conjectureConjecture \newsiamthmexampleExample \newsiamthmproblemProblem \newsiamthmquestionQuestion \newsiamthmassumptionAssumption \newsiamremarkremarkRemark \newsiamremarkhypothesisHypothesis \headersZeroth-Order Regularized Optimization (ZORO)HanQin Cai, Daniel Mckenzie, Wotao Yin, and Zhenliang Zhang

Zeroth-Order Regularized Optimization (ZORO): Approximately Sparse Gradients and Adaptive Sampling††thanks: This paper has been accepted to SIAM Journal on Optimization (SIOPT) and will be published electronically soon.

Abstract

We consider the problem of minimizing a high-dimensional objective function, which may include a regularization term, using only noisy evaluations of the function. Such optimization is also called derivative-free, zeroth-order, or black-box optimization. We propose a new Zeroth-Order Regularized Optimization method, dubbed ZORO. When the underlying gradient is approximately sparse at an iterate, ZORO needs very few objective function evaluations to obtain a new iterate that decreases the objective function. We achieve this with an adaptive, randomized gradient estimator, followed by an inexact proximal-gradient scheme. Under a novel approximately sparse gradient assumption and various different convex settings, we show the (theoretical and empirical) convergence rate of ZORO is only logarithmically dependent on the problem dimension. Numerical experiments show ZORO outperforms existing methods on both synthetic and real datasets.

keywords:

zeroth-order optimization, black-box optimization, derivative-free optimization, compressible gradients, sparse gradients, sparse adversarial attack90C56, 65K05 , 68T05, 68Q25

1 Introduction

Zeroth-order optimization, also known as derivative-free or black-box optimization, appears in a wide range of applications where either the objective function is implicit or its gradient is impossible or too expensive to compute. These applications include structured prediction [47], reinforcement learning [14], bandit optimization [17, 41] optimal setting search in material science experiments [31], adversarial attacks on neural networks [25, 36], and hyper-parameter tuning [42]. In this work, we propose a new method, which we coin ZORO, for high dimensional regularized zeroth-order optimization problems:

| (1) |

where is an explicit convex extended real-valued function (i.e. ) and is accessible only via a noisy zeroth-order oracle:

| (2) |

where is the unknown oracle noise. When we call the oracle with an input , it returns in which changes every time. Employing a regularizer allows us to use prior knowledge about the problem structure explicitly, without expending additional queries. For example, regularizers can be used to enforce or encourage non-negativity (), box constraints (), or solution sparsity (). Allowing to be extended real-valued means any constrained problem: with convex can be reduced to (1); just take to be the indicator function defined as:

Gradient compressibility

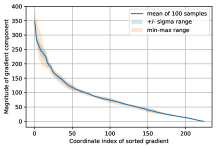

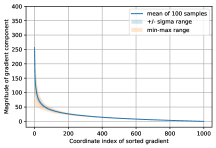

Since queries are typically assumed to be expensive, the appropriate metric for comparing zeroth-order methods is the number of oracle queries needed to achieve a target accuracy. In order to find an -optimal solution, a generic zeroth-order algorithm requires at least queries [21]. When is large, this cost can be prohibitive. ZORO reduces the dependence on from linear to logarithmic by exploiting gradient compressibility, by which we mean that the sorted components of decay like for some exponent . Gradient compressibility is largely unexplored in the zeroth-order optimization community, although we note the works [48, 1] which exploit the more restrictive gradient sparsity assumption (see Assumption 1.2.a). However, in many common applications of zeroth-order optimization (for example, hyperparameter tuning [6] and simulation-based optimization [24]), it has been empirically observed that is sensitive to only a few variables at a time. These variables thus carry significantly larger weights in , making it compressible. Our own experiments (see Figure 1) reinforce the idea that gradient compressibility is surprisingly ubiquitous in real-world problems. We emphasize that by assuming gradient compressibility instead of gradient sparsity, we are allowing for completely dense gradients (see Figure 1). Moreover, the subset of indices corresponding to the largest entries in can change for different .

Inexact prox-gradient descent

ZORO’s main iteration is based on the prox-gradient descent method but uses an approximate gradient constructed using randomized finite differences and compressed sensing. Key to our analysis is a careful estimation of the gradient error, , which comes from the following four components: the oracle noise, the finite differencing, the error due to compressed sensing, and the “tail error” due to approximating by its best -sparse approximation. Although there are many prior results in the literature characterizing the iteration complexity of (prox-) gradient descent using an inexact gradient [39, 19, 46, 4], they do not precisely fit our situation. For example, [39] requires with , which is not the case for ZORO. Thus we prove new results on convergence of inexact (prox-) gradient descent that may be of independent interest.

Lower query complexity

Our improved analysis of prox-gradient descent, together with our gradient error estimates, enable us to prove ZORO exceeds the state-of-the-art in terms of query complexity, at least for functions exhibiting gradient sparsity or compressibility. Specifically, for convex , ZORO finds an -optimal solution using only queries. For restricted strongly convex , this complexity improves to . For non-convex , ZORO finds an -stationary point using queries. We mention two caveats to these results. Firstly, they require where is a constant controlled primarily by the magnitude of the oracle noise . As we do not assume zero-mean oracle noise, such a lower bound on achievable accuracy is unavoidable. Secondly, as ZORO incorporates some stochasticity, these results are probabilistic. However, the probability of failure is so infinitesimally small, it is almost certain to never occur.

Adaptive sampling

Empirically, we have observed gradients are less compressible for closer to the optimal solution. Hence, practical methods need to dynamically choose the number of large components of to target. To this end, we introduce AdaZORO, a version of ZORO employing an adaptive sampling strategy. In the absence of gradient compressibility AdaZORO reduces to a fixed step-size descent method using the “linear interpolation” gradient estimator shown to be effective in [3]. So, AdaZORO exploits sparsity when it is present, and incurs no penalty when it is not.

