A class of short-term models for the oil industry addressing speculative storage

Abstract

We propose a plausible mechanism for the short term dynamics of the oil market based on the interaction of economic agents, namely a major agent (a monopolistic cartel), a fringe of competitive producers and a crowd of arbitrageurs who store the resource. This model is linked to a separate work by the same authors on a long term model for the oil industry. The present model leads to a system of two coupled non linear partial differential equations, with a new type of boundary conditions linked to constraints on the storage capacity. These boundary conditions play a key role and translate the fact that when storage is either full or empty, the cartel has an enhanced strategic power, and may tune the price of the resource. The model is discussed in details, as well as some simpler variants. A finite difference scheme is proposed and numerical simulations are reported. The latter result in apparently surprising facts: 1) the optimal control of the cartel (i.e. its level of production) is a discontinuous function of the state variables; 2) there is a cycle, which takes place around the shock line. We discuss these phenomena in details, and show that they may explain what happened in 2015 and 2020.

1 Introduction

For several decades, the oil industry has had structural characteristics that make it exceptional from the viewpoint of economic theory. A main feature is the existence of a monopolistic cartel of producers lasting since 1960. This is partly explained by the fact that international law does not prohibit a worldwide coalition, while in most countries, the law forbids lasting and non regulated nationwide monopolies. Regardless of legal issues, the existence of a lasting equilibrium between a cartel and a competitive fringe of producers may arise only in particular economic situations. In a separate work in progress, see [1], we have proposed an economic model that we have named Edmond 1111 after the famous writer Edmond Rostand ([7]), a relative of one of the authors, that is motivated by the following observations:

-

•

First, oil reserves and production capacity 222In our model, the production of the competitive fringe is always the same fraction of the capacity of production, which is of course an approximation of what actually happens in the industry. Thanks to this proportionality, we can use as a state variable the annual production of the fringe. have been driven for several decades by production and investment. Of course, production makes reserves decrease; conversely, new reserves can be found and new production facilities can be built. Moreover, for most oil fields, the necessary investments from prospecting to construction of production facilities (CAPEX), have been rather stable for several decades, of the order of 10 to 20 dollars per barrel eventually produced . Due to inefficiencies that will be discussed later, the flow of CAPEX, i.e. the CAPEX per year, has a decreasing yield. Indeed, it is observed that the yearly increase in production capacity is proportional to the square root of CAPEX flow .333This means that if during a given year, the flow of CAPEX is of Bn $ and increases the production capacity by say Bn barrels, then, during the same year, a flow of CAPEX of Bn $ would have increased the capacity by Bn barrels.

Notice that this first observation leads us to a radical departure from Hotelling’s framework. Indeed, on the time scale considered here (i.e. decades, not centuries), it appears that new reserves are the results of research efforts and investments that are endogenously determined; therefore, exhaustibility of the resource is not relevant. Models for mining industries which do not belong to the Hotelling framework have already been studied by some of the authors, see [2].

-

•

The second observation that explains the equilibrium between the cartel and the competitive fringe is that the investments on capacity by the fringe producers are limited by credit constraints. Indeed, most producers in the competitive fringe can invest only from their own cash flows; more precisely, almost all fringe producers can invest only if the price of the barrel is high enough, i.e. above a given threshold, and their investments increase linearly with respect to the price of the barrel when it is above the threshold.

This constraint on investments is mostly due to a set of major risk factors (operational risks, duration of projects, sovereign risk, etc…). This gives an important strategic lever to the monopolistic cartel, all the more important given that the elasticity of demand is extremely low. Indeed,

-

–

In the short run, the price elasticity is around , so that a small increase in the cartel’s production drives down prices by a substantial amount. This stops investment by the fringe and drives down their capacity, allowing the monopolist to increase market share

-

–

Conversely, when the cartel reduces its production by a relatively small amount, the price increases substantially and the fringe producers invest. However, since all fringe producers are investing at the same time, the CAPEX required to obtain an additional unit of capacity is high. In other words, these simultaneous investments by the fringe producers are inefficient.

This gives the cartel more strategic power and allows the cartel to make additional profits for a rather long period.

-

–

The two observations are key ingredients for the equilibrium described in the long term model [1], that exhibits fluctuations between high prices that lead to immediate benefits but also a decrease in the cartel’s future market shares and low prices which have the opposite effects.

The model in [1] is stationary except for a single multiplicative factor on the demand curve. A numerical calibration shows that it is capable of matching key moments of the observed time series in the oil market

Our long term model [1] leaves aside

detailed interactions between the producers and the business of oil storage: it uses a very simple approximation

to the behavior of the arbitrageurs who buy, store and then sell

the resource. This simple approximation is sufficiently good fot studying long term dynamics over decades. Yet, at the time scale of a few years, the interaction of the monopolistic cartel with the storage business leads to particular strategic effects.

The aim of the present paper is to propose a model named Edmond 2, which focuses on these interactions in order to shed some light on unusual but striking features of the oil markets’ prices, production and investments.

The new model, otherwise as in [1] produces an equilibrium which in some aspects is quite distinct 444The strategic interactions are quite different from those described in the long term model [1]. Therefore, the two models should be considered as complementary insights on the oil markets. We have not mixed them in order to avoid that a complexity that would hide the different insights. - in particular it can generate very large and brutal changes,

namely discontinuities in prices, and in the optimal strategies of the cartel as functions of the state variables, in the absence of noise.

We will consider a large number of arbitrageurs who behave competitively. As is often the case in economics, a competitive set of arbitrageurs limits the freedom of the cartel to implement strategies that depend on price changes as in [1]. But, in the oil industry, arbitrageurs have their own limits. Indeed, a key element in the present model is the existence of capacity constraints (there is a minimum and a maximum capacity) on storage.

These one-side constraints allow the cartel more strategic power when the capacity limits are reached.

These key features linked to the arbitrageurs’ constraints result in three different regimes for the slope of the futures curve, namely ’contango’, ’backwardization’ and ’standard’, as will be seen in Section 6.

The paper is organized as follows: the main part of the new model is discussed in Section 2; mathematically, it leads to a system of partial differential equations. Section 2 also includes the description of simpler variants. The issue of the boundary conditions corresponding to situations when the storage facilities are either empty or full is particularly delicate: it is dealt with in Section 3. To the best of our knowledge, such boundary conditions appear to be completely new. Their mathematical analysis seems quite delicate, and we give partial theoretical results in Section 4. Section 5 is devoted to a finite difference method for solving the system of PDEs supplemented with the above mentioned boundary conditions. Finally, numerical simulations are reported in Section 6: in particular, we find large shocks in the oil price. We then comment on the simulations, and stress the qualitative agreement with what occurred at least twice in the recent history, 2015 and 2020.

