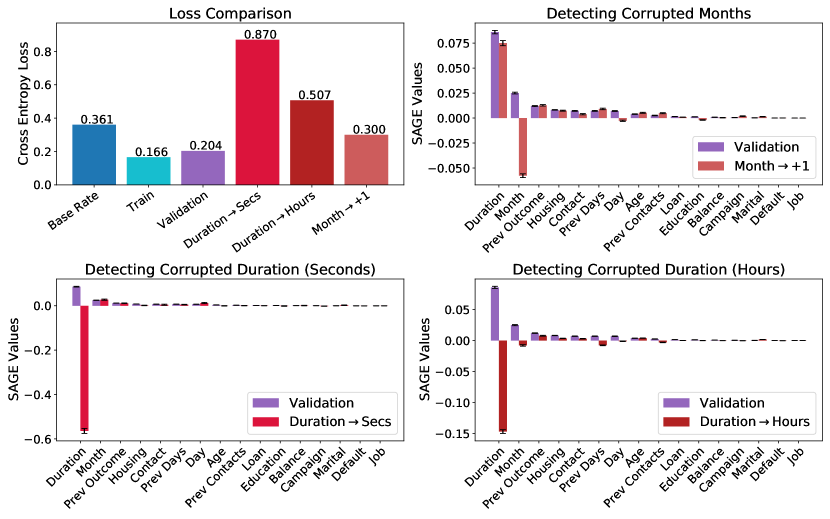

Our experiments have focused thus far on accurate models, but SAGE can also be used to understand sub-optimal models. In a model monitoring context, SAGE can identify features that are corrupted or incorrectly encoded. Figure 3 shows an example where SAGE values are compared across several versions of the bank marketing dataset, including three test sets where the model accuracy decreased because a single feature is encoded inconsistently. When the month feature is incremented by one, the corresponding SAGE value is much lower than in the validation split; and when the call duration is no longer encoded in minutes, the corresponding SAGE values makes this change apparent.

From a computational perspective, our sampling algorithm (Section 3.3) is significantly faster than a naive calculation via local SHAP values. Our approach aims directly at a global explanation, whereas with SHAP one must generate and then average local explanations for hundreds or thousands of examples. We found that the indirect approach using SHAP required 2-4 orders of magnitude more model evaluations to calculate the same values, which roughly corresponds to the dataset size (see Supplement H for details). This shows that SAGE is much faster for providing global explanations.

6 Conclusion

In this work we presented a unifying framework for global feature importance methods, as well as a new model-agnostic approach (SAGE) that accounts for complex feature interactions. Our perspective of quantifying predictive power shows that numerous existing methods make trade-offs regarding how to handle feature interactions; revealing each method’s implicit assumptions allows users to reason explicitly about which tools to use. The method we introduced satisfies numerous desirable properties, and because of the sampling approach we propose, SAGE values can be calculated orders of magnitude faster than with a naive calculation via SHAP values. Future work will focus on estimating SAGE values even more efficiently and providing approximations that better model the conditional distribution of held out features.

Broader Impact

This work contributes to a growing literature of methods that can provide researchers, engineers, and users with an understanding of how machine learning models work. By focusing on global explanations, our method produces succinct insights that the target audience may find more digestible than a large number of local explanations. Our work aims to contribute positive social impact, but as with any model explanation tool, there is a danger of deliberate misuse or adversarial use that could provide misleading information or be used to gain approval for bad practices.

Acknowledgments and Disclosure of Funding

This work was funded by the National Science Foundation [CAREER DBI-1552309, and DBI-1759487]; the American Cancer Society [127332-RSG-15-097-01-TBG]; and the National Institutes of Health [R35 GM 128638, and R01 NIA AG 061132]. We would like to thank members of the Lee Lab and NeurIPS reviewers for feedback that greatly improved this work.

Appendix A Convention for Handling Missing Features

To examine how a model performs when deprived of certain information, we require a convention for evaluating with arbitrary subsets of features . For this, we defined the restricted model as

Although we use an approximation in practice (Section 3.3), we have several reasons for defining SAGE using this convention. The reasons are: (i) the model is as close as possible to the full model , (ii) the convention yields connections with intrinsic properties of the data distribution (such as mutual information), and (iii) alternative conventions often involve evaluating the model off the manifold of real data examples. We explain these points in detail below.

