On the Role of Surrogates in the Efficient Estimation of Treatment Effects with Limited Outcome Data

Abstract

In many investigations, the primary outcome of interest is difficult or expensive to collect. Examples include long-term health effects of medical interventions, measurements requiring expensive testing or follow-up, and outcomes only measurable on small panels as in marketing. This reduces effective sample sizes for estimating the average treatment effect (ATE). However, there is often an abundance of observations on surrogate outcomes not of primary interest, such as short-term health effects or online-ad click-through. We study the role of such surrogate observations in the efficient estimation of treatment effects. To quantify their value, we derive the semiparametric efficiency bounds on ATE estimation with and without the presence of surrogates and several intermediary settings. The difference between these characterize the efficiency gains from optimally leveraging surrogates. We study two regimes: when the number of surrogate observations is comparable to primary-outcome observations and when the former dominates the latter. We take an agnostic missing-data approach circumventing strong surrogate conditions previously assumed. To leverage surrogates’ efficiency gains, we develop efficient ATE estimation and inference based on flexible machine-learning estimates of nuisance functions appearing in the influence functions we derive. We empirically demonstrate the gains by studying the long-term earnings effect of job training.

Keywords: Surrogate Observations, Causal Inference, Average Treatment Effect, Semiparametric Efficiency, Double Robustness.

1 Introduction

In many causal inference applications, it may be expensive, inconvenient or infeasible to measure the outcome of primary interest. Nevertheless, some auxiliary variables that are faster or easier to measure may be available. In clinical trials for AIDS treatment, the primary outcome is often mortality, which may take years of follow-up to fully reveal. But clinically relevant biomarkers like viral loads or CD4 counts can be measured quite rapidly (Fleming et al., 1994). In comparative effectiveness research for long-term impact of therapies, e.g., long-term quality of life measures, many patients may drop-out so their responses are missing. But short-term outcomes, e.g., responses shortly after the therapy, may be well recorded (Post et al., 2010). In program evaluation for addiction prevention projects, accurately measuring the primary outcome, e.g., smoking behavior, may require costly chemical analysis of saliva samples for the presence of cotinine, and thus are available for only a limited number of participants. Yet self-report data are relatively inexpensive to collect (Pepe, 1992). In offline conversion analysis, we wish to assess the effect of a digital marketing campaign on visitation to a brick-and-mortar location. And, while we can only observe visitation for individuals for whom we have cellphone geolocation data and who we can match to ad identifiers, we can observe digital ad clicks for all units. We refer to these easy-to-obtain auxiliary variables as surrogate outcomes or simply surrogates, which are often informative about or correlate with the primary outcome of interest.

There has been considerable interest in using surrogates as a replacement for the missing primary outcome to reduce data collection costs in causal inference. For example, the U.S. Food and Drug Administration (FDA) launched the Accelerated Approval Program to allow for early approval of drugs based on a clinically relevant surrogates, aiming to speed up clinical trials for drug approval (FDA, 2016). This program is spurred by the urgent need to determine the efficacy of new drugs quickly and economically. As stated by the National Center for Advancing Translational Sciences (NCATS) of the U.S. National Institutes of Health, many thousands of diseases known to affect humans do not have any approved treatment yet; meanwhile, a novel drug can “take 10 to 15 years and more than $2 billion to develop” (NCATS, 2019). Therefore, accelerating drug approval is of great value and urgency to both pharmaceutical companies and patients. Using surrogates that can be measured more easily provides a promising way toward this goal.

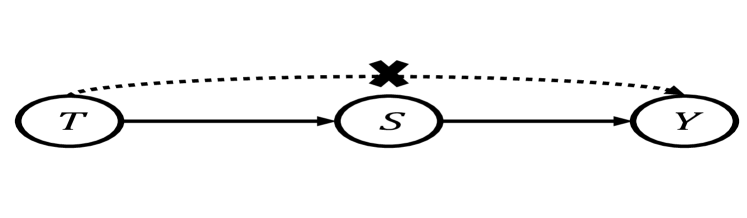

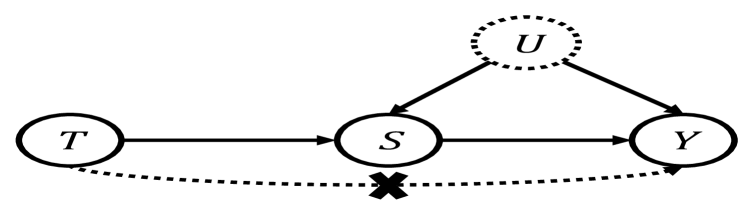

However, one major challenge is that surrogates may not be perfectly indicative of the primary outcome, so a misuse may lead to severe or even disastrous consequences. For example, three drugs (encainide, flecainide, and moricizine) were approved by FDA based on early success of supressing ventricular arrhythmia (surrogate), but in later follow-up trials the drugs alarmingly increased mortality (primary outcome) (Fleming and DeMets, 1996; Echt et al., 1991). It was estimated that the use of these drugs resulted in 50,000 excess deaths in the U.S. (Moore, 1997). To resolve these problems, a wide variety of criteria have been proposed to ensure that it is adequate to base causal inference solely on the surrogate without observing the primary outcome at all. However, using these criteria to search for a valid surrogate to replace the primary outcome is still extremely challenging, since the criteria impose stringent assumptions that may often be violated in practice (see Related Literature in Section 1.2 and Appendix A). For example, the “statistical surrogate” condition (e.g., Prentice, 1989; Athey et al., 2019) requires the primary outcome to be conditionally independent of the treatment given surrogates, i.e., surrogates must fully explain away the dependence of the outcome on the intervention meant to affect it. Not only does this condition require full mediation of the treatment effect, it is also easily invalidated if there is any other common cause of both surrogates and the primary outcome, which is often unavoidable even in ideal randomized trial settings (see Appendix A). Thus this surrogate condition, and similarly many other criteria that render surrogates perfect replacements for primary outcomes, are very prone to violation in practice.

In this paper, we view surrogates as supplements instead of replacements for the primary outcome. We consider combining surrogates with the primary outcome, and investigate how this proposal can improve the efficiency of treatment effect estimation. Such combination is possible because in practice paired observations of both the primary outcome and surrogates are often available for at least some units. By incorporating a limited number of primary-outcome observations, we can avoid the aforementioned problems resulting from relying on surrogates alone, and circumvent stringent surrogate conditions. Instead, we only assume standard causal inference assumptions and a typical missing data assumption that the primary outcome is missing (conditionally) at random (MAR), i.e., any interdependence between the primary outcome value and whether it is observed or not may be explained by other observed variables (i.e., pre-treatment covariates, treatment, surrogates). Similar missingness conditions are also commonly assumed in previous literature that combine different datasets (e.g., Athey et al., 2019; Cheng et al., 2018; Zhang and Bradic, 2019). Under only these standard assumptions, and in particular no overly restrictive surrogate conditions, we aim to investigate the role of surrogates in estimating treatment effects when the primary-outcome observations are limited.

We first study the possible extent of benefit achievable by leveraging surrogate information. Using the theory of semiparametric efficiency, we derive the efficiency lower bound of estimating the average treatment effect (ATE) on the primary outcome (Theorem 2.1). This lower bound characterizes the fundamental statistical limit in estimating ATE under our assumptions, in that it is the best possible precision of ATE estimation that can be asymptotically achieved by any regular estimator. By comparing the efficiency lower bounds both with and without the presence of surrogates, and bounds in several intermediary settings (Theorems 2.2 and 2.2.1), we precisely quantify the efficiency gains from surrogates, namely, the benefit of surrogates in terms of allowing us to estimate treatment effects up to the same precision with fewer observations of the primary outcome.

We find that using surrogates is particularly advantageous when (i) the primary outcome is missing for a large number of units, and (ii) the surrogates are reasonably predictive of the primary outcome, in that they can account for large variations of the primary outcome that cannot be explained by the pre-treatment covariates, but they need not determine them exactly or render them independent of treatment. These theoretical results provide insightful guidelines for understanding when surrogates can yield significant benefits. Moreover, we show that essentially the same efficiency lower bound (under appropriate reformulation) reigns across two different regimes: when the size of the unlabeled data is comparable to the size of the labeled data (Theorem 2.1), and when the former is much larger than the latter (Theorems 4.1 and 4.2). In the second regime, the commonly assumed overlap condition (Assumption 3 condition (8)) fails and the efficiency analysis under MAR setting becomes more challenging. Our paper tackles this very practical setting when enormous amounts of cheap unlabeled data may be available.

We further propose an ATE estimator that can optimally leverage the efficiency gains from surrogates and achieves the efficiency lower bound. The proposed estimator involves some nuisance parameters that are of no intrinsic interest but need to be estimated first. By employing a cross-fitting technique (e.g., Chernozhukov et al., 2018; Zheng and Laan, 2011), we can allow for any flexible machine learning estimators to be used for the nuisance parameters as long as they satisfy some generic convergence rate conditions. We show that the proposed estimator converges to the true ATE value, even if only some but not all nuisance parameters are consistently estimated (Theorem 3.1). If all nuisance parameters are indeed consistently estimated under generic rate conditions, then the proposed estimator is asymptotically normal centered at the true ATE value and its asymptotic variance attains the efficiency lower bound (Theorems 3.2 and 4.2). Furthermore, we construct asymptotically valid confidence intervals based on a simple plug-in estimator for the asymptotic variance of our ATE estimator (Theorem 3.3). In summary, we propose an ATE estimator that can leverage the power of flexible machine learning estimators for nuisance estimation, is robust to nuisance estimation errors, achieves full asymptotic efficiency in leveraging surrogate information, and may be combined with easy-to-use inference.

