Partial least squares for sparsely observed curves with measurement errors

Abstract

Functional partial least squares (FPLS) is commonly used for fitting scalar-on-function regression models. For the sake of accuracy, FPLS demands that each realization of the functional predictor is recorded as densely as possible over the entire time span; however, this condition is sometimes violated in, e.g., longitudinal studies and missing data research. Targeting this point, we adapt FPLS to scenarios in which the number of measurements per subject is small and bounded from above. The resulting proposal is abbreviated as PLEASS. Under certain regularity conditions, we establish the consistency of estimators and give confidence intervals for scalar responses. Simulation studies and real-data applications illustrate the competitive accuracy of PLEASS.

Keywords: Functional data analysis; Functional linear model; Krylov subspace; PACE; Principal component analysis

1 Introduction

Scalar-on-function (linear) regression (SoFR) is a basic model in functional data analysis (FDA). People have applied it to domains including chemometrics (e.g., Goutis 1998), food manufacturing (e.g., Aguilera et al. 2010), geoscience (e.g., Baíllo 2009), medical imaging (e.g., Goldsmith et al. 2011), and many others. This model bridges a scalar response to a functional predictor (), with the argument of often referred to as “time” and confined to a bounded and closed interval . (Without loss of generality, we take throughout this paper and omit it in integrals.) To be specific,

| (1) |

where: (resp. ) is the expectation of (resp. ); the coefficient to be estimated, , belongs to (viz. -space on with respect to (w.r.t.) the Lebesgue measure); zero-mean noise is of variance one; and the notation is short for . The auto-covariance function of is denoted by

| (2) |

and is assumed to be continuous on . Thus has countably many eigenvalues, say , such that . Corresponding eigenfunctions are respectively . In order to ensure the identifiability of , we assume the coefficient function belongs to , where denotes the linear space spanned by functions in the parentheses with the overline representing the closure. Corresponding to , the auto-covariance operator is defined by, for each ,

| (3) |

In this case, the (Hilbert-Schmidt) operator norm of equals , viz. the -norm of . We abuse too for the matrix norm induced by the Euclidean norm, i.e., for arbitrary and , . It is well known that is actually the largest eigenvalue of and reduces to the Euclidean norm for vectors.

The typical first step in estimating is to project it onto a space spanned by basis functions either fixed (e.g., wavelets or splines) or data-driven (e.g., functional principal component (FPC) or functional partial least squares (FPLS)). There are already numerous studies comparing FPC and FPLS (e.g., Reiss & Ogden 2007, Aguilera et al. 2010). They concluded that FPLS is superior to FPC in the sense that the former provides a more accurate parameter estimation and yields more parsimonious models (Albaqshi 2017, pp. 53).

1.1 Introduction to functional partial least squares

Partial least squares (PLS) is a name shared by diverse algorithms in the multivariate context, including nonlinear iterative PLS (NIPALS, Wold 1975) and the statistically inspired modification of PLS (SIMPLS, de Jong 1993) as two of the most well-known. Analogously, the implementation of FPLS is far from unique: it constructs basis functions by recursively maximizing (the functional version of) Tucker’s criterion (see, e.g., Proposition 1 of Preda & Saporta 2005, for its expression) subject to various orthonormality constraints. For FoFR, Delaigle & Hall (2012b) observed the equivalence between functional extensions of NIPALS and SIMPLS: the first basis functions arising via these two distinct routes span spaces identical to the functional version of -dimensional Krylov subspace (KS), namely,

| (4) |

where is the th power of , and

| (5) |

To be explicit, starting with , we define recursively, by

| (6) |

Delaigle & Hall (2012b, Theorem 3.2) showed that must be located in . Hence is the limit (in the sense) of

Once we obtain by (modified-Gram-Schmidt) orthonormalizing w.r.t. (following Algorithm 1 below or Lange 2010, pp. 102), can then be rewritten as

| (7) |

where

| (8) |

Now consider a new pair . Then as ,

| (9) |

approaches the conditional expectation of given , viz.

| (10) |

in which

| (11) |

We refer to as the th FPLS score (associated with ). (Henceforth superscript * indicates items associated with the new realization .) Plugging empirical counterparts into (7) and (10), the proposal of Delaigle & Hall (2012b, Section 4) is equivalent (in terms of estimating as well as predicting ) to functional counterparts of NIPALS and SIMPLS.

1.2 Sparsity and measurement errors

Like most FDA techniques, FPLS algorithms are designed for dense settings, i.e., realizations of are supposed to be densely observed, since their implementations inevitably involve approximations to integrals. This condition is not expected to be fulfilled under all circumstances. For example, in typical clinical trials, participants cannot be monitored 24/7; instead, they are required to visit the clinic repeatedly on specific dates. Due to cost and convenience, the scheduled visiting frequency is doomed to be sparse for essentially every subject. What is worse is that subjects tend to show up on their own basis with frequencies lower and more irregular than scheduled. Similar difficulties can arise in missing data problems where a number of recordings are lost for whatever reason.

The training sample consists of two-tuples independently and identically distributed (iid) as . Specifying the sparsity and measurement errors simultaneously, we suppose the th trajectory is measured at only (random) time points (say ) with corresponding contaminated observations

| (12) |

where and the are white noise with mean zero and variance one. We assume that all the time points and error terms are independent across subjects and from each other. More rigorous description is detailed in Appendix B. This joint setup of sparsity and error-in-variable is also considered in existing literature including but not limited to Yao et al. (2005a, b), Xiao et al. (2018), and Rubín & Panaretos (2020).