Boundedness of iterates

Let denote the solution set of (1) (taking for simplicity). A common difficulty in analyzing the convergence of many iterative zeroth-order (and first-order) optimization methods is to show the sequence of distances between the iterates and remains bounded. Typically, this is either assumed directly [4] or shown by assuming (i) is a singleton (i.e. ) [39, 20], or (ii) there exists an such that for all in the level set [44, 46, 5]. For convex , this “bounded level sets” assumption (i.e. assumption (ii)) is equivalent to assuming is compact [7, Proposition B.10], in which case (i) is a special case of (ii). However, for many functions exhibiting gradient sparsity or compressibility, is decidedly non-compact. For example, the sparse quadratic problem (see synthetic dataset I, case (a) in Section 7.1) has . As such we cannot use the usual tools for showing boundedness of the iterates, and are forced to develop a new approach using an extended notion of coercivity.

Empirical validation

ZORO achieves its improved query complexity by exploiting gradient compressibility. Thus, it is natural to question how common this property is in real-world problems. We show empirically that gradients for two common problems, portfolio optimization and adversarial attacks on neural networks, are indeed highly compressible (see Figure 1). We show for such problems the theoretical query complexity of ZORO is realized in practice.

The rest of the paper is laid out as follows. In the remainder of Section 1, we discuss the necessary assumptions and notation, summarize the major contributions of this work, and state our main results. In Section 2, we provide bounds on the gradient estimate error in ZORO. Sections 3 and 4 contain our technical results on the convergence rates of inexact (prox-) gradient descent while Section 5 discusses the issue of iterate boundedness. Section 6 presents ZORO with Adaptive sampling (AdaZORO) while Section 7 contains the results of our numerical experiments. Finally, in Appendix A we clarify several issues regarding functions with sparse gradients that were unclear in the prior literature.

1.1 Notation

For an integer , we define . For any vector or matrix, counts the non-zero entries, is the entry-wise norm, and is the norm. We shall frequently use , or simply when the point in question is clear. We write and , when . Similarly, or when , where is the -th iterate. By we mean the best -sparse approximation to :

while denotes the -th largest-in-magnitude component of . We use to denote the sub-differential of at , a potentially set-valued operator. As is convex this is always well-defined. By we shall mean the limiting sub-differential: (recall ) [29]. A necessary, but not sufficient, condition for to be a minimizer of is [30]. If is convex we say is a -optimal solution to (1) if . For non-convex we say is -stationary if there exists a satisfying . Recall denotes the solution set of (1). For convex , and non-empty define . As is convex (because is) this projection is well defined.

1.2 Assumptions

We present a series of assumptions used in this paper. {assumption}[Sparse/compressible gradients]

Compressibility does not explicitly specify support size , but for it implies [33, Section 2.5]:

| (3) | |||

| (4) |

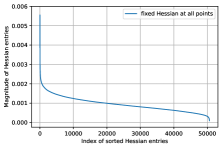

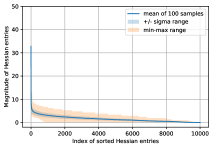

We also need an assumption which encodes the rapid decay of the sorted entries of the Hessian (see Figure 2). We follow [48] and assume: {assumption}[Weakly sparse Hessian] is twice differentiable and there exists a constant such that for all . Figure 2 suggests we may take to be small, as and the sorted decay rapidly. It is possible to weaken Assumption 1.2 substantially; the bound on need only hold for in the level set . For ease of exposition we do not do so here. Next we combine two standard assumptions on smoothness and existence of minimizers. {assumption}[Solution existence and Lipschitz gradients] (i) The solution set of is non-empty. (ii) is -Lipschitz differentiable, i.e. for any . We are not assuming access to , only that the Lipschitz property holds. {assumption}[Adversarially noisy oracle] We only have access to through a noisy zeroth-order oracle: with for all .

Remark 1.1.

In the stochastic optimization literature (e.g. [20, 1]), it is common to assume where is a random variable and while placing a bound on the second moment of the gradient: . Although our bounded noise model is a somewhat stronger assumption, it allows us to consider noise which is not zero-mean — the so-called adversarial noise model as it allows for an adversary that chooses each perturbation maliciously.

The final two assumptions prescribe a growth rate on . {assumption}[Restricted strong convexity] (i.e. either or ) is restricted -strongly convex, i.e. for all :

| (5) |

1.3 Prior work

Many approaches to zeroth-order optimization use the following template:

-

1.

Construct an estimator of .

-

2.

Take a negative gradient step .

The finite difference approach: , where is a sampling radius and denotes the -th canonical basis vector was introduced as FDSA [22]. This results in an accurate estimator, but requires queries per iteration, and thus is not query-efficient. To overcome this, randomized estimators were employed in SPSA [43] and Random Search [34, 35] that use only two queries per iteration. We mention also the work of [17], which requires only one query per iteration (but at the cost of a slower convergence rate) and the coordinate-descent-style approaches of [44, 23]. Variance reduced versions of Random Search [12, 27, 38, 1] which use queries to produce a lower variance estimator yield empirically better performance, but achieve the same asymptotic rate of convergence as Random Search. Recently, several works [48, 14, 10, 3, 9] have considered finite differences as noisy approximations to the directional derivatives and investigated various regression schemes for recovering from these linear measurements. We discuss the relationship between this line of work and our own in Section 2.

As querying the oracle is typically expensive, the most important metric for comparing zeroth-order optimization algorithms is their query complexity, defined as the number of queries required to find an iterate such that . Here, there are two different approaches to the analysis. One can assume that the oracle noise, , is zero mean, in which case arbitrarily small is possible. If is not zero mean, there is a lower bound on stemming from the fact that when the magnitude of the gradient is of the same order as the noise no further progress can be made. The former approach yields higher complexity; [20] showed if is Lipschitz differentiable and convex then Random Search finds an -optimal solution in queries, while [21] showed any algorithm for this problem necessarily requires queries. Faster rates are achievable in the latter approach, but only for lower bounded by a constant depending on the noise level. Common to both approaches is a polynomial dependence of query complexity on .