Our paper is organized as follows. In Section 1.1, we set up the problem of treatment effect estimation with surrogates when the primary outcome is not fully observed, and introduce our notation. In Section 2, we derive the efficiency lower bound for ATE estimation in our setting, and compare it with bounds in other benchmark settings to characterize the efficiency gains from surrogates. We then construct an asymptotically efficient estimator and prove its asymptotic properties in Section 3. In Section 4, we extend the efficiency and estimation results to the setting where the amount of unlabeled data is much larger than amount of labeled data. We point out the efficiency and estimation results in this setting are consistent with those in Sections 2 and 3. In Section 5, we use our methods to study the effect of a job training intervention on earnings at a later follow up using data from a large-scale randomized controlled trial (Hotz et al., 2006; Athey et al., 2019) and we demonstrate the gains due to employing surrogates and due to our methods. We provide concluding remarks in Section 6. In Appendices B, A and C, we provide supplementary discussions about the “statistical surrogate” condition, the connection of our work to some previous literature, and additional details that expand on our results from Section 4, respectively. All proofs are relegated to Appendix D.

1.1 Problem Setup

Let denote a treatment indicator variable (i.e., means being treated with a therapy of interest, and means control), denote baseline covariates measured prior to treatment (e.g., patients’ demographic characteristics and health measurements before treatment), and denotes the outcome variable of primary interest (e.g., patients’ health outcome after treatment). Following the Neyman-Rubin potential outcome framework (Neyman, 1923; Rubin, 2005), we assume the existence of two potential outcomes corresponding to the outcomes that would have been realized under each treatment option. We assume that the actual observed outcome is the potential outcome corresponding to the actual treatment, i.e., , which encapsulates the non-interference and consistency assumptions in causal inference (Imbens and Rubin, 2015). Our goal is to estimate the average treatment effect (ATE):

| (1) |

If we could observe for all units, then we could estimate the ATE by many existing methods (e.g., Imbens and Rubin, 2015).

In this paper, we consider a more challenging setting where the primary outcome cannot be observed for all units, due to long follow-up, drop-out, budget constraints, etc. Nonetheless, we can observe for all units some surrogates (i.e., intermediate outcomes) that may be informative about the primary outcome (i.e., a long-term outcome). Since surrogates are measured after the treatment assignment, they may also be affected by the treatment. Thus we hypothesize the existence of two potential surrogate outcomes analogously, and assume . We use to denote the indicator of whether the primary outcome is observed. In summary, we can observe a labeled subset , and an unlabeled subset , where NA stands for “not available” (missing value), and and are the index sets for labeled data and unlabeled data respectively. We denote , as the corresponding sample sizes for these two datasets, and as the total sample size. We represent the th data point as , and assume that each data point (in both labeled subset and unlabeled subset) is given by coarsening an independent and identically distributed (i.i.d) draw from a population with distribution characterized by a probability measure . In particular, the coarsening map transforming such draws to the data we actually observe is given by

| (2) |

We let denote the distribution on induced by . Depending on the context, we may use to denote expectation with respect to either or .

Assumption 1 (Unconfoundedness).

For ,

| (3) |

In Assumption 1, we first assume that the treatment assignment is unconfounded in the combined population of labelled and unlabelled data. In Lemma 2.2, we will show that this condition is guaranteed if the treatment is unconfounded in both the labelled and unlabelled subpopulation, separately, when additional missing-at-random assumptions are imposed. This condition requires that include all potential confounders that can affect the primary outcome and treatment simultaneously, or the surrogate and treatment simultaneously. It is trivially satisfied by design in clinical trials where the treatment is assigned totally at random.

Assumption 2 (Missing at random).

For ,

| (4) |

In Assumption 2, we assume that the primary outcome is missing (conditionally) at random (MAR), i.e., the indicator depends on only observed variables, including pre-treatment covariates , the surrogates , and the treatment . This condition guarantees that the distribution of the primary outcome on the labeled data and unlabeled data are comparable after accounting for the observed variables, so that we can use the labeled data to infer information about the missing primary outcome in the unlabeled data. This condition is considerably weaker than the missing completely at random (MCAR) condition typically assumed in previous semi-supervised inference literature (e.g., Cheng et al., 2018; Zhang and Bradic, 2019), since MCAR does not allow the missingness of the primary outcome to depend on any other variable. Assumption 2 may be satisfied by design in a two-phase sampling scheme (e.g., Wang et al., 2009; Cochran, 2007): in the first phase, relatively cheap measurements of are available for all units, and in the second phase, expensive measurements of the primary outcome are collected for a validation subsample selected according to a selection rule based on variables measured in the first phase. For example, we may want to oversample units who self-report no-smoking behavior for further chemical analysis, if we suspect more misreporting in this subpopulation.

We next define some important quantities for ATE estimation. We first define the regression function of the primary outcome in the labeled dataset, conditional on treatment, covariates, and surrogates, and also the projection of onto the whole population, conditional on only treatment and covariates:

| (5) | ||||

| (6) |

We also define the propensity scores for treatment and labeling respectively:

Although these quantities are useful for estimating the ATE, they are of no intrinsic interest by themselves, so we refer to them as nuisance parameters. We let be the collection of the true nuisances. We further assume the following strict overlap assumption for the two propensity scores.

Assumption 3 (Strict Overlap).

There exist such that almost surely we have

| (7) | ||||

| (8) |

This assumption states that units with any given values of the conditioning variables above have at least probability of to receive each treatment option, and to get their primary outcome measured. This overlap assumption is common in causal inference and missing data literature (e.g., Imbens and Rubin, 2015; Little and Rubin, 2019). Note condition (8) implies that , so the size of the unlabeled data is necessarily comparable to the size of the labeled data, i.e., (unless all data is labeled). In Section 4, we will relax this condition and consider the setting where enormous cheap unlabeled data are available so that .

Below we show identification of the the ATE parameter .

Lemma 1.1.

If Assumptions 2, 1 and 3 hold, then

| (9) |

In this paper, we focus on the efficient estimation of ATE (i.e., in Eq. 1) when the primary outcome is missing for many units while surrogates can be fully observed for all. Notably, we only assume Assumptions 1 and 3 (and some straightforward variants) that are very typical in causal inference and missing data literature. In particular, we do not assume any strong surrogate conditions such as the “statistical surrogate” condition, , which may impose restrictions that can easily be violated in practice (see Section 1.2 and Appendix A for more discussion).

Notation.

We use to denote the nonstochastic and stochastic asymptotic orders, respectively. For nonstochastic sequences and , if and if . For a random variable sequence , we denote if for any positive constant , there exists a finite positive constant such that , and we denote if for any positive constant , as . We also use the notation and for asymptotic orders (both stochastic and nonstochastic). For example, for nonstochastic asymptotic order, if and , if , and if . For an appropriately measurable and integrable function , we use , , to denote the , and norms with respective to the measure : , , and . Throughout this paper, we use to denote unknown population quantities like and , and use denote estimators, i.e., .

1.2 Related Literature

Causal inference with surrogates.

Many different surrogate criteria have been proposed to guarantee that the treatment effect on a surrogate will reliably predict the treatment effect on the primary outcome. The statistical surrogate criterion proposed by Prentice (1989) was the first such criterion, which requires the primary outcome to be conditionally independent of the treatment, given the surrogate. Since then, many other criteria have been proposed to improve upon the statistical surrogate criterion, such as the principal surrogate criterion (Frangakis and Rubin, 2002), strong surrogate criterion (Lauritzen et al., 2004), consistent surrogate criterion (Chen et al., 2007), among many others. However, almost all of these criteria involve quantities that cannot be identified from the observed data, so they are unverifiable in practice. Moreover, many of them can easily run into a logical paradox described by Chen et al. (2007). See VanderWeele (2013) for a comprehensive review of surrogate criteria and Appendix A for a detailed discussion about the statistical surrogate condition.

While the literature above mostly focus on a single surrogate, Price et al. (2018); Wang et al. (2020) propose to estimate transformations of multiple surrogates to optimally approximate the primary outcome using labelled experimental data. Their optimal transformations can avoid the surrogate paradox described in Chen et al. (2007). Athey et al. (2019) consider identifying and estimating the average treatment effect with multiple surrogates in the setting where the primary outcome cannot be observed simultaneously with treatment variable and are instead observed in two separate datasets, connected only by the surrogates and covariates. This setting is practically very challenging, since the two datasets have no complete observations at all, with the primary outcome missing in one dataset and treatment missing in the other. To fuse these two incomplete datasets and have hope of relating the effect of treatments on downstream outcomes, they have to assume the statistical surrogate condition, which, however, may be too strong in practice as it requires both full mediation of treatment effect by the surrogates and the absence of any other common cause of primary outcome and surrogate (see Appendix A). Athey et al. (2020); imbens2022long use surrogates to combine experimental data with short-term observations and confounded observational data with long-term observations, the former using a latent unconfoundedness assumption and latter using multiple sequential surrogates as proxy variables. All of these focus on leveraging surrogates to enable identification, rather than improve efficiency in already-identified settings, as we do here.