2 The models and the systems of partial differential equations

We consider a cartel producing a natural resource

and facing both a competitive fringe of small producers and a competitive set of arbitrageurs.

Even though our motivation is to understand some aspects of the oil market in the short or middle term (of the order of few years)

and we may sometimes use a terminology linked to the oil industry (for example, oil for the resource, OPEC for the cartel),

the models proposed below may be applied in other settings.

There are four types of agents: consumers, a cartel or major agent (OPEC), minor producers forming a competitive fringe, and the arbitrageurs that buy, store and then sell the resource. The arbitrageurs will most often limit price changes,

but when storage capacity limits are reached, the strategic power of the cartel increases dramatically. When no resource is stored, the cartel has the power to drive prices up by cutting production; conversely, when storage is at its maximal level, the cartel can drive prices down by increasing production.

For simplicity, we will not consider the decision making process of the competitive fringe of small producers but

instead assume that the dynamics of their global production rate is given as a function of the current state of the world;

see the above remarks on credit constraints.

In contrast to the long-run analysis in [1], our aim is to model the dynamics in horizons of the order of a few years. For this reason, we will take the demand function by final consumers as constant. This assumption is a good approximation for oil markets, since, except for the occurrence of major unexpected shocks - such as the arrival of the pandemic in 2020 - there is little variation in the demand function on a yearly horizon (see paragraph 6.4 for a discussion). Nonetheless we will comment on the effect of rare disasters on equilibria; see paragraph 6.4.

The class of models described below involves two state variables:

-

1.

the level of speculative storage

-

2.

the level of aggregate output of the competitive fringe.

While , i.e. the level of speculative storage, takes its value in a given interval, say ,

the second state variable, i.e. , may be either discrete or continuous. The physical constraints on the storage capacity will play a key role. Indeed, it will be shown that in some situations and when the storage level is either minimal or maximal, the cartel directly controls the price of the resource.

Mathematically, all the variants of the model lead to systems of partial differential equations coupling a Hamilton-Jacobi-Bellman equation for the cartel (major agent) and an equation of the type “master equation” for the price of the resource, see [6, 4, 3]. Note that in the present case, the master equation does not model a crowd of players as in mean field games, but rather an equilibrium reached by a crowd of arbitrageurs. It seems to be the first example in which the master equation does not involve the value of a game between competitive agents, but rather a price fixed by an arbitrage relationship. Other examples will be supplied in forthcoming papers. To the best of our knowledge, the boundary conditions arising from the state constraints are completely new as well.

Our model has several variants, mathematically simpler but more limited from the modeling viewpoint:

-

1.

In the first variant, the global production rate of the competitive fringe takes its values in the interval

-

2.

In the second variant, can take a finite number of values , , for a positive integer (we will only discuss the cases when and ).

2.1 A model with two continuous state variables

2.1.1 The dynamics of and

The global production rate of the competitive fringe is assumed to follow the dynamics

| (1) |

where stands for the unitary price of the resource and is a given smooth function, which we take of the form

| (2) |

The first term in (2), i.e. expresses the direct impact of prices on investments, hence on production capacity, as it has been explained in the introduction. A typical possible choice for the second term in (2) is

with suitable positive constants and , in such a way that has a significant effect on only for values of close to or . The term can therefore be seen as a modulation of the first term in near the limits of . It is a proxy for the time delays between the investment decisions of the producers belonging to the competitive fringe and the actual creation of new capacities of production. Indeed, it would be a strong simplification to assume that the investment has an instantaneous effect. This simplification proves acceptable in a very long term model like [1], i.e. at the scale of decades; it permits to keep the theoretical complexity of the latter model at a reasonable level. The situation is much different when one deals with the short term, of the order of a few years: it seems necessary to model inertia effects, memory effects and anticipations of delays between investments and the creation of capacity. Nevertheless, since we wish to keep the model as simple as possible, we limit ourselves to a proxy when addressing the delay effects. The function accounts for a little increase (respectively decrease) in production capacities when the storage facilities are close to empty (respectively full). Indeed, close to empty storage must follow a period when the price is high, thus the investments of the producers in the competitive fringe are at a high level; the latter result in an increase of production capacity, i.e. an increase of , even if the instantaneous price has decreased. The mechanism has to be reversed when the storage facilities are close to full. Hence, we choose which takes a value of the order of for and for . Note that an accurate model with more state variables is possible, but it would be more difficult to understand and to simulate numerically (in particular because it would increase the dimensionality of the problem).

Remark 2.1.

We may add some in the dynamics of and replace (1) with

| (3) |

where is a Brownian motion. This randomness brings the model closer to reality, since a large number of various shocks with relatively small amplitudes arise in the whole industry, from production to demand.

Remark 2.2.

For the numerical simulations, we have to limit ourselves to for . The bounds and are chosen from historical data. Hence, it is convenient to add to another term which vanishes away from and , and which is negative near and positive near . The role of this term is purely technical, and it does not affect the numerical results far enough from and . Therefore, we do not wish to lean too much on it. However, this explains why, in what follows, may also depend explicitly on .

Let us compare the choice of made in (2) with the one made in the long term model [1]. In [1] (with a very simplified description of the storage business), we take as follows:

| (4) |

with , et . The fact that the storage is not involved in (4) obviously comes from the fact that it is not a state variable in [1]. On the other hand, observe that in the oil industry, the range of the storage available for arbitrageurs is relatively small (of the order of of annual production, see Section 6). Given this small range and the small elasticity of demand (see the next paragraph), the strategy of the cartel can be implemented by tuning its production within a small range of values. Indeed, it has been observed for decades that the spare production capacity of the cartel mostly varies between and and that the market share of the cartel stays close to . This aspect is taken into account in [1] and explained immediately after equation (6) in paragraph 2.1.2. But, to keep the present model focused on the interactions between the cartel and the arbitrageurs, we will describe the range of possible production strategies of the cartel by a proxy, namely a cost for the deviation of the cartel’s production from a target production ; this cost will have the form and be a part of the running cost in the optimal control problem solved by the cartel. As a consequence, will stay close to . Therefore, in the present model, since the time scale is of the order of a few years, we may neglect the variations of in (4) because they are small on this time scale (these small variations would induce only a small correction in the strategy of the cartel), i.e. replace the term by .

The demand of the consumers is a decreasing function of the price of the resource; after a suitable choice of units, the simplest demand function is

where the parameter stands for the elasticity of demand. Note that it would be more appropriate to set

, but in the regime that will be considered, the price will never exceed . This linear demand function fits well the observed data in the usual range of oil prices.

The control variable of the monopoly is its production rate . Matching demand and supply yields

.