Remark 1.

For each , it is not necessary to order in a specific way. Additionally we suggest not viewing as the sum of and a white noise process, otherwise more mathematical effort is needed in the definition to ensure rigor. We utilize only (univariate) random variables and never attempt to approximate integrals involving an entire function .

As pioneers who extended classical FPC to this challenging setting, James et al. (2000) postulated a reduced rank mixed effects model fitted by the expectation-maximization algorithm and penalized least squares. Abbreviated as PACE, the proposal of Yao et al. (2005a, b) introduces a local linear smoother (LLS) estimator for followed by FPC scores () which are approximated by conditional expectations. To the best of our knowledge, there are still few extensions of FPLS applicable to such a scenario. In this work, we attempt to fill in this blank by developing a new technique named Partial LEAst Squares for Sparsity (PLEASS), handling sparse observations and measurement errors simultaneously.

Here is a sketch of the procedure for PLEASS. First, thanks to the iid assumption on subjects, we are able to pool together all the observations in order to recover the variance and covariance functions from which basis functions are extracted. Then, is estimated by plugging empirical counterparts into at (7). It is worth noting that, since is not observed densely, PLEASS does not give a consistent prediction for at (10); instead it constructs a confidence interval (CI) for through conditional expectation.

The remainder of this paper is organized as follows. Section 2 details the implementation procedure for PLEASS. In Section 3, we present asymptotic results on the consistency of estimators and on the distribution of . Section 4 applies PACE and PLEASS to both simulated and authentic datasets and compares their resulting performances. Concluding remarks are given in Section 5. Finally we include more technical arguments in appendices.

2 Methodology

2.1 Estimation and prediction

The first phase of PLEASS is to find estimators for at (1), at (2), at (5), and at (12), respectively, say, , , and . Existing methods for reconstructing the variance and covariance structure from sparse observations roughly fall into three categories: i) kernel smoothing (e.g., Yao et al. 2005a, b, LLS in and Li & Hsing 2010 and Paul & Peng 2011, the modified kernel smoothing in), ii) spline smoothing (e.g., fast covariance estimation (FACE) by Xiao et al. 2018), and iii) maximum likelihood (ML, e.g., James et al. 2000, restricted ML in and Peng & Paul 2009 and Zhou et al. 2018, quasi-ML in). Typically, the third category requires initial values obtained through the first two and is hence more time-consuming. In the numerical study (Section 4 below), we adopt both LLS (whose details are relegated to Appendix A, following Yao et al. 2005a, b) and FACE. LLS, which is also exploited by PACE, has nice asymptotic properties (Hall et al. 2006), whereas FACE runs faster and has competitive accuracy.

Remark 2.

In theory, the framework of PLEASS is flexible as to how to estimate , , , and , as long as , , , and all converge to zero as diverges (with denoting the -norm). It is even more flexible in practice and permits any way of recovery preferred by users. Theoretical results in upcoming Section 3 are merely demos corresponding to LLS; our results can be adapted to other approaches.

It is understood that in numerical implementation integrals have to be approximated by, e.g., quadrature rules. Tasaki (2009) gave upper bounds on the (absolute) approximation errors for Riemann and trapezoidal sums; these bounds tend to zero as the discretized grid becomes dense. We hereafter use (abuse) the integral notation even for corresponding numerical approximations.

Recursively define the empirical counterpart of at (6) by

| (13) |

The recursion is initialized by taking to be the identity operator. Then orthogonal basis functions are constructed from (following Algorithm 1 or Lange 2010, pp. 102). Evidently a plug-in estimator for is given by

| (14) |

These estimators converge to the true as and , respectively, diverge at specific rates (see Theorem 1), with

| (15) |

estimating (8).

Predicting at (10) is a problem fairly different from estimation. Since (viz. the contaminated ) is only observed at () time points, it is not practical to numerically integrate the product of and . Instead we target the prediction of a surrogate for . That surrogate, denoted by , is defined at (18) below. Write

and, for integer ,

Conditional on and , in view of the identity

the best linear unbiased prediction for is

| (16) |

This predictor minimizes over all linear functions subject to . It is even the best prediction over all measurable , linear or not, as long as and are jointly Gaussian (Harville 1976, Theorem 1). Geometrically speaking, at (16) is the (orthogonal) projection of at (11) onto (given and ). Then the projection of onto the same space is ; recall is defined at (9). If we define the matrix , then we have

| (17) |

Accordingly,

| (18) |

is a natural surrogate for at (10).

It is therefore justified to predict by the empirical counterpart of (17), namely,

| (19) |

which is constructed by replacing population quantities , , , , and all at (17) with, respectively, , at (15), and

| (20) | ||||

| (21) | ||||

| (22) |

It remains to construct a CI for at (10). From the perspective of projection again, we have

Under Gaussian assumptions (as in Corollary 1) and conditioning on and , the error is asymptotically normally distributed. An asymptotic (conditional Wald) CI for at (10) is then

where is the standard normal quantile.

