Optimal periodic dividend strategies for spectrally positive Lévy risk processes with fixed transaction costs

Abstract

We consider the general class of spectrally positive Lévy risk processes, which are appropriate for businesses with continuous expenses and lump sum gains whose timing and sizes are stochastic. Motivated by the fact that dividends cannot be paid at any time in real life, we study periodic dividend strategies whereby dividend decisions are made according to a separate arrival process.

In this paper, we investigate the impact of fixed transaction costs on the optimal periodic dividend strategy, and show that a periodic strategy is optimal when decision times arrive according to an independent Poisson process. Such a strategy leads to lump sum dividends that bring the surplus back to as long as it is no less than at a dividend decision time. The expected present value of dividends (net of transaction costs) is provided explicitly with the help of scale functions. Results are illustrated.

keywords:

Optimal dividends, Periodic dividends, Dual risk model, Fixed transaction costs, SPLP JEL codes: C44 , C61 , G24 , G32 , G351 Introduction

The literature on the stability problem (see, e.g. Bühlmann, 1970) is prolific. One possibility criterion for stability is the expected present value of dividends, first proposed by de Finetti (1957). A dividend strategy defines when and how much dividends should be paid, and its optimal version is (often) the one that maximises the expected present value of dividends (see for instance Albrecher and Thonhauser, 2009).

Stylised models of an insurance company were first studied by pioneers such as Lundberg (1909); Cramér (1930); Borch (1967). They considered the specific case of insurance, where income is relatively certain (premiums are determined in advance) and outflows (mainly insurance claims) are random. In this paper, we consider the class of spectrally positive Lévy processes, whereby expenses are continuous and more certain (although still potentially perturbed by diffusion), and where the stochastic behaviour of the surplus process is on the upside, that is, gains happen at random times and with random amounts (Bayraktar, Kyprianou, and Yamazaki, 2013; Pérez and Yamazaki, 2017). This model is sometimes referred to as “dual model” because it is dual to the insurance model briefly described above (see, e.g. Mazza and Rullière, 2004). Such a model is obviously relevant to most risky business, but particularly so for commission-based businesses, pharmaceutical companies, petroleum companies (Avanzi, Gerber, and Shiu, 2007), and also for valuing venture capital investments (Bayraktar and Egami, 2008). Cheung and Wong (2017) further discuss the relevance of the model, as well as its connection with queuing models.

When dividends can be paid at any time (which we also refer to as ”continuous decision making”), optimal dividend strategies for the dual model were determined in general by Bayraktar, Kyprianou, and Yamazaki (2013, 2014, without, and with fixed transaction costs, respectively). On the other hand, “periodic” dividends as introduced by Albrecher, Cheung, and Thonhauser (2011) were first considered in the dual model by Avanzi, Cheung, Wong, and Woo (2013), with optimality results in Avanzi, Tu, and Wong (2016); Pérez and Yamazaki (2017). When the surplus is a spectrally negative Lévy process (with a completely monotone Lévy density), Loeffen (2008b, 2009) showed that a barrier strategy implemented in continuous time is optimal with and without fixed transaction costs, respectively. Noba, Pérez, Yamazaki, and Yano (2018) extended the result in Loeffen (2008a) in a periodic setting (without fixed transactions costs) and showed that such class of strategy if implemented in periodic time is also optimal in the periodic setting.

In this paper, we focus on “periodic” dividends, and consider fixed transaction costs in a spectrally positive Lévy risk process. While proportional transaction costs affect the level of the optimal barrier, they do not change results qualitatively, which makes sense as they can be interpreted as a simple change of currency. We show that fixed transaction costs lead to a split barrier being optimal. This again mirrors analogous results in a continuous decision making framework; see e.g. Yao, Yang, and Wang (2011). We further illustrate numerically that our result is consistent with Bayraktar, Kyprianou, and Yamazaki (2014) and Pérez and Yamazaki (2017) when the frequency of the dividend payment time goes to infinity and the fixed transaction costs are reduced to zero, respectively.

The paper is organised as follows. In Section 2, we define the mathematical model, whereas in Section 3 we define more rigorously what the class of strategies is. We then briefly review in Sections 4 and 5 scale functions and related results which will be needed later in the paper. Section 6 gives a sufficient condition for a strategy to be optimal (verification lemma). Section 7 computes the value function of a given periodic strategy. Following that, Section 8.1 studies the smoothness condition of the value function, which is the first step to choose our candidate strategy, where Section 8.2 elucidates the second step to choose our candidate strategy, which involves the derivative of the value function at the lower barrier. At the end of Section 8 it is shown that the 2 conditions proposed in Sections 8.1 and 8.2 regarding the parameters and can always be satisfied (existence). Section 9 confirms that the candidate we constructed in Sections 8.1 and 8.2 is indeed optimal (using the verification lemma of Section 6), and that it is unique. Finally, numerical illustrations are provided in Section 10. Section 11 concludes.

2 The model

In this paper we use a standard set-up for stochastic processes (e.g. Bertoin, 1998, Chapter 0). We first define a spectrally negative Lévy process . It is well known that the law of a Lévy proccess can be uniquely characterised by its characteristic exponent. For , its Laplace exponent is given by

| (2.1) |

and

| (2.2) |

with

| (2.3) |

where are the Lévy triplet of . In order to avoid trivial cases, we also require that does not have a monotonic path. We then construct a spectrally positive Lévy process starting at (initial surplus) as

| (2.4) |

that is, we shift the process upwards by units. We denote its law by and the mathematical expectation operator related to it as . Next, we define periodic dividend decision times (the time where one has to decide how much to pay and the payment occurs instantaneously), or in short decision times. Decision times are the times when the Poisson process (independent of ) with rate , , has increments, i.e. the set , with

| (2.5) |

where throughout this paper we adopt the convention

| (2.6) |

In words, it means that the -th decision time, , corresponds to the time when jumps from to . Let be the filtration generated by the process . Then, a periodic dividend strategy (defined by the cumulative dividends paid) is a non-decreasing, right-continuous and -adapted process, which admits the form

| (2.7) |

Hence, the dividend amount paid at is (the increment of at ) and the strategy can also be specified in terms of . The modified surplus is defined as

| (2.8) |

where the ruin time is defined as

| (2.9) |

the instant that the modified surplus goes below for the first time.