However, we will instead consider a slightly more general dynamics of , possibly including some small noise in storage capacities:

| (5) |

where is a Brownian motion. We suppose that the volatility is a smooth nonnegative function that vanishes at and and that the quantities and are bounded. This assumption will play an important role in the discussion of the boundary conditions that will be made in paragraph 3 below.

2.1.2 Equilibrium

We look for a stationary equilibrium. Given the unit price of the resource, the cartel solves an optimal control problem.

Let be the associated value function. The price, described by a function , is fixed by ruling out

opportunities for arbitrage. We will see that the functions and satisfy a system of two coupled partial differential equations.

The optimal control problem solved by the cartel knowing the trajectory of is:

| (6) |

where is a positive discount factor, is the cost related to the production of a unit of resource. To complement what has already been said in paragraph 2.1.1, the penalty term is introduced because for decades, the interactions between the cartel and the competitive fringe have resulted in the fact the production level of the cartel has oscillated around with a standard deviation of a few . These interactions have been modeled in [1] and briefly described in the introduction. They partly rely on the fact that the cartel can tune its spare production capacities (in a range varying from to ) in order to drive prices up or down and possibly to deter the fringe from investing. Here, as already explained in paragraph 2.1.1, this aspect is taken into account via a proxy, namely the contribution to the cost.

The dynamic programming principle yields that the value function is a solution of the following Hamilton-Jacobi-Bellman equation:

| (7) |

Introducing the Hamiltonian

in which the maximum is reached by , (7) can be written:

Since, in the regime that will be considered, will always be nonnegative, we omit for simplicity the constraint in the definition of the Hamiltonian: hereafter, we set

| (8) |

and the optimal production rate at and is given by the feedback law

| (9) |

Let us now turn to the price of a unit of resource : ruling out opportunities for arbitrage implies that the price process obeys the following relation,

where is the cost of storing a unit of resource per unit of time when the level of storage is . Recalling that , Ito formula yields:

To summarize, the system of PDEs satisfied by is

| (10) | |||||

| (11) |

for and and with given by (8). We will see in Section 6 below that (10-11) may have singular solutions, which consist of a discontinuous dynamics and price discontinuities, which are actually observed in the historical data (see paragraph 6)

Remark 2.3.

Note that equation (11) is nonlinear with respect to . It is reminiscent of the master equations discussed in [3].

Note also that it seems possible to refine the present model by considering that the arbitrageurs running the speculative storage business are rational agents playing a mean field game. This would lead to a more involved model of a mean field game with a major agent, see [5]. Yet, the resulting system of partial differential equations would have the same structure as (10)-(11).

2.2 A variant in which the production of the fringe is a two-state Poisson process

We now introduce a variant which aims at keeping the essential features of the previous model while being simpler mathematically. We consider a situation in which the production rate can take only two values and is described by a stochastic Poisson process with intensities that may depend on and :

| (12) |

All the other features of the model are the same as in paragraph 2.1, in particular,

the dynamics of is still given by (5). The optimal value of the cartel and the price are described by

and ,

where for , the real values functions are defined on

and satisfy a system of four coupled differential equations.

Introducing the Hamiltonians

(we still omit the constraint that the production rate is nonnegative), and repeating the arguments contained in paragraph 2.1.2, we get the following system of differential equations:

| (13) | |||||

| (14) |

for , , and . The optimal drift of in (5) is then given by if .

Remark 2.4.

Here again, the boundary conditions will be important and non standard.

2.3 An even simpler model

It is possible to simplify further the model by assuming that the production rate of the competitive fringe is a constant . Introducing the Hamiltonian

and repeating the arguments contained in paragraph 2.1.2, we get the following system of two differential equations:

| (15) | |||||

| (16) |

for .

3 Boundary conditions

The systems of partial differential equations must be supplemented by boundary conditions. We are going to discuss the boundary conditions for the full model, and more briefly for the simplified variants proposed in 2.2 and 2.3.

These boundary conditions will translate mathematically the main change in strategic power created by the constraints: while the price is determined by the arbitrageurs when storage is neither full nor empty, the price is driven by the cartel when storage is full or empty. As always in partial differential equations, these boundary conditions are key for the determination of the solution, and therefore of the behaviours of both the cartel and the arbitrageurs. For example, if the range was very small, then the solution would be mostly determined by the boundary conditions, which translates the fact that the cartel could neglect the impact of the arbitrageurs.

3.1 The boundary conditions associated with the model discussed in paragraph 2.1

3.1.1 Boundary conditions at

No boundary conditions are needed at and , because of the assumptions on .

3.1.2 Boundary conditions at and

Preliminary : monotone envelopes of .

For describing the boundary conditions linked to the state constraints , it is useful to introduce the nonincreasing and nondecreasing envelopes of the function : we set

| (17) |

and

| (18) |

The Hamiltonian (resp. ) corresponds to the controls such that the drift of in (5) is nonpositive (resp. nonnegative). It may also be convenient to set

| (19) |

which corresponds to the control for which the drift of in (5) vanishes. Note that is strongly concave with respect . It is easy to check that

The optimal values of in the definition of and are

| (20) | |||

| (21) |

Hence,

| (22) | |||

| (23) |

Assumption 3.1.

Hereafter, we assume that for all , , , the function is strongly concave.

Boundary conditions at .

In view of the assumptions made on , it is not restrictive to focus

on the deterministic case: we take for simplicity.

The state constraint implies that .

Two situations may occur:

-

1.

If for near , then the optimal strategy results in increasing the level of storage. This means that in (11), the drift is positive for near , and no boundary condition is needed for .

-

2.

On the contrary, if for near , then the optimal drift of in (5) must vanish at , i.e. . This relation and the strict monotonicity of imply that can be considered as the control variable at . In other words, the monopoly directly controls the price in this situation.

On the other hand, to rule out arbitrage opportunities but taking into account the state constraints, it is immediate that the price process satisfies

Since the optimal drift of is , we obtain

(24) Another way to understand (24) is as follows: we expect that, in the present case, is nonincreasing with respect to for near . Indeed, if was increasing with respect to for near , then the arbitrageurs would increase the level of storage, i.e. would be positive, in contradiction with the assumption. Then, plugging this information in (11) implies (24).

Turning back to the cartel, we deduce from the considerations above that, among the strategies consisting of keeping fixed at for , the optimal one is

(25) (26) where

(27) and is defined in (19). Note that is unique from Assumption 3.1 and depends on . In this situation, the nonlinear boundary condition

(28) must be imposed at .

Summary.

Boundary conditions at .

Arguing as above and setting , the boundary conditions at can be written as follows:

3.2 The boundary conditions associated with the model in 2.2

The boundary conditions associated with the system (13-14) are obtained in the same manner as in the previous case.