Cheng et al. (2018) study efficient ATE estimation when combining a small number of primary-outcome observations with many observations of the surrogates, without assuming any surrogate criteria like those mentioned above. Their setting is closest to ours, except that they focus on the case when the unlabeled dataset is much larger than the labeled dataset, i.e., and they assume that the primary outcome is MCAR. In contrast, our paper studies both and and considers a more general MAR setting. By studying both and , we discover that essentially the same efficiency lower bound governs both regimes. Moreover, Cheng et al. (2018) consider certain specialized estimators based on parametric regressions and kernel smoothing, while our proposed estimator can leverage flexible machine learning nuisance estimation. See Appendix B for a more detailed comparison of our work with Cheng et al. (2018).

Semi-supervised inference.

Our paper is related to the growing body of literature on parameter estimation and inference in the semi-supervised setting where a small labeled dataset is enriched with a large unlabeled dataset. A stream of research has investigated how to the use unlabeled data to aid in the estimation of a wide variety of parameters, including regression coefficients (Azriel et al., 2016; Chakrabortty et al., 2018; Hou et al., 2021), population mean and average treatment effect (Zhang et al., 2019; Zhang and Bradic, 2019; Chakrabortty et al., 2022b; Zhang et al., 2021), quantiles and quantile treatment effect (Chakrabortty et al., 2022a, b), performance measures of a given classifier (Gronsbell and Cai, 2018), covariance (Chan et al., 2020), etc. These papers typically propose estimators for a finite dimensional target parameter and study their asymptotic performance, which supplement extensive literature on semi-supervised learning of predictive models (see Zhu and Goldberg, 2009, for a comprehensive review). Nearly all of these literature implicitly or explicitly assume that labels are MCAR. Our paper relaxes this assumption by allowing the labeling process to depend on pre-treatment covariates, the treatment, and even the surrogates, which is more realistic if the labeling process is not completely controlled by design. Moreover, while we study the intermediate setting of partial outcome labeling, our paper also studies and focuses on the use of surrogates as a source of extra information. Interestingly, when viewing the surrogates in our paper as empty, our results also recover results in existing semi-supervised inference literature, for example, Zhang and Bradic (2019). See Appendix B for details.

Measurement error problems with a validation sample.

We can also view our problem as a measurement error problem: abundant mismeasurements of the primary outcome (i.e., the surrogate observations) are available, while accurate measurements (i.e., the primary outcomes itself) are observed only on a small validation sample (i.e., the labeled dataset). In similar data settings, a variety of methods have been proposed to leverage observations with measurement noise to improve the efficiency of estimating regression coefficients (e.g., Pepe et al., 1994; Pepe, 1992; Reilly and Pepe, 1995; Engel and Walstra, 1991; Carroll and Wand, 1991; Chen and Chen, 2000) or solutions to estimation equations (e.g., Chen et al., 2008a, 2003, 2005, b), when either the outcome or covariates of interest are mismeasured. In particular, some of these works (e.g., Pepe, 1992; Chen et al., 2005) employ semiparametric methods that do not impose restrictive assumptions on the measurement errors, and use the validation sample to nonparametrically estimate the relationship between surrogate variables and the primary variable. Our paper follows the same principle, but we allow for arbitrary machine learning nuisance estimators under only generic rate conditions. Some literature also cast this type of problem as a missing data problem where the variables of primary interest are missing for all units not in the validation sample, and they study the semiparametric efficiency lower bound and efficient estimator for parameters in regression problems (e.g., Robins and Rotnitzky, 1995; Robins et al., 1994; Yu and Nan, 2006; Chen and Breslow, 2004). Our paper builds on the missing data framework to study the efficiency of estimating treatment effects in presence of surrogates. Moreover, in contrast to the missing data literature that commonly assume the proportion of complete observations to be bounded away from , our paper allows the complete-case proportion to vanish to in order to model the setting with enormous amounts of unlabeled surrogate data.

2 Efficiency Analysis

In this section we derive the efficiency lower bounds and efficient influence functions in a sequence of models ranging from no surrogate observations to full outcome observations on all data points, crucially including our primary setting of interest as a practical middle ground (see Table 1(a)). This serves to quantify both the information gain from surrogate observations relative to no surrogate observations and the gap remaining relative to full outcome observations. Later, this will also serve as motivation for the construction of our efficient ATE estimator.

2.1 Efficiency Analysis in the Presence of Surrogates

We first derive the efficiency lower bound for ATE estimation in our primary setting of interest as described in Section 1.1.

Theorem 2.1.

Let be the set of all distributions on induced by the coarsening map in Eq. 2 applied to any distribution on satisfying Assumptions 1, 3 and 2. The semiparametric efficiency lower bound for under model is where

| (10) |

Theorem 2.1 reveals the fundamental statistical limit in estimating with surrogates under Assumptions 1 and 3: for any regular estimator , the variance of the limiting distribution of must be no smaller than . In other words, is the best possible precision we can aim to achieve asymptotically among all regular estimators. The function is the efficient influence function for , which will be used to construct efficient estimators for in Section 3.

Notably, the efficiency lower bound here corresponds to the model that only assumes Assumptions 1 and 3, but not any other strong surrogate condition. To study the role of surrogates in the efficient estimation of ATE, we next consider the efficiency bound in a few other settings.

2.2 Efficiency Analysis in Other Settings

| ✓ | ✓ | ? | ✓ | |

| ⋮ | ⋮ | ⋮ | ⋮ | |

| ✓ | ✓ | ? | ✓ | |

| ✓ | ✓ | ? | ? | |

| ⋮ | ⋮ | ⋮ | ⋮ | |

| ✓ | ✓ | ? | ? |

| ✓ | ✓ | ✓ | ✓ | |

| ⋮ | ⋮ | ⋮ | ⋮ | |

| ✓ | ✓ | ✓ | ✓ | |

| ✓ | ✓ | ? | ? | |

| ⋮ | ⋮ | ⋮ | ⋮ | |

| ✓ | ✓ | ? | ? |

| ✓ | ✓ | ✓ | ✓ | |

| ⋮ | ⋮ | ⋮ | ⋮ | |

| ✓ | ✓ | ✓ | ✓ | |

| ✓ | ✓ | ✓ | ? | |

| ⋮ | ⋮ | ⋮ | ⋮ | |

| ✓ | ✓ | ✓ | ? |

| ✓ | ✓ | ✓ | ✓ | |

| ⋮ | ⋮ | ⋮ | ⋮ | |

| ✓ | ✓ | ✓ | ✓ | |

| ✓ | ✓ | ✓ | ✓ | |

| ⋮ | ⋮ | ⋮ | ⋮ | |

| ✓ | ✓ | ✓ | ✓ |

To quantify the benefit of surrogates in estimating ATE, we compare the efficiency lower bounds in following different settings.

Definition 1 (Four different settings).

- Setting I: no surrogate (Table 1(a)).

-

We observe for and observe for ;

- Setting II: surrogate only on labeled data (Table 1(b)).

-

We observe for and observe for ;

- Setting III: surrogate on all data (Table 1(c)).

-

We observe for and observe for ;

- Setting IV: fully labeled data (Table 1(d)).

-

We observe for all units.

From setting I to setting IV in Definition 1, more information is increasingly observed . Setting I corresponds to one extreme where no surrogates are observed at all, and setting IV corresponds to the other extreme where all variables (including the primary outcome) are always completely observed. In the intermediate setting II, we observe surrogates only for units whose primary outcome is already observed, and setting III corresponds to our primary problem setup in Section 1.1, where surrogates are always observed.

Each of these settings can be described by different choices for the coarsening map . To compare the efficiency gains of the additional information in each setting, we can consider the efficiency bound corresponding to the same as different coarsening maps are applied, each corresponding to one of the above settings. Each map induces a model given by the distributions induced by all that satisfy Assumptions 1 and 3. Crucially, we will need that in each setting we have identifiability, meaning that if and induce the same data distributions, , under , then they also induce the same ATE, , so that is a valid function of . This ensures we are in fact considering the same estimand in each of the models. In our primary setting (i.e., setting III), restricting to to satisfy Assumptions 1, 3 and 2 is enough to ensure identifiability. In settings I and II, since surrogates are not observed for some units, we need to further assume that whether the primary outcome is observed or not, i.e., indicator variable , does not depend on surrogates.

Assumption 4 (Missing at random, cont’d).

For , .

With this additional assumption, the ATE parameter is identifiable in all four settings, so we can compare the efficiency of estimating the same ATE in these different settings.

Lemma 2.1.

If Assumptions 1, 3, 2 and 4 all hold, then the ATE parameter is identified in all four settings in Definition 1.

In the following lemma, we summarize some additional implications of Assumption 4.

Lemma 2.2.

If Assumptions 2 and 4 hold, then Assumption 1 holds if and only if

| (11) |

Moreover, when Assumption 4 holds, and .

In Lemma 2.2, Equation 11 shows that under the missing-at-random assumptions in Assumptions 4 and 2, the treatment unconfoundedness over the combined population of the labelled and unlabelled data in Assumption 1 is equivalent to unconfoundedness over the two v subpopulations respectively. Moreover, Lemma 2.2 shows that Assumption 4 can also simplify two nuisances that appear in the efficient influence function in Theorem 2.1. This is very beneficial because the simplified nuisances are easier to estimate. For example, the nuisance function can be directly estimated by running regressions. In contrast, estimating the nuisance function in Equation 6 requires first estimating another nuisance in Equation 5 and then further projecting the estimated nuisances.