We now introduce the constraints for the periodic dividend strategy. Intuitively, given that a fixed transaction cost is incurred on each dividend payment, the (gross) amount of dividend should be large enough to pay the transaction cost, i.e.

| (2.10) |

This holds naturally (see property 5 in Remark 2.1 below). Since we are not allowed to inject capital into the surplus, and since a dividend payment cannot exceed the current surplus, we have the following restrictions:

| (2.11) |

which translates to

| (2.12) |

as the jump times of and the periodic decision times are distinct with probability .

We can see from the above definition that, at a decision time, a decision to not pay any dividend is also allowed. In this case, no transaction cost is incurred. It is also possible that a dividend payment can cause ruin, which refers to liquidation of the company, i.e. the company chose to close its business by distributing all the available surplus (at its first opportunity). This strategy is called a liquidation-at-first-opportunity strategy. We denote the set of all admissible strategies and define the set of all admissible strategies such that (2.10) holds.

Lastly, we introduce the time preference parameter . The value function of a strategy with initial surplus is denoted as, . We define

| (2.13) |

Note that we have and for all strategies since ruin at with is certain for a spectrally positive Lévy process with no monotonic paths. Our goal is to find an optimal strategy (if it exists) such that

| (2.14) |

Remark 2.1.

From the definitions of and , we have for any

-

1.

and

-

2.

for all , and

-

3.

for all , and

-

4.

for all and , and

-

5.

.

Proof of 5.

Note this property justifies our statement just after (2.10). To prove this property, it suffices to show that all strategies in can be outperformed by the strategies in . If a strategy is in , there are some dividend payments smaller than . Those will contribute a negative value to the value function. By choosing not to pay dividends at those dividend decision times, call it strategy , we can remove those negative contributions while having a higher surplus level at those times, resulting in a smaller probability of ruin, or for all and for all . Thus, we have . Finally we note that either pays dividends above or equal to , or does not pay any dividend, thus is inside the set . ∎

Thanks to the fifth property in Remark 2.1, it suffices to consider only the strategies in . Therefore, in the remaining of this paper, we restrict ourselves to strategies in .

3 Candidate strategy

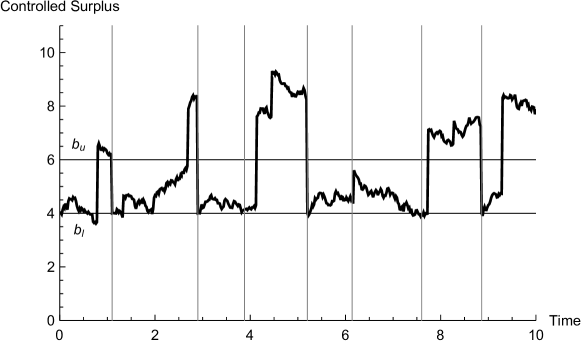

Inspired by the form of optimal strategies in the literature, e.g. Bayraktar, Kyprianou, and Yamazaki (2014), Pérez and Yamazaki (2017), Loeffen (2008a) and Noba, Pérez, Yamazaki, and Yano (2018), we conjecture that an optimal periodic strategy will be of the form , as defined in Definition 3.1 and illustrated in Figure 1.

Definition 3.1 (Periodic () strategy).

A periodic strategy with is the strategy that pays whenever the surplus is above or equal to , at decision times. This reduces the surplus level to .

By denoting the strategy as , we have

| (3.1) |

Clearly, we have

Remark 3.1.

Similarly, a periodic barrier strategy at barrier level , denoted as , is defined as

| (3.2) |

4 Definition of scale functions

This section gives definitions of scale functions for our purpose, that is, to calculate the value function of a periodic strategy. The central idea of scale function is based on path decomposition of Lévy processes, i.e. Wiener-Hopf factorisation and Itô’s excursion theory. Interested readers can refer to good textbooks including Bertoin (1998) and Kyprianou (2006). Additional references regarding the general theories of spectrally negative Lévy processes includes Chaumont and Doney (2005), Loeffen, Renaud, and Zhou (2014), Pardo, Pérez, and Rivero (2015) and Pérez and Yamazaki (2018), where some useful identities are also available. Examples of the applications of fluctuation theories include Furrer (1998), Avram, Palmowski, and Pistorius (2007), Cheung, Yang, and Zhang (2017) and Yang, Yang, and Zhang (2013). Recently, Avram, Grahovac, and Vardar-Acarceren (2017) summarised the identities and the applications of fluctuation theories on risk theory.

The -scale function, , for , is defined through the inverse Laplace transform of , i.e.

where

Moreover, for the “tilted” -scale function is defined as

| (4.1) |

In particular, we also define for

| (4.2) | ||||

| (4.3) |

where the equality in (4.2) is due to .

For , we define

| (4.4) | ||||

| (4.5) | ||||

| (4.6) | ||||

| (4.7) |

We also define the integral of functions by adding an overhead line to them, such that

where we also define for .

In addition, we also define and

| (4.8) | ||||

| (4.9) |

5 Preliminaries: results on periodic barrier strategies

In this section, we list some useful results related to periodic barrier strategies which will be used in later sections. First, we present the following identity extracted from Equation (5) in Albrecher, Ivanovs, and Zhou (2016): for ,

| (5.1) |

where and for any . Hence, we have

| (5.2) |

which is analogous to in Bayraktar, Kyprianou, and Yamazaki (2014).

In addition, using existing results in scale function as in Appendix A, one can deduce that

| (5.3) |

From Pérez and Yamazaki (2017), we know that

| (5.4) |

and that

| (5.5) |

where is a periodic barrier, and is the unique solution of

| (5.6) |

given that . Otherwise, . In addition, if , (resp. ) if (resp. ). Hence, we can deduce that for

| (5.7) |

Furthermore, we have

| (5.8) |

To supplement the results in Pérez and Yamazaki (2017), we establish the following results:

Lemma 5.1.

It holds that

| (5.9) |

Proof of Lemma 5.1.

It suffices to show that is strictly increasing in , i.e.

Regarding the construction of the law of on the probability space of the sample path, , we shall assume that and refer to the law the law of under . In this sense, in the following, we will only work with the primary measure , which have also taken into account of the (for example by taking the product measure).