In order to break this unfortunate dependence on , [48] and [1] assume exact gradient sparsity (Assumption 1.2.a). Specifically, [48] uses LASSO to construct and assumes zero mean noise to achieve a query complexity of . [1] claims that gradient descent, using the Random Search estimator , benefits from implicit regularization and automatically achieves a query complexity of , assuming zero mean noise, as long as the step size is carefully chosen. Unfortunately, their analysis is flawed and only holds when the support of is the same for all . We discuss this further in Appendix A. Neither of these works considers compressible gradients, (Assumption 1.2.b), non zero-mean noise or any notion of strong convexity.

Finally, we note the many works [26, 8, 39, 19, 32, 4] that study gradient descent: , where is a biased estimator of the true gradient . As any estimator derived from zeroth-order queries is necessarily biased, these results are closely connected to the convergence analysis of zeroth-order methods. We discuss the relationship between these results and our own in Sections 3 and 4.

1.4 Contributions

We summarize the contributions of this paper.

-

(i)

We introduce the idea of gradient compressibility to zeroth-order optimization.

-

(ii)

We propose an algorithm, ZORO, which exploits gradient compressibility.

-

(iii)

We show theoretically ZORO has a query complexity only logarithmically dependent on the extrinsic dimension . Proving this requires overcoming a number of technical challenges, particularly analyzing inexact prox-gradient descent with constant gradient error and proving the iterates remain bounded even though the level sets of are not bounded.

-

(iv)

We propose a heuristic improvement to ZORO, called AdaZORO, which dynamically adapts to varying levels of gradient compressibility.

-

(v)

We provide empirical evidence that gradient compressibility occurs in real-world applications. We also show numerically ZORO (and AdaZORO) can successfully exploit this gradient compressibility.

1.5 Main results

Our first result is for the non-regularized case, but allows for compressible gradients. Theorems 1.2 and 1.3 (and Lemma 3.1 and Theorem 4.1) depend on a constant satisfying for all .This is analogous to the constant in [4, Assumption 4.5], the constant in [5, Assumption 5.1], the “level set radius” in [46] or the diameter of the feasible set in [48, Assumption 2]. Indeed, in the special case where is the indicator function of a compact convex set one can simply take . As discussed in Section 1, we cannot use the bounded level sets assumption because many exhibiting sparse gradients do not have this property. In Section 5, we deduce the existence of such an from coercivity properties of (i.e. Assumption 1.2).

Theorem 1.2 (No regularizer, compressible gradients).

Suppose is convex and satisfies Assumptions 1.2.b, 1.2, 1.2, 1.2.a and 1.2.b. Choose large enough so and choose . Then ZORO finds an -optimal solution in queries for any . If instead of Assumptions 1.2.a and 1.2.b, satisfies Assumption 1.1, then this query complexity improves to:

Both query complexities hold with probability .

Our second result allows for . Due to technical difficulties, we only prove this result for sparse gradients. Empirically, we have observed excellent performance of ZORO with regularizer for having merely compressible gradients (see Section 7.3).

Theorem 1.3 (Regularized, sparse gradients).

Suppose is convex and satisfies Assumptions 1.2.a, 1.2–1.2. Suppose is convex and satisfies Assumptions 1.2.a and 1.2.c. Choose and . Then ZORO finds an -optimal solution in queries, for any . If instead of Assumptions 1.2.a and 1.2.c satisfies Assumption 1.1, this query complexity improves to:

for any . Again, both query complexities hold with probability .

Remark 1.4.

The constants – arise from the use of compressed sensing to reconstruct . They depend on the particular algorithm used (we use CoSaMP) and the number of iterations this algorithm is run for. They do not depend on or .

We also provide the following convergence-to-stationarity theorem for non-convex , which does not require any coercivity assumptions

2 Estimating the gradient

Choose the number of queries and a sampling radius , and let be Rademacher random vectors (i.e. with equal probability for ). Other types of random vectors certainly work too, but for conceptual clarity we restrict to Rademacher. Each measurement is:

| (6) |

As in [48, 13] we think of the as noisy approximations to directional derivatives:

Proof 2.2 (Proof of Lemma 2.1).

Let , and . Define to be the sensing matrix whose -th row is . Then:

| (7) |

Several recent works attempt to recover from (7). [3] considers taking measurements and solving the linear system, while [48] assumes is exactly sparse and solves the LASSO problem111Their approach is slightly different as they approximate and using the same LASSO problem:

| (8) |

In [13], recovering by solving the more general regularized regression problem:

is proposed, and in the special case (i.e. LP decoding) bounds on are proved which allow for an extraordinary amount of noise, but require . In this work, we approximate by using a greedy approach on the nonconvex problem:

| (9) |

Let us briefly mention several advantages this approach enjoys over prior work:

- (i)

- (ii)

- (iii)

- (iv)

We shall use CoSaMP [33] for (9). We emphasize that is a sparse approximation to the true gradient . When is sparse or compressible, this approximation is highly accurate. When is neither sparse nor compressible, is still likely to be a descent direction, and thus can still be used within a gradient descent scheme.

2.1 Analysis of CoSaMP for gradient estimation

has the -Restricted Isometry Property (-RIP) if, for all with :

for some . If is proportional to then as constructed above will have the -RIP almost surely:

Theorem 2.3 (Theorem 5.2 of [2]).

If , then has the -RIP with with probability . Here and are constants independent of and .

The choice of is to match with the assumptions of [18], the main result of which we state next. Recall denotes the best -sparse approximation to .

Theorem 2.4 (Theorem 5 of [18]).

We emphasize this result is universal, i.e. it holds for all with the stated probability. The exact values of and are provided in [18]. One can make smaller by making larger [18]. The constants are the same as in Theorem 2.3. Other initializations are possible; for example, we have found using at the -th iteration offers a modest speedup.

Theorem 2.5.

Proof 2.6.

We now bound the error terms in our measurements:

Lemma 2.7.

and .

Proof 2.8.

Theorem 2.9.

If , i.e. the oracle is noise-free, the second term on the right-hand side of (11) drops out and one can make the third term arbitrarily small by choosing the sampling radius sufficiently small. If then there is a lower bound to how small we can make the right-hand side of (11):

Corollary 2.10.