In the following theorem, we derive efficiency lower bounds for ATE in the four settings in Definition 1. We impose Assumption 4 even in settings III and IV where it is not needed for identification, else the four settings would not be comparable.

Theorem 2.2.

Under Assumptions 1, 3, 4 and 2, the efficiency lower bounds for in setting is for , where

In Theorem 2.2, we prove that the efficiency lower bound for setting III is identical to the bound in Theorem 2.1, meaning that the additional Assumption 4 has no impact on the efficiency bound. Moreover, we note that even though we have access to surrogates for at least a subset of units in setting II and IV, their efficiency lower bounds do not depend on surrogates . This means that surrogates cannot improve the efficiency of ATE estimation if surrogates are observed only when the primary outcome is already observed. Indeed, for units whose primary outcome is already observed, surrogates can provide no extra information for ATE, especially considering that we do not restrict the relationship between surrogates and the primary outcome at all (i.e., no parametric modeling assumptions). In contrast, for units whose primary outcome is missing, the observed surrogates do provide extra information, because under Assumptions 1, 3 and 2, we can learn the relationship between surrogates and the primary outcome based on the labeled data and extrapolate it to the unlabeled data to impute the missing primary outcome.

Corollary 2.2.1.

Suppose Assumptions 1, 3, 4 and 2 hold. Then:

-

1.

The efficiency gain from observing the surrogates on all units is measured by

-

2.

The information loss due to not fully observing the primary outcome is measured by

-

3.

Observing additional outcomes on the labeled data alone provides no improvement, that is, .

Corollary 2.2.1 quantifies the efficiency gain from optimally leveraging surrogates, and the efficiency gap to the ideal setting where the primary outcome is fully observed. It shows that the efficiency benefits of surrogates crucially depend on two factors: the predictiveness of the surrogates with respect to the primary outcome and the extent of missingness of the primary outcome.

Predictiveness of the surrogates. The efficiency gain due to surrogates (i.e., ) positively depends on the terms for i.e., the variations of the primary outcome that can be explained by surrogates but not by pre-treatment covariates. Similarly, the efficiency loss compared to the ideal setting (i.e., ) positively depends on for , i.e., the residual variations of the primary outcome that cannot be explained by either the surrogates or the pre-treatment covariates. This means that the more predictive the surrogates are, the more efficiency improvement can be achieved by leveraging the surrogates (i.e., larger ), and the closer the efficiency bound is to the ideal limit with fully observed primary outcome (i.e., smaller ). In the extreme, if surrogates can perfectly predict , i.e., there exists a deterministic function that maps to , then observing surrogates is equivalent to observing the primary outcome, and thus . Note this deterministic function need not be known.

Missingness of the primary outcome. Both quantities in Corollary 2.2.1 decrease with the labeling propensity scores and . This means that when the primary outcome is less missing (i.e., overall higher labeling propensity scores), the efficiency gains from additionally observing surrogates or the primary outcome both decrease. Indeed, if the primary outcome is already observed for most of the units, then the room for extra efficiency gain from observing surrogates (or, from observing more primary outcomes, for that matter) is small.

The efficiency analysis above provides important guidelines on when leveraging surrogates can improve the efficiency of ATE estimation. It shows that surrogates are particularly beneficial for ATE estimation when (1) surrogates can account for large variations of the primary outcome that cannot be explained by the pre-treatment covariates, and (2) the primary outcome for a large number of units is missing.

2.3 Aside: Other Target Populations

In the above we considered our estimand to be the ATE on the whole population described by . To identify this estimand, we require the treatment assignment to be unconfounded on the whole population (Assumption 1). According to Lemma 2.2, under the missing-at-random assumptions in Assumptions 4 and 2, the whole-population unconfoundedness Assumption 1 amounts to unconfoundedness on both the labelled () and unlabelled () subpopulations, separately.

We could easily consider the ATE on other target populations, for example, for either , that is, the ATE on the unlabeled or labeled subpopulation. We may be interested in if, for example, the unlabeled data is collected from an auxiliary source to augment a small study already involving the population of interest. Or, we may be interested in if the unlabelled data are easier to collect and more representative of the population of interest. For these alternative estimands, we only need the treatment assignment to be unconfounded for the target population of interest.

When the target estimand is the ATE on the labelled population , we only need unconfoundedness on the labelled population, i.e., . Moreover, we only need strict overlap assumption on the treatment assignment (namely, Equation 7 in Assumption 3). In particular, the missing-at-random assumptions in Assumptions 4 and 2 are not required. In this case, the surrogates are not useful since we already fully observe the primary outcome in the labelled population of interest. The semiparametric efficiency analysis of immediately follow from existing literature such as Hahn (1998).

When the target estimand is the ATE on the unlabelled population , we only need unconfoundedness on the unlabelled population. In the following theorem, we show the identification of and its semiparametric efficiency bound.

Theorem 2.3.

If and Assumptions 2 and 3 hold, then

The corresponding semiparametric efficiency bound is , where

and , .

Based on the efficient influence function in Theorem 2.3, we can easily adapt our estimation method in Section 3 to construct efficient estimators for the parameter .

3 Treatment Effect Estimator

In this section we develop our treatment effect estimator that efficiently leverages surrogates and achieves the bound derived in Section 2.1. We first show how to construct the estimator in Section 3.1. Then we establish the asymptotic guarantees for our estimator in Section 3.2.

3.1 Constructing an Efficient Estimator

Our analysis in Section 2.1 not only provides the efficiency bound for ATE estimation, but also guides us directly in the construction of an efficient estimator. In particular, Theorem 2.1 suggests one hypothetical estimator if the nuisance parameters were known: specifically, the efficient influence function itself in Theorem 2.1 gives the estimator that solves the following estimating equation:

| (12) |

It is then easy to verify by the Central Limit Theorem (CLT) that , which validates the efficiency of .

However, in practice, we do not know the nuisance parameters, so the estimator is infeasible. Instead, our approach will be to construct some nuisance parameter estimators first, and then plug them into Eq. 12 in place of . We could estimate using parametric models (e.g., linear regression, logistic regression), but this would risk model misspecification and lead to inconsistent estimates, let alone efficiency. This is particularly a concern when either covariates or surrogates are rich, which should normally be regarded as a good thing as it can make Assumption 1 more defensible as well as increase surrogates’ predictiveness and hence the efficiency gains from surrogate observations. Hence, we prefer flexible machine learning estimators that avoid restrictive parametric assumptions on the nuisance parameters to avoid misspecification error. For example, estimating amounts to learning conditional probabilities from binary classification data, and estimating is essentially learning two regression functions. For both tasks many successful machine learning methods exist, such as random forest (Breiman, 2001), gradient boosting (Friedman, 2001; Chen and Guestrin, 2016), neural networks (Goodfellow et al., 2016; Farrell et al., 2021), etc.

Although flexible machine learning estimators are less prone to model misspecification, we must be careful that their slow convergence and possible biases do not impact our estimator badly so that the resulting feasible ATE estimator is still root- consistent and asymptotically normal, just like the hypothetical estimator in Equation 12. Luckily, the efficient influence function we derive in Theorem 2.1 has a special multiplicative bias structure that makes it naturally insensitive to errors in .

Lemma 3.1.

For any such that satisfy Assumption 3 and any ,

Lemma 3.1 suggest that replacing with in Eq. 12, the estimate will remain consistent even if only one of and and one of and are consistent, as we will show in Theorem 3.1. More crucially, Lemma 3.1 suggests that if all nuisance estimators are consistent but converge slowly, then the overall error in using in place of in Eq. 12 will converge as the product of the slow rates. If this product is faster than the convergence of itself, e.g., each rate is , then our feasible estimator will asymptotically behave the same as the infeasible one up to leading orders (see Theorem 3.2 below for the formal statements). The property shown in Lemma 3.1 implies the Neyman orthogonality property that plays a central role in the recent debiased machine learning literature (e.g., Chernozhukov et al., 2018; Newey and Robins, 2018; Chernozhukov et al., 2022).

To construct our estimator, we further employ cross-fitting in nuisance estimation. We divide the data into multiple folds, use data in all but one fold to estimate nuisances, and apply the estimated nuisance only to the hold-out fold. This technique prevents each nuisance estimator from overfitting to the data where it is evaluated, and eschews stringent Donsker conditions on the nuisance estimators, which has been widely used in semiparametric estimation problems (e.g., Chernozhukov et al., 2018; Newey and Robins, 2018; Zheng and Laan, 2011; Chernozhukov et al., 2022).

Definition 2 (Cross-fitted Estimator).

Let be a fixed positive interger that does not change with sample size . Take -fold random partitions and of the labeled and unlabeled index sets and , respecitvely. Then constitutes a K-fold random partition of the whole index set . For each , we define , and use all but the th fold data to train machine learning estimators for the nuisance parameters: . The final ATE estimator is that solves the following equation:

| (13) |

or equivalently,

where is the empirical average over the fold, i.e., .

3.2 Asymptotic Properties of the Estimator

In this section we establish the insensitivity of our estimator to the estimation of nuisances. Namely, we establish both a double robustness property as well as efficiency. We then proceed to use our results to also construct valid confidence intervals.

Our results will depend on the asymptotic behavior of our nuisance estimates, . To state our results, we use the next assumption to define both the limit point of the estimates and the convergence rate. Note it is only an “assumption” once we specify a certain limit point and rate. In particular, the below allows the nuisance estimators to be misspecified in that the limit point need not be equal to .