Consider how we can measure the deviation between a model on all features and a model on a subset of features . We consider this separately for regression tasks and classification tasks. For a regression model that makes prediction in , a natural way to determine how much its prediction given differs from that of given is with the squared Euclidean distance . In expectation, the squared deviation between and is equal to:

From this, it is clear that the model deviates least from on average.

Next, consider a classification model that outputs probabilities for a -class categorical variable. To be explicit that the prediction is a vector of probabilities, we denote the model output as , where we have for and . The Kullback-Leibler (KL) divergence is a natural way to measure the deviation of the predictions from and . The mean deviation between and can then be expressed as:

With this way of rewriting the mean KL divergence, it becomes clear that the model is closest to in expectation.

These derivations show that in both cases, our convention for (marginalizing out features using their conditional distribution) yields the model that is closest to on average. When analyzing the performance degradation when is deprived of certain features, it is most conservative to use a restricted model that is as faithful to as possible, because doing otherwise may result in inflated estimates of the impact on model performance.

Next, handling missing features with yields connections with intrinsic properties of the data distribution, such as mutual information and conditional variance (Section C). That happens because when our convention is applied to an optimal model (e.g., the Bayes classifier), it preserves the model’s optimality. For example, the Bayes classifier becomes the Bayes classifier , and the conditional expectation becomes the conditional expectation . Our definition of is the unique convention that has this property.

Finally, the convention only considers values of such that has support under the full data distribution . That property is a benefit of handling missing features using their conditional distribution . By contrast, other conventions may lead to implausible feature combinations with no support under the data distribution.

As an example, one alternative is to use the marginal distribution:

This is what we do in practice (Section 3.3), but this breaks feature dependencies and may result in combinations of values that are off-manifold (e.g., if there are two perfectly correlated features and one is removed). We view this as an undesirable property and encourage work that removes the need for this approximation in practice.

Another option is to use the mean prediction when the missing features are drawn from the product of their marginal distributions, as in QII [9]. This convention is even more likely to result in off-manifold examples, because in addition to breaking dependencies between and , it also breaks dependencies within .

Appendix B Model-Based and Universal Predictive Power

In the main text, we introduce two set functions to represent different notions of predictive power. The function represents the universal predictive power and quantifies the amount of signal that can hypothetically be derived from a set of features :

In contrast, the function represents a model-based notion of predictive power and quantifies how much signal derives from a given set of features:

The two quantities are different but related. To estimate , a natural approach would be to train a model using , learn the optimal constant prediction , and then use the performance of those models as plug-in estimators for the two terms in . The model-based predictive power can be viewed as an single-model approximation to this, where, instead of training a model from scratch on , we obtain the model via an existing model trained using all features.

Under certain circumstances when the model is optimal, we can see that and coincide exactly for all . Two simple cases where this holds are (i) for a regression task that uses the conditional expectation and mean squared error (MSE) loss, and (ii) for a classification task that uses the Bayes classifier and cross entropy loss. We show equality in the first case as follows:

Similarly, we show equality in the second case as follows:

Besides these two cases, equality between and holds for optimal models when using a specific class of loss function— loss functions that satisfy the property that an optimal model for yields an optimal model for . For example, this property holds for all strictly proper scoring rules, because optimal models under these loss functions are probabilistic forecasts [13]

Appendix C SAGE Properties with Optimal Models

C.1 Properties with Bayes Classifier

Here, we derive the properties of SAGE when it is applied to the Bayes classifier with cross entropy loss. We derive the claim from scratch, beginning with a proof that the Bayes classifier is optimal. To be explicit that the prediction is a vector of probabilities, we denote the model output as , where we have for and . We also use to denote entropy and to denote mutual information.

For a classification model trained with cross entropy loss, we decompose the population risk as follows to reveal the optimal classifier:

The entropy term is constant, so the optimal prediction model is the Bayes classifier . We now consider the application of SAGE to the model . The restricted models are the following:

The risk incurred by the restricted model is then:

We can now see that the cooperative game is:

In the expression for Shapley values, the weighted summation has terms of the following form:

This completes the derivation for the result in the main text, because we see that the Shapley values are equal to

C.2 Properties with Conditional Expectation

We now show a similar result for optimal regression models when using mean squared error (MSE) loss. We assume that the predictions are scalars, although a similar result holds for vector-valued predictions. We first decompose the population risk to determine the optimal model:

Only the first term depends on , so it is clear that the conditional expectation function is optimal. We now consider the application of SAGE to the model . The restricted models are the following:

The last line follows from the law of iterated expectations. The risk incurred by the restricted model is then:

We now see that the cooperative game is:

The last line follows from the law of total variance. The difference terms in the Shapley summation are the following:

The last line also follows from the law of total variance. Intuitively, these terms quantify the average amount of variation left in the random variable when is unknown but distributed according to . If the amount of variation is high, then contains significant incremental information about . The above expression is analogous to from the classification case.