To avoid repetitions, we focus on the boundary , because

the needed modifications with respect to paragraph 3.1.2 are similar for and .

The interested reader will easily find the boundary conditions at from paragraph 3.1.2 and what follows.

As above, we set

| (38) | |||||

The optimal values of in the definition of and are

| (41) | |||

| (42) |

Boundary conditions at .

Setting , , the boundary conditions at are as follows: for and ,

-

•

a condition of the form

(43) understood in a weak sense, (i.e. it holds only if for near ), where achieves the maximum in (46) below (it is supposed to be unique).

-

•

the equation for can be written

(44) with

(45) (46) with , and

(47)

3.3 The boundary conditions associated with the model discussed in paragraph 2.3

Here also, we focus on to avoid repetitions. Let us set

| (48) | |||||

Boundary conditions at .

Setting , the boundary conditions at are as follows:

-

•

a condition of the form

(51) understood in a weak sense, (i.e. it holds only if for near ), where achieves the maximum in (54) below ( is unique).

-

•

the equation for can be written

(52) with

(53) (54)

4 Mathematical analysis of the boundary conditions in the one dimensional model

In what follows, we discuss how the boundary conditions from paragraph 3.3 determine uniquely solution of (15)-(16) near the boundary. Although the argument proposed below is rather formal, it gives useful information on the solutions. More precisely, we are going to see that the boundary conditions induce a unique expansion of the function and of the derivative of the value function near the boundary. The system of PDEs satisfied by and is as follows:

| (55) | |||||

| (56) |

for .

We focus on the boundary conditions at .

First, in the case in which the drift is positive near , and are expected to be smooth at the boundary.

Hence, we focus on the case in which the drift points toward the boundary (i.e. ).

We make the following ansatz:

| (57) | |||||

| (58) |

with . For shortening the notation, let us define the pair .

4.1 A singularity is expected

Let us explain why a singular behavior should be expected near the boundary . Indeed, assume that this is not the case and that ; in this situation, from the assumption made on the sign of the drift near the boundary and the constraint , we deduce that

| (59) |

Then, plugging the ansatz for and into (55)-(56) and focusing on the zeroth order terms, we obtain that

| (60) |

The equations in (60) and (59) form a linear system which is over-determined except for a single value of . Thus, the values of , and are determined. Passing to the first order terms in the expansion of the system, we obtain two second order polynomial equations in and , while is already known. It is then easy to observe that for a generic choice of the parameters, this system of second order equations is not consistent with the already obtained values of , and .

Remark 4.1.

Recall that in the case in which the drift is positive near , no singularity is expected.

4.2 Characterization of the singularity

Proposition 4.2.

Remark 4.3.

The latter condition on will be fulfilled in the numerical simulations in § 6 below.

Remark 4.4.

The value of is obviously which has been defined in paragraph 3.3.

Proof.

Plugging the ansatz into (55)-(56), and using both the boundedness of and the fact that vanishes near , we deduce that

| (61) |

by identifying the higher order terms in the expansion. From the state constraint and the sign assumption on the drift, the following also holds:

| (62) |

Since , we deduce that

| (63) |

Identifying the higher order terms in the expansion, we see that if , then . Therefore, . Now, if , identifying the terms of order leads to

| (64) |

The latter system yields that . Thus . The only possible value of is since the case has

already been ruled out.

Considering the zeroth order terms, we conclude that

| (65) |

Let us introduce the parameter

| (66) |

which is well defined since . Observe that . We deduce that

| (67) |

then that

| (68) |

Defining the numbers by

| (69) |

we finally obtain that

| (70) |

Rewriting the second equation in (65), we obtain

| (71) |

Thus, is impossible if . An easy calculation leads to the fact that this last condition is satisfied (i.e. is large enough) if

| (72) |

∎

5 Approximation by a finite difference method

As already mentioned, the solutions of the system of PDEs may be discontinuous. The numerical scheme must be designed in order to handle these discontinuities.

Let us focus on the case when

| (73) |

We are going to use the latter conservative form in the numerical scheme for (11). Note that

It is useful to introduce the following numerical flux function:

| (74) |

and straightforward calculus leads to

| (75) |

Consider a uniform grid on the rectangle : we set , , with and , , with The discrete approximation of and are respectively named and .

5.1 The discrete version of the system (10-11)

We use the following notation for the three nodes centered finite difference approximation of the second order derivative with respect to :

Consider also the first order one sided finite difference approximations of and , namely

The advection term with respect to in (10) will be discretized with a first order upwind scheme. The discrete version of the Hamiltonian involves the function ,

where , and are respectively defined in (22), (23) and (19).

Note that is nonincreasing with respect to and nondecreasing with respect to .

The discrete version of (10) (monotone and first order scheme) is as follows:

| (76) |

for and . Note that the scheme is actually well defined at (with a slight abuse of notation), because, since , it does not involve . A similar remark can be made in the case when .

We choose the following discrete version of (11):

for and .

The choice of a monotone scheme for (10)-(11) will allow us to capture the shocks that have been already mentioned.

Remark 5.1.

Note that in (10)-(11), neglecting all the viscous effects and taking the derivative of (10) with respect to leads to a weakly hyperbolic system, (only weakly because the Jacobian matrix has repeated eigenvalues and an incomplete set of eigenvectors, i.e. it is not diagonalizable). The scheme proposed above may be modified in order to handle what physicists and mathematicians call sonic points and rarefaction waves, by following the ideas in [8]; in the application presently discussed, it turns out that such an improvement is not necessary because we did not observe any rarefaction wave. In a forthcoming paer, we will consider an economic model described by a weakly hyperbolic system leading to sonic points, and we will discuss a numerical scheme which copes with rarefaction waves.

5.2 The discrete scheme at

In order to write the discrete version of the boundary conditions at , we set

| (80) | |||||

| (81) |

where

| (82) |

and

| (83) |

The numerical scheme corresponding to the boundary condition at consists of two equations for each :

-

1.

the first equation is

(84) - 2.

5.3 The discrete scheme at

For brevity, we do not write the numerical scheme corresponding to the boundary condition at , because the equations (two equations for each value of , ,) may be obtained in exactly the same way as in the previous paragraph.

5.4 Solving the system of nonlinear equations: a long time approximation

The system of equations including (76)-(5.1) for and , and the discrete versions of the boundary conditions at and described above, can be written in an abstract form as follows:

| (90) |

where is a nonlinear map from to such that the Jacobian matrix of has negative diagonal entries.

We aim at solving the discrete system (90) by a long time approximation involving an explicit scheme. The reason for choosing an explicit scheme lies in the complexity of the boundary conditions. Finding an implicit or semi-implicit scheme consistent with the nonlinear boundary conditions seems challenging.