2.2 Selection of number of basis functions

We are unclear on how to estimate the degrees of freedom (DoF) asscociated with PLEASS prediction at (19), partially because of its intrinsic complexity; at least there seems no natural extension from the work of Krämer & Sugiyama (2011) on DoF computation for (multivariate) PLS. As a consequence, rather than using generalized cross validation (Craven & Wahba 1979) and various information criteria, it sounds more reasonable to employ (leave-one-out) cross-validation (CV) as the tuning scheme: choose an integer by minimizing

in which predicts the th response with all the other subjects kept for training. Define by (with replaced by empirical counterparts in practice) the fraction of variance explained (FVE) by the first eigenfunctions. An upper bound for is then given by, e.g.,

| (23) |

This cut-off is one of the default truncation rules frequently used for the Karhunen-Loève series. Since, as mentioned in Section 1, FPLS typically needs fewer terms than FPC to reach a comparable accuracy, (23) is very likely to be large enough for tuning PLEASS. Another heuristic upper bound is provided by Delaigle & Hall (2012a, Section 3): , acceptable for a small or moderate .

3 Asymptotic properties

Our theoretical results are established under (C1)–(C16) in Appendix B. The first six of these assumptions formalize the setup of sparsity and measurement errors; (C7)–(C14) are prepared for the consistency of LLS in Appendix A. For arbitrary fixed , the consistency of at (14) is a direct corollary of Zhou (2019, Theorem 1). Unfortunately, this argument may not apply to the scenario with diverging , since the sequential construction in (13) tends to induce a bias accumulating with increasing . As a result, it is indispensable to impose a sufficiently slow divergence rate on , such as, e.g., those required by (C15) or (C16).

Theorem 1.

Analogous to PACE, our PLEASS results in an inconsistent prediction (see Theorem 2): the discrepancy between our forecast and our surrogate converges to zero (unconditionally and in probability) but not the discrepancy between our forecast and the true mean of . Nevertheless, this phenomenon is far from disappointing: one implication is that is asymptotically distributed as ; an asymptotic distribution of hence follows. In particular, the result for Gaussian cases is presented in Corollary 1.

Theorem 2.

4 Numerical illustration

PLEASS is compared here with PACE in terms of finite-sample numerical performance. As mentioned in Section 2.1, both LLS and FACE (implemented respectively via R packages fdapace (Carroll et al. 2020) and face (Xiao et al. 2019)) were utilized to eestimate population quantities at (1), at (2), at (5), and at (12). Resulting combinations, viz. PLEASS+LLS, PACE+LLS, PLEASS+FACE and PACE+FACE, are abbreviated as PLEASS.L, PACE.L, PLEASS.F and PACE.F, respectively. Our code trunks are accessible at https://github.com/ZhiyangGeeZhou/PLEASS.

4.1 Simulation

Each sample consisted of iid paired realizations of with and both of zero mean. was set up as a Gaussian process, i.e., were all iid as standard normal. Error terms were also standard normal. We took 100, 90, 80, 10, 9, 8, 1, 0.9, and 0.8 as the top nine eigenvalues of operator at (3); all the rest were 0. Correspondingly, the top nine eigenfunctions were taken to be (normalized) shifted Legendre polynomials (refer to Hochstrasser 1972, pp. 773–774) of order 1 to 9, say ; unit-normed and mutually orthogonal on , they were generated through R-package orthopolynom (Novomestky 2013). The slope function was given by one of the following cases:

| (24) | ||||

| (25) | ||||

| (26) |

Two sorts of signal-to-noise-ratio (SNR) were defined, i.e., and . For simplicity, we took ( or ). To embody the sparsity assumptions, in each sample, was observed only at () points uniformly selected from . In total there were six combinations of settings. 200 iid samples were generated for each of them. We randomly reserved 20% of the subjects in each sample for testing and used the remainder for training. After running through all samples, we computed 200 values of relative integrated squared estimation error (ReISEE)