Finally, we see that the SAGE values are equal to

Appendix D SAGE Sampling

Here, we describe our sampling algorithm in greater detail and discuss the consequences of using the marginal rather than conditional distribution.

D.1 SAGE Sampling Algorithm

Our sampling approach is displayed below in Algorithm 1. In Algorithm 1, each feature’s score is estimated by attempting to average many samples of the form , or the incremental improvement in the loss when incorporating for a particular input-label pair . In each sample, we draw from the empirical data distribution, we determine based on a random permutation of feature indices , and we estimate via Monte Carlo approximation with a distribution substituted for .

One practical option for the distribution , which we use in our experiments, is to sample from the marginal distribution , which corresponds to an assumption of feature independence. Another option is to mean impute the missing features, which corresponds to a further assumption of model linearity [27].

D.2 Properties with Marginal Sampling

SAGE’s properties change when Algorithm 1 is run with sampling from the marginal distribution rather than the conditional distribution . Sampling from the marginal instead of the conditional changes the underlying cooperative game and means that we no longer estimate the Shapley values , but rather the Shapley values of a different game.

Sampling from the marginal distribution means that in the inner loop of Algorithm 1, the Monte Carlo approximation estimates . We adopt the notation to denote an alternative restricted model (instead of ):

We then adopt the notation to denote the new cooperative game using , which is

Sampling from the marginal distribution means that we estimate the Shapley values instead of . Some of the properties of the importance scores differ from those described in Section 3.1:

-

1.

Due to the efficiency property, the scores satisfy . Because we have and for all (i.e., the models are the same given either all features or no features), we also have .

-

2.

Due to the symmetry property, we have when for all . That holds if we have for all . Given our definition of , there is no simple sufficient condition for when this holds for . Unlike in the original formulation, perfectly correlated features may not receive equal importance.

-

3.

Due to the dummy property, we have if for all . A sufficient condition for this to hold is that the model is invariant to . That means that the value for a sensitive attribute (e.g., race) may be zero even if the model depends on correlated features (e.g., zip code).

-

4.

Due to the monotonicity property, if we have two response variables with models , and we have for all , then we have . This means that if contributes more predictive power to than to , then it receives more importance for .

-

5.

Due to the linearity property, the values are the expectation of per-instance loss SHAP values computed using the marginal distribution. If we define the game as

then we have . These are loss SHAP values computed with the same feature independence assumption [27].

-

6.

As in the original formulation, the values are invariant to invertible transformations of the features.

One elegant aspect of the original formulation of SAGE is a connection with intrinsic properties of the data distribution when applied with optimal models (e.g., the Bayes classifier). We lose these connections when using the marginal distribution because the restricted models based on optimal models are no longer optimal for . This formulation is therefore less aligned with the information value of each feature.

However, some recent work has advocated for advantages of sampling from the marginal distribution in SHAP [18]. The most appealing property is that features that are not used by the model always receive zero attribution, a property that we showed also holds for SAGE.

Appendix E Proofs

The two results from Section 3.3 of the main text are restated and proved below.

Theorem 1. The SAGE value estimates from Algorithm 1 converge to the correct values when run with , , with an arbitrarily large dataset , and with sampling from the correct conditional distribution .

Proof.

At a high level, the algorithm has an outer loop that contributes one sample to each of the SAGE value estimates . Each estimate can be interpreted as a sample mean that converges to its expectation as becomes large. Our proof proceeds by considering the value of the expectation under the assumptions that and .

Each estimate is the average of many samples of the random variable which we define here as

| (9) |

Specifically, we have

| (10) |

where are fixed and and are determined by each iteration of Algorithm 1. Even for fixed , note that is a random variable because each and are independent samples from the distributions and respectively. We begin by analyzing the random variable and what it converges to as .