Suppose , for a given sample path of starting at , the modified sample path with units shifted upward (denoted ) can never exceed that with units shifted up (denoted ), because a dividend either brings both surplus down to ( for some ), or brings the closer to such that for some . Using the same argument, it is clear that can never receive more dividends than . This shows . Note on the (-a.s.) event , there is a positive probability that hits above at before ruin, giving the strict inequality.

For , we have . Hence, it suffices to show . Again, on the (-a.s.) event , there is a positive probability that hits above at before ruin, showing the strict inequality. ∎

Lemma 5.2.

For , we have:

| (5.10) |

6 Verification lemma

In this section, we give a sufficient condition for a strategy to be optimal. We first characterise the smoothness of a function by the following definition.

Definition 6.1.

If is of unbounded variation, a function is smooth if . Otherwise if is of bounded variation, a function is smooth if .

Remark 6.1.

It is well-known that has path of bounded variation if and only if and . Examples of SPLP with bounded variation include the compound Poisson process with negative drift. Examples of SPLP with unbounded variation include Brownian motion with upward jumps, see Section 10 for illustrations.

The extended generator for applied on a function , , is given by

| (6.1) |

whenever it () is well defined (if is sufficiently smooth), and where the term is understood to vanish if is of bounded variation (no Gaussian component). Lemma 6.2 characterises sufficient conditions that a strategy need to satisfy in order to be optimal.

Lemma 6.2.

Suppose and its value function satisfies

-

1.

is smooth,

-

2.

,

-

3.

, ,

then is optimal, i.e. for all .

7 Value function of a periodic strategy

In the following, we first calculate the value function of a periodic strategy with any choices of and such that . The value function of is given by the following theorem.

Theorem 7.1.

For , the value function is given by

| (7.1) |

where

| (7.2) | ||||

| (7.3) | ||||

| (7.4) |

The constants and are given by

| (7.5) | ||||

| (7.6) |

if

| (7.7) |

Otherwise, we have

| (7.8) | ||||

| (7.9) |

8 Construction of a candidate optimal strategy

In this section, we construct a candidate optimal strategy, making two educated guesses for the optimality conditions, which we implement sequentially: smoothness (Section 8.1), and a further condition on the derivative at the optimal lower barrier (Section 8.2). Existence is established at the end of Section 8.2, but proof of uniqueness is postponed until the end of Section 9, where we verify that it is indeed the optimal strategy thanks to the verification lemma developed in Section 6.

8.1 First step: a smoothness condition

Based on a smooth fitting argument, the optimal value function should have one more degree of smoothness (compared to that of a general strategy). In this section, we investigate which condition the value function must satisfy in order to be smooth according to Definition 6.1. This is summarised in the following lemma.

Lemma 8.1.

is smooth if and only if

| (8.1) |

Proof of Lemma 8.1.

First, note that

and also that

. In addition, it is well known that

From , we have

Therefore, we get from Theorem 7.1 that

On the other hand, we have

when is of bounded variation and

when is of unbounded variation. Similarly,

when is of bounded variation and

when is of unbounded variation.

Therefore,

when is of bounded variation and

when is of unbounded variation. Hence,

is the smoothness condition.

∎

Remark 8.1.

By rearranging (8.1), we have

| (8.2) |

This is equivalent to the continuity condition when dividends can be made at any time (see, e.g. Bayraktar, Kyprianou, and Yamazaki, 2014; Jeanblanc-Picqué and Shiryaev, 1995; Loeffen, 2008a). In words, it means that the difference in value between both barriers and is exactly equal to the net (of transaction costs ) dividend paid between those two levels.

It is remarkable that this relation holds for any smooth strategy in the periodic decision making framework considered in this paper.

Remark 8.2.

Lemma 8.1 characterised the condition for the value function of a strategy to be smooth. The following lemma characterises the smoothness condition explicitly in terms of and .

Lemma 8.2.

The smoothness condition (8.1) is equivalent to , where and is defined as

| (8.6) |

Remark 8.3.

The choice of notation reflects naturally the structure of the construction of the value function, which is first anchored at through a derivative. The distance between both barriers then depends directly on the level of fixed transaction costs, and has a direct interpretation as being the minimum viable amount of dividends to be paid. More rationale for this choice can be found in Tu (2017, Remark A.3.1), who revisited the original results of Jeanblanc-Picqué and Shiryaev (1995).

The following proposition assures the existence of a periodic strategy that satisfies the smoothness condition (8.1).

Proposition 8.3.

For any , there is a unique with such that . Moreover, such is a continuous function of . In particular, implies

| (8.7) |

Remark 8.4.

When a liquidation-at-first-opportunity is considered, i.e. , then the smoothness condition (8.1) is equivalent to

| (8.8) |

If the process survives until the next dividend decision time, then the net dividend payment will be at least . So, should be that quantity, discounted over the time to next dividend decision time where a dividend can be paid, times the probability that this will happen (all in an expected sense). What this formula says is that smoothness ensures that it all balances out so as to obtain an expected present value of .

This can be used to intuitively explain how Proposition 8.3 is proved. Consider the following two extreme cases. When is , the left hand side is a value function which is positive, which is greater than the right hand side which is zero. On the other hand when is large (close to infinity), the left hand side is , which is approximately since is large. This quantity is smaller than , the right hand side. In other words, since we are in periodic setting, we need to wait for the first opportunity to liquidate, the discounting effect is dominant when is large, resulting in the left hand side being smaller. Now it should be clear that there is a “sweet spot” such that the equation holds.

When a similar reasoning applies, although the proof is more involved; see Appendix D.

Thanks to Proposition 8.3, we know that for a given , we can always find a () such that the smoothness condition (8.1) is met. We call those strategies “smooth strategy” and denote those strategies as (the value function of the strategy is smooth). We should remember that is uniquely determined by . In the following, we assume , and are fixed, i.e. we are looking at a particular smooth strategy. The value function of such strategy is denoted as when the initial surplus is . In the case where confusion may arise, we will write it explicitly as .

8.2 Second step: a condition on the derivative of at

From last section, we know that for a fixed , we can always choose a unique such that is smooth. This is our first step to optimality, i.e. we shall only look at those strategies.