We fix a time step .

Setting and , we compute the sequence by the induction:

| (91) |

and expect that the sequence converges as . It the latter case, the limit is a solution of (90).

6 Numerical simulations

6.1 The parameters

The numerical simulations reported below aim at describing some aspects of the short term dynamics of the oil market. Some of the parameters come from the calibration of the model [1] to prices, CAPEX, OPEX, capacities and production observed in the last three decades. The value of is qualitative reasonable guess, since there is no direct observation of the arbitraged storage. Indeed, the real storage includes strategic, operational and arbitraged storage. The other parameters and functions are qualitatively reasonable guesses to obtain the proxy of the investments delay effects and the costs of storage.

We believe that these numerical simulations make it possible to explain the sharp drops in prices and the general dynamics of the oil industry that have been observed in 2015 and 2020.

We take

with

We set , , and . We refer to Appendix A for a simulation in which the cost of storage is not zero and penalizes situations in which the storage capacities are close to full.

In order to keep the expression of simple, we have decided not to write explicitly the perturbations of near and , which do not impact the solution in the region of interest. In the same vein, recall that and are technical bounds on which are only useful for numerical purposes, i.e. in order to work in a bounded domain: another sensible choice of and would not change the solution in the region of interest.

The mesh parameters are , and the time step is .