Assumption 5 (Nuisance Estimator Convergence Rate).

For , the nuisance estimators converge to their limit in mean sqaured error at the following rates:

Furthermore, the propensity score estimators and their asymptotic limits are almost surely bounded: and with probability .

We further assume the following boundedness on the variance of the primary outcome.

Assumption 6 (Bounded Moments).

There exist constants such that

Our next result establishes formally the notion that only one of and and one of and need be consistent for to be consistent.

Theorem 3.1 (Double Robustness).

Theorem 3.1 states that the proposed estimator converges to the true ATE, as long as all nuisance estimators converge to a limit point and at least one of the limit points, but not necessarily both, in each pair of and is equal to the corresponding true value. Thus the consistency of our estimator does not require all nuisance parameters to be correctly estimated, nor the knowledge of which one is correctly estimated. This means that our estimator is robust to misspecification errors of estimating some nuisance parameters, as long as the rest are consistently estimated. This property is called “double robustness” in causal inference literature (e.g., Scharfstein et al., 1999; Kang et al., 2007).

Our next result formalizes the notion that slow convergence rates in nuisance estimation multiply, causing the effect of estimating nuisances to be negligible in analyzing and its first-order behavior to be similar to that uses the true nuisances.

Theorem 3.2 (Asymptotic Normality).

Under assumptions in Theorem 3.1, if we further assume , , and that all nuisance components are correctly specified so that , then as ,

| (14) |

where is the efficiency lower bound in Theorem 2.1.

Theorem 3.2 further shows that if all nuisance estimators converge to the truth at sufficiently fast rate, then the proposed estimator converges at rate , and it is asymptotically normal with the efficiency lower bound as its limiting variance. The rate requirement is lax and can be satisfied even if all nuisance estimators converge to true values at rates, i.e., much slower than the parametric rate . Therefore, the estimation errors of machine learning nuisance estimators may not undermine the asymptotic behavior of our ATE estimator and it can still achieve the efficiency bound of Theorem 2.1 similarly to the infeasible estimator .

Notably, we do not restrict the nuisance estimators to Donsker or bounded entropy classes (van der Vaart, 1998), which flexible machine learning methods usually violate. Instead, we only require a lax rate condition on the nuisance estimators. This rate requirement can be achieved by many machine learning estimators in high dimensions under appropriate conditions (see, e.g., Benkeser and van der Laan, 2016; Bibaut and van der Laan, 2019; Farrell et al., 2021). Moreover, we allow estimators converging at faster rate to compensate for those converging at slower rate. For example, if we have strong domain knowledge about the labeling process and treatment assignment process (e.g., in a randomized experiment with two-phase sampling design) so that we can estimate the labeling propensity score and treatment propensity score at very fast rate, then we can allow for very flexible regression estimators that converge at slow rates.

In the next result we propose a way to consistently estimate the efficient variance, , which immediately lends itself to confidence interval construction.

Theorem 3.3 (Variance Estimation and Confidence Interval).

Under the assumptions in Theorem 3.2,

Consequently, the following confidence interval

| (15) |

with as the cumulative density function of standard normal distribution satisfies that

Theorem 3.3 shows that under the same conditions, a consistent estimator for the efficiency lower bound can be obtained by forming the sample analogue of with cross-fitting nuisance estimators and the proposed estimator . The resulting confidence interval in Eq. 15 asymptotically achieves correct coverage probability. Also, since the proposed estimator asymptotically achieves the smallest possible variance, the confidence interval in Eq. 15 tends to be shorter than confidence intervals based on other less efficient estimators.

4 Extension: Very Large Unlabeled Data

In this section, we consider the setting where the size of unlabeled data is much larger than the size of the labeled data, i.e., . This is a practically relevant setting since in many cases we may have only very few units being followed in a study while at the same time we may cheaply collect massive amounts of data without outcomes from existing databases, such as from electronic medical records (Cheng et al., 2018). Despite its practical relevance, this setting cannot be directly accommodated by our efficiency and estimation theory in Sections 2 and 3. This is because previous results all hinge on the overlap condition (8) in Assumption 3, which implies that the marginal labeling probability is positive, , and thus with high probability. This rules out the setting with many more unlabeled data, that is, and . In fact, in the very-many-unlabeled-data setting, we can show that almost surely (Lemma D.2), so previous efficiency lower bounds based on are invalid. Despite these drastic differences, we will show that essentially the same efficiency results and estimation strategy actually still apply in the very-many-unlabeled-data setting, as long as we change the perspective and scaling appropriately.

4.1 Efficiency Analysis

To accommodate this setting, we change the efficiency considerations mainly in two aspects. First, instead of using , we characterize efficiency in terms of the density ratio

where and are the conditional and unconditional density functions of corresponding to the target distribution with respect to an appropriate dominating measure (e.g., Lebesgue measure). This density ratio is well-defined and bounded almost surely as long as the distribution of on the labeled data and that on the unlabeled data sufficiently overlap, regardless of whether or .

Second, we will focus on ATE estimators whose convergence rates scale with the sample size of labeled data instead of the total sample size. This is crucial since, in the current setting, the size of the labeled data becomes the bottleneck for accurate ATE estimation, since the primary outcome observed in the labeled data is the primary source of information on the ATE, but its sample size, , is on a different scale than the total sample size, .

Since , from the perspective of the behavior as , the size of the unlabeled dataset appears infinitely larger and thus its distribution, i.e., the distribution of given , appears virtually known. Moreover, in the asymptotic limit, the labeled dataset is negligible, and the combined dataset is virtually identical to the unlabeled dataset (). Thus the unconditional distribution of is the same as their conditional distribution given for the unlabeled data, thus the unconditional distribution can also be viewed as known from the perspective of labeled data. The efficiency lower bound from this perspective is formalized in the following theorem.

Theorem 4.1.

Suppose our data consists of i.i.d draws from the conditional distribution of given . Suppose Assumptions 1, 2 and 4 and Assumption 3 Equation 7 hold, the unconditional distribution of is known, and assume an additional simplifying condition . Then the efficiency lower bound is , where the new nuisance parameters are , and

| (16) |

Theorem 4.1 assumes the MAR assumptions in Assumptions 4 and 2, which strictly generalizes the results in Cheng et al. (2018) under the more restrictive MCAR condition. This generalization is possible mainly because we formulate the efficiency lower bound in terms of the density ratio, as opposed to inverse labeling propensity score formulation that is more commonly used but ill-defined in the current setting. Although the assumption of exactly knowing the distribution of in Theorem 4.1 seems idealized, we will confirm in Theorem 4.2 below that this indeed characterizes the role of unlabeled data in an asymptotic sense from the perspective of labeled data. In Theorem 4.1, we assume the condition to obtain a simplied result. In the proof for Theorem 4.1, we also derive the efficiency bound for the more general setting without this condition.

4.2 Constructing an Efficient Estimator

Our efficiency analysis above is asymptotic, where asymptotically we have and hence . In terms of estimation from an actual finite sample, however, we do have some labeled data, albeit much less than unlabeled data. Therefore, the observation model of having i.i.d. draws from is inappropriate as it implies we observe no outcome data with probability 1, which would make estimation impossible. Instead, we modify our observation model slightly to allow for the marginal probability of labeling, which we denote as , to vary with the total sample size . We only require that and that the expected labeled sample size satisfies as . We then consider the observation model where we have i.i.d. draws, for each of which with probability we sample the observation from the conditional distribution of given and with probability we sample from the conditional distribution given . That is, we define for any event measurable with respect to and we observe i.i.d. draws from . This specification aptly models the regime of interest: even when , the labeled data are always available in finite sample, and asymptotically its absolute size grows to infinity despite the fact that its relative size as a fraction of vanishes as . In fact, this specification is very general: it can accommodate both the current setting by letting , and the original setting (see Section 1.1) by letting .

We now follow our estimation strategy in Definition 2 to construct an analogous ATE estimator that can attain the efficiency lower bound in Theorem 4.1.

Definition 3 (Revised Estimator).

We take the -fold random partitions as in Definition 2, and analogously construct nuisance estimators for . The resulting ATE estimator is

| (17) |

where estimates , and is the empirical average operator for data in the th fold (in triangular array), i.e., .

This estimator is almost the same as the previous estimator in Definition 2, except that is based on nuisance estimators for the density ratio , while is based on nuisance estimators for the labeling propensity score . In Theorem 4.2, we will show that these two estimators are asymptotically equivalent if the overlap condition (8) holds. But when the overlap condition indeed holds, we prefer the estimator as it only requires estimating the labeling propensity score , i.e., the conditional probability function in a classification task with the label , for which many machine learning methods exist and which is arguably easier to estimate than the density ratio in . When the overlap condition does not hold and , estimating the labeling propensity score may be very unstable given the extremely imbalanced data, with imbalance going to an extreme as . Therefore, in the very-large-unlabeled-data setting, we prefer the estimator as it uses the density ratio , which is stable as varies. Machine learning estimators for density ratios are reviewed in Sugiyama and Kawanabe (2012); Sugiyama et al. (2012).

In the following theorem, we show the asymptotic normality and efficiency of estimator under conditions analogous to those in Theorem 3.2. Notably, we consider a generic limiting marginal probability that can be either (i.e., the setting in this section) or strictly positive (i.e., the setting in Section 3).