The second step to optimality concerns the derivative of the value function at . Specifically, if , we call the liquidation-at-first-opportunity strategy “optimal” and denote it as . This means we choose . On the other hand, if and there are such that

| (8.9) |

then we also call it “optimal” and denote it as . Hence, the notation with stands for an “optimal strategy”. The value function when a chosen optimal strategy (for ) is applied is denoted as , or if the dependence of and needs to be stressed.

Of course, our goal is to show that an “optimal” strategy exists and is optimal in the sense of (2.14). The first goal (existence) is established at the end of this section after the following remarks while the second goal (optimality) will be achieved in Section 9.

Remark 8.5.

In the space of strategies being considered, it is useful to know the following relationship.

Ultimately, we want to select an element in the set of optimal strategy to serve our candidate strategy to be verified optimal. To do that, we need to make sure that there is at least one element in the first set. Specifically, Proposition 8.3 ensures that the middle set has as many elements as the real line (and therefore is non-empty). Lemma 8.4 (which appears later) guarantees that there is at least one element in the first set.

Remark 8.6.

The derivative of the value function represents the marginal (discounted) rate of return from investing in the company. When the derivative is greater than 1, it means that an extra one dollar invested in the company will generate more than one dollar of return and therefore we should leave that dollar in the surplus, i.e. pay no dividends. On the other hand, if the derivative is less than 1, the company cannot generate enough profit and hence it would be better off paying out the cash as dividends. Following this argument, we can see that if the company wants to maximise the total discounted dividends, it should pay dividends until it reaches a level where the derivative is . This explains (8.9) and is a standard behaviour observed when (optimal) barriers are applied.

Furthermore, the condition represents the scenario that the company does not have a good prospects anywhere, so liquidating the company as soon as possible is desired, i.e. choose . On the other hand, the condition represents the scenario that the company has a good prospect and therefore we should keep the company running, i.e. choose . In summary, we have

| (8.10) |

Remark 8.7.

Recall from Remark 8.6 that can be interpreted as a marginal profitability rate. When and satisfy the smoothness condition (8.1), by rearranging the terms we get

| (8.11) |

which means that the distance between and must be such that the integrated “profitability shortfall” is exactly .

Interestingly, (8.11) always holds when dividends can be paid at any time (see, e.g., Equation (3.13) of Jeanblanc-Picqué and Shiryaev, 1995). In our framework, this becomes a necessary (but not sufficient) condition for optimality. The condition becomes sufficient when is chosen so as to minimise the distance in (8.11), which is when (8.9) holds.

Remark 8.8.

Recall from Remark 8.2 that the value function of a smooth periodic stategy simplifies, especially at . The following displays the relationship between the optimal barriers versus the optimal barriers under different settings. For the optimal continuous barrier , it holds that , and the value at the barrier simplifies. For the optimal periodic barrier (without costs), we have

and further simplifications can be made. In our case however, we only have if which yields in view of (8.3) and (8.7)

| (8.12) |

when the smoothness condition is verified, and (8.3) does not seem to simplify further.

We now proceed to prove the existence of , i.e. the following proposition.

Lemma 8.4.

If , then there exists with such that (8.9) holds, i.e. exists.

Proof of Lemma 8.4.

From Proposition 8.3, we know that the mapping is a continuous function on the domain . The given condition in the lemma is the same as assuming the function value at is greater than . Hence, we are done if we can show that the function value is negative at . From (8.3), such condition is the same as

with being the unique solution to (see Proposition 8.3). However, such condition is precisely Lemma 5.2. ∎

9 Verification of the optimality of the candidate strategy

The previous section ensures that there is at least one (defined by (8.1) and (8.9), see Remark 8.5 for details). In this section, unless otherwise specified, we work on a chosen optimal strategy and show its optimality. Recall that the value function of such strategy is denoted as or . Moreover, all properties derived for are automatically satisfied by . The optimality of a is summarised by the following theorem.

Proposition 9.1.

The strategy is optimal, i.e. for .

Lemma 9.2.

for .

Proof of Lemma 9.2.

Lemma 9.3.

The derivative of the value function, , has at most one turning point on .

Proof of Lemma 9.3.

Note that . In addition, from (8.3), we have

| (9.4) |

Hence, we have

| (9.5) | ||||

| (9.6) |

If , we have from (9.5) that for all since by (8.7), which means that there is no turning point in this case. On the other hand, if , we have from (9.6)

Noting from (5.2) that is (strictly) increasing in , we can conclude that there is at most one turning point for . ∎

Lemma 9.4.

If and , then , .

Proof of Lemma 9.4.

From the proof of Lemma 9.3, we know that cannot go from positive to negative when increases. Hence, we can conclude that there are only three possibilities regarding the sign of on :

-

1.

for all ;

-

2.

There exists a point such that

-

3.

for all .

Case (1) is impossible since it implies , which contradicts to Lemma 9.2. For case (2), unless we can use the same argument as in Case (1) to conclude that it is impossible. Therefore, we have for . Case (3) directly leads to for . ∎

Lemma 9.5.

For , we have

| (9.7) |

Proof of Lemma 9.5.

From equations (4.20), (4.21), (4.18) and (4.22) in Pérez and Yamazaki (2017), we have

| (9.8) | ||||

| (9.9) | ||||

| (9.10) | ||||

| (9.11) |

By following exactly the same steps, it can be shown that

| (9.12) | |||||

| (9.13) |

Next, from the definition of and Lemma 9.2, when , we have that for in all 3 cases stated in the proof of Lemma 9.4 regarding the sign of . When , only cases 2 and 3 are possible. Hence, we have for by Lemma 9.4. Combining with Lemma 9.2, we have

| (9.14) |

and subsequently

| (9.15) |

Next, we verify that for a fixed , maximises

| (9.16) |

with the support of being .

First, we consider the support on . Since is a continuous differentiable function (as is) and the support is bounded, the maximum value of the function is attended at either or at the boundaries. Now, by taking the derivative of , we have

| (9.17) |

thanks to (9.14). Hence, the maximum value of on is attained at since is strictly decreasing on . Now, we should compare the value of at and to find the maximum. Clearly, . When , , since for all . Thus, the maximum value attains at . On the other hand, if , then if and only if by (9.15). In summary, attains its maximum when if , and if .

We are now ready to prove Proposition 9.1.

Proof of Proposition 9.1.

It suffices to show that satisfies all 3 conditions in Lemma 6.2.