Suppose and that the other assumptions are as in Theorem 2.9. Choosing provides the tightest possible error bound of:

Proof 2.11.

This follows by minimizing with respect to .

3 Gradient descent with relative and absolute errors

We consider the problem of minimizing using inexact gradient descent: , where

| (12) |

Lemma 3.1.

Suppose is convex and satisfies Assumptions 1.2, 1.2.a and 1.2.b. Suppose for all satisfies (12) with . Choose . Then:

where is a constant satisfying for all determined by the coercivity conditions (1.2.a and 1.2.b). If instead of Assumptions 1.2.a and 1.2.b we assume satisfies Assumption 1.1 then this rate improves to:

Various forms of this result are well-known ([4, 19] and [7, Section 1.2]), but we were unable to find a precise statement in the literature allowing for non-decreasing and or restricted strongly convex . Hence, we provide a proof in Section 3.2.

3.1 Deducing Theorem 1.2 from Lemma 3.1

Before proving Lemma 3.1 let us explain how Theorem 1.2 will follow from it. Squaring Corollary 2.10:

with probability . Choose , the number of iterations of CoSaMP performed, large enough so , in which case as long as . Note that . For any we may solve for guaranteeing :

Recall ZORO makes queries per iteration. Multiplying this number by the number of required iterations (i.e. ) yields the first result. For strongly convex by the same line of reasoning for any we may guarantee as long as:

Again, multiplying by the number of queries per iteration yields the result.

3.2 Proof of Lemma 3.1

First, we need two lemmas:

Lemma 3.2 (Sequence analysis I).

Consider a sequence with and for all , where and . If we have

while if we have for all .

Proof 3.3.

If , then , so . Dividing the condition by and reorganizing yields

Summing, we obtain when and when . Inverting both sides yields the claim.

Lemma 3.4 (Sequence analysis II).

Consider a sequence with and for all , where and . Then .

Proof 3.5.

Applying the condition recursively, we get:

Thus proving the claim.

We now prove the main result of this section:

Proof 3.6 (Proof of Lemma 3.1).

4 Prox-gradient descent using inexact gradients

Here, we consider minimizing using prox-gradient descent (also known as forward-backward splitting): . Recall the proximal operator is defined as:

When exact gradients are available and is exactly computable, prox-gradient descent is known to converge at the same rate as gradient descent [37]. This is particularly useful when is non-smooth. We consider the situation where one can compute exactly but one only has access to inexact gradients of satisfying . In this section .

Theorem 4.1.

Suppose is convex and satisfies Assumption 1.2. Suppose is convex and satisfies Assumptions 1.2.a and 1.2.c. Suppose for all while can be computed precisely. Choose . Then:

where and is a constant satisfying for all determined by the coercivity conditions (1.2.a and 1.2.c). If instead of Assumption 1.2 satisfies Assumption 1.1 then:

In simpler terms, this theorem gives convergence to an error horizon proportional to . If is -restricted strongly convex then we get linear convergence to an error horizon proportional to . [39] proves a similar rate, without error horizon, for the case where with the sequence summable.

4.1 Deducing Theorem 1.3 from Theorem 4.1

Let us again explain how one can deduce the query complexity for ZORO (Theorem 1.3) from Theorem 4.1. If satisfies Assumption 1.2.a then from Corollary 2.10:

for all with probability , choosing sufficiently large so . For any we solve for to guarantee :

Multiplying this number by , as in the proof of Theorem 1.2, yields the first result. If is restricted strongly convex, then by the same line of reasoning for any , we get from Theorem 4.1 that for:

Multiplying by the number of queries per iteration yields the claimed query complexity.

4.2 Proof of Theorem 4.1

Before proceeding we quantify, under very general conditions, the expected decrease per iteration. From the first order optimality condition of prox: , where . It will be convenient to introduce the following notation:

| Actual direction: | ||||

| Ideal direction: | ||||

| Stationarity: |

Lemma 4.2 (Descent Lemma).

Proof 4.3.

An immediate consequence of Lemma 4.2 is the following result:

Theorem 4.4.

Proof 4.5.

Lemma 4.6 (Sequence analysis III).

Consider a sequence with and

| (21) |

where . Let . Then for .

Note that the logarithm makes much smaller than .

Proof 4.7.

Partition into disjoint sets and . For we have geometric decrease: .

In the rest of this proof, we restrict ourselves to the set of such that and no longer state it explicitly. For example, by , we mean in the intersection of and the restriction. Note that, when , the set has all . The restriction gives us

so is monotonically non-increasing. It takes at most first entries to ensure, for , we have , so define and we get for . Dividing (21) by and reorganizing:

So except for no more than iterations, we have . In each of those iterations, does not increase. Hence, the stated result holds.

Lemma 4.8 (Sequence analysis IV).

Consider a sequence with and , where , for all . Then for .

Proof 4.9.

Rearranging the recurrence relation gives us . Applying this recursively yields:

We now prove our main results by showing that satisfies the recurrences described in Propositions 4.6 and 4.8.

Lemma 4.10.

Proof 4.11.

Using boundedness of the iterates (proved below in Section 5) and the above lemmas we now prove the main result of this section.

Proof 4.12 (Proof of Theorem 4.1).

5 Boundedness

In this section, we show the coercivity assumptions (Assumption 1.2) are sufficient to guarantee the sequence is bounded.

Proposition 5.1.

Proof 5.2.

This proof proceeds via three steps.

-

1.

For any , define the level set . As is coercive, for any , there exists an such that if then . Equivalently, for all .

-

2.

Rewriting (13), we obtain:

(22) As , we have . As is coercive with respect to , there exists a such that if then (where are as in (22)). We use this to establish, via induction, that:

(23) From (22) one easily checks the base case: . Suppose that (23) holds at the -th step. Then either , in which case appealing to (22), we obtain:

or whence (by the coercivity of ) we obtain:

-

3.

Finally, let . From part 2, it follows that for all . From part 1, it then follows that there exists an such that for all , thus proving the theorem.

Our second result allows for regularization () but requires .