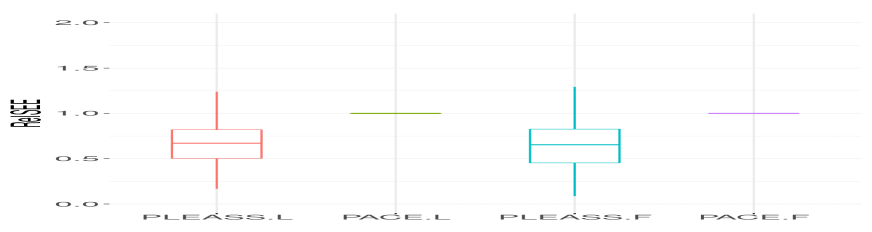

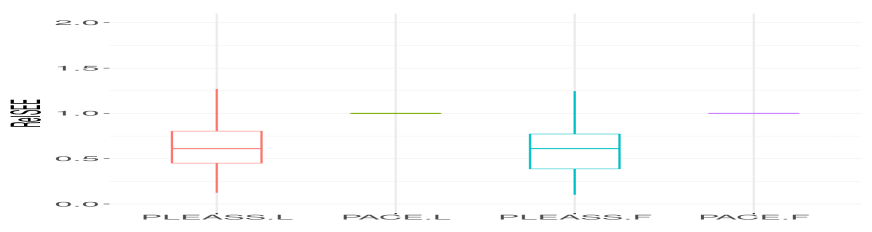

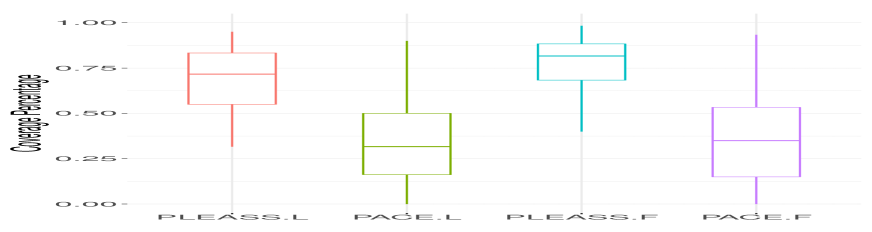

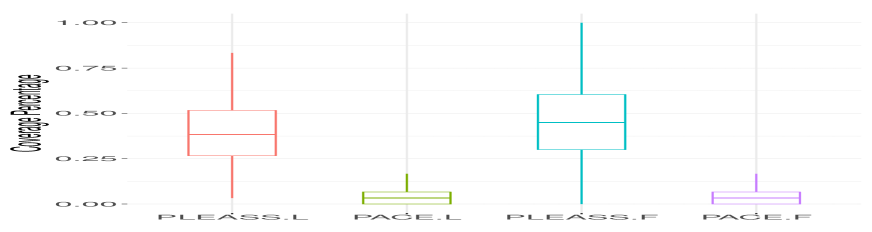

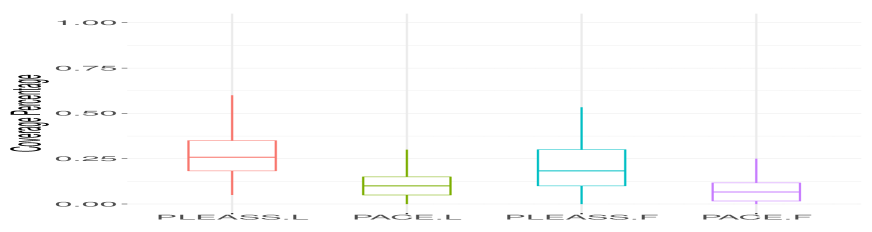

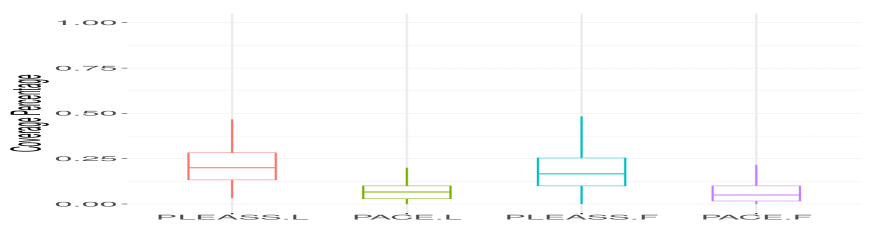

Since neither PACE nor PLEASS leads to consistent predictions, it is better to evaluate the prediction quality via the coverage percentage (CP) of CIs constructed for testing subjects, viz.

where is the asymptotic (95%) CI for , and is the index set for testing portion with cardinality .

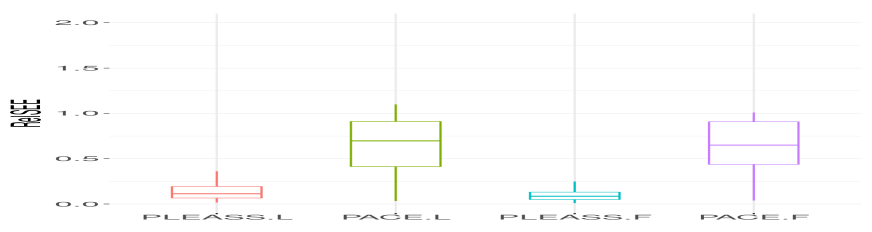

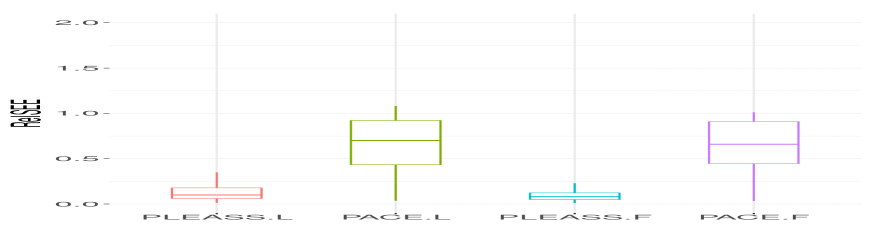

When was constructed from eigenfunctions corresponding to large or moderate eigenvalues (viz. at (24) or (25)), PLEASS performed better in term of ReISEE; see the first two rows of Figure 1. Particularly, at the second row of Figure 1, ReISEE values of PLEASS were mostly lower than one, while PACE boxes was trapped at one. An ReISEE box sticking around one implied estimates concentrated around the most trivial , i.e., the corresponding method failed to output non-trivial estimates. This failure was caused by zero inner products between and estimated basis functions; this happened frequently if was mainly associated with a small portion of total variation (of ) that was likely to be smoothed out in recovering and . Such was exactly the case for PACE in the scenario (25) and for both PACE and PLEASS with at (26).

As seen in Figure 2, CP boxes belonging to PACE stayed at a low level, especially for scenarios (25) and (26). This phenomenon was consistent with the performance of PACE in estimating under corresponding settings. In contrast, PLEASS was more likely to output CP values closer to the stated level (95%), though we must admit that their coverages were still far from satisfactory especially with at (25) and (26). Looking into those not covered by , we noticed that the majority of missed fell at the right-hand side of . A possible cause of miss-covering lay in the bias of estimates for means of and ; a larger size of training set might be helpful. Moreover, although SNR had little impact on estimation (compare the two columns of Figure 1), CP values appeared to be higher with a smaller SNR (compare the two columns of Figure 2): did not vary with SNR, while larger (resulting from smaller SNR) widened and enhanced the coverage of .