Consider the first term in Eq. 9. The mean prediction provides a Monte Carlo approximation of

We assume that samples are from the true conditional distribution , so the average prediction is in fact an approximation of . When we let the law of large numbers says that

| (11) |

where denotes convergence in probability. By an identical argument for the second term in Eq. 9, because of sampling from , we see that

| (12) |

as . This lets us conclude that for fixed , converges as as follows:

| (13) |

With this result, we define . We now consider the fact that the final estimates are the average of many samples , or many samples in the limit . We will determine the expected value of and argue that it converges to this value as .

First, consider the distribution from which is implicitly drawn. In Algorithm 1, is determined by a permutation of the feature indices and it contains indices that are already included when we arrive at feature . The number of indices preceding is uniformly distributed between and , and the preceding indices are chosen uniformly at random among the possible combinations. We can therefore write a probability mass function for subsets that may be included by the time when is added:

| (14) |

When we take the expectation of over , we have

| (15) |

The expression above already resembles the Shapley value because of the weighted summation over subsets. We can now incorporate an expectation over pairs drawn from the data distribution and see that the Shapley value arises naturally:

| (16) |

Finally, we invoke the law of large numbers again to conclude that in the limit of an arbitrarily large dataset drawn from , we have the convergence result

| (17) |

as .

In summary, our proof is the following:

∎

We now prove the second result.

Theorem 2. The SAGE value estimates from Algorithm 1 have variance that reduces at the rate of .

Proof.

At a high level, the algorithm has an outer loop that contributes one sample (see Eq. 9) to each of the SAGE estimates , where randomness arises from the sampling of and and the inner loop samples (see Eq. 10). Regardless of how is chosen and the number of inner loop samples , the central limit theorem says that as becomes large, the sample mean converges in distribution to a Gaussian with mean and variance equal to

| (18) |

Although we do not have access to the numerator , we can conclude that the variance of the estimates behaves as .

∎

Appendix F Function Sensitivity

Several recent papers considered a related question of a function’s sensitivity to its various inputs [29, 30, 37]. We briefly describe the problem to illustrate how it differs from our work.

For a scalar real-valued function defined on multiple features , this body of work seeks to assign a sensitivity value to each feature. This is done with a variance-based measure of the dependence of on each feature, through an analysis of the cooperative game

| (19) |

The Shapley values serve as sensitivity measures for each feature . In prior work, Owen connected this measure of feature importance to the two Sobol’ indices [29], Owen and Prieur considered special cases with closed form solutions [30], and Song et al. provided a sampling-based approximation algorithm [37].

Our work considers the problem of assessing feature importance for black-box machine learning models. In contrast with the function sensitivity work, we allow for a response variable that is jointly distributed with , which is not necessarily in , and we consider how predictive each feature is of . The work on function sensitivity is equivalent to an application of SAGE to the special case where , where the model output is real-valued , and where the loss is MSE loss.

For cases with a response variable , a natural question is whether there is a relationship between and . The only case when these values coincide is when the loss is MSE and the model is the conditional expectation . Equality of the Shapley values follows from equality of the cooperative games:

Outside of this special case, the sensitivity values differ from the SAGE values .

Appendix G Summary of Additive Importance Measures

Table 3 summarizes the additive importance measures described in Section 2.3. For each method, we indicate which part of the subdomain of it prioritizes and show whether it approximates (universal predictive power) or (model-based predictive power).

Permutation tests, conditional permutation tests and mean importance assign scores in a similar manner. Each of these methods make different assumptions to approximate the difference

where the restricted model is given by:

Conditional permutation tests make the closest approximation, but they have the expectation over outside the loss function instead of inside it. Permutation tests make an assumption of feature independence by sampling from its marginal distribution instead of from its conditional distribution . And finally, mean importance makes a further assumption of model linearity by simply using the marginal mean .

| Subdomain | Approximates | Method | Importance Values |

|---|---|---|---|

| Feature Ablation | |||

| Permutation Test | |||

| Conditional Permutation Test | |||

| Mean Importance | |||

| Univariate Predictors | |||

| Squared Correlation | |||

| Shapley Net Effects | |||

| SAGE |

Appendix H Experiment Details

This section provides more details about our experiments, as well as several additional results.