Proposition 5.3.

Proof 5.4.

This proof is similar to that of Proposition 5.1.

-

1.

For any define the level set . Again, as is coercive there exists an such that for all .

-

2.

Using , from (18), we get:

(24) Because is coercive with respect to , there exists a such that if then for all . We now establish, via induction, that:

(25) The base case () is easily verified. So, suppose (25) holds at , i.e. . Now, either or . If the former holds, we are done. So, suppose the latter. By the coercivity of , we have as (see the definition in Section 4.2) whence by (24),

(26) -

3.

Finally, let . From part 2, it follows for all , and by construction. Appealing to part 1, there again exists an such that for all .

For any adversarially noisy oracle (Assumption 1.2), these coercivity conditions are also necessary. To see this, consider the following one-dimensional example. Take and let be the Huber loss function:

While is coercive, is not coercive with respect to (i.e. does not satisfy Assumption 1.2.b). Suppose in Assumption 1.2 satisfies . From Corollary 2.10, we get, at worst,

That is, for all , the noise can be chosen adversarially such that , hence the inexact gradient descent may diverge.

6 Adaptive sampling

Ideally, ZORO should work without assuming gradient compressibility, but still be able to exploit this when it arises. Moreover, the support of the previous gradient estimate is important information that should not be ignored. We present an algorithm, coined Adaptive ZORO (AdaZORO), incorporating these observations as Algorithm 2. Informally, the gradient estimator in AdaZORO proceeds as:

- 1.

- 2.

- 3.

At worst, AdaZORO makes queries per iteration. Empirically, AdaZORO works very well on real-world datasets. For example, in the asset risk management experiment (see Section 7.3), but AdaZORO converges rapidly with approximate gradients having only to nonzero entries.

7 Numerical experiments

We compared ZORO to FDSA [22], SPSA [43] and the LASSO-based algorithm from [48] (abbreviated as LASSO in the rest of this section). We did not test any global algorithms (e.g. REMBO [49]) due to their strong correlations with problem structures. For the synthetic experiments in Sections 7.1 and 7.2, we only use vanilla ZORO (i.e. Algorithm 1), so we do not gain extra advantage with adaptive sampling. We use AdaZORO (i.e. Algorithm 2) for the real-world asset risk management problem in Section 7.3. For sparse adversarial attack problem in Section 7.4, we find the gradients are highly compressible and using vanilla ZORO is sufficient. A sample implementation of ZORO and AdaZORO can be found online at https://github.com/caesarcai/ZORO.

7.1 Synthetic dataset I: Query efficiency

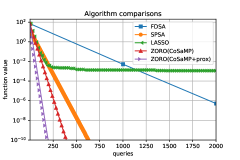

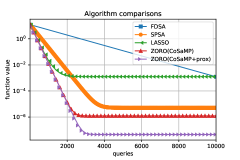

Consider , where is a diagonal matrix. We tested: (a) exactly sparse case with 20 randomly generated diagonal positive numbers; (b) compressible case where diagonal elements are non-zeros that diminish exponentially— with . For both cases, we used two versions of ZORO: ZORO(CoSaMP) without enforcing any constraints and ZORO(CoSaMPprox) with a proximal operator to enforce non-negativity.

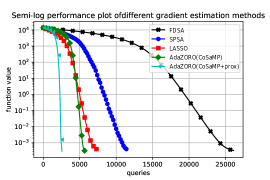

The results of case (a) are shown in Figure 3a. ZORO(CoSaMPprox) required -th of the queries that FDSA required, and a third of the queries required by SPSA. Without the proximal operator, ZORO(CoSaMP) has less of an advantage, but is still noticeably cheaper than FDSA and SPSA, in terms of queries. LASSO consistently gets stuck around an accuracy of , and required more queries than both versions of ZORO before it converged.

The results of test (b) are summarized in Figure 3b. Due to the ill-conditioned nature of the problem, none of the tested methods converged to arbitrarily small accuracy. However, ZORO(CoSaMPprox) and ZORO(CoSaMP) achieved the best and second-best accuracy, respectively. They also exhibited the best query efficiency.

We conducted two additional experiments to further illustrate the advantages of using ZORO over SPSA222Note that our implementation of SPSA uses Rademacher random perturbation vectors . Thus, it coincides with Random Search.. We used the following two challenging objective functions:

Max--squared-sum function

, where is the -th largest-in-magnitude entry of . This function has sparse gradients, and achieves every possible support set .

Rotated sparse quadratic function

Pick an arbitrary sparse binary vector with 10% randomly located entries equal to 1. Consider the function , where is a random orthonormal matrix and is a diagonal matrix with uniform random entries. The gradients of are not obviously compressible, but empirically most randomly sampled gradients are. The solution is sparse, so we can incorporate this prior knowledge using a regularizer to accelerate convergence.

For both functions we repeated 10 experiments per dimension, using random initial points with unit norm. We ran each experiment until the objective error reached a threshold of of the initial objective error. Figure 4 depicts the means and standard deviations of the number of queries used for both functions. As is apparent, the query complexity of ZORO increases much more slowly than that of SPSA. In Figure 4a, where is fixed while increases, it is clear that the query complexity of ZORO is only weakly dependent on .

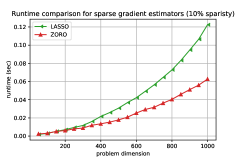

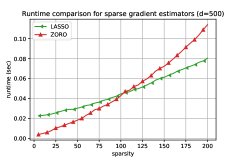

7.2 Synthetic dataset II: Computational efficiency

In this section, we investigate the computational efficiency of the sparse gradient estimators in LASSO and ZORO. The experiments were executed on a Windows 10 laptop with Intel i7-8750H CPU (6 cores at 2.2GHz) and 32GB of RAM.