4.2 Application to real datasets

We then applied PLEASS to two real datasets. The first came from a clinical trial, whereas the second was densely observed but recorded with missing values.

- Primary Biliary Cholangitis (PBC) data.

-

Initially shared by Therneau & Grambsch (2000), the dataset pbcseq (accessible in R-package survival, Therneau 2020) was collected in a randomized placebo controlled trial of D-penicillamine, a drug designed for PBC. PBC is a chronic disease in which bile ducts in the liver are slowly destroyed; it can cause more serious problems including liver cancer. All the participants of the clinical trial were supposed to revisit the Mayo Clinic at six months, one year, and annually after their initial diagnoses. However, participants’ actual visiting frequencies, with an average of 6, varied among patients, ranging from 1 to 16. This led to sparse and irregular recordings. Although the clinical trial lasted from January 1974 through May 1984, to satisfy the prerequisites of LLS, we included only measurements within the first 3000 days and kicked out subjects with fewer than two visits. At each visit, several body indexes were measured and recorded, including alkaline phosphatase (ALP, in U/L) and aspartate aminotransferase (AST, in U/mL), both evaluating the health condition of liver. We focused on this pair of indicators and attempted to model a linear connection between participants’ latest AST measurements (response) and their ALP profiles (functional predictor).

- Diffusion tensor imaging (DTI) data.

-

Fractional anisotropy (FA) is measured at a specific spot in the white matter in the brain, ranging from 0 to 1 and reflecting the fiber density, axonal diameter and myelination. Along a tract of interest, these values forms an FA tract profile. Collected at the Johns Hopkins University and Kennedy-Krieger Institute, dataset DTI (in R-package refund, Goldsmith et al. 2019) contained FA tract profiles for the corpus callosum measured via DTI. Though these trajectories were not sparsely measured, a few of them suffered from missing records which could be handled by PACE and PLEASS without presmoothing or interpolation. We investigated the relationship between participants’ FA tract profiles (predictor) and their Paced Auditory Serial Addition Test (PASAT) scores (response), where PASAT is a traditional tool assessing impairments in the cognitive functioning and is extensively used in the diagnosis of, e.g., the multiple sclerosis (Tombaugh 2006).

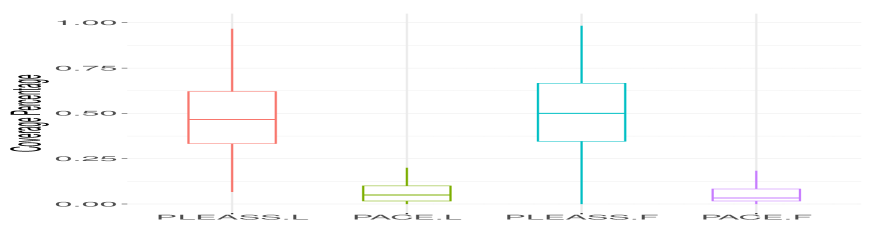

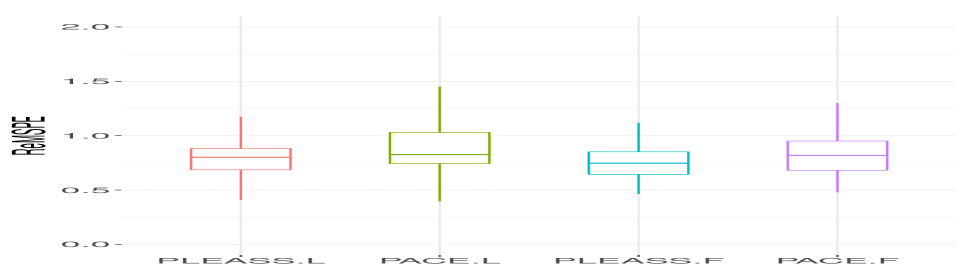

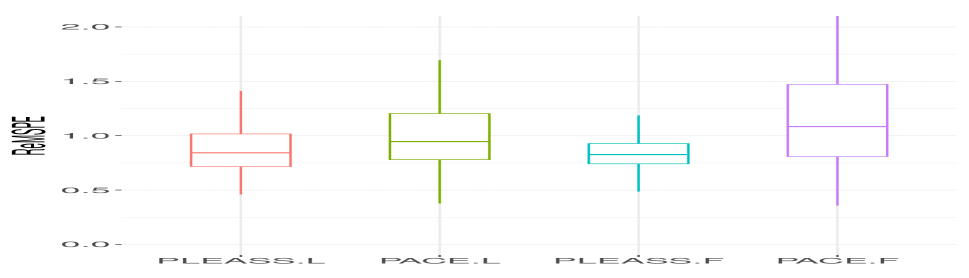

For each dataset, 200 random splits were carried out. In each split, (roughly) 80% of the subjects were put into the training set while the remainder were kept for testing. After predicting responses for the test set, we generated values of relative mean squared prediction error (ReMSPE), viz.

for each approach and each split. Here is the prediction for the th response, and is the mean training response. ReMSPE values for PBC and DTI cases were collected and summarized into boxes; see Figure 3. In both applications, PLEASS was demonstrated to be more competitive than PACE, enjoying lower medians and smaller dispersion of ReMSPE values. Analogous to the previous simulation study, Figure 3 shows that FACE performs close to LLS when used with PLEASS. As a result, PLEASS.F might be preferred if a low time consumption were particularly appreciated.