H.1 Datasets and Hyperparameters

Table 4 provides information about the datasets, models and validation/test splits used in our experiments. All hyperparameters were chosen using the validation data (number of rounds for decision trees, regularization for BRCA, early stopping for the MLP) and the test data were reserved for measuring model performance and calculating feature importance.

The BRCA data required a small amount of pre-processing. We manually selected a small set of genes with known BRCA associations and then selected the remaining genes uniformly at random to have total genes. A small number of missing expression values were imputed with their mean.

| Dataset | Features | Examples | Split Size | Classes | Loss | Model Type |

|---|---|---|---|---|---|---|

| Bank Marketing | (, , ) | Cross Entropy | CatBoost | |||

| Bike Rental | (, , ) | – | MSE | XGBoost | ||

| Credit Default | (, , ) | Cross Entropy | CatBoost | |||

| Breast Cancer | (, , ) | Cross Entropy | Logistic Regression | |||

| MNIST | (, , ) | Cross Entropy | MLP (256, 256) |

When calculating feature importance, our sampling approximation for SAGE (Algorithm 1) was run using draws from the marginal distribution. We used a fixed set of background samples for the bank, bike and credit datasets, for MNIST, and all training examples for BRCA.

When generating random subsets for the correlation experiment in the main text, we first sampled the number of included features uniformly at random and then generated a random subset of indices. We used random subsets for the bank, bike, credit and BRCA datasets, and subsets for MNIST.

H.2 Additional Results

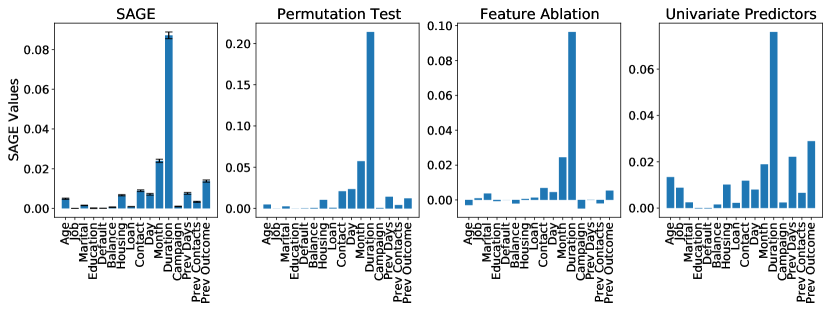

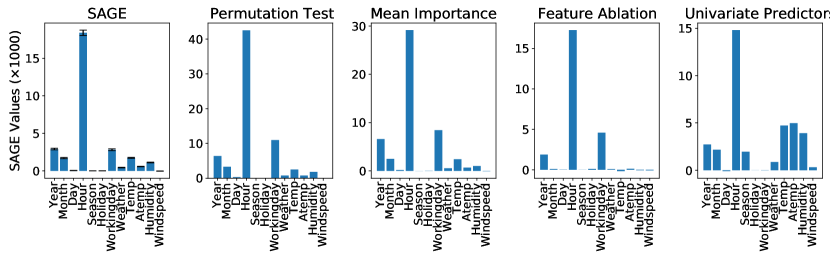

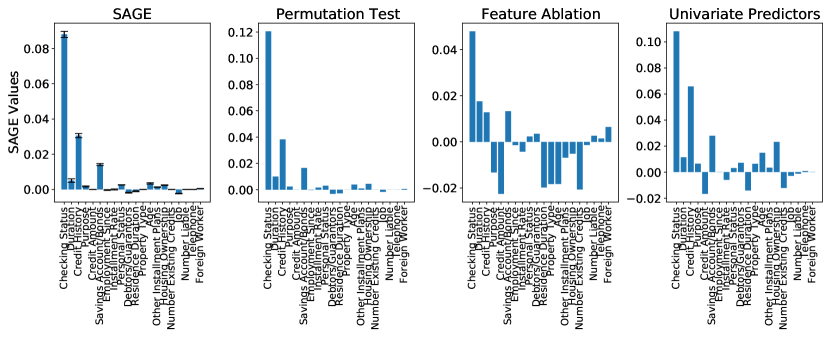

Global explanations for several datasets are provided for visual comparison. Figure 4 shows the bank marketing explanations, Figure 5 shows the bike demand explanations, and Figure 6 shows the credit quality explanations. The error bars in the SAGE explanations indicate 95% confidence intervals. The explanations have clear differences, but the differences are less pronounced than with the higher dimensional datasets (MNIST and BRCA).