6.2 The results

Comments

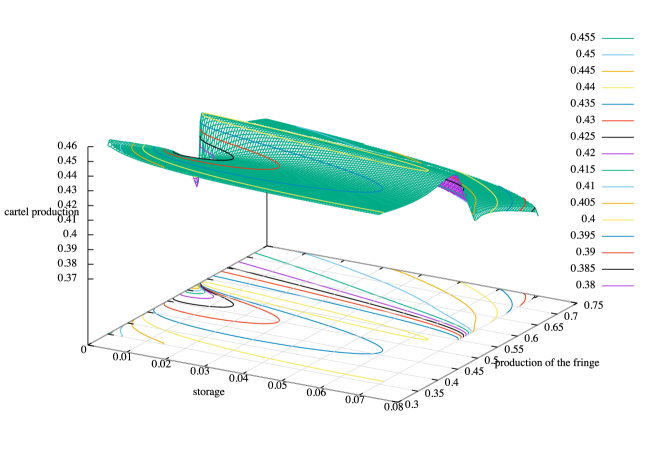

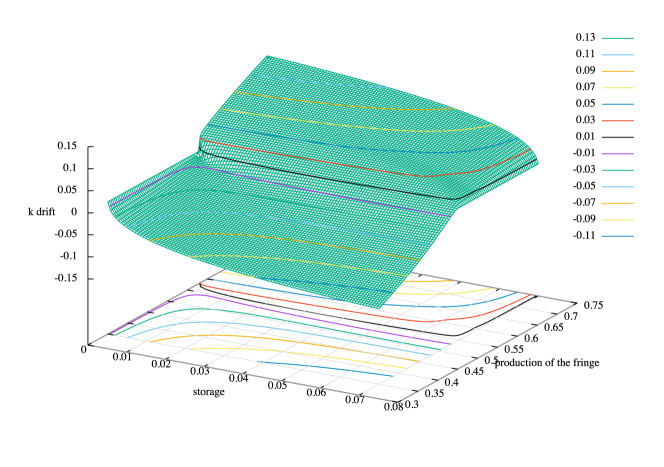

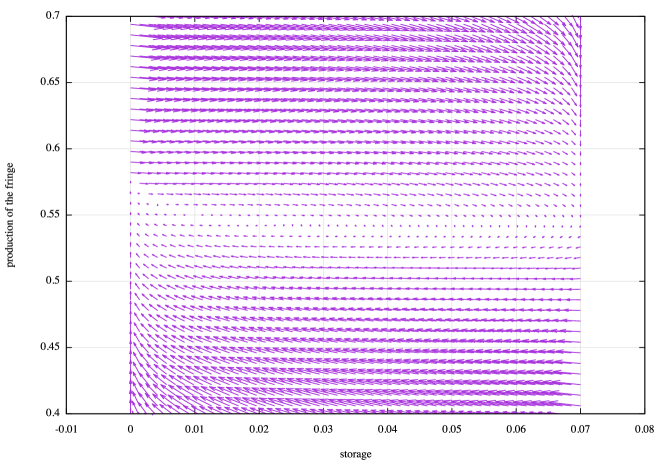

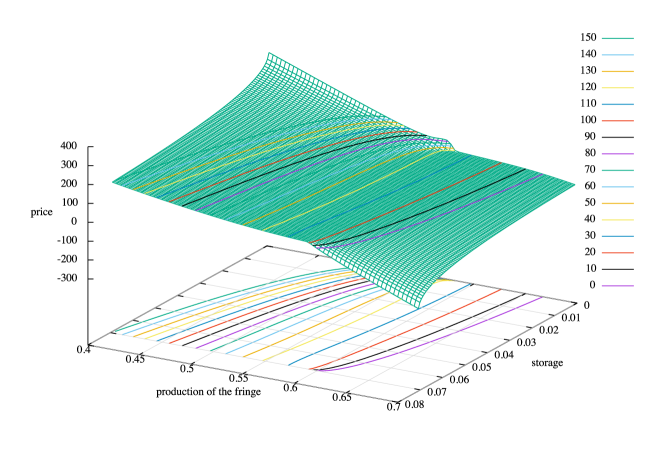

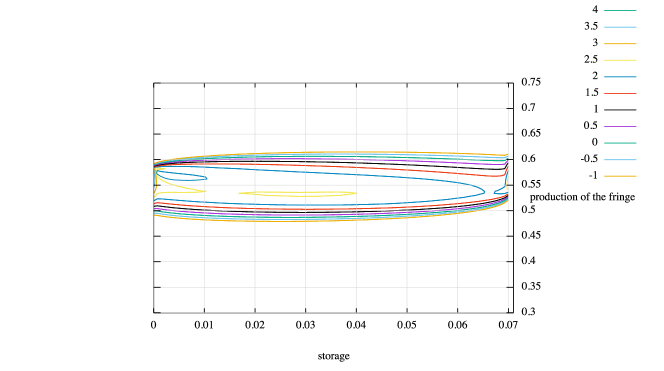

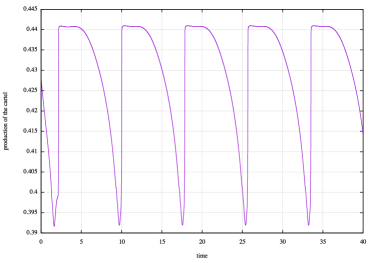

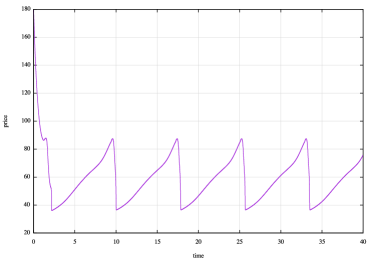

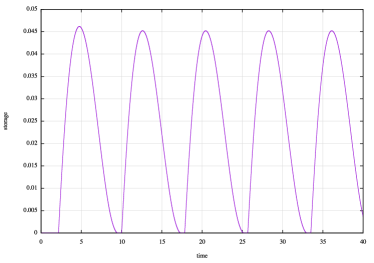

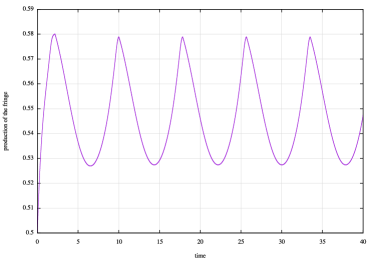

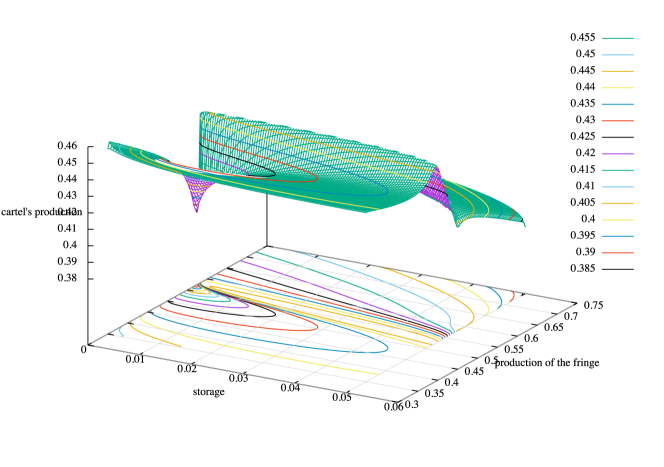

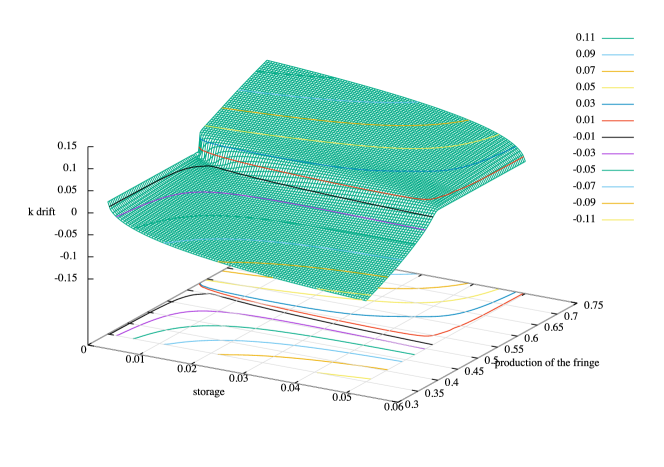

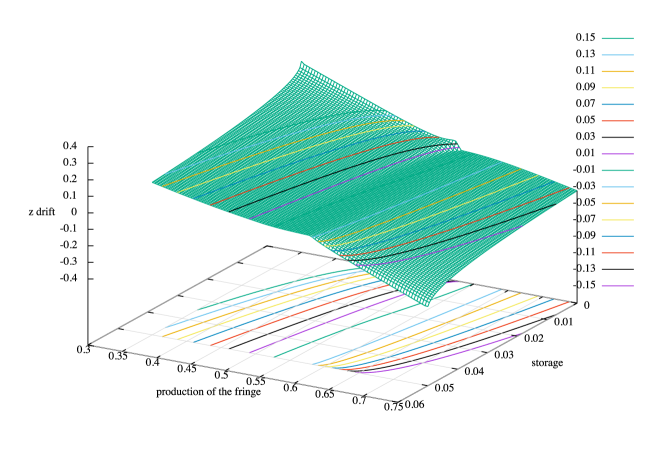

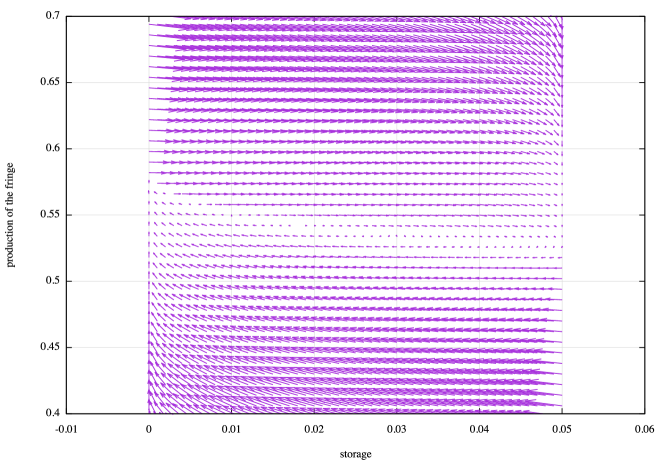

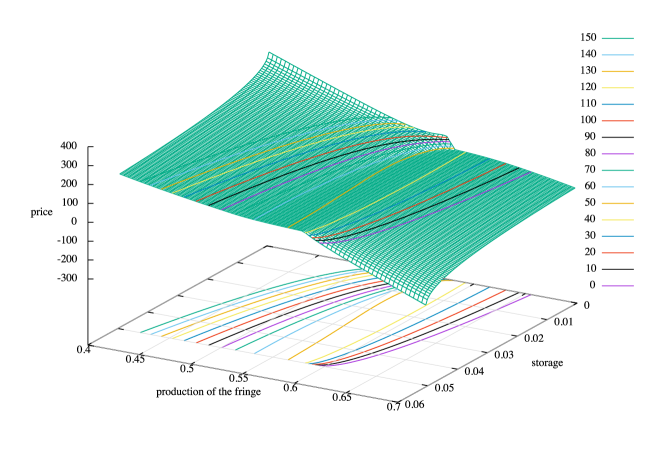

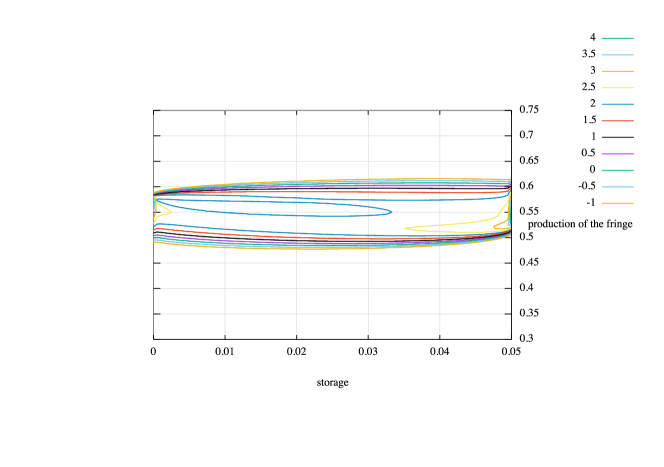

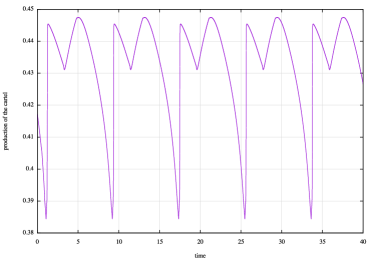

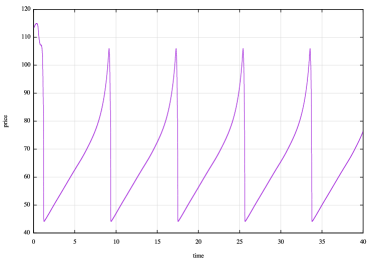

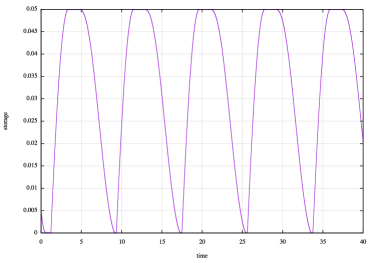

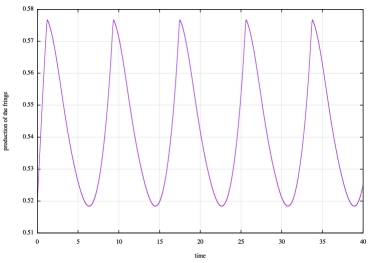

The numerical results are displayed on Figures 6.2-6.2: Figure 6.2 contains the graph and the contour lines of the optimal production level of the cartel as a function of and : is discontinuous across a line in the plane (the discontinuity is smeared a little due to the small diffusion). The amplitude of the discontinuity is maximal at and vanishes at , i.e. at , the optimal production depends continuously on . Further comments on the optimal policy will be made below. Figures 6.2-6.2 give information on the dynamics of and resulting from the optimal policy. Figure 6.2 contains the graph and the contour lines of the drift of the storage level , i.e. , as a function of and . It is of course discontinuous across the same shock line as . Roughly speaking, the region located above (respectively below) the shock in the plane corresponds to a regime when storage increases, (respectively decreases). Note the characteristic behaviour of the optimal drift of for small values of near : it is negative and vanishes at like , in agreement with the theoretical results contained in paragraph 4. The same behavior is observed for large values of near : the optimal drift is positive and vanishes at like . The -component of the drift, i.e. , discontinuous across the same shock line, is displayed on Figure 6.2. the optimal drift vector in the plane is plotted on Figure 6.2. Figure 6.2 contains the graph and the contour lines of as a function of and , which also has a shock. On Figure 6.2, we display the contour lines of the invariant measure of the process : we see that it is concentrated around a cycle that takes place around the shock line. Finally, in Figure 6.2, with the functions and computed numerically by the finite difference method, we neglected the noise and simulated a trajectory starting from the point by means of a standard Euler scheme: we see that after a small delay, the trajectory becomes periodic with respect to time, with a period of the order of years. This will be commented and interpreted below. Note that we purposely initialized the trajectory at which does not belong to the cycle, in order to illustrate the fact that the cycle is attractive.

It is remarkable that the system of PDEs (10)-(11), supplemented with the boundary conditions linked with the constraints on the state variable and discussed in paragraph 3.1.2, leads to a discontinuous optimal strategy as in Figure 6.2. The discontinuous solutions obtained in the simulations may seem surprising. We are going to explain why, on the contrary, the simulated optimal policy matches qualitatively well what has been observed in the past few years. We are first going to see that a cyclic strategy of the cartel is naturally linked to the singularity displayed on Figure 6.2. After having described the cycle, we will explain how these results shed a light on what has been observed in 2015 and in 2020.