5 Conclusion and discussion

The main contributions of our work are summarized as follows. First, we propose PLEASS, a variant of FPLS modified for scenarios in which functional predictors are observed sparsely and with contamination. Second, not only do we give estimators and predictions via PLEASS, but also we construct CIs for mean responses. Allowing to diverge as a function of , our theoretical work is among the few asymptotic results available for FPLS and its variants. Third, we numerically reveal the advantage of PLEASS in specific scenarios.

Estimators for the variance and covariance structure may be further revised. If trajectories are no longer independent of each other (e.g., spatially correlated curves representing distinct cities), it is more reasonable to employ the proposal of Paul & Peng (2011), viz. a weighted version of LLS. Another concern is the nature of missingness: the mode of sparsity here is assumed independent across trajectories and measurement errors. Even if the missingness is permitted to be correlated with the values of unobserved time points, we speculate that, after necessary modifications, estimates of the ML type would be still promising in estimating components of covariance structure.

In contrast with PLEASS, which is for now concentrated on SoFR only, PACE is more versatile: it is applicable even to function-on-function regression (FoFR, with response and predictor both functional) and is capable as well of recovering predictor trajectories. Merging PLEASS into the framework of Zhou (2020), we may adapt it to FoFR with sparsely/densely observed functional predictors/responses. Moreover the application of PLEASS is not limited to linear models, since it is practicable to embed FPLS techniques into the iteratively reweighted least squares for maximizing likelihood (Marx 1996); Albaqshi (2017) and Wang et al. (2020) successfully applied this idea to functional logistic regression and functional joint modeling, respectively.

Acknowledgment

Special thanks go to Professors Ling Zhou and Huazhen Lin (both serving for the Southwestern University of Finance and Economics, China) and Professor Hua Liang (George Washington University, United States) for the generous sharing of their source codes. The authors’ work is financially supported by the Natural Sciences and Engineering Research Council of Canada (NSERC).

Appendix A Local linear smoother

Let be a function on satisfying (C8)–(C10) in Appendix B; examples include the symmetric Beta family (Fan & Gijbels 1996, Eq. 2.5) which has the Epanechnikov kernel as a special case. LLS actually falls into the framework of weighted least squares (WLS) (Fan & Gijbels 1996, pp. 58–59). Given integers and (with values specified in the following cases (i)–(iv)) and matrices (the -vector of ones), (an -vector), (an matrix) and (an non-negative definite matrix), one solves

for a scalar and an -vector . In fact, LLS only uses the WLS solution for , namely,

| (27) |

in which the Moore-Penrose generalized inverse is denoted by “” and In particular, four different combinations of , and yield estimates of the four targets of interest, , , , and , as follows:

- (i)

- (ii)

- (iii)

- (iv)

Bandwidths , , and are all tuned through GCV, i.e., they are chosen to minimize

with their respective corresponding , and . Fan & Gijbels (1996, Eq. 4.3) suggested a rule of thumb which is a good starting point in determining candidate pools for bandwidths.

Appendix B Technical details: assumptions, lemmas, and proofs

Recall the setting of sparsity and error-in-variable: for the th subject, given the number of observation times (satisfying (C1)), noisy trajectories are observed only at time points such that , , where () are underlying functional predictors, and measurement errors are iid as . The independence is imposed as in (C2), with requirement (C3) on moments. Write , , and as the respective density functions of , , and . These density functions are expected be somehow smooth, as demanded by (C4)–(C6). Without the continuity assumed in (C7) it would be logically impossible to recover functions , , and by LLS. Hyper-parameters of LLS are restricted by conditions (C8)–(C14): the first three exclude certain commonly used kernels (e.g., the Gaussian kernel) but admit at least the symmetric Beta family (Fan & Gijbels 1996, Eq. 2.5); the remaining four of (C8)–(C14) comprise the cornerstone of the consistency of LLS recovery, making sure that bandwidths converge at proper rates (as diverges). Condition (C15) (resp. (C16)) implies the convergence rate of PLEASS coefficient estimator in the (resp. ) sense. Importantly conditions (C15) and (C16) restrict the divergence rate of () to be at most if and even slower once . This restriction on is pretty close to the setting of Delaigle & Hall (2012b, Theorem 5.3) who limited the discussion to cases of only (which is reachable by changing the scale on which is measured). In detail our assumptions are:

-

(C1)

and .

-

(C2)

and are all independent of in the sense that, given , and are all independent and the conditional laws are those of , , and .

-

(C3)

.

-

(C4)

exists and is continuous on . The support of is .

-

(C5)

exists and is uniformly continuous on .

-

(C6)

, and all exist and are uniformly continuous on .

-

(C7)

and are both continuous on , and is continuous on . Hence , , and are all finite.

-

(C8)

The kernel function in Appendix A is symmetric (w.r.t. the axis) and nonnegative on such that .

-

(C9)

The kernel function is compactly supported, i.e., is bounded.

-

(C10)

The Fourier transform of is absolutely integrable, i.e., . An implication is the continuity of (almost everywhere) within . Holding (C9) too, we automatically have two moment conditions on : and .

-

(C11)

, , and , as . Hence .

-

(C12)

, , and , as . Hence .

-

(C13)

, , and , as . Hence .

-

(C14)

, , and , as . Hence .

-

(C15)

As , . Additional requirements on vary with the magnitude of ; they also depend on the smallest eigenvalue of which is defined at (32).

-

•

and are both of order I if ;

-

•

if , then and are both of order .

-

•

-

(C16)

Condition (C15) holds with the -norm replaced by the infinity norm .

The first fourteen of the conditions above are inherited from Yao et al. (2005a, b). So is Lemma 1 which states the convergence rate of LLS estimators. We then extend (28) to a more general version (see Lemma 2).