Since both and are finite, combining with (8.5) and Lemma 9.2, we have

| (9.20) |

showing that is finite. This together with Proposition 8.3 shows the first condition. The second condition is satisfied by (9.20) together with the fact that ; see the discussion after (2.13). The third condition is a simple consequence of (9.19) and (9.12). ∎

From Lemma 8.4 and Proposition 9.1, we know that there exists a pair of () such that is optimal. The following lemma states that the choice of () is unique.

Lemma 9.6.

There is only one pair of such that the strategy qualifies as .

Proof of Lemma 9.6.

If , clearly it is unique. Otherwise, suppose we have two strategies, namely and . From Proposition 9.1, we have

| (9.21) |

As a result, by using the definition of and , we have

| (9.22) |

From equation (9.14), we have for , which gives . Similarly, we have . Therefore, we have . Recall from Proposition 8.3 that for a given there is a unique to achieve smoothness.. Hence, implies . In other words, there is only one .

∎

We are now ready to state our main result:

Theorem 9.7.

Denote the barriers of the unique , the strategy is optimal, i.e.

Proof.

Proposition 9.1 states that the family of optimal strategies is optimal. Lemma 8.4 states that the family of optimal strategies has at least one element while Lemma 9.6 states that the family of optimal strategies has at most one element. All together, it means there exists a unique (optimal) periodic strategy which is optimal in the sense of (2.14). ∎

10 Numerical illustrations

In this section, a diffusion process with Poissonian upward exponential jumps is used, i.e.

| (10.1) |

where is a collection of i.i.d. exponential random variables with mean , is a standard diffusion process and is a Poisson process with rate such that . The baseline parameters used are , , , , , and .

In the terminology of (2.2), the Laplace exponent in our illustration is

which is slightly different but can be rewritten in the form of (2.2) easily. This is further explicitly evaluated as

It is easy to show that is a rational function with 3 distinct roots and therefore its reciprocal can be rewritten using partial fraction as

where , are the roots of . The -scale function can then be computed explicitly by inverting the Laplace transform. All other scale functions can then be computed explicitly afterwards.

To find the optimal barriers , we make use of Proposition 8.3 and Lemma 8.4. To be more specific, we perform the following:

-

1.

Find using (5.6). Specifically, if , then set , otherwise, solve such that . This can be done by (1) trying a large enough such that following by (2) a bisection method on the range .

-

2.

Write a function on to output from Proposition 8.3 with a similar method as the previous step (using range for large enough ), then calculate the derivative of the value function at and return this number. Say we call this function .

- 3.

Remark 10.1.

We remark that gradient descend type of methods typically do not work well because a realatively large increment of the parameters (barriers) only results in a small change of the objective function (i.e. plateau). Therefore, analytic methods (such as used in this paper) are needed. Perhaps more importantly, this shows that in practice one typically have more flexibility to deviate from the optimal strategy to incorporate other considerations.

Remark 10.2.

Note that , and are forces of dividend decisions, continuous interest, and gain occurrence, per unit of time, respectively. Therefore, the value of needs to be compared with those of and . Similarly, the value of is in currency unit. Along those lines, it needs to be commensurate with those of , and .

Remark 10.3.

The numerical values chosen are inspired by the following fictitious business. A real estate business which on average sells 50 houses a year and pays biannual dividend, i.e. and and the time unit is (roughly) a week. Hence, implies an annual force of interest of . In addition, for each house sold, the commission gained is on average unit, i.e. . (For instance, typical commission rates in Sydney are and the median house price is about $1,150,000, so that would be or 0.03 million) Furthermore, to illustrate the riskiness of the business, we assume and such that the cost of the business is of its expected gain. Lastly, the size of is assumed to be , approximately 2 weeks of cost.

Illustrations include the impact, on the optimal dividend strategy, of the transaction costs and the interplay of dividend decision frequency and force of interest.

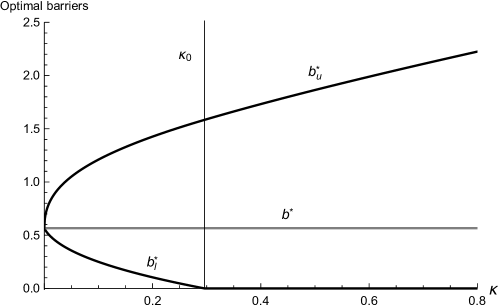

10.1 Impact of the fixed transaction costs

Figure 2 plots the optimal barriers and against fixed transaction costs . We also denote as the optimal barrier when there is no transaction costs, see e.g. Pérez and Yamazaki (2017) for details. This figure illustrates that when the transaction cost increases from , the optimal barrier without transaction costs splits into the upper and the lower barrier and , respectively. As further increases, the distance between both barriers increases, too; see also Remark 8.7. When the transaction costs are more than a certain quantity which we denote , then and a liquidation at first opportunity is optimal. This illustrates that despite the profitability (), the business would not have good prospect if the costs of paying the shareholders () are too high. Lemma 10.1 establishes (partially) the existence of .

Lemma 10.1.

There exists a threshold such that .

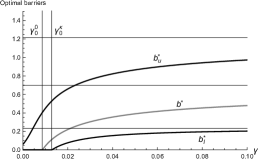

10.2 Impact of the time parameters and

Figure 3 plots the optimal barriers , and (the optimal periodic barrier when ) against the frequency parameter of dividend decisions . By looking at the graphs from left to right, we can see the convergence of , and to their “continuous” counterparts (that is, the optimal impulse strategy when dividends can be paid at any time; see references below), as indicated by the 3 horizontal lines. These limits can be calculated, for example, using the results from Bayraktar, Kyprianou, and Yamazaki (2013, 2014, without and with transaction costs, respectively). The expected present value of dividends under (in this case with ) can itself be calculated using the results from Pérez and Yamazaki (2017). The curves for and developed in this paper are calculated using Proposition 8.3 and Lemma 8.4, respectively.

Again, one can see that the barrier is sandwiched between both levels of the strategy. Furthermore, as the ‘time impatience’ parameter increases, it becomes more important to pay more dividends earlier (as compared to avoid ruin), and the barrier levels decrease. However, at the same time, the intensity at which dividends decisions are made (in a way, how often they can be paid) also need to be higher, lest a liquidation-at-first-opportunity strategy becomes optimal. Indeed, we can see that there is a threshold for such that below this threshold a liquidation-at-first-opportunity strategy is optimal, that is, . This threshold (in presence of fixed transaction costs ) is obtained in a similar way to (see Lemma 10.1). Obviously, the introduction of transaction costs pushes this threshold upwards, which explains why leaves the axis earlier (at ).