Theorem 4.2.

Suppose that the assumptions in Theorem 4.1 hold, for any finite , and as , and mild moment regularity conditions given in Appendix Assumption 7. We assume that for , the convergence rates of nuisance estimators to the true nuisance parameters are , , , and respectively (see Appendix Assumption 8 for precise definitions), , and almost surely. We further assume that are all and . Moreover, we suppose that they satisfy , , and . Then estimator given in Definition 3 satisfies that

| (18) | ||||

| (19) | ||||

If the overlap condition in Eq. 8 holds so that , and we further assume the conditions in Theorem 3.2, then estimator in Definition 2 is asymptotically equivalent to estimator , i.e.,

| (20) |

If , then is equal to the efficiency lower bound given in Theorem 4.1.

Theorem 4.2 shows that if the overlap condition in Eq. 8 holds and nuisance estimators are accurate enough, then estimators and are asymptotically equivalent, and they are both asymptotically efficient. Their asymptotic variance can be viewed as an equivalent reformulation of the efficient lower bound in Theorem 2.1 from the perspective of the labeled data. In particular, in contrast to the scaling factor of and the inverse labeling propensity score in , is formulated in terms of the scaling factor and the density ratio appearing in . This new formulation is not only valid under the overlap condition, but also particularly suitable for the current setting where . In the current setting, although the estimated labeling probability in converges to , the scaling factor effectively stabilizes the asymptotic variance of and ensures meaningful asymptotic distribution (see Eq. 18). In contrast, the scaling factor will be far too large: if the data points consist mostly of unlabeled data, we cannot hope for -rate convergence. Moreover, the density ratio formulation circumvents the inverse labeling propensity score that is ill-defined in the current setting.

Theorem 4.2 also demonstrates that our efficiency analysis in Theorem 4.1 is appropriate: in the regime where , our estimator achieves the efficiency bound in Theorem 4.1 where the unconditional distribution of is assumed to be known. In particular, the last two terms in the asymptotic variance , which involve the limiting labeling probability , quantify the estimation variance due to not knowing the unconditional distribution of . When , this unconditional distribution can be viewed as known from the perspective of labelled data, so the last two variance terms drop out and only the first term remains. These efficiency and estimation results thus reveal the whole spectrum of efficiency in estimating ATE with surrogates, and feature a smooth transition from the regime to the regime . In Appendix Theorem C.1, we further extend Theorems 2.2 and 2.2.1 to the regime , and we again confirm that more predictive surrogates result in bigger efficiency gains.

All results above depend on the density ratio , which might be challenging to estimate in practice, especially if the pre-treatment covariates are high dimensional. One straightforward setting where we can avoid estimation is when the primary outcome is MCAR, which was studied in Cheng et al. (2018); Zhang and Bradic (2019). In this special setting, is independent with all other variables, so does not need to be estimated, and the estimator in Definition 3 reduces to

This estimator is exactly identical to the estimator in Definition 2 under the MCAR assumption. In Appendix B, we further discuss how this estimator connects to those in Cheng et al. (2018); Zhang and Bradic (2019), and how our result generalizes those in previous literature.

5 Numerical Studies

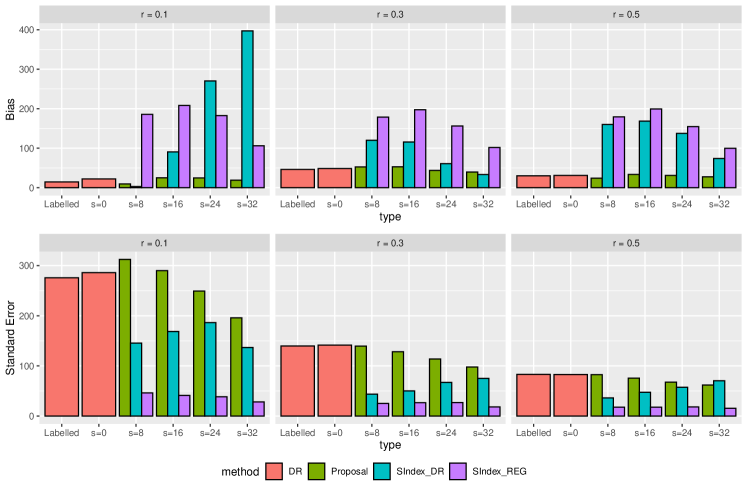

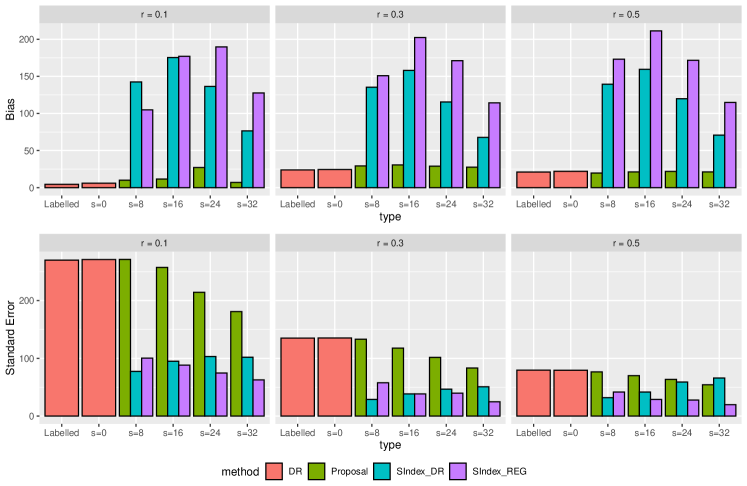

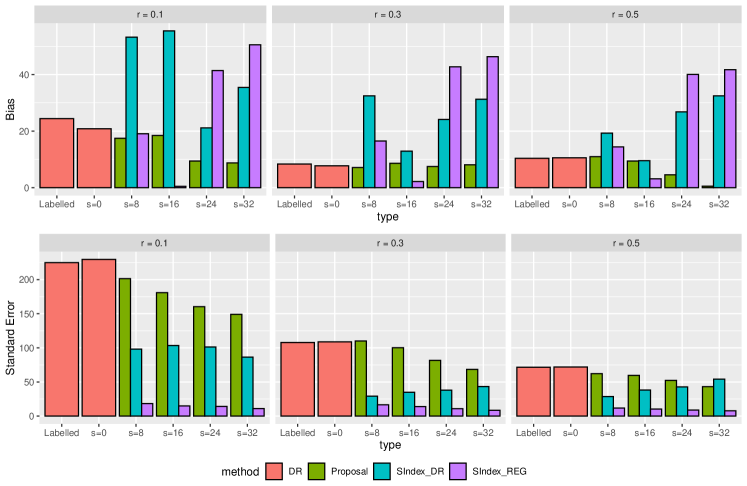

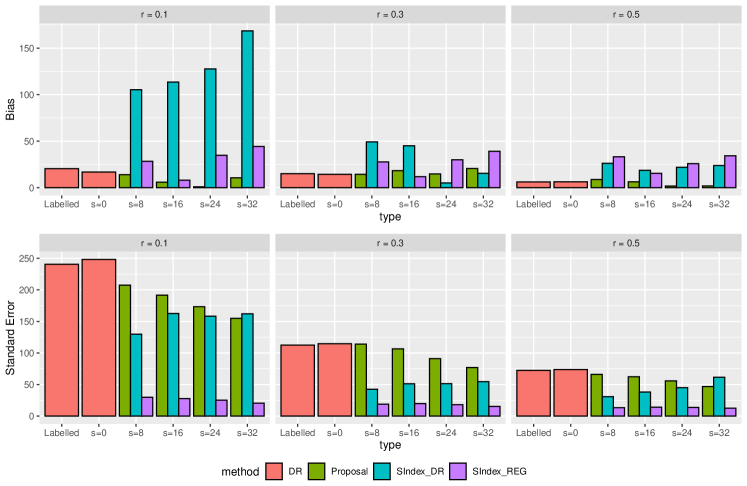

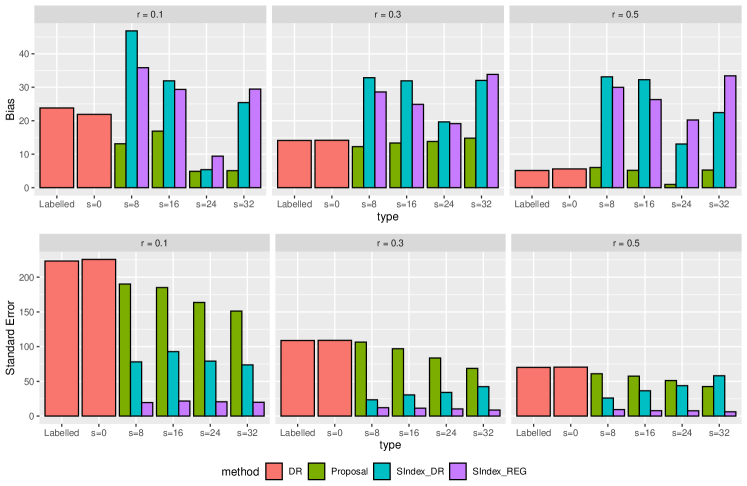

In this section, we demonstrate the performance of our proposed estimators using experimental data for the Greater Avenues to Independence (GAIN) job training program, a job assistance program designed in the late 1980s for low-income people in California. We employ the dataset analyzed in Athey et al. (2019), which contains results from a large-scale randomized experiment in four counties in California (Alameda, Los Angeles, and San Diego and Riverside). For each experiment participant, this dataset records a binary treatment variable indicating whether being treated by the GAIN program or not, quarterly earnings after treatment assignments, and other covariate information, etc. In this section, we illustrate the performance of our proposed estimator and other benchmarks in estimating the average treatment effect in long-term earnings using the Riverside data. We provide additional results for Los Angeles data and San Diego data in Appendix E (Alameda dataset is very small and thus omitted). The code underlying this numerical study is available at https://github.com/CausalML/Efficient_estimation_surrogate.