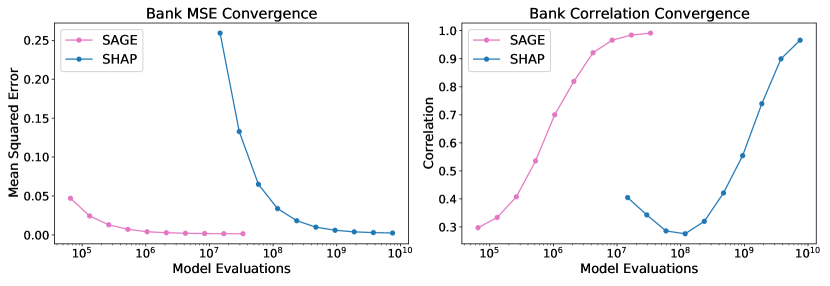

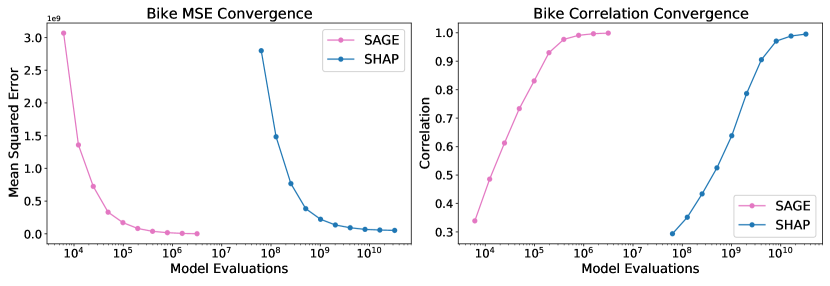

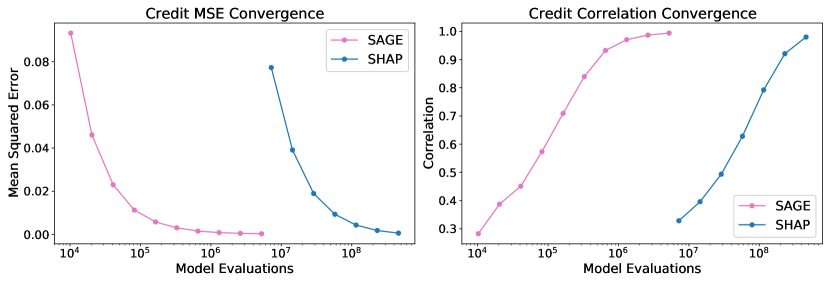

To contextualize the computational cost of calculating SAGE values, we performed a direct comparison between our proposed approach and a naive calculation via SHAP. Recall that SAGE values are the expectation of loss SHAP values across the entire dataset, which must be calculated separately for each instance (see Section 3.1 of the main text). We estimated SAGE values using both approaches to compare how quickly each converges.

To quantify SAGE’s convergence speed, we ran the sampling algorithm for a variable number of iterations and then calculated the result’s mean similarity with the correct values, which were determined by running the sampling algorithm until the convergence criterion was satisfied for (see Section 3.3 of the main text). For SHAP, we determined the mean number of iterations required for a local explanation to converge (again, with ) and generated multiple local explanations with this number of samples; we then averaged a variable number of local explanations and calculated the similarity with the true SAGE explanation.

Figure 7 shows the results, using both MSE and correlation as metrics. The results show that both approaches eventually converge to the correct values, but SHAP requires 2-4 orders of magnitude more model evaluations. The results could be made more favorable to SHAP by using a more liberal convergence criterion for the local explanations; SAGE shows that spreading computation across examples yields the correct result more efficiently. However, these barely-converged SHAP values would not be useful as local explanations. We conclude that our sampling approach is far more practical when users only require the global explanation.

References

- [1] Kjersti Aas, Martin Jullum, and Anders Løland. Explaining individual predictions when features are dependent: More accurate approximations to Shapley values. arXiv preprint arXiv:1903.10464, 2019.

- [2] Eric Bengtson and Dan Roth. Understanding the value of features for coreference resolution. In Proceedings of the 2008 Conference on Empirical Methods in Natural Language Processing, pages 294–303, 2008.