Generally speaking, when (when a liquidation-at-first-opportunity strategy is optimal), the difference is strictly larger than the transaction costs to allow for a strictly positive final dividend (upon liquidation) even when the current surplus is below (not enough to pay the liquidation cost); see Appendix D for details. However, when becomes small (and one will have to wait longer to be able to liquidate), one would give up the buffer to exchange for a higher chance of exiting the business. Eventually, when tends to , decreases to exactly so that intersects the -axis at .

Furthermore, it is interesting to note that the ‘periodic’ is strictly below the split barrier (impulse) strategy of the ‘continuous’ case (when dividends can be paid at any time)—indicated with horizontal gray barriers in Figure 3. In the case of this is because the strategy compensates for the cost of having to wait another period if dividends are not paid immediately. This difference is larger (and convergence slower) as increases, which makes sense. The convergence of seems to be quicker than that of , simply because in its case the danger associated with being too close to 0 is likely to overpower the force described earlier in this paragraph (and which would push it down).

11 Concluding remarks

In this paper, we determined the form of the optimal periodic dividend strategy when there are fixed transaction costs, when the dividend decisions are Poissonian, and where the underlying model is a spectrally positive Lévy process. Using exiting identities and the strong Markov properties, we were able to compute the value function of a periodic strategy concisely in terms of scale functions.

We proceeded to identify the best strategy among the class of periodic strategies, namely the periodic strategy, in 2 steps and verified its optimality. A number of new insights were gained while doing so. In particular, the difference in the barriers is always strictly greater than the transaction cost such that the net dividend is at least , i.e. a buffer. Moreover, despite the profitability , when the transaction costs are too high, it is optimal to close the business.

Finally, we numerically illustrated the convergence of our results with that of Bayraktar, Kyprianou, and Yamazaki (2014) and Pérez and Yamazaki (2017), as well as the impact of the transaction costs and the frequency of dividend decisions on the optimal barriers.

This paper is a significant step towards answering a number of open questions, including: (i) can hybrid (periodic and continuous) dividend strategies (see Avanzi, Tu, and Wong, 2016) be optimal in presence of fixed transaction costs, and if so, under what conditions? (ii) is the optimal periodic dividend strategy still a strategy when inter-dividend decision times are Erlang distributed, ? (iii) are strategies also optimal in spectrally negative Lévy risk processes?

Acknowledgments

The authors are indebted to two anonymous referees, whose comments led to significant improvements of the manuscript.

This paper was presented at the Australasian Actuarial Education and Research Symposium in December 2017 in Sydney (Australia), at the 10th Conference in Actuarial Science & Finance on Samos (Greece) in June 2018, at the International Congress on Insurance: Mathematics and Economics (Sydney, Australia) in July 2018, and at the European Actuarial Journal Conference (Leuven, Belgium) in September 2018. The authors are grateful for constructive comments received from colleagues who provided constructive comments on the paper.

This research was supported under Australian Research Council’s Linkage (LP130100723) and Discovery (DP200101859) Projects funding schemes. Hayden Lau acknowledges financial support from an Australian Postgraduate Award and supplementary scholarships provided by the UNSW Australia Business School. The views expressed herein are those of the authors and are not necessarily those of the supporting organisations.

References

References

- Albrecher et al. (2011) Albrecher, H., Cheung, E. C. K., Thonhauser, S., 2011. Randomized observation periods for the compound poisson risk model: dividends. ASTIN Bulletin 41 (2), 645–672.

- Albrecher et al. (2016) Albrecher, H., Ivanovs, J., Zhou, X., 2016. Exit identities for Lévy processes observed at poisson arrival times. Bernoulli 22, 1364–1382.

- Albrecher and Thonhauser (2009) Albrecher, H., Thonhauser, S., 2009. Optimality results for dividend problems in insurance. RACSAM Revista de la Real Academia de Ciencias; Serie A, Mathemáticas 100 (2), 295–320.

- Avanzi et al. (2013) Avanzi, B., Cheung, E. C. K., Wong, B., Woo, J.-K., 2013. On a periodic dividend barrier strategy in the dual model with continuous monitoring of solvency. Insurance: Mathematics and Economics 52 (1), 98–113.

- Avanzi et al. (2007) Avanzi, B., Gerber, H. U., Shiu, E. S. W., 2007. Optimal dividends in the dual model. Insurance: Mathematics and Economics 41 (1), 111–123.

- Avanzi et al. (2016) Avanzi, B., Tu, V. W., Wong, B., 2016. On the interface between optimal periodic and continuous dividend strategies in the presence of transaction costs. ASTIN Bulletin 46 (3), 709–746.

- Avram et al. (2017) Avram, F., Grahovac, D., Vardar-Acarceren, C., 2017. The scale functions kit for first passage problems of spectrally negative lévy processes, and applications to the optimization of dividends. Tech. rep., arXiv preprint arXiv:1706.06841.

- Avram et al. (2007) Avram, F., Palmowski, Z., Pistorius, M. R., 2007. On the optimal dividend problem for a spectrally negative Lévy process. Annals of Applied Probability 17 (1), 156–180.

- Bayraktar and Egami (2008) Bayraktar, E., Egami, M., 2008. Optimizing venture capital investments in a jump diffusion model. Mathematical Methods of Operations Research 67 (1), 21–42.

- Bayraktar et al. (2013) Bayraktar, E., Kyprianou, A. E., Yamazaki, K., 2013. On optimal dividends in the dual model. ASTIN Bulletin 43 (3), 359–372.

- Bayraktar et al. (2014) Bayraktar, E., Kyprianou, A. E., Yamazaki, K., 2014. Optimal dividends in the dual model under transaction costs. Insurance: Mathematics and Economics 54, 133–143.

- Bertoin (1998) Bertoin, J., 1998. Lévy Processes. Cambridge Tracts in Mathematics. Cambridge University Press, Cambridge, UK.

- Borch (1967) Borch, K., 1967. The theory of risk. Journal of the Royal Statistical Society. Series B (Methodological) 29 (3), 432–467.