Lemma 2.

Proof of Lemma 2.

Recall the definitions of in (3) and of in (13). Since and , Lemma 2 reduces to (28) when . For integer and each , the identity

implies that

On iteration these two inequalities give that, respectively,

| (29) | ||||

| (30) |

For each , there is such that, for all , we have

| and | ||||

with constant , by Lemma 1. It follows from (29) that

where and . It is worth noting that we have assumed that the range of is constrained in ; the quantity may not be bounded if diverges too fast. Similarly, inequality (30) implies that, for ,

∎

Proof of Theorem 1.

The following alternative expression for (7), drawn from Delaigle & Hall (2012b, Eq. 3.6), dramatically facilitates our further moves:

| (31) |

where

| (32) | |||

| (33) |

with and . As is known, and are bounded, respectively, as

| (34) |

and

| (35) |

Corresponding to (31), at (14) is rewritten as

| (36) |

in which and are respective empirical counterparts of at (32) and at (33), with and .

Observe that, by the Cauchy-Schwarz inequality,

For every and , there is such that, ,

with constants . Analogously, writing , the Cauchy-Schwarz inequality implies that

and further, by Lemmas 1 and 2, as long as ,

where and are positive constants. Thus, if , then

| (37) |

In a similar manner, one proves that

| (38) |

Denote by the smallest eigenvalue of . Notice that, for ,

Provided that (C15) holds, for sufficiently large , one has , for some . In this case, Delaigle & Hall (2012b, Eq. 7.18) argued that, as goes to infinity,

which can be rewritten as

| (39) |

Combining (34), (35), (38) and (39), one obtains

| (40) |

Next, for each , we have

Thus is bounded as below:

| (41) | ||||

| (42) |

Owing to (40),

the rate of (42) is given by (35) and 2 jointly, i.e.,

In this way we deduce

| (43) |

Condition (C15) then implies that both (41) and (42) converge to 0 in probability. The consistency of PLEASS estimators in the sense follows, from the convergence of to (Delaigle & Hall 2012b, Theorem 3.2).

Proof of Theorem 2.

Recall the definitions of at (7) and at (14). Introduce and its empirical version . Note the identities that and . Thus, conditions (C1)–(C15) jointly ensure that, for arbitrarily given ,

The convergence to 0 (in probability and conditional on and ) of (with at (19) and at (18)) follows from Lemma 1 and the continuous mapping and Slutsky’s theorems. Since and are arbitrary the dominated convergence theorem enables us to drop the conditioning. This completes the proof of Theorem 2. ∎

References

- (1)

- Aguilera et al. (2010) Aguilera, A. M., Escabias, M., Preda, C. & Saporta, G. (2010), ‘Using basis expansions for estimating functional PLS regression: Applications with chemometric data’, Chemometrics Intell. Lab. Syst. 104(2), 289–305.

- Albaqshi (2017) Albaqshi, A. M. H. (2017), Generalized Partial Least Squares Approach for Nominal Multinomial Logit Regression Models with a Functional Covariate, PhD thesis, University of Northern Colorado.

- Baíllo (2009) Baíllo, A. (2009), ‘A note on functional linear regression’, J. Stat. Comput. Simul. 79, 657–669.

-

Carroll et al. (2020)

Carroll, C., Gajardo, A., Chen, Y., Dai, X., Fan, J., Hadjipantelis, P. Z.,

Han, K., Ji, H., Mueller, H.-G. & Wang, J.-L. (2020), fdapace: Functional Data Analysis and Empirical

Dynamics.

R package version 0.5.4.

https://CRAN.R-project.org/package=fdapace - Craven & Wahba (1979) Craven, P. & Wahba, G. (1979), ‘Smoothing noisy data with spline functions’, Numer. Math. 31, 377–403.

- de Jong (1993) de Jong, S. (1993), ‘SIMPLS: An alternative approach to partial least squares regression’, Chemometrics Intell. Lab. Syst. 18, 251–263.

- Delaigle & Hall (2012a) Delaigle, A. & Hall, P. (2012a), ‘Achieving near perfect classification for functional data’, J. R. Stat. Soc. Ser. B-Stat. Methodol. 74, 267–286.

- Delaigle & Hall (2012b) Delaigle, A. & Hall, P. (2012b), ‘Methodology and theory for partial least squares applied to functional data’, Ann. Stat. 40, 322–352.

- Fan & Gijbels (1996) Fan, J. & Gijbels, I. (1996), Local Polynomial Modelling and Its Applications, Monographs on Statistics and Applied Probability, Chapman & Hall/CRC, Boca Raton.

- Goldsmith et al. (2011) Goldsmith, J., Bob, J., Crainiceanu, C. M., Caffo, B. & Reich, D. (2011), ‘Penalized functional regression’, J. Comput. Graph. Stat. 20, 830–851.

-

Goldsmith et al. (2019)

Goldsmith, J., Scheipl, F., Huang, L., Wrobel, J., Di, C., Gellar, J.,

Harezlak, J., McLean, M. W., Swihart, B., Xiao, L., Crainiceanu, C.

& Reiss, P. T. (2019), refund: Regression with Functional Data.

R package version 0.1-21.

https://CRAN.R-project.org/package=refund - Goutis (1998) Goutis, C. (1998), ‘Second‐derivative functional regression with applications to near infra‐red spectroscopy’, J. R. Stat. Soc. Ser. B-Stat. Methodol. 60, 103–114.