- [3] Nazih Benoumechiara and Kevin Elie-Dit-Cosaque. Shapley effects for sensitivity analysis with dependent inputs: bootstrap and kriging-based algorithms. ESAIM: Proceedings and Surveys, 65:266–293, 2019.

- [4] Ashton C Berger, Anil Korkut, Rupa S Kanchi, Apurva M Hegde, Walter Lenoir, Wenbin Liu, Yuexin Liu, Huihui Fan, Hui Shen, Visweswaran Ravikumar, et al. A comprehensive pan-cancer molecular study of gynecologic and breast cancers. Cancer Cell, 33(4):690–705, 2018.

- [5] Leo Breiman. Random forests. Machine Learning, 45(1):5–32, 2001.

- [6] A Charnes, B Golany, M Keane, and J Rousseau. Extremal principle solutions of games in characteristic function form: core, Chebychev and Shapley value generalizations. In Econometrics of Planning and Efficiency, pages 123–133. Springer, 1988.

- [7] Jianbo Chen, Le Song, Martin J Wainwright, and Michael I Jordan. L-Shapley and C-Shapley: Efficient model interpretation for structured data. arXiv preprint arXiv:1808.02610, 2018.

- [8] Tianqi Chen and Carlos Guestrin. Xgboost: A scalable tree boosting system. In Proceedings of the 22nd acm sigkdd international conference on knowledge discovery and data mining, pages 785–794, 2016.

- [9] Anupam Datta, Shayak Sen, and Yair Zick. Algorithmic transparency via quantitative input influence: Theory and experiments with learning systems. In 2016 IEEE Symposium on Security and Privacy (SP), pages 598–617. IEEE, 2016.

- [10] Hadi Fanaee-T and Joao Gama. Event labeling combining ensemble detectors and background knowledge. Progress in Artificial Intelligence, 2(2-3):113–127, 2014.

- [11] Harvey R Fernandez, Shreyas M Gadre, Mingjun Tan, Garrett T Graham, Rami Mosaoa, Martin S Ongkeko, Kyu Ah Kim, Rebecca B Riggins, Erika Parasido, Iacopo Petrini, et al. The mitochondrial citrate carrier, slc25a1, drives stemness and therapy resistance in non-small cell lung cancer. Cell Death & Differentiation, 25(7):1239–1258, 2018.

- [12] Jerome Friedman, Trevor Hastie, and Robert Tibshirani. The Elements of Statistical Learning, volume 1. Springer Series in Statistics New York, 2001.

- [13] Tilmann Gneiting and Adrian E Raftery. Strictly proper scoring rules, prediction, and estimation. Journal of the American Statistical Association, 102(477):359–378, 2007.

- [14] Isabelle Guyon and André Elisseeff. An introduction to variable and feature selection. Journal of Machine Learning Research, 3(Mar):1157–1182, 2003.

- [15] Isabelle Guyon, Jason Weston, Stephen Barnhill, and Vladimir Vapnik. Gene selection for cancer classification using support vector machines. Machine Learning, 46(1-3):389–422, 2002.

- [16] Giles Hooker and Lucas Mentch. Please stop permuting features: An explanation and alternatives. arXiv preprint arXiv:1905.03151, 2019.

- [17] Enguerrand Horel, Virgile Mison, Tao Xiong, Kay Giesecke, and Lidia Mangu. Sensitivity based neural networks explanations. arXiv preprint arXiv:1812.01029, 2018.

- [18] Dominik Janzing, Lenon Minorics, and Patrick Blöbaum. Feature relevance quantification in explainable AI: a causality problem. arXiv preprint arXiv:1910.13413, 2019.

- [19] Walid T Khaled, Song Choon Lee, John Stingl, Xiongfeng Chen, H Raza Ali, Oscar M Rueda, Fazal Hadi, Juexuan Wang, Yong Yu, Suet-Feung Chin, et al. Bcl11a is a triple-negative breast cancer gene with critical functions in stem and progenitor cells. Nature Communications, 6(1):1–10, 2015.

- [20] Igor Kononenko et al. An efficient explanation of individual classifications using game theory. Journal of Machine Learning Research, 11(Jan):1–18, 2010.

- [21] Yann LeCun, Corinna Cortes, and CJ Burges. Mnist handwritten digit database. at&t labs, 2010.