- Bühlmann (1970) Bühlmann, H., 1970. Mathematical Methods in Risk Theory. Grundlehren der mathematischen Wissenschaften. Springer-Verlag, Berlin, Heidelberg, New York.

- Chaumont and Doney (2005) Chaumont, L., Doney, R., 2005. On Lévy processes conditioned to stay positive. Electronic Journal of Probability 10 (28), 948–961.

- Chen et al. (2017) Chen, P., Yang, H., Yongxia, Z., 2017. Optimal periodic dividend and capital injection problem for spectrally positive lévy processes. Insurance: Mathematics and Economics 74, 135–146.

- Cheung and Wong (2017) Cheung, E., Wong, J., 2017. On the dual risk model with parisian implementation delays in dividend payments. European Journal of Operational Research 257, 159–173.

- Cheung et al. (2017) Cheung, E., Yang, H., Zhang, Z., 2017. Lévy insurance risk process with poissonian taxation. Scandinavian Actuarial Journal 2017 (1), 51–87.

- Cramér (1930) Cramér, H., 1930. On the mathematical theory of risk. Skand. Jubilee Volume. Stockholm.

- de Finetti (1957) de Finetti, B., 1957. Su un’impostazione alternativa della teoria collettiva del rischio. Transactions of the XVth International Congress of Actuaries 2, 433–443.

- Furrer (1998) Furrer, H., 1998. Risk processes perturbed by alpha-stable Lévy motion. Scandinavian Actuarial Journal 1998 (1), 59–74.

- Jeanblanc-Picqué and Shiryaev (1995) Jeanblanc-Picqué, M., Shiryaev, A. N., 1995. Optimization of the flow of dividends. Russian Mathematical Surveys 50 (2), 257–277.

- Kuznetsov et al. (2013) Kuznetsov, A., Kyprianou, A. E., Rivero, V., 2013. The theory of scale functions for spectrally negative Lévy processes. In: Lévy Matters II, Springer Lecture Notes in Mathematics. Springer.

- Kyprianou (2006) Kyprianou, A. E., 2006. Introductory lectures on fluctuations of Lévy processes with applications. Springer, Berlin.

- Kyprianou (2014) Kyprianou, A. E., 2014. Introductory Lectures on Fluctuations of Lévy Processes with Applications, 2nd Edition. Springer-Verlag: Berlin.

- Loeffen (2008a) Loeffen, R., 2008a. An optimal dividends problem with transaction costs for spectrally negative Lévy processes. Radon Institute for Computational and Applied Mathematics, Austrian Academy of Sciences.

- Loeffen (2009) Loeffen, R., 2009. An optimal dividends problem with a terminal value for spectrally negative lévy processes with a completely monotone jump density. Journal of Applied Probability 46 (1), 85–98.

- Loeffen et al. (2014) Loeffen, R., Renaud, J., Zhou, X., 2014. Occupation times of intervals until first passage times for spectrally negative Lévy processes. Stochastic Processes and their Applications 124 (3), 1408–1435.

- Loeffen (2008b) Loeffen, R. L., 2008b. On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes. Annals of Applied Probability 18 (5), 1669–1680.

- Lundberg (1909) Lundberg, F., 1909. Über die Theorie der Rückversicherung. Transactions of the VIth International Congress of Actuaries 1, 877–948.

- Mazza and Rullière (2004) Mazza, C., Rullière, D., 2004. A link between wave governed random motions and ruin processes. Insurance: Mathematics and Economics 35 (2), 205–222.

- Noba et al. (2018) Noba, K., Pérez, J.-L., Yamazaki, K., Yano, K., 2018. On optimal periodic dividend strategies for Lévy processes. Insurance: Mathematics and Economics 80, 29–44.

- Pardo et al. (2015) Pardo, J., Pérez, J., Rivero, V., 2015. The excursion measure away from zero for spectrally negative Lévy processes. Annales de l’Institut Henri Poincaré Probabilités et Statistiques 54 (1).

- Pérez and Yamazaki (2018) Pérez, J., Yamazaki, K., 2018. Mixed periodic-classical barrier strategies for Lévy risk processes. Risks 6 (2).

- Pérez and Yamazaki (2017) Pérez, J.-L., Yamazaki, K., 2017. On the optimality of periodic barrier strategies for a spectrally positive Lévy process. Insurance: Mathematics and Economics 77, 1–13.

- Protter (2005) Protter, P., 2005. Stochastic Integration and Differential Equations, 2nd Edition. Springer-Verlag, Berlin-Heidelberg.

- Tu (2017) Tu, V., 2017. On optimal period dividend strategies in actuarial surplus models. Ph.D. thesis, UNSW.

- Yang et al. (2013) Yang, H., Yang, H., Zhang, Z., 2013. On a Sparre Andersen risk model perturbed by a spectrally negative Lévy process. Scandinavian Actuarial Journal 2013 (3), 213–239.

- Yao et al. (2011) Yao, D., Yang, H., Wang, R., 2011. Optimal dividend and capital injection problem in the dual model with proportional and fixed transaction costs. European Journal of Operational Research 211, 568–576.

A Proof of Equation (5.3)

From equation (8.9) in Kyprianou (2014), we have for

and therefore by taking derivative of the function , we can conclude that such function is decreasing. Hence we have

for . Further noting that for and the function is an increasing function in and using (see Lemma 3.3 in Kuznetsov, Kyprianou, and Rivero, 2013) we get

This shows that for

i.e. the function is an increasing fucntion. Consequently, by using the second expression in (4.2) we have that

is an increasing function in . This gives

as desired.

B Proof of Lemma 6.2

We express the Lévy process using Lévy-Itô decomposition as

| (B.1) |

where is a standard Brownian motion and is a Poisson random measure (independent of the Brownian motion ) in the measure space (see e.g. Kyprianou (2014) Chapter 2 for details).

For any , the corresponding surplus process is a semi-martingale which takes the form

| (B.2) |

Here we note that is an adapted pure jump process which does not jump at the same time as a.s. In addition, Condition 2 implies that is bounded on sets for all .