- Hall et al. (2006) Hall, P., Müller, H.-G. & Wang, J.-L. (2006), ‘Properties of principal component methods for functional and longitudinal data analysis’, Ann. Stat. 34, 1493–1517.

- Harville (1976) Harville, D. (1976), ‘Extension of the Gauss-Markov theorem to include the estimation of random effects’, Ann. Stat. 4, 384–395.

- Hochstrasser (1972) Hochstrasser, U. W. (1972), Orthogonal polynomials, in M. Abramowitz & I. A. Stegun, eds, ‘Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables’, Applied Mathematics Series 55, Dover Publications, Inc., New York, pp. 773–802. Tenth original printing with corrections.

- James et al. (2000) James, G. M., Hastie, T. J. & Sugar, C. A. (2000), ‘Principal component models for sparse functional data’, Biometrika 87, 587–602.

- Krämer & Sugiyama (2011) Krämer, N. & Sugiyama, M. (2011), ‘The degrees of freedom of partial least squares regression’, J. Am. Stat. Assoc. 106, 697–705.

- Lange (2010) Lange, K. (2010), Numerical Analysis for Statisticians, 2nd edn, Springer, New York.

- Li & Hsing (2010) Li, Y. & Hsing, T. (2010), ‘Uniform convergence rates for nonparametric regression and principal component analysis in functional/longitudinal data’, Ann. Stat. 38, 3321–3351.

- Marx (1996) Marx, B. D. (1996), ‘Iteratively reweighted partial least squares estimation for generalized linear regression’, Technometrics 38, 374–381.

-

Novomestky (2013)

Novomestky, F. (2013), orthopolynom:

Collection of functions for orthogonal and orthonormal polynomials.

R package version 1.0-5.

https://CRAN.R-project.org/package=orthopolynom - Paul & Peng (2011) Paul, D. & Peng, J. (2011), ‘Principal components analysis for sparsely observed correlated functional data using a kernel smoothing approach’, Electron. J. Stat. 5, 1960–2003.

- Peng & Paul (2009) Peng, J. & Paul, D. (2009), ‘A geometric approach to maximum likelihood estimation of the functional principal components from sparse longitudinal data’, J. Comput. Graph. Stat. 18, 995–1015.

- Preda & Saporta (2005) Preda, C. & Saporta, G. (2005), ‘PLS regression on a stochastic process’, Comput. Stat. Data Anal. 48, 149–158.

- Reiss & Ogden (2007) Reiss, P. T. & Ogden, R. T. (2007), ‘Functional principal component regression and functional partial least squares’, J. Am. Stat. Assoc. 102, 984–996.

- Rubín & Panaretos (2020) Rubín, T. & Panaretos, V. M. (2020), ‘Sparsely observed functional time series: estimation and prediction’, Electron. J. Stat. 14, 1137–1210.

- Tasaki (2009) Tasaki, H. (2009), ‘Convergence rates of approximate sums of riemann integrals’, J. Approx. Theory 161, 477–490.

-

Therneau (2020)

Therneau, T. M. (2020), A Package for

Survival Analysis in R.

R package version 3.2-3.

https://CRAN.R-project.org/package=survival - Therneau & Grambsch (2000) Therneau, T. M. & Grambsch, P. M. (2000), Modeling Survival Data: Extending the Cox Model, Springer, New York.

- Tombaugh (2006) Tombaugh, T. N. (2006), ‘A comprehensive review of the Paced Auditory Serial Addition Test (PASAT)’, Arch. Clin. Neuropsych. 21, 53–76.

- Wang et al. (2020) Wang, Y., Ibrahim, J. G. & Zhu, H. (2020), ‘Partial least squares for functional joint models with applications to the alzheimer’s disease neuroimaging initiative study’, Biometrics . in press.

- Wold (1975) Wold, H. (1975), Path models with latent variables: the NIPALS approach, in H. Blalock, A. Aganbegian, F. M. Borodkin, R. Boudon & V. Capecchi, eds, ‘Quantitative Sociology: International Perspectives on Mathematical and Statistical Model Building’, Academic Press, New York, pp. 307–335.

- Xiao et al. (2018) Xiao, L., Li, C., Checkley, W. & Crainiceanu, C. (2018), ‘Fast covariance estimation for sparse functional data’, Stat. Comput. 28, 511–522.

-

Xiao et al. (2019)

Xiao, L., Li, C., Checkley, W. & Crainiceanu, C. (2019), face: Fast Covariance Estimation for Sparse

Functional Data.

R package version 0.1-5.

https://CRAN.R-project.org/package=face - Yao et al. (2005a) Yao, F., Müller, H.-G. & Wang, J.-L. (2005a), ‘Functional data analysis for sparse longitudinal data’, J. Am. Stat. Assoc. 100, 577–590.

- Yao et al. (2005b) Yao, F., Müller, H.-G. & Wang, J.-L. (2005b), ‘Functional linear regression analysis for longitudinal data’, Ann. Stat. 33, 2873–2903.

- Zhou et al. (2018) Zhou, L., Lin, H. & Liang, H. (2018), ‘Efficient estimation of the nonparametric mean and covariance functions for longitudinal and sparse functional data’, J. Am. Stat. Assoc. 113, 1550–1564.

- Zhou (2019) Zhou, Z. (2019), ‘Functional continuum regression’, J. Multivariate Anal. 173, 328–346.

- Zhou (2020) Zhou, Z. (2020), Partial least squares for function-on-function regression via Krylov subspaces. arXiv:2005.04798.