We consider the quadratic function , where is a diagonal matrix with non-zero randomly generated positive elements. As shown in Figure 3a, LASSO has trouble estimating the gradients precisely when close to the optimal points, so we compared the speed of the sparse gradient estimators by averaging the results at randomly selected points. We use the same function queries for both gradient estimators. We emphasize that ZORO does not gain any additional advantage from a lower number of samples or better convergence in these speed experiments. The runtime per gradient estimation was evaluated with varying problem dimension (see Figure 5a) and sparsity level (see Figure 5b). We find the gradient estimator in ZORO is faster when the problem dimension is large and sparsity level is small while the gradient estimator in LASSO is faster when is small and is large. Since we are more interested in the high dimensional problems with sparse gradients, ZORO appears to have noticeable speed advantage in our problem setting.

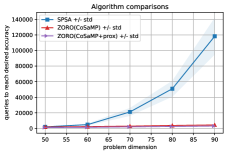

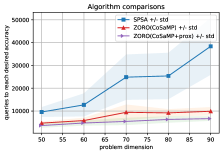

7.3 Asset risk management

Consider a portfolio consisting of different assets, where and denote the fraction of the portfolio invested in, and the expected return of, asset respectively. denotes the covariance matrix of asset returns. The portfolio risk, which we aim to minimize, is . We used the correlation, mean, and standard deviation of 225 assets from the dataset of [11]. Our goal is to minimize the risk function subject to the expected return constraint We penalize the risk to formulate the problem as:

Optionally, a non-negative constraint ( for all ) can be added to this problem, and it can be imposed by a proximal operator. In this experiment, instead of solving this quadratic program directly, consider a problem proposer who wishes to keep the formulation and data private and only offers noisy zeroth-order oracle access.

As the appropriate is not clear a priori, we use the adaptive sampling strategy (i.e. AdaZORO) for this problem. The results are shown in Figure 6. When was unconstrained, the query efficiency of AdaZORO(CoSaMP) was twice as good as SPSA and five times as good as FDSA; moreover, it saves around queries as compared to LASSO. When imposing the non-negativity constraint via a proximal operator, AdaZORO(CoSaMPprox) further improved the query efficiency to be twice as good as LASSO. All solutions in this test matched the optimal value found via quadratic programming (using full knowledge of ), which is approximately .

7.4 Sparse adversarial attack on ImageNet

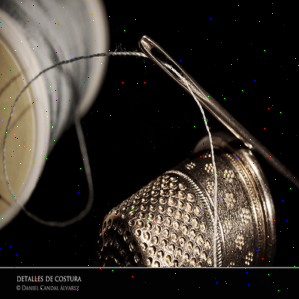

We tested generating black-box adversarial examples using ZORO. We used Inception-V3 model [45] on ImageNet [15] and focused on per-image adversarial attacks. The authors in [12] considered a similar problem by optimizing the attack loss and the norm of image distortion. In contrast, we aimed to find distortions for single images such that the attack loss and the norm of distortion are minimized: Similar to [12], we use ZORO to attack 100 random images from ImageNet that are correctly classified by Inception-V3. We compared ZORO with ZO-AdaMM, ZO-SGD, and ZO-SCD [12]. ZO-SCD is essentially a variation of FDSA, and ZO-SGD is a mini-batched version of SPSA. All of these methods led to extremely large distortions, except ZO-SCD, which had the worse distortion. Hence, successful attacks required distorting nearly all pixels. We used the same setup in [12]: queries at each iteration and check if the attack succeeds before iterations. As the problem dimension is very large () we use a block coordinate descent version of ZORO. In each iteration we randomly selected a subspace of 2000 dimensions (pixels) and generated random perturbations only in this subspace. We took and , and performed iterations. Although prior sparse adversarial attacks exist (e.g. SparseFool [28]), we appear to be the first to connect adversarial attacks to sparse zeroth-order optimization. Table 1 presents the experimental results. ZORO had the highest attack success rate while having the lowest average distortion. Surprisingly, the average distortion of ZORO was also the best. The average query complexity of ZORO is slightly worse than the other methods tested, as it uses more queries at each iteration. Some pictures of successful sparse attacks by ZORO are presented in Figure 7.

| Methods | ASR | dist | dist | Iter |

|---|---|---|---|---|

| ZO-SCD | ||||

| ZO-SGD | ||||

| ZO-AdaMM | ||||

| ZORO | 90 | 0.73 | 21.1 | 59 |

| Median filter | RSR | Dist rate | TOT reduction |

|---|---|---|---|

| size = 2 | |||

| size = 3 | 92 | 7 | 14 |

| size = 4 | |||

| size = 5 |

Out of curiosity, we tested mitigating our sparse attacks by applying a median filter, a common method to remove speckle noise. We used Inception-V3 on the attacked-then-filtered imaged to check whether true labels are obtained, i.e. whether or not the attack has been mitigated. We also applied the same filter to the original (un-attacked) images to check if they reduced label accuracy. Let denote the set of adversarial images that are successfully attacked by ZORO, denote the set of image IDs that are not recovered, and denote the set of image IDs that are mis-classified. The recovery success rate (RSR), , is the ratio of images in been identified to the true label after filtering. The distortion rate, , is the ratio of images been assigned an incorrect label. Note that there are some overlapping IDs in and . The total accuracy reduction, , summarizes these two experiments. The test results are presented in Table 2. While mitigating many attacks, the median filter also distorted the original images, causing lower classification accuracies.

References

- [1] K. Balasubramanian and S. Ghadimi, Zeroth-order (non)-convex stochastic optimization via conditional gradient and gradient updates, in Advances in Neural Information Processing Systems, 2018, pp. 3455–3464.

- [2] R. Baraniuk, M. Davenport, R. DeVore, and M. Wakin, A simple proof of the restricted isometry property for random matrices, Constructive Approximation, 28 (2008), pp. 253–263.

- [3] A. S. Berahas, L. Cao, K. Choromanski, and K. Scheinberg, A theoretical and empirical comparison of gradient approximations in derivative-free optimization, Foundations of Computational Mathematics, (2021), pp. 1–54.

- [4] A. S. Berahas, L. Cao, and K. Scheinberg, Global convergence rate analysis of a generic line search algorithm with noise, SIAM Journal on Optimization, 31 (2021), pp. 1489–1518.