Let be the sequence of stopping times defined by , by applying the change of variables formula (Theorem II.32 of Protter (2005)) to the stopped process , conditioning on , we have

| (B.3) |

Plugging in the formula of from (B.1) and collecting the terms for , we get

| (B.4) |

where

| (B.5) |

We further express (B.4) as

| (B.6) |

By denoting , where

| (B.7) |

we can rewrite (B.6) as

where by condition 3 we have

or equivalently

since by Condition 2.

Condition 1 implies that is a zero mean martingale, hence by taking expectation we have

Finally, note that a.s. and that by Condition 2 . By applying Fatou’s lemma, we have

| (B.8) |

C Proof of Theorem 7.1

We proceed using exiting identities (from Albrecher, Ivanovs, and Zhou, 2016) together with strong Markov properties, which is a standard probabilistic argument. In particular, we will borrow some results from Chen, Yang, and Yongxia (2017), where the expected values of interest are computed.

Due to the nature of the strategy, the surplus process is controlled only when . Therefore, we derive the expressions of for and separately. We start with the case when . We now define the following quantities:

| (C.1) | ||||

| (C.2) | ||||

| (C.3) | ||||

| (C.4) |

The value function for is given by the following lemma.

Lemma C.1.

For , we have

| (C.5) |

Proof of Lemma C.1.

Next, we consider the case when .

Lemma C.2.

For , we have

| (C.11) | |||

| (C.12) |

where

| (C.13) | |||

| (C.14) | |||

| (C.15) |

For the functions and defined, we present the following identities, which will be used in the next proof:

| (C.16) | |||

| (C.17) |

The value function for is given by the following lemma.

Lemma C.3.

For , we have

| (C.18) |

Proof of Lemma C.3.

It should be clear that the value function can be expressed in terms of and for all . We still need to find the 2 constants. We divide it into two cases depending on whether or not.

When , a liquidation at first opportunity strategy, in view of (C.18), using , we have

Further substituting and using , we obtain

or equivalently

| (C.21) |

When , substituting and in (C.18) and noticing , we have

| (C.22) | ||||

| (C.23) |

To solve and , we need to make sure that the determinant of

is non-zero. This property can be checked by noticing that it is always negative, i.e.

which is always true since the expression on the left hand side is equal to by (15) in Albrecher, Ivanovs, and Zhou (2016). Hence, we are able to solve and using (C.22) and (C.23). The values of the constants, and , are given by

| (C.24) | ||||

| (C.25) |

D Proof of Lemma 8.2 and Proposition 8.3

D.1 Proof of Lemma 8.2

D.2 Proof of Proposition 8.3

The goal is to show that there is a unique root for , .

We first show the existence of a root. This is achieved by showing (1) goes to infinity when goes to infinity and (2) so that a root for exists by continuity.

To compute the derivative, we will use the following identity:

| (D.1) |

This can be shown by the following:

Hence, we have

| (D.2) |

Furthermore, by direct computation, we have

| (D.3) |

Therefore, we have

| (D.4) |

Using (C.19), putting , we have

| (D.5) |

Substituting (D.5) into (D.4), we get

| (D.6) |

Hence, we have

| (D.7) |

since from (4.2) is increasing in , is bounded above by , and is bounded below by . This implies

Next, we show that . Suppose and therefore we have . In view of the definition of in (8.6), we have

| (D.8) |

Hence, it suffices to show that the term inside the last bracket above is strictly positive for . To do so, we use the following inequality for ,

which is justified by the fact that the function defined above is the value function of a (continuous) barrier strategy with barrier level in Bayraktar, Kyprianou, and Yamazaki (2013), which is by definition non-negative. In particular, inserting in the above yields

| (D.9) |

To this end, we notice that equation (5.3) readily yields , which further implies , for . Thus, we have from (D.9) that

On the other hand, if , in view of the definition of in (8.6), when , we have

| (D.10) |

which is essentially the same as if we replace and by and respectively. In this sense, if we differentiate the above w.r.t. , we will obtain the formula (D.6) except we do not have the term , i.e.

Now, by noting that the term inside the last bracket in the first term is

for due to (5.7). Therefore, we can conclude that

Combining with , we can conclude that there is a root for provided that .

Finally, we show the uniqueness of the root. Suppose there is a root satisfying , then we have by the definition of , where . From (8.4), we have

and subsequently

| (D.11) |

Now, if there is a such that and , there must exist another root such that and since , and is continuously differentiable. However, this leads to a contradiction as is negative if and only if and (see Section 5).

Next, if there is a such that and , we have and hence by (8.3)

However, the right hand side of the equation is by (5.5) while the left hand side is at most . This is a contradiction as for all .

Therefore, it is impossible to have and at the same time. Hence we have whenever , which implies that is the only root such that as is continuous.

Thus, there is one and only one root for .

Finally, to show , we observe

| (D.12) |

Remark D.1.

We should note that the root is continuous in , because (i) the root is unique with strictly positive derivative and (ii) the formula of defined in (8.6), as a function of , is continuous.

E Proof of Lemma 10.1

We first establish the following:

-

1.

as a function of is strictly increasing on , and

-

2.

for , and

-

3.

for any .

Proof of Property 1.

Via differentiating with respect to , we get

| (E.1) | ||||

because of (8.7). Hence, the proof is complete. ∎

Proof of Property 2.

Proof of Property 3.

We want to show for any . The case for is trivial. For , Property 2 implies that exists. Using the fact that , we can conclude that exists. We shall show the limit is zero. Note that the smoothness condition for is equivalent to

| (E.3) |

Since the left hand side is a strictly increasing function, for any , there is a corresponding to such such that the value function of the periodic strategy is smooth. As a result, we have . Furthermore, since exists, we can conclude that

for large enough . Now, we can write

where . It should be clear that the expected value goes to when goes to infinity. Therefore, we can conclude for any . ∎

Suppose when the transacion costs are , we have , or equivalently , where satisfies the smoothness condition (E.3). This means

| (E.4) |

Now, suppose further the fixed transaction costs increases to . In view of Property 1, it means an increase in on the r.h.s. of (E.3) must be compensated by an increase in on the r.h.s. of (E.3). Hence, we must choose a larger for to achieve smoothness. The new upper barrier is denoted as . Since for a fixed , is decreasing in (Property 2), we have

| (E.5) |

which shows when the transaction costs are .

In summary, increasing can never help to avoid . As such, we shall choose

| (E.6) |

with the convention .