Note that the level of noise in the present simulation is smaller than it is actually. We have underestimated the noise in order to shed some light on the mechanism resulting from the model, which would appear less clearly in the presence of noise. Note also that, knowing and from the simulation of the system of PDEs (10)-(11), we purposely simulated (1) and (5) instead of (3) and (5), (recall that ), in order to exhibit a stable cycle and its time periodicity. As we can see on Figures 6.2, 6.2 and 6.2, the present model, in the absence of noise, leads to a cyclic behaviour on the time scale of few years (more details will be given below). Since there are important noise and risk factors in the oil market, such a cyclic behaviour is not always observed, but is has actually been observed twice in the recent past, in 2015 and in 2020.

6.3 Interpretation of the observed cycle

The cycle that is observed in the numerical simulations, see Figures 6.2 and 6.2, is drawn schematically on Figure 6.3. In the absence of substantial randomness, we can make out four phases.

Below, we describe the four phases and relate them to Figure 6.2, focusing for example on the time period approximately from to (years).

- Phase ():

-

in this phase, which corresponds to the time interval approximately from to (or to ) on Figure 6.2, storage is close to minimal, i.e. (recall that we only deal with the storage managed by the arbitrageurs). The monopolistic cartel has therefore the power to drive the price up by maintaining a low level of production. When the price goes up, the fringe producers invest in new production capacities and increase gradually their market share. At some point, the monopolistic cartel would like to drive price down. However, the monopolistic cartel is aware that when it does so by increasing its own production, arbitrageurs start storing the resource, which diminishes the intended impact of the policy. In order to prevent the period of low prices from lasting too long, it is therefore optimal for the monopolistic cartel to brutally increase its production, thereby initiating the phases that bring the monopolistic cartel back to its zone of profit. This is what shows the numerical simulation of Edmond 2; the strategic shock appears clearly on Figure 6.2: indeed, it can be seen that when storage is minimal, the production of the monopolistic cartel increases brutally when , the production of the fringe crosses a critical value. Then, on Figure 6.2, we see that this brutal increase in production makes the price fall. This phenomenon has been observed in 2015 and 2020.

- Phase ():

-

the time interval approximately from to on Figure 6.2. When the price has fallen, the stored quantity of resource increases rapidly, and the state is drifted to the right with a velocity nearly parallel to the -axis. After having brutally increased its production, the cartel may let it decrease smoothly until storage gets full. In this regime, the arbitrageurs fix the price and the price increases almost linearly with respect to time, at a rate close to the interest rate .