- [22] Jing Lei, Max G’Sell, Alessandro Rinaldo, Ryan J Tibshirani, and Larry Wasserman. Distribution-free predictive inference for regression. Journal of the American Statistical Association, 113(523):1094–1111, 2018.

- [23] Moshe Lichman et al. Uci machine learning repository, 2013.

- [24] Stan Lipovetsky and Michael Conklin. Analysis of regression in game theory approach. Applied Stochastic Models in Business and Industry, 17(4):319–330, 2001.

- [25] Yao-Zhong Liu, Yu-Fang Pei, Jian-Feng Liu, Fang Yang, Yan Guo, Lei Zhang, Xiao-Gang Liu, Han Yan, Liang Wang, Yin-Ping Zhang, et al. Powerful bivariate genome-wide association analyses suggest the sox6 gene influencing both obesity and osteoporosis phenotypes in males. PloS One, 4(8), 2009.

- [26] Scott M. Lundberg, Gabriel Erion, Hugh Chen, Alex DeGrave, Jordan M. Prutkin, Bala Nair, Ronit Katz, Jonathan Himmelfarb, Nisha Bansal, and Su-In Lee. From local explanations to global understanding with explainable AI for trees. Nature Machine Intelligence, 2(1):56–67, 2020.

- [27] Scott M Lundberg and Su-In Lee. A unified approach to interpreting model predictions. In Advances in Neural Information Processing Systems, pages 4765–4774, 2017.

- [28] Sérgio Moro, Paulo Cortez, and Paulo Rita. A data-driven approach to predict the success of bank telemarketing. Decision Support Systems, 62:22–31, 2014.

- [29] Art B Owen. Sobol’ indices and Shapley value. SIAM/ASA Journal on Uncertainty Quantification, 2(1):245–251, 2014.

- [30] Art B Owen and Clémentine Prieur. On Shapley value for measuring importance of dependent inputs. SIAM/ASA Journal on Uncertainty Quantification, 5(1):986–1002, 2017.

- [31] Liudmila Prokhorenkova, Gleb Gusev, Aleksandr Vorobev, Anna Veronika Dorogush, and Andrey Gulin. Catboost: unbiased boosting with categorical features. In Advances in neural information processing systems, pages 6638–6648, 2018.

- [32] Marco Tulio Ribeiro, Sameer Singh, and Carlos Guestrin. “Why should I trust you?” Explaining the predictions of any classifier. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 1135–1144, 2016.

- [33] Andrea Saltelli, Stefano Tarantola, Francesca Campolongo, and Marco Ratto. Sensitivity Analysis in Practice: a Guide to Assessing Scientific Models, volume 1. Wiley Online Library, 2004.

- [34] Rudy Setiono and Huan Liu. Neural-network feature selector. IEEE Transactions on Neural Networks, 8(3):654–662, 1997.

- [35] Lloyd S Shapley. A value for n-person games. Contributions to the Theory of Games, 2(28):307–317, 1953.

- [36] Karen Simonyan, Andrea Vedaldi, and Andrew Zisserman. Deep inside convolutional networks: Visualising image classification models and saliency maps. arXiv preprint arXiv:1312.6034, 2013.

- [37] Eunhye Song, Barry L Nelson, and Jeremy Staum. Shapley effects for global sensitivity analysis: theory and computation. SIAM/ASA Journal on Uncertainty Quantification, 4(1):1060–1083, 2016.

- [38] Carolin Strobl, Anne-Laure Boulesteix, Thomas Kneib, Thomas Augustin, and Achim Zeileis. Conditional variable importance for random forests. BMC Bioinformatics, 9(1):307, 2008.

- [39] Erik Štrumbelj and Igor Kononenko. Explaining prediction models and individual predictions with feature contributions. Knowledge and Information Systems, 41(3):647–665, 2014.

- [40] Mukund Sundararajan, Ankur Taly, and Qiqi Yan. Axiomatic attribution for deep networks. In Proceedings of the 34th International Conference on Machine Learning-Volume 70, pages 3319–3328. JMLR. org, 2017.

- [41] Katarzyna Tomczak, Patrycja Czerwińska, and Maciej Wiznerowicz. The cancer genome atlas (TCGA): an immeasurable source of knowledge. Contemporary Oncology, 19(1A):A68, 2015.

- [42] Vladimir Vapnik. The nature of statistical learning theory. Springer Science & Business Media, 2013.