- [5] E. H. Bergou, E. Gorbunov, and P. Richtarik, Stochastic three points method for unconstrained smooth minimization, SIAM Journal on Optimization, 30 (2020), pp. 2726–2749.

- [6] J. Bergstra and Y. Bengio, Random search for hyper-parameter optimization, The Journal of Machine Learning Research, 13 (2012), pp. 281–305.

- [7] D. P. Bertsekas, Nonlinear programming, Journal of the Operational Research Society, 48 (1997), pp. 334–334.

- [8] D. Blatt, A. O. Hero, and H. Gauchman, A convergent incremental gradient method with a constant step size, SIAM Journal on Optimization, 18 (2007), pp. 29–51.

- [9] H. Cai, Y. Lou, D. Mckenzie, and W. Yin, A zeroth-order block coordinate descent algorithm for huge-scale black-box optimization, in International Conference on Machine Learning, PMLR, 2021, pp. 1193–1203.

- [10] H. Cai, D. Mckenzie, W. Yin, and Z. Zhang, A one-bit, comparison-based gradient estimator, arXiv preprint arXiv:2010.02479, (2020).

- [11] T.-J. Chang, N. Meade, J. E. Beasley, and Y. M. Sharaiha, Heuristics for cardinality constrained portfolio optimisation, Computers & Operations Research, 27 (2000), pp. 1271–1302.

- [12] X. Chen, S. Liu, K. Xu, X. Li, X. Lin, M. Hong, and D. Cox, ZO-AdaMM: Zeroth-order adaptive momentum method for black-box optimization, in Advances in Neural Information Processing Systems, 2019, pp. 7202–7213.

- [13] K. Choromanski, A. Pacchiano, J. Parker-Holder, Y. Tang, D. Jain, Y. Yang, A. Iscen, J. Hsu, and V. Sindhwani, Provably robust blackbox optimization for reinforcement learning, in Conference on Robot Learning, 2020, pp. 683–696.

- [14] K. Choromanski, M. Rowland, V. Sindhwani, R. Turner, and A. Weller, Structured evolution with compact architectures for scalable policy optimization, in International Conference on Machine Learning, PMLR, 2018, pp. 970–978.

- [15] J. Deng, W. Dong, R. Socher, L.-J. Li, K. Li, and L. Fei-Fei, Imagenet: A large-scale hierarchical image database, in 2009 IEEE conference on computer vision and pattern recognition, Ieee, 2009, pp. 248–255.

- [16] J. Fan and R. Li, Variable selection via nonconcave penalized likelihood and its oracle properties, Journal of the American statistical Association, 96 (2001), pp. 1348–1360.

- [17] A. D. Flaxman, A. T. Kalai, and H. B. McMahan, Online convex optimization in the bandit setting: gradient descent without a gradient, arXiv preprint cs/0408007, (2004).

- [18] S. Foucart, Sparse recovery algorithms: sufficient conditions in terms of restricted isometry constants, in Approximation Theory XIII: San Antonio 2010, Springer, 2012, pp. 65–77.

- [19] M. P. Friedlander and M. Schmidt, Hybrid deterministic-stochastic methods for data fitting, SIAM Journal on Scientific Computing, 34 (2012), pp. A1380–A1405.

- [20] S. Ghadimi and G. Lan, Stochastic first-and zeroth-order methods for nonconvex stochastic programming, SIAM Journal on Optimization, 23 (2013), pp. 2341–2368.

- [21] K. G. Jamieson, R. Nowak, and B. Recht, Query complexity of derivative-free optimization, in Advances in Neural Information Processing Systems, 2012, pp. 2672–2680.

- [22] J. Kiefer, J. Wolfowitz, et al., Stochastic estimation of the maximum of a regression function, The Annals of Mathematical Statistics, 23 (1952), pp. 462–466.

- [23] B. Kim, H. Cai, D. McKenzie, and W. Yin, Curvature-aware derivative-free optimization, arXiv preprint arXiv:2109.13391, (2021).

- [24] C. G. Knight, S. H. Knight, N. Massey, T. Aina, C. Christensen, D. J. Frame, J. A. Kettleborough, A. Martin, S. Pascoe, B. Sanderson, et al., Association of parameter, software, and hardware variation with large-scale behavior across 57,000 climate models, Proceedings of the National Academy of Sciences, 104 (2007), pp. 12259–12264.

- [25] A. Kurakin, I. Goodfellow, and S. Bengio, Adversarial machine learning at scale, in International Conference on Learning Representations, 2017.

- [26] Z.-Q. Luo and P. Tseng, Error bounds and convergence analysis of feasible descent methods: a general approach, Annals of Operations Research, 46 (1993), pp. 157–178.

- [27] H. Mania, A. Guy, and B. Recht, Simple random search provides a competitive approach to reinforcement learning, arXiv preprint arXiv:1803.07055, (2018).

- [28] A. Modas, S.-M. Moosavi-Dezfooli, and P. Frossard, Sparsefool: a few pixels make a big difference, in Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, 2019, pp. 9087–9096.

- [29] B. S. Mordukhovich, Variational analysis and generalized differentiation I: Basic theory, vol. 330, Springer Science & Business Media, 2006.

- [30] B. S. Mordukhovich, N. M. Nam, and N. Yen, Fréchet subdifferential calculus and optimality conditions in nondifferentiable programming, Optimization, 55 (2006), pp. 685–708.

- [31] N. Nakamura, J. Seepaul, J. B. Kadane, and B. Reeja-Jayan, Design for low-temperature microwave-assisted crystallization of ceramic thin films, Applied Stochastic Models in Business and Industry, 33 (2017), pp. 314–321.

- [32] A. Nedić and D. P. Bertsekas, The effect of deterministic noise in subgradient methods, Mathematical programming, 125 (2010), pp. 75–99.

- [33] D. Needell and J. A. Tropp, CoSaMP: Iterative signal recovery from incomplete and inaccurate samples, Applied and computational harmonic analysis, 26 (2009), pp. 301–321.