- Phase ():

-

the time interval approximately from to on Figure 6.2. Storage is full. The monopolistic cartel can now increase its production again and maintain the low level of price as long as necessary in order to deter the fringe from investing or even to diminish its existing capacities (see below). The production of the fringe, , decreases to the value that suits the cartel.

- Phase ():

-

the time interval approximately from to on Figure 6.2. Since the value of is low enough, the monopolistic cartel may reduce its production. Then the stored quantity of resource decreases and the price is driven up more rapidly than in the phases and . When storage is empty, the cartel can start the phase of the cycle and raise price to the optimal value.

Even if some aspects may vary with the choice of parameters, see for example Appendix A, the main features discussed above seem robust with respect to the choice of the parameters: the discontinuity and the cycle comprising a low price period in order for the cartel to recover market shares and a high price period leading to large profits. One can also see that the present model gives rise to backwardization and contango periods: indeed, taking as an approximation for the slope of the futures curve, Figure 6.2 shows that backwardization (resp. contango) occurs when storage is empty (resp. full). Note that given the noise, backwardization and contango may also occur when the constraints on storage are still not binding.

6.4 Discussion on what happened in 2015 and 2020

- In 2015,

-

OPEC had decided to reconquer the market share that had been lost due to the fast development of the US shale industry from 2009 to 2015. The price drop was then strong and sudden: prices dropped from to per barrel in a few months. At that time, this price drop was analyzed as an attack against US shale. In the spirit of the present model, it was rather an attack against all competitors, aimed at recovering market share. Indeed, the OPEC strategy had a strong impact not only on the US shale industry, which in fact, proved strong resiliency and coping abilities, but in many other fringe producers.

- In 2020,

-

things happened in a less “classical” way. A “rare disaster” occured. An exogenous shock to demand occurred in the first quarter of the year, with a magnitude of the order of ten times the standard deviation of the usual shocks to demand . Although it was not designed to handle such situations, our model seems to give a good explanation of what happened. In order to understand 2020, let us recall that in the present model, (resp. ) is the ratio of the non OPEC capacity of production to the global level of demand, (resp. the ratio of the OPEC production to the global level of demand). Before 2020, the global level of demand increased regularly from year to year (and rather slowly) with an annual growth rate of the order of . In the first semester of 2020, the sanitary crisis resulted in a sudden, unexpected and exceptional drop of the global demand, of the order of to . Therefore, the variable got suddenly increased by to , and the monopolistic cartel got carried to the upper side of the shock. In our model, the optimal response was to increase immediately production. This is precisely what happened to the surprise of many. Many observers have considered that what seemed a conflict between OPEC and Russia, which led to an increase in production while the demand collapsed, was suicidal. However, from the viewpoint of our model, this strategy was simply intended at entering the phases of the cycle, which drive to the value desired by the cartel. In other words, the aim was to reduce the capacity of production of the competitors as fast as possible. Indeed, as soon as OPEC had increased its production after the collapse of the demand, storage became rapidly full (stage ). The maximal level was reached in a few weeks, and the cartel could drive prices to a very low level (prices even went negative during a very short period). Many planned investments stopped, and some production units were definitely closed. After this period, OPEC started to strongly reduce its production. The production drop was strong in absolute value, but not so strong relatively to the global demand, hence in good agreement with our model (recall that all the quantities in the present model are reduced by taking the ratio over the global demand). Then, in the second semester of 2020 and in 2021, the demand should increase, which would imply a fast decrease of .

Hence, despite the fact that the collapse of the global demand in 2020 was rare event, (seven to ten times the standard deviation of the historical shocks to global demand), our model gives a satisfactory qualitative explanation of the cycle that is being observed (in a very accelerated version) in 2020.

7 Conclusion

We have proposed a model which presents new aspects:

-

•

new ideas on the interactions between a cartel (dominant player) and a crowd of arbitrageurs, emphasizing the impact of the constraints on the arbitrageurs,

-

•

a new system of coupled non linear PDEs and boundary conditions,

-

•

a new kind of discontinuous optimal strategy for the dominant player facing the crowd,

-

•

original numerical schemes, robust enough to catch the latter discontinuous solution.

Finally, the output of the model shed original light on an unprecedented crisis.

Acknowledgement 1.

This research was supported by Kayrros. Y. Achdou, C. Bertucci, J-M. Lasry and P-L. Lions acknowledge partial support from the Chair Finance and Sustainable Development and the FiME Lab (Institut Europlace de Finance). Y Achdou and C. Bertucci acknowledge partial support from the ANR (Agence Nationale de la Recherche) through MFG project ANR-16-CE40-0015-01.

References

- [1] Yves Achdou, Charles Bertucci, Jean-Michel Lasry, Pierre-Louis Lions, Antoine Rostand, and José Scheinkman. A long-term mathematical model for the oil industry. in preparation.

- [2] Yves Achdou, Pierre-Noel Giraud, Jean-Michel Lasry, and Pierre-Louis Lions. A long-term mathematical model for mining industries. Appl. Math. Optim., 74(3):579–618, 2016.

- [3] Charles Bertucci, Jean-Michel Lasry, and Pierre-Louis Lions. Some remarks on mean field games. Comm. Partial Differential Equations, 44(3):205–227, 2019.

- [4] Pierre Cardaliaguet, François Delarue, Jean-Michel Lasry, and Pierre-Louis Lions. The master equation and the convergence problem in mean field games, volume 201 of Annals of Mathematics Studies. Princeton University Press, Princeton, NJ, 2019.

- [5] Jean-Michel Lasry and Pierre-Louis Lions. Mean-field games with a major player. C. R. Math. Acad. Sci. Paris, 356(8):886–890, 2018.

- [6] Pierre-Louis. Lions. Cours du Collège de France. http://www.college-de-france.fr/default/EN/all/equ-der/, 2011-2014.

- [7] Edmond Rostand. Cyrano de Bergerac. 1897.

- [8] Timothy A. Smith, David J. Petty, and Carlos Pantano. A Roe-like numerical method for weakly hyperbolic systems of equations in conservation and non-conservation form. J. Comput. Phys., 316:117–138, 2016.

Appendix A A simulation with a cost of storage

Here, we keep the parameters as in Section 6, except that we take and we suppose that there is a cost of storage, which has the form

Such a cost heavily penalizes the situations in which storage is close to full.

The results have been obtained using exactly the same method as in Section 6, and are represented on Figures A, A, A, A, A and A. The results look rather similar, but since is larger than in Section 6, and since that near to full storage is penalized, these is no phase in the cycle, as can be seen on Figure A.