We construct a labelled dataset and unlabelled dataset based on the Riverside data (, with treated units and control units). We randomly draw a fraction of units from the Riverside data as the labelled data () and use the rest as the unlabelled data (). In our analysis, the primary outcome is the long-term earning in the th quarter after the treatment assignment, and surrogates are quarterly earnings up to quarters after the treatment, where . We also consider additional covariates including age, gender, education, and ethnicity. The surrogates and covariates are observed on both labelled and unlabelled data, but the primary outcome is only observed on the labelled data.

We apply five types of estimators to estimate the average treatment effect in the primary outcome: our proposed estimator in Definition 2 (denoted as “Proposal”), the surrogate index estimator based on regression imputation proposed in Athey et al. (2019) (denoted as “SIndex_REG”), the semiparametrically efficient surrogate index estimator proposed in Chen and Ritzwoller (2021) (denoted as “SIndex_DR”), the doubly robust estimator that uses both datasets but ignores the surrogates, corresponding to the influence function in Theorem 2.2 (denoted as “DR” with type ), and the doubly robust estimator that only uses the labelled dataset (denoted as “DR” with type “Labelled”). We estimate the nuisance functions in these estimators by fitting random forests, gradient boosting, and LASSO respectively, all cross-fitted with folds. The SIndex_DR estimator is implemented by the longterm R package developed by Chen and Ritzwoller (2021), where all hyperparameters in nuisance estimation are automatically tuned by cross-validation. All other estimators (including our proposal) are implemented using R packages ranger (for fitting random forests), gbm (for fitting gradient boosting), and glmnet (for fitting LASSO). The hyperparameters in random forests and boosting are set as default values without any tuning, and those in LASSO are tuned by cross-validation. Note that in our data generating process, both the treatment assignments and the primary outcome missingness are completely at random, so we directly use sample frequencies as estimates for the corresponding propensity nuisances. These propensity score estimates are trivially consistent. In this section, we focus on estimation results with random forest nuisance estimators. Additional results for other nuisance estimators are provided in the appendix.

The upper row in Figure 1 shows the bias of different treatment effect estimators with nuisances estimated by random forests, over repetitions of the experiments on the Riverside data. We observe that the surrogate index estimators always have high bias. This bias is not primarily caused by nuisance estimation, since according to the theory in Chen and Ritzwoller (2021), the efficient surrogate index estimator (SIndex_DR) should be robust to the nuisance estimation bias given that the propensities are well estimated (its bias is indeed lower than the bias of SIndex_Reg). Instead, the high bias may be plausibly attributed to the violation of the statistical surrogate condition assumed for the surrogate index methods. As the number of surrogates grows, the violation of the statistical surrogate condition is alleviated, so the bias of surrogate index estimators drops, but it still remains very high, posing serious challenges for statistical inference. In contrast, our proposed estimator has very low bias across all settings.

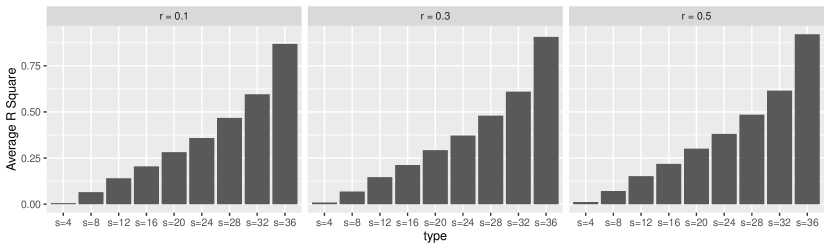

The lower row in Figure 1 shows the standard errors of different treatment effect estimators. We note that the standard errors of our proposed estimator decrease with the number of surrogates. This is because with more surrogates we can better predict the primary outcome, as we validate in Figure 2. Moreover, the amount of standard error reduction due to introducing surrogates is overall higher when the missingness of the primary outcome is more severe (smaller ). These empirical observations support our qualitative conclusions from the efficiency analysis in Corollary 2.2.1: the efficiency gains from leveraging surrogates improve for more predictive surrogates and more missing primary outcome. Interestingly, we find that the standard errors of surrogate index estimators may not decrease with the number of surrogates.

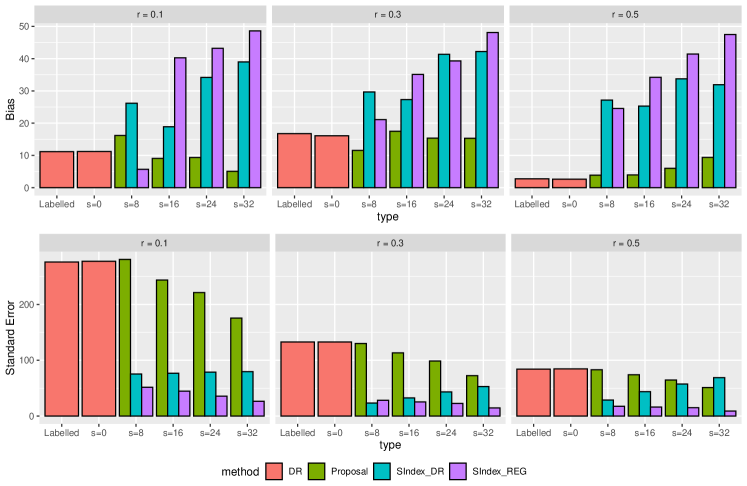

In Appendix E, we provide additional results for other types of nuisance estimators (Gradient Boosting and LASSO) and results for Los Angeles data and San Diego data. These additional results show similar patterns of bias and standard error.

6 Conclusion

We study the estimation of average treatment effect with only a limited number of primary outcome observations but abundant observations of surrogates. Particularly, we avoid stringent surrogate conditions that are prone to violation in practice and only assume standard causal inference and missing data assumptions.

We investigated the role of surrogates by comparing the efficiency lower bounds of ATE with and without presence of surrogates, and also bounds in some intermediary cases. We find that efficiency gains from optimally leveraging surrogates crucially depend on how well surrogates can predict the primary outcome and also the fraction of missing outcome data. These results provide valuable insights on when leveraging surrogates can be beneficial. We also show that the efficiency results are valid in two regimes: when the size of surrogate observations is comparable to the size of primary-outcome observations (i.e., ), and when the former is much larger than the other (i.e., ). The second regime violates the overlap condition commonly assumed in the literature and was thus understudied in the past, even though it is highly relevant in modern data collection. Our analysis shows that the second regime can be viewed as a limiting case of the first regime, which reveals the intimate connection between these two regimes.

Moreover, we propose ATE estimators that can employ any flexible machine learning method for nuisance parameter estimation. We provide strong statistical guarantee for the proposed estimators by showing that they are robust to nuisance estimation bias, and they asymptotically achieve the semiparametric efficiency lower bounds under high-level rate conditions for the machine learning nuisance estimators. We further develop consistent estimators for the efficiency lower bounds and construct asymptotically valid confidence intervals for ATE. In summary, our methods provide a principled approach to optimally leverage surrogate observations when only a limited number of primary-outcome observations are available and without using strong surrogacy assumptions.

References

- Athey et al. [2019] Susan Athey, Raj Chetty, Guido W Imbens, and Hyunseung Kang. The surrogate index: Combining short-term proxies to estimate long-term treatment effects more rapidly and precisely. Technical report, National Bureau of Economic Research, 2019.

- Athey et al. [2020] Susan Athey, Raj Chetty, and Guido Imbens. Combining experimental and observational data to estimate treatment effects on long term outcomes, 2020.

- Azriel et al. [2016] David Azriel, Lawrence D Brown, Michael Sklar, Richard Berk, Andreas Buja, and Linda Zhao. Semi-supervised linear regression. arXiv preprint arXiv:1612.02391, 2016.

- Benkeser and van der Laan [2016] David Benkeser and Mark van der Laan. The highly adaptive lasso estimator. In 2016 IEEE International Conference on Data Science and Advanced Analytics (DSAA), volume 2016, pages 689–696. IEEE, 2016.

- Bibaut and van der Laan [2019] Aurélien F Bibaut and Mark J van der Laan. Fast rates for empirical risk minimization over cadlag functions with bounded sectional variation norm. arXiv preprint arXiv:1907.09244, 2019.

- Breiman [2001] Leo Breiman. Random forests. Machine learning, 45(1):5–32, 2001.

- Carroll and Wand [1991] Raymond J Carroll and Matt P Wand. Semiparametric estimation in logistic measurement error models. Journal of the Royal Statistical Society: Series B (Methodological), 53(3):573–585, 1991.

- Chakrabortty et al. [2018] Abhishek Chakrabortty, Tianxi Cai, et al. Efficient and adaptive linear regression in semi-supervised settings. The Annals of Statistics, 46(4):1541–1572, 2018.