- [34] Y. Nesterov and V. Spokoiny, Random gradient-free minimization of convex functions, Technical report, Universite catholique de Louvain, Center for Operations Research and Econometrics, (2011).

- [35] Y. Nesterov and V. Spokoiny, Random gradient-free minimization of convex functions, Foundations of Computational Mathematics, 17 (2017), pp. 527–566.

- [36] N. Papernot, P. McDaniel, I. Goodfellow, S. Jha, Z. B. Celik, and A. Swami, Practical black-box attacks against machine learning, in Proceedings of the 2017 ACM on Asia conference on computer and communications security, 2017, pp. 506–519.

- [37] E. Ryu and W. Yin, Large-scale convex optimization via monotone operators, 2020.

- [38] T. Salimans, J. Ho, X. Chen, S. Sidor, and I. Sutskever, Evolution strategies as a scalable alternative to reinforcement learning, arXiv preprint arXiv:1703.03864, (2017).

- [39] M. Schmidt, N. L. Roux, and F. R. Bach, Convergence rates of inexact proximal-gradient methods for convex optimization, in Advances in neural information processing systems, 2011, pp. 1458–1466.

- [40] F. Schöpfer, Linear convergence of descent methods for the unconstrained minimization of restricted strongly convex functions, SIAM Journal on Optimization, 26 (2016), pp. 1883–1911.

- [41] O. Shamir, On the complexity of bandit and derivative-free stochastic convex optimization, in Conference on Learning Theory, 2013, pp. 3–24.

- [42] J. Snoek, H. Larochelle, and R. P. Adams, Practical bayesian optimization of machine learning algorithms, in Advances in neural information processing systems, 2012, pp. 2951–2959.

- [43] J. C. Spall, An overview of the simultaneous perturbation method for efficient optimization, Johns Hopkins apl technical digest, 19 (1998), pp. 482–492.

- [44] S. U. Stich, C. L. Muller, and B. Gartner, Optimization of convex functions with random pursuit, SIAM Journal on Optimization, 23 (2013), pp. 1284–1309.

- [45] C. Szegedy, V. Vanhoucke, S. Ioffe, J. Shlens, and Z. Wojna, Rethinking the inception architecture for computer vision, in Proceedings of the IEEE conference on computer vision and pattern recognition, 2016, pp. 2818–2826.

- [46] R. Tappenden, P. Richtárik, and J. Gondzio, Inexact coordinate descent: complexity and preconditioning, Journal of Optimization Theory and Applications, 170 (2016), pp. 144–176.

- [47] B. Taskar, V. Chatalbashev, D. Koller, and C. Guestrin, Learning structured prediction models: A large margin approach, in Proceedings of the 22nd international conference on Machine learning, 2005, pp. 896–903.

- [48] Y. Wang, S. Du, S. Balakrishnan, and A. Singh, Stochastic zeroth-order optimization in high dimensions, in International Conference on Artificial Intelligence and Statistics, 2018, pp. 1356–1365.

- [49] Z. Wang, M. Zoghi, F. Hutter, D. Matheson, and N. De Freitas, Bayesian optimization in high dimensions via random embeddings, in Twenty-Third International Joint Conference on Artificial Intelligence, 2013.

- [50] H. Zhang, The restricted strong convexity revisited: analysis of equivalence to error bound and quadratic growth, Optimization Letters, 11 (2017), pp. 817–833.

Appendix A Functions with sparse gradients

Let be a zero-mean Gaussian random vector with covariance matrix the identity. Define , the Gaussian smoothing of . In [1] it is claimed, below Assumption 4 on pg. 7, that if then . This is false in general, as Theorem A.1 shows. Because this is not true, the following key line (see pg. 4 of the supplementary) in the proof of Lemma C.2 of [1]:

is not correct, and thus Lemma C.2 is false. Because Lemma C.2 is crucial for the proofs of Theorems 3.1 and 3.2 in [1], these Theorems are also false. As far as we can tell, the only way to fix these theorems is to replace the assumption: for all with the more restrictive fixed support assumption: for all for some fixed .

Theorem A.1.

Suppose is continuously differentiable and for all . If there exist with , then for all .

Before proving this theorem, it is useful to introduce some notation and provide some preliminary lemmas. Let denotes the Gaussian kernel:

| (27) |

Observe that is the convolution of and :

Lemma A.2.

Suppose is continuously differentiable and let . If there exists an open set such that for all then for all .

Proof A.3.

First, observe that if is continuously differentiable then:

| (28) |

where is a well-known property of convolutions. Because is an analytic function, is also analytic as convolution preserves analyticity. But then it follows from basic properties of analytic functions that if is zero on an open set it is zero everywhere.

We now prove the theorem by using some fundamental results in Fourier analysis:

Proof A.4.

Let denote the Fourier transform. Suppose that are continuously differentiable. We shall use the following well-known facts about :

-

1.

.

-

2.

If then .

-

3.

Let be the Gaussian kernel (27). Then .

Pick any and let We claim that . First, observe is continuously differentiable (in fact, analytic) because is analytic. Thus, there exists an open set containing upon which the support of is constant: for all . Pick any . If then for all . Then, by Lemma A.2, for all . Now apply the Fourier transform:

where (a) follows from (28), (b) follows from Fact 1, and (c) follows from Fact 3. In other words:

But, for all , hence for all . That is, is the zero function. Appealing to Fact 2 above, is also the zero function. That is, for all . This is a contradiction as so by definition . Hence we must have , and thus . The same argument implies that . Because but we have that , thus proving the theorem.

Theorem A.5.

Suppose is continuously differentiable and for all . Then cannot be strongly convex.

Proof A.6.

Recall if is strongly convex then there exists a such that for all :

| (29) |

Pick any and let . As in the proof of Theorem A.1, because is continuously differentiable there exists an open set such that for all . Shrinking further if necessary we may assume is convex. Pick any and let denote the -th canonical basis vector; then clearly for all . Choose , where is small enough such that . By the fundamental theorem of calculus:

where (a) holds because is convex and thus for all . Moreover, . Returning to (29), if were strongly convex we would have for some , a clear contradiction.