- Chakrabortty et al. [2022a] Abhishek Chakrabortty, Guorong Dai, and Raymond J Carroll. Semi-supervised quantile estimation: Robust and efficient inference in high dimensional settings. arXiv preprint arXiv:2201.10208, 2022a.

- Chakrabortty et al. [2022b] Abhishek Chakrabortty, Guorong Dai, and Eric Tchetgen Tchetgen. A general framework for treatment effect estimation in semi-supervised and high dimensional settings. arXiv preprint arXiv:2201.00468, 2022b.

- Chan et al. [2020] Stephanie F Chan, Boris P Hejblum, Abhishek Chakrabortty, and Tianxi Cai. Semi-supervised estimation of covariance with application to phenome-wide association studies with electronic medical records data. Statistical Methods in Medical Research, 29(2):455–465, 2020.

- Chen et al. [2007] Hua Chen, Zhi Geng, and Jinzhu Jia. Criteria for surrogate end points. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 69(5):919–932, 2007.

- Chen and Ritzwoller [2021] Jiafeng Chen and David M Ritzwoller. Semiparametric estimation of long-term treatment effects. arXiv preprint arXiv:2107.14405, 2021.

- Chen and Breslow [2004] Jinbo Chen and Norman E Breslow. Semiparametric efficient estimation for the auxiliary outcome problem with the conditional mean model. Canadian Journal of Statistics, 32(4):359–372, 2004.

- Chen et al. [2003] Song Xi Chen, Denis H Y Leung, and Jing Qin. Information recovery in a study with surrogate endpoints. Journal of the American Statistical Association, 98(464):1052–1062, 2003.

- Chen et al. [2008a] Song Xi Chen, Denis HY Leung, and Jing Qin. Improving semiparametric estimation by using surrogate data. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 70(4):803–823, 2008a.

- Chen and Guestrin [2016] Tianqi Chen and Carlos Guestrin. Xgboost: A scalable tree boosting system. In Proceedings of the 22nd acm sigkdd international conference on knowledge discovery and data mining, pages 785–794, 2016.

- Chen et al. [2005] Xiaohong Chen, Han Hong, and Elie Tamer. Measurement error models with auxiliary data. The Review of Economic Studies, 72(2):343–366, 2005.

- Chen et al. [2008b] Xiaohong Chen, Han Hong, Alessandro Tarozzi, et al. Semiparametric efficiency in gmm models with auxiliary data. The Annals of Statistics, 36(2):808–843, 2008b.

- Chen and Chen [2000] Yi-Hau Chen and Hung Chen. A unified approach to regression analysis under double-sampling designs. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 62(3):449–460, 2000.

- Cheng et al. [2018] David Cheng, Ashwin Ananthakrishnan, and Tianxi Cai. Efficient and robust semi-supervised estimation of average treatment effects in electronic medical records data. arXiv preprint arXiv:1804.00195, 2018.

- Chernozhukov et al. [2018] Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters, 2018.

- Chernozhukov et al. [2022] Victor Chernozhukov, Juan Carlos Escanciano, Hidehiko Ichimura, Whitney K Newey, and James M Robins. Locally robust semiparametric estimation. Econometrica, 90(4):1501–1535, 2022.

- Cochran [2007] William G Cochran. Sampling techniques. John Wiley & Sons, 2007.

- Echt et al. [1991] Debra S Echt, Philip R Liebson, L Brent Mitchell, Robert W Peters, Dulce Obias-Manno, Allan H Barker, Daniel Arensberg, Andrea Baker, Lawrence Friedman, H Leon Greene, et al. Mortality and morbidity in patients receiving encainide, flecainide, or placebo: the cardiac arrhythmia suppression trial. New England journal of medicine, 324(12):781–788, 1991.

- Elwert and Winship [2014] Felix Elwert and Christopher Winship. Endogenous selection bias: The problem of conditioning on a collider variable. Annual review of sociology, 40:31–53, 2014.

- Engel and Walstra [1991] B Engel and P Walstra. Increasing precision or reducing expense in regression experiments by using information from a concomitant variable. Biometrics, pages 13–20, 1991.

- Farrell et al. [2021] Max H Farrell, Tengyuan Liang, and Sanjog Misra. Deep neural networks for estimation and inference. Econometrica, 89(1):181–213, 2021.

- FDA [2016] FDA. Accelerated approval program. 2016. URL https://www.fda.gov/drugs/information-healthcare-professionals-drugs/accelerated-approval-program.

- Fleming and DeMets [1996] Thomas R Fleming and David L DeMets. Surrogate end points in clinical trials: are we being misled? Annals of internal medicine, 125(7):605–613, 1996.

- Fleming et al. [1994] Thomas R Fleming, Ross L Prentice, Margaret S Pepe, and David Glidden. Surrogate and auxiliary endpoints in clinical trials, with potential applications in cancer and aids research. Statistics in medicine, 13(9):955–968, 1994.

- Frangakis and Rubin [2002] Constantine E Frangakis and Donald B Rubin. Principal stratification in causal inference. Biometrics, 58(1):21–29, 2002.

- Freedman et al. [1992] Laurence S Freedman, Barry I Graubard, and Arthur Schatzkin. Statistical validation of intermediate endpoints for chronic diseases. Statistics in medicine, 11(2):167–178, 1992.

- Friedman [2001] Jerome H Friedman. Greedy function approximation: a gradient boosting machine. Annals of statistics, pages 1189–1232, 2001.

- Goodfellow et al. [2016] Ian Goodfellow, Yoshua Bengio, and Aaron Courville. Deep learning. MIT press, 2016.

- Gronsbell and Cai [2018] Jessica L Gronsbell and Tianxi Cai. Semi-supervised approaches to efficient evaluation of model prediction performance. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(3):579–594, 2018.

- Hahn [1998] Jinyong Hahn. On the role of the propensity score in efficient semiparametric estimation of average treatment effects. Econometrica, pages 315–331, 1998.

- Hotz et al. [2006] V Joseph Hotz, Guido W Imbens, and Jacob A Klerman. Evaluating the differential effects of alternative welfare-to-work training components: A reanalysis of the california gain program. Journal of Labor Economics, 24(3):521–566, 2006.

- Hou et al. [2021] Jue Hou, Zijian Guo, and Tianxi Cai. Surrogate assisted semi-supervised inference for high dimensional risk prediction. arXiv preprint arXiv:2105.01264, 2021.

- Imai et al. [2011] Kosuke Imai, Luke Keele, Dustin Tingley, and Teppei Yamamoto. Unpacking the black box of causality: Learning about causal mechanisms from experimental and observational studies. American Political Science Review, 105(4):765–789, 2011.

- Imbens and Rubin [2015] Guido W Imbens and Donald B Rubin. Causal inference in statistics, social, and biomedical sciences. Cambridge University Press, 2015.

- Jankova et al. [2018] Jana Jankova, Sara Van De Geer, et al. Semiparametric efficiency bounds for high-dimensional models. The Annals of Statistics, 46(5):2336–2359, 2018.

- Kang et al. [2007] Joseph DY Kang, Joseph L Schafer, et al. Demystifying double robustness: A comparison of alternative strategies for estimating a population mean from incomplete data. Statistical science, 22(4):523–539, 2007.

- Lauritzen et al. [2004] Steffen L Lauritzen, Odd O Aalen, Donald B Rubin, and Elja Arjas. Discussion on causality [with reply]. Scandinavian Journal of Statistics, 31(2):189–201, 2004.

- Little and Rubin [2019] Roderick JA Little and Donald B Rubin. Statistical analysis with missing data, volume 793. John Wiley & Sons, 2019.

- Moore [1997] Thomas J Moore. Deadly medicine: Why tens of thousands of patients died in america’s worst drug disaster. Statistics in Medicine, 16:2507–2510, 1997.

- NCATS [2019] NCATS. About the national center for advancing translational sciences. 2019. URL https://ncats.nih.gov/about.

- Newey and Robins [2018] Whitney K Newey and James R Robins. Cross-fitting and fast remainder rates for semiparametric estimation. arXiv preprint arXiv:1801.09138, 2018.

- Neyman [1923] Jersey Neyman. Sur les applications de la théorie des probabilités aux experiences agricoles: Essai des principes. Roczniki Nauk Rolniczych, 10:1–51, 1923.

- Pearl [2009] Judea Pearl. Causality. Cambridge university press, 2009.

- Pepe [1992] Margaret Sullivan Pepe. Inference using surrogate outcome data and a validation sample. Biometrika, 79(2):355–365, 1992.

- Pepe et al. [1994] Margaret Sullivan Pepe, Marie Reilly, and Thomas R Fleming. Auxiliary outcome data and the mean score method. Journal of Statistical Planning and Inference, 42(1-2):137–160, 1994.

- Post et al. [2010] Wendy J Post, Ciska Buijs, Ronald P Stolk, Elisabeth GE de Vries, and Saskia Le Cessie. The analysis of longitudinal quality of life measures with informative drop-out: a pattern mixture approach. Quality of Life Research, 19(1):137–148, 2010.

- Prentice [1989] Ross L Prentice. Surrogate endpoints in clinical trials: definition and operational criteria. Statistics in medicine, 8(4):431–440, 1989.

- Price et al. [2018] Brenda L Price, Peter B Gilbert, and Mark J van der Laan. Estimation of the optimal surrogate based on a randomized trial. Biometrics, 74(4):1271–1281